Fitting Semiparametric Cumulative Probability Models for Big Data

Abstract

Cumulative probability models (CPMs) are a robust alternative to linear models for continuous outcomes. However, they are not feasible for very large datasets due to elevated running time and memory usage, which depend on the sample size, the number of predictors, and the number of distinct outcomes. We describe three approaches to address this problem. In the divide-and-combine approach, we divide the data into subsets, fit a CPM to each subset, and then aggregate the information. In the binning and rounding approaches, the outcome variable is redefined to have a greatly reduced number of distinct values. We consider rounding to a decimal place and rounding to significant digits, both with a refinement step to help achieve the desired number of distinct outcomes. We show with simulations that these approaches perform well and their parameter estimates are consistent. We investigate how running time and peak memory usage are influenced by the sample size, the number of distinct outcomes, and the number of predictors. As an illustration, we apply the approaches to a large publicly available dataset investigating matrix multiplication runtime with nearly one million observations.

Keywords: Cumulative probability models; semiparametric; big data

1 Introduction

Continuous outcomes often require a transformation prior to fitting linear models. The choice of transformation is not always clear, and different transformations may result in different conclusions. Semiparametric linear transformation models (Zeng and Lin, 2007) assume a linear model after a monotonic transformation which is nonparametrically estimated. The outcome and predictor variables are linked through an unobserved latent variable, where the latent variable is connected to the predictors as in a traditional linear model and to the outcome through an unknown monotonic transformation. These models are desirable because they require neither an explicit transformation of the outcome nor a model for the conditional expectation. Instead, the conditional distribution given covariate values is modeled, from which conditional expectations, quantiles, and other quantities can be derived.

Recently, Liu et al. (2017) showed that semiparametric linear transformation models can be fit using cumulative probability models (CPMs). CPMs have typically been reserved for the analysis of ordered categorical response variables; e.g., proportional odds and other “cumulative link models” (McCullagh 1980; Agresti 2010). With CPMs, the continuous outcome variable is effectively treated as if it were ordinal because what matters is the order of the outcome values, not the values themselves. Liu et al. (2017) showed that the multinomial likelihood used for CPMs is the likelihood of a semiparametric linear transformation model. Using computer simulations, they showed that CPMs perform well in many scenarios. Under mild conditions, CPMs yield estimates that are consistent and asymptotically normal (Li et al. 2021).

Because the transformation between the outcome and the latent variable is modeled nonparametrically, CPMs can be slow to fit with large samples, especially when there are many unique outcome values (Liu et al., 2017). The sparse nature of the score and Hessian matrices of CPMs can be exploited to make computation feasible for sample sizes in the thousands (Harrell, 2020). However, even when employing computationally efficient algorithms, CPMs are not able to handle larger sample sizes. For example, we cannot fit a CPM to a simulated dataset with 50,000 distinct outcomes on a server with 48 cores and 192 gigabytes of memory. The robustness and flexibility of CPMs make them desirable for analyses of large datasets; however, current big data implementations are not feasible.

The purpose of this paper is to describe and evaluate methods for fitting CPMs for big data, either by reducing the sample size through dividing the data into subsets or by reducing the number of distinct outcomes via binning or rounding. In Section 2, we introduce three approaches to fitting a CPM for a large dataset. In the divide-and-combine approach, the sample size of each individual CPM is greatly reduced. In the binning and rounding approaches, the outcome variable is redefined to have a greatly reduced number of distinct values. We carry out computer simulations to evaluate and compare these approaches in Section 3, and apply them to a real data example in Section 4. Section 5 contains a discussion.

2 Methods

2.1 Cumulative probability models

In this subsection we briefly describe cumulative probability models (CPMs) and relevant notation; details can be found in Liu et al. (2017). One way to motivate CPMs for a countinuous outcome is through a linear transformation model,

| (1) |

where is a vector of predictors, with known, and the transformation is assumed to be non-decreasing and otherwise unknown. It is easy to show that for any ,

Let and . Then model (1) becomes a CPM,

| (2) |

where is a link function. The “intercept” in the CPM has a nice interpretation: It is a transformation of the outcome such that the transformed value is related to the predictors linearly. This is because model (1) can be alternatively expressed as .

Now consider a dataset , where is the sample size. We first consider the scenario where there are no ties in the outcomes. The CPM in (2) becomes

| (3) |

where . Without loss of generality, we assume ; then . Model (3) is identical to some models for ordered categorical outcomes: for example, proportional odds model (when is the logistic distribution) and probit model (when is the normal distribution). It becomes the proportional hazards model when is the left-skewed Gumbel distribution.

As described in Liu et al. (2017), the nonparametric likelihood for the model is

Here is an auxiliary parameter and . Because is maximized when and , it can be simplified as

| (4) |

This is the same as the likelihood when the outcomes are treated as if they were ordered categorical. We can obtain the nonparametric maximum likelihood estimates (NPMLE) from this likelihood. Then the NPMLE of the transformation function is . It is an increasing step function, with a step for each of the intervals between adjacent outcome values from to .

When there are ties in the outcomes, the above derivations still apply with a slight modification. Here model (3) is applicable for every distinct outcome value, and for each such value, there is a corresponding value. Let be the number of distinct outcome values. The NPMLE of becomes , an increasing step function with a step for each of the intervals between adjacent distinct outcome values.

Using modern empirical process theory and under mild regularity conditions, Li et al. (2021) showed the consistency and asymptotic normality of the NPMLEs, . Asymptotic theory relies on compactness of the estimator of , which does not hold if is unbounded. Hence, Li et al (2021) specify lower and upper bounds for , and respectively, such that any observation outside the the interval is censored. The corresponding censored data likelihood is equivalent to a likelihood that treats these values as belonging to the lowest / highest ordered categories. Under this censoring, is consistent for for . In addition, converges weakly to a tight Gaussian process whose variance can be estimated as the inverse of the Hessian matrix. Furthermore, the asymptotic variance of attains the semiparametric efficiency bound. Details are in Li et al. (2021).

The Hessian matrix has dimensions . Because of the special structure of the likelihood function (4), the portion of the Hessian matrix with respect to the alpha parameters is tridiagonal. This allows matrix inversion efficiently through Cholesky decomposition (Sall 1991). Taking advantage of these facts, Harrell implemented a computationally efficient algorithm in the orm() function in the rms R package (Harrell 2020) to fit CPMs. However, as the number of parameters increases with the number of distinct outcome values, the function eventually fails for very large datasets due to heavy demand on computation time and memory usage. The next three subsections describe approaches to fit CPMs for very large datasets.

2.2 Divide and combine

In the divide-and-combine approach, the data are evenly divided into subsets, a CPM is fit to each subset, followed by a final step to aggregate all the information. The goal is to make the sample sizes of the subsets small enough to fit CPMs relatively quickly with a reasonable amount of computer resources. Let be a target number of subsets, and be the size of subset (). If is a multiple of then . If not, our implementation ensures that for any two subsets. Let be the number of unique outcome values in subset . Let be the vector of parameter estimates from subset , where has length and has length . Let be the -th element of .

As is estimated nonparametrically, it is defined only over the range of outcomes in the data used to fit a CPM. To ensure that is available over the widest range of outcomes from all the subsets, in the partition step, we randomly assign the observations that have the smallest outcome values one to each subset, and similarly, randomly assign the observations that have the largest outcome values one to each subset. The rest are allocated to the subsets randomly. This way, will be available from all the subsets over the interval , spanning from the -th smallest to the -th largest outcome values.

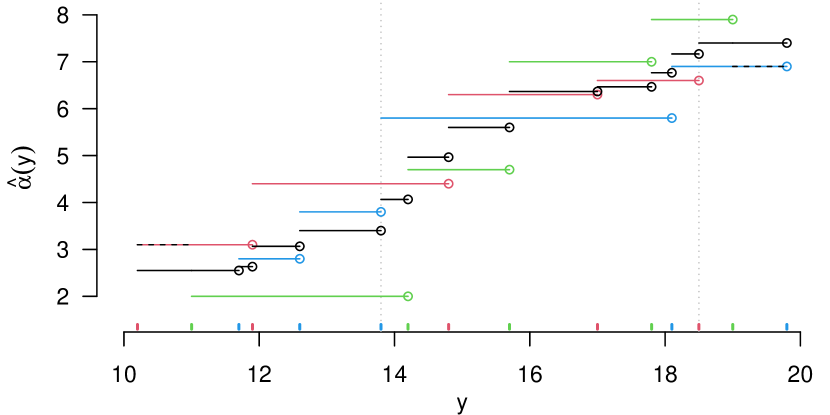

After fitting individual CPMs to subsets, we compute the estimates of (an -vector) and (a -vector). The estimates of the beta parameters are straightforward to compute as they are the average of the corresponding beta estimates from the subsets. However for a parameter in , due to random partitioning, the corresponding alpha estimates in the subsets can be at different index positions; we thus define a -vector for each parameter to indicate which estimate from the individual models will be used in the computation. Figure 1 illustrates the definition. For example, a -vector of indicates that the corresponding estimate is an average of . The first and last several parameters in will not have estimates available from all the subsets; in the -vector, we use to indicate that the corresponding model is not contributing. There are at most such alpha parameters at each end. -vectors can also be defined for the beta parameters: for , for , etc.

Once we have defined all the -vectors, we can compute the final parameter estimates. Given a -vector , the corresponding parameter estimate is an average,

When , the average is always over values. Since is non-decreasing for every , the final alpha estimates over are also non-decreasing. This monotonicity is not guaranteed at the ends. To ensure monotonicity at the ends, we apply the following constraints sequentially: Backwardly for , if then set ; forwardly for , if then set .

The estimates of using this divide and combine approach for a fixed are consistent and asymptotically normal under the same conditions that are required for consistency and asymptotic normality of the standard CPM estimators. In short, under these conditions, each of the estimates in the separate analyses is consistent and asymptotically normal, and as the analyses are independent, their average is also consistent and asymptotically normal.

Because of the independence between the separate analyses, the variance-covariance matrix for can be computed easily with -vectors. Let be the variance-covariance matrix of , and be its element at . The variance of a parameter in with -vector is estimated as

The covariance between a parameter with -vector and another with -vector is estimated as

We note that the variance estimates for the alpha parameters at the ends may be slightly overestimated because the monotonicity constraints would likely reduce the variation of the final estimates. The whole variance-covariance matrix has dimensions , which can be very large. For example, when and , the matrix has more than 10 billion numbers. This is a challenge in both computation and storage. In our implementation, we calculate the diagonal values (i.e., the variances) for the alpha portion and the full variance-covariance matrix for the beta portion. One consequence of this choice is that the conditional mean or median given covariate values would not have an estimated standard error as they require covariances in the computation.

2.3 Equal-quantile binning

In equal-quantile binning, we first group the outcomes into equal-quantile bins and then assign a new outcome value to the observations in each bin. Specifically, we define a new outcome variable, , which for each bin , takes the value for all the observations in the bin. When there are not many ties in the original outcome, the number of distinct values in is often the number of bins, , which can be predetermined. We then fit a CPM of on the predictor variables.

To ensure that the observations are divided to bins as evenly as possible, we implement the following algorithm: Express as

where is the floor of (i.e., the quotient) and is the remainder (i.e., ); when is a multiple of . There will be bins, each with observations, and bins, each with observations. To achieve this, we first generate a random list of length , in which the value occurs times and occurs times. We then sort the observations by the outcome, and group them according to the values in the random list. For example, if the list is , those with the smallest outcome values are in the first bin, the next set of observations are in the second bin, etc.

One advantage of binning is that it is scale-independent with respect to the outcome, a feature shared by the CPM itself. Another advantage is that it allows us to control the refinement in the new outcome variable because the number of bins can be predetermined. Note that in the binning approach, extends only to the median values of the first and last bins instead of the ends of the original outcome.

It is well-known that with ordinal data, CPMs estimate the same beta parameter if one combines adjacent ordinal categories [REF]. Similarly, with continuous data, when one bins outcomes, one estimates the same beta parameter as if one had fit a CPM to the continuous data. Specifically, let , where is the binning function. From (1), where is the resultant transformation from the latent variable scale to the binned observed outcome scale. Because is monotonic, then is monotonic, although the inverse transformation, , is not one-to-one because of the binned nature of the data. The estimator for , , remains consistent and asymptotically normal. The estimator, is consistent for which is a discretized version of . As the binning becomes finer, i.e., , . Hence, as one would expect, the accuracy of for estimating depends on the fineness of the binning. With that said, with large sample sizes and continuous data, any bias in due to binning except in the tails of the distribution, is often negligible, as will be seen in Section 3.

2.4 Rounding with refinement

Rounding can also reduce the number of distinct outcomes. While binning can substantially redefine the outcomes at the extreme ends, rounding often keeps those values nearly unchanged. For example, suppose the largest five values of a dataset are , and bins are chosen to be of size 5. Then binning would collapse these values to their median, . In contrast, rounding to integers would keep these values largely unchanged with little loss of information. However, rounding to a decimal place can be a poor choice for skewed outcomes. For example, suppose the smallest five observations from that same dataset are . Then rounding to the integer could result in a substantial loss of information at the lower end. For this reason we consider two general rounding strategies: rounding to decimals and rounding to significant digits. We also describe a refinement step, which allows both rounding strategies to approximately result in a target number of distinct values.

Let be an integer, and be the result of rounding a number to decimal place (when ), to an integer (when ), or to (when ). For example, , , and . When , we omit the subscript and write . Let () be the result of rounding to significant digits. Let be the place of the first significant digit of . Then . For example, .

We now refine these two types of rounding. When we round to an integer, is the integer that is closest to . We could refine this by rounding to the closest multiple of , which is effectively . Similarly, is to round to the closest multiple of . In general, for any real number , is to round to the closest multiple of . As increases from to , more refined rounding is achieved; when , we reach . For any integer and any number , we define

as the value after rounding to place at refinement level . When , ; as increases, becomes more refined and . Similarly, for any integer and any number , we define

as the value after rounding to significant digits at refinement level . When , ; as increases, becomes more refined and .

We now describe the two rounding algorithms for a given dataset. Let

be the number of distinct values after rounding the outcomes to

place at refinement level . Similarly, let be that after

rounding to significant digits at refinement level . Let

be a target number of distinct outcomes after rounding. Our two

rounding algorithms are:

Decimal place rounding with refinement:

-

(Ia)

Identify such that ;

-

(Ib)

If , set . Otherwise, search over a grid in to identify such that is closest to , as measured by the smallest ;

-

(Ic)

Define a new outcome variable such that its value is for observation .

Significant digit rounding with refinement:

-

(IIa)

Identify such that ;

-

(IIb)

If , set . Otherwise, search over a grid in to identify such that is closest to , as measured by the smallest ;

-

(IIc)

Define a new outcome variable such that its value is for observation .

In our implementation of these rounding algorithms, the grid for has increment of , and the resulting numbers of distinct values in have been always different from the target number . Compared to the binning approach, these rounding approaches do not require sorting of the outcomes, but they are scale-dependent with respect to the outcome.

The theoretical justification for rounding is identical to that for binning because they both merge adjacent values in discretized categories.

3 Simulations and Results

3.1 Simulation setup

We simulated datasets with various sample sizes and with predictor variables. Half of the predictors are binary with success probabilities ranging from 0.05 to 0.5, and half are continuous from normal distributions with mean ranging from 0 to 2.4 and variance 1. The beta coefficients for half of the predictors were specified in the range and those for the other predictors were set as zero. We then generated , where , and . We considered six scenarios, corresponding to the combinations of three options for and two options for . The three options for are: (1) , for which the inverse is ; (2) , for which ; and (3) , where is added to ensure for all the simulated ; for this transformation, . The two options of are: (i) the logistic distribution ; (ii) the Gumbel distribution .

We simulated datasets with sample size , and . The smaller sample sizes allow us to compare the three new approaches with the “gold standard” approach of fitting a single CPM to the original data. We also compared the parameter estimates with the true parameters used in data generation. In the divide-and-combine approach, the data were partitioned into subsets when , when , and when . In the binning approach, the outcomes were grouped into bins when , and bins otherwise. In the rounding approach, the outcomes were rounded with a target number of when , and otherwise. These settings are displayed in Table 1.

| Truth | Whole data | Divide-and-combine | Binning | Rounding | ||

|---|---|---|---|---|---|---|

| ✓ | ✓ | ✓() | ✓() | ✓() | ||

| ✓ | ✓ | ✓() | ✓() | ✓() | ||

| ✓ | ✓() | ✓() | ✓() |

The endpoints we evaluated include: (1) the estimates of the parameters in and , and their standard errors; (2) estimates of conditional mean and median at 10 sets of randomly selected from the simulated datasets. Specifically, let () be the -th smallest distinct outcome value. Given , the cumulative distribution function of is estimated as when , and when . The corresponding probability mass function is estimated as (), where . We then computed the conditional mean, ; and the conditional median as the average of the two adjacent and for which and . The true conditional mean and median at were empirically obtained by first generating values of and corresponding , and then computing their mean and median.

3.2 Simulation results

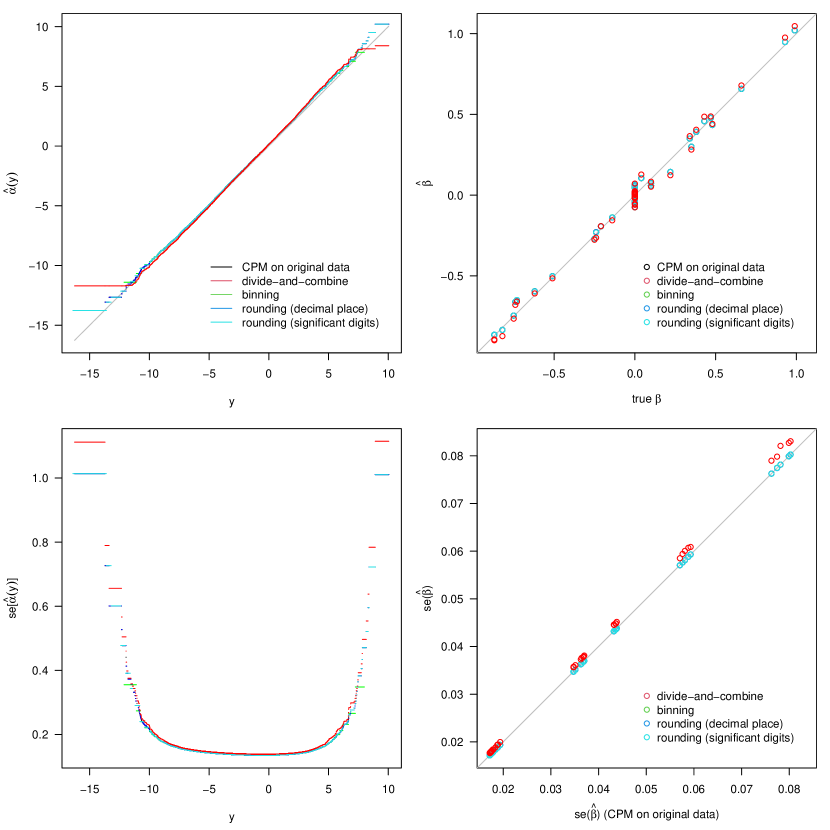

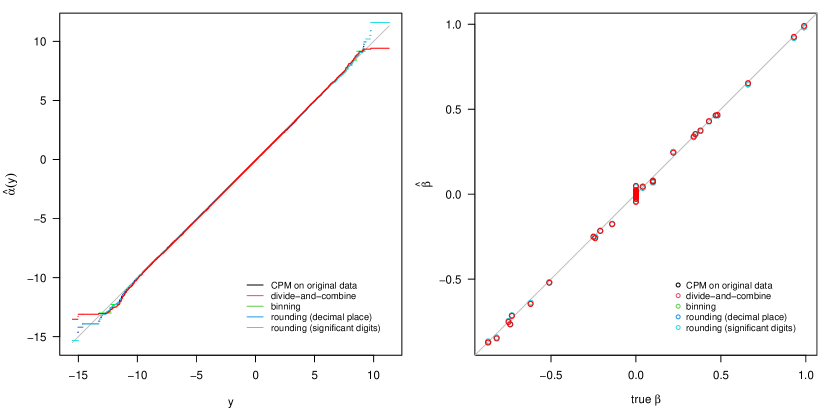

Figure 2 shows the parameter estimates and their standard errors from the three new approaches for the simulation scenario with logistic residual distribution, identity transformation , and . The results of the “gold standard” approach of fitting a CPM with the whole dataset are also shown.

The from all the approaches agreed very well with the true over a wide range of from percentile to percentile. The standard error for was also relatively low in this range due to the high data density. There was some departure of from the truth at the ends, with relatively high standard errors, probably due to a lack of information as a result of data sparcity.

In the divide-and-combine approach, started to nearly flatten out at and . This approach also yielded slightly higher standard errors than the other approaches. In the binning approach, by definition, extends only to the median values of the first and last bins. The rounding to decimal place approach had nearly identical estimates of the alpha parameters and their standard errors as the “gold standard” approach. This is because the outcome in this simulation scenario had a relatively symmetric distribution, for which rounding to a decimal place tends to have little effect at the ends where the values are relatively large. In comparison, rounding to significant digits tends to have a slightly larger effect at the ends.

The estimates of the beta parameters were also quite accurate for all approaches. The binning and rounding approaches and the “gold standard” approach had nearly identical estimates of the beta parameters and their standard errors. In comparison, the divide-and-combine approach yielded slightly different parameter estimates and slightly higher standard errors.

The results for the other transformations and for the Gumbel residual distribution showed similar patterns (Supplemental Material). Note that for very skewed outcomes, the rounding to significant digits approach had nearly identical estimates of all the parameters and their standard errors as the “gold standard” approach, while rounding to a certain decimal place rounded many values at the lower end to a single value, which is undesirable.

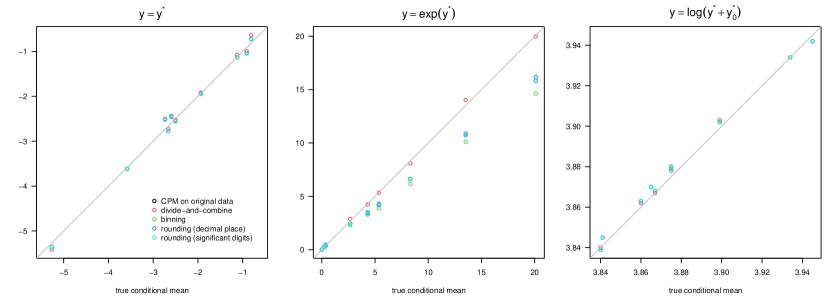

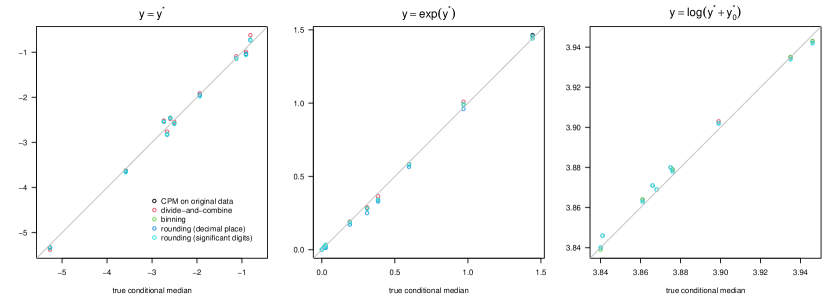

Figure 3 shows the estimated conditional mean and median for 10 sets of randomly selected from the simulated datasets. When the conditional distribution is relatively symmetric, as in the scenarios with and , the estimation of conditional mean performed well. When the conditional distribution is very skewed, as in the scenario with , the estimation of conditional mean performed poorly. We repeated the simulations under the latter scenario with multiple replicates and found a high variation in the results, presumable due to high variation in the alpha estimates at the high end of the outcomes. The pattern we observed seems to be overestimation from the divide-and-combine approach and underestimation from the other approaches including the “gold standard” CPM on the original data. In contrast, the conditional medians performed quite well for all the approaches in all the scenarios. The results for the Gumbel residual distribution have similar patterns (Supplemental Material).

Figure 4 shows the estimates of the parameters for sample sizes and with logistic residual distribution and . In comparison to the results for in Figure 2, a larger sample size clearly led to a smaller difference between the estimates and the truth, illustrating that the approaches yield consistent parameter estimates. The standard error estimates also became smaller as the sample size increased (Supplemental Material).

The divide-and-combine approach introduces variation due to random partitioning. However, the variation due to random partitioning is minor relative to that from random sampling (see details in Supplemental Material).

3.3 Time and peak memory usage

To help determine the number of subsets in the divide-and-combine approach

and the target number of distinct values in the binning and rounding

approaches, we evaluate the running time and peak memory usage when fitting a

single CPM with respect to the sample size, the number of distinct outcome

values, and the number of predictors. We generated datasets with various

values of (sample size: ),

(number of distinct outcome values: ), and

(number of predictors: ). All variables were continuous.

When , equal-quantile binning was used to achieve the desired .

There are 18 combinations of and for each value of , and there are

a total of 72 datasets. We fit orm() to each dataset and recorded the

running time and peak memory usage.

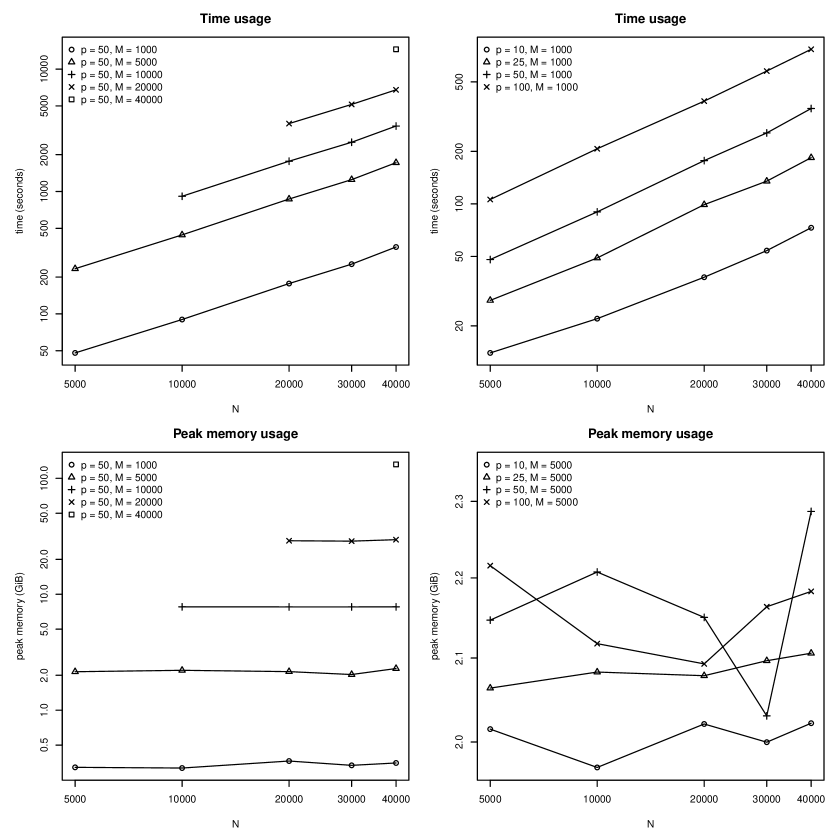

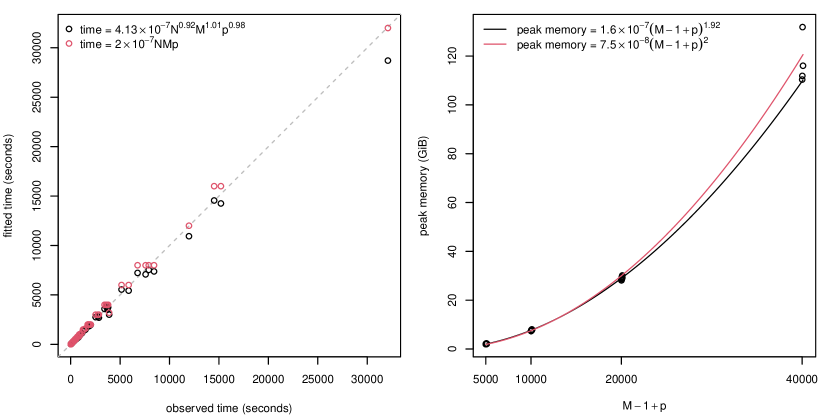

The top row in Figure 5 shows the time usage with respect to changes in and when (left), and with respect to changes in and when (right). The patterns are similar for other values of and . The results indicate a log-log linear relationship of time on , , and . We therefore fit a log-log linear model, which is multiplicative on the time scale: ; this model had . Thus time is approximately proportional to ; we found that seems to fit well to our results. The left panel of Figure 6 shows the comparison of the observed running time and the fitted values from these two models. Note that the constant factor depends on our server configuration and may vary greatly across hardware configurations.

The bottom row in Figure 5 shows the peak memory usage under the same settings as in the top row; again, the results for other values of and have similar patterns. The results suggest that peak memory usage is influenced heavily by , to a much less degree by , and almost ignorably by . An examination of the log-log plot of peak memory usage versus (in Supplemental Material) suggested that the peak memory usages for datasets with fall along a line while those for are far above that line, presumably due to overhead operations that can dominate memory usage for a relatively small . We thus fit a log-log linear model to the results with , which led to: , with . This model suggests that peak memory usage is approximately proportional to , at least for . This makes sense as the memory usage is probably devoted mostly to the Hessian matrix, which has dimensions . For our data, seems to fit well. The right panel of Figure 6 shows the peak memory usage versus , and the curves of these two models.

The results that the running time of a single CPM is approximately proportional to and that the peak memory usage is approximately proportional to is helpful when determining the number of subsets in the divide-and-combine approach and the target number of distinct values in the binning and rounding approaches. In the divide-and-combine approach, a subset has much smaller and than those in the original data, and the individual jobs take much less time and memory to run. This also allows simultaneous model fitting for multiple subsets, further speeding up the process. In the binning and rounding approaches, and are typically much smaller than in the original data. As a result, these approaches also take much less time and memory, making it feasible to fit a CPM even with a large sample size.

4 A Data Example

We applied our approaches to a publicly available dataset, in which an

algorithm for multiplying two matrices of dimensions was

evaluated for its running time on a parameterizable SGEMM GPU kernel

(Nugteren and Codreanu 2015; Ballester-Ripoll et al. 2017). The algorithm

has 14 parameters, and parameter combinations were feasible due

to various kernel constraints. For each combination, 4 runs were performed

and the running time was recorded in milliseconds. For this dataset,

and , and there are distinct outcome

values. More details can be found at the University of California Irvine

Machine Learning Repository

(http://archive.ics.uci.edu/ml/datasets/SGEMM+GPU+kernel+performance).

The outcome variable, the algorithm running time, is very skewed, with skewness 3.93 and a range from 13.25 to 3397.08 milliseconds. One could apply a transformation (e.g., logarithm) on the outcome and then fit a linear model, not knowing if the transformation would be a good choice. The CPM instead allows us to obtain a suitable transformation empirically.

| range | # obs | # distinct values | |||||

|---|---|---|---|---|---|---|---|

| 563831 | 8453 | 88 | 862 | 862 | 8453 | 4424 | |

| 368366 | 70217 | 900 | 8855 | 900 | 8855 | 4635 | |

| 34203 | 28129 | 1875 | 12356 | 207 | 1875 | 1009 | |

| Total | 966400 | 106799 | 2863 | 22073 | 1969 | 19183 | 10068 |

We fit CPMs of the outcome on the 14 predictor variables with the three methods described in Section 2. In the divide-and-combine approach the data were divided into subsets of size or . In binning and rounding, the target number of distinct outcome values was set as , and the final numbers of distinct outcome values were and , respectively. For rounding, we chose to round to significant digits. The rationale behind this decision can be seen in Table 2, where we divide the outcomes into three regions: , , and those . The 2nd and 3rd columns display the number of observations and the number of distinct outcome values in these regions. For this dataset, rounding to a decimal place (columns 4–5) would result in very few distinct values representing the outcomes in , but a lot more distinct values representing the outcomes that are . In contrast, rounding to a certain number of significant digits (columns 6–8) gives more balanced categorizations of the outcome. The selected rounding scheme was rounding to significant digits at refinement level (column 8), resulted in a fairly good balance and . The divide-and-combine approach took 2 hours 37 minutes on our server while the binning and rounding approaches each took 7 hours 12 minutes.

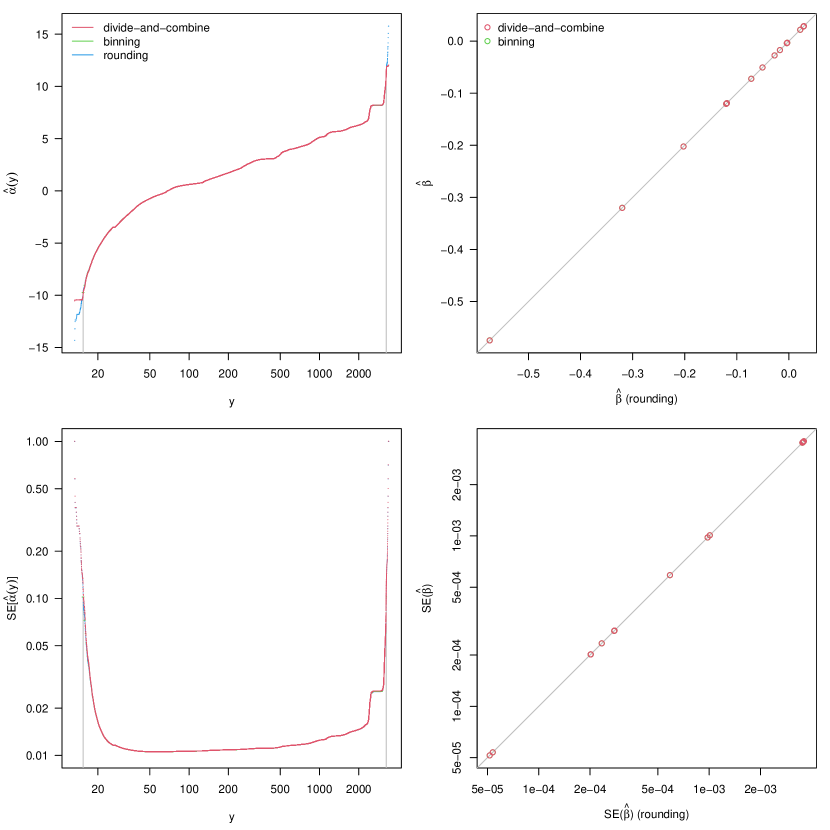

The results are summarized in Figure 7. The top left plot shows the alpha estimates as functions of the outcome. The outcome range was in the original data, after binning, and after rounding. The three alpha estimates agreed remarkably well with each other from the percentile to the percentile of the outcome . Note that is an estimated transformation of the outcome such that the transformed value would relate to the predictors linearly. Here all three are very different from a log transformation, which would be a straight line on this plot as the x-axis is on the log scale. This indicates that the true transformation must be very different from logarithm, which would often be used to transform a skewed outcome in a traditional analysis. The bottom left plot shows the standard errors of the alpha estimates, which are also very similar from to percentiles. The top right plot of Figure 3 shows comparisons of the beta estimates from the three methods, with the results of rounding on the x-axis and those of the other two methods on the y-axis. Again, the three methods’ beta estimates and standard errors (bottom right plot) agree remarkably well.

5 Discussion

Cumulative probability models (CPMs) are a robust alternative to linear models. However they are not feasible for very large datasets as the running time and memory usage increase with the sample size, the number of distinct outcomes, and the number of predictors. In this paper, we addressed this problem with three approaches. The divide-and-combine approach focuses on reducing the sample size of individual CPMs, and the binning and rounding approaches focus on reducing the number of distinct outcome values. With computer simulations, we showed that these approaches perform quite well, with estimates of parameters and their standard errors very similar to those from a single CPM on the whole dataset (when the latter is feasible), and with consistent parameter estimates. The rounding approach has two algorithms, rounding to a decimal place (for not-too-skewed outcomes) and rounding to significant digits (for skewed outcomes). Both algorithms have a refinement step to achieve the desired number of distinct outcomes. All three approaches yielded comparable results when applied to a large dataset with nearly one million observations.

We also studied the running time and peak memory usage in relation to the sample size , the number of distinct outcomes , and the number of predictors . We showed that the running time is approximately proportional to , and that the peak memory usage is approximately proportional to . These results can help plan the analysis by determining the number of subsets in the divide-and-combine approach and the number of target distinct outcomes in the binning and rounding approaches. There is a trade-off between speed and accuracy. Therefore, for the divide-and-combine approach, we recommend as few subsets as allowed by computer resources, and for the binning and rounding approaches, we recommend as large target number of distinct outcomes as allowed by computer resources.

There are some limitations in the divide-and-combine approach. When the sample size is very large, computation of the covariances in the variance-covariance matrix will be infeasible as it requires a large amount of storage space. In addition, when a predictor variable has a vast majority of the observations having one value and only a few observations having a different value, a subset may have all its observations having the same value in the variable. In this case, there would be no estimate for the corresponding coefficient. Similarly, a categorical predictor variable having a rare category may also cause a problem. Therefore it might be necessary to pre-screen and remove such predictor variables, or consider the predictor variables when dividing the data in a manner to ensure feasible estimation in each subset. Given these limitations of the divide-and-combine approach and the simplicity of binning and rounding, one might prefer one of the latter approaches.

We focused on generic binning and rounding algorithms: equal-quantile binning, rounding to a decimal place, and rounding to significant digits. Alternative, and probably more ad hoc, binning and rounding approaches might be desirable in certain applications. For example, one might bin the outcome with more convenient or interpretable cutoff values, or transform the outcome to a different scale and then round it, or round the outcome differently in different regions.

In summary, we have provided three approaches to the problem of fitting CPMs

to big data. They perform quite well and take a reasonable amount of time

and computer resources to finish. These approaches have been implemented in

our cpmBigData R package.

6 References

Zeng D, Lin DY. Maximum likelihood estimation in semiparametric regression models with censored data. J R Stat Soc Series B (Methodol). 2007;69(4):507–564.

Liu Q, Shepherd BE, Li C, Harrell Jr FE. Modeling continuous response variables using ordinal regression. Statistics in Medicine. 2017;36:4316–4335.

McCullagh P. Regression models for ordinal data. J R Stat Soc Series B (Methodol). 1980;42(2):109–142.

Agresti A. Analysis of Ordinal Categorical Data. Second edn. Hoboken, New Jersey: John Wiley & Sons; 2010.

Li C, Zeng D, Tian Y, Shepherd BE. A semiparametric transformation model for continuous outcomes. 2021 (submitted)

Sall J. A monotone regression smoother based on ordinal cumulative logistic regression. In: ASA Proceedings of Statistical Computing Section, Atlanta, Georgia; 1991:276–281.

Harrell FE. rms: Regression modeling strategies.

http://CRAN.R-project.org/package=rms, R package version 6.0-1; 2020.

Nugteren C, Codreanu V. CLTune: A generic auto-tuner for OpenCL kernels. In 2015 IEEE 9th International Symposium on Embedded Multicore/Many-core Systems-on-Chip; 2015.

Ballester-Ripoll R, Paredes EG, Pajarola R. Sobol tensor trains for global sensitivity analysis. arXiv Computer Science / Numerical Analysis. 2017;arXiv:1712.00233