SDEs with no strong solution arising from a problem of stochastic control

Abstract.

We study a two-dimensional stochastic differential equation that has a unique weak solution but no strong solution. We show that this SDE shares notable properties with Tsirelson’s example of a one-dimensional SDE with no strong solution. In contrast to Tsirelson’s equation, which has a non-Markovian drift, we consider a strong Markov martingale with Markovian diffusion coefficient. We show that there is no strong solution of the SDE and that the natural filtration of the weak solution is generated by a Brownian motion. We also discuss an application of our results to a stochastic control problem for martingales with fixed quadratic variation in a radially symmetric environment.

The authors are grateful to the anonymous referee, whose comments led to strengthening the main results of this article.

1. Introduction

In this paper, we study the following two-dimensional SDE with Markovian diffusion coefficient, started from the origin. Let be a real-valued Brownian motion and consider the SDE

| (1.1) |

where we denote . It is shown by Larsson and Ruf in [10] that the SDE (1.1) has a weak solution. Here we show that there does not exist a strong solution of (1.1). Moreover, we show that uniqueness in law holds for (1.1) and that the weak solution shares notable properties with Tsirelson’s example of an SDE with no strong solution given in [20]. In particular, the natural filtration of the weak solution is generated by a Brownian motion, which implies that the initial sigma-algebra is trivial. We also show that the angle process of the solution is independent of its increments and deduce that it is independent of the driving Brownian motion. Together, these properties imply that the filtration generated by the weak solution at any positive time contains some additional information not present at time zero. This remarkable property of Tsirelson’s equation is emphasised by Rogers and Williams in [17, V.18].

Tsirelson’s example is a one-dimensional SDE with path-dependent drift. A result of Zvonkin [26] shows that this path dependence is necessary; for a one-dimensional SDE of the form , with bounded and measurable, a strong solution always exists. In contrast to Tsirelson’s example, the SDE (1.1) that we study defines a two-dimensional martingale, and the diffusion coefficient is Markovian.

We will show that the weak solution of (1.1) generates a Brownian filtration, by making use of a connection with circular Brownian motion. We take inspiration from the paper [6], in which Émery and Schachermayer showed that a weak solution of Tsirelson’s equation generates a Brownian filtration, by constructing a bijection with a circular Brownian motion.

In [3], we studied a control problem for martingales with a fixed quadratic variation, for which we can explicitly identify the value function and the optimal controls. Under certain conditions, the weak solution of (1.1) is optimal. However, under a particular growth condition on the cost function, the question of whether weak and strong versions of the control problem coincide is left open. In this paper, we will show that such problems are in fact equivalent, and that the cost induced by the weak solution of (1.1) attains the strong value function.

1.1. Main results

The main contribution of this paper is to present an SDE for a martingale with Markovian diffusion coefficient, which has no strong solution and shares many interesting properties with Tsirelson’s path-dependent one-dimensional example from [20].

Theorem 1.1.

There exists a unique (in law) weak solution of the SDE (1.1), but there is no strong solution. Moreover,

-

the process generates a Brownian filtration;

-

after a deterministic time-change, the angle process of is uniformly distributed and independent of the driving Brownian motion;

-

taking the supremum of the natural filtration of at any time and the sigma-algebra generated by the angle process of at any time recovers the natural filtration of at time ;

-

the process is a strong Markov process.

We further obtain a result on non-existence of strong solutions of the following SDEs, whose behaviour approximates that of solutions of the SDE (1.1). Let be a one-dimensional Brownian motion and let be a fixed constant. Consider the two-dimensional SDE

| (1.2) |

Theorem 1.2.

We will also show that, after a deterministic time change, the radius of the weak solution of (1.2) is a -dimensional Bessel process.

1.2. SDEs with no strong solution in the literature

We begin by recalling the properties of two classical examples of SDEs with no strong solution, which will be instructive for the study of the SDE (1.1). We emphasise the significance of Tsirelson’s example in Section 1.2.2. For further instructive examples, see [2, Section 1.3].

1.2.1. Tanaka’s example

A well-known example of an SDE with no strong solution is Tanaka’s SDE, which is the following one-dimensional equation:

| (1.3) |

The SDE (1.3) admits a unique (in law) weak solution but no strong solution. The proof of this can be found, for example, in Example 3.5 of [9, Chapter 5].

To prove that there is no strong solution, the key idea is to show, using the Itô-Tanaka formula, that the inclusion

| (1.4) |

holds for all . Then it is impossible for to be adapted to , since for all .

In order to prove Theorem 1.1, we show similar inclusions to the ones above, where the increments of the solution of the SDE (1.1) play the role of the absolute value of the solution of Tanaka’s SDE.

1.2.2. Tsirelson’s example

In his 1976 paper [20], Tsirelson introduced the following notable example of an SDE with no strong solution, but for which weak existence and uniqueness in law holds. Tsirelson’s example is the one-dimensional equation

| (1.5) |

with initial condition , where is chosen as follows.

Fix a decreasing sequence such that and . Denote the increments of and by and , respectively, and define

| (1.6) |

At time , for some , is the fractional part of .

The weak solution of the SDE (1.5) has the following properties, as proved, for example, in Theorem 18.3 of [17, Chapter V]:

-

(T1)

At any time , the natural filtration of the solution has the decomposition

(1.7) -

(T2)

For each , is uniformly distributed on and independent of ;

-

(T3)

The sigma-algebra is trivial.

Note that the drift term (1.6) in Tsirelson’s SDE depends on the history of the process . As remarked in [17, Chapter V], for bounded drifts depending only on the current value of the process, Zvonkin proved in [26] that a strong solution of (1.5) always exists. Therefore the path-dependence of the drift is necessary for strong existence to fail. We emphasise that, in contrast to Tsirelson’s SDE (1.5), the two-dimensional SDE (1.1) defines a martingale with Markovian diffusion coefficient. Nevertheless, we will show that (1.1) exhibits similar properties to (T1), (T2) and (T3) above.

1.3. Brownian filtrations and circular Brownian motion

A natural question that arises when considering continuous-time stochastic processes is whether the natural filtration of a process is generated by a Brownian motion. In Proposition 2 of [6], Émery and Schachermayer define a Brownian filtration as follows.

Definition 1.3 (Brownian filtration).

A filtration is called Brownian if it is the natural filtration of a real-valued Brownian motion starting from the origin.

Note that this definition agrees with the definition of a strong Brownian filtration given in Mansuy and Yor’s book [13, Definition 6.1].

In the case of Tanaka’s SDE (1.3), any weak solution is a Brownian motion, as discussed in Example 3.5 of [9, Chapter 5], and so in this case a weak solution trivially generates a Brownian filtration. For Tsirelson’s example, this question remained open until the work of Émery and Schachermayer in 1999 [6], in which they showed that the solution of Tsirelson’s equation does indeed generate a Brownian filtration.

In [4], Dubins, Feldman, Smorodinsky and Tsirelson settled an open question by presenting an example of a process that does not generate a Brownian filtration. Their proof relies on the concept of standardness, an invariant of filtrations first introduced by Vershik in the setting of ergodic theory in his doctoral thesis [22].

Another example of a process that does not generate a Brownian filtration is the diffusion that Walsh defined in [24], now known as Walsh’s Brownian motion. In [21], Tsirelson proved that Walsh’s Brownian motion does not generate a Brownian filtration, by introducing a new invariant of filtrations known as cosiness. Warren later used the same technique in [25] to prove that sticky Brownian motion also does not generate a Brownian filtration. In [7], Émery and Schachermayer provide a discussion of the relationship between the two invariants standardness and cosiness, along with further references to examples of their application.

In order to prove that the solution of Tsirelson’s equation generates a Brownian filtration, neither of these invariants are used. Rather, in [6], Émery and Schachermayer show that there is an isomorphism between the solution of Tsirelson’s equation and an eternal Brownian motion on the circle, which they call circular Brownian motion and define as follows.

Definition 1.4 (circular Brownian motion).

Let be a continuous -valued process. For any with , denote by the -valued random variable that depends continuously on , vanishes for , and satisfies

| (1.8) |

Let be a filtration. We say that is a circular Brownian motion for if is adapted to and, for each , the process

| (1.9) |

is a standard Brownian motion for the filtration .

Proposition 3 of [6] shows that any deterministic time-change of a circular Brownian motion generates a Brownian filtration. The proof uses the notion of chopped Brownian motion and a coupling argument.

In this work, we show that the angle process of the weak solution of the SDE (1.1) is a deterministic time-change of a circular Brownian motion, thus relating this SDE to Tsirelson’s example. We frequently make use of the connection to circular Brownian motion and the results of [6] to show that the SDE (1.1) has no strong solution and that the weak solution generates a Brownian filtration.

Having shown that the weak solution of (1.1) generates a Brownian filtration, an immediate consequence will be that the initial sigma-algebra is trivial. Therefore, for any fixed , . On the other hand, for any , we will show that . Since is not a strong solution, . In fact, we have the strict inclusion

| (1.10) |

Exchanging the order of taking intersections and suprema of sigma-algebras are discussed in detail by von Weizsäcker in [23]. The inclusion above holds in general, and von Weizsäcker gives conditions under which there is equality. Both the SDE (1.1) that we study in this paper and Tsirelson’s example (1.5) give continuous-time counterexamples, for which von Weizsäcker’s conditions are not satisfied and the inclusion is strict. A related discrete-time counterexample is given in [23].

1.4. Application to a control problem

In the paper [3], we study the following control problem. We seek the value

| (1.11) |

where the infimum is taken over a set of martingales with fixed quadratic variation, stopped on exiting a ball in , and the value function is radially symmetric. The main result of [3] is that there is a closed form expression for the value function, and that an optimal control is to switch between two regimes. The first of these regimes is a one-dimensional Brownian motion on a radial line, while the second is a weak solution of the SDE (1.1). In [3] we call the behaviour of solutions of (1.1) tangential motion, since such a process moves on a tangent to its current position. The remarkable property of this process is that it is a two-dimensional martingale whose radius is deterministically increasing. In particular, for a cost function that is radially decreasing, we show that tangential motion is optimal. In general, we identify optimal controls only in a weak sense, but we show that weak and strong formulations of the control problem coincide, similarly to the results of [5]. However, when weak solutions of (1.1) are optimal, under a particular growth condition on the cost function, the question of equality between weak and strong value functions is left open in [3]. In Section 4 of the present paper we settle this question, showing that the value functions are in fact equal. Since the weak solution of the SDE (1.1) generates a Brownian filtration, we can argue by isomorphism that there is a strong control that attains the same value as the optimal weak control.

1.5. Organisation of the article

In Section 2, we state and prove our main result Theorem 2.1 on solutions of the SDE (1.1). We start by introducing circular Brownian motion and discussing its properties in Section 2.1. The relation between circular Brownian motion and the SDE (1.1) then leads us to show that the weak solution of (1.1) generates a Brownian filtration, among other notable properties. In Section 2.2, we conclude that there exists no strong solution of (1.1).

Section 3 treats the class of SDEs of the form (1.2). We show that (1.2) has similar properties to (1.1) and, in Theorem 3.1, we prove that (1.2) has no strong solution.

In Section 4, we apply Theorem 2.1 to the control problem studied in [3]. In Section 4.1, we extend the main result of [3], by proving Theorem 4.1. In Section 4.2, we discuss an open question on optimality of feedback controls.

Throughout the paper, all filtrations are assumed to satisfy the usual conditions, and the following notation will be used. For a stochastic process , its natural filtration augmented to satisfy the usual conditions is denoted . The quadratic variation of a process is denoted . The sigma-algebra generated by a random variable is denoted .

2. An SDE with no strong solution

Let be a real-valued Brownian motion and consider the two-dimensional SDE

| (2.1) |

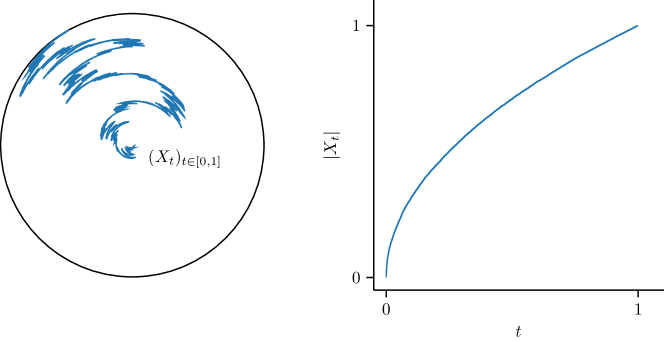

By [10], the SDE (2.1) has a weak solution. A simulation of such a solution is shown in Figure 1. The main result of the present paper is that the SDE (2.1) has no strong solution and, furthermore, that a weak solution exhibits many of the same properties as Tsirelson’s famous example (1.5) from [20], including uniqueness in law. It is notable that our two-dimensional example is a strong Markov martingale with Markovian diffusion coefficient, in contrast to Tsirelson’s one-dimensional SDE which has a non-Markovian drift.

We now state the main result concerning solutions of the SDE (2.1). This is a more precise restatement of Theorem 1.1

Theorem 2.1.

There exists a weak solution but no strong solution of the SDE (2.1). Moreover, uniqueness in law holds and the weak solution of (2.1) has the following properties:

-

(S1)

The natural filtration is generated by a Brownian motion; in particular, the initial sigma-algebra is trivial;

-

(S2)

For any , the value of the time-changed angle process is uniformly distributed on and independent of ;

-

(S3)

For any , the natural filtration of at time can be decomposed as , for any ;

-

(S4)

The process is a strong Markov process.

The existence of a weak solution of (2.1) is proved by Larsson and Ruf in Theorem 4.3 of [10]. We will now investigate the properties of such a weak solution and conclude that there exists no strong solution.

2.1. Properties of weak solutions

The key observation in our proof of Theorem 2.1 is that the angle process of any solution of the SDE (2.1) is a deterministic time-change of a circular Brownian motion, as defined in Definition 1.4.

We now state two properties of circular Brownian motion that are proved in [6]. For a circular Brownian motion , define the innovation filtration to be the filtration generated by the increments of ; i.e.

| (2.2) |

Then Proposition 1 of [6] states that, for any ,

-

(C1)

is uniformly distributed;

-

(C2)

is independent of .

We note the parallel between properties (C1) and (C2) of circular Brownian motion and the property (T2) of Tsirelson’s equation (1.5) stated in Section 1.2.2.

Next, we show how a circular Brownian motion arises in our example.

Lemma 2.2.

There exists a weak solution of the SDE (2.1), and any such solution satisfies

| (2.3) |

where is a -valued process satisfying

| (2.4) |

In particular, the radius of is given by the deterministically increasing function , for .

Proof.

The existence of a weak solution of the SDE (2.1) is given by [10, Theorem 4.3]. By Itô’s formula, for , we find that (c.f. [3, Lemma 3.1, Lemma 3.4]). Now, for , we can write the -valued random variable as

| (2.5) |

for a -valued random variable . Applying Itô’s formula once again, we see that the process satisfies (2.4). ∎

We call the process given in Lemma 2.2 the angle process of the solution . We now show that this angle process is a circular Brownian motion, up to a time-change. We define a regular time-change as in [6].

Definition 2.3.

A function is a regular time-change if is an increasing absolutely continuous bijection with absolutely continuous inverse.

Proposition 2.4.

Let be a weak solution of the SDE (2.1). Then the associated angle process is a regular time-change of a circular Brownian motion. Moreover, for any , the angle process is distributed as , independently of .

Proof.

Define the function by , . Then is a regular time-change. Define the time-changed process

| (2.6) |

Since, for any , there is a one-to-one deterministic correspondence between and , the angle process is adapted to . Now define the time-changed filtration

| (2.7) |

We will show that is a circular Brownian motion for .

Since is a regular time-change, is adapted to . We also see that the -valued process is continuous. Now fix and consider the process

| (2.8) |

Since is an -Brownian motion and is a regular time-change, we have that

| (2.9) |

is a -martingale, with quadratic variation

| (2.10) |

and so

| (2.11) |

is a continuous -martingale. We can calculate the quadratic variation

| (2.12) |

since , for any .

Therefore, by Lévy’s characterisation of Brownian motion, the process

| (2.13) |

is an -Brownian motion. Hence is a circular Brownian motion for . It follows from properties of circular Brownian motion proved in Proposition 1 of [6] that, for any , is independent of and uniformly distributed on . ∎

Corollary 2.5.

Uniqueness in law holds for the SDE (2.1).

Proof.

Let and be weak solutions of the SDE (2.1) and write , for the angle processes of , , respectively, given in Lemma 2.2. By Proposition 2.4, each angle process is a regular time-change of a circular Brownian motion. As remarked in [6], any circular Brownian motion has the same law, as a consequence of the uniformity and independence properties shown in [6, Proposition 1]. Hence . By Lemma 2.2, (resp. ) is a deterministic function of (resp. ), for , and so it follows that . ∎

A key contribution of Émery and Schachermayer’s paper [6] is to show that solutions of Tsirelson’s equation generate a Brownian filtration. As discussed in Section 1.3, this is done as follows. In Proposition 4 of [6], the authors show that there is an isomorphism between solutions of Tsirelson’s equation and circular Brownian motion, and in Proposition 3 of [6], they prove that a regular time-change of a circular Brownian motion generates a Brownian filtration. It is this latter property that we exploit here, having already shown a connection between solutions of (2.1) and circular Brownian motion in Proposition 2.4.

Corollary 2.6.

Let be a weak solution of the SDE (2.1). Then generates a Brownian filtration.

Proof.

Write

| (2.14) |

where is the angle process of the solution, and let be the filtration generated by . Then, since is fixed, and is a deterministic bijective function of for each , we have

| (2.15) |

where is the filtration generated by .

We have seen in Proposition 2.4 that is a regular time-change of a circular Brownian motion. Propositions 2 and 3 of [6] together immediately imply that the natural filtration of any regular time-change of a circular Brownian motion is Brownian. Hence is Brownian, and it follows that is Brownian. ∎

In the next section, we will show that the SDE (2.1) has no strong solution, and so the Brownian motion that generates the natural filtration of a weak solution cannot be the driving Brownian motion of the SDE.

2.2. Non-existence of strong solutions

The proof of non-existence of a strong solution in Theorem 2.1 relies on the following property of the angle process that arises from the theory of circular Brownian motion discussed in Section 2.1.

Lemma 2.7.

Let be a real-valued Brownian motion with natural filtration and let be an -valued process. Suppose that satisfies

| (2.16) |

where the random variables on the left-hand side are defined analogously to those in Definition 1.4.

Then cannot be adapted to .

Proof.

Suppose for contradiction that is adapted to the natural filtration of .

Define the regular time-change by for all , as in the proof of Proposition 2.4, and denote the time-changed processes

Since the time-change is deterministic, the natural filtrations and of the time-changed processes and are given by

| (2.17) |

Hence is adapted to .

By the same arugments as in the proof of Proposition 2.4, is a circular Brownian motion for and, for any with ,

| (2.18) |

To arrive at a contradiction, we will exploit a property of circular Brownian motion that is proved in Proposition 1 of [6].

Let be the innovation filtration of . Recall that, for each , is the sigma-algebra generated by the increments of up to time ; i.e.

| (2.19) |

Then we have

| (2.20) |

In fact, the first inclusion must be strict, as we now show. As remarked in Section 2.1, Proposition 1 of [6] tells us that, for each , the value of the circular Brownian motion is uniformly distributed on and, moreover, is independent of . Hence, for each ,

| (2.21) |

Now, taking the limit as , almost surely, and so is -measurable. This implies that

| (2.23) |

contradicting the strict inclusion in (2.21). ∎

We are now ready to prove Theorem 2.1, showing in particular that the SDE (2.1) has no strong solution.

Proof of Theorem 2.1.

As noted after the statement of the theorem, the existence of a weak solution is proved by Larsson and Ruf in Theorem 4.3 of [10]. We prove uniqueness in law in Corollary 2.5. By Corollary 2.6, a weak solution generates a Brownian filtration, and by Blumenthal’s zero-one law, the initial sigma-algebra is trivial. The uniform distribution of the time-changed angle process and its independence from its increments are shown in Proposition 2.4. It remains to prove that statements (S3) and (S4) of the theorem hold, and that there does not exist a strong solution. We now check statement (S3) of the theorem.

Let be a weak solution of (2.1), write for the angle process, and recall that . We are in the setting of Lemma 2.7 and so, similarly to the proof of the lemma, we find that . Clearly, for any , , and so we also have the inclusion . On the other hand, writing

| (2.24) |

we see that , and we conclude that .

To verify the strong Markov property, statement (S4) of the theorem, we first observe that the Markov property at time zero together with the strong Markov property on for all implies the strong Markov property on (see e.g. [14, Lemma A.2]). Fix . By Lemma 2.2, the radius of the weak solution is given by the deterministically increasing function , and so we have for . The diffusion coefficient of the SDE (2.1) is Lipschitz on the set , and so we can follow standard arguments (c.f. [12, Theorem 8.3]) to show that the weak solution is in fact strong on . This implies that the strong Markov property holds on , by [12, Corollary 8.8]. Moreover, the Markov property at time zero follows immediately from the fact that the initial sigma-algebra is trivial. We conclude that is a strong Markov process.

To conclude the proof of Theorem 2.1 it remains to show non-existence of strong solutions. Suppose for contradiction that is a strong solution of the SDE (2.1). Then is adapted to the filtration ; i.e

| (2.25) |

Then, since the angle process satisfies (2.4), we have

| (2.26) |

for any . Therefore, by Lemma 2.7, is not adapted to . We have already seen in the proof of Corollary 2.6 that

| (2.27) |

Therefore is not adapted to . This contradicts the inclusion (2.25). Hence the SDE (2.1) has no strong solution. ∎

Remark 2.8.

Recalling Corollary 2.6, we have shown that, although the SDE (2.1) has no strong solution, there exists a unique (in law) weak solution, which generates a Brownian filtration. As discussed in Section 1.3, this places our example into the more common class of SDEs whose weak solutions are not strong but do generate a Brownian filtration, as is the case for the examples of Tanaka and Tsirelson.

3. Approximating SDEs have no strong solution

In this section, we consider a class of SDEs whose behaviour approximates that of the SDE (2.1) studied in Section 2. We show that such SDEs exhibit similar properites to the SDE (2.1) and that there do not exist strong solutions. In Section 4 we will relate these SDEs and the SDE (2.1) to a control problem for two-dimensional martingales that is studied in [3]. In particular, as remarked after Proposition 4.6, the non-existence of strong solutions gives an insight into the problem of optimising over feedback controls — see Section 4.2. The main result of this section is the following restatement of Theorem 1.2.

Theorem 3.1.

Let be a one-dimensional Brownian motion and let be a fixed constant. Then there exists no strong solution of the SDE

| (3.1) |

Uniqueness in law holds for (3.1) on the time interval , where .

We first observe that the squared radius process of a solution of (3.1) can be rescaled to a squared Bessel process, as defined in Definition 1.1 of [15, Chapter XI]. We will show that the event of returning to the origin before leaving the domain satisfies the following zero-one law. For , returns to the origin with probability zero; for , returns to the origin with probability one. The critical value corresponds to the -dimensional squared Bessel process, which has the same law as the squared radius process of a -dimensional Brownian motion. This remark plays an important role in the study of uniqueness of multi-dimensional martingales with given marginals in [14].

Proposition 3.2.

Let and suppose that solves the SDE (3.1). Write for any and define the rescaled process by .

Then is the square of a -dimensional Bessel process started from , where . Moreover, defining , we have

| (3.2) |

Proof.

Applying Itô’s formula, we see that satisfies

| (3.3) |

with . Note that

| (3.4) |

is a standard Brownian motion. Therefore, for any ,

| (3.5) |

Set . Then, referring to Definition 1.1 of [15, Chapter XI], we see that is the square of a -dimensional Bessel process.

Now suppose that , so that

| (3.6) |

The discussion that immediately precedes Proposition 1.5 in [15, Chapter XI] tells us that the set is polar for . By the definition of a polar set given in Definition 2.6 of [15, Chapter V], we have that almost surely never returns to the origin in finite time, and the rescaled process has the same property.

On the other hand, suppose that . Then

| (3.7) |

and so, by the same discussion in [15, Chapter XI], returns to the origin in finite time with probability . Again the rescaled process has the same property. ∎

Remark 3.3.

Define the process by , for . Since is the square of a -dimensional Bessel process, we have that is a Bessel process (see [15, Definition XI.1.9]). Rescaling the SDE for the Bessel process (see [1, Eq. (4)]), we see that satisfies

| (3.8) |

By [1, Theorem 3.2 (i)], is the unique non-negative solution of (3.8) and it is a strong solution.

Suppose that . By Proposition 3.2, almost surely never returns to the origin after time , and so pathwise uniqueness holds after time , by [1, Theorem 3.2 (ii)]. On the other hand, suppose that . Then [1, Theorem 3.2 (iii)] shows that even uniqueness in law does not hold, and by Proposition 3.2 returns to the origin almost surely in finite time. Inspecting the proof of [1, Theorem 3.2], we see that pathwise uniqueness for (3.8) holds after time up to the first hitting time of the origin. We will therefore only consider the SDE (3.8) up to the hitting time , as defined in Proposition 3.2, in this case.

We now turn to the proof of Theorem 3.1, where we show that there do not exist strong solutions of (3.1), following a similar strategy to the proof of Theorem 2.1. Here, the angle process of a solution of (3.1) is no longer a circular Brownian motion, as was the case for solutions of (2.1) in Proposition 2.4. However, this process does have similar properties. We will show that, conditioned on the value of the radius, the angle process is uniformly distributed and independent of its increments. Here, we adapt Émery and Schachermayer’s proof that the value of a circular Brownian motion at any time is uniformly distributed and independent of its increments, from Proposition 1 of [6]. We will deduce the result of Theorem 3.1 from the following proposition.

Proposition 3.4.

Fix . For any weak solution of the SDE (3.1), let be the radius process and the angle process, so that we can write

| (3.10) |

Denote the hitting times of by

| (3.11) |

Then, for any with ,

| (3.12) |

Moreover, is independent of

| (3.13) |

The above result relies in turn on the following technical lemma, which guarantees that the increments of the angle process at the hitting times of the radius process do not have a lattice distribution.

Lemma 3.5.

Let be the angle process defined in Proposition 3.4 and fix such that . Then, for any ,

| (3.14) |

Proof.

Suppose for contradiction that there exists such that

| (3.15) |

Let be the radius process and the angle process, as defined in Proposition 3.4, and recall that and satisfy the SDEs (3.8) and (3.9), respectively.

We will use a coupling argument to arrive at a contradiction. Consider two independent weak solutions , of the SDEs (3.8) and (3.9) on a common probability space. For and any , denote the hitting time

| (3.16) |

Note that, as we observed in Remark 3.3, given the value of at radius , the process is uniquely defined via the SDE (3.9) up to the first return to the origin.

Fix such that , and shift and to define

| (3.17) |

Then, at the first hitting time of radius , the values of the processes and are almost surely equal to and , respectively, and these shifted processes still satisfy the SDE (3.9).

Suppose that there exists some radius such that

| (3.18) |

Then we can couple the two processes as follows. Define by

| (3.19) |

Then we see that the trajectories of and coincide on the set . Moreover, by the Markov property, the process still satisfies the SDE (3.9). Therefore, by condition (3.15),

But, by our choice of , the above values are not equal, contradicting the coupling of the trajectories. This shows that, on the set , the supports of and must be disjoint.

Since our choice of the shifts and was arbitrary, the only feasible supports of are the rays connecting the points and , for . This would imply that and are deterministic, but this is not the case for .

Hence there is no such that (3.15) holds. ∎

We now use this lemma to prove Proposition 3.4 on the uniformity and independence properties of the angle process.

Proof of Proposition 3.4.

Fix such that . We show that is uniformly distributed on by using the characteristic function of the random variable on the torus, following the proof of Proposition 1 of [6]. For any and , define the characteristic function

| (3.20) |

Fix and with . We aim to show that .

Let . Then, writing

| (3.21) |

and denoting by the expectation with respect to the given probability measure , we have

In order to break up the expectation on the right hand side into the product of expectations, we use the following conditional independence. We see that future increments of depend only on the history of through the current value of , since is Markovian. That is, for any ,

| (3.22) |

Now note that, taking , the -algebra is trivial, and so future increments of are independent of , without any conditioning. Hence

| (3.23) |

We will now consider the increment . We claim that, for small radii , the value of this increment approaches a uniform distribution on . We show this by using a scaling argument, as follows.

Fix and rescale time by defining for . Then, for , define

| (3.24) |

so that

| (3.25) |

We can calculate

and

And so, after this rescaling, and satisfy the same SDEs (3.8) and (3.9) as and .

For , let be the first time that the process hits , having started from the origin. Then we have the following equality in distribution:

| (3.26) |

where the first equality holds pointwise by rescaling, and the second equality holds in distribution because the rescaled processes satisfy the same SDEs as the original processes.

Moreover, recalling our observation that increments of between hitting times of are independent, we see that the increments

| (3.27) |

are independent and identically distributed when .

Now let and set . We can write the increment of as a sum of i.i.d. random variables

| (3.28) |

and so

| (3.29) |

By Jensen’s inequality,

| (3.30) |

with equality if and only if there exists such that

| (3.31) |

By Lemma 3.5, no such exists, and so the inequality (3.30) is strict. We then have that

| (3.32) |

Returning to our calculation of the characteristic function of in (3.23), we have

Hence is uniformly distributed on .

We now show that is independent of , the sigma-algebra generated by all increments of .

Let be a strictly positive decreasing sequence with . For each , define

| (3.33) |

the sigma-algebra generated by all increments of after the first hitting time of .

Recalling that we are working with filtrations that satisfy the usual conditions, we have that , since almost surely as . Therefore, by martingale convergence (see e.g. Theorem 4.3 of [18, Chapter VII]),

| (3.34) |

in and almost surely.

We now fix and consider

By the same conditional independence arguments as we used in the proof of uniformity, is independent of . Since pointwise, is -measurable. Therefore

by the uniformity of .

Hence

| (3.35) |

and so, by martingale convergence,

| (3.36) |

Taking to be any bounded -measurable random variable, we then have

| (3.37) |

Hence is independent of . ∎

The following uniqueness result is an immediate corollary of Proposition 3.4.

Corollary 3.6.

Uniqueness in law holds for (3.1) up to the first hitting time of the origin.

Proof.

Given a pair of processes satisfying (3.1), write and for the radius and angle processes of , respectively. Then, as shown in Remark 3.3, is the unique non-negative solution of (3.8). Recall the notation for . Then, by Remark 3.3 again, (3.9) uniquely determines the path of , given the value of for some with . Moreover, we have , by Proposition 3.4, and so the law of is unique. Uniqueness in law for (3.1) on now follows. ∎

We now apply the independence result of Proposition 3.4 to conclude that the SDE (3.1) has no strong solution.

Proof of Theorem 3.1.

The statement on uniqueness in law is proved in Corollary 3.6. Now suppose that is a strong solution of the SDE (3.1). Then there is an -valued -adapted process satisfying the SDE (3.8) with , and an -valued -adapted process satisfying the SDE (3.9) such that

| (3.38) |

Recall the definition

| (3.39) |

and fix such that . Then, by Proposition 3.4, is independent of .

Under our assumption that is adapted to , this implies that

| (3.40) |

However, we claim that is adapted to .

To prove this claim, observe that, for any , the random variable

| (3.41) |

is -measurable. Since almost surely for , as we proved in Proposition 3.2, is also -measurable.

4. Application to a problem of stochastic control of martingales

We now apply the result of Theorem 2.1 to the control problem studied in [3]. In [3], we find the value function for a -dimensional control problem with radially symmetric running cost , under mild regularity assumptions, including that is continuous away from the origin. We reformulate the control problem here as follows.

Fix , , and define the domain . Also define the set of matrices . The strong control problem is to find the value function , given by

| (4.1) |

where is the set of progressively measurable -valued process, and for , and . There is a corresponding weak version of the control problem, to find the weak value function , where we optimise over solutions of martingale problems, rather than stochastic integrals.

In dimension , the result [3, Theorem 5.12] does not treat the strong control problem at the origin under the condition that but for all . We will apply Theorem 2.1 to extend the result to this case.

We recall the definition of the candidate value function from [3, Definition 4.6]. For and , introduce the constant

| (4.2) |

and consider the following two cases. If is increasing in , then set , define by

and let be such that . For , define

If is decreasing in , then set , define by

and let be such that . For , define

Note in particular that, in the case that is decreasing on the interval , satisfies

| (4.3) |

for any with .

The generalisation of [3, Theorem 5.12] is the following.

Theorem 4.1.

Suppose that is continuous on and monotone on some interval , and that the one-sided derivative exists for all and changes sign only finitely many times. Then

| (4.4) |

In [3] we show that the weak value function has the form given in Theorem 4.1. Moreover, we show that except possibly in the two-dimensional case at the origin when

| (4.5) |

To conclude the proof of Theorem 4.1 we will now show that under the above conditions.

4.1. Equivalence of weak and strong control problems

Fix a probability space on which a -valued Brownian motion is defined with natural filtration . We know that there exists a weak solution of (2.1) by Theorem 4.3 of [10]. For , we can calculate that

| (4.6) |

We will show that there exists an -martingale that is equal in law to . This is the key step required to complete the proof of Theorem 4.1.

We will make use of the notion of isomorphisms between filtered probability spaces in the following proof. We take the following definitions from the paper [7] of Émery and Schachermayer.

Definition 4.2 (Isomorphism).

Given a probability space , denote the set of random variables on that probability space by . An embedding of into another probability space is a map

| (4.7) |

that commutes with Borel operations on random variables and preserves probability laws.

An isomorphism from to is an embedding that is bijective.

Remark 4.3.

We follow the same convention as in [11] and also write for the map in the above definition acting on sigma-algebras, stochastic processes and filtrations.

Definition 4.4.

Two filtered probability spaces and , with and , are isomorphic if there exists an isomorphism

| (4.8) |

such that .

In [11], Laurent gives similar definitions to the above for filtrations in discrete negative time. We will refer to results from [11] in the following proof.

Proof of Theorem 4.1.

It is shown in [3, Theorem 5.12] that the conclusion of the theorem holds in all cases except in dimension at the origin, under the conditions

| (4.9) |

In this case, [3, Lemma 5.11] shows that . We now prove that , thus completing the proof of the theorem.

Fix a probability space on which a -valued Brownian motion is defined with natural filtration , and recall the definition of the control set given above. We will construct an -martingale such that, for any ,

| (4.10) |

for some , and

| (4.11) |

By Theorem 2.1, there exists a unique (in law) weak solution of the SDE (2.1) and that the process generates a Brownian filtration. That is, there exists a Brownian motion on the probability space with natural filtration such that the natural filtration of is equal to .

Since and are both -valued Brownian motions, they have have the same law and so, as noted in Section 1.6 of [11], the filtered probability spaces

| (4.12) |

are isomorphic, as defined in Definition 4.4. That is, there exists an isomorphism

| (4.13) |

as defined in Definition 4.2, such that

| (4.14) |

Now define a process on the probability space by

| (4.15) |

For any , we have that and is an isomorphism, as noted after the definition of an isomorphism in [7]. Therefore, since is adapted to , it follows that is adapted to .

Now fix . Then, using Lemma 5.3 of [11] to apply the isomorphism to a conditional expectation, we see that

where the third equality follows from the fact that is an -martingale. Hence is an -martingale. By the definition of an isomorphism in Definition 4.2, we also have that the processes and are equal in law.

We now apply the martingale representation theorem, as found for example in Theorem 3.4 of [15, Chapter 5]. This result implies that is continuous and there exists an -progressively measurable -valued process such that, for any , we have the representation

| (4.16) |

We can also deduce that has quadratic variation , as follows. The quadratic variation of is , and so is an -martingale. Using Lemma 5.3 of [11] again, we calculate that, for any ,

Hence is an -martingale and so, for any , . From the representation (4.16), we also have that

| (4.17) |

Hence , for any , and so .

4.2. Feedback controls

A further question of interest is whether the value function remains the same when we restrict to feedback controls. A control is a feedback control if it is of the form , where is a strong solution of the SDE , , for some Borel function . Such controls are also referred to as Markov controls in the thesis [16] and are defined similarly in Section 3 of [8, Chapter IV] and Section 3.1 of [19].

In our problem, if there were a strong solution of the SDE (2.1), then this would give an optimal feedback control. Having shown that this is not the case in Theorem 2.1, we are left with the open questions of whether the value function can be attained by some feedback control, and whether it can be approximated by a sequence of such controls. In regards to the first question, we have the following result, whose proof can be found in the thesis [16].

Proposition 4.5.

Let be a probability space on which an -valued Brownian motion is defined with natural filtration . Suppose there exists a Borel function such that the SDE

| (4.21) |

has a strong solution with deterministically increasing. Then there exists a Borel function such that, for any ,

| (4.22) |

Moreover, , for all , and for , , and a continuous function, we have

| (4.23) |

Therefore to answer the question of existence of feedback controls that attain the strong value function, one needs to study the existence of strong solutions of SDEs of the form given in Proposition 4.5. The methods used in Section 2.2 do not apply directly here when we now consider a two-dimensional Brownian motion.

The result of Theorem 3.1 contributes to investigating whether the value function can be approximated by feedback controls, as the next result shows.

Proposition 4.6.

Again, we refer to the thesis [16] for a proof. Since Theorem 3.1 shows that (3.1) has no strong solution for , we have ruled out one potential approximating sequence of feedback controls. We leave open the question of whether the values coincide for the problems of optimising over strong controls and over feedback controls.

References

- [1] A. Cherny. On the strong and weak solutions of stochastic differential equations governing Bessel processes. Stochastics and Stochastic Reports, 70(3-4):213–219, Sept. 2000.

- [2] A. S. Cherny and H.-J. Engelbert. Singular Stochastic Differential Equations, volume 1858 of Lecture Notes in Mathematics. Springer Berlin Heidelberg, Berlin, Heidelberg, 2005.

- [3] A. M. G. Cox and B. A. Robinson. Optimal control of martingales in a radially symmetric environment. Stochastic Processes and their Applications, 159:149–198, May 2023.

- [4] L. Dubins, J. Feldman, M. Smorodinsky, and B. Tsirelson. Decreasing Sequences of Sigma-Fields and a Measure Change for Brownian Motion. The Annals of Probability, 24(2):882–904, 1996.

- [5] N. El Karoui and X. Tan. Capacities, Measurable Selection and Dynamic Programming Part II: Application in Stochastic Control Problems. arXiv:1310.3364 [math], Oct. 2013.

- [6] M. Émery and W. Schachermayer. A remark on Tsirelson’s stochastic differential equation. In J. Azéma, M. Émery, M. Ledoux, and M. Yor, editors, Séminaire de Probabilités XXXIII, volume 1709, pages 291–303. Springer Berlin Heidelberg, Berlin, Heidelberg, 1999.

- [7] M. Émery and W. Schachermayer. On Vershik’s Standardness Criterion and Tsirelson’s Notion of Cosiness. In J. Azéma, M. Émery, M. Ledoux, and M. Yor, editors, Séminaire de Probabilités XXXV, volume 1755, pages 265–305. Springer Berlin Heidelberg, Berlin, Heidelberg, 2001.

- [8] W. H. Fleming and H. M. Soner. Controlled Markov Processes and Viscosity Solutions, volume 25 of Stochastic Modelling and Applied Probability. Springer, New York, second edition, 2006.

- [9] I. Karatzas and S. E. Shreve. Brownian Motion and Stochastic Calculus, volume 113 of Graduate Texts in Mathematics. Springer New York, New York, NY, second edition, 1998.

- [10] M. Larsson and J. Ruf. Relative arbitrage: Sharp time horizons and motion by curvature. Mathematical Finance, 31(3):885–906, July 2021.

- [11] S. Laurent. On Standardness and I-cosiness. In C. Donati-Martin, A. Lejay, and A. Rouault, editors, Séminaire de Probabilités XLIII, volume 2006, pages 127–186. Springer Berlin Heidelberg, Berlin, Heidelberg, 2011.

- [12] J.-F. Le Gall. Brownian Motion, Martingales, and Stochastic Calculus, volume 274 of Graduate Texts in Mathematics. Springer International Publishing, Cham, 2016.

- [13] R. Mansuy and M. Yor. Random Times and Enlargements of Filtrations in a Brownian Setting, volume 1873 of Lecture Notes in Mathematics. Springer-Verlag, Berlin/Heidelberg, 2006.

- [14] G. Pammer, B. A. Robinson, and W. Schachermayer. A regularized Kellerer theorem in arbitrary dimension. arXiv:2210.13847 [math], Oct. 2022.

- [15] D. Revuz and M. Yor. Continuous Martingales and Brownian Motion, volume 293 of Grundlehren Der Mathematischen Wissenschaften. Springer Berlin Heidelberg, Berlin, Heidelberg, third edition, 1999.

- [16] B. A. Robinson. Stochastic Control Problems for Multidimensional Martingales. PhD thesis, University of Bath, 2020.

- [17] L. C. G. Rogers and D. Williams. Diffusions, Markov Processes and Martingales. Vol.2. Itô calculus. Cambridge University Press, second edition, 2000.

- [18] A. N. Shiryaev. Probability, volume 95 of Graduate Texts in Mathematics. Springer Science & Business Media, second edition, 1996.

- [19] N. Touzi. Optimal Stochastic Control, Stochastic Target Problems, and Backward SDE, volume 29 of Fields Institute Monographs. Springer New York, New York, NY, 2013.

- [20] B. Tsirelson. An Example of a Stochastic Differential Equation Having No Strong Solution. Theory of Probability & Its Applications, 20(2):416–418, Mar. 1976.

- [21] B. Tsirelson. Triple Points: From Non-Brownian Filtrations to Harmonic Measures. Geometric And Functional Analysis, 7(6):1096–1142, Dec. 1997.

- [22] A. Vershik. Approximation in measure theory. Doctoral Thesis, Leningrad University, 1973.

- [23] H. von Weizsäcker. Exchanging the order of taking suprema and countable intersections of -algebras. Annales de l’I.H.P. Probabilités et statistiques, 19(1):91–100, 1983.

- [24] J. B. Walsh. A diffusion with a discontinuous local time. Astérisque, 52–53:37–45, 1978.

- [25] J. Warren. On the joining of sticky Brownian motion. In J. Azéma, M. Émery, M. Ledoux, and M. Yor, editors, Séminaire de Probabilités XXXIII, volume 1709, pages 257–266. Springer Berlin Heidelberg, Berlin, Heidelberg, 1999.

- [26] A. K. Zvonkin. A transformation of the phase space of a diffusion process that removes the drift. Mathematics of the USSR-Sbornik, 22(1):129–149, Feb. 1974.