Minimal Kullback-Leibler Divergence for Constrained Lévy-Itô Processes

Abstract

Given an -dimensional stochastic process driven by -Brownian motions and Poisson random measures, we seek the probability measure , with minimal relative entropy to , such that the -expectations of some terminal and running costs are constrained. We prove existence and uniqueness of the optimal probability measure, derive the explicit form of the measure change, and characterise the optimal drift and compensator adjustments under the optimal measure. We provide an analytical solution for Value-at-Risk (quantile) constraints, discuss how to perturb a Brownian motion to have arbitrary variance, and show that pinned measures arise as a limiting case of optimal measures. The results are illustrated in a risk management setting – including an algorithm to simulate under the optimal measure – and explore an example where an agent seeks to answer the question: what dynamics are induced by a perturbation of the Value-at-Risk and the average time spent below a barrier on the reference process?

keywords:

circled[2] \endlocaldefs

, and

1 Introduction

We consider stochastic processes that follow Lévy-Itô dynamics under a reference probability measure over a finite time horizon. The reference measure may arise in a data driven way and / or from modelling assumptions, however, it does not precisely capture all probabilistic beliefs of a modeller. In this work, misspecification under are characterised via expected values of functions of the stochastic process at terminal time and expected running costs of the processes over the entire time horizon. To mitigate model error, we seek over all absolutely continuous probability measures, under which the process satisfies these constraints, the one which is closest to the reference measure in relative entropy, also called Kullback-Leibler (KL) divergence. Thus, the key contribution of this work is solving the following constrained optimisation problem: Find the probability measure(s) that has minimal KL-divergence subject to constraints that can be written as (i) expected values of functions applied to the stochastic process at terminal time, and (ii) expected running costs of the processes over the entire time horizon.

We proceed to solve the optimisation problem by first considering a related optimisation problem where we seek over a subset of probability measures. Specifically, the subset consists of equivalent probability measures that arise from Doléans-Dade exponentials and we study this related problem using stochastic control techniques for Lévy-Itô processes. That is, we solve the dynamic programming equations and characterise a candidate solution (Proposition 2.5), prove that the candidate solution is indeed the value function associated with the optimisation problem and that the resulting controls (which induce the optimal measure change) are admissible (Theorems 2.6 and 2.9). Furthermore, we show that the optimal measure change can be written as the exponential of a collection of random variables corresponding to the constraints (Corollary 2.8 and Theorem 2.9). Finally, we prove that if a solution to the sub-problem (seeking over the subset of equivalent measures) exits, then it is unique and, moreover, it is the unique solution to the original optimisation problem, where we seek over all absolutely continuous probability measures (Theorem 2.11).

We illustrate the dynamics of the stochastic process under the optimal measure using multiple examples. For example, for the case of two Value-at-Risk (also known as quantile) constraints, we provide an analytical expression for the optimal measure change. We further show how to optimally change the dynamics of a Brownian motion to have zero mean and arbitrary variance. We also discuss the connection of the solution to our constrained optimisation problem to pinned measures; probability measures where the terminal value of the process lies almost surely within a Borel measurable set. While such measures are not equivalent with respect to and thus do not fall into the set of admissible measures of our related problem, we derive them as a limiting case of solutions to our optimisation problem. We further consider infinitesimal perturbations; that is, we solve the problem where the constraints are equal to their -expectation plus multiplied with a direction . In this setup, we prove that the Lagrange multiplier is, up to order , the inverse of the -covariance matrix of the constraint functions multiplied by and the direction of the perturbation. Using this result, we define a derivative – termed entropic derivative – of a risk functional along constraints in direction of least relative entropy. As examples we show the connection of the entropic derivative to differential sensitivities of risk functionals such as the Tail-Value-at-Risk and distortion risk measures. Finally, we provide an algorithm for solving and simulating from the optimal probability measure and illustrate the numerical results on a running cost constraint in a financial setting on real data.

Studying minimal relative entropy subject to constraints has a long history starting with the seminal paper of [7]. Applications to model risk assessment include [11] which uses the relative entropy to quantify worst-case model errors in a static setting. Similarly and also in a static setting, [5] proposes to quantify distributional model risk by considering alternative models that lie within a KL-tolerance distance from a reference measure. The work in [16] investigates what happens in the limit of small KL-tolerances. Conceptually close to our work – though in a static setting – is [19] which considers a reference probability measure and finds the probability measure that satisfies risk measure constraints with minimal relative entropy to the reference measure. None of these works, however, consider stochastic processes and thus do not consider running cost constraints.

The KL-divergence has many applications in financial mathematics. Starting with the influential work of [21], the vast majority of the literature on minimising relative entropy focuses on its application for derivative pricing in incomplete markets. To avoid arbitrage, such questions require restricting to martingale measures. Articles [3, 2], for example, consider a reference model and seek over all equivalent martingale measures, in a simple diffusive setting, to ensure that a collection of prices of European contingent claims are matched correctly. Article [6] extends [2] by using a compound Poisson process (with discrete jump sizes) as a reference model. The work in [14] studies the problem of finding martingale measures for exponential Lévy processes that minimise Rényi- and KL-divergences, and [8] uses convex regularisation techniques, motivated by KL-divergence as a regulariser, to calibrate local volatility models. In this exposition, we consider a different problem in that we do not restrict to martingale measures but solve for the optimal dynamics of the process such that given constraints are fulfilled. In particular, in contrast to our setup, all of the above mentioned literature work with risk-neutral measures (i.e., martingale measures). Moreover, the running cost constraint considered in this work is novel. A natural interpretation of the running costs constraint in mathematical finance is that of the average time spent below a barrier which we consider in the numerical example section.

Optimising the (relative) entropy has a long tradition and many applications in physics. Article [13] for example investigates the problem of specifying expectations of observables (random variables) and seek over distributions (models) that match these expectations, and which maximise the Shannon entropy to obtain the model that best reflects the information contained in the expectations. This work has been extended in many directions, and for instance [18] shows how relative entropy may inform about the arrow of time by looking at the relative entropy between the distribution of a process forward in time and its reversed version. As another example, [22] proposes a process for how a (physical) system may evolve to a state of minimal relative entropy, subject to an energy and mass constraint, based on the speed-gradient principle (see, e.g., [10]).

Calculations of the KL-divergence of processes has been studied by [23], which establishes that -divergences, and hence the KL-divergence, between two probability measures on path space may be approximated by focusing on their finite dimensional distributions. An application to uncertainty quantification in a dynamic setting is [9], which uses a variational representation of the Rényi-divergence which encompasses the KL-divergence to provide uncertainty quantification bounds for rare events.

This paper is structured as follows. Section 2.1 introduces the necessary notation and the two constraint optimisation problems we consider. We present a formal derivation of a candidate solution and a verification theorem in Section 2.2. Section 2.3 contains an alternative representation of the associated Radon-Nikodym derivatives and in Section 2.4 we state the existence and uniqueness of the solutions to both optimisation problems. Examples including analytical solution for Value-at-Risk (quantile) constraints, Brownian motion with arbitrary variance, and the connection of the solution to our optimisation problem to pinned measures are discussed in Section 3. In Section 4.1 we consider infinitesimal perturbations, that is the optimisation problem where the constraints their -expectations plus multiplied by a direction , and derive the optimal Lagrange multiplier up to order . In Section 4.2 we define the entropic derivative an relate it to differential sensitivities of risk functionals. Section 5 proposes an algorithm for calculating the dynamics of the process under the optimal measure, which we illustrate on a financial dataset and a running cost constraint.

2 Optimisation Problem and its Solution

2.1 Model Setup and Optimisation Problems

We work on a complete filtered probability space with time horizon , and refer to as the physical (or real-world) probability measure. On this space we introduce families of so-called Lévy-Itô processes. For aspects of the theory of such processes see [1, 17, 4]. Here, we consider an -dimensional -Brownian motion and independent Poisson random measures (PRM) , , , associated with one-dimensional independent Lévy processes with finite second moments for all . Further, we denote by the compensator of and by the compensated measure.111In the present framework can be written as and we use them interchangeably. That is, for any , is the compensator associated with and the compensated random measure under .

We consider an -dimensional stochastic process starting at and which evolves according to the stochastic differential equation (SDE) under

| (1) |

where , , and satisfy the standing Assumption 2.1 below. Equation (1) is the matrix notation meaning that the -th component of satisfies the SDE under

with , , and , for and . For , we use the notation to refer to the -th column of . Furthermore, we assume that each column , , depends on only through , i.e., .

Throughout we use the following notation. For a function we write for the vector of its partial derivatives and for the Hessian matrix of (mixed) second derivatives. We further define

| (2a) | ||||

| (2b) | ||||

The next assumption guarantees that the stochastic process given in (1) is well-defined.

Assumption 2.1.

The functions , , and satisfy the usual linear growth and Lipschitz continuity conditions. That is for all and there exists such that

where is the Euclidean norm and the Frobenius norm. Moreover, for all , , and there exists such that

As a consequence of Assumption 2.1 and by Theorem 1.19 in [17], there exists a unique càdlàg adapted process starting at that satisfies the SDE in (1); we refer to that process as this unique càdlàg solution . Moreover, it holds for all that

We use the Kullback-Leibler (KL) divergence also called relative entropy to quantify the distance between probability measures. Recall that the KL-divergence of a probability measure with respect to is given by

where we use the convention that . For a probability measures we write when we consider the -expectation and for notational simplicity set .

Now we are ready to formally introduce the optimisation problem which we will solve in the subsequent sections.

Optimisation 2.2.

For functions and constants , with , , we consider the optimisation problem

| () | ||||

where the infimum is taken over probability measures that are absolutely continuous with respect to .

For and , we call the equations and constraints, and and constraint functions.

Before solving the optimisation problem () we study the following closely related problem. Specifically, we consider optimisation problem () however seek only over a subset of equivalent probability measures – the set of equivalent probability measures characterised by Doléans-Dade exponentials. For this, we define the following sets of stochastic processes:

and

Here stands for the Hadamard product for vectors, which is defined for by , and the inequality is to be understood componentwise. For and , we define the process , given for by

| (3) | ||||

where . This process is a Doléans-Dade exponential and with, e.g., the Novikov assumption, defines a Radon-Nikodym (RN) derivative. We recall the Novikov’s condition on which is

and which establishes sufficient conditions on and such that and is a martingale. Thus, the measure characterised by the RN-derivative

is a probability measure that is absolutely continuous with respect to ; see Theorem 1.36 in [17]. We denote the probability measure by subscripts to indicates that it arises from an -valued process and an -valued random field .

With the above definitions we are ready to introduce a subset of absolutely continuous probability measures with respect to given in (), that are characterised by RN-densities with and

| (4) |

Note that we do not assume Novikov’s condition in (4).

Using the above class of equivalent probability measures, we consider the following optimisation problem, which is optimisation problem () but where we seek over the subset of probability measures .

Optimisation 2.3.

For functions and constants , with , , we consider the optimisation problem

| () | ||||

For , and as a consequence of Girsanov’s Theorem, defined by

is an -dimensional -Brownian motion and the -compensator of is

For notational simplicity we write and as they only explicitly depend on and , respectively.

Using the above results, the KL-divergence from to becomes

Next, we discuss assumptions needed for the existence and uniqueness of the Lagrangian associated with optimisation problem (), which we introduce in the next section. For this we first define the moment generating function (mgf) and the cumulant generating function (cgf) for random vectors. For a random vector , , we define the set

where denotes the interior of a set. We note that is the interior of a convex set. If , then the mgf and cgf of at exist and are respectively given by

Assumption 2.4.

Let denote the -dimensional random vector given by

where , , and constants , and . Here the integral in is understood to be applied componentwise. We assume that and that there exists such that

| (5) |

2.2 Candidate Solution and Verification

We proceed with a formal derivation of a candidate for the value function associated with the constrained optimisation problem (). After, we provide a verification theorem that allows us to conclude that the candidate solution is indeed the value function.

Let with and , then the Lagrangian of the constrained problem () with Lagrange multipliers and is given by

where denotes the dot product. We define for a fixed control pair , the value associated with the Lagrangian by

| (6) |

where denotes the -expectation conditioned on the event . Observe that the expectation in (6) is finite because of the definition of – recall that . We further define the optimal value function, which we often just refer to as the value function, by

| (7) |

For the purposes of the formal derivation we assume that the infimum in (7) is finite. We observe that as a consequence of the dynamic programming principle and Itô’s formula – under the assumption that – we have the following dynamic programming equation (DPE)

| (8) |

where the linear operator is the -generator of , and acts on functions as follows

where is defined in (2). The specific form of the DPE follows from writing (1) in terms of and , so that

The measurable global minimisers and (in feedback form) of the infimum in (8) are given by

where stands for .

It follows immediately that is componentwise bounded from above by unity. Inserting the optimal controls and in feedback form back into the DPE (8) (omitting the arguments when possible) we obtain that

| (9) |

together with the terminal condition . We observe that (9) can be written as

| (10) |

where the linear operator is the -generator of the continuous part222The continuous part of is defined by , , where . of and acts on functions as follows

Next, we construct a candidate of the solution to (10) by introducing the change of variables . Hence,

and furthermore . Equation (10) thus becomes

| (11) |

with . Multiplying (11) by , we have that

where we use the fact that

By the Feynman-Kac representation, we conclude that can be written as

The above formal calculations provide the following candidate solution for the value function.

Proposition 2.5.

A candidate solution to the value function (7) is given by

with the optimal Markovian controls given by

Next, we prove that, under certain conditions and for fixed Lagrange multipliers, this candidate solution does indeed coincide with the value function.

Theorem 2.6 (Verification).

Under Assumption 2.1, let and . Define

where

| (12) |

and suppose that with having at most quadratic growth, i.e., there is such that . Let

| (13a) | ||||

| (13b) | ||||

and assume that

| (14) |

| (15) |

and

| (16) |

Then, and are admissible controls and .

Proof.

Note that (14) and (16) are sufficient to guarantee that and are admissible and that they induce a measure that is well-defined – this is a consequence of Novikov’s condition and the definition of . Next, we observe that

Then, for arbitrary s.t. , , and a stopping time , for , we use Dynkin’s formula to obtain

and as

we conclude that

Since we have that

where we used that for . Similarly, by (15)

Finally, using the quadratic growth condition imposed on , we have

and the right hand side of the inequality is integrable with respect to because . Thus, as a consequence of the dominated convergence theorem, we can take the limit when to obtain for all

and by continuity of , as we send , we obtain

After rearranging the above equation we have that , and as a consequence of the arbitrariness of and , we obtain .

Finally, using a similar localisation technique as above, this time with and corresponding measure , and since it holds by construction that

we have that

Therefore, after rearranging, we have that . Combining both inequalities we obtain that which concludes the proof. ∎

We introduce the notation to refer to the measure change induced by choosing as in (13).

2.3 Representation of RN-density

The next result shows that for with carefully chosen and , the corresponding RN-density of has an alternative representation. This leads to a simple representation of the RN-density that characterises a solution to , see Corollary 2.8.

Theorem 2.7 (Representation of RN-density).

Let Assumption 2.1 be fulfilled. Let be given in (3) with specifically chosen to be

where is

with and for some such that , and is and such that for .333From this property, it follows that , and . In fact, a simple calculation shows that is of the form for some constant . We assume that and are such that and

| (17) |

Then, we have, for all , that

and, noting that and ,

Proof.

For simplicity we drop the superscripts of and just write . By (17) we have that is a martingale and thus for , where . As is a stochastic exponential, from Itô’s lemma, we have that

| (18) |

Next, we observe that the process

is a martingale. Given that , it follows that satisfies the following SDE

and as is a martingale, we have the following identity

| (19) |

Next, we introduce the process , which can be written as where , and

Thus, by the multidimensional Lévy-Itô formula, we have that (we omit the arguments of the functions when there is no confusion)

and using the identity in (19) we have

| (20) |

Next, define the process for . We claim that for all for some constant . To see this, note that

which after direct substitution, using (20), (18), and the formula for , we have

As and , after a short calculation we find that cancels with . Similarly, cancels with by factoring out of the operator. Then, it follows that reduces to

| (21) |

Note that (as and ), hence , and thus

Using this relationship, the and terms in (21) cancel, in which case we have

From the definition of , we see that and cancel. Finally we have

The last equality follows by collecting like terms in the preceding lines. Thus, for all , and some . As and , it follows that

from which we obtain the required results

∎

Corollary 2.8.

Proof.

Note that the above corollary states that the RN-density is a function only of the terminal value of the processes and the running costs . Thus, even though the RN-density was characterised by the stochastic process and the random vector field , it has a representation where it does not (explicitly) depend on them. As we show in the next subsection, an optimal RN-density which attains the infimum in the optimisation problem () will be of the form (22) for some and and moreover it will indirectly depend on them through the constraints.

2.4 Solution to Optimisation Problems () and ()

In this section, we present the solution to the control problem () and show that, if the solution exists, it is also the unique the constrained optimisation problem (). The next result states the solution to the optimisation problem ().

Theorem 2.9 (Solution to ()).

Let Assumptions 2.1 and 2.4 be fulfilled and suppose that , are as in Theorem 2.6, with Lagrange multipliers solving Equation (5), and satisfy its assumptions. Then, there exits a solution to () which is given in Corollary 2.8 with optimal Lagrange multipliers and where , generate the measure change.

Proof.

For fixed , we take , , and as given in (12) and (13). Denote the corresponding measure by . Recall that . Then we may rewrite the constraints as

| (23) | ||||

By Corollary 2.8 we further have that

which allows to rewrite the set of equations (23) as

The above set of equations can be compactly written as the system of equations

which, by Assumption 2.4, has a solution, denoted here by . Further, if for this choice of Lagrange multipliers, the assumptions in Theorem 2.6 are satisfied then, by Theorem 2.6, the corresponding optimal controls are attainable and generate the required measure change . ∎

Proposition 2.10 (SDE under ).

Proof.

This follows immediately from Girsanov’s Theorem and by writing (1) in terms of and . ∎

Proof.

By Theorem 2.9 a solution to optimisation problem () is where , , and are as in Theorem 2.6 with Lagrange multipliers solving Equation (5). By Corollary 2.8 (multiplying and dividing by the constants), we have that

Next, let be any probability measure that is absolutely continuous with respect to and under which the constraints are fulfilled. Then, observe that

Using the above equality, the KL-divergence from to can be bounded below as follows

Thus, is indeed a solution to (). Uniqueness of the solution to () follows by strict convexity of the KL-divergence, which implies uniqueness of (). ∎

3 Analytically Tractable Examples

In this section we provide examples illustrating how the dynamics of processes change when moving from to . First, we discuss the sign of the optimal Lagrange multiplier under one single constraint. Second, we consider how the solution to the optimisation problem () is connected to pinned measures. Third, we provide explicit expressions for the Lagrange multipliers and the optimal RN-density under two VaR constraints. Forth, we consider a constraint on the mean when the underlying process has independent increments. Finally, we study how a Brownian motion is perturbed when we keep its mean equal to 0 but alter its standard deviation.

3.1 Sign of Lagrange multiplier for Single Constraint

For the case when there is only one constraint, i.e., , , or , , we can specify the sign of the Lagrange multiplier. For simplicity we assume that however the following proposition also holds for one running cost constraint.

Proposition 3.1 (Sign of Lagrange multiplier).

Proof.

Using the optimal RN-density given in Corollary 2.8, the optimal Lagrange multiplier fulfils

As the derivative of a cgf of a random variable , , is strictly increasing in its argument , we have that is strictly decreasing in . Moreover,

Clearly, if the rhs vanishes, then . Further, if , we must have . Similarly, if , we must have . ∎

The above proposition states that a constraint , i.e., an increase in the expected value of from to , corresponds to a negative optimal Lagrange multiplier. Similarly, if the expected value of is decreased from to , then is positive.

3.2 Pinned Measures

Consider a Borel measurable set and the constraint function which results in the constraint , where we choose , . For each , the optimal probability measures is

| (24) |

where and is such that the constraint is binding. We include the subscript index on as we aim to consider the limiting measure for . By enforcing the constraint, we have that

which gives

| (25) |

Substituting (25) into Equation (24), the RN-density becomes

The limiting measure induced by the RN-density coincides with the so-called pinned measures. Pinned measures are those for which the terminal value of the process must lie within the set . Note this limiting measure is not equivalent to , but absolutely continuous .

3.3 VaR Constraints

We consider the constraint functions and with such that and . The corresponding constraints are , , , which are Value-at-Risk444For a univariate random variable and a probability measure , the -Value-at-Risk at level is defined as . For simplicity of notation we write . (VaR) constraints at levels if the -distribution of is continuous. Next, we rewrite the second constraint as

and by Corollary 2.8 the RN-density for fixed Lagrange multipliers becomes

| (26) |

where is the normalising constant. Further, the optimal Lagrange multipliers and satisfy

Inserting this into (26) the optimal RN-density is

Moreover, the optimal Lagrange multipliers are given by

and the normalising constant simplifies to .

3.4 Linear Constraint Function for Process with Independent Increments

For simplicity we consider a one-dimensional process and a linear constraint function. That is, we let be the solution to the SDE under

where is a one-dimensional -Brownian motion, the Poisson random measure describing Poisson arrivals of independent and identically distributed marks, and . We consider optimisation problem () with a constraint on the expected value of , i.e. , . Note that this constraint encompasses linear constraint functions , with , , as, for this choice of , the constraint is equivalent to .

From Theorem 2.6 for fixed Lagrange multiplier , and as has independent increments, we have

We note that and that , induce .

If we further assume that where is the rate parameter of the Poisson process and is the distribution function of the marks – here is the distribution function of a standard normal random variable. Then, for fixed and the constraint equation becomes (after some calculations)

| (27) |

where and . The optimal Lagrange multiplier that binds the constraint exists since the lhs of (27) is continuous in and diverges to for and diverges to for . Uniqueness of follows by uniqueness of the solution to ().

3.5 Brownian Motion with Arbitrary Variance

Let , , be a one-dimensional -Brownian motion and consider the constraints and , for , . Note that since and the constraints result that under the optimal probability measure, the mean of is kept fixed to its value while the variance is scaled by . For Lagrange multipliers we have by Theorem 2.6 that

Therefore, satisfies the following SDE under

where is a -Brownian motion, , and with to be determined to bind the constraints. By employing Itô’s formula on the process

we obtain that

As the coefficient of the Itô integral is deterministic, is normally distributed, and as the Itô integral has zero -mean, we see that to enforce the mean constraint. Using Itô’s isometry we find that is required to enforce the variance constraint. Note that if – a reduction of the variance under –, then , which implies that the process mean-reverts around zero to reduce the variance; similarly, if – an increase of the variance under –, then , which implies that the process is mean-avoiding to increase the variance. Finally, under the optimal measure the process satisfies the SDE

where is a -Brownian motion. The above SDE shows that is a Ornstein-Uhlenbeck process. Note the coefficient of the drift remains finite for all .

4 Infinitesimal Perturbations

In this section we consider small perturbations, that is constraints where the -expectations equal their -expectations plus , where is the direction of the perturbation and is small. We prove, in this setup, that the optimal Lagrange multiplier is, up to order , the inverse of the -covariance matrix of the constraint functions multiplied by and the direction of the perturbation. Using the results on infinitesimal perturbations, we define a directional derivative – termed entropic derivative – of risk functionals in the direction of least relative entropy in Section 4.2.

4.1 Optimal Lagrange Multiplier

For functions with and , we define the random vector

| (28) | ||||

We assume throughout this section that , where denotes the -covariance, for all . Using the above notation, we state the optimisation problem concerning infinitesimal perturbations.

Optimisation 4.1.

For , , and a random vector given in (28), we consider the optimisation problem

| () |

where the constraints are understood as a system of equations.

If a solution to optimisation problem () exists, we denote the probability measure attaining the infimum by . This probability measure may be viewed as arising from small perturbations of in direction of . The next result shows that the optimal Lagrange multiplier is, up to , equal to the inverse of the -covariance matrix of the constraint functions multiplied by and the direction of the perturbation . We first prove this result for a single constraint and then, using slightly stronger assumptions, for a collection of constraints.

Theorem 4.2 (Single Constraint).

Let , and write , i.e. we only consider one constraint, and assume that satisfies . Under the Assumptions of Theorem 2.9, the optimisation problem () has a unique solution with Lagrange multiplier satisfying

where denotes the -variance of . Moreover, the KL-divergence of with respect to is

Proof.

By Theorem 2.9, the solution to problem () is

where the Lagrange multiplier solves the equation . Let , where and is the error term satisfying . Then for to bind the constraint, we require that

| (29) |

where we set the random variable . Next, we show that is an error term of order . For this we first apply the Taylor theorem to calculate the Taylor approximation of around , and obtain that for all

where the random variable is the error term of the Taylor approximation of and (potentially depending on ) lies between and . Inserting the expansion of into (29) we obtain

Noting that , the above becomes

| (30) |

Using the Lagrange form of the error term, we may write

where we set , where is the second derivative of with respect to . Note that is continuous so that . Moreover, calculations show that which by assumption implies that and .

Therefore, Equation (30) admits the quadratic form

which has solutions

Note that the positive root, , is not a viable solution since is satisfies

which contradicts that must converge to 0 as . For the negative root, , we apply Taylor’s theorem for , and obtain, recall that ,

Thus, indeed .

Next, we calculate the RN-density. For this we first use Taylor’s theorems for , and then, in the third equation, Taylor’s theorem for ,

Finally, we calculate the KL-divergence, using Taylor’s theorem for ,

∎

We prove the result for multiple constraints using a different proof which requires slightly stronger assumptions.

Theorem 4.3 (Multiple Constraints).

Let the Assumptions of Theorem 2.9 be fulfilled. Further, assume that the Lagrange multiplier corresponding to optimisation problem () is component-wise differentiable in and that for all . Then, optimisation problem () has a unique solution with Lagrange multiplier satisfying

where the matrix has components , . Furthermore, the KL-divergence of with respect to is

Proof.

By Theorem 2.9, the solution to problem () is

where the Lagrange multipliers solve the system of equations . The constraints impose that for all

| (31) |

where the random variable for . Let , where , , is the error term satisfying component-wise . Next, we show that is of order . For this we first apply Taylor’s theorem to calculate the Taylor approximation of . Indeed, for all

| (32) |

where the random variable is the error term of the Taylor approximation of , i.e. in integral form

where . Inserting (32), the expansion of , into (31) we obtain for all

| (33) |

Note that , where is the -th row of , and . Thus, Equation (33) becomes

| (34) |

Note that

where

and . Next, define the matrix whose entries are . Taking derivative of (34) with respect to , then stacking the equations and isolating for , we have

Further, after some tedious computations, and defining ,

Hence, under the assumption of bounded fourth moments, and applying L’Hôpital’s rule, we obtain (component-wise)

which implies that .

To calculate the KL-divergence, we first calculate the RN-density, using similar steps to the proof of Theorem 4.2,

Thus, the KL-divergence becomes

which concludes the proof. ∎

4.2 Entropic Derivative

In this section, we define a derivative of a risk functional along constraints in the direction of least relative entropy. For this we use the same notation as in Section 4.1 and denote by a vector of constraints given in (28) and by the direction of the derivative.

Definition 4.4 (Entropic Derivative).

Let be a random vector with representation as in (28) and . Then the entropic derivative of an -measureable random variable in direction along the constraint at time is

The entropic derivative is 1-homogeneous, in that for all , and additive, i.e. , for all -measureable random variables. Furthermore, the entropic derivative satisfies for all , if and are independent; a result following from the next proposition.

Proposition 4.5.

The entropic derivative of in direction of along the constraint at time has representation

At time , the derivative may be written as

Proof.

Using Theorem 4.3 and in particular the approximation of , we have for

The representation for follows by noting that . ∎

Next, we provide an example of an entropic risk measure and relate it to the sensitivity of the Tail-Value-at-Risk (TVaR) to a sub-portfolio. Recall that for a random variable and a probability measures , the -TVaR at level is defined as

where the -quantile function of is given by . For simplicity of notation, we write

Example (TVaR Sensitivity).

Suppose we have the process and consider , where , and . For simplicitly assume that the quantile function of is continuous around , then the constraint corresponds to a small perturbation constraint of

Moreover, the entropic derivative of in direction along at time is

where . In particular, if and for , we obtain

We note that is the sensitivity of TVaR in direction of sub-portfolio ; see e.g. [12].

Next, we generalise the entropic derivative to the class of distortion risk measures, which subsumes TVaR. First introduced by [24], distortion risk measures include a wide range of risk measures used in financial risk management and behavioural economics.

Definition 4.6 (Distortion Risk Measures).

For a function with , the distortion risk measure of a random variable with weight function under a probability measure is given by

We set . A distortion risk measure satisfies the properties of coherence if the distortion weight function is non-decreasing [15].

Proposition 4.7 (Distortion Risk Measures).

Let be a distortion risk measure under and a absolutely continuous -measurable random variable with support . Then the entropic derivative of the distortion risk measure of in direction along the constraint at time is

where .

Proof.

Note that the -distortion risk measures can be written as an expectation under the reference probability

where is a standard uniform random variable under . Using this representation, the derivative becomes

Next, we calculate the derivative of the -quantile function of with respect to . For this, note that for all , differentiating the equation gives

| (35) |

where is the -density of . To simplify (35), we calculate the -distribution function of using the approximation of in Theorem 4.3

and thus (35) becomes

Collecting, and using a change of variable in the second equation, we have

∎

Example.

(Sensitivity for Distortion Risk Measures) Consider the one-dimensional process and a constraint satisfying -a.s. and . Thus, we can write which is a distorted distribution function of .

Then the entropic derivative of a distortion risk measure of in direction along the constraint at time is

where the last equality follows from Proposition 4.2 in [20] and where and is a -uniform comonontonic to , i.e. , and , . We note that is the sensitivity of a distortion risk measure to for a perturbation with the mixture distribution to , see Proposition 4.2 in [20]. We refer to [20] for a discussion on differential sensitivities to distortion risk measures.

5 Numerical Example

In this section, we illustrate how our methodology may be applied in practice. In particular, for simplicity of exposition, we assume that is a one-dimensional Itô process, which more specifically satisfies the SDE under

| (36) |

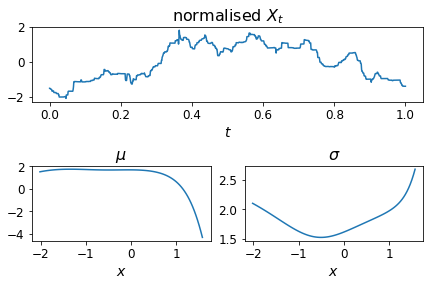

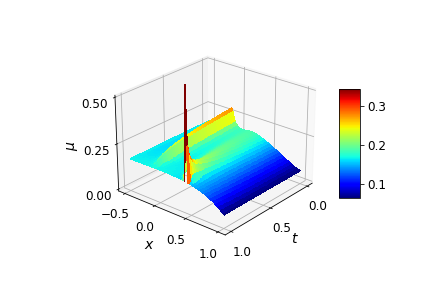

where and are parameterised by artificial neural networks. We estimate and using maximum likelihood estimation (MLE) based on an Euler discretisation of the SDE (36). The data is from an automatic marker making (AMM) pool known as sushi-swap for the USDC-WETH cryptocurrency pair, and represents the price of exchanging one USDC for -WETH. We normalise prices by shifting and scaling them using the mean and standard deviation of the sample path. The data considered is for the entire day of June 29, 2021, and Figure 1 shows the normalised data and the estimated drift and volatility functions. The estimation of and seen in the figure illustrate that as prices increase, the volatility increases while the drift decreases.

A trader may have a specific view on, e.g., the expected return in the cryptocurrency pool and / or the expected time that prices spend below some level. Using the methodology we developed in this paper, the trader then wishes to update the model estimated on historical data to reflect their beliefs. Hence, with and estimated (under ), and a specified set of constraints, the trader proceeds to estimate the optimal measure using the algorithmic steps shown in Algorithm 1.

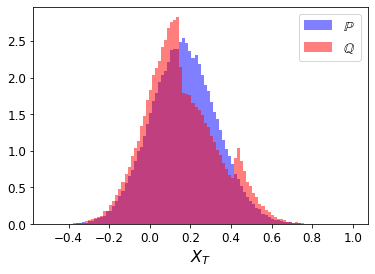

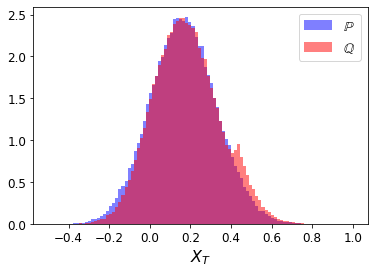

We consider two numerical examples (i) we increase by 10% and decrease by 10%, and (ii) we increase the by 10% and reduce the average time spent below the barrier by 50%; all percentages are relative to their values under the reference measure . The constraints are induced by constraint functions with constraint constants , i.e. , and where are the VaR values under . The average time time spent below a barrier is achieved by imposing a running cost constraint. To this end, define

Thus, the constraint

corresponds to constraining the average time spent below the barrier to be equal to .

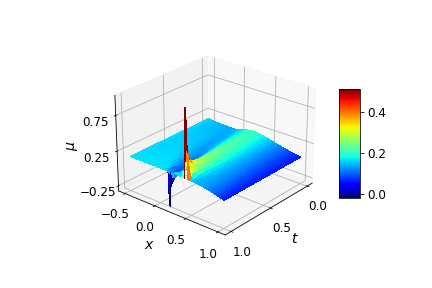

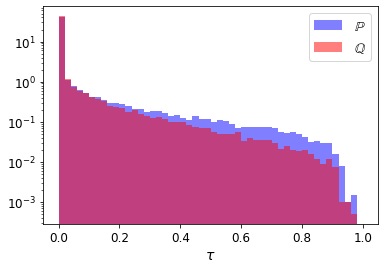

We first investigate the case of the two VaR constraints, example (i). The histogram of under the reference measure and the optimal measure is show in the left panel of Figure 2. From the left panel, we observe, when comparing the distribution of under with , that probability mass from the centre of the distribution is pushed into the left and right tails to ensure that the median is reduced and the 90%-quantile is increased. The right panel of Figure 2 shows the drift under . Recall that under the drift is a function of the process only – see (36); under , however, the drift depends on the value of the process and on time. From the right panel of Figure 2, we observe that the probability mass transport seen in the histograms of in the left panel, is achieved by having excess positive / negative drift to the right / left of the original median value. Moreover, we see upward / downward spikes at the locations of the new quantiles whose intensity increases as the terminal time approaches.

Next, we next investigate the case of a 10% increasing in the 90%-quantile and a 50% reduction the average time spent below the barrier, i.e., example (ii). The right top panel of Figure 3 displays the histogram of under the reference and optimal measure . The figure shows that under , the amount of time spent below the barrier is more concentrated towards zero than it is under the reference measure. The top left panel shows the histogram of , and while under the 90%-quantile is increased, which is seen by the additional mass in the right tail, the running cost constraint moves mass away from the left tail. The bottom panel of the figure shows the drift under . We observe that as the process crosses to negative values, it receives a positive drift which prevents the process from spending additional time below the barrier. The process also receives a drift if it approaches the target quantile whose intensity increases as the terminal time approaches.

[Acknowledgments]

SJ and SP acknowledge support from the Natural Sciences and Engineering Research Council of Canada (grants RGPIN-2018-05705, RGPAS-2018-522715, and DGECR-2020-00333, RGPIN-2020-04289). We are grateful to L. P. Hughston for helpful comments.

References

- [1] {bbook}[author] \bauthor\bsnmApplebaum, \bfnmDavid\binitsD. (\byear2009). \btitleLévy Processes and Stochastic Calculus. \bpublisherCambridge University Press. \endbibitem

- [2] {barticle}[author] \bauthor\bsnmAvellaneda, \bfnmMarco\binitsM. (\byear1998). \btitleMinimum-relative-entropy calibration of asset-pricing models. \bjournalInternational Journal of Theoretical and Applied Finance \bvolume1 \bpages447–472. \endbibitem

- [3] {barticle}[author] \bauthor\bsnmAvellaneda, \bfnmMarco\binitsM., \bauthor\bsnmFriedman, \bfnmCraig\binitsC., \bauthor\bsnmHolmes, \bfnmRichard\binitsR. and \bauthor\bsnmSamperi, \bfnmDominick\binitsD. (\byear1997). \btitleCalibrating volatility surfaces via relative-entropy minimization. \bjournalApplied Mathematical Finance \bvolume4 \bpages37–64. \endbibitem

- [4] {barticle}[author] \bauthor\bsnmBouzianis, \bfnmGeorge\binitsG., \bauthor\bsnmHughston, \bfnmLane P\binitsL. P., \bauthor\bsnmJaimungal, \bfnmSebastian\binitsS. and \bauthor\bsnmSánchez-Betancourt, \bfnmLeandro\binitsL. (\byear2021). \btitleLévy-Ito models in finance. \bjournalProbability Surveys \bvolume18 \bpages132–178. \endbibitem

- [5] {barticle}[author] \bauthor\bsnmBreuer, \bfnmThomas\binitsT. and \bauthor\bsnmCsiszár, \bfnmImre\binitsI. (\byear2016). \btitleMeasuring distribution model risk. \bjournalMathematical Finance \bvolume26 \bpages395–411. \endbibitem

- [6] {barticle}[author] \bauthor\bsnmCont, \bfnmRama\binitsR. and \bauthor\bsnmTankov, \bfnmPeter\binitsP. (\byear2004). \btitleNonparametric calibration of jump-diffusion option pricing models. \bjournalThe Journal of Computational Finance \bvolume7 \bpages1–49. \endbibitem

- [7] {barticle}[author] \bauthor\bsnmCsiszár, \bfnmImre\binitsI. (\byear1975). \btitleI-divergence geometry of probability distributions and minimization problems. \bjournalThe Annals of Probability \bpages146–158. \endbibitem

- [8] {barticle}[author] \bauthor\bsnmDe Cezaro, \bfnmA\binitsA., \bauthor\bsnmScherzer, \bfnmO\binitsO. and \bauthor\bsnmZubelli, \bfnmJP\binitsJ. (\byear2012). \btitleConvex regularization of local volatility models from option prices: convergence analysis and rates. \bjournalNonlinear Analysis: Theory, Methods & Applications \bvolume75 \bpages2398–2415. \endbibitem

- [9] {barticle}[author] \bauthor\bsnmDupuis, \bfnmPaul\binitsP., \bauthor\bsnmKatsoulakis, \bfnmMarkos A\binitsM. A., \bauthor\bsnmPantazis, \bfnmYannis\binitsY. and \bauthor\bsnmRey-Bellet, \bfnmLuc\binitsL. (\byear2020). \btitleSensitivity analysis for rare events based on Rényi divergence. \bjournalThe Annals of Applied Probability \bvolume30 \bpages1507–1533. \endbibitem

- [10] {barticle}[author] \bauthor\bsnmFradkov, \bfnmAlexander\binitsA. (\byear2008). \btitleSpeed-gradient entropy principle for nonstationary processes. \bjournalEntropy \bvolume10 \bpages757–764. \endbibitem

- [11] {barticle}[author] \bauthor\bsnmGlasserman, \bfnmPaul\binitsP. and \bauthor\bsnmXu, \bfnmXingbo\binitsX. (\byear2014). \btitleRobust risk measurement and model risk. \bjournalQuantitative Finance \bvolume14 \bpages29–58. \endbibitem

- [12] {barticle}[author] \bauthor\bsnmHong, \bfnmL Jeff\binitsL. J. and \bauthor\bsnmLiu, \bfnmGuangwu\binitsG. (\byear2009). \btitleSimulating sensitivities of conditional value at risk. \bjournalManagement Science \bvolume55 \bpages281–293. \endbibitem

- [13] {barticle}[author] \bauthor\bsnmJaynes, \bfnmEdwin T\binitsE. T. (\byear1957). \btitleInformation theory and statistical mechanics. \bjournalPhysical review \bvolume106 \bpages620. \endbibitem

- [14] {barticle}[author] \bauthor\bsnmJeanblanc, \bfnmMonique\binitsM., \bauthor\bsnmKlöppel, \bfnmSusanne\binitsS. and \bauthor\bsnmMiyahara, \bfnmYoshio\binitsY. (\byear2007). \btitleMinimal measures for exponential Lévy processes. \bjournalThe Annals of Applied Probability \bvolume17 \bpages1615–1638. \endbibitem

- [15] {bincollection}[author] \bauthor\bsnmKusuoka, \bfnmShigeo\binitsS. (\byear2001). \btitleOn law invariant coherent risk measures. In \bbooktitleAdvances in Mathematical Economics \bpages83–95. \bpublisherSpringer. \endbibitem

- [16] {barticle}[author] \bauthor\bsnmLam, \bfnmHenry\binitsH. (\byear2016). \btitleRobust sensitivity analysis for stochastic systems. \bjournalMathematics of Operations Research \bvolume41 \bpages1248–1275. \endbibitem

- [17] {bbook}[author] \bauthor\bsnmØksendal, \bfnmBernt\binitsB. and \bauthor\bsnmSulem, \bfnmAgnès\binitsA. (\byear2019). \btitleApplied Stochastic Control of Jump Diffusions. \bpublisherSpringer. \endbibitem

- [18] {barticle}[author] \bauthor\bsnmParrondo, \bfnmJuan MR\binitsJ. M., \bauthor\bparticleVan den \bsnmBroeck, \bfnmChristian\binitsC. and \bauthor\bsnmKawai, \bfnmRyoichi\binitsR. (\byear2009). \btitleEntropy production and the arrow of time. \bjournalNew Journal of Physics \bvolume11 \bpages073008. \endbibitem

- [19] {barticle}[author] \bauthor\bsnmPesenti, \bfnmSilvana M\binitsS. M., \bauthor\bsnmMillossovich, \bfnmPietro\binitsP. and \bauthor\bsnmTsanakas, \bfnmAndreas\binitsA. (\byear2019). \btitleReverse sensitivity testing: What does it take to break the model? \bjournalEuropean Journal of Operational Research \bvolume274 \bpages654–670. \endbibitem

- [20] {barticle}[author] \bauthor\bsnmPesenti, \bfnmSilvana M\binitsS. M., \bauthor\bsnmMillossovich, \bfnmPietro\binitsP. and \bauthor\bsnmTsanakas, \bfnmAndreas\binitsA. (\byear2021). \btitleCascade sensitivity measures. \bjournalRisk Analysis \bvolume41 \bpages2392–2414. \endbibitem

- [21] {barticle}[author] \bauthor\bsnmSchweizer, \bfnmMartin\binitsM. (\byear1992). \btitleMean-variance hedging for general claims. \bjournalThe Annals of Applied Probability \bvolume2 \bpages171–179. \endbibitem

- [22] {barticle}[author] \bauthor\bsnmShalymov, \bfnmDmitry\binitsD., \bauthor\bsnmFradkov, \bfnmAlexander\binitsA., \bauthor\bsnmLiubchich, \bfnmSvetlana\binitsS. and \bauthor\bsnmSokolov, \bfnmBoris\binitsB. (\byear2017). \btitleDynamics of the relative entropy minimization processes. \bjournalCybernetics and physics \bvolume6 \bpages80–87. \endbibitem

- [23] {barticle}[author] \bauthor\bsnmVajda, \bfnmIgor\binitsI. (\byear1990). \btitleDistances and discrimination rates for stochastic processes. \bjournalStochastic Processes and their Applications \bvolume35 \bpages47–57. \endbibitem

- [24] {barticle}[author] \bauthor\bsnmYaari, \bfnmMenahem E\binitsM. E. (\byear1987). \btitleThe dual theory of choice under risk. \bjournalEconometrica: Journal of the Econometric Society \bpages95–115. \endbibitem