Data-Driven Approximations of Chance Constrained Programs in Nonstationary Environments

Abstract

We study sample average approximations (SAA) of chance constrained programs. SAA methods typically approximate the actual distribution in the chance constraint using an empirical distribution constructed from random samples assumed to be independent and identically distributed according to the actual distribution. In this paper, we consider a nonstationary variant of this problem, where the random samples are assumed to be independently drawn in a sequential fashion from an unknown and possibly time-varying distribution. This nonstationarity may be driven by changing environmental conditions present in many real-world applications. To account for the potential nonstationarity in the data generation process, we propose a novel robust SAA method exploiting information about the Wasserstein distance between the sequence of data-generating distributions and the actual chance constraint distribution. As a key result, we obtain distribution-free estimates of the sample size required to ensure that the robust SAA method will yield solutions that are feasible for the chance constraint under the actual distribution with high confidence.

Chance constrained programs, data-driven optimization, nonstationary environments, Wasserstein metric.

1 Introduction

We consider a class of chance constrained optimization problems of the form

| (1) |

Here, denotes the optimization variable, is a deterministic set, is the objective function, is a given constraint function, and is an -valued random vector whose probability distribution is supported on a set . The random vector reflects uncertainty in the constraint function, and the risk parameter encodes the maximum probability of constraint violation that the decision maker is willing to tolerate.

Chance constrained programs (CCPs) can be difficult to solve for several reasons. First, chance constraints typically result in nonconvex feasible sets [1], and have been shown to result in NP-hard optimization problems in certain settings [2]. Second, the underlying probability distribution of the random variable is often unknown. These issues render the exact solution of CCPs intractable, and motivate the development of data-driven approximation methods.

Well-known approximation techniques include the sample average approximation (SAA) method [3] and the scenario approach [4, 5]. Both methods approximate the original chance constraint using randomly sampled constraints, which are based on samples assumed to be drawn in an independent and identically distributed (i.i.d.) fashion from the actual distribution used in the definition of the original chance constraint. However, in many real-world applications where the underlying data-generating processes may be nonstationary in nature, it may not be possible to obtain i.i.d. samples from the actual distribution of interest. This nonstationarity may be driven by gradual sensor degradation over time, sudden hardware faults, changing environmental conditions, or shifting users behavior [6]. Many distributionally robust optimization methods [7, 8, 9, 10, 11, 12, 13, 14] have been developed to compensate for potential discrepancies between the data-generating distribution and the actual distribution of interest. Importantly, these methods rely on the assumption that the random samples are drawn from a common distribution. This assumption may fail to hold in nonstationary environments, where the random samples are drawn from possibly different distributions over time.111Although one could apply the distributionally robust approach in nonstationary environments by considering the worst-case discrepancy between the sequence of data-generating distributions and the chance constraint distribution, such a procedure is likely overly conservative.

Summary of Contributions

This paper addresses this gap by developing SAA schemes tailored to nonstationary environments. We begin by studying SAA schemes in stationary environments. As a first contribution, we establish a new bound on the probability that a feasible solution to the SAA violates the original chance constraint, improving upon the previously best-known bound [3, Theorem 10]. As a second contribution, we turn to nonstationary environments and propose a novel robust SAA scheme utilizing information about the distance between the sequence of unknown data-generating distributions and the actual chance constraint distribution. While the classic SAA scheme only enforces sampled constraints at the random samples, the key novelty of our approach is to require that each sampled constraint be enforced robustly with respect to an uncertainty set defined as the intersection of the support set and a norm-ball centered at each random sample with a radius . The radius depends explicitly on the distance between the data-generating distribution and the chance constraint distribution. The idea of imposing constraints robustly around the samples is also used in distributionally robust optimization methods (e.g. [14, 12]) to approximate ambiguous CCPs by robust sampled programs. An advantage of our approach is that different radii can be used for different samples to capture variations in data-generating distributions. By using the Wasserstein metric to quantify the distance between distributions, we provide upper bounds on the probability that a feasible solution to the proposed robust SAA violates the original chance constraint (which is termed the probability of infeasibility), as a function of the radii. We first derive our results for sets with finite cardinality and then suggest an extension of the proposed approach to generic bounded sets , under an additional Lipschitz assumption on the given constraint function.

Organization

The remainder of this paper is organized as follows. In Section 2, we recap results pertaining to sample average approximations of CCPs in stationary environments, present a new and improved upper bound on the probability of infeasibility, and compare our bound with the previously best-known bound [3, Theorem 10]. In Section 3, we introduce the nonstationary data-generation model, propose a robust SAA scheme tailored to this setting, and derive upper bounds on the corresponding probability of infeasibility. Section 4 concludes the paper.

Notation

Let , and denote the sets of real numbers, nonnegative real numbers and integers, respectively. Given a positive integer , we let denote the set of the first integers. Given a real number , we denote its ceiling by , its floor by , and its positive part by . We use boldface symbols to denote random variables, and non-boldface symbols to denote particular values in the range of a random variable and other deterministic quantities. We let denote the probability of an event , and denote the expected value of a random variable . The indicator function is denoted by .

2 Sample Average Approximation in Stationary Environments

We first rewrite the chance constrained problem (1) as

where denotes the constraint violation probability at a point . To ensure that the function is well defined, the function is assumed to be measurable for every . The feasible region of problem (1) is denoted by

In this section, we consider a stationary data-generating environment and assume that i.i.d. random samples can be drawn from the actual distribution specifying the chance constraint. Based on these samples, one can approximate the chance constraint by replacing the data-generating distribution with the empirical distribution. This results in an empirical approximation of as

where is the sample size and is a constraint tightening parameter. Using this empirical approximation of the constraint violation probability, Luedtke and Ahmed [3] define the sample average approximation of problem (1) as

| (2) |

where the fixed risk level is a design parameter and may be chosen to be smaller than the original risk level to compensate for the discrepancy between the actual and empirical distribution. Overall, the parameters and require the strict satisfaction of at least of the sampled constraints with a margin .222For , the SAA (2) reduces to a scenario approximation of the CCP, requiring that all sampled constraints be satisfied (e.g., [4, 15]).

It is reasonable to expect that, for risk levels , any feasible solution to the SAA (2) will be feasible for problem (1) with high probability given a large enough sample size . To formalize this intuition, we denote the feasible region of problem (2) by

and derive bounds on the probability that any feasible solution to the SAA (2) violates the original chance constraint, which we refer to as the probability of infeasibility.

2.1 Finite

Before stating our main result of this section, we recall a known result providing an upper bound on the probability of infeasibility, as defined above, for sets of finite cardinality.

Theorem 1 ([3, Theorem 5])

Suppose that . Let . Then

where

denotes the cumulative distribution function of a binomial random variable with trials and success probability .

A similar upper bound using the finite cardinality assumption is also established in [16, Theorem 2].

2.2 Lipschitz Continuous

As argued in [3], it is possible to extend Theorem 1 to settings where the set is not finite by relying on the following regularity assumptions.

Assumption 1

There exists a constant such that for all and .

Assumption 2

There exists a constant such that .

Assumptions 1 and 2 ensure boundedness of the constraint function with respect to the optimization variable over the set . Using these assumptions, we provide a novel upper bound on the probability of infeasibility, which improves upon the previously best-known upper bound provided in [3, Theorem 10] under certain conditions.

Proof 2.1.

Let and . Since , it follows from Assumption 2 that there exists an -dimensional hypercube with edge length equal to that contains the set . Thus, there exists an internal -covering of the set that satisfies where denotes the closed -ball of radius centered at the point . It follows from classical internal-covering number bounds [17, Lemma 5.7] that Let for . It follows that

| (4) |

Note that for any , it holds that

| (5) |

The final inequality is a consequence of Assumption 1 and the facts that and , which together imply that

for all and . Therefore, for all and .

This implies that for all , which proves inequality (5). It also holds that

| (6) |

The equality follows from the fact is a binomial random variable with trials and a success probability . The inequality follows from , which is a consequence of . Combining inequalities (4), (5), (6), and the fact that , the desired result follows.

Remark 14 (Comparison to [3]).

The upper bound on the probability of infeasibility given in [3, Theorem 10] is

| (7) |

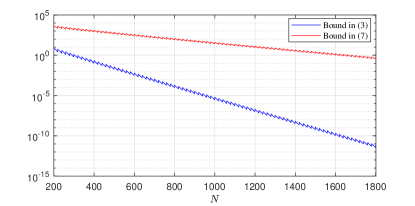

where is an additional parameter associated with the specific approach used in [3] to derive such upper bound. Since and for any , it is straightforward to see that the bound (3) provided in this paper strictly improves upon the bound (LABEL:eq:_Luedtke_bound) if the margin satisfies . In Figure 1, we provide a graphical comparison of the bounds, which shows that the bound (3) provided in this paper improves upon the bound (LABEL:eq:_Luedtke_bound) by many orders of magnitude for modest sample sizes .

3 Robust Sample Average Approximation in Nonstationary Environments

In this section, we consider a nonstationary variant of the SAA problem, where the random sample is drawn in a sequential fashion from an unknown distribution that may change over time as defined in Section 3.1. To account for the potential nonstationarity in the data-generating process, we propose a novel robust SAA in Section 3.2. Finally, in Sections 3.3 and 3.4, we establish upper bounds on the corresponding probability of infeasibility in terms of a target distribution that reflects the current state of the environment.

3.1 Nonstationary Data-Generation Model

We first introduce the nonstationary data-generation model considered in this paper. Specifically, the random sample is assumed to be independent but not necessarily identically distributed. We denote by the probability measure according to which the random variable is defined. All of the probability measures considered are defined on a common measurable space , where is the Borel sigma-algebra of Borel sets of . The set is also assumed to be a Polish space.

The dependence on time is captured by the index of each random variable , where larger indices correspond to more recently sampled data, and smaller indices correspond to older data. To constrain the temporal changes in the data-generating distribution over time, we employ the 1-Wasserstein metric, which is defined as follows.

Definition 16.

The 1-Wasserstein distance between two probability measures and on is defined as

| (8) |

where is a norm on , and denotes the set of all joint probability distributions of and with marginal distributions and , respectively.

Note that a joint distribution (coupling) that achieves the infimum in (8) is guaranteed to exist, as we have assumed that is a Polish space [18, Proposition 1.3]. The existence of such couplings will play an instrumental role in the proof of Lemma 18, which is a key building block in the derivation of the main results of this section.

Using the 1-Wasserstein metric, we constrain the allowable changes in the data-generating process according to

| (9) |

for all indices and , where is a known function satisfying . The function can be understood as a variation budget, limiting the extent to which the underlying data-generating distribution can change over a given span of time periods. It allows for a broad range of temporal shifts in the data-generating process, including gradual drifts over time, large but infrequent changes, or a combination thereof.

We note that, while our model uses the 1-Wasserstein metric, the results of this section also hold for alternative probability metrics/distances that imply the satisfaction of condition (9) under the 1-Wasserstein metric. We refer the reader to [19] for a survey of bounds relating different probability metrics/distances to the 1-Wasserstein metric.

3.2 Robust Sample Average Approximation

Given a random sample , we are interested in constructing a sample average approximation of the chance constrained feasible region defined in terms of the distribution of the ensuing -th random variable . We denote the corresponding feasible region by

where denotes the target constraint violation probability at a point under the target distribution . The target distribution should be understood as reflecting the current state of the environment. To account for the potential discrepancy between the sequence of sampling distributions and the target distribution , we consider a robust empirical estimate of the target constraint violation probability given by

where

| (10) |

denotes the intersection of and a closed norm-ball of radius centered at the sample for all . The radii of the norm-balls used in the above approximation are design parameters to be specified by the user. Using the above approximation of the target constraint violation probability, we define a robust sample average approximation of the feasible region as

| (11) |

Note that the robust SAA (11) reduces to the conventional SAA if the norm-ball radii are all equal to zero. If, on the other hand, the norm-balls have nonzero radii, then the robust SAA requires the satisfaction of at least of the robust sampled constraints given by

| (12) |

where can be interpreted as the uncertainty set associated with each constraint.

Naturally, the radii of uncertainty sets can be designed to compensate for the worst-case discrepancy between the sequence of sampling distributions and the target distribution . Intuitively, the target random variable will lie within the uncertainty set with high probability if its radius is sufficiently large. Building on this intuition, we prove the following result, which relates the robust constraint satisfaction probabilities to the target constraint satisfaction probability.

Lemma 18.

Let . For all , it holds that

Proof 3.1.

Let be a sequence of i.i.d. random variables, where each random variable in the sequence is identically distributed to . Also, for all , let each pair of random variables be coupled according to the joint distribution that attains the 1-Wasserstein distance between their respective distributions and . As we assume that is a Polish space, such an optimal coupling exists [18, Proposition 1.3]. This, together with (9), implies

By the law of total probability, we have that, for all and ,

where the second to last inequality follows from the application of Markov’s inequality. The last inequality follows from the facts that is identically distributed to and , completing the proof.

Before presenting the main result of this section, it is helpful to define the family of Poisson binomial random variables.

Definition 28.

A Poisson binomial random variable is defined as a finite sum , where are independent Bernoulli random variables with expectations . Its cumulative distribution function is given by where is the set of all subsets of of cardinality . We denote its cumulative distribution function by for .

3.3 Finite

The main result of this paper is given in Theorem 31, providing an upper bound on the probability of infeasibility for finite in nonstationary environments.

Theorem 31.

Suppose that . Then

where

for .

Proof 3.2.

Let . We have that

The final equality follows from the fact that is a Poisson binomial random variable. Specifically, it is the sum of independent Bernoulli random variables with heterogeneous success probabilities given by for . Note that, for all and , it holds that

The first inequality follows from Lemma 18 since . The second inequality follows from . Therefore,

for all and . The claim follows, as

Remark 41 (Choosing the Uncertainty Sets).

Each of the uncertainty sets specified in (10) is defined as a norm-ball intersected with the support set . An important consequence of this definition is that the feasible set of the robust SAA defined in (11) is guaranteed to contain the so-called robust feasible set associated with this problem, that is,

| (13) |

It follows from (13) that nonemptiness of the robust feasible set implies nonemptiness of the robust SAA feasible set. However, defining the uncertainty sets in this manner requires knowledge of the underlying support set. If this information is not available, then the uncertainty sets in (12) can be redefined as norm-balls without intersecting them with the support set. Although the resulting robust SAA will yield solutions that are potentially more conservative, the claim in Theorem 31 continues to hold true.

Remark 42 (Tractability of the Robust Approximation).

The robust sampled constraints defined in (12) admit computationally tractable reformulations for a large family of constraint functions and uncertainty sets. For example, if the constraint function is a bi-affine function of the form and the uncertainty sets can be described as convex polytopes (e.g., if is a convex polytope and is the or -norm), then each of the robust constraints in (12) can be reformulated as a finite collection of linear constraints. We refer the reader to [20] for a comprehensive discussion about the families of robust constraints that admit equivalent reformulations as tractable convex constraints.

Remark 43 (Choice of Radii).

Theorem 31 allows for flexibility in how to choose the uncertainty set radii. A natural choice is to let each radius be proportional to the Wasserstein distance between the sampling distribution and the target distribution , that is,

| (14) |

for some constant . We note that this choice of radii has an intuitive interpretation: older (less informative) samples are associated with uncertainty sets with larger radii to account for the greater potential discrepancy between their distributions and the target distribution. Therefore, it is natural to expect that robust constraints associated with older samples (larger uncertainty sets) are more likely to be discarded when solving the resulting robust SAA, as their exclusion will frequently result in the greatest enlargement of the feasible region . Note that for , at most constraints can be discarded.

By using Hoeffding’s inequality [21], one can upper bound the tail of the Poisson binomial distribution in Theorem 31 as

if . This upper bound can be used to characterize a distribution-free lower bound on the sample size needed to ensure that is contained within with a given confidence . Corollary 44 illustrates this procedure for the choice of radii given in (14).

Corollary 44.

Let , , and . If the uncertainty set radii are specified as for all and

| (15) |

then .

3.4 Lipschitz Continuous

In this section, we propose a slight modification of the robust SAA to address problems where the set may not be finite. We modify the approximation by incorporating a constraint tightening parameter as in Section 2.2. Using the modified approximation, we provide an upper bound on the probability of infeasibility that holds under Assumptions 1 and 2. The modified robust SAA of is defined as

where , , and

4 Conclusion

We investigate sample average approximations for chance constraints in both stationary and nonstationary environments. For stationary environments, we provide a new upper bound on the probability of infeasibility for the setting in which has possibly infinite cardinality. For nonstationary environments, we propose a robust SAA scheme in which each random sample encodes a robust sampled constraint defined in terms of an uncertainty set whose radius depends on the distributional uncertainty of the associated random sample. We derive upper bounds on the corresponding probability of infeasibility for this class of approximations.

References

- [1] S. Ahmed and A. Shapiro, “Solving chance-constrained stochastic programs via sampling and integer programming,” in State-of-the-Art Decision-Making Tools in the Information-Intensive Age. INFORMS, 2008, pp. 261–269.

- [2] J. Luedtke, S. Ahmed, and G. L. Nemhauser, “An integer programming approach for linear programs with probabilistic constraints,” Mathematical Programming, vol. 122, no. 2, pp. 247–272, 2010.

- [3] J. Luedtke and S. Ahmed, “A sample approximation approach for optimization with probabilistic constraints,” SIAM Journal on Optimization, vol. 19, no. 2, pp. 674–699, 2008.

- [4] M. C. Campi and S. Garatti, “The exact feasibility of randomized solutions of uncertain convex programs,” SIAM Journal on Optimization, vol. 19, no. 3, pp. 1211–1230, 2008.

- [5] G. Calafiore and M. Campi, “The scenario approach to robust control design,” IEEE Transactions on Automatic Control, vol. 51, no. 5, pp. 742–753, 2006.

- [6] G. Ditzler, M. Roveri, C. Alippi, and R. Polikar, “Learning in nonstationary environments: A survey,” IEEE Computational Intelligence Magazine, vol. 10, no. 4, pp. 12–25, 2015.

- [7] E. Delage and Y. Ye, “Distributionally robust optimization under moment uncertainty with application to data-driven problems,” Operations Research, vol. 58, no. 3, pp. 595–612, 2010.

- [8] W. Wiesemann, D. Kuhn, and M. Sim, “Distributionally robust convex optimization,” Operations Research, vol. 62, no. 6, pp. 1358–1376, 2014.

- [9] P. M. Esfahani and D. Kuhn, “Data-driven distributionally robust optimization using the wasserstein metric: Performance guarantees and tractable reformulations,” Mathematical Programming, vol. 171, no. 1, pp. 115–166, 2018.

- [10] Z. Hu and L. J. Hong, “Kullback-leibler divergence constrained distributionally robust optimization,” Available at Optimization Online, pp. 1695–1724, 2013.

- [11] A. Nemirovski and A. Shapiro, “Convex approximations of chance constrained programs,” SIAM Journal on Optimization, vol. 17, no. 4, pp. 969–996, 2007.

- [12] S.-H. Tseng, E. Bitar, and A. Tang, “Random convex approximations of ambiguous chance constrained programs,” in Proceedings of 55th IEEE Conference on Decision and Control. IEEE, 2016, pp. 6210–6215.

- [13] A. Shapiro, “Distributionally robust stochastic programming,” SIAM Journal on Optimization, vol. 27, no. 4, pp. 2258–2275, 2017.

- [14] E. Erdoğan and G. Iyengar, “Ambiguous chance constrained problems and robust optimization,” Mathematical Programming, vol. 107, no. 1-2, pp. 37–61, 2006.

- [15] G. C. Calafiore, “Random convex programs,” SIAM Journal on Optimization, vol. 20, no. 6, pp. 3427–3464, 2010.

- [16] T. Alamo, R. Tempo, A. Luque, and D. R. Ramirez, “Randomized methods for design of uncertain systems: Sample complexity and sequential algorithms,” Automatica, vol. 52, pp. 160–172, 2015.

- [17] M. J. Wainwright, High-Dimensional Statistics: A Non-Asymptotic Viewpoint, ser. Cambridge Series in Statistical and Probabilistic Mathematics. Cambridge University Press, 2019.

- [18] F.-Y. Wang, “Coupling and applications,” in Stochastic Analysis and Applications to Finance: Essays in Honour of Jia-an Yan. World Scientific, 2012, pp. 411–424.

- [19] A. L. Gibbs and F. E. Su, “On choosing and bounding probability metrics,” International statistical review, vol. 70, no. 3, pp. 419–435, 2002.

- [20] D. Bertsimas, D. B. Brown, and C. Caramanis, “Theory and applications of robust optimization,” SIAM review, vol. 53, no. 3, pp. 464–501, 2011.

- [21] W. Hoeffding, “Probability inequalities for sums of bounded random variables,” Journal of the American Statistical Association, vol. 58, no. 301, pp. 13–30, 1963.