Large Bayesian VARs with Factor Stochastic Volatility: Identification, Order Invariance and Structural Analysis

Abstract

Vector autoregressions (VARs) with multivariate stochastic volatility are widely used for structural analysis. Often the structural model identified through economically meaningful restrictions—e.g., sign restrictions—is supposed to be independent of how the dependent variables are ordered. But since the reduced-form model is not order invariant, results from the structural analysis depend on the order of the variables. We consider a VAR based on the factor stochastic volatility that is constructed to be order invariant. We show that the presence of multivariate stochastic volatility allows for statistical identification of the model. We further prove that, with a suitable set of sign restrictions, the corresponding structural model is point-identified. An additional appeal of the proposed approach is that it can easily handle a large number of dependent variables as well as sign restrictions. We demonstrate the methodology through a structural analysis in which we use a 20-variable VAR with sign restrictions to identify 5 structural shocks.

Keywords: vector autoregression, factor model, stochastic volatility, Bayesian model comparison, sign restriction

JEL classifications: C11, C35, C52, E44

1 Introduction

Bayesian vector autoregressions (VARs) with multivariate stochastic volatility, first developed in Cogley and Sargent (2005) and Primiceri (2005), are now the workhorse models in empirical macroeconomics. These multivariate stochastic volatility models, however, have the undesirable property that the implied likelihoods are not invariant to the order of the dependent variables.111This non-invariance problem is explicitly acknowledged and discussed in both Cogley and Sargent (2005) and Primiceri (2005). See also the discussion in Carriero, Clark, and Marcellino (2019). This ordering issue has become an increasingly pertinent problem due to two prominent developments in the VAR literature. First, in the last two decades there has been a gradual departure from conventional recursive or zero identification restrictions to other more credible identification schemes—such as identification by sign restrictions (Faust, 1998; Canova and De Nicolo, 2002; Uhlig, 2005)—that do not restrict the order of the variables. Despite this development, models of Cogley and Sargent (2005) and Primiceri (2005) continue to be used to first obtain reduced-form estimates, which are then taken as inputs in the subsequent structural analysis. Since the reduced-form estimates are not order invariant, the results from the structural analysis depend on the order of the variables in a subtle way, often without explicit recognition by the user.222The implications of this non-invariance problem for structural analysis have been illustrated in Bognanni (2018) and Hartwig (2019).

Second, following the seminal contributions by Banbura, Giannone, and Reichlin (2010) and Koop (2013), there is an increasing desire to use large VARs involving more than dozens of dependent variables for structural analysis. This development is partly motivated by the concern of informational deficiency of using a limited information set—by expanding the set of relevant variables, one can alleviate this concern (see, e.g., Hansen and Sargent, 1991; Lippi and Reichlin, 1993, 1994). However, unless there is a natural variable ordering (e.g., using recursive identification restrictions), the ordering issue becomes more severe as the number of ways to order the variables increases exponentially with the number of variables.

In view of these developments, we consider an alternative Bayesian VAR based on the factor stochastic volatility that is constructed to be invariant to the order of the dependent variables. Factor stochastic volatility models are commonly used for modeling high-dimensional financial data, but are less widely employed in empirical macroeconomics.333A notable exception is Kastner and Huber (2020), who use Bayesian VARs with factor stochastic volatility for macroeconomic forecasting. Carriero, Clark, and Marcellino (2018) consider a related multiplicative 2-factor stochastic volatility model to study the impact of macroeconomic and financial uncertainty. In specifying a suitable factor stochastic volatility model, there is often a tension between identification and order invariance. On the one hand, one can identify the factors and the associated factor loadings by fixing the orientation of the factors (e.g., as in Geweke and Zhou, 1996; Chib, Nardari, and Shephard, 2006). But this identification strategy essentially fixes the order of the variables, and therefore the identified model is not order invariant (see, e.g., the discussion in Chan, Leon-Gonzalez, and Strachan, 2018). On the other hand, one could avoid fixing the orientation of the factors and obtain an order-invariant model, but it is unclear that the factors and the loadings are identified.444For example, Kastner (2019) does not impose any orientation restrictions on the factors, arguing that identification of the factor loadings is not necessary for his purpose of estimating the reduced-form covariance matrix.

We solve this dilemma between achieving identification and order invariance by carefully teasing out a set of conditions strong enough for identification, yet they are weak enough that the model remains order invariant. More specifically, we construct a VAR in which the innovations have a factor structure, and both the factors and the idiosyncratic errors follow stochastic volatility processes. We first show that the likelihood implied by this model is invariant to the order of the dependent variables. We then discuss sufficient conditions for identification of the factors and the factor loadings, building upon the approach in Sentana and Fiorentini (2001) and extending it to a more general setting in which both the factors and the idiosyncratic errors are heteroscedastic. Under mild regularity conditions, we show that the factor loadings under our setup are identified up to permutation and sign changes. Furthermore, with additional sign restrictions that satisfy a set of conditions, we show that the factor loadings and the associated factors are point-identified.

To determine the number of factors, we develop an estimator of the marginal likelihood based on an importance sampling approach to evaluate the observed-data or integrated likelihood. Through a series of Monte Carlo experiments, we show that our marginal likelihood estimator works well and is able to select the correct number of factors under a variety of settings.

We then discuss how our VAR with factor stochastic volatility (VAR-FSV) can be used for structural analysis. More specifically, we develop various structural analysis tools for VAR-FSV similar to those designed for standard structural VARs. In particular, we describe methods to construct structural impulse response functions, forecast error variance decompositions and historical decompositions. We demonstrate the methodology by revisiting the 6-variable VAR identified by a set of sign restrictions on the contemporaneous impact matrix considered in Furlanetto, Ravazzolo, and Sarferaz (2019). We augment their system to a 20-variable VAR by including additional, seemingly relevant macroeconomic and financial variables, which helps alleviate the concern of informational deficiency. In addition, the impulse responses obtained using the VAR-FSV with the sign restrictions imposed are point-identified. Empirically, we show that by including the additional variables and sign restrictions, one can substantially sharpen inference.

Our paper is related to the recent work by Korobilis (2020), who uses a VAR with a factor error structure for structural analysis. His work is motivated by the computational challenge of imposing a large number of sign restrictions to obtain admissible draws using conventional accept-reject methods (such as the widely used algorithm in Rubio-Ramirez, Waggoner, and Zha, 2010). This computational hurdle has so far limited the use of sign restrictions to relatively small systems with at most half a dozen dependent variables.555Large VARs, on the other hand, are mostly identified using recursive or zero restrictions. See, for example, Leeper, Sims, and Zha (1996), Banbura, Giannone, and Reichlin (2010) and Ellahie and Ricco (2017). Instead of using standard structural VARs, Korobilis (2020) assumes that the factors in his model play the role of structural shocks, and shows that in this case structural analysis can be done efficiently even when one imposes a large number of sign restrictions. His model, however, is homoscedastic, and consequently it is only set-identified. By contrast, in our VAR-FSV both the factors and the idiosyncratic errors follow stochastic volatility processes. This feature does not only accommodate the empirical finding that macroeconomic and financial variables typically exhibit time-varying volatility (see, e.g., Clark, 2011; Clark and Ravazzolo, 2015), it also allows us to achieve point-identification of the factors and the factor loadings.

Our work also contributes to the recent literature on using heteroscedasticity to identify conventional structural VARs, including Wozniak and Droumaguet (2015), Lanne, Lütkepohl, and Maciejowska (2010), Herwartz and Lütkepohl (2014), Bertsche and Braun (2020), Lewis (2021) and Brunnermeier, Palia, Sastry, and Sims (2021). Our paper considers the alternative setting of a VAR with a factor stochastic volatility specification and establishes sufficient conditions for identification. One key advantage of using VAR-FSV for structural analysis, compared to structural VARs, is that under VAR-FSV it is computationally feasible to estimate large systems and impose a large number of sign restrictions.

Our work is also related to the growing literature on constructing multivariate stochastic volatility models that are order invariant. One approach is based on Wishart or inverse-Wishart processes; examples include Philipov and Glickman (2006), Asai and McAleer (2009), Chan, Doucet, León-González, and Strachan (2018) and Shin and Zhong (2020). These models, however, are typically computationally intensive to estimate as the estimation involves drawing from non-standard high-dimensional distributions. As such, these models are generally not applicable to large datasets. An alternative approach is based on the common stochastic volatility models in Carriero, Clark, and Marcellino (2016) and Chan (2020). Although these models are designed for large systems and can be estimated quickly, they are more restrictive since the time-varying error covariance matrix depends on a single stochastic volatility process—in particular, the error variances are always proportional to each other.

There are also order-invariant models that are based on the discounted Wishart process, such as those in Uhlig (1997), West and Harrison (2006) and Bognanni (2018). These models are convenient to estimate as they admit Kalman-filter type filtering and smoothing algorithms. The cost for this tractability, however, is that they are generally too tightly parameterized, and consequently, they tend to underperform in forecasting macroeconomic variables relative to standard stochastic volatility models such as Cogley and Sargent (2005) and Primiceri (2005) (see Arias, Rubio-Ramirez, and Shin, 2021, for an example). Lastly, the recent paper Chan, Koop, and Yu (2021) extends the stochastic volatility model of Cogley and Sargent (2005) by avoiding the use of Cholesky decomposition so that the extension is order-invariant. So far this reduced-form VAR is used for forecasting, and further research is needed to incorporate identification restrictions for structural analysis.

The rest of this paper is organized as follows. Section 2 first introduces the VAR with factor stochastic volatility. Its theoretical properties, including order invariance and sufficient conditions for identification, are discussed in Section 3. We then outline a posterior sampler and a marginal likelihood estimator for the model in Section 4 and Section 5, respectively. Next, Section 6 develops various structural analysis tools for the VAR-FSV model, including algorithms to construct structural impulse response functions and to perform various decompositions. Then, Section 7 presents Monte Carlo results to illustrate how well the marginal likelihood estimator works under a variety of settings. We next demonstrate the proposed methodology via a structural analysis with sign restrictions in Section 8. Finally, Section 9 concludes and discusses some future research directions.

2 A Bayesian VAR with Factor Stochastic Volatility

In this section we outline a Bayesian VAR with factor stochastic volatility (FSV) and the associated prior distributions. To that end, let be an vector of dependent variables at time . Then, for , consider the following VAR-FSV model:

| (1) | ||||

| (2) |

where denotes a vector of latent factors and is an matrix of factor loadings. Note also that is unrestricted. The disturbances and the latent factors are assumed to be independent at all leads and lags. Moreover, they are specified as jointly Gaussian:

| (3) |

where and are diagonal matrices. For , the log-volatilities evolve as:

| (4) | ||||

| (5) |

where we impose to ensure stationarity. Finally, the initial conditions follow the stationary distributions and . Note that the stationary distributions of the log-volatilities associated with the idiosyncratic errors have nonzero means, whereas the means of those associated with the factors are set to be zero for normalization.

To facilitate estimation, we rewrite the VAR in (1) as

| (6) |

where is the identity matrix of dimension , is the Kronecker product, and is a vector of intercept and lagged values with .

Next, we specify the prior distributions on the model parameters. Let and denote the VAR coefficients and the elements of in the -th equation, respectively, for . We assume the following independent priors on and for :

We elicit the prior mean vector and the prior covariance matrix similar to the Minnesota prior (Doan, Litterman, and Sims, 1984; Litterman, 1986; Kadiyala and Karlsson, 1993). Specifically, for growth rates data, we set to shrink the VAR coefficients to zero. For level data, is set to be zero as well except for the coefficient associated with the first own lag, which is set to be one. The prior covariance matrix is constructed so that it depends on two key hyperparameters, and , that control respectively the overall shrinkage strength of ‘own’ lags and ‘other’ lags. For a more detailed discussion of the Minnesota prior, see, e.g., Koop and Korobilis (2010), Del Negro and Schorfheide (2011) or Karlsson (2013).

Finally, for the parameters in the stochastic volatility equations, we assume the priors:

and .

3 Order Invariance and Identification

In this section we describe a few important properties of the VAR-FSV model specified in (1)-(5). First, the likelihood implied by the model is invariant to the order of the variables (after permuting the relevant parameters appropriately). To see that, let be an permutation matrix such that . For the -variate Gaussian density with mean vector and covariance matrix , it is easy to see that .

Next, we derive an expression of the likelihood function. To that end, stack and . We similarly define and . In addition, we let , , and . Then, the state equations (4)-(5) imply that the densities of and for , are, respectively,

where is the element-wise multiplication. Moreover, the initial conditions and have, respectively, the densities

where denotes the element-wise division.

Next, using the representation in (6) and integrating out the factors, the density of given the parameters and log-volatilities is . Stacking , the likelihood function, or more precisely the integrated or observed-data likelihood, can therefore be written as

| (7) |

Now, for an arbitrary permutation matrix , suppose we permute the order of the dependent variables and the associated lagged values , where . We claim that the likelihood implied by the VAR-FSV model is invariant to the permutation in the sense that

where and .666Note that the permuted vector consists of the VAR coefficients of the following system stacked by rows: where and That is, That is, we obtain the same likelihood value for any permutation of if the lagged values and the parameters are permuted accordingly.

This claim of order invariance can be readily verified as follows. First, noting that

we therefore obtain

where . Similarly, we also have

Since the Gaussian densities in (7) are equal to their permuted counterparts, the integrand in is exactly the same as that in (7). The only difference between the two integrals is the order of integration: versus . But since the integral is finite, one can change the order of integration without changing the integral. Hence, the desired result follows. The following proposition summarizes this result.

Proposition 1 (Order Invariance).

Let denote the likelihood of the VAR-FSV model with lagged values . Let be an arbitrary permutation matrix and define and , where . Then, the VAR-FSV with dependent variables and lagged values has the same likelihood. More precisely,

where and .

Next, we discuss sufficient conditions for identification of the factor loadings and latent factors. We mainly follow the approach in Sentana and Fiorentini (2001), but consider a more general setting in which the idiosyncratic errors in (2) are also heteroscedastic. First, note that it follows from (2) and (3) that the covariance matrix of is given by . The covariance structure of any observationally equivalent model to (1)–(3) with the same number of factors must satisfy for all , where is and is . Furthermore, for a square matrix of dimension , we define to be the vector that stores its diagonal elements. Now, we consider the following assumptions that are used throughout the paper.

Assumption 1.

The stochastic processes in are linearly independent, i.e., there does not exist , such that for all .

Assumption 2.

If any row of the matrix of factor loadings is deleted, there remain two disjoint submatrices of rank .

Assumption 1 requires that no stochastic volatilities in the common factors can be expressed as a linear combination of other factor stochastic volatilities. Under our factor stochastic volatility model, this assumption is automatically satisfied. Assumption 2 limits the extent of sparseness in the factor loadings matrix to ensure one can separately identify the common and the idiosyncratic components. This assumption can be traced back to Anderson and Rubin (1956), and is widely adopted in the literature. Implicitly, it also requires that . Since factor models are mostly applied to situations where the number of variables is much larger than the number of factors , this is not a stringent condition.

With Assumptions 1 and 2, one can show that the factor stochastic volatility model specified in (2)-(3) is identified up to permutations and sign changes of the factors. The identification results are summarized in the following proposition.

Proposition 2 (Identification of the Common Variance Component).

We prove the proposition by adapting the results in Anderson and Rubin (1956) and Sentana and Fiorentini (2001) to our setting. The details are provided in Appendix A. Proposition 2 contains two sets of identification results. First, it shows that the common and idiosyncratic variance components can be separately identified. Second, the common variance component is identified up to permutations and sign switches of the latent factors.

So far we have only considered the case where all factors are heteroskedastic. It turns out this is not necessary for identification of the common variance component. More generally, one can show that part of the factor loadings matrix is identified even when some of the factors are homoskedastic (their variances are normalized to be one). The following proposition summarizes such a partial identification result.

Proposition 3 (Partial Identification of the Common Variance Component When the Number of Heteroskedastic Factors Is ).

Let , where is a covariance matrix and is the -dimensional identity matrix with . Similarly partition such that is and is . If satisfies Assumption 1 and satisfies Assumption 2, then is identified up to permutations and sign switches.

The proof of this proposition is given in Appendix A. The condition that satisfies Assumption 1—i.e., are linearly independent for all —requires all stochastic processes in to be non-degenerate. (Otherwise those homoskedastic factors should be relocated to the homoskedastic part.) It is also worth noting that Proposition 3 does not imply that for , the common variance component is not identifiable. In fact, it turns out that the minimum number of heteroskedastic factors for identifying (up to permutations and sign switches) is . We summarize this result in the following corollary.

Corollary 1.

Under the assumptions in Proposition 3, if the number of heteroskedastic factors is , then is identified up to permutations and sign switches.

The reason why only heteroskedastic factors are needed for identification is intuitive. Under the assumptions in Proposition 3, when , only one element in is normalized to one; the remaining stochastic processes in are linearly independent. Consequently, also satisfies Assumption 1. And Corollary 1 follows from Proposition 2.

For , part of the factor loadings matrix is invariant under general orthogonal transformation. To see that, suppose , and hence has at least columns. Let be a orthogonal matrix other than permutation or reflection such that .777The only one-dimensional orthogonal matrices are reflections, namely, and . Hence, must be at least 2. Then, we have Hence, and form an observationally equivalent model.

For point-identification, one needs additional restrictions on (or the latent factors) to pin down the unique permutation and sign configuration. As is common in macroeconomic analysis using VARs, sign restrictions implied by economic theory are often available to assist structural identification. For a recent contribution linking sign restrictions and factor models, see Korobilis (2020). Below we describe how we can incorporate sign restrictions to achieve point-identification. To that end, let denote the matrix that collects the corresponding restrictions on the factor loadings matrix . The entries of can take four values: 1, , 0 and N/A, which denotes positive restriction, negative restriction, zero restriction and no restrictions, respectively. For example, if economic theory implies that , then ; if there are no restrictions on , then .

Recall that under Assumptions 1-2, Proposition 2 dictates that the factor loadings matrix of any observationally equivalent model must be of the form , where is a product of a reflection and a permutation. To be observationally equivalent with the sign restrictions imposed—i.e., satisfying exactly the same sign restrictions—we must have . Intuitively then, for point-identification of there must be enough structure in such that the only possible is the identify matrix. Now, suppose that each column of has at least one sign restriction and no columns are the same or negative of any other columns. These conditions are sufficient as they rule out any permutations or sign changes except the identity.

To see that the conditions are necessary, suppose there is a column that has no sign restrictions. Then, changing the sign of the associated column in (and the associated rows in ) would leave the model observationally equivalent. Next, suppose one column is the same or the negative of any other column, then we can permute (and change signs if necessary) the relevant columns to leave the model observationally equivalent. We summarize these results in the following corollary.

Corollary 2.

Under Assumptions 1-2, the necessary and sufficient conditions for point-identification of the factor loadings matrix are that each column of has at least one sign restriction and no columns are the same or negative of any other columns.

4 Bayesian Estimation

In this section we describe an efficient posterior sampler to estimate the model in (1)–(5) with signs or zero restrictions specified in . Below we note a few details in our implementation with the goal of improving speed and sampling efficiency. First, even though the factors are conditionally independent given the data and other parameters, we sample them jointly in one step using the precision sampler of Chan and Jeliazkov (2009)—instead of drawing them sequentially in a for-loop—to speed up the computations.

Second, since VARs tend to have a lot of parameters even for small and medium systems, we implement an equation-by-equation estimation approach similar in spirit to that in Carriero, Clark, and Marcellino (2019) to sample the VAR coefficients. Specifically, given the latent factors , the VAR becomes unrelated regressions, and one can sample the VAR coefficients equation by equation without any loss of efficiency. Third, with the sign restrictions imposed in , the full conditional distribution of the factor loadings in each equation becomes a truncated multivariate normal distribution. To sample from such a distribution, we use the algorithm in Botev (2017) that is based on quadratic programming.

For notational convenience, stack and . In addition, let denote the vector of observed values for the -th variable, . We similarly define . Then, posterior draws can be obtained by sampling sequentially from:

-

1.

;

-

2.

;

-

3.

;

-

4.

;

-

5.

;

-

6.

.

Step 1. As mentioned above, since the factors are conditionally independent given other parameters, in principle one can sample each factor sequentially in a for-loop. Here, however, we vectorize all the operations and sample them jointly in one step to improve computational speed. More specifically, we first stack the VAR in (1)-(2) over and write it as:

where is the matrix of intercepts and lagged values and with . In addition, it follows from (3) that where with .

Then, by standard linear regression results (see, e.g., Chan, Koop, Poirier, and Tobias, 2019, chapter 12), we have

| (8) |

where

| (9) |

Note that the precision matrix is a band matrix, i.e., it is sparse and all the nonzero entries are arranged along the diagonal bands above and below the main diagonal. As such, once can use the precision sampler of Chan and Jeliazkov (2009) to sample efficiently.

Step 2. Next, we sample and jointly to improve sampling efficiency. Given the latent factors , the VAR becomes unrelated regressions and we can sample and equation by equation. Recall that is defined to be the vector of observations for the -th variable; and that and represent, respectively, the VAR coefficients and the factor loadings in the -th equation. Then, the -th equation of the VAR can be written as

where is the matrix of factors with . The vector of disturbances is distributed as , where .888Note that zero restrictions on can be easily handled by redefining and appropriately. For example, if the first element of is restricted to be zero, we can define to be the vector consisting of the second to -th elements of and . Then, we replace by . Letting and , we can further write the VAR systems as

Let be the support of defined by the sign restrictions specified in the -th row of . Then, using standard linear regression results, we obtain:

where

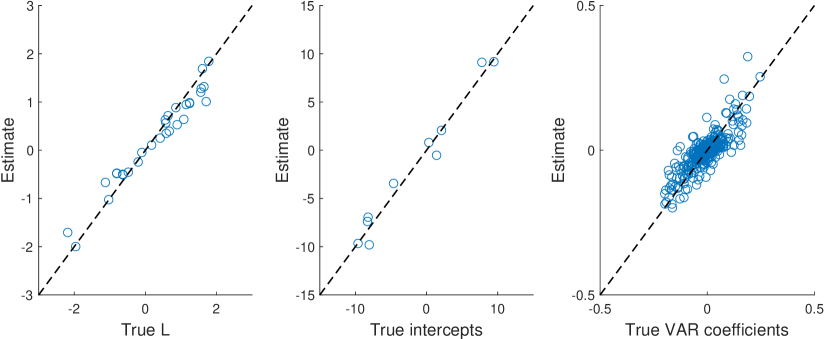

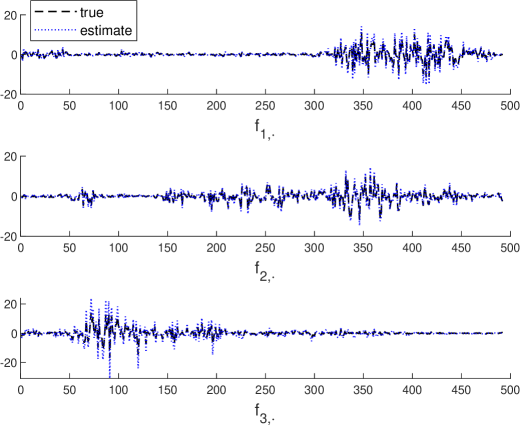

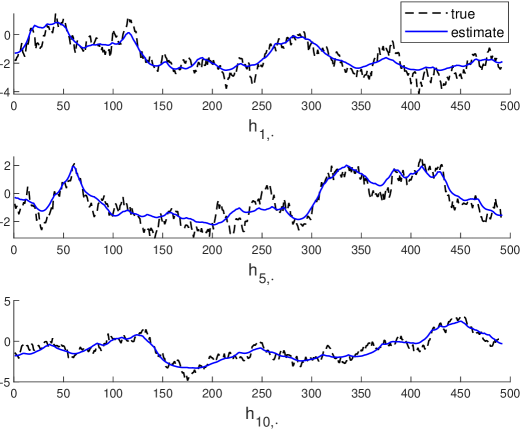

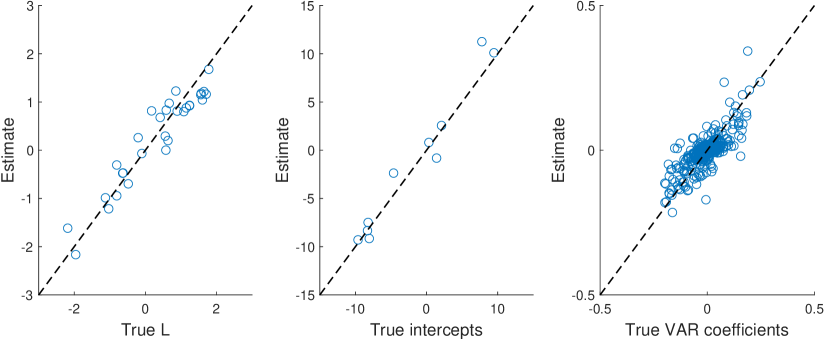

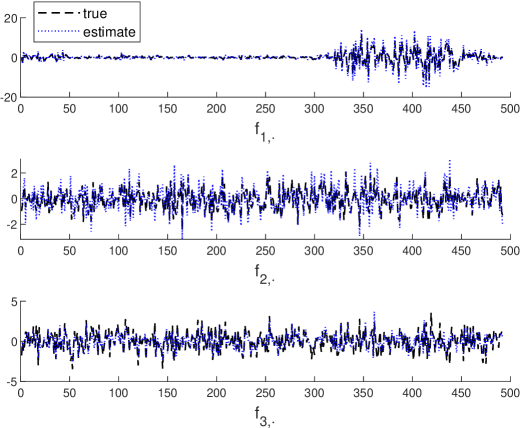

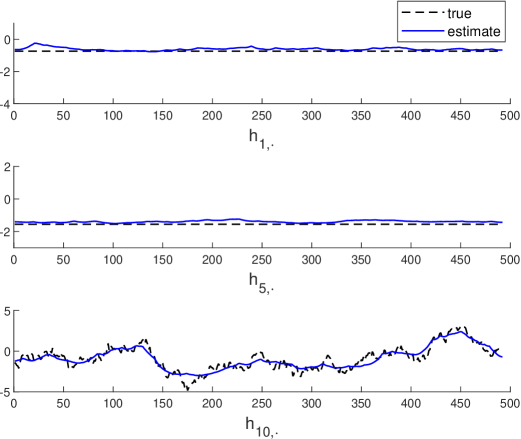

with and . A draw from this truncated multivariate normal distribution can be obtained using the algorithm in Botev (2017). The remaining steps are standard and we leave the details to Appendix B. Some simulation results are reported in Appendix D to show that the posterior sampler works well and the posterior estimates track the true values closely.

It is worth noting that Proposition 2 only guarantees that the factors and factor loadings are identified up to permutations and sign changes. Hence, in practice one might encounter the so-called label-switching problem. One way to handle this issue is to post-process the posterior draws to sort them into the correct categories; see, e.g., Kaufmann and Schumacher (2019) for such an approach. In our empirical application we impose sign restrictions that satisfy Corollary 2—and consequently the factors and factor loadings are point-identified.

Next, we document the runtimes of estimating the VAR-FSV of different dimensions to assess how well the posterior sampler scales to higher dimensions. More specifically, we report in Table 1 the computation times (in minutes) to obtain 10,000 posterior draws from the VAR-FSV of dimensions and sample sizes . The posterior sampler is implemented in on a typical desktop with an Intel Core i5-9600 @3.10 GHz processor and 16 GB memory. It is evident from the table that even for high-dimensional applications with 50 variables, the VAR-FSV model with sign restrictions imposed on the factor loadings can be estimated fairly quickly.

| 12.5 | 25.7 | 45.0 | 33.3 | 67.3 | 110.2 |

5 Bayesian Model Comparison

This section first gives a brief overview on the theory of Bayesian model comparison via the marginal likelihood. Then, we introduce an algorithm to evaluate the likelihood, or more precisely the integrated likelihood marginal of the latent states, implied by the VAR-FSV model. Finally, we present an adaptive importance sampling algorithm to estimate the marginal likelihood under the VAR-FSV model.

Suppose we wish to compare a collection of models , where each model is defined by a likelihood function and a prior on the model-specific parameter vector denoted by . The gold standard for Bayesian model comparison is the Bayes factor in favor of against , defined as

where

| (10) |

is the marginal likelihood under model , This Bayes factor is related to the posterior odds ratio between the two models:

where is the prior odds ratio. It if clear that if both models are equally probable a priori, i.e., , then the posterior odds ratio between the two models is equal to the Bayes factor. Hence, the Bayes factor has a natural interpretation and is easy to understand. For example, under equal prior odds, if , then model is 50 times more likely than model given the data. For a more detailed discussion of the Bayes factor and its role in Bayesian model comparison, see Koop (2003) or Chan, Koop, Poirier, and Tobias (2019). From here onwards we suppress the model indicator.

5.1 Integrated Likelihood Evaluation

To estimate the marginal likelihood, we first present an efficient way to evaluate the likelihood, or more precisely the integrated likelihood marginal of the latent states, given in (7) . For notational convenience, we rewrite (7) as

| (11) |

where the conditional density of given but marginal of has the explicit expression

The second term of the integrand, , is a -variate Gaussian density implied by the state equations specified in (4)-(5). Its analytical expression is given in Appendix C, and in particular, its precision matrix is banded. Hence, both densities can be evaluated quickly.

The main difficulty in evaluating the integrated likelihood in (11), however, is that it requires integrating out all the latent log-volatilities, which involves solving a -dimensional integral. In what follows, we adopt the importance sampling approach developed for time-varying parameter VARs in Chan and Eisenstat (2018) to our setting.999There is a long tradition of using importance sampling to evaluate the integrated likelihood of stochastic volatility models. Earlier papers, such as Durbin and Koopman (1997), Shephard and Pitt (1997), Koopman and Hol Uspensky (2002), Frühwirth-Schnatter and Wagner (2008), McCausland (2012), have focused mostly on univariate stochastic volatility models. More specifically, given an importance sampling density —that might depend on model parameters and the data—we evaluate the integrated likelihood via importance sampling:

| (12) |

where are independent draws from .

The choice of the importance sampling density is vital as it determines the variance of the estimator. In general, we would like to use an importance sampling density so that it well approximates the integrand in (11). Our particular choice is motivated by the observation that there is, in fact, a theoretical zero-variance importance sampling density—it is , the conditional posterior distribution of given the other parameters but marginal of . In practice, however, this density cannot be used as an importance sampling density as it is non-standard (e.g., its normalizing constant is unknown and it is unclear how one can efficiently generate samples from this density). But this observation provides us guidance for selecting a good importance sampling density.

In particular, we aim to approximate this ideal importance sampling density using a Gaussian density. This is accomplished as follows. We first develop an expectation-maximization (EM) algorithm to locate the mode of , denoted as . Then, we obtain the negative Hessian of this log-density evaluated at the mode, denoted as . The mode and the negative Hessian are then used, respectively, as the mean vector and precision matrix of the Gaussian approximation. That is, the importance sampling density is We leave the technical details to Appendix C. Below we comment on a few computational details.

First, in the M-step of the EM algorithm, one needs to solve a -dimensional maximization problem, which is in general extremely computationally intensive. In our case, however, we are able to obtain analytical expressions of the gradient and the Hessian of the objective function (i.e., the Q-function), which allows us to implement the Newton-Raphson method. Furthermore, one can show that the Hessian is a) negative definite anywhere in , and b) a band matrix. The former property guarantees rapid convergence of the Newton-Raphson method, while the latter property substantially speeds up the computations.

Second, to construct the importance sampling estimator in (12), one needs to both evaluate and sample from the -dimensional Gaussian importance sampling density times. For very high-dimensional Gaussian densities, both operations are generally computational costly. For our Gaussian importance sampling density, however, we can show that its precision matrix is banded. As such, samples from this Gaussian density can be obtained quickly using the precision sampler in Chan and Jeliazkov (2009). Evaluation of the density can be done just as quickly. We summarize the evaluation of the integrated likelihood in Algorithm 1.

Given the parameters , and , complete the following two steps.

-

1.

Obtain the mean vector and precision matrix of the Gaussian importance sampling density detailed in Appendix C.

-

2.

For , simulate using the precision sampler in Chan and Jeliazkov (2009), and compute the average

5.2 Marginal Likelihood Estimation

Next, we discuss the marginal likelihood estimation of the VAR-FSV model using an adaptive importance sampling approach called the improved cross-entropy method. This method requires little explicit analysis from the user and is applicable to a wide variety of problems (in contrast to the importance sampling estimator of the integrated likelihood estimation presented in Algorithm 1 that requires a lot of analysis). More specifically, suppose we wish to estimate the marginal likelihood given in (10) using the following importance sampling estimator:

| (13) |

where are independent draws from the importance sampling density . In particular, for our FSV model, . While this importance sampling estimator in theory is unbiased and simulation consistent for any —as long as it dominates , i.e., —in practice its performance heavily depends on the choice of . Here we follow Chan and Eisenstat (2015) to use the improved cross-entropy method to construct optimally.101010The original cross-entropy method was developed for rare-event simulation by Rubinstein (1997, 1999) using a multi-level procedure to construct the optimal importance sampling density. Chan and Eisenstat (2015) later show that this optimal importance sampling density can be obtained more accurately in one step using Markov chain Monte Carlo methods.

To motivate the improved cross-entropy method, first note that the ideal zero-variance importance sampling density is the posterior density . That is, if we use as the importance sampling density, then the associated estimator in (13) has zero variance. Unfortunately, cannot be used in practice as its normalization constant is precisely the marginal likelihood, the unknown quantity we aim to estimate. This nevertheless provides a benchmark to construct an optimal importance sampling density. More specifically, we aim to find a density that is ‘close’ to this benchmark that can be used as an importance sampling density.

To that end, consider a parametric family indexed by the parameter vector . We then find the density such that it is, in a well-defined sense, the ‘closest’ to . One convenient measure of closeness between densities is the Kullback-Leibler divergence or the cross-entropy distance. More precisely, for two density functions and , the cross-entropy distance from to is defined as:

Given this measure of closeness, we obtain the density such that is minimized, i.e., . It can be shown that solving the CE minimization problem is equivalent to finding

In general this optimization problem is difficult to solve analytically as it involves a high-dimensional integral. Instead, we consider its stochastic counterpart:

| (14) |

where are posterior draws from . It is useful to note that is exactly the maximum likelihood estimate for if we view as the likelihood function with parameter vector and as an observed sample. Since finding the maximum likelihood estimator is a standard problem, solving (14) is typically easy. For example, analytical solutions to (14) are available for the exponential family (e.g., Rubinstein and Kroese, 2004, p. 70).

Next, we discuss the choice of the parametric family . One convenient class of densities is one in which each member is a product of probability densities, e.g., , where and . One main advantage of this choice is that we can then reduce the generally high-dimensional maximization problem (14) into separate low-dimensional maximization problems. For example, for the our FSV model, we divide into 5 natural blocks, and consider the parametric family

where and are, respectively, the Gaussian and the inverse-gamma densities. Given this choice of the parametric family, the maximization problem in (14) can be readily solved (either analytically or using numerical optimization).

Given the optimal importance density, denoted as , we construct the following importance sampling estimator:

| (15) |

where are independent draws from and is the integrated likelihood, which can be estimated using the estimator in (12). We refer the readers to Chan and Eisenstat (2015) for a more thorough discussion of this adaptive importance sampling approach. We summarize the algorithm in Algorithm 2.

Note that Algorithm 2 has two nested importance sampling steps, and it falls within the importance sampling squared (IS2) framework in Tran, Scharth, Pitt, and Kohn (2014). We follow their recommendation to set , the simulation size of the inner importance sampling loop (the importance sampling step for estimating the integrated likelihood), adaptively so that the variance of the log integrated likelihood is around 1. See also the discussion in Pitt, dos Santos Silva, Giordani, and Kohn (2012).

The marginal likelihood can be estimated using the following steps.

6 Structural Analysis with the VAR-FSV

The VAR-FSV in (1)-(2) can be used to draw structural inference by employing standard tools such as impulse response functions, forecast error variance decompositions and historical decompositions. In particular, letting , where is the lag operator, the representation

| (16) |

where is well-defined assuming for all (i.e., the process is covariance-stationary).

Although does not contain structural shocks (since its elements are correlated), the reduced-form representation (16) can be matched to a hypothetical structural representation of the form

| (17) |

where is a vector of structural shock, and hence, its elements are uncorrelated. Note that is time-varying because is time-varying; consequently, hypothetical structural representations that can be matched to (16) will generally have time-varying parameters.

The standard structural VAR approach is to assume that (i) is and (ii) , where is a constant matrix with and . Then, and satisfies

In this case, identification of requires additional restrictions since

for all , given an arbitrary orthonormal matrix (i.e. satisfying ).

An alternative way to obtain structural inference in our settings—similar to Korobilis (2020)—is to assume that is and is , such that

| (18) |

where and . In this case, is also , which in departure from standard structural VARs leads to a ‘short’ system (Forni, Gambetti, and Sala, 2019).

Identification of impulse response functions and forecast error variance decompositions in short systems is generally problematic (Pagan and Robinson, 2022; Canova and Ferroni, 2022). However, in the formulation above, is identified due to being restricted to a diagonal matrix and being identified by sign restrictions as described in Section 3. Hence, impulse response functions and forecast error variance decompositions to all shocks in are identified, even though is generally not recoverable from past and future observations of , as defined in Chahrour and Jurado (2021).

In our setting, the main interest lies in quantifying the effects of shocks in , and therefore, sign restrictions on play the role of endowing these shocks with economic meaning. The remaining elements in are not of direct interest and we do not treat them as economically meaningful shocks. Nevertheless, the restriction that is diagonal plays a crucial role in the overall identification strategy along with an economically meaningful interpretation of . We provide explicit expressions for computing impulse response functions and forecast error variance decompositions in Appendix F.

Finally, computing historical decompositions requires and (see Appendix F for details). The fact that is not recoverable implies that historical decompositions may not be point identified. In a Bayesian setting, however, the posterior distribution of a historical decomposition at each horizon may still be constructed using draws from the posterior distribution of the VAR-FSV parameters together with draws of .

In the algorithm developed in Section 4, draws of are a by-product of simulation, while is easily obtained as

for each draw of . Therefore, draws from the posterior distribution of a HD are straightforward to compute.

In addition, can be regarded as being recoverable in the limit as from the VAR residual (and therefore past and present ) under a suitable assumption on the factor loadings . To see this, let denote the Moore–Penrose inverse of . By Assumption 2, and . It also follows that a right inverse (although not a Moore-Penrose inverse) of is

| (19) | ||||

| Consequently, | ||||

| (20) | ||||

In the factor model literature, a standard assumption (e.g. Bai, 2003; Forni, Giannone, Lippi, and Reichlin, 2009) is that as , where is a constant (strictly) positive-definite matrix. It implies that the factors are pervasive in the sense that they significantly affect most of the variables on impact.111111It is worth emphasising, however, that this does not imply is a vector of idiosyncratic errors, as defined by Forni, Hallin, Lippi, and Reichlin (2000); Forni and Lippi (2001) in the context of generalised dynamic factor models. In particular, the overall effect of on is , which is generally pervasive, albeit with a delay. An immediate consequence of the pervasiveness assumption, together the regularity condition that for all , is . Combining this result with (20) yields

| (21) |

Consequently, is recoverable from in the limit.121212A more general result on recoverability with a fixed is given in Chahrour and Jurado (2021).

7 A Monte Carlo Study: Determining the Number of Factors

In this section we conduct a series of simulation experiments to assess the adequacy of using the proposed marginal likelihood estimator to determine the number of factors. More specifically, we generate datasets from the VAR-FSV in (1)–(5), but we change the error structure to , where measures the signal-to-noise ratio, following Bai and Ng (2002). We set parameter values so that if , the idiosyncratic component will then have the same variance as the common component. In particular, we generate for and and set for so that the log-volatility processes associated with the idiosyncratic errors have 0 unconditional mean.

The remaining parameters are generated as follows. The intercepts are drawn independently from the uniform distribution on the interval , i.e., . For the VAR coefficients, the diagonal elements of the first VAR coefficient matrix are iid and the off-diagonal elements are from ; all other elements of the -th () VAR coefficient matrices are iid Finally, for the log-volatility processes, we set and for .

In this Monte Carlo study, we select the true number of factors and ; and we consider the number of variables and sample size . For each set of , we generate 100 datasets. For each dataset, we estimate the VAR-FSV models with factors and compute the associated marginal likelihood values. For this Monte Carlo experiment, a total of 14,400 separate MCMCs and marginal likelihood estimation are run (24 settings 6 factor models 100 datasets). Among the 6 factor models for each dataset and parameter setting, we select the one with the largest marginal likelihood value. Table 2 reports the selection frequency.

| True | |||||||||

| 15 | 1 | 1 | 300 | 0.90 | 0.10 | 0 | 0 | 0 | 0 |

| 500 | 0.96 | 0.04 | 0 | 0 | 0 | 0 | |||

| 800 | 0.99 | 0.01 | 0 | 0 | 0 | 0 | |||

| 3 | 3 | 300 | 0 | 0.13 | 0.83 | 0.04 | 0 | 0 | |

| 500 | 0 | 0.02 | 0.97 | 0.01 | 0 | 0 | |||

| 800 | 0 | 0 | 0.99 | 0.01 | 0 | 0 | |||

| 5 | 5 | 300 | 0 | 0.01 | 0.12 | 0.49 | 0.38 | 0 | |

| 500 | 0 | 0 | 0.01 | 0.25 | 0.74 | 0 | |||

| 800 | 0 | 0 | 0.01 | 0.05 | 0.94 | 0 | |||

| 10 | 5 | 300 | 0 | 0.07 | 0.3 | 0.46 | 0.16 | 0.01 | |

| 500 | 0 | 0 | 0.1 | 0.48 | 0.42 | 0 | |||

| 800 | 0 | 0 | 0.02 | 0.11 | 0.87 | 0 | |||

| 30 | 1 | 1 | 300 | 0.76 | 0.24 | 0 | 0 | 0 | 0 |

| 500 | 0.97 | 0.02 | 0 | 0 | 0 | 0.01 | |||

| 800 | 1.00 | 0 | 0 | 0 | 0 | 0 | |||

| 3 | 3 | 300 | 0 | 0.02 | 0.86 | 0.11 | 0.01 | 0 | |

| 500 | 0 | 0.01 | 0.98 | 0.01 | 0 | 0 | |||

| 800 | 0 | 0 | 1.00 | 0 | 0 | 0 | |||

| 5 | 5 | 300 | 0 | 0 | 0.01 | 0.18 | 0.80 | 0.01 | |

| 500 | 0 | 0 | 0 | 0.02 | 0.97 | 0.01 | |||

| 800 | 0 | 0 | 0 | 0.01 | 0.99 | 0 | |||

| 10 | 5 | 300 | 0 | 0.01 | 0.1 | 0.36 | 0.53 | 0 | |

| 500 | 0 | 0 | 0 | 0.16 | 0.84 | 0 | |||

| 800 | 0 | 0 | 0 | 0.02 | 0.98 | 0 |

The Monte Carlo results show that the marginal likelihood estimator generally performs well in selecting the correct number of factors under a variety of settings. For example, for and (moderate signal-to-noise ratio), the marginal likelihood estimator is able to pick the correct number of factors 83% of the times; for the rest of the cases, the model with one fewer factor (13%) or one more factor (4%) is selected. In addition, as the sample size increases to 500, the selection frequency of the factor model increases to 97%. More generally, the selection frequency of the correct number of factors increases as the sample size increases for all cases considered, confirming that the marginal likelihood is a consistent model selection criterion.

8 Application: The Role of Financial Shocks in Economic Fluctuations

We illustrate the proposed methodology by revisiting the structural analysis in Furlanetto, Ravazzolo, and Sarferaz (2019) that is based on a standard structural VAR. More specifically, they use a 6-variable structural VAR to study the impacts of 5 structural shocks—demand, supply, monetary, investment and financial shocks—on a number of key economic variables, where these structural shocks are identified using sign restrictions on the contemporaneous impact matrix. The size of the VAR in their application is typical among empirical works that use sign restrictions for identification because of the computational burden.131313For their 6-variable structural VAR, Furlanetto, Ravazzolo, and Sarferaz (2019) report estimation time of about a week using a 12-core workstation.

However, there are a number of reasons in favor of using a larger set of macroeconomic and financial variables. First, in practice the mapping from variables in an economic model to the data is often not unique. For example, as argued in (Loria, Matthes, and Wang, 2021), the economic variable inflation could be matched to data based on the CPI, PCE, or the GDP deflator, and it is not obvious which time series should be used. Instead of arbitrarily choosing one inflation measure, it is more appropriate to include multiple time series corresponding to the same economic variable in the analysis.

Second, one might be concerned about the problem of informational deficiency that arises from using a limited information set. More specifically, influential papers such as Hansen and Sargent (1991) and Lippi and Reichlin (1993, 1994) have pointed out that when the econometrician considers a narrower set of variables than the economic agent, the underlying model used by the econometrician is non-fundamental. That is, current and past observations of the variables do not span the same space spanned by the structural shocks. As a consequence, structural shocks cannot be recovered from the model. A natural way to alleviate this concern of informational deficiency is to use a larger set of relevant variables (see, e.g., Gambetti, 2021, for a recent review on non-fundamentalness).

In view of these considerations, we augment the 6-variable VAR with additional macroeconomic and financial variables, and consider a 20-variable VAR with factor stochastic volatility identified using sign restrictions. There are two related papers that use large VARs to study the role of financial shocks in economic fluctuations. First, Chan (2021) considers a 15-variable structural VAR with a new asymmetric conjugate prior to identify the financial shocks. Given the larger system and the large number of sign restrictions, estimation time is about a week to obtain 1,000 admissible draws using the algorithm of Rubio-Ramirez, Waggoner, and Zha (2010). In contrast, the proposed approach takes less than a minute to obtain the same number of admissible draws, and is applicable to even larger systems. Second, Korobilis (2020) uses a 15-variable VAR with a factor error structure to identify the financial shocks, which can also be done quickly. The main advantage of our approach, however, is that the structural shocks obtained using our factor stochastic volatility model are point-identified, whereas they are only set-identified under a homoskedastic VAR. In practice, our approach can often provide sharper inference.

8.1 Data

We use a dataset that consists of 20 US quarterly variables, which are constructed from raw time-series taken from from different sources, including the Federal Reserve Bank of Philadelphia and the FRED database at the Federal Reserve Bank of St. Louis. For easy comparison with the results in Furlanetto, Ravazzolo, and Sarferaz (2019), we use the same sample period that spans from 1985:Q1 to 2013:Q2. The complete list of these time-series and their sources are given in Appendix E.

We include the same 6 variables used in the baseline model in Furlanetto, Ravazzolo, and Sarferaz (2019), namely, real GDP, GDP deflator, 3-month treasury rate, ratio of private investment over output, S&P 500 index and a credit spread defined as the difference between Moody’s baa corporate bond yield and the federal funds rate. In addition, we also include 14 additional macroeconomic and financial variables, such as the ratio of total credit over real estate value, labor market variables, mortgage rates, as well as other measures of inflation, interest rates and stock prices. These 20 variables are listed in Table 3 and the details of the raw data are given in Appendix E.

8.2 Sign Restrictions and Impulse Responses

In this section we re-examine the empirical application in Furlanetto, Ravazzolo, and Sarferaz (2019) that identifies 5 structural shocks using a structural VAR with sign restrictions on the contemporaneous impact matrix. We first use the proposed VAR-FSV model to replicate their baseline results from a 6-variable VAR, but here we impose the sign restrictions on the factor loadings instead of the impact matrix. We then consider a larger VAR-FSV model with 20 variables to identify the same structural shocks.

Now, we first employ the same 6 variables and the associated sign restrictions used in Furlanetto, Ravazzolo, and Sarferaz (2019), which are presented in the first six rows of Table 3. The sign restrictions to identify the supply, demand, monetary, investment and financial shocks are exactly the same as in Furlanetto, Ravazzolo, and Sarferaz (2019), and we refer the readers to their paper for more details. Here we only note that in order to distinguish investment and financial shocks from demand shocks, they are assumed to have different effects on the ratio of investment over output. In particular, positive investment and financial shocks have a positive effect on the ratio, motivating by the idea that investment and financial shocks create investment booms. By contrast, positive demand shocks reduce the ratio of investment over output, i.e., even though investment level could increase in response to demand shocks, it does not increase as much as other components of output.

We compute the impulse responses from the VAR-FSV with 5 factors, where the sign restrictions are imposed on the factor loadings. Since Furlanetto, Ravazzolo, and Sarferaz (2019) use an improper/non-informative prior in their analysis, to make our results comparable, we consider a proper but relatively vague prior by setting .141414The variables are expressed in level. As such, the prior means of the first own lags are all set to be 1, whereas those of other VAR coefficients are set to be 0. In addition, the prior mean of , the mean of the idiosyncratic log-volatility for the -th variable, is set to be . That is, a priori about 10% of the sample variance is attributed to idiosyncratic component. Finally, the prior variance is set to be 10 for . We use the Gibbs sampler described in Section 4 to obtain 50,000 posterior, storing every 10-th draw, after a burn-in period of 5,000.

| Supply | Demand | Monetary | Investment | Financial | |

|---|---|---|---|---|---|

| GDP | + | + | + | + | |

| GDP deflator | + | + | + | + | |

| 3-month tbill rate | NA | + | + | + | |

| Investment/output | NA | NA | + | + | |

| S&P 500 | + | NA | NA | + | |

| Spread | NA | NA | NA | NA | NA |

| Spread 2 | NA | NA | NA | NA | NA |

| Credit/Real estate value | NA | NA | NA | NA | NA |

| Mortgage rates | NA | NA | NA | NA | NA |

| Personal consumption expenditures | + | + | + | + | + |

| Industrial production | + | + | + | + | + |

| Industrial production: final | + | + | + | + | + |

| CPI | + | + | + | + | |

| PCE index | + | + | + | + | |

| Employment | NA | NA | NA | NA | NA |

| All employees: Manufacturing | NA | NA | NA | NA | NA |

| 1-year tbill rate | NA | + | + | + | |

| 10-year tnote rate | NA | + | + | + | |

| DJIA | + | NA | NA | + | |

| NASDAQ | + | NA | NA | + |

Note: the variable spread is defined as the difference between Moody’s baa corporate bond yield and the federal funds rate. Spread 2 is the difference between Moody’s baa corporate bond yield and 10-year treasury yield.

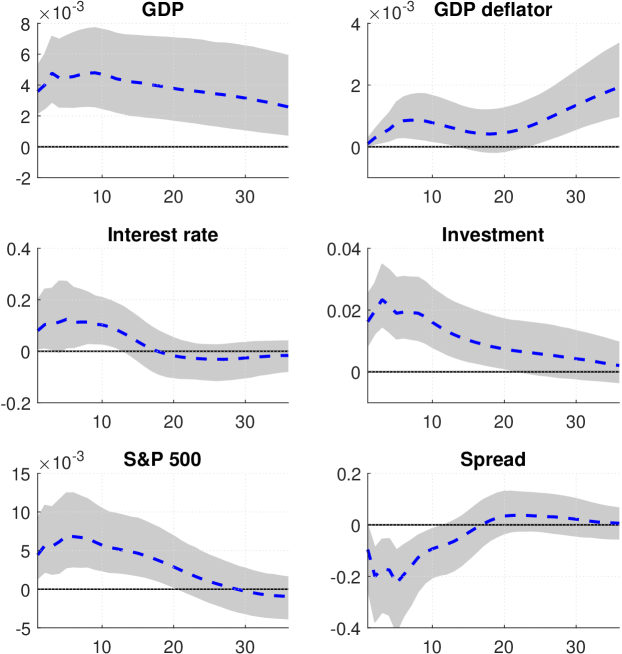

Figure 1 plots the impulse responses of the 6 variables to an one-standard-deviation financial shock. Despite the differences in methodology, the impulse responses are very similar to those given in Furlanetto, Ravazzolo, and Sarferaz (2019). Consistent with the findings in Furlanetto, Ravazzolo, and Sarferaz (2019), the results show that financial shocks have a substantial impact on output, stock prices and investment, but have a limited impact on inflation (measured by GDP deflator). Furthermore, even though the impact on the spread is unrestricted, we find that its reaction to financial shocks is significantly counter-cyclical. These results highlight one advantage of the proposed methodology: the median impulse responses from the VAR-FSV are very similar to those obtained using a standard structural VAR, but instead of using an accept-reject algorithm to obtain admissible draws, the sign restrictions can be easily incorporated in the estimation, and consequently, it can be done much faster.

Next, we augment the 6-variable VAR with 14 additional macroeconomic and financial variables. Many of these new variables are alternative data series corresponding to the same economic variable. For example, in addition to GDP deflator as prices, we also include CPI and PCE index as alternative measures. Similarly, Dow Jones Industrial Average and NASDAQ indexes are added as alternative measures of stock prices. Furthermore, other seemingly relevant variables, such as labor market and national accounts variables, are also included to alleviate the concern of informational deficiency. The additional variables and the corresponding sign restrictions are listed in rows 7-20 of Table 3.

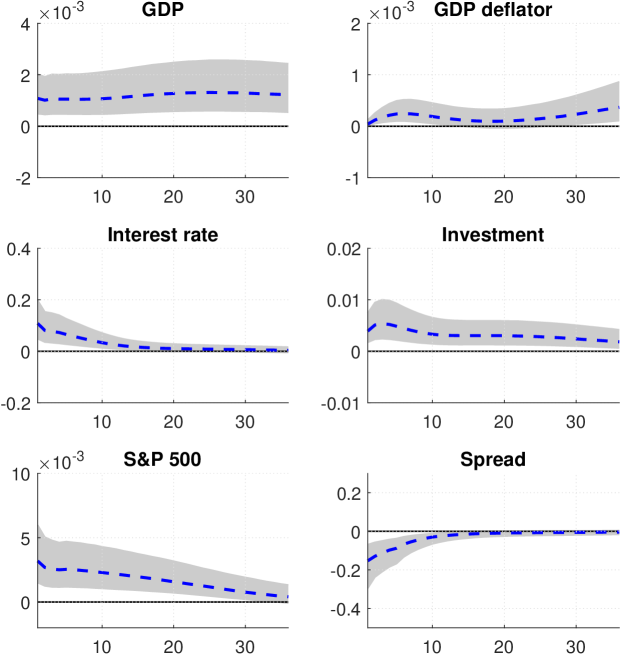

With variables and factors, this large VAR-FSV satisfies the condition that . In addition, it is easy to verify that the sign restrictions given in Table 3 satisfy the conditions in Corollary 2, and therefore the latent factors, which we interpret as structural shocks, are point-identified. Given the large number of variables, it is crucial to apply proper shrinkage on the VAR coefficients. Following the bulk of the literature (e.g., Carriero, Clark, and Marcellino, 2015), we set and —i.e., the VAR coefficients associated with lags of other variables are shrunk more strongly to 0 than those on own lags. Again we obtain 50,000 posterior after a burn-in period of 5,000 to compute the impulse responses. The results are reported in Figure 2.

The impulse responses from this 20-variable VAR-FSV are qualitatively similar to those from the smaller system, but the inference is much sharper. Specifically, the credible intervals of the 6 impulse response functions are much narrower, highlighting the benefits of incorporating more relevant information—more variables and sign restrictions as well as a more informative prior—to sharpen inference. For example, the credible intervals associated with the responses of investment and stock prices exclude zero for the first 32 quarters after the initial impact of a financial shock. This is in contrast to the much wider credible intervals from the 6-variable VAR (the median impulse responses of stock prices even become negative at longer horizons). The results from this large system therefore better highlight the impact of a positive financial shock, which Furlanetto, Ravazzolo, and Sarferaz (2019) define as “a shock that generates an investment and a stock market boom.”

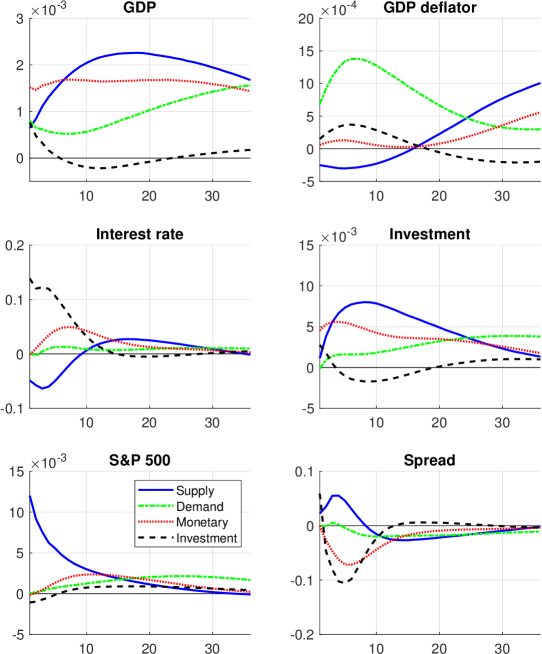

Next, we plot in Figure 3 the median impulse responses of the 6 variables from the remaining 4 structural shocks. These impulse responses are similar to those presented in Figure 3 in Furlanetto, Ravazzolo, and Sarferaz (2019). In particular, we confirm that supply shocks generate large effects not only on output, but also on investment and stock prices. On the other hand, demand shocks have smaller effects on output, investment and stock prices, at least for short to medium horizons, but they are the main driver of prices. Finally, while we also find that monetary shocks have a protracted positive effect on output, their effects on stock prices are more subdued.

8.3 Historical and Forecast Error Variance Decompositions

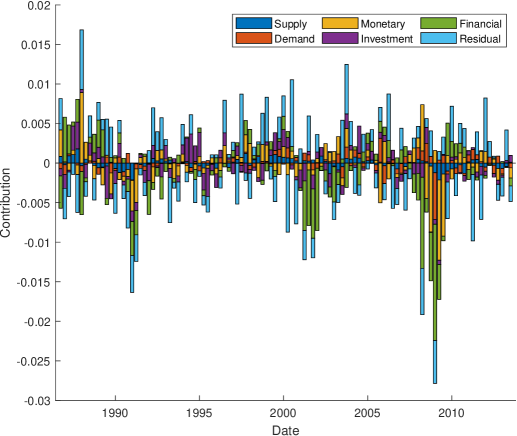

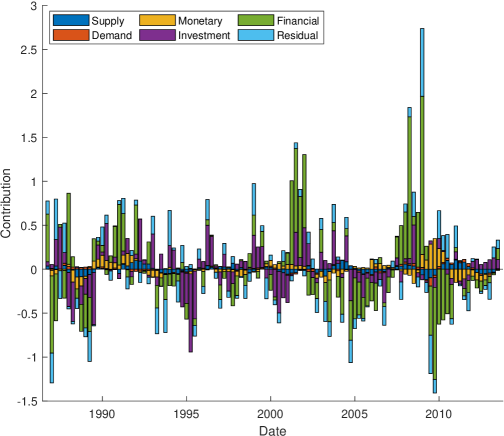

To quantify how much of the historical fluctuations in GDP and spread can be attributed to each of the structural shocks, we compute the historical decompositions of these two variables using the formulas derived in Appendix F. The results are reported in Figure 4 and Figure 5.

These historical fluctuations from the VAR-FSV are in line with those obtained using a standard structural VAR presented in Furlanetto, Ravazzolo, and Sarferaz (2019). In particular, financial shocks play a large role in explaining the historical fluctuations in both GDP and spread, especially in the lead-up and aftermath of the Great Recession of 2007-2009.

Next, we quantify the amount of the prediction mean squared errors of 6 selected variables accounted for by each of the 5 structural shocks at different forecast horizons. More specifically, using the expressions developed in Appendix F, we compute the forecast error variance decompositions of the variables and the results are presented in Table 4.

| Horizon | Supply | Demand | Monetary | Investment | Financial | |

|---|---|---|---|---|---|---|

| GDP | 1 | 0.08 | 0.13 | 0.45 | 0.11 | 0.23 |

| 5 | 0.12 | 0.11 | 0.46 | 0.08 | 0.23 | |

| 20 | 0.16 | 0.10 | 0.46 | 0.06 | 0.22 | |

| GDP deflator | 1 | 0.11 | 0.84 | 0.01 | 0.04 | 0.00 |

| 5 | 0.09 | 0.84 | 0.01 | 0.05 | 0.01 | |

| 20 | 0.07 | 0.85 | 0.01 | 0.05 | 0.02 | |

| Interest rate | 1 | 0.07 | 0.00 | 0.00 | 0.58 | 0.35 |

| 5 | 0.10 | 0.00 | 0.00 | 0.58 | 0.32 | |

| 20 | 0.12 | 0.00 | 0.01 | 0.58 | 0.29 | |

| Investment | 1 | 0.07 | 0.01 | 0.44 | 0.16 | 0.33 |

| 5 | 0.15 | 0.02 | 0.40 | 0.09 | 0.34 | |

| 20 | 0.23 | 0.02 | 0.37 | 0.06 | 0.32 | |

| S&P 500 | 1 | 0.92 | 0.00 | 0.00 | 0.01 | 0.07 |

| 5 | 0.91 | 0.00 | 0.00 | 0.01 | 0.07 | |

| 20 | 0.91 | 0.00 | 0.00 | 0.01 | 0.08 | |

| Spread | 1 | 0.02 | 0.00 | 0.00 | 0.13 | 0.85 |

| 5 | 0.04 | 0.00 | 0.01 | 0.15 | 0.79 | |

| 20 | 0.07 | 0.01 | 0.04 | 0.19 | 0.69 |

Overall, financial shocks play a large role in explaining the forecast error variances of the majority of the variables. The two exceptions are prices (measured by GDP deflator), which are mainly impacted by demand shocks, and stock prices (measured by S&P 500 index), which are mostly driven by supply shocks.

9 Concluding Remarks

We have considered an order-invariant VAR with factor stochastic volatility and shown how the presence of multivariate stochastic volatility allows for statistical identification of the model. Furthermore, we have worked out sufficient conditions in terms of sign restrictions on the impact of the structural shocks for point-identification of the corresponding structural model. To estimate the proposed order-invariant VAR, we developed an efficient MCMC algorithm that can incorporate a large number of variables and sign restrictions. In an empirical application involving 20 macroeconomic and financial variables, we demonstrated the ability of our methods to produce more precise impulse responses compared to a medium-sized structural VAR.

Appendix A: Proofs of Propositions

In this appendix we provide the proofs of the propositions and corollaries stated in the main text. To that end, we first consider the following two lemmas.

Lemma 1 (Magnus and Neudecker (2019), Theorem 2.13, pp. 43).

A necessary and sufficient condition for the matrix equation to have a solution is that

| (22) |

where denotes the Moore–Penrose inverse of . In this case the general solution is

| (23) |

where is an arbitrary matrix of the appropriate dimension. In particular, if has full column rank and has full row rank, then the unique solution is given by:

| (24) |

Proof of Lemma 1: The proof that (22) is the necessary and sufficient condition and that the general solution has the form in (23) follows directly from Magnus and Neudecker (2019). For uniqueness (24), note that if and have full column and row rank, respectively, their Moore–Penrose inverses can be computed as:

It then follows that and , and therefore (23) reduces to (24). ∎

The next lemma adapts a theorem in Anderson and Rubin (1956) to our setting with heteroskedastic factors.

Lemma 2 (Anderson and Rubin (1956), Theorem 5.1, pp. 118).

Under Assumption 2, the common and idiosyncratic variance components are separately identified. That is, for two observationally equivalent models such that , we have and .

Proof of Lemma 2: Suppose we have two observationally equivalent models such that . We wish to show that and . Since the off-diagonal elements of and of are the corresponding off-diagonal elements of , it suffices to show that the diagonal elements of are equal to the diagonal elements of . First note that Assumption 2 implies that . Furthermore, let

where and are nonsingular square matrices of dimension , is the -th row, and is of dimension (it can be null if ); is partitioned into submatrices similarly. Then, we have

and has the same form. Since , , are off-diagonal, , and . Note that since and are nonsingular, so is . Next, since is of rank , any square submatrix of dimension larger than is singular. In particular,

Similarly, . Since , we must have . In the same fashion, we can show that the other diagonal elements of are equal to those of . ∎

Proof of Proposition 2: Suppose we have two observationally equivalent models such that . Under Assumption 2, Lemma 2 implies that the common and the idiosyncratic variance components can be separately identified, i.e., and .

For notational convenience, let and . Consider the first identity . By Lemma 1, the necessary and sufficient condition to solve the system of equations for is

| (25) |

where and since has full column rank. Let and denote, respectively, the element of and the product . Equation (25) implies that , . Under the assumption that the elements in are linearly independent (i.e., the only solution to for all is ), we must have . Hence, is obtained once is determined. We consider . As will be clear later, the same conclusion applies for the case .

We next turn to the determination of . Since has full column rank, again by Lemma 1, the unique solution to is . In particular, since is diagonal, we have for and . These restrictions can be more succinctly expressed as , where and is . Given that the rank of is when the processes in are linearly independent for , the only solution to such a set of homogeneous linear equations is irrespective of and . Therefore, each column of contains at most one nonzero element (otherwise for some column there exist nonzero elements and with such that , contradicting ). In this scenario, similar to Bertsche and Braun (2020), we can write , where is one of the permutation matrices, is a reflection matrix that corresponds to one of the ways to switch the signs of the columns, and is an arbitrary diagonal scaling matrix of dimension .

Next, we show that must be an identity matrix. Using the fact that , we can write the observationally equivalent factors as . Without loss of generality, we consider solely the scaling effect, i.e., . Now, , where

| (26) |

Since we standardize the unconditional variances of the log stochastic volatility processes to be one, we must have for , which implies that . Thus, , and the only form can take is . ∎

Proof of Proposition 3: The proposition is equivalent to the claim that the only feasible factor loadings submatrix under the assumptions must satisfy , where . In what follows, we prove the claim by using a similar approach as in the proof of Proposition 2. First notice that since satisfies Assumption 2, any observationally equivalent model must satisfy . Applying the same argument as in the proof of Proposition 2, the solution must be in the form , and it follows that . Partition conformably as , where is and is . We thus have

| (27) |

Again, since is diagonal, the off-diagonal elements of must be zero, i.e., for and , where is the -th element in .

For a given pair , these restrictions can be expressed as , where is a matrix, for , . Given that the rank of is when the processes in are linearly independent, the only solution to such a set of homogeneous linear equations is irrespective of and . Therefore, applying the same argument as before, the condition that the first restrictions in —i.e., —implies that each column of contains at most one element that is different from 0.

Next, we show that any nonzero elements can only be in the upper rows of , which in turn makes the lower rows a zero submatrix. To that end, we partition conformably and write (27) as:

Since is diagonal, we must have

| (28) | ||||

| (29) | ||||

and is diagonal. Using exactly the same argument in analyzing (27), being diagonal implies a set of homogeneous linear equations of dimension . It follows that each column of contains at most one nonzero element. Since earlier we have proved the same result for , it must be the case that all the nonzero elements are in , i.e., . Otherwise, there is a least one row in whose elements are all 0, say row with , which implies that

| (30) |

where denotes the -th element of . It is clear that (30) violates the assumption that are linearly independent for all .

Now, using the fact that in (28), it follows is an orthogonal matrix. Next, using the fact that in (29), we have since the orthogonal matrix is invertible. Subsequently, the -th block of reduces to . From the earlier conclusion that each column of has at most one nonzero element and the standardization requirement as shown in (26), it is clear that must be of the form . To summarize, we have shown that

where is an orthogonal matrix of dimension . ∎

Proof of Corollary 1: The proof follows directly from the proof of Proposition 3. More specifically, under the assumption , is an orthogonal matrix of dimension 1. Thus the only admissible is . So the full matrix is also of the form . ∎

Appendix B: Estimation Details

In this appendix we provide the estimation details for fitting the model in (1)–(5). More specifically, posterior draws can be obtained by sampling sequentially from the following distributions:

-

1.

;

-

2.

;

-

3.

;

-

4.

;

-

5.

;

-

6.

.

In Section 4 of the main text we describe the implementation details of Step 1 and Step2. Below we give the details of the remaining steps.

Step 3: Sample . Again given the latent factors , the VAR becomes unrelated regressions and we can sample each vector of log-volatilities separately. More specifically, we can directly apply the auxiliary mixture sampler in Kim, Shephard, and Chib (1998) in conjunction with the precision sampler of Chan and Jeliazkov (2009) to sample from for . For a textbook treatment, see, e.g., Chan, Koop, Poirier, and Tobias (2019) chapter 19.

Step 4: Sample . This step can be done easily, as the elements of are conditionally independent and, for , each follows an inverse-gamma distribution:

where , with the understanding that for .

Step 5: Sample . It is also straightforward to implement this step, as the elements of are conditionally independent and, for , each follows a normal distribution:

where

Step 6: To sample , note that

where and is the truncated normal prior, with the understanding that for . The conditional density is non-standard, but a draw from it can be obtained by using an independence-chain Metropolis-Hastings step with proposal distribution , where

Then, given the current draw , a proposal is accepted with probability ; otherwise the Markov chain stays at the current state .

Appendix C: Technical Details on Integrated Likelihood Evaluation

In this appendix we provide the technical details for evaluating the integrated likelihood outlined in Section 5.1. Recall that the integrated likelihood can be written as

| (31) |

where the first term in the integrant has the following expression

Next, we derive the joint density of the log-volatilities . To that end, stack the state equations (4)-(5) over :

where and

Or equivalently

as the determinant of the square matrix is one and is thus invertible. It follows that with log-density

Next, we introduce an importance sampling estimator to evaluate the integral in (31). The ideal zero-variance importance sampling density in this case is the conditional density of given the data and other parameters but marginal of , i.e., . But this density cannot be directly used as an importance sampling density as it is non-standard. We instead approximate it using a Gaussian density, which is then used as the importance sampling density.

An EM Algorithm to Obtain the Mode of

We first develop an EM algorithm to find the maximizer of the log marginal density . To implement the E-step, we compute the following conditional expectation for an arbitrary vector :

where the expectation is taken with respect to . As discussed in Section 4 of the main text, the latent factors are conditionally independent given the data and model parameters. In fact, for , they have the following Gaussian distributions:

where

Note that here we use to construct and instead of .

Then, an explicit expression of can be derived as follows:

where and is a constant not dependent on .

In the M-step, we maximize the function with respect to . This can be done using the Newton-Raphson method (see, e.g., Kroese, Taimre, and Botev, 2011). To compute the gradient and Hessian of , let denote the -th diagonal element of , . Similarly, let denote the -th diagonal element of , . Finally, define , where . Then, we can rewrite more compactly as

Hence, the gradient is given by

and the Hessian is

| (32) |

where denotes the entry-wise product. Since the determinant is strictly positive and the diagonal elements of are positive, the Hessian is negative definite for all . This guarantees fast convergence of the Newton-Raphson method. In addition, the Hessian is a band matrix. This property can be used to further speed up computations with sparse and band matrix routines.

Given the E- and M-steps above, the EM algorithm can be implemented as follows. We initialize the algorithm with for some constant vector . At the -th iteration, we obtain and , where and are evaluated using . Then, we compute

using the Newton-Raphson method. We repeat the E- and M-steps until some convergence criterion is met, e.g., the norm between consecutive is less than a pre-determined tolerance value. At the end of the EM algorithm, we obtain the mode of the density , which is denoted by . We summarize the EM algorithm in Algorithm 3.

Suppose we have an initial guess and error tolerance levels and , say, . The EM algorithm consists of iterating the following steps for :

-

1.

E-Step: Given the current value , compute , and

-

2.

M-Step: Maximize with respect to by the Newton-Raphson method. That is, set and iterate the following steps for :

-

(a)

Compute and using , and obtained in the E-step, and set

-

(b)

Update

-

(c)

If, for example, , terminate the iteration and set .

-

(a)

-

3.

Stopping condition: if, for example, , terminate the algorithm.

Computing the Hessian of

After obtaining the mode of the log density , next we compute the Hessian evaluated at . Here we describe two approaches to do so. In the first approach, we provide an approximation of the Hessian using the EM algorithm. The resulting matrix is banded and is guaranteed to be negative definite. In the second approach, we directly compute the Hessian of . In our experience the two approaches give very similar results, but the first approach is more numerically stable.

In what follows, we start with the first approach. Note that by Bayes’ theorem, we have

If we take the log of both sides and then take expectation with respect to , we obtain the identity

| (33) |

where .

It follows that the Hessian of evaluated at is simply the sum of the Hessians of and with . Note that the Hessian of comes out as a by-product of the EM algorithm; an analytical expression is given in (32). We use it as an approximation of the Hessian of evaluated at . Next, we derive an analytical expression for :

where is a constant not dependent on and . In the above derivation we have used the fact that under , the quadratic form is a chi-squared random variable and its expectation does not depend on (and thus absorbed into the constant ).

To compute the Hessian of , we first note that

where is the -th row of . Next, using standard results of matrix differentiation, we obtain

Hence, the Hessian is block diagonal (and hence banded). More specifically, the Hessian of can be written in the following matrix form

where with

Finally, let denote the Hessian of evaluated at . Then, the negative Hessian of the log marginal density of evaluated at is simply , which is used as the precision matrix of the Gaussian approximation. Note that since both and are band matrices, so is .

The second approach directly computes the Hessian of the log marginal density:

where , and and are constants not dependent on . Next we derive the Hessians of the functions and .

Let . Then, . Using a similar derivation of in the EM algorithm, it is easy to see that the Hessian of is given by:

where with . It is also clear that the Hessian of is simply

Next, we derive the Hessian of below. First note that

where is the -th row of . Next, using standard results of matrix differentiation, we obtain

More specifically, the Hessian of can be written in the following matrix form