Convergence of the dynamical discrete web to the dynamical Brownian web

Abstract

In this paper we study the convergence of dynamical discrete web (DyDW) to the dynamical Brownian web (DyBW) in the path space topology. We show that almost surely the DyBW has RCLL paths taking values in an appropriate metric space and as a sequence of RCLL paths, the scaled dynamical discrete web converges to the DyBW. This proves weak convergence of the DyDW process to the DyBW process.

1 Introduction and main result

In this paper, we present a number of results concerning a dynamical version of the Brownian web (BW), known as the dynamical Brownian web (DyBW) and convergence to it for a dynamical version of coalescing random walks model known as the dynamical discrete web (DyDW). The DyDW was introduced by Howitt and Warren [HW09], is a system of coalescing simple symmetric one-dimensional random walks evolving over a dynamic time interval . We first describe the DyDW model briefly.

The discrete web (DW) is a collection of one-dimensional simple symmetric random walks starting from every point in the discrete space-time domain . We consider an i.i.d. collection of random variables such that

where gives the random walk increment at location at time . Following the walk, the walker at goes to along the edge . Thus, following the edges in DW we get a (random) collection of paths. The motivation for calling this system as the DW comes from the fact that under diffusive scaling as a collection of paths, the DW converges to the BW (Theorem 6.1 of [FINR04]). For the dynamical version, we start with an ordinary DW at dynamic time and at each lattice point, direction of the outgoing edge switches at a fixed rate independently of all other lattice points. This gives DyDW as a process of collection of paths evolving dynamically over the time interval .

Howitt and Warren [HW09] rightly guessed that if we slow down the rate of switching (of outgoings edges) by , then under diffusive scaling, there should be a non-trivial scaling limit the dynamical Brownian web process . Assuming existence of such a process, it’s finite dimensional distributions were analysed in [HW09] and it was shown that for , the distribution of is given by sticky pair of Brownian webs with degree of stickiness is given by (for a definition of sticky pair of Brownian webs see Section 3.2.1). Existence of a consistent family of finite dimensional distribution for follows from this and stationarity and Markov property proved in Theorem 6.2 of [NRS10] . In [NRS10], Newman et al. proved that such a process uniquely exists and provided a rigorous construction of the DyBW as well. In another work [NRS09A], a sketch of the proof of convergence of finite dimensional distributions of DyDW to that of DyBW was given. But to the best of our knowledge, weak convergence of the DyDW process to the DyBW process has not been shown so far. Our goal in this paper is to provide a stronger topological setting for studying this convergence and give a proof for convergence in that setting, namely as a process with RCLL paths. We state our result in detail in Theorem 3.2. Towards this, we established that the DyBW process has RCLL paths a.s. (taking values in an appropriate metric space). We prove this in Theorem 2.2.

The paper is organised as follows. In Section 2 we prove that the DyBW has RCLL paths taking values in an appropriate metric space a.s. Details of the relevant metric space have also been described. In Section 3 we describe the DyDW model and prove that it’s finite dimensional distributions converges to that of DyBW. The main argument for the same was already developed in [NRS09A]. Finally, in Section 4 we prove that as a sequence of RCLL paths, the sequence of scaled dynamic discrete webs is tight and hence, we have process level convergence.

2 DyBW is a.s. RCLL path process

In this section we show that the DyBW process has RCLL paths a.s. (Theorem 2.2). The standard BW originated in the work of Arratia ( see [A79] and [A81]) as the scaling limit of the voter model on . Later Tóth and Werner [TW98] gave a construction of a system of coalescing Brownian motions starting from every point in space-time plane and used it to construct the true self-repelling motion. Intuitively, the BW can be thought of as a collection of one-dimensional coalescing Brownian motions starting from every point in the space time plane . Later Fontes et. al. [FINR04] provided a framework in which the Brownian web is realized as a random variable taking values in a Polish space, which enabled them to prove the weak convergence to the Brownian web of coalescing random walks starting from every point of the space-time lattice in the diffusive scaling limit. In the following section we recall relevant details from [FINR04] to describe the Polish space of our interest.

2.1 Preliminary details about Polish space of collection of paths

Let denote the completion of the space time plane with respect to the metric

As a topological space can be identified with the continuous image of under a map that identifies the line with the point , and the line with the point . A path in with starting time is a mapping such that and is a continuous map from to . We then define to be the space of all paths in with all possible starting times in . The following metric, for

makes a complete, separable metric space. Convergence in this metric can be described as locally uniform convergence of paths as well as convergence of starting times. Let be the space of compact subsets of equipped with the Hausdorff metric given by,

The space is a complete separable metric space. Let be the Borel algebra on the metric space . The Brownian web is an valued random variable. Below we state Theorem 2.1 of [FINR04] characterizing the Brownian web as a -valued random variable.

Theorem 2.1 (Theorem 2.1 of [FINR04]).

There exists an -valued random variable whose distribution is uniquely determined by the following properties:

-

from any deterministic point , there is almost surely a unique path starting from ;

-

for a finite set of deterministic points , the collection is distributed as coalescing Brownian motions starting from ;

-

for any countable deterministic dense set of , is the closure of in almost surely.

The DyBW is defined as a -valued process evolving over dynamic time domain with finite dimensional distributions as mentioned in Section 3.2.1. Newman et. al. [NRS10] provided a rigorous construction and showed that such a process indeed exists. Our next result shows that the DyBW process has -valued RCLL paths a.s.

Theorem 2.2.

The DyBW process has RCLL paths a.s.

In what follows, we denote the Polish space of -valued RCLL paths defined over with Skorohod metric as . In other words, Theorem 2.2 gives us that the DyBW is a valued random variable.

While providing a a rigorous construction of the DyBW , Newman et. al. developed an alternate construction of the Brownian net as well. Their work presents a construction of the DyBW and the Brownian net both constructed on a common probability space. In this work we will extensively use this correspondence and refer this as ‘the corresponding net ’ of the DyBW and vice versa. In the next section we describe their common construction and the corresponding net briefly. For details we refer the reader to Theorem 5.5 and Proposition 6.1 of [NRS10].

2.2 The ‘corresponding’ Brownian net

The approach of Newman et. al. [NRS10] is based on the construction of a certain Poissonian marking which is governed by local time of the forward web along the backward web, i.e., construction of a three-dimensional Poisson point process with intensity measure , where is Lebesgue measure and is the local time measure of the forward web along the backward web. For a deterministic point almost surely there is exactly one outgoing path starting at and no incoming path passing through in the Brownian web.

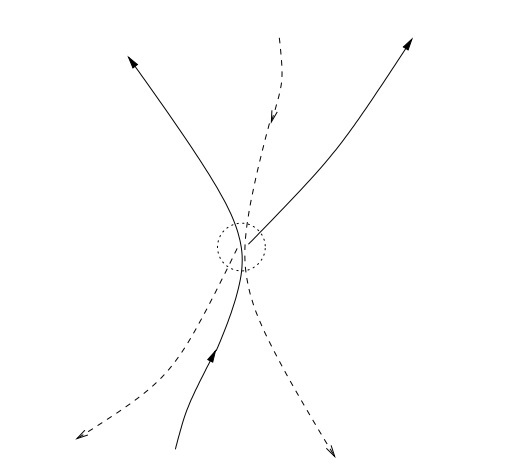

But there are random points in the BW where a single Brownian web path enters the point from an earlier time and two paths leave from that. Among the two outgoing paths, exactly one path is the continuation of the (incoming) path coming from earlier time and the other one is “newly-born” (see Figure 1).

Further, points of BW are precisely those at which a forward and a backward path meet and the set of ‘marked points’ will be supported on the set of points. Each point has a preferred left or right “direction” and accordingly it is denoted as or . For a () point, the continuing path (coming in from earlier time) is to the right (left) of the “newly-born” path. One of the major observation of [NRS10] is that at the continuum level, the analogue of DyDW switching will simply be change of directions at all marked (1, 2) points. In other words, the DyBW at dynamic time , denoted by , will be deduced from the initial BW by switching directions of all marked points, marked during dynamic time interval . We should mention that the situation is much more complicated here since, is not locally finite as the set of points is dense in . However, as showed in [NRS10], one can approximate by a sequence of locally finite measures and do the markings using , and then let .

Further, it was shown that the same marked point process gives an alternate construction of the Brownian net, viz., for a marked point, which was originally an point say, the Brownian net includes not only paths that connect to the left outgoing path (as in the original web) but also ones that connect to the right outgoing path. Formally, for deterministic consider the a.s. unique starting from in the initial BW . For each consider the set of all the paths obtained by continuing along both the right and left outgoing paths at each ‘marked’ point on the trajectory of and this collection gives the standard Brownian net (Theorem 5.5 of [NRS10]). The above construction using Poissonian marking of (1,2) points allows us to have the standard DyBW and the standard Brownian net defined on the same probability space. In this paper, we refer this as the “corresponding” Brownian net corresponding to the DyBW and we will use this correspondence extensively. We note that the Brownian net uniquely defines the dual net. This allows us to define the “the corresponding” double Brownian net vector where is the dual for .

We note here that for any interval (open or closed) we use the same construction to construct the ‘corresponding’ net corresponding to the DyBW process considering ‘markings’ only in the dynamic time interval . For any deterministic we have

Before ending this section we need to define some important quantities associated with the corresponding Brownian net .

For any path and for , its restriction over the time domain is denoted as . For and for any interval , the notation is defined as

In other words, the quantity does not consider distance between starting points and represents distance between restricted trajectories of these two paths w.r.t. spatial part of metric restricted over the time interval . For a general collection of paths we describe the notion of separation points as follows.

Definition 2.3.

For a path family , a point is said to be a ‘separation point’ if there exist such that the following conditions are satisfied :

-

(i)

and , i.e., both the paths start strictly before time and pass through the point ;

-

(ii)

The first meeting time of after defined as

is strictly bigger than .

Let denote the set of separation points in . Definition of a separating point suggests that for each separating point there exist paths which get separated at and create an excursion set, which is a subset of , in between them over the time interval . The (random) set of separation points in the corresponding Brownian net is denoted as . We mention here that our notion of separation points for is slightly different from the notion of separation points as introduced in [NRS10] which we mention below:

Definition 2.4 (Definition 7.2 [NRS10]).

For a (random) point with is said to be a separation point iff there are two paths and in the Brownian net starting from and separating at which do not touch (intersect) on .

Let denote the set of all separating points in the corresponding Brownian net . We observe that a.s. for all .

Clearly, for Brownian net a separation point must necessarily be a marked point. There can be several excursion sets created at a separation point . We are going to define the maximal excursion set and several other quantities related to maximal excursion set generated at a separation point, i.e., at a marked type point here:

-

(1)

Maximal excursion set generated at a separating point is denoted by and defined as

-

(2)

Diameter/width at a separating point (of the maximal excursion set at ) is denoted by and defined as

-

(3)

Survival time of a separating point (of the maximal excursion set at ) is denoted by and defined as

-

(4)

Age of a separating point (of the maximal excursion set at ) is denoted by and defined as

For , the set of separating points in with diameter more than is denoted as and defined as

Similarly, the sets and are defined.

For ease of notation, for an interval for ease of notation, let denote the set of separation points . Next, for a separating point based on the path family , we define the diameter, age and survival time quantities denoted by respectively. Based on the above quantities, for we define the following random set of separation points:

For deterministic we have

Fix . For for ease of notation we set

In the next section we use the correspondence between the DyBW and the Brownian net and prove Theorem 2.2.

2.3 Proof of Theorem 2.2

We first start with some basics on RCLL paths. Let denote a general metric space. For a valued function defined over and for any subset we define

For , the notation denotes the natural extension of modulus of continuity for a general function defined as

where the infimum is taken over all partitions of , with for all . We have the following characterisation of RCLL functions (see page 123 of [B99]):

Lemma 2.5.

is RCLL if and only if .

Before we proceed further, we want to make an useful observation regarding the function that just follows from the triangle inequality.

Remark 2.6.

For an RCLL function and for any which is not a jump point, we have

Considering the dynamical Brownian web (DyBW) as a -valued stochastic process over the dynamic time domain , with a slight of abuse of notation, we denote corresponding quantities for the DyBW as . Because of Lemma 2.5, in order to prove Theorem 2.2, it suffices to prove the following proposition.

Proposition 2.7.

For any a.s. there exists (random) such that for all , we have .

In other words Proposition 2.7 tells us that a.s. Proposition 2.7 will be proved through a sequence of lemmas.

We recall the notations introduced in the previous section and it is straightforward to observe that for any we have

Before we proceed further, we make some important remarks.

Remark 2.8.

-

(i)

We observe that a type point of belongs to the set of separating points of the corresponding Brownian net only if it undergoes switching during the interval which means that the Poisson clock triggering switching event associated to must ring during this interval. That is it is a “marked” point and marking occurs during the interval .

-

(ii)

For , let and denote the trajectory of a ‘skeletal’ Brownian path at dynamic times respectively. As is a skeletal Brownian path (starting from a point in ), we have . If none of the type points on the trajectory of belongs to the set , then we must have .

The next lemma shows that for any , the quantity must be sufficiently large as well.

Lemma 2.9.

Fix . For any interval there exists (which does not depend on ) such that a.s. we have .

Proof.

We observe that

where denotes the corresponding Brownian net. We also note that a.s. paths in the Brownian net form an equicontinuous path family. This allows us to define as

| (1) |

By definition, we have a.s. Equation (2.3) ensures that for any with and for any interval satisfying for all , we have . This follows from the observation that

For any there exist paths in the corresponding Brownian net passing through with . In order to have , we must have

In other words, the paths and are allowed to intersect only after time where . This implies that and completes the proof. ∎

Next, for and for any interval we define

| (2) |

where is as in (2.3). For simplicity of notations, we set . It is not difficult to observe that for any we have .

Lemma 2.9 gives us that

Lemma 2.10.

Fix . There exists such that for any interval we have

| (3) |

Proof.

By definition, for any we have

Hence, we can choose such that for any both the following conditions hold:

-

(i)

as well as

-

(ii)

at least one of the two outgoing paths starting from intersects the region .

We will show that there exists such that the region contains the set . We will present a sketch of the proof here.

First we Consider outgoing paths starting from -type points from left of the box . For we define the rectangle as . A non-negative integer valued r.v. is defined as

We need to show that is a.s. finite. Towards that for we define the event:

For , the total number of points in is dominated by the total number of type points in . The total number of type points in is of finite expectation and hence, Markov’s inequality gives us . By applying Borel Cantelli lemma we conclude that is finite a.s.

Next, we define the r.v. as

In order to prove Lemma 2.10 it suffices to show that the r.v. is also a.s. finite. Towards that, for we define the event

For let denote the event that . Note that the collection gives a partition of . For any we show that on the event we have

| (4) |

By Borel Cantelli lemma, Equation (4) implies that on the event the r.v. is a.s. finite. As forms a partition of the whole space, this completes the proof.

The argument for showing (4) is standard and we only give a sketch here. With a slight abuse of notation let denote a Brownian motion with drift . Application of union bound together with translation invariance nature of our model allows us to bound the probability for any as

As the probability decays exponentially in and hence, we have for all . This completes the proof. ∎

Next, we show that the set must be finite a.s. Let be an a.s. strictly positive random variable defined as

| (5) |

where is as in (2.3). We are now ready to state the next lemma.

Lemma 2.11.

Proof.

As argued earlier, it is enough to prove Lemma 2.11 for . Because of Lemma 2.10, it suffices to show that any in must belong to for some . By definition, for any , we must have for some . The choice of ensures that in the corresponding Brownian net , there must be an incoming path which starts before and passes through . On the other hand, Lemma 2.9 ensures that we also have .

This ensures that in the corresponding Brownian net , there are two outgoing paths which start before time , get separated at and thereafter, they are not allowed to meet before time . Finally, for any deterministic , the set can not contain any type points. So for any , there must exist such that and the outgoing paths remain separated till time . Together with Lemma 2.10, this completes the proof. ∎

For any interval we consider the set and the set of corresponding Poisson clock rings for switching events is denoted as . Clearly, is a random subset of . For ease of notation the set is simply denoted as . Clearly, for any we have

Since are locally finite (see Proposition 7.9 of [NRS10]) Lemma 2.11 gives us that the set is finite almost surely . This implies that that the set is a.s. finite as well. The next lemma shows that for any in order to have the set must be non-empty.

Lemma 2.12.

For and for , on the event we must have .

Proof.

We first observe that in order to have , there must be dynamic times with and a skeletal Brownian path (i.e., starting from a point in ) such that

| (6) |

where denotes the trajectory of the skeletal path at dynamic time . A skeletal path starts from a point in (which is not a type point a.s.) and hence starting time of a skeletal path does not change over dynamic time interval. Therefore the starting time of a skeletal path does not depend on dynamic time and denoted by .

Equation (6) necessarily implies that where denotes the trajectory of the same skeletal path at dynamic time . Hence, in order to have (6), there must be a separating point on the trajectory of , as a point of separation between and , such that

In other words, in order to have (6), the set must be non-empty. We observe that for any type point to be in the set , the associated Poisson clock must ring during the interval . Recall that the set represents Poisson clock rings associated to points in the set , where is as in (2.3).

Let us assume that . By Remark 2.8 this event equivalently implies that the set is empty as well. Further, the condition implies that for any , we must have . We will show that under this assumption, we can’t have (6) and henceforth we obtain a contradiction.

Choose to be a (random) point on the trajectory of such that and is not a type point. Under our assumption , the trajectory of restricted over time domain can not have a point in the set . As is not a type point, there exists a unique path in starting from the point . Our assumption also ensures that there is no point in which belongs to the trajectory of . Finally, as we have , we obtain

This completes the proof. ∎

Now we are ready to complete the proof of Proposition 2.7 and thereby proving that the DyBW is RCLL a.s.

3 Finite dimensional distribution convergence of the DyDW to the DyBW

In this section we describe finite dimensional convergence of the DyDW to the DyBW. As commented earlier, the main argument for the same was already done in [NRS09A] and we have followed the same strategy. We first start with describing the dynamic discrete web model. After that we describe finite dimensional distributions of the DyBW and in Section 3.2 we present the required finite dimensional convergence.

3.1 Dynamic discrete web (DyDW) model

The discrete web (DW) is a system of coalescing simple symmetric one-dimensional random walks starting from everywhere on the space time even lattice . We described in the beginning that we have an i.i.d. collection of Rademacher random variables where gives increment of the walker at location at time . Following the walk, the walker at reaches and this next step is denoted as . Set and for , define . Joining the successive steps we get the path starting from . The collection of all paths obtained from the DW is denoted as . For and for any , let denote the -th order diffusively scaled map given by

With a slight abuse of notation for we denote as . For and for , we define and by identifying each path with it’s graph as a subset of . For any closure of the set taken in metric is denoted as . This gives a valued random variable. Fontes et. al. [FINR04] proved that as a sequence of valued random variables, converges in distribution to the Brownian web.

Theorem 3.1 (Theorem 5.1 of [FINR04]).

As , converges in distribution to the Brownian web .

The DyDW is a dynamic evolution of the discrete web where the arrow configuration evolves continuously over dynamic time such that at each space-time point , the outgoing arrow switches at unit rate independent of everything else. In order to define the DyDW we consider independent sequences of collections of i.i.d. random variables . For each we consider a Poisson point process which is a Markov process with state space evolving over dynamic time with unit intensity. In other words, for any we have

We further assume that these Markov processes, as varies over , are mutually independent of each other. At dynamic time , for each we use the increment and this gives us a distributionally equivalent copy of the DW. Altogether, this represents the DyDW as an -valued stationary Markov process evolving over dynamic time domain .

Mathematically, for and dynamic time , next step at that instant is denoted as and given as

, i.e., the -th step at dynamic time instant is similarly defined. The path starting from at dynamic time is obtained by linearly joining successive steps . The collection of all paths obtained from DyDW at dynamic time is denoted as and represents the DyDW process defined over the dynamic time domain .

Fix and now we are going to define the -th diffusively scaled DyDW. Let denote a collection of independent Poisson processes with intensity , i.e.,

Corresponding to these Markov processes, we define

as the next step at dynamic time . The path at dynamic time is obtained by linearly joining successive steps . Let . Let denote the -th scaled collection of paths and the -th scaled DyDW process is denoted by .

In this paper we show that as the scaled DyDW as a process with RCLL paths converges to the DyBW.

Theorem 3.2.

As , the DyDW process converges to the DyBW where the convergence happens as valued random variables.

In the next section we show that the finite dimensional distributions of the DyDW process converge to that of the DyBW. A detailed sketch of the argument for the same was earlier presented in [NRS09A]. But to the best of our knowledge, weak convergence of the DyDW process to the DyBW process has not been shown so far. In Section 4 we prove tightness of the scaled DyDW and thereby complete the proof of Theorem 3.2.

3.2 Finite dimensional distribution convergence

In this section we prove the following proposition which proves finite dimensional distributional convergence for the scaled DyDW to the DyBW.

Proposition 3.3.

Fix deterministic . Then as , we have

as valued random variables.

In the next section, we describe finite dimensional distributions of the DyBW process. We prove Proposition 3.3 after that.

3.2.1 Finite dimensional distributions of the DyBW

We first recall the definition of a one-dimensional sticky (at the origin) Brownian motion.

Definition 3.4.

is a -sticky Brownian motion starting at iff there exists a one-dimensional standard Brownian motion s.t.

| (7) |

and is constrained to stay positive as soon as it hits zero.

It is known that (7) has a unique (weak) solution. For this solution can be constructed from a time-changed reflected Brownian motion as follows. Consider

| (8) |

where is the reflected Brownian motion and is its local time at the origin. Then there exists a Brownian motion such that is a solution of (7). The sticky Brownian motion is obtained from the reflected Brownian motion by “transforming” the local time into real time and as a result, it spends positive Lebesgue measure time at the origin. The larger the “degree of stickiness” is, the more the path sticks to the origin.

We now describe finite dimensional distributions of the DyBW. We first present the definition of sticky pair of Brownian motions starting from any two points in taken from [NRS10].

Definition 3.5.

is a -sticky pair of Brownian motions iff:

-

(i)

and are both Brownian motions starting at and that move independently when they do not coincide.

-

(ii)

For , define . Conditioned on , the process is a - sticky Brownian motion starting at (see Definition 7).

We call a collection of -sticking-coalescing Brownian motions, if and are each distributed as a set of coalescing Brownian motions and for any and , the pair is a -sticky pair of Brownian motions.

We will say that is a -sticky pair of Brownian webs if satisfies the following properties:

-

(a)

, resp. , is distributed as the standard Brownian web.

-

(b)

For any finite deterministic set , the subset of paths in starting from these points are jointly distributed as a collection of -sticking- coalescing Brownian motions starting from the given sets of points.

Newman et. al. [NRS10] presented a rigorous construction of the process such that for any the pair equidistributed as which has the same distribution as -sticky pair of Brownian webs. Our next remark explains that the distribution of uniquely specifies finite dimensional distributions of the DyBW process. Remark 3.6 essentially follows from stationarity and Markov property of theorem 6.2 of [NRS10].

Remark 3.6.

Set and fix . Let be such that for all , we have

| (9) |

where the notation stands for same distribution. Further, for any many deterministic points , let denote the a.s. unique path in starting from . Equation (9) guarantees existence and uniqueness of such . Suppose distribution satisfies the following:

-

(a)

For each , marginally the random path is distributed as the standard Brownian motion starting from .

-

(b)

As long as the paths are disjoint, they evolve like independent Brownian motions.

-

(c)

As soon as any two paths intersect, due to sticky interaction they spend non-trivial time together. Precisely, if paths and intersect, together they evolve like a -sticky Brownian motion.

Then we must have

where denotes the DyBW at dynamic time .

3.2.2 Proof or Proposition 3.3

Proof of Proposition 3.3: Note that the sequence is a tight sequence of -valued random variables. Consider any sub-sequential limit of the above sequence. The work of Fontes et al. [FINR04] ensures that

Because of Remark 3.6, in order to prove Proposition 3.3 it suffices to show that satisfies conditions (b) and (c) as well. Condition (a) follows from the fact that, as long as the scaled discrete web paths are disjoint, they evolve independently.

To show condition (a) we fix . Set , i.e., -th and -th path both start from origin. The DW paths evolve independently as long as they are supported on disjoint sets of lattice points and hence, taking two different starting points does not pose any additional challenge. For each , the collection denotes a collection of i.i.d. Poisson processes with intensity and these processes are taken to be independent. Corresponding to this, and denote the unscaled DW paths starting from the origin at dynamic times and respectively. We comment here that the marginal distribution of does not depend on but the joint distribution of depends on . To simplify our notation, we denote these two paths simply as and respectively. W.l.o.g. we assume that . Corresponding pair of -th order diffusivelly scaled paths are given by

For this part of the proof we follow the ideas in [NRS09] and in [NRS09A]. We observe that the pair of ‘scaled’ DW paths and alternates between times at which these two paths are equal (i.e., they “stick together”) and times at which they move independently. As soon as the paths and meet at time for some , they continue to coincide and move together as long as the clock at for some does not ring during the interval . After such a clock ticks, the two random walk paths are independent till the time they meet again. This suggests the following time decomposition. Set and for we define

As discussed before, on the interval , both the scaled paths and coincide and at time they start moving independently until meeting at . In other words, if we skip the intervals , the pair behave as two independent diffusively scaled random walks , while if we skip intervals , the two walks coincide to form a single diffusively scaled random walk which evolves independent of . We define and we have

Further, the collection is independent of the rescaled random walk paths. This analysis, which is a scaled version of Lemma 3.2 of [NRS09], is summarised as follows:

Distributionally this scaled pair is equivalent to

where are three independent rescaled random walks, and is the right continuous inverse of with,

-

(i)

;

-

(ii)

,

where ’s are i.i.d. non-negative random variables with .

Then we have

We know that converges in distribution to where is the local time at zero of where and are two independent Brownian motions (see Theorem 1.1 of [B82] and Theorem 4.1 of [K63]).

By Skorohod’s representation theorem we assume that we are working on a probability space such that converges almost surely to . Note that the scaled independent random walks are measurable. Let us denote the probability space for the i.i.d. collections as and let . Then we have

Therefore we have a.s. as . Thus we have converges to in Probability. Since,

Therefore, we have converges to in probability which implies convergence in distribution for local times. This completes the proof for Proposition 3.3.

4 Tightness part

In this section we finally prove that the scaled DyDW processes form a tight sequence as valued random variables and thereby completes the proof of Theorem 3.2.

4.0.1 Description of notations

Recall that the -th scaled discrete DyDW process is denoted as , a -valued stochastic process evolving over the dynamic time interval .

Fix . We consider the scaled DyDW process . We denote the random configuration of all outgoing edges observed over the dynamic time interval as

The random quantity basically denotes the random configuration of all ‘arrow’s observed over dynamic time domain as described in [SS08]. An -path, is the graph of a function , with , such that and is linear on the interval for all , while whenever .

The closure of collection of all -paths, i.e., paths along the arrows in , is denoted as . We observe that denotes the -th scaled discrete net considered in [SS08] and is a -valued random variable.

More generally, for any dynamic time interval collection of all outgoing edges observed over is denoted as

and the closure of collection of all -paths is denoted as .

Sun et. al showed that the discrete net converges in distribution to the standard Brownian net (Theorem 1.1 of [SS08]). Their argument also proves that for any deterministic we have

Fix . For and for any interval considering -valued random variable we define the following quantities:

For a scaled lattice point may belong to the set only if the associated Markov process ticks at least once during the dynamic time interval . In fact, for , to be in the set , the associated Markov process must tick at least once during the interval . We define the (random) set as

where is defined as in (2.3). The notation denotes the random set of Poisson clock rings attached to points in the set over dynamic time interval . For simplicity of notation we set

As observed earlier, for all and any we have and a.s.

4.0.2 Proof of tightness

First we need to show that the scaled DyDW process has RCLL -valued paths a.s. We will prove a weaker version that for all large , the process has RCLL paths a.s. For with a slight abuse of notation let denote the (generalised) modulus of continuity for the DyDW process . We first show that the same argument of Lemma 2.12 holds for the scaled DyDW process as well and gives the following lemma.

Lemma 4.1.

Fix and . For all large on the event we must have .

Proof.

The argument is essentially same as that of Lemma 2.12 and we only give a sketch of the proof here. As argued earlier, in order to have there must be a scaled path for some with a scaled separating (branching) point on it’s trajectory such that .

We choose a scaled lattice point on the trajectory of the path and above such that the difference between and starting time of in metric lies in . For large enough, we can always make such a choice and only for this part of the argument we require to be large. Under the assumption we have as well and consequently it follows that for all , the scaled path starting from at dynamic time does not have a member of on it’s trajectory. Rest of the argument is exactly same as Lemma 2.12. ∎

Lemma 4.2.

For each , the scaled DyDW process is RCLL a.s.

Proof.

The DyDW process is constructed on the discrete set of scaled lattice points. Because of Lemma 4.1, for each to show that the process is RCLL, it is enough to show that the set is contained in a compact box a.s. Fix . Properties of the metric space ensures that there exists such that

-

(i)

any scaled lattice point in the set must have and

-

(ii)

at least one of the two outgoing paths starting from must intersect with the box .

Since, the scaled DyDW paths start from scaled lattice points and for any the modulus of continuity of all the paths in is uniformly bounded by , condition (i) and (ii) ensure that the set of points in must be contained in a compact box. This completes the proof. ∎

In order to show that the sequence is tight we need to show the following proposition.

Proposition 4.3.

Fix and . There exist and such that

| (10) |

We first describe a strategy to prove the above proposition. Because of Lemma 4.1, in order to prove Proposition 4.3 it suffices to show that there exist and such that with probability bigger than , for all there exists a partition (possibly random) of with

-

(i)

and

-

(ii)

for all .

Towards this we choose (we will specify the choice of later) and partition the interval into many intervals of length given by . For simplicity of notation we denote simply as . We note that we have considered instead of and the reason for considering will be explained shortly. For any set let denote the cardinality of . We define the event

| (11) |

In other words, the event ensures that for any the set can have at most one element. Further, if the set is non-empty, then both the ‘neighbouring’ sets and must be empty.

On the event for let be such that is non-empty if and only if and set

Precisely, for each , the set is a singleton set denoted by . This allows us to choose a partition of the unit interval as

In other words, for we modify the partition as . Choose and we observe that each interval in the above partition has length strictly bigger than . For with we have implying . On the other hand for , a.s. is not a jump point and Remark 2.6 ensures that we have

| (12) |

For both the intervals on the R.H.S., we have that the corresponding sets are empty giving us that . Similar logic applies for the part too, as we have . This shows that on the event for any we have . Hence, in order to prove Proposition 4.3, it is enough to prove the following proposition.

Proposition 4.4.

Fix and . There exist such that

| (13) |

This proposition will be proved through a sequence of lemmas. We first describe our heuristics in words. The exact value of will be specified later (see (18)). We consider a partition of the unit interval into sub intervals of width . Corresponding to the partition of we consider the set for . We choose large enough so that for any the set contains at most one element and for most ’s, the set is empty. Precisely we define an event such that

and choose large enough so that is close to one. Here is a brief justification about why such a choice of is always possible. As the set is a.s. finite, the r.v. is strictly positive with probability . We observe that on the event , the event holds for any with . As decreases to zero as , we can choose large enough to make arbitrarily close to one.

Based on the above choice of we show that with high probability for all large the set is non-empty only if the set is non-empty and a non-empty contains exactly one element. This implies (13). In other words, to prove (13) it suffices to show that there exist such that

| (14) |

In the following, through a sequence of lemmas we prove (14) and thereby prove Proposition 4.4 to obtain tightness. Towards this we work on a specific probability space to use properties of almost sure convergence. Below we will construct our required probability space of almost sure convergence.

We consider a partition of the unit interval into sub intervals of width . Corresponding to this partition of the dynamic time interval, the dimensional vector of ‘corresponding’ nets is given by

We observe that for any we have . Further, we observe that

The next proposition proves that as , the vector of scaled discrete nets as valued random variable converges in distribution to the vector of corresponding nets .

Proposition 4.5.

As , we have

as valued random variables.

We postpone proving Proposition 4.5 for the moment and proceed. In fact, as the DyDW paths are independent till the time they meet, Sun et. al. [SS08] showed that the scaled rightmost and leftmost paths jointly with their first meeting times converge to left right Brownian paths and their first meeting times. The same holds for each of the dynamic time interval for . We need to introduce some notations. For let and respectively denote the leftmost and rightmost path in the Brownian net starting from . Let and respectively denote the same for the Brownian net constructed over dynamic time interval . For let denote the first meeting time of and and let denote the same for paths and . For let be such that as . For let and respectively denote the scaled leftmost and rightmost DW path in starting from . and denote the same in . For the first meeting times and are similarly defined. Assuming Proposition 4.5, we have

| (15) |

Here we give a brief justification of Equation (4.0.2). From Proposition 4.5 we have joint convergence of the vector of scaled discrete nets to the vector of Brownian nets. This guarantees that the vector of left right scaled DyDW paths in (4.0.2) converges to the vector of respective left right coalescing Brownian motions. Since, scaled DyDW paths are independent till the time they meet (at a fixed dynamic time point), respective first intersection times jointly converge too.

By Skorohod’s embedding, we assume that we are working on a probability space so that the convergence as in (4.0.2) happens almost surely. In what follows, we will continue to work on this probability space and we will use consequences of this almost sure convergence extensively. It should be mentioned here that the exact choice of will be mentioned later in Equation (18).

The next lemma follows from consequences of almost sure convergence in path space.

Lemma 4.6.

For any , we have equality of the following events

Proof.

Because of stationary nature of our model, it suffices to prove Lemma 4.6 for . On the event , we must have as the set consists of Poisson clock rings in the dynamic time interval associated to points in the set . On the other hand, it is not difficult to see that we must have

as there must be some switching event in the interval (actually ) in order to have the set non-empty. Hence, the two events are equal. Similar reasoning holds for discrete scaled nets as well. Hence, to prove Lemma 4.6 it is enough to show equality of the following events

On the event , almost sure convergence of path families ensures that the limiting Brownian net (constructed over dynamic time interval ) must have a separation point with an incoming forward path of age at least . Further, diameter of the maximal excursion set generated at is bigger than . This implies that the set must be non-empty. Hence, we have

On the other hand, on the event consider a separating point . There must exist skeletal rightmost and leftmost Brownian paths passing through and forming the right boundary and left boundary of the maximal excursion set generated at respectively. Further, their first meeting time must be smaller than . Almost sure convergence of rightmost and leftmost path families together with their first meeting times ensure that there must be sequences of paths and approximating paths and respectively and their first meeting time converges to that of and which is smaller than .

After intersection, scaled discrete web paths (rightmost and leftmost) continue to move together till they encounter a separating point (for path family ). As and approximate paths and with an fat maximal excursion set in between them, after the first meeting time there must be a separating point on their trajectory with maximal excursion set of diameter at least. More precisely, for infinitely many ’s there exist such that

To complete the proof we need to ensure that as well. This follows from the fact that the limiting net has incoming path(s) at of age at least. For large , there must be approximating incoming path(s) in passing through . This completes the proof. ∎

Lemma 4.6 suggests that for all , on the event , we must have that the r.v. is a.s. finite. This observation is used to prove the next lemma.

Lemma 4.7.

For each , there exist such that

| (16) |

Proof.

We note that the random set is a.s. finite. Further as , the set monotonically decreases to empty set. Hence, we can choose such that

where is defined considering the DyBW process over dynamic time interval . We define as the non-negative integer valued random variable

By the previous lemma on the event , the set must be non-empty. This gives us that

Hence, we can choose such that . This completes the proof. ∎

Now we are ready to prove Proposition 4.4.

Proof of Proposition 4.4: As discussed earlier, it suffices to prove Equation (14). Fix and . Remember that we need to find and such that Equation (14) holds.

For we define the event as

| (17) |

We first choose such that . Recall that the random set consists of finitely many distinct points a.s. and hence, such a choice of is always possible. Further, on the event we must have

Next, using Lemma 4.7 we choose and such that

| (18) |

As , we observe that on the event , any interval of the form can have at most one element from the set and for any such interval, the neighbouring interval(s) cannot have any element from the set .

For , let denote a non-negative integer valued random variable defined as

Lemma 4.6 ensures that the non-negative r.v. is a.s. finite. Using the collection we define

which is an a.s. finite non-negative integer valued r.v. as well. We choose so that

| (19) |

We will show that with the above choice of and with Equation (13) holds. We define the event as

With the choice of and are as before, we observe the following inclusion of events:

Hence, in order to prove (13), it is enough to show that

| (20) |

The choice of and ensure that it suffices to show that

Let denote the collection of all possible subsets of the set with at most many elements such that these subsets do not have consecutive elements. In other words,

For we define the event as

It is not difficult to see that for with , the events and are disjoint. By definition, on the event we have . Hence, Lemma 4.6 gives us the following inclusion relation

Therefore, we can express as

| (21) |

The last step follows from the fact that given that the event has occurred for some , the only way that the complement event can occur is due to the set for some and for some . Further, Lemma 4.6 ensures that on the event , the set must be non-empty. Hence, for any conditional that the event has occurred, we have the following event inclusion

This justifies the last inequality in (4.0.2). We can now write (4.0.2) as

| (22) |

The last inequality follows from application of union bound and the fact that for all . We observe that the collection of random variables depends on the evolution of the i.i.d. Markov processes over dynamic time domain .

Fix . For let denote the non-negative integer valued random variable defined as . For we define

which takes vales in . The next lemma shows that the set forms an i.i.d. collection of random variables taking vales in .

Lemma 4.8.

forms an i.i.d. collection of random variables.

Proof.

Because of stationarity of our process, it follows that for fixed the random variables ’s for are identically distributed. Fix Borel subsets in appropriate space. Let be the indicator random variable of the event . For , set the -field

Now we have

where the penultimate step follows from the fact that the r.v. is measurable w.r.t. the -field . The last equality follows from stationarity nature of our model which ensures equality of distribution of ’s. Applying the same argument repetitively completes the proof. ∎

Lemma 4.8 gives us that the event does not depend on the collection . Note that the event is measurable w.r.t. the -field . Hence, Equation (4.0.2) becomes

| (23) |

The last step follows from stationarity of our model. We recall that for any the set is defined based on the scaled DyDW (dynamic discrete web) restricted over dynamic time interval only. We define,

We observe that for every , the r.v. is a stopping time w.r.t. the filtration

The strong Markov property of the scaled process (w.r.t. dynamic time) allows us to obtain

| (24) |

As is a stopping time for the scaled DyDW process, applying Lemma 4.7 to (4.0.2) we obtain

Finally, putting this estimate in (4.0.2) gives us that

As discussed earlier, this completes the proof of (13) and thereby proves Proposition 4.4. ∎

In order to complete our proof we need to prove Proposition 4.5. To prove Proposition 4.5 we need the following notion of hopping at intersection times which is taken from [SS08].

For any collection of paths we let denote the smallest set of paths containing that is closed under hopping at intersection times, that is, is the set of all paths of the form

| (25) |

where , , and is an intersection time of and for each .

The following corollary gives us a way to identify the corresponding Brownian net corresponding to the DyBW .

Corollary 4.9.

Let denote the DyBW process with denoting the corresponding net. Let denote the collection of paths

| (26) |

consisting of DyBW paths at rational dynamic time points. Let be a standard Brownian net defined on the same probability space such that a.s. Then we must have a.s., i.e., must be the corresponding net only.

Proof.

We proved that the DyBW has -valued RCLL paths a.s. Hence, contains the set . As gives a compact collection collection of paths, our assumption

This implies that

| (27) |

Next for any , paths in the ‘corresponding’ partial net belong to . By definition for any we have . Since, Brownian net is closed under hopping (see Proposition 1.4. of [SS08]), for every Equation (27) allows us to obtain

On the other hand, [NRS10] showed (see Theorem of [NRS10]) for the corresponding net that

As is a compact collection of paths a.s., this implies that as well. Since they both have the same distribution, can not have more paths and we must have a.s. This completes the proof. ∎

Next we present an extension of the above corollary. Recall the dimensional random vector of the “corresponding” Brownian nets where is constructed using markings in the dynamic time interval only.

Corollary 4.10.

Let denote a dimensional random vector of Brownian nets such that and for any , we have . Suppose there exists a DyBW process define on the same probability space such that we have

Then we must have

where the l.h.s. denotes the random vector of ‘corresponding’ Brownian nets for the DyBW process .

The proof follows from the same argument as the earlier one. Now we are ready to prove Proposition 4.5.

Proof of Proposition 4.5 : In Section 3.2 we proved finite dimensional convergence for the scaled DyDW to the DyBW. This implies following distributional convergence

as a sequence of valued random variables.

We consider the sequence of valued random variables

It is not difficult to see that the above sequence is tight.

Let be a subsequential limit of of the above sequence. By Skorohod’s embedding theorem we assume that we are working on a probability space where we have almost sure convergence. By the work of [SS08] for all we have that

Further our construction ensures that for any we have,

In other words, for all we have

Hence, the limiting random variable must contain the set of paths . By Corollary 4.10 we have that

This completes the proof. ∎

Acknowledgement: Part of the work on this paper was done when K.S. visited K.R at NYU Abu Dhabi. Both authors wish to thank NYU Abu Dhabi for hospitality and support.

References

- [A79] R. Arratia. Coalescing Brownian motions on the line. Ph.D. Thesis, University of Wisconsin, Madison, 1979.

- [A81] R. Arratia. Coalescing Brownian motions on and the voter model on . Uncompleted manuscript available on request to the author, 1981.

- [B82] A.N. Borodin. On the asymptotic behavior of local times of recurrent random walks with finite variance. Theory of Probability and It’s Applications XXVI, 756–772, 1982.

- [B99] P. Billingsley. Convergence of probability measures, Wiley, 1999.

- [CFD09] C.F. Coletti, L.R.G. Fontes, and E.S. Dias. Scaling limit for a drainage network model. J. Appl. Probab. 46, 1184–1197, 2009.

- [FINR04] L.R.G. Fontes, M. Isopi, C.M. Newman, and K. Ravishankar. The Brownian web: characterization and convergence. Ann. Probab. 32(4), 2857–2883, 2004.

- [FNRS09] L.R.G. Fontes,C.M. Newman, K. Ravishankar and E. Schertzer. Exceptional times for the dynamical discrete web. Stochastic Processes and their Applications 119, 2832–-2858, 2009.

- [HW09] C. Howitt and J. Warren. Dynamics for the Brownian web and the erosion flow. Stoc. Proc. Appl. 119, 2028–2051, 2009.

- [GRS04] S. Gangopadhyay, R. Roy, and A. Sarkar. Random oriented Trees: a Model of drainage networks. Ann. Appl. Probab., 14, 1242–1266, 2004.

- [K63] F. B. Knight. Random walks and sojourn density process of Brownian motion. Trans. Amer. Math. Soc., 109, 56–86, 1963.

- [NRS09] L.R.G. Fontes, C.M. Newman, K. Ravishankar, and E. Schertzer. Exceptional times for the dynamical discrete web. Stoc. Proc. Appl. 119, 2832–2858, 2009.

- [NRS09A] L.R.G. Fontes, C.M. Newman, K. Ravishankar, and E. Schertzer. The dynamical discrete web. arXiv:0704.2706

- [NRS10] C.M. Newman, K. Ravishankar, and E. Schertzer. Marking points of the Brownian web and applications. AIHP 46, 537–574, 2010.

- [SS08] R. Sun, R. and J. M. Swart, “The Brownian net”, Ann. Probab., 36:1153-1208, 2008.

- [SSS09] E. Schertzer, R. Sun, and J. M. Swart, “Special points of the Brownian net”, Electron. J. Probab., 14: 805-864, 2009.

- [TW98] B. Tóth and W. Werner. The true self-repelling motion. Probability Theory and Related Fields, 111:375–452, 1998.

Department of Mathematics, 1 Hawk Drive, New Paltz, NY 12561

E-mail address, K. Ravishankar: ravi101048@gmail.com

Department of Mathematics, Ashoka University, Sonipat, India

E-mail address, K. Saha: kumarjitsaha@gmail.com