Cost-efficient Payoffs under Model Ambiguity

Abstract

Dybvig (1988a, b) solves in a complete market setting the problem of finding a payoff that is cheapest possible in reaching a given target distribution (“cost-efficient payoff”). In the presence of ambiguity, the distribution of a payoff is, however, no longer known with certainty. We study the problem of finding the cheapest possible payoff whose worst-case distribution stochastically dominates a given target distribution (“robust cost-efficient payoff”) and determine solutions under certain conditions. We study the link between “robust cost-efficiency” and the maxmin expected utility setting of Gilboa and Schmeidler, as well as more generally with robust preferences in a possibly non-expected utility setting. Specifically, we show that solutions to maxmin robust expected utility are necessarily robust cost-efficient. We illustrate our study with examples involving uncertainty both on the drift and on the volatility of the

risky asset.

KEYWORDS: Cost-efficient payoffs, model ambiguity, maxmin utility,

robust preferences, drift and volatility uncertainty

JEL classification: C02, C63, D80

AMS classification: 91B30, 62E17

1 Introduction

In a (complete) market without ambiguity, Dybvig (1988a, b) characterizes optimal payoffs for agents having law-invariant increasing preferences (e.g., expected utility maximizers). His result is based on the observation that any optimal payoff must be cost-efficient in the sense that there cannot exist another payoff with the same probability distribution that is strictly cheaper than . He then derives, for a given target distribution of terminal wealth, the payoff that achieves this target distribution at the lowest possible cost (cost-efficient payoff). Optimal portfolios are thus driven by distributional constraints rather than appearing as a solution to some optimal expected utility problem. In this regard, Brennan and Solanki (1981) note that “from a practical point of view it may well prove easier for the investor to choose directly his optimal payoff function than it would be for him to communicate his utility function to a portfolio manager.” Sharpe et al. (2000) and Goldstein et al. (2008) introduce a tool called the distribution builder, which makes it possible for investors to analyze distributions of terminal wealth and to choose their preferred one among alternatives with equal cost; see also Sharpe (2011) and Monin (2014). Moreover, Goldstein et al. (2008) argue that such a tool makes it possible to better elicit investor’s preferences.

Our main objective is to extend Dybvig’s results when there is uncertainty on the real-world probability measure. Uncertainty has become a prime issue in many academic domains, from economics to environmental science and psychology. Model ambiguity refers to random phenomena or outcomes whose probabilities are themselves unknown. For instance, the random outcome of a coin toss is subject to model uncertainty when the probability of the coin showing either a head or a tail is not or is at most partially known. This notion of model ambiguity goes back to Knight (1921) and is therefore commonly referred to as Knightian uncertainty.

In the presence of ambiguity, the probability distribution of a payoff is not anymore determined. Thus, looking for a minimum cost payoff with a given probability distribution is no longer possible. However, investors may still determine a desired distribution function that they would like to achieve “at least”. In this paper, we look for a minimum cost payoff that dominates a target distribution for a chosen stochastic integral order under any plausible real-world probability distribution. Our contributions are three-fold. First, we solve this problem explicitly for a general stochastic ordering under certain assumptions. Solutions to this problem are called “robust cost-efficient.” Second, we draw connections between such a minimum cost payoff and the problem of finding an optimal portfolio under ambiguity for general sets of robust preferences. Third, we present a number of examples, including one on the robust portfolio choice in the presence of volatility uncertainty.

Our results generalize the results on cost-efficiency given in Dybvig (1988a, b), Cox and Leland (2000) and Bernard et al. (2014, 2015). When there is no ambiguity on the real-world probability, the robust cost efficient payoffs coincide with the cost-efficient payoffs studied in the literature. To derive our results, we build on the so-called quantile approach to solve the optimization of a law invariant increasing functional, e.g., Schied (2004), Carlier and Dana (2006, 2008, 2011), Jin and Zhou (2008), He and Zhou (2011a, b), Bernard et al. (2014), Xu (2016) and Rüschendorf and Vanduffel (2020).

Specifically, we consider a static setting but we have incomplete markets and are thus able to address uncertainty about volatility. We show that, under certain conditions, the solution to a general robust portfolio maximization problem is equal to the solution of a classical portfolio maximization problem under a least favorable measure with respect to some stochastic ordering. This was already shown by Schied (2005) for the case of robust expected utility theory and using first order stochastic dominance ordering; here, however, we show that these results extend to the case of more general preferences. Specifically, we focus on the case of first order and second order stochastic dominance.

Furthermore, we show that there is a natural correspondence between optimal portfolios in the maxmin utility setting of Gilboa and Schmeidler (1989), with a concave increasing utility, and robust cost-efficient payoffs: for any robust cost-efficient payoff , there is a utility function such that solves the maxmin expected utility maximization problem. We further show that the solution to a robust maximization problem with respect to a general family of preferences is cost-efficient. This result implies that instead of solving a robust maximization problem with respect to a general family of preferences one could solve an expected utility maximization problem under the single measure for a suitable concave utility function.

The literature on optimal payoff choice under ambiguity includes the seminal setting of Gilboa and Schmeidler (1989) that is, the so-called “maxmin expected utility,” which was later referred to as robust utility functional by Schied et al. (2009). Specifically, these authors characterize preferences that have a robust utility numerical representation for some set of probabilities . Gundel (2005) provides a dual characterization of the solution for robust utility maximization in both a complete and an incomplete market model. Klibanoff et al. (2005) distinguish between subjective beliefs, e.g., the definition of the set of possible or plausible subjective probability measures, and ambiguity attitude, i.e., a characterization of the agent’s behavior toward ambiguity. Based on Klibanoff et al. (2005), Gollier (2011) analyzes the effect of ambiguity aversion on the demand for the uncertain asset in a portfolio choice problem.

Schied (2005) solves the maximization problem of maxmin expected utility of Gilboa and Schmeidler (1989) in a general complete market model with dynamic trading, provided there is a least favorable measure with respect to FSD ordering. Specifically, he finds that the optimum for the maxmin utility setting of Gilboa and Schmeidler (1989) can be derived in the standard expected utility setting under the least favorable measure. Schied (2005) works with a complete market model and mainly in a static setting; dynamics only come into play when the martingale method is applied to the static solutions. A survey on robust preferences and robust portfolio choice can be found in Schied et al. (2009).

The paper is organized as follows. The robust cost-efficiency problem is described in Section 2. In Section 3, we solve the robust cost-efficiency problem, and we include two examples in a log-normal market with uncertainty on the drift and the volatility along with another example in a Lévy market in which the physical measure is obtained by the Esscher transform. In Section 4, we develop the correspondence between robust cost-efficient payoffs and strategies that solve a robust optimal portfolio problem, including the maxmin utility setting of Gilboa and Schmeidler (1989) as a special case. In Section 5, we show that the solution to a general robust optimal portfolio problem can also be obtained as a solution to the maximization of the maxmin utility setting of Gilboa and Schmeidler (1989) for a well-chosen concave utility function. Section 6 concludes.

2 Problem statement

We assume a static market setting in which trading only takes place today and at the end of the planning horizon . There is a bank account earning the continuously compounded risk-free interest rate . Let . Let represent the random value of a risky asset at maturity. We denote by its current value and by the -algebra generates. Let be a set of equivalent real-world probability measures on . The set can be thought of as a collection of probability measures that the investor deems plausible for the market. We define the set of payoffs where is a martingale measure, equivalent to all Furthermore, for any , its price is given by .

Remark 2.1.

Under the assumption that all call options , are traded and under the condition that the function mapping every to the price of is twice differentiable with respect to , Breeden and Litzenberger (1978) show that any can almost surely be replicated using a static portfolio of calls.

Consider an investor with a finite budget and planning horizon who wishes to invest in the market whilst having ambiguous views on the real-world probability measure. How can she find her optimal investment strategy? As in Schied (2005), she could maximize some robust expected utility à la Gilboa and Schmeidler (1989). The basic idea is then to look for a payoff that maximizes the worst case expected utility, reflecting the idea that the investor aims to protect against the worst whilst hoping for the best. However, it seems easier for investors to specify the desired probability distribution of the terminal wealth rather than a utility function (Brennan and Solanki (1981), Sharpe et al. (2000), Goldstein et al. (2008)).

As in Dybvig (1988), Sharpe et al. (2000), Vrecko and Langer (2013), and Bernard et al. (2014), we thus assume in this paper that the investor specifies a desired (cumulative) distribution function of future terminal wealth. Once the investor understands which distribution function is acceptable to her, the natural question arises as to how to find, under ambiguity, the cheapest portfolio with a distribution function at maturity that is “at least as good” as . This is the robust cost-efficiency problem formalized hereafter. In this regard, we need to recall the concept of integral stochastic ordering, see e.g., Denuit et al. (2005). In this paper, we denote by a set of measurable functions from to .

Definition 2.2 (Stochastic integral ordering).

Let and be two distribution functions with support on . The distribution function dominates the distribution function in integral stochastic ordering with respect to the set , in notation , if

such that expectations are finite.

Let denote the set of all non-decreasing functions from to . The corresponding stochastic integral ordering is called first order stochastic dominance (FSD). Furthermore, let denote the set of all non-decreasing and concave functions from to . The corresponding stochastic integral ordering is called second order stochastic dominance (SSD). It is well-known that FSD reflects the common agreement of all investors with law-invariant increasing preferences (Bernard et al., 2015, Theorem 1), whereas SSD order reflects the common agreement of those who have law-invariant increasing and diversification loving preferences (risk averse investors) (Bernard and Sturm, 2023, Corollary 2.6).

Problem 1 (Robust cost-efficiency problem).

The robust cost-efficiency problem for a distribution function is defined as

| (2.1) |

in which denotes a class of admissible payoffs defined as

A solution to (2.1) is called a robust cost-efficient payoff.

As discussed above, the target distribution function of the investor is . That is, we are interested in all payoffs that have a distribution function at maturity that is at least as good as under all plausible scenarios . For example, when , we care about payoffs having distribution functions that dominate in FSD. In order not to “throw away investors’ money”, see Dybvig (1988), we then aim to determine the cheapest payoff among the payoffs in the admissible set . In Theorem 3.1 we provide solutions to the robust cost-efficiency problem (2.1) under regularity conditions on the set and .

Dybvig (1988a, b) introduced the standard cost-efficiency problem without ambiguity on the set of physical measures; that is, when . Specifically, for some fixed , the problem he considered reads as

| (2.2) |

where

We refer to this problem as the standard cost-efficiency problem. Furthermore, we say that a payoff that is distributed with is cost-efficient if solves the standard cost-efficiency problem (2.2) under w.r.t. . By Bernard et al. (2014), a payoff is cost-efficient if and only if is non-increasing in the state price a.s., see also Schied (2004, Proposition 2.5).

The standard cost-efficiency problem (2.2) has been solved in Dybvig (1988a, b) and in Bernard et al. (2014), see also Lemma B.1 in the Appendix. In Corollary 3.5 we show that in the case in which is a singleton, the solution to the robust cost-efficiency problem is unique and coincides with the solution to the standard cost-efficiency problem.

Remark 2.3.

For a fixed , we have that in general cannot be equal to for all . Therefore, we replace the condition in the standard cost-efficiency problem with in the robust setting.

The next example anticipates Sections 3.1.1 and 3.1.2 and is designed to help distinguish between the standard and the robust cost-efficiency problem.

Example 2.4.

(Cost-efficient payoffs). Assume the real-world distribution function of is log-normal. There are three investors: one investor assumes that the drift of under the physical measure, denoted by , is equal to . Another investor assumes that the drift is given by under the physical measure, denoted by . A third investor has ambiguity and assumes that the drift lies in the interval , and thus considers a set as the set of all plausible probability measures on . The cheapest payoffs to obtain a fixed target distribution function are well-known for investor one and two and are given by

respectively; see Proposition 3 in Bernard et al. (2014). Within the set , corresponds to a pessimistic view of the stock price behavior, and we will see in Section 3.1.1 that also solves the robust cost-efficiency problem for if . In the case in which , also solves the robust cost-efficiency problem if additionally is concave; see Section 3.1.2. This example illustrates that the solution to the standard cost-efficiency problem for arbitrarily and the solution to the robust cost-efficiency problem generally do not coincide.

Remark 2.5 (Uncertainty on target distribution ).

As in Rüschendorf and Wolf (2016), we could also consider uncertainty on the target distribution function Specifically, in Rüschendorf and Wolf (2016) it is assumed that the investor specifies finitely many acceptable distribution functions . As all distribution functions are acceptable to the investor, she could solve the robust cost-efficiency problem times and buy the cheapest solution among the solutions. It is also possible to consider a continuum of acceptable distribution functions: generalizing Rüschendorf and Wolf (2016) slightly, we could consider the set

as the set of distribution functions that are acceptable to the investor or client. We could then consider the cost-efficiency problem with uncertainty on the physical measure and the target distribution by

| (2.3) |

However, if is transitive, it holds that , i.e., problem (2.1) without uncertainty on the target distribution and problem (2.3) are equivalent.

2.1 Assumptions

In order to solve the robust cost efficiency problem (2.1), we need some regularity conditions on the set and on the target distribution . In this regard, we define some concepts.

Recall first the concept of a least favorable measure introduced by Schied (2005) for the case For , we define the corresponding likelihood ratio111 The random variable is also called state price because the price of a payoff can be expressed by by .

Definition 2.6 (Least favorable measure with respect to ).

A measure with corresponding likelihood ratio is called a least favorable measure with respect to if for all .

Definition 2.6 generalizes Definition 2.1 of Schied (2005), who assumed the existence of a least favorable measure w.r.t. to determine payoffs that solve the robust expected utility problem of Gilboa-Schmeidler. We also need the following definition.

Definition 2.7 (Composition-consistency of ).

The set is said to be composition-consistent if for also .

Note that the sets and are composition-consistent. This follows from the fact that the composition of non-decreasing (resp. non-decreasing and concave) functions is again non-decreasing (resp. non-decreasing and concave).

The following proposition provides conditions that guarantee the existence of a least favorable measure and turns out to be very useful for applications.

Proposition 2.8 (Sufficient conditions for the existence of a least favorable measure).

Assume that is composition consistent. If for some and all and for some , then is a least favorable measure w.r.t. . If, additionally, is continuously distributed under and is strictly increasing, then is continuously distributed under .

Proof.

Let . Let be a payoff and . Note that if and only if for all such that expectations are finite. Because is composition-consistent, it follows that

| (2.4) |

The expression then follows by Equation (2.4). Let be strictly increasing. By Embrechts and Hofert (2013), the generalized inverse of is continuous on the range of . Thus, it holds that

which implies that is continuously distributed under . ∎

We also need a definition that is, to the best of our knowledge, new to the literature.

Definition 2.9 (Cost-consistency of ).

The set is called cost-consistent if for all and all such that are cost-efficient, implies and, additionally, implies .

As the set is contained in , the following proposition implies that and are cost-consistent. In Example 3.6 we discuss a set that is not cost-consistent.

Proposition 2.10.

is cost-consistent. Moreover, if , then is cost-consistent.

Proof.

The cost-consistency of can be proven along the lines of the proof of Lemma 2 in Bernard et al. (2019). Furthermore, implies , which finishes the proof. ∎

We now list a series of conditions that we often use to derive our main results:

Condition C1.

is square integrable, i.e., , and for .

Condition C2.

The set is composition-consistent and cost-consistent.

Condition C3.

The set contains a least favorable measure with respect to We denote this least favorable measure by

Condition C4.

Denote by the likelihood ratio of the least favorable measure We assume that is continuous and that has finite variance under .

Condition C1 is technical and ensures that the robust cost-efficiency problem is well-posed, i.e., is not empty, see Theorem 3.1.

Condition C3 can also be found in Schied (2005) for the case Note that when becomes larger, the condition C3 becomes stronger. Specifically, requiring a least favorable measure with respect to is more stringent than in the case . In particular, Proposition 2.8 provides sufficient conditions for the existence of a least favorable measure with respect to .

The condition in C4 that is continuous distribution function under is also made in a setting without ambiguity in e.g., Jin and Zhou (2008), He and Zhou (2011a, b), Bernard et al. (2014) and Xu (2016) among many others. It is a strong assumption in the sense that we essentially exclude discrete settings.

3 Solution of the robust cost-efficiency problem

In the next theorem, we make the assumption that . Note that this assumption is always true if . The assumption is also true if , provided that is concave.

Theorem 3.1 (robust cost-efficient payoff).

Proof.

Recall that denotes the likelihood ratio that corresponds to . Let

As is uniformly distributed under (Condition C4), it follows by Lemma B.1 that ; and, by condition C1 it holds that

Condition C4 thus implies that because

Therefore, . By conditions C2 and C3 and as , it follows from Equation (2.4) that for all ; hence, . Let and define

Then is cost-efficient for and we have . By condition C2, is cost-consistent, which implies that . Hence, every admissible payoff is more expensive than . We now show uniqueness. Let be another solution to the robust cost-efficiency problem. It holds that . If and , then , a.s. by Lemma B.1 because the solution corresponds to the solution of the standard cost-efficiency problem for , which has a unique solution. If , then because is cost-consistent. Hence, is the unique solution to the robust cost-efficiency problem. ∎

Remark 3.2.

Instead of requiring that is square integrable, the proof of Theorem 3.1 shows that it is sufficient to assume that has finite price.

Remark 3.3.

Does ambiguity increase costs? Let the assumptions of Theorem 3.1 be in force. Let us compare two investors. Investor A has ambiguity and considers the set as the set of possible real-world measures. Investor B has, e.g., based on a deep market analysis or insider knowledge, no ambiguity and knows that is the true real-world measure. Both investors consider as the target distribution function. Investor A buys according to Theorem 3.1, whereas investor B buys (see Lemma B.1). As , it holds that . As the set is cost-consistent, it follows that . If we additionally have , then it follows that . In the robust setting we end up with a payoff whose distribution , dominates in stochastic ordering for all . That is, under ambiguity, the preferred payoff has a (strictly) higher price and the optimal robust choice typically will not match the choice without uncertainty.

Remark 3.4.

The next corollary shows that the standard and the robust cost-efficiency problem coincide in a setting without uncertainty. Note that we do not require as in Theorem 3.1.

Corollary 3.5.

Proof.

Note that when , then is a least favorable measure. By Lemma B.1, ) is the unique solution to the standard cost-efficiency problem. As in the proof of Theorem 3.1, one can show that . Then follows immediately because . As in the proof of Theorem 3.1, one can show that is the only admissible payoff solving the robust cost-efficiency problem. ∎

The sets and are cost- and composition-consistent. We provide examples of sets of functions that are not cost- or composition-consistent so that Theorem 3.1 cannot be applied to find robust optimal payoffs.

Example 3.6.

Third order stochastic dominance is the stochastic integral ordering that arises from the set , containing all functions such that , and . The set is composition-consistent but is in general not cost-consistent: see Appendix A.

Example 3.7.

Example 3.8.

Rothschild and Stiglitz (1970) introduced concave stochastic order, which is defined via the set of all concave (but not necessarily non-decreasing) functions. Concave stochastic order coincides with SSD if we compare two payoffs with the same mean (Föllmer and Schied, 2011, Remark 2.63). The set of all concave functions is cost-consistent but not composition-consistent.

In the following section we illustrate Theorem 3.1 in a log-normal market setting with uncertainty on the drift and volatility, whereas in Section 3.2 we deal with a more general market setting.

3.1 Robust cost-efficient payoffs in lognormal markets

We assume that under the pricing measure , has a log-normal distribution function with parameters and with stock price today, interest rate , time horizon and volatility . Under , is log-normally distributed with density , where for and we define

| (3.1) |

3.1.1 Drift uncertainty: robust cost-efficient payoff (Schied, 2005)

The real-world distribution function of is assumed to be log-normal with parameters and , but there is uncertainty about the precise level of the drift parameter . In particular, the agent only expects the true drift parameter to lie in the interval for , and thus she considers as the set of all plausible probability measures on . Under , is log-normal with density . It follows that for all , where . Let , . A straightforward computation shows that

| (3.2) |

As and is a strictly increasing function of . Furthermore, has finite variance. By Proposition 2.8, is a least favorable measure with corresponding likelihood ratio , i.e., conditions C3 and C4 are satisfied. Theorem 3.1 shows that the robust cost-efficient payoff for a distribution function satisfying condition C1 is given by

The second equality follows from the increasingness of in . The agent thus chooses the optimal payoff as if she believes that the worst-case plausible value for the drift parameter , i.e., , will materialize. This finding is consistent with the results obtained by Schied (2005, Section 3.1) on the impact of drift uncertainty on optimal payoff choice in a Black-Scholes setting.

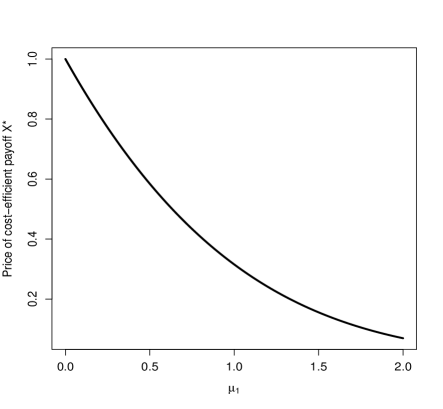

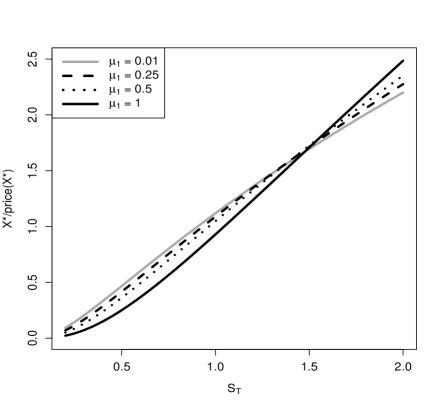

Example 3.9.

We consider next the exponential distribution for the distribution function , i.e., , , which satisfies condition C1. Panel A of Figure 1 displays the price of the robust cost-efficient payoff for varying levels of the parameter , which describes the ambiguity that the agent faces (consistently with Remark 3.3). The higher , the smaller the set , i.e., the lower the degree of ambiguity, and the cheaper . In panel B of Figure 1 we display, for several values of , the robust cost-efficient payoff normalized for its initial price as a function of realizations of ; i.e., we display the curve

where . We observe that the curve is flatter when is smaller, i.e., more ambiguity gives rise to payoffs that reflect a higher degree of conservatism.

|

|

| Panel A | Panel B |

3.1.2 Drift and volatility uncertainty: robust cost-efficient payoff

The real-world distribution function of is assumed to be log-normal with parameters and , but now the agent faces uncertainty about the precise level of the parameters and . In particular, the agent only expects the true parameters to lie within the cube

for and , and thus she considers as the set of all plausible probability measures on . Under , is log-normal with density , defined in Equation (3.1). In this regard, note that while is a natural assumption, there is some empirical evidence for the hypothesis that ; see Table 1 in Christensen and Prabhala (1998) and Table 1 in Christensen and Hansen (2002).

Remark 3.10.

In contrast to the dynamic Black-Scholes model, in which the stock price is also log-normally distributed, we work in a static market setting. In a dynamic Black-Scholes framework where continuous trading is allowed at zero transaction cost, the absence of arbitrage opportunities implies that the volatility of the stock does not change when moving from the real-world measure to the risk-neutral measure, i.e., there does not exist uncertainty about the volatility in a dynamic Black-Scholes model. Here, however, we do not assume dynamic trading. Hence, even when call option prices reflect a risk neutral distribution function for that is log-normally distributed, the agent may have a view on the real-world distribution that is different from a log-normal and, in particular, may be unsure about the exact values for drift and volatility.

In the next proposition, we assume that

| (3.3) |

For example, and or and imply Equation (3.3), that is: there are economically reasonable environments such that Equation (3.3) holds.

Proposition 3.11 (robust cost-efficient payoff).

Proof.

For a log-normal distribution function with parameters and , it holds that

where denotes the distribution function of a standard normal random variable. It follows that

Hence, , . As in Section 3.1.1, let

Hence, the likelihood ratio is strictly increasing and concave in if (3.3) is satisfied. By Proposition 2.8, conditions C3 and C4 are satisfied for the set with least favorable measure with likelihood ratio As in Section 3.1.1, some simple calculations and Theorem 3.1 show that the robust cost-efficient payoff for the distribution function is given by (3.4). ∎

We provide an example for that make it possible to apply Proposition 3.11 to determine robust cost-efficient payoffs. In this regard, observe that in Proposition 3.11 is the log-normal distribution with parameters and for .

Example 3.12.

If is the log-normal distribution with parameters and , then in Proposition 3.11 is concave if because

3.2 Robust cost-efficient payoffs in general markets using Esscher transform

Inspired by Corcuera et al. (2009), let and and be a payoff with mean zero and variance one. Under , assume that has density , and model the future stock price at date by

where is a mean correcting term, i.e., is chosen such that

The density of under is

The corresponding density of under is denoted by , and it holds that

Let and be a set containing such that exists for all . Define a family of probability measures as follows: is a measure such that has density under , where is obtained from by applying the Esscher transform. The use of the Esscher transform can be supported by a utility maximizing argument; see Gerber and Shiu (1996). In particular, we define such that

It follows that

The density crosses only once from above for ; hence, by Denuit et al. (2005, Property 3.3.32), it follows that

For the likelihood ratio it, holds that

which is strictly increasing in as and concave if . We can apply Proposition 2.8 to show that conditions C3 and C4 are satisfied for the sets and with least favorable measure and corresponding likelihood ratio We can use Theorem 3.1 to compute the cost-efficient payoff of a distribution function .

4 Robust portfolio selection

Gilboa and Schmeidler (1989) provide axioms that justify a maxmin expected utility framework to make robust decisions when there is ambiguity on the probability measure , i.e., when In this framework, Schied (2005) shows that when a least favorable measure with respect to FSD ordering (e.g., the stochastic integral ordering induced by the set as defined in Section 3) exists, an optimal portfolio can be derived. In this section, we extend the work of Schied (2005) in two different ways. First, we account for preferences beyond expected utility. Specifically, we derive optimal portfolios for robust preferences that are in accord with expected utility theory, rank dependent utility theory and Yaari’s dual theory. Second, assuming the existence of a least favorable measure with respect to a general stochastic integral ordering induced by some set , not necessarily identical to , we derive the optimal portfolio. Specifically, we derive optimal portfolios when a least favorable measure with respect to SSD ordering exists (see Proposition 2.8 for a sufficient condition) and the target distribution is sufficiently light tailed (see Remark 3.4).

4.1 Family consistent preferences

A preference is defined as a functional from the set of payoffs to the real line (He et al. (2017), Assa and Zimper (2018)). Under preference , the payoff is preferred to if . In general, may depend on the different measures in a complicated way. In what follows, we denote a preference that depends solely on some by .

Definition 4.1.

Let be a family of preferences. The preference , is called law invariant if implies that . The family is called law invariant if each individual preference is law invariant.

Example 4.2.

A standard example of a law invariant preference is for some increasing utility function . In this case, amounts to the worst-case expected utility, commonly called robust expected utility, which was introduced in Gilboa and Schmeidler (1989). It is also referred to a robust utility functional in Schied et al. (2009).

To the best of our knowledge, the next definition is new to the literature. It will be helpful in solving robust portfolio choice problems.

Definition 4.3.

Let be a family of preferences. Let . The family of preferences is called family consistent on with respect to if for all the inequality

implies that

family consistency of with respect to some has the following interpretation: if a measure yields the most pessimistic view of any payoff w.r.t. the stochastic ordering induced by some set , then the preference under that measure is the lowest as well.

Next, we discuss some examples. Let be a set of payoffs and let be the set of cumulative distribution functions induced by , i.e.,

Let us consider an agent taking into account a family of law invariant preferences i.e.,

| (4.1) |

for some well defined . If respects integral stochastic ordering, i.e.,

| (4.2) |

then is family consistent on with respect to . We provide some specific examples in the contexts of expected utility theory, Yaari’s dual theory of choice and rank-dependent expected utility theory:

Example 4.4.

Let . Let with and . For a given distribution function , define

where we tacitly assume that all integrals exist. It is straightforward to show that when and are non-decreasing, it holds that the family of preferences induced by , or as in (4.1) is family consistent on where is restricted to contain random variables such that all relevant integrals exist. Furthermore, if is strictly increasing and concave and is strictly increasing, continuously differentiable and convex, we obtain that such a family is a family consistent on ; see Yaari (1987), Wang and Young (1998), He et al. (2017) and Ryan (2006).

4.2 Optimal portfolio for robust preferences

Problem 2.

Let be the initial wealth. Let be a family of preferences. We consider the robust maximization problem

| (4.3) |

where and

| (4.4) |

It turns out that under certain conditions a solution to the robust optimization problem (4.3) can be found as a solution to a maximization problem under a single measure .

Problem 3.

Let be the initial wealth. Let , be a preference. We consider the maximization problem

| (4.5) |

Under the assumption of the existence of a least favorable measure with respect to FSD ordering, Schied (2005) showed that in order to solve the robust maximization problem (4.3) for preferences , , it actually suffices to solve the single measure maximization problem (4.5). The following theorem generalizes this result beyond the expected utility setting to a general law invariant family of preferences . The theorem is illustrated in Section 4.3, where we consider a robust rank-dependent expected utility maximization problem for an investor with ambiguity on the trend and/or volatility of the risky asset.

Theorem 4.6.

Proof.

Let such that . Then, it holds by the family consistency, condition C3 and (2.4) that

| (4.6) |

Let

Then solves the standard cost-efficiency problem for and thus and ; hence, by the law invariance of , it holds that . It further holds that is a non-decreasing function of . It follows by (4.6) that

where the last inequality follows by . ∎

From Theorem 4.6, it follows immediately that solving robust preference maximization problems may reduce to solving an optimization problem under a single probability measure. The following example illustrates this consequence.

Example 4.7.

The main assumption in Theorem 4.6 that is needed to solve the robust maximization problem (4.3) in the case of a family of law invariant preferences is the existence of a least favorable measure with respect to . In the following theorem we show that it is possible to weaken this assumption in that we only require existence of a least favorable measure with respect to some , e.g., . The theorem is illustrated in Section 4.3, where we consider a robust rank-dependent expected utility maximization problem for an investor who faces ambiguity on expected return and volatility of the risky asset.

Theorem 4.8.

Proof.

Note that, as compared to the statements in Theorem 4.6, in Theorem 4.8 the do not need to be law-invariant. Moreover, as long as the solution can be expressed as a certain function of the likelihood ratio , the preferences do not need to be increasing, i.e., does not need to imply As pointed out, Theorem 4.8 is applicable, in particular, for the case . However, the requirement that can be a.s. expressed as for some is equivalent to being increasing and concave. This property is difficult to verify ex-ante. Hereafter, we show that in the case in which is an expected utility, this condition translates into an easy-to-verify condition on the utility function. We formulate the following theorem.

Theorem 4.9.

Let with likelihood ratio . Let be a differentiable, concave and strictly increasing utility function such that is strictly decreasing. If the maximization problem (4.5) under has a solution, then the solution is a non-decreasing and concave function of if and only if is convex. If is three times differentiable, is convex if and only if

| (4.7) |

in which refers to the absolute risk aversion measure and to the absolute prudence.

Proof.

By Lemma 2 in Bernard et al. (2015), the solution to (4.5) is unique and given by for some . See also Merton (1971) for a proof in a context in which Inada’s conditions are satisfied. Note that and that is strictly increasing. Observe that the inverse of is , which is hence also strictly increasing. The inverse of a convex (concave) and strictly increasing function is concave (convex). For the second assertion, observe that and that a function is convex on an open interval if and only if its second derivative is non-negative. Then (4.7) follows immediately. ∎

Remark 4.10.

Maggi et al. (2006) have shown that if and only if the utility has increasing absolute risk aversion, which is somewhat unusual (it is typically assumed that agents have decreasing absolute risk aversion given that they become less risk averse as their wealth increases). Here, our condition (4.7) is not incompatible with decreasing absolute risk aversion due to the factor .

Condition (4.7) has appeared several times in the literature. It has been found to play a role in the context of insurance models in Bourlès (2017), but it also appeared as a condition in the opening of a new asset market (Gollier and Kimball (1996)), when there is uncertainty on the size (Gollier et al. (2000)) or the probability of losses (Gollier (2002)) and under contingent auditing (Sinclair-Desgagné and Gabel (1997)). Further interpretation of this condition and, in particular, of the degree of concavity of the inverse of the marginal utility can be found in Bourlès (2017). This condition also appears in Varian (1985) in the context of portfolio selection under ambiguity.

Example 4.11.

As an illustration of Theorem 4.9, we provide two utility functions, which are differentiable, concave and strictly increasing functions such that one over the marginal utility is convex.

-

•

The exponential utility for risk-averse agents: for . It holds that , which is strictly increasing and convex.

-

•

CRRA utility: for . It holds that , which is strictly increasing and convex.

4.3 Rank-dependent utility in log-normal markets

We now discuss some examples to illustrate Section 4.2 in a log-normal market setting with uncertainty on the drift and volatility. In particular, we explicitly solve a robust rank-dependent expected utility problem using Theorems 4.6 and 4.8. As in Section 3.1.2, we assume that the real-world distribution of is log-normal with parameters and and that the investor has uncertainty on the trend and potentially also the volatility. She may expect the true parameters to lie within the cube

for and . The investor thus considers as the set of all plausible probability measures on . Note that if the investor only faces drift ambiguity; otherwise, she considers ambiguity on both trend and volatility. Under , is log-normal with density , defined in Equation (3.1). In the next example, is the standard normal distribution function.

Example 4.12.

Let , for be the CRRA utility function. Let and let , denote the so-called Wang transform, which is increasing concave if and increasing convex if . Consider the following portfolio choice problem; in which the investor maximizes her expected rank-dependent utility:

| (4.8) |

where is the initial wealth and . Let . The solution to (4.8) is given by

| (4.9) |

where depends on , and , see Equations (4.11), (4.12) and (4.13). The solution to the robust rank-dependent utility problem

| (4.10) |

is given by if there is no ambiguity on the volatility, i.e., when . If there is ambiguity on the volatility, and , then still solves (4.10).

Proof.

We first prove that solves (4.8). Let . The state price is log-normally distributed with parameters and , see Equation (3.2). Hence, as , it holds that

and

Let

The solution to the classical rank-utility problem (4.8) is well-known (see for instance Theorem 4.1 in Xu (2016) or Section 3.2 in Rüschendorf and Vanduffel (2020)), and is given by

where is determined by and is the concave envelope of . Using , after some calculations, we obtain that

We distinguish two cases to find a more explicit expression for . Case 1: . Then, is non-increasing and hence is concave and equal to . As , it is easy to see that

If , then is constant and it holds that

| (4.11) |

Otherwise, is log-normally distributed and it follows that

| (4.12) |

Case 2: Assume . Then, is convex. Note that and . As is convex, the concave envelope of is given by . Then and

Therefore, , and hence

| (4.13) |

Assume that there is no ambiguity on the volatility, i.e., . Section 3.1.1 shows that the least favorable measure with respect to is given by with corresponding likelihood ratio . By Example 4.4, the preference in (4.10) is family consistent and Theorem 4.6 shows that solves the robust rank-dependent utility problem (4.10). Lastly, assume that there is ambiguity on the volatility. If , Proposition 3.11 shows that the least favorable measure with respect to is also . If , is a concave and non-decreasing function of . By Example 4.4, the preference in (4.10) is family consistent. Apply Theorem 4.8 to show that also in this case, solves the robust rank-dependent utility problem (4.10). ∎

To better understand the solution in Example 4.12, we “rationalize” the solution as in Bernard et al. (2015), i.e., we show that the optimal investment strategy in the robust rank-dependent setting also solves an expected utility maximization problem. Example 4.13 shows that the solution to the expected rank-dependent utility problems (4.8) and (4.10) involving a Wang transform with parameter and a CRRA utility function with parameter can be rationalized by a CRRA utility with parameter .

Example 4.13.

Let , , , and as in Example 4.12, such that and . solves the following expected utility maximization problem:

for the utility function

| (4.14) |

The function is non-decreasing and concave.

Proof.

Note that implies . Let . Let . As in Bernard et al. (2015), let and define

is log-normally distributed. It follows that

where is a suitable constant. Thus,

In summary, as is only determined up to positive affine transformations, solves the expected utility maximization problem for the utility given in (4.14): see Theorem 2 in Bernard et al. (2015). ∎

5 Rationalizing robust cost-efficient payoffs

When there is no ambiguity on the probability measure , there is a close relationship between cost-efficiency and portfolio optimization: for any cost-efficient payoff , there exists a utility function (unique up to a linear transformation) such that also solves the expected utility maximization problem (Bernard et al. (2015)). In this section, we show that this result can be generalized to the robust setting developed previously in that robust cost-efficient payoffs can be rationalized in terms of the maxmin utility framework introduced in Gilboa and Schmeidler (1989). Specifically, we show under the same assumptions as in Theorems 4.6 and 4.8 that payoffs maximize a robust utility functional as in Gilboa and Schmeidler (1989) if and only if they are robust cost-efficient.

In the following theorem we distinguish two cases: a) we deal with law-invariant preferences and FSD ordering and assume that the various (robust) maximization problems have unique solutions. Or, b) we deal with general preferences and stochastic ordering and we do not require uniqueness of the solutions but assume that the solution of the various maximization problems can be written as for some .

Theorem 5.1.

- i)

-

is cost-efficient under .

- ii)

-

It holds that , a.s.

- iii)

-

is a.s. non-decreasing in .

- iv)

-

solves the robust cost-efficiency problem for .

- v)

-

solves the expected utility maximization problem under for the utility function

- vi)

-

solves the robust expected utility problem for the utility function

and the solution is unique if condition (a) is satisfied.

- vii)

-

There is a family of preferences that is family consistent on with respect to such that and is the solution to the maximization problem under

and the solution is unique and the family of preferences is law invariant if condition (a) is satisfied.

- viii)

-

There is a family of preferences that is family consistent on with respect to such that is the solution to the robust maximization problem

and the solution is unique and the family of preferences is law invariant if condition (a) is satisfied.

Proof.

The equivalence between i), ii) and iii) follows from Lemma B.1. The equivalence between iv) and ii) follows from Theorem 3.1 and Remark 3.2. Note that is always true. By Theorem 3 in Bernard et al. (2015), i) implies v). By Lemma B.3 and Lemma 3 in Bernard et al. (2015), v) implies i). By Example 4.4, v) implies vii) trivially, define for all . v) implies vi), if (a) holds, by Theorem 4.6 and Example 4.4 as for all by assumption. v) implies vi), if (b) holds, by Theorem 4.8. vi) implies viii) trivially. By Lemma B.3 and Lemma B.4, if (a) holds, vi)i) and vii)i) and viii)i). Note that, if (b) holds, iii) is always true because is non-decreasing. ∎

Remark 5.2.

Assuming that all functions in are non-decreasing, i.e., that , is not really a restriction. Otherwise, there are two sure payoffs , i.e., are constant, such that but the distribution of does not dominate the distribution function of in integral stochastic ordering.

Example 5.3.

Assume . Consider the robust rank-dependent expected utility maximization problem in Example 4.12 with solution defined in (4.9). Let and . With the help of the explicit expressions of and from the proofs of Examples 4.12 and 4.13, it is easy to see that (b) in Theorem 5.1 holds if .

Let us start from viii) in Theorem 5.1. Equation (4.9) implies that the optimal solution is a non-decreasing function of . Hence, iii) in Theorem 5.1 is satisfied. As shown by Example 4.13, also solves an expected utility maximization problem for the utility in (4.14), which illustrates v) in Theorem 5.1. One can easily verify that ii) in Theorem 5.1 is respected by . Hence, Theorem 3.1 implies that solves the robust cost-efficiency problem as stated in iv) in Theorem 5.1.

The preferences in Theorem 5.1 for case (b) do not need to be law-invariant or increasing, i.e., does not need to imply . We provide a simple example of such a preference.

Example 5.4.

Define for some . Let . For , define

which is trivially family consistent. An agent with such a preference only likes and neglects everything else. She is not law-invariant and does not prefer more to less. Someone interested only in the market portfolio or in the risk-free bond might have such a preference. The solution to the robust maximization problem ix) is , which is cost-efficient because is non-decreasing in . A utility function for v) can be constructed as in (5.1).

6 Final Remarks

In this paper we assume that the agent has Knightian uncertainty. She is unsure about the precise physical measure describing the financial market and knows only that the true physical measure lies within a set of probability measures. Given this ambiguity, it is no longer possible to target a payoff with a given probability distribution function. In particular, the close relation between payoffs that are the cheapest possible in reaching a target distribution function and the optimality thereof under law-invariant increasing preferences (Dybvig (1988a, b), Sharpe et al. (2000), Goldstein et al. (2008), Bernard et al. (2015)) is a priori lost, as there is no consensus regarding what probability distribution to adopt. For this reason, we introduce the notion of a robust cost-efficient payoff.

For a given distribution function , the robust cost-efficiency problem aims at finding the cheapest payoff whose distribution function dominates under all possible physical measures in some integral stochastic ordering. We solve this problem under some conditions (namely, where there exists a least favorable measure and the integral stochastic ordering is cost-consistent). The solution is identical to the solution to the cost-efficiency problem without model ambiguity under the physical measure and given in closed-form. We are thus able to reduce the problem formulated in a robust setting to a problem formulated in a standard setting without model ambiguity.

Finally, we show that this notion of robust cost-efficiency plays a key role in optimal robust portfolio selection and that a very general class of robust portfolio selection problems (possibly in a non-expected utility setting) can be reduced to the maxmin expected utility setting of Gilboa and Schmeidler (1989) for a well-chosen concave utility function.

For this to hold, we make a relatively minor assumption on the family of preferences, i.e., that it is family consistent: if the measure is the most pessimistic view of a payoff , then the preference under that measure is the lowest as well. To the best of our knowledge, family consistency is new to the literature, and we provide several examples in the context of expected utility theory, Yaari’s dual theory and rank-dependent utility theory.

We assume a static setting in which intermediate trading is not possible. Whilst allowing for dynamic rebalancing may make it possible to achieve higher levels for the objective at hand (e.g., robust expected utility), this possibility is only clear when there are no transaction costs, which is not realistic. In practice, transaction costs usually contain a fixed part, and hence dynamic trading can only occur a finite number of times since otherwise bankruptcy occurs. The study of optimal investments in the presence of fixed costs is not yet very well understood. Recently, Belak et al. (2022) and Bayraktar et al. (2022) provide optimal strategies in a Black-Scholes market without ambiguity and assuming expected utility. By contrast our static setting makes it possible to deal with ambiguity and to address fairly general objectives.

Appendix

Appendix A Proof for Example 3.6

Lemma A.1.

Let and be two cdfs. It holds that if and only if

Proof.

See Theorem 2.2 of Gotoh and Konno (2000). ∎

We are now ready to construct the counterexample stated in Example 3.6.

Proof.

Apply the chain rule to show that is composition-consistent.

Next, we construct two distribution functions such that one dominates

the other in TSD but is cheaper.

Step 1: define some market setting as in Section 3.1.1:

let , , and . Then, .

Choose such that it holds that ,

i.e., . Under

the stock is log-normally distributed with parameters

and . Under , the stock is also log-normally

distributed with parameters

and . is a least favorable measure

with respect to the set , and so hence also is

because .

Step 2: define two distribution functions: Let

and, for , let

is the uniform distribution function and jumps at zero and at one. It follows that and that

Step 3: show that dominates in TSD: It holds for that

and that

Hence, if or, equivalently,

, it follows that .

Step 4: compute the lowest cost of both distribution functions:

The cost-efficient payoff for is

The lowest price of can be computed numerically:

The cost-efficient payoff for is

Its price is

Under , is uniform distributed and is a digital option. If , the lowest price for is , which is greater than the lowest price to be paid for . But in this case : hence, TSD is not cost-consistent. ∎

Appendix B Auxiliary results

Lemma B.1.

Fix . Let be the Radon–Nikodym derivative of with respect to . Assume that under is continuously distributed and that has finite variance. There is a a.s. unique optimizer to the standard cost-efficiency problem under the probability measure given by

is left-continuous and non-decreasing a.s.

Proof.

Let . Then, This claim follows both from Dybvig (1988a, b) and from Corollary 2 in Bernard et al. (2014). See also Schied (2004, Proposition 2.7) for the importance of the continuity assumption of in obtaining the uniqueness.

∎

Lemma B.2.

Fix . Let . Assume that is continuously distributed under . A payoff is cost-efficient if and only if it is non-decreasing in , almost surely.

Proof.

See Bernard et al. (2014, Corollary 2 and Proposition 2). ∎

In the following two lemmas we show that the solution of the single or robust maximization problem is cost-efficient if it is unique.

Lemma B.3.

Let with corresponding likelihood ratio . Assume that is continuously distributed and that is law invariant and is a a.s. unique solution to the maximization problem (4.5) under . Then, is cost-efficient.

Proof.

Let

Then solves the standard cost-efficiency problem for and thus and ; hence, by the law invariance of , it holds that . It follows by law invariance that

As is the unique solution, it must hold that , a.s., and thus is cost-efficient. ∎

Lemma B.4.

Proof.

References

- Assa and Zimper (2018) Hirbod Assa and Alexander Zimper. Preferences over all random variables: Incompatibility of convexity and continuity. Journal of Mathematical Economics, 75:71–83, 2018.

- Bayraktar et al. (2022) Erhan Bayraktar, Christoph Belak, Sören Christensen, and Frank Seifried. Convergence of optimal investment problems in the vanishing fixed cost limit. SIAM Journal on Control and Optimization, 60(5):2712–2736, 2022.

- Belak et al. (2022) Christoph Belak, Lukas Mich, and Frank T Seifried. Optimal investment for retail investors. Mathematical Finance, 32(2):555–594, 2022.

- Bernard and Sturm (2023) Carole Bernard and Stephan Sturm. Cost-efficiency in incomplete markets. Working Paper available on Arxiv, 2023.

- Bernard et al. (2014) Carole Bernard, Phelim Boyle, and Steven Vanduffel. Explicit representation of cost-efficient strategies. Finance, 35:5–55, 2014.

- Bernard et al. (2015) Carole Bernard, Jit Seng Chen, and Steven Vanduffel. Rationalizing investors’ choices. Journal of Mathematical Economics, 59:10–23, 2015.

- Bernard et al. (2019) Carole Bernard, Steven Vanduffel, and Jiang Ye. Optimal strategies under Omega ratio. European Journal of Operational Research, 275(2):755–767, 2019.

- Bourlès (2017) Renaud Bourlès. Prevention incentives in long-term insurance contracts. Journal of Economics & Management Strategy, 26(3):661–674, 2017.

- Breeden and Litzenberger (1978) Douglas T. Breeden and Robert H. Litzenberger. Prices of state-contingent claims implicit in option prices. Journal of Business, 1(51):621–651, 1978.

- Brennan and Solanki (1981) Michael J Brennan and Ray Solanki. Optimal portfolio insurance. Journal of financial and quantitative analysis, 16(3):279–300, 1981.

- Carlier and Dana (2008) Guillaume Carlier and R-A Dana. Two-persons efficient risk-sharing and equilibria for concave law-invariant utilities. Economic Theory, 36(2):189–223, 2008.

- Carlier and Dana (2011) Guillaume Carlier and R-A Dana. Optimal demand for contingent claims when agents have law invariant utilities. Mathematical Finance: An International Journal of Mathematics, Statistics and Financial Economics, 21(2):169–201, 2011.

- Carlier and Dana (2006) Guillaume Carlier and Rose-Anne Dana. Law invariant concave utility functions and optimization problems with monotonicity and comonotonicity constraints. Statistics & Risk Modeling, 24(1):127–152, 2006.

- Christensen and Prabhala (1998) Bent J Christensen and Nagpurnanand R Prabhala. The relation between implied and realized volatility. Journal of Financial Economics, 50(2):125–150, 1998.

- Christensen and Hansen (2002) Bent Jesper Christensen and Charlotte Strunk Hansen. New evidence on the implied-realized volatility relation. European Journal of Finance, 8(2):187–205, 2002.

- Corcuera et al. (2009) José Manuel Corcuera, Florence Guillaume, Peter Leoni, and Wim Schoutens. Implied Lévy volatility. Quantitative Finance, 9(4):383–393, 2009.

- Cox and Leland (2000) John C Cox and Hayne E Leland. On dynamic investment strategies. Journal of Economic Dynamics and Control, 24(11):1859–1880, 2000.

- Denuit et al. (2005) Michel Denuit, Jan Dhaene, Marc Goovaerts, and Rob Kaas. Actuarial Theory for Dependent Risks. John Wiley & Sons, 2005.

- Dybvig (1988a) P. Dybvig. Distributional analysis of portfolio choice. Journal of Business, 61(3):369–393, 1988a.

- Dybvig (1988b) P. Dybvig. Inefficient dynamic portfolio strategies or how to throw away a million dollars in the stock market. Review of Financial Studies, 1(1):67–88, 1988b.

- Dybvig (1988) Philip H Dybvig. Inefficient dynamic portfolio strategies or how to throw away a million dollars in the stock market. Review of Financial Studies, 1(1):67–88, 1988.

- Embrechts and Hofert (2013) Paul Embrechts and Marius Hofert. A note on generalized inverses. Mathematical Methods of Operations Research, 77(3):423–432, 2013.

- Föllmer and Schied (2011) Hans Föllmer and Alexander Schied. Stochastic finance: an introduction in discrete time. Walter de Gruyter, 2011.

- Gerber and Shiu (1996) Hans U Gerber and Elias SW Shiu. Actuarial bridges to dynamic hedging and option pricing. Insurance: Mathematics and Economics, 18(3):183–218, 1996.

- Gilboa and Schmeidler (1989) Itzhak Gilboa and David Schmeidler. Maxmin expected utility with non-unique prior. Journal of Mathematical Economics, 18(2):141–153, 1989.

- Goldstein et al. (2008) Daniel G Goldstein, Eric J Johnson, and William F Sharpe. Choosing outcomes versus choosing products: Consumer-focused retirement investment advice. Journal of Consumer Research, 35(3):440–456, 2008.

- Gollier (2002) Christian Gollier. Optimal prevention of unknown risks: A dynamic approach with learning. Open Access publications from University of Toulouse 1 Capitole, 2002.

- Gollier (2011) Christian Gollier. Portfolio choices and asset prices: The comparative statics of ambiguity aversion. Review of Economic Studies, 78(4):1329–1344, 2011.

- Gollier and Kimball (1996) Christian Gollier and Miles S Kimball. Toward a systematic approach to the economic effects of uncertainty: characterizing utility functions. Technical report, Discussion paper, University of Michigan, 1996.

- Gollier et al. (2000) Christian Gollier, Bruno Jullien, and Nicolas Treich. Scientific progress and irreversibility: an economic interpretation of the ’precautionary principle’. Journal of Public Economics, 75(2):229–253, 2000.

- Gotoh and Konno (2000) Jun-ya Gotoh and Hiroshi Konno. Third degree stochastic dominance and mean-risk analysis. Management Science, 46(2):289–301, 2000.

- Gundel (2005) Anne Gundel. Robust utility maximization for complete and incomplete market models. Finance and Stochastics, 9(2):151–176, 2005.

- He and Zhou (2011a) Xue Dong He and Xun Yu Zhou. Portfolio choice under cumulative prospect theory: An analytical treatment. Management Science, 57(2):315–331, 2011a.

- He and Zhou (2011b) Xue Dong He and Xun Yu Zhou. Portfolio choice via quantiles. Mathematical Finance: An International Journal of Mathematics, Statistics and Financial Economics, 21(2):203–231, 2011b.

- He et al. (2017) Xue Dong He, Roy Kouwenberg, and Xun Yu Zhou. Rank-dependent utility and risk taking in complete markets. SIAM Journal on Financial Mathematics, 8(1):214–239, 2017.

- Jin and Zhou (2008) Hanqing Jin and Xun Yu Zhou. Behavioral portfolio selection in continous time. Math. Finance, 18(3):385–426, 2008.

- Klibanoff et al. (2005) Peter Klibanoff, Massimo Marinacci, and Sujoy Mukerji. A smooth model of decision making under ambiguity. Econometrica, 73(6):1849–1892, 2005.

- Knight (1921) Frank Hyneman Knight. Risk, uncertainty and profit, volume 31. Houghton Mifflin, 1921.

- Maggi et al. (2006) Mario A Maggi, Umberto Magnani, and Mario Menegatti. On the relationship between absolute prudence and absolute risk aversion. Decisions in Economics and Finance, 29(2):155–160, 2006.

- Merton (1971) Robert C Merton. Optimal consumption and portfolio rules in a continuous-time model. Journal of Economic Theory, 3:373–413, 1971.

- Monin (2014) Phillip Monin. On a dynamic adaptation of the distribution builder approach to investment decisions. Quantitative Finance, 14(5):749–760, 2014.

- Müller et al. (2017) Alfred Müller, Marco Scarsini, Ilia Tsetlin, and Robert L Winkler. Between first-and second-order stochastic dominance. Management Science, 63(9):2933–2947, 2017.

- Rothschild and Stiglitz (1970) Michael Rothschild and Joseph E Stiglitz. Increasing risk: I. a definition. Journal of Economic theory, 2(3):225–243, 1970.

- Rüschendorf and Vanduffel (2020) Ludger Rüschendorf and Steven Vanduffel. On the construction of optimal payoffs. Decisions in Economics and Finance, 43(1):129–153, 2020.

- Rüschendorf and Wolf (2016) Ludger Rüschendorf and Viktor Wolf. On the method of optimal portfolio choice by cost-efficiency. Applied Mathematical Finance, 23(2):158–173, 2016.

- Ryan (2006) Matthew J Ryan. Risk aversion in rdeu. Journal of Mathematical Economics, 42(6):675–697, 2006.

- Schied (2004) Alexander Schied. On the neyman–pearson problem for law-invariant risk measures and robust utility functionals. The Annals of Applied Probability, 14(3):1398–1423, 2004.

- Schied (2005) Alexander Schied. Optimal investments for robust utility functionals in complete market models. Mathematics of Operations Research, 30(3):750–764, 2005.

- Schied et al. (2009) Alexander Schied, Hans Föllmer, and Stefan Weber. Robust preferences and robust portfolio choice. Handbook of Numerical Analysis, 15:29–87, 2009.

- Shaked and Shanthikumar (2007) Moshe Shaked and J George Shanthikumar. Stochastic orders. Springer Science & Business Media, 2007.

- Sharpe (2011) William F Sharpe. Investors and markets. In Investors and Markets. Princeton university press, 2011.

- Sharpe et al. (2000) William F Sharpe, Daniel G Goldstein, and Phil W Blythe. The distribution builder: A tool for inferring investor preferences. preprint, 2000.

- Sinclair-Desgagné and Gabel (1997) Bernard Sinclair-Desgagné and H Landis Gabel. Environmental auditing in management systems and public policy. Journal of Environmental Economics and Management, 33(3):331–346, 1997.

- Varian (1985) Hal R Varian. Divergence of opinion in complete markets: A note. Journal of Finance, 40(1):309–317, 1985.

- Vrecko and Langer (2013) Dennis Vrecko and Thomas Langer. What are investors willing to pay to customize their investment product? Management Science, 59(8):1855–1870, 2013.

- Wang and Young (1998) Shaun S Wang and Virginia R Young. Ordering risks: Expected utility theory versus yaari’s dual theory of risk. Insurance: Mathematics and Economics, 22(2):145–161, 1998.

- Xu (2016) Zuo Quan Xu. A note on the quantile formulation. Mathematical Finance, 26(3):589–601, 2016.

- Yaari (1987) Menahem E Yaari. The dual theory of choice under risk. Econometrica: Journal of the Econometric Society, pages 95–115, 1987.