[type=editor, style=chinese, auid=000, bioid=1]

[type=editor, style=chinese, auid=000, bioid=1]

[type=editor, style=chinese, auid=000, bioid=1] \cormark[1]

[type=editor, style=chinese, auid=000, bioid=1]

[type=editor, style=chinese, auid=000, bioid=1]

[type=editor, style=chinese, auid=000, bioid=1]

[cor1]Corresponding author. \nonumnoteEmail: liwenkai871@gmail.com (W. Li), csxqli@gmail.com (X. Li)

A Survey of DeFi Security: Challenges and Opportunities

Abstract

DeFi, or Decentralized Finance, is based on a distributed ledger called blockchain technology. Using blockchain, DeFi may customize the execution of predetermined operations between parties. The DeFi system use blockchain technology to execute user transactions, such as lending and exchanging. The total value locked in DeFi decreased from $200 billion in April 2022 to $80 billion in July 2022, indicating that security in this area remained problematic. In this paper, we address the deficiency in DeFi security studies. To our best knowledge, our paper is the first to make a systematic analysis of DeFi security. First, we summarize the DeFi-related vulnerabilities in each blockchain layer. Additionally, application-level vulnerabilities are also analyzed. Then we classify and analyze real-world DeFi attacks based on the principles that correlate to the vulnerabilities. In addition, we collect optimization strategies from the data, network, consensus, smart contract, and application layers. And then, we describe the weaknesses and technical approaches they address. On the basis of this comprehensive analysis, we summarize several challenges and possible future directions in DeFi to offer ideas for further research.

keywords:

Blockchain \sepCryptocurrency \sepDecentralized Finance \sepSmart Contract1 Introduction

The blockchain concept originated from the research of Haber and Stornetta (1990) added timestamps to text, audio, and video files in digital form to guarantee their authenticity. When Nakamoto (2008) refined the blockchain concept for the first time, blockchain began to serve as a decentralized network with numerous properties, attracting considerable research. At the same time, the application of cryptography principles (Nakamoto, 2008) and the promotion of consensus mechanisms (Jakobsson and Juels, 1999) have enabled digital currencies with blockchain as the core to allow untrusting parties to complete transactions securely.

Suppose blockchain-based Bitcoin transactions represent the blockchain 1.0 era. In that case, the combination of smart contracts and blockchain signifies the era of blockchain 2.0. Szabo (1996) first introduced the concept of the smart contract, which denoted a promise or agreement in digital form. Buterin et al. (2014) proposed Ethereum, which updates and verifies blockchain data via the state. Ethereum is currently a significant platform for smart contracts and decentralized applications. The emergence of the Ethereum platform has stimulated the emergence of various blockchain platforms, such as BNB and Polygon.

In addition, Decentralized Finance (DeFi) is a decentralized application that uses blockchain in the financial domain to implement pre-defined financial protocols. Blockchain technology is widely used in various fields, such as education, health, and finance. Moreover, since the Ethereum blockchain technology integrated with finance more effectively during the Bitcoin era, DeFi technology in the financial field is gaining more attention.

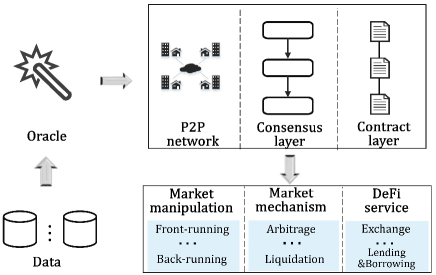

Moreover, the blockchain serves as the foundation of the DeFi application and enables transactions on DeFi to be completed securely. Blockchain’s consensus mechanism ensures the integrity of DeFi transactions. The consensus mechanism selects the ledger nodes for the blockchain. The nodes with bookkeeping rights incorporate the DeFi application’s transactions into a new block. The proper execution of the financial logic of the DeFi application relies on smart contracts (Jensen et al., 2021). The smart contract isolates from the outside world and cannot be modified once deployed on the blockchain. In detail, to get reliable real-world asset price information, DeFi introduces the oracle (Werner et al., 2021), which is a system to provide real-world financial asset price information.

| Reference | Contributions | Date | Categories |

| Jensen et al. (2021) | It focuses on the analysis of financial services. It classifies the risks of users, liquidity providers, arbitrageurs and application designers separately. | April 2021 | Financial Risk |

| Werner et al. (2021) | It focuses on the economic aspects and classifies the financial risks encountered by DeFi. And it analyzes the DeFi protocol and ecosystem. | September 2021 | Financial Risk |

| Qin et al. (2021b) | It first introduces the breadth of the lending market (a DeFi service). It quantifies the instability of lending protocols. | November 2021 | Financial Risk |

| Gudgeon et al. (2020) | It introduces a new type of Flash Loan attack and demonstrates the weaknesses and price fluctuations of the DeFi protocol. | June 2020 | Technical Risk |

| Qin et al. (2021a) | It compares the differences between traditional CeFi and DeFi, including legal, economic, and security. | June 2021 | Financial Risk |

| Amler et al. (2021) | It classifies DeFi services through the economics dimension, highlighting the advantages of DeFi compared to traditional finance. | September 2021 | Financial Risk |

| Bartoletti et al. (2021) | It formalizes DeFi theory in order to analyze various DeFi incentive mechanisms and design principles. | September 2021 | Technical Optimization |

| Liu et al. (2020) | Markov Chain and volatility prediction risk management are proposed. Loss distribution reduces mortgage rates, and VaR calculates external risks. | October 2020 | Technical Optimization |

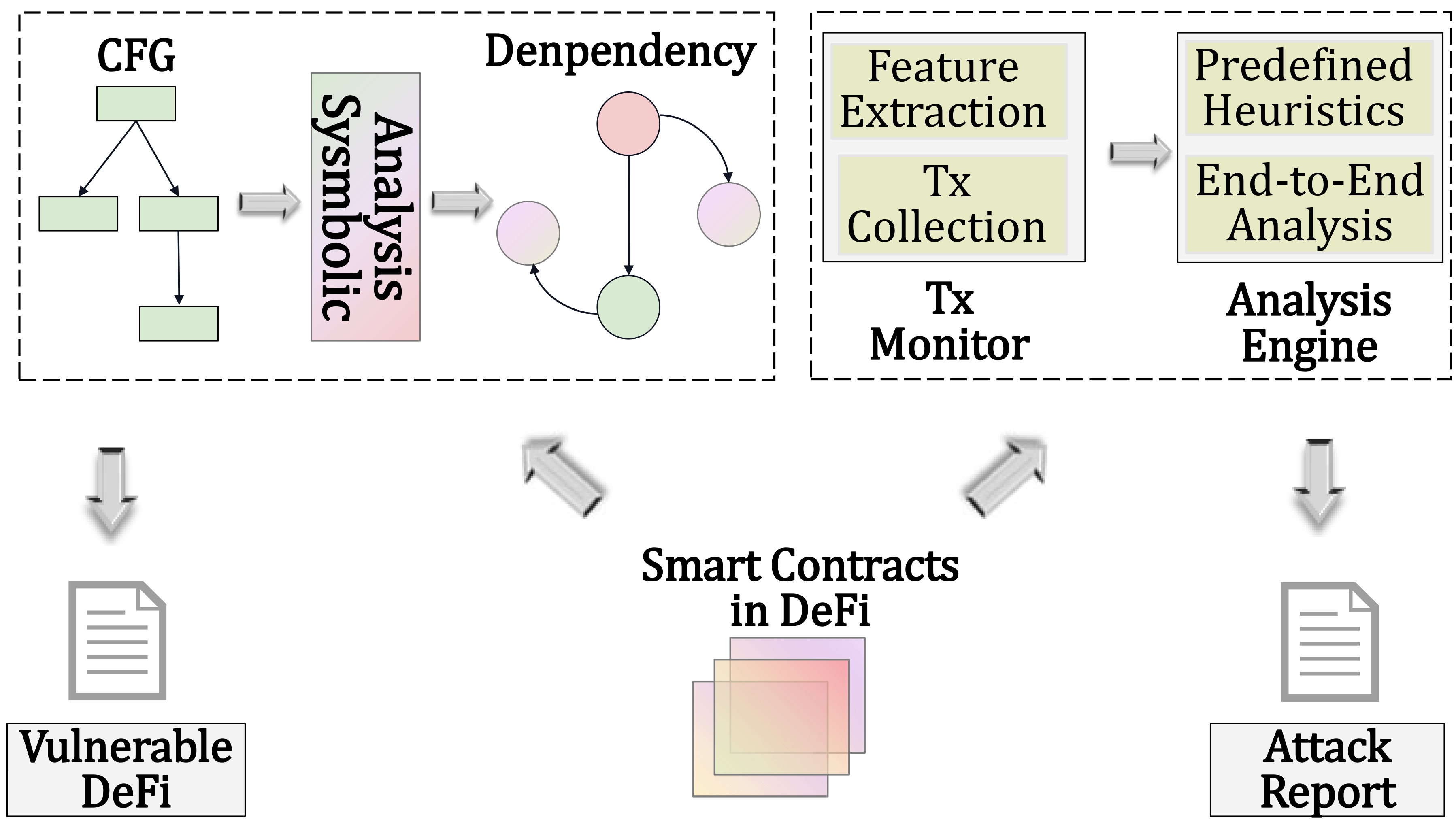

| Wang et al. (2021a) | It proposes a DeFi attack detection system that collects and analyzes transactions using symbol execution and transaction monitoring. | March 2021 | Technical Optimization |

| Bekemeier (2021) | It presents the first systematic risk and is the first empirical guide to stylized facts both at the technical level and economic level. | December 2021 | Technical and Financial Risk |

| Our study | It is the first to provide a systematic summary of DeFi security incidents and systematically analyze the vulnerabilities. We also provide future directions. | —— | Systematic Review |

With the rapid development of DeFi, it can be divided into stablecoin, Decentralized Exchange (DEX), cryptocurrency market, and insurance. Additionally, it had locked in $200 billion until April 2022 (Shaman et al., 2022). However, the value locked up in the entire DeFi dropped by around $85 billion in July 2022, causing us to ponder the security of DeFi.

While some studies about the risk of DeFi are in Table 1, they paid more attention to financial issues. Werner et al. (2021) classified attacks according to risk categories from an economic perspective. Qin et al. (2021b) systematically and quantitatively compared various lending systems and measured the risks that participants may encounter. Gudgeon et al. (2020) described the design flaws in lending protocols and DeFi losses due to price volatility. Qin et al. (2021a) systematically compared Centralized Finance (CeFi) and DeFi, including legal, economic, and market. Bartoletti et al. (2021) formalized the DeFi theory, which was used to understand systematically and analyze the incentives in DeFi to balance interest rates and prices. Other studies proposed by Jensen et al. (2021) and Amler et al. (2021) were used to analyze the risk of assets in DeFi on Blockchain.

In addition to the research of financial risks in DeFi, optimization schemes were also widely studied, as shown in Table 1. Liu et al. (2020) used a mathematical-statistical approach to the market for four types of assets and clearing to construct MovER, a framework for controlling the risk of the system. Wang et al. (2021a) proposed Blockeye, which constructed state dependencies from smart contracts and used the collected transactions to analyze whether it is subject to a DeFi attack. Even though there are some optimized solutions to vulnerabilities, attacks keep appearing, such as the Ronin Bridge incident (Network, 2022).

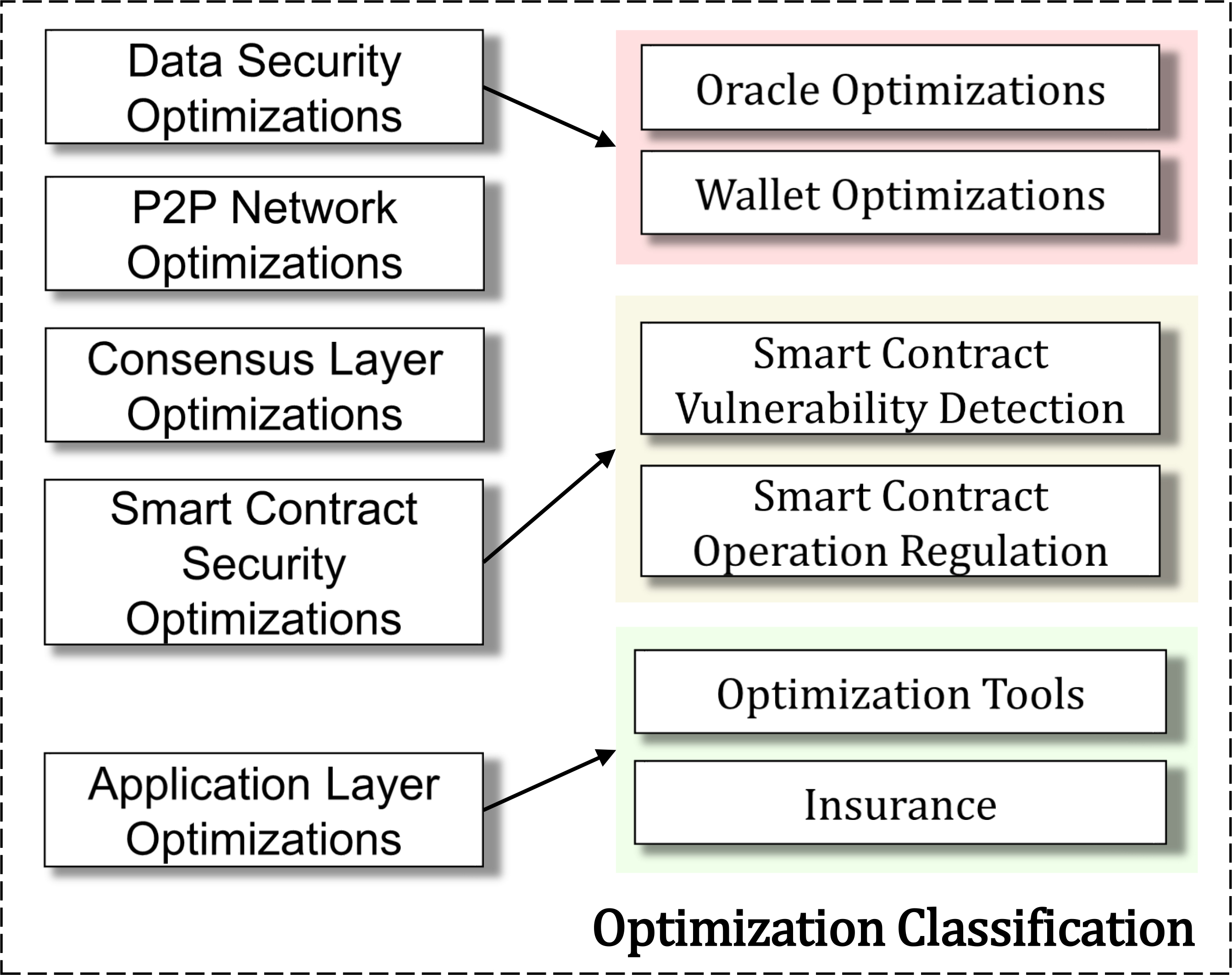

Similar work to ours was proposed by Bekemeier (2021), it discussed systemic risk, both at the technical level of the blockchain and the economic level, and provided experience analysis. The difference is that our work is more comprehensive. Our work in this paper systematically summarizes vulnerabilities at all technical levels, following the analytical path shown in Figure 1. In addition, we analyze the attack events caused by the vulnerabilities. Most importantly, we also summarize the most state-of-the-art optimizations at each layer. Finally, we conclude with some challenges and possible future directions.

The main contributions of this paper are as follows:

-

(i)

To the best of our knowledge, we conducted the first systematic examination of the security issues of the DeFi ecosystem built on blockchain.

-

(ii)

We systematically summarize the vulnerabilities of the Ethereum-based DeFi system, investigate real-world attack events related to DeFi and classify them according to their vulnerability principles.

-

(iii)

We survey the security optimizations in DeFi from the system level and conclude the challenges to suggest future research directions in this area.

The rest of the paper is structured as follows. Section 2 presents the background of the paper. In Section 3, we examine some vulnerabilities in DeFi, and in Section 4, we analyze real-world attacks. Section 5 provides several security optimizations, while Section 6 highlights DeFi’s challenges and future directions. Finally, Section 7 concludes the paper.

2 Background

2.1 Blockchain

| Names | Supported Consensus Algorithms | EVM-Compatible | Features | Ratio | |||

| Sec | TP | Sca | TC | ||||

| Ethereum (Buterin et al., 2014) | PoW & PoS & PoA | ✓ | ● | ● | ◑ | ● | 38.3% |

| BNB (huang et al., 2020) | PoSA | ✓ | ◐ | ◐ | ◐ | ◑ | 34.7% |

| Polygon (Kanani et al., 2021) | PoS | ✓ | ○ | ◐ | ● | ○ | 12.4% |

| TRON (liu et al., 2018) | DPoS & TPoS | ✓ | ◐ | ● | ◐ | ◑ | 5.5% |

| Tezos (Goodman, 2014) | Emmy∗ & Tenderbake | ● | ◐ | ○ | ◑ | 2.1% | |

Blockchain (Li et al., 2020c) is an advanced Peer-to-Peer (P2P) database system constructed using cryptography and consensus algorithms. According to its evolution, four distinct eras can be distinguished. Bitcoin, which represents the Blockchain 1.0 era, focuses primarily on decentralized and cryptocurrency properties. With the introduction of smart contract technology, blockchain technology has entered the 2.0 era, which is dominated by Ethereum. Integration of smart contracts accelerates the advancement of DeFi technology (Zhang et al., 2022). To improve the scalability of blockchain in the 3.0 era, blockchain platforms such as EOS permit real-time interaction between multiple chains. The 4.0 era is defined by the optimal integration of blockchain technology and conventional industry.

In Table 2, we survey the 525 most popular DeFi applications by popularity (Dapp.com, 2022) on 9 September 2022. With the advent of various blockchains, there are more options for DeFi applications deployment, such as Binance Smart Chain (BSC or BNB) (huang et al., 2020), Polygon (Kanani et al., 2021), TRON (liu et al., 2018), Tezos (Goodman, 2014), and others. Moreover, we discovered that the Ethereum comprised the largest proportion, followed by the BNB chain. In addition, in the "Features" column, ’Sec’, ’TP’, ’Sca’, and ’TC’ represents Security, Transparency, Scalability, and Transaction Costs, respectively. They are ranged with index units expressed as ○, ◐, ◑ and ● in order from weak to good. We found that these blockchain platforms account for over 90% of the 525 DeFi applications, with the majority of them supporting Ethereum virtual machine (EVM). Furthermore, other platforms are optimized based on Ethereum, sacrificing security or transparency to optimize scalability and transaction costs. Therefore, we prioritize Ethereum during the analysis in the rest of the paper.

2.1.1 Ethereum

Ethereum is a public blockchain system initialized using the Proof-of-Work (PoW) consensus mechanism, in which miners fight for control of blocks using computing power in exchange for incentives (Li et al., 2020c). However, it has subsequently shifted to the Proof-of-Stake (PoS) algorithm in September 2022, which is based on the quantity and age of stakes held (Wahab and Mehmood, 2018). It first uses the Turing-complete programming language Solidity, Vyper, and others to develop smart contracts (Chen et al., 2020c; Li et al., 2020b). On the Ethereum blockchain, anyone can deploy decentralized applications (DAPPs) that can interact with other network nodes. DeFi, an application that provides various financial services, is the current market leader and one of the most popular applications in the financial industry.

2.1.2 Other Blockchains

The BNB chain (huang et al., 2020) is a blockchain compatible with Ethereum Virtual Machine (EVM) that employs the Proof of Stake Authority (PoSA) consensus algorithm. Polygon (Kanani et al., 2021) is an extension chain for the Ethereum. It utilizes the PoS consensus algorithm to increase transaction speed and the ZK-Rollup zero-knowledge proof technology to ensure transaction security. TRON (liu et al., 2018) developed a TRON Virtual Machine (TVM) that is fully compatible with Ethereum smart contracts. It uses the TPoS consensus algorithm that combines DPoS and PBFT to balance security and Scalability. Tezos (Goodman, 2014) employs the Emmy∗ and Tenderbake protocol based on the PoS consensus algorithm. It employs formal verification techniques at the protocol and application layers to ensure security. Moreover, it scales utilizing a mechanism that can be upgraded.

2.2 Consensus Mechanism of Blockchain

The consensus mechanism is the basic technology of the blockchain, which ensures the blockchain’s secure, stable, and efficient operation. At the same time, the consensus mechanism enables the "mistrustful" parties on Ethereum to complete the verification and confirmation of transactions. Researchers are continuously improving various consensus mechanisms such as PoW, PoS, and DPoS (Lashkari and Musilek, 2021).

Nakamoto (2008) proposed PoW to prevent double spending on cryptocurrencies. The core idea of PoW is to compete among nodes for the bookkeeping rights and rewards of each block through their computing power (Mingxiao et al., 2017). All miner nodes in the network use the information in the previous block, such as previous block hash, timestamp, and nonce, to determine the next block. In PoW, miner nodes find the hash value by continuously trying random number nonce, which is difficult to calculate but simple to verify.

Mingxiao et al. (2017) proposed PoS, whose core idea is that the greater the ownership of a node to a specific amount of cryptocurrency, the greater the equity of the node. In PoS, it filters nodes by calculating the number of currencies in the nodes as a percentage of the total currencies and the time of holding currencies. This approach starts by selecting nodes, and only then moves on to carry out arithmetic operations. As a result, a significant amount of computational resources are not wasted.

Initial implementation of the PoA (Wood, 2016) consensus protocol occurred on the Ethereum test chain. It requires the same authentication nodes as the PoS consensus algorithm, but its authentication nodes must pass more stringent and complex standards. On this basis, consensus can be reached without communication; however, the identity of the verification node is visible, and the rate of node forgery is proportional to the shareholding ratio.

DPoS is an additional PoS (Wood, 2016) consensus algorithm variant. Participants combine their assets into a single pool of assets. Participants vote for the verifier, who then executes the asset pool trade. Moreover, the previous block’s representative cannot be applied to the next block. Unlike PoS consensus, DPoS elects the verifier by vote without regard to the proportion of account assets.

PoSA (RugDocWiki, 2021) is the synthesis of PoS and PoA consensus. It specifies a fixed number of verifiers ranked by the number of assets they possess. These verifiers are publicly accessible on the blockchain and take turns validating blocks. For instance, the BSC chain has 21 verifiers, whereas Ethereum has over 70,000. It compromises security for the sake of speed.

Castro et al. (1999) proposed the PBFT algorithm based on state machine copy replication, where transactions are modeled as state machines, and the state machines are replicated at different nodes of the blockchain. Each copy of the state machine preserves the state of the transaction. The state is changed only when the blockchain reaches consensus, ensuring the strong consistency of the blockchain in real-time.

TPoS (Illia, 2018) incorporates PBFT to improve the decentralization of DPoS. The final number of witness seats is used as the threshold, and each block slot has a default number of witness seats. Once all participants meet the criterion, a consensus is reached and rewards are given.

Emmy∗ (Goodman, 2014) utilizes 5256 block slots and determines if a block can be generated based on its block priority. Similarly to TPoS, the number of block endorsements greater than the total number of block slots is also used as a consensus reference factor.

Tenderbake (Nomadic, 2021) is an Emmy∗-optimized consensus mechanism that utilizes two votes to determine which blocks achieve consensus the fastest. It decreases the time required to generate a block and allows the vote to be validated only once, which increases the network’s stability.

2.3 Layers of DAPP on Blockchains

DAPPs, like traditional software architectures, can be separated into six layers as follows (Duan et al., 2022): (1) The data layer handles off-chain data before passing it on to the network layer. (2) The network layer is peer-to-peer, assuring network node autonomy. (3) The consensus layer guarantees that miners package network layer requests. (4) The incentive and consensus layers are interrelated, and the incentive layer ensures that miners do not behave maliciously. (5) The smart contract layer connects the consensus with application layers and exchanges data between them, and (6) the application layer binds the information from the smart contract layer and shows it to the user after processing.

2.4 Transaction Process on Blockchain

When a user interacts with the applications and begins a transaction request using the interfaces provided by the smart contract, the transaction request broadcasts to all nodes on the P2P network chain (Li, 2021). When the miner gets the request, it selects and packages the transaction into blocks. The miner adds blocks to the chain using the consensus algorithm and synchronizes them with all nodes on the network. Simultaneously, the smart contract changes the state variables depending on transaction data and visualizes them in the application.

2.4.1 Geth

Go-Ethereum (Geth) is an official Ethereum client implemented in the go programming language (Adam et al., 2013). It includes instructions for several tasks, such as creating an Ethereum private chain and interacting with the network environment.

2.4.2 Gas

To avoid the overuse of network resources, all transactions on Ethereum are paid a cost called gas, and the transaction fee equals the amounts of gas multiplied by gasPrice (Chen et al., 2017a, 2020b). The user who proposes transactions sets the gasPrice, and miners with high computing resources would conduct the transaction earlier if the gasPrice is high (Chen et al., 2018a). There is also a concept called gaslimit, which is used to limit the maximum amount of gas that can be used for a transaction (Chen et al., 2017b). It means that the maximum charge for a transaction is gaslimit multiplied by gasPrice.

2.4.3 Maximal Extractable Value (MEV)

Regarding blockchains with PoW, the MEV is the value that can be extracted by the miner. However, the maximum extractable value may make more sense for blockchains utilizing PoS or other consensus algorithms.

Miner extractable value refers to the profit miners make by performing a series of operations on the blocks they mine (Qin et al., 2022). For example, miners reorder transactions to optimize the initial ordering of transactions and earn additional Ordering Optimization (OO) fees (Daian et al., 2020). And the phenomenon that miners sell priority in blocks to make users keep raising the cost of gas is called Priority Gas Auctions (PGA).

Maximal Extractable Value is the maximum value that the validator can extract by reordering, inserting, or not executing the transactions in the block. In addition, we assume that the balance in before the transaction is and is after the transaction. So the value obtained by sequential execution equals , and means the order of transactions is in full array. Thus the maximal extractable value can be defined as .

2.5 DeFi

2.5.1 Development of DeFi

The introduction of blockchain technology (Nakamoto, 2008) has changed the traditional financial ecosystem. With the advent of Ethereum, smart contracts became the basis for the development and implementation of DeFi. Since the landing of MakerDAO in 2014, which is the first Ethereum-based DeFi project, several DeFi protocols have emerged to implement functions of traditional CeFi, such as lending platforms, exchanges, derivatives, and margin trading systems (Wang et al., 2022). As liquidity mining mentioned in 2020, DeFi applications were pushed into high gear with the emergence of DEXs such as Compound, which were entirely managed by smart contracts. Asset Legos brings unlimited creativity to DeFi products. It means that a new financial product can be realized by combining the underlying DeFi protocols (Popescu et al., 2020). In 2022, regulated Decentralized Finance (rDeFi) becomes the new trend in DeFi development (Coinchange, 2022).

2.5.2 DeFi Service

As depicted in Figure 1, DeFi applications can be made up of DeFi services, also known as protocols, such as exchange, lending, and asset operation. Blockchain will wait for assets or data to be processed through protocols before uploading them to the application layer, which is the market (Schär, 2021). The DEX serves as a forum for asset suppliers and buyers to engage. It can be separated into two types: centralized order system and Automated Market Maker (AMM) (Zhou et al., 2021b). The former is comparable to a regular exchange in that customers produce trade orders following transactions start. The latter is accomplished quickly by initiating a transaction using a previously constructed asset price algorithm.

2.5.3 Market Mechanism

In addition to technological issues, DeFi has an economic mode of operation, which is the market mechanism. Users can control and alter numerous assets using the DeFi service normally. However, attackers can benefit by manipulating the asset through market-based strategies at the economic level.

3 Analysis of Vulnerabilities

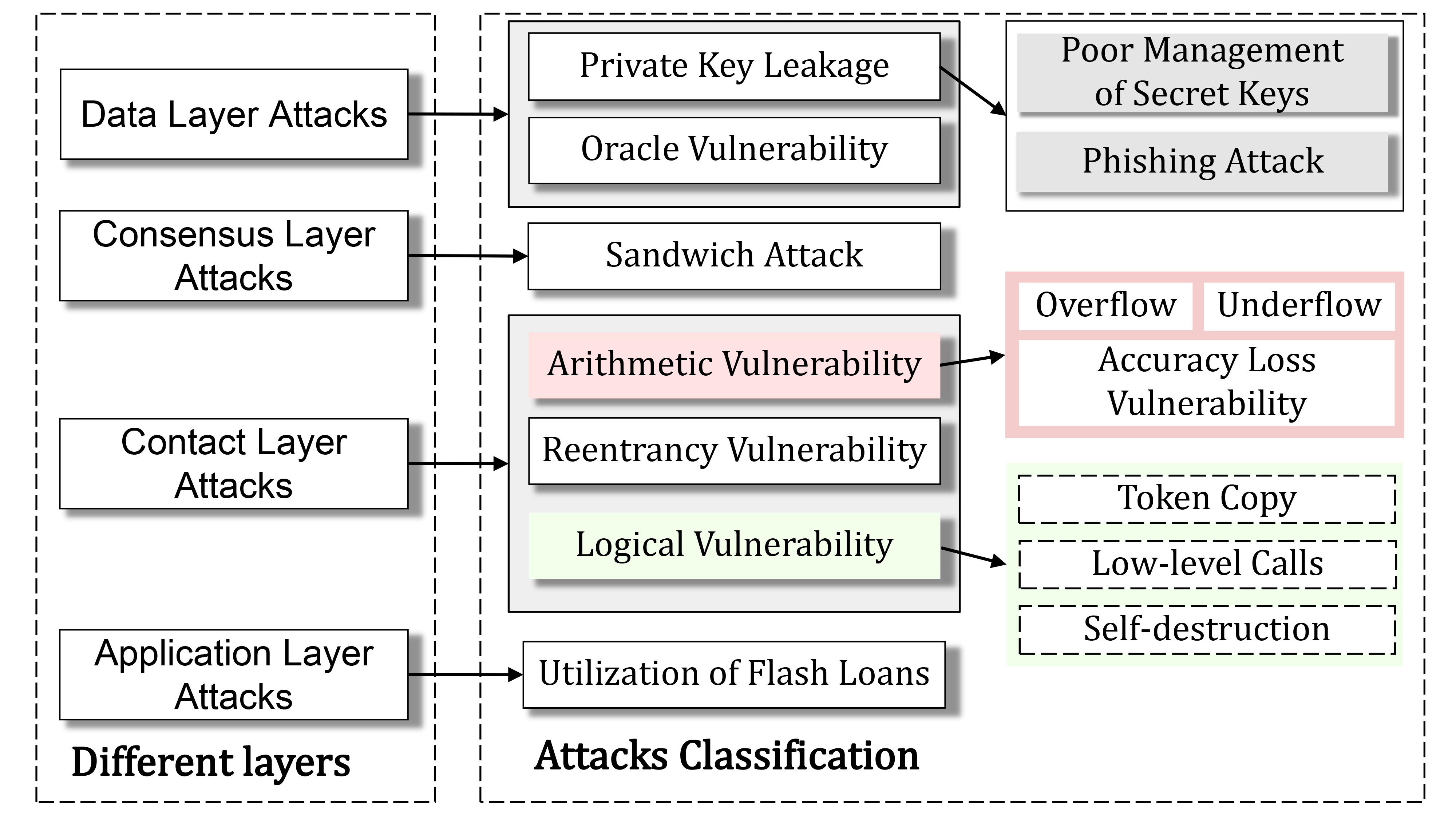

From the proposal of DeFi to 2022, various vulnerabilities have emerged to promote the ecological development of DAPPs. Therefore, studying the vulnerabilities associated with DeFi facilitates comprehension of attack defense techniques. In order to provide a concise summary of the dangers posed by DeFi, we will concentrate on the data, consensus, contract, and application layers.

3.1 Data Security Vulnerabilities

For the data layer, if attackers change the data under the chain during the uploading process to the chain, it will result in irreversible mistakes due to the immutability of the blockchain. Figure 2 shows that it could encounter oracle mechanism vulnerability and inappropriate key management.

3.1.1 Oracle Mechanism Vulnerability

The oracle is an automated service mechanism that allows the system to obtain the off-chain asset price data as input (Werner et al., 2021). And smart contracts rely on the exchange rates of prices provided by oracle for proper operation. However, as Figure 1 shows, the risk to oracle grows drastically when a single point of failure occurs. For example, over 3 million sETH were arbitrated due to the oracle errors in Synthetix, a protocol that converts entity into synthetic (Synthetix, 2019). Oracle risks can be divided into technical and social problems.

Technical oracle problems may be defined as a process of passing data with three key elements: (1) How to collect all the data accurately? (2) How to process the data with as few errors as possible? And (3) How to upload the processed data to the smart contract?

Furthermore, the current oracle form may be centralized and distributed. Centralized oracle uses trusted third parties to collect, process, and transfer data to smart contracts. Distributed oracle consists of numerous nodes that take data from multi-sources and process it using an algorithm, such as a consensus (Kumar et al., 2020) or weighted voting method (Angeris and Chitra, 2020). Finally, the oracle system assesses the chain information.

| Wallets | Descriptions | Features | ||||

| Flex | Sec | Sca | TP | TxC | ||

| Local Storage | Keys are stored centrally in the file system by default | - | - | - | - | - |

| Hardware Wallet | Hardware devices can isolate external networks and transport operations | ✓ | - | |||

| QR Code Wallet | QR code generated from the address and scanned to obtain the address | ✓ | - | |||

| Simple Wallet | It can simply handle cryptocurrencies and tokens for raw transactions | ✓ | - | ✓ | - | ✓ |

| Multi-Sig Wallet | The transaction process requires multiple owners to sign to ensure users’ security | ✓ | ✓ | ✓ | ✓ | |

| Forwarder Wallets | Forwarding assets to a master wallet and users only need to preserve the subkey | ✓ | ✓ | ✓ | ✓ | |

| Controlled Wallets | The third party keeps the key and anyone who uses the key needs authorization | ✓ | ✓ | |||

| Update Wallets | Users can customize the update by selecting some parts to be updated | ✓ | ✓ | ✓ | ✓ | |

| Smart Wallets | Wallets with enhanced functionality that achieve expansion of normal functions | ✓ | ✓ | ✓ | ||

There are not only technical problems but also social problems in oracle (Caldarelli and Ellul, 2021; Egberts, 2017). Assuming such a game where there exists an Oracle . The picks the off-chain data and processes it as . The contract uses for transactions , where is the function in the contract . If an attacker pays to modify in , and obtains benefits . When the cost by the attacker is less than the benefits , the attacker gets a profit that would be attractive to other attackers. While the cannot be measured directly from technical methods, it requires analysis of specific social situations, so the oracle problem is controversial in terms of social issues.

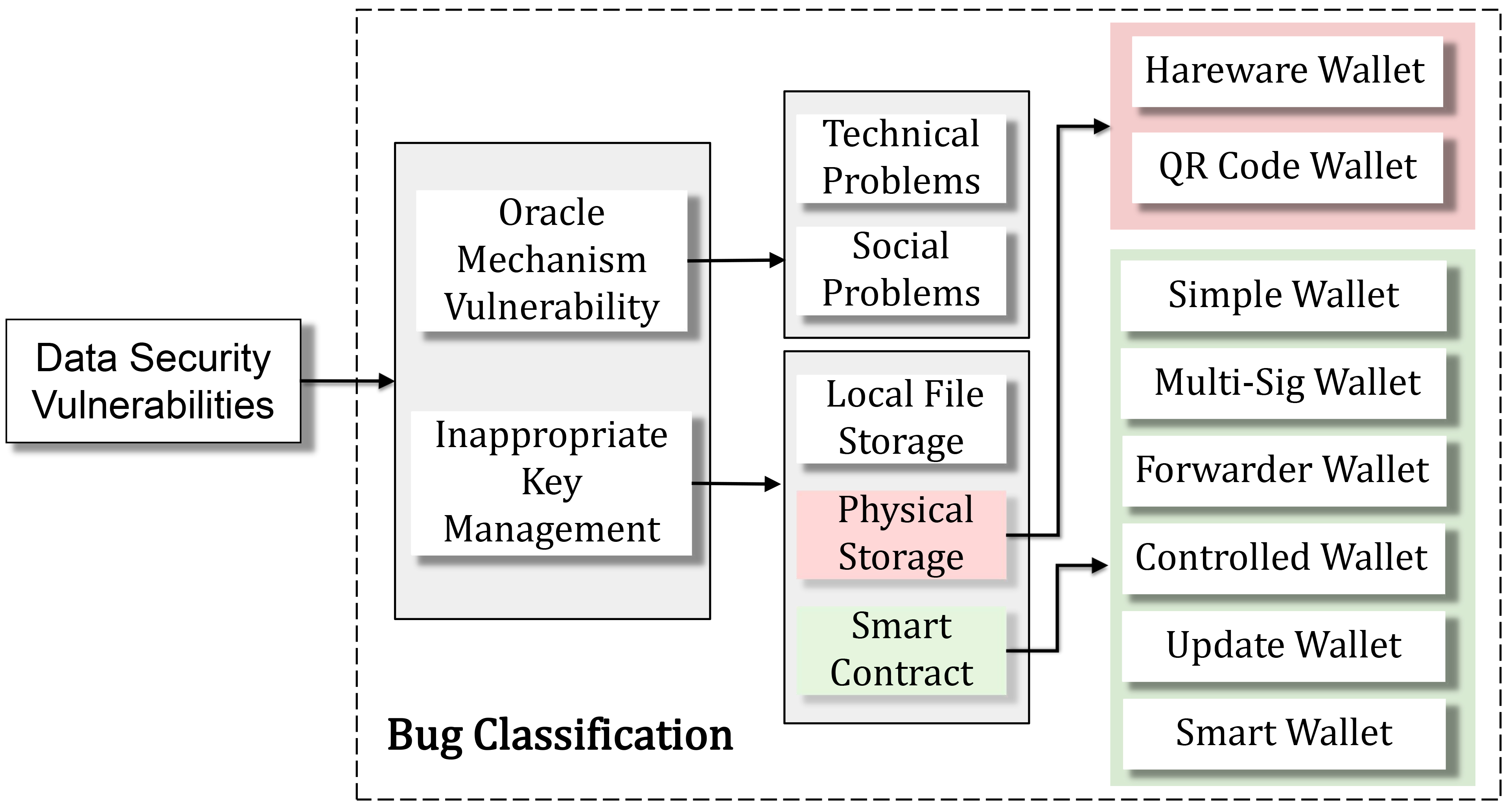

3.1.2 Inappropriate Key Management

In the DeFi ecosystem, wallets are used to manage private keys, and asset authentication is based on keys in most cases. However, similar to Bitcoin, the DeFi system suffers from the problem of improper key management. Existing key management methods, such as physical storage (Dabrowski et al., 2021; Shbair et al., 2021), offline wallets (Khan et al., 2019; He et al., 2018), and password-derived wallets (Kaliski, 2000), have some drawbacks. In Table 3, we summarize nine forms of wallets, where local storage is the initial form of local file storage, hardware wallets and QR code wallets both belong to physical storage wallets. The remains belong to smart contract wallets. Moreover, ’Flex’ in Table 3 is the Flexibility, above the Local Storage is a , and vice versa is a . The same applies to ’Sec’, ’Sca’, ’TP’, and ’TxC’, representing Security, Scalability, Transparency, and Transaction Costs, respectively.

In Ethereum, users can access the Ethereum chain by using Geth. When a user creates an account , the client generates a file to be stored locally, which contains the unique key associated with the account . Before the account initiates a transaction or mining, the client reads the in the file. However, anyone without restricted access can read the file and even falsify for profit.

There are three types of wallets, software, hardware, and paper, depending on the form in which they exist (Suratkar et al., 2020). Hardware and paper-based storage, which are physical storage, are more secure because they store keys in a way that isolates them from multi-user interaction. Nevertheless, it also has the weaknesses of poor scalability (Arapinis et al., 2019) and the inability to have a single point of failure caused by the architecture design (Dabrowski et al., 2021).

Smart contract wallets are divided into six types in (Di Angelo and Salzer, 2020). They restrict the direct access to assets and provide some Application Binary Interfaces (ABIs) for manipulating data.

Simple Wallet. It is the initial form of wallet, offering simply raw transaction capability and storing all keys in files. When a malicious parity obtains file system permissions, keys can be read or even manipulated.

Multi-signature Wallet. It requires the co-signature of many owners for increased protection. The combination of many signatures dilutes the individual’s influence, providing decentralization. And the public multiple signature combination could enhance transparency.

Forwarder Wallet. It adds forwarding operations to the signing process, such as password-derived wallets, which allow users to customize the master key and then derive sub-keys from controlling the asset. The forwarding operation faces a balance between transparency and security. If the derivation algorithm is publicly available, attackers who got the master key in some ways will reproduce the derivation process to obtain all sub-keys.

Controlled Wallet. The custodial wallet is an example of a controlled wallet since it keeps ownership of the account and grants access to users. It offers some protection by centralized management, but the non-transparent action also tests managers’ credibility.

Update Wallet. Update wallets permit users to modify updates depending on features, allowing for greater flexibility in wallet operation. However, compatibility across many versions might result in worse security.

Smart Wallet. Smart wallets include some sophisticated features, such as key recovery. As a result, the smart contract enables wallets to execute various services in addition to transferring money. However, it adds to the dangers involved with smart contracts in Section 3.3.

| Brief Explanation | Descriptions | Date | Severity |

| Journaling Mechanism | Geth can’t restore a deleted empty account due to out-of-gas | November 2016 | High |

| EVM Stack Underflow | SWAP, DUP, and BALANCE underflow the EVM stack | February 2017 | High |

| Stack Elements | In a static environment with fewer than three stack elements | October 2017 | Low |

| Encryption Algorithm | The elliptic curve algorithm was not fully validated | February 2018 | High |

| Timestamp Overflow | Timestamp, state variables in blocks, overflow | March 2019 | High |

| Shallow Copy | Pre-compile contract, making Geth inconsistent with memory | July 2020 | High |

| Ether Shift | Transfering the balance of the deleted account to the new account | August 2020 | High |

| Certain Sequences | Certain transaction sequences can lead to the failure of consensus | December 2020 | Middle |

| Incorrect Requirements | Failure to properly authorize timestamp leads to double spending | February 2021 | High |

| Memory Corruption | RETURNDATA corruption due to data replication, resulting in forking | August 2021 | High |

| Denial of Service (DoS) | Combination of short-term restructuring and delayed consensus decision | October 2021 | Critical |

| Bignum Overflow | Some large values in consensus specification overflow leads to a fork | April 2022 | High |

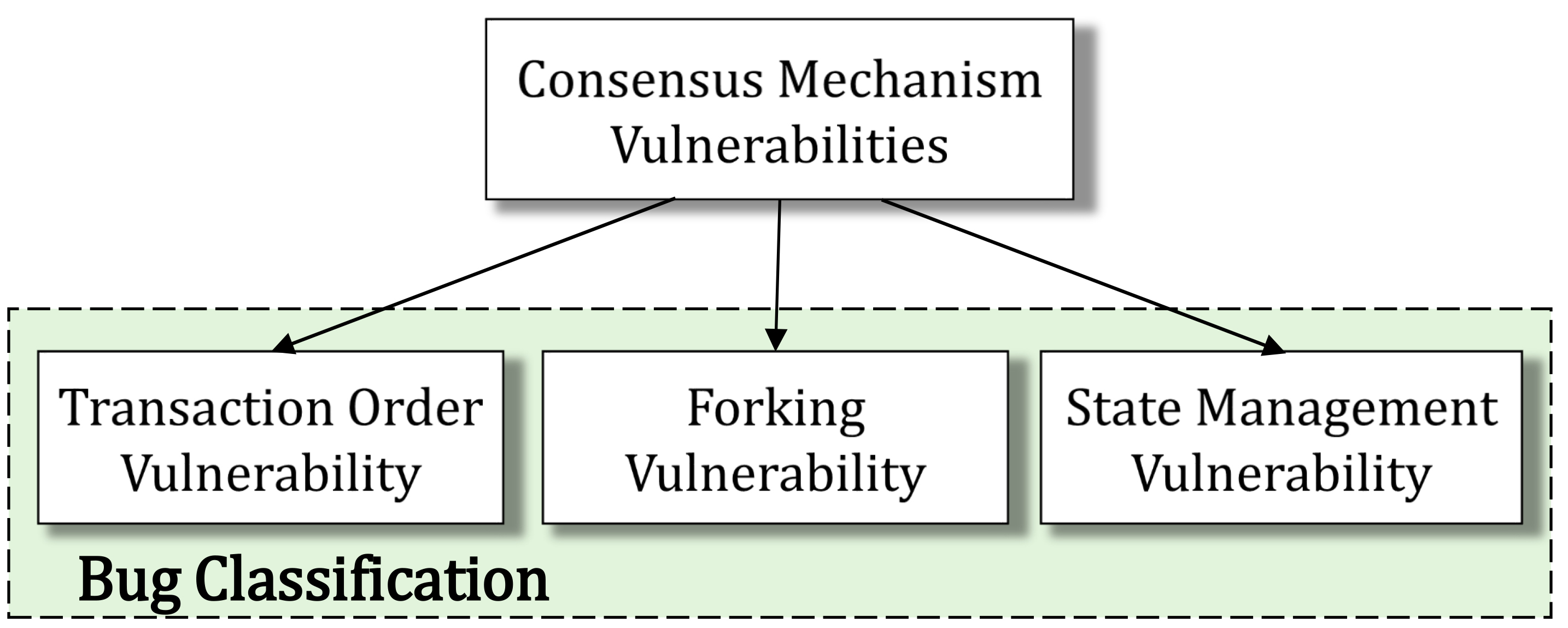

3.2 Consensus Mechanism Vulnerabilities

Blockchains, such as Ethereum and others, are consensus-based. Up to now, many significant works have already been done in design, testing, auditing, and maintenance. So there are not many consensus flaws, but we gather the consensus bugs that occurred in Geth according to (NVD, 2022; Yang et al., 2021; Luu et al., 2015) in Table 4, and we classify them from three aspects in Figure 3. There are four severity categories, with low suggesting that the developer resolved before they occur. The ’Middle’ was deployed to the test network before being discovered, while the ‘High’ was in the main chain. The ’Critical’ implied that the vulnerability was widely available and had a significant impact on the integrity of the network.

Certain malicious behaviors utilize consensus rules to affect the sequences of transactions. There are a variety of attacks combined with MEV, such as flash loans (Qin et al., 2021c; Zhou et al., 2021a), sandwich attacks (Zhou et al., 2021b; Qin et al., 2022), and forking attacks (Daian et al., 2020). As Figure 3 depicts, we classify this part into three segments: 1) Transaction Order Vulnerability, 2) Forking Vulnerability, 3) State Management Vulnerability.

3.2.1 Transaction Order Vulnerability

Transaction order vulnerability describes that an attacker alters the initial sequence of transactions by leveraging the miner’s desire for profit. The sandwich attack (Zhou et al., 2021b) is a typical example. The attacker predicts that the victim will buy asset A, and pays a higher gas fee to acquire it before the victim at a lower price. And then, they sell A at a higher price for arbitrage since the victim’s purchase boosts the price.

Front Running Attack. A front-running attack (Zhou et al., 2021b) employs a high mining cost to induce miners to block the original block and give the trade of attackers priority over the original trade, thereby modifying the status information of the actual trade in order to profit. In one instance, an attacker configures a bot to monitor profitable trades automatically and then attacks them automatically. However, as more individuals attack the same transaction, the potential for profit from each attack diminishes.

Sandwich Attack. The sandwich attack (Zhou et al., 2021b) is a variant of the front run attack that employs both a front running attack and an end running attack, in which a second trade is made after the initial trade to maximize the benefit gained from the initial trade. In some DEXs, trades between decentralized market makers are automated. Trades have acceptable price slippage. When the price slip threshold is reached, the transaction is canceled. However, sandwich attacks permit the victim’s trade to return to the slippage point. Moreover, we explain how it attacks in detail in Section 4.2.1.

3.2.2 Forking Vulnerability

Forking events in DeFi are generally associated with transaction fee-based forks and time-bandit attacks (Daian et al., 2020). Mining revenue incentivizes miners to perform honestly, but the OO fee motivates them to reorder transactions in the block, enhancing the income. There are already many classical fork attacks in blockchain, including 51% attacks (Moroz et al., 2020) and selfish mining (Kędziora et al., 2019) based on PoW, and Nothing at Stake attacks (Wiki, 2022) based on PoS consensus. Most bugs contain forking vulnerabilities in Table 4, for example, memory corruption, incorrect requirements, shallow copy, and certain sequences.

51% Attack. The 51% attack (Moroz et al., 2020) occurs when attackers take control of the block generation. They possess the majority of hash computing power, which is the ability to solve difficult problems in a PoW consensus-based blockchain network. Typically, it can be separated into the direct profit and the indirect profit. The former is a double-spending attack in which the user’s transaction is paid twice, doubling the profit. The later refers to DoS attacks that block transactions to compel other miners to join their pool, thereby increasing computing power and making it easier to generate a profit. Moreover, we have summarized some typical 51% attack cases in Table 6.

Selfish Mining. Selfish mining (Kędziora et al., 2019) is that miners do not disclose the first mined block and then disclose two blocks after digging the second block, resulting in a fork of the current blockchain network. The advantage of this strategy is that one block has a high level of dominance over the others, which makes getting two blocks in a row more advantageous. In order to perform this attack, the adversary must maintain two blockchains. The first is public for connecting to the mainnet chain, while the second is private for mining a second block. Once the first block is mined, it starts mining the second block. Even if other mines in the mainnet chain extract the block, the attacker can open their own mined block, possessing the priority to extract the second block based on the first height.

Nothing at Stake. Nothing at stake (Wiki, 2022) implies that, after the system used the PoS consensus algorithm has reached consensus with a block, it discovers that the block contains no information but still causes a fork. Even though the block reaches consensus with the chain, it takes the stake to another fork. The PoS consensus algorithm determines that the specified extractor generated the block if is greater than the threshold. Where represents the random number generated by the extractor ID and public key, $ represents the number of assets in the system, and represents the time of the extractor on the block that cannot be determined. Time and number of assets as common factors in reaching consensus, so attackers can use the little stake to reach consensus in many forks.

3.2.3 State Management Vulnerability

Transactions in Ethereum are based on updating states between blocks (Wood et al., 2014). According to the consensus rules, the confirmation between the old and new blocks needs to be completed within certain minutes. Therefore, if attackers complete the extraction of the state variables within the block, then they can attack the transaction within the specified time. For example, timestamp overflow and incorrect requirements are in Table 4. The former is because the timestamp exceeds the representation of uint64, resulting in a hash error in the block (Yang et al., 2021). The latter is that the timestamp in a block gets the permission mistake, which means the block is to be refused by the chain permanently, causing a chain fork and the execution of a double-spending attack (NVD, 2022).

Timestamp Overflow. An attacker uses an operation, such as uint64 in Ethereum, to make a timestamp attribute in a block exceed what it can represent. The false representation of the timestamp causes the block’s hash value to change, preventing it from agreeing with the other nodes in the blockchain. In addition, the attack is typically caused by poorly designed modules that can obtain the blockchain’s state. Moreover, it is available in Table 5 about smart contracts vulnerabilities.

Incorrect Requirement. Incorrect Requirement refers to the attacker exploiting a configuration error in the server node timestamp information to render the block authentication invalid, resulting in node operation deformation. In some blockchains, network nodes are required to authorize the timestamp information for their nodes. However, there are some special conditions exist, such as the server setting the incorrect time zone or the network latency between network nodes.

3.2.4 Others Consensus Attacks

Block Discard. Block Discard is also called "Block Withholding". It indicates the phenomenon in mining pools where malicious miners send partial proofs of work to the pool manager and discard the full proofs of work (Rosenfeld, 2011). This attack is commonly seen in competition between different mining pools.

Pool Hopping Attack. After analyzing the revenue of multiple mining pools, the attacker will choose to join the one with the highest revenue to join and allocate a portion of the arithmetic power to prevent it from mining blocks (Rosenfeld, 2011). Similarly, when the mining pool manager finds that a certain blockchain network can get higher revenue, he will transfer the computing power to that network. However, the revenue of miners in the pool is still distributed according to the original revenue. The mining pool management can get more revenue.

Distributed Denial of Service Attack. Distributed Denial of Service (DDOS) attackers sever connections between multiple nodes and the network, thereby impacting the availability of the network or system. Regarding blockchain platforms, a DDoS attack against multiple nodes has a greater negative impact on DeFi than a DoS attack against a single node (Singh et al., 2020). Additionally, DDoS attacks deplete the victim’s computing and communication resources in a short period, slowing down the consensus agreement.

Eclipse Attack. When all other nodes connected to the current node are attacked, the current node is under eclipse attack (Xu et al., 2020). The attack prevents the P2P network’s nodes from controlling information access. When all the nodes connected to the current node are the attacking node, the current node has suffered an eclipse attack. The attack prevents the P2P network’s nodes from controlling information access. In reality, not all network nodes are interconnected, meaning that the attacker who takes control of a subset of the network can launch an eclipse attack. Furthermore, it can benefit from combined with a double spending attack (Marcus et al., 2018).

Sybil Attack. The Sybil attack and the eclipse attack are similar, but the target of the attack is different. The eclipse attack intends to control the information in a specific node. In contrast, the Sybil attack prefers to attack all the nodes, reducing the backup function of the network. The Sybil attacker masquerades as a node participating in the election to deceive other honest nodes. It misleads other nodes by sending messages using fake identities to determine the connection status of blockchain (Bhutta et al., 2021). When a certain number of fake nodes affects the blockchain’s consensus, combining Sybil and 51% attacks increases the ratio of a successful double spending attack. Sybil attacks are available in two modes, 1) the direct attack, where honest nodes are affected directly by fake nodes, and 2) the indirect attack, where honest nodes are impacted by nodes that communicate with Sybil nodes. Sybil attacks (YADULLAH, 2022) also occur in blockchains, where attackers create multiple fake network identities to inflate the value of the Sabre protocol and the Solana blockchain.

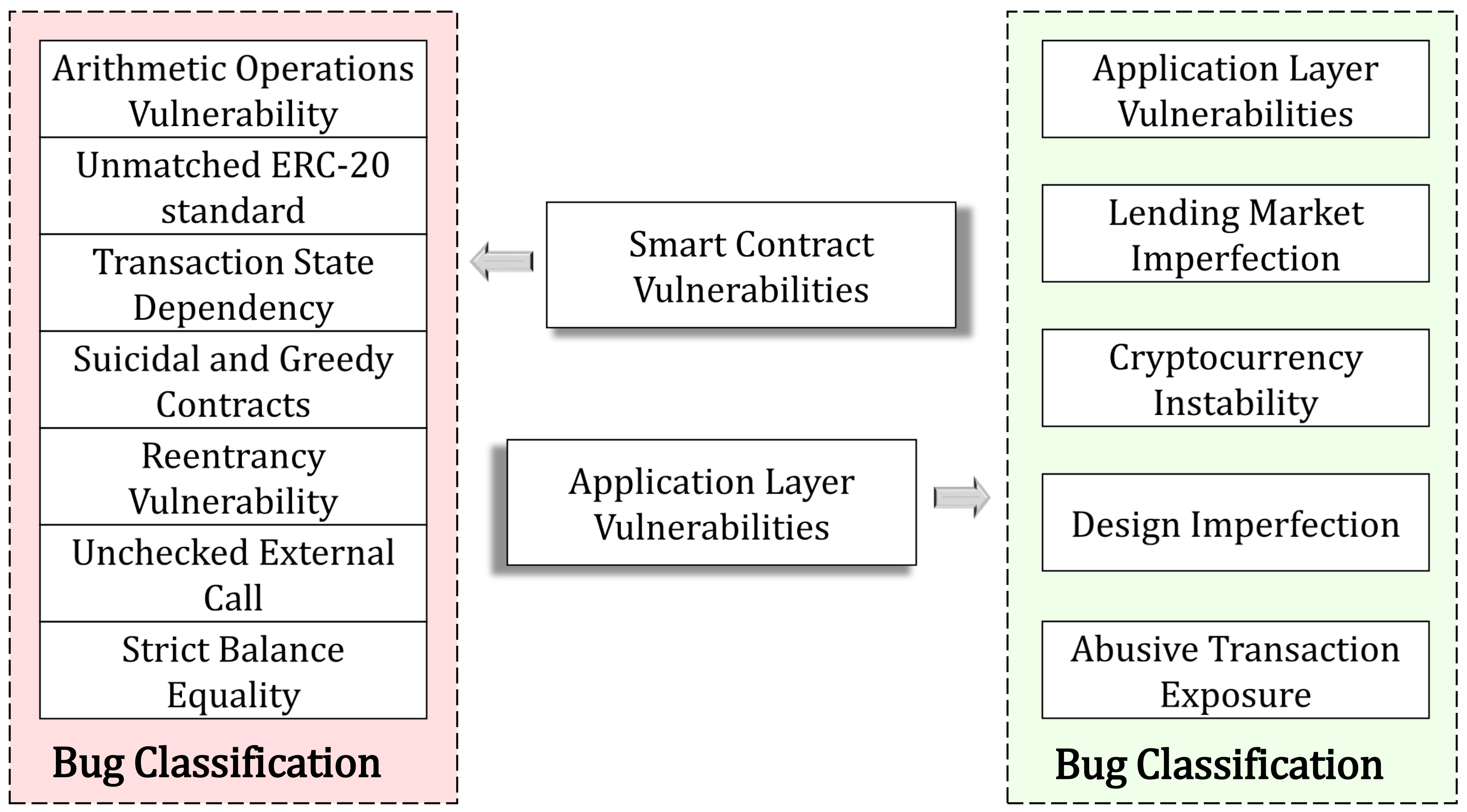

3.3 Smart Contract Vulnerabilities

There are 20 types of smart contract vulnerabilities in blockchain defined in (Chen et al., 2020a), of which Table 5 shows the weaknesses that attackers might use to make a profit. We searched Common Vulnerabilities & Exposures (CVE) and summarized over 500 vulnerabilities (CVE, 2022). In Figure 4, we describe the classification of smart contract vulnerabilities in this paper. And Table 5 shows that bugs written by Solidity were categorized into several types as detailed below:

| Categories | Causes | Categories | Causes |

| Unchecked External Calls | Without checking return values | Reentrancy | Repeated calls before completed |

| Unexpected Permission Check | Failure to check permissions | Nested Call | Unrestricted call depth |

| DoS Under External Influence | External exceptions inside loops | Missing Return | Denote return but no value |

| Unmatched ERC-20 Standard | Not follow the standard | Greedy Contracts | Receive but do not withdraw Ethers |

| Strict Balance Equality | Balance check failed | Block Info Dependency | Status in blocks leakage |

| Misleading Data Location | Incorrect storage type | Missing Interrupter | No backdoor to handle crises |

| Transaction State Dependency | Error using tx.origin | Arithmetic Bugs | Unmatched type to values |

3.3.1 Arithmetic Operations Vulnerability

There are a wide variety of bugs affecting the Solidity programming language. Common arithmetic manipulation bug includes integer overflow, float lack of precision, and division by zero.

An upward overflow can occur if a memory integer exceeds the maximum range, e.g., uint256 is a default type of integer that can express the number from to . In Listing 1, the function allows the owner to add tokens to the user, but a sufficient amount on line 3 can make the balance in balance[target] vanish.

Since Solidity lacks the float type of data structure, the phenomenon in which the float result of an operation might lose coins. When one integer is divided by a larger integer, the result is always 0. For example, 1 ETH divided by 10 Eth equals 0. Even some contracts do not restrict the operation of division by zero, which results in code logic errors as the result of the calculation becomes big infinitely.

3.3.2 Unmatched ERC-20 Standard

Ethereum provides various APIs for developers to implement certain functions, such as transferring money, but some developers may not adhere to all standards, resulting in problems in smart contracts. The ERC-20 standard is one of the APIs used to manipulate cryptocurrencies, including how to transfer tokens between addresses and access token data (Richards et al., 2022a). When transferring tokens, for example, transfer(), transferFrom(), and approve() will return a boolean value to indicate whether the function succeeded, and many smart contracts cause transfer mistakes since they do not verify the return value.

3.3.3 Transaction State Dependency

Contracts should check the permissions of certain sensitive invocations that use the global variable tx.origin, which points to the address in the entire call stack where the transaction was originally sent (Chen et al., 2021). Assume the Wallet contract in Listing 2 sends a transaction to the Attack contract, and then the attack() function invokes the transfer() function in the Wallet contract, at which point tx.origin meets the detection in line 6, making the success of the attack.

3.3.4 Suicidal and Greedy Contracts

Smart contracts usually include a provision enabling the owner to commit suicide if the contract is challenged. The SELFDESTRUCT operational code (opcode) in a suicidal contract can ignore all contract code logic, even the fallback() function (Li et al., 2021). However, attackers utilize this feature to corrupt the logic of some contracts, which leads to restrictions on all other operations that depend on the contracts. For example, the Parity wallet was attacked by a suicidal contract in 2017 (Li et al., 2020a), which resulted in a permanent lock of all cryptocurrencies that transferred to the wallet before the wallet maintainer fixed the vulnerability.

Similar to the suicidal contract, the greedy contract locks up the ether, but it is alive. Greedy contracts do not have instructions related to the withdraw and send (Nikolić et al., 2018), such as send, and transfer, so it locks all ethers and cannot withdraw. Therefore, making sure there are means to get ether out before transferring it to a contract (Chen et al., 2020a).

3.3.5 Reentrancy Vulnerability

The concept of threads does not exist in Solidity, so it cannot execute more than two operations concurrently. This means that when a contract initiates a call via call(), it must wait for the completion of the call before making the next call. However, it would be attacked if the callee contracts change the global state during the waiting (Luu et al., 2016). The DAO attack leverages the recursive invocations to make the system keep cycling until internal assets run out. It exits in line 4 of Listing 3 (Daian, 2016), where the original recipient continues executing call.value() after a successful transfer.

3.3.6 Unchecked External Call

The return value or the arguments of an external call can affect the states of the code. Many contracts do not check the return value, which leads to vulnerabilities. The mode of logic used in this bug is similar to that of misuse ERC-20 standard. When a function calls code logic outside the contract, it is equivalent to the entire runtime in a black box. At this point, failure to check the return value of the external call may cause the logic of the contract to break. For example, when multiple functions are nested, and the external call does not check, the return value of the internal call in time can go wrong (Chen et al., 2020a).

Smart contracts in the DeFi trade by using external call functions including delegatecall(), call(), send(). More crucially, a failed external call in these methods results in a transaction not being rolled back, which can cause logical effects.

3.3.7 Strict Balance Equality

Equations are commonly used in programs to make decisions concerning contract logic. When an attacker employs some methods, such as a suicide transfer ether, to alter the state of the variables utilized in the equation, rendering the judgments of the equation incorrect, the attack affects the logic of the code that follows the equation. For example, in Listing 4, when the balance in the account is 1 ether, it passes the check in line 2. In line 3, the attacker transfers ether into the account, causing the judgment to fail, so the transfer in line 4 does not follow the normal logic. It is a loophole caused by not fully checking the judgment conditions of the equation.

3.4 Application Layer Vulnerabilities

The application layer visualizes the state in the chain and interacts directly with the user. In this paper, we focus on DAPPs in the financial domain. DeFi applications generally suffer from price manipulation attacks similar to traditional centralized financial applications. With the current development, the problems in the application layer could be divided into lending market imperfection, cryptocurrency instability, design imperfection, and abusive transaction exposure in Figure 4.

3.4.1 Lending Market Imperfection

When the prices in the market are out of balance, it will result in bad debts for one of the participants in the lending market. To get more loans, attackers can boost the cryptocurrency exchange rate on the oracle by modifying the real-time price-related status before the loan is made. For example, an attacker can gain a larger quantity of tokens by directly manipulating token prices in the asset pool or increasing the price of collateral before lending (Wu et al., 2021), putting the borrower in danger of bad debt.

3.4.2 Cryptocurrency Instability

The large fluctuations of cryptocurrencies come from many reasons, one of which is the Pump-and-Dump. The instability can easily trigger liquidation procedures. Exchanges have chosen stablecoins, which are tied to the price of real-world money, as the pricing standard to minimize losses, but they still exist as a risk. For example, a 99.98 % plunge in May 2022 in the price of the luna coin, whose value is tied to a stablecoin called Terra, left the entire crypto market with over $700 million in collateral liquidated (Lyanchev, 2022).

3.4.3 Design Imperfection

The attackers utilize incorrectly configured functionality or specific convenience features of DeFi platform exchanges (Wang et al., 2021b). Flash loan is designed as risk-free loans to be a convenient improvement to the loan that needs to borrow the flash loan, exchange it for currency, and repay the loan in an atomic transaction. For example, attackers borrow the flash loan to receive collateral at a premium and make a profit in this atomic transaction (Yazdanparast, 2021), which results in bad debts for the users who borrow money from attackers.

3.4.4 Abusive Transaction Exposure

Exchanges disclose all transactions as soon as feasible to ensure completely behavioral transparency because off-chain matching services are not automated. Unfortunately, exchanges can restrict access to select users and launch Denial of Service (DoS) or Decentralized Denial of Service (DDoS) attacks (Baum et al., 2021) to dominate the market, audit transactions, and even front-run orders.

4 Analysis of Attack Events

In this section, we investigate real-world attacks in the DeFi ecosystem (CryptoSec, 2022; Bouteloup, 2022) and analyze the vulnerabilities exploited in the attacks with the classification shown in Figure 5.

| Vulnerabilities | Features | Victims | Platform | Date |

|

||

| Private Key Leakage | The private keys of DeFi deployers are under threat due to poor private key management or phishing attacks. The key authorizes and verifies the transactions of the user. When an attacker utilizes the key, it is simple to tamper with the transaction, putting the trader’s interests at risk. The attacker alters the website’s Application Programming Interface (API) and embeds the vulnerability to get the user’s personal information, including the user’s key. | Meerkat Finance | BSC | March 2021 | 31 | ||

| Paid Network | Ethereum | March 2021 | 160 | ||||

| Roll | Ethereum | March 2021 | 5 | ||||

| EasyFi | Ploygon | April 2021 | 80 | ||||

| bZx | Ethereum | November 2021 | 55 | ||||

| 8ight Finance | Harmony | December 2021 | 1 | ||||

| BitMart | Ethereum | December 2021 | 150 | ||||

| AscendEX | Ethereum | December 2021 | 77 | ||||

| Vulcan Forged | BSC | December 2021 | 140 | ||||

| LCX | Ethereum | January 2022 | 6 | ||||

| Ronin Bridge | Ethereum | March 2022 | 624 | ||||

| Poly Network | BSC | September 2021 | 600 | ||||

| Oracle Attacks | The oracle price data feed can be manipulated by the attackers who change the asset data for the smart contracts. When an oracle is attacked, real-world data posted to the blockchain changes. It mismatches on-chain data with the real world, harming users. | bZx | Ethereum | February 2020 | 0.9 | ||

| Harvest Finance | BSC | October 2020 | 24 | ||||

| Cheese Bank | Ethereum | November 2020 | 3 | ||||

| PancakeBunny | BSC | July 2021 | 2 | ||||

| Vee Finance | Multichain | September 2021 | 35 | ||||

| Vesper Finance | Ethereum | December 2021 | 1 | ||||

| DDoS Attacks | The attacker uses massive throughput to disrupt the device or server. | McAfee DEX | Multichain | October 2019 | – | ||

| Youbi DEX | Multichain | November 2020 | – | ||||

| Sandwich Attacks | Attackers use two transactions to clip victim’s transaction and profit from it. | Uniswap | Ethereum | May 2021 | 0.2 | ||

| Uniswap & Linch | Ethereum | August 2022 | 3.7 | ||||

| 51% Attacks | Attackers can create fraudulently some transactions, when they control over 50% of the blockchain’s computing power. | Ethereum Classic | Ethereum | January 2019 | 5.6 | ||

| ZenCash | Zendoo | June 2018 | 0.5 | ||||

| PegNet | Multichain | April 2020 | 0.6 | ||||

| Sybil Attack | Attackers create multiple fake nodes to influence the blockchain network state. | Solana | Solana | August 2022 | – | ||

| Ribbon Finance | Ethereum | October 2021 | 2.5 | ||||

4.1 Date Layer Events

4.1.1 Utilization of Private Key Leakage

The developer deploys DeFi applications on blockchain through private keys managed in the wallet. Also, users confirm and initiate transactions on the DeFi app through the private key. We summarize real-world DeFi security events due to private key leaks in Table 6. We believe there are two reasons for these security incidents: (1) poor management of secret keys; (2) phishing attacks.

Poor Management of Secret Keys. In the Meerkat Finance (Obelisk, 2021) incident, the administrator of the project used a private key and a false time lock in the contract. It transferred about $30 million worth of BNB tokens from the BNB Vault. In Listing 5 (Bscscan, 2021a), the administrator used the visual ambiguity of the number "0" and the letter "o" to make the variable slot values in the admin() and setAdmin() functions differently. This means that the time lock of BNB Vault is false, and the administrator can transfer the BNB tokens via the backdoor.

Phishing Attack. The scripts embedded in the DeFi website interact with the wallet, which may give opportunities for phishing attacks (Winter et al., 2021). In the BadgerDAO incident (BadgerDAO, 2021), the attackers stole the Badger developer’s secret keys and injected malicious scripts into BadgerDAO’s web pages. The scripts intercepted the user’s transactions and prompted the user to allow the attacker to operate on the ERC-20 tokens in their wallets.

The transparent nature of DeFi allowed the attacker to easily gather information about the developers. The attacker sent malicious emails to bZx developers, stealing the private management key of bZx deployed on the BSC and Polygon chains. The attackers used the management private key to upgrade the contract to mint unlimited tokens (bZx Contributor, 2021).

Backdoor Attack. A backdoor attack involves unauthorized access to a program or system that bypasses the software’s security checks. The input is only sent to the attacker’s subtask when the set trigger is activated. This attack does not affect the system’s regular operation, so only the attacker can trigger and profit from it. Furthermore, systems that automatically collect and process data, such as oracle, can reach the problem at the functional level. It can be through the introduction of data with hidden vulnerabilities in large quantities, in addition to the attacker inserting his event at the code level.

The Ronin Bridge network incident in Table 6 (Network, 2022), which is a sidechain of Ethereum, was attacked by a backdoor attack in March 2022. It established a new record for the most significant losses in the DeFi space with 624 million USD. There are nine authentication nodes in the Ronin chain, with access being granted after getting verification at five of them. Through a backdoor, the attacker has access to and control over the five private keys, the authentication, and thus the withdrawal event.

Hash Collision. When compiling the smart contract source code into bytecode, the first 4 bytes of the hash of the method name are used as the token. It can be utilized by an attacker to generate a signature that satisfies the specified 4-bytes token through a hash collision. When a contract can be executed by passing method names as parameters, it is possible to hack the contract by using the hash collision. The poly network case is where the attacker constructs specific method signatures through hash collisions to execute some special functions as a contract manager (SlowMist, 2021a).

In the PloyNetwork event (SlowMist, 2021a) on the BSC chain, the attackers used hash collisions to construct Keeper’s signatures and modified Keeper’s public keys through the putCurEpochConPubKeyBytes() function in the management contract. This incident resulted in a loss of 600 million USD.

4.1.2 Utilization of Oracle Vulnerability

The DeFi ecosystem relies heavily on oracle to provide off-chain or on-chain asset data, and cannot verify the accuracy of the data. This means that if the DeFi protocol uses only a single DEX as the source of asset prices, then the DeFi protocol will assume that it is true and accurate regardless of the movement of its asset price data.

In Table 6, oracle attacks have caused significant damage to DeFi applications. Most of the oracle attacks are based on the following steps (Wang et al., 2021c).

-

(i)

Preparation of Funds. The attacker borrows a large number of assets unsecured through various Flash Loan providers, e.g., bZx, dYdX. He/She intends to inject the assets into other DeFi agreements to inflate their prices while hoarding the target assets.

-

(ii)

Raising the Price of Target Assets. The attacker manipulates the oracle by balancing the target assets stored in the liquidity pool, i.e., by exchanging a large number of tokens back and forth between different liquidity pools. Since a single oracle is used, it passes the manipulated price data into the DeFi protocol.

-

(iii)

Profiting. The attacker exchanges the target asset for money borrowed by the Flash Loan, a service provided by DeFi, e.g., collateralized borrowing. As the attacker inflates the price of the target asset, it can exchange the target asset for a larger amount of other assets. By this step, the attacker will gain much profit.

-

(iv)

Loan Repayment. The attacker restores the assets in the liquidity pool to their initial state to avoid losses caused by price slippage (Wang et al., 2021c), and repays the loan.

The bZx attack (PeckShield, 2020) happened in February 2020, and it was through the above attack steps that the attackers made a profit of about $0.9 million. The attacker borrowed lots of ETH through the bZx platform. At KyberSwap AMM, a portion of the ETH was exchanged for sUSD tokens to drive up the price of sUSD. Next, the attacker bought the sUSD from the Synthetic Depot contract at the normal price. The attacker pledged the sUSD in the account into the bZx protocol in exchange for ETH. As the price of sUSD in bZx was inflated, it could be exchanged for more ETH. Finally, the attacker repaid the loan.

In 2021, Vee Finance lost 35 million USD due to the oracle vulnerability (Werner et al., 2021). It had only one oracle as a price input source. At the same time, the attackers profited by using errors in the contract to bypass the slippage protection checks. Similarly, the Harvest protocol used the USDT price in Curve as the price data. Since the USDT price became lower at this point, the attacker could pledge more USDT with the same assets. The attacker performed 32 attacks and profited 24 million USD from the protocol.

4.1.3 Distributed Denial of Service Attack Events

A Distributed Denial of Service (DDoS) attack can be a DOS attack performed on multiple nodes to some extent. Due to the large number of nodes and the unpredictability of block-generating nodes, DoS attacks on blockchain systems such as Ethereum are less detrimental. However, the DDoS attack can typically cause network nodes to fail or slow down transactions across the network by running out of memory due to many transaction requests. It causes these nodes to be unable to close the transaction they are processing, and other nodes are unable to perform the transaction. Attackers typically combine other attacks to cause damage to blockchain-based DeFi applications.

Numerous DeFi applications in Table 6, such as McAfee (Adam and Jose, 2019) and Youbi DEX (BEOSIN, 2020), have recently been subjected to DDoS attacks, causing substantial harm to the DeFi ecosystem. At the initial launch, the McAfee DEX was under a DDoS attack. Due to the number of user nodes being insufficient, the failure of some users had a more significant impact on the entire network.

4.2 Consensus Layer Events

4.2.1 Sandwich Attack Events

Sandwich attack capitalizes on miners’ pursuit of MEV by reordering transactions to achieve the attack’s objective. According to the consensus rule, the node with control over the block can choose the order of transactions. The dependency on transaction order vulnerability is one of the factors affecting the security of smart contracts, and it also applies to DeFi applications.

The Sandwich attack applies to AMMs like Uniswap and takes advantage of a special feature of AMMs, such as the fact that for every token swap that occurs on an AMM like Uniswap, the price of its swapped tokens changes. The steps of the Sandwich attack are as follows:

-

(i)

Network Spy. There are some spy nodes deployed on the network to collect all the transactions for asset exchanges. If attackers consider that a transaction that exchanges token for token is profitable, they will create two transactions for racing to control the transaction and make a profit. It means that the price of token in the liquidity pool will be increased.

-

(ii)

Transaction Creation. The attacker creates a front-running transaction to exchange token for token , and the price of token in the liquidity pool will be raised. Suppose the price of token rises too much. In that case, the slippage detection may be triggered, and the attack will be failed, so the attacker will generally control the number of tokens purchased. The victim is also exchanging token for token , which causes the price of token to continue to rise. As the attacker’s front-running trading causes the price of token to rise, the victim can only obtain less than the expected amount of token . Finally, after the victim’s transaction, the attackers would create a back-running transaction that converts token into token , thus making a profit.

According to our research, sandwich attacks often occur on AMMs, such as Uniswap, Linch, and SushiSwap. About 4 thousand sandwich attacks have occurred on Ethereum, which allowed the attackers to generate a profit of 3.7 million USD (EigenPhi, 2022).

4.2.2 51% Attack Events

To achieve the 51% attack, the attacker creates a transaction that transfers tokens to the victim (Moroz et al., 2020). Concurrently, the attacker generates an alternative chain. If more than 51% of nodes in the network support the alternative chain generated by the attacker, the consensus mechanism deems the original chain invalid. The attack requires most of the computing power in the whole network, so the greater the computing power of honest nodes on blockchain platforms, such as Bitcoin, the more difficult it is to profit from the attack (Crypto51, 2022).

In Table 6, we gathered some DeFi projects with 51% attacks. Considering the significance of the situation, the amount of damage is not particularly severe. The 51% attack exploits a well-known vulnerability that manifests itself frequently in decentralized exchanges.

4.2.3 Sybil Attack Events

To execute a Sybil attack, the attacker typically chooses to control the network through multiple accounts or nodes. The attack slows down the entire network and can impact DeFi transactions when the number of affected nodes exceeds a certain threshold.

In Table 6, a Sybil attack in 2022 was observed on Solana, where the attacker kept constructing a network of protocols to deceive asset owners into believing they were popular, resulting in the TVL of 7.5 billion USD. Ribbon Finance is an option-based financial program. It is constantly creating as many wallets as possible in 2021 to profit from airdrops to users with more than $100. The Sybil attack has significantly impacted asset market users in terms of their regular trading and losses.

4.3 Contract Layer Events

Smart contracts are the basis for decentralized financial instruments. When the DeFi applications were deployed on the blockchain (Torres et al., 2018), it was possible that smart contract errors would cause irreparable harm to DeFi.

4.3.1 Utilization of Arithmetic Vulnerability

Almost every DeFi use case involves performing arithmetic operations on different forms of currency. Among these operations are adjusting account balances by adding or subtracting amounts and converting exchange rates between various tokens (Werner et al., 2021). In the DeFi ecosystem, overflow and precision loss vulnerabilities have been identified. These arithmetic bugs have caused significant damage.

Overflow. In April 2018, multiple DeFi applications on Ethereum, including OKEx, were forced to shut down because of an overflow vulnerability in an ERC-20 token contract. MESH and UGToken were among these applications. OKEx was one of the applications forced to close due to astronomical losses. This overflow event shares several characteristics, including the difficulty caused by the transferProxy() function in Listing 6 (Etherscan, 2018).

In line 2 of Listing 6 (Etherscan, 2018), it contains the potentially dangerous overflow vulnerability. Since both fee and value are input parameters, and they are susceptible to be manipulated by humans. An adversary can then construct the incoming parameters so that their size exceeds the storage range of the uint data type, resulting in an overflow. When an overflow occurs, the entire value of the unsigned integer becomes 0. It indicates that an attacker can bypass the check performed by the if statement on the second line (Billy, 2018) and cause tokens to be transferred to an empty address.

Underflow. The larger loss in arithmetic vulnerability is Compound Finance. Its reward payouts CompSpeed could be set to 0, which indicated that reward payouts were suspended, and the market award index supplyIndex was 0. For new users, their award index supplierIndex was initialized to CompInitialIndex presented by Compound as . An underflow vulnerability occurred in Listing 7 (Flatow et al., 2021) at line 8. This caused the formula for calculating the difference in the index deltaIndex = sub_(supplierIndex = 0, supplierIndex=) to underflow and became a very large value, while the Compound Finance reward calculation relied on the value of deltaIndex.

There was no attacker in this security incident, but rather an overpayment of rewards due to an underflow vulnerability in the contract. This incident caused the Compound 80 million USD in damages. In 2022, Umbrella NetWork also lost 0.7 million USD due to an underflow vulnerability.

| Vulnerabilities | Features | Victims | Platform | Date |

|

||

| Arithmetic Vulnerability | The attacker passes in specific parameters that cause the arithmetic operations in the contract to overflow. | Uranium Finance | BNB | April 2020 | 50 | ||

| Compound | Ethereum | September 2021 | 80 | ||||

| Pizza DeFi | EOS | December 2021 | 5 | ||||

| Umbrella Network | Ethereum | March 2022 | 0.7 | ||||

| Reentrancy Vulnerability | When a function calls an untrusted contract and that contract recursively calls the original function, it’s reentrant. | dForce | Ethereum | April 2020 | 24 | ||

| Akropolis | Ethereum | November 2020 | 2 | ||||

| Grim Finance | Fantom | December 2021 | 30 | ||||

| Logical Vulnerability | The adversary employs unique methods to alter the contract program logic inadvertently and cause the loss of the DeFi application. It comprises possessing a token copy, low-level calls, self-destroying, and transaction rollback attack. | Betdice | EOS | December 2018 | 3 | ||

| EOS MAX | EOS | December 2018 | 0.9 | ||||

| Ethereum Classic | Ethereum | January 2019 | 0.5 | ||||

| Furucombo | Ethereum | February 2020 | 14 | ||||

| bZx | Ethereum | November 2020 | 8 | ||||

| BurgerSwap | BNB | May 2021 | 7 | ||||

| Eleven Finance | Polygon | June 2021 | 4 | ||||

| Punk Protocol | Ethereum | August 2021 | 3 | ||||

| Starstream Finance | Ethereum | April 2022 | 4 | ||||

| Flash Loan | It allows users to borrow and settle loans in real-time in a single transaction without providing any collateral. | Warp Finance | Ethereum | December 2020 | 7 | ||

| Alpha Homora | Ethereum | February 2021 | 37 | ||||

| Elephant Money | BNB | April 2022 | 11 | ||||

| Pump-and-Dump attack | The attacker organizes many individuals torise significantly for a brief period and profits from it. | Cryptopia DEX | Multichain | November 2018 | 157 | ||

| Binance DEX | BNB | May 2019 | 50 | ||||

| Squid | BNB | November 2021 | 300 | ||||

Accuracy Loss Vulnerability. The Uranium Finance contract allowed users to borrow money using Flash Loan. However, the contract suffered from accuracy handling errors when calculating the amount to be returned, resulting in the amount that was 100 times larger than expectation (SlowMist, 2021b). The attacker only needs to return a small portion of the loan to pass the check of the require statement in Listing 8 (Bscscan, 2021b) and pays off the loan.

4.3.2 Utilization of Reentrancy Vulnerability

A contract executing a transaction invokes a malicious contract account, and the malicious contract account invokes a function in the contract before the contract state changes (Rodler et al., 2019). The most significant reentrancy attack on Ethereum was the DAO attack (Buterin, 2016), which caused a hard fork of Ethereum by constantly calling the withdrawBalance() function to achieve an infinite transfer operation. Reentrancy attacks were applied to the DeFi protocol with its development. In Table 7, 54 million USD was lost to DeFi due to a reentrancy vulnerability.

In April 2020, the dForce protocol suffered a reentrancy, losing about 24 million USD. The attackers exploited the ERC-777 (Richards et al., 2022b) compliant imBTC tokens. Compared to the ERC-20 token standard, the ERC-777 token standard has one feature. When ERC-777 tokens were sent or received, they would go through Hook in the form of a callback to notify the sender or recipient. The attacker in the incident (Werner et al., 2021) took advantage of this feature and re-entered the dForce contract to increase the amount of imBTC collateral and get a higher yield.

Grim Finance on the Fantom (Cronje et al., 2022) chain lost 30 million USD due to a re-entry vulnerability. First, the attacker created a contract to inject the cryptocurrency borrowed through the Flash Loan service into Spirit Swap (SpiritSwap, 2022) to obtain Spirit-LP certificates. Next, the Spirit-LP certificates were pledged to the GrimBoostVault contract in exchange for the GB-BTC-FTM, which was a token, via the depositFor() function in Listing 9 (FTMScan, 2021). Since the legitimacy of the token contract was not verified, the attacker re-called the depositFor() function in the safeTransferFrom() function of the malicious contract, implementing reentrancy to collateralize more GB-BTC-FTM for profit. The attacker has finally paid back the loan.

4.3.3 Utilization of Logical Vulnerability

According to our investigation, a large number of vulnerabilities in the DeFi application stem from the simple programming errors in the smart contract (Werner et al., 2021). Due to the tamper-evident nature of the blockchain, these errors can cause significant damage to the DeFi application.

Token Copy. This was the third attack on bZx in 2020. The attackers exploited a vulnerability in the contract by passing the same address to the sender parameter balancesFrom and the receiver parameter balancesTo in the bZx contract, thus copying the balance in the account (Kistner, 2021).

Low-level Calls. Starstream Finance on Ethereum is a DeFi project on the Metis Andromeda network. As seen in Listing 10 (Baranov, 2022), the vulnerability was due to the public function execute() of the DistributorTreasury contract using an unchecked external call to.call(), allowing anyone to make an external call. It meant that an attacker could use the function to generate a call to the withdrawTokens() function to extract the STAR Token in the StarstreamTreasury contract.

Self-destruction. Self-destruction of contracts and destruction of tokens in contracts are both common operations in the DeFi ecosystem. Usually, attackers will transfer stolen valuable cryptocurrency into the contract under their control. To avoid being traced, the attackers will destroy the attack contract after transferring the tokens in their contracts.

The Eleven Finance attack (REKT, 2021) was caused by the fact that the attacker could not destroy the proof of assets when withdrawing them from the contract, thus enabling the withdrawal of the deposit twice. The specific reason for this attack was that the emergencyBurn() function in the ElevenNeverSellV insurance contract allowed the attacker to withdraw the deposited assets without destroying their proofs. Afterward, the attacker called the withdraw() function in Listing 11 (Eleven, 2021) to perform the normal process of withdrawing the assets. This incident caused a loss of approximately 4 million USD to Eleven Finance on the Polygon chain.

Transaction Rollback Attack. Several blockchain platforms, including TORN, EOS, etc., have been subject to transaction rollback attacks. Hackers use an inline function to undo a transaction. There are multiple activities within a transaction; as long as one activity is abnormal, all the activities in the transaction will fail. For example, in 2019, attackers in Ethereum Classic rolled back transactions by coding their contract service (DAN, 2019). They continued attempting until the result of the function call satisfied the requirements. As the result in Table 7 shows, multiple double spending vulnerabilities were introduced into Ethereum Classic, acquiring approximately 0.5 million USD.

4.4 Application Layer Events

Some application layer attacks are caused by the lending market imperfections and abusive transaction exposure, whereas design imperfections and cryptocurrency instability directly cause others. The Pump-and-dump attack is a result of the cryptocurrency instability, and the use of Flash Loan is a result of the design imperfections. Some DDoS attacks in Section 4.1.3 cause the lending market imperfections, and the sandwich attacks caused by the abusive transaction exposure are in Section 4.2.1.

4.4.1 Utilization of Flash Loans

Flash Loans are an unsecured form of lending that adds vitality to DeFi. Blockchain transactions’ atomicity validates these loans’ legitimacy at the execution time (Qin et al., 2021c). Unfortunately, attackers have access to Flash Loan, reducing the cost of their attack. According to our survey results, most DeFi attacks targeted Flash Loan services.