Provably Auditing Ordinary Least Squares

in Low Dimensions

Abstract

Measuring the stability of conclusions derived from Ordinary Least Squares linear regression is critically important, but most metrics either only measure local stability (i.e. against infinitesimal changes in the data), or are only interpretable under statistical assumptions. Recent work proposes a simple, global, finite-sample stability metric: the minimum number of samples that need to be removed so that rerunning the analysis overturns the conclusion [BGM20], specifically meaning that the sign of a particular coefficient of the estimated regressor changes. However, besides the trivial exponential-time algorithm, the only approach for computing this metric is a greedy heuristic that lacks provable guarantees under reasonable, verifiable assumptions; the heuristic provides a loose upper bound on the stability and also cannot certify lower bounds on it.

We show that in the low-dimensional regime where the number of covariates is a constant but the number of samples is large, there are efficient algorithms for provably estimating (a fractional version of) this metric. Applying our algorithms to the Boston Housing dataset, we exhibit regression analyses where we can estimate the stability up to a factor of better than the greedy heuristic, and analyses where we can certify stability to dropping even a majority of the samples.

1 Introduction

In applied statistics and machine learning, a common task is to estimate the effect of some real-valued treatment variable (e.g. years of education) on a real-valued response variable (e.g. income) in the presence of a small number of real-valued controls. In particular, it might be especially important to understand whether the effect is positive or not; this may inform e.g. governmental policy decisions. The most basic model for this task is linear regression, and the most common estimator for this model is Ordinary Least Squares. In their seminal 1980 book Regression Diagnostics [BKW80], Belsley, Kuh, and Welsch observe:

Over the last several decades the linear regression model and its more sophisticated offshoots…have surely become among the most widely employed quantitative tools of the applied social sciences and many of the physical sciences. The popularity of ordinary least squares is attributable to its low computational costs, its intuitive plausibility in a wide variety of circumstances, and its support by a broad and sophisticated body of statistical inference.

While the intervening decades have seen the development of increasingly sophisticated statistical estimators, and increasingly complex machine learning models, this observation still holds.

For samples where each sample consists of a treatment , a response , and controls , the linear regression model posits that there is a linear relationship where is the ground truth regressor. Then, is the posited effect of the treatment. Of course, is unknown. The Ordinary Least Squares (OLS) estimator for is

| (1) |

and then is the estimated effect of the treatment.

Under strong statistical assumptions (e.g. that the model is well-specified with exogenous error term), the OLS estimator has compelling statistical guarantees (e.g. consistency, meaning that in probability), and it is possible to compute statistical confidence that the estimated effect is real rather than produced by chance (e.g. by -statistics). But real-world data is (almost de facto) misspecified, with nonlinearities, endogeneity, heavy-tailed errors, or even gross outliers. When these irregularities cannot be easily modeled, practitioners may simply apply the OLS estimator anyways. Hence,

The practitioner is frequently left with the uneasy feeling that his regression results are less meaningful and less trustworthy than might otherwise be the case because of possible problems with the data – problems that are typically ignored in practice. The researcher…may notice that regressions based on different subsets of the data produce very different results, raising questions of model stability. A related problem occurs when the practitioner knows that certain observations pertain to unusual circumstances, such as strikes or war years, but he is unsure of the extent to which the results depend, for good or ill, on these few data points. ([BKW80])

Ultimately, the goal of a scientific study is to extract conclusions from data that will generalize to broader populations. Perhaps the best way of validating studies is to collect new data and replicate the results, but this is labor-intensive and often inconclusive [Bak16]. The simpler alternative, pursued in this work, is to audit conclusions based on the data which has already been collected.111We are auditing for robustness, which should not be confused with the (philosophically related) notion of auditing for fairness [KNRW18].

1.1 Finite-sample stability

In recent work, Broderick, Giordano, and Meager propose assessing the sensitivity of a given statistical analysis by computing the minimum number of samples that need to be removed from the dataset to overturn the conclusion [BGM20]; we call this the finite-sample stability of the conclusion. Intuitively, if the stability is very small, this means the conclusion is driven by samples from a small subpopulation, and may not generalize well. Conversely, if the stability is large, then we may have more confidence that the conclusion is broadly true. Finite-sample stability is distinct from common statistical notions of confidence [BGM20], and in fact the authors discovered several important economics studies where statistically significant conclusions can be overturned by dropping less than of the data. Their finding underscores the importance of auditing conclusions for stability. While the oft-cited scientific “replication crisis” [Ioa05] will not be easily solved, at the least it may be partially alleviated by thorough audits.

Unfortunately, the obvious algorithm for determining whether a conclusion derived from samples can be overturned by removing e.g. of the data would require rerunning the analysis times, which is computationally intractable even for fairly small . Instead, [BGM20] proposes a heuristic (applicable to any differentiable -estimator) for guessing which size- subset of the data will most heavily influence the conclusion: essentially, they choose the samples with the largest individual influences. Whenever removing this subset overturns the conclusion, then the heuristic has proven that the conclusion was not stable.

What the heuristic cannot do is provably certify that a particular conclusion is stable to dropping a few samples. Even for the OLS estimator, there are simple examples where the estimate can be changed dramatically by dropping a few samples, but the greedy approach fails to identify these samples (see Section 2 for discussion). This motivates the following question: Are there efficient algorithms with provable guarantees for estimating the finite-sample stability of an OLS estimate (concretely, the number of samples that need to be dropped to change the sign of the first coordinate of the estimated regressor)?

This question is even interesting in the low-dimensional regime. In applications to e.g. econometrics, the number of covariates may be very small [ML92]; nevertheless, as evidenced by [BGM20], the conclusions of these studies may be very sensitive. Even high-dimensional machine learning algorithms frequently build upon low-dimensional OLS paired with feature selection methods [Hal00, TG07, HWD18]; thus, estimating stability of OLS is a prerequisite for estimating stability of these algorithms. Our work provides provable and efficient algorithms to not only better diagnose sensitive conclusions obtained by low-dimensional OLS regressions, but also validate robust conclusions.

1.2 Formal problem statement

We are given a deterministic and arbitrary set of samples , where each is a vector of real-valued covariates, and each is a real-valued response. We are interested in a single coefficient of the OLS regressor (without loss of generality, the first coordinate): in an application, the first covariate may be the treatment and the rest may be controls. The sign of this coefficient is important because it estimates whether the treatment has a positive or negative effect. Thus, we want to determine if it can be changed by dropping a few samples from the regression. Formally, we consider the fractional relaxation, where we allow dropping fractions of samples:222This relaxation does not change the interpretation of the metric. Obviously, the fractional stability lower bounds the integral stability. Moreover, there is always an optimal weight vector with at most non-integral weights.

Definition 1.1.

Fix with and . For any , the weight- OLS solution set of is

The finite-sample stability of is

This is the minimum number of samples (in a fractional sense) which need to be removed to zero out the first coordinate of the OLS regressor. If the OLS solution set contains multiple regressors, then it suffices if any regressor in the solution set has . Our algorithmic goal is to compute , or at least to approximate up to an additive error.

1.3 Results

By brute-force search, the (integral) stability can be computed in time . However, because the complexity is exponential in the number of samples, it is computationally infeasible even when the dimension of the data is low, which is a common situation in many scientific applications. Similarly, the fractional stability (Definition 1.1) is the solution to a non-convex optimization problem in more than variables, which seems no simpler. Can we still hope for a polynomial-time algorithm in constant dimensions? We show that the answer is yes.

Theorem 1.2.

There is an -time algorithm which, given arbitrary samples with and , and given , decides whether .

We also show that the exponential dependence on dimension is necessary under standard complexity assumptions:

Theorem 1.3.

Under the Exponential Time Hypothesis, there is no -time algorithm which, given and , decides whether .

This lower bound in particular rules out fixed-parameter tractability, i.e. algorithms with time complexity . However, it only applies to exact algorithms. In practice, it is unlikely to matter whether or ; in both cases, the conclusion is sensitive to dropping a very small fraction of the data. This motivates our next two algorithmic results on -additive approximation of the stability (where we think of as a constant). First, we make a mild anti-concentration assumption, under which the stability can -approximated in time roughly . While still not fixed-parameter tractable, this algorithm can now be run on moderate sized problems in low dimensions, unlike the algorithm in Theorem 1.2.

Assumption A.

Let . We say that samples satisfy -anti-concentration if for every , it holds that

where is the matrix with rows , and is any unweighted OLS regressor of against .

Under this assumption, we present an -approximation algorithm:

Theorem 1.4.

For any , there is an algorithm PartitionAndApprox with time complexity

which, given , , , and samples satisfying -anti-concentration, returns an estimate such that with probability at least ,

In fact, PartitionAndApprox can detect failure of the anti-concentration assumption (see Theorem C.6 for the precise statement). Moreover, the required anti-concentration is very mild. If are constants, the algorithm has time complexity , so long as the samples satisfy -anti-concentration. This is true for arbitrary smoothed data (Appendix E.1). Finally, unlike the exact algorithm, PartitionAndApprox avoids heavy algorithmic machinery; it only requires solving linear programs.

Fixed-parameter tractability?

Our final result is that -approximation of the stability is in fact fixed-parameter tractable, under a stronger anti-concentration assumption.

Assumption B.

Let . We say that samples satisfy -strong anti-concentration if for every , it holds that

where is the matrix with columns .

Although this assumption is stronger than the previous, it still holds with constant under certain distributional assumptions on , e.g. centered Gaussian mixtures with uniformly bounded condition number (Appendix E.2).

Theorem 1.5.

For any , there is a -time algorithm NetApprox which, given ,, and samples satisfying -strong anti-concentration, returns an estimate satisfying

Moreover, holds for arbitrary .

Extensions.

Another model, frequently used in causal inference and econometrics, is instrumental variables (IV) linear regression. When the noise in a hypothesized causal relationship is believed to be endogenous (i.e. correlated with ), a common approach [Sar58, AIR96, Car01] is to find a -dimensional variable (the instrument) for which domain knowledge suggests that . Positing that is identified by the moment condition , the IV estimator set given samples is then

where denotes elementwise product, and and are the matrices of instruments and covariates respectively. Stability can be defined as in Definition 1.1. Although for simplicity we state all of our results for OLS (i.e. the special case ), it can be seen that Theorem 1.2 and Theorem 1.5 both extend directly to the IV regression setting. See Appendix F for further discussion.

Experiments.

We implement modifications of NetApprox and PartitionAndApprox which give unconditional, exact upper and lower bounds on stability, respectively. We use these algorithms to obtain tight data-dependent bounds on stability of isotropic Gaussian datasets for a broad range of signal-to-noise ratios, and we demonstrate heterogeneous synthetic datasets where our algorithms’ upper bounds are an order of magnitude better than upper bounds obtained by the prior heuristic. On the Boston Housing dataset [HJR78], we regress house values against all pairs of features. For the majority of these regressions, we bound the stability within a factor of two. On the one hand, we detect many sensitive conclusions (including some which the greedy heuristic claims are stable); on the other hand, we certify that some conclusions are stable to dropping as much as half the dataset.

Broader Context.

Taking a step back, OLS is important not only in its own right but also as a key building block in more complex machine learning systems, ranging from regression trees [Loh11] to generative adversarial networks [MLX+17] and policy iteration in linear MDPs [LP03]. Our work on estimating stability of OLS is also a first step towards estimating stability for these systems.

1.4 Organization

2 Related work

Local and global sensitivity metrics.

Post-hoc evaluation of the sensitivity of a statistical inference to various types of model misspecification has long been recognized as an important research direction. Within this area, there is a distinction between local sensitivity metrics, which measure the sensitivity of the inference to infinitesimal misspecifications of the assumed model (e.g. [Pol84, CHCFC04, BKW80]), and global sensitivity metrics, which measure the set of possible inferences as the model ranges in some fixed set around (e.g. [Lea84, THW89, ČAH13]). For OLS in particular, there is a well-established literature on the influences of individual data points [Coo77, CH86], which falls under local sensitivity analysis, since deleting a single data point is an infinitesimal perturbation to a dataset of size as . In contrast, identifying jointly influential subsets of the data (the “global” analogue) has been a long-standing challenge due to computational issues (see e.g. page 274 of [BKW80]). Existing approaches typically focus on identifying outliers in a generic sense rather than with respect to a specific inference [HS93], or study computationally tractable variations of deletion (e.g. constant-factor reweighting [Lea84]).

Finite-sample stability.

Finite-sample stability is a global sensitivity metric; it essentially seeks to identify jointly influential subsets. Most directly related to our work is the prior work on heuristics for the finite-sample stability [BGM20, KZC21]. The heuristic given by [BGM20] (to approximate the most-influential samples) is simply the local approximation: compute the local influence of each sample at , sort the samples from largest to smallest influence, and output the top samples. Subsequent work [KZC21] proposed refining this heuristic by recomputing the influences after removing each sample, which alleviates issues such as masking [CH86]. But this is still just a greedy heuristic, and it may fail when samples are jointly influential but not individually influential. Except under the strong assumption that the sample covariance remains nearly constant when we remove any samples (see Theorem 1 in [BGM20], which relies on Condition 1 in [GSL+19]), the local influence approach can upper bound the finite-sample stability but cannot provably lower bound it. In fact, in Section 5 we provide examples where the greedy heuristic of [KZC21] is very inaccurate due to instability in the sample covariance.

The -value.

Closely related to finite-sample stability, the -value [GR21] is the minimum Kullback-Leibler divergence over all distributions for which the conclusion is null, where is the empirical distribution of the samples. Unfortunately, while the -value is an interesting and well-motivated metric, computing the -value for OLS estimation appears to be computationally intractable, and the algorithms given by [GR21] lack provable guarantees.

Robustified estimators.

Ever since the work of Tukey and Huber, one of the central areas of statistics has been robustifying statistical estimators to be resilient to outliers (see, e.g. [Hub04]). While a valuable branch of research, we view robust statistics as incomparable if not orthogonal to post-hoc sensitivity evaluation, for three reasons. First, samples that drive the conclusion (in the sense that deleting them would nullify the conclusion) are not synonymous with outliers: removing an outlier that works against the conclusion only makes the conclusion stronger. Indeed, outlier-trimmed datasets are not necessarily finite-sample robust [BGM20]. Rather, finite-sample stability (along with the -value [GR21]), in the regime where a constant fraction of samples is removed, may be thought of as a measure of resilience to heterogeneity and distribution shift.

Second, it is unreasonable to argue that using robustified estimators obviates the need for sensitivity evaluation. Robust statistics has seen a recent algorithmic revival, with the development of computationally efficient estimators, for problems such as linear regression, that are robust in the strong contamination model (e.g. [KKM18, DKK+19, BP21]). However, even positing that the strong contamination model is correct, estimation guarantees for these algorithms require strong, unverifiable (and unavoidable [KKM18]) assumptions about the uncorrupted data, such as hypercontractivity. Sensitivity analyses should support modeling assumptions, not depend upon them.

Third and perhaps most salient, classical estimators such as OLS are ubiquitous in practice, despite the existence of robust estimators. This alone justifies sensitivity analysis of the resulting scientific conclusions.

Distributionally robust optimization.

Our motivations mirror a recent line of work in machine learning [SNVD17, DN18, CGAD20, JN20] which suggests that the lack of resilience of Empirical Risk Minimization to distribution shift can be mitigated by minimizing the supremum of risks with respect to distributions near the empirical training distribution (under e.g. Wasserstein distance or an -divergence). Again, this approach of robustifying the estimator is valuable but incomparable to sensitivity analysis.

3 Preliminaries

For vectors , we let denote the elementwise product . Throughout the paper, we will frequently use the closed-form expression for the (weighted) OLS solution set

where is the matrix with rows . In particular, setting , this means that the finite-sample stability can be rewritten as

| (2) |

where (here and throughout the paper) is the matrix with columns .

4 Overview of Algorithms

An exact algorithm.

Our main tool for Theorem 1.2 is the following special case of an important result due to [Ren92] on solving quantified polynomial systems of inequalities:

Theorem 4.1 ([Ren92]).

Given an expression

where is a system of polynomial inequalities with maximum degree , the truth value of the expression can be decided in time .333This is in the real number model; a similar statement can be made in the bit complexity model.

Roughly, for a constant number of quantifier alternations, a quantified polynomial system can be decided in time exponential in the number of variables. Unfortunately, a naive formulation of the expression , by direct evaluation of Equation 2, has variables:

Intuitively, it may not be necessary to search over all ; for fixed , the maximum-weight is described by a simple linear program. Formally, the linear program can be rewritten (Lemma A.1) by the separating hyperplane theorem, so that the overall expression becomes:

| (3) |

Now, for fixed and , the maximum-weight has very simple description: it only depends on the relative ordering of the summands . By classical results on connected components of varieties, since the summands have only variables, the number of achievable orderings is only rather than , and the orderings can be enumerated efficiently [Mil64, Ren92]. This allows the quantifier over to be replaced by a quantifier over the achievable orderings, after which Theorem 4.1 implies that the overall expression can be decided in time . See Appendix A for details.

Approximation via partitioning.

Next, we show how to avoid the heavy algorithmic machinery used in the previous result. For Theorem 1.4, the strategy is to partition the OLS solution space into roughly regions, such that if we restrict to any one region, the bilinear program which defines the stability can be approximated by a linear program.

Concretely, we start by writing the formulation (2) as

| (4) |

This has a nonlinear (and nonconvex) constraint due to the pointwise product between and the residual vector . Thus, we can introduce the change of variables for . This causes two issues. First, the constraint becomes , which is no longer linear. To fix this, suppose that instead of maximizing over all , we maximize over a region where each residual has constant sign . The constraint then becomes one of two linear constraints, depending on . Let denote the value of Program 4 restricted to . Then with the change of variables, we have that

with the convention that . Now the constraints are linear. Unfortunately, (and this is the second issue), the objective is no longer linear. The solution is to partition the region further: if the region were small enough that every residual had at most -multiplicative variation, then the objective could be approximated to within by a linear objective.

How many regions do we need? Let be the unweighted OLS error. If all the residuals were bounded between and in magnitude, for all , then the regions could be demarcated by hyperplanes, for a total of regions. Of course, for some , some residuals may be very small or very large. But -anti-concentration implies that for every , at most residuals are very small, and it can be shown that if is a weighted OLS solution, the total weight on samples with large residuals is low. Thus, for any region, we can exclude from the objective function the samples with residuals that are not well-approximated within the region, and this only affects the objective by .

This gives an algorithm with time complexity . To achieve the time complexity in Theorem 1.4, where the is additive rather than multiplicative, we use subsampling. Every residual is still partitioned by sign, but we multiplicatively partition only a random -size subset of the residuals. Intuitively, most residuals will still be well-approximated in any given region. This can roughly be formalized via a VC dimension argument, albeit with some technical complications. See Section C for details and Appendix I for formal pseudocode of the algorithm PartitionAndApprox.

Net-based approximation.

The algorithm for Theorem 1.5 is intuitively the simplest. For any fixed , Program 2 reduces to a linear program with value denoted . Thus, an obvious approach is to construct a net in some appropriate metric, and compute . This always upper bounds the stability, but to prove that it’s an approximate lower bound, we need to be Lipschitz under the metric.

The right metric turns out to be

Under this metric, essentially embeds into a -dimensional subspace of the Euclidean sphere , and therefore has a -net of size . Why is Lipschitz under ? First, if equals up to rescaling, then it can be seen from Program 4 that . More generally, if the residuals are close up to rescaling, we apply the dual formulation of from expression (3):

For any , the optimal for and can be rounded to some feasible for and without decreasing the norm too much, under strong anti-concentration. This shows that and are close. See Appendix D for details and Appendix I for formal pseudocode of the algorithm NetApprox.

5 Experiments

In this section, we apply (modifications of) NetApprox and PartitionAndApprox to various datasets. The modifications are made for practical reasons, and while our theory will no longer apply, we emphasize that the modified NetApprox will still provide an unconditional upper bound on stability (referred to henceforth as “net upper bound”), and the modified PartitionAndApprox now provides an unconditional lower bound (“LP lower bound”).

As a baseline upper bound, we implement the greedy heuristic of [KZC21] which refines [BGM20]. We are not aware of any prior work on lower bounding stability, so we implement a simplification of our full lower bound algorithm as a baseline. See Appendix G for implementation details and hyperparameter choices of our algorithms and baselines. All error bars are at th and th percentiles over independent trials.

5.1 Synthetic data

Heterogeneous data.

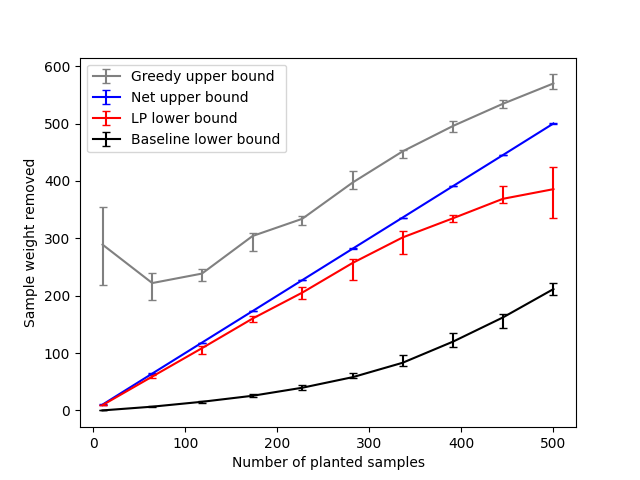

We start with a simple two-dimensional dataset with two disparate subpopulations, where the greedy baseline fails to estimate the stability but our algorithms give tight estimates. For parameters , , and , we generate independent samples , where has independent coordinates and , and . Then, we generate independent samples where and , and . It always suffices to remove the first subpopulation, so the stability is at most . However, the first subpopulation has small individual influences, because the OLS regressor on the whole dataset can nearly interpolate the first subpopulation. Thus, we expect that the greedy algorithm will fail to notice the first subpopulation, and therefore remove far more than samples.

Indeed, this is what happens. For and varying from to , we compare our net upper bound and LP lower bound with the baselines. As seen in Figure 1, our methods are always better than the baselines, and certifiably approximate the stability within a small constant factor. In the regime where is small, our upper bound outperforms the greedy upper bound by a factor of .

Covariance shift.

In the previous example, removing samples caused a pathological change in the sample covariance; it became singular. However, even modest, constant-factor instability in the sample covariance can cause the greedy algorithm to fail; see Appendix G.4 for details.

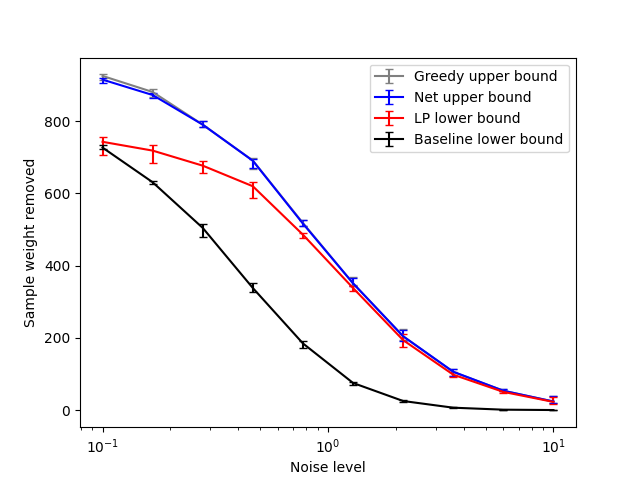

Isotropic Gaussian data.

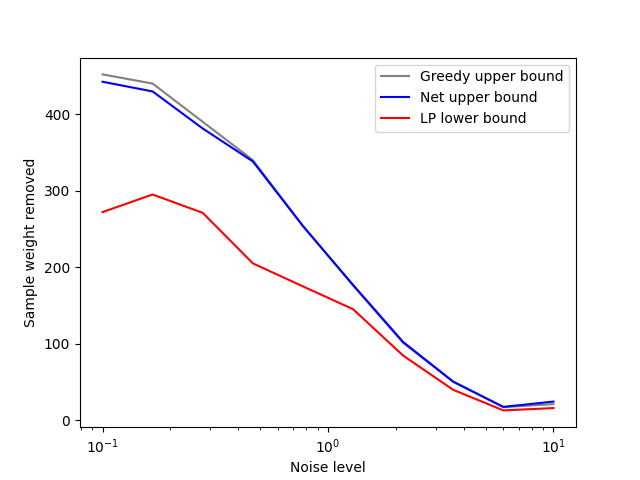

Instability can arise even in homogeneous data, as a result of a low signal-to-noise ratio [BGM20]. But when the noise level is low, can we certify stability? For a broad range of noise levels, we experimentally show that this is the case. Specifically, for and noise parameter ranging from to , we generate independent samples where and . For and (Figure 2(a)), our LP lower bound is nearly tight with the upper bounds, particularly as the noise level increases (in comparison, the baseline lower bound quickly degenerates towards zero). For and (Figure 2(b)), the bounds are looser for small noise levels but still always within a small constant factor.

5.2 Boston Housing dataset

The Boston Housing dataset [HJR78, GP+96] consists of data from census tracts of Greater Boston in the 1970 Census. There are real-valued features, one of which—the median house value in USD 1000s—we designate as the response. Unfortunately the entire set of features is too large for our algorithms, so for our experiments we pick various subsets of two or three features to use as covariates.

A Tale of Two Datasets.

We exemplify our results with two particular feature subsets. First, we investigate the effect of zn (percentage of residential land zoned for large lots) on house values, controlling for rm (average number of rooms per home) and rad (highway accessibility index) but no bias term. On the entire dataset, we find a modest positive effect: the estimated coefficient of zn is roughly . Both the greedy heuristic and our net algorithm find subsets of just of the data (- samples) which, if removed, would nullify the effect. But is this tight, or could there be a much smaller subset with the same effect? Our LP lower bound certifies that removing at least samples is necessary.

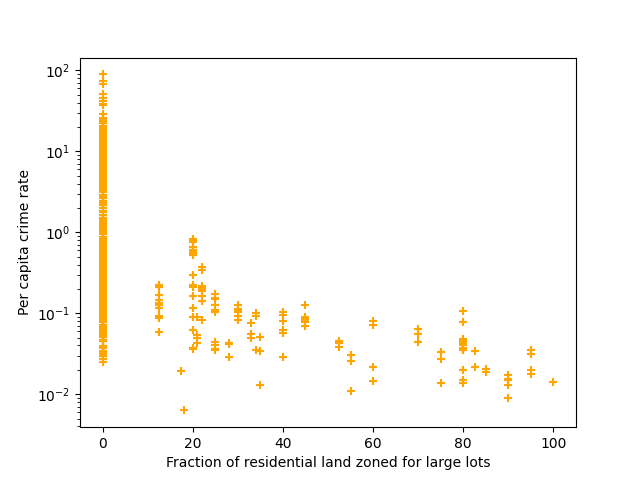

Second, we investigate the effect of zn on house values, this time controlling only for crim (per capita crime rate). Our net algorithm finds a subset of just of the data which was driving the effect, and the LP lower bound certifies that the stability is at least . But this time, the greedy algorithm removes of the samples, a clear failure. What happened? Plotting zn against crim reveals a striking heterogeneity in the data: of the samples have , and the remaining of the samples (precisely those removed by the net algorithm) have , i.e. very low crime rates. As in the synthetic example, this heterogeneity explains the greedy algorithm’s failure. But heterogeneity is very common in real data: in this case, it’s between the city proper and the suburbs, and in fact the OLS regressors of these two subpopulations on all features are markedly different (Appendix G.5). Thus, it’s important to have algorithms with provable guarantees for detecting when heterogeneity causes (or doesn’t cause) unstable conclusions.

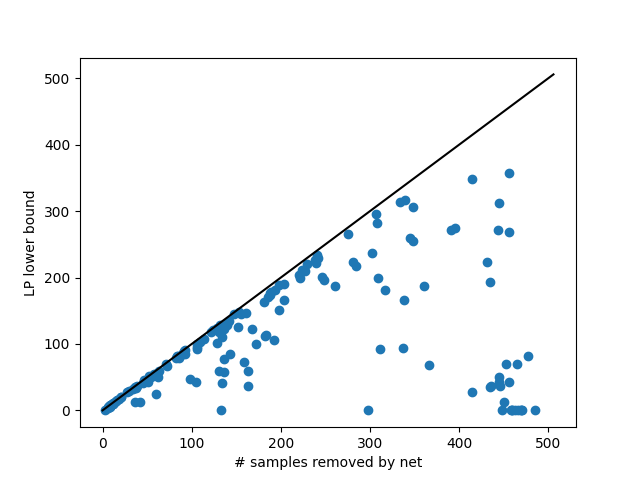

All-feature-pairs analysis.

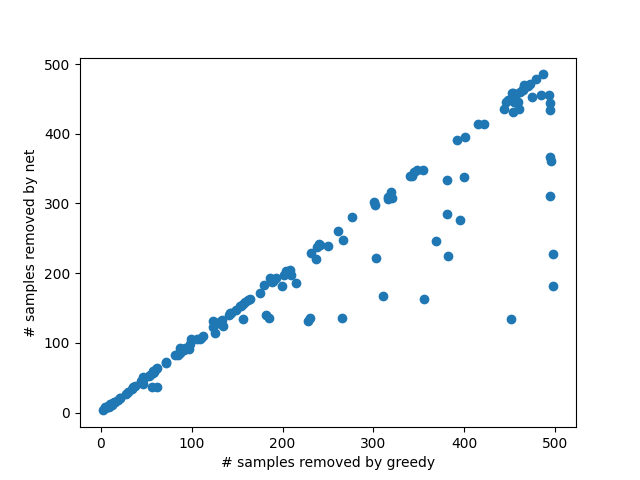

To be thorough, we also apply our algorithms to all ordered pairs of features. For each pair, we regress the response (i.e. median house value) against the two features by Ordinary Least Squares, and we use our algorithms on this -dimensional dataset to estimate how many samples need to be removed to nullify the effect of the first feature on the response. We also compare to the greedy upper bound. See Figure 3 for a perspective on the results. In each figure, each point corresponds to the results of one dataset. The left figure plots the net upper bound against the greedy upper bound: we can see that our net algorithm substantially outperforms the greedy heuristic on some datasets (i.e. finds a much smaller upper bound) and never performs much worse. The right figure plots the LP lower bound against the net upper bound (along with the line ). For a majority of the datasets, the upper bound and lower bound are close. Concretely, for of the datasets, we certifiably estimate the stability up to a factor of two – some are sensitive to removing less than samples, and some are stable to removing even a majority of the samples.

Acknowledgments.

We thank Allen Liu, Morris Yau, Fred Koehler, Jon Kelner, Sam Hopkins, and Vasilis Syrgkanis for valuable conversations on this and related topics.

References

- [AIR96] Joshua D Angrist, Guido W Imbens, and Donald B Rubin, Identification of causal effects using instrumental variables, Journal of the American statistical Association 91 (1996), no. 434, 444–455.

- [Bak16] Monya Baker, 1,500 scientists lift the lid on reproducibility, Nature 533 (2016), no. 7604.

- [BGM20] Tamara Broderick, Ryan Giordano, and Rachael Meager, An automatic finite-sample robustness metric: Can dropping a little data change conclusions, arXiv preprint arXiv:2011.14999 (2020), 16.

- [BKW80] David A Belsley, Edwin Kuh, and Roy E Welsch, Regression diagnostics: Identifying influential data and sources of collinearity, John Wiley & Sons, 1980.

- [BP21] Ainesh Bakshi and Adarsh Prasad, Robust linear regression: Optimal rates in polynomial time, Proceedings of the 53rd Annual ACM SIGACT Symposium on Theory of Computing, 2021, pp. 102–115.

- [ČAH13] Michal Černỳ, Jaromír Antoch, and Milan Hladík, On the possibilistic approach to linear regression models involving uncertain, indeterminate or interval data, Information Sciences 244 (2013), 26–47.

- [Car01] David Card, Estimating the return to schooling: Progress on some persistent econometric problems, Econometrica 69 (2001), no. 5, 1127–1160.

- [CGAD20] Maxime Cauchois, Suyash Gupta, Alnur Ali, and John C Duchi, Robust validation: Confident predictions even when distributions shift, arXiv preprint arXiv:2008.04267 (2020).

- [CH86] Samprit Chatterjee and Ali S Hadi, Influential observations, high leverage points, and outliers in linear regression, Statistical science (1986), 379–393.

- [CHCFC04] Enrique Castillo, Ali S Hadi, Antonio Conejo, and Alfonso Fernández-Canteli, A general method for local sensitivity analysis with application to regression models and other optimization problems, Technometrics 46 (2004), no. 4, 430–444.

- [Coo77] R Dennis Cook, Detection of influential observation in linear regression, Technometrics 19 (1977), no. 1, 15–18.

- [DKK+19] Ilias Diakonikolas, Gautam Kamath, Daniel Kane, Jerry Li, Jacob Steinhardt, and Alistair Stewart, Sever: A robust meta-algorithm for stochastic optimization, International Conference on Machine Learning, PMLR, 2019, pp. 1596–1606.

- [DN18] John Duchi and Hongseok Namkoong, Learning models with uniform performance via distributionally robust optimization, arXiv preprint arXiv:1810.08750 (2018).

- [GKR09] Panos Giannopoulos, Christian Knauer, and Günter Rote, The parameterized complexity of some geometric problems in unbounded dimension, International Workshop on Parameterized and Exact Computation, Springer, 2009, pp. 198–209.

- [GP+96] Otis W Gilley, R Kelley Pace, et al., On the harrison and rubinfeld data, Journal of Environmental Economics and Management 31 (1996), no. 3, 403–405.

- [GR21] Suyash Gupta and Dominik Rothenhäusler, The -value: evaluating stability with respect to distributional shifts, arXiv preprint arXiv:2105.03067 (2021).

- [GSL+19] Ryan Giordano, William Stephenson, Runjing Liu, Michael Jordan, and Tamara Broderick, A swiss army infinitesimal jackknife, The 22nd International Conference on Artificial Intelligence and Statistics, PMLR, 2019, pp. 1139–1147.

- [Gur22] Gurobi Optimization, LLC, Gurobi Optimizer Reference Manual, 2022.

- [Hal00] Mark A Hall, Correlation-based feature selection of discrete and numeric class machine learning.

- [HJR78] David Harrison Jr and Daniel L Rubinfeld, Hedonic housing prices and the demand for clean air, Journal of environmental economics and management 5 (1978), no. 1, 81–102.

- [HS93] Ali S Hadi and Jeffrey S Simonoff, Procedures for the identification of multiple outliers in linear models, Journal of the American statistical association 88 (1993), no. 424, 1264–1272.

- [Hub04] Peter J Huber, Robust statistics, vol. 523, John Wiley & Sons, 2004.

- [HWD18] Georg Heinze, Christine Wallisch, and Daniela Dunkler, Variable selection–a review and recommendations for the practicing statistician, Biometrical journal 60 (2018), no. 3, 431–449.

- [Ioa05] John PA Ioannidis, Why most published research findings are false, PLoS medicine 2 (2005), no. 8, e124.

- [JN20] Sookyo Jeong and Hongseok Namkoong, Robust causal inference under covariate shift via worst-case subpopulation treatment effects, Conference on Learning Theory, PMLR, 2020, pp. 2079–2084.

- [KKM18] Adam Klivans, Pravesh K Kothari, and Raghu Meka, Efficient algorithms for outlier-robust regression, Conference On Learning Theory, PMLR, 2018, pp. 1420–1430.

- [KNRW18] Michael Kearns, Seth Neel, Aaron Roth, and Zhiwei Steven Wu, Preventing fairness gerrymandering: Auditing and learning for subgroup fairness, International Conference on Machine Learning, PMLR, 2018, pp. 2564–2572.

- [KV94] Michael J Kearns and Umesh Vazirani, An introduction to computational learning theory, MIT press, 1994.

- [KZC21] Nikolas Kuschnig, Gregor Zens, and Jes Cuaresma, Hidden in plain sight: Influential sets in linear models.

- [Lea84] Edward E Leamer, Global sensitivity results for generalized least squares estimates, Journal of the American Statistical Association 79 (1984), no. 388, 867–870.

- [Loh11] Wei-Yin Loh, Classification and regression trees, Wiley interdisciplinary reviews: data mining and knowledge discovery 1 (2011), no. 1, 14–23.

- [LP03] Michail G Lagoudakis and Ronald Parr, Least-squares policy iteration, The Journal of Machine Learning Research 4 (2003), 1107–1149.

- [Mil64] John Milnor, On the betti numbers of real varieties, Proceedings of the American Mathematical Society 15 (1964), no. 2, 275–280.

- [ML92] Gangadharrao S Maddala and Kajal Lahiri, Introduction to econometrics, vol. 2, Macmillan New York, 1992.

- [MLX+17] Xudong Mao, Qing Li, Haoran Xie, Raymond YK Lau, Zhen Wang, and Stephen Paul Smolley, Least squares generative adversarial networks, Proceedings of the IEEE international conference on computer vision, 2017, pp. 2794–2802.

- [Pol84] Wolfgang Polasek, Regression diagnostics for general linear regression models, Journal of the American Statistical Association 79 (1984), no. 386, 336–340.

- [Ren92] James Renegar, On the computational complexity and geometry of the first-order theory of the reals. part i: Introduction. preliminaries. the geometry of semi-algebraic sets. the decision problem for the existential theory of the reals, Journal of symbolic computation 13 (1992), no. 3, 255–299.

- [Sar58] John D Sargan, The estimation of economic relationships using instrumental variables, Econometrica: Journal of the Econometric Society (1958), 393–415.

- [SNVD17] Aman Sinha, Hongseok Namkoong, Riccardo Volpi, and John Duchi, Certifying some distributional robustness with principled adversarial training, arXiv preprint arXiv:1710.10571 (2017).

- [TG07] Joel A Tropp and Anna C Gilbert, Signal recovery from random measurements via orthogonal matching pursuit, IEEE Transactions on information theory 53 (2007), no. 12, 4655–4666.

- [THW89] Hideo Tanaka, Isao Hayashi, and Junzo Watada, Possibilistic linear regression analysis for fuzzy data, European Journal of Operational Research 40 (1989), no. 3, 389–396.

- [Ver18] Roman Vershynin, High-dimensional probability: An introduction with applications in data science, vol. 47, Cambridge university press, 2018.

Appendix A Proof of Theorem 1.2

In this section, we show how to exactly compute the stability of a -dimensional dataset in time , proving Theorem 1.2. Our main tool is Theorem 4.1, a special case of an important result due to [Ren92] on solving quantified polynomial systems of inequalities.

The expression can indeed be written as a polynomial system of (degree-) equations, with only an quantifier. Unfortunately, the number of variables in this naive formulation is ( for the weights and for the regressor), which yields an algorithm exponential in . Thus, to take advantage of the above theorem, we need to reformulate the expression with fewer variables. The following lemma rewrites the stability, via the separation theorem for convex sets, in a form where the variable reduction will become apparent.

Lemma A.1.

For any and , it holds that if and only if

| (5) |

where is the matrix with columns .

Proof.

From formulation (2) of the stability, we know that if and only if

Fix . Define the set

We are interested in the predicate , or equivalently . Observe that is convex, since ranges over a convex set. Thus, by the separation theorem for a point and a convex set, if and only if for every , we have . If is not orthogonal to , then the inner product can be made arbitrarily large. Thus, it suffices to restrict to , in which case the supremum is simply over . That is, if and only if

Quantifying over , we get the claimed expression. ∎

The expression in Lemma A.1 still has variables. However, we can now actually eliminate the variable at the cost of increasing the number of equations. This is because the optimal for fixed and only depends on the relative order of the terms . We make the following definition:

Definition A.2.

For any and , let be the unique permutation on such that for all ,

and such that equality implies . Let .

Then it can be seen that for fixed and , the optimal choice of has coefficients on , and coefficient for : if there is any feasible which makes the sum non-negative, then this choice of makes the sum non-negative as well. Denoting this vector by , we have that in Equation 5 it suffices to restrict to .

A priori, the number of achievable permutations could be , in which case we would not have gained anything. However, because is defined by low-degree polynomials in only variables, we can actually show that is at most exponential in , using the following result:

Theorem A.3 (Sign Partitions [Mil64, Ren92]).

Let be arbitrary polynomials each with total degree at most . Let be the set of vectors such that is an achievable sign vector, i.e. there exists some with for all . Then . Moreover, can be enumerated in time .

Putting everything together, we have the following theorem, which proves Theorem 1.2.

Theorem A.4.

For any permutation on , define by

Then for any , it holds that if and only if

| (6) |

Moreover, can be enumerated in time . Thus, the expression can be decided in time .

Proof.

Fix and . If

| (7) |

then because , we obviously get

| (8) |

Conversely, if (7) is false, then in particular produces a negative sum . But by construction, maximizes this sum, over all with . Therefore no weight vector with norm exactly produces a nonnegative sum, and increasing the norm cannot help. Thus, (8) and (7) are equivalent. Quantifying over and , we have if and only if

Taking the negation yields expression (6). If we can compute , then this expression is a -system of polynomial inequalities with variables and degree- inequalities, so by Theorem 4.1 it can be decided in time . It remains to show that can be enumerated in time (which bounds ).

For any with define the polynomial

For any and , the permutation is determined by the signs of the polynomials at . But by Theorem A.3, the set of sign vectors can be computed in time . So can be found in time as well. ∎

Appendix B Proof of Theorem 1.3

In this section, we prove Theorem 1.3. That is, we show that exactly computing the stability requires time under the Exponential Time Hypothesis, by a simple reduction from the Maximum Feasible Subsystem problem. This latter problem is already known to take time in dimensions under the Exponential Time Hypothesis:

Theorem B.1 (Theorem 13 in [GKR09]).

Suppose that there is an -time algorithm for the following problem: given vectors , real numbers , and an integer , determine whether

Then the Exponential Time Hypothesis is false.

From this, it can be easily seen that (exactly) computing stability also requires time.

Theorem B.2.

Suppose that there is an -time algorithm for the following problem: given and , as well as an integer , determine whether

Then the Exponential Time Hypothesis is false.

Proof.

We reduce to Maximum Feasible Subsystem. Given and , define and . Then the regressor perfectly fits the data set, i.e.

Thus, for any ,

Suppose that . Then there is some and with and . Let be the support of ; then . Moreover for every , it holds that . Since , by definition of and , this implies that . Thus,

Conversely, suppose that there exists some and set of size such that for all . Define , and define . Then it is clear that

Thus, , so . This completes the reduction. ∎

Remark B.3.

Maximum Feasible Subsystem does have an -additive approximation algorithm in time , by subsampling. Thus, proving -hardness for -approximation of stability would require a different technique.

Appendix C Proof of Theorem 1.4

In this section, we prove Theorem 1.4. The main idea of PartitionAndApprox is that under Assumption A, we can approximate the stability by partitioning into roughly regions and solving a linear program on each region. See Appendix I for the complete algorithm.

C.1 Partitioning scheme

Given samples , let , where . Let be a uniformly random size- subset of . Let be the closed connected subsets of cut out by the following set of equations :

Formally, we define a region for every feasible assignment of equations to , and then replace each strict inequality by a non-strict inequality, so that the region is closed. First, we observe that the number of regions is not too large, and in fact we can enumerate the regions efficiently.

Lemma C.1.

Each region is the intersection of linear equalities or inequalities. Moreover, the regions can be enumerated in time .

Proof.

Order the set of equations arbitrarily. We recursively construct the set of regions demarcated by the first equations. For each such region, we solve a linear program to check if the th hyperplane intersects the interior of the region. If so, we split the region according to the sign of the th hyperplane. The overall time complexity of this procedure is , where is the final number of regions. But the number of regions which can be cut out by hyperplanes in is at most by standard arguments. ∎

Next, we argue that even though we only multiplicatively partitioned a small subset of the residuals, with high probability most residuals are well-approximated. More precisely, we show that for the (random) region containing a fixed point , with high probability, for every other in the region, most residuals at are multiplicatively close to the corresponding residuals at . This can be proven by the generalization bound for function classes with low VC dimension:

Theorem C.2 (Theorem 3.4 in [KV94]).

Let be a set. Let be a binary concept class with VC dimension . Let be a distribution on . Let and pick satisfying

for a sufficiently large constant . Let be independent samples from . Then with probability at least , the following holds. For all with for all ,

Specifically, for any , we define a function as the indicator function of samples for which the residual at is close to the residual at . Then the region containing is precisely the set of functions which perfectly fit , and the generalization bound implies that all such functions fit most of , which is what we wanted to show. The following lemma formalizes this argument, with some additional steps to deal with very small and very large residuals.

Lemma C.3.

Let and let . Let be the region containing . Let be the set of such that , and let be the set of such that . If

for an absolute constant , then with probability at least over the choice of , the following holds. For every , the number of such that

is at most .

Proof.

Let be defined by . Note that by construction of the regions, for every .

Let . If , then the lemma statement is trivially true. Otherwise, by a Chernoff bound,

Condition on the event . Then is uniform over size- subsets of . Define , and define a concept class as the set of binary functions

Let be the distribution on where has and . Then consists of at least independent samples from . For any , we claim that the function fits perfectly. Indeed, for any , we know that , since . So by construction of the regions, it holds that

From the right-hand side of the equation, we precisely get that , as claimed. By Lemma C.4, we have . Thus, since

if is a sufficiently large absolute constant, we can apply Theorem C.2 with failure parameter to get that with probability at least ,

Equivalently, for every , the number of such that is at most . An identical argument with the binary functions

proves that with probability at least , for every , the number of such that is at most . Overall, by the union bound (taking into account the event that ), with probability at least it holds that for every , the number of such that either or is at most as claimed. ∎

It remains to bound the VC dimension of the function class.

Lemma C.4.

For any and any , the VC dimension of the concept class , where

is at most .

Proof.

Note that extending the domain of the concepts cannot decrease the VC dimension. Thus, if we define by

then . But all of the concepts in are affine halfspaces in dimensions, so . ∎

C.2 Algorithm

For every region we can identify some arbitrary representative and a sign pattern such that implies for all , and implies for all . Ideally, we want to compute where

| (9) |

However, this is not a linear program. Let be the set of such that , and let be the set of such that . For each region we compute

| (10) | |||

| (11) |

and define

with the convention that . Note that although there is a in the objective of Program 11, it is equivalent to a linear program by a standard transformation: we can introduce variables with the constraints and , and change the objective to maximize . That is, the following program also computes :

| (12) | |||

| (13) |

Lemma C.5.

Proof.

For the RHS, observe that for any region , if we define by , with the convention that , then the second and third constraints of Program 11 ensure that . Additionally, the first constraint ensures that

Thus, is feasible for the original problem. This means that .

To prove the lower bound, suppose that . Consider the specific region containing the optimal parameter vector (if there are multiple choose any), and let and . Define by . Let be the set of such that

By Lemma C.3 (applied specifically to ), we know . By assumption, we know that . And we know that if then , so the same holds for all and in particular for . Thus

where the third inequality is because , and the equality is by definition of . Finally, for any , we have

Therefore

The sum in the last line above is precisely the objective of Program 11 at . Moreover, is feasible for Program 11 because and for all . Thus, the optimal solution satisfies the inequality

Finally, let be the set of such that

By Lemma C.3, the residuals at multiplicatively approximate the residuals at except for samples, and the residuals at also multiplicatively approximate the residuals at except for samples. Thus, , so we have

We conclude that . Since , simplifying gives as claimed. ∎

Using the above lemma in conjunction with Lemma C.3 immediately gives the desired theorem (from which Theorem 1.4 is a direct corollary).

Theorem C.6.

For any , there is an algorithm PartitionAndApprox with time complexity

which, given , , , and arbitrary samples , either outputs or an estimate . If the output is , then the samples do not satisfy -anti-concentration (Assumption A). Moreover, the probability that the output is some such that

is at most .

Proof.

The algorithm PartitionAndApprox does the following (see Appendix I for pseudocode). Let where is the constant specified in Lemma C.3, and let where . Let be the set of equations described in Section C.1, with respect to a uniformly random subset of size . Let be the closed connected regions cut out by . By Lemma C.1, we can enumerate in time ; each is described by at most linear constraints. For each , we can find a representative by solving a feasibility LP on , and by solving LPs on , we can find a sign pattern such that implies for all , and implies for all . We also compute and . If , then return . Otherwise, compute , the solution to Program 13, and compute . Finally, after iterating through all regions, output .

Appendix D Proof of Theorem 1.5

In the previous section, we approximated the nonlinear program (2) by partitioning into regions where the program could be approximated by a linear program. This approach had the disadvantage of requiring that in each region, the signs of the residuals were constant (so that the program could be reparametrized to have linear constraints), which necessitates making regions. In this section, we instead make use of the fact that for fixed , Program 2 is a linear program and therefore efficiently solvable. Our algorithm NetApprox is simply to (carefully) choose a finite subset , solve the linear program for each , and pick the best answer.

The following lemma describes how to compute , which will be an -net over in an appropriate metric.

Lemma D.1.

For any and , there is a set of size such that for any with , there is some with , and some , such that

Moreover, can be computed in time .

Proof.

Let be the matrix with columns . Let and let be the singular value decomposition of , where is the diagonal matrix of nonzero singular values of . Let be a “marginally-random” -net over the unit sphere under the metric, where by “marginally-random” we mean that is chosen from some distribution, and every point of the net has marginal distribution uniform over (e.g. take any fixed -net and apply a uniformly random rotation). Also define . Suppose is not identically zero. Then define

Since each is a generic unit vector (by the marginally-random property) and is nonzero, we have that all are nonzero with probability , so the above set is well-defined. Moreover, for any ,

Now let with , and define . Observe that

So there is some with . Let and let . Then

and

Thus,

as desired. On the other hand, if is identically zero, then , so . This boundary case can be avoided by picking any nonzero covariate among and replacing by for a generic ; this does not change .

Note that a -net of with can be constructed in time by discretizing the cube . Thus, can be constructed in time as well, and . ∎

All that is left is to show that under strong anti-concentration, the value of the linear program is Lipschitz in (under the metric described in the previous lemma). This proves Theorem 1.5.

Theorem D.2.

Let . There is an algorithm NetApprox with time complexity which, given arbitrary samples , produces an estimate satisfying . Moreover, if satisfy -strong anti-concentration, then in fact

Proof.

For any , define

so that . For any fixed , we can compute in polynomial time, since it is defined as an LP with variables and constraints. Fix . The algorithm NetApprox does the following (see Appendix I for pseudocode): if has a solution, then output . Otherwise, let be the net guaranteed by Lemma D.1. Then compute for every , and output the estimate

Since the algorithm involves solving linear programs, the time complexity is as claimed. Next, since the algorithm is maximizing over a subset of , it’s clear that . It remains to prove the upper bound on . Recall from Lemma A.1 that for any ,

Let be a maximizer of and for notational convenience let . If , then the algorithm correctly outputs . Otherwise, by the guarantee of Lemma D.1, there is some with and such that

Pick any . Since , there is some such that and

Without loss of generality, there is at most one coordinate such that is strictly between and . Also, the above inequality implies that

where the last two inequalities are by Cauchy-Schwarz and the guarantee of Lemma D.1, respectively. Now define by the following procedure. Initially set . Iterate through in increasing order of and repeatedly set the current coordinate , until

Obviously, this procedure will terminate with a feasible . If it terminates after making updates, then . Throughout the procedure, the sum is non-decreasing. If and and , then the sum increases by at least . So the number of such steps is at most . But the number of steps with is at most by -strong anti-concentration. Similarly, the number of steps with is at most . And the number of steps with is at most . Thus, . We conclude that , so . ∎

Appendix E Motivation for anti-concentration assumptions

E.1 Smoothing implies anti-concentration

In this section, we show that anti-concentration (Assumption A) holds under the mild assumption that the response variable is smoothed. In the following proposition, notice that we always have the crude bound .

Proposition E.1.

Let and let be arbitrary with and . Suppose that are independent Gaussian random variables, and define for . Then with probability at least , the dataset satisfies -anti-concentration where

and .

Proof.

Without loss of generality, . Define ; we want to upper bound . Let ; then . But , and is stochastically dominated by . So with probability at least , by the tail bound for random variables.

Next, we claim that with high probability, for every set of size , there is no such that for all . Fix some . We bound the probability that for all ,

because this event contains the event that all residuals in are at most . Now it suffices to restrict to the OLS estimator . Now defining , we have

Note that is an orthogonal projection onto a space of dimension , so there is a matrix be such that and . Then we can write

for a random vector This means that . But for any , note that stochastically dominates where , so stochastically dominates , and thus stochastically dominates . Therefore

For any , since the density of is bounded above by , we have

Recalling that , this shows that for a fixed of size , with probability at least , there is no with for all . A union bound over sets of size proves the claim.

Finally, we use the above bounds to show that the smoothed data satisfies -anti-concentration. We consider two cases. First, if , then with probability we have , so for any , the number of satisfying

is at most . ∎

E.2 Distributional Assumptions for strong anti-concentration

In this section, we show that under reasonable distributional assumptions on the samples , strong anti-concentration (Assumption B) holds with constant . First, it holds if the samples are i.i.d. and have an arbitrary multivariate Gaussian joint distribution.

Proposition E.2.

Let and set . Let be symmetric and positive-definite. Let be independent and identically distributed. If for some absolute constant , then with probability at least , samples satisfy -strong anti-concentration, i.e. for all , it holds that

where is the matrix with rows .

Proof.

Let . Then by concentration of Wishart matrices, it holds with probability at least that (see e.g. Exercise 4.7.3 in [Ver18]). In this event, for all .

Let be the class of binary functions . Observe that every function in is the intersection of parallel half-spaces, so has VC dimension . Moreover, for any ,

since , and Gaussian random variables are anti-concentrated ( for any and ). Thus, by the Vapnik-Chervonenkis bound and assumption on ,

So with probability at least it holds that for all ,

This means that with probability at least , we have that for all ,

as desired. ∎

Second, strong anti-concentration holds if the samples are drawn from a mixture of centered Gaussian distributions, with arbitrary weights, so long as each covariance matrix has bounded largest and smallest eigenvalues.

Proposition E.3.

Let and let be symmetric and positive-definite matrices. Suppose that there are constants such that , and define . For arbitrary weights with , let be independent and identically distributed. If for some absolute constant , then with probability at least , samples satisfy -strong anti-concentration.

Proof.

The proof is similar to that of the previous proposition. First, note that each can be coupled with so that . So with probability at least it holds that and thus for all .

Next, let be the class of binary functions . Then has VC dimension , and for any ,

since is stochastically dominated by . By the Vapnik-Chervonenkis bound, with probability at least , we get that for all ,

Combining with the upper bound on , we have with probability at least that for all ,

as claimed. ∎

Appendix F Extension to IV Linear Regression

We extend the definition of stability to measure the stability of the sign of a coefficient of the IV linear regressor:

Definition F.1.

For samples with covariates , response , and instruments , the ordinary IV estimator set with weight vector is

The finite-sample stability of is then defined

For any , the expression is still defined as a bilinear system of equations in and . Our exact algorithm for never uses that the weighted residual is multiplied by in the OLS solution set, rather than some arbitrary matrix ; all that matters is that this matrix has at most rows. Thus, with a bound on the number of instruments, the algorithm generalizes to computing :

Theorem F.2.

There is an -time algorithm which, given arbitrary samples with and and , and given , decides whether .

The algorithm NetApprox also generalizes to IV regression. To state the guarantee, we define an anti-concentration assumption for IV regression data.

Assumption C.

Let . We say that samples satisfy -strong anti-concentration if for every and it holds that

and

Then it is easy to see that the proof of Theorem 1.5 immediately extends to give the following result:

Theorem F.3.

For any , there is a -time algorithm which, given , and samples satisfying -strong anti-concentration, returns an estimate satisfying

Appendix G Further experimental details

G.1 Implemented algorithms

Net upper bound.

We implement NetApprox with one modification: instead of deterministically picking the net by discretization (see Lemma D.1), we let be a set of random unit vectors from , and then compute as in Lemma D.1. Instead of parametrizing the algorithm by the desired approximation error , we parametrize by . Despite this change, the algorithm still provides a provable, exact upper bound on .

LP lower bound.

The disadvantage of NetApprox is that it only lower bounds the stability under an assumption that seems hard to check. The PartitionAndApprox algorithm is better, because it unconditionally, with high probability, outputs either an accurate estimate or a failure symbol . However, the time complexity (needed so that in each region, all residuals have constant sign) may be prohibitively slow in practice. For this reason, we introduce a heuristic simplification of PartitionAndApprox which provably lower bounds the stability with no assumptions.

At a high level, we decrease the number of regions by ignoring the requirement that within each region all residuals have constant sign. The algorithm is parametrized by a list of thresholds and a subset size , and the regions are demarcated by the hyperplanes for random choices and all . Now, for samples which do not have constant residual in a particular region , the constraints are nonconvex after the change of variables. We relax these constraints to linear constraints, and relax the objective function to skip the “bad” samples. Heuristically, this relaxation should not lose too much on samples where the residual remains small throughout , but may be problematic if the residual blows up. This motivates the use of a complementary lower bound heuristic based on the minimum squared-loss achievable by any . See Appendix H for details.

Baseline greedy upper bound [BGM20, KZC21].

Baseline lower bound.

This algorithm simply computes the squared-loss-based lower bound (used in our full lower bound algorithm) for each region. See Appendix H for details.

G.2 Hyperparameter choices

The net upper bound has only one hyperparameter (the number of trials), which should be chosen as large as possible subject to computational constraints. The LP lower bound has two hyperparameters (the size of the random subsample, and the set of thresholds). We choose these ad hoc subject to our computational constraints. Experiments to determine the optimal tradeoff between the subsample size and threshold set could be useful. However, we note that because the LP lower bound unconditionally lower bounds the stability, no matter what hyperparameters we choose, in practice it suffices to try several sets of hyperparameters and compute the maximum of the resulting lower bounds.

Heterogeneous data experiment.

For each dataset, we applied the net upper bound with trials, the LP lower bound with and , and the baseline lower bound with and .

Isotropic Gaussian data.

For each dataset with noise level , we applied the net upper bound with trials, the LP lower bound with and , and the baseline lower bound with and .

Boston Housing dataset.

For the two-dimensional datasets, we applied the net upper bound with trials and the LP lower bound with and . For the three-dimensional dataset we applied the net upper bound with trials and the LP lower bound with and .

G.3 Computational details

All experiments were done in Python on a Microsoft Surface Laptop, using GUROBI [Gur22] with an Academic License to solve the linear programs. Each plot took at most hours to generate (specifically, the three-dimensional Gaussian isotropic data experiment took hours for each of the datasets, dominated by the time required for the LP lower bound algorithm; other plots were faster).

G.4 Omitted experiment: Covariance Shift

Consider a dataset with samples drawn from and , where . Additionally, there are outliers, in two types: the type-I outliers have and large and negative; the one type-II outlier has and chosen to exactly lie on the OLS best-fit hyperplane . Initially, , and clearly removing the last samples suffices to flip the sign. However, the initial sample covariance is roughly . The influence of a sample on coordinate of the OLS regressor is . As a result, the type-I outliers have negative influence on , so the greedy algorithm initially does not remove them. The influence only becomes positive after removing the type-II outlier, because this shifts the sample covariance to , and therefore flips the sign of .

Constructing this example experimentally requires some care in the choices of , , and : we need the total influence of type-A outliers (proportional to ) large enough that , and need small enough that the type-I outliers don’t affect the sample covariance much. Moreover, the number of trials needed by the net algorithm roughly scales with . We take , , , and . Applying the greedy baseline and the net upper bound (with trials), we find that the former removes samples while the latter removes roughly samples. In this example, the failure of the greedy baseline can be attributed to the constant-factor shift in the sample covariance achieved by removing the type-B outlier.

G.5 Omitted figures

Appendix H Heuristic for lower bounding stability

In this section we further explain the “LP lower bound” which we applied in Section 5 to provide exact lower bounds on stability of various datasets.

Given a list of thresholds and a subset size , we randomly pick a set of size , and enumerate the regions defined by the hyperplanes

Fix one such region . Similar to PartitionAndApprox, we use the change of variables , and enforce the constraint . For some of the , the residual will have constant sign on the entire region. For these samples, we enforce the constraint (if the residual is non-negative) or (if the residual is non-positive). However, because we didn’t include a hyperplane for every sample, it’s likely that for some , the residual attains both signs within the region, in which case the constraint is not convex in and . Thus, we relax the constraint to

Note that this is indeed a relaxation, because the interval contains . Finally, let be the set of indices for which the residual is non-negative on , and let be the set of indices for which the residual is non-positive. Then we minimize the objective

Because this objective is less than or equal to , and because we only relaxed constraints, this program has value at most (the value of the exact non-linear program restricted to ).

Compared to the provable approximation algorithm described previously, this algorithm is a heuristic because each region will typically have samples for which the residual changes sign within the region. As rough intuition, if the residual remains fairly small throughout the region then the relaxation of the constraint on may not be problematic. However, if the residual can attain large magnitude in the region, then relaxing the constraint on may significantly change the value of the program. However, we may expect that if the partition is sufficiently fine, then a region where some residual is allowed to blow up may have many samples whose residuals are forced to be large. This motivates the use of an additional heuristic to refine the certification algorithm: if are the optimal solution to the sensitivity problem, and is the original regressor, then it must hold that

However, if is the region containing the optimal solution and if , then

Thus, if we compute (by computing the interval of achievable residuals) for each , then we can lower bound (conditioned on containing the optimal solution) by sorting and finding the smallest subset such that .