Difference-in-Differences for Policy Evaluation††thanks: I thank John Gardner, Jon Roth, and Pedro Sant’Anna for helpful comments.

Abstract

Difference-in-differences is one of the most used identification strategies in empirical work in economics. This chapter reviews a number of important, recent developments related to difference-in-differences. First, this chapter reviews recent work pointing out limitations of two way fixed effects regressions (these are panel data regressions that have been the dominant approach to implementing difference-in-differences identification strategies) that arise in empirically relevant settings where there are more than two time periods, variation in treatment timing across units, and treatment effect heterogeneity. Second, this chapter reviews recently proposed alternative approaches that are able to circumvent these issues without being substantially more complicated to implement. Third, this chapter covers a number of extensions to these results, paying particular attention to (i) parallel trends assumptions that hold only after conditioning on observed covariates and (ii) strategies to partially identify causal effect parameters in difference-in-differences applications in cases where the parallel trends assumption may be violated.

JEL Codes:

C14, C21, C23

Keywords:

Difference-in-differences, policy evaluation, panel data, treatment effect heterogeneity, parallel trends, two way fixed effects, event study

1 Introduction

This chapter reviews a number of recent contributions related to difference-in-differences (DID) approaches to evaluate economic policies. Difference-in-differences approaches are extremely popular in applied work in economics,222For example, [39], which uses text analysis to study trends over time in methodological approaches in economics, notes about the popularity of DID approaches in empirical work in economics: “It is quite striking that today almost 25 percent of all NBER working papers in applied micro make references to difference-in-differences” (p. 45). and difference-in-differences methodology features prominently in well known textbooks such as [3, 38]. Although difference-in-differences identification strategies have been popular in empirical work for roughly the past 30 years ([30, 31]), there has been renewed interest in methodological issues related to difference-in-differences approaches in recent years. This interest stems from several highly influential papers that have pointed out potentially severe weaknesses with the two way fixed effects (TWFE) regressions that have been the primary way that DID identification strategies have been implemented ([63, 41, 14, 50, 76, 8, 57]). One of the main goals of this chapter is to summarize these papers as well as to review a number of recently proposed approaches that are able to circumvent the limitations of TWFE regressions.

Before proceeding along these lines, it is worth fixing ideas on what exactly DID is as well as pointing out some peculiarities of DID identification strategies. First, DID identification strategies involve observing some units in some period(s) before they become treated as well as in some period(s) after they become treated — collectively, these units are referred to as the “treated group.” Observing some units in time periods before and after they become treated is a particularly powerful framework for learning about causal effects. This is arguably the reason that DID identification strategies are often included among “natural experiment” methods in economics and is a primary difference relative to traditional panel data approaches in economics.

Second, difference-in-differences strategies typically focus on identifying and estimating the Average Treatment Effect on the Treated (ATT); this is exactly the average effect of the treatment among those who switch from being untreated to being treated. The ATT is equal to the average path of outcomes experienced over time by the treated group relative to the average path of outcomes that the treated group would have experienced had it not participated in the treatment. Thus, the key identification challenge in DID applications is recovering this “counterfactual” path of outcomes for the treated group. The main identifying assumption underlying DID is called the parallel trends assumption. It says that, in the absence of participating in the treatment, the counterfactual path of outcomes for the treated group is the same as the path of outcomes that the “untreated group” (the group of units that did not participate in the treatment) actually experienced. Third, DID identification strategies allow for treatment effect heterogeneity; that is, that the effect of participating in the treatment can vary across units (within time periods), across time periods, and across length of exposure to the treatment.

The dominant approach to implementing DID identification strategies has been to use two-way fixed effects (TWFE) regressions. The simplest and most common version of this approach is the following regression

| (1) |

where is the outcome of interest, is a time fixed effect, is a unit fixed effect, is an indicator for whether or not unit participated in the treatment in time period , and are idiosyncratic, time-varying unobservables.

Under treatment effect homogeneity (and under the parallel trends assumption), in the TWFE regression is equal to the causal effect of participating in the treatment. However, in cases with treatment effect heterogeneity, researchers have often (loosely) interpreted as an overall average treatment effect. That a TWFE regression delivers a single summary measure of the effect of the treatment is appealing in many applications. Unfortunately, this kind of TWFE regression is not generally robust to treatment effect heterogeneity ([50, 41, 14]).333TWFE regressions do have some robustness to treatment effect heterogeneity; for example, it is straightforward to show that this TWFE regression does perform well in the case with exactly two time periods even in the presence of treatment effect heterogeneity (see discussion in Section 2 below for more details), but it has less than full robustness to treatment effect heterogeneity. Section 3 discusses these issues extensively, but a rough intuition is that researchers ask “too much” out of a TWFE regression; that is, they ask the TWFE regression to both allow for treatment effect heterogeneity and to fully summarize the causal effect of participating in the treatment into a single number , but the TWFE regression can only do one of these.444It is understandable why researchers would like a single summary measure of the causal effect of a particular policy as these can easily be reported in research (e.g., in the abstract of an empirical paper) or explained to policymakers. TWFE do provide a single summary measure, but they come with the additional conditions (often implicit) that treatment effects do not vary across time, group, or length of exposure to the treatment. For example, [77, p. 34 ] notes that “One of the important conclusions is that there is nothing inherently wrong with TWFE as an estimation method. The problem is that it is often applied to a model that is too restrictive.” [77] goes on to propose an alternative TWFE regression that includes a large number of interaction terms, thus allowing for general forms of treatment effect heterogeneity, but coming at the “cost” of requiring a second “aggregation step” in order to deliver a single summary parameter. [50] provides an alternative explanation for the non-robustness of TWFE regressions to treatment effect heterogeneity: can be shown to be equal to a weighted average of underlying comparisons of paths of outcomes among groups whose treatment status changes relative to groups whose treatment status remains the same across time periods. These comparisons include both (i) using groups that are not-yet-treated as the comparison group and (ii) using groups that were treated in previous periods as the comparison group. The first comparison is exactly the type of comparison that should be used in DID applications, but the second type of comparison (sometimes called “bad comparisons” or “forbidden comparisons”) is generally not desirable in applications and can lead to poor estimates of causal effect parameters, particularly in the presence of treatment effect dynamics. Even in cases without treatment effect dynamics, the weights on underlying treatment effect parameters are still (undesirably) driven by the estimation method which can lead to estimates of overall treatment effects being different from the actual overall treatment effect. Both of these issues open up the possibility of poor estimates of causal effect parameters due to the estimation strategy, even when the identification strategy is valid. These are major weaknesses of using TWFE regressions in this context.

One of the main contributions of recent work on DID is to more clearly separate identification and estimation. In particular, following [29], the current chapter defines group-time average treatment effects, , to be the average treatment effect for a particular group at a particular point in time; a leading example of a group is to define it by the time period when a unit first becomes treated. The group-time average treatment effect is a natural generalization of the from the case with two time periods to the case with more time periods and variation in treatment timing. Identification arguments for group-time average treatment effects are essentially analogous to identification arguments for the in the two period case, and identification holds under the parallel trends assumptions without requiring additional assumptions restricting treatment effect heterogeneity. Group-time average treatment effects can provide important information about treatment effect heterogeneity with respect to group and time period and/or length of exposure to the treatment. Perhaps more importantly, group-time average treatment effects can play the role of a building-block for more aggregated treatment effect parameters. For example, if desired by the researcher, they can be aggregated into alternative target parameters such as an overall parameter or into an event study.

Interestingly, the usefulness of the strategy of identifying group-time average treatment effects in the presence of multiple time periods, variation in treatment timing, and treatment effect heterogeneity applies much more broadly than just to DID applications. In particular, this strategy provides a path to extending any sort of identification arguments from the case without variation in treatment timing to cases with more time periods and variation in treatment timing. See Remark 2 below for additional discussion along these lines.

Another main goal of this chapter is to compare some of the main new approaches to estimating causal effect parameters that have been proposed recently proposed; this chapter mainly considers the approach proposed in [29], the “imputation” approaches proposed in [60, 48, 14], and the regression approaches proposed in [76, 77].555This part of the chapter complements [10] which provides a detailed comparison of the approaches in [29, 76] and “stacked regression” as in [32]. All of these procedures follow similar high-level strategies: in a first step, they explicitly make the same “good comparisons” that show up in the TWFE regression (i.e., the comparisons that use units that become treated relative to units that are not-yet-treated) while explicitly avoiding the “bad comparisons” that show up in the TWFE regression (i.e., the comparisons that use already-treated units as the comparison group). Then, in a second step, they combine these underlying treatment effect parameters into target parameters of interest such as an overall average treatment effect on the treated or into an event study. This discussion suggests a high degree of similarity between all of these approaches. That being said, these approaches typically do not lead to exactly the same estimates of causal effect parameters (except in a few special cases). One main reason for this is different default choices in the software implementations of different procedures.666For example, by default, the software implementations of [29, 76] only impose parallel trends assumptions from the period right before treatment starts until the last time period while software implementations of [48, 14, 77] impose parallel trends in all time periods. In practice, estimation strategies that impose parallel trends assumptions across more periods tend to be more efficient while estimation strategies that impose parallel trends assumptions across fewer periods tend to be more robust to violations of parallel trends assumptions in some periods. But these are not fundamental differences across methods; it is relatively straightforward to adapt each of these estimation strategies to exploit more or less parallel trends assumptions. To my knowledge, there are perhaps only two meaningful differences between approaches. In cases where the parallel trends assumption includes covariates, the doubly robust approach in [29] generally imposes weaker functional form requirements on the way covariates enter the model than alternative approaches; moreover, these types of identification arguments can be connected to the literature on double/de-biased machine learning (e.g., [35, 34]) which could further substantially weaken functional form requirements with respect to observed covariates. On the other hand, imputation strategies are often very convenient to implement in that they only involve estimating panel data-type regressions and computing predicting values. This is an important advantage particularly in “non-standard” setups.777To give a concrete example, consider the case with a multi-valued treatment and where the amount of the treatment can change for a particular unit across different points in time. To my knowledge, there is no existing software package that directly implements any of the new approaches to DID in this context. That said, it would be relatively straightforward to use an imputation estimator in this case. That being said, even these differences are arguably second order relative to the first order issues with TWFE regressions that all of these approaches address.

Next, the chapter turns to two useful extensions of the previous results. The first extension is to the case where the parallel trends assumption holds only after conditioning on some covariates. To give a simple example where conditioning on covariates in the parallel trends assumption is useful, consider a labor economist interested in the effect of some treatment on a person’s earnings. In this type of application, it seems likely that paths of earnings (in the absence of participating in the treatment) depend on things like demographic characteristics and years of education. If these variables are distributed differently among the treated and untreated group, then the “unconditional” parallel trends assumptions considered so far are generally violated. The new approaches to DID discussed above can readily accommodate including covariates in the parallel trends assumption; moreover, the chapter further reviews the case where the covariates may themselves be affected by participating in the treatment (sometimes referred to as a “bad control” problem) and discusses recent methodological innovations in this context as well.

The second extension is for the case where parallel trends is violated (even after potentially conditioning on covariates). It is important to emphasize that the parallel trends assumption does not hold automatically in applications with repeated observations over time. The most common way to rationalize the parallel trends assumption is using the following model for untreated potential outcomes

| (2) |

where denotes unit ’s untreated potential outcome in time period — this is the outcome that unit would have experienced in time period if it had not participated in the treatment, is a time fixed effect, is an individual fixed effect that can follow a different distribution for the treated group relative to the untreated group, and are (idiosyncratic) time varying unobservables (see, for example, [12, 48, 14]).888To conserve on notation, the current chapter uses , , and as generic notation for time fixed effects, unit fixed effects, and idiosyncratic time-varying unobservables, respectively. Therefore, although the notation is similar here as for the TWFE regression in Equation 1, these should not be interpreted as being the same across the two equations. There are a number of attractive features of this model. First, it does not put any structure on how untreated potential outcomes are generated at all. Second, it allows for arbitrary treatment effect heterogeneity. Third, units can select into the treatment on the basis of their treated potential outcomes or on their time invariant unobservables that affect untreated potential outcomes, , but not on the basis of the time varying unobservables, .

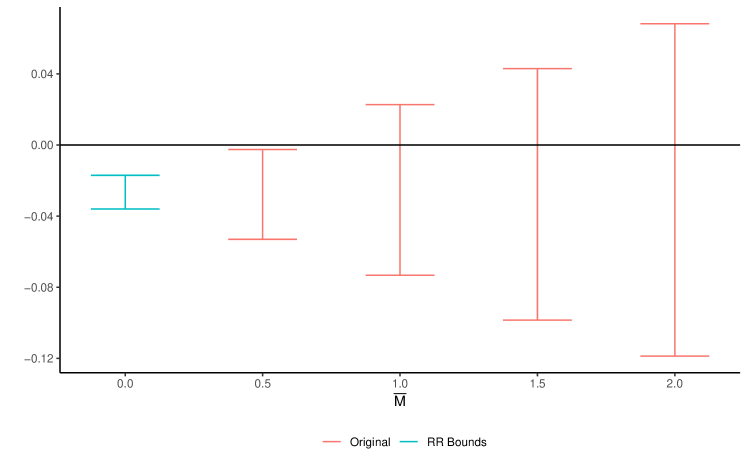

Besides these, many economic models involve unobserved heterogeneity (like ) that may be distributed differently between the treated group and the untreated group as well as trends in outcomes over time (like ). However, the parallel trends assumption also relies heavily on the additive separability between the time and individual effects; this additive separability is often not explicitly implied by economic theory. And, in many cases, it seems like it would be hard for researchers to ex ante evaluate its validity. Therefore, the chapter also emphasizes recent contributions from [61, 66] related to bounding treatment effects in a DID setup. Roughly, the idea of these papers is to consider how large violations of parallel trends assumptions can be before the results in post-treatment periods break down. One general challenge in the sensitivity analysis literature is that it is often not clear what constitutes a “large” amount of robustness to violations of underlying assumptions. However, DID applications, particularly those with additional pre-treatment time periods, are particularly attractive in this context because the magnitude of treatment effects in post-treatment time periods can be compared to the size of violations of parallel trends in pre-treatment time periods.

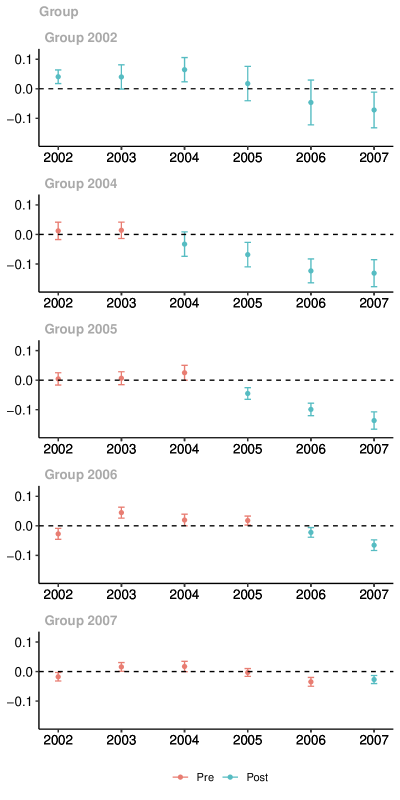

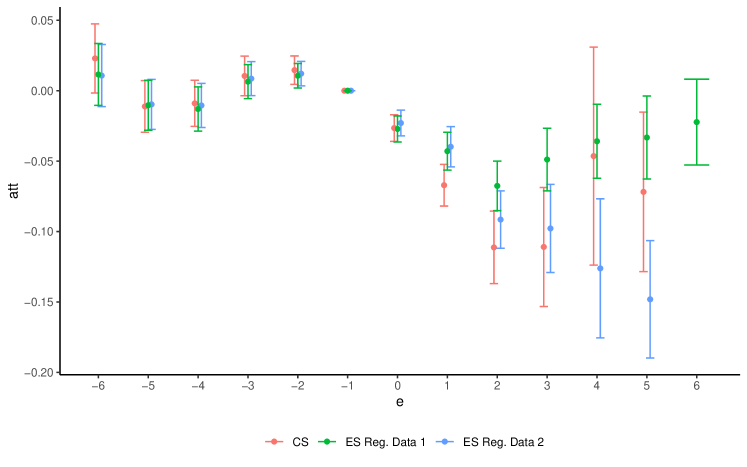

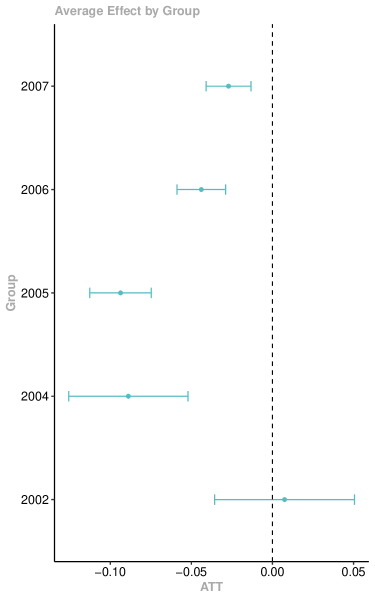

To conclude, the chapter provides an application on the minimum wage and employment as a way to illustrate the methodological points. This application comes from (and expands) the application in [29]. The application focuses on a period from 2001-2007 where the federal minimum wage was constant over time and uses changes in state-level minimum wage policies over time to identify effects of minimum wage increases on employment among teenagers. This example is merely intended to be illustrative of the methodological issues discussed in this chapter, and there are some notable weaknesses (discussed in more detail below). That said, the point of the application is to illustrate the empirical relevance of new approaches to DID in a relatively realistic application. Broadly, there are three main takeaways from the application. First, while the results from using traditional TWFE and event study regressions are not radically different from the results using new approaches, they are different enough to suggest that researchers should prefer using the new methods. Second, the new approaches all impose that the researcher make a number of good choices in the context of DID (such as not including units that are already treated in the first period or including time periods after all units become treated). While TWFE regressions can still suffer from negative weights and weights undesirably driven the estimation in this case, making these same sorts of “good choices” tends to notably improve the performance of regression-based estimation strategies. Finally, it is important to emphasize that the new approaches all still rely on the validity of the parallel trends assumption. Combining the [66] sensitivity analysis with new approaches to DID turns out to be very useful in this application as there appear to be moderately-sized violations of parallel trends in pre-treatment periods.

2 Baseline Case: Two Periods and Two Groups

This section considers the simplest, “textbook” version of DID — the case where there are exactly two time periods, where no units are treated in the first time periods, and where some units (the treated group) become treated in the second time period while other units (the untreated group) remain untreated in the second time period.

Notation:

This section uses the following notation. Denote the two time periods by and and define a treatment indicator , so that for units that participate in the treatment and for units that do not participate in the treatment. Next, for , define to be unit ’s treated potential outcome in time period (this is the outcome that it would experience if it were in the treated group), and define to be unit ’s untreated potential outcome in time period (this is the outcome that it would experience if it were in the untreated group).999For simplicity, this chapter focuses on the case where the researcher has access to balanced panel data. Most of the arguments in the chapter essentially immediately apply to the case with repeated cross sections and can be extended to cases with unbalanced panel data (under standard assumptions). See Table 4 for additional, related references. The next condition is that for all units. This is a no-anticipation condition (which is discussed more carefully in the next section) which rules out the treatment affecting outcomes in periods before the treatment takes place. Under these conditions, the observed outcomes in each time period are and . In other words, in the first time period, one observes untreated potential outcomes for all units; and in the second time period, one observes treated potential outcomes for treated units and untreated potential outcomes for untreated units.

Target Parameters:

Most commonly, DID identification strategies target the average treatment effect on the treated (ATT), which is defined as:

The ATT is the mean difference between treated and untreated potential outcomes among the treated group. Perhaps a main reason that the DID literature most often considers identifying the ATT rather than, say, the ATE is that, for the treated group, the researcher observes untreated potential outcomes (in pre-treatment time periods) and treated potential outcomes (in post-treatment time periods). DID identification strategies exploit this framework, and, therefore, it is natural to identify causal effect parameters that are local to the treated group.

Identification:

The main identifying assumption underlying the DID approach is the parallel trends assumption, which in the case with two time periods, is given by

Assumption 1 (Parallel Trends).

As discussed in the introduction, Assumption 1 says that the path of untreated potential outcomes is, on average, the same between the treated group and the untreated group. This seems immediately useful from an identification standpoint because the path of untreated potential outcomes is not observed for the treated group, but the path of untreated potential outcomes is observed for units in the untreated group. In fact, this assumption is strong enough to identify . To see this, notice that

| (3) |

where the first equality comes from the definition of , the second equality holds by adding and subtracting , the third equality holds because and are observed outcomes for the treated group, the fourth equality uses the parallel trends assumption, and the last equality holds because corresponds to the observed path of outcomes for units in the untreated group.

The expression in Equation 3 implies that is identified under Assumption 1, and the particular expression on the right hand side of Equation 3 is where difference-in-differences gets its name. Under parallel trends, is equal to the average difference in outcomes over time for the treated group adjusted by the average difference in outcomes over time for the untreated group. An alternative intuition for the expression in Equation 3 is the following: The researcher observes the path of outcomes over time for the treated group. The parallel trends assumption says that one can obtain the path of outcomes that the treated group would have experienced if they had not participated in the treatment from the untreated group. Therefore, the is equal to the actual path of outcomes experienced by the treated group adjusted by the path of outcomes of the untreated group. As an additional remark, notice that the above arguments have not imposed any assumptions restricting treatment effect heterogeneity.

Estimation:

The expression in Equation 3 immediately suggests an estimator for by replacing population means with sample averages given by

| (4) |

where is the number of treated observations and is the number of untreated observations. Rather than taking this approach, most often is estimated using the TWFE regression in Equation 1. In the case considered in this section with exactly two periods, this regression is exactly equivalent to the simple linear regression of on given by

| (5) |

where .

Interestingly, although the regression above appears to have restricted the effect of participating in the treatment to be constant (and given by ) across all units, it is straightforward to show that in this case

and, likewise, that

In other words, in the case with exactly two time periods, the TWFE regression is robust to treatment effect heterogeneity.101010The argument for this is not complicated and follows because Equation 5 is saturated and by standard regression algebra. The regression in Equation 5 is as straightforward to estimate as the averages in Equation 4. Moreover, this regression provides a convenient way to recover standard errors and to conduct inference using standard statistical software. The combination of robustness and simplicity of the TWFE regression in this case provides an explanation for its popularity.

Finally, and at the risk of belaboring the point, it is also worth mentioning how to estimate using an imputation approach in this relatively simple setting (this is instructive for the more complicated cases considered in the next section). Imputation estimators work by estimating the model for untreated potential outcomes in Equation 2 using all available untreated observations. Because the researcher does not observe untreated potential outcomes for the treated group, after taking first differences (or making a within transformation — which are equivalent in this case), this amounts to the regression

using observations from the untreated group and which, for simplicity, imposes the normalization that . In this case, . Furthermore, can be “imputed” for the treated group using

and, therefore,

This discussion suggests that, estimating ATT by (i) the sample analogue of Equation 3, (ii) TWFE regression, or (iii) imputation, all result in numerically identical estimates in the textbook case for DID with exactly two time periods. The next section shows that this equivalence is lost when one considers more complicated cases with more periods and variation in treatment timing.

3 Multiple Periods and Variation in Treatment Timing

Much of the recent difference-in-differences literature has been interested in questions surrounding how well DID identification and estimation strategies scale to settings where there are more than two time periods and there is variation in treatment timing. These sorts of cases are often encountered in applied work. This section primarily covers (i) several recent results on the limitations of TWFE regressions to implement DID identification strategies and (ii) a number of recently suggested approaches that can circumvent the limitations that TWFE regressions suffer from. To fix ideas, this section primarily focuses on the staggered treatment adoption case as in the following assumption.

Assumption 2 (Staggered Treatment Adoption).

For all units and for all , .

Staggered treatment adoption means that once a unit becomes treated, that unit remains treated in future time periods. Staggered treatment adoption occurs in applications where different locations implement policies at different points in time (and then those policies remain in place). Staggered treatment adoption also applies in many applications where the unit is not literally treated over and over across periods, but rather that treatment is “scarring”. For example, researchers studying the effects of job training programs typically categorize individuals as being treated at the first time they participate in job training and in all subsequent periods (see, [76] for more discussion along these lines).111111Staggered treatment adoption is not actually fundamentally important for most of the results below, but rather (for identification) it greatly decreases the number of “groups” to keep track of and therefore notably simplifies some of the arguments below and (for estimation) it avoids a curse of dimensionality related to the number of observations per “group” potentially becoming very small. Some work (for example, [23, 42]) has also considered more complicated treatment regimes such as cases where units can move into and out of the treatment or cases where the treatment can be multi-valued or continuous. For simplicity, this chapter mostly focuses on the staggered adoption case though many of the insights in this case can apply to more complicated treatment regimes.

Notation:

This section extends the notation from the previous section. Now consider a case with time periods and with staggered treatment adoption. Towards this end, define groups by the time period when a unit first becomes treated; for a particular unit, let indicate its group and denote the set of all groups by .121212If there is a group that is already treated at , the setup in this section implies that this group is omitted. The reasons to omit this group are (i) untreated potential outcomes are never observed for this group so they are not useful as a comparison group, and (ii) because no pre-treatment period is observed for this group, it is not possible to use a parallel trends assumption to identify treatment effect parameters for this group either. Further, define which is the set of groups excluding the never-treated group. Under staggered treatment adoption, knowing a unit’s group implies that the researcher knows its entire path of participating in the treatment across all time periods. For units that do not participate in the treatment, arbitrarily set their group to be (which somewhat lessens the notational burden for a few lines of algebra in the next section but is otherwise inconsequential). It is also convenient to define the variable that is equal to 1 for units in the “never-treated” group and is otherwise equal to 0 for units that ever participate in the treatment.131313This chapter considers the case where the researcher has access to a never-treated group. This is essentially without loss of generality, as in cases where all units eventually become treated, one would limit the analysis to time periods where the researcher has access to a group that is not yet treated. After subsetting the available time periods, there is a never-treated group (at least over the periods being considered). Even though this procedure results in a loss of data in some time periods, these are time periods where DID identification strategies would not be useful for identifying treatment effect parameters as there is no available comparison group in these periods. Next, define potential outcomes by a unit’s group; in particular, is the outcome that unit would experience in time period if it became treated in period . Also, continue to denote as the potential outcome that unit would experience in time period if it did not participate in the treatment in any time period.

Assumption 3 (No Anticipation).

For all units and time period (pre-treatment time periods), .

Assumption 3 says that participating in the treatment does not have an effect on a unit’s outcomes in time periods before the treatment actually occurs. In some applications, it could be the case that some units anticipate being treated and “make adjustments” that affect their outcomes in periods before the treatment takes place. It is relatively straightforward to accommodate anticipation in a DID framework; in particular, one can essentially “back up” the analysis far enough in time and only include as pre-treatment periods those periods that are “far enough” before the treatment actually begins (see, for example, [29, 76]). For simplicity, this chapter mostly ignores issues related to violations of the anticipation condition above.

Under Assumption 3, observed outcomes are given by when and when . In other words, in pre-treatment periods, the researcher observes untreated potential outcomes, and, in post-treatment periods, the researcher observes potential outcomes corresponding to the unit’s actual group.

The next assumption provides an extended version of the parallel trends assumption to accommodate multiple time periods and variation in treatment timing.

Assumption 4 (Parallel Trends for Multiple Periods and Variation in Treatment Timing).

For all , and for all ,

Assumption 4 says that average paths of untreated potential outcomes are the same for all groups and all time periods. This is a natural generalization of the parallel trends assumption in Assumption 1 to the case with multiple periods and variation in treatment timing. Like that assumption, Assumption 4 allows for heterogeneous treatment effects (both across units and with respect to time and/or length of exposure to the treatment). It also does not place any restriction on treated potential outcomes at all, and it is compatible with a fixed effects model for untreated potential outcomes like the one in Equation 2 across all time periods while allowing for the distribution of the individual fixed effect, , to arbitrarily vary across groups. That said, there are alternative versions of parallel trends assumptions that researchers could invoke here. One example that is discussed in the next section, is when parallel trends only holds among those with similar observed characteristics. Another similar (and weaker) assumption would be to assume that parallel trends only holds relative to the never treated group and only for certain time periods. See [62] for a detailed discussion and comparison of several different possible parallel trends assumptions. To give one more example, another interesting assumption is that parallel trends holds only among groups that ever participate in the treatment. This chapter focuses on the version of parallel trends in Assumption 4, but many of the approaches considered below could be implemented under alternative parallel trends assumptions with only slight modification.

Target Parameters:

There are a large number of parameters that a researcher could potentially be interested in when there are multiple periods and variation in treatment timing. This section considers three main parameters of interest: group-time average treatment effects, overall average treatment effects, and event studies; several additional parameters are considered in [29].

To start with, define group-time average treatment effects which are given by

These are the average treatment effect for group in time period . is an important parameter in the DID literature. First, from an identification standpoint, the next section shows that can be identified using essentially the same arguments as in the case with exactly two periods considered above. Second, under Assumption 4, recent work shows that in the TWFE regression can be related to “underlying” ’s. Third, can be used to highlight treatment effect heterogeneity with respect to group, time period, and/or length of exposure to the treatment. In some applications, the number of group-time average treatment effects may be large (e.g., this happens when the number of groups and time periods is relatively large) and, therefore, may be challenging to report and/or interpret. ’s can also serve as the building block for more aggregated treatment effect parameters.

Towards this end, among units that ever participate in the treatment, define , which is the average treatment effect for unit across all of its post-treatment time periods. One version of an overall treatment effect parameter is

where conditioning on amounts to conditioning on becoming treated in any period from . This is a natural analogue for in the case with multiple periods and variation in treatment timing. It is the average effect of participating in the treatment among those that participate in the treatment across all their post-treatment time periods. Like the coefficient on in a TWFE regression, is a single number; it can be used to summarize the causal effect of participating in the treatment among those that ever participated. [29] show that

where

That is, can be recovered as a weighted average of where the weights depend on (i) the relative size of the group among all groups that ever participate in the treatment (from the term , and (ii) the number of post-treatment time periods for a particular group (from the second term) which arises due to applying equal weight across all treated units.

Another common target parameter in DID applications are event study parameters that summarize the effect of participating in the treatment at different lengths of exposure to the treatment. In particular, among units such that , define ; this is the causal effect of the treatment periods after exposure to the treatment (this notation uses the convention in the literature of having in the period where the treatment occurs). One can summarize treatment effects across different lengths of exposure using the following parameter

That is, is the average treatment effect among those that have been exposed for exactly periods conditional on being observed having participated in the treatment for that number of periods (the condition that ) and ever-participating in the treatment ().141414Notice that the set of groups that contribute to can change across different values of . This can make difficult to interpret across different values of especially in cases where, for example, earlier treated or later treated groups experience systematically different effects of participating in the treatment. To be clear here, is the average treatment effect at different lengths of exposure to the treatment (among those groups that ever experience periods of the treatment); but differences across different values of may not necessarily indicate dynamic effects across different lengths of exposure due to the composition of groups also potentially changing across different values of . There are strategies to deal with these sorts of issues; particularly, related to computing event study parameters while keeping the composition of groups constant across different values of ; see, for example, [29, 76]. [29] show that can be recovered from underlying group-time average treatment effects; in particular,

where

Thus, can be recovered as a weighted average of underlying ’s. This average is given by collecting ’s that satisfy (i.e., finding the period for a particular group where it has been exposed to the treatment for exactly periods) and then by weighting by the relative size of the group (among those groups that are ever observed to participate in the treatment for exactly periods).

Remark 1.

Given that and can be recovered from underlying ’s, the identification arguments below focus on .

Remark 2.

Another notable feature of the discussion in this section is that these arguments apply quite generally for identifying causal effect parameters in applications with multiple time periods. In particular, the identification arguments below focus on identifying in a DID context. However, in cases where a researcher wanted to use some other identification strategy besides DID, given that is somehow identified, then the aggregations to overall treatment effect parameters, event studies, etc. continue to apply. See [26, 24] for examples along these lines in the context of unconfoundedness (conditional on lagged outcomes) and interactive fixed effects models, respectively.

3.1 Problems with TWFE Regressions

As discussed in the introduction, the dominant approach to implementing DID identification strategies has been to use the TWFE regression in Equation 1. In this context, researchers are primarily interested in which has typically (though often loosely) been interpreted as an overall average treatment effect among those that ever participate in the treatment; i.e., along the lines of the definition of above. Recent research, particularly [63, 41, 14, 50, 8], has pointed out a number of weaknesses of this estimation strategy in cases where (i) there are more than two time periods, (ii) there is variation in treatment timing, and (iii) there is treatment effect heterogeneity — all of which are very common in applications in economics.

TWFE Regressions under Treatment Effect Homogeneity

To start with, it is worth considering where this specification comes from, and, additionally, why this approach would work well under treatment effect homogeneity. A natural starting point is the model for untreated potential outcomes in Equation 2. Next, notice that, in the setup with multiple time periods and variation in treatment timing (and under a no-anticipation condition), observed outcomes can be expressed in terms of potential outcomes by

| (6) |

Next, a mathematical expression for treatment effect homogeneity is the condition that for all units in all post-treatment time periods (i.e., periods where ). This condition implies that the effect of being treated does not vary across units; moreover, within units, the effect of the treatment does not vary across time periods, length of exposure, or depend on the time period when a unit becomes treated. It implies that, in post-treatment time periods, . Plugging in the model for untreated potential outcomes in Equation 2 into Equation 6, using the treatment effect homogeneity condition, and noticing that implies that

thus giving rise to the TWFE regression above. Under treatment effect homogeneity, the estimate of from this regression can be interpreted as an estimate of the causal effect of participating in the treatment.

TWFE Regressions under Treatment Effect Heterogeneity

This section considers the same TWFE regression but relaxes the treatment effect homogeneity condition. Section 2 showed that, in the textbook case with two periods, from the TWFE regression was generally robust to treatment effect heterogeneity. In contrast, this section shows that is not generally robust to treatment effect heterogeneity when there are multiple periods and variation in treatment timing.151515It is worth pointing out that there are multiple ways to estimate in Equation 1. The discussion in this section focuses on estimating after taking a within transformation. See [41] for an additional discussion of the alternative approach of estimation in first differences; in that case, the arguments need to be slightly modified but the same sort of issues continue to apply.

Notation:

The discussion in this section requires some extensions to the notation used so far. First, define

which is the double de-meaned version of . Next, for any groups and , define

which are the fraction of periods for which group participates in the treatment, the overall probability of being in group , and the probability of being in group conditional on either being in group or group , respectively. For , let

which are the average outcome for unit between periods and and the average group-time average treatment effect for group from period to , respectively. For two groups and with (i.e., group becomes treated before group ), it is also helpful to define the short-hand notation

which are the average outcome for unit in periods before either group becomes treated, the average outcome for unit in periods after group becomes treated but before group becomes treated, and the average outcome for group after both group and group have become treated, respectively. Similarly, define

which are the average group-time average treatment effect for group in “MID” periods, the average group-time average treatment effect for group in “POST” periods, and the average group-time average treatment effect for group in “POST” periods, respectively.

There are several different variations of the following sort of result on interpreting from the TWFE regression in Equation 1; the one provided below is the “Bacon Decomposition” ([50]). It provides a decomposition of from the TWFE regression into a number of underlying comparisons. It is a decomposition in the sense that it does not invoke a parallel trends assumption, but rather relates to underlying components that are themselves related to DID types of arguments. This sort of result is extremely helpful for understanding the mechanics of the TWFE regression.

Proposition 1 (Bacon Decomposition, [50]).

Under the setup considered in this section,

where

where and for all and such that ; in addition, .

The proof of Proposition 1 is provided in Appendix A. It mimics the proof in [50] with minor adjustments mainly related to notation. It is worth explaining this result in some more detail. First, the double sum in the expression for is first over all groups (the summation involving ) and then over all groups that are “later-treated” than group (the summation involving ).161616In [50], the never-treated group is treated separately; in the expression for in Proposition 1, it is included alongside “later-treated” groups. Then, is a weighted average of

-

(1)

comparisons of paths of outcomes from “PRE” periods (where neither group nor group is treated) to “MID” periods (where group is treated but group is not treated) between an early-treated group (group ) and a later-treated group (group ).

-

(2)

comparisons of paths of outcomes from “MID” periods to “POST” periods (where both group and group are treated) for the later treated group (group ) relative to an early-treated group (group ).

The comparisons in (1) are “good comparisons” in the sense that, under Assumption 4,

An informal intuition here is that parallel trends assumptions rationalize comparing paths of outcomes for early-treated groups to not-yet-treated groups and interpreting differences in these paths as being due to the effect of participating in the treatment.

However, a key limitation of the TWFE regression is due to the “bad comparisons” in (2). This is a comparison between a late-treated group to an already treated group. That is, the first main issue being pointed out in Proposition 1 is that already-treated units sometimes serve as the comparison group. Assumption 4 alone, however, does not justify using already treated units in the comparison group (instead, it rationalizes using never treated or not-yet-treated units in the comparison group). It is interesting to further expand the terms that show up in (2). Under Assumption 4, this second term can be expressed as

where the first equality holds by adding and subtracting terms, and the second equality uses Assumption 4. This means that, comparisons of paths of outcomes for a later-treated group (here, group ) to paths of outcomes for an already treated group (here, group ) deliver an parameter for group (the first term above) but that is confounded by treatment effect dynamics (the second term above) for the already treated group. This expression is also the source of the “negative weighting” issue emphasized in [41]. Negative weights imply that it is, at least in principle, possible for TWFE regression to deliver very poor estimates of causal effects. For example, in extreme cases, it would be possible for all ’s to be positive, but due to negative weighting, for to be negative.

Furthermore, notice that the additional condition of treatment effect homogeneity does justify using already treated units as the comparison group because, under treatment effect homogeneity, there are no treatment effect dynamics. Moreover, a more limited form of treatment effect homogeneity — ruling out treatment effect dynamics but allowing for heterogeneous effects across groups — is sufficient to eliminate the negative weighting issue.

Avoiding the negative weighting issue implies that some of the worst-cases for TWFE regressions will be avoided. However, even without treatment effect dynamics, this is still not strong enough to guarantee that ; in particular, define to be the average treatment effect for group and note that without treatment effect dynamics, for any value of . In this case, under parallel trends, delivers a weighted average of across groups, but, in general, the weights are not equal to the relative size of the group. This implies that the TWFE estimates of can still deliver a poor estimate of when treatment effects vary across groups. To give an example where this would be undesirable, notice that the weights depend on the timing of particular groups becoming treated; in an application where parallel trends holds across all time periods, the weights on underlying ’s would change depending on how many pre-treatment periods a researcher includes in the estimation. In the presence of heterogeneous treatment effects across groups, this would lead to the value of changing even though parallel trends holds across all periods and with underlying ’s fixed.

To summarize the results in this section, unlike the two period case, using TWFE regressions to implement DID identification strategies with multiple periods and variation in treatment timing is not robust to treatment effect heterogeneity. In order for to generally be equal to , it would require that is constant across groups and time periods. This does allow for some limited forms of treatment effect heterogeneity (e.g., it is weaker than requiring exact treatment effect heterogeneity across all units and time periods), but it is not generally robust to treatment effect heterogeneity with respect to group or time/length of exposure to the treatment. In some sense, this is a major theme of recent work critiquing TWFE regressions for implementing DID identification strategies — that they implicitly impose stronger requirements on the data generating process than the DID identification strategy would suggest, and that the failure of these additional requirements to holds (particularly various forms of treatment effect homogeneity) can lead to poor estimates of treatment effect parameters of interest. The next section shows that a number of alternative approaches can be used to directly target particular parameters of interest while (i) being robust to general forms of treatment effect heterogeneity and (ii) not being much more complicated to implement than a TWFE regression.

3.2 Alternative Approaches

The previous section suggested notable limitations of TWFE regressions for implementing difference-in-differences identification strategies, particularly in the presence of treatment effect heterogeneity. This section considers alternative approaches that are robust to treatment effect heterogeneity. One of the themes of this section is to more clearly separate identification from estimation, and then to develop estimation strategies that directly target identified parameters of interest. The first part shows that group-time average treatment effects (and hence , , as well as other aggregations of group-time average treatment effects) are nonparametrically identified under Assumption 4 and without requiring additional assumptions restricting treatment effect heterogeneity. The second part considers alternative estimation strategies to TWFE regressions mainly focusing on the approach suggested in [29], the “imputation” approaches suggested in [60, 48, 14], and the “regression” approaches suggested in [76, 77].

Identification

To start with, consider identifying . The following result shows that is identified in a DID setup without imposing assumptions limiting treatment effect heterogeneity.

Proposition 2 ([29]).

In the setup considered in this section and under Assumptions 3 and 4, , and for all (i.e., post-treatment time periods for group ),

The proof of Proposition 2 is provided in Appendix A. The result is quite similar to the one provided in Section 2 in the two period case. In particular, can be recovered by taking the actual path of outcomes experienced by group from its “base period” (this is period which is the period right before group becomes treated) to period and comparing it to the path of outcomes that group would have experienced over these time periods if it had not become treated. Under parallel trends, this counterfactual path of outcomes can be recovered by the path of outcomes that the never-treated group experienced over the same time periods.171717It is worth pointing out that the result in Proposition 2 can hold under weaker versions of the parallel trends assumption than the one that is provided in Assumption 4. In particular, this result does not require parallel trends to hold in all time periods and for all groups. This can be important particularly in applications where the number of time periods (especially pre-treatment time periods) is relatively large. See [29, 62] for more discussions along these lines. Given that is identified for all and post-treatment time periods, this further implies that other treatment effect parameters such as and can be recovered as well.

Estimation

This section introduces and compares several recently proposed estimation strategies that are able to circumvent the problems with TWFE regressions discussed above. In particular, this section discusses [29], the imputation approaches proposed in [60, 48, 14] and regression approaches proposed in [76, 77]. In the presence of treatment effect heterogeneity, all of these approaches are notably more robust than conventional TWFE regressions in applications with multiple time periods and variation in treatment timing. Compared to each other, these approaches differ in terms of (i) how they have been implemented in software, (ii) how they handle covariates, and (iii) some differences related to trading off robustness and efficiency.

Moreover, all of these approaches follow roughly the same strategy. Each of them involves a two-step procedure where the first step targets underlying treatment effect parameters (e.g., ’s) without imposing restrictions on treatment effect heterogeneity and involving only the “good comparisons” that show up in the TWFE regression above while explicitly omitting the “bad comparisons” that also show up there. In a second step, these approaches aggregate the underlying treatment effect parameters back into target parameters of interest such as an overall or into an event study.

To start with, consider the case where Assumption 4 holds and consider estimating .

[29]:

[29] propose several estimators of group-time average treatment effects. The simplest approach, based on the constructive identification result in Proposition 2, is to simply replace population moments with their sample counterpart; that is,

In other words, take the average path of outcomes experienced by group from their “base period” to the current period and adjust it by the path of outcomes taken by the never-treated group over the same time periods. There are alternative related estimators that can be rationalized under Assumption 4. For example, using not-yet-treated units as the comparison group results in

Under the full version of Assumption 4, both of these estimators leave some information on the table. First, neither uses information in periods before period . Second, neither uses information on units that become treated after period but before period . Along these lines, further consider

where . This is a variation of the build-the-trend estimator proposed in [62] which uses all available untreated units in each period to “build” the trend between periods and . Relative to [62], the difference is that this approach uses all available pre-treatment periods as the “base period” and averages over all of them (see Section A.1 for a more detailed explanation of where this estimator comes from). At any rate, this estimator addresses both of pieces of information that were not used above.

Imputation Approaches:

Imputation estimators for DID are proposed in [60, 48, 14]. The intuition for the imputation approach is to exploit the close connection between parallel trends assumptions and the model for untreated potential outcomes given in Equation 2. To more deeply understand this approach, it is helpful to define as the set of observations where (in particular, this includes all observations for the never-treated group as well as pre-treatment observations for units that eventually become treated) and to define as the set of observations where (which includes post-treatment observations for units that ever participate in the treatment). The imputation algorithm proceeds as follows.

Step 1: Using the set of observations , estimate the model for untreated potential outcomes in Equation 2. Note that, even in the case where the data itself is a balanced panel, this regression uses the data in which is an unbalanced panel. This results in estimates of both the time fixed effects and the unit fixed effects, and , for all time periods and all units.181818Note that this step enforces the requirements that (i) there are no units already treated in the first period, and (ii) there can be no time periods after which all units become treated. For (i), any units that are already treated by the first period will not have any observations in , and, therefore, their unit fixed effects cannot be estimated. For (ii), if there are time periods after all units have become treated, there will be no observations from those time periods in , and no time period fixed effects can be estimated in those periods.

Step 2: For each observation in , impute its untreated potential outcome by Given this step, for observations in , both and are now available.

Given the imputation procedure above, one can compute estimates of treatment effect parameters of interest by calculating particular averages of differences between observed outcomes and imputed outcomes among observations in . For example, an estimate of is given by

There are also interesting connections between the imputation approach and the [29] approach. For example, notice that can be expressed as an imputation.

where

In other words, the imputed value of the untreated potential outcome using [29] is whatever the outcome was in the “base period” plus the average path of outcomes experienced by the treated group. Alternatively, if one were to estimate the model in Equation 2 using only the never treated group and set , then the imputation estimator here would be numerically equal to .

Regression Approaches:

To conclude this section, consider the approaches proposed in [76, 77]. These approaches both estimate group-time average treatment effects using regressions, and, additionally provide further interesting connections between the various different alternative approaches to TWFE regressions that have been discussed above. [76] propose a fully interacted regression to recover estimates of group-specific ATTs that avoid the issues related to TWFE regressions191919[76] use the terminology cohort-specific ATTs. “Cohort” has the same meaning as “group” in the terminology of the current chapter. [76] also write their target parameters in terms of event-time rather than calendar time; and, in particular, that paper targets estimating the closely related parameter cohort-specific ATT, (which is the average treatment effect for group when they have been exposed to the treatment for exactly periods). In terms of group-time average treatment effects .

| (7) |

Interestingly, one can show that .202020This expression holds for post-treatment time periods (that is, for ). In pre-treatment periods, the default implementation of [29] varies the “base period” across different pre-treatment periods while the default implementation of [76] fixes the “base period” to be the period right before treatment (i.e., when ) for both pre- and post-treatment periods. This leads to different estimates (and different interpretations) in pre-treatment periods between the two approaches. However, if one uses the approach in [29] and fixes the base period to be the period right before treatment, then both approaches deliver identical estimates in pre-treatment periods as well. This suggests a close connection between the [29] approach of directly calculating averages and regression-based approaches. However, this equality should not be surprising as the fully interacted regression proposed in [76] can be seen as a way to use a regression to calculate a large number of averages. In fact, this also provides an explanation for why TWFE regressions work well in the case with only two time periods — in that case, like the [76] regression with multiple periods and variation in treatment timing, the model is fully saturated in terms of interactions between groups and time periods.

Next, consider the approach suggested in [77] which involves estimating group-time average treatment effects using the following regression212121[77] primarily discusses an alternative pooled OLS regression that includes group indicators rather than the unit fixed effect in Equation 8; however, [77] points out the equivalence of these regressions and this chapter emphasizes the TWFE version of the regression only because it is more straightforward to compare it to the other approaches discussed in this chapter.

| (8) |

This regression is very similar to the one suggested in [76] (the differences about being written in terms of event time or calendar time are unimportant because one can easily switch between the two). Relative to the regression in Equation 7, the more important difference is that this regression only includes post-treatment interaction terms. There is tradeoff between these two approaches. [76] delivers estimates of treatment effect parameters in pre-treatment time periods, which can be used for pre-testing the parallel trends assumption, while the regression in Equation 8 does not. On the other hand, the regression in Equation 8 can be shown to be more efficient (under some conditions) where the intuition for this sort of result is that this regression exploits the extra information coming from parallel trends holding in all pre-treatment periods. That said, the regression in Equation 7 tends to be more robust in the sense that violations of parallel trends in pre-treatment periods do not lead to biased estimates of treatment effect parameters in post-treatment periods (as long as parallel trends holds in the post-treatment periods).

Another interesting feature of the regression in Equation 8 is that ; that is, the regression in Equation 8 delivers numerically identical estimates as the imputation approach discussed above. This suggests a high degree of similarity between all the approaches that have been discussed so far: one version of [29] gives numerically identical estimates as the fully-interacted regression of [76]; the fully interacted regression of [76] only differs from the regression proposed in [77] in terms of whether or not it includes interactions in pre-treatment periods (trading off robustness and efficiency); and the regression in [77] delivers numerically identical results to the imputation procedure discussed above.

One final comment is that the regression approaches in [76, 77] may be particularly appealing in applications where the researcher is primarily interested in estimating and conducting inference on the group-time average treatment effects themselves — in this case, these approaches can be implemented using standard software for panel data regressions. In cases where the researcher is interested in aggregated treatment effect parameters such as or , then all of the procedures that have been discussed involve two-step estimation procedures where inference is complicated by needing to account for first-step estimation effects, and, therefore, one would typically need to use specialized software implementations of different approaches.

3.3 Event Studies and Pre-Testing

The TWFE regressions that have been discussed so far target estimating a single overall treatment effect parameter. The next most common target parameter in applied work is the event study; that is . Event studies are useful to understand treatment effect dynamics (i.e., how the effect of participating in the treatment varies with length of exposure to the treatment) as well as to implement “pre-tests” of the parallel trends assumption by computing for values of less than 0. If the parallel trends assumption holds, then these pre-treatment versions of should be equal to 0.

Similar to the TWFE regression in Equation 1 above, event studies have often been implemented with the following event study regression:

| (9) |

where is a binary variable that is equal to 1 for unit in period if unit has been treated for exactly periods in period and is equal to 0 otherwise. For example, is equal to one for units that become treated in period and is equal to zero for all other units; is equal to one for units that became treated in period and is equal to zero for all other units; and is equal to all units that become treated in period and is equal to 0 for all other units. For units that do not participate in the treatment in any time period, for all values of .222222While the event study regression in Equation 9 — sometimes called the “fully dynamic” event study regression — is probably the most common in applications, there are alternative versions of event study regressions that show up in applications. For example, a number of papers “bin” the endpoints; i.e., group all event times far enough before or after the treatment takes place. To keep the arguments from becoming too complicated, the current chapter focuses here on a main case for the event study regression but [14, 76] include substantially more details and cover more general cases than those considered here.

Notation:

To provide a decomposition result for the event study regression in Equation 9 requires introducing some more notation. First, define

where collects across all possible values of , averages across time periods, and is the double de-meaned version of (with respect to unit and time fixed effects). These are all dimensional vectors. Further, recall that knowing a unit’s group pins down its entire path of participating in the treatment; the decomposition below provides group-specific weights and it is therefore helpful to have an expression converting between and group. Along these lines, define . One can show that . Defining to be the dimensional vector that collects for , this implies that (see discussion around Equation 20 in Appendix A for additional explanation).

The next result considers interpreting event study regressions in the presence of heterogeneous treatment effects. It is a simplified version of the main result in [76]. In particular, it is specialized to the case where (i) there are no units that are already treated in the first time period (or those units are dropped), (ii) all leads and lags of participating in the treatment except are included in the event study regression (which is the most common practice in applications), and (iii) there is a never treated group (or, alternatively, post-treatment periods after all units have become treated are excluded).232323One other difference is that the next result as stated is a decomposition in the sense that it does not use the parallel trends assumption or involve potential outcomes; this is a minor difference though and is done here mainly to make this result more comparable to the Bacon decomposition in Proposition 1.

Proposition 3 ([76]).

Under the setup considered in this section,

where which satisfies the following properties:

(i)

(ii) for ,

The result in Proposition 3 is interesting along several dimensions. First, notice that, under Assumption 4,

As expected, this suggests a relationship between the event study regression and group-time average treatment effects at the corresponding length of exposure.

The main negative implication of Proposition 3 is that includes differences in paths of outcomes at other lengths of exposure to the treatment besides . As for the TWFE regression considered above, this means that, for certain patterns of group-time average treatment effects, could be much different from . Second, at the “correct” length of exposure to the treatment (as in property (i) of the weights in Proposition 3), the weights sum to 1 across groups; this is a good property though, unlike , the weights on underlying group-time average treatment effects are not equal to the relative size of a particular group (i.e., in general, ). Third, as in property (ii) of the weights, the weights at “incorrect” lengths of exposure sum to 0. An interesting implication of these properties of the weights is that a sufficient condition for to be equal to is that be constant across groups for all .242424In this case, property (ii) implies that does not include for any any ; property (i) further implies that will be equal to the “weighted average” of across groups but these are all equal to each other in this case so that . Relative to the approaches in [29, 76], this suggests that for to equal requires the additional condition limiting treatment effect heterogeneity that does not vary across groups. Relative to the TWFE regression considered earlier though, the event study regression does not require the additional condition that is constant across in order to recover its target parameter.

That being said, this discussion still suggests important advantages of the new DID approaches relative to running an event study regression — they can directly target the natural target parameter without requiring additional conditions limiting treatment effect heterogeneity. Furthermore, the setup in Proposition 3 is favorable for an event study regression; like the TWFE regression, it is very easy to introduce conceptual mistakes such as including units that are already treated in the first period or to estimate event studies in periods where no untreated comparison group is available. The event study regression can still “run” in these cases though the problems with it are likely to be more severe in these sorts of setups (see [14, 76] for more details about more complicated setups). This suggests further advantages of using new approaches in this context.

Finally, event study regressions are also commonly used to “pre-test” the parallel trends assumption — that is, to attempt to check if the parallel trends assumption held in periods before the treatment was implemented as a way to validate the parallel trends assumption. Proposition 3 suggests a major limitation of using the event study regression for this purpose because group-time average treatment effects at other lengths of exposure (including post-treatment group-time average treatment effects) show up in for values of . By way of contrast, for values of , can be used to pre-test the parallel trends assumption and does not contain group-time average treatment effects from any incorrect lengths of exposure. Although pre-testing the parallel trends assumption is very useful in most applications, there are some important limitations that researchers should be aware of. First, pre-tests can have low power. That is, there can be meaningful violations of parallel trends that pre-tests may fail to detect. Second, conditioning on passing a pre-test (i.e., only reporting results that pass a pre-test) can lead to distorted inferences. [69] discusses both of these issues extensively; see also [71] for more details as well.

4 Extensions

There are a number of useful extensions to the results from the previous section. This section covers what are arguably two of the most useful extensions: (i) cases where the parallel trends assumption only holds after conditioning on some observed covariates, and (ii) how to use a sensitivity analysis in the case where the researcher is worried that parallel trends assumptions may be violated. Table 4 below provides additional references for more extensions.

4.1 Conditional Parallel Trends Assumptions

Parallel trends assumptions can often be substantially more plausible if they involve conditioning on observed covariates. The idea here is to compare the paths of outcomes among treated and untreated units conditional on having the same characteristics. This section separately considers cases where the covariates are time-invariant and time-varying which are, to some degree, conceptually different.

Time Invariant Covariates

To start with, consider the case where a researcher wants to make the parallel trends assumptions conditional on time-invariant covariates. This is a leading case in a number of applications. For example, in industrial organization applications using firm-level data, a researcher may wish to condition on a firm’s industry (which is time-invariant) in the parallel trends assumption. Similarly, in applications in labor economics with individual level data, the most important covariates are often variables like a person’s background/demographic characteristics or other variables like a person’s education that either do not vary over time at all or vary so little (e.g., years of education for adults) that they are effectively time-invariant. A version of the parallel trends assumption that conditions on time-invariant covariates is given by

Assumption 5.

For all , and for all ,

This assumption says that, conditional on covariates , paths of untreated potential outcomes are the same for all groups. As in Section 3, there are multiple possible identification arguments and estimation strategies that are available under this assumption. The next result provides a doubly robust expression for under Assumption 5.

Proposition 4.

Under Assumption 5 and additional regularity conditions (see [29, Theorem 1 ]),

where , (which is the probability of being in group conditional on covariates and either being in group or being in the never-treated group), and .

Moreover, this expression for is doubly robust in the sense that, given parametric working models and for the propensity score and outcome regression, respectively, the sample analogue of this expression is consistent for if either model is correctly specified.

The proof of Proposition 4 is provided in Appendix A and comes from [72, 29]. It is alternatively possible to develop “regression adjustment” ([53]) or propensity score weighting ([1]) estimands for . The main attractive property of the doubly robust estimand given above is that it gives the researcher two chances to correctly specify a model — either for or — and delivers consistent estimates of if either model is correctly specified. Moreover, this sort of estimand is also closely related to the literature on double/de-biased machine learning, and [34] uses this sort of doubly robust expression in order to be able to use modern machine learning techniques to estimate and .

The expression in Proposition 4 appears rather complicated, and it is therefore useful to take it apart to some extent. Towards this end, it is useful to re-write the expression for as

where, in order to illustrate the double robustness property, the expression has replaced the population quantities and with the parametric working models and , respectively (and where and are the pseudo-true values of the parametric working models); to make the arguments concrete, it is reasonable to think of these as being a linear regression model and logit model, respectively. If is correctly specified, then the first term above is equal to and is closely related to regression adjustment DID strategies; moreover, the second term is equal to 0 in this case. If is incorrectly specified, then the first term is generally biased for . However, if the is correctly specified, then the second term effectively de-biases the first term; notice that it amounts to re-weighting the residuals from the regression of on among the never treated group. See [75] for additional discussion along these lines.252525It is also worth pointing out that the “weights” in Proposition 4 are very similar to those that show up in the propensity score weighting literature (e.g., [1]). These weights balance the distribution of covariates to be the same in the untreated group as it is for group . The term in the denominator of the weights, , turns out to be equal to one (see Appendix A for details), but in estimation ensures that the second part of the weights have mean one in finite samples (this type of adjustment often leads to improved finite sample performance; see, for example, [17]). Other work on double robustness includes [68, 73, 58].

Alternatively, imputation estimation strategies can also be used in the context of the conditional parallel trends assumption in Assumption 5. In particular, similar to the imputation estimator discussed in Section 3, one can estimate the model

using all available untreated observations, and then impute untreated potential outcomes for treated observations by

Given this imputation, one can compute treatment effect parameters of interest as in the previous section. This is conceptually similar to the regression adjustment strategy discussed above, but it provides a convenient way to globally estimate a model for untreated potential outcomes which is both relatively simple and can be more efficient than running separate group by time regressions. As a final comment, the [29] and imputation are quite similar; the [29] approach is able to more flexibly deal with covariates while the imputation tends to be simpler to implement as it only involves running regressions, computing predicted values, and averaging.

Time Varying Covariates