From prediction markets to interpretable collective intelligence

Abstract.

We outline how to create a mechanism that provides an optimal way to elicit, from an arbitrary group of experts, the probability of the truth of an arbitrary logical proposition together with collective information that has an explicit form and interprets this probability. Namely, we provide strong arguments for the possibility of the development of a self-resolving prediction market with play money that incentivizes direct information exchange between experts. Such a system could, in particular, motivate simultaneously many experts to collectively solve scientific or medical problems in a very efficient manner. We also note that in our considerations, experts are not assumed to be Bayesian.

Key words and phrases:

wisdom of crowd, consensus probability, play-money prediction market, self-resolving prediction market, non-Bayesian learning, Nash equilibrium, lottery dependent utility, double relativity principle1. Introduction

Suppose we have a proposition that may be either true or false. Our goal is to provide strong arguments for the possibility of the creation of a system that can elicit, from an arbitrary group of experts, the probability of the truth of the proposition together with the relevant collective information in a comprehensible form. This information will fully substantiate (interpret) the group probability. More precisely, we outline a way to create a self-resolving prediction market with play money that, in addition, incentivizes direct information exchange between experts. This simultaneously solves the following three problems:

-

•

information exchange in an ordinary prediction market may be broken;

-

•

all information aggregated by an ordinary market is encoded in the final price, which is a non-interpretable value between and ;

-

•

we can resolve an ordinary market and distribute gains and losses only after it becomes publicly known whether the proposition in question is true or false.

Since the proposed system overcomes these limitations, it could incentivize experts from all over the world to brainstorm scientific or medical problems in a very efficient manner.

We say that a prediction market is self-resolving if it distributes final gains and losses relying on its internal state and does not need verifiable ground truth for that. We borrow this term from [1, 2], where similar markets are experimentally studied in another context. Another example of self-resolving markets is described in [3]. Different approaches to the situation where ground truth is non-verifiable, are developed, for example, in [4] or in [5]. We note that in addition to the admissibility of non-verifiable ground truth, our proposed system could enhance the dynamic mutual learning of experts through price (a core property of prediction markets) into a direct exchange of knowledge of arbitrary nature.

Note that even conventional prediction markets have proved to be useful in science and medicine, for example, for making diagnosis in complex medical cases [6], for forecasting the spread of infectious diseases [7], or even for solving some general scientific problems [8]. We could meet the same challenges with our system, while taking full advantage of the self-resolvability and interpretability properties. In fact, these properties remove any restrictions on the range of problems that can be addressed with the system.

We could even try the following general approach. For any problem, we could put into the system a logical proposition that the problem will be solved after collecting information in the system (surely, we need to describe exactly what we mean by “will be solved”). The system will incentivize experts to share reasoned arguments about what obstacles might be in solving the problem, or what might help to overcome known difficulties and to solve it anyway. The final result will be an aggregated information concerning the problem, together with the probability that it will be solved, given this information.

Later, we will provide some preliminaries on regular prediction markets. If the reader is already familiar with this concept, the following preliminary intuition about the system we propose may be also helpful.

-

•

We consider a binary prediction market and offer experts to trade as if it were related to a certain proposition that may be either true or false.

-

•

At the same time, we make it public that final gains and losses will actually be distributed in accordance with a binary random generator with the probability parameter equal to the final price in the market.

-

•

We assume that the final price cannot be distorted by trading actions of any individual expert, but can be changed due to the actions of many experts. We will discuss how to achieve such a property in practice.

-

•

One of the possible strategies for an expert is the following. If an expert sees that his or her individual probability of truth of does not coincide with the current price, then he or she can make a transaction as if the market were resolved in accordance with , and after that share his or her information that explains why the current price is not fair with respect to the probability of . The purpose of information sharing is to change others’ beliefs on and, as a consequence, to favorably alter the final price, which will be the random generator parameter.

-

•

It can be seen that such strategies form a natural Nash equilibrium. In particular, this fact leads experts to follow our initial suggestion to behave as if the market were regular and related to .

In Section 3, we will provide a formal theoretical model that incorporates this intuition, and discuss its implementability. We note in advance that our models do not assume that experts are Bayesian, i.e. their beliefs do not need to be conditional probabilities.

2. Preliminaries

First, we present our basic notation, which is partially borrowed from [9] and is convenient for our non-Bayesian setting.

-

•

Suppose there is a proposition that may be revealed to be either true or false. This means that we have a propositional variable . By we denote a population of experts whose collective belief and information about we would like to obtain. Our object of study is the pair .

-

•

The notions of the truth and falsity of propositions can be formalized in terms of assignments to propositional variables. Let be a set of propositional variables. Then the notation means that is an assignment to , i.e. is a function from to . An assignment is also called a world. In particular, for the one-element set we have two assignments: the world where is true, and the world where is false.

-

•

We tell that worlds and are consistent (and write ) if they assigns the same values to the variables in : .

2.1. Experts’ probabilities

Assumption 2.1.

There exists a finite set such that for each expert , his or her probability of is a number that is completely determined by a certain subset , i.e. , where is a fixed set function from to . We call the elements of signals and call each set the knowledge of the expert . The experts’ probabilities of are determined in the same way by the set function . We also assume that .

In some cases it will be convenient for us to rely on the additional assumption that the elements of are propositional variables with certain values already assigned to them: there is collective information generated by the real world, and each expert knows the corresponding part of it determined by the relation (or, what is the same, by the identity ).

We may interpret as a set containing at least every signal that is

-

•

relevant to ,

-

•

is known to at least one of the experts,

-

•

and is not known to all the experts at once.

In other words, there are only irrelevant or public signals outside of . This somewhat vague interpretation becomes completely formalized if we consider Assumption 2.1 as a consequence of basic axioms that can be found in Appendix A: see Assumptions A.1–A.3 together with Proposition A.1.

We emphasize that the functional is not a conditional probability. However it may (but does not have to) be generated by a Bayesian model. Indeed, let . Consider the set of all possible assignments as a sample space. Let be a probability measure over . Any assignment to any subset can be associated with the event . This applies to the assignment as well as to any assignment for any (in particular, to and to itself). Relying on such associating and additionally assuming that , we could introduce our functional by the formula

| (1) |

2.2. Prediction markets

Suppose each expert possesses a certain amount of units that are valuable for him or her (real money or some play money). We use the following terminology (see, e.g., [10]).

Definition 2.1.

A contract on is the obligation that can be sold by one expert to another and that binds a seller to pay a buyer unit once it is revealed that is true.

We can associate with a prediction market where the experts would be trading contracts on with each other. The potential ability of the price in a prediction market to aggregate experts’ information and to converge to a collective probability of has been the subject of many empirical and theoretical studies. Below we provide a brief description of a classical Bayesian model, and many further details can be found in Appendix B.

But before the formal model, we informally describe an important example that is a slight variation of an example from [11] and shows how experts’ information and beliefs may vary during the trade even if the initial beliefs are identical. Suppose there is an event with three mutually exclusive outcomes , , and . Let be the proposition that has been realized. Suppose a random half of the experts know that has not been realized and the other half know that has not been realized. All the experts also know that a random half of them know about and the other half know about . If the experts reckon with the principle of indifference, they will have identical initial probabilities , . In this situation, any static probability aggregation scheme yields nothing better than . On the other hand, if the experts generate a prediction market and are sophisticated enough to judge about others’ probabilities by watching others’ behavior in this market, then their beliefs will change toward .

The discrete model of prediction market from [12] is one way to formally describe how the price and beliefs cease to fluctuate in a single consensus point, in particular in the -example. Here we provide those part of that model that is a direct consequence of the classical results of [13] that, in its turn, extend the line of research started in [14] (see also Appendix B.1 for further discussion of that model).

First, assume that we are in the Bayesian setting as it is described at the end of Section 2.1: there is a probability measure over , where is the set of all assignments to . Additionally assume that the sets are pairwise disjoint and that each of them consists of a single signal. Of course, in this situation we can use a more conventional notation. Namely, following [12] (see also the survey [15]), we consider the information structure

and bit arrays . This is the same as to consider a set consisting of propositional variables, with all possible assignments .

Assumption 2.2 (the model of Feigenbaum et al.).

-

(i)

A vector is the real state of the world ( in our notation), and each expert privy to one bit of information.

-

(ii)

The experts’ probabilities of (of in our notation) are conditional probabilities generated by a probability measure over such that (the world is not unexpected).

-

(iii)

There is a prediction market that proceeds in rounds. The clearing price is publicly revealed after each round, and it turns out to be the mean of the experts’ beliefs before the round.

-

(iv)

Such means are the only information channel between the experts.

-

(v)

All of the above is common knowledge (including the structure and the measure ).

By and we denote the experts’ beliefs before the -th round and the clearing price after it, respectively. We can write (iii) as

| (2) |

We note that (2) means that the price combines information exchange with averaging, which is more than can be said for the price in a real prediction market (see Appendix C).

By we denote the public information accumulated by the market for the first rounds:

where are the prices in a world (in particular, ). The information of an expert before the -th round is

and we have We note that events for may be irreducible to the partial assignments arising in (1), and, therefore, after the first round the corresponding probabilities may not always be described within the non-Bayesian context.

Since , there exists a moment when the information stops accumulating:

In [12], the authors notice that the results of [13] immediately imply that at each expert’s belief turns out to be independent of his or her own private information and all the beliefs stabilize at one point. Namely, we have the following proposition.

Proposition 2.1.

For all we have

| (3) |

Now we can formalize the -example as follows.

Example 2.1.

Suppose and , and set

If , then we have , , and .

Finally, we can state the obvious fact that nothing changes when some experts are ignorant.

Fact 2.1.

Consider a situation where the dimension of is strictly less than : experts privy to bits of as in (i) from Assumption 2.2, while remaining experts know no bits at all. We suppose (ii)–(v) from Assumption 2.2 remain fulfilled for all experts: in particular, both and are assumed to be common knowledge. Under these conditions, relation (3) remains valid and we can shorten (3) by dropping the second identity: it becomes a part of the first.

3. Main results

In fact, there is empirical evidence that prediction market prices are indeed able to aggregate information, but may fail to do so if they are the only information channel between the experts: see, for example, the study [8], which is also discussed in detail in Appendix B.6. The same study shows that direct information exchange could greatly improve the reliability of prediction markets, but does not offer a way to automatically induce such exchange. In addition to the possibility of broken information exchange through prices, there are the following two problems. First, we must reliably know the value of in order to resolve our market and to distribute gains and losses. This severely restricts the applicability of prediction markets. Second, consider an external ignorant observer who does not know the nature of experts’ information (in terms of the model discussed in Section 2.2, he or she does not know the probability space ). Then he or she sees prices, but cannot obtain the information that generates them: results are not interpretable. Below we present a theoretical non-Bayesian model that incorporates the idea that all these problems can (and should) be solved simultaneously. After that we discuss the possibility of its practical implementation.

3.1. Theoretical model of collective intelligence

First, we need a binary random generator that takes a parameter and returns either with probability or with probability . Here is a probability just in the sense that it is a parameter of our random generator, which can be of a physical or algorithmic nature. Concerning algorithmic randomness, see the survey [16, Section 2.6] with references to Knuth, Kolmogorov, Martin-Löf, von Mises, et al. Regardless of the implementation details, we formalize the generator as the parametric family of propositional variables which correspond to the following propositions: if we call the generator with parameter , then it will return . We also note that there are two assignments over each one-element set .

Now we are ready to present our model and its consequences. We emphasize that what follows is not the desired mechanism itself, but only its simplified model that incorporates the main properties of the system in question. The implementability of the system is discussed in Section 3.2.

Assumption 3.1 (a theoretical model of an interpretable self-resolving market).

-

(i)

We are within Assumptions 2.1, and there is a non-empty set of experts with only public or irrelevant knowledge: if , then

Initially, we have a prediction market where only the experts from participate.

-

(ii)

At the beginning of each round , the current participants from trade for a period of time and come to a price known to all the experts.

-

(iii)

After that, a new expert may join to by making a transaction at the price : he or she may choose whether to buy or to sell contracts. After that, the expert may either share all his or her private information with the other experts in , or remain completely silent (see also the discussion below). The next round begins with , and the public information is updated either as or as . The individual information of each is determined as .

-

(iv)

Since is finite, there exists a final round when no one wishes to join . After , we resolve the market (distribute gains and losses) in accordance with : each contract brings unit in the world and nothing in the world . If in a round an expert believes that111Hereinafter, the word “believes” means “takes for granted in the further logical inference”. If we would like to be even more formal, we can consider our experts as a calculus with an input (see [16, Section 1.3.1]). he or she exactly knows the value that will take, then he or she treats this value as the probability of . Hereinafter, we denote such a probability as (see (v) and (vi)).

-

(v)

All the experts are myopic and risk neutral in the following sense.

-

•

Any expert does not consider the situation where someone outside participates in the market. If someone else joins , this attitude is instantly carried over to , and so forth.

-

•

If the expert joins to and has a certain probability , then his or her expected profit on the joining transaction is strictly greater than zero:

(4) Here the sign depends on whether has bought or sold contracts, and is their quantity.

-

•

If there is an expert that can achieve (4), then the round cannot be the last.

-

•

-

(vi)

If during stage (ii) of a round , all the experts have probabilities and they coincide with each other and do not vary with time, then will coincide with them.

We provide arguments for our assumptions to be quite natural and weak.

First, we note that the model does not specify the order in which experts enter the market, but only assumes that trading cannot stop if there is an expert who believes that he or she can make a profitable transaction.

Concerning (ii) and (vi), the model makes no assumptions on the details of the way the experts trade (in particular, on the matching mechanism), but only the assumption that experts whose beliefs are constant and identical to one and the same value, generate the price equal to that value.

Concerning (iii), we will see below that the purpose of sharing information is to change others’ beliefs and, as a consequence, to profitably change . In order to achieve this goal in reality, an expert should confirm the truth of the information provided. For example, if the source information is a result of the expert’s study, he or she may provide its verified copy: a publication in a peer-reviewed journal. In the above model we identify the expert’s information with its verified copy that is transmitted to others. Transmitting unverifiable information is identified with silence. This is a deliberate modeling simplification: here we only show that under certain conditions, fully and accurately disclosing an expert’s true information is at least preferable for him or her to being totally silent. In Appendix C.5, we discuss the real situation in its entirety.

Concerning (v), we note that the myopia assumption is natural in a context where an expert knows nothing about those who are outside (even about their existence). Certain forms of myopia and risk neutrality are also featured in [12, 15].

Definition 3.1.

We say that the market in Assumption 3.1 is efficient if the following holds for all the rounds .

-

(eff1)

Each expert has shared all his or her information.

-

(eff2)

All the experts rely in their trading on their mental probabilities of . Namely, we have that during stage (ii), the experts have the probabilities and they coincide with the corresponding probabilities .

-

(eff3)

The joining transactions are also regulated by the experts’ probabilities of :

-

•

if there is with , then ;

-

•

an expert with does not wish to join .

-

•

If the market in question is efficient, then it is in a certain form of a Nash equilibrium. Namely, we have the following result.

Theorem 3.1.

Suppose during all the rounds , an expert believes

- (m1)

-

(m2)

that he or she cannot resist the concerted actions of others in the sense that the set is not empty and (vi) is true even when substituting for .

Proof.

Suppose the expert silently joins . Due to (m1), he or she believes that during stage (ii) of the round , the probabilities coincide with for , where

Due to (m2) and the myopia described in the first item of (v), the expert believes

Therefore, we obtain that when the expert enters the market, he or she has

| (5) |

and thus the expected profit on his or her joining transaction is zero. This contradicts the second item of (v), and thus satisfies (eff1).

Suppose the expert belongs to and is at stage (ii) of the round . We have just proved that he or she has shared his or her information and believes

The myopia of , together with assumptions (m1) and (m2), implies that believes

Namely, he or she has

and satisfies (eff2).

First, we note that item (m2) concerns a robustness property that is fulfilled if, for example, the price can be calculated as the median of beliefs. This can be seen as a model of the real situation discussed in Appendix C.5, where we rely (instead of the price) on the so-called market-driven median of experts’ beliefs.

Second, we note that it may be expected that the described equilibrium will naturally arise if we publicly offer the experts to trade as though the market will be resolved in accordance with , and to share their information in order for the system to be able to model this.

Finally, we obviously have the following analogue of (3).

Fact 3.1.

If the market in Assumption 3.1 is efficient, then

| (6) |

This means that for each , the information is either a part of , or the expert does not understand how may affect . It is also important (!) that the information has been directly revealed by experts, does not requires computing skills to be elicited, and is fully accessible to any external observer.

Since the subset of experts with is not empty, we can make a remark similar to Fact 2.1.

Fact 3.2.

We can shorten (6) by dropping the second identity: it is a part of the first.

In the -example, the experts have certain information about each other, and there are no ignorant experts with only common signals. These two facts do not allow us to incorporate this example directly into the setting of Assumption 3.1. But making appropriate adjustments, we come to the following situation.

Example 3.1.

Suppose , , and are mutually exclusive and exhaustive outcomes and this fact is known to all the experts in . Let , , and be propositional variables corresponding respectively to the propositions that , , or has been realized. Suppose and are false. Formally, we have

We also assume that for any , the set is or or . If the mechanism described in Assumption 3.1 arises (in particular, ) and it is efficient, then we will have , , and .

Indeed, during the first round ignorant experts generate the price , and one of the experts with or has to enter the market and to share his or her information. Therefore, the second round results in , there exists an expert with , and one of such experts has to enter the market and to share the remaining information. Thus, we have and the third round ends with .

3.2. Implementability

Here we very briefly describe how the ideas presented in Section 3.1 can be implemented in reality. In particular, we discuss how to achieve the robustness property (m2) from Theorem 3.1. The detailed description can be found in Appendix C (see also Appendix B, which introduces some necessary notation).

-

•

First, we can describe, relying on the detailed data collected from sports prediction markets, a data-driven model of how real experts behave in regular continuous prediction markets (see details in Appendices C.1–C.4). We can show that an algorithm based on that model can be applied to the data in order to get a value that effectively predicts the consensus probability. Such an estimate can play the role of a price that cannot be affected by trading actions of an individual expert. The assumptions of that continuous model have been themselves derived from the data, but at the same time they make perfect sense in terms of modern economic theory.

-

•

We can present (see Appendix C.5) not fully mathematically rigorous but quite detailed arguments showing that using our data-driven model of a regular prediction market and the corresponding algorithm for robust estimation of consensus probability mentioned above, we can transfer to reality the principles contained in our theoretical model of a self-resolving market. Thus, we can make a strong case that it is possible to create the desired system.

Now we provide some additional insight into the mentioned data-driven model of a regular continuous prediction market and the corresponding algorithm for estimating the consensus probability. In order to combine information exchange in a prediction market and averaging of experts’ probabilities, we introduce (see Appendices B.2–B.4) the notion of the market-driven median of experts’ opinions. For each expert , it takes into account the entire history of how his or her mental probability has varied during his or her trading and learning (accumulation of information) in a continuous prediction market. It also assigns certain weights to all values in accordance with the trading activity of each expert from at each time . In the definition of the market-driven median time runs a large hypothetical interval during which trading can potentially continue. However, it turns out (see Appendices C.1–C.4) that it does not require much time to effectively estimate : under certain model assumptions, we can derive from market data an estimate that stabilizes much faster than the clearing price . We can also show that within these assumptions the data are consistent with the hypothesis that , , and all converge to one and the same value as (cf. (3) given Fact 2.1).

The mentioned model assumptions are themselves derived from the data, and the key one concerns the utility function of the experts in question. It turns out to be non-standard and only locally satisfying the classical von Neumann–Morgenstern axioms. Let lotteries be finite probability distributions over : they assign probabilities to experts’ possessions. In particular, experts’ trading actions lead to various lotteries. Consider an expert with a budget and consider all the lotteries with together with the inaction lottery with . Here and are the minimum and maximum possible possessions of the expert due to . Thus, we exclude from consideration all the lotteries where win is possible and loss is impossible or vice versa. We introduce the lottery dependent utility function

| (7) |

We also pass to the limit and set . When the expert relies on this function to compare the lotteries under consideration, we say that he or she is subject to the double relativity principle: the scale of the possible results is considered relatively to its minimum and maximum , and the scale of utility is considered relatively to the expert’s status quo in the denominator of (7). We note that such functions do not fit into the existent theories of lottery dependent utilities (such as [17, 18, 19]). We detail how function (7) describes experts’ behavior in Appendix C and continue to discuss it (together with appropriate axioms) in Appendix D.

References

- [1] K. Ahlstrom-Vij and N. Williams “Self-resolving Information Markets: An Experimental Case Study” In J. Predict. Markets 12.2, 2018, pp. 47–67 DOI: 10.5750/jpm.v12i2.1555

- [2] K. Ahlstrom-Vij “Self-resolving Information Markets: A Comparative Study” In J. Predict. Markets 13.1, 2019, pp. 29–49 DOI: 10.5750/jpm.v13i1.1687

- [3] E. Dahan et al. “Securities Trading of Concepts (STOC)” In J. Mark. Res. 48.3, 2011, pp. 497–517 DOI: 10.1509/jmkr.48.3.497

- [4] D. Prelec “A Bayesian Truth Serum for Subjective Data” In Science 306.5695, 2004, pp. 462–466 DOI: 10.1126/science.1102081

- [5] A. Baillon “Bayesian markets to elicit private information” In Proc. Natl. Acad. Sci. U.S.A. 114.30, 2017, pp. 7958–7962 DOI: 10.1073/pnas.1703486114

- [6] A… Meyer, C.. Longhurst and H. Singh “Crowdsourcing Diagnosis for Patients With Undiagnosed Illnesses: An Evaluation of CrowdMed” In J. Med. Internet Res. 18.1, 2016, pp. e12 DOI: 10.2196/jmir.4887

- [7] P.. Polgreen, F.. Nelson, G.. Neumann and R.. Weinstein “Use of Prediction Markets to Forecast Infectious Disease Activity” In Clin. Infect. Dis. 44.2, 2007, pp. 272–279 DOI: 10.1086/510427

- [8] J. Almenberg, K. Kittlitz and T. Pfeiffer “An Experiment on Prediction Markets in Science” In PLOS ONE 4.12, 2009, pp. 1–7 DOI: 10.1371/journal.pone.0008500

- [9] J. Williamson “Philosophies of Probability” In Handbook of the Philosophy of Mathematics North Holland: Elsevier, 2009, pp. 493–533 DRAFT: https://blogs.kent.ac.uk/jonw/files/2015/04/philprob2009.pdf

- [10] C.. Manski “Interpreting the Predictions of Prediction Markets” In Econ. Lett. 91.3, 2006, pp. 425–429 DOI: 10.1016/j.econlet.2006.01.004

- [11] C.. Plott and S. Sunder “Rational Expectations and the Aggregation of Diverse Information in Laboratory Security Markets” In Econometrica 56.5, 1988, pp. 1085–1118 DOI: 10.2307/1911360

- [12] J. Feigenbaum, L. Fortnow, D.. Pennock and R. Sami “Computation in a distributed information market” In Theor. Comput. Sci. 343.1–2, 2005, pp. 114–132 DOI: 10.1016/j.tcs.2005.05.010

- [13] L.T. Nielsen et al. “Common knowledge of an aggregate of expectations” In Econometrica 58.5, 1990, pp. 1235–1238 DOI: 10.2307/2938308

- [14] R.. Aumann “Agreeing to Disagree” In Ann. Stat. 4.6, 1976, pp. 1236–1239 DOI: 10.1214/aos/1176343654

- [15] D.. Pennock and R. Sami “Computational Aspects of Prediction Markets” In Algorithmic Game Theory Cambridge: Cambridge University Press, 2007, pp. 651–676 DOI: 10.1017/CBO9780511800481.028

- [16] V.. Uspensky and A.. Semenov “Algorithms: Main Ideas and Applications” Dordrecht: Springer, 1993 DOI: 10.1007/978-94-015-8232-2

- [17] J.. Becker and R.. Sarin “Lottery Dependent Utility” In Manag. Sci. 33.11, 1987, pp. 1337–1382 DOI: 10.1287/mnsc.33.11.1367

- [18] M. Cohen “Security level, potential level, expected utility: A three-criteria decision model under risk” In Theory Decis. 33.2, 1992, pp. 101–134 DOI: 10.1007/BF00134092

- [19] U. Schmidt “Lottery Dependent Utility: a Reexamination” In Theory Decis. 50.1, 2001, pp. 35–58 DOI: 10.1023/A:1005219005058

- [20] P.. Fishburn “The Axioms of Subjective Probability” In Stat. Sci. 1.3, 1986, pp. 335–345 DOI: 10.1214/ss/1177013611

- [21] G. Parmigiani and L… Inoue “Decision Theory: Principles and Approaches” John WileySons, 2009

- [22] R.. Nau “De Finetti was Right: Probability Does Not Exist.” In Theory Decis. 51, 2001, pp. 89–124 DOI: 10.1023/A:1015525808214

- [23] R.. Cox “Probability, Frequency and Reasonable Expectation” In Am. J. Phys. 14.1, 1946, pp. 1–13 DOI: 10.1119/1.1990764

- [24] E.. Jaynes “Probability Theory: The Logic of Science” Cambridge University Press, 2003 DOI: 10.1017/CBO9780511790423

- [25] I. Arieli, Y. Babichenko and R. Smorodinsky “Robust Forecast Aggregation” In Proc. Natl. Acad. Sci. U.S.A. 115.52, 2018, pp. E12135–E12143 DOI: 10.1073/pnas.1813934115

- [26] J. Williamson “Objective Bayesianism, Bayesian conditionalisation and voluntarism” In Synthese 178.1, 2011, pp. 67–85 DOI: 10.1007/s11229-009-9515-y

- [27] A. Tversky and D. Kahneman “Judgment under Uncertainty: Heuristics and Biases” In Science 185.4157, 1974, pp. 1124–1131 DOI: 10.1126/science.185.4157.1124

- [28] D. Kahneman and A. Tversky “Intuitive Prediction: Biases and Corrective Procedures”, 1977 CITESEERX: 10.1.1.469.2095

- [29] B. Finetti “Foresight: Its Logical Laws, Its Subjective Sources” In Breakthroughs in Statistics New York: Springer, 1992, pp. 134–174 DOI: 10.1007/978-1-4612-0919-5˙10

- [30] J.. Kadane and R.. Winkler “Separating Probability Elicitation From Utilities” In J. Am. Stat. Assoc. 83.402, 1988, pp. 357–363 DOI: 10.2307/2288850

- [31] R.. Clemen and R.. Winkler “Aggregating Probability Distributions” In Advances in Decision Analysis: From Foundations to Applications Cambridge: Cambridge University Press, 2007, pp. 154–176 DOI: 10.1017/CBO9780511611308.010

- [32] A.. Palley and J.. Soll “Extracting the Wisdom of Crowds When Information Is Shared” In Manag. Sci. 65.5, 2019, pp. 2291–2309 DOI: 10.1287/mnsc.2018.3047

- [33] D. Prelec, H.. Seung and J. McCoy “A solution to the single-question crowd wisdom problem” In Nature 541, 2017, pp. 532–535 DOI: 10.1038/nature21054

- [34] C. Peker “Extracting the collective wisdom in probabilistic judgments” In Theory Decis., 2022 DOI: 10.1007/s11238-022-09899-4

- [35] L. Page and R.. Clemen “Do prediction markets produce well-calibrated probability forecasts?” In Econ. J. 123.568, 2013, pp. 491–513 DOI: 10.1111/j.1468-0297.2012.02561.x

- [36] D.. Pennock, S. Lawrence, C.. Giles and F.. Nielsen “The Real Power of Artificial Markets” In Science 291.5506, 2001, pp. 987–988 DOI: 10.1126/science.291.5506.987

- [37] E. Servan‐Schreiber, J. Wolfers, D.. Pennock and B. Galebach “Prediction Markets: Does Money Matter?” In Electron. Mark. 14.3, 2004, pp. 243–251 DOI: 10.1080/1019678042000245254

- [38] E.. Rosenbloom and W. Notz “Statistical Tests of Real-Money versus Play-Money Prediction Markets” In Electron. Mark. 16.1, 2006, pp. 63–69 DOI: 10.1080/10196780500491303

- [39] M.. DeGroot and S.. Fienberg “Assessing probability assessors: calibration and refinement” In Theory and Related Topics III Academic Press, 1982, pp. 291–314

- [40] R. Forsythe and R. Lundholm “Information Aggregation in an Experimental Market” In Econometrica 58.2, 1990, pp. 309–347 DOI: 10.2307/2938206

- [41] R. Hanson “Logarithmic market scoring rules for modular combinatorial information aggregation” In J. Predict. Markets 1.1, 2007, pp. 3–15 DOI: 10.5750/jpm.v1i1.417

- [42] A.. Osipov and N.. Osipov “Data and scripts for collective intelligence research”, 2023 DOI: 10.5281/zenodo.8308376

- [43] R Core Team “R: A Language and Environment for Statistical Computing”, 2021 R Foundation for Statistical Computing URL: https://www.R-project.org/

- [44] H. Wickham “ggplot2: Elegant Graphics for Data Analysis” New York: Springer, 2016 DOI: 10.1007/978-0-387-98141-3

- [45] A.. Shiryaev “Probability” New York: Springer, 1996 DOI: 10.1007/978-1-4757-2539-1

- [46] J. Wolfers and E. Zitzewitz “Interpreting Prediction Market Prices as Probabilities”, 2006 DOI: 10.3386/w12200

- [47] N.. Weinstein “Unrealistic optimism about future life events” In J. Pers. Soc. Psychol. 39.5, 1980, pp. 806–820 DOI: 10.1037/0022-3514.39.5.806

- [48] D. Dillenberger, A. Postlewaite and K. Rozen “Optimism and Pessimism with Expected Utility” In J. Eur. Econ. Assoc. 15.5, 2017, pp. 1158–1175 DOI: 10.1093/jeea/jvx002

- [49] E. Weinstock and D. Sonsino “Are risk-seekers more optimistic? Non-parametric approach” In J. Econ. Behav. Organ. 108, 2014, pp. 236–251 DOI: 10.1016/j.jebo.2014.10.002

- [50] D. Ellsberg “Risk, Ambiguity, and the Savage Axioms” In Q. J. Econ. 75.4, 1961, pp. 643–669 DOI: 10.2307/1884324

- [51] C.. Fox and A. Tversky “Ambiguity Aversion and Comparative Ignorance” In Q. J. Econ. 110.3, 1995, pp. 585–603 DOI: 10.2307/2946693

- [52] А.. Харкевич “О ценности информации [On the value of information]” In Проблемы кибернетики 4, 1960, pp. 54–58

- [53] P. Rocchi and A. Resca “The creativity of authors in defining the concept of information” In J. Doc. 74.5, 2018, pp. 1074–1103 DOI: 10.1108/JD-05-2017-0077

- [54] R. Hanson, R. Oprea and D. Porter “Information aggregation and manipulation in an experimental market” In J. Econ. Behav. Organ. 60.4, 2006, pp. 449–459 DOI: 10.1016/j.jebo.2004.09.011

- [55] L. Jian and R. Sami “Aggregation and Manipulation in Prediction Markets: Effects of Trading Mechanism and Information Distribution” In Manag. Sci. 58.1, 2012, pp. 123–140 DOI: 10.1287/mnsc.1110.1404

- [56] K.. Leung, R.. Elashoff and A.. Afifi “Censoring Issues In Survival Analysis” In Annu. Rev. Public Health 18, 1997, pp. 83–104 DOI: 10.1146/annurev.publhealth.18.1.83

- [57] A. Othman and T. Sandholm “Profit-Charging Market Makers with Bounded Loss, Vanishing Bid/Ask Spreads, and Unlimited Market Depth” In Proceedings of the 13th ACM Conference on Electronic Commerce, EC ’12, 2012, pp. 790–807 DOI: 10.1145/2229012.2229074

- [58] S. Gjerstad “Risk Aversion, Beliefs, and Prediction Market Equilibrium”, 2004

- [59] M. Ottaviani and P.. Sørensen “Aggregation of Information and Beliefs in Prediction Markets”, 2007 CITESEERX: 10.1.1.224.8757

- [60] J.. Nelder and R. Mead “A simplex algorithm for function minimization” In Comput. J. 7.4, 1965, pp. 308–313 DOI: 10.1093/comjnl/7.4.308

- [61] W. Samuelson and R. Zeckhauser “Status Quo Bias in Decision Making” In J. Risk Uncertain. 1.1, 1988, pp. 7–59 DOI: 10.1007/BF00055564

- [62] Y. Masatlioglu and E.. Ok “Rational choice with status quo bias” In J. Econ. Theory 121.1, 2005, pp. 1–29 DOI: 10.1016/j.jet.2004.03.007

- [63] D. Kahneman and A. Tversky “Prospect Theory: An Analysis of Decision under Risk” In Econometrica 47.2, 1979, pp. 263–291 DOI: 10.2307/1914185

- [64] В.. Успенский and А.. Семёнов “Теория алгоритмов: основные открытия и приложения” Москва: Наука, 1987

- [65] B. Finetti “La prévision : ses lois logiques, ses sources subjectives” In Ann. de l’inst. Henri Poincaré 7.1, 1937, pp. 1–68

- [66] А.. Ширяев “Вероятность” Москва: Наука, 1989

Appendix A Extension of Section 2.1

Here we detail what we mean by experts’ probabilities and information. There are many ways to assign personal probabilities to individuals: see the survey [20] or the book [21] with references to de Finetti, Ramsey, Savage, et al. Here we present a construction that is different from these theories and is more suitable for our goal of combining experts’ information as well as for separating probabilities from our unconventional utilities (7). In other words, we are inspired by the viewpoint of [9] rather than the one reflected in [22]. However we do not regard our construction as a philosophical system, but only as a preliminary model convenient for further considerations.

First, we give its brief description. We simply postulate that for any expert there exists a unique value in that is considered in our models as the expert ’s probability of . We do not fix what each expert means by his or her probability: this is determined, together with the probability itself, by objective signals the expert has received during the lifetime. Namely, we introduce a system of axioms that implies Assumption 2.1, i.e. that all these probabilities are values of a functional over , where is a finite set of objective signals, each of which is known to one or more experts in . These signals are units of raw information that have been generated directly by external events in the experts’ empirical experience. Below we formalize each signal as a propositional variable with a value already assigned to it. In fact, we can formalize signals as abstract elements of a set: we need propositional logic notation only to show (see Section 2.1) the relation between our construction and the classical Bayesian model of knowledge, which appears in various forms, e.g., in [23, 24, 14, 12, 15, 25]

In addition to the existence of a set and a functional over , our axioms imply that if a signal is known to an expert in and lies outside , then it is either known to all the experts in at once, or irrelevant to at all.

A.1. Objective beliefs

We fix a current time and attribute to it all the objects introduced below until Section B.2.

Assumption A.1 (existence axiom).

We assume that for each expert , there exists a unique value that is known to and is referred to as the expert ’s mental probability of . The expert ’s probability of exists in the same sense and equals .

We also refer to the values as beliefs. We provide Assumptions A.2 and A.3, which are partially inspired by [9] and incorporates the idea of the objectivity of beliefs. Informally, we would like to say that there exists a finite collection of objectively true signals such that an expert’s mental probability of is determined by those of them that are known to him or her. The informal concept of “an objectively true signal” suggests some dualism and independence from an expert. We formalize this concept as a propositional variable with a value already assigned to it: this value can be either or and cannot be different for different experts.

Assumption A.2 (signals objectivity axiom).

With each expert , we can associate a finite set of propositional variables with an assignment . We assume that for every . We set and denote by a unique assignment such that for all . For any , we can recombine any expert with the knowledge and obtain a new mental probability . Namely, Assumption A.1 is assumed to remain true for the modified expert . In particular, we have .

Assumption A.2 does not suggest the uniqueness of objects introduced in it. Suppose we have some constructed in accordance with Assumption A.2. Then any can be endowed with the structure inherited from : we can set

and define an expert recombined with within as recombined with

within . We have For any and connected in such a way, we write .

Assumption A.3 (beliefs objectivity axiom).

The mechanisms in Assumption A.2 may differ from each other only because of a finite number of the experts’ signals that are not included in . Namely, we can choose with the following property. For any satisfying Assumption A.2 and such that , the corresponding mechanisms do not depend on : . In particular, we have a single mechanism over itself.

The variables in with assigned values represent very basic objective signals without any derivations. In other words, the knowledge is ontological, not epistemological. We have a finite number of signals that binary encode the experts’ empirical experience consisting of outer events. These “raw” signals determine the experts’ knowledge on as well as how they derive their probabilities from this knowledge. In particular, we may assume that the presence or absence of certain ontological signals in an expert’s experience determine his or her epistemological language as well as his or her type of rationality or irrationality (e.g., Bayesian rationality as in [23, 24], or rationality based on the maximum entropy principle as in [9, 26], or irrationality as in [27, 28], and so forth). The ontological nature of the signals justifies the assumption that they may be considered separately from the experts. Assumption A.3 means that by “scooping out” such signals, we can come to a situation where all the experts are coherent and any signal outside is common to them or is irrelevant to . This statement acquires a precise meaning due to the following proposition.

Proposition A.1.

If satisfies Assumption A.2 and , then the following statements are equivalent.

-

(st1)

For any such that , the mechanisms do not depend on .

-

(st2)

The mechanisms do not depend on , and for any , we have

(8)

Proof.

Since we assume that satisfies Assumptions A.2 and A.3, Proposition A.1 implies that the value of is one and the same for all and we arrive at the following definition.

Definition A.1.

We call the collective probability.

Appendix B Extension of Section 2.2

B.1. Bayesian discrete model continued

As we have indicated, the first result of Feigenbaum et al. [12, 15] presented in Proposition 2.1 is not their main contribution: it is a direct consequence of the classical study [13]. Here we provide the second (and main) result of [12]. First, following [12] we assume that the experts believe they can completely restore from .

Assumption B.1 (Feigenbaum et al’s model continued).

We have

where is a given Boolean function.

The main result of [12] is the following fact that complements Proposition 2.1 and generalizes Example 2.1.

Theorem B.1.

Under additional Assumption B.1, a necessary and sufficient condition on that guarantees the identity

| (9) |

for any and any is the following. There must exist weights such that

| (10) |

For our part, we note that the existence of functions not satisfying (10) is not a problem in itself: the measure must, in addition, satisfy rather special conditions in order for identity (9) to be violated. For example, if consists of two experts and is the XOR function, then we have the following proposition (it would also be desirable to obtain its extension to the general case).

Proposition B.1.

Proof.

We denote . Under the condition

| (12) |

we have

This implies that if (11) and (12) hold, then , and that if (11) does not hold and (12) holds, then (9) holds. If (11) holds and (12) does not, then or , because the other four relations in (12) follow from (11), and we have . Any violation of (12) implies (9), and we have that if (11) and (12) does not hold, then (9) holds. ∎

B.2. Continuous prediction markets

In a real prediction market, trading goes on continuously in real time and experts’ behavior may be complex.

| Demand | Supply | |

The following method for elicitation of experts’ probabilities goes back to de Finetti [29] and may give some insight into how prediction markets work in reality. We ask an expert : what is the maximum price of one contract on at which he or she would agree to buy contracts? It is easy to see that the expert’s answer tends to as , provided his or her preferences are determined by and a von Neumann–Morgenstern utility function (see, e.g., the discussion in [30]). On the other hand, the impact of utilities (7) does not depend on and cannot be eliminated from the answer to de Finetti’s question in such a way. Nevertheless, in Section C we will see how this impact vanishes during trading in a prediction market.

Now we give the following formal definition, which describes a prediction market in reality.

Definition B.1.

A prediction market for is a sequence of orders where runs over a finite subset of . Each order means that at time , an expert claims that he or she is ready to buy (for orders with ) or to sell (for orders with ) contracts on by a price .

We assume that orders are matched with each other in real time by natural rules, i.e. that our prediction market is arranged as a continuous double auction (CDA). We skip the details of these rules, but note that at a moment we will see a situation shown in Table 1. Here

are all the prices with non-zero total demand or total supply of contracts at time . For any of these prices, the number of concluded transactions and the number of contracts available for immediate selling or buying, are

respectively. An expert may withdraw any portion of his or her offer that has not been matched yet. The bid price is the best price for immediate selling at time : it is the highest price where demand is greater than supply. The ask price is the best price for immediate buying at time : it is the lowest price where supply is greater than demand. By we denote the current clearing price: the price of the last concluded transaction.

B.3. Beliefs in a continuous prediction market

As a basis for further considerations in Section C, we consider a purely hypothetical, but imaginable experiment where all the experts in participate in a time-unlimited prediction market and where they are isolated from external signals (i.e., they receive information only from each other, e.g., via the market). The isolation of can be formalized as the constancy of the collective probability in the course of the experiment.

Assumption B.2 (continuous prediction market pre-model).

There is the possibility of an experiment satisfying the following conditions.

-

(i)

At the moment , all the experts in are given the opportunity to participate in a CDA-type prediction market for , and they know about that.

- (ii)

-

(iii)

The collective probabilities do not vary throughout the experiment:

-

(iv)

There is a moment when the last transaction is concluded: no orders are matched with each other during , where is a sufficiently large pre-announced timeout. We complete the experiment at and, after that, distribute awards once we know the value of .

We refer to the market from Assumption B.2 as the unlimited market.

Definition B.2.

We call the price of the last concluded transaction in the unlimited market the ultimate price.

B.4. Trading as weighted voting

It is worth noting that here we only introduce a certain convenient terminology and do not establish any relations with the voting theory, which is a part of the social choice theory.

Consider the total risks

for prices and times (see Table 1). We call units constituting these quantities votes for and votes for , respectively. Due to discrete nature of any operations with real or play money in any real or imaginable market, we can normalize and in such a way that they will become integers and each vote will correspond to a single expert who has placed it. Let be the set of size of all the votes at time . We note that since the experts may withdraw non-matched votes, it is possible that for . Suppose we are in the setting of the unlimited market from Assumption B.2. Let . We can assign to each vote the belief with which the corresponding expert has placed it at time .

Definition B.3.

We call the market-driven median of beliefs.

The market-driven median weighs the experts’ beliefs and takes into account information exchange between them. We can demonstrate that it is a better choice than the mean of . Suppose there is an expert who has understood that is true and, therefore, is ready to spend his or her entire budget on contracts on the truth of , buying them at any price . If he or she buys contracts at a price from another expert, then such a transaction will generate votes associated with the probability and votes associated with the probability . Therefore, the median of the corresponding probabilities will be equal to , while the mean will not.

B.5. Consensus conjecture

Here we formulate a conjecture that is a continuous counterpart of both

- •

- •

Conjecture B.1.

For any , we have

We announce that in Section C we build a model that allows us to elicit estimates of from real market data accumulated during intervals . Inter alia, the model has a parameter that measures how beliefs , , fluctuate on . The estimates quickly stabilize (become almost constant), while the estimates decrease. We note that the announced model implicitly implies that if we consider for as time series, then and will stop fluctuating simultaneously at the same level . We may assume that after this moment, the experts will have identical beliefs that will remain stable under information exchange. As in the discrete setting, the question of the coincidence between this stable shared belief and requires a separate discussion (see, e.g., the next section B.6).

It is also worth noting the following. Let stand for various static aggregation schemes that take as arguments only the initial probabilities (without involving external weights or information exchange between the experts). There is an extensive literature on the choice of in various situations. See, e.g., the survey [31] or the recent article [25]. We make general comments on the comparison of , , and static schemes as ways to approximate . The prices oscillate because of the fluctuations of , while the estimates remove, like any averaging, these fluctuations. On the other hand, unlike static averages , the estimates take into account information exchange between the experts: they may work in situations like the -example (see Section 2.2), where any returns nothing better than . Thus, the estimates combine the advantages of and .222 We also note that do not provide a way to operationally elicit its arguments from the experts, while the model for calculating solves the problem of operationalization as well. See also the studies [32, 33, 34], which propose alternative approaches to aggregating opinions.

B.6. Empirical evidence for

There is a crude (but supported by a vast amount of data) argument in favor of the hypothesis

| (13) |

Namely, there are many studies revealing the fact that last observed prices in prediction markets are well-calibrated (but with certain reservations; see, e.g., [35]). We refer to the articles [36, 37, 38] that confirm this fact both for prediction markets with real money and with play money. However the calibration is only indirectly related to the hypothesis in question: even if we reasonably suppose that and are both well-calibrated (i.e. that is not worse than the last observed price and is not worse than ), this will not imply the identity between them. Concerning calibration and refinement (a more subtle measure of forecast accuracy), see [39] or an exposition in [21, Section 10.4].

In order to provide a direct empirical verification of the hypothesis, we need to be able to directly calculate . This is partially possible only in a controlled experiment where we regulate (to some extent) the initial information of each expert. An interesting example is the study [8] (see also the classic studies [11, 40]), where the authors also support the idea of utilizing play-money prediction markets in the life sciences. Their experiment simulates the search for an answer to a scientific question (in what order three genes activate each other). There are differences from our setting: experts trade contracts of six types that correspond to six mutually exclusive outcomes , an automated market maker is used (see [41]), and new external information is revealed to experts in the course of trading (that means that the collective probabilities vary). Nevertheless, these differences do not reduce the importance of the discussed experiment to us. We briefly describe the situations that have been modeled in the course of it.

- Public setting:

-

The initial information on is public from the outset. We note that even in an experiment where the information is under control, it is impossible to make all identical. In addition to direct information on , each contains personal signals that determine how the corresponding expert processes such information. This explains why in [8], the prices have oscillated even in the public setting. Nevertheless, in such a setting the prices have become close to the collective probabilities that means that prediction markets at least do not “lose” public information.

- Private setting:

-

The information of each expert is private and is transmitted to others through the prices only. Six experimental markets have been organized in the private setting. In half of the cases, the markets have succeeded to aggregate information: the results do not contradict hypothesis (13). In three remaining markets the prices have not converged to the collective probabilities: better approximations have been obtained by deriving theoretical beliefs from the initial private information of each expert and by averaging them. It is reasonable to assume that estimates of the corresponding market-driven medians could give better results, provided we could elicit them from the market data.

- Mixed setting:

-

The information of each expert is initially private, but becomes public after a while (direct information exchange is simulated). All six corresponding markets have succeeded to aggregate information in such a setting. The results are almost the same as in the public setting.

Thus, we have empirical evidence that prediction market prices are able to aggregate information, but may fail to do so if they are the only information channel between the experts. As might be expected, direct information exchange can greatly improve the reliability of prediction markets.

Appendix C Extension of Section 3.2

Here we present the data-driven continuous model of regular prediction markets that has been repeatedly mentioned above, and show that within its framework, our data [42] do not contradict Conjecture B.1. We also show that there exist estimates of that converge rapidly and remain stable under trading actions of experts. We discuss how these facts can be exploited in order to create a real continuous self-resolving prediction mechanism with direct information exchange.

C.1. Data

Our goal is the creation of a collective intelligence based on play-money prediction markets and intended for use in science, medicine, and engineering. Nevertheless, for the construction and verification of our continuous model we need the extensive and detailed data [42] collected from CDA-type real-money prediction markets related to sporting events. The resulting model seems fairly general and independent of whether relates to sports or to science. Eventually we come to the consideration of a continuous self-resolving prediction market with play money.

| q | |||

| 0.4167 | 6.6 | 0.0 | |

| 0.4505 | 501.9 | 0.0 | |

| 0.4808 | 315.5 | 20.0 | |

| 0.4854 | 544.3 | 149.4 | |

| 261.5 | 261.1 | ||

| 0.4950 | 588.0 | 588.0 | |

| 304.1 | 668.3 | ||

| 0.5025 | 450.3 | 1007.9 | |

| 0.5051 | 8.2 | 8.2 | |

| 0.5076 | 926.3 | 926.3 | |

| 0.5102 | 1091.9 | 1561.0 | |

| 0.5128 | 405.8 | 630.9 | |

| 0.5155 | 73.6 | 73.6 | |

| 0.5181 | 48.4 | 63.8 | |

| 0.5236 | 0.0 | 13.0 | |

| 0.5263 | 0.0 | 2642.5 |

The data concern 24 soccer games of 2013–2014. Several markets are considered for each game, and each market contains several mutually exclusive outcomes. If there are more than outcomes in a market, then compound matching is possible and we cannot, generally speaking, reduce the situation to separate markets associated with separate propositional variables. But we have collected data for each outcome of each market separately. Such data contain the dynamics of demand and supply of contracts on the occurrence of the outcome (together with the volumes of concluded transactions). There may be transactions that have been concluded due to compound matching, but this is not reflected in the data and is not important for our model. Thus, the data for each outcome of each market fit into the pattern from Table 1, and it is possible to treat them as data of a separate market for a separate propositional variable (we can merge data if there are exactly complementary outcomes in a market).

Let represent one of outcomes from one of 96 markets related to one of 24 soccer games mentioned above. Let be the interval333At the pre-announced time all non-matched votes have been returned to the owners, and very shortly after that the corresponding soccer game have started (together with a so-called live market). where the corresponding market has existed. Then the data for can be represented as a collection of time series of volumes in dollars that have the same meaning as in Section B.4. Here runs over the finite (but quite dense) grid of all prices available for trading, and runs over an observation interval (where the changes of market state have been checked with frequency of approximately second and ). We note that for each , the corresponding aggregated data represent the whole interval , not only : we have started by obtaining and, after that, have scanned subsequent changes.

Repository [42] contains our PostgreSQL data and R scripts as well as the R workspace CI.RData where all the scripts and some data for two soccer events (see the data frames data12+ and All calls given in this article should be made from CI.RData. For example, the following call returns the data in the -form for an outcome of a French soccer event.

AggData(dat = data13, # 08 March 2014, Guingamp vs. Evian TG

outcome = 1, # Guingamp win outcome

time = 30*60) # t = t_1 + 30 min.

The result is partially shown in Table 2. It is fully consistent with Table 1.

C.2. Continuous model assumptions: probabilities

Suppose there is a prediction market for that exists during a pre-announced interval , generates volumes , and yields a sample of all the experts who add some orders to it during . The first two model assumptions concern the experts’ probabilities and connect the model with the pre-model described in Assumption B.2.

Assumption C.1 (connection with the pre-model).

We refer to the market that is introduced above and satisfies Assumption C.1, as the regular market.

In the regular market, we can, as in Section B.4, consider where runs over the sets of normalized votes. The next assumption postulates (inter alia) that in spite of a limited time and number of participants, the regular market is representative for the unlimited market from Assumption B.2 with respect to . Let and be the density and cumulative distribution functions of , and let be the delta measure concentrated at .

Assumption C.2 (beliefs normality and representativeness).

Let . We assume that votes have been generated by separate orders and that the values are i.i.d. with distribution . It is a modifications of the normal distribution with all the values outside the unit interval reset to the points and , i.e. with the density functions

We assume that does not depend on and represents the market-driven median that would generated by the unlimited market if it was started instead of the regular market at the same point :

The sample is what we initially have or what we can control. What a population it represents is a matter of common sense and situation, not mathematics. At least, we must have reason to believe that . In particular, we may set . If we talk about our data [42], they have been collected from the largest platform with sports CDA markets. Its numerous users represent most of the countries, and we may assume that is the population of all the people except some insiders.444We assume that coaches or team members do not participate in the trade.

Next, we note that in fact, Assumption C.2 generates a collection of models: for each interval , we have its own averaged dispersion of beliefs. Each such model concerns the aggregated data that include no time-related information on how these volumes have been produced during . In fact, we do not introduce here a stochastic process that accurately models the dynamics of , but rather make a certain ergodicity assumption: loosely speaking, there exist such that the quantities

become small as increases (cf. [45, Section V.3.4, Problem 3]).

Concerning the distributions , we note that they have the desired property that the values and are not excluded from consideration. See also [46, Figure 5], which empirically justifies our choice of distribution.

C.3. Continuous model assumptions: utilities

Here we rely on the lottery-dependent utility function that incorporates the double relativity principle and is defined by formula (7). We continue to discuss such functions in Section D.3.

Assumption C.3 (experts’ utilities).

Let , , be any order in the regular market. By we denote the budget of the expert that he or she has had immediately before placement of . We assume that in addition to , the expert associates with some values

that play, in accordance with inequality (14) below, the role of probabilities of the events “ will be completely matched” and “ will remain completely unmatched”, respectively. The alternative “ will be partially matched” is not considered at all. We consider the lottery that corresponds to the possible variations of the possession due to the order . We assume that placing , the expert believes (in terms of the double relativity) that is better than inaction. Namely, if is a buy order, then either or

| (14) |

where is the expected utility of the order as though it has been completely matched:

| (15) |

where

For a sell order, we swap with and with .

We make some comments on this assumption. First, the quantity is the result that the expert has expected, before placement of , from the market in the worst-case scenario. In other words, is the amount available for trading at time . The expert may be already involved in a lottery at time due to previous orders, but we assume that he or she thinks locally and decides whether to leave the amount untouched or to use a part of it in a new lottery (which is considered separately). We will see below that nothing depends on the values at all.

Second, the assumption that the expert does not believe the order may be partially matched is consistent with the fact that in Assumption C.2 we represent the market as a flaw of small “unit” orders.

By combining formula (7) for with relations (14) and (15) and by making simple equivalent transformations, we reach the following consequence.

Proposition C.1.

Let , and let be one of the votes constituting for some . Consider the order that have generated at time . We have

| (16) |

and satisfies Assumption C.3 if and only if

| (17) |

If is one of votes and is the corresponding order, then we have

| (18) |

and satisfies Assumption C.3 if and only if

| (19) |

Note that in Proposition C.1, nothing depends on , , or .

Hereinafter, we use some non-standard but convenient notation for certain limit relations. By the symbol we denote the relation “decreases to”. Formally speaking, “ as ” means that is an increasing function of and .

Assumption C.4 (connecting all together).

Suppose Assumptions C.2 and C.3 hold for our regular market. Fix and suppose runs over . We consider all the orders that have generated the votes in . In Assumption C.3, we take the identical parameters for all such . In addition, we assume that there is a fixed relation between and the parameters and (see Assumption C.2), provided . Namely, we have , where

is a certain function such that

| (20) |

Similar to the situation with , for each time we have a specific parameter applied to the whole interval . Subsequently, we use a specific function that is derived from certain conditions of economic equilibrium inspired by [10, 46]. It is constructed for not too large , but this does not prevent its use in any practical situation. Details are provided in Section D.2.

We have the following simple fact.

Fact C.1.

Under Assumption C.4, we have and

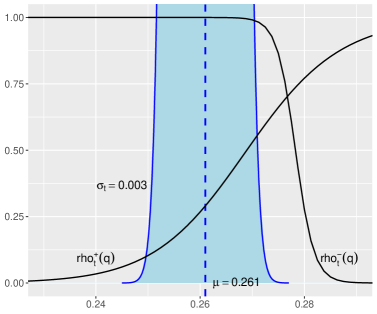

We can give the following interpretation of this fact. The less the dispersion of beliefs is, the less each expert expects that he or she does not know something that others do and that his or her probability can be refined. High confidence in his or her probability causes to be less deviating from it and to be less inclined to trade at unfavorable prices: to buy at or to sell at . An extreme example is where all the experts reliably know that represents a fair coin toss, and have no reason to be risk-seekers.

This can also be treated as follows. A possible gain or loss in a lottery connected with makes the outcomes and positive or negative for an expert who measures this lottery. This fact leads to optimism bias [47]. In other words, the expert ’s mental probabilities of winning and losing the lottery does not coincide with his or her probabilities and of the underlying outcomes. In this interpretation, Fact C.1 implies that less ambiguity leads to less optimism bias. For classical von Neumann–Morgenstern utilities, a similar relation between optimism/pessimism, risk seeking/aversion, and ambiguity is formalized in [48] (see also the experimental study [49]).

The optimistic behavior discussed above does not contradict ambiguity aversion [50], which is another well known behavioral characteristic of decision makers. Namely, an expert can always choose to wait until his or her comparative ignorance [51], causing the feeling of ambiguity, decreases. This is not the same as to choose inaction and to leave the market: we do not even measure the waiting alternative in terms of utility. The expert’s optimism also decreases, but at some point a certain lottery may become preferable to further waiting. We will see further that decreases over time together with the overall comparative ignorance. The tendency for experts to wait is confirmed by the fact that the intensity of trading increases over time.

C.4. Continuous model meets real data

Suppose represents one of the outcomes described in Section C.1 and the volumes represent the corresponding real data in [42]. Let be from the observation interval . We can calculate the probability of the event that satisfy inequalities (17) and (19) where runs over and all coincide with single . We interpret the logarithm of this probability as a log-likelihood function:

| (21) |

Certain issues concerning the validity of applying the function are discussed in Section D.1. It turns out that we can choose for which a numerical optimization of over and gives estimates and such that . Details of the corresponding algorithm can be found in Section D.2. Now we employ this approach to We make the following calls.

gr <- GetGraphOperTime(dat = data13, outcome = 1, voldlt = 1000)

PlotMuSgm(gr) # requires ggplot2 and grid.

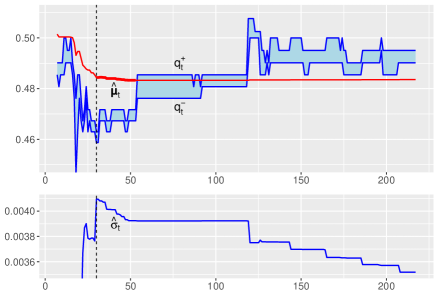

The result is shown in Figure 1, where all the graphs are presented in the operational time that corresponds to the total volume of votes:

The numbers under the graphs are the volume in thousands of dollars. The price oscillates somewhere between and , while oscillate themselves throughout . At the same time, the estimate quickly converges and remains extremely stable in spite of huge volumes of offers. The estimate measures the average variability of beliefs during . In Figure 1, it begins to decrease after has stabilized (after the dashed line).

Suppose and consider a price . Suppose we are within Assumption C.4 (which includes Assumptions C.2 and C.3), and suppose we begin to reduce . Then, due to Fact C.1, after a certain point we will have and will continue to shrink (together with the density of the distribution of beliefs around ). Therefore, according to (17), we will observe an unlimited decrease in the probability of occurrence of beliefs that could generate buy orders for . Again, due to Fact C.1 and (19), the same is true for sell orders for any price . Thus, informally speaking, a range of prices where concluded transactions are probable will shrink around . This reasoning, together with the constancy of and a developing decrease in observed in Figure 1, leads to the following conclusion.

Conclusion 1.

Consider the regular market, which is introduced at the beginning of Section C.2 and satisfies Assumption C.1. There exists its reasonable model (by which we mean Assumption C.4) such that our data, interpreted through this model, do not contradict the following hypothesis. In the unlimited market, which is introduced in Assumption B.2 and is partially implemented by the regular market, the beliefs would approaches , transactions would conclude at prices increasingly close to , and we would finally have

| (22) |

Conclusion 2.

The model under discussion gives an algorithm that allows us to derive, from our data, the estimate of that becomes extremely stable after a certain point. It is reasonable to assume that if in the regular market the estimate is public at , then we will have

| (23) |

Fact 2.1 implies that identities (22) and (23) can be considered as an analogue of relation (3). We also note that the additional identity does not contradict theoretical and empirical considerations presented in Sections B.1 and B.6. In Section D.1, we show that the data does not contradict the continuous model itself, and in Sections D.2 and D.3, we describe how this model has been chosen.

C.5. Interpretable collective intelligence: continuous considerations

Consider the regular market that is described at the beginning of Section C.2 and is assumed to satisfy Assumption C.1. Suppose there is a pre-announced algorithm for eliciting from , and is public at . We introduce the following modifications of the market.

-

(md1)

Each participant gets one and the same volume of play money that can be employed in this market (and only in it): the experts are assumed to have an equal opportunity to affect the market by trading.

-

(md2)

We resolve the market in accordance with .

In addition to Assumption C.1, we make an assumption that is a variety of the temporal coherence property. An expert is temporal coherent if he or she cannot predict whether his or her belief will increase or decrease on average (see also the discussion in [21, 23–26]). In the Bayesian setting, this means that his or her learning scheme forms a martingale. In our pre-Bayesian language, temporal coherence between and can be postulated as follows.

Assumption C.5 (temporal coherence).

For and , we have

where the existence of the left expression is postulated as in Assumption A.1 with instead of .

We refer to the market in question, which is modified in accordance with (md1) and (md2) and satisfies Assumptions C.1 and C.5, as the collective intelligence.

Definition C.1.

The collective intelligence is -efficient if each expert satisfies the following conditions.

-

(1)

At each time , there exists such that the expert believes that if he or she publicly generates, during an interval , certain signals (i.e. makes a part of ), then this will lead to the identity whatever orders the expert will place during .

-

(2)

If places an order , then he or she believes that he or she will indeed publicly generate during .

We make some comments concerning (1) and (2). First, we emphasize that the signals do not depend on the expert ’s planned voting actions: is going to transmit these signals to others directly. Second, we clarify that depends on and : the interval must be long enough for the collective intelligence to manage to process the new information. Third, we note that Assumption C.5 implies that if satisfies (1) and believes that he or she will generate during , then

| (24) |

We come to the following statement.

Fact C.2.

Finally, substituting for in (1), we immediately come to the following fact, which may, due to Fact 3.2, be viewed as an analogue of Fact 3.1.

Fact C.3.

The property of -efficiency includes property (23).

We present heuristic arguments that -efficiency is some sort of equilibrium in a sense close to Theorem 3.1. We note that for further studies, the experimental verification and the practical implementation of our ideas seem to be much more preferable and realistic than a complete formalization of the considerations below. We also need to adapt to each other an automated market maker and our algorithm for eliciting (see also Section D.1).

Consider an individual expert and make the following assumption.

Assumption C.6.

Section C.4 and further details in Section D justify the existence of a suitable algorithm that induces (ii) and can be taken as .

Due to Fact C.2, the expert believes that the others rely on in their trading. From his or her point of view, the collective intelligence looks like a normal market where constraints on experts’ ability to transmit information through trading are compensated by direct information exchange. Concerning the constraints just mentioned, in the private setting of the experiment [8] (see also Section B.6) we can presumably see that critical information may be poorly transmitted through an ordinary market with (md1). We may assume that this effect strengthens as the number of experts without this information increases. Suppose the expert indeed believes he or she cannot distort the others’ probabilities by voting. Since regards the collective intelligence as the regular market with an active channel for direct information exchange, and believes that in the regular market the algorithm would give the estimate remaining stable under the order flaw after a certain point, the following assumption is justified.

Inference 1.

At each time , the expert believes that he or she cannot affect by his or her voting actions alone.

The expert also believes that gives relation (23) in the regular market. Therefore, since treats the collective intelligence as the regular market with the main information channel separated from the market itself, we may assume that if the expert timely adds, like the others, his or her information to this channel, then he or she will believe that regardless of his or her voting actions. Namely, we can make the following assumption.

Inference 2.