Optimal Quasi-Bayesian reduced rank regression with incomplete response

Norwegian University of Science and Technology, Norway.

(2) RIKEN AIP, Japan. )

Abstract

The aim of reduced rank regression is to connect multiple response variables to multiple predictors. This model is very popular, especially in biostatistics where multiple measurements on individuals can be re-used to predict multiple outputs. Unfortunately, there are often missing data in such datasets, making it difficult to use standard estimation tools. In this paper, we study the problem of reduced rank regression where the response matrix is incomplete. We propose a quasi-Bayesian approach to this problem, in the sense that the likelihood is replaced by a quasi-likelihood. We provide a tight oracle inequality, proving that our method is adaptive to the rank of the coefficient matrix. We describe a Langevin Monte Carlo algorithm for the computation of the posterior mean. Numerical comparison on synthetic and real data show that our method are competitive to the state-of-the-art where the rank is chosen by cross validation, and sometimes lead to an improvement.

Keywords:

reduced rank regression, low-rank matrix, PAC-Bayesian bound, Langevin Monte Carlo, missing data.

1 Introduction

Reduced rank regression (RRR) is a popular model widely used in studying the relationship between multiple response variables and a set of predictors [5, 35, 36, 61]. Connecting predictors to response variables via a linear relation requires the estimation of coefficients, which might be difficult or impossible when and/or is large. RRR uses a low-rank constraint to reduce the dimension of the problem. This dimension reduction makes accurate estimation possible in large dimension [8]. Moreover, the span of the regression matrix can receive a nice interpretation in terms of a small number of latent variables explaining all the response variables. Various methods were proposed for estimation in RRR, including frequentist and Bayesian approaches [30, 37, 15, 59, 1]. It was also proposed to add more constraints in the model, such as sparsity [31, 13, 62].

Bayesian RRR has been successfully applied in many applications, for example in biostatistics and genomics [47, 65]. However, in this field, most datasets have missing data [42, 47] and data with missing value are often removed or imputed before applying the model. However, incorrect imputation might result in estimation bias, and we are not aware of any theoretical guarantees for these procedures in this context. From a theoretical perspective, RRR is a special case of the so-called trace regression model. In [40], the authors study penalized least-square estimation in the trace regression model, and prove tight oracle inequalities. The reference [43] studied some penalized likelihood estimation procedure for RRR with incomplete response. However, there is no current available Bayesian approach could deal with missing data in RRR.

In this paper, we focus on quasi-Bayesian estimation in the reduced rank regression model with missing observations, in the sense that the response matrix is incomplete. We propose to use a multivariate Student prior. We prove that the posterior mean satisfies a tight oracle inequality: even when the true rank is unknown, it converges at the optimal rate we could hope when knowing the rank. We also prove a contraction of the posterior result. We develop a Langevin Monte Carlo (LMC) approach to compute the posterior mean and to sample from the posterior. We show that it is comparable to the frequentist estimator on both simulated and real datasets.

Quasi-Bayesian estimation is an extension of the Bayesian approach where the quality of the data fit is not necessarily measured by the likelihood, but by a more general notion of risk or a quasi-likelihood. This approach is increasingly popular in generalized Bayesian inference and machine learning [6, 39]. First, it allows to avoid restrictive assumptions on the data generating process. Moreover, it allows to focus on some aspects of the problem in mind (for example, prediction rather than estimation).

Our theoretical results on quasi-posteriors are derived from PAC-Bayes bounds. These bounds were introduced by [50, 60, 41, 49, 29] to provide numerical generalization certificates on quasi-Bayesian estimators. They were later extended by [11, 12] as tools to provide oracle inequalities for such estimators, this approach is strongly related to the so-called “information bounds” of [64, 58]. We refer the reader to [33, 2] for introductions to this topic. PAC-Bayes bounds were used to prove oracle inequalities for matrix estimation problems such as matrix completion [45, 16] and quantum tomography [46]. One of the byproducts of this approach is that we don’t have to assume anything about the distribution of the missing entries in the response matrix. This is in contrast with previous works on matrix completion such as [9, 40] where the location of the missing entries is assumed to be uniform. These assumptions were relaxed in further works [27, 38, 52], but we are not aware of any result without any assumption on this distribution.

The idea that multivariate Student priors lead to optimal rates in high-dimensional estimation problems is due to [17, 23]. Since then, these priors were used in matrix completion [63, 44] and image denoising [19]. Although the scaled spectral Student prior is not conjugate in our problem, it is particularly convenient for implementing gradient-based sampling method. We propose an LMC algorithm for sampling from the (quasi) posterior and for the computation of the posterior mean. The LMC method was introduced in physics based on Langevin diffusions [26] and became popular in statistics and machine learning following the paper [57]. Recent advances in the study of LMC make it particularly suitable for high-dimensional problems [18, 24, 25, 22].

The paper is organized as follows. In Section 2 we introduce the notations for the RRR model, the quasi-Bayesian approach and our spectral Student prior. In Section 3 we prove the convergence of the posterior mean, and the contraction of the posterior. In Section 4 we describe the Langevin MC method we implemented, we then compare it to the frequentist (penalized) estimator in Section 5. All the proofs are gathered in the appendix A.

2 Reduced rank regression with incomplete response

2.1 Notations

The set of matrices with real coefficients is denoted by . For any and , we denote by the coefficient on the -th row and -th column of . We let denote the transpose of . The matrix in with all entries equal to is denoted by . For a square matrix we let denote its trace. We denote the identity matrix in by . For , we define its sup-norm ; its Frobenius norm is defined by and its rank. For a probability distribution on , we generalize this notation by ; note that when is the uniform distribution, then .

2.2 Model

Let , and be integers: is the number of individuals, the number of explanatory variables and the number of response variables. We assume that we observe a design matrix and i.i.d random pairs given by

| (1) |

where is the unknown matrix to be estimated. The noise variables are assumed to be independent with The variables are i.i.d copies of a random variable having distribution on the set , we put . We call reduced rank regression (RRR) with missing entries the model in (1) under the assumption that .

Let us comment on this model. First, when and is the identity matrix, we recover the matrix completion as a special case [40]. However, we will focus here in the case where contains explanatory variables. Also note that there are two approaches to model the observed entries of : with, or without replacement. In the matrix completion problem, both were studied, see for example [9] for the case without replacement and [40] with replacement. Both settings correspond to practical applications, and the same estimation methods are used in both cases. We chose to develop our theory for i.i.d variables , which means that it is possible in our context to observe the same entry multiple times. Note that, thanks to the results in Section 6 of [34], our results can be extended directly to the case of sampling without replacement on the condition that they are sampled uniformly, and that there is no observation noise: . Finally, technical moment assumptions on the will be provided below. The independence assumption between these variables is standard in regression; it is possible to remove if in matrix completion [3], at the cost of technical weak dependence assumptions that we will not discuss here.

Let us now state our assumptions on this model.

Assumption 1.

There is a known constant such that

Assumption 2.

The noise variables are independent and independent of . There exist two known constants and such that

Assumption 1 states that is bounded for any . In the case of matrix completion, and thus this simply boils down to assuming that . Assumption 2 states that the noise is sub-exponential: this include a wide class of possible noises such as bounded noise and Gaussian noise. We refer the reader e.g. to Chapter 2 in [7] for more on sub-exponential variables. Assumption 1 and 2 are both standard, they have been used in [43] for theoretical analysis of reduced rank regression and in [40] for trace regression.

The frequentist methods in this model are based on minimization of the least square criterion with a low-rank inducing penalty. There is a subtlety in our case: under Assumption 1, we know that it makes no sense to return predictions with entries that are outside of . However, it is extremely convenient to use an unbounded prior for . Thus, we propose to use indeed unbounded distributions for , but to use as a predictor a truncated version of rather than itself. For a matrix , let

be the orthogonal projection of on matrices with entries bounded by . Note that is simply obtained by replacing entries of larger than by , and entries smaller than by .

For a matrix , we denote by the “empirical risk” or least-square criterion of ,

Its expectation is denoted by

In this paper, we will focus on the predictive aspects of the model: a matrix predicts almost as well as if is small. Under the assumption that has a finite variance, thanks to the Pythagorean theorem, we have

| (2) |

for any , which means that our results can also be interpreted in terms of estimation of with respect to a generalized Frobenius norm.

2.3 The Quasi-Bayesian approach

Let be a prior distribution on (we will specify low-rank inducing priors in the Subsection 2.4). For any , we define the quasi-posterior

Note that, for , this is exactly the posterior that we would be obtain for a Gaussian noise (conditionally on this ’s). However, our theoretical results will hold under a more general class of noise. Indeed, it is known that a small enough will lead to robustness to noise misspecification [32]. Moreover, even in the case of a Gaussian noise, in high-dimensional settings, taking smaller than leads to better adaptation properties [17, 23]. We will actually specify our choice of below.

The truncated posterior mean of is given by

| (3) |

Remark 1.

Let us comment briefly on the projection . First, note that using reasonable values for , the Monte Carlo algorithm we used in the simulations never sampled matrices such that . In other words, this projection is necessary for technical reasons, but has very little impact in practice. If one wants to build an estimator of instead of an estimator of , when is invertible, we can simply define and note that .

2.4 Prior specification

We consider the following spectral scaled Student prior, with parameter ,

| (4) |

To illustrate that this prior has the potential to encourage the low-rankness of , one can check that

where denotes the largest singular value of . It is well known that the log-sum function used by [10, 63] to enforce approximate sparsity on the singular values . Alternatively, one can recognize a scaled Student distribution evaluated at in the last display above which induces approximate sparsity on the [23]. Thus, under the prior, most of the are close to , which means that is well approximated by a low-rank matrix.

Although this prior is not conjugate in our problem, it is particularly convenient to implement the Langevin Monte Carlo algorithms, see Section 4. This prior has been considered before in the context of image denoising [19]. It can also be seen as the marginal distribution of the Gaussian-inverse Wishart prior that is explored in [63] in the context of matrix completion where the precision matrix is integrated out.

3 Theoretical analysis

3.1 Main results

In this section, we derive the statistical properties of the posterior and the mean estimator . Let us put

Theorem 1.

Note that the above formula does not actually require , if we have then and we interpret as . As mentioned in the introduction, the proof of this theorem relies on the PAC-Bayes theory. It is provided in the appendix. In particular, we can upper bound the infimum on by taking , which leads to the following result.

Corollary 1.

Under the same assumptions and the same as in Theorem 1, let . Put

then

and in particular, if the sampling distribution is uniform,

Remark 2.

A minimax lower-bound on the estimation of in the trace regression problem (which includes RRR) was derived by [40]: . Thus, is minimax-optimal (at most up to a log term).

While Theorem 1 states that the posterior mean leads to optimal estimation of , it is actually possible to prove that the quasi-posterior contracts around at the optimal rate.

Theorem 2.

Under the same assumptions for Theorem 1, and the same definition for and , let be any sequence in such that when . Define

Then

4 Computational approximation implementation

4.1 Langevin Monte Carlo algorithm

In this section, we propose to compute an approximation of the (quasi) posterior by a suitable version of the LMC algorithm, a gradient-based sampling method. First, we write the logarithm of the density of the posterior

Let us now differentiate this expression in . Note that the term does actually not depend on locally if , in this case its differential with respect to is . Otherwise, In order to be able to differentiate the term , let us introduce a notation for the entries of : . Then where the matrix satisfies . Then

In this work, we use a constant step-size unadjusted LMC algorithm, see [25] for more details. The algorithm is given by an initial matrix and the recursion

| (5) |

where is the step-size and are independent random matrices with i.i.d. standard Gaussian entries. We provide a pseudo-code for LMC in Algorithm 1.

In the case of very large , the LMC algorithm in (5) still requires to calculate a matrix inversion at each iteration, this might be expensive and can slow down the algorithm. Therefore, we could replace this matrix inversion by its accurately approximation through a convex optimization. It is noted that the matrix is the solution to the following convex optimization problem

The solution of this optimization problem can be conveniently obtained by using the package ‘glmnet’ [28] (with the family option ‘mgaussian’). This avoids to perform matrix inversion or other costly calculation. However, we note here that the LMC algorithm is being used with approximate gradient evaluation, theoretical assessment of this approach can be found in [21].

Remark 3.

For small values of the step-size , the output of Algorithm 1, , is very close to the integral (3) of interest. However, for some that may not small enough, the Markov process can be transient and as a consequence the sum explodes [56]. Several strategies are available to address this issue: one can take a smaller h and restart the algorithm or a Metropolis–Hastings correction can be included in the algorithm. The Metropolis–Hastings approach ensures the convergence to the desired distribution, however, the algorithm is greatly slowed down because of an additional acception/rejection step at each iteration. Taking a smaller also slows down the algorithm but we keep some control on its time of execution.

4.2 A Metropolis-adjusted Langevin algorithm

Here, we propose a Metropolis-Hasting correction to the Algorithm 1. This approach guarantees the convergence to the (quasi) posterior and it also provides a useful way for choosing . More precisely, we consider the update rule in (5) as a proposal for a new state,

| (6) |

Note that the matrix is normally distributed with mean and the covariance matrices equal to times the identity matrices. This proposal is accepted or rejected according to the Metropolis-Hastings algorithm that the proposal is accepted with probability:

| (7) |

where

is the transition probability density from to . The details of the Metropolis-adjusted Langevin algorithm (denoted by MALA) are presented Algorithm 2. Compared to random-walk Metropolis–Hastings, the advantage of MALA is that it usually proposes moves into regions of higher probability, which are then more likely to be accepted.

5 Numerical studies

5.1 Simulation setups

First, we perform some numerical studies on simulated data to access the performance of our proposed algorithms. The experiments are carried by using the R statistical software [53]. We compare our algorithms LMC, MALA to the ‘mRRR’ method in [43]. The ‘mRRR’ method is a frequentist approach where the rank is selected by using 5-fold cross validation. The mRRR method is available from the R package ‘rrpack’ [14].

We consider the following model setting. Setting I is a low-dimensional setup with and the true rank . The design matrix is generated from where the covariance matrix is with diagonal entries 1 and off-diagonal entries , we consider and . Following [43], the true coefficient matrix is generated as where is an orthogonal matrix from the QR decomposition of a random matrix filled with entries, and all entries in are i.i.d sampled from . The full response matrix , as in [43], is generated as where is matrix with entries sampled from .

Setting II is similar to Setting I, however, we consider a higher dimensional setup with . Setting III is an approximate low-rank set up: This series of simulation is similar to the Setting I, except that the true coefficient is no longer rank 2, but it can be well approximated by a rank 2 matrix: where is matrix with entries sampled from . Setting IV is also similar to Setting I, however we consider a heavy tail noise for the model (1) where the noise is now assumed to follow a -Student distribution with 3 degrees of freedom.

In each simulation run, once the full data matrices are simulated, we randomly sample entries in with, or without replacement: we let denote the observed entries, , the set of observed entries, the set of non-observed entries and its cardinality. Comparison of the results of our method with and without replacement are provided in Appendix B, they are actually quite comparable. On the other hand, the ‘mRRR’ is only implemented in the case without replacement, so we focus the rest of this section to the case without replacement.

These entries are set as missing values that . Under each setting, the entire data generation process is replicated 100 times. The evaluations are done by using the estimation error (Est) and the prediction error (Pred) as

The LMC, MALA are run with iterations and we take the first steps as burn-in. We fixed and in all models. The choice of the step-size parameters is in the form where is chosen such that the acceptance rate of MALA algorithm is between 0.4 and 0.6. This interval is chosen to enclose 0.574, the optimum acceptance probability for the Langevin MC algorithm [55]. For example: for Setting I (), for Setting III ().

5.2 Simulation results

The results from the simulations are given in Tables 1, 2, 3 and 4. In general, these 3 methods yield comparable results in Setting I and II, where as the mRRR method is a bit better with less missing data. However, the case of approximate low-rank matrix in Setting III shows that our proposed methods, especially MALA, return better results compared to mRRR. In Setting IV, where our theoretical results do not cover, we observe that mRRR is more stable than our approach.

Looking at the performance of LMC versus MALA, we see that in all settings LMC yields comparable results with MALA while its running time is faster than MALA (as do not require MH correction). However, when the dimension increasing, LMC can return a better result compared to MALA, as in Table 3. This can be explained as that LMC converge faster to an approximate distribution whose the mean could be very closed to the target distribution’s mean. See also Table 7. MALA is usually the best method with smallest errors. Moreover, as shown as an example in Table 5, MALA comes with reliable credible intervals while the credible intervals output from LMC have smaller coverage rate.

We further access the affect of changing in our proposed algorithms LMC and MALA, especially we emphasize on the empirical coverage of the 95% credible interval. The LMC, MALA are run with 10000 iterations and we take the first steps as burn-in. The results are given in Table 5 where we examine Setting III for the case of and the missing rate in is . The message from these results is that taking smaller could improve the empirical coverage rate, however the cost is in increasing the mean squared error. We also see that the value is good choice that we have used in all our simulations. Some results for different values of in the prior are given in Table 6. We see that the different values of will effect differently on LMC and MALA thus we stick a fixed value of in our simulations. It is worth noted that the choices of and are greatly effect to the values of the step-size .

6 Real data application

6.1 Galaxy COMBO17 data: imcomplete data again full data

This particular subset of the COMBO17 data set, see [36], consists of the n = 3,438 objects in the Chandra Deep Field South that are classified as “Galaxies” and for which there are no missing values. We also omitted five redundant variables and all error variables in the data set; the 29 remaining variables were then divided into a group of 23 variables as predictor matrix and a group of 6 variables as response matrix , details can be found in Table 7.2 in [36].

Here we emphasize that the response matrix is fully observed. The study in this section aims at finding how the missing rate in the response matrix affects to the estimation procedure. As this dataset contains data at different scale, we further rescale the data so that its columns has 0-mean and 1-variance. We first estimate, by using the OLS (ordinary least squares) method, the parameter matrix given fully observed data and denote this estimation by . Then, we randomly remove and entries of and re-estimate the parameter matrix. This procedure is repeated 100 times and we report the average results. The LMC, MALA are run with 15000 iterations and we take the first steps as burn-in.

To access the accuracy, we consider the estimation error and the prediction error as

The result outputs are given in Table 7. It is interesting to see that LMC here is the method returns with smallest errors for the cases of 20% and 50% missing rate. However, when the missing rate is 80% MALA method is better than LMC. In all cases, mRRR method comes with higher errors compared with LMC and MALA.

6.2 Yeast cell cycle data with imcomplete response

The dataset is available in the ‘secure’ R-package [51]. The analysis of the yeast cell cycle enables us to identify transcription factors (TFs) which regulate ribonucleic acid (RNA) levels within the eukaryotic cell cycle. The dataset contains two components: the chromatin immunoprecipitation (ChIP) data and eukaryotic cell cycle data. The binding information of a subset of 1790 genes and 113 TFs was included in the ChIP data [42], which results in the design matrix of dimension . The cell cycle data were obtained by measuring the RNA levels every 7 minutes for 119 minutes, thus a total of 18 time points. The resulting response matrix is of dimension . There are 626 missing entries in the response matrix which is around . We further rescale the data so that its columns has 0-mean and 1-variance.

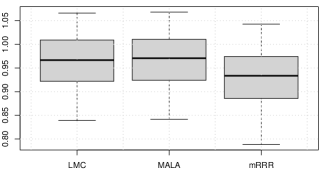

The data are randomly divided into a training set and a test set of size and with respect to the sample size. Model estimation is done by using the training data. Then the predictive performance is calculated on the test data by its mean squared prediction error (the missing entries are discarded in calculation error), where denotes the test set. We repeat the random training/test splitting process times and report the average mean squared prediction error for each method. We ran LMC and MALA with 30000 iterations and the first 5000 steps are ignored as burn-in period. The results are given in Figure 1, we can see that LMC and MALA yield similar results, while mRRR method returns slightly smaller prediction error than LMC and MALA.

7 Conclusion

We proposed a quasi-Bayesian estimation method for reduced rank regression with incomplete responses. We proved the contraction of the posterior and the convergence of the posterior mean at the optimal rate. We implemented our algorithm via LMC and MALA, with promising results. Some questions remain open, such as missing entries in the covariate matrix , and theoretical properties for the case of sampling without replacement might be the object of future works.

Acknowledgments

TTM is supported by the Norwegian Research Council, grant number 309960 through the Centre for Geophysical Forecasting at NTNU.

Availability of data and materials

The R codes and data used in the numerical experiments are available at: https://github.com/tienmt/BRRR_missing .

Errors LMC MALA mRRR LMC MALA mRRR Est 0.165 (0.026) 0.163 (0.026) 0.072 (0.038) 0.157 (0.023) 0.156 (0.024) 0.083 (0.047) Pred 2.234 (0.236) 2.233 (0.234) 2.099 (0.216) 2.174 (0.206) 2.171 (0.210) 2.091 (0.208) Est 0.293 (0.052) 0.288 (0.051) 0.315 (0.278) 0.295 (0.050) 0.286 (0.047) 0.366 (0.210) Pred 2.322 (0.160) 2.313 (0.157) 2.315 (0.338) 2.349 (0.169) 2.338 (0.161) 2.402 (0.281) Est 14.41 (26.59) 1.689 (0.507) 1.707 (0.614) 5.057 (4.356) 1.568 (0.462) 1.328 (0.625) Pred 19.79 (32.99) 3.966 (0.632) 3.718 (0.653) 8.147 (5.418) 3.832 (0.585) 3.345 (0.661)

Errors LMC MALA mRRR LMC MALA mRRR Est 0.104 (0.004) 0.104 (0.004) 0.011 (0.001) 0.107 (0.004) 0.114 (0.004) 0.066 (0.077) Pred 2.118 (0.038) 2.119 (0.038) 2.015 (0.036) 2.116 (0.041) 2.123 (0.042) 2.062 (0.088) Est 0.179 (0.006) 0.178 (0.006) 0.017 (0.002) 0.186 (0.007) 0.198 (0.008) 0.074 (0.068) Pred 2.195 (0.028) 2.195 (0.027) 2.019 (0.025) 2.203 (0.028) 2.217 (0.028) 2.075 (0.071) Est 0.663 (0.032) 0.632 (0.031) 1.902 (0.367) 0.742 (0.037) 0.723 (0.036) 1.483 (0.660) Pred 2.728 (0.045) 2.691 (0.042) 3.899 (0.371) 2.814 (0.054) 2.790 (0.051) 3.480 (0.658)

Errors LMC MALA mRRR LMC MALA mRRR Est 0.157 (0.026) 0.156 (0.025) 0.313 (0.671) 0.161 (0.026) 0.160 (0.025) 0.322 (0.545) Pred 2.184 (0.220) 2.182 (0.218) 2.277 (0.552) 2.193 (0.222) 2.198 (0.226) 2.361 (0.638) Est 0.286 (0.050) 0.281 (0.049) 0.563 (0.660) 0.293 (0.051) 0.288 (0.050) 0.630 (0.698) Pred 2.304 (0.182) 2.298 (0.103) 2.565 (0.733) 2.337 (0.181) 2.332 (0.179) 2.631 (0.731) Est 7.766 (15.18) 1.708 (0.683) 2.985 (1.971) 5.224 (4.204) 1.645 (0.523) 2.444 (1.500) Pred 11.51 (18.81) 3.985 (0.907) 5.097 (2.069) 8.351 (5.232) 3.918 (0.660) 4.505 (1.509)

Errors LMC MALA mRRR LMC MALA mRRR Est 0.470 (0.149) 0.465 (0.148) 0.416 (0.353) 0.460 (0.159) 0.455 (0.158) 0.311 (0.190) Pred 4.439 (1.305) 4.435 (1.305) 4.355 (1.348) 4.379 (1.273) 4.374 (1.271) 4.159 (1.274) Est 0.829 (0.230) 0.812 (0.225) 0.681 (0.341) 0.862 (0.372) 0.840 (0.365) 0.517 (0.213) Pred 4.799 (1.340) 4.777 (1.334) 4.533 (1.306) 4.900 (1.688) 4.870 (1.685) 4.455 (1.521) Est 11.65 (12.26) 4.706 (3.256) 1.457 (0.593) 7.905 (4.779) 3.986 (1.870) 1.012 (0.458) Pred 18.09 (15.31) 9.420 (4.068) 5.546 (1.772) 13.32 (5.885) 8.510 (2.374) 4.986 (0.961)

| LMC | MSE | 0.279 (0.046) | 0.280 (0.046) | 0.288 (0.049) | 0.347 (0.064) |

|---|---|---|---|---|---|

| ECovR | 0.776 (0.047) | 0.911 (0.032) | 0.999 (0.003) | 1.0 (0.0) | |

| MALA | MSE | 0.277 (0.045) | 0.276 (0.045) | 0.276 (0.046) | 0.323 (0.065) |

| ECovR | 0.840 (0.041) | 0.950 (0.026) | 1.000 (0.001) | 1.0 (0.0) |

| LMC | MSE | 0.287 (0.044) | 0.291 (0.045) | 0.393 (0.060) | 1.415 (1.899) |

|---|---|---|---|---|---|

| ECovR | 0.909 (0.034) | 0.905 (0.033) | 0.858 (0.038) | 0.575 (0.072) | |

| MALA | MSE | 0.283 (0.044) | 0.278 (0.044) | 0.224 (0.037) | 2.508 (4.473) |

| ECovR | 0.949 (0.023) | 0.949 (0.022) | 0.955 (0.024) | 0.459 (0.095) |

| missing rate | method | Est | Pred |

|---|---|---|---|

| LMC | 0.023 (0.004) | 0.633 (0.050) | |

| MALA | 0.030 (0.005) | 0.639 (0.054) | |

| mRRR | 0.117 (0.028) | 0.704 (0.056) | |

| LMC | 0.051 (0.021) | 0.670 (0.049) | |

| MALA | 0.057 (0.021) | 0.673 (0.049) | |

| mRRR | 0.131 (0.030) | 0.724 (0.060) | |

| LMC | 0.213 (0.106) | 0.844 (0.134) | |

| MALA | 0.185 (0.097) | 0.803 (0.123) | |

| mRRR | 0.341 (0.006) | 0.914 (0.012) |

Appendix A Appendix: proofs

As mentioned above, our strategy for the proofs is to use oracle type PAC-Bayes bounds, in the spirit of [11]. We start with a few preliminary lemmas, we then provide the proof of Theorem 1 and the proof of Theorem 2.

A.1 Preliminary results

First, we state a version of Bernstein’s inequality taken from [48], (2.21) in Proposition 2.9 page 24.

Lemma 1 (Bernstein’s inequality).

Let , …, be independent real valued random variables. Let us assume that there are two constants and such that and for all integers , Then, for any ,

Another basic tool to derive PAC-Bayes bounds is Donsker and Varadhan’s variational inequality, that we recap here. We refer to Lemma 1.1.3 in Catoni [12] for a proof (among others). From now, for any or , we let denote the set of all probability distributions on equipped with the Borel -algebra. We remind that when , the Kullback-Leibler divergence is defined by if admits a density with respect to , and otherwise.

Lemma 2 (Donsker and Varadhan’s variational formula).

Let . For any measurable, bounded function we have:

Moreover, the supremum with respect to in the right-hand side is reached for the Gibbs measure defined by its density with respect to

| (8) |

These two lemmas are the only tools we need to prove Theorem 1 and Theorem 2. Their proof is quite similar, with a few differences. In order not to do the same derivation twice, we will state the common parts of the proofs as a separate result: Lemma 3. Note that the proof of this lemma will already use Lemmas 1 and 2.

Proof of Lemma 3.

We start by proving the first inequality, that is (11). Fix any with and put

Note that are independent by construction. We have

Next we have, for any integer , that

and use the fact that, for any , to obtain

Thus, we can apply Lemma 1 with , , and . We obtain, for any ,

Rearranging terms, and using the definition of (that is (9)),

Multiplying both sides by and then integrating w.r.t. the probability distribution , we get

Next, Fubini’s theorem gives

and note that for any measurable function ,

to get (11).

Let us now prove (12). Here again, we start with an application of Lemma 1, but this time with (we keep , and ). We obtain, for any ,

Rearranging terms, using the definition of (that is (10)) and multiplying both sides by , we obtain

We integrate with respect to and use Fubini to get:

Here, we use a different argument from the proof of the first inequality: we use Lemma 2 on the integral, this gives directly (12). ∎

Finally, in both proofs, we will use quite often distributions that will be defined as translations of the prior . We introduce the following notation.

Definition 1.

For any matrix , we define by

The following technical lemmas, that can be found for example in [19], will also be useful in the proofs.

Lemma 4 (Lemma 1 in [19]).

We have

Lemma 5 (Lemma 2 in [19]).

For any , we have

with the convention .

A.2 Proof of Theorem 1

Proof of Theorem 1.

We apply Lemma 3, and will start to work on its first inequality (11). An application of Jensen’s inequality yields

We now use the standard Chernoff’s trick to transform an exponential moment inequality into a deviation inequality, that is: , we obtain

| (13) |

Using (2) we have

where we used Jensen’s inequality from the first to the second line, and the definition of from the second to the third. Plugging this into our probability bound (13), and dividing both sides by , we obtain

under the additional condition that is such that , that we will assume from now (note that this is satisfied by ). Using Lemma 2 we can rewrite this as

| (14) |

We stop these derivations for one moment and instead consider now the consequences of the second inequality in Lemma 3, that is (12). Chernoff’s trick and rearranging terms a little, we get

which we can rewrite as

| (15) |

Combining (15) and (14) with a union bound argument gives the bound

It is possible to simplify this bound a little by noting that, for any , implies that and thus

The end of the proof consists in making the right-hand side in the inequality more explicit. In order to do so, we restrict the infimum bound above to the distributions given by Definition 1.

| (16) |

We see immediately that Dalalyan’s lemma will be extremely useful for that. First, Lemma 5 provides an upper bound on . Moreover,

The second term in the right-hand side is null because is centered, and thus

where we used elementary properties of the Frobenius norm, and Lemma 4 in the last line. We can now plug this (and Lemma 5) back into (16) to get:

The result is essentially proven, we just explicit the constants. First, if , then and thus

Then, leads to

Note that satisfies these two conditions, so from now . We also use the following:

So far the bound is:

In particular, with probability at least , the choice gives

∎

A.3 Proof of theorem 2

Proof of Theorem 2.

We also start with an application of Lemma 3, and focus on (11), applied to , that is:

Using Chernoff’s trick, this gives:

where

Using the definition of , for we have

Now, let us define

Using (12), we have that

We will now prove that, if is such that ,

which, together with

will bring

In order to do so, assume that we are on the set , and let . Then,

that is,

or, rewriting it in terms of norms,

We upper-bound the right-hand side exactly as in the proof of Theorem 2, this gives .

∎

Appendix B Appendix: Additional simulations

observed 80% without replacement observed 80% with replacement Errors LMC MALA mRRR LMC MALA mRRR Est 0.165 (0.026) 0.163 (0.026) 0.072 (0.038) 0.190 (0.030) 0.188 (0.030) NA Pred 2.234 (0.236) 2.233 (0.234) 2.099 (0.216) 0.222 (0.044) 0.220 (0.043) NA observed 50% without replacement observed 50% with replacement Est 0.293 (0.052) 0.288 (0.051) 0.315 (0.278) 0.341 (0.071) 0.336 (0.071) NA Pred 2.322 (0.160) 2.313 (0.157) 2.315 (0.338) 0.397 (0.097) 0.391 (0.096) NA observed 20% without replacement observed 20% with replacement Est 14.41 (26.59) 1.689 (0.507) 1.707 (0.614) 8.948 (9.350) 2.280 (0.927) NA Pred 19.79 (32.99) 3.966 (0.632) 3.718 (0.653) 10.76 (11.39) 2.651 (1.125) NA

observed 80% without replacement observed 80% with replacement Errors LMC MALA mRRR LMC MALA mRRR Est 0.157 (0.026) 0.156 (0.025) 0.313 (0.671) 0.185 (0.026) 0.183 (0.027) NA Pred 2.184 (0.220) 2.182 (0.218) 2.277 (0.552) 0.215 (0.038) 0.214 (0.039) NA observed 50% without replacement observed 50% with replacement Est 0.286 (0.050) 0.281 (0.049) 0.563 (0.660) 0.340 (0.062) 0.337 (0.061) NA Pred 2.304 (0.182) 2.298 (0.103) 2.565 (0.733) 0.397 (0.084) 0.392 (0.082) NA observed 20% without replacement observed 20% with replacement Est 7.766 (15.18) 1.708 (0.683) 2.985 (1.971) 7.049 (6.238) 2.207 (0.803) NA Pred 11.51 (18.81) 3.985 (0.907) 5.097 (2.069) 8.473 (7.611) 2.569 (0.980) NA

References

- [1] P. Alquier. Bayesian methods for low-rank matrix estimation: short survey and theoretical study. In International Conference on Algorithmic Learning Theory, pages 309–323. Springer, 2013.

- [2] P. Alquier. User-friendly introduction to PAC-Bayes bounds. preprint arXiv:2110.11216, 2021.

- [3] P. Alquier, N. Marie, and A. Rosier. Tight risk bound for high dimensional time series completion. Electronic Journal of Statistics, 16(1):3001–3035, 2022.

- [4] P. Alquier, J. Ridgway, and N. Chopin. On the properties of variational approximations of Gibbs posteriors. The Journal of Machine Learning Research, 17(1):8374–8414, 2016.

- [5] T. W. Anderson. Estimating linear restrictions on regression coefficients for multivariate normal distributions. Annals of mathematical statistics, 22(3):327–351, 1951.

- [6] P. G. Bissiri, C. C. Holmes, and S. G. Walker. A general framework for updating belief distributions. Journal of the Royal Statistical Society: Series B (Statistical Methodology), pages n/a–n/a, 2016.

- [7] S. Boucheron, G. Lugosi, and P. Massart. Concentration inequalities: A nonasymptotic theory of independence. Oxford University Press, Oxford, 2013.

- [8] F. Bunea, Y. She, and M. H. Wegkamp. Optimal selection of reduced rank estimators of high-dimensional matrices. The Annals of Statistics, 39(2):1282–1309, 2011.

- [9] E. J. Candès and Y. Plan. Matrix completion with noise. Proceedings of the IEEE, 98(6):925–936, 2010.

- [10] E. J. Candes, M. B. Wakin, and S. P. Boyd. Enhancing sparsity by reweighted minimization. Journal of Fourier analysis and applications, 14(5-6):877–905, 2008.

- [11] O. Catoni. Statistical learning theory and stochastic optimization, volume 1851 of Saint-Flour Summer School on Probability Theory 2001 (Jean Picard ed.), Lecture Notes in Mathematics. Springer-Verlag, Berlin, 2004.

- [12] O. Catoni. PAC-Bayesian supervised classification: the thermodynamics of statistical learning. IMS Lecture Notes—Monograph Series, 56. Institute of Mathematical Statistics, Beachwood, OH, 2007.

- [13] A. Chakraborty, A. Bhattacharya, and B. K. Mallick. Bayesian sparse multiple regression for simultaneous rank reduction and variable selection. Biometrika, 107(1):205–221, 2020.

- [14] K. Chen. rrpack: Reduced-Rank Regression, 2022. R package version 0.1-12.

- [15] J. Corander and M. Villani. Bayesian assessment of dimensionality in reduced rank regression. Statistica Neerlandica, 58(3):255–270, 2004.

- [16] V. Cottet and P. Alquier. 1-Bit matrix completion: PAC-Bayesian analysis of a variational approximation. Machine Learning, 107(3):579–603, 2018.

- [17] A. Dalalyan and A. B. Tsybakov. Aggregation by exponential weighting, sharp PAC-Bayesian bounds and sparsity. Machine Learning, 72(1-2):39–61, 2008.

- [18] A. S. Dalalyan. Theoretical guarantees for approximate sampling from smooth and log-concave densities. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 3(79):651–676, 2017.

- [19] A. S. Dalalyan. Exponential weights in multivariate regression and a low-rankness favoring prior. In Annales de l’Institut Henri Poincaré, Probabilités et Statistiques, volume 56, pages 1465–1483. Institut Henri Poincaré, 2020.

- [20] A. S. Dalalyan, E. Grappin, and Q. Paris. On the exponentially weighted aggregate with the laplace prior. The Annals of Statistics, 46(5):2452–2478, 2018.

- [21] A. S. Dalalyan and A. Karagulyan. User-friendly guarantees for the langevin monte carlo with inaccurate gradient. Stochastic Processes and their Applications, 129(12):5278–5311, 2019.

- [22] A. S. Dalalyan and L. Riou-Durand. On sampling from a log-concave density using kinetic langevin diffusions. Bernoulli, 26(3):1956–1988, 2020.

- [23] A. S. Dalalyan and A. B. Tsybakov. Sparse regression learning by aggregation and langevin monte-carlo. Journal of Computer and System Sciences, 78(5):1423–1443, 2012.

- [24] A. Durmus and E. Moulines. Nonasymptotic convergence analysis for the unadjusted langevin algorithm. The Annals of Applied Probability, 27(3):1551–1587, 2017.

- [25] A. Durmus and E. Moulines. High-dimensional Bayesian inference via the unadjusted langevin algorithm. Bernoulli, 25(4A):2854–2882, 2019.

- [26] D. L. Ermak. A computer simulation of charged particles in solution. i. technique and equilibrium properties. The Journal of Chemical Physics, 62(10):4189–4196, 1975.

- [27] R. Foygel, O. Shamir, N. Srebro, and R. Salakhutdinov. Learning with the weighted trace-norm under arbitrary sampling distributions. In Advances in Neural Information Processing Systems, pages 2133–2141, 2011.

- [28] J. Friedman, T. Hastie, and R. Tibshirani. Regularization paths for generalized linear models via coordinate descent. Journal of Statistical Software, 33(1):1–22, 2010.

- [29] P. Germain, A. Lacasse, F. Laviolette, and M. Marchand. PAC-Bayesian learning of linear classifiers. In Proceedings of the 26th Annual International Conference on Machine Learning, pages 353–360, 2009.

- [30] J. Geweke. Bayesian reduced rank regression in econometrics. Journal of econometrics, 75(1):121–146, 1996.

- [31] G. Goh, D. K. Dey, and K. Chen. Bayesian sparse reduced rank multivariate regression. Journal of multivariate analysis, 157:14–28, 2017.

- [32] P. Grünwald and T. Van Ommen. Inconsistency of Bayesian inference for misspecified linear models, and a proposal for repairing it. Bayesian Analysis, 12(4):1069–1103, 2017.

- [33] B. Guedj. A primer on PAC-Bayesian learning. In Proceedings of the second congress of the French Mathematical Society, 2019.

- [34] W. Hoeffding. Probability inequalities for sums of bounded random variables. Journal of the American Statistical Association, 58(301):13–30, 1963.

- [35] A. J. Izenman. Reduced-rank regression for the multivariate linear model. Journal of multivariate analysis, 5(2):248–264, 1975.

- [36] A. J. Izenman. Modern multivariate statistical techniques. Regression, classification and manifold learning, 10:978–0, 2008.

- [37] F. Kleibergen and R. Paap. Priors, posteriors and Bayes factors for a Bayesian analysis of cointegration. Journal of Econometrics, 111(2):223–249, 2002.

- [38] O. Klopp. Noisy low-rank matrix completion with general sampling distribution. Bernoulli, 20(1):282–303, 2014.

- [39] J. Knoblauch, J. Jewson, and T. Damoulas. Generalized variational inference. arXiv preprint arXiv:1904.02063, 2019.

- [40] V. Koltchinskii, K. Lounici, and A. B. Tsybakov. Nuclear-norm penalization and optimal rates for noisy low-rank matrix completion. Ann. Statist., 39(5):2302–2329, 2011.

- [41] J. Langford and J. Shawe-Taylor. PAC-Bayes & margins. In Proceedings of the 15th International Conference on Neural Information Processing Systems, pages 439–446. MIT Press, 2002.

- [42] T. I. Lee, N. J. Rinaldi, F. Robert, D. T. Odom, Z. Bar-Joseph, G. K. Gerber, N. M. Hannett, C. T. Harbison, C. M. Thompson, and I. Simon. Transcriptional regulatory networks in saccharomyces cerevisiae. science, 298(5594):799–804, 2002.

- [43] C. Luo, J. Liang, G. Li, F. Wang, C. Zhang, D. K. Dey, and K. Chen. Leveraging mixed and incomplete outcomes via reduced-rank modeling. Journal of Multivariate Analysis, 167:378–394, 2018.

- [44] T. T. Mai. PAC-Bayesian matrix completion with a spectral scaled Student prior. In Fourth Symposium on Advances in Approximate Bayesian Inference, 2022.

- [45] T. T. Mai and P. Alquier. A Bayesian approach for noisy matrix completion: Optimal rate under general sampling distribution. Electron. J. Statist., 9(1):823–841, 2015.

- [46] T. T. Mai and P. Alquier. Pseudo-Bayesian quantum tomography with rank-adaptation. Journal of Statistical Planning and Inference, 184:62–76, 2017.

- [47] P. Marttinen, M. Pirinen, A.-P. Sarin, J. Gillberg, J. Kettunen, I. Surakka, A. J. Kangas, P. Soininen, P. O’Reilly, and M. Kaakinen. Assessing multivariate gene-metabolome associations with rare variants using Bayesian reduced rank regression. Bioinformatics, 30(14):2026–2034, 2014.

- [48] P. Massart. Concentration inequalities and model selection, volume 1896 of Lecture Notes in Mathematics. Springer, Berlin, 2007. Lectures from the 33rd Summer School on Probability Theory held in Saint-Flour, July 6–23, 2003, Edited by Jean Picard.

- [49] A. Maurer. A note on the PAC Bayesian theorem. arXiv preprint cs/0411099, 2004.

- [50] D. McAllester. Some PAC-Bayesian theorems. In Proceedings of the Eleventh Annual Conference on Computational Learning Theory, pages 230–234, New York, 1998. ACM.

- [51] A. Mishra, D. K. Dey, and K. Chen. Sequential co-sparse factor regression. Journal of Computational and Graphical Statistics, 26(4):814–825, 2017.

- [52] S. Negahban and M. J. Wainwright. Restricted strong convexity and weighted matrix completion: optimal bounds with noise. J. Mach. Learn. Res., 13:1665–1697, 2012.

- [53] R Core Team. R: A Language and Environment for Statistical Computing. R Foundation for Statistical Computing, Vienna, Austria, 2021.

- [54] P. Rigollet and A. B. Tsybakov. Sparse estimation by exponential weighting. Statistical Science, 27(4):558–575, 2012.

- [55] G. O. Roberts and J. S. Rosenthal. Optimal scaling of discrete approximations to langevin diffusions. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 60(1):255–268, 1998.

- [56] G. O. Roberts and O. Stramer. Langevin diffusions and metropolis-hastings algorithms. Methodology and computing in applied probability, 4(4):337–357, 2002.

- [57] G. O. Roberts and R. L. Tweedie. Exponential convergence of langevin distributions and their discrete approximations. Bernoulli, 2(4):341–363, 1996.

- [58] D. Russo and J. Zou. How much does your data exploration overfit? controlling bias via information usage. IEEE Transactions on Information Theory, 66(1):302–323, 2019.

- [59] H. Schmidli. Bayesian reduced rank regression for classification. In Applications in Statistical Computing, pages 19–30. Springer, 2019.

- [60] M. Seeger. PAC-Bayesian generalisation error bounds for Gaussian process classification. Journal of machine learning research, 3(Oct):233–269, 2002.

- [61] R. Velu and G. C. Reinsel. Multivariate reduced-rank regression: theory and applications, volume 136. Springer Science & Business Media, 2013.

- [62] D. Yang, G. Goh, and H. Wang. A fully Bayesian approach to sparse reduced-rank multivariate regression. Statistical Modelling, 2020.

- [63] L. Yang, J. Fang, H. Duan, H. Li, and B. Zeng. Fast low-rank Bayesian matrix completion with hierarchical gaussian prior models. IEEE Transactions on Signal Processing, 66(11):2804–2817, 2018.

- [64] T. Zhang. Information-theoretic upper and lower bounds for statistical estimation. IEEE Transactions on Information Theory, 52(4):1307–1321, 2006.

- [65] H. Zhu, Z. Khondker, Z. Lu, and J. G. Ibrahim. Bayesian generalized low rank regression models for neuroimaging phenotypes and genetic markers. Journal of the American Statistical Association, 109(507):977–990, 2014.