Crypto Rewards in Fundraising: Evidence from Crypto Donations to Ukraine

Abstract

Extrinsic incentives such as a conditional thank-you gift have shown both positive and negative impacts on charitable fundraising. Leveraging the crypto donations to a Ukrainian fundraising plea that accepts Ether (i.e., the currency of the Ethereum blockchain) and Bitcoin (i.e., the currency of the Bitcoin blockchain) over a seven-day period, we analyze the impact of crypto rewards that lasted for more than 24 hours. Crypto rewards are newly minted tokens that are usually valueless initially and grow in value if the corresponding cause is well received. Separately, we find that crypto rewards have a positive impact on the donation count but a negative impact on the average donation size for donations from both blockchains. Comparatively, we further find that the crypto rewards lead to an 812.48% stronger donation count increase for Ethereum than Bitcoin, given that the crypto rewards are more likely to be issued on the Ethereum blockchain, which has higher programmability to support smart contracts. We also find a 30.1% stronger decrease in average donation amount from Ethereum for small donations (); the rewards pose similar impacts on the average donation size for the two blockchains for large donations (). Our study is the first work to look into crypto rewards as incentives for fundraising. Our findings indicate that the positive effect of crypto rewards is more likely to manifest in donation count, and the negative effect of crypto rewards is more likely to manifest in donation size.

Keywords Charitable Giving Cryptocurrency Monetary Incentive Ethereum Bitcoin Difference-in-Difference

1 Introduction

Cryptocurrency has not only changed the financial world but also charitable fundraising. Annual crypto donations have skyrocketed from $4.2 million in 2020 to $69.6 million in 2021. 42% of those donations used Ether (ETH) currency, and 36% of the donations used Bitcoin (BIC) currency (Hrywna, 2022). ETH is the digital currency of the Ethereum blockchain, and BIC is the digital currency of the Bitcoin blockchain. The great potential of cryptocurrency in fundraising lies in the prosociality of crypto asset holders who have a strong desire to support freedom, democracy, and people’s ability to have their own personal and financial lives peacefully, according to Ethereum co-founder Vitalik Buterin (Ramaswamy, 2022). More importantly, we propose that the promise of crypto fundraising stems from “crypto rewards” that are fungible or non-fungible tokens (NFT) to recognize contributors for their support.

Crypto rewards are operationalized as “airdrops.” An airdrop is considered a marketing initiative to raise awareness or crypto funds for a cause (Sergeenkov, 2022). Marketers send out fungible tokens that are newly minted to their community members for free or in exchange for completing a task (e.g., following a Twitter account, joining a Telegram group, donating to a designated wallet). These reward tokens are mostly valueless initially but will increase when the corresponding cause is well received and when the tokens begin trading on an exchange. These causes are usually blockchain-based projects, and the reward tokens are a currency that could be used in these projects. This is referred to as initial coin offering (ICO) (Arnold et al., 2019) in contrast to initial public offering (IPO). In this study, we go beyond the original definition of ICO and examine the impact of crypto rewards in crypto fundraising for social causes that are not blockchain-based. This extension of ICO could potentially change the landscape of fundraising, affording attention from the blockchain community, non-profit sector, and policymakers.

In essence, crypto rewards are extrinsic incentives to promote charitable giving, whose impact is mixed, according to past studies. Extrinsic incentives have been widely adopted to promote giving as self-interest is considered a primary motivation for human behavior (Kohn, 2008). Without an extrinsic incentive, people are hesitant to donate even if they have strong feelings of compassion for a cause (Miller and Prentice, 1994). Thus, other than its direct impact, the extrinsic incentive serves as an “excuse” for people to conceal their prosocial motivation and act “rationally,” affecting their decisions indirectly (Holmes et al., 2002). To this end, crypto rewards could cause an increase in giving. At the same time, this extrinsic motivation may undermine people’s intrinsic motivation by activating a more self-interested mindset (Chao and Fisher, 2021), which subsequently reduces giving, as predicted in the theories of motivation crowding-out (Frey and Jegen, 2001; Frey and Oberholzer-Gee, 1997). The relative strength of these opposing predictions rests on the choice and framing of the rewards (Zlatev and Miller, 2016). Different from the widely studied thank-you gifts of mugs and t-shirts, crypto rewards’ value could increase over time. They are more likely to be considered investment products that could carry high value. Given these unique features, analyzing the impact of crypto rewards will not only generate insights about incentives for prosocial behavior but also enhance the understanding of the business value of blockchain technology (Bénabou and Tirole, 2006).

We examine the impact of crypto rewards in fundraising by leveraging the crypto fundraising event initialized by the Ukrainian government during Russia’s invasion of Ukraine. On Feb. 26, 2022, the Ukrainian government announced that they would accept crypto donations and publicized their Ethereum and Bitcoin wallet addresses. On March 2, 2022, the Ukrainian government further announced an airdrop with the donor list snapshot to be taken the next day (Time, 2022). Although the Ukrainian government canceled this airdrop several hours before the snapshot, it mobilized a large number of donors and resulted in record donations totaling more than $25 million from more than 84,000 cryptocurrency donations in only one week. We first perform an interrupted time series (ITS) analysis under the framework of Autoregressive Integrated Moving Average (ARIMA) to estimate the impact of the airdrop on the Ethereum and Bitcoin blockchains separately (Schaffer et al., 2021). We further perform a comparative ITS analysis, or difference-in-difference (DiD), to exploit the differential impacts of this airdrop on Ethereum and Bitcoin by estimating an ordered treatment effect (Callaway and Sant’Anna, 2021). The DiD analysis leverages the differential programmability capabilities of Bitcoin and Ethereum, where an airdrop is much more likely to be implemented in the Ethereum blockchain than the Bitcoin blockchain (Cointelegraph, 2021). Both analyses are widely used to analyze policy interventions, and the comparative ITS (DiD) allows stronger identification by better controlling for temporal effects of fundraising (e.g., awareness of the cause, dynamic situations in Ukraine).

From the ITS analysis, we find that crypto rewards effectively increased donation count and decreased average donation size for both Ethereum and Bitcoin blockchains. From the comparative ITS analysis, we further find that the average donation count for Ethereum increased 812.48% more than Bitcoin in response to the crypto rewards. However, the treatment effect on the average donation size is not significantly different for these two blockchains. In our split-sample analysis, we further find that the crypto rewards more aggressively increased donation counts and decreased average donation size for the Ethereum blockchain as compared to the Bitcoin blockchain when the donations are small (). When the donations are large (), we only observe a more positive effect on donation count from Ethereum; we did not observe a more negative effect on average donation size from Ethereum compared to Bitcoin.

Our study leveraged an unprecedented crypto fundraising event that offered crypto rewards in the form of an airdrop to its supporters. This event is the first of its kind and is of vital importance for the crypto community that seeks to expand the societal influence of blockchains, policymakers who need to understand the economic implications of crypto donations, and non-profit organizations who are turning to crypto to raise funds for emerging crises. Theoretically, we reconcile and extend past findings that either identified a positive or a negative impact of thank-you gifts by showing that the positive effect is more likely to manifest in donation count and the negative effect is more likely to manifest in donation size. Such insights deepen our understanding of charitable giving as sequential decisions of whether to give and how much to give. Moreover, we identify the economic value of crypto rewards and contribute to the understanding of extrinsic motivations in charitable giving.

2 Theory and Literature

The effect of extrinsic incentives on prosocial behavior has been widely studied in the literature of economics, psychology, and information systems (Newman and Shen, 2012; Gneezy and Rustichini, 2000; Liu and Feng, 2021). In this study, we focus on the effect of crypto rewards on “first-time” donations (instead of the long-term consequences of monetary incentives). The nature of crypto rewards is a “thank-you” gift for contributing a crypto donation. Conditional thank-you gifts are a common form of extrinsic incentives, where a donor gets a gift (e.g., mug, water bottle) conditional on his or her charitable contribution. Prior works find mixed evidence regarding the effect of conditional gifts.

On the one hand, extrinsic motivations predict an increase in giving because most people are primarily motivated by self-interest (Kohn, 2008). As a matter of fact, self-interest has become a social norm to the extent that people overestimate the salience of self-interest such that they would be hesitant to donate to a charitable cause even when they have strong feelings of compassion (Miller and Prentice, 1994; Miller, 1999). In such cases, extrinsic incentives could work as an “excuse” to rationalize people’s prosocial behavior by concealing their prosocial motivations (Holmes et al., 2002). As evidence, Falk (2007) finds that the frequency of donations increased by 17% when a small gift was given to donors and by 75% when a large gift was given. Similarly, Alpizar et al. (2008) find that small gifts prior to the donation request increased the proportion of donations by 5%.

Past works usually consider thank-you gifts that are of relatively low and static value (e.g., CDs, mugs, and t-shirts) (Shang and Croson, 2006). While crypto rewards are also of low value initially (e.g., newly minted tokens), their value could increase over time. When the value of the thank-you gifts is volatile and potentially high,111While most airdrop rewards are below $20, the reward can be more than a thousand dollars (Boom, 2022). the rewards could have a direct and positive impact on prospective donors’ funding decisions. At the same time, the acts of giving become more likely to be considered an investing behavior, and the indirect impact of thank-you gifts as an excuse for prosocial behavior is more pronounced. Through the above mechanism, extrinsic incentives could motivate people who would not otherwise donate to make a contribution (Ratner et al., 2011). Extrinsic incentives can hardly increase the contribution size through this mechanism because increasing contribution size at a fixed (and unknown) reward is not economically rational. Thus, we propose our first hypothesis for the outcome of donation count.

Hypothesis 1 (H1):

Offering a crypto reward, as reflected in an airdrop, would lead to an increased count of donations.

On the other hand, the theories of motivation crowding-out predict that people would reduce giving when extrinsic incentives are provided because extrinsic motivations would crowd out intrinsic motivations (Frey and Oberholzer-Gee, 1997; Frey and Jegen, 2001; Gneezy and Rustichini, 2000; Bénabou and Tirole, 2006). Extrinsic motivations are activated by monetary rewards, praise, or fame, and intrinsic motivations are related to activities that people undertake because they derive satisfaction from them. As Frey and Oberholzer-Gee (1997, p.746) stated, “If a person derives intrinsic benefits simply by behaving in an altruistic manner or by living up to her civic duty, paying her for this service reduces her option of indulging in altruistic feelings.” Many studies discover evidence in support of the motivation crowding-out theory. Newman and Shen (2012) find that among the donors who are willing to contribute, those who were offered a thank-you gift donated a significantly lower amount than those who were not offered a thank-you gift. Chao (2017) further finds that the negative effect of extrinsic motivation from a thank-you gift is only present when the gift is visually salient to occupy the prospective donor’s attention.

The crypto rewards in our context are significant enough to occupy the donors’ attention because the reward tokens are immutable proof of the donors’ good deeds. They are particularly likely to elicit a self-interested mindset because, as we stated in the development of H1, the value of the rewards could increase as the cause becomes more salient, and the reward tokens are essentially financial investment products. As a result, the crypto rewards likely activate the crowding-out effect to reduce people’s giving. We consider the decisions of whether to give and how much to give sequential. While the investment product feature could positively affect the initial decision of whether to give, it leads to a more pronounced self-interested mindset such that the negative crowding-out effect will manifest in the subsequent decision of how much to give. Thus, the average contribution size would be lower than in the case when no crypto rewards are available.

Hypothesis 2 (H2):

Offering a crypto reward, as reflected in an airdrop, would lead to a decreased average donation size.

3 Research Context

3.1 Cryptocurrency Donations and an Airdrop

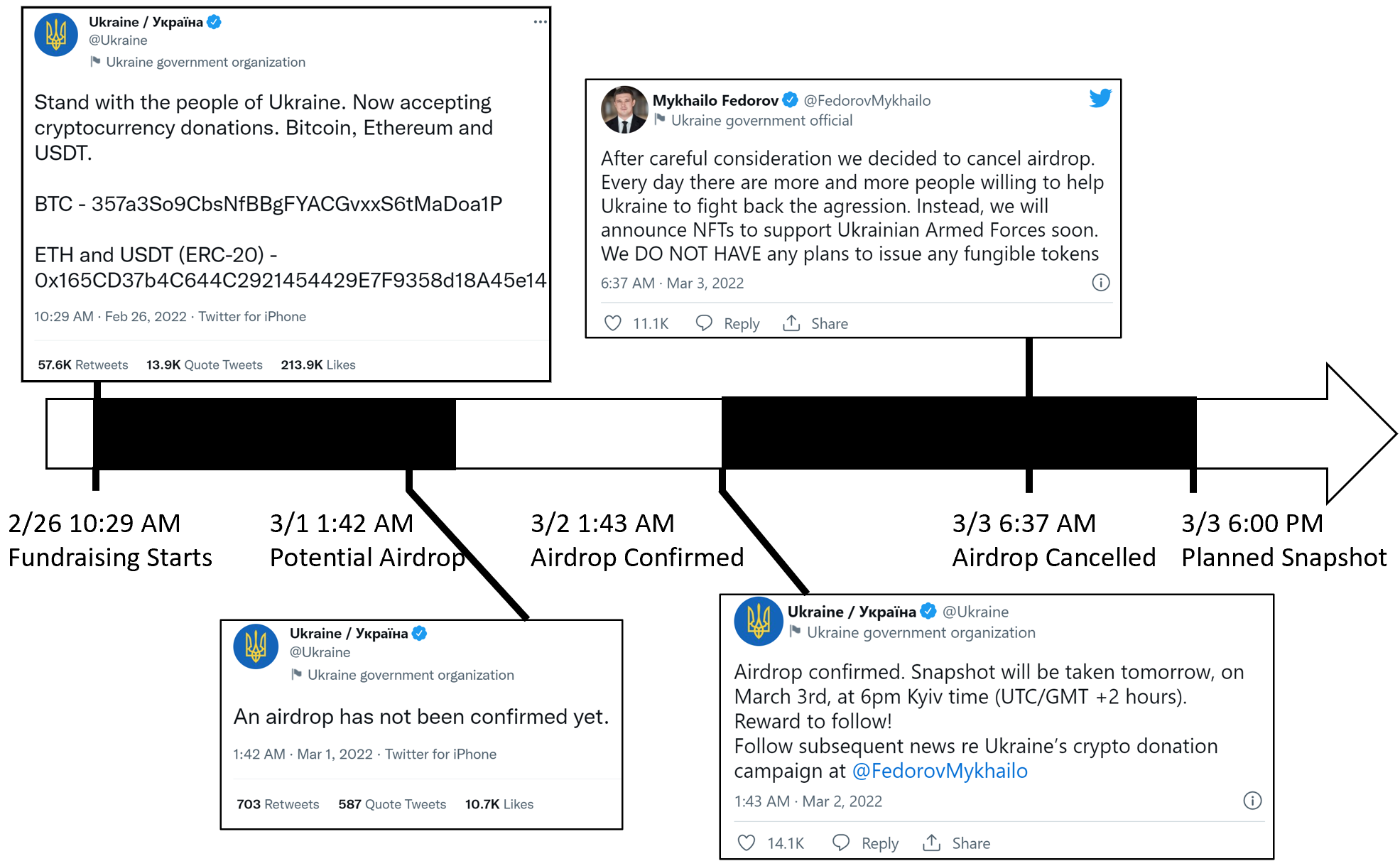

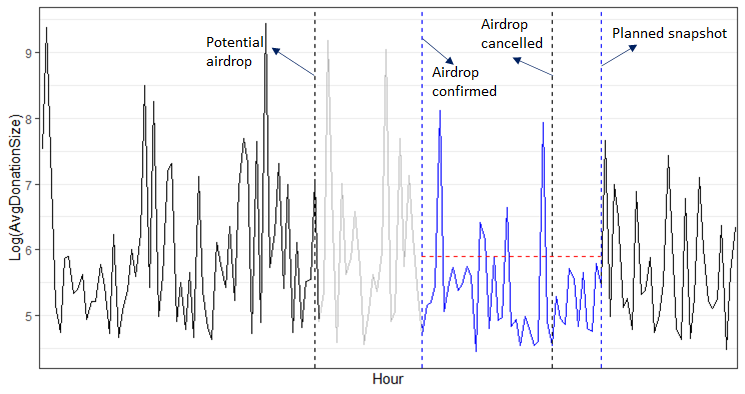

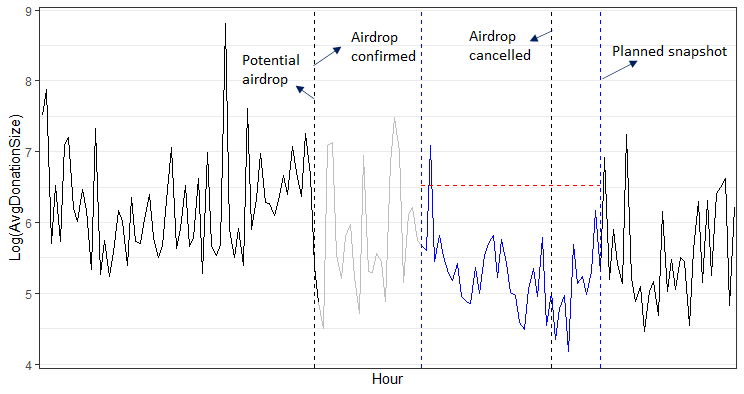

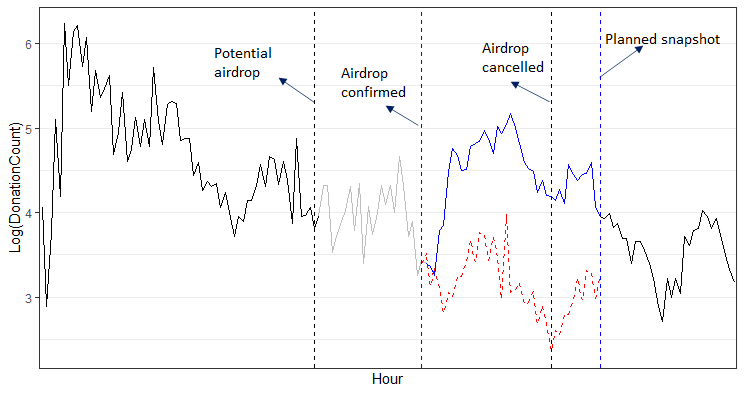

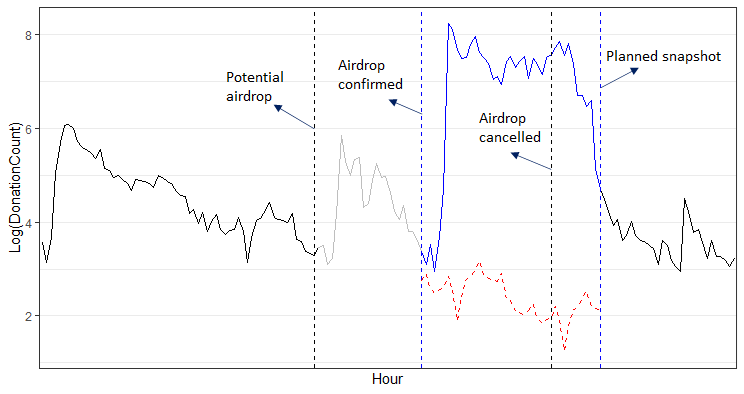

In this section, we introduce the relevant Ukrainian crypto fundraising activity and illustrate its timeline in Figure 1. The Ukrainian government posted pleas for cryptocurrency donations on Feb. 26 at 10:29 AM, 2022 (UTC). Since the banking system of Ukraine was at risk from a Russian attack, crypto offered an alternative financial structure because it uses cryptography to secure transactions (Time, 2022). In a tweet, the Ukrainian government announced their Ethereum and Bitcoin wallet addresses (Figure 1).222 The Ministry of Digital Transformation later started accepting more currencies, including SOL, DOGE, and DOT. Ether (ETH) is the native currency traded on the Ethereum blockchain, and Bitcoin (BTC) is the currency traded on the Bitcoin blockchain. Both ETH and BTC are digital currencies based on the distributed ledger technology of blockchain (Cointelegraph, 2021).

On March 1 at 1:43 AM, Ukraine announced that an “airdrop” has not been confirmed, but formally announced it on March 2 at 1:43 AM that they will reward donors who supported Ukraine with an airdrop. The planned snapshot of the list of donor wallet addresses would be taken the next day. While the initial announcement that “An airdrop has not been confirmed yet” does not officially start the airdrop, it is a signal that there is a potential airdrop. Thus, people may react to this potential airdrop even before the official announcement is posted.

One day later on March 3 at 6:37 AM, the vice prime minister of Ukraine and the Minister of Digital Transformation of Ukraine announced the cancellation of this airdrop several hours before the scheduled snapshot. It was believed that the cancellation was due to crypto holders’ unethical behavior of donating a minimal amount to profit from the airdrop (Strachan, 2022).

3.2 Bitcoin and Ethereum

In this section, we present background knowledge about why the airdrop is much more likely to be implemented on Ethereum than Bitcoin. Bitcoin was created as an alternative to national currencies and designed to be a medium of value exchange. Ethereum was created to go beyond the function of a digital currency given that it is more programmable; it is also a software platform to facilitate and monetize smart contracts and decentralized applications. While the Ukrainian government did not explicitly mention that the airdrop would be performed on Ethereum, it is highly likely the case for the following reasons. First, while an airdrop can be issued in both Ethereum and Bitcoin theoretically,333El Salvador has airdropped each of its citizens $30 worth of Bitcoin to promote this new currency. an airdrop is much more likely to be issued on the Ethereum blockchain due to its better programmable capacities to support smart contracts. According to Airdrop King, 81% of airdrops are issued on the Ethereum blockchain. Second, the Ukrainian government did not specify the reward to be airdropped, and the reward could be either fungible tokens or NFTs. Airdropping NFTs is only possible on Ethereum as it concerns smart contracts. Third, it is a consensus among the crypto community that airdrops will be issued on the Ethereum blockchain. As anecdotal evidence, a crypto Youtuber with 166,000 subscribers uploaded a video tutorial for Ukraine’s crypto airdrop and suggested people not to donate to the Bitcoin address if they would like to qualify for this airdrop.444The Youtuber is Crypto Hustle, and the video can be found here. Indeed, while the Ukrainian government canceled this airdrop, they later airdropped NFTs to 34,000 Ether donors as promised. This is another piece of evidence that the airdrop was most likely to be issued on the Ethereum blockchain.

4 Data

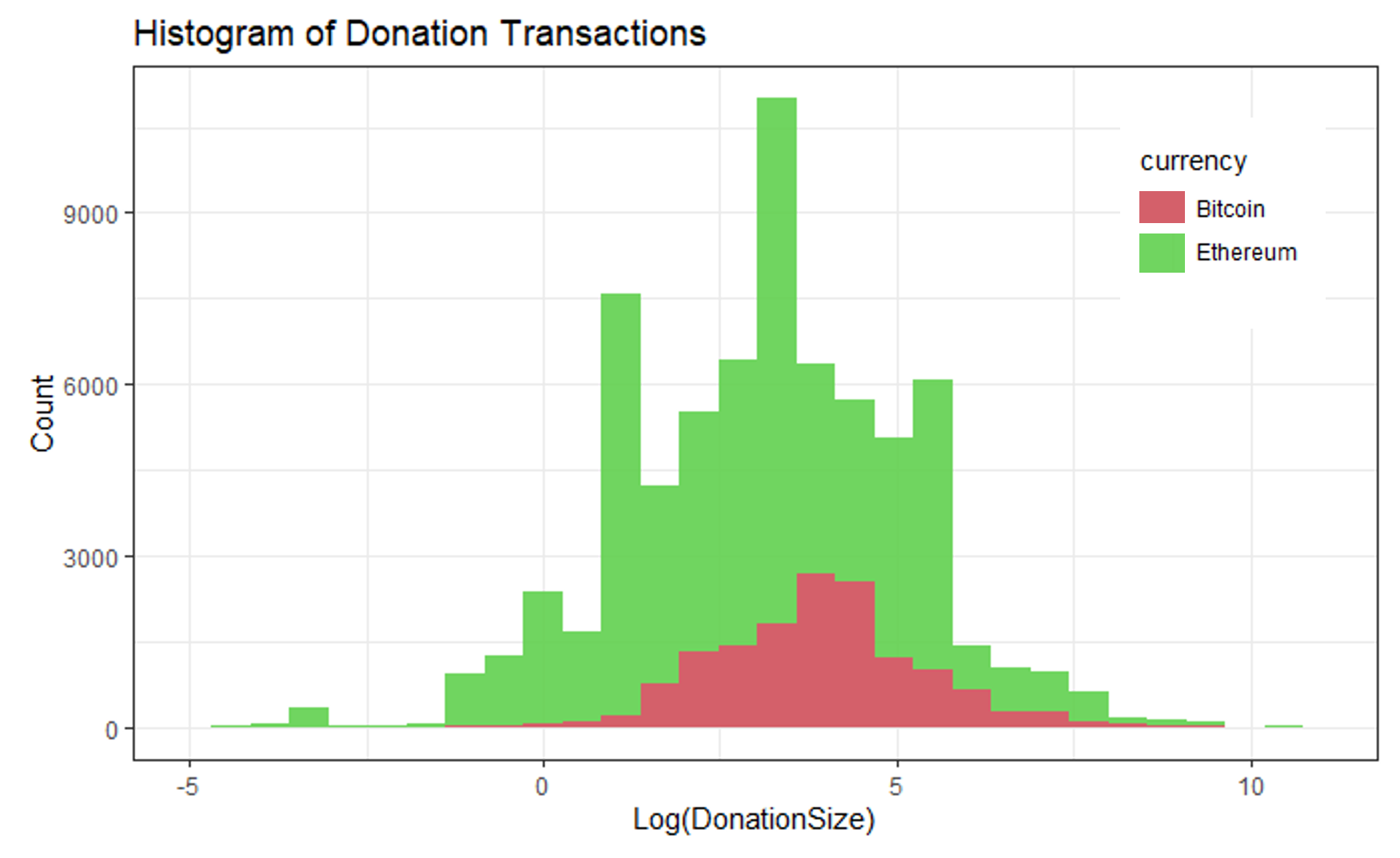

We collected donation transactions between February 26 and March 4, 2022, from the public wallet of Ukraine donations to focus on the airdrop, with the time zone being UTC. Transactions of Bitcoin were collected from the blockchain tracker,555The address is 357a3So9CbsNfBBgFYACGvxxS6tMaDoa1P. and transactions of the Ethereum blockchain were collected from the etherscan tracker.666The address is 0x165CD37b4C644C2921454429E7F9358d18A45e14. We calculated the USD value of donation contributions using the historical prices of Bitcoin and Ethereum. Bitcoin prices were retrieved from Yahoo Finance at a daily frequency, and we used the opening price. Ethereum prices vary by minute, and we retrieved the historical price for every transaction based on the timestamps of the transactions. There were 14,903 donation transactions on the Bitcoin blockchain and 69,740 donation transactions on the Ethereum blockchain during this observation window. In total, $9,874,757 was raised from the Bitcoin blockchain, and $16,043,036 was raised from the Ethereum blockchain. We plot the histogram of the log-transformed donation transaction size (with no aggregation) for Bitcoin and Ethereum in Figure 2. We notice some extremely small donations () for Ethereum. We show in a robustness check that this small set of donations has no major impact on our findings.

| Min | Q1 | Median | Mean | S.D. | Q3 | Max | |

|---|---|---|---|---|---|---|---|

| 0 | 0 | 0.50 | 0.50 | 0.50 | 1 | 1 | |

| 0 | 0 | 0 | 0.31 | 0.46 | 1 | 1 | |

| 0 | 43 | 78.5 | 302.06 | 606.72 | 155.25 | 3720 | |

| 64.04 | 160.39 | 252.60 | 573.65 | 1233.90 | 495.54 | 12568.55 |

We aggregate data at an hourly level during this time window. For the first day of our observation (Feb. 26, 2022), we have 14 hourly observations for both Bitcoin and Ethereum because the announcement to accept crypto donations was posted on Feb 26 at 10:29 AM. The first donation for BTC was performed on Feb. 26 at 12:01 PM, and the first donation for Ether on Feb. 26 at 11:54 AM. We started the observation at 11:00 AM, and the first observation for BTC corresponds to zero donations. For the remaining days (Feb. 27 through March 4), we have 24 observations each day except for the period of a “potential but not confirmed airdrop.” Remember that an announcement was posted about the airdrop not being confirmed on March 1 at 1:42 AM, and the official confirmation was on Mar 2 at 1:43 AM (Figure 1). After excluding the time window of the potential airdrop, we observe the outcomes of our interest at 134 discrete observation points (hours) for both Ethereum and Bitcoin.

We use subscript to refer to currencies, where can take for Bitcoin and for Ether. We use subscript to refer to the index of time that ranges from the to the hour. The dependent variables of our interest include:

-

•

: the average contribution size for currency during time .

-

•

: the hourly number of donations for currency during time .

Our key independent variables include the currency dummy and a binary variable indicating whether the airdrop is actively available (See below). The airdrop is considered available between March 2 at 2:00 AM and March 3 at 6:00 PM, as the airdrop was announced on March 2 at 1:43 AM and scheduled to snapshot at March 3 at 6:00 PM. Although the airdrop was canceled on March 3 at 6:37 AM, we consider the end of the treatment to be the planned snapshot because many people are not aware of the cancellation. We note that our results stay unchanged even if we change the end time of the treatment to the cancellation of the treatment. This is reported in a robustness check.

-

•

: a binary variable that takes the value of one if the currency is Ether and zero if it is Bitcoin.

-

•

: a binary variable that takes the value of one if the airdrop is actively available and zero otherwise.

The summary statistics are reported in Table 1. Other than these reported variables, we also coded hourly dummy variables to account for the temporal trends of giving, which are likely affected by the media coverage of this event and the changing situations in Ukraine.

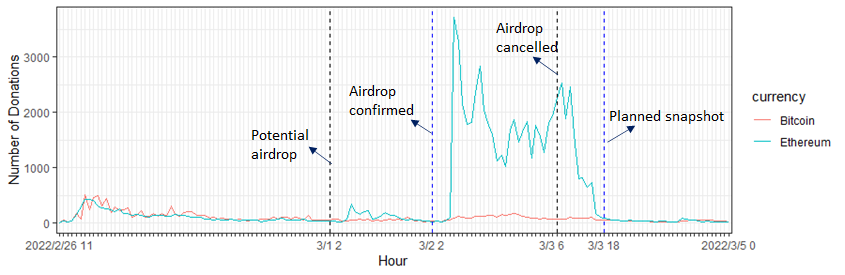

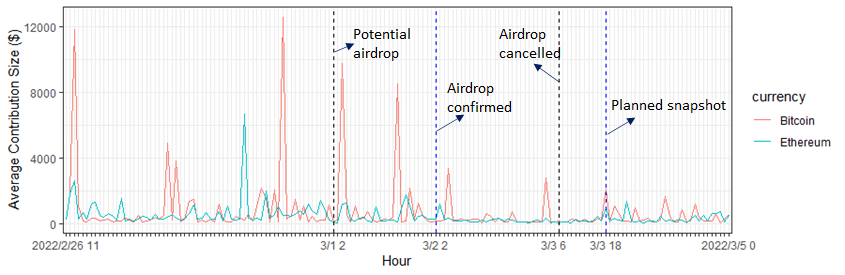

To illustrate the data patterns, we further report the breakdown of the summary statistics by groups in Table 2 and plot the variations of the variables over time in Figures 4 and 4. As can be seen in Figure 4, there was a hike in donation counts for Ethereum in comparison to Bitcoin while the airdrop was available. According to Table 2, the average number of hourly donations was 107.32 on Bitcoin when the airdrop was not available and 87.98 when it was available. However, the difference in donation count for BIC is not statistically significant (=1.54). The average number of hourly donations on Ethereum was 106.48 when the airdrop was not available and 1400.78 when the airdrop was available. This substantial increase in the hourly number of donations is statically significant (=-8.56). As can be seen in Figure 4, there is a decrease in average donation size when the airdrop was available. The decrease is statistically significant both for Bitcoin and Ethereum. The average donation size dropped from an average of $814.80 to $390.51 for Bitcoin (=1.92) and from an average of $566.54 to $233.04 for Ethereum (=3.90).

| =0 | =1 | Paired -test | |||||

|---|---|---|---|---|---|---|---|

| Mean | Median | S.E. | Mean | Median | S.E. | -stats | |

| Panel A. Contributions on Bitcoin (=0) | |||||||

| 107.32 | 70 | 105.48 | 87.98 | 88 | 39.64 | 1.54 | |

| 814.8 | 241.35 | 1872.25 | 390.51 | 195.66 | 658.10 | 1.92* | |

| Panel B. Contributions on Ethereum (=1) | |||||||

| 106.48 | 59 | 123.48 | 1400.78 | 1600 | 965.11 | -8.56*** | |

| 566.54 | 364.49 | 1872.25 | 233.04 | 185.89 | 180.96 | 3.90*** | |

| Note: | ∗p0.1; ∗∗p0.05; ∗∗∗p0.01 | ||||||

5 Empirical Design and Analyses

The introduction of an airdrop as a reward to crypto donors is a quasi-experiment. This context is different from a policy intervention that happens to everyone because the airdrop has a much more pronounced impact on the Ethereum blockchain than the Bitcoin blockchain. This context is also different from a randomized controlled trial, which requires a control group unaffected by the intervention.777In a randomized controlled trial, participants have no knowledge of whether they are in the control group or treatment group. In our context, people have information about the different chances of getting rewards on the two different blockchains. Although the Bitcoin blockchain is likely less affected by the airdrop than the Ethereum blockchain, it is still affected. This is especially the case because Ether and Bitcoin are currencies that are exchangeable, despite the exchange fees.

Since the intervention can potentially affect both the Bitcoin and the Ethereum blockchains, we perform an interrupted time series analysis (ITS) under the framework of Autoregressive Integrated Moving Average (ARIMA) modeling in Section 5.1 to estimate the impact of the intervention on Bitcoin and Ethereum separately (Schaffer et al., 2021). This ITS design does not account for the potential time confoundedness. We handle the temporal effects that could confound the effect of the intervention using a comparative interrupted time series design, or difference-in-difference (DiD) analysis, in Section 5.2 to estimate the ordered treatment effect by exploiting the airdrop’s differential impacts on Ethereum and Bitcoin blockchains (Callaway and Sant’Anna, 2021).

5.1 Separate Effects of the Intervention

In this analysis, we evaluate the impact of this airdrop on Bitcoin and Ethereum blockchains separately by performing an interrupted time series analysis (ITS) under the framework of Autoregressive Integrated Moving Average (ARIMA) modeling. ITS is one of the best designs to estimate the causal impact of a policy intervention when randomized controlled trials are not available (Bernal et al., 2017; Kontopantelis et al., 2015). We use the pre-intervention period data to fit an ARIMA model, with which we forecast the fundraising outcomes in the absence of the intervention. We then use the forecast counterfactual as the dependent variable and allow the observed data to be the independent variables to estimate the effect of the intervention. ITS could be operationalized as a simple segmented regression which typically requires the time series to have an easy-to-model trend. In our context, we apply the ITS on an ARIMA model to make better predictions by accounting for autocorrelation, seasonality, and underlying time trends (Schaffer et al., 2021).

5.1.1 Method

We divide the time window into a pre-intervention period, an intervention period, and an after-intervention period. The pre-intervention period lasts from Feb. 26 at 11:00 AM to March 1 at 2:00 AM, corresponding to the time interval between the Ukrainian government’s announcement to accept crypto donations and the statement that an airdrop was not confirmed. As mentioned previously, we exclude the duration between the announcement that an airdrop was not confirmed and the airdrop confirmation because it is hard to know whether the intervention has an effect during that period. Thus, the intervention period starts from the official confirmation on March 2 at 2:00 AM and ends at the planned snapshot on March 3 at 6:00 PM. Although a cancellation was announced on March 1 at 1:42 AM, it did not reach the audience effectively; people continued to participate actively in the airdrop until the planned snapshot. The post-intervention periods correspond to the remaining hours on March 3, 2022 after the planned snapshot and the entirety of March 4, 2022. Given this data strategy, our estimation of the effect of airdrop is conservative. Our results remain unchanged when we consider the cancellation to be the ending of the intervention.

For each currency, we use the automated algorithm to select the best fitting ARIMA model for the outcomes of and using the pre-intervention period data. To reduce non-stationarity, which is a key assumption for ARIMA, we log-transform all the outcome variables. An ARIMA model is specified ARIMA if no seasonal adjustment is made and ARIMA if the seasonal adjustment is performed, where:

-

•

= the order of the autoregressive (AR) component to include lags of the dependent variable

-

•

= the degree of non-seasonal differencing

-

•

= the order of the moving average (MA) component to include lags of the error

-

•

= the order of the AR component for the seasonal part

-

•

= the degree of seasonal differencing

-

•

= the order of the seasonal differencing part

We perform the model selection based on minimizing the information criteria of AIC and BIC. For Bitcoin, the best model for is ARIMA(0,0,0). That is to say, the errors are uncorrelated across time - they are white noises. For Ether, the best model for is ARIMA(1,1,2). This suggests some autocorrelation and non-stationarity. For BIC, the best model for is ARIMA; for Ether, the best model is ARIMA. Both models include an adjustment for seasonality based on the hour of the day. The degree of seasonal differencing is one, meaning that we adjust for seasonality by taking the difference between each observation and the previous value at lag 24. This is intuitive because people’s time availability varies across the day. This hour of day adjustment was not needed for the average donation size because the average donation size does not fluctuate over the day. Also, first differencing needs to be performed on both Bitcoin and Ethereum with the outcome of donation count. This indicates non-stationarity, which is expected because the fundraising performance is affected by the spread of the information (i.e., Ukraine is accepting crypto donations) and the dynamic situations in Ukraine. We then forecast the outcomes for the intervention period and use the forecasts as the outcome variable, with the dependent variable being the observed outcomes, . We estimate a linear regression without intercept, and the estimated coefficients reflect the effect of the intervention. Note that no other variables are needed in this regression because the time trends, seasonality, and autocorrelation of the outcome have already been accounted for in the forecasting process (Schaffer et al., 2021).

5.1.2 Results

We plot the actual data in solid lines and the predicted outcome in dashed lines for each outcome and each currency in Figures 5 through 8. As can be seen in Figures 8 and 8, the observed average donation size (solid blue line) is lower than the predicted value (red dashed line). In Figures 8 and 8, the observed count of donations (solid blue line) is much higher than the predicted value (red dashed line). Comparing Figure 8 with Figure 8, we find that the effect of the intervention is much more substantial for ETH than BIC.

According to the estimation results, the airdrop lowered the log-transformed average donation size by 7.22% () for Bitcoin and by 18.66% () for Ethereum. Further, the log-transformed count of hourly donations increased by 41.64% for BIC and by 199.57% for Ether in response to the intervention. Thus, both H1 and H2 are supported.

Finally, we report the comparisons between the forecasts and the post-intervention period observations. We find that the observed log-transformed average donation size is 1.16% lower than the prediction for BIC and is 13.74% lower than prediction for ETH. We also find that the observed log-transformed donation count is 0.91% lower for BIC and 18.82% higher for ETH. This indicates that the treatment effect likely continued to manifest for ETH after the planned snapshot, but the magnitude of the effect has been greatly reduced.

The analyses above separately estimate the impact of the airdrop on BTC and ETH. By checking the ACF plots of the residuals for each ARIMA model, we observe no autocorrelation or non-stationarity (Appendix A), demonstrating the validity of our analysis. However, this analysis has several limitations. First, it is hard to gauge whether the decrease in the average donation size is due to motivation crowd-out or a selection issue (i.e., the donors who contribute after the availability of the crypto rewards may be systematically different from early donors). Second, while the ARIMA model accounted for seasonality, there could be other non-linear temporal trends that could confound the observed treatment effects. For example, there could be an abrupt change in Ukraine that coincides with the introduction of the airdrop. As such, we perform a comparative ITS, or a DiD analysis, to compare the differential impacts of the airdrop on the Bitcoin and Ethereum blockchains in the next section.

5.2 Comparative Effects of the Intervention

To address the limitations stated above, we lend support from a comparative interrupted time series design, or DiD research design, to enhance identification by estimating an ordered treatment effect to exploit the difference between the impacts of the airdrop on Bitcoin and Ethereum (Wing et al., 2018). We adopt an extension of DiD with two treatment conditions of different intensities (Callaway and Sant’Anna, 2021; Fricke, 2017). This is a special condition of DiD without controls that compares a strong treatment with a weak treatment and has been widely used to understand interventions without controls. For example, Duflo (2001) used this framework to study the effect of school construction on schooling and labor market outcomes by comparing regions with low and high levels of newly constructed schools. Felfe et al. (2015) leveraged the regional variation in childcare expansion rates to understand the effect of formal childcare on maternal employment as well as child development.

5.2.1 Method

In the comparative ITS (DiD), we aim to identify the ordered treatment effect, or the average treatment effect on the treated (Ethereum), represented by , where represents the expected outcome, with and . We use to illustrate the treatment to get an airdrop reward with a low probability as in the Bitcoin blockchain; we use to illustrate the treatment to get an airdrop reward with a high probability as in the Ethereum blockchain; we use to illustrate the condition when the treatment of an airdrop is not available. We use to denote the time when the airdrop was available and to denote the time when it is not available. This is equivalent to the local treatment effects discussed in Angrist and Imbens (1995). We can re-write this equation such that:

| (1) |

We observe but not , and draw inferences from the Bitcoin blockchain by leveraging the strong parallel assumption that . This assumption is an equal effect size assumption that likely holds in our context if ETH holders and BIC holders are equivalently sensitive to external rewards. We believe that this assumption holds because people’s choice between BIC and ETH is a financial decision unrelated to their prosocial motivations. With this assumption, we can re-write such that:

| (2) |

where every component of the right side of Equation (2) is observed. Even if we believe that this assumption does not hold (e.g., ETH holders may react more aggressively to the airdrop), we can partially identify the ordered treatment effects as long as . This common trend assumption is widely used in classic DiD designs and highly likely to hold given the parallel pre-intervention trends in Figures 2 and 3 (Callaway and Sant’Anna, 2021). Fricke (2017) prove that with partial identification, we can interpret the estimates as the lower bound in the magnitude for the treatment effect.

The econometric model we estimate is specified as:

| (3) |

where the dependent variable can be operationalized as the logarithm of the number of hourly donations () or the logarithm of the average contribution size (). These outcomes are both log-transformed after adding one because they are highly skewed. To identify the ordered treatment effect, we use two-way fixed effects (Callaway and Sant’Anna, 2021). represents the hourly time dummy variables that account for the time fixed effects. The time effects could source from the dynamic situations in Ukraine, the awareness of the crypto fundraising event, or simply the varying availability of time people have at different times. Such temporal trends affect the Bitcoin and Ethereum blockchains in the same way. The systematic difference between BIC and ETH is the group level fixed effects, and we control for it using . The coefficient of our interest is as it indicates the differential impacts of the airdrop on the blockchains of Bitcoin and Ethereum.

5.2.2 Results

We first run the regression following Equation (3) for the full sample and report the results in Table 3. We can see from Model (1) of Table 3 that the coefficient for is significantly positive for the outcome of donation counts (, ). Specifically, the average hourly donation count of the Ethereum blockchain has increased 812.48% more than the Bitcoin blockchain in the intervention.

However, from Model (2) of Table 3, the coefficient for is insignificant for the outcome of average donation size (, ). That is to say, the average donation size for Ethereum did not change differently from that for Bitcoin during this intervention. We note that the observation number for Model (2) of Table 3 is 267 but that for Model (1) is 268 because there were no donations in the first hour of fundraising for BIC and the outcome of average donation size was un-defined in that case.

| Dependent variable: | ||

| Log() | Log() | |

| (1) | (2) | |

| Intercept | ||

| Time Dummy | Yes | Yes |

| Observations | 268 | 267 |

| R2 | 0.895 | 0.659 |

| Adjusted R2 | 0.788 | 0.307 |

| Note: | ∗p0.1; ∗∗p0.05; ∗∗∗p0.01 | |

| Dependent variable: | ||||

| Log() | Log() | Log() | Log() | |

| (1) | (2) | (3) | (4) | |

| (0.167) | (0.052) | (0.149) | (0.215) | |

| (0.636) | (0.244) | (0.568) | (1.005) | |

| (0.092) | (0.029) | (0.083) | (0.120) | |

| Intercept | ||||

| (0.448) | (0.199) | (0.400) | (0.820) | |

| Time Dummy | Yes | Yes | Yes | Yes |

| Observations | 268 | 267 | 268 | 267 |

| R2 | 0.888 | 0.729 | 0.886 | 0.622 |

| Adjusted R2 | 0.773 | 0.450 | 0.768 | 0.233 |

| Note: | ∗p0.1; ∗∗p0.05; ∗∗∗p0.01 | |||

These findings add to our results in the separate analysis in Section 5.1. To derive more insights, we re-process our data by constructing the data for small donations () and large donations () separately. We chose the threshold of $250 because the median of average donation size is $252.60. We separately run the regressions for the two datasets and report our findings in Table 4. For small donations, we find from Model (1) and Model (2) that the airdrop increased the number of donations more aggressively for Ethereum (, ) and decreased the average donation size more aggressively for Ethereum (, ). Specifically, the average donation size dropped by 30.1% more for Ethereum as compared to Bitcoin during this intervention. However, for large donations, as in Model (3) and Model (4) of Table 4, we only find a more aggressive increase in the average donation count from Ethereum (, ), but the decrease in the average donation size was similar between Ethereum and Bitcoin (, ). This explained the insignificance of the coefficient for in the main model in Table 3, which could be due to the greater variance in donation size for large donations. While these findings do not speak directly to our hypotheses, they offer better understanding of the mechanisms and stronger identifications. We discuss the details in later sections.

6 Robustness Checks

To validate our results, we perform three robustness checks. The first tests whether the reduction in donation size is caused by the existence of extremely small donations, thus, the split-sample analysis is performed. The second rules out an alternative explanation about donation motivation and serves to confirm our main finding, thus, the full-sample analysis is performed. The third is about the sensitivity of time, and the full-sample analysis is performed.

6.1 Exclude Extremely Small Donations

One of our major explanations for the more aggressive reduction in contribution sizes for small donations on Ethereum is motivation crowding-out. However, this finding could also be driven by extremely small donations made by self-interested donors who seek to profit from this fundraising activity. Indeed, we observe a few extremely small donations () in Figure 2 for the Ethereum blockchain. In this robustness check, we keep only donations that are more than $30 for both Bitcoin and Ethereum. We aggregate our data again and re-run our models. As can be seen from Table 5, our findings remain unchanged.

6.2 Exclude ENS Users

In this robustness check, we exclude Ethereum users who adopted the Ethereum Name Service (ENS). ENS is a naming system to map human-readable names such as “chiemsee.eth” to a machine-readable wallet address like “0xe817FfE0893Dee3e870c37F94b6e2Ada2e02BBBc.” This naming service costs $8.80 and is a way for donors to reveal their identity. Past literature indicates that identity plays an important role in charitable giving as it is associated with additional extrinsic motivations such as reputation (Reinstein and Riener, 2012). The availability of ENS in Ethereum and its unavailability in Bitcoin could potentially make these two blockchains incomparable. Thus, we removed all the ENS users and re-run our DiD analysis for the full sample. We report the results in Table 6, and our findings stay robust.

| Dependent variable: | ||||

| Log() | Log() | Log() | Log() | |

| (1) | (2) | (3) | (4) | |

| Intercept | ||||

| (0.382) | (0.109) | (0.400) | (0.820) | |

| Time Dummy | Yes | Yes | Yes | Yes |

| Observations | 268 | 267 | 268 | 267 |

| R2 | 0.889 | 0.676 | 0.886 | 0.622 |

| Adjusted R2 | 0.776 | 0.343 | 0.768 | 0.233 |

| Note: | ∗p0.1; ∗∗p0.05; ∗∗∗p0.01 | |||

| Dependent variable: | ||

| Log() | Log() | |

| (1) | (2) | |

| Intercept | ||

| Time Dummy | Yes | Yes |

| Observations | 268 | 267 |

| R2 | 0.888 | 0.657 |

| Adjusted R2 | 0.773 | 0.303 |

| Note: | ∗p0.1; ∗∗p0.05; ∗∗∗p0.01 | |

6.3 Alternative Observation Window

In our main analysis, we consider the observation window from Feb. 26, 2022 to March 4, 2022, with the treatment lasting from the official confirmation of the airdrop till the planned snapshot. In this robustness check, we restrict the observation window to start on Feb. 26, 2022 and end at the cancellation of the airdrop on March 3, 2022. This time window captures the treatment more strictly. The exclusion of the post-intervention period further allows a conservative estimation of the treatment effect. We re-run our analyses and report the results in Table 7; our results stay consistent.

| Dependent variable: | ||

| Log() | Log() | |

| (1) | (2) | |

| Intercept | ||

| Time Dummy | Yes | Yes |

| Observations | 184 | 183 |

| R2 | 0.883 | 0.656 |

| Adjusted R2 | 0.763 | 0.296 |

| Note: | ∗p0.1; ∗∗p0.05; ∗∗∗p0.01 | |

7 Conclusions

7.1 Mechanism Discussions

From our analysis of the separate effects of the intervention in Section 5.1, we find that crypto rewards effectively increase donation counts but decrease average donation size. From our analysis of the comparative effects of the intervention in Section 5.2, we further find that the donation count increase is more aggressive for donations on Ethereum than Bitcoin. This is because the crypto rewards are much more likely to be issued on the Ethereum blockchain. However, the rewards did not affect donation sizes on Ethereum and Bitcoin in statistically different ways. Further split-sample studies reveal that there is a more aggressive decrease in average donation sizes from Ethereum for small donations but not for large donations.

These findings suggest that the extrinsic incentive in the format of crypto rewards has a positive impact on people’s decisions of whether to donate and a negative impact on the decision of how much to donate. Below we discuss the possible mechanisms that drive such findings. For the donation count increase, two mechanisms may be at play at the same time. First, the donation count increases because people are self-interested and want to profit from the crypto rewards. If this is the case, a fundraiser would need to increase the rewards to attract more donations, with no guarantee that the “net profit” of the fundraising activities would benefit from the rewards. While we cannot rule out this potential mechanism, we stress that the cost of rewards is low for crypto fundraising because the reward tokens are usually valueless in the beginning. The value of the rewards may increase later when the fungible or non-fungible tokens are sold, but the promotional expenditure will be paid by future buyers instead of the fundraising organizations. Thus, the crypto rewards are a novel way to reduce fundraising costs and improve the efficiency of fundraising. Meanwhile, we highlight the importance of the second mechanism that the donation count may increase because people use the rewards as an excuse to rationalize their prosocial behavior. This mechanism is likely at play because prospective donors respond more aggressively to Ethereum where the treatment is stronger. In addition, the donation sizes of crypto donations are generally large to indicate altruism (Jha, 2022). As we reported in Table 2, the median of the daily average donation size was $241.35 for Bitcoin and $364.49 for Ethereum before the airdrop. It was $195.66 for Bitcoin and $185.89 for Ethereum when the airdrop became available. As a matter of fact, the minimum daily average donation size was $87.46 for Bitcoin and $85.58 for Ethereum before the rewards were available and $84.57 for Bitcoin and $64.12 for Ethereum when the crypto rewards were available. If people donate purely for the purpose of profiting, they would not contribute so much because the Ukrainian government did not specify the crypto rewards, and donors have no way to evaluate the cost and benefit of their contributions accurately.

Similarly, two mechanisms could drive the decrease in contribution size. First, the average donation size decreased because the extrinsic rewards shifted people’s mindset from “a socially-minded altruistic perspective to a more economically minded, monetary perspective” Newman and Shen (2012, p.95). We believe that this mindset-shifting mechanism is at play because a stronger incentive (the intervention is stronger in Ethereum than in Bitcoin) corresponds to a more significant donation size decrease for small donations (). At the same time, the smaller average contribution size could be due to the selection process that donors who contributed when the airdrop was available systematically donated less because of their budget limitations or preferential reasons. While this mechanism is likely at play because we observe a reduction in donation size for both blockchains in our separate analysis, it does not affect the validity of the first mechanism because our results hold in the DiD analysis for small donations. Further, our results hold even if we remove opportunistic donors who made extremely small donations.

7.2 Managerial Implications

Our study generates rich implications for the crypto community. First, while ICO has been widely used as a promotional strategy for blockchain-based projects, its extension to support social causes that are not blockchain-based is a novel application that has never been studied. Our study suggests that ICO has a great potential to stimulate donations by either directly leveraging the self-interested motivation or making use of the excuses people need to behave prosocially. To increase the societal impact of blockchain technology and accelerate the adoption of blockchain, the founders and designers of blockchain should consider applying crypto rewards to various social movements and activities. Second, our finding also indicates the necessity for blockchains to support airdrops. While Bitcoin has a greater market cap than Ethereum, Ethereum has grown more rapidly than Bitcoin. Our study shows that Ethereum’s compatibility with smart contracts could effectively improve fundraising performance. Blockchain designers should continue to improve the design of blockchains to support airdrops better. For example, currently, airdrops can only be issued if a donor makes a direct transfer of funds to the recipient’s wallet. Donors who use intermediary platforms (e.g., Coinbase) will not receive the airdrop due to technology limitations. Blockchain designers can work with intermediary platforms to design and streamline the airdrop process better.

Our study is also important for fundraising organizations. While many non-profit organizations have started to accept cryptocurrency as donations, they have little experience in how to raise crypto funds. Our study suggests that crypto rewards are an effective way to acquire donors. Fundraisers can feature the potential value increase of the crypto rewards to encourage charitable giving. Such a strategy is likely effective for both self-interested and socially conscious people. In the meantime, we find a potential decrease in donation size. While this decrease only occurs in small donations, it suggests the possibility of motivation crowding-out that may be triggered in other crypto fundraising activities. Our findings that more aggressive donation size decrease happens only among small donations but not large donations inspire future works to propose strategies to alleviate such donation size decreases with better crypto reward designs.

Finally, our study is of great value for policymakers regarding blockchain legislation. Cryptocurrency is considered a capital asset for federal income tax. To enjoy tax benefits, people could donate cryptocurrency to avoid capital gains tax.888Crypto donations are tax-deductible at the fair market value at the time of the donations. We show that airdrops are effective promotional strategies for crypto fundraising. Policymakers should discuss topics about whether airdrops should be taxed and how they should be taxed. For example, when reward tokens are re-sold, the new buyers actually pay for the fundraising cost of the initial cause. The associated tax policy would play an important role in the implementation of crypto rewards in fundraising. In addition, our findings imply that with the presence of crypto rewards, donors take into account the future salience of a cause when making contributions. Crypto rewards could possibly change the allocation of funds in the society by making people more forward-looking.

7.3 Limitations and Future Works

Our study captures a unique crypto fundraising event, which was the first of its kind, to understand the impact of crypto rewards in fundraising for social causes. Despite the unique research opportunity and our best efforts, we have limitations that could be addressed by future studies.

First, while we analyzed both the separate effects and the comparative effects of crypto rewards, we did not compare the crypto rewards with other traditional thank-you gifts with a constant value. Future works could leverage experiments to understand how people perceive a thank-you gift of a fixed value and varying value differently. Second, we did not look into the specifications of crypto rewards as the fundraiser of our context did not specify the rewards. Future works could look into the design of crypto rewards (e.g., compare fungible tokens with non-fungible tokens). Third, we analyze a quasi-experiment, and our analysis is subject to corresponding limitations. The separate intervention analysis did not fully account for the time confoundedness, and the comparative study does not have a control group. While we have used various ways to account for such issues, a randomized controlled trial could better solve these challenges. Last but not least, our study focuses on the first crypto fundraising event for a social cause. As more and more fundraising activities use similar promotional strategies, the effect of the crypto rewards could decay over time. Future works can analyze the time effect on the effectiveness of an airdrop.

We believe that crypto fundraising is a fertile area for research and a promising tool for practice. We hope that our work paves the way for future studies to continue understanding how the invention of blockchain could transform into societal value.

Appendix A - ARIMA Model

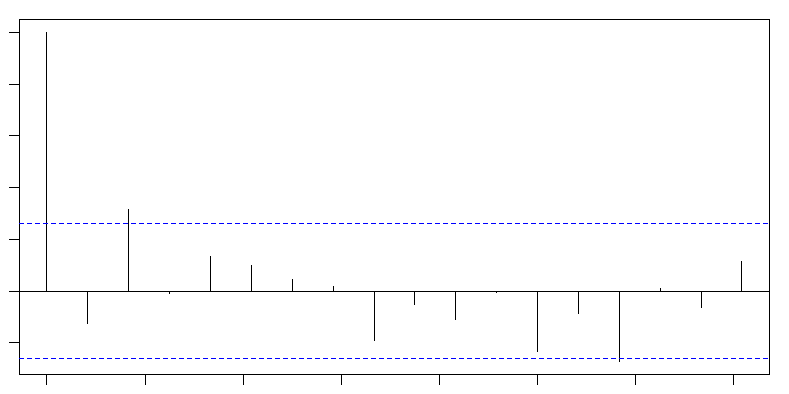

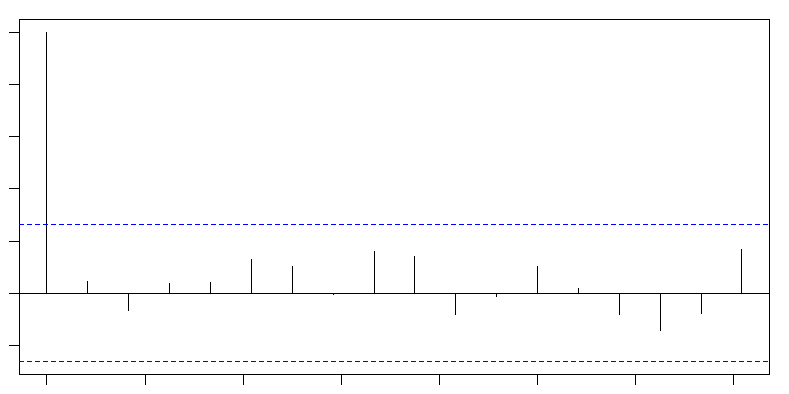

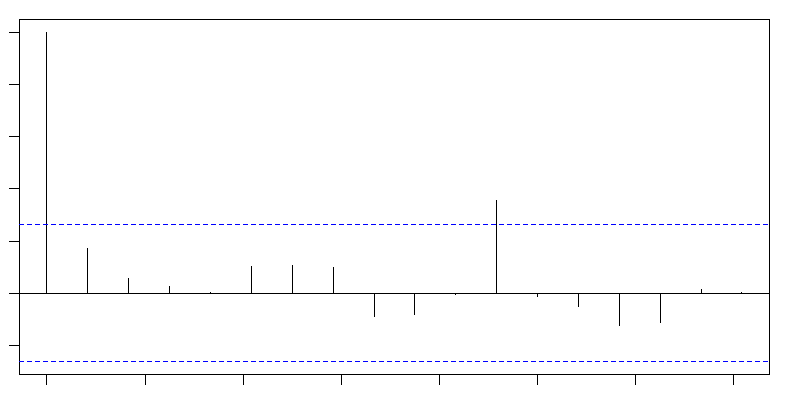

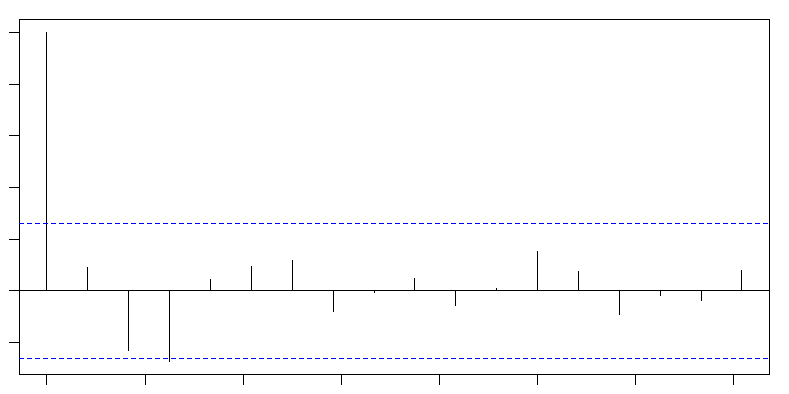

Below we present the ACF plots to show that the chosen ARIMA models are not affected by autocorrelation concerns. The ACF generates a numeric vector with the correlations of the residuals of the model. The x-axis corresponds to different lags of the residuals, and the y-axis represents the correlation. We can see from the figures below that the correlations are mostly between the significance level (the blue dashed lines). Thus, the residuals of our regressions are not autocorrelated.

References

- Alpizar et al. [2008] Francisco Alpizar, Fredrik Carlsson, and Olof Johansson-Stenman. Does context matter more for hypothetical than for actual contributions? evidence from a natural field experiment. Experimental Economics, 11(3):299–314, 2008.

- Angrist and Imbens [1995] Joshua Angrist and Guido Imbens. Identification and estimation of local average treatment effects, 1995.

- Arnold et al. [2019] Laurin Arnold, Martin Brennecke, Patrick Camus, Gilbert Fridgen, Tobias Guggenberger, Sven Radszuwill, Alexander Rieger, André Schweizer, and Nils Urbach. Blockchain and initial coin offerings: blockchain’s implications for crowdfunding. In Business transformation through blockchain, pages 233–272. Springer, 2019.

- Bénabou and Tirole [2006] Roland Bénabou and Jean Tirole. Incentives and prosocial behavior. American economic review, 96(5):1652–1678, 2006.

- Bernal et al. [2017] James Lopez Bernal, Steven Cummins, and Antonio Gasparrini. Interrupted time series regression for the evaluation of public health interventions: a tutorial. International journal of epidemiology, 46(1):348–355, 2017.

- Boom [2022] Daniel Van Boom. Crypto airdrop season: Why people are making thousands for ’free’, Jan 2022. URL https://www.cnet.com/personal-finance/crypto/crypto-airdrop-season-why-people-are-making-thousands-for-free/.

- Callaway and Sant’Anna [2021] Brantly Callaway and Pedro HC Sant’Anna. Difference-in-differences with multiple time periods. Journal of Econometrics, 225(2):200–230, 2021.

- Chao [2017] Matthew Chao. Demotivating incentives and motivation crowding out in charitable giving. Proceedings of the National Academy of Sciences, 114(28):7301–7306, 2017.

- Chao and Fisher [2021] Matthew Chao and Geoffrey Fisher. Self-interested giving: The relationship between conditional gifts, charitable donations, and donor self-interestedness. Management Science, 2021.

- Cointelegraph [2021] Cointelegraph. Bitcoin vs. ethereum: Key differences between btc and eth, Dec 2021. URL https://cointelegraph.com/ethereum-for-beginners/bitcoin-vs-ethereum-key-differences-between-btc-and-eth.

- Duflo [2001] Esther Duflo. Schooling and labor market consequences of school construction in indonesia: Evidence from an unusual policy experiment. American economic review, 91(4):795–813, 2001.

- Falk [2007] Armin Falk. Gift exchange in the field. Econometrica, 75(5):1501–1511, 2007.

- Felfe et al. [2015] Christina Felfe, Natalia Nollenberger, and Núria Rodríguez-Planas. Can’t buy mommy’s love? universal childcare and children’s long-term cognitive development. Journal of population economics, 28(2):393–422, 2015.

- Frey and Jegen [2001] Bruno S Frey and Reto Jegen. Motivation crowding theory. Journal of economic surveys, 15(5):589–611, 2001.

- Frey and Oberholzer-Gee [1997] Bruno S Frey and Felix Oberholzer-Gee. The cost of price incentives: An empirical analysis of motivation crowding-out. The American economic review, 87(4):746–755, 1997.

- Fricke [2017] Hans Fricke. Identification based on difference-in-differences approaches with multiple treatments. Oxford Bulletin of Economics and Statistics, 79(3):426–433, 2017.

- Gneezy and Rustichini [2000] Uri Gneezy and Aldo Rustichini. A fine is a price. The journal of legal studies, 29(1):1–17, 2000.

- Holmes et al. [2002] John G Holmes, Dale T Miller, and Melvin J Lerner. Committing altruism under the cloak of self-interest: The exchange fiction. Journal of experimental social psychology, 38(2):144–151, 2002.

- Hrywna [2022] Mark Hrywna. Crypto donations skyrocketed in 2021, Feb 2022. URL https://www.thenonprofittimes.com/technology/crypto-donations-skyrocketed-in-2021/.

- Jha [2022] Prashant Jha. Crypto donations jumped nearly 16x in 2021, new report says, Feb 2022. URL https://cointelegraph.com/news/crypto-donations-jumped-nearly-16x-in-2021-new-report-says.

- Kohn [2008] Alfie Kohn. The brighter side of human nature: Altruism and empathy in everyday life. Basic Books, 2008.

- Kontopantelis et al. [2015] Evangelos Kontopantelis, Tim Doran, David A Springate, Iain Buchan, and David Reeves. Regression based quasi-experimental approach when randomisation is not an option: interrupted time series analysis. bmj, 350, 2015.

- Liu and Feng [2021] Yuewen Liu and Juan Feng. Does money talk? the impact of monetary incentives on user-generated content contributions. Information Systems Research, 32(2):394–409, 2021.

- Miller [1999] Dale T Miller. The norm of self-interest. American Psychologist, 54(12):1053, 1999.

- Miller and Prentice [1994] Dale T Miller and Deborah A Prentice. Collective errors and errors about the collective. Personality and Social Psychology Bulletin, 20(5):541–550, 1994.

- Newman and Shen [2012] George E Newman and Y Jeremy Shen. The counterintuitive effects of thank-you gifts on charitable giving. Journal of economic psychology, 33(5):973–983, 2012.

- Ramaswamy [2022] Anita Ramaswamy. Why web3’s wealthy are donating crypto instead of cash, Mar 2022. URL https://techcrunch.com/2022/03/20/web3-charity-donate-crypto-cryptocurrency-nonprofit-cash/.

- Ratner et al. [2011] Rebecca K Ratner, Min Zhao, and Jennifer A Clarke. The norm of self-interest: Implications for charitable giving. The Science of Giving, pages 113–131, 2011.

- Reinstein and Riener [2012] David Reinstein and Gerhard Riener. Reputation and influence in charitable giving: an experiment. Theory and decision, 72(2):221–243, 2012.

- Schaffer et al. [2021] Andrea L Schaffer, Timothy A Dobbins, and Sallie-Anne Pearson. Interrupted time series analysis using autoregressive integrated moving average (arima) models: a guide for evaluating large-scale health interventions. BMC medical research methodology, 21(1):1–12, 2021.

- Sergeenkov [2022] Andrey Sergeenkov. What is a crypto airdrop?, Jan 2022. URL https://www.coindesk.com/learn/what-is-a-crypto-airdrop/.

- Shang and Croson [2006] Jen Shang and Rachel Croson. The impact of social comparisons on nonprofit fund raising. In Experiments investigating fundraising and charitable contributors, volume 11, pages 143–156. Emerald Group Publishing Limited, 2006.

- Strachan [2022] Maxwell Strachan. Ukraine canceled crypto airdrop because unethical investors wanted ’profit’, Mar 2022. URL https://www.vice.com/en/article/n7nk87/ukraine-canceled-crypto-airdrop-because-unethical-investors-wanted-profit.

- Time [2022] Time. How to donate crypto to ukraine?, Mar 2022. URL https://time.com/nextadvisor/investing/cryptocurrency/donate-crypto-to-ukraine/.

- Wing et al. [2018] Coady Wing, Kosali Simon, and Ricardo A Bello-Gomez. Designing difference in difference studies: best practices for public health policy research. Annu Rev Public Health, 39(1):453–469, 2018.

- Zlatev and Miller [2016] Julian J Zlatev and Dale T Miller. Selfishly benevolent or benevolently selfish: When self-interest undermines versus promotes prosocial behavior. Organizational Behavior and Human Decision Processes, 137:112–122, 2016.