A multi-task network approach for calculating discrimination-free insurance prices

Abstract.

In applications of predictive modeling, such as insurance pricing, indirect or proxy discrimination is an issue of major concern. Namely, there exists the possibility that protected policyholder characteristics are implicitly inferred from non-protected ones by predictive models, and are thus having an undesirable (or illegal) impact on prices. A technical solution to this problem relies on building a best-estimate model using all policyholder characteristics (including protected ones) and then averaging out the protected characteristics for calculating individual prices. However, such approaches require full knowledge of policyholders’ protected characteristics, which may in itself be problematic. Here, we address this issue by using a multi-task neural network architecture for claim predictions, which can be trained using only partial information on protected characteristics, and it produces prices that are free from proxy discrimination. We demonstrate the use of the proposed model and we find that its predictive accuracy is comparable to a conventional feed-forward neural network (on full information). However, this multi-task network has clearly superior performance in the case of partially missing policyholder information.

Keywords: Indirect discrimination, proxy discrimination, discrimination-free insurance pricing, unawareness price, best-estimate price, protected information, discriminatory covariates, fairness, incomplete information, multi-task learning, multi-output network.

1. Introduction

The question of avoiding discrimination in insurance pricing is becoming increasingly important in many markets and jurisdictions. For example, the European Council [5] prohibits using gender information as a rating factor for insurance pricing; for an actuarial overview on discrimination regulation we refer to Frees–Huang [6]. While regulation varies across jurisdictions, it is typically required that both direct and indirect discrimination be avoided. If denotes protected information whose use is regarded as discriminatory, direct discrimination is avoided by merely not including in the regression model used for insurance pricing. However, not including protected information in the regression model is not necessarily sufficient for avoiding discrimination more broadly, because the protected information may also be (implicitly) inferred from the non-protected variables, denoted by . We call the impact of such inference on prices indirect discrimination. We note that this is a narrow use of the latter term, equivalent to what is also known as proxy discrimination, and does not consider any aspects of fairness and disparate impact; we also refer to Prince–Schwarcz [10], Frees–Huang [6], Lindholm et al. [9], Xin–Huang [16] and Grari et al. [7] for relevant discussions.

In this paper, we address the problem of avoiding indirect discrimination in the calculation of insurance prices. Lindholm et al. [9] give a mathematical definition of direct and indirect discrimination. Their approach for avoiding indirect discrimination amounts to, first, using all available information to calculate the so-called best-estimate price. In a second step, one removes the potential discriminatory dependence between and by marginalizing the best-estimate price w.r.t. a pricing distribution which does not allow one to infer (or proxy) the protected information from the non-protected variables . This step removes the statistical dependence between the two sets of information and results in the so-called discrimination-free insurance price as defined in Lindholm et al. [9]. This removal of statistical dependence can be motivated (and justified) by concepts of causal statistics, see Lindholm et al. [9] and Araiza Iturria et al. [1]; for an antecedent of this approach in economics, see Pope–Sydnor [12].

An attractive feature of the above discrimination-free insurance pricing approach is that any pricing model can be used to obtain the best-estimate price, which is subsequently adjusted to remove the potential for to be proxied by . Moreover, the suggested procedure ensures that all potential indirect discrimination is removed, where it exists, and this is achieved regardless of the ability of the particular class of regression model used to infer information about from . In particular, there is no need to explicitly quantify the potential impact of indirect discrimination before applying the method.

Thus, the calculation of discrimination-free insurance prices can be carried out using any reasonable pricing model, if one has access to the full covariate information . In practice, however, one may assume that the protected characteristics contain covariates that are considered sensitive, such as, e.g., ethnicity. Then, it will generally not be feasible to collect this information for all insurance contracts in the portfolio. As a consequence, it remains unclear how a model for discrimination-free insurance prices should be fitted, when discriminatory information is incomplete. The goal of this paper is to address precisely this issue. We present a multi-output neural network for multi-task learning, i.e., the proposed network architecture performs simultaneously different regression tasks. This proposed network architecture can also be fitted on incomplete protected information, and still provides accurate results. That is, to fit our network architecture we only need the protected information on a part of the portfolio, but we can still receive a good predictive regression model for discrimination-free insurance pricing. In particular, our proposal allows for more robust fitting compared to just ignoring insurance policies with missing protected information.

We illustrate the proposed methodology via a detailed case study, using a synthetic data set. The example demonstrates, first, that the multi-output network architecture provides results of comparable accuracy to a conventional feed-forward neural network, when complete information on policyholder characteristics is available. Second, when information on policyholder data is incomplete, the multi-task network greatly outperforms a conventional approach, whereby a regression model is only trained on those instances for which the full information is available – both in the case where data are missing at random and not at random. The superiority of the multi-task architecture is more prevalent in the more realistic case where the data drop-out of protected characteristics is high.

Organization of manuscript. In the next section we review the framework of discrimination-free insurance pricing as introduced in Lindholm et al. [9]. Section 3 presents our solution to the problem of having incomplete protected information, by gradually building up towards the multi-task network architecture. Section 4 provides the synthetic data example, which verifies the superior predictive power of our proposal against a naive way of just ignoring insurance policies with incomplete data. Finally, in Section 5 we give some concluding remarks.

2. Discrimination-free insurance pricing

We first recall the mathematical definitions of the best-estimate, unawareness and discrimination-free insurance prices, as they were introduced in Lindholm et al. [9]. Throughout, we work on a probability space that is assumed to be sufficiently rich to carry all the objects that we would like to study, and denotes the physical probability measure. Our goal is to employ a regression model that calculates the prices of insurance policies that satisfy the property of being discrimination-free according to Definition 12 of Lindholm et al. [9].

We assume that the vector of covariates can be partitioned into non-discriminatory covariates and discriminatory covariates (protected characteristics) . This split into and is given exogenously, e.g., by law or by societal norms and preferences. The distribution of the covariates of a randomly selected policyholder is described by . The (insurance) claim of this policyholder is denoted by , and we assume that this claim depends on the covariates . That is, we typically would like to study the conditional distribution function

of a selected policyholder having covariates .

The best-estimate price of the policyholder with covariates is defined by the conditional expectation (subject to existence)

| (1) |

This price is called best-estimate because, under square integrability, it minimizes the conditional mean squared error of prediction (MSEP), given full information . Thus, the best-estimate price (1) is the most accurate price we can calculate under full covariate information . The general statistical problem is to optimally determine (estimate) this regression function

| (2) |

from past data (and maybe expert opinion). Below, we are going to use a neural network regression approach for this task.

Obviously this best-estimate price (1) (potentially) directly discriminates because it uses the discriminatory covariates as input. This motivates the definition of the unawareness price, ignoring any knowledge about the discriminatory covariates ,

| (3) |

The unawareness price (3) avoids direct discrimination according to Definition 10 of Lindholm et al. [9] because we no longer need any information about the discriminatory covariates to calculate this price. Using the tower property of conditional expectations, we can rewrite the unawareness price as follows

| (4) |

where describes the conditional distribution of the discriminatory covariates , given the non-discriminatory information . It is exactly this link which is problematic, namely, having broad non-discriminatory information may (easily) allow us to infer the discriminatory information . Such an inference of the protected characteristics is therefore implicit in the definition of the unawareness price. This implicit inference has been coined in insurance as proxy discrimination, see, e.g., Frees–Huang [6] and Xin–Huang [16], or indirect discrimination, see Lindolm et al. [9]. To prevent indirect discrimination, one needs to break the link that allows one to infer from . This can be done purely statistically by just replacing the outer distribution in (4) by an unconditional one. This replacement can be justified by arguments from causal statistics if insurance claims follow a certain causal relationship, see Lindholm et al. [9] and Araiza Iturria et al. [1].

These arguments motivate the definition of the discrimination-free insurance price

| (5) |

where the pricing distribution is dominated by the marginal distribution of the discriminatory covariates .

Discrimination-free insurance pricing (5) has two ingredients, namely, the regression function , see (2), and the pricing distribution . The most natural choice for this pricing distribution is simply the marginal distribution , but there may be other (justified) choices, e.g., providing unbiasedness of discrimination-free insurance prices; for a broader discussion on the choice of we refer to Remark 7 and Section 4 in Lindholm et al. [9].

In this paper we are more concerned about the first issue, namely, about selecting, estimating and applying the (best-estimate) regression function . In practice, this requires that we hold both non-discriminatory and discriminatory information from the insurance policyholders for regression model fitting, and the discriminatory information is integrated out (adjusted for) only in the subsequent (second) step (5). However, in many cases it is problematic to collect this discriminatory information over the entire insurance portfolio. Therefore, fitting the regression function (5) might not be practical. In the next section, we provide a technical workaround which requires discriminatory information only for part of the portfolio, but it will still equip us with accurate predictive models.

Remark 1.

The discrimination-free insurance price (5) is defined within a given model specification, i.e., for a given distributional model for , see Definition 12 of Lindholm et al. [9]. This does not consider model error coming from a poorly specified stochastic model for , which may result in a different form of discrimination, e.g., arising from a certain sub-population being under-represented in the data. Naturally, on the corresponding part of the covariate space we have greater model uncertainty, because we have less data for an accurate model fit. This may result in forms of demographic discrimination that are outside of our (more narrow) scope which is always attached to a given stochastic model. For a discussion of discrimination arising from unrepresentative data in a different context, see Buolamwini–Gebru [2].

3. Multi-output network regression model

We present statistical modeling of the regression function within the framework of feed-forward neural networks (FNNs). We start by introducing a standard (plain-vanilla) FNN architecture, and in a second step we discuss how this FNN architecture can be modified to serve our purpose of deriving discrimination-free insurance prices with partial information of the protected characteristics. The notation and terminology of neural network regression modeling is taken from Wüthrich–Merz [15].

3.1. Feed-forward neural network regression model

Assume that the regression function can be modeled by a FNN architecture taking the following form

| (6) |

where is a strictly monotone and smooth link function, is a FNN of depth , and is the readout parameter providing the scalar product on the right-hand side of (6)

The FNN of depth is a composition of hidden FNN layers , , providing

This maps the -dimensional vector-valued input to a new (learned) -dimensional representation of the original non-discriminatory and discriminatory covariates .

Summarizing, FNN regression modeling requires specification of the network architecture. This involves the depth , the number of neurons in each hidden layer , the activation function in each of these neurons, as well as the link function . Such a network architecture can then be fitted (trained) to the available data, which means that the readout parameter as well as all parameters in the hidden layers (called network weights ) are fitted to the available data. Successful FNN fitting involves in most cases an early stopping strategy to prevent (in-sample) over-fitting the model to the training data, i.e., targeting for an optimal out-of-sample predictive performance; for a detailed description of network fitting we refer to Chapter 7 of Wüthrich–Merz [15].

This fitted FNN (6) provides the best-estimate prices

| (7) |

for the insurance claims , being described by the covariates . From this we can calculate the discrimination-free insurance prices with formula (5) by specifying a suitable pricing distribution . A standard choice is to use the marginal distribution of from the part of the portfolio where the protected information of is known.

The difficulty in practice with this approach, and similar regression approaches such as generalized linear models (GLMs), is that it requires full knowledge of the discriminatory information of the policyholders. Otherwise one cannot fit this FNN (6) on the available (past) data. A naive solution is to just fit this FNN architecture on the sub-portfolio where is available. We call this the (naive) plain-vanilla FNN approach because it is clearly non-optimal to disregard any insurance policy where there is no complete information about the covariates available.

Remark 2.

In the introduction we have mentioned that discrimination-free insurance pricing can be applied to any pricing (regression) model. Here, we restrict to FNN architectures which seems rather limiting. However, we would like to mention that large FNN architectures provide the universal approximation property. This implies that within FNN architectures we can mimick any other (sufficiently regular) regression model.

3.2. Multi-output neural network regression model

In constructing (and fitting) the plain-vanilla FNN best-estimate prices (7), we directly use the discriminatory information of the policyholders as an input variable to the FNN. Our proposal is to change this FNN architecture such that only the non-discriminatory information is used as an input variable to the network, but at the same time we generate a whole family of best-estimate prices that reflects the different specifications (levels) of the discriminatory information. In the present section we introduce this new network architecture. We call it a multi-output FNN architecture because it has multiple outputs that generate the family of models. In Section 3.3, below, we extend this multi-output FNN architecture to a multi-task FNN architecture which not only generates a whole family of models, but it also (internally) predicts the discriminatory information on the insurance policies where this information is missing. It will exactly be this multi-task FNN architecture that we promote for discrimination-free insurance pricing under incomplete discriminatory information, as it can deal with the issue of missing protected information, but still provides good predictive models. In this approach protected information will only be needed on part of the portfolio for model training.

Assume that the discriminatory information only takes finitely many values . Typically, we think of discriminatory information being of categorical type, e.g., gender or ethnicity. If this is not the case, discriminatory information can be discretized, and one should work with this discretized version. We modify the above plain-vanilla FNN (6) such that it only considers non-discriminatory covariates as an input giving us the learned representation

This learned representation should be sufficiently rich such that it provides a whole family of suitable regression functions, parametrized by . This typically requires that the number of hidden neurons, in particular in the last hidden layer, is not too small. This learned representation is now used to calculate the best-estimate prices simultaneously for all discriminatory specifications , that is, we set for the multi-output FNN architecture

| (8) |

In other words, for every non-discriminatory input we generate a whole family of outputs that simultaneously provide the best-estimate prices for all levels , , of the discriminatory information. The different specifications of the discriminatory covariates are encoded in the readout parameters , and the only remaining question is about fitting these parameters (as well as the network weights in the hidden layers) to the available data.

We start by describing how the plain-vanilla FNN (6) is fitted to i.i.d. data following the same model. For the moment we assume to be in the situation of complete information. We choose a loss function to assess the quality of a fit. This loss function can be the square loss function, a deviance loss function, or any other sensible choice that fits to the estimation problem to be solved. If collects all parameters to be estimated/fitted, then, typically, an optimal parameter is found by solving (M-estimation)

| (9) |

where in the regression function we highlight its dependence on the parameter to be optimized. This is the process to fit the plain-vanilla FNN given in (7), subject to early stopping to prevent from in-sample over-fitting; for a detailed discussion of FNN fitting we refer to Section 7.2.3 in Wüthrich–Merz [15].

For fitting the multi-output FNN (8) we modify this fitting procedure as follows

where collects all readout parameters and the network weights, see (8). That is, we add an indicator referring to the discriminatory information of observation , which, in turn, trains the corresponding readout parameter of the multi-output FNN (8). Note that this is the only step where the protected information is used in the multi-output FNN approach.

Having the fitted multi-output FNN (8) we arrive at the discrimination-free insurance prices

| (11) |

for each possible choice of the pricing distribution on the finite set .

To conclude, the multi-output FNN (8) generates a whole family of best-estimate prices of the discriminatory information in . This discriminatory information only enters the loss function in the fitting procedure (3.2), and once this model is fitted we no longer need discriminatory information to calculate the discrimination-free insurance price (11) for any (new) insurance policy.

3.3. Multi-task learning and incomplete discriminatory information

We extend the multi-output FNN architecture from the previous section to a multi-task learning model. This will be especially suitable for our problem of incomplete discriminatory information, because, as a second task, this extended multi-output FNN will predict the discriminatory information on the policies where this information is not available.

We define the categorical probabilities for , ,

We choose two separate FNNs for representation learning

| (12) |

For simplicity we assume that these two FNNs have exactly the same network architecture, but, typically, their network weights (parameters) and differ. The first FNN is used to model the best-estimate prices

| (13) |

and with readout parameters . The second FNN is used to model the categorical probabilities . Using the softmax output function and for readout parameters we receive the FNN classification model

| (14) |

At the current stage these two networks are completely unrelated because they run in parallel, and they can be fitted independently from each other. We now make them related by (internally) calculating the unawareness price using the tower property (4), i.e.,

| (15) |

Combining (13), (14) and (15) we receive the multi-task FNN architecture

| (16) |

with network parameter . As input this multi-task FNN only uses the non-discriminatory information . Remark that the unawareness price in (16) is calculated internally in the network using (15).

We now assume that the discriminatory information is only available on part of the insurance policies . This requires that we mask for the policies where no discriminatory information is available. As mask we set for . This will ignore the parts of the following loss function for which the discriminatory information is not available. We set for the new optimization problem

for given loss functions and . This network fitting problem (3.3) provides the interaction between the two FNNs, and it only considers the parts of the loss function where the corresponding information is available.

Remark 3.

-

•

The multi-output network (16) adds extra components to predict the discriminatory information from the non-discriminatory . Moreover, we directly determine the unawareness price , defined through (15), and this is integrated into the last term of (3.3). This model can be fitted by solving the optimization (3.3). For the loss function we typically either use the square loss function or the deviance loss function (within the exponential dispersion family), and for the loss function we are going to use the multinomial cross-entropy loss. Intuitively, one should scale the loss functions and such that they live on a comparable scale. In our numerical examples, the results have shown little sensitivity in such a scaling, therefore, we will just use the standard form of the deviance losses below, i.e., without any additional scaling.

-

•

In our multi-task FNN we consider two parallel FNNs, and the interaction is only considered by the joint parameter estimation in (3.3). We could also consider other network architectures where, e.g., we learn a common representation which serves to construct the readouts of and , . In our numerical experiments this latter approach was less competitive in terms of predictive power compared to the first one, but more work would be required to come to a conclusive answer about the ’best’ network architecture for this multi-task learning problem.

-

•

The last component of the objective function in (3.3) compares the (internally) calculated unawareness price to the response . Alternatively, we could fit another regression model for the unawareness price. This can be done because it does not involve any protected information . A variant of (3.3) then replaces the last objective function in (3.3) as follows

for given loss functions , and . This approach can be useful in certain situations of over-fitting, but it requires a high-quality model for in order to outperform the fitting procedure (3.3).

-

•

The multi-task FNN (16) is solely used to model the discrimination-free insurance price through (5). There are many different notions and definitions of fairness that may complement the discrimination-free insurance prices; see, e.g., Grari et al. [7]. Multi-task learning (16)-(3.3) can be extended by such complementary fairness notions. This requires that the notion of the chosen fairness criteria can be encoded into sensible scores that can be added to the optimization (3.3), and depending on the quantities needed in these additional scores, we may need to add corresponding outputs to the multi-task learning (16). As a result the multi-output network will be regularized by the corresponding scoring parts that account for the selected notions of fairness.

-

•

Alternatively to using certain scores for regularization, one can also set-up a generative-adversarial network (GAN), that tries to infer protected information from the prices. A successful implementation of such a GAN architecture will force the pricing network to design a pricing functional from which the gender cannot be inferred, we also refer to Grari et al. [7].

4. Synthetic health insurance example

We design a synthetic health insurance example that is similar to Lindholm et al. [9], but with a slightly more complicated underlying regression function. Working with a synthetic example, that is, knowing the true data generating model, has the advantage of being able to benchmark the estimated models to the ground truth.

4.1. Data generation

Let the discriminatory information be the gender of the policyholder. The non-discriminatory information is assumed to have two components, with denoting the age of the policyholder and the smoking status of the policyholder. There are different claim types: claims that mainly affect females between ages 20 and 40 and males after age 60 (type 1), claims with a higher frequency for smokers and also for females (type 2), and general claims due to other disabilities (type 3). The logged expected frequencies of these claim types are given by

with the following parameters: , , and . We set for the (true) total expected claim frequency

If we assume that the number of claims of an insurance policyholder with covariates is Poisson distributed with expected value , then we obtain the (true) best-estimate price

| (19) |

where, for simplicity, here we only focus on claim counts. Since in practice this true best-estimate price is not known, we estimate it from the available data using a regression function denoted by . We therefore first use a plain-vanilla FNN to model based on the full input , see (7). In the next steps we study the multi-output FNN (8) and the multi-task FNNs (16), which only use the non-discriminatory information as a network input, while the available discriminatory information is only used in the loss functions for model fitting; see (3.2), (3.3) and (• ‣ 3), respectively. Table 1 illustrates all models that we are going to consider, the labeling (a)-(f) will be kept throughout this example.

| label | regression model |

|---|---|

| (a) | true model with regression function given by (19) |

| (b) | plain-vanilla FNN regression function given by (7) |

| (c) | multi-output FNN regression function given by (8) |

| (d) | multi-task FNN () regression function given by (16) and (3.3) |

| (e) | multi-task FNN () regression function given by (16) and (• ‣ 3) |

| (f) | regression tree boosting (best-estimate benchmark) |

To fit these FNNs we first need to generate i.i.d. data . We select a portfolio of sample size as follows. The age variable is assumed to be independent of the smoking habits and the gender , and we choose the age distribution as given in Figure 4 of Lindholm et al. [9]. Moreover, we choose , and . This fully specifies the distribution of the covariates , making smoking more common among females compared to males in this population. We simulate independent insurance policies from this covariate distribution. This provides us with an empirical proportion of females in the simulated data of 0.4505, fairly close to the true ratio of 0.45. Later, we use this proportion for obtaining the pricing distribution, i.e., we set ; as explained in Lindholm et al. [9], this is a canonical choice for . Finally, we simulate independent observations , , giving the (pseudo-)sample , representing the portfolio of policies. In the next section we assume the availability of full covariate information for the protected characteristics , whereas in Section 4.3 we will assume only partial access to such information.

4.2. Full availability of discriminatory information

4.2.1. Plain-vanilla feed-forward neural network

We start with the plain-vanilla FNN (7), which takes as input the covariates with ; we use dummy coding for both the gender variable and the smoking habits . We choose a network of depth with hidden neurons in the three hidden layers, the ReLU activation function, and the log-link , which is the canonical link of the Poisson regression model. This network has a parameter of dimension 566. To implement this FNN we use the library Keras [4] within the statistical computing software R [11].

We fit this FNN to the simulated data ; assuming for now access to the full policyholder information, including . We use the Poisson deviance loss function for in (9), the nadam version of stochastic gradient descent, a batch size of 50 policies, and we explore early stopping based on a 80/20 training-validation split. This is similar to Section 7.3.2 in Wüthrich–Merz [15]; for more details we refer to that source. Since network fitting involves several elements of randomness, see Remarks 7.7 in Wüthrich–Merz [15], we average over 10 different FNN calibrations, resulting in the nagging predictor of Richman–Wüthrich [13].

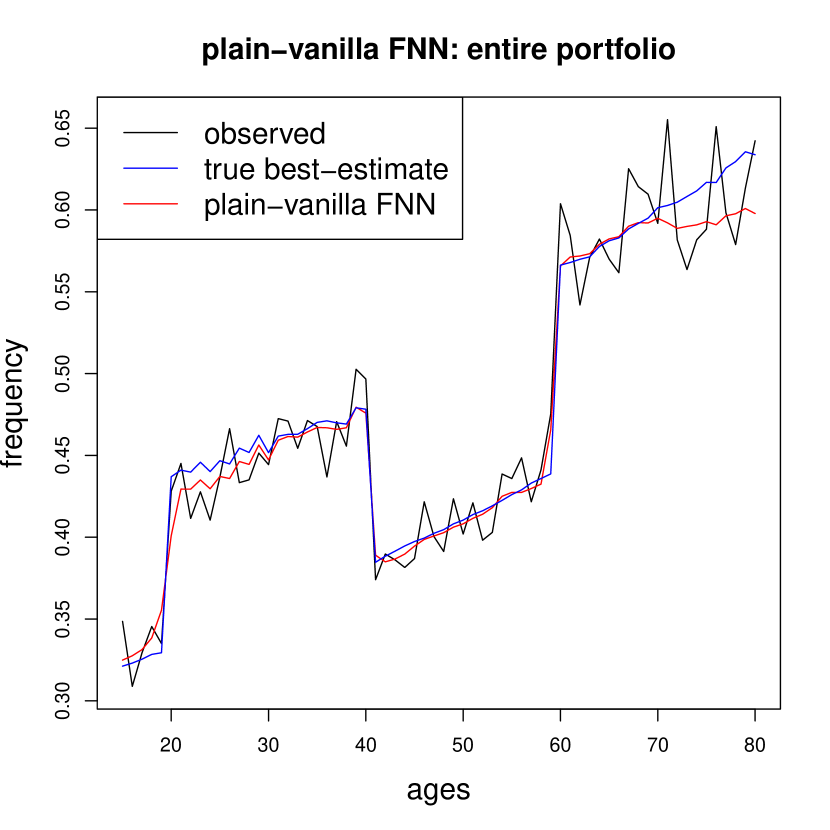

The results are given in Figure 1. The blue line shows the true best-estimate price as a function of the age variable , averaged over the smoking habits and the gender variable w.r.t. the empirical population density. The black color shows the corresponding observations and the red color the plain-vanilla FNN fitted best-estimate price using the full inputs . Overall, Figure 1 suggests a rather accurate fit; only at the age boundaries there are some differences which are caused by the noise in the observations .

Since we know the true regression function , we can explicitly quantify the accuracy of the estimated FNN regression function . That is, we do not need to validate the estimated model on a test data sample, but we can directly compare it to the true model. We use the Kullback–Leibler (KL) divergence to compare the estimated model to the true one. In the case of the Poisson model the KL divergence for given covariate values is given by

| (20) | |||||

We average the KL divergence of a single instance over the empirical population distribution, which gives us the KL divergence from the estimated model to the true model on our portfolio

| (21) |

This gives us a measure of model accuracy for the different estimated models; the KL divergence is zero if and only if the estimated model is identical to the true model on the selected portfolio; see Section 2.3 in Wüthrich–Merz [15].

| KL divergence (21) | |

|---|---|

| to | |

| (b) plain-vanilla FNN: full data | 0.2204 |

| (c) multi-output FNN: full data | 0.2567 |

| (d) multi-task FNN (): full data | 0.2823 |

| (e) multi-task FNN (): full data | 0.3070 |

| (f) regression tree boosting: full data | 0.5170 |

Row (b) of Table 2 shows the KL divergence (21) of the fitted plain-vanilla FNN best-estimate price to the true best-estimate price . The resulting KL divergence is , which is much smaller than a comparable regression tree boosting model that results in a KL divergence of , shown in row (f) of Table 2.

This fitted FNN can now be used for discrimination-free insurance pricing according to formula (5) for the given selected measure . However, we cannot calculate the unawareness price from (3) because this requires the knowledge of the probabilities , see (4). Alternatively, we could directly fit a plain-vanilla FNN for estimating the unawareness price, a route we do not pursue here. We come back to this topic when discussing the multi-task FNN.

4.2.2. Multi-output feed-forward neural network

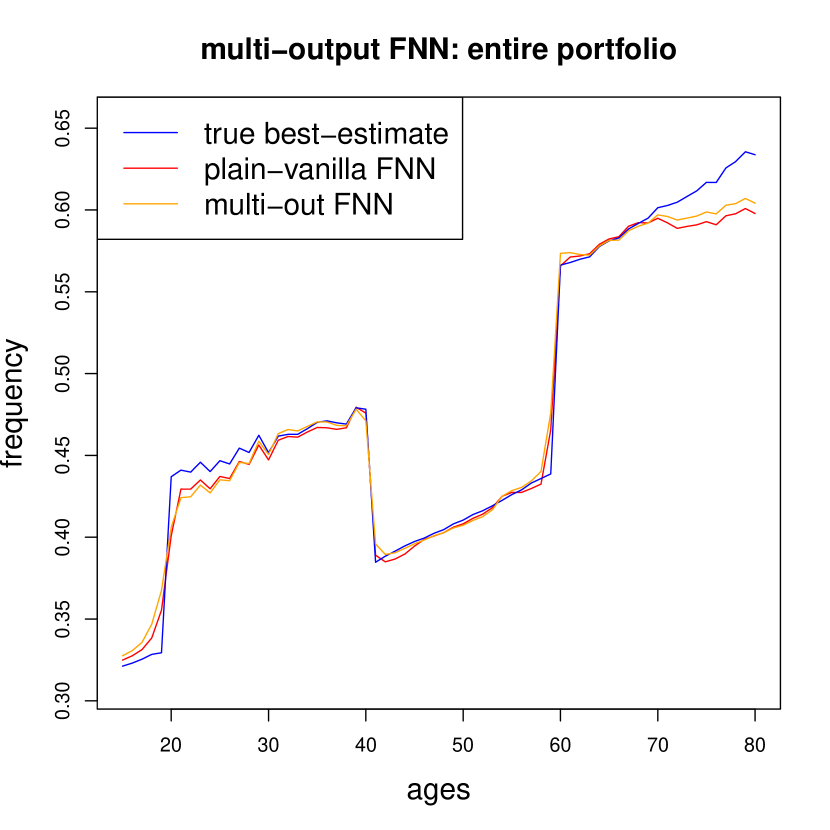

Next, we fit the multi-output FNN (8) to the same data, only using the non-discriminatory covariates as input to the network. This reduces the input dimension to , but on the other hand we have two outputs and in the multi-output FNN. The former reduces the dimension of the network parameter and the latter increases the dimension of the network parameter, resulting in a network parameter of dimension 557. We fit this multi-output FNN using exactly the same fitting strategy as above. The results are presented in orange color in Figure 2 (lhs), and they are compared to the plain-vanilla FNN best-estimates in red color and the true best-estimates in blue color. We conclude that the two networks (orange and red) provide rather similar results.

Table 2 shows a slightly higher accuracy of the plain-vanilla FNN (row (b)) compared to the multi-output FNN (row (c)), with respective KL divergence values of vs. . In general, these numbers are quite small and the models are rather accurate, which is in support of both FNN models.

4.2.3. Multi-task feed-forward neural network

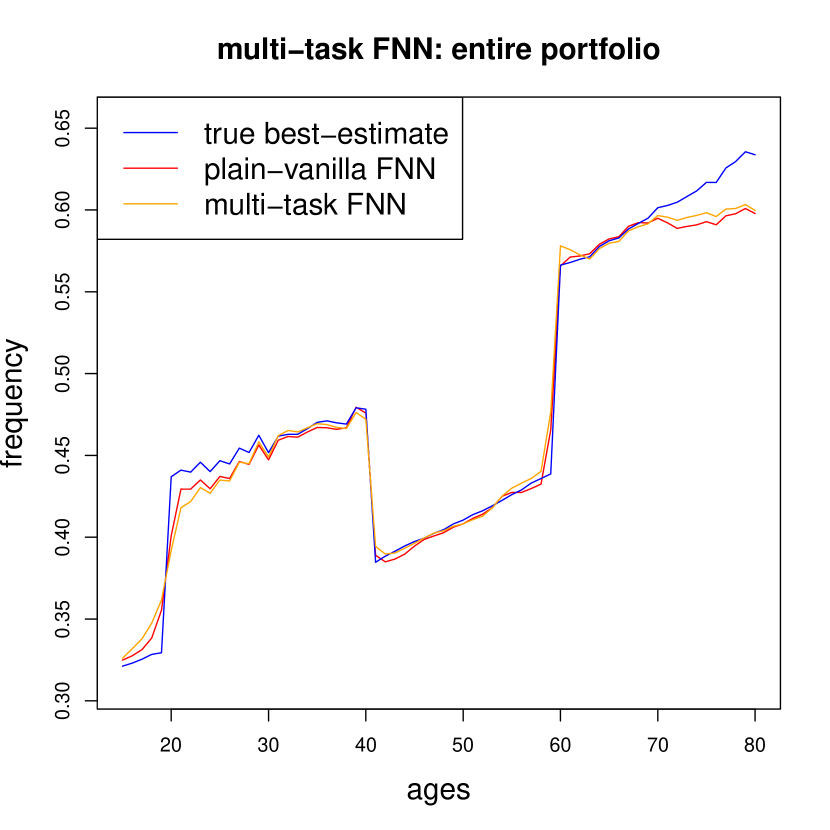

We now fit the multi-task FNN (16) to the data, still assuming full knowledge of the discriminatory information . The multi-task FNN additionally predicts the discriminatory covariates which are then (internally) used to calculate the unawareness price , see (15)-(16). That is, in contrast to the plain-vanilla FNN and the multi-output FNN, this is the only one of the three approaches that allows us to directly calculate the unawareness prices within the same model as the best-estimate prices. We start with objective function (3.3) considering the response for assessing the unawareness price .

We use exactly the same fitting strategy as in the previous two modeling approaches. Figure 2 (rhs) shows the resulting best-estimate prices (in orange color) compared to the ones of the plain-vanilla FNN (in red color). Row (d) of Table 2 provides a resulting KL divergence to the true model of . This is slightly higher than in the other two approaches, but still gives a very competitive result. The full advantage of the multi-task FNN approach will become clear once we start working with incomplete discriminatory information in Section 4.3 below.

Finally, we present the fitting results of the multi-task FNN (16) when using objective function (• ‣ 3). For this we first fit a plain-vanilla FNN to the unawareness price (only considering ). This is done completely analogously to Section 4.2.1 except that we drop the discriminatory information from the input. We then use this fitted FNN in objective function (• ‣ 3), and we use the KL divergence (20) for to measure the divergence from to . The results are presented on row (e) of Table 2. We observe that this is the least accurate of all FNN models, the main issue probably being that the regression function is not sufficiently accurate, and we should rather directly compare the unawareness price to the observations as done in (3.3). For this reason, we will not further pursue this approach below.

4.2.4. Discrimination-free insurance pricing

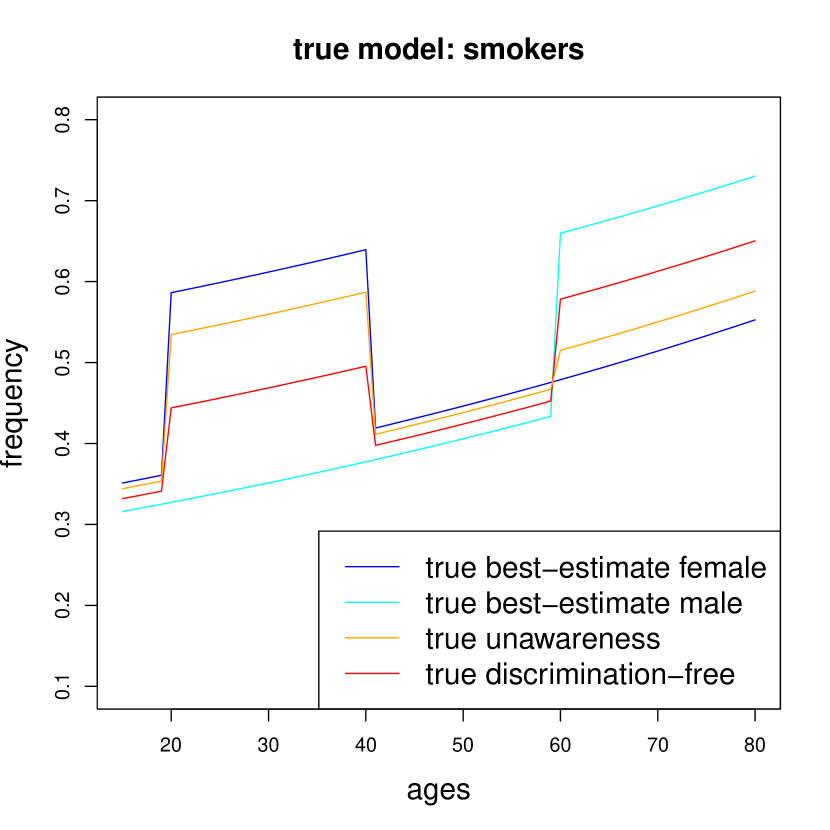

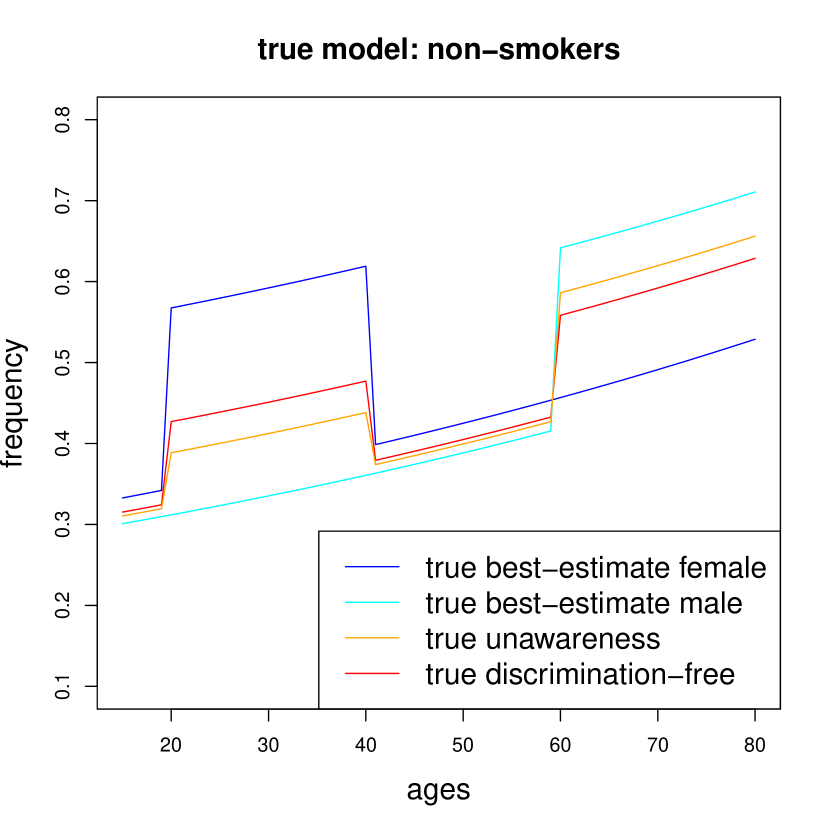

Having fitted the three FNNs, we can calculate the discrimination-free insurance prices by (11), using the empirical gender distribution as the pricing distribution. We start by considering the true model . We calculate the discrimination-free insurance prices and the unawareness prices in the true model. This can be done because all necessary information is available. The corresponding graphs are shown in Figure 3, and they will serve as a benchmark for the estimated FNNs. It is seen that the unawareness prices closely follow the best-estimate prices of females for smokers, and the best-estimate prices of males for non-smokers. This reflects the fact that, in our example, smoking habits are rather informative for predicting the gender. The discrimination-free insurance prices exactly correct for this inference potential: as seen from Figure 3, while smokers of either gender have higher predicted claims frequencies than non-smokers, discrimination-free insurance prices lie between the best-estimate prices for males and females, following the same pattern regardless of smoking status.

| KL divergence (21) | |

|---|---|

| to | |

| (a0) true unawareness price | 6.3174 |

| (d0) multi-task FNN () unawareness price | 6.4932 |

| (a1) true discrimination-free price | 7.8857 |

| (b1) plain-vanilla FNN discrimination-free price | 8.3222 |

| (c1) multi-output FNN discrimination-free price | 8.2669 |

| (d1) multi-task FNN () discrimination-free price | 8.2915 |

Table 3 presents the corresponding numerical results. The unawareness price in the true model has a KL divergence to the best-estimate price of , see row (a0). That is, we sacrifice quite some predictive accuracy by ignoring the protected information in the unawareness price . This approach still internally infers the gender from the non-discriminatory information, see (4). Breaking this link further decreases the predictive accuracy, resulting in a KL divergence from the discrimination-free insurance price to the best-estimate price of , see Table 3, row (a1).

Furthermore, Table 3 provides all KL divergences to the true best-estimate price that can be calculated from the three fitted FNNs: row (b1) considers the discrimination-free insurance price in the plain-vanilla FNN (6), row (c1) the discrimination-free insurance price in the multi-output FNN (8) and rows (d0) and (d1) the unawareness price and the discrimination-free insurance price in the multi-task FNN (16) using objective function (3.3). The last FNN is the only one that directly provides the unawareness price . The accuracy of the resulting discrimination-free insurance prices is rather similar between the three network approaches (KL divergences on rows (b1)-(d1) of Table 3). Clearly we sacrifice quite some predictive power by not being allowed to use the protected information , such that the KL divergences increase from in Table 2 to roughly in Table 3.

| KL divergence (21) | |

|---|---|

| to | |

| (b2) plain-vanilla FNN discrimination-free price | 0.1748 |

| (c2) multi-output FNN discrimination-free price | 0.1885 |

| (d2) multi-task FNN discrimination-free price | 0.2323 |

Table 4 compares in KL divergence the discrimination-free insurance prices of the three fitted FNNs to the true discrimination-free insurance price . The plain-vanilla FNN provides slightly more accurate results compared to the multi-output and the multi-task FNNs. Note that the different rankings in Tables 3 and 4 may be caused by the randomness in the data and by potentially different over- or under-fitting to the data. A verification of the explicit reasons for these different rankings is difficult, and different samples may also change this order.

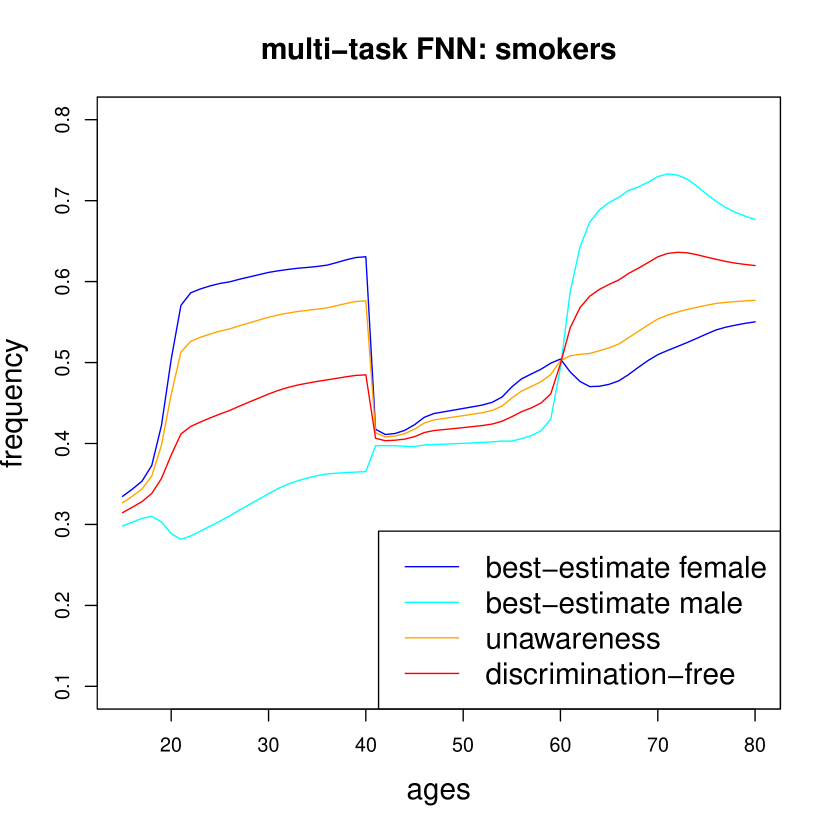

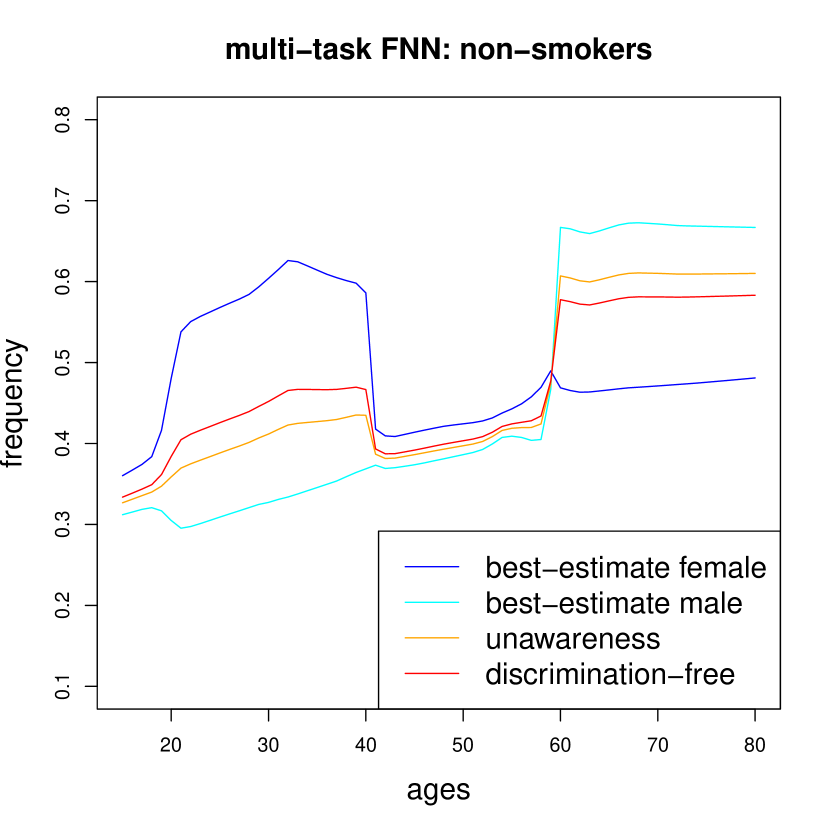

Finally, Figure 4 illustrates the resulting prices from the multi-task FNN. They should be compared to the true ones in Figure 3. The interpretation is the same in the two figures. Comparing the two plots we can also clearly see the impact of model uncertainty in Figure 4, which can only be mitigated by having larger sample sizes.

4.2.5. Quantification of direct and indirect discrimination

The results of Tables 2-4 give motivation to quantify the potential for direct and indirect discrimination. In contrast to these former results, we now compare the unawareness price and the discrimination-free insurance price to the best-estimate price within a given model. The step from the best-estimate price to the unawareness price accounts for direct discrimination by quantifying the effect of simply being blind w.r.t. the protected information . Going from the unawareness price to the discrimination-free insurance price accounts for indirect discrimination. However, these steps are more subtle for several reasons. First, the KL divergence does not satisfy the triangle inequality and, hence, divergences cannot simply be decomposed along a certain path. Second, in some models we cannot simultaneously calculate the best-estimate, the unawareness and the discrimination-free insurance prices, but need to use different models to estimate these quantities. This applies, e.g., to the multi-output FNN where we do not receive the unawareness price within that network model, but we have to explore another (separate) model to estimate this unawareness price. This critical point does not apply to the multi-task FNN, where we consistently calculate all terms within the same model. Third, interpreting the potential for indirect discrimination more broadly, there are two ingredients, namely, the inference part and the best-estimate prices . Only if both of them are sufficiently imbalanced, indirect discrimination becomes relevant (and visible). If we think of different insurance companies selling the same product (with the same underwriting standards and the same claim costs), these companies should use the same best-estimate prices . Indirect discrimination will typically differ between these companies, because they will generally have different portfolio distributions , resulting in different inference potentials. Thus, the statistical dependence between and is company-specific, and so is the amount of indirect discrimination.

| KL divergences to the best-estimates: | ||

| unawareness | discrimination-free | |

| (a) true model | 6.3174 | 7.8857 |

| 100% | 125% | |

| (d) multi-task FNN | 6.7980 | 8.5339 |

| 100% | 126% | |

Table 5 reflects the loss of model accuracy if we deviate from the best-estimate price. These losses can be interpreted as the quantification of direct and indirect discrimination. If we normalize the KL divergence of the unawareness price to 100%, then the discrimination-free insurance price adds another 25% to the loss of model accuracy compared to the unawareness price. Thus, direct discrimination is clearly the dominant term, here. Nonetheless, we not that the numbers in Table 5 reflect portfolio considerations, and the impact of indirect discrimination on particular sub-populations or individual policies may be more substantial.

4.3. Partial availability of discriminatory information

4.3.1. Missing completely at random

So far, all numerical results have been based on full knowledge of the data . Next, we turn our attention to the problem of having incomplete discriminatory information, and analyze how well we can fit our FNNs under this partial information setting. We therefore randomly remove from the information set. This is done by independently (across the entire portfolio) setting with increasing (drop-out) probabilities of . That is, in the last case only roughly 10% of the discriminatory labels are available, and in the first case roughly 90% of all discriminatory labels are available. Working with these drop-outs also changes the empirical female ratio that can be calculated on the policies with full information. We state these in Table 6 (row ‘empirical ’) as we use them for the pricing measure .

| drop-out | 90% | 80% | 70% | 60% | 50% | 40% | 30% | 20% | 10% | 0% |

|---|---|---|---|---|---|---|---|---|---|---|

| available | 10% | 20% | 30% | 40% | 50% | 60% | 70% | 80% | 90% | 100% |

| empirical | 44.8% | 44.5% | 44.3% | 44.5% | 44.6% | 45.5% | 45.4% | 45.2% | 45.1% | 45.1% |

| multi-task | 45.8% | 44.8% | 44.3% | 44.5% | 44.7% | 45.5% | 45.4% | 45.2% | 45.0% | 45.1% |

We use these data sets with drop-outs (incomplete protected information) to perform two different model fittings. Firstly, in a more naive approach, we just fit a plain-vanilla FNN (6), such that we only use those observations for which the discriminatory information is available and we drop all insurance policies with incomplete information. Thus, if e.g. the drop-out probability is 80% we only use the remaining 20% of the data for model fitting, for which the discriminatory information is available. Secondly, this naive approach is challenged by a multi-task FNN (16) fitted with the loss function (3.3), which accounts for partial availability of discriminatory information, but uses the entire portfolio for model fitting.

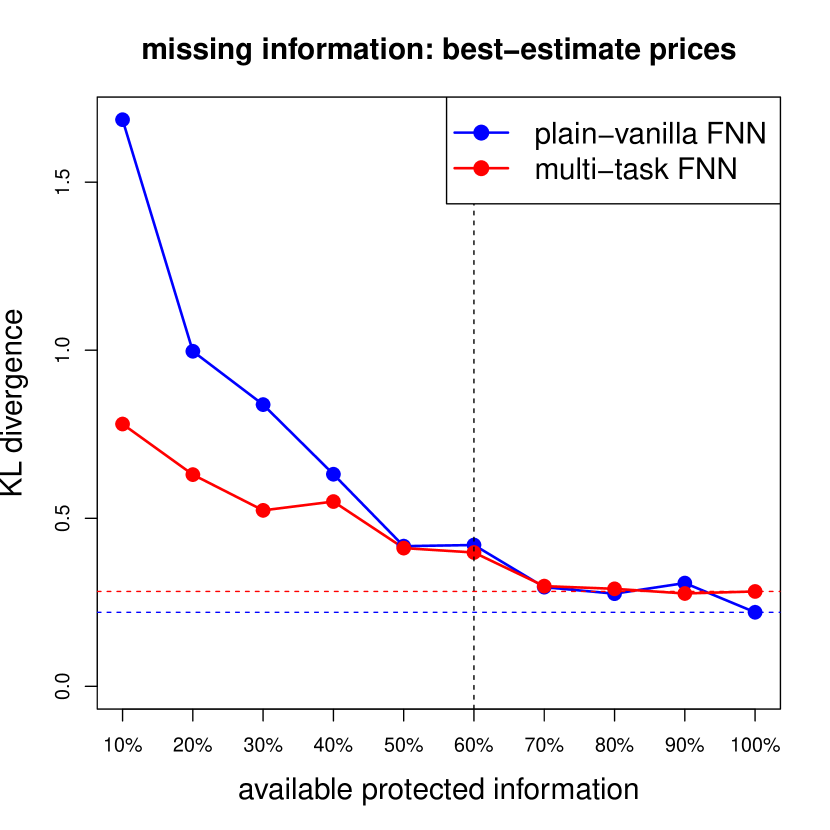

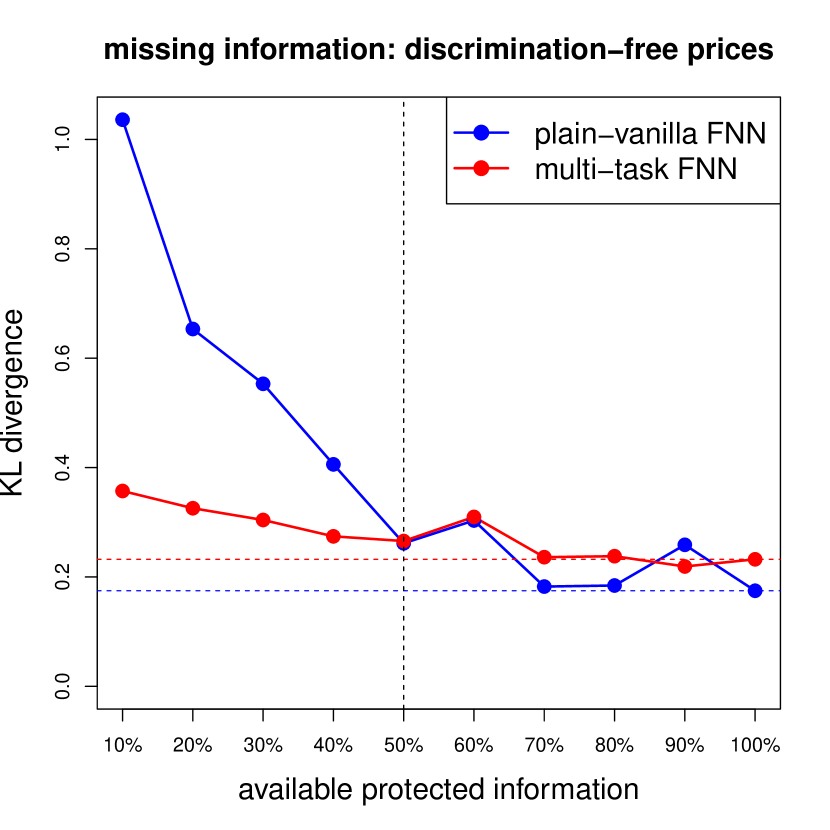

The results are presented in Figure 5. This figure shows the KL divergences from the fitted best-estimate prices to the true best-estimate price ; the dotted horizontal lines illustrate the results of Table 2 reflecting the case of full discriminatory information. We observe that if sufficient discriminatory information is available, then we have a similar performance between the plain-vanilla FNN and the multi-task FNN. However, below a critical amount of discriminatory information (60% in our case; vertical dotted line) we give clear preference to the multi-task FNN because its KL divergence from the true model is clearly smaller, i.e., we receive a more accurate model from the multi-task FNN.

This preference for the multi-task FNN carries over to the discrimination-free insurance prices. In Figure 6 we illustrate the KL divergences from the estimated discrimination-free insurance prices to the true discrimination-free insurance price ; the case of full discriminatory information is denoted by the horizontal dotted lines and corresponds to rows (b2) and (d2) of Table 4. We observe smaller KL divergences of the multi-task FNN approach if we have discriminatory information on less than 50% of the policies (vertical black dotted line). Furthermore, we notice that in the multi-task FNN case, the KL divergence deteriorates only mildly, when the availability of discriminatory information decreases beyond the 50% point.

The discrimination-free insurance prices of Figure 6 have simply used the empirical estimates for from the insurance policies where full information is available, see row ‘empirical ’ of Table 6. Having the fitted multi-task FNN we can also use the estimated categorical probabilities , , from (16) to estimate the distribution of the protected covariates. Namely, we get an estimate

| (22) |

These estimates (in the binary gender case ) are presented on the last row of Table 6. We observe that they match the empirical estimates, and only for high drop-out probabilities we have some differences to the empirical estimates. The specific choice only has a marginal influence on the prices.

4.3.2. Not missing completely at random

In the last example, illustrated by Figures 5 and 6, discriminatory information was removed completely at random, i.e., was set to NA by an i.i.d. Bernoulli random variable with a fixed drop-out rate. However, it might be that the missingness of protected information is not completely independent from the remaining covariates . Of course, there are many different ways in which this could happen, and we just provide here one particular example. We take as a baseline the i.i.d. Bernoulli case with a drop-out probability of 70%. We then modify this case by choosing a higher drop-out rate for the gender information on the policies . Besides the base case of 70%, we choose the drop-out rates of 80% and 90% on . Note that collects the smokers with ages below 45, and by the choice of our population distribution, 79.9% on this sub-portfolio are female.

| missing at random | not missing at random | ||

|---|---|---|---|

| drop-out rate on | 70% | 80% | 90% |

| overall drop-out rate | 70% | 78% | 86% |

| empirical | 44.3% | 42.4% | 40.3% |

| multi-task | 44.3% | 45.0% | 44.9% |

Table 7 shows the resulting overall drop-out rates. These drop-out rates are no longer missing completely at random, because we have higher drop-out rates on . In our case this results in a biased empirical gender estimate. This can be seen from the row ‘empirical ’ which simply calculates the empirical female ratio on the policies where full information is available. Having the fitted multi-task FNN, we can also estimate the female ratio using the categorical probability estimates of , see (22). This provides us with the results on the last row of Table 7. We observe that these estimates are close to unbiased, the true value being 45%. We can use this multi-task FNN to estimate as pricing measure for the discrimination-free insurance price in the case of data not missing completely at random.

| KL divergence (21) to | |||

|---|---|---|---|

| missing at random | not missing at random | ||

| drop-out rate on | 70% | 80% | 90% |

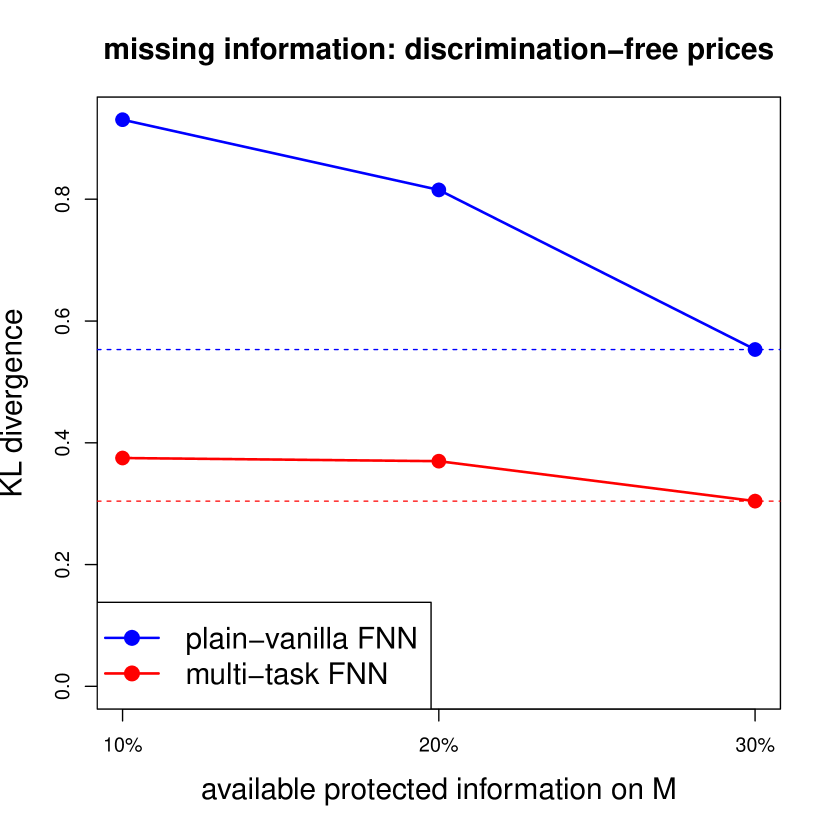

| (b3) plain-vanilla FNN discrimination-free | 0.5532 | 0.8153 | 0.9306 |

| (d3) multi-task FNN discrimination-free | 0.3042 | 0.3698 | 0.3750 |

Table 8 and Figure 7 present the results. The base case is the i.i.d. Bernoulli drop-out case with a drop-out rate of 70%, taken from Figure 6. This base case is modified to a higher drop-out rate of 80% and 90%, respectively, on sub-portfolio ; see Table 7 for the resulting overall drop-out rates. For the pricing measure we choose the empirical probability in the plain-vanilla FNN case and the multi-task FNN estimate in the multi-task FNN case, see Table 7. At the first sight, this does not seem to be an entirely fair comparison because the former estimates are biased. However, there is no simple way in the plain-vanilla FNN case to receive better gender estimates, whereas in the multi-task FNN case we obtain these better estimates as an integral part of the prediction model. In this not missing completely at random example we arrive at the the same conclusion, namely, that the multi-task FNN shows superior performance. We remark that even if we would use the same biased gender estimates also in the multi-task FNN to calculate the discrimination-free insurance prices we would come to the same conclusion.

Remark 4.

In Remark 1 we have discussed that discrimination may also result from the fact that a certain sub-population is under-represented in the data and, hence, we may have a poorly fitted model on this part of the covariate space. This form of discrimination is directly related to incomplete data not missing completely at random, which is relevant when fitting the best-estimate price . The present section has shown that the multi-task FNN can help to improve model accuracy if under-representation is caused by missing discriminatory information. However, if the sub-population is under-represented per se, e.g., there are only few elderly female smokers in the portfolio, then this multi-task FNN cannot resolve the fundamental class imbalance problem.

5. Concluding remarks

Addressing the problem of indirect or proxy discrimination involves an apparent paradox: in order to compensate for the potentially discriminatory effect of implicitly inferring policyholders’ protected characteristics, information on these very characteristics must be available for regression modeling. Resolving this tension poses clear legal, regulatory and technical challenges. Here, focusing on the latter, we provided a multi-task neural network learning framework, which can generate insurance prices that are free from indirect discrimination. We demonstrated that this multi-task architecture is competitive to conventional approaches when full information is available, while clearly outperforming them in the case of partial information.

Nonetheless, there is an aspect of the technical challenge that we have not yet fully addressed. Practically, we still need discriminatory information for a part of the portfolio in order to fit our model. Hence, a scheme needs to be in place that allows insurers to access such protected information for a subset of policies. Such a scheme may be constructed commercially, e.g., by offering special discounts to customers who are willing to disclose information on protected characteristics. Besides addressing privacy concerns, a difficulty with such an approach is to ensure (or mitigate) the potential selection bias that such a commercial promotion will generally have. While our case study illustrated good performance of our model when data are not missing at random, further work on this topic is required.

A related issue is that, to go from best-estimate prices to discrimination-free insurance prices, we need to choose the pricing measure . A natural candidate is to use the empirical version of , but since this choice will be based on a subset of the portfolio, the question again arises as to whether this subset is representative of the entire portfolio. In the multi-task FNN we receive an estimate for as an integral part of the prediction model by the averaging in (22) of the estimated categorical probabilities . Alternatively, techniques from survey sampling could be used in order to obtain an estimate of , using so-called indirect questioning. These techniques were constructed in order to obtain unbiased estimates of population proportions of a single sensitive dichotomous characteristic, such as drug use and sexual preference, based on open answer questionnaires, see the seminal paper by Warner [14]. For more general categorical sensitive characteristics, alternative techniques can be used; see Lagerås–Lindholm [8] and the survey of Chaudhuri–Christofides [3]. Regardless of the specific technique employed, by obtaining a suitable total population estimate for it is possible to assess whether the sub-portfolio has been sampled with data missing completely at random or not.

References

- [1] Araiza Iturria, C.A., Hardy, M., Marriott, P. (2022). A discrimination-free premium under a causal framework. SSRN Manuscript ID 4079068.

- [2] Buolamwini, J., Gebru, T., (2018). Gender shades: intersectional accuracy disparities in commercial gender classification. In: Conference on Fairness, Accountability and Transparency, Proceedings of Machine Learning Research 81, 77-91.

- [3] Chaudhuri, A., Christofides, T.C. (2013). Indirect Questioning in Sample Surveys. Springer.

- [4] Chollet, F., Allaire, J.J., and others (2017). R interface to Keras. https://github.com/rstudio/keras

- [5] European Council (2004). COUNCIL DIRECTIVE 2004/113/EC - implementing the principle of equal treatment between men and women in the access to and supply of goods and services. Official Journal of the European Union L 373, 37-43.

- [6] Frees, E.W.J., Huang, F. (2022). The discriminating (pricing) actuary. North American Actuarial Journal, in press.

- [7] Grari, V., Charpentier, A., Lamprier, S., Detyniecki, M. (2022). A fair pricing model via adversarial learning. arXiv:2202.12008v2.

- [8] Lagerås, A., Lindholm, M. (2020). How to ask sensitive multiple-choice questions. Scandinavian Journal of Statistics 47(2), 397-424.

- [9] Lindholm, M., Richman, R., Tsanakas, A., Wüthrich, M.V. (2022). Discrimination-free insurance pricing. ASTIN Bulletin 52(2), 55-89.

- [10] Prince, A.E.R., Schwarcz, D. (2020). Proxy discrimination in the age of artificial intelligence and big data. Iowa Law Review 105(3), 1257-1318.

- [11] R Core Team (2021). R: a language and environment for statistical computing. R Foundation for Statistical Computing, Vienna, Austria. https://www.R-project.org/

- [12] Pope, D.V., Sydnor, J.R. (2011). Implementing anti-discrimination policies in statistical profiling models. American Economic Journal 3(3), 206-231.

- [13] Richman, R., Wüthrich, M.V. (2020). Nagging predictors. Risks 8/3, article 83.

- [14] Warner, S.L. (1965). Randomized response: a survey technique for eliminating evasive answer bias. Journal of the American Statistical Association 60(309), 3-69.

- [15] Wüthrich, M.V., Merz, M. (2022). Statistical Foundations of Actuarial Learning and Its Applications. Springer Actuarial, in press. SSRN Manuscript ID 3822407.

- [16] Xin, X., Huang, F. (2021). Anti-discrimination insurance pricing: regulations, fairness criteria, and models. SSRN Manuscript ID 3850420.