A Poor Agent and Subsidy: An investigation through CCM Model

Abstract

In this work, the dynamics of agents below a threshold line in some modified CCM type kinetic wealth exchange models are studied. These agents are eligible for subsidy as can be seen in any real economy. An interaction is prohibited if both of the interacting agents’ wealth fall below the threshold line. A walk for such agents can be conceived in the abstract Gain-Loss Space(GLS) and is macroscopically compared to a lazy walk. The effect of giving subsidy once to such agents is checked over giving repeated subsidy from the point of view of the walk in GLS. It is seen that the walk has more positive drift if the subsidy is given once. The correlations and other interesting quantities are studied.

I Introduction

In any economy the distribution of wealth among individuals follows a pattern for large values of wealth , to be specific, it decays as for large where is called the Pareto exponent [1]. Pareto exponent usually varies between and [2, 3, 4, 5, 6, 7, 8, 9]. A number of models have been proposed to reproduce the observed features of an economy [10, 11, 12, 13, 14]. One important objective of several such econophysical models is to reproduce the Pareto tail in the wealth/income distribution. Some of the models were inspired by the kinetic theory of gases which derives the average macroscopic behaviour from the microscopic interactions among molecules. In these models traders/agents are treated as molecules of gas. A typical trading process between two such traders/agents maintaining local conservation of wealth can be compared to an interaction between two gas molecules maintaining local energy conservation in gas. These models follow a microcanonical description, i.e., the total wealth is a conserved quantity. Several such models are studied [3, 4, 15] where debt is allowed for a trader/agent. However, in our case we consider no agent can end up with a negative wealth, i.e., debt is not allowed in a trading.

Thus, if there are two agents and who before taking part in the trading had wealth

and respectively at time , will have wealths according to the following relations

at the next time step :

| (1) | ||||

There are several other models of the wealth distribution which do not consider the kinetic theory concept.

In [16], a very simple model of economy was discussed, where the time evolution

was described by an equation involving exchange between individuals and

random speculative trading in such a way that under an arbitrary change of monetary units

the fundamental symmetry of the economy

is obeyed.

A mean-field limit of this

equation was investigated there and the distribution of wealth came out to be of the Pareto type.

Another model is the Lotka-Volterra

model which is again a kind of mean field model where wealth of an agent at a particular time

depends on her/his wealth in the previous step as well as the average

wealth of all agents [17, 18]. Apart from these, there are other

models which depend on stochastic processes [19, 20]. The main problem in the last two type

models is that here wealth

exchange between agents is not allowed

and therefore cannot be realized as a real trading process. Although in [16], wealth exchange is

considered, according to the authors, it is again not a fully realistic one, as mean field concept is used.

In some models,

instead of considering binary collision-like trading, just as in case of a rarefied classical gas, simultaneous

multiple interactions are taken into account to model a socio-economic phenomena

in a multi-agent system [21].

In the gas-like models, the wealth exchange between agents follow the same rule as energy exchange between two gas

molecules in kinetic theory; that is why they are called kinetic wealth exchange models.

Bachelier in his PhD. thesis developed a ’theory of speculation’ [22],

where he suggested a practical connection between stochastic theory

and financial analysis.

The idea that velocity distribution for gas molecules and income distribution for agents

can be compared was first addressed in [23],

although no specific reason behind this was addressed. The

first simplest conservative model of this kind was proposed by

Dragulescu and Yakovenko (DY model) [11]. In that model, agents

randomly exchange wealth pairwise keeping the total wealth constant.

It is shown that the steady-state () wealth there follows a Boltzmann-Gibbs distribution:

; [13].

A modification to this model considering the fact that agents save a definite fraction of their wealth before

taking part in any trading, termed as saving propensity, was addressed first by Chakraborti

and Chakrabarti [12]

(CC model).

This results in a wealth

distribution close to Gamma distributions [24, 25] and is seen

to fit well to empirical data for low and middle wealth regime of an economy [8].

Later, a model was proposed by Chatterjee et. al. [26]

(CCM model) where distributed saving propensities were assumed for individuals.

The importance of the model is that it led to a wealth distribution

with a Pareto-tail. Apart from wealth distribution, people often study network like features in these models

[27, 28, 29, 30], a few of which address preferential interaction between agents. In [30]

it was considered that two agents will interact with more probability if their wealths are “close” or if

they have interacted before.

In a real economy, however, this preferential interaction often

depend on some other factors. Restriction in interaction may arise in some situations as we have recently

seen in the Pandemic situation. This type of restricted interaction is studied in [31].

Also during the economic crisis in Argentina during another restricted interaction was studied in [32].

There may be restriction in interaction for other reasons too.

It is known that

a poverty line exists in any economy [33, 34]. In various cases, the poverty line is estimated

near of the median of income[34]. People below the poverty line often get

subsidy from the Government. Also, it is a general notion that a person feels insecure if her/his

wealth falls below a specific level, may be termed as a threshold line.

In this work, a threshold line is introduced in an otherwise CCM like model, which is below

the defined poverty line in

an economy. The wealths of agents

are chosen from the uniform distribution and the total wealth is taken as .

The agents whose wealth are assigned below the threshold line are Below Threshold Line (BTL) agents. The subsidy

is given to the BTL agents in such a way that it can just promote

the agents above threshold line.

Once an agent is marked a BTL one, he/she remains eligible for subsidy always.

However, those who are

above the threshold line at the beginning are not getting any subsidy

even if their wealth fall below the threshold

line after a certain number of interactions.

Also an interaction will not occur at all if both the interacting agents are having wealth below the threshold line

because of human psychology of insecurity.

In some earlier works to study the dynamics of the transactions, a walk was conceived for the

agents in an abstract -D Gain-Loss space (GLS) [35, 36].

The corresponding walk was compared to a biased random walk.

In this work, we compare the walk of a tagged agent to a lazy random walk for different values of

saving propensity . The difference from earlier work is that, here a

tagged agent is a BTL one and except from moving Right/Left, the walker

may stay put to its position in the GLS if the interaction does not occur at all. It is seen that average distance

travelled in the GLS, i.e.,

for some . The value of is slightly different from what

we found in [36]. The wealth distribution and several other features

of the lazy walker are studied in this context. The objective of this study is to check whether there is any difference

in the agent’s upliftment in the wealth space

if the subsidy is given repeatedly to a BTL agent or only once.

II Model Description

We consider CCM model with agents. The total money is distributed randomly among the agents.

The key feature of CCM model is that here the saving propensities of agents are chosen from a uniform distribution.

The wealth exchange between two traders and can be represented as:

| (2) | ||||

Here are the saving propensities of agents respectively and is a random fraction related to stochastic nature of a trading process. In addition to this regular interaction, a threshold line is proposed here. We assumed the poverty line near of the average wealth of the economy as indicated in [34] and the threshold line is chosen below that. At the time of wealth assignment if an agent is found to be below the line she/he will be marked as BTL and a subsidy is assigned. As the wealths of agents are assigned from a uniform distribution the median is same as the average wealth. This means a certain fraction of the people will get subsidy. However, during course of interaction, an agent who is not a BTL one, falls below the threshold line she/he is not eligible for subsidy. Two types of models are studied here as follows:

-

•

Model A : For this, the BTL agents are stamped as “BTL” at the time of wealth assignment and the subsidy equal to is given to the BTL agents at the beginning of each configuration.

-

•

Model B : In this, again, some are stamped “BTL” at the beginning but the subsidy equal to is given to them at each Monte Carlo (MC) step, where one MC step consists of interactions. This means if a BTL agent goes above the threshold line after one or few MC steps, she/he is still eligible for subsidy (exactly as in any caste based system).

In both the cases, the subsidy given promotes the BTL agent above the threshold line , if the agent is below that. At every interaction, the wealths of the interacting agents are checked. An interaction is prohibited only if both of the interacting agents fall below the threshold line. In subsequent interactions, however, there is always a chance that such an agent is promoted above the line. The stationary state is obtained after a typical relaxation time and the distribution of wealth and the walk in the GLS are studied. It is to be noted that the subsidy here is given from the tax payed by the people above the threshold line. In this way, the economy is closed and total wealth remains conserved.

III Agent Dynamics

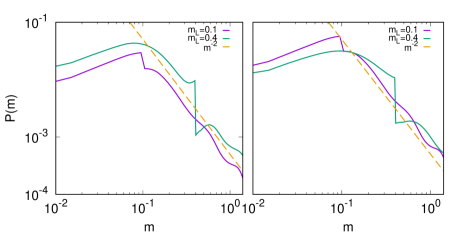

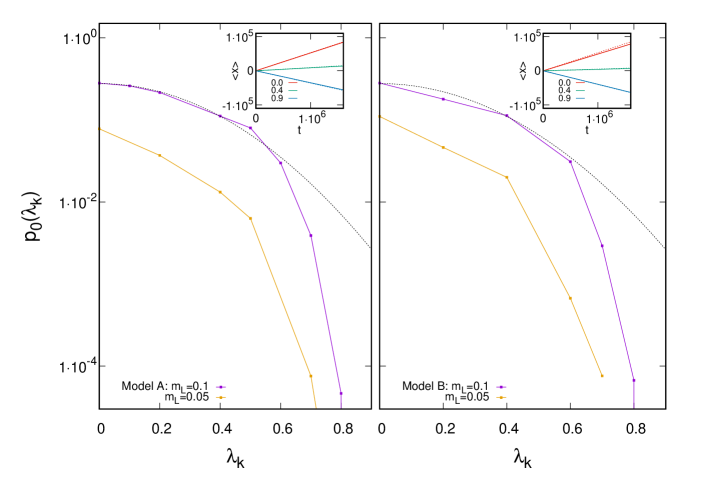

Although the actual form of wealth distribution depends on the form of saving propensity distribution, there is one thing common for all. The Pareto tail is present whatever be the form of the saving propensity distribution; the only difference is in the value of the exponent. Here, the saving propensities of all the agents are chosen from a uniform distribution which is the simplest one. Although in this work, we are actually interested in the dynamics of a tagged agent, the behaviour of overall distribution of wealth is also of great importance. The overall wealth distribution shows the Pareto exponent to be roughly as in case of conventional CCM model [13] except from the fact that near there is a sharp change in the profile. This behaviour can be understood by studying individual agent’s wealth distribution which will be addressed in the next section. The wealth distribution is shown in Fig. 1 for model A (Left) and model B (right) for two different .

We perform numerical simulation for a system of agents and look for the dynamics of a tagged agent who is a BTL one with a predefined saving propensity. As we have stated earlier we use two models, namely A and B, for assigning subsidy.

III.1 Wealth Distribution

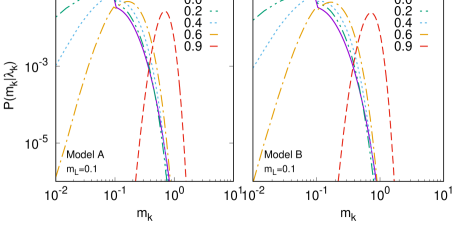

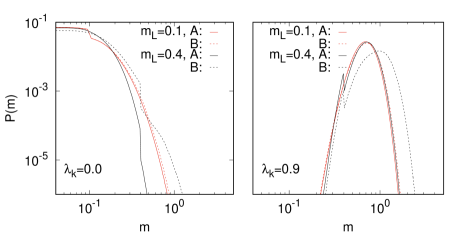

The distribution of wealth for different of the tagged BTL agent are shown in Fig. 2 for both the models A and B for . For both the cases the nature of wealth distribution is similar to what observed in [35] and earlier [13, 26] with the exception that as the tagged agent is a BTL one and she/he is assigned a wealth equal to , there is a higher probability near than what observed earlier. For small values of the agent has a small amount of wealth compared to the average wealth of the economy and for higher the wealth possessed by the agent is comparable to the average wealth. It is to be noted that as our agent is a BTL one, the average wealth she/he possessed is smaller compared to that predicted by the usual CCM model. As we increase to higher values, higher is more probable. The models A and B show similar distribution for all if is low but their nature is different for higher . It is seen that for higher threshold line the distribution for model B shifts to higher compared to model A. This can be understood easily. For model B, we are assigning the subsidy to BTL agents at every MC steps without checking whether they are below the threshold line or not. Therefore, higher value of wealth is more probable. This can also be realized from another aspect of the CCM model. When we set a higher , that means a larger number of agents is below that line compared to the case of a smaller . That means we are moving closer to the usual CCM picture where we choose an agent irrespective of the initial wealth possessed by her/him. These are shown in Fig. 3 for and for .

IV Walk in the GLS: Comparison to a Lazy Walker

To investigate the dynamics of this model in more detail at the microscopic level,

one may conceive a walk for the agents in the GLS.

It is well known that the usual CCM walk can be compared to a biased

random walk (BRW) whose forward bias decreases as we increase

from zero. The walk has no bias at a particular and then it decreases further and becomes negative

on increasing [35, 36]. The steps in those

studies were taken as Right/Left according to whether it is Gain/Loss.

In this study we are going to take a similar approach

for this CCM walk with a modification. Except for Gain and Loss, there is a third possibility.

When an agent

gains she/he moves a step towards Right and if she/he incurs a

loss moves a step towards Left. Apart from these two, the third possibility demands

that the BTL tagged agent may not interact

with another one if any one of them or both possesses a wealth less than and

therefore the corresponding walker may stay put at its position in the GLS.

The walks are correlated as when two

agents interact, if any one takes a right step, the other has to move towards left. Also if one is stay put,

the other should stay put too.

IV.1 Measurement of bias

For a lazy walker we know that it can have steps . It is obvious therefore that the CCM walk in this study can be

compared to a lazy walk. If the agent gains then the corresponding walker moves one step to

the right, if loses, the walker moves towards left. If the interaction is missed due to either one of them

or both falling below the threshold line, the walker remains in its

position in the GLS. Just like earlier works, here also

the amount of gain/loss is not important.

Consider a biased lazy walker with probability of going towards right , towards left and probability to stay put

. Obviously . The average distance traveled by such a walker is linear in . Precisely, the average

distance traversed can be written as

. Here is the slope of the line,

a measure for the amount of drift.

As in any ballistic diffusion, here we have for all except

when . For , we have observed that

.

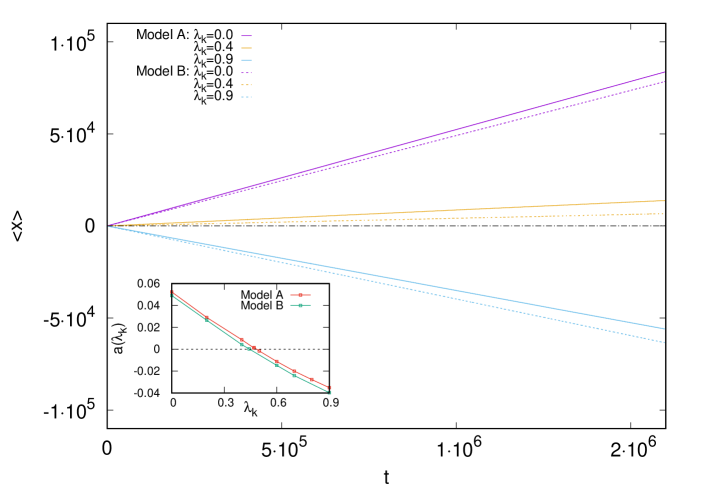

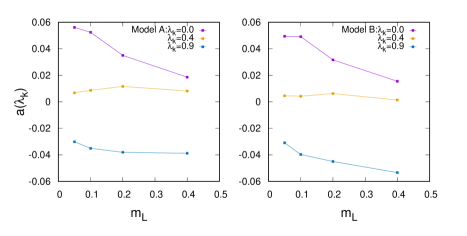

In Fig. 4, the variation

of against is shown for and for the

BTL tagged agent walker for both models A and B. Here we have taken and .

Inset shows the plot of drift as a function of . The drifts are obtained from the slopes

of versus plot.

At , for both the models we have found that and therefore drift .

The precise value of is found to be

for model A and for model B.

For any

the slope is more positive for low and less positive for larger . However, close to , the effect is

almost negligible.

This is shown in Fig.

5. This can be interpreted in the following way. The BTL agents’ subsidy come

from other agents’ taxes, i.e., at the cost of others. As we increase , number of BTL agents

increase and the subsidy amount coming from the taxes of others increase. Therefore possibility of having an interaction

decreases and the tendency to gain also decreases. As our definition for model B demands giving subsidy

to the agent at every MC step, and that has to come from the others above the threshold line, therefore,

the effect is more pronounced for model B compared to A.

However, the amount of wealth possessed by a BTL agent increases as we

increase for any specific .

We check the exact number of right, left and zero steps for the modified CCM walk and try to find out how

the probabilities change with for a specific . As we know that

, from Fig. 4 it is clear that,

and are functions of .

The specific probabilities for

two values will be found

in the Table 1. For both the models the variation of against

are shown in Fig. 6

for two different .

It is seen that the nature of variation matches well with the form

for both the models A and B,

where and

are two parameters, for low values of . The plots show discrepancy for high values

from the predicted behaviour.

Now if we simulate a lazy

walker with those and values that should show a similar versus behaviour.

In the inset of Fig.

6, the versus graph is compared with the same of a

lazy walker for a few specific and therefore and values values.

| Model A | Model B | ||||||

|---|---|---|---|---|---|---|---|

| 0.1 | 0.0 | 0.285 | 0.384 | 0.331 | 0.282 | 0.386 | 0.332 |

| 0.4 | 0.111 | 0.449 | 0.439 | 0.113 | 0.446 | 0.441 | |

| 0.9 | 0.0 | 0.482 | 0.518 | 0.0 | 0.480 | 0.520 | |

| 0.05 | 0.0 | 0.078 | 0.492 | 0.430 | 0.110 | 0.474 | 0.416 |

| 0.4 | 0.013 | 0.496 | 0.490 | 0.020 | 0.492 | 0.488 | |

| 0.9 | 0.0 | 0.481 | 0.519 | 0.0 | 0.480 | 0.520 | |

IV.2 Distribution of Path Lengths in the GLS

We have seen in the previous section, how the probabilities changes with . To have a detailed understanding about the probabilities we are now going to study how the quantities vary with walk length . A path length here signifies the length traversed at a stretch without changing direction. For the Right/Left direction, this means the agent will gain/lose for steps continuously and after that it will either make a loss/gain or stay put. Here we study three such quantities and where the suffix indicates whether it is a gain or loss or no interaction. The distribution of path lengths in the GLS is an interesting quantity to study and was studied earlier in [36] where there were only Right/Left movements. Here, it is clear that:

| (3) |

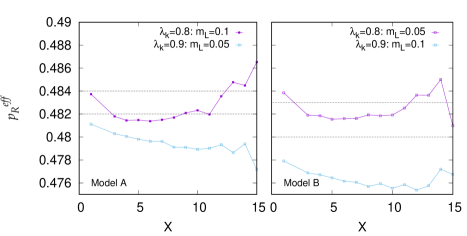

We now wish to extract the values of for a specific and from the distribution of path lengths at a stretch. For high values, e.g., , the probability is extremely small, and therefore the walk is very similar to a biased random walk. In that case, it is easy to extract some as then we can approximately write

| (4) |

is calculated numerically for a and . The is shown as a function of in Fig. 7 for a few values for both model A and B. The value has some variation over and not constant as predicted in Table 1.

For smaller however we cannot use Eq. 4. As for a lazy walker there are three parameters involved, we can use the obtained value of to check whether we are getting the same value as in Table 1 from this path length distribution data or not. For this we use the following:

| (5) |

For the BTL tagged agent’s walk in GLS, we calculate numerically for specific values of and . The obtained values do not match well except for the low values of .

From the above two aspects, therefore, we can say that the walker is not behaving like an usual biased lazy walker. The variation of and as a function of are shown in Fig. 8 a, b for A and B. As it can be seen the individual path distributions vary approximately as an exponential. It is to be noted here that all the variations are shown such that where . Also the relative variation of path distributions and as a function of are shown in Fig. 8 c, d, considering for all . It is clear from Fig. 8 c, d that for large , and decreases and finally comes to zero. That means long paths at a stretch for Gain/Loss are less probable. However, long paths are possible.

Another interesting quantity to check here is the direction reversal probability. For lazy walker, the direction reversal probability is . For our walk we consider the following quantity:

| (6) |

Here is the average distance traveled in any particular direction (Gain, Loss or no movement) at a stretch. Obviously, the direction reversal probability is given by .

The results are shown for some specific and for A and B. It is seen that for our walker, probability is very high for all values which saturates to a value close to for high . This is expected as when is high, number of missed interactions become negligible. Therefore, the dynamics is controlled only through and the situation becomes similar as in case of Right/Left movement. These are shown in Fig. 9. We also simulated a lazy walk using the parameters and calculated for that. For the lazy walker although the nature of variation is similar and tends to for high as in case of our walker, the exact probabilities do not match.

V Correlation

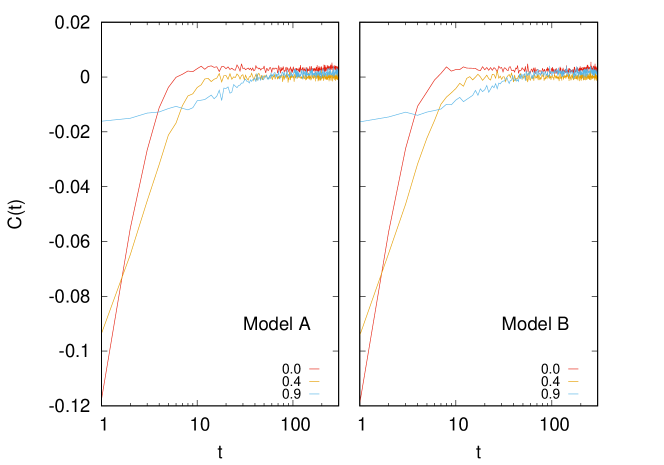

We have seen that the steps of the walker have three possible values. Therefore, we need to analyze the time series for such a walk. Let the step taken at a time be written as . The corresponding time correlation function can be written as: where . This can be written as we know that here is independent of and therefore . Just as in CCM walk, here unless near for both the model A and B. The correlations for model A and B are shown in Fig. 10. It is seen that there is a strong correlation near which gradually decreases with increasing .The short time correlations in both models A and B are negative. This is consistent with the fact that direction reversal probability is greater than . However, for one particular the correlation ultimately saturates to a value when .

This kind of feature was earlier noticed in [36]. The saturation value is estimated by averaging near the end over a few hundred values of . as a function of is shown for for both models A and B in Fig. 11 a. It is seen that reaches a minimum close to which is for model A and for model B. The minimum value of as observed for a is . Also as we observe the strongest correlation is changing with , we plot the same in Fig. 11 b. It is observed that as we increase threshold line , the correlation over one step becomes weaker and weaker for lower values. However for high for all values, is almost a constant. This feature is similar in model A and B but for higher values of the strength of maximum correlation, i.e., is weaker for a particular in model . This is shown in Fig. 11 c.

VI Reason Behind High Direction Reversal

It is already seen that the probability of direction reversal in the GLS is very high. This signature is also clear from

the strong correlation for small . In this part, we are going to analyze why this direction reversal is preferred

by an agent in this walk.

For our convenience, we choose the DY model which is the simplest among all and the form of wealth distribution is well known. For this we mimic a situation when the agent ends up with gain and then again interacts. The probability that the agent will incur a loss in the next step requires that she/he has to interact with another with low value of wealth. We consider our agent ends up with wealth in the first step. However, there are two possibilities in this case. If the second agent’s wealth is between and then there will be no interaction at all and if that is higher than and less than , our agent may lose some. The conditional probability that the agent will have a loss after a gain is

| (7) |

and the probability that the interaction will not occur is

| (8) |

But the probability that the previous step was a gain is . Considering the wealth distribution of the form

, the probability that it will either lose or stay put is

where .

Similarly the conditional probability of having a Loss in the first step and then either a Gain or a no interaction is

| (9) |

where .

Therefore .

Proceeding in a similar manner we can show that

| (10) |

where .

Thus, the probability of direction reversal is

| (11) |

In any case we can show that

| (12) |

Using the obtained values of and for different and we check the lower bound of the direction reversal probabilities from the Eq. 12. for a few and values obtained using Eq. 12 and from the model are compared in Table 2.

| From Eq. 12 | From Lazywalk | From model | ||

|---|---|---|---|---|

| 0.1 | 0.0 | 0.672 | 0.661 | 0.580 |

| 0.4 | 0.598 | 0.593 | 0.593 | |

| 0.9 | 0.548 | 0.499 | 0.508 | |

| 0.05 | 0.0 | 0.560 | 0.567 | 0.600 |

| 0.4 | 0.530 | 0.513 | 0.552 | |

| 0.9 | 0.525 | 0.499 | 0.508 | |

As we can see from Table 2, there is good agreement of the lower bound of the inequality with the lazy walker except when is very high. Also the agreement is not that good for the data obtained from our model. This indicates that the walk of our agent is not exactly a lazy walk. As becomes very high the DY model approximation is no longer valid and therefore there is discrepancy from the direction reversal probability obtained from Eq. 12.

VII Summary and Conclusion

In this work, the nature of transactions

made in CCM model with some modification is studied. We used the idea of threshold line below which an agent is

identified as a BTL one at the time of assigning wealth.

These agents are always eligible for subsidy. This is similar to giving opportunity to

some backward class people in any caste-based system.

The threshold line is important in another way.

It dictates whether an interaction will occur or not. Any agent, either BTL or not, having

wealth below that line at any point of interaction is considered insecure as in

any real situation. If either one or both the interacting agents’ wealth is below the

threshold line, the interaction will not occur. We also considered

an equivalent picture of a D walk in an abstract space for Gains and Losses. Here amount of Gain/Loss is not important;

we have just used the information whether it is a Gain or Loss. As a tagged agent may have Gain, Loss or no interaction,

the corresponding walker is a lazy walker which in addition to

Left/Right movement, may stay put at a position. The high direction reversal probability indicates

that there is a high tendency of individuals to make

a gain or to stay put immediately after a loss and vice versa. This kind of effect was studied for usual CCM model before.

Here also we found this to be compatible with

human psychology. From the high direction reversal probability it is clear that after a ’no’ interaction the agent will

try to interact immediately at the next step. Also a person may take part in an interaction which may lead either to a loss

or to no interaction, when she/he had a

gain in the previous step. After suffering a loss, in a same manner, a person

will either try to have a gain or may stay put due to

insecurity. This

effect is maximum for zero saving propensity and decreases with increased saving. The data obtained

from correlation for one step

also indicates that there will be high tendency of gain after loss and vice versa. (of course, there may be stay

puts in between).

The subsidy is given here in two ways, firstly at the time of assigning the wealth to the agents initially (Model A),

and secondly,

at each MC step (Model B).

It is seen that if subsidy is given repeatedly (i.e., at each MC step),

the agent moves with a less positive drift in the GLS for Model B compared

to Model A for any particular

(Fig. 4). This can be understood, as, giving repeated subsidy to a BTL agent will affect the wealth of others

and as the walks are actually correlated, it affects the tagged BTL walk in turn. The amount of wealth possessed by such an agent

is greater in Model B compared to Model A. The parameters and are

obtained from the walk of the tagged BTL agent and with those a lazy walk is simulated. It is seen that the BTL agent’s

CCM-like walk is not exactly similar to a biased lazy walk. The walk has no bias for some saving propensity which is

different for models A and B.

The distribution of path traveled at a stretch is studied for Right/Left movements and staying put. The quantities are and where the suffix indicates whether it is a gain or loss or no interaction. Using that we calculated the direction reversal probability and the same is calculated analytically for a DY model. Using the lazy walker parameters we compared the analytical direction reversal probability with those obtained from the walk. The analytical approach indicates that must be greater than . However, the analytical treatment was done using the DY model wealth distribution and therefore is not in good agreement to our case, when saving propensity is high. From different calculations shown here it is clear that for Model A, and for model B it is close to . Although for Model A it is close to the obtained for usual CCM model, i.e., , for Model B the result is different.

Finally, our study shows a modified CCM model with the concept of a Threshold line. The threshold line in addition to identification of BTL agents, puts restriction to interactions. We have seen that putting restriction changes the distribution which is dependent on the threshold line as shown in Fig. 3. The dynamics of a tagged BTL agent is compared to a Lazy walker in GLS. The high direction reversal probability for such a walker indicates that one can afford to have a loss or may stay put he/she has gained begore. Also after suffering a loss, it may stay put or may try to make a gain. This is completely compatible with human psychology. Also, it is seen that the value of is independent of for both the models A and B as shown in Fig. 5. The effect of giving subsidy once over giving repeated subsidy to such agents is checked from the point of view of the walk in GLS. The walk is seen to have more positive drift when the subsidy is given once.

References

- [1] Pareto V. 1897 Cours d’economie Politique. Paris, Lausanne : Rouge F.

- [2] Madelbrot BB. 1960 The Pareto-Levy Law And The Distribution Of Income. Int. Econ. Rev. 1, 79-106.

- [3] Chakrabarti BK, Chakraborti A, Chakravarty SR, Chatterjee A. 2013 Econophysics of Income and Wealth Distributions. Cambridge, Cambridge University Press.

- [4] Chatterjee A, Yarlagadda S, Chakrabarti BK, eds. 2005 Econophysics of Wealth Distributions. Milan, Springer Verlag.

- [5] Chakrabarti BK, Chakraborti A, Chatterjee A, eds. 2006 Econophysics and Sociophysics. Berlin, Wiley-VCH.

- [6] Sinha S, Chatterjee A, Chakraborti A, Chakrabarti BK. 2010. Econophysics: An Introduction. Berlin, Wiley-VCH.

- [7] Yakovenko VM, Barkley Rosser J Jr. 2009 Colloquium: Statistical mechanics of money, wealth, and income. Rev. Mod. Phys. 81, 1703-1725.

- [8] Silva AC, Yakovenko VM. 2005 Temporal evolution of the ”thermal” and ”superthermal” income classes in the USA during 1983-2001. Europhys. Letts. 69(2), 304-310.

- [9] Drăgulescu AA, Yakovenko VM. 2001 Evidence for the exponential distribution of income in the USA. Eur. Phys. J. B 20, 585-589; Drăgulescu AA, Yakovenko VM. 2001 Exponential and power-law probabilitydistributions of wealth and income in the UnitedKingdom and the United States. Physica A 299, 213-221); Levy M, Solomon S. 1997 New evidence for the power-law distribution of wealth. Physica A 242(1), 90-94; Sinha S. 2006 Evidence for Power-law tail of the Wealth Distribution in India. Physica A 359, 555-562; Aoyama H, Souma W, Fujiwara Y. 2003 Growth and fluctuations of personal and company’s income Physica A 324 (1-2), 352-358; Matteo TD, Aste T, Hyde ST. 2004 Exchanges in complex networks: income and wealth distributions IN The Physics of Complex Systems (New Advances and Perspectives), (eds Mallamace F, Stanley HE), pp. 435-442. Amsterdam, IOS Press; Clementi F, Gallegati M. 2005 Power Law Tails in the Italian Personal Income Distribution. Physica A 350 (2-4), 427-438; Ding N, Wang Y. 2007 Power-Law Tail in the Chinese Wealth Distribution. Chinese Phys. Letts. 24, 2434-2436.

- [10] Chakrabarti BK, Marjit S. 1995 Self-organisation in Game of Life and economics. Ind. J. Phys. B 69, 681-698; Ispolatov S, Krapivsky PL, Redner S. 1998 Wealth Distributions in Asset Exchange Models. Eur. Phys. J. B 2, 267-276.

- [11] Drăgulescu AA, Yakovenko VM. 2000 Statistical mechanics of money. Eur. Phys. J. B 17, 723-729.

- [12] Chakraborti A, Chakrabarti BK. 2000 Statistical mechanics of money: how saving propensity affects its distribution. Eur. Phys. J. B 17, 167-170.

- [13] Chatterjee A, Chakrabarti BK, 2007 Kinetic exchange models for income and wealth distributions. Eur. Phys. J. B 60, 135-149; Chatterjee A, Sinha S, Chakrabarti BK. 2007 Economic inequality: Is it natural?. Current Science 92(10), 1383-1389.

- [14] Chatterjee A. 2010 On kinetic asset exchange models and beyond:microeconomic formulation, trade network, and all that IN Mathematical Modeling of Collective Behavior in Socio-Economic and Life Sciences(eds Naldi G. et. al.) pp. 31-50. Boston, Birkhaüser.

- [15] Torregrossa M., Toscani G. 2018 Wealth distribution in presence of debts: A Fokker-Planck description. CMS 16(2), 537-560.

- [16] Bouchaud J. P., Mézard M. 2000 Wealth condensation in a simple model of economy. Physica A 282(3-4), 536-545.

- [17] Solomon S, Richmond P. 2001 A simple model of bank bankruptcies. Physica A 299 (1-2), 188-197.

- [18] Malcai O, Biham O, Richmond P, Solomon S. 2002 Theoretical analysis and simulations of the generalized Lotka-Volterra model. Phys. Rev. E 66, 031102.

- [19] Garlaschelli D, Loffredo MI. 2008 Effects of network topology on wealth distributions. J. Phys. A : Math Theor. 41, 224018.

- [20] Sornette D, Cont R. 1997 Convergent Multiplicative Processes repelled fom zero : power laws and truncated power laws. J. Phys. I 7, 431-444.

- [21] Toscani G., Tosin A., Zanella M. 2020 Kinetic modelling of multiple interactions in socio-economic systems. Netw. Heterog. Media, 15(3), 519-542.

- [22] Bachelier L. 1900 Théorie de la spéculation. Ann. Sci. Ecole Norm. Sup. 3, 21-86.

- [23] Saha MN, Srivastava BN. 1931 A Treatise on Heat. Allahabad, Indian Press.

- [24] Patriarca M, Chakraborti A, Kaski K. 2004 Statistical model with a standard distribution. Phys. Rev. E 70, 016104.

- [25] Repetowicz P, Hutzler S, Richmond P. 2005 Dynamics of money and income distributions. Physica A 356, 641-654.

- [26] Chatterjee A, Chakrabarti BK, Manna SS. 2004 Pareto Law in a Kinetic Model of Market with Random Saving Propensity. Physica A 335, 155-163; 2003 Money in Gas-Like Markets: Gibbs and Pareto Laws. Phys. Scr. T 106, 36-38.

- [27] Tumminello M, Lillo F, Piilo J, Mantegna RN. 2012 Identification of clusters of investors from their real trading activity in a financial market. New Journal of Physics 14 013041.

- [28] Gabaix X, Gopikrishnan P, Plerou V, Stanley HE. 2003 A Theory of Large Fluctuations in Stock Market Activity. MIT Working Paper Series 3-30, 1-46.

- [29] Chakraborty A, Manna SS. 2010 Weighted trade network in a model of preferential bipartite transactions. Phys. Rev. E 81, 016111.

- [30] Goswami S, Sen P. 2014 Agent based models for wealth distribution with preference in interaction. Physica A 415, 514-524.

- [31] Dimarco G., Pareschi L., Toscani G., Zanella M. 2020 Wealth distribution under the spread of infectious diseases. Phys. Rev. E 102, 02230.

- [32] Ferrero J. C. 2010 The individual income distribution in Argentina in the period 2000-2009. A unique source of non stationary data. arXiv:1006.2057.

- [33] Govt. of India Planning Commission. 2014 Report of The Expert Group to Review The Methodology for Measurement of Poverty.

- [34] Brady D, Fullerton AS, Cross JM. 2009 Putting Poverty in Political Context: A Multi-Level Analysis of Adult Poverty across 18 Affluent Democracies. Social Forces 88(1), 271-299.

- [35] Chatterjee A, Sen P. 2010 Agent dynamics in kinetic models of wealth exchange. Phys. Rev. E 82, 056117.

- [36] Goswami S, Chatterjee A, Sen P. 2011 Antipersistent dynamics in kinetic models of wealth exchange. Phys. Rev. E 84, 051118.