The heat modulated infinite dimensional Heston model and its numerical approximation

Abstract.

The HEat modulated Infinite DImensional Heston (HEIDIH) model and its numerical approximation are introduced and analyzed. This model falls into the general framework of infinite dimensional Heston stochastic volatility models of (F.E. Benth, I.C. Simonsen ’18), introduced for the pricing of forward contracts. The HEIDIH model consists of a one-dimensional stochastic advection equation coupled with a stochastic volatility process, defined as a Cholesky-type decomposition of the tensor product of a Hilbert-space valued Ornstein-Uhlenbeck process, the mild solution to the stochastic heat equation on the real half-line. The advection and heat equations are driven by independent space-time Gaussian processes which are white in time and colored in space, with the latter covariance structure expressed by two different kernels. First, a class of weight-stationary kernels are given, under which regularity results for the HEIDIH model in fractional Sobolev spaces are formulated. In particular, the class includes weighted Matérn kernels. Second, numerical approximation of the model is considered. An error decomposition formula, pointwise in space and time, for a finite-difference scheme is proven. For a special case, essentially sharp convergence rates are obtained when this is combined with a fully discrete finite element approximation of the stochastic heat equation. The analysis takes into account a localization error, a pointwise-in-space finite element discretization error and an error stemming from the noise being sampled pointwise in space. The rates obtained in the analysis are higher than what would be obtained using a standard Sobolev embedding technique. Numerical simulations illustrate the results.

Key words and phrases:

stochastic partial differential equations, infinite dimensional Heston model, forward prices, stochastic heat equation, stochastic advection equation, reproducing kernel Hilbert spaces, finite element method1991 Mathematics Subject Classification:

60H15, 60H35, 65M60, 46E22, 46N301. Introduction

This paper introduces the HEat modulated Infinite DImensional Heston (HEIDIH) model as a special case of the infinite dimensional stochastic volatility model of [8] and study its numerical approximation. We give a background to the class of models considered in [8] before discussing our results in detail.

1.1. Stochastic volatility models in infinite dimensions

In the last few years, infinite dimensional stochastic volatility models have garnered increasing interest from both analytical (e.g., in [8, 16, 12, 13]), financial (in [7, 4]), as well as most recently (see [5, 29]) also from numerical perspectives. One of the motivations stems from modeling the risk-neutral dynamics of the forward price of a contract at time delivering a commodity (e.g., an instantaneous amount of energy) at time . Under a Musiela parametrization the dynamics are interpreted as solving a stochastic partial differential equation (SPDE) on . The solution is formally given by

| (1) |

with initial value . Here is the left-shift semigroup on functions on , is a family of Brownian motions and an appropriate stochastic volatility term. This is made rigorous by interpreting (1) as the mild solution of a stochastic evolution equation in a Hilbert space (in the Da Prato–Zabczyk framework [17]) of continuous and eventually constant functions on , driven by a Wiener process in . We emphasize that (1) models the risk-neutral dynamics of forward prices. For the actual market dynamics one would need to include additional terms, such as a seasonality dependent drift. We refer to [6, 7] for more details on the infinite dimensional approach to forward price dynamics in commodity markets, as well as to [25, 20] for predecessor models in interest rate markets.

Once the model (1) has been completely specified (by choosing and appropriately), a natural next step is to analyze the numerical approximation of the forward problem. By this we mean the problem of simulating approximate realizations of (1) and quantifying the uncertainty stemming from the numerical approximation necessary in any infinite-dimensional model. This is important, not only for Monte Carlo approaches to pricing derivatives written on , but also to efficiently solve inverse problems stemming from real-world data using approaches that rely on simulations of (1), such as machine learning algorithms.

1.2. The HEIDIH model

In this paper, we present, analyze and study the numerical approximation of the HEIDIH model. It is a special case of the infinite dimensional stochastic volatility model introduced in [8, 4], in turn a special case of (1). The price process and a volatility process are coupled via another process in the system of stochastic evolution equations

| (2) |

for . Here a Hilbert space of functions on on which the semigroup is strongly continuous. With being another strongly continuous semigroup, and denote the generators of and , respectively. By and we denote two independent cylindrical Wiener processes in . The operator-valued mapping corresponds to in (1) and is given by . Here, the stochastic process takes values on the unit ball in and denotes the Hilbert tensor product. The process is an intrinsic part of the model and each choice yields different dynamics. One example is the setting for all , where is a deterministic function with unit norm. Another is obtained by letting for and otherwise. In any case , where is the adjoint of , so that is a square root of the stochastic variance process [8, Proposition 7]. This is why the system is referred to as a Heston stochastic volatility model in Hilbert space.

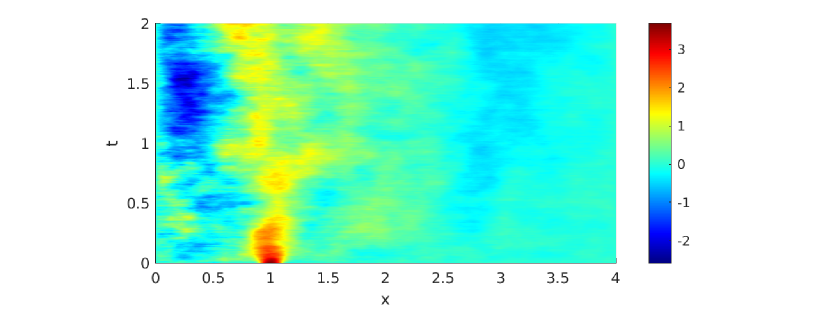

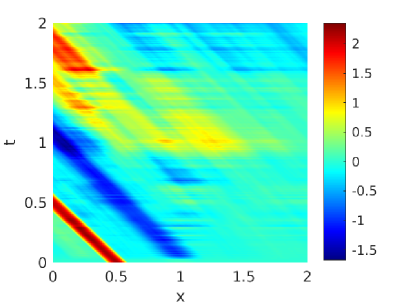

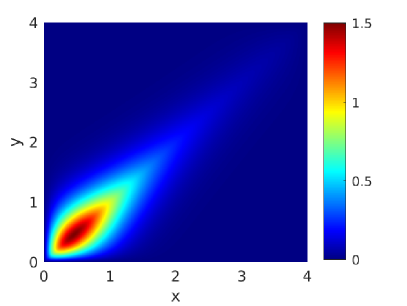

The HEIDIH model is obtained by specifying in (2), which is the Laplacian with either Dirichlet or Neumann boundary conditions at coupled with a diffusivity constant . Then is the solution to a stochastic heat equation. For the state space we adopt the setting of [19] and choose where is a fractional Sobolev space and . Then and may be regarded as random field-valued processes. An example of a realization of and for this model when for all and fixed is shown in Figures 1(a) and 1(b), see Remark 4.6 for precise parameter choices.

We emphasize that to analyze the numerical approximation of (2) in detail, both the generator and the Hilbert space have to be completely specified. We believe the HEIDIH specification may be appropriate since

-

(i)

the model directly displays the Samuelson effect. This says that the volatility should be decreasing in time to maturity (see, e.g., [3] for a discussion of this in a commodity pricing context) i.e., that as the time to maturity . This is obtained from the fact that , see also Figure 1(a). Moreover,

-

(ii)

by properties of the heat kernel, as (see Figure 1(c)). The left-shift property of the semigroup implies that

The dependence of the volatility of with regards to time to maturity is therefore local. This is realistic, since contracts close in maturity affect each other. Furthermore,

-

(iii)

freedom is still left to the practitioner to specify the model further given the specific context at hand. This is done in a parsimonious way by appropriately choosing the coefficient (which regulates the degree to which the dependence of the volatility with regards to time to maturity is local) the initial functions and and the dynamics of and in terms of their covariance kernels. Finally,

-

(iv)

precise regularity results and approximation convergence rates can be obtained under realistic conditions on the covariance kernels of and , which is vital to designing an efficient simulation algorithm.

The latter point is the main focus of our paper, which contains, to the best of our knowledge, the first analysis of the numerical approximation of the infinite dimensional Heston model introduced in [8, 4]. Note that the model may easily be modified by adding additional terms to either of the equations in (2) without violating the validity of the points above. For instance, one may add a deterministic drift term to corresponding to seasonal volatility, which might be present even under the risk-neutral measure.

1.3. Contributions of this paper

Having introduced the model, let us now enumerate the main contributions of this paper.

In the context of forward pricing, the properties of are often discussed in terms of its (incremental) covariance kernel . At the same time, it is common to assume that is a -Wiener process, see, e.g., [2, 8, 4]. It is, however, rare to find any discussion on what properties a given kernel should have in order for (or ) to be well-defined in either as a cylindrical or as a -Wiener process, thus allowing for the existence of in a given Hilbert space . Thanks to our particular choice of state space from [19], we are able to

-

(i)

completely characterize the kernels that yield classical -Wiener processes in (Theorem 3.1) and

-

(ii)

construct a class of kernels, which we call weight-stationary kernels, that allow for precise regularity and sharp numerical convergence results for and (Theorem 3.4).

The constructed class includes weighted versions of kernels commonly encountered in applications, such as Matérn kernels. We believe these general ideas are of interest also for infinite-dimensional models outside the context of forward price modeling in commodity markets. Note that no results of this nature are present in [19]. Since the underlying spatial domain is unbounded, non-trivial arguments are needed to derive these theorems, including the use of results from [24] on the decay of entropy numbers of embeddings between weighted Besov-type spaces.

When analyzing a numerical approximation of the HEIDIH model, the most natural errors to analyze are pointwise in space, since evaluated at corresponds to the forward price of a contract with maturity time . Like most algorithms in the numerical analysis literature on SPDEs, the convergence rates of our particular approximation depend on the regularity of the parts making up the model, in particular on and . Whereas Sobolev regularity (as well as existence and uniqueness) of and follow from classical results of [17] and [28] when weight-stationary kernels are considered for and , it turns out that this is not enough for pointwise-in-space. Instead, for sharp numerical results, we have to derive

-

(iii)

spatiotemporal regularity estimates of in a Hölder sense (Proposition 4.3) applicable to weight-stationary kernels.

These estimates cannot be obtained from classical results via a Sobolev embedding technique.

Having studied the regularity of the model, the component is approximated by means of a fully discrete finite difference scheme. We supply

- (iv)

The resulting error depends on how well the process can be approximated. We then focus on approximation of in the special case of Dirichlet boundary conditions and . A backward Euler discretization in time is combined with a finite element approximation in space. While this particular discretization of the stochastic heat equation is well-studied (see Section 6 for a comparison to existing results), the situation in our case stands out for three reasons. First, we need to take into account a truncation of our unbounded domain , resulting in localization errors. Second, we consider pointwise-in-space errors, which means we cannot rely on standard estimates for the finite element method. Third, we need to simulate the noise efficiently using the circulant embedding method, which results in an additional source of errors, since the noise is interpolated rather than projected onto the finite element space. With this in mind, we

-

(v)

derive sharp error convergence estimates for the approximation of (Proposition 5.4) which shows how the error depends on localization, SPDE discretization and noise interpolation error sources.

The sharpness is demonstrated in simulations (Figures 2 and 3). Combining Propositions 5.1 and 5.4, we then finally

-

(vi)

obtain a full error estimate for the approximation of (Theorem 5.8).

This estimate states how the error for the approximation of depends on the quality of the approximation of . Not only is this relevant from a mathematical point of view, but has practical implications too. The explicit dependence of the error on the different sources outlined above informs practitioners how the computational effort should be divided so that each source contributes equally. This leads to a computationally efficient algorithm. We demonstrate this point in simulations using different choices of spatial and temporal step sizes for (Figures 4 and 5). Our earlier regularity theory reveals how the different step sizes should be tuned for computational efficiency, connecting theory to practice.

1.4. Outline

We end this section with a brief outline of this paper. In Section 2 we introduce the necessary mathematical background and notation. Section 3 contains our results on cylindrical Wiener processes in , followed by the regularity theory for the HEIDIH model in Section 4. Our numerical analysis along with accompanying simulations are contained in Section 5. In Section 6 we discuss how our results relate to the existing literature for numerical approximations of SPDEs and outline future work.

2. Preliminaries

This section briefly presents the mathematical machinery necessary for our results.

2.1. Notation and operator theory

Let and be Banach spaces. All Banach spaces in this paper are taken over unless otherwise stated. We denote by the space of bounded linear operators from to equipped with the usual operator norm. If and are separable Hilbert spaces we write for the space Hilbert–Schmidt operators. This is a separable Hilbert space with an inner product, for an arbitrary ONB (orthonormal basis) of , given by

We have if and only if and their norms coincide. We use the shorthand notations and when and we write for the class of positive semidefinite operators when is a Hilbert space. For operators , we say that they are trace class if for one, equivalently all, ONBs of .

For Hilbert spaces and , the tensor is regarded as an element of by the relation for and .

We need the concepts of approximation and entropy numbers from [37]. Both types of numbers are used to derive suitable properties of a class of covariance kernels in Theorem 3.4. Approximation numbers also comes into the numerical analysis of the stochastic heat equation approximation in Proposition 5.4. Given a linear operator between Banach spaces and , its th approximation number is given by

, while its th entropy number is

Here and denote the unit spheres in and , respectively. By [37, Theorems 11.2.3, 12.1.3], both types of numbers satisfy

| (3) |

Both numbers are also multiplicative in that, if and for some additional Banach space , then

| (4) |

for all [37, Theorems 11.9.2 and 12.1.5]. If and are Hilbert spaces, then

| (5) |

for all and

| (6) |

where denotes the usual space of -summable sequences [37, Theorems 11.3.4, 12.3.1 and 15.5.5]. Taking (3) and (4) into account, this means in particular that is an operator ideal.

For two Banach spaces and , we write if and for some constant and all , i.e., the embedding operator . For Hilbert spaces, we write as shorthand for

Throughout this paper, we adopt the notion of generic constants, which may vary from occurrence to occurrence and are independent of any parameter of interest, such as spatial or temporal step sizes. By , for , we denote the existence of a generic constant such that .

2.2. Reproducing kernel Hilbert spaces

We make heavy use of the theory of reproducing kernel Hilbert spaces (RKHSs). The properties that we are going to need are listed here, we refer to, e.g., [9, 44] for further details. Throughout the paper we consider symmetric positive semidefinite kernels on a non-empty subset but usually just refer to as a kernel on when there is no risk of confusion. A Hilbert space is said to be the RKHS of a kernel if it is a Hilbert space of real-valued functions on a non-empty index set such that the conditions

-

(i)

for all and

-

(ii)

for all ,

are satisfied. The property (ii) is referred to as the reproducing kernel property of the space . For each kernel there is one and only one Hilbert space of functions on with these two properties. Moreover, a Hilbert space of functions on is a RKHS if and only if the evaluation functional , defined by , is continuous for all [44, Theorem 10.2]. We write for when it is clear from the context what index set we have in mind. Since is positive semidefinite, for all .

If is separable with an ONB , [9, Theorem 14] yields the kernel decomposition , the sum being convergent in . This implies that with convergence in . For index sets that are domains in , continuity of is a sufficient condition for separability [9, Theorem 15].

Suppose that we are given two RKHSs on an index set with kernels and . Then if and only if there is some constant such that is a positive semidefinite kernel [1, Theorem I.13.IV, Corollary I.13.IV.2]. We express this by writing .

For any Hilbert spaces and operator , we may interpret the range as a Hilbert space when equipped with the inner product , where is the pseudoinverse of [38, Proposition C.0.3]. The norm on may also be represented by

see [38, Remark C.0.2]. Applying this to a RKHS and the operator that restricts functions on to functions on a subset , it follows from [9, Theorem 6] that maps to and with equal norms. Moreover, by [44, Theorem 10.46] there is a linear extension operator of functions on to functions on such that .

2.3. Fractional Sobolev spaces

For a possibly unbounded , we write , , for the usual Banach space of -integrable equivalence classes of functions with respect to the Lebesgue measure. We omit when it is clear from the context which domain we refer to. The fractional Sobolev space , , is a separable Hilbert space and a generalization of the usual Sobolev space , . It consists of all such that

where is the Fourier transform of . For , the fractional Sobolev space , , consists of all for which for some . It is equipped with the norm

Since is an interval, has a bounded extension operator. It therefore coincides with the usual Sobolev space with equivalent norms. We refer to [40, Chapter VI] for more details on this. In terms of the restriction operator , we have with equal norms. We again omit from when it is clear from the context which domain we refer to.

If , then , , is a RKHS with a stationary (that is, for ) kernel given by

see [44, Chapter 10]. Here denotes the modified Bessel function of the second kind and order . Note that is continuous and bounded on . By the reproducing property, we obtain that all functions are continuous and bounded, which is a special case of the classical Sobolev embedding theorem.

We also make use of the weighted spaces where . For these we introduce the weight function given by for . We set . These are special cases of the weighted spaces considered in [24], which we refer to for further details, see also [42, Theorems 2.3.9 and 2.5.6]. They are Hilbert spaces equipped with the inner product . For , with the embedding being compact if and only if both inequalities are strict and [24, Theorem 2.3]. For , we note that for all and that for ,

From this, we obtain that is a RKHS with kernel .

The state space that we will work with for the HEIDIH model is given by , . We define it for . It consists of all where and . It is equipped with the norm

When , it is a RKHS with a kernel given by . We consider as a subspace of by identifying it with .

3. Cylindrical Wiener processes in fractional Sobolev spaces

In this section, we recall the concept of cylindrical Wiener processes with a focus on processes that have a covariance kernel. We prove a result that completely characterizes -Wiener processes in the state space . Then, we outline the assumptions on the kernels and that are made in the forthcoming sections. Finally, we construct the class of weight-stationary kernels, that fulfill all the assumptions made.

Consider , a filtered probability space fulfilling the usual conditions and a Hilbert space . We follow [39] and define a (strongly) cylindrical Wiener process as a process such that is a real-valued Wiener process for all . This definition agrees with what is called a generalized Wiener process in [17].

Given a separable RKHS with ONB and a sequence of real-valued Wiener processes, we construct a cylindrical Wiener process in by

| (7) |

which converges in , see [39, Remark 7.3]. Note that for . The representation does not depend on in the sense that if is another ONB of and we define a real-valued Wiener processes by , then

If is another Hilbert space such that , we obtain a cylindrical Wiener process in by replacing in (7) with . In , will have an incremental covariance operator given by in the sense that for all . Similarly, has covariance in . These operators have unique positive square roots. By [17, Corollary B.3], . In this sense, the distribution of does not depend on the choice of in (7). Therefore, we are justified in calling a cylindrical Wiener process with kernel and need not specify in which Hilbert space we consider it.

The SPDEs we consider in the paper are built on stochastic integrals with respect to cylindrical Wiener processes . Consider a predictable process . Itô integrals taking values in are well-defined with

for , provided that the integral on the right hand side is finite. We refer to [39] and [17, Section 4.2] for more details on Wiener processes in Hilbert spaces and the Itô integral.

If , the sum

converges in . It is then called a -Wiener process, and its covariance operator is trace-class. It induces a cylindrical Wiener process by and we do not make a notational difference between the two concepts. Many papers dealing with SPDE models for forward prices assume that is a -Wiener process, see, e.g., [4, 8]. It is therefore important to clarify when this is the case in our setting with the state space . The following theorem completely characterizes the kernels that satisfy , so that is a -Wiener process in .

Theorem 3.1.

There is a separable RKHS such that if and only if there is a separable RKHS such that , a function and a constant with

for all .

If this holds for , then the cylindrical Wiener process with kernel is an -valued -Wiener process and fulfills

for all .

If this holds for , then is a mean square continuous and bounded random field for all and for all .

Note that if for some , without the property of the embedding, there might not be a -Wiener process with covariance function . However, as long as , this theorem shows that we can still interpret as the covariance function of in a weaker sense. One might also consider embeddings in negatively weighted spaces. We do not pursue this direction but focus instead on constructing kernels such that .

Proof of Theorem 3.1.

First, suppose that there is a separable RKHS such that . Let be an ONB of and write with . Since

| (8) |

we have . Moreover, due to the fact that , the evaluation operator is well-defined on . Since

we may define a kernel by

for . The kernel is symmetric and positive semidefinite. We define a Hilbert space by

An ONB of this space is . Moreover, is a RKHS: for and ,

Since also and , we find that is the RKHS of . The fact that follows directly from (8). Let . Then

where the split is justified by and for all . By setting and we obtain one direction of the first claim of Theorem 3.1. The other direction is obtained by analogous arguments.

For the second claim, consider the same setting as above. Since ,

| (9) |

Applying this identity with yields

The exchange of summation and integration in the last step is justified in the first case by

using Hölder’s inequality twice. The justification in the second and third cases is similar.

Up to this point, we have let denote a general cylindrical Wiener process. We now introduce the key assumptions on the kernels of and in (2) which we use to deduce regularity results for this system in Section 4. Due to the presence of the term in (2), the assumptions mostly concern the covariance of .

Assumption 3.2.

Let and in (2) be cylindrical Wiener processes with kernels and , respectively. Let and . Assume the following for the RKHSs and on :

-

(i)

The embedding holds true.

-

(ii)

The embedding holds true.

-

(iii)

There is an ONB of such that .

We also need the following assumption for our numerical analysis of approximations to in Section 5.

Assumption 3.3.

Under the same conditions as in Assumption 3.2, let be defined on . For some and , .

We end this section with an example of a class of kernels that fulfill all parts of these assumptions. They are based on stationary kernels that are positive definite, integrable and continuous on . We recall that under these conditions, has a positive Fourier transform which is also integrable on , see [44, Chapter 6].

Theorem 3.4 (Weight-stationary kernels).

Let be a stationary positive definite kernel with a spectral density such that for some constant , , for all . Let be a continuous symmetric function such that the mapping , , is bounded with respect to for some . Let be an arbitrary non-negative constant and let the kernel on be defined by

Then fulfills

-

(i)

for all ,

-

(ii)

for all , and

-

(iii)

there is an ONB of such that .

For the proof of this theorem, we need two lemmas. The first deals with the restriction of kernels on to kernels on .

Lemma 3.5.

Let be a possibly unbounded interval and let be a kernel on such that is separable. Then is separable and

-

(i)

if , then and

-

(ii)

if there is an ONB of such that , then there is an ONB of such that .

Proof.

We recall that with equal norms. Therefore, if is an ONB of , an ONB of is obtained by letting for all . This shows that is separable.

The next lemma shows that part (i) of Theorem 3.4 is satisfied and also that Assumption 3.3 is fulfilled.

Lemma 3.6.

Under the conditions of Theorem 3.4, .

Proof.

The proof is divided into two steps. First, we show that . Then we show that . Here we write for the weighted Matérn kernel , where is a given function on .

For the first step, it suffices to check that . This means that there is some constant such that for all and ,

Since is a strictly positive function, this is equivalent to showing that there is some constant such that for all and ,

This in turn is equivalent to . We now use the fact (see [36, Proposition 5.20]) that . Here , which is closed in by continuity of the evaluation operator. The norm of this RKHS may be represented by for the unique such that . Moreover, since we have assumed that the mapping belongs to , we have for all that . This shows that .

We are now ready to prove the rest of Theorem 3.4.

Proof of Theorem 3.4..

Since is continuous, is separable. With this in mind, let us first show Theorem 3.4(ii). By Lemmas 3.5 and 3.6, it suffices to show that . We do this by combining the approximation number properties (5) and (6) with the observation that . This observation follows from the results of [24], wherein entropy numbers of embeddings between weighted Besov-type spaces are studied. We note that with equivalent norms for all [42, Theorems 2.3.9 and 2.5.6]. With this in mind, we have by [24, Theorem 4.2] that is bounded from above and below by a constant (independent of ) times in the case that and in the case that . In either of these two cases, therefore, the number is bounded by for some so that . In case we can find some so that , hence we arrive at the same conclusion. We note at this point that the results of [24] are for spaces of complex-valued functions, but it follows directly from the definition that the entropy numbers of embeddings of our real-valued spaces are bounded by those of the complex-valued spaces.

For the claim (iii), we recall that an operator , where is a separable Hilbert space and is a Banach space, is said to be -radonifying if

where this operator norm is independent of the choice of ONB of and sequence of iid standard Gaussian random variables [43, Corollary 3.21]. We will show that , from which the result follows by [43, Theorem 3.23] and Lemma 3.5. First, we note that the class of -radonifying operators is an operator ideal [43, Theorem 6.2]. Moreover, , a consequence of [42, Proposition 2.5.7]. We also have

Therefore, by Lemma 3.6, it suffices to note that . This follows from [32, (2.2)] if it holds that . Using [24, Theorem 4.2], (3) and (4), we see that is bounded by a constant times if , by if and by if . From this the result follows. ∎

Remark 3.7.

For the weight in Theorem 3.4, possible choices include with (or a rescaling thereof) or smooth bump functions. For the stationary kernel , one might choose it to be a Matérn kernel. This class includes exponential kernels as special cases and is defined by

for . Here is the modified Bessel function of the second kind with order and is the Gamma function. It is scaled by the positive parameters, the variance and the correlation length . The assumption on in Theorem 3.4 holds with , see, e.g., [35, Example 6.8]. The exponential kernel is obtained with .

Remark 3.8.

Since we are mainly interested in Wiener processes on the half-space , we restricted ourselves to this case. Theorem 3.4 can be seen to hold true also in , with the bounds on and replaced by dimension-dependent constants. Moreover, if the application at hand calls for genuinely non-stationary kernels, Hölder conditions could be analyzed using similar techniques.

4. Existence, uniqueness and Sobolev regularity of the HEIDIH model

In this section we discuss existence and uniqueness of the two components and in the HEIDIH model (2). We start with the volatility process , which is the mild solution

| (10) |

to the stochastic heat equation

| (11) |

starting at on . We recall that denotes the Laplacian with homogeneous zero boundary conditions at of either Dirichlet or Neumann type scaled by a diffusion coefficient . We derive spatial regularity results in a fractional Sobolev sense along with a pointwise-in-space Hölder regularity result. The latter is needed for the numerical approximation in the next section. With these results in place, we consider the full system (2) and derive existence, uniqueness and fractional Sobolev regularity for the mild solution

| (12) |

under suitable assumptions on , and .

4.1. The stochastic heat equation

We pose (11) as an equation in the space , but impose sufficient regularity of the components to guarantee that it takes values in for . We let the operator be the realization of the Laplacian in . Since the spectrum is contained in , is a sectorial operator for all . Fractional powers of the self-adjoint and positive definite operator are therefore well-defined and is the generator of an analytic semigroup [45, Section 2.7,Theorem 3.1]. By the proofs of [21, Theorems 1-2], we have the following characterizations of the domains of the operators for small :

| (13) |

In the case of Dirichlet boundary conditions we have , while in the case of Neumann boundary conditions we have . Here, we also made implicit use of the fact that the Bessel potential norm and the so called Sobolev–Slobodeckij norm (see, e.g., [45, (1.70)]) are equivalent in our setting, which follows from the existence of an extension operator, see, e.g., [45, Theorem 1.33]. The equality (13) should be understood as the existence of a canonical isomorphism with norm equivalence, with respect to the Hilbert space structure of when this is equipped with the graph norm . The sequence consists of spaces that are continuously and densely embedded into one another. By interpolation techniques (cf. [45, Theorem 16.3]) one may show that for all .

Let the Wiener process in (2) have covariance kernel fulfilling Assumption 3.2(ii) for some . If we regard as a -Wiener process in , its covariance operator is given by . Since , we have if and only if , provided that . Therefore, [28, Assumption 3] is fulfilled and we obtain the following existence, uniqueness and regularity result.

Theorem 4.1 ([28, Theorem 1]).

Remark 4.2.

By the Sobolev embedding theorem, we obtain from the estimate (14) that there is a constant such that for all and , for all . If , we therefore obtain that is Hölder continuous with respect to the root mean squared norm with exponent up to . Similarly, is Hölder continuous with exponent up to . However, also for such relatively rough noise, the Hölder exponents can be improved, provided that Assumption 3.2(iii) is fulfilled. This we show in the next proposition. A concrete example of a covariance kernel in this setting includes a weighted Matérn kernel with smoothness parameter close to , see Remark 3.7. For the proof, we recall that the semigroup associated with has an explicit representation by the reflection method. Indeed, with , , denoting the heat kernel,

| (15) |

for . The sign is positive for Neumann boundary conditions and negative for Dirichlet boundary conditions. This can be seen by the density of smooth functions with compact support in . Alternatively, we may write

| (16) |

where is an even extension of around for Neumann boundary conditions and an odd extension in the Dirichlet case.

Proposition 4.3.

Proof.

By differentiation of , we have, in the notation of (16),

Since and integrates to and , we obtain for . Moreover, is stable in in the sense that for all . Combining these two estimates yields, for all , a constant such that for all and ,

| (17) |

We now prove claim (i) for . The general case follows immediately by the estimates above, noting that by the Sobolev embedding theorem.

Since is continuous on for , Theorem 4.1 justifies moving inside the Itô integral below, so that by the Itô isometry

| (18) |

Here, we let be an ONB of such that , see Assumption 3.2(iii). Then, the claimed estimate follows by making use of (17) for the second term and stability of in for the first term.

4.2. Regularity of the HEIDIH model

For the full model (2), we let and be Wiener processes with kernels and . For , we assume that Assumption 3.2(i) is fulfilled and for the components of we consider the same setting as in Theorem 4.1. For the process , we make the following assumption.

Assumption 4.4.

Let, for some , be an adapted stochastic process in fulfilling for all . Let be such that the -valued process given by , is predictable and fulfills

In [8], two examples for are studied in detail. First, the constant setting for all with . Second, the setting in which is the unique positive definite square root of , i.e., letting

see [8, Proposition 4]. Note that with . For these two examples, is an adapted process with a continuous version. This follows from the continuity of , see [8, Lemma 5]. We note that the authors of [8] assume that the covariance operator of is trace-class when confirming that the integral in Assumption 4.4 is finite for these two examples, see [8, Lemma 8]. For us, this translates to . However, it is sufficient to require that , since

| (19) |

almost surely and for .

The regularity of , as well as its existence and uniqueness as a process in , now follows from [17, Theorem 6.10]. This makes use of the fact that is a contraction -semigroup on . This is true under the convention for , see [19, Appendix A.1].

We summarize these remarks in the following theorem.

Theorem 4.5.

We end this section by commenting on the special case that for all . Let be an ONB of . By (7) and approximation by simple functions, it follows from independence of and that for

| (20) |

where

| (21) |

is a real-valued Wiener process. We see that in this case the stochastic volatility is directly given by while is a global (in ) scaling parameter. A convenient choice for is to first set for some constants and points , , where we recall that is the kernel of . This class of functions is dense in , see [9, Corollary 2]. Then

so with we obtain the expression

which can readily be computed.

Remark 4.6.

An example of the setting above with , is shown in Figures 1(a) and 1(b). Here and are smooth bump functions while , where and is a Matérn kernel with and unit variance, see Remark 3.7. In we have set . By Theorems 4.1 and 4.5, we obtain that both and take values in for . We have chosen and in such a way that with .

5. Numerical approximation

A rigorous understanding of convergence rates in numerical approximations of SPDEs is vital for several reasons. First, they allow us to theoretically understand different approximation methods with respect to computational speed. Second, if the approximations are used in Monte Carlo methods, the convergence rates can help us to choose sample sizes in an optimal way [33]. Third, understanding how different sources of errors contribute in different ways to the overall error lets us tune the various parts of the algorithm, so that each error source contributes equally, leading to a computationally efficient algorithm. We return to this last part in Section 5.2.

Arguably, most literature on numerical approximation of SPDEs focus on the analysis of errors as measured in a spatial -norm in some mean square sense, see, e.g., [27, 31, 35] and the references within. This is especially true for finite element approximations. In the context of SPDE models of forward prices, the convergence discussed for the discontinuous Galerkin finite element method in [2] is of this type. In our setting, this would translate to errors of the form in the numerical approximation of the HEIDIH model, where refers to a given approximation and are points on a temporal grid. However, the spatial argument in refers to time to maturity. To price contracts delivering a commodity at a fixed time, therefore, we should instead consider pointwise-in-space errors, i.e., errors of the form where are points on a space-time grid. This is the approach we take below, where we first prove a general error decomposition formula for . We then restrict ourselves to the setting that for all and is equipped with Dirichlet boundary conditions. In this case we derive sharp convergence rates with respect to pointwise-in-space errors for fully discrete approximations of and .

5.1. Error decomposition formula for a finite difference scheme in space and time

We consider approximating the process on a spatiotemporal grid using finite differences with equal uniform step sizes in both time and space. The approximation is denoted by and we set . Otherwise, is defined on the grid by the recursion

| (22) |

where the -valued stochastic processes are given approximations and , respectively, and . Iterating this, we obtain in closed form

| (23) |

This leads to the following error decomposition. We remark that since we do not use any particular property of , this result applies to any Heston stochastic volatility model of forward prices in the sense of [4, 8]. Note also that, due to the use of a grid with equal step sizes in both space and time, the part of (12) associated with is solved exactly.

Proposition 5.1.

Suppose that are such that is a predictable -valued process fulfilling

The approximation error at the points and can be decomposed as

In the special case that ,

Proof.

5.2. A localized finite element discretization of the stochastic heat equation

The second part of Proposition 5.1 shows that in the case that , it suffices to deduce a pointwise-in-space error estimate for an approximation of in order to derive a corresponding estimate for . We turn to this setting now, and assume in addition that is equipped with Dirichlet zero boundary conditions at .

The approximation scheme we use for below is semi-implicit in time. This means that we must formulate it on a finite domain for sufficiently large . From (23) we see that we must at least take if we want to evaluate up to . We restrict the initial condition and the noise using the restriction operator and introduce an artificial boundary condition at . This causes a so called localization error. Such errors were recently investigated in detail in the Walsh setting in [11], considering localization of stochastic heat equations on to . We use similar arguments for the semigroup framework of [17] that we have adopted here.

We let denote the realization in of the Laplacian with Dirichlet zero boundary conditions at and . The analytic semigroup of contractions generated by maps into a space of continuous and bounded functions on . It has an explicit representation by

for and , where

with and for , . Directly from this representation, we obtain the rescaling property

| (24) |

Using the fact that the sine functions are uniformly bounded in with respect to , this can be used to see that there is a constant such that for all , and ,

| (25) |

Moreover, for all and , is stable in the sense that

We now let be the mild solution

to

with initial condition . Fractional powers , are well-defined since is self-adjoint and positive definite. They are explicitly given by

in terms of the eigenvalues and eigenfunctions of , cf. [31, Appendix B]. This is well-defined for such that the sequence on the right hand side is summable. This space is denoted by and by another appeal to [21, Theorem 1],

| (26) |

with equivalent norms.

Under Assumption 3.2(ii), the ideal property of yields that for

| (27) |

The setting of Theorem 4.1 therefore suffices to ensure that the stochastic convolution has a continuous modification in for all . This may not hold for the entire process since does not ensure that . However, does guarantee that is bounded and Hölder continuous with exponent . We use these properties to deduce the following pointwise-in-space localization error between and .

Proposition 5.2.

Proof.

We assume for simplicity that since the terms involving and can be estimated by similar arguments as below. First, pointwise evaluation of is admissible since the process takes values in for all by (27). Therefore, by the Itô isometry, we have for any ,

| (28) |

where is an arbitrary ONB of . We choose the ONB in Assumption 3.2(iii). For , we use the kernel (15) and make the split

We note that

for and . Applying this to the first term, it is bounded by

which in turn can be bounded by . For the term , we use the fact that

to rewrite it as

Using the non-negativity and symmetry of , it is bounded by

These estimates along with Assumption 3.2(iii) in (28) finish the proof. ∎

We now introduce a fully discrete approximation of based on finite elements and the backward Euler scheme. For this we consider a spatial as well as a temporal grid for . As before and , and we assume for simplicity that and . We let be the space of piecewise linear functions on the spatial grid and the subspace of functions that are zero at and . Both are finite dimensional Hilbert subspaces of when equipped with the topology of this space. The latter is a subspace of . We define a discrete operator on by

We write for the orthogonal -projection onto and define the interpolant by for . The latter is bounded on for . A discretization of is now given by the -valued sequence which is defined by and

| (29) |

where denotes the identity on , otherwise.

The last term in (29) is well-defined since is bounded on for all . Therefore is well-defined on and

since has finite-dimensional range. Note that, since is bounded on , we have similarly

where is an ONB of . Since is an ONB of , we obtain

Therefore, may be obtained by sampling a Gaussian random vector in with covariance matrix , having entries . For (weighted) Matérn covariance functions this can be accomplished in log-linear complexity with respect to by using a circulant embedding algorithm (see [22]) and multiplying by the weight function.

We define an approximation of the semigroup by

where is the indicator function. Here we have extended the temporal grid by for . This allows us to write (29) in closed form by

| (30) |

for . Like , this operator family has a scaling property

| (31) |

In order to derive a a pointwise-in-space error bound for , we need some stability and error estimates for the finite element method. We collect them in the following lemma.

Lemma 5.3.

In the setting outlined above, the following estimates hold:

-

(i)

-

(ii)

,

-

(iii)

, and

-

(iv)

.

Proof.

The stability estimate (i) is [15, Theorem 1]. This is stated for , but the proof holds also for general with no change in the bound.

A proof of the interpolation error (ii) is given in [18, Example 3] for domains and , but the argument is the same in our case, noting that does not depend on the size of . The restriction is required in for to be well-defined on , but suffices in our case. The proof uses the Sobolev–Slobodeckij norm, but this is bounded by the norm of and, crucially, the bound is uniform in .

For the semigroup error bound (iii), we first use (i) along with [14, (1.17)] to obtain a constant such that for all , and , . By [14, (1.14) and (1.21)], there is a constant such that for all , , and ,

Combining these estimates with (24), (25) and (31) yields the existence of a constant such that for all , , and ,

The same rescaling argument yields stability of for general , whence we obtain (iii).

We are now ready to prove a pointwise-in-space error bound for .

Proposition 5.4.

Proof.

In an argument similar to the proof of Proposition 4.3, we again use the fact that is continuous on for any when applying the Itô isometry and then bound the integrands by the norm. With the mild formulas (10) and (30), we split the error into three parts,

for any . Again, the ONB of is arbitrary. The first term on the right hand side is handled directly by Lemma 5.3(iii).

For the second term, we choose the ONB of Assumption 3.2(iii) and use Lemma 5.3(iii) to see that it is bounded by a constant times

for all .

For the third term we use the Poincaré inequality

for along with an interpolation argument and a Sobolev embedding to obtain that for all it is bounded by

We use the identity (6) to obtain a bound on the integrand in terms of approximation numbers. In order to make use of (4), the sum is split into two parts:

| (32) |

For the first sum, we use (3), (4) and (5) to see that for all

By Lemma 5.3(ii) and (iv) along with Hölder’s inequality for sequence spaces, therefore, it is bounded by a constant times

for all such that . As in the proof of Theorem 3.4, for sufficiently small , . Letting yields . By the min-max principle, the eigenvalues of are bounded from below by the eigenvalues of . Since approximation numbers coincide with eigenvalues for self-adjoint operators on Hilbert spaces (see [37, Proposition 11.3.3]), it follows that

Since , this sum is finite as long as is sufficiently small. The second sum in (32) is handled in the same way, so that

Remark 5.5.

The singularity may be removed by assuming sufficient regularity of , cf. [14, Theorem 3.6]. We do not discuss this further other than noting that this requires for . In practice this entails assuming that has compact support since we employ as an approximation of with increasing .

Remark 5.6.

Suppose that and that is given by a weight-stationary kernel as in Theorem 3.4 with smoothness parameter and weight parameter . Taking also Lemma 3.6 into account, the result of Proposition 5.4 reads: there is for all and a constant such that for all , , , and ,

We see that the rate in time is essentially no matter the value of while the rate in space varies between and . If we had sampled the noise by directly in (29) instead of employing we would see a convergence rate of in space no matter the value of . A covariance matrix of the elements in the vector corresponding to can be computed and used for this purpose. There are two problems with this approach, however. First, the matrix involves integrals that must in general be computed numerically. This can be very expensive. Second, even for weighted Matérn kernels, there are no theoretical guarantees that circulant embedding algorithms can be employed. Then more expensive methods, such as using a Cholesky decompositions and multiplying with the resulting dense matrix for sampling, must be employed.

Remark 5.7.

In the proof of Proposition 5.4, we used a Sobolev embedding technique for the term involving . Had we also used it for the other integral term, we could employ classical techniques (see, e.g., [46, Theorem 1.1]) combined with interpolation between error estimates in measured in and norms (cf. [31, Lemma 3.12]) to obtain a convergence rate of essentially . That is, assuming that no essential smoothness of the kernel in the Hilbert–Schmidt sense was available. This is the case if a weight-stationary kernel as in Theorem 3.4 with and small is used. From the previous remark, we see that this rate would be suboptimal in time. It would also be suboptimal in space if we were to sample the noise by directly.

Traditionally, finite element approximations of the stochastic heat equation have been analyzed in norms in space, see, e.g., [46, 31]. In the same setting as in Remark 5.6, suppose also for simplicity that . Then, an application of [30, Lemma 3.12] and Lemma 5.3(ii) yields for all and , the existence of a constant such that for all , ,

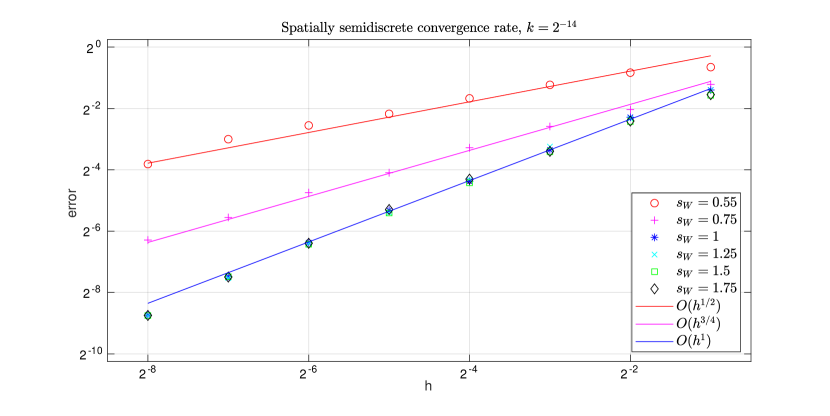

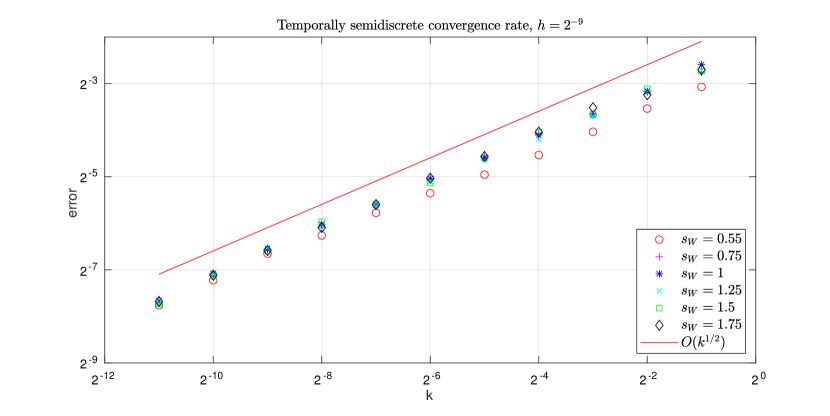

Compared to the results of Proposition 5.4, we see that if is close to , the same rate is obtained. Otherwise, the rate can be as high as in space and in time. The reason for the potentially higher rate is that Assumption 3.2(ii) may be used with combined with (26). Since no such equivalence is available in our setting, a lower rate is obtained. This is however sharp, which we now demonstrate in simulations.

We let , and . We let the kernel of be of Matérn class (see Remark 3.7) with and increasing . This may be regarded as a weighted stationary kernel in Theorem 3.4 by choosing the weight function as a smooth bump function with large but finite support and equal to in a sufficiently large neighborhood of . In this context, the results of Proposition 5.4 hold true with . We plot approximations of the errors

| (33) |

based on Monte Carlo approximations with sample size . First, we fix and examine the spatial convergence rate for decreasing . We replace with a reference solution computed at . As we see from Figure 2, the convergence rate increases from essentially when to when . This is in line with the results of Theorem 3.4. Next, we fix and examine the temporal convergence rate for decreasing . We replace with a reference solution computed at . We see from Figure 3, that the convergence rate stays constant no matter the value of . This is again in line with the results of Theorem 3.4.

The sample size was chosen to ensure that the plots in Figures 2 and 3 were sufficiently stable. We used the same samples of across all values of for a given value of . The samples across different were drawn independently of each other. The sample size does not yield a precise estimate of (33). However, we are only interested in observing the rate with which the error decrease as or tends to , and in this sense the Monte Carlo error will never dominate, at least in a mean square sense and for fixed , . For, with , it follows from Proposition 5.4 that

where are the independent samples of that make up the Monte Carlo estimate.

5.3. A fully discrete finite difference-finite element discretization of the HEIDIH model

We end this section on numerical approximation by combining the results of Propositions 5.1, 5.2 and 5.4, thereby obtaining a fully discrete approximation result for the HEIDIH model in the case that for all .

We employ the same finite difference method of Section 5.1 to define an approximation on a space-time grid with equal spatial and temporal step sizes . Recalling (20), this is defined by

| (34) |

for and . Here is the approximation of defined by (29) and the real-valued Wiener process defined in (21) with . Note that is computed on a space-time grid with temporal step size and spatial mesh size that may not be equal. Since is a piecewise linear function on , the scheme (34) is well-defined even if . The closed form is given by

| (35) |

Theorem 5.8.

Proof.

While it might not be possible to extend to if is big, the equations (20) and (35) are well-defined so that we may use the second error decomposition formula in Proposition 5.1 and split the error by

The first and fourth term are bounded by a constant times by Lemma 5.3(i) along with Theorem 4.1 and a Sobolev embedding argument. The second is treated by Proposition 5.4 with and , the third by Proposition 5.2 and the last two by Proposition 4.3. ∎

Remark 5.9.

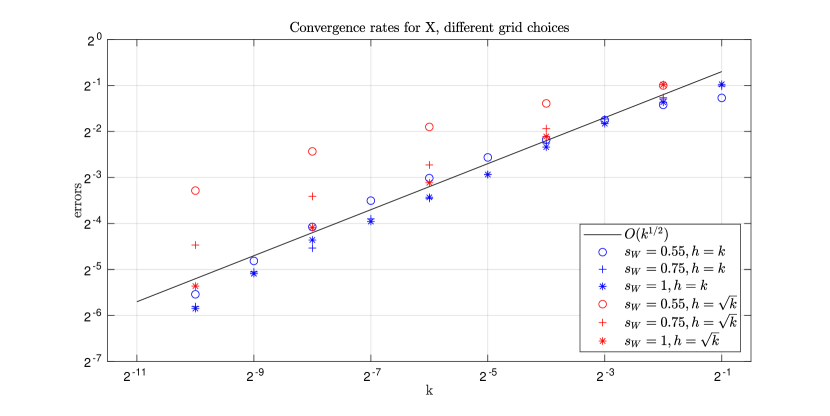

Suppose that is large, so that the error is dominated by the space and time discretization. The relationship between the spatial step size and time step size have important consequences for the efficiency of the algorithm. If is close to , we must choose on the same order of magnitude as in order for the term not to dominate in the error estimate of Theorem 5.8. If , we can choose on the same order as and still achieve a convergence rate of as . We illustrate this point in Figure 4, where we have let and , and chosen and so that . We have chosen as in Remark 4.6 with being a Matérn kernel with . We let range from to and plot the error

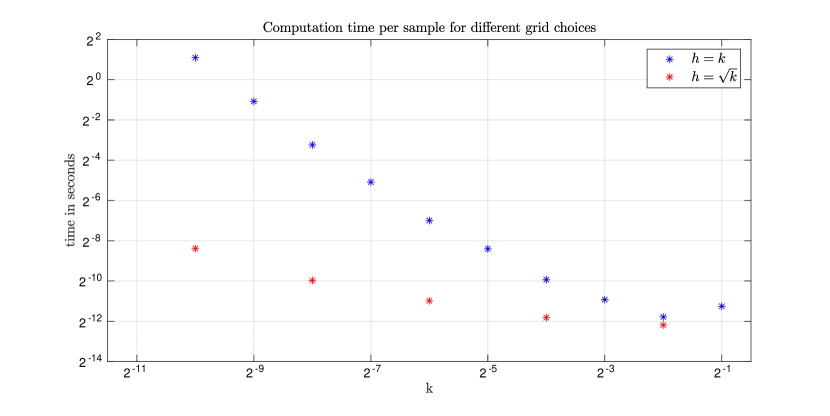

for decreasing and choose either or . We have replaced with a reference solution at in the first case, in the second, and used samples in a Monte Carlo approximation of the error. We see that, as expected, the rate is achieved for all when but only for when . If , it is important that the choice is made, however, since this yields a much faster algorithm with the same convergence rate compared to , see Figure 5.

6. Discussion and future research

We end this paper with a brief discussion of our results with regard to novelty and future research.

The HEIDIH model was introduced as a special case of the infinite dimensional Heston stochastic volatility model of [8]. As far as we know, this paper is the first to consider numerical approximation of such a model, as well as providing a detailed regularity analysis. In particular, we focused on how regularity of the covariance kernels of the driving Wiener processes influence regularity of the model and gave concrete examples of covariance kernels that fit into our setting. A basic result for finite difference approximations that applies to all infinite dimensional Heston stochastic volatility models of forward prices was proven in Proposition 5.1. In the special case that for all we were able to deduce and prove sharp convergence rates for a fully implementable and computationally efficient algorithm in Theorem 5.8. Future areas of research include the approximation of the HEIDIH model with other choices of , such as for . The main challenge then is to find an efficient way of computing the terms and in (22). Had this could be solved by numerical integration, but for the problem is harder. Another area for numerical development is other boundary conditions for . The Dirichlet condition was in our numerical simulations chosen due to the availability of suitable deterministic non-smooth data error estimates [14]. This led to relatively low convergence rates, as noted in Section 5.2.

A large part of our numerical analysis was dedicated to finding sharp convergence rates for numerical approximations to the stochastic heat equation. There is a large body of literature dedicated to this topic, see [27] for a review of early results. In our setting, the situation is complicated by the fact that we need pointwise-in-space error estimates, that localization errors need to be taken into account and that sampling the Wiener process pointwise causes an additional error.

We are not aware of any pointwise-in-space error estimates for finite element approximations of the stochastic heat equation. However, for finite difference schemes there is a long tradition, starting with [23] in the Walsh setting. The results of [23] is for noise that is white in both space and time. We are not aware of any case for which noise colored by a concrete covariance kernel was considered for finite difference approximations.

Localization have been dealt with before in the Walsh setting, in [11] for example. We showed how similar arguments can be adapted to the semigroup framework of [17] considered in [8].

The question of how sampling the Wiener process pointwise affect the convergence of approximations of the stochastic heat equation has, as far as we know, barely been analyzed at all in the literature. In terms of finite elements it means replacing the -projection with the interpolant in and the question of what effect this has is mentioned as open in [31, Section 6.2]. We showed in theory as well as by numerical simulations that there is a negative effect on the convergence if the noise is rough (i.e., if for ) but not otherwise. After the submitting the first version of this paper, the result of replacing of with was analyzed in detail for a semi-linear SPDE with multiplicative noise on a bounded polygon [34].

References

- [1] N. Aronszajn. Theory of reproducing kernels. Trans. Am. Math. Soc., 68:337–404, 1950.

- [2] A. Barth and F. E. Benth. The forward dynamics in energy markets – infinite-dimensional modelling and simulation. Stochastics, 86(6):932–966, 2014.

- [3] F. E. Benth, J. S. Benth, and S. Koekebakker. Stochastic modeling of electricity and related markets, volume 11 of Advanced Series on Statistical Science & Applied Probability. World Scientific Publishing, Singapore, Singapore, April 2008.

- [4] F. E. Benth, G. Di Nunno, and I. C. Simonsen. Sensitivity analysis in the infinite dimensional Heston model. Infin. Dimens. Anal. Quantum Probab. Relat. Top., 24(2):29, 2021. Id/No 2150014.

- [5] F. E. Benth and H. Eyjolfsson. Robustness of Hilbert space-valued stochastic volatility models, 2022. Preprint at arXiv:2211.16071.

- [6] F. E. Benth and P. Krühner. Representation of infinite-dimensional forward price models in commodity markets. Commun. Math. Stat., 2(1):47–106, 2014.

- [7] F. E. Benth and P. Krühner. Derivatives pricing in energy markets: an infinite-dimensional approach. SIAM J. Financ. Math., 6:825–869, 2015.

- [8] F. E. Benth and I. C. Simonsen. The Heston stochastic volatility model in Hilbert space. Stoch. Anal. Appl., 36(4):733–750, 2018.

- [9] A. Berlinet and C. Thomas-Agnan. Reproducing kernel Hilbert spaces in probability and statistics. Kluwer Academic Publishers, Boston, MA, 2004.

- [10] J. H. Bramble and X. Zhang. The analysis of multigrid methods. In Handbook of numerical analysis, Vol. VII, Handb. Numer. Anal., VII, pages 173–415. North-Holland, Amsterdam, 2000.

- [11] D. J.-M. Candil. Localization errors of the stochastic heat equation. PhD thesis, 2022. Available at https://infoscience.epfl.ch/record/291119.

- [12] S. Cox, S. Karbach, and A. Khedher. Affine pure-jump processes on positive Hilbert-Schmidt operators. Stochastic Process. Appl., 151:191–229, 2022.

- [13] S. Cox, S. Karbach, and A. Khedher. An infinite-dimensional affine stochastic volatility model. Math. Finance, 32(3):878–906, 2022.

- [14] M. Crouzeix, S. Larsson, and V. Thomée. Resolvent estimates for elliptic finite element operators in one dimension. Math. Comput., 63(207):121–140, 1994.

- [15] M. Crouzeix and V. Thomée. The stability in and of the -projection onto finite element function spaces. Math. Comput., 48:521–532, 1987.

- [16] C. Cuchiero and J. Teichmann. Generalized Feller processes and Markovian lifts of stochastic Volterra processes: the affine case. J. Evol. Equ., 20(4):1301–1348, 2020.

- [17] G. Da Prato and J. Zabczyk. Stochastic equations in infinite dimensions, volume 152 of Encyclopedia of mathematics and its applications. Cambridge University Press, Cambridge, second edition, 2014.

- [18] T. Dupont and R. Scott. Polynomial approximation of functions in Sobolev spaces. Math. Comp., 34(150):441–463, 1980.

- [19] I. Ekeland and E. Taflin. Optimal bond portfolios. In Paris-Princeton lectures on mathematical finance 2004., pages 51–102. Berlin: Springer, 2007.

- [20] D. Filipović. Consistency problems for Heath-Jarrow-Morton interest rate models, volume 1760 of Lect. Notes Math. Berlin: Springer, 2001.

- [21] D. Fujiwara. Concrete characterization of the domains of fractional powers of some elliptic differential operators of the second order. Proc. Japan Acad., 43:82–86, 1967.

- [22] I. G. Graham, F. Y. Kuo, D. Nuyens, R. Scheichl, and I. H. Sloan. Analysis of circulant embedding methods for sampling stationary random fields. SIAM J. Numer. Anal., 56(3):1871–1895, 2018.

- [23] I. Gyöngy. Lattice approximations for stochastic quasi-linear parabolic partial differential equations driven by space-time white noise. II. Potential Anal., 11(1):1–37, 1999.

- [24] D. Haroske and H. Triebel. Entropy numbers in weighted function spaces and eigenvalue distributions of some degenerate pseudodifferential operators. I. Math. Nachr., 167:131–156, 1994.

- [25] D. Heath, R. Jarrow, and A. Morton. Bond pricing and the term structure of interest rates: A new methodology for contingent claims valuation. Econometrica, 60(1):77–105, 1992.

- [26] T. Hsing and R. Eubank. Theoretical foundations of functional data analysis, with an introduction to linear operators. Wiley Series in Probability and Statistics. John Wiley & Sons, Ltd., Chichester, 2015.

- [27] A. Jentzen and P. E. Kloeden. The numerical approximation of stochastic partial differential equations. Milan J. Math., 77(1):205–244, 2009.

- [28] A. Jentzen and M. Röckner. Regularity analysis for stochastic partial differential equations with nonlinear multiplicative trace class noise. Journal of Differential Equations, 252(1):114–136, 2012.

- [29] S. Karbach. Finite-rank approximation of affine processes on positive Hilbert-Schmidt operators, 2023. Preprint at arXiv:2301.06992.

- [30] R. Khasminskii. Stochastic Stability of Differential Equations, volume 66 of Stochastic Modelling and Applied Probability. Springer, 2012.

- [31] R. Kruse. Strong and weak approximation of semilinear stochastic evolution equations, volume 2093 of Lecture notes in mathematics. Springer, Cham, 2014.

- [32] T. Kühn and W. Linde. Gaussian approximation numbers and metric entropy. J. Math. Sci., New York, 238(4):471–483, 2019.

- [33] A. Lang. A note on the importance of weak convergence rates for SPDE approximations in multilevel Monte Carlo schemes. In R. Cools and D. Nuyens, editors, Monte Carlo and quasi-Monte Carlo methods, MCQMC, Leuven, Belgium, April 2014, volume 163 of Springer Proceedings in Mathematics & Statistics, pages 489–505, 2016.

- [34] G. Lord and A. Petersson. Piecewise linear interpolation of noise in finite element approximations of parabolic SPDEs, 2022. Preprint at arXiv:2210.11102.

- [35] G. J. Lord, C. E. Powell, and T. Shardlow. An introduction to computational stochastic PDEs. Cambridge Texts in Applied Mathematics. Cambridge University Press, 2014.

- [36] V. I. Paulsen and M. Raghupathi. An introduction to the theory of reproducing kernel Hilbert spaces, volume 152. Cambridge: Cambridge University Press, 2016.

- [37] A. Pietsch. Operator ideals. Licenced ed, volume 20. Elsevier (North-Holland), Amsterdam, 1980.

- [38] C. Prévôt and M. Röckner. A Concise Course on Stochastic Partial Differential Equations, volume 1905 of Lecture notes in mathematics. Springer, Berlin, 2007.

- [39] M. Riedle. Cylindrical Wiener processes. In Séminaire de Probabilités XLIII, volume 2006 of Lecture Notes in Math., pages 191–214. Springer, Berlin, 2011.

- [40] E. M. Stein. Singular integrals and differentiability properties of functions, volume 30 of Princeton Math. Ser. Princeton University Press, Princeton, NJ, 1970.

- [41] V. Thomée. Galerkin finite element methods for parabolic problems, volume 25 of Springer Series in Computational Mathematics. Springer-Verlag, Berlin, second edition, 2006.

- [42] H. Triebel. Theory of function spaces, volume 78 of Monographs in Mathematics. Birkhäuser Verlag, Basel, 1983.

- [43] J. van Neerven. -radonifying operators—a survey. In The AMSI-ANU Workshop on Spectral Theory and Harmonic Analysis, volume 44 of Proc. Centre Math. Appl. Austral. Nat. Univ., pages 1–61. Austral. Nat. Univ., Canberra, 2010.

- [44] H. Wendland. Scattered data approximation, volume 17 of Cambridge Monographs on Applied and Computational Mathematics. Cambridge University Press, Cambridge, 2005.

- [45] A. Yagi. Abstract parabolic evolution equations and their applications. Springer Monographs in Mathematics. Springer-Verlag, Berlin, 2010.

- [46] Y. Yan. Galerkin finite element methods for stochastic parabolic partial differential equations. SIAM J. Numer. Anal., 43(4):1363–1384, 2005.