Online Score Statistics for Detecting Clustered Change in Network Point Processes

Rui Zhang*, Haoyun Wang*, Yao Xie

School of Industrial and Systems Engineering (ISyE),

Georgia Institute of Technology, Atlanta, Georgia, USA.

* Authors have equal contribution.

Abstract:

We consider online monitoring of the network event data to detect local changes in a cluster when the affected data stream distribution shifts from one point process to another with different parameters. Specifically, we are interested in detecting a change point that causes a shift of the underlying data distribution that follows a multivariate Hawkes process with exponential decay temporal kernel, whereby the Hawkes process is considered to account for spatio-temporal correlation between observations. The proposed detection procedure is based on scan score statistics. We derive the asymptotic distribution of the statistic, which enables the self-normalizing property and facilitates the approximation of the instantaneous false alarm probability and the average run length. When detecting a change in the Hawkes process with non-vanishing self-excitation, the procedure does not require estimating the post-change network parameter while assuming the temporal decay parameter, which enjoys computational efficiency. We further present an efficient procedure to accurately determine the false discovery rate via importance sampling, as validated by numerical examples. Using simulated and real stock exchange data, we show the effectiveness of the proposed method in detecting change while enjoying computational efficiency.

Keywords: Change-point detection; Graph scanning statistics; Score statistics

Subject Classifications: Primary 62L10; Secondary 62G10, 62G32.

1. INTRODUCTION

Network Hawkes point processes recently became a popular model for sequential events data over networks, a widely encountered data type in modern applications. Such data usually capture the temporal and spatial information of the events, i.e., a sequence of event times, the corresponding event location, and additional information. Multivariate Hawkes process can model the influence of the previous events on the subsequent events, for instance, exciting the subsequent events or causing them more likely to happen. Hawkes processes have been widely used in many areas such as finance (Hawkes, 2018), social media (Rizoiu et al., 2017), epidemiology (Rizoiu, 2018), seismology (Ogata, 1998).

Change-point detection is a fundamental problem in statistics; aiming to detect a transition in the distribution of the sequential data, which often represents a state transition (see, e.g., Moustakides (2008); Poor (2008); Xie and Siegmund (2013); Veeravalli and Banerjee (2014); Tartakovsky (2019); Xie et al. (2021)). For example, in water quality monitoring, a change-point can be due to a water contamination event (Chen et al., 2020); in public health, they may represent a disease outbreak (Christakis and Fowler, 2010). The goal is to develop a procedure that can raise the alarm as soon as possible after the change-point while controlling the false-alarm rate.

Detecting change-points for Hawkes processes is an important problem for monitoring large-scale networks using discrete events data. Online detection of change-points detection in Hawkes processes is considered challenging due to the asynchronous nature of discrete events and temporal dependence, which is far from the traditional i.i.d. setting considered in change-point detection literature. In Wang et al. (2021), the authors propose an adapted version of the CUSUM procedure to account for the dynamic behavior assuming known post-change parameters. When post-change parameters are unknown, a classic method is the generalized likelihood ratio (GLR) procedure, and Li et al. (2017) use the Expectation-Maximization type of algorithm to estimate the post-change parameters of Hawkes processes and then compute the generalized likelihood ratios. This method needs large memory and computation time to obtain the maximum likelihood estimates at each time instance. An alternative to GLR is the score test (Rao, 2005), which does not require computing the MLE. The score test is well studied and widely applied. In the univariate case, the score test is the most powerful test for small deviation from the null hypothesis. For multi-stream network data, a strategy is needed to combine the high dimensional statistic – Xie and Xie (2021) proposed a graph scanning statistics by computing the statistics for subgraphs which is helpful to detect and identify the local changes. Besides online change-point detection, recent work by Wang et al. (2020) also developed methods and established theoretical guarantees for offline change-point detection for Hawkes processes.

In this paper, we present a graph scan score statistic for detecting local changes that happen as a cluster in the network when observing sequential discrete event data that can be modeled using point processes. The change causes an unknown shift in the underlying parameter of the Hawkes process over a sub-network. We assume the parameters of the pre-change distributions are known since typically abundant “normal” and “in-control” data can be used to estimate the pre-change parameters with good precision. We assume the post-change parameters are unknown since they are typically due to an unexpected anomaly. This motivates us to consider the score statistic, which detects a departure from the “normal” data without having to estimate the post-change parameters. We present the asymptotic distribution of the score statistic, which enables us to develop the self-normalizing scan statistic over pre-defined candidate scanning clusters. This also leads to an accurate approximation of the instantaneous false alarm probability, the false alarm rate, the average run length and an efficient procedure to accurately determine the false discovery rate via importance sampling, as validated by numerical examples. The good performance of our procedures compared with the benchmarks is tested with numerical experiments with simulated and real stock exchange data.

The rest of our paper is organized as follows. Section 2 provides the background knowledge of the multivariate Hawkes process. Section 3 presents the definition of our problem. Section 4 proposes our detection procedure and includes the analysis of our scan score statistics. In section 5, there are experiments of a simulation study and real-world data application. Section 6 concludes our paper.

2. PRELIMINARIES

A multivariate Hawkes process is a self-exciting process over a network. Let denote the number of nodes in the network and denote . The data is of the form , where denotes the location of the th event and denotes the time of the th event. A multivariate Hawkes Process is actually a special case of spatio-temporal counting process (Rathbun, 1996). Let denote the history before time , i.e. the -algebras of events before time ; is a filtration, an increasing sequence of -algebras. Let denote the number of events on th node up to time , i.e., a counting process,

where denotes the indicator variable. Then, a multivariate Hawkes process can be determined by the following conditional intensity function (Reinhart, 2018):

| (2.1) |

For a multivariate Hawkes process, the conditional intensity function takes the form:

| (2.2) |

Here is the base intensity and is the kernel function that characterized the influence of the previous events. Specifically, we assume a commonly used exponential kernel, i.e.,

| (2.3) |

where is a parameter that controls the decay rate. Let and , of which the th entry is . A multivariate Hawkes process with exponential kernel is parametrized by the base intensity , influence matrix and decay rate . Given all the events in time window , the log likelihood function is given by:

| (2.4) |

where denote the number of events before time . Note that when , the process becomes a multivariate Poisson process.

3. PROBLEM SETUP

Consider a network with nodes; we can observe a sequence of events on each node over time. There may exist a change-point in time if the following applies. Before time , the events of the network follow a multivariate Hawkes process withparameters , , and . After time , the events of the network follow a multivariate Hawkes of which the influence matrix change from to . The pre-change and post-change multivariate Hawkes processes are assumed to be stationary, i.e., and where represents the spectral norm. To detect whether a change-point exists in the given data, we consider the following hypothesis test:

| (3.1) |

where is the true conditional intensity of node at time , and are the th entry of and , respectively. In particular, we refer to and as the network parameters as they describe the interactions (influences) between nodes in the network.

4. SCAN SCORE STATISTICS DETECTION PROCEDURE

To perform the sequential hypothesis test (3.1), we proposed a detection procedure base on scan score statistics. A score statistics corresponds to the first-order derivative of the log-likelihood function. In a multivariate Hawkes network, we are interested in the influence between multiple pairs of nodes (i.e., the entries in the influence matrix ). For each pair, we can derive the score statistics which leads to a multi-dimensional vector of score statistics. Based on that, we use a scanning strategy to compute our test statistics, similar to Chen et al. (2020); He et al. (2018). Specifically, we divide the network into several clusters, compute the score statistics in each cluster at each time , and then obtain a detection statistic for each cluster by summing up the standardized score statistics in the corresponding cluster. Finally, we take the maximum over all the clusters to form the scan score statistics at time for the entire network. More details will be discussed in this section.

4.1. Score Statistics

Since the change in hypothesis test (3.1) is caused by the change of influence matrix, we define the following score statistics, given data up to time , with respect to :

| (4.1) |

Moreover, define is the vector of all elements in . According to Theorem 1 in Rathbun (1996), we have the following corollary.

Lemma 4.1.

Under the assumptions in Rathbun (1996), assume the influence matrix of the multivariate Hawkes Process is . The score function satisfies that,

where is the Fisher information.

4.1.1. Theoretical Characterization of Fisher Information

When , it is possible to compute as shown in the following theorem. For simplicity, let’s define as the set of events at node before time , i.e. .

4.1.2. Estimation of

When , it is difficult to compute the variance theoretically. According to Rathbun (1996), we have the following approximation of .

Theorem 4.2.

With the same assumption as in Theorem 4.1. We have the following estimation of fisher information. Let

| (4.4) |

We have , i.e. ,

| (4.5) |

where is the asymptotic (co)variance of and .

4.2. Scan Score Statistics

To combine all the score statistics and complete the detection procedure, we compute the scan statistics based on given clusters. A cluster is a directed subgraph, with the set of nodes and the set of edges , where is the number of clusters. In practice, to reduce the computation cost, we only compute the score statistics given data in a time window of length , and update the statistics every time units, where . Specifically, at time which is a multiple of , for the th cluster, we compute all the interested score statistics at the pre-change parameter with data in and have a vector of score statistics denoted as . Let and denote the dimension and Fisher information corresponds to edges in respectively. Then the detection statistics for cluster at time , with window length is:

| (4.6) |

Note that the scan statistic has a “self-normalizing” property in that their asymptotic distributions are standard normal for multiple candidate clusters, which will facilitate the false alarm control by choosing a threshold. For example if we are interested in detecting a shift from a Poisson process, all we need is to evaluate , which only requires the pre-change parameter without having to estimate the post-change parameter . The estimation of can be difficult to perform online given limited post-change observations, since we would like to detect the change quickly.

Then at each time , we compute the scan score statistics over the candidate clusters:

Given a threshold , we stop our procedure and raise an alarm to detect a local change-point using the following rule:

| (4.7) |

In the following, we discuss the false alarm probability at any instant in Section 4.2.1, then provide the performance analysis of in Section 4.2.2. Here the choice of the threshold controls the tradeoff between the false alarm rate and average run length versus the detection delay. The proposed method can also be used to localize the change once an alarm is raised, and we briefly discuss the false discovery rate in Appendix A.

4.2.1. Instantaneous False Alarm Probability of Scan Statistics at a Given

According to Lemma 4.1, the score converge in distribution to as . Since the Hawkes process is stationary, also converge to the same distribution as . The statistics are linear combinations of , then after scaling the time by , the process converge pointwise to a Gaussian process as , and the covariance can be characterized by

| (4.8) |

where the covariance between and can be found in close form when using Theorem 4.1 and estimated using historical data by Theorem 4.2. At time , we want to control the instantaneous false alarm probability

| (4.9) | |||||

Let denote the vector of s. To control the upper bound of the instantaneous false alarm probability, we compute (4.9) with the technique in Botev (2015):

| (4.10) |

where is the permutation matrix interchanging first entry and the th entry, and

| (4.20) |

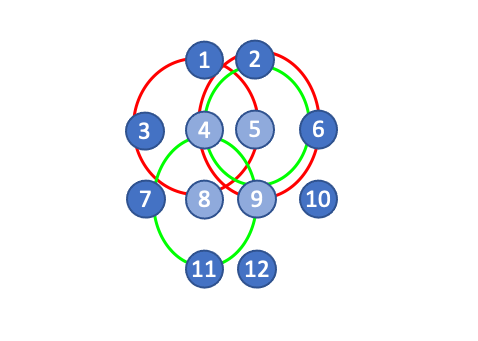

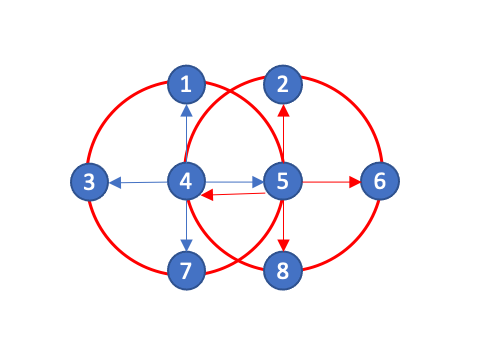

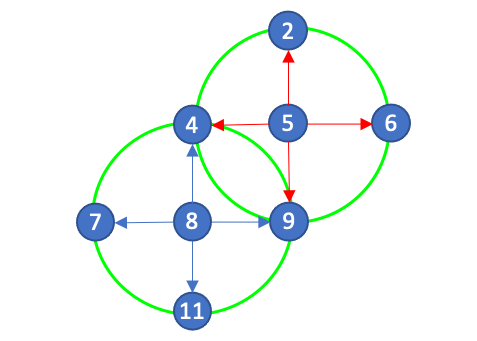

Here follows a Gaussian distribution where the covariance can be computed with (4.8) according to the network topology and the score statistics in the clusters. In Botev (2015), the authors provide an importance sampling algorithm to estimate (4.2.1). Figure 1 is an example of the cluster structure and the corresponding when .

Remark 4.1.

Since our scan statistics are standardized, determining the threshold with the method in eq.(4.2.1) does not depend on the window length . However, with a larger the Gaussian process approximation would be better. In Table 1, we can see, as window length increases, the instantaneous false alarm probability would be better controlled.

| 50 | 3 | 0.0174 | |

| 100 | 3 | 0.0146 | |

| 200 | 3 | 0.0114 | |

| 50 | 2.8 | 0.0282 | |

| 100 | 2.8 | 0.0226 | |

| 200 | 2.8 | 0.0210 |

4.2.2. Performance metrics of the stopping time

In this part, we provide an upper bound of the false alarm rate (FAR) and average run length (ARL) based on the Gaussian process approximation and the analysis of the instantaneous false alarm probability. Then we discuss the detection delay and the choice of the window length and update interval .

The FAR is the conditional probability that the procedure will stop at the next update, given that there has been no false alarm yet.

We have the following result on the FAR.

Theorem 4.3.

As , if is upper bounded by some constant ,

The ARL of is , the expected stopping time under . To evaluate the ARL, we are going to show that is approximately exponential distribution with some parameter . The analysis is similar to Yakir (2009). Let , such that is in the same order as the instantaneous false alarm probability. For any and interval , we decompose it into sub-intervals with length , i.e . For simplicity, we assume and are integers.

Let indicator denotes , and define , then we have

To prove that is approximately exponential, it is same to prove is approximately Poisson distributed. We herein apply the result from Arratia et al. (1989). According to the Theorem I in Arratia et al. (1989), we establish the following theorem.

Theorem 4.4.

Let be the stopping time defined in eq.(4.7), be the indicator defined above and be the sum of the indicators. With , for any fixed ,

| (4.21) |

The theorem above can be used to obtain an approximation of ARL. According to the construction of , we have

By Theorem 4.4, and

| (4.22) | |||||

| (4.23) |

Therefore, we can use our instantaneous false alarm probability approximation in Section 4.2.1 to approximate (4.22). We can numerically verify that this is a reasonably accurate approximation, in Section 5.1.

Remark 4.2.

To evaluate the performance of our scanning statistics, we also need the expected detection delay (EDD). Since we are using a Shewhart chart type of detecting procedure, the EDD varies with the window length. In practice, the window length can be chosen by considering the smallest change we want to detect on each cluster. Then will be the smallest window length that has enough power to detect the change successfully, i.e., under the post-change scenario, if the change happens on the -th cluster.

Remark 4.3.

The performance of our scanning statistic also depends on the update interval , where a smaller results in both a smaller ARL and EDD. However, there seems to be little point in choosing to frequently check for a potential change-point while sacrificing computation efficiency because we expect the change is not too large and cannot be reflected immediately in the detecting statistic .

5. EXPERIMENTS

5.1. Simulated Result of ARL and EDD

In this experiment, the network is set up as shown in Figure 1. The event in each node follows a Poisson process with , and we set the . The window length is set to be , and the statistics are computed for each time unit. In Table 2, we show the estimated ARL from simulation with the threshold estimated by (4.22) and (4.23) for and , which corresponds to .

To obtain the simulated ARL, we generate events in time window and compute the run length when the statistics exceed the corresponding threshold. Note that this approximation will always underestimate the ARL since we can only generate events in a finite time window. We can see the thresholds computed from (4.22) give us desired results. However, (4.23) tends to overestimate the threshold.

| theoretic ARL | simulated ARL | ||

|---|---|---|---|

| Results of (4.22), | 3.3718 | 10000 | 9189 |

| Results of (4.22), | 3.3859 | 10000 | 9561 |

| Results of (4.23) | 3.6625 | 10000 | 21773 |

| Results of (4.22), | 3.5824 | 20000 | 17158 |

| Results of (4.22), | 3.5867 | 20000 | 17655 |

| Results of (4.23) | 3.8352 | 20000 | 41701 |

Now, let’s compare the expected detection delay (EDD) of our proposed method with the generalized likelihood ratio (GLR) method in Li et al. (2017). In the experiments of EDD, the distribution under is set as mentioned above. The thresholds of our methods are set according to the estimate of eq.(4.22) with , so that our desired ARL are 10000 or 20000 (see details in Table 2). As for the GLR, we compute the log generalized likelihood ratio with frequency per time unit and window length with and without the cluster structure. For the GLR with the cluster structure (GLR-C), similar to the proposed method, we compute the statistic on each of the clusters and take the maximum. For the vanilla GLR we consider a change on the 16 edges in the union of the 4 clusters. The maximum likelihood estimates of the and are computed by the EM method. The thresholds of the desired ARLs are estimated with simulation.

We compare the performance of our methods with GLR and GLR-C in different settings and the results are shown in Table 3. The EDDs are shown in columns 4-9 of Table 4. The results show that our proposed method achieves better performance when the change is within cluster and balanced on the edges (Case ()-()). In Case where the change happens on multiple clusters and in Case where the change happens on only part of a cluster, the proposed method is comparable to GLR with or without the cluster structure. Table 5 shows the advantage of our method: the computation time of our proposed methods is much less than the GLR methods, since our method does not require estimating the post-change distribution parameters. However in Case if the change happens on a single edge, in other words, the clusters cannot accurately capture the topology of the local change, the performance of score based method can be worse than GLR.

| Changed parameters in post-change distribution | |

|---|---|

| Case i | |

| Case ii | |

| Case iii | |

| Case iv | |

| Case v | |

| Case vi | |

| Case vii |

| Method | threshold | ARL | Case i | Case ii | Case iii | Case iv | Case v | Case vi | Case vii |

|---|---|---|---|---|---|---|---|---|---|

| Proposed | 3.400 | 10000 | 104.5 | 44.43 | 46.89 | 54.02 | 45.34 | 81.92 | 159.0 |

| GLR-C | 7.705 | 10000 | 108.9 | 48.77 | 47.77 | 51.38 | 39.61 | 68.71 | 97.91 |

| GLR | 11.35 | 10000 | 119.1 | 52.36 | 51.73 | 52.20 | 41.06 | 74.23 | 105.6 |

| Proposed | 3.635 | 20000 | 111.9 | 47.40 | 49.54 | 57.82 | 49.31 | 89.16 | 176.9 |

| GLR-C | 8.600 | 20000 | 117.0 | 51.82 | 50.33 | 55.74 | 42.42 | 72.85 | 103.84 |

| GLR | 12.45 | 20000 | 128.2 | 55.30 | 55.16 | 55.85 | 42.81 | 79.49 | 112.5 |

| Method | Proposed | GLR-C | GLR |

|---|---|---|---|

| Duration (s) | 3.789 | 20.47 | 72.97 |

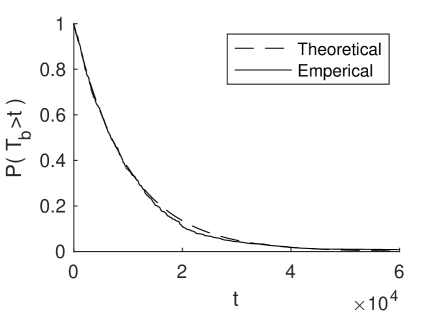

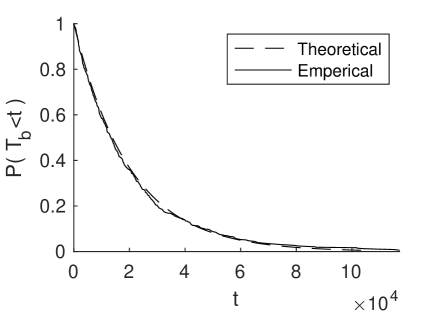

Finally, we can verify the exponentiality of the run length by comparing the empirical c.d.f. over 500 experiments vs. the theoretical one, as shown in Figure 2.

5.2. Real-data

In this section, we apply our scan statistics on a memetracker data and stock data.

-

•

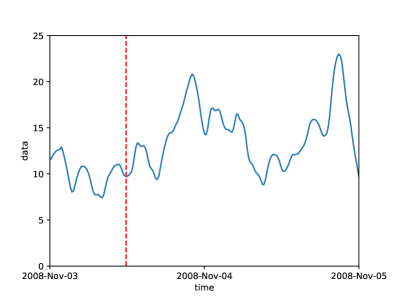

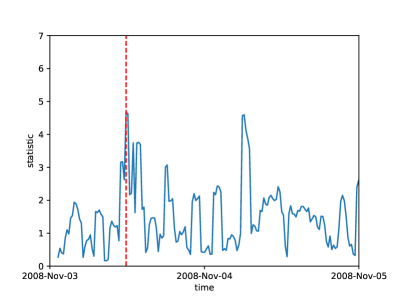

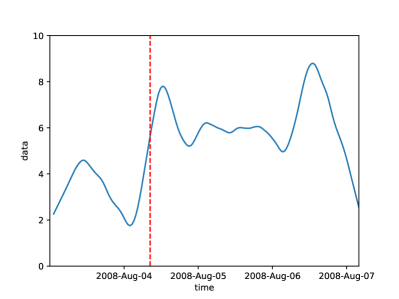

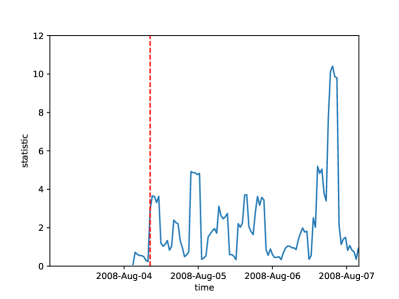

memetracker data: It tracks texts and phrases, which are called memes, over different websites. This data is used to study information diffusion via social media and blogs. We use three meme data in Li et al. (2017). The first data is “Barack Obama was elected as the 44th president of the United States”. We use data from the top 40 news websites, which include Yahoo, CNN, Nydaily, The Guardian, etc. We use the data from Nov.01.2008 to Nov.02.2008 as the training data and the data from Nov.03.2008 to Nov.05.2008 as the test data. Our procedure detects a change at the time around 7 pm on Nov. 03, which is a few hours before the votes. The second data is “the summer Olympics game in Beijing”. We use data from Aug.01.2008 to Aug.03.2008 as the training data and data from Aug.04.2008 to Aug.15.2008 as the test set.

-

•

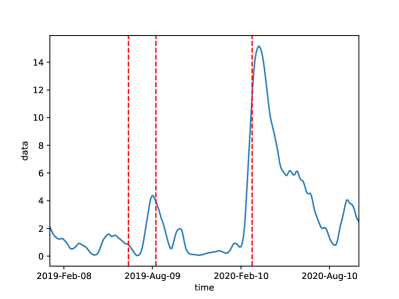

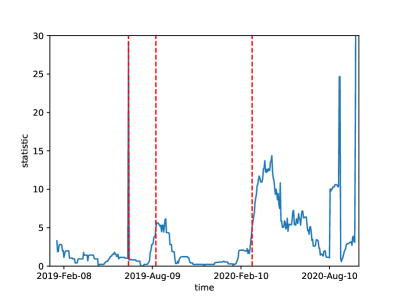

Stock price data: This data is downloaded from Yahoo Finance. We collect the closing price and trading volume of stock tickers: SPY, QQQ, DIA, EFA, and IWM, which are all index-type stocks and can reflect the situation of the overall stock market. For each ticker, we construct 3 types of events. High return: the day with a return over 90 percentile. Low return: the day with a return below 10 percentile. High volume: the day with trading volume over 90 percentile. Therefore, in this data, we have a network with 15 nodes. Such extreme trading events are of interest in the study of finance Embrechts et al. (2011). We use the data from Jan.04.2016 to Dec.31.2018 as the training data and data from Jan.01.2019 to Dec.31.2020 as the test data.

For each data, we apply the Newton method to fit the MLE of the parameters for the training set. Then, we use the fitted parameters to compute the scan statistics on the test set. For memetracker data, we construct the cluster by applying community detection methods on the fitted . For stock data, each cluster is the events that are related to a certain ticker. Details are shown in table 6. The change point detected from the “Obama” data is around 7 am on 2008.11.03. The result indicates that the public opinion of Barack Obama changed around one day before the votes. For the “Olympic” data, our procedure detects a change on Aug.04, three days before the Olympic game. For the stock data, we detect three-time intervals of which the starting dates are 2019.06.21, 2019.08.16, and 2020.03.04. According to the news, the first change-point 2019.06.21 is the date that the S&P 500 hit a new record high, and the three major stock indexes surged on different scales. The second change-point 2019.08.16 is related to the US-China trade war. In August 2019, both US and China made multiple announcements about their tariffs. The last change-point is 2020.03.04, which is three business days before the first circuit breaker in 2020. There are many change-points after the first circuit breaker 2020.03.09, which indicates a long-term change in the stock market caused by pandemics and trade war. Real data results show that our proposed scan statistics achieve good performance in detecting the real change in different areas such as social media and financial markets.

| Data | training set | test set | # of cluster | thresholds | change-points |

|---|---|---|---|---|---|

| “Obama” | 08.11.01-08.11.02 | 08.11.03-08.11.05 | 5 | 4 | 11.03 7am |

| “Olympic” | 08.08.01-08.08.03 | 08.08.04-08.08.08 | 4 | 4 | 08.04 6pm |

| stock data | 16.01.04-18.12.31 | 19.01.01-20.12.31 | 5 | 4 | 19.06.21, 19.08.16, 20.03.04 |

6. CONCLUSION

In this paper, we propose scan score statistics for detecting the change-points of network point processes. We use the multivariate Hawkes process to model the sequential event data. Our proposed method is based on score statistics without the requirement to estimate the post-change network parameters, which can be difficult to perform given limited post-change samples since we would like to detect the change quickly. In this sense, our method is more computationally efficient than the conventional GLR method, which is essential in online detection. We derive the asymptotic properties of the scan statistic, which enables us to provide further analysis of the instantaneous false alarm probability, false alarm rate, average run length and develop a computationally efficient procedure to calibrate the threshold for false alarm control. In experiments, we first use simulated data to verify our theoretical results. We also perform our method in real-world data, which shows a promising detection performance. Future work includes providing a more detailed discussion on the false discovery rate of localizing the unknown change (some initial results are in Appendix A).

ACKNOWLEDGEMENT

The authors would like to thank the anonymous referees, an Associate Editor and the Editor for their constructive comments that improved the quality of this paper. The work is partially supported by NSF CCF-1650913, NSF DMS-1938106, NSF DMS-1830210, and CMMI-2015787.

References

- (1)

- Arratia et al. (1989) Arratia, R., Goldstein, L., and Gordon, L. (1989). Two Moments Suffice for Poisson Approximations: the Chen-Stein Method, The Annals of Probability 17(1): 9-25.

- Botev (2015) Botev, Z. I., Mandjes, M., and Ridder, A. (2015). Tail Distribution of the Maximum of Correlated Gaussian Random Variables, 2015 Winter Simulation Conference (WSC): 633-642.

- Chen et al. (2020) Chen, J., Kim, S. H., and Xie, Y. (2020). S 3 T: A Score Statistic for Spatiotemporal Change Point Detection, Sequential Analysis 39(4): 563-592.

- Christakis and Fowler (2010) Christakis, N. A. and Fowler, J. H. (2010). Social Network Sensors for Early Detection of Contagious Outbreaks, PloS One 5(9): e12948.

- Feller (1957) Feller, W. (1957). An Introduction to Probability Theory and Its Applications.

- Hawkes (1971) Hawkes, A. G. (1971). Spectra of Some Self-exciting and Mutually Exciting Point Processes, Biometrika 58(1): 83-90.

- Hawkes (2018) Hawkes, A. G. (2018). Hawkes Processes and Their Applications to Finance: A Review, Quantitative Finance 18(2): 193-198.

- Embrechts et al. (2011) Embrechts, P., Liniger, T., and Lin, L. (2011). Multivariate Hawkes Processes: An Application to Financial Data, Journal of Applied Probability 48(A): 367-378.

- He et al. (2018) He, X., Xie, Y., Wu, S. M., and Lin, F. C. (2018). Sequential Graph Scanning Statistic for Change-point Detection, 2018 52nd Asilomar Conference on Signals, Systems, and Computers: 1317-1321.

- Li et al. (2017) Li, S., Xie, Y., Farajtabar, M., Verma, A., and Song, L. (2017). Detecting Changes in Dynamic Events Over Networks, IEEE Transactions on Signal and Information Processing over Networks 3(2): 346-359.

- Moustakides (2008) Moustakides, G.V. (2008). Sequential change detection revisited. The Annals of Statistics 36(2): 787-807.

- Ogata (1998) Ogata, Y. (1998). Space-Time Point-Process Models for Earthquake Occurrences, Annals of the Institute of Statistical Mathematics 50(2): 379–402.

- Poor (2008) Poor, H.V. and Hadjiliadis, O. (2008). Quickest detection. Cambridge University Press.

- Rao (2005) Rao, C.R. (2005). Score test: historical review and recent developments. Advances in ranking and selection, multiple comparisons, and reliability: 3-20.

- Rathbun (1996) Rathbun, S. L. (1996). Asymptotic Properties of the Maximum Likelihood Estimator for Spatio-temporal Point Processes, Journal of Statistical Planning and Inference 51(1): 55-74.

- Reinhart (2018) Reinhart, A. (2018). A Review of Self-exciting Spatio-temporal Point Processes and Their Applications, Statistical Science 33(3): 299-318.

- Rizoiu et al. (2017) Rizoiu, M. A., Lee, Y., Mishra, S., and Xie. L. (2017). Hawkes Processes for Events in Social Media, Frontiers of Multimedia Research: 191–218.

- Rizoiu (2018) Rizoiu, M. A., Mishra, S., Kong, Q., Carman, M., and Xie, L. (2018). SIR-Hawkes: Linking Epidemic Models and Hawkes Processes to Model Diffusions in Finite Populations, in proceedings of 2018 world wide web conference: 419-428.

- Siegmund et al. (2011) Siegmund, D. O., Zhang, N. R., and Yakir, B. (2011). False Discovery Rate for Scanning Statistics, Biometrika 98(4): 979-985.

- Tartakovsky (2019) Tartakovsky, A.G. (2019). Sequential change detection and hypothesis testing: general non-iid stochastic models and asymptotically optimal rules. Chapman and Hall/CRC.

- Veeravalli and Banerjee (2014) Veeravalli, V.V. and Banerjee, T. (2014). Quickest change detection. Academic press library in signal processing 3: 209-255. Elsevier.

- Wang et al. (2021) Wang, H., Xie, L., Xie, Y., Cuozzo, A., and Mak, S. (2022). Sequential Change-point Detection for Mutually Exciting Point Processes over Networks. Accepted, Technometrics and arXiv preprint arXiv:2102.05724.

- Wang et al. (2020) Wang, D., Yu, Y., and Willett, R. (2020). Detecting Abrupt Changes in High-Dimensional Self-Exciting Poisson Processes. arXiv preprint arXiv:2006.03572.

- Xie and Siegmund (2013) Xie, Y. and Siegmund, D. (2013). Sequential multi-sensor change-point detection. The Annals of Statistics, 41(2): 670-692.

- Xie et al. (2021) Xie, L., Zou, S., Xie, Y., Veeravalli, V. (2021). Sequential (quickest) change detection: Classical results and new directions, IEEE Journal on Selected Areas in Information Theory 2(2): 494-514.

- Xie and Xie (2021) Xie, L. and Xie, Y. (2021). Optimality of Graph Scanning Statistic for Online Community Detection, 2021 IEEE International Symposium on Information Theory (ISIT): 386-390.

- Yakir (2009) Yakir, B. (2009). Multi-channel Change-point Detection Statistic with Applications in DNA Copy-number Variation and Sequential Monitoring, in proceedings of Second International Workshop in Sequential Methodologies: 15-17.

Appendix Appendix A Extension: False Discovery Rate of Change Localization

This section discusses an extension of the change-point detection: false identification after the change detection. After a change has been detected, it is sometimes also of interest to localize it and find the cluster where it happens. This corresponds to multiple hypothesis tests given all the information up to . More specifically, at a given , we check whether is true or not, for . Our procedure stops, whenever there is at least one discovery, i.e. , such that . Let denote the number of such discoveries. Among these discoveries, there are true discoveries and false discoveries. Let denote the number of false discoveries. Then the false discovery rate is defined as:

| (A.1) |

which is of interest in the study of scanning statistics.

Siegmund et al. (2011) provides an estimator for the FDR, under the assumptions: (i) is Poisson distributed with expected value ; and (ii) the number of false discoveries is independent of the number of true discoveries . The estimator is given by:

In our procedure, assume that and is large, with similar proof of Theorem 4.4, we can also show that the first assumption is satisfied, i.e:

| (A.2) |

As for the second assumption, similar to the discussion in Siegmund et al. (2011), if each cluster does not largely overlap with each other, most of them are independent. In such a case, the false positives should be an approximately uniform distribution over all clusters. If the true signals do not frequently occur, a false positive is close to a true signal with a very small probability. Therefore, the second assumption is approximately satisfied too. To control the false discovery rate, we only need to compute the threshold according to eq.(A.2) for a desired . Recall that .

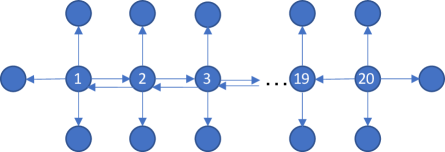

Below, we present several simulated examples to demonstrate that the simulated result of the estimation in eq.(A.2) provides an accurate approximation of the actual discovery rate. In this experiment, the network contains 20 clusters as shown in Figure 4. All the clusters are placed in a line. Same as the previous simulated study, the pre-change distribution is a Poisson process with . After , the distribution of one cluster change to a Hawkes process with all the cross-excitation from the center to the neighboring nodes equal to 0.2. We generated the data of total length equal to 400 with and . All the clusters are scanned with all the data up to 400. The experiments are repeated 200 times to compute the average number of false discovery, true discovery and false discovery rates. Table 7 is the result. Notice that and it is close to the numbers in the last column, which shows a good approximation of eq.(A.2).

| 1.6 | 0.530 | 2.11 | 0.285 | 2.19 |

| 1.8 | 0.406 | 1.35 | 0.24 | 1.44 |

| 2 | 0.281 | 0.8 | 0.185 | 0.91 |

| 2.2 | 0.174 | 0.455 | 0.15 | 0.556 |

| 2.4 | 0.113 | 0.28 | 0.12 | 0.328 |

| 2.6 | 0.064 | 0.155 | 0.095 | 0.186 |

| 2.8 | 0.038 | 0.085 | 0.075 | 0.102 |

| 3.0 | 0.026 | 0.055 | 0.06 | 0.054 |

| 3.2 | 0.018 | 0.035 | 0.045 | 0.027 |

| 3.4 | 0.010 | 0.002 | 0.035 | 0.013 |

Appendix Appendix B Proof of Theorem 4.1

Proof..

-

(i)

Since under , has the same the distribution as the univariate case.

-

(ii)

To prove the variance of , we use the fact that . Then

(B.1) (B.2) (B.3) (B.4) (B.5) where and are the number of events in on nodes and respectively. In eq(B.2), we use the fact that for Poissson process, the arrival times follow uniform distribution when it is conditional on the number of arrivals. With this fact, in eq(B.3), we define

Since , then

which proves the eq(B.4). Since and follow Poisson distribution with mean and , respectively. Therefore eq(B.5) is prooved.

-

(iii)

Follow the similar techniques in (ii), we can prove

∎

Appendix Appendix C Proof of Theorem 4.2

Proof..

Follow the definition in Rathbun (1996), let’s define the kernel function,

where Then, we can define the conditional intensity function:

where , if , and is the vector that th entry is 1 and other entries are 0. Further, define a measure with delta function:

We can write the likelihood function as the following:

We can easily check this define the same multivariate Hawkes process in eq.(2.2), (2.3), (2.4). Define the function as:

where is the partial derivative of with respect to . Therefore, by the result in eq.(4.7) of Rathbun (1996), we have:

By direct computation, we can have the result of eq.(4.4) ∎

Appendix Appendix D Proof of Theorem 4.3

Proof..

For every , let . Then . For the smallest , clearly there is equals to the instantaneous false alarm probability. Also there is for every ,

Since and are independent, we have

As , the instantaneous false alarm probability goes to 0, and for large enough , there exists some , , such that . Then by induction we can see for every ,

∎

Appendix Appendix E Proof of Theorem 4.4

Proof..

According to the Theorem I in Arratia et al. (1989), let’s define the “neighbor of dependence” for index , , with simple modification for and , for , and are independent for . Therefore the dependence of elements not in the neighbor vanished, i.e. and equals to 0.

| (E.1) | |||||

Note that the event is the union of and , and the former is independent of . The same decomposition can be done to . Then can be upper bounded by

| (E.2) | |||||

With the inequality of the tail probability of normal distribution in Feller (1957),

where is the tail probability of standard normal random variable. With the same computation, we can show

Therefore with the Theorem 1 in Arratia et al. (1989),

| (E.3) | |||||

| (E.4) | |||||

| (E.5) | |||||

| (E.6) | |||||

| (E.7) |

which becomes small when and . ∎