Defending Against Advanced Persistent Threats using

Game-Theory222This is a correction to the published version, available from https://journals.plos.org/plosone/article?id=10.1371/journal.pone.0168675. The correction has been submitted to the journal office in Feb. 2022, and is pending for publication, in which case this version will become replaced.

Stefan Rass1,3,*, Sandra König2, Stefan Schauer2,

1 Universität Klagenfurt, Department of Artificial Intelligence and Cybersecurity,

Klagenfurt, Austria

2 Austrian Institute of Technology, Safety & Security Department,

Klagenfurt, Austria

3 LIT Secure and Correct Systems Lab, Johannes Kepler University Linz, Austria

* stefan.rass@aau.at

Abstract

Advanced persistent threats (APT) combine a variety of different attack forms ranging from social engineering to technical exploits. The diversity and usual stealthiness of APT turns them into a central problem of contemporary practical system security, since information on attacks, the current system status or the attacker’s incentives is often vague, uncertain and in many cases even unavailable. Game theory is a natural approach to model the conflict between the attacker and the defender, and this work investigates a generalized class of matrix games as a risk mitigation tool for an advanced persistent threat (APT) defense. Unlike standard game and decision theory, our model is tailored to capture and handle the full uncertainty that is immanent to APTs, such as disagreement among qualitative expert risk assessments, unknown adversarial incentives and uncertainty about the current system state (in terms of how deeply the attacker may have penetrated into the system’s protective shells already). Practically, game-theoretic APT models can be derived straightforwardly from topological vulnerability analysis, together with risk assessments as they are done in common risk management standards like the ISO 31000 family. Theoretically, these models come with different properties than classical game theoretic models, whose technical solution presented in this work may be of independent interest.

1 Introduction

The increasing heterogeneity, connectivity and openness of today’s information systems often lets cyber-attackers find ways into a system on a considerably large lot of different paths. Today, security is commonly support by semi-automated tools and techniques to detect and mitigate vulnerabilities, for example using topological vulnerability analysis (TVA), but this progress is paired with the parallel evolution and improvements to the related attacks. APTs naturally respond to the increasing diversity of security precautions by mounting attacks in a stealthy and equally diverse fashion, so as to remain “under the radar” for as long as is required until the target system has been penetrated, infected and can be attacked as intended. Countermeasures may then come too late to be effective any more, since the damage has already been caused by the time when the attack is detected.

Mitigating APTs is in most cases not only a matter of technical precautions, but also some sort of fight against an invisible opponent and external influences on the system (coming from other connected systems but primarily due to the APT remaining hidden). Thus, any security measure taken may or may not be effective on the current system state, depending on how far the APT has evolved already. The question of economics then becomes particularly difficult and fuzzy, since the return on security investments is almost impossible to quantify in light of many factors that are outside the security officer’s scope of influence.

1.1 Related Work

In the last decade, the number of APTs [1] increased rapidly and numerous related security incidents were reported all over the world. One major reason therefore is that APTs are not focusing on a single vulnerability in a system (which could be detected and eliminated easily), but are using a chain of vulnerabilities in different systems to reach high-security areas within a company network. In this context, adversaries often exploit the fact that most of the protection efforts go into perimeter protection, so that moving inside the infrastructure is much easier and the attacker has a good chance to go unnoticed once being inside. Overcoming the perimeter protection by social engineering or malware (even unknowingly) carried inside by legitimate persons (bring-your-own-device problem) are only two ways to penetrate the perimeter security. Once the perimeter has been overcome, insider attacks are considered as an even bigger threat [2]. Extensive guidelines and recommendations exist to secure this internal area [3], e.g., the demilitarized zone (DMZ) but the intensity of the surveillance is limited. Specialized tools for intrusion detection or intrusion prevention require a large amount of administration and human resources to monitor the output of these systems.

APTs are characterized by a combination of several different attack methods (social engineering, technical hacks, malware, etc.) that is being tailored to and optimized for the specific organization, its IT network infrastructure and the existing security measures therein. Often, even yet not officially reported weaknesses, known as zero-day vulnerabilities, of the network infrastructure are in additional use. Especially the application of social engineering in the beginning stages of an APT lets the attacker bypass many technical measures like intrusion detection and prevention systems, so as to efficiently (and economically) get through the outer protection (perimeter) of the IT network. A prominent APT attack was the application of the Stuxnet malware in 2008 [4, 5, 6], which was introduced into Iran’s nuclear plants sabotaging the nuclear centrifuges. In the following years, other APT attacks, like Operation Aurora, Shady Rat, Red October or MiniDuke [1, 7, 8] have become public. Additionally, the Mandiant Report [9] explicitly states how APTs are used on a global scale for industrial espionage and that the attackers are often closely connected to governmental organizations.

The detection of APT attacks has therefore become an object of extensive research over the past years. As perimeter protection tools are occasionally failing to prevent intrusions, anomaly detection methods have been inspected to provide additional protection [10, 11]. The main idea is to detect the presence of an adversary inside an organization’s network, based on the adversary’s actions when it moves from one spot to another, or tries to access sensitive data (honeypots). Often, the detection rests on log file analysis, with data collected from all over the network and applications therein. Designated logging engines (e.g., syslog (http://tools.ietf.org/html/rfc5424) or logging management solutions (e.g., Graylog (http://graylog2.org/) are usually in charge here. Nevertheless, the detection of exceptional events in these log files alone is insufficient, since anomalies are often exposed not before events are correlated with each other [12, 13]. Since today’s systems are heavily connected and interchange a large amount of data on a regular basis, the size of the logging information increases drastically, making an evaluation quite difficult.

An example for a tool realizing this approach is AECID (Automatic Event Correlation for Incident Detection) [14, 15]. AECID enforces white-lists and monitors system events, their occurrences as well as the interdependencies between different systems. In the course of this, the system is able to get an overview on the “normal” behavior of the infrastructure. If some systems start to act differently from this normal behavior, an attack is suspected and an alert is raised.

Whereas AECID (and similar tools) are detective measures (as they trigger alerts based on specific events that have happened already), our approach in the following is preventive in the sense of estimating and minimizing the risk of a successful APT from the beginning (cf. Section 1.2). Game theory is here applied to optimize the defense against a stealthy invader, who attempts to sneak into the system on a set of known paths, while the defender does its best to guard all these ways simultaneously. This is the abstract version of the situation that is normally summarized under the term APT.

Game theory appears as a natural tool to analyze conflicts of interest, such as obviously arise between the defender and the attacker mounting an APT. Powerful techniques to defend against stealthy takeover have been defined (partially originating from [16, 17] but also based on a variety of precursor and independent approaches, such as collected in [18]), but a method that fits into established risk management processes and can be instantiated with vague, fuzzy and qualitative risk assessments (such as uttered by domain experts) is demanding yet missing. Particularly intricate are matters of social risk response, say, if an enterprise seeks to minimize losses of reputation besides direct costs; assessing the public community’s response to certain actions being taken is a vague and difficult issue, to which sophisticated game theoretic [19, 20, 21, 22] and agent based models [23] can be applied for an analysis and risk quantification. A recognized feature of any game-theoretic treatment of APT and in general every cyber-security scenario is the lack and asymmetry of information (say, the absence of knowledge about the attacker’s strategy spaces or payoffs, cf. [24, 25], while the attacker may have full information about the target system). This asymmetry is even stronger than what can be captured by many game-theoretic models, since organizational constraints may enforce the defender to act only at certain points in time, while the attacker is free to become active at any time. That is, the game is discrete time for one player, but continuous time for the other player – a setting that is hardly considered in game-theoretic literature related to security, and as such a central novelty in this work.

As we will show later (cf. Section 10.1 and Lemma 9), matrix games are nonetheless a proper model to account for what the defender can do against an APT, if we confine ourselves with the goal of playing the game to the best of our own protection and allow the outcomes to be random and unpredictable. Under this relaxation over the conventional game theoretic modelling, we can account for the outcome to be dependent on an action that is taken at different points in time, and especially also for actions that were interrupted before they could carry to completion. This addresses the issue identified by [26], who pointed out that moves may take a variable amount of time rather than being instantaneous (and thus atomic).

Ultimately, a significant obstacle for practitioners in the application of any game theoretic model is the lack of understanding of the ingredients to the game. That is, no matter how sophisticated the model may be, it nevertheless needs to be instantiated with whatever data is available. In many cases, this data is either qualitative (fuzzy) expert knowledge (formulated in some taxonomy, e.g., [27]) or obtained from simulation (see [28] for one example). Either may not be suitable to instantiate the proper APT model, even though the APT-game model would be quite sophisticated and powerful (such as [29]) in its capabilities for risk mitigation. In any case, this takes us to empirical game-theoretic models; a category into which this work falls.

1.2 Our Contribution

We present a novel form of capturing payoff uncertainty in game theoretic models. We deviate from standard games in the conceptual way of measuring the outcome of a gameplay not in crisp terms, but by an entire probability distribution object. That is, we play game theory on the abstract space of distributions for the following reasons:

-

1.

The specification of losses and payoffs in a game is often difficult: how would we accurately quantify the results of a defense in light of an attack? Do we count the number of infected machines (such as done in [16])? Shall we work with monetary loss (causing difficulties in how to “price-tag” loss of reputation or consumer’s trust)? Conversely, can we play games over a categorical scale of payoffs, such as risk is being quantified in many standards like ISO 31000 [30] or similar?

We can elegantly avoid any such issue by letting the game being defined by any outcome that can be ordered (as in conventional game theory), but in addition, allowing an action to have many different random outcomes (this is usually not possible in standard games). In doing so, we gain a considerable flexibility and degree of freedom to tackle a variety of issues, which we will discuss later on.

-

2.

There is a strong asymmetry in the player’s information in many senses: first, the game structure itself is not common knowledge, since the defender knows only little about the opponent, while the opponent knows very much about the defender’s infrastructure (as lies in the nature of APTs, since these typically include an a-priori phase of investigation and espionage). Second, the game play is different for both players, since moves are not mutually observable, nor must happen instantaneously or even at the same times.

Again, this can be captured by letting the effects of action be nondeterministic and random even if both, the attacker’s and defender’s action were both known.

-

3.

Any game-theoretic model for security may itself be only part of an outer risk management process, and as such must be “compatible” with the surrounding workflows, which cover APT mitigation among other aspects. That is, the game theoretic model’s input and output must be useful with what the risk management process can deliver and requires. Our APT-games will be designed to fulfil this need.

-

4.

Conventional stochastic models like Bayesian games indeed also capture uncertainty, but do so by letting the modeler describe a variety of different possible game structures, among which nature chooses at random in the actual gameplay. While different such structures can embody different outcomes, and the likelihood for these can be specified as a distribution (similar to what we do), each of these possible game structures must be specified in the classical way, thus effectively “multiplying” the problems of practitioners (if one game is difficult to specify, the specification of several ones does not appear to ease matters). Our approach avoids these issues by working with empirical data directly, and keeping the game models simple at the same time.

In light of the last point in particular, we will restrict our attention in the following to the problem of how to define games over qualitatively assessed outcomes that may be random. That is, the central question that this work discusses is essentially a form of reasoning under uncertainty:

Given some possibilities to act, what would be the best choice if the consequences of an action are intrinsically random?

We will show how to answer this question if the randomness can be modeled in the most general form by specifying probability distributions for the outcome. However, unlike normal optimization that maximizes some numeric quantity derived from the distribution of a random variable , our games will optimize the shape of ’s distribution itself.

The presentation will heavily use examples for illustration, yet the concepts themselves will be described and also defined in a general form. To get started, consider the following example of decision making under the setting that we consider. Example 1 is about the protection of intellectual property rights (IPR), whose theft can be a reason to mount an APT.

Example 1 (Assigning IPR Responsibilities).

Assume that an enterprise runs a project and is worried about protection of IPR. To mitigate this issue, one or more persons shall be put in charge of IPR protection. For this, say, three options are available:

-

1.

Assign IPR responsibility to one person: This will increase the workload of the employee, and must be made w.r.t. available resources and skills. Neither is precisely quantifiable nor may be sufficient at all times. Thus, even assuming a strong commitment of the person to its role, some residual risk of damage occurring remains (human error of subordinates cannot be ultimately ruled out despite any strong supervision).

-

2.

Assign IPR responsibility to a team of two or three persons: Resources and skills may be much richer in this setting, but there is a danger of mutual reliance on one another, such that in the worst case, no-one really does the job (as a result of social coordination failure). Chances for this worst case to occur may be even higher than for option 1.

-

3.

Do security/IPR training sessions: here, we would completely rely the joint behavior of the employee’s and their commitment to the confidentiality of project content and adherence to the training’s messages. Nevertheless, chances for IPR loss due to human error (e.g., an unencrypted email leaking confidential information, or similar) may be lowered only temporarily, so that the training would have to be repeated from time to time.

The optimal choice in Example 1 is not obvious, since consequences are not all entirely guaranteed for always foreseeable. Intuitively, we would go with the setting under which loss of intellectual property is least likely. Later, in Section 4, we will construct an ordering relation that does exactly this if the loss distributions are defined on a scale of damage whose maximum is the loss of intellectual property (e.g., quantified by the business value attached to it). So, if we are somehow able to model possible random outcomes in each of the three scenarios, we can (algorithmically) compute the “best” (i.e., -minimal) loss distribution to be the best choice among the three above. This is a matter of loss distribution specification, which we will discuss in Section 5.1.

1.3 Organization of the paper

Section 2 briefly introduces the tools and concepts that our models are built upon. We will strongly rely on TVA (see Section 2.1) and human expertise in our model building, which we believe to be a viable approximation of how security risk management works in practice. Section 3 presents an example, which we will carry through the article to illustrate the concepts and approach as a whole. Section 4 introduces the theory of how decisions can be made if their outcome is rated through an entire probability distribution object (rather than a number), and Section 5 takes this basis to define games, equilibria and to highlight similarities but also an important qualitative difference between the so-generalized games and their classical counterparts (among others, [31] showed that fictitious play can converge to a point that is not necessarily an equilibrium, which led to the introduction of a lexicographic Nash equilibrium as a new concept in [32]; we will go into more details later in Section 5). Sections 6 and 7 apply the framework to APTs by picking up the example from Section 3, and give algorithmic details on how to practically work out results (the aforementioned differences between our and classical games call for various mathematical tricks here). Section 8 briefly discusses generalizations towards multi-criteria decision making. Section 9 finishes the example from Section 3 by presenting results and security protection advices obtained from our game-theoretic APT mitigation game. Section 10 presents a critical discussion in terms of answering direct questions that were collected from practical experience with the proposed method in a research project (see the acknowledgment section at the end of the paper). Conclusions are drawn in Section 11.

2 Preliminaries and Notation

Vectors and matrices will be denoted as bold-face letters in lower case for vectors and upper case for matrices. -Matrices over a set are denoted as , and the symbol is a shorthand for sequences. We use upper case normal font letters like to denote random variables, and write to express that the RV has the distribution function . The respective density belonging to is the corresponding lower case letter , and where necessary, we add the subscript or to indicate the related RV for the density or distribution. For a given (finite) set , we let be the set of all discrete probability distributions (the simplex) over . Likewise, all families of sets, RVs or distribution functions are denoted in calligraphic letters (such as or ). Estimates of a value are indicated by a hat, such as , to mean empirical distributions (normalized histograms). Approximations of an object or (scalar, distribution, etc.) are marked by a tilde, e.g., .

2.1 Topological Vulnerability Analysis

Topological vulnerability analysis [33] is the systematic identification of attacks to a system, based on the system’s structure and especially its network topology. The process usually consists of creating a complete picture of the infrastructure augmented by all available details about the components. Modeling the system’s topology as an (undirected) graph with a designated target node , we can use standard path searching algorithms to identify paths from the exterior of towards the target node . Whatever structure is dug up by the TVA, an immediate question concerns the applicability of known attack patterns to the infrastructure model (similar to virus patterns being looked up in software). Graph matching techniques (see [34, 35] for example) appear as an interesting tool to apply here. The known (or suspected) vulnerabilities/exploits related to the nodes in then determines which paths are theoretically open to to successfully attack the system. These attack paths are thus sequences of vulnerabilities (augmented with the respective preconditions to exploit a vulnerability), and are the main output of a TVA. An APT can then (in a slightly simplified perspective) be viewed as the entirety of attack paths, and is physically mounted by sequentially working along a chosen attack path in a way that avoids detection of the attack at all stages (stealthy). Particular practical risk arises from exploits of not yet known vulnerabilities, which are commonly called zero-day exploits. Uncertainty about these partially roots in the complexity of the network, so that graph entropy measures (see, e.g., [36]) may be considered as a measure to help quantifying the chances of attacks coming over paths that were missed during the analysis. The practical handling of this residual risk is often a matter of using domain knowledge, collecting expert opinions, experience and information mining, combined with suitable mathematical models (e.g., [37, 38]). Our model immanently includes a zero-day vulnerability measure, as will be discussed in Section 7.2.

2.2 Attack Graphs and Attack Trees

The entirety of ways into a system, including intersections and alternative routes on attack paths makes up the attack graph [39]. It is essentially a representation based on the system topology , in which outgoing links of a node are retained only if some exploit on enables reaching ’s neighbor (see Figs 1 and 2 for an example). In terms of representation, an attack graph is to be distinguished from an attack tree, which is usually an AND/OR tree representing the possible exploit chains in a different way. Regardless of which is available, the main object of interest for our purposes is the set of attack paths, which directly corresponds to the action set of player 2 in our APT-games.

2.3 Extensive Form Games

Towards a game theoretic model of APT, we will use extensive form games. While a full fledged formal definition of EFG is lengthy and complex, it will suffice to give a description of it to highlight the similarities to APTs. Formally, EFG are described by a tree , with a designated root node that represents the starting stage in the game. Consequently, has edges directed outwards from the root. For an APT, the root corresponds to the (hypothetical) point representing the exterior of the network graph . The EFG is played between a set of (for our purposes two) players, including a hypothetical player “chance” that represents random moves in the game. Each node in the game tree carries an information on which player is currently at move (including the “chance” player). Furthermore, moves that are indistinguishable by other players are collected in a player’s information set. This, from the opponent’s perspective, represents the uncertainty about what a player has currently done in the game. In an APT model, the information set would correspond to possible locations where the attacker could currently be (again, recalling that an APT is stealthy). The EFG description is completed by assigning a vector of outcomes to the leaf nodes in the game tree. Normally, the outcomes are real values and specified for all players. Viewing an APT as an EFG, we would thus require to specify our own damage when the APT has been carried to the end (i.e., the target node has been reached), but also the payoff to the adversary would needed to be known. The latter is a practical issue, since the uncertainty in the game is not only due to the attacker’s moves themselves, but also caused by external influences outside any of the player’s influences. Shifting all this uncertainty induced exteriorly to the chance-node in the EFG description appears infeasible, since much of it may depend on the particular action and current (even past) moves of both players (defender being player 1 and the attacker being player 2 in an APT game). However, given that the two players have different information on the current stage of the game play (only the attacker knows its precise position, the defender knows nothing; not even the presence of the attacker is assured), defining the information sets appears hardly doable.

Since the concept of EFG as being games with imperfect information essentially rests on information sets, any best behavior in the game play will inevitably rest on hypotheses on the player’s moves. For an EFG, we would describe these hypotheses as probability distributions on the information sets. In lack of these, we can only model the outcome based on the known defender’s actions and assuming the attacker to be possibly everywhere in the system. Practically, these hypotheses will rarely be available as hard figures and mostly come in qualitative terms like “low”, “medium” or “high” risk. Classical game theory is not naturally designed to work in such fuzzy terms.

Finally, an assumption of frequent criticism concerns the game model to be common knowledge to both players. This is certainly questionable in APT scenarios. In fact, a defender may in practice only have limited and widely uncertain information about the attacker’s incentives, current moves, current location or even its presence in the game. Thus, the information set would in the worst case cover the entirety of the game graph, and neither is the payoff to the attacker precisely quantifiable in most cases.

To avoid all these issues, we propose to replace the attacker’s payoffs by our own losses (in an implicit assumption of a zero-sum competition), in which an equilibrium behavior is a provable bound (see Lemma 9) to the payoff for the player having modeled the game . Second, we avoid difficulties of uncertain payoffs by defining the game play itself as a one-shot event, in which both players choose their strategies for the round of the game and the payoff is determined by that choice (thus, shifting all matters of uncertainty about where a player is in the game entirely to the payoffs). To this end, we will model an APT as a game with complete information but uncertain payoffs. In fact, the payoffs will be entire probability distributions rather than numbers.

3 A Running Example

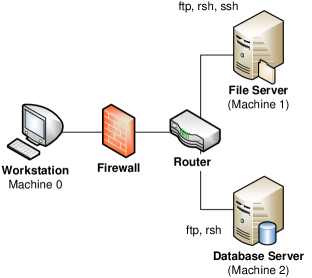

Throughout this work, we will illustrate the steps and concepts using a running example borrowed from [40]. This reference describes a simple version of TVA (see, e.g., [33]) and attack graph modeling, based on a small infrastructure that is shown in Fig 1: The system consists of three machines (numbered as 0, 1 and 2), with several services being open on each node (such as file transfer protocol (FTP), remote shell (RSH) and secure shell (SSH)). The adversary attempts to gain access to machine 2, hereafter denoted as (the predicate) full_access(2). Towards its goal, the attacker may run different exploits from various points in the network, such as:

- •

-

•

a secure shell buffer overflow at node y, remotely initiated from node x, hereafter denoted as sshd_bof(x,y).

-

•

local buffer overflows in node x, hereafter denoted as local_bof(x).

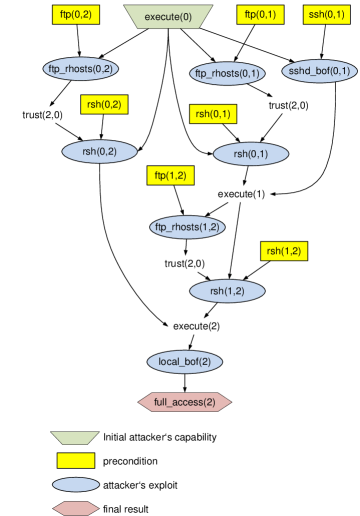

The actual APT is the attempt to use these exploits (and combinations thereof) in a stealthy fashion to penetrate the entire system towards establishing full access to the target machine 2. Naturally, exploits of any kind are subject to preconditions holding on the machine from which the exploit is initiated. We denote such a precondition on machine x to target a machine y in predicate notation as ftp(x,y), rsh(x,y) and ssh(x,y), w.r.t. the protocol being used. Depending on which services are enabled and responsive on each machine, a TVA can then be used to compile an attack graph (see 2), which roots at the initial condition of having execution privileges on machine 0, denoted as execute(0), from which attacks can be mounted under the relevant preconditions. A particular APT scenario can be viewed as a path in the graph that starts from the root (execute(0)) via trust relations established between connected machines x and y (denoted as trust(x,y)), until the goal (full_access(2)).

Running the plain task of computing and enumerating all paths in the attack graph from execute(0) to full_access(2) digs up 8 attack vectors in our example. Each of these corresponds to one particular APT scenario, and the entirety of which makes up the adversary’s action set, denoted as (the subscript is used for consistency with the subsequent game theoretic model, in which the attacker is player 2. The defender will be player 1, respectively).

The next step in the risk mitigation process is the derivation of countermeasures from the identified attacks, such as, for example, the deactivation of services (to violate the necessary preconditions), or a patching strategy (to remove buffer overflow vulnerabilities), to name only two possibilities. Alas, none of these precautions is guaranteed to be feasible or even to work, as for instance:

-

•

services may be vital to the system, say, deactivating an FTP connection may render the service offered by machine 1 useless.

-

•

patches may work against a known buffer overflow, but an unknown number of similar exploits may nonetheless remain (thus enabling zero day attacks upon vulnerabilities found and offered for sale on the black market).

On the positive side, even unknown malware may be classified as such based on heuristics, experience or innovative antivirus technologies, all of which adds to the chances for the identified mitigation strategies to succeed. The practical issue here is, however, to deal with the residual risks and the inevitable uncertainty in the effectiveness of a protection. Ways to capture and handle these issues are theoretically described in Section 4 and applied to this example in Section 6.

For the time being, let us assume that a (non-exhaustive) selection of countermeasures has been identified and listed in Table 1. We call this list the defender’s action set, denoted as to indicate the defender as being player 1 in the subsequent APT game (Section 6). We leave this set incomplete here for the only sake of simplicity (in reality, the analysis would dig up a much richer set of countermeasures, such as can be based on the security controls catalog of relevant norms as ISO 27001 [41] or related).

| Countermeasure | Comment |

|---|---|

| deactivation of services (FTP, RSH, SSH) | these may not be permanently disabled, but could be temporar- ily turned off or be requested on demand (provided that either is feasible in the organizational structure and its workflows) |

| software patches | this may catch known vulnerabilities (but not necessarily all of them), but can be done only if a patch is currently available |

| reinstalling entire machines | this wipes out unknown malware but comes at the cost of a temporary outage of a machine (thus, causing potential trouble with the overall system services) |

| organizational precautions | for example, repeated security trainings for the employees. These may also have only a temporary effect, since the security awareness is raised during the training, but the effect decays over time, which makes a repetition of the training necessary to have a permanent effect. |

In general, the effect of an action, precaution, countermeasure, etc. is in most cases not deterministic and influenced by external factors beyond the defender’s influence and not even fully determined by the attacker’s actions. Furthermore, actions on both sides are usually not for free, and costs/losses on the defender’s side are induced by system outages (say, during a reinstall), staff unavailability (say, when people are in a training that itself may be costly), etc. Some of these costs may be precisely calculated, but others (say, if the system is offline during a reinstall) may depend on the current workload and thus be difficult to quantify.

Therefore, a qualitative risk assessment is often the only practical option (and an explicit recommendation by various standards such as ISO 31000 and by the German Federal Office of Information Security (BSI)). For a game theoretic analysis, however, this is inconvenient as it may result in a quite vague assessment of a countermeasure that may look like shown in Table 2.

| Countermeasure: patching | |

|---|---|

| Aspect | Expert’s assessment |

| applicability | not always available |

| effectiveness | low or high (depending on the exploit) |

| cost | low to medium (e.g., if the system needs to be rebooted) |

Similar assessments can be made for other protective measures as well, with quantitative figures occasionally being available (such as the costs for a security training, or the cost to install a new firewall or intrusion detection system). However, ambiguous and even inconsistent opinions may be obtained on the effectiveness and applicability of a certain action. Even if only one expert does the assessment in categorical terms as shown in Table 2, uncertainty may at least arise from none of the offered categories being appropriate for the real setting. That is, with “medium effectiveness” being a vaguely understood term in that context, an expert may utter a range of possibilities rather than confining her/himself to a specific statement. The example in Table 2 illustrates this by saying that the effectiveness of a patch can be either high (if the patch closes precisely the buffer overflow that was intended by the adversary), or even low, if the exploit has already been used to install a backdoor, so that the buffer overflow – even if it gets fixed – is no longer needed for the APT to continue. What is even worse, both assessments are at opposite ends of the scale (low/high), and can both be justified, thus telling hardly anything informative in this case.

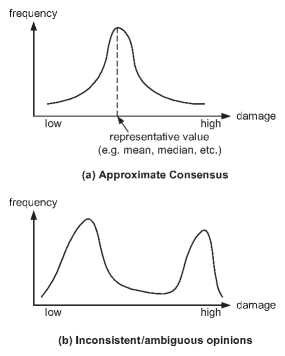

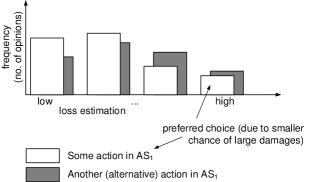

It is this point, where further opinions should be sought, which naturally will create a number of different assessments, some of which may be even mutually inconsistent (see Fig 3 for an illustration of how different opinions may accumulate at different points on the risk scale).

All this hinders the application of conventional decision or game theory, since in either approach (game or decision theoretic), we require a reasonably measurable effect for an action, and also a way to uniquely rank (order) different effects when a “best” action is sought.

4 Modeling Uncertainty for Decision-Support

If the outcomes of an action are uncertain, even random, then the most powerful model to express these would be to:

-

•

collect as much data, expert opinions, etc. as is available,

-

•

and compile a probability distribution from the available data, to capture the uncertainty in the assessments. Though this preserves all available information in the distribution object, the issue of working with it is more involved and a central technical contribution in this work.

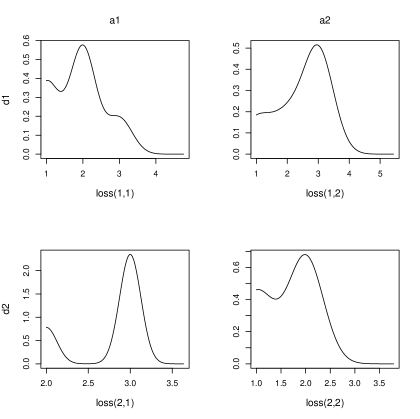

In the best case, the assessments turn out to be quite consistent, with only a few outliers, in which case we may be able to define a reasonable representative (say, the average assessment; see Fig 3a). In other cases, however, the distribution may be multimodal, with each peak corresponding to different answers that may all have their own justification as being plausible (Fig 3b shows an example of many experts agreeing on either low or high effectiveness of the patching strategy).

Finding a best action is typically done by assigning a utility value (see Section 2.2 in [42]) to the actions to choose from , and looking for the maximal such utility for both sides (defender and attacker). In quantitative risk management, a popular choice for this utility value is the expected damage, computed as

| (1) |

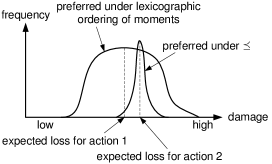

which enjoys wide use throughout the literature (e.g., the ISO 31000 [30] or ISO 27000 [43] family of standards). This convention is easily recognized as being the first moment of some (usually not explicitly modeled) payoff distribution, and as such, is not satisfying in practice, as the mean tells us nothing about possible variations about it (Fig 4 illustrates the issue graphically). So, the variance would be the next natural value to ask for in addition to (1). Continuing this approach, we can describe a distribution more and more accurately by using more and more moments, and indeed, the mapping

provides a bijective link between a distribution function and a representative infinite sequence of real numbers, provided that all moments exist. In a simple use of this representation, we could just lexicographically compare the sequences, letting the first judgement be based on the mean, and in case of equality, compare the variances, and so on. Such an ordering, however, appears undesirable in light of easy to construct examples that yield quite implausible preferences. Fig 4 shows an example.

An approach that preserves all information is treating the moment sequence as a hyperreal number , so that we get a “natural ordering” on the distributions as it exists in the hyperreal space ; see [44] for a full detailed treatment, which we leave here as being out of the scope of this work.

Nevertheless, it is important to recognize that the trick of embedding a distribution in the ordered field of hyperreals equips us with a full-fledged arithmetic applicable to random payoff distributions, as well as a stochastic ordering, so that “optimality” of decisions can be defined soundly (later done in Definition 3). This implies that many well known and useful results from game and decision theory remain applicable in our setting (almost) as they are. Essentially, this saves us the labour of re-establishing a lot of theory, as would be necessary if another stochastic order (such as one in [45]) would be used.

Definition 2 will suitably restrict the class of loss distributions to ensure that all moments exist. Before that, however, let us briefly recap where the loss distributions will come from:

Given the attack graph that describes all APT scenarios and treating it as an EFG game description, we apply the same conversion of an EFG into the normal form of the game, which is a matrix. Let be the number of threat mitigation strategies and possible exploits, which correspond to the action sets of both players (paths through the infrastructure determined by the possible exploits; cf. Table 3). Whereas a classical game would be described as a real valued payoff matrix , the outcome in the APT game is not deterministic and as such will be described by a matrix of RVs . Each variable describes the random loss (effect) of taking mitigation strategy relative to the unknown -th move of the adversary.

| 1 | execute(0) ftp_rhosts(0,1) rsh(0,1) ftp_rhosts(1,2) rsh(1,2) local_bof(2) full_access(2) |

|---|---|

| 2 | execute(0) ftp_rhosts(0,1) rsh(0,1) rsh(1,2) local_bof(2) full_access(2) |

| 3 | execute(0) ftp_rhosts(0,2) rsh(0,2) local_bof(2) full_access(2) |

| 4 | execute(0) rsh(0,1) ftp_rhosts(1,2) rsh(1,2) local_bof(2) full_access(2) |

| 5 | execute(0) rsh(0,1) rsh(1,2) local_bof(2) full_access(2) |

| 6 | execute(0) rsh(0,2) local_bof(2) full_access(2) |

| 7 | execute(0) sshd_bof(0,1) ftp_rhosts(1,2) rsh(1,2) local_bof(2) full_access(2) |

| 8 | execute(0) sshd_bof(0,1) rsh(1,2) local_bof(2) full_access(2) |

Definition 2 ((Random) Loss).

A real-valued RV is called a (random) loss, if the following conditions are satisfied:

-

•

(this can be assumed w.l.o.g.)

-

•

The support of , being , is bounded (where the bar means the topological closure).

-

•

has a density w.r.t. either the counting- or the Lebesgue-measure. In the latter case, we assume the density to be continuous and piecewise polynomial over a finite partition of its support.

Define the set of loss distributions to contain all distribution functions related to random losses.

We stress that the conditions of Def. 2 only mildly constrain the set of choices, since (by Weierstraß’ theorem), all smooth distributions allow a polynomial approximation in the desired sense, if they are compactly supported.

4.1 Optimal Decisions if Consequences are Uncertain

Definition 2 assures that the density function of any random loss admits moments of all orders , so that we get a well-defined condition for an ordering based on moment sequences:

Definition 3 (-Preference between Loss Distributions).

Let be losses with . We prefer over , written as , if there is an index so that for all . We synonymously write whenever we explicitly refer to distributions rather than RVs.

A minor technical difficulty arises from the yet unsettled issue of whether or not there are non-isomorphic instances of , in which case we could get ambiguities in the -ordering. The next result, however, rules out this danger.

While the theoretical definition is easy, important practical questions about this preference demand an answer, in particular:

-

1.

What is the practical meaning of the -ordering for risk management?

-

2.

If is practically meaningful, how can we (efficiently) decide it?

Let us postpone the answer to the first question until Section 4.3, and come to the algorithmic matters of deciding first. The answer to the second question will then also deliver the answer to the first one.

4.2 Practical Decision of -Preferences

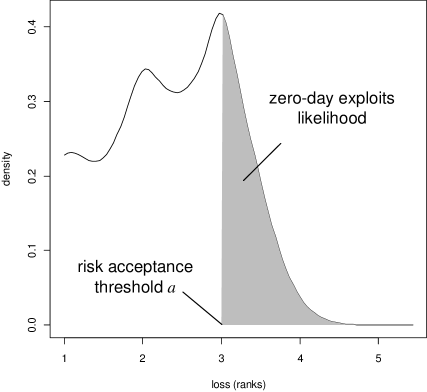

Let us first discuss the case where the loss distribution is continuous. Common examples in risk management (cf. [47]) are extreme value distribution or stable distribution (with fat tails). Although such distributions may not necessarily have a bounded support (thus not corresponding to a random loss in the sense of definition 2), we can approximate the distributions by random losses via defining a risk acceptance threshold , and truncating the distribution outside the range . The concrete value can be chosen upon a desired accuracy , for which we can choose large enough to have the residual likelihood of damage is smaller than , or formally, (we will come back to the choice of in section 10.2).

Practically, the risk acceptance threshold is the value above which risks are simply “being taken” or are covered by proper insurance contracts. Thus, specifying the value and truncating the loss distributions accordingly makes distributions with fat and/or unbounded tails fit as approximate versions into definition 2.

If have the same compact support , and since the respective density functions are assumed continuous, both admit limits and . For the moment, assume , i.e., (the case of equality is treated later). The continuity of both functions implies that holds in an entire left neighborhood of for some . It is then a simple matter of calculus to verify that (since both ), the speed of divergence of the respective moment sequences and is determined by which density function takes larger values in the region , recalling that both densities vanish at . That is, we have

| (2) |

and the condition of Definition 3 is ultimately satisfied (in either way).

Lemma 5.

Let be two random loss variables with continuous distribution functions , and let denote the respective densities. If both RVs are supported in an interval for , and there is some such that for all , then .

Lemma 5 (see [46] for a proof) offers an easy way to decide preferences based on the RV’s density functions only. The procedure is the following: Call the common support of both loss variables , and consider the density functions :

-

•

If , then ,

-

•

Otherwise, if , then .

Upon a tie, i.e., , we need to either decrease , truncate the distributions properly, and repeat the analysis, or we may look at derivatives at to tell us which density takes larger values locally near . The latter approach is further expanded in Section 7.1.

If the distribution is discrete, say, if the available data is not continuous but qualitative (e.g., categorical), then things are even simpler: if are both distributions over the same categories, then , if puts less likelihood to categories of large damage than (see Fig 5 for an example).

Formally, thus boils down to a humble lexicographic ordering whenever the losses have categorical distributions.

Definition 6 (lexicographic ordering).

For two vectors and of not necessarily the same length, we define if and only if there is an index so that and whenever .

For two categorical distributions given in matrix notation and letting the support be given in descending order of risk levels , we observe that , when the distributions are:

That is, the action with the higher likelihood of extreme damage is less favorable, and upon a tie (equal chances of large damages), the likelihood for the next smaller risk level tips the scale, etc. Rephrasing the classical saddle-point condition in terms of such a lexicographic order leads to a new concept that coincides with (standard) Nash equilibria only in the 1-dimensional case (as observed by [31]). In higher dimensions, corresponding to non-scalar losses, such as categorical loss distributions, an optimum w.r.t. the lexicographic order, does not necessarily also induce a saddle point in the sense of . We will hence use different names to distinguish classical from lexicographic equilibria, later in Section 5 and onwards.

4.3 Practical Meaning of -Preferences

Summarizing the previous discussion in concise form directly takes us to the practical meaning of -preferences:

We have , if large damages (near the maximum) are more likely to occur under than under .

This is just an intuitive re-statement of Lemma 5. However, and remarkably, the converse to it is also true, if the density is piecewise polynomial (see [32, 31] as an extension to the original Thm. 2.14 in [46]):

Theorem 7.

Let be two RVs with distribution functions . If , then a threshold exists such that for every .

Restating this intuitively again, Theorem 7 tells that:

a -minimal decision among two choices with respective consequences and minimizes the chances for large damages to occur.

This is exactly what we are looking for: Risk management is in many cases focusing on extreme events rather than small distortions (which the system’s “natural” resilience is expected to handle anyway), and the focus of the -relation to prefer distributions with lighter tails perfectly accounts for this. Having as a total ordering with a practical interpretation as being “risk-averse”, this already addresses the simple case of decision making among finitely many choices (as discussed in the next Section 5).

5 Practical Decision-Making

Remembering our example of APT mitigation, suppose that as an initial attempt, we would consider the installation of permanent security precautions, such as (additional) firewalls, access controls, physical protection, etc. Moreover, organizational changes such as were discussed in example 1 may be under discussion. However, all of these may have uncertain effectiveness, but the -relation now helps out.

In general and abstractly, the decision problem and procedure is the following:

-

•

A set of choices (e.g., security precautions) is available (e.g., defense actions for APT mitigation), each of which comes with a random consequence/effect captured by random losses .

-

•

By looking for the -minimum among the distributions of , we can take an optimal decision under uncertainty.

An open issue so far is where to get the losses from, an issue that will be revisited several times throughout this paper.

5.1 Constructing Loss Distributions

The simplest approach to construct loss distributions that satisfy definition 2 is to either:

-

•

collect as much data as is available, and compile an empirical distribution from it,

-

•

or define the loss distribution directly based on expertise (say, if the action’s incurred loss has a known distribution), if this is possible.

The latter case may occur seldom in practice, unless the particular threat has been studied specifically (such as disaster management or value at risk calls for extreme value distributions, etc.), and the “adversary” is nature itself. Against a rational adversary such as business competitors, hackers, etc., threat intelligence and expertise is the fundament upon which loss may be measured. Often, this assessment is made in qualitative terms for several (good) reasons, such as:

-

•

Human reasoning is neither numeric nor crisp, i.e., experts may find it simpler to give assessments like “high risk” instead of having to specify a hard figure.

-

•

Numerical precision can create the illusion of accuracy where there is none. There are only few types of incidents on which reliable statistical data is available, and having huge amounts of data on APTs attacks on general cybersecurity incidents may be unrealistic (and also undesirable if the incidents concern oneself).

In practice, rating actions w.r.t. their outcomes is naturally a matter of expert surveys, with answers possibly looking like shown in Table 2. Collecting many such opinions and putting them together in an empirical distribution about a precaution’s performance may give distributions whose shape is unimodal (if a consensus among opinions is found), or multimodal, if disagreeing opinions are reported. Whatever happens or whether or not the outcome looks like illustrated in Fig 3, the -preference relation now allows for an elegant deal with this kind of uncertainty.

5.2 Games and Equilibria

With the uncertain outcome in a scenario of defense vs. attack being captured by a (perhaps empirical) probability distribution , and the complete set of distributions being totally ordered w.r.t. , it is a simple and straightforward manner to define matrix games and equilibria in the well-known way, but will need to bear in mind that the resulting concepts will not exactly resemble (classical) equilibria in all senses, as we will explain later. For convenience of the reader, we give the necessary concepts and definitions here from classical game theory.

Let be the action spaces for player 1 and 2, respectively, with cardinalities and . Let be a matrix of RVs that are all supported on the same compact set . Let be the distribution function of the random loss . In each round of the game, the random outcome is conditional on the chosen actions of player 1 and player 2, and has the distribution if player 1 chooses action and player 2 chooses action .

We consider randomized choice rules and , i.e., the vectors describe the likelihoods of actions being taken by either player. In that case, the random outcome has a distribution computed from the law of total probability, which is

| (3) |

assuming a stochastically independent choice of actions by both players. This is the utility function in case of random outcomes (note that (3) is exactly the same formula as is familiar from matrix game theory). So, the actual gameplay is not about maximizing the average revenue (as usual in game theory), but towards optimally “shaping” the outcome distribution towards -minimality. That is, in a zero-sum competition, player 1 and player 2 seek to choose their actions in order to minimize/maximize the likelihood of extreme events. Speaking differently again, player 1 attempts to shift the mass allocated by the respective density towards lowest damages, whereas player 2 tries his best to shape the density towards putting more likelihood on larger damages. This is the essential technical process of our game-theoretic APT risk mitigation strategies, whose optimality is that of a lexicographic Nash equilibrium [32], which is, in the 1-dimensional case (only), the same as a standard Nash equilibrium (see [31] for a detailed example, and [48] for a formal treatment of the classical case). In general, a lexicographic equilibrium respects goal priorities, which are here equal to the ordering on the loss scale, taking highest losses as most important to avoid (and breaking ties by moving to the next lower loss category). Similar as a standard equilibrium, a lexicographic equilibrium penalizes unilateral deviations, but in doing so, opens up a possibility for the second player to improve its own revenue in a (less important) other goal (e.g., causing more likely damage of a lower loss category). The theoretical facts about (real-valued) Nash equilibria in games, by the transfer principle, translate likewise to hyperreal terms. The practical difference relates to computability, since the defenses that we can find (algorithmically) in games over loss distributions are obtained from lexicographic equilibria. We will disambiguate the two hereafter by speaking about (standard) Nash equilibria to mean the classical concept, and lexicographic (Nash) equilibria to denote the other.

As for standard games, it can be shown that the saddle-point value is invariant w.r.t. different (standard) Nash equilibria, and that equilibria defined w.r.t. exist (and can be generalized to standard Nash-equilibria in -person games in the canonic way). The way of proving it makes use of the embedding of distributions into the hyperreal space , where all the known results necessary to re-establish the fundament of game theory are available (yet further substantiating our loss representation by a moment sequence). Unfortunately, however, not all properties are directly inherited, such as a central computational feature of zero-sum games is absent in our setting:

Proposition 8.

Proposition 8 is proved by constructing a concrete example (see [51]) of a game that cannot be solved using fictitious play. Thus, it is an unfortunate obstacle in applying well-known game theory to our new setting. The formal fix relies on yet another representation of the loss densities, which admits converting a matrix game over into a set of standard matrix games over , which can be solved by fictitious play again. However, the result is still not just a Nash equilibrium over the hyperreal numbers, as was observed by [31], but has a lexicographic optimality property that is nonetheless appropriate for our matters of risk management. The details of this are postponed until Section 7, culminating in the main Theorem 14 that assures that we can ultimately escape the situation that proposition 8 warns us about. Interestingly, this fix has a useful side-effect, whose physical meaning is a heuristic account for zero-day exploits. We will revisit this aspect in more detail later in Section 7.2.

6 APTs as Games

Suppose that a TVA has been done and that an attack graph is available. Towards a game-theoretic model of APTs, let us think of the attack graph as sort of an extensive form game (EFG) with perfect information. Although the attack graph or tree may not follow the proper syntax of an EFG, we can nevertheless convert it into syntactically correct normal form game in the same way as we would do with an EFG. That is, we would traverse the graph from the initial stage of the game until the stage where payoffs are issued to all players. From the exhaustive list of all these paths, we can define the strategies of both players as rules about what to do at which stage, given the other player’s move. Likewise, an APT would in this view be mounted along any of the existing paths from the root of the attack graph down to the goal, with the difference to EFG mostly being the fact that the “game” does not clearly define when the players are taking their moves (this is a conceptual difference to EFG, where the assignment of which player’s move it is part of the EFG description).

In both cases, EFG and APT attack graphs, we can compile a set of paths from the start to the finish, from which strategies for both players can be identified. While this identification comes from the definition of the EFG, for APTs, the strategies are delivered only for the opponent player 2, which is the attacker. Player 1, the defender, needs to derive its action set based on player 2’s actions . Table 4 summarizes the correspondence between EFG and APT attack trees.

| Extensive form game | Attack tree/graph |

|---|---|

| start of the game | root of the tree/graph |

| stage of the gameplay | node in the tree/graph |

| allowed moves at each stage (for the adversary) | possible exploits at each node |

| end of the game | leaf node (attack target) |

| strategies | paths from the root to the leaf ( attack vectors) |

| information sets | uncertainty in the attacker’s current position and move |

The nature of APTs induces a difficulty in the game specification here, since we usually do not know how deep the attacker may have penetrated into the system, and because of this, the current stage of the game is expectedly unknown to the defender. Countermeasures against exploits in each stage may be identified, but not always possible, feasible or successful. Allowing for a random outcome with the possible event of an action to fail elegantly tackles this issue in our setting.

If countermeasures have no permanent effect or are likely to fail, then we may need to repeat them. For example, a security training may cause only temporarily raised security awareness. Likewise, updating a software once is clearly useless unless the system is continuously kept up to date.

Given that the defense actions in must be repeated, we can set up a matrix game to tell us the best way to do so. Since precautions cannot be applied everywhere at all times, we need to define the game as one where the defender takes random moves, based on a hypothesis where the attacker may currently be. Alas, it would probably not be feasible to rely on Bayesian updating towards refining our hypotheses, since this assumes much data, i.e., many incidents to occur, and hence is exactly what APT mitigation seeks to prevent. Thus, many popular tools from game theory like perfect Bayesian equilibria or related appear unattractive in our setting.

To simplify the issue in general, let us assume that the defender can access all parts of the system (thus, take moves related to any stage of the game as defined by the attack tree), whereas the attacker can move only from its current location (node) to the successor (child node) location. The game play is thus a matter of the defender seeking the optimal way of applying its threat mitigation moves anywhere at random in the infrastructure, in an attempt to keep the adversary away from its target. Unlike a Bayesian or sequential game approach, the application of defense actions is not based on hypotheses of where the attacker currently is, but will assume a worst-case behavior of the attacker (thus, switching from the Bayesian towards the minimax decision theoretic paradigm).

For example, applying a patch at some point may close a previously established backdoor and send the adversary back to the start again. However, if the patch is currently unavailable, not effective or simply applied to the wrong machine, the defense move will have no effect at all. Towards modeling this uncertainty, let us first become more specific on what the payoffs in the example game will be.

Following the common qualitative risk assessments, we may define categories of risk depending on “how far away” the adversary is from its destination in the attack graph. Collecting the lengths of all paths listed in Table 3, we see that their lengths range between 4 and 8 nodes (including the start execute(0) and finish node full_access(2)). In any such case, we may simply map the distances to qualitative scores, such as Table 5 proposes here.

| Distance | Risk |

|---|---|

| 7…8 | low |

| 3…6 | medium |

| 0…2 | high |

The concrete mapping of distances to risk levels can, however, already induces uncertainty. For example, assume that an attacker has already gained execution privileges on machine 1 (denoted as execute(1) in the attack graph), then it may either continue its way on path 4 in Table 3 (via a remote FTP connection from machine 1 to machine 2; node ftp_rhosts(1,2)) or on path 5 in Table 3 (via an RSH connection from machine 1 to machine 2; node rsh(1,2)). On path 4, the distance to full_access(2) is 3 nodes (ftp_rhosts(1,2) rsh(1,2) local_bof(2)), while on path 5, the distance is only 2 nodes (rsh(1,2) local_bof(2)). In light of the a-priori specified mapping of distance to risk levels as in Table 5, the risk would be classified as either “medium” or “high”, depending on which path has been chosen. The usual stealthiness of APTs hence causes uncertainty in the risk assessment, which needs to be captured by a proper decision- or game-theoretic APT mitigation approach.

6.1 Identifying Mitigation Strategies

Having the attack graph and once attack vectors have been derived from it, all of which are collected in the adversary’s action space , the next step is the identification of mitigation strategies. This process is a standard phase in many risk management practices, and often based on known countermeasures against the identified threats (accounting for unexpected events is a matter of zero-day exploit handling, which we will revisit shortly in Section 7.2). Since the process of defining countermeasures is a task that highly depends on the attack vectors , we cannot define a general purpose procedure to identify here (it is individual and different for various infrastructures). For the sake of generality and conciseness of presentation in this work, let us therefore assume that all relevant defense actions are available and constitute the action set for the defender. It may well be the case that not all actions are effective against all threats, and neither may a designated countermeasure be necessarily effective against threat . In that case, we may pessimistically assume maximal damage to be likely in scenario . Matching all defenses in against all attack vectors in is a matter of defining the game’s loss distributions, which is the next step towards completing the game model in Section 6.2. To simplify the notation in the following, let us abstractly denote the action spaces as and , with the specific details of the -th defense and the -th attack for all being available in the risk management documentation (in the background of our modeling).

6.2 Defining the APT Game

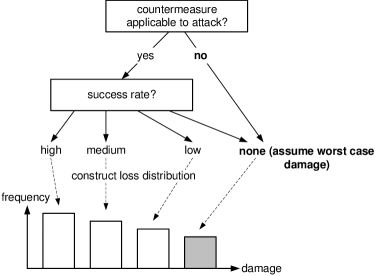

Towards a matrix game model of APTs, it remains to specify the outcome of each attack/defense scenario. To capture the intrinsic uncertainty here, we will resort to a qualitative assessment like sketched above and/or arising from vague opinions like Table 2 illustrates. The APT game is then defined upon loss distributions according to definition 2 to describe the potential loss in each scenario . In cases where we are unable to come up with a reasonable guess on the distributions, a pessimistic approach towards a worst-case assessment could work as follows (we will later revisit the issue in the discussion Section 10.2):

-

1.

Fix a particular position in the network, i.e., a certain point where an attack is considered. Let the hypothesized attack be the one with index .

-

2.

Fix a defense action .

-

3.

In lack of better knowledge, assume a uniform distribution of all possible , including , and rate the success probability of the defense conditional on (i.e., if your guess was right). This rating can also be made conditional on the expected “doability” of the current defense (e.g., if the defense means patching, the patch may not be available at all times, or it may be ineffective). Fig 6 displays the process as a decision tree, in which the worst case outcome (highlighted in gray) is taken if either the countermeasure is considered as possibly effective but may still fail (with a certain likelihood), or if the countermeasure is not applicable at all. In any case, the expert – based on the assumed attacker’s behavior – is not bound to confine her/himself to a single answer, and may rate all the possibilities with different likelihoods

-

4.

If possible, collect many such assessments (say, from surveys, simulations, etc.), and compile an empirical distribution from the available data. This empirical distribution is then nothing else than a histogram recording the number of uttered opinions (shown as the bar chart in Fig 6) Note that the uniformity assumption on the attacker’s location can be replaced by a more informed guess, if one is available. For example, the adversarial risk analysis (ARA) framework [52, 53, 54] addresses exactly this issue.

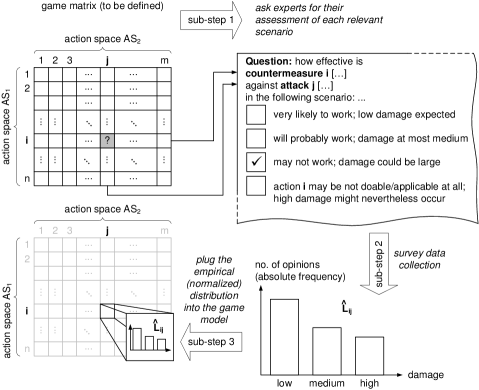

This procedure is repeated for the entirety of scenarios in , i.e., until the full game matrix has been specified. Fig 7 illustrates the three sub-steps per entry of this procedure in the game matrix (note that the right-most decision path (bold-printed in Fig 6) is reflected as the fourth choice option in the example survey shown in Fig 7). We stress that the full lot of may hardly be necessary to put to a survey, since not all actions are effective against one another (defenses may work against specific threats, so only a few combinations in need to be polled explicitly, and others can rely on default settings; cf. Fig 6). Furthermore, some loss distributions can be equally well computed from simulations (cf., e.g., [55]).

By construction of the total ordering, the game that we define to minimize the loss would then be played towards minimizing the likelihood for large damages (by Theorem 7). Returning to our example sketched in Section 3, the uncertainty in a risk level quantification based on distance in the graph would thus mean that the gameplay is such as to keep the adversary “as far away as possible” from its target. This is indeed what we would naturally expect, and the -relation acting on loss distributions that are based on distance achieve precisely this kind of defense.

Although this modeling of APTs is heavily based on (subjective) expertise and manual labour, it fits quite well into standard risk management processes (such as ISO 31000 [30] or ISO 27005 [56]), and nevertheless greatly simplifies matters of modelling over the classical approach, as a variety of issues are elegantly solved. A selection is summarized in Table 6, with a complementary discussion given in Section 10.2. Additional help in the specification of risk assessments is also offered by thinking about costs of an exploit or known ratings of vulnerabilities such as by common vulnerability scoring system (CVSS) [57]. Such ratings are commonly delivered along with the TVA (e.g., by tools like OpenVAS).

| Issue | Classical game-theoretic modelling | How this is handled in distribution-valued games |

|---|---|---|

| Payoff uncertainty | Either switching to special forms of equilibria (disturbed, trembling hands, etc.) or agreeing on a simultaneously representative value for all possible outcomes (“consolidation of different opinions”) | No consolidation or representation needed; we can simply work with the (normalized) histogram of all possible outcomes (or opinions on what could happen) |

| Non-realizable strategy | Separating out cases where a strategy can be played or not. This would amount to specifying two versions of the strategy (one that is successful and one that fails) | Since actions can by construction have many different outcomes, success and failure are just two realizations of the corresponding loss RV , each of which may occur with a known (or estimated) probability. The entirety of these probabilities makes the sought density function of the RV . |

| Imperfect information | Working with hypotheses on expected moves in stages of the game where no precise information is available. The hypotheses can be learnt from past history and are taken into account when defining the optimal behavior (e.g., Bayesian perfect equilibrium) | Is directly incorporated in the uncertainty of the outcome, since an unknown move corresponds in a perceived random payoff; thus, there is no intrinsic conceptual difference here |

| Random changes in the game-play (stochastic games [58]) | Resorting to special forms of equilibria, such as distorted or trembling hands equilibria or stochastic games [58, 48] | As long as the outcome remains identically (stationarily) distributed across several rounds of the gameplay, there is no specific treatment required upon random changes in the gameplay. The known theory of Markov chains can be used here to analyze the changes in the gameplay for stationarity. |

7 Practical Computation of Optimal Defenses

Essentially, our APT game model is a matrix game , in which each defense vs. each attack in is rated in terms of a probability distribution (uncertain outcome) . By defining the losses in the gameplay to be the gain for the adversary (i.e., making the competition zero-sum), we obtain a valid worst-case approximation that enjoys the following useful property:

Lemma 9.

Let be the action spaces for the defender and the attacker, respectively, with cardinalities and . Furthermore, let be the (unknown) matrix of true payoffs for the attacker, and let be the loss matrix for the defender. If the saddle-point values of the zero-sum matrix game is , and is any standard equilibrium payoff in the bimatrix game induced by , then we have:

| (4) |

provided that the defender plays a zero-sum equilibrium strategy (induced by ) in both games, the zero-sum game and the bi-matrix game .

Lemma 9 directly follows from the definition of standard Nash equilibria, and is a well known fact; cf. [18] for a more elaborate discussion. The computation of equilibria in the sense of Lemma 9 requires hyperreal arithmetic, but lexicographic Nash equilibria are computable by conventional means only, and the bound in (4) then remains valid w.r.t. a descending order of categories on the loss scale. This is nothing but a risk-averse optimization of worst-case outcomes.

Intuitively, Lemma 4 says that the worst case attack occurs when the adversary’s incentives are exactly opposite to our own interest. In particular, observe that the upper bound (4) is independent of the adversary’s payoff/incentive structure , and optimizes the chances to suffer worst-case losses (and breaking ties by optimizing the losses in descending order of categories). The irrelevance of in the upper bound tells that we do not require any information about the adversary’s intentions or incentives, as can be determined only based on the defender’s possible losses, and for a lexicographic order of losses, corresponding to a worst-case avoiding defense. Thus, in playing the zero-sum defense we obtain a baseline security that is guaranteed irrespectively of how the adversary behaves, provided it acts only within its action set . The case of unexpected behavior, that is, actions outside , corresponds to an unforeseen zero-day exploit. A remarkable feature of the game model using distribution-valued payoffs is its natural account for such outcomes, which we will further discuss in Section 7.2.

Our use of non-standard calculus somewhat limits the practically doable arithmetic, since for example, divisions in require an ultrafilter to fully describe (which is unavailable since is defined non-constructively; see [44]). Fortunately, however, these issues do not apply for our matrix games here, since lexicographic Nash equilibria can still be computed by fictitious play (FP) [50, 49, 59] which uses practically doable -comparisons only. The unpleasant possibility of non-convergent FP (proposition 8 warns us about this) is escaped by using non-parametric (kernel density) models for the payoff distributions, and using Lemma 18 to decide . The respective details are laid out in section 7.1. This closes a gap left open in [60].

7.1 Computing Optimal Defenses (Equilibria)

To avoid proposition 8 to apply for our APT-games, we need to assure that all loss distributions share the same support (the counterexample used to prove proposition 8 relies on different losses whose supports that are strictly contained in one another). To this end, we will introduce another representation of a loss distribution as a sequence, so that the lexicographic ordering on the new sequence equals the -ordering of definition 3.

To make things precise, let us assume that a particular empirical loss distribution has been compiled from the data , as obtained from simulations or expert questionnaires. Moreover, assume that is categorical, so that the underlying data points (answers) can be ranked within a finite range (in the example in Fig 7, we have three categories, e.g., {“low”, “medium”, “high”}, which correspond to the ordered ranks ). The case when the loss distributions is continuous is in fact even simpler, and discussed later in remark 10. For now, let us stick with the expectedly more common practical case where risk assessments are made in categories rather than hard figures.

First, the empirical distribution (normalized histogram) is replaced by a kernel density estimator (KDE) using Gaussian kernels of a fixed bandwidth to define

| (5) |

where

-

•

is the standard Gaussian function,

-

•

and is a bandwidth parameter that can be estimated using (any) standard statistical rule (of thumb, e.g., Silverman’s formula [61]).

Although any such nonparametric estimation can be quite inaccurate, yet as the data on which it is based is subjective anyway, the additional approximation error may not be as significant (nor in any sense quantifiable; still, Nadaraja’s theorem (see [62]) would assure that a continuous unknown underlying loss distribution would be approximated arbitrarily well in probability, as , provided that is chosen as for any two constants and .)

Using the KDE (5), we can cast the distribution-valued game back into a regular matrix-game over the reals. Note that in choosing Gaussian kernels, we naturally extend all density functions to the entirety of . Such distributions would not be losses in the sense of definition 2, as the supports are no longer bounded.

Using the aforementioned risk acceptance threshold to truncate all loss distributions at , casts the loss distributions into the proper form. We can then expand the (truncated) loss density into a Taylor series for every scenario . To ease notation in the following, let us drop the double index and simply write to mean the kernel density approximation of the empirical distribution in the given scenario, based on data samples. Then, its Taylor series expansion at point is

| (6) |

which converges everywhere on by our choice of the Gaussian kernel. The -th inner derivative is obtained from the kernel density definition (5) as,

| (7) |

Here, our use of Gaussian density pays a second time, since the -th derivative of the exponential term can be expressed in closed form using Hermite polynomials by exploiting the relation

| (8) |

in which is the -th Hermite polynomial, defined recursively as upon and . Plugging (8) into (7), and after rearranging terms, we find

| (9) |

Evaluating the derivatives up to some order and substituting the values back into (6), we could numerically construct the kernel density estimator. Fortunately, there is a shortcut here to avoid this, if we use the vector of derivatives with alternating signs to represent the Taylor-series expansion, and in turn the KDE, by

| (10) |

where the entries of the sequence can be computed from (9).

Interestingly, under the assumptions made (i.e., truncation at a point and approximating the empirical distribution by a Gaussian KDE), the lexicographic order on the series representation (9) equals the preference order on the hyperreal representation of the loss distribution (see Lemma 18 in the appendix for a proof). That is, we can decide between two sequence representations and of the form (10) as follows:

-

•

If , then . If , then . Otherwise, , and we check

-

•

if , then . If , then . Otherwise, , and we check

-

•

if , then , etc.

Remark 10 (Continuous loss models).

If a continuous loss model is specified, differentiability may be not be an issue if the density has derivatives of all orders. Otherwise, we can convolve by a Gaussian density with small variance to get an approximation at any desired precision. Kernel density estimates are exactly such convolutions and thus provide convenient differentiability properties here.