Incrementality Bidding via Reinforcement Learning under Mixed and Delayed Reward††thanks: Part of the work of Haifeng Xu was completed while visiting Google Research.

Abstract

Incrementality, which measures the causal effect of showing an ad to a potential customer (e.g. a user in an internet platform) versus not, is a central object for advertisers in online advertising platforms. This paper investigates the problem of how an advertiser can learn to optimize the bidding sequence in an online manner without knowing the incrementality parameters in advance. We formulate the offline version of this problem as a specially structured episodic Markov Decision Process (MDP) and then, for its online learning counterpart, propose a novel reinforcement learning (RL) algorithm with regret at most , which depends on the number of rounds and number of episodes , but does not depend on the number of actions (i.e., possible bids). A fundamental difference between our learning problem from standard RL problems is that the realized reward feedback from conversion incrementality is mixed and delayed. To handle this difficulty we propose and analyze a novel pairwise moment-matching algorithm to learn the conversion incrementality, which we believe is of independent interest.

1 Introduction

Nowadays, online advertising systems (e.g. Google, Facebook, and Amazon) have demonstrated their significant power for connecting advertisers and potential customers. Moreover, automated auctions are widely used in online ad platforms for matching advertisers and users, and for price discovery (Varian, 2006; Edelman et al., 2007). Many advertisers are bidding repeatedly online to show ads to users. Therefore, an important problem for advertisers is to design efficient bidding algorithms to maximize their accumulated utility. Moreover, this is also an important problem for online ad platforms, because auto-bidding — i.e., the advertisers authorize ad platforms to bid on behalf of them —has become prevalent in online advertising (Facebook, 2022; Google, 2022).

A growing body of work is investigating the problem of learning to bid in repeated auctions (Weed et al., 2016; Feng et al., 2018; Balseiro et al., 2019; Han et al., 2020b, a; Badanidiyuru et al., 2021b; Noti and Syrgkanis, 2021; Nedelec et al., 2022). However, existing work assumes that the value of showing ads to a user (after winning the auction) comes from either an oblivious adversary or is sampled from an underlying fixed distribution. Unfortunately, this ignored the crucial causal effect of showing an ad to a potential customer and cannot capture how much an ad will change the user’s conversion rate, which should have been what the advertiser is bidding for. For example, if a user sees the same ad multiple times in a very short time period, then the conversion 111A conversion represents a desired interaction between the user and advertiser, e.g., download the App or buy the products from the advertiser. of this user may not be much better — in fact, may even be worse — than that of showing ads to this user only once within this period. Such multiple redundant ad placements are commonly known in reality to be cost-inefficient for the advertisers, but cannot be captured by previous models of learning to bid with either random or completely adversarial ad values. To overcome the drawbacks of previous approaches in measuring the value of an advertising opportunity, a recent visionary whitepaper by Lewis and Wong (2018) introduced the important notion of incrementality, which properly quantifies this causal effect of showing an ad to the user as validated by massive real data from leading advertising platforms. However, Lewis and Wong (2018) focuses on the offline learning problem of estimating incrementality from past data. The online learning of incrementality parameters, as well as how to utilize it to optimize bidding sequences, has not been studied; this is what we embark on in this paper.

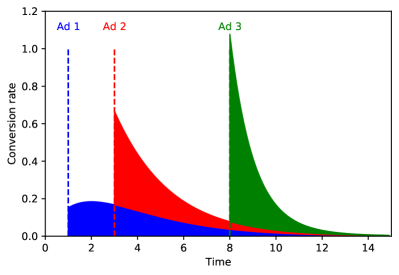

In Figure 1, we visualize the conversion incrementality caused by three ad placements and used the colored areas to capture the incrementality caused by each ad placement. There are two main challenges in learning incrementality, i.e., delayed and mixed conversion feedback. First, the conversion may not happen immediately when the ad is shown to the user, even though the conversion rate may quickly peak after showing the ad (see Ad 2 and Ad 3 in Figure 1).

Such delayed conversion feedback in online advertising is studied only recently in offline setups, e.g., (Chapelle, 2014; Saito et al., 2020; Su et al., 2021; Badanidiyuru et al., 2021a). Second, when a conversion happens, it is a mixed effect from multiple previous ad placements before the conversion. In this work, we formulate incrementality bidding as an episodic Markov Decision Process (MDP), where each episode represents an interaction with a single user drawn from a population of the same characteristics (and thus assumed to have the same incrementality parameters). The advertiser wants to learn the incrementality and optimize bidding for this user population. This is hardly possible in general given the two difficulties above as well as the potentially complex dependence of incrementality on the entire history. We thus make a Markovian assumption that the conversion incrementality of an ad placement at each round only depends on its last ad impression shown before this round. In addition, we introduce the heterogeneous Poisson process to formally capture the mixed and delayed rewards feedback in the conversion process (Poisson process is also mentioned by Lewis and Wong (2018), but only qualitatively).

To optimize the sequential bidding strategies in the online setup, there is an intrinsic exploration versus exploitation tradeoff in incrementality bidding. On one hand, the advertiser needs to bid high in order to win the ad placement opportunity and also to learn the conversion incrementality. On the other hand, she also doesn’t want to bid too high such that her conversion reward may be less than her cost, i.e., the payment due to winning the auction. This observation naturally motivates our design of a model-based RL algorithm that adopts a UCB-style approach to balance exploration and exploitation.222We remark that designing model-free no-regret RL algorithms is an intriguing open problem. Due to delayed and mixed reward feedback, it appears challenging to use algorithms like Q-learning in the incrementality bidding problem.

Our Results and Contributions.

The main contributions of this paper are two folds: (1) we introduce an episodic MDP, coupled with a heterogeneous Poisson process, to capture the incrementality bidding problem; (2) we design a novel reinforcement learning algorithm for the advertiser to optimize her sequential bidding while learning incrementality simultaneously. Technically, our main result is the design of an RL algorithm for incrementality bidding that provably has regret at most and is near-optimal in terms of the dependence on . Conceptually, our result demonstrates the possibility of designing highly-efficient RL algorithms for incrementality bidding despite its various challenges. To the best of our knowledge, this is the first work that analyzes incrementality bidding in an online setting theoretically.

Notably, our regret bound is independent of the number of possible bids (equiv. actions in standard RL). This is due to the special structures of the incrementality bidding problem, which has a small effective action space. Specifically, there are only two effective outcomes for an advertiser—winning or losing— that eventually affect the state transitions. The conversion incrementality only happens if the learner wins. Finally, we remark that our results are independent of auction formats and all our results hold for second price auctions, first price auctions, and other standard single-item auction formats. To achieve this regret bound, we provide a novel regret decomposition to incorporate with the convergence rate analysis of our novel parameter estimation method.

One key technical novelty of this paper is a new parameter estimation method, Pairwise Moment-Matching (PAMM) algorithm, that can estimate reward parameters under mixed and delayed conversion feedback. In this type of models with mixture effects, standard likelihood-based model fitting procedure would lead to solving non-convex optimization problems resulting in difficulties for computation and analysis, as well as unpleasant gap between theory and algorithm (Jain and Kar, 2017). However, PAMM estimates incrementality parameters in an online and computationally efficient manner without the need of solving nonconvex optimization problems. The estimators are provably consistent with a nearly-optimal convergence rate. We believe this novel technique will be of independent interest for other online learning problems with delayed and mixed reward feedback.

Related Work.

As mentioned in the introduction, our work is highly inspired by the visionary work of Lewis and Wong (2018), who firstly proposed incrementality bidding (and attribution). However, the method proposed in (Lewis and Wong, 2018) lacks a theoretical guarantee and cannot be adapted to online learning settings. Our work is generally related to the learning to bid literature (Weed et al., 2016; Feng et al., 2018; Balseiro et al., 2019; Han et al., 2020b, a; Badanidiyuru et al., 2021b). However, all these existing papers usually model this problem as (contextual) bandits and don’t consider the causal effect of showing an ad to the user captured by incrementality (i.e., the additional value or conversion given the ad placements in previous rounds), which causes the main difference from this paper. Specifically, in all these previous works (Weed et al., 2016; Feng et al., 2018; Balseiro et al., 2019; Han et al., 2020b, a; Badanidiyuru et al., 2021b), the reward for an ad impression is realized immediately at the current round whereas, in our model, any ad impression only increases the rate of conversions, which however may be realized in any later time following a Poisson process and, more importantly, is mixed with the incrementality of other ad impressions. We believe our model captures the effect of advertising more realistically. Some other less related works include delayed feedback in other different RL problems, which have only been studied recently (Lancewicki et al., 2022; Howson et al., 2021). We handle delayed conversion feedback through a parametric inhomogeneous Poisson process, which is different from these works.

2 The Sequential Optimization Problem of Incrementality Bidding (IB)

This paper adopts the perspective of an online advertiser, and studies the advertiser’s learning problem of optimizing her sequential bidding policy. Next, we will first describe the background and motivation of this problem and then introduce the formal model.

We consider the sequential bidding problem for a single advertiser — i.e., the decision maker or learner — in online advertising systems. The advertiser participates online advertising auctions in order to win opportunities for showing ads to Internet users and, ultimately, gain conversions (i.e., purchases of products or services) from Internet users. The interaction between the advertiser and Internet users happens in an episodic manner; each episode corresponds to one Internet user. Specifically, each episode has rounds, during which the advertiser (learner) will interact with the user of that episode for at most times. Notably, is a finite number since (1) an interaction happens only when a user visits a particular webpage and (2) if an advertiser already bids for a user for sufficiently many times and still was not able to get conversion, the advertiser typically will cease to advertise to this user (at least for some time). We use to denote the total number of episodes.333In reality, is usually at the scale of around (the number of times an advertiser would like to interact with a user), whereas the number of similar Internet users (i.e., episodes) is of the scale of millions. To focus on the fundamentals of the problem, this work studies the basic setup with i.i.d. episodes (i.e., Internet users) that occur sequentially and evenly distributed rounds at integer time point within each episode. Interesting future directions include examining the more general settings in which each Internet user in the corresponding episode may depend on a context feature, the time points of the rounds are different for different episodes, and the episodes may happen in batch (i.e., multiple similar users arrive at the same time).

Conversion incrementality.

Central to our bidding optimization problem is the notion of “conversion incrementality” (Lewis and Wong, 2018). Intuitively, incrementality captures how much increase the advertiser’s ads can boost the user’s conversion rates. Notably, the reward of showing an ad is the incrementality while not the conversion rate itself. This is very different from the previous learning to bid literature since they assume the conversion (or value) comes independently with the previous ad placements (i.e., from oblivious adversary or an underlying distribution). This is why previous studies almost all use the (contextual) bandits setup, while not MDP.

We now formally describe the model of incrementality bidding, following Lewis and Wong (2018). Within any episode , each round has an incrementality rate function for any continuous time which is the “density” of the conservation incrementality at any time . Intuitively, models how much an ad shown at round boosts the conversion rate density at any future time . Notably, the integral of this rate function does not need to be 1 as there may be many conversions per user impression. We assume that depends on an to-be-learnt unknown parameter and additionally a subset containing all previous rounds, at which our learner’s ads were shown to the corresponding user of this episode. Let denote all the to-be-learnt parameters.

It is generally intractable to learn an arbitrary rate function . Next, we introduce a natural parameterized family of functions for , with to-be-learnt parameters, in order to capture advertising applications. First, we have the following assumption for ,

Assumption 1 (Markovian Incrementality).

is only affected by the learner’s last ad impression before , rather than the entire history of the learner’s advertising performance. Formally, at current round , suppose the last round at which the learner’s ad was shown is , then the incrementality function . 444It is possible to have more features of the last ad impressions (instead of just the time gap ) in the state and our analysis will still go through as long as the number of states is still finite. For theoretical simplicity, in this paper, we focus on the case that the state is just .

The above assumption is built upon the sense that the users normally weighs more on the recently visited ads and are generally memory-less. Moreover, we assume each incrementality rate function for any has the following parametric form:

| (1) |

in which contain all the parameters at round of the given IB instance. In other words, the incrementality rate is a re-scaled exponential distribution and the re-scaling is due to fact that each user impression may lead to more (or less) than one user conversions. In our RL formulation of the problem, these are all the to-be-learnt parameters. The Markovian property is reflected in . Note that . So can be viewed as the expected number of conversions triggered by the ad impression at round , given the last time for showing the learner’s ad is rounds before. In this paper, we assume for some positive constants and . Without loss of generality, we assume . 555 In this paper, we assume to be strictly positive, however, the conversion incrementality can be negative in practice, e.g., keep seeing the same ads very often may decrease the conversion from the users. Indeed, our results still hold when allowing negative , as long as and the time-varying rate are bounded from zero. See the discussion in the proof of Theorem 1 in Appendix B.

Remark 1.

The assumption of exponential decaying rate in Equation (1) is not necessary for our approach to work, and is primarily for the exposition. Our techniques can be applied to most parametric family of rate functions such as truncated exponential, logistic, Beta, and Gamma distributions (Lewis and Wong, 2018), as long as the CDF function is invertible.

From conversion incrementality to realized conversions.

While incrementality captures how the rate of conversions increases, it did not model how conversions are realized in reality. This would be important when we introduce our reinforcement learning problem — after all, in real applications, the only observations our learner (an advertiser) can see are the realized conversions at different time, rather than the continuous conversion rate function. To capture this, we adopt the standard assumption that conversions are realized based on a continuous-time inhomogeneous Poisson process (Lewis and Wong, 2018). More specifically, let the ordered subset denote the rounds at which the learning agent wins within the episode (for convenience, let ). Then the conversions arrive according to a Poisson process with a time-varying rate , defined as follows

| (2) |

More details of inhomogeneous Poisson process is deferred to Appendix A.

The optimization problem of bidding for incrementality.

While the above incrementality modeling of user conversions originates from the influential idea of Lewis and Wong (2018), our following formulation of the optimal bidding problem under their user modeling is new to the best of our knowledge, and so is its reinforcement learning solutions presented in this paper for addressing the situations with unknown environment parameters.

Following current practice, we assume online ad opportunities are sold to advertisers by auctions, and our learner is one of these advertisers. For the ease of presentation, we restrict our descriptions to the widely adopted second price auctions; however, all our results can be easily adapted to any single-item auction format without entry fees (e.g., the first price auction). Let denote the bidding space, which may be continuous. Notably, , meaning the bidder/learner can choose to not participate this round’s auction. Moreover, denote the distribution of the highest bid among other bidders (HOB) at round as (the cumulative distribution function or CDF). For any episode (corresponding to an Internet user), at each round , the learner submits a bid and wins the opportunity to show its ad to the user if her bid is the highest. Let represents the average (conditional) payment function of the learner if she wins. Let denote the learner’s average value per conversion, which is known to the learner. We assume is bounded, w.l.o.g., within . Moreover, we can assume . Then for any bid , given the current state , the immediate expected utility of the learner at round (for any episode) is,

| (3) |

The astute reader may already find the expected utility function of the learner doesn’t depend on parameter . This raises the question why we still need to know the function class of (i.e., exponential function) and why we still need to learn parameter . As we will see later in Section 4, due to the complexity of inhomogeneous Poisson process, it is crucial to know the function class of and we have to learn parameters first in order to get a good estimator to afterwards. In second price auctions, is the expected second highest bid conditioning on winning, which can be computed as follows

| (4) |

As mentioned above, our techniques apply to other auction formats as well. For example, in first price auctions, has an even simpler format.

3 The Optimal Policy of IB and its Reinforcement Learning

While it may not appear obvious at the first glance, we explain how IB can be reduced to a finite-horizon Markov Decision Process (MDP) in this section and then introduce the corresponding reinforcement learning problem for IB when the environment parameters — namely, the incrementality parameters and HOB distribution — are unknown.

3.1 The Offline Optimal Policy of IB

We now formulate the optimal planning problem for the IB problem in its offline version, i.e., when all environment parameters are known. We start by defining what is a policy for the IB problem.

Definition 1 (Policy).

A deterministic (dynamic) policy is a sequence of mappings , in which mapping maps any to a bid. Here, is chosen such that the last winning of the learner happens at round .

Note that it suffice to consider policies that depend only on the number of consecutive loses due to the Markovian property of incrementality as mentioned above.

The MDP re-formulation of IB.

The MDP will have states, with state denoting that the last winning round is rounds ago from current round. The action set is , containing all possible bids. Both the state and action space are the same for each round , however the transition and rewards are different for different rounds. Specifically, at round , the transition probability from state and action is to enter state at round with probability , i.e., the probability of winning the auction, and to enter state with probability . The immediate reward from transitioning is for tuple (the winning case) and for tuple (the losing case). This last statement depends crucially on the independence of the incrementality across different winning rounds. The initial state of this MDP is always the lowest state, i.e., .

Consequently, the optimal policy in IB can be computed via standard dynamic programming. Specifically, when the action set has finite support (i.e., the advertiser has finite bids to choose from), the following proposition follows from the fact that MDPs with finite states, actions and horizons can be solved efficiently by dynamic programming Agarwal et al. (2019).

Proposition 1.

The offline optimal policy for any IB instance can be computed by dynamic programming in time.

We remark that even when is continuous with upper bound , an -optimal policy can be computed in time since the reward function is continuous in and an -optimal action can be found at each round during the backward induction by discretizing the entire line of bid into segments. This -optimal action choices lead to an approximately optimal policy Agarwal et al. (2019).

3.2 Reinforcement Learning of IB with Unknown Parameters

We now turn to the much more interesting and realistic situation of the online learning, particularly reinforcement learning, of the optimal IB solution. While we have shown that the offline version of IB problem can be viewed as an MDP, its online counterpart cannot be similarly tackled by standard reinforcement learning techniques due to the following novel challenges specific to the IB problem:

-

•

Challenge 1: mixed reward feedback. Any realized learner reward, arising from a user conversion, is naturally a mixture effect of all the previous winning rounds, as modeled by the accumulated incrementality rate in Equation (2). This is in contrast to standard MDP, in which the reward of this round is realized independently, conditioned on its state. It is not difficult to see that the loglikelihood of our mixed rewards model is non-convex, which renders the standard RL techniques based on maximum likelihood estimation for reward parameter estimation not applicable.

-

•

Challenge 2: delayed reward realizations. Moreover, the conversions in the IB problem follow a intricate Poisson process with heterogeneous rate and thus has delays. That is, showing an ad may not immediately lead to conversions. Such lack of immediate reward feedback renders standard Q-learning style of algorithms not easily applicable to our setup since we cannot use immediate reward feedback to update Q-functions any more.

To overcome the first challenges above, we design a novel parameter estimation methods based on moment matching to estimate ’s from mixed reward feedback, and prove its convergence rate in Section 4. To address the second challenge above, we design a model-based no-regret RL algorithm that integrate the parameter estimation above, and analyze its regret in Section 5.

Learner’s Observations.

We now formalize our learning setup. We consider the episodic online learning setting, where the learner does not know the IB parameters for each neither the distribution of the highest other bid (HOB) . Following the typical practice, we assume that the learner can always observe the realized HOB at any round in each episode, denoted as , regardless whether the learner wins or loses. This is usually termed as “full information feedback” in the literature of learning to bid.666This assumption is practical. First, in online ad systems, the manual bidder can always get this feedback (also known as “minimum bid to win”) no matter she wins or not, e.g., in Google Ad exchange platform (Developers, 2022). Second, for the auto bidding algorithms, they are designed by the platform and it does know the realized bids at each round. Moreover, the learner also knows the set of its winning rounds denoted by an ordered set as well as the set of the time stamps of all conversions (a subset of ) from each episode.

In the online learning setting, the learner aims to design a bidding algorithm to minimize the expected regret defined in the following,

| (5) |

where represents the optimal expected utility achieved by the learner at each episode if the ground-truth parameters and are given (recall that the MDP always starts from state ), represents the expectation over the randomness of algorithm , and is the policy in the episode generated by the algorithm . Here, we slightly abuse the notation to denote as the expected utility achieved by policy for estimated parameters and .

| (6) |

where represents the joint distribution of states induced by a bidding policy in the MDP formulated in Section 3.1 with estimated parameters and . Note, for second price auctions, (replacing by in Eq. (4)). In other words, captures the expected total reward in the MDP when the reward function and transition probability are parameterized by and .

Assumption 2 (Non-degeneracy Assumption on the learner).

We assume that the learner’s bidding space is upper bounded away from extreme bids. More formally, there exists a small constant such that for any (i.e., no feasible bids guarantee sure winning). We call such learner -bounded.

There are two reasons for making this assumption. The first is a technical reason: it makes sure that the learner always has at least probability to lose, which turns out to be crucial to estimate the incrementality parameters, as we do in the next section. This is because incrementality captures the difference between winning and losing. If the probability of losing is extremely small, there is generally no way to accurately estimate their differences (though it turns out that we can afford small winning probabilities). The second reason for assuming -bounded learners is realistic motivations since in auto bidding practice, bidders typically explicitly specify upper bounds of their bids, under which the bidder’s winning probability is almost always capped strictly below .

4 Incrementality Parameter Estimation via Pairwise Moment-Matching

Though maximum likelihood estimation (MLE) is a natural and straightforward parameter estimation strategy, it comes with many drawbacks we want to avoid. First, the MLE criterion under our model of mixed rewards is not a convex problem and optimizing the likelihood would suffer from multiple local optimal or saddle point issues. The theoretical claims may not match the true algorithm performance. Secondly, the computational efficiency of the MLE problem is worse than what we will introduce next, which makes it less attractive in large-scale problems. Our algorithm is carefully tailored for estimating parameters of our model, given the observed trajectories of first rounds. Specifically, the trajectory of each episode can be described by two sequences: (1) the time stamps of realized conversions within time ; and (2) the ordered subset which contains all the winning steps within this episode (for convenience, we extend the above notations and by letting ), where denotes the number of winning events (showing the ad) in the episode . Equivalently, we can also represent by a -length binary sequence such that if and only if episode wins at time . Notably, both and may be empty if there is no conversion nor winning. Our estimation is based on an online algorithm: from a high-level perspective, it progresses by time intervals sequentially to produce estimates of parameters , by pairwisely coupling episodes and matching statistical moments. Therefore, we call it the pairwise moment-matching (PAMM) algorithm, described in Algorithm 1.

| (7) |

| (8) |

| (9) |

| (10) |

| (12) |

The PAMM algorithm is specifically designed for estimating parameters from mixed reward signals, each drawn from a Poisson process. Its primary advantage lies in its online nature, guaranteed convergence and efficient computation. This is achieved by the following observations. First, all information about reward scale parameter and reward variance parameter is intrinsically reflected only in the “differential behaviors” for those episodes which had conversions vs. those episodes which did not have conversions at time step , conditioning their matched history before time as defined in the sample matching step. This is due to the Markovian property for the Poisson process, and our moment matching is hinged into this property. Second, for the Poisson distribution (as a member of the exponential family), the method of matching the canonical parameter (mean) gives an equivalent estimator as the MLE in a single Poisson case (but not necessary in our more complicated model). These two ideas motivate our procedure, by matching the episodes, we precisely locate the needed Poisson signals and solve the estimators by the mean value structure. Because of this, the PAMM can recover the parameters with essentially optimal rate (in the online sense), even though we do not use the full likelihood that would result in non-convexity and an unpleasant gap between the theory and the practical algorithm.

In practice, terms in (10) and (12) may result in , but such an event only happens with probability tending to zero (which is why Theorem 1 has high probability guarantees). Standard numerical protection can be introduced in practice which will not change our theoretical claims. Moreover, from the implementation perspective, one start from the first interval and move forward by running PAMM for each . In each new interval, the matching step can be directly carried over by further refining the matching of the previous interval. As a result, the whole estimation procedure only involves one sweep of the data without the commuting back and forth between different time intervals. We have introduced the PAMM algorithm in the current form as a self-contained algorithm for estimating the inhomogeneous Poisson process, which can be of independent interest. However, the steps of PAMM can be easily embedded in our online learning algorithm presented in Section 5 without losing its validity.

Theorem 1 (Estimation Errors with Finite Samples).

Suppose there exist positive constants and , such that and for any and , and the learner is -bounded (see Assumption 2). Also assume that the expected number of total conversions for each episode within each interval is always bounded above by a constant . Let be the total number of winning episodes at time and be the total number of winning episodes at time with state . Let and be the estimators obtained from Algorithm 1. Then, for any and any , we have the following guarantees for PAMM:

-

1.

For any , with probability at least , .

-

2.

For any , with probability at least ,

In the above results, and , where is the Bernstein constant (see Lemma 1).

5 The Full RL Algorithm and its Regret Analysis

We propose a reinforcement learning algorithm by incorporating our parameter estimation method PAMM and the optimal offline planning for the MDP mentioned in Section 3 to learn parameters as well as the conversion incrementality and decide the bid at each round.

Our algorithm adopts a UCB-style procedure to handle the exploration-exploitation tradeoff in incrementality bidding, which is summarized in Algorithm 2. The algorithm adopts pure explorations in several beginning episodes so that we can get enough ad impressions for each state in every round. These pure explorations are achieved by setting bids appropriately such that we can enforce to explore one pair in each exploration (Line 4 in Algorithm 2)777When , setting means a “fake” winning at round and it is consistent with our assumption that initial state .. In particular, we need explorations to make sure so that we can provide a regret bound with high probability, where is a positive constant explicitly defined in Theorem 1. Recall is the total number of winnings at round given the state is .

After pure explorations, at each episode , we use the PAMM algorithm to get an estimator (resp. ) given the observed ad impression time and the conversion time up to episode . In addition, we can estimate easily using empirical distribution function and this implies we can get a uniform convergence for the transition probabilities for any action given any state . Then we apply UCB-style RL algorithm with estimated parameters to decide the policy in next episode. Specifically, given the estimated , we construct a confidence region centered at and we do offline planning for the optimism in the confidence region to get the policy in next episode.

| (13) |

Remark 2 (Computational Efficiency of Alg. 2).

Regret Analysis.

Combining the convergence rate analysis from Theorem 1 and a novel regret decomposition technique (necessary for our particular setup), we are able to prove the regret guarantee of our online bidding algorithm. Our regret bound is summarized in Theorem 2, the proof of which is deferred to Appendix C.

6 Discussions and Future Work

Our RL algorithm lies in the model-based RL algorithm literature. The best known regret bound for model-based RL is (Azar et al., 2017), where is the number of states and is the number of actions. Since in our case, our regret bound is slightly worse from the best possible by an factor of , but is independent of the number of actions. This may be due to the complexity of our model. Whether we can close this gap is an interesting open question. As we mentioned earlier, our algorithm can be extended to handle continuous bidding space and our regret analysis still works. In this paper, we assume the conversion rate function doesn’t depend on the shown ads of other bidders but only on the learner’s last ad impression. Relaxing these assumptions may result in very interesting future work.

Acknowledgment.

Haifeng Xu is supported by a Google Faculty Research Award. Tianxi Li is supported by the NSF grant DMS-2015298.

References

- Agarwal et al. [2019] A. Agarwal, N. Jiang, S. M. Kakade, and W. Sun. Reinforcement learning: Theory and algorithms. Working Draft, 2019.

- Azar et al. [2017] M. G. Azar, I. Osband, and R. Munos. Minimax regret bounds for reinforcement learning. In Proceedings of the 34th International Conference on Machine Learning, volume 70 of Proceedings of Machine Learning Research, pages 263–272. PMLR, 06–11 Aug 2017.

- Badanidiyuru et al. [2021a] A. Badanidiyuru, A. Evdokimov, V. Krishnan, P. Li, W. Vonnegut, and J. Wang. Handling many conversions per click in modeling delayed feedback. AdKDD, 2021a.

- Badanidiyuru et al. [2021b] A. Badanidiyuru, Z. Feng, and G. Guruganesh. Learning to bid in contextual first price auctions. CoRR, abs/2109.03173, 2021b.

- Balseiro et al. [2019] S. Balseiro, N. Golrezaei, M. Mahdian, V. Mirrokni, and J. Schneider. Contextual bandits with cross-learning. In Advances in Neural Information Processing Systems 32, pages 9679–9688. 2019.

- Chapelle [2014] O. Chapelle. Modeling delayed feedback in display advertising. In Proceedings of the 20th ACM SIGKDD International Conference on Knowledge Discovery and Data Mining, page 1097–1105, 2014.

- Developers [2022] G. Developers. Real-time bidding. https://developers.google.com/authorized-buyers/rtb/request-guide, 2022.

- Edelman et al. [2007] B. Edelman, M. Ostrovsky, and M. Schwarz. Internet advertising and the generalized second-price auction: Selling billions of dollars worth of keywords. American Economic Review, 97(1):242–259, March 2007.

- Facebook [2022] Facebook. About bid strategies. https://www.facebook.com/business/help/403 1619591734742116?id=2196356200683573, 2022.

- Feng et al. [2018] Z. Feng, C. Podimata, and V. Syrgkanis. Learning to bid without knowing your value. In Proceedings of the 2018 ACM Conference on Economics and Computation, page 505–522, 2018.

- Google [2022] Google. Autobidding support page. https://support.google.com/google-ads/405 answer/2979071, 2022.

- Han et al. [2020a] Y. Han, Z. Zhou, A. Flores, E. Ordentlich, and T. Weissman. Learning to bid optimally and efficiently in adversarial first-price auctions. CoRR, abs/2007.04568, 2020a.

- Han et al. [2020b] Y. Han, Z. Zhou, and T. Weissman. Optimal no-regret learning in repeated first-price auctions. CoRR, abs/2003.09795, 2020b.

- Howson et al. [2021] B. Howson, C. Pike-Burke, and S. Filippi. Delayed feedback in episodic reinforcement learning. arXiv preprint arXiv:2111.07615, 2021.

- Jain and Kar [2017] P. Jain and P. Kar. Non-convex optimization for machine learning. arXiv preprint arXiv:1712.07897, 2017.

- Kearns and Singh [2002] M. Kearns and S. Singh. Near-optimal reinforcement learning in polynomial time. Machine Learning, 49:209–232, 2002.

- Lancewicki et al. [2022] T. Lancewicki, A. Rosenberg, and Y. Mansour. Learning adversarial markov decision processes with delayed feedback. In Proceedings of the AAAI Conference on Artificial Intelligence, 2022.

- Lewis and Wong [2018] R. A. Lewis and J. Wong. Incrementality bidding & attribution. Available on SSRN, 2018.

- Nedelec et al. [2022] T. Nedelec, C. Calauzènes, N. E. Karoui, and V. Perchet. Learning in repeated auctions. Foundations and Trends® in Machine Learning, 15(3):176–334, 2022. ISSN 1935-8237. doi: 10.1561/2200000077.

- Noti and Syrgkanis [2021] G. Noti and V. Syrgkanis. Bid prediction in repeated auctions with learning. In Proceedings of the Web Conference 2021, WWW ’21, page 3953–3964, New York, NY, USA, 2021. Association for Computing Machinery. ISBN 9781450383127.

- Saito et al. [2020] Y. Saito, G. Morisihta, and S. Yasui. Dual Learning Algorithm for Delayed Conversions, page 1849–1852. 2020.

- Su et al. [2021] Y. Su, L. Zhang, Q. Dai, B. Zhang, J. Yan, D. Wang, Y. Bao, S. Xu, Y. He, and W. Yan. An attention-based model for conversion rate prediction with delayed feedback via post-click calibration. In Proceedings of the Twenty-Ninth International Joint Conference on Artificial Intelligence, IJCAI’20, 2021.

- Varian [2006] H. R. Varian. Position auction. International Journal of Industrial Organization, 2006.

- Vershynin [2018] R. Vershynin. High-dimensional probability: An introduction with applications in data science, volume 47. Cambridge university press, 2018.

- Weed et al. [2016] J. Weed, V. Perchet, and P. Rigollet. Online learning in repeated auctions. In 29th Annual Conference on Learning Theory, pages 1562–1583, 2016.

Incrementality Bidding via Reinforcement Learning under Mixed and Delayed Rewards

Appendix

Appendix A Formal Definition of Inhomogeneous Poisson Process

The inhomogeneous Poisson (point) process is a Poisson point process with a Poisson parameter set as some time-dependent function . In particular, the expected number of points observed in a time interval is . Let represent the number of points of inhomogeneous Poisson process with intensity function occurring in the interval , then the probability of points existing in the interval is given by,

In this paper, the points mean the conversions and the time-dependent intensity function is defined in Eq. (2) and it depends on the realization of the conversions and parameter .

Appendix B Poisson Process Estimation

Lemma 1 (Bernstein’s Inequality [Vershynin, 2018]).

Suppose are independent, mean-zero, sub-exponential random variables, and is an dimensional constanst vector. Then, for every , we have

where is the sub-exponential norm (Orlicz norm) of and is an absolute constant (Bernstein constant). is the Euclidean norm and .

Proof of Theorem 1.

Denote . We first introduce the main idea of the the PAMM algorithm. Since conversions follow the Poisson process, we have and independently.

Note that for all and , their history winning records before are exactly the same. Suppose . It is not difficult to see that

| (14) |

where and are two arbitrary episodes in and (nonempty). Similarly, we have

| (15) |

Therefore, and precisely locate the parameter of interest, . By aggregating the information over different , we can thus estimate and based on the method of moments. Notice that is shared for all episodes with the same while is shared only within a subset of , for a given . Therefore, we will tailor the moment match operations according to different aggregation levels, as indicated in (10) and (12). Next, we proceed to study the theoretical property of the algorithm. Define

and

Taking the logarithm of the ratio between the two quantities, we get

Our estimator is motivated by the above identity with the observation that

We start with deriving the concentration of . Note that the terms in (7) are Poisson random variables, with their expectation upper bounded by

Therefore, each of these items is a sub-exponential random variable with . To use Lemma 1, we can see that the vector corresponding to (9) reads as

where is the harmonic mean of and . Also, we have

Define . With the -bounded assumption and the exploration stage requirement for sample, it is easy to see that we have (happening with probability tending to 1 regarding the randomness of bidding). Therefore, for sufficiently large , by Lemma 1, we have,

for constant . Assuming , and setting , we will be able to use the sub-gaussian bound of the concentration, which gives

For notational convenience, we will denote this relation by

| (16) |

where refers to any generic term in the order of with probability at least .

Furthermore, by Taylor expansion, we have

Since and , we have

| (17) |

in which the right hand side is a constant. Therefore, we have

Similarly, because

| (18) |

we can also show the same property for with

Combining the results for and , we know that

Note that our proof allows negative values be . This is because the only places where we use the lower bound so far are (17) and (18). In general, as long as we can have a lower bound for and , the proof still works.

For the estimation of , a similar approach can be taken, but the stratum of focus will be on the slide . First, notice that (B) and (15) remain valid for . Indeed, all of the ’s share the same expectation. Define

Now the moment matching equation becomes

In this case, we still have

and

Therefore, we just need to check the concentration bounds of and . Define where is the harmonic mean of and . With the assumption that , by the same derivation as for , we can get

as long as . Similarly,

Now, define . By multivariate Taylor expansion, we have

where is the gradient with

Substituting and into the gradient leads to

Therefore, we have

Notice that we have and .

∎

Appendix C Proof of Theorem 2

To prove Theorem 2, we need several auxiliary lemmas. First, we provide a lemma to bound . The importance of this lemma is that we provide a reformulation of function by utilizing the fact that the conversion incrementality can only happen if the learner wins the opportunity to show the ad to the user. This observation makes our regret bound independent of the number of actions.

Lemma 2.

Given estimated parameters and , for any bidding policy , we have

where is the probability of sequence induced by the MDP parameterized by and by adopting policy and models whether the learner wins () or not () at round with bid (given HOB follows distribution at each round ).

Proof.

Recall, by definition of in Eq. (6), for any and ,

| (19) |

Let denote the realized outcome of the learner at round , s.t.,

| (20) |

Given the above reformulation of , we can derive the difference between and for any bidding policy and any distribution of HOB at each round ,

| (21) |

∎

Second, we extend the well-known simulation lemma in standard RL Kearns and Singh [2002] to our case. Please note both transition probability and expected utility function of the learner (Eq. (3)) depend on .

Lemma 3.

For any fixed bidding strategy , we have

| (22) |

holds with probability at least . In addition, we have with probability at least ,

Proof.

Denote as the MDP induced by a bidding policy and parameters . Similarly, let represent the MDP for a bidding policy with parameters and . Let and be the transition at round for MDP and , respectively.

Given the MDP re-formulation in Subsection 3.1, we have for any and ,

In addition, we denote as the expected reward function for the MDP at round , similarly, we can also define for the MDP . For any , we can bound as below:

where the first equality is based on the definition of and , the second inequality is based on triangle inequality and the last inequality holds because of the fact that and .

By DKW inequality (Lemma 4) and union bound, with probability at least , we have for all

Given the above bound of transition and reward between two MDPs and and the Simulation Lemma (Lemma 6), with probability at least , we have

| (23) | |||||

| (24) |

For notation simplicity, we denote as the optimal bidding policy corresponding to parameters and , then we have

where the first inequality holds because of the definition of and the second inequality is based on Eq. (22) for the fixed bidding policy . Using the same argument as in Eq. (23), we complete the proof.

∎

Given the above two auxiliary lemmas, we are ready to prove Theorem 2.

Proof of Theorem 2.

For notation simplicity, let

In addition, we denote as the number of episodes for pure explorations. Note, in each pure exploration , we exactly increase by 1 for one pair. To make sure , we only need .

We first propose a new decomposition of the expected regret in the following way,

| (25) |

The first inequality above is based on the fact the reward (expected utility of the learner) at each round is bounded by . Then we bound the above terms separately in the following.

Term (i). By Lemma 3, for any fixed , we have holds with probability at least . Then by union bound over , we have

holds with probability at least .

Term (ii). After pure explorations, for any , we have . Then by Theorem 1, we have with probability at least , the true parameter . Then by the definition of , for any , we have holds with probability . Taking union bound over , then with probability at least , we have

Term (iii). For notation simplicity, let be the parameter corresponding to . Actually, it is the Then we can bound Term (iii) as below,

| (26) |

where the inequality is based on Lemma 2 in Appendix. Here we slightly abuse the notation, let . An important observation is that can be viewed as the action the learner takes at round in the episode and it only contains two different options, i.e., (lose) or (win). This rewriting can help us reduce the dependency of regret bound with number of bids, and we can easily extend to handle continuous bid space. Let represent the total number observations of pair up to round and episode. Then we have,

| (27) |

where the first inequality is based on the fact that and in episode given the definition in Algorithm 2. The third inequality is based on Lemma 5.

Term (iv). Again, applying Lemma 3 and union bound over , we can bound term (iv) in the following way,

Putting it all together, we can bound the regret as below,

holds with probability at least . ∎

Appendix D Auxiliary Technical Lemmas

In this section, we enumerate several useful technical lemmas used in this paper. First, we introduce the well-known Dvoretzky–Kiefer–Wolfowitz (DKW) inequality which is used to bound the gap between and .

Lemma 4 (DKW Inequality).

For any episode , at each round , holds with probability at least .

Second, we describe the celebrated simulation lemma, which was introduced and named in Kearns and Singh [2002]. For completeness of the presentation, we provide the proof for this lemma.

Lemma 5 (Lemma 7.5 in Agarwal et al. [2019]).

Consider arbitrary sequence of trajectories, for , we have

Finally, we describe the well-known simulation lemma. For completeness of exposition, we provide a simple proof for this lemma.

Lemma 6 (Simulation Lemma Kearns and Singh [2002]).

Consider two different MDPs and with the same state and action spaces, and . If the transition ( and resp.) and reward functions ( and resp., bounded by ) of these two MDPs satisfy

Then for every non-stationary policy and fixed initial state , the two MDPs satisfy

| (28) |

Proof.

First, we denote as the total reward from round to when the state at round is . Similarly we can define .

Then Eq. (28) is equivalent to show and we will prove it using the inductive hypothesis that for any state , policy and round ,

For , the hypothesis is clearly true since reward of two MDPs at round only differs at most and this establishes the base case.

For the inductive step, we utilize the recursive formula of and in the following way,

where the first inequality holds since ; the second inequality is based on the triangle inequality; the third inequality is because of the fact that (recall the reward at each round is bounded by ); the fourth inequality holds due to the inductive hypothesis. Then we complete the proof.

∎