Nonparametric conditional local

independence testing

Abstract.

Conditional local independence is an asymmetric independence relation among continuous time stochastic processes. It describes whether the evolution of one process is directly influenced by another process given the histories of additional processes, and it is important for the description and learning of causal relations among processes. We formulate a model-free framework for testing the hypothesis that a counting process is conditionally locally independent of another process. To this end, we introduce a new functional parameter called the Local Covariance Measure (LCM), which quantifies deviations from the hypothesis. Following the principles of double machine learning, we propose an estimator of the LCM and a test of the hypothesis using nonparametric estimators and sample splitting or cross-fitting. We call this test the (cross-fitted) Local Covariance Test ((X)-LCT), and we show that its level and power can be controlled uniformly, provided that the nonparametric estimators are consistent with modest rates. We illustrate the theory by an example based on a marginalized Cox model with time-dependent covariates, and we show in simulations that when double machine learning is used in combination with cross-fitting, then the test works well without restrictive parametric assumptions.

1. Introduction

Notions of how one variable influences a target variable are central to both predictive and causal modeling. Depending on the objective, the relevant notion of influence can be variable importance in a predictive model of the target, but it can also be the causal effect of the variable on the target. In either case, we can investigate influence conditionally on a third variable – to quantify the added predictive value, the direct causal effect or the causal effect adjusted for a confounder. Our interests are in an asymmetric notion of direct influence among stochastic processes, which is not adequately captured by classical (symmetric) notions of conditional dependence. The objective of this paper is therefore to quantify this notion of asymmetric influence and specifically to develop a new nonparametric test of the hypothesis that one stochastic process does not directly influence another.

The hypothesis we consider is formalized as the hypothesis of conditional local independent – a concept introduced by Schweder (1970) as a continuous time formalization of the phenomenon that the past of one stochastic process does not directly influence the evolution of another stochastic process. As such, conditional local independence is a continuous time version of the discrete time concept of Granger non-causality (Granger, 1969).

To illustrate the concept of conditional local independence we will in this introduction consider an example involving three processes: , and – see Figure 1. The process is the indicator of death, , for an individual with survival time , and denotes the total pension savings of the individual at time . The process is a covariate process, e.g., health variables or employment status, that may directly affect both the pension savings and the survival time. This is indicated in Figure 1 by edges pointing from to and . Edges pointing from to and indicate that a death event directly affects both and (which take the values and , respectively, after time , see Section 2.2).

To define conditional local independence let denote the filtration generated by the - and -processes. The -algebra represents the information contained in the - and the - processes before time . Informally, the process is conditionally locally independent of the process given if does not add predictable information to about the infinitesimal evolution of . For this particular example this means that the conditional hazard function of does not depend on given . In Figure 1 the hypothesis of interest, that is conditionally locally independent of given , is represented by the lack of an edge from to .

A systematic investigation of algebraic properties of conditional local independence was initiated by Didelez (2006, 2008, 2015). She also introduced local independence graphs, such as the directed graph in Figure 1, to graphically represent all conditional local independencies among several processes, and she studied the semantics of these graphs. This work was extended further by Mogensen & Hansen (2020) to graphical representations of partially observed systems. While we will not formally discuss local independence graphs, the problem of learning such graphs from data was an important motivation for us to develop a nonparametric test of conditional local independence. A constraint based learning algorithm of local independence graphs was given by Mogensen et al. (2018) in terms of a conditional local independence oracle, but a practical algorithm requires that the oracle is replaced by conditional local independence tests.

Another important motivation for considering conditional local independence arises from causal models. With a structural assumption about the stochastic process specification, a conditional local independence has a causal interpretation (Aalen, 1987; Aalen et al., 2012; Commenges & Gégout-Petit, 2009), and if the causal stochastic system is completely observed, a test of conditional local independence is a test of no direct causal effect. If the causal stochastic system is only partially observed, a conditional local dependency need not correspond to a direct causal effect due to unobserved confounding, but the projected local independence graph, as introduced by Mogensen & Hansen (2020), retains a causal interpretation, and its Markov equivalence class can be learned by conditional local independence testing. In addition, within the framework of structural nested models, testing the hypothesis of no total causal effect can also be cast as a test of conditional local independence (Lok, 2008).

To appreciate what conditional local independence means – and, in particular, what it does not mean – it is useful to compare with classical conditional independence. In our example, is conditionally locally independent of given , but this implies neither that (as processes), nor that . In fact, these conditional independencies cannot hold in this example where for – except in special cases such as being a deterministic function of . Theorem 2 in Didelez (2008) gives a sufficient condition for to hold in terms of the local independence graph, but this condition is also not fulfilled by the graph in Figure 1 due to the edge from to . Didelez (2008) argues that being conditionally locally independent of given heuristically means that , but this is technically problematic in continuous time. If has a continuous distribution, then for any fixed , almost surely, whence is almost surely -measurable and conditionally independent of anything given . It is thus not possible to use this heuristic to formally define conditional local independence in continuous time. See instead the formal Definition 2 by Didelez (2008) or our Definition 2.1.

Several examples from health sciences given by Didelez (2008) demonstrate the usefulness of conditional local independence for multivariate event systems, and more recent attention to event systems in the machine learning community (Zhou et al., 2013; Xu et al., 2016; Achab et al., 2017; Bacry et al., 2018; Cai et al., 2022) testifies to the relevance of conditional local independence. This line of research relies primarily on the linear Hawkes process model, which is effectively used to infer local independence graphs – sometimes even interpreted causally. The Hawkes model is attractive because conditional local independencies can be inferred from corresponding kernel functions being zero – and statistical tests can readily be based on parametric or nonparametric estimation of kernels. A less attractive property of the Hawkes model is that any such test cannot be expected to maintain level if the model is misspecified. This is compounded by the Hawkes model not being closed under marginalization (also known as non-collapsibility), which means that even within a subsystem of a linear Hawkes process, conditional local independence cannot be tested correctly using a Hawkes model.

The challenge of model misspecification and non-collapsibility is investigated further in Sections 2.2 and 6 based on an extension of our introductory example and Cox’s survival model. Both the Hawkes model and the Cox model illustrate that conditional local independence might be expressed and tested within a (semi-)parametric model, but non-collapsibility – and model misspecification, in general – makes us question the validity of a model based test. Thus there is a need for a nonparametric test of the hypothesis of conditional local independence. Moreover, since we cannot translate the hypothesis into an equivalent hypothesis about classical conditional independence, we cannot directly use existing nonparametric tests, such as the GHCM (Lundborg, Shah & Peters, 2022), of conditional independence.

We propose a new nonparametric test when the target process is a counting process and is a real valued process, and where the hypothesis is that is conditionally locally independent of given a filtration . In the context of the introductory example, . We consider a counting process target primarily because the theory of conditional local independence is most complete in this case, but generalizations are possible – we refer to the discussion in Section 7. Within our framework we base our test on an infinite dimensional parameter, which we call the Local Covariance Measure (LCM). It is a function of time, which is constantly equal to zero under the hypothesis. Our main result is that the LCM can be estimated by using the ideas of double machine learning (Chernozhukov et al., 2018) in such a way that the estimator converges uniformly at a -rate to a mean zero Gaussian martingale under the hypothesis of conditional local independence. We use the LCM to develop the (cross-fitted) Local Covariance Test ((X)-LCT), for which we derive uniform level and power results.

1.1. Organization of the paper

In Section 2 we introduce the general framework for formulating the hypothesis of conditional local independence. This includes the introduction in Section 2.1 of an abstract residual process, which is used to define the LCM as a functional target parameter indexed by time. The LCM equals the zero-function under the hypothesis of conditional local independence, and to test this hypothesis we introduce an estimator of the LCM in Section 2.3. The estimator is a stochastic process, and we describe how sample splitting is to be used for its computation via the estimation of two unknown components.

In Section 3 we give interpretations of the LCM and its estimator. We show that the LCM estimator is a Neyman orthogonalized score statistic in Section 3.1, and in Section 3.2 we relate LCM to the partial copula when is time-independent.

In Section 4 we state the main results of the paper. We establish in Section 4.1 that the LCM estimator generally approximates the LCM with an error of order . Under the hypothesis of conditional local independence, we show that the (scaled) LCM estimator converges weakly to a mean zero Gaussian martingale. The estimator requires a model of the target process as well as the process conditionally on to achieve the orthogonalization at the core of double machine learning. The model of is in this paper expressed indirectly in terms of the residual process, and we show that if we can learn the residual process at rate and the model of at rate such that and for then we achieve a -rate convergence of the LCM estimator. We also show that the variance function of the Gaussian martingale can be estimated consistently, and we give a general result on the asymptotic distribution of univariate test statistics based on the LCM estimator. All asymptotic results are presented in the framework of uniform stochastic convergence.

Section 5 gives explicit examples of univariate test statistics, including the Local Covariance Test based on the normalized supremum of the LCM estimator. Its asymptotic distribution is derived and we present results on uniform asymptotic level and power. In Section 5.2 we present the generalization from the sample split estimator to the cross-fit estimator. Though this estimator and the corresponding cross-fit Local Covariance Test (X-LCT) are a bit more involved to compute and analyze, X-LCT is more powerful and thus our recommended test for practical usage.

The survival example from the introduction is used and elaborated upon throughout the paper. We introduce a Cox model in terms of the time-varying covariate processes, and we report in Section 6 the results from a simulation study based on this model.

The paper is concluded by a discussion in Section 7, and Appendices A through E contain: proofs of results in this paper (A); definitions and results on uniform asymptotics (B); a uniform version of Rebolledo’s martingale CLT (C); an overview of achievable rate results for estimation of nuisance parameters that enter into the LCM estimator (D); and additional results from the simulation study (E).

2. The Local Covariance Measure

In this section we present the general framework of the paper, we define conditional local independence and we introduce the Local Covariance Measure as a means to quantify deviations from conditional local independence. In Section 2.3 we outline how the Local Covariance Measure can be estimated using double machine learning and sample splitting. We illustrate the central concepts and methods by an example based on Cox’s survival model with time-varying covariates.

We consider a counting process and another real value process , both defined on the probability space . All processes are assumed to be defined on a common compact time interval. We assume, without loss of generality, that the time interval is . We will assume that is adapted w.r.t. a right continuous and complete filtration , and we denote by the right continuous and complete filtration generated by and . We assume throughout that is càglàd (that is, has sample paths that are continuous from the left and with limits from the right), which will ensure bounded sample paths and that the process is -predictable.

In the survival example of the introduction, is the indicator of whether death has happened by time , and there can only be one event per individual observed. Furthermore, and . Our general setup works for any counting process, thus it allows for recurrent events and adapted censoring, and the filtration can contain the histories of any number of processes in addition to the history of itself.

2.1. The hypothesis of conditional local independence

The counting process is assumed to have an -intensity , that is, is -predictable and with

being the compensator of ,

| (1) |

is a local -martingale. Within this framework we can define the hypothesis of conditional local independence precisely.

Definition 2.1 (Conditional local independence).

We say that is conditionally locally independent of given if the local -martingale defined by (1) is also a local -martingale.

For simplicity, we will refer to this hypothesis as local independence and write

| (2) |

As argued in the introduction, the hypothesis of local independence is the hypothesis that observing on does not add any information to about whether an -event will happen in an infinitesimal time interval . Definition 2.1 captures this interpretation by requiring that the -compensator, , of is also the -compensator. Thus, is also the -intensity under .

If has -intensity , the innovation theorem, Theorem II.T14 in Brémaud (1981), gives that the predictable projection is the (predictable) -intensity. Local independence follows if is -predictable. Intensities are, however, only unique almost surely, and we can have local independence even if is not a priori -predictable but have an -predictable version. When has -intensity , is thus equivalent to having an -predictable version. We find Definition 2.1 preferable because it directly gives an operational criterion for determining whether has an -predictable version of a -intensity.

Since is assumed càglàd, and thus especially -predictable, the stochastic integral

| (3) |

is under a local -martingale. A test could be based on detecting whether (3) is, indeed, a local martingale. We will take a slightly different approach where we replace the integrand by a residual process as defined below. We do so for two reasons. First, to achieve a -rate via double machine learning we need the integrand to fulfill (4) below. Second, other choices of integrands than could potentially lead to more powerful tests.

Definition 2.2 (Residual Process).

A residual process of given is a càglàd stochastic process that is -adapted and satisfies

| (4) |

The geometric interpretation is that the residual process evolves such that is orthogonal to within at each time . One obvious residual process is the additive residual process given by

where denotes the predictable projection of the càglàd process , see Theorem VI.19.2 in (Rogers & Williams, 2000). The additive residual projects onto the orthogonal complement of , but this may not necessarily remove all -predictable information from . An alternative choice that does so under sufficient regularity conditions is the quantile residual process given by

where is the conditional distribution function given by . The quantile residual process satisfies (4) provided that is continuous. In Section 3.1 we discuss additional transformations of that can also be applied before any residualization procedure.

We will formulate the general results in terms of an abstract residual process, but we focus on the additive residual process in the examples. Any non-degenerate residual process will contain a predictive model of (aspects of) given in order to satisfy (4). We use to denote the residual obtained by plugging in an estimate of that predictive model. For the additive residual process, the predictive model is and . For the quantile residual process, the predictive model is and .

We can now define our functional target parameter of interest, which we call the Local Covariance Measure.

Definition 2.3 (Local Covariance Measure).

With a residual process, define for

| (5) |

whenever the expectation is well defined. We call the function the Local Covariance Measure (LCM).

The following propositions illuminate how relates to the null hypothesis of being conditionally locally independent of given .

Proposition 2.4.

Under , the process is a local -martingale with . If is a martingale, then for .

To interpret in the alternative, we assume that has -intensity .

Proposition 2.5.

If , then for every ,

In particular, is the zero-function if and only if for almost all .

We note that under , the condition is sufficient to ensure that is a martingale and for all . By Proposition 2.5, the LCM quantifies deviations from in terms of the covariance between the residual process and the difference of the - and -intensities. To this end, note that if happens to be -adapted, then and is trivially locally independent of . The hypothesis of local independence is only of interest when is a strictly larger filtration than , that is, when provides information not already in .

For the additive residual process, where ,

provided that the expectations are well defined. Since the predictable projection has a càglàd version and is -predictable, and since is a local -martingale, is a local -martingale. If it is a martingale, it is a mean zero martingale, and

| (6) |

The computation above shows that the additive residual process defines the same functional target parameter as the stochastic integral (3) would. It is, however, the representation of as the expectation of the residualized stochastic integral that will allow us to achieve a -rate of convergence of the estimator of in cases where the estimator of converges at a slower rate.

2.2. A Cox model with a partially observed covariate process

To further illustrate the hypothesis of conditional local independence and the Local Covariance Measure we consider an example based on Cox’s survival model with time dependent covariates. This is an extension of the example from the introduction with being the time to death of an individual, and with and being time-varying processes. There is, moreover, one additional time-varying process in the full model.

An interpretation of the processes is as follows:

Periods of overweight or obesity may influence blood pressure in the long term, and due to, e.g., job market discrimination, high BMI could influence pension savings negatively. Death risk is influenced directly by BMI and blood pressure but not the size of your pension savings. Figure 2 illustrates two possible dependence structures among the three processes and the death time as local independence graphs, and we will use these two graphs to discuss the concept of conditional local independence of pension savings on time to death.

We assume that and that , and have continuous sample paths. Recall also that is the death indicator process. To maintain some form of realism, all processes are stopped at time of death, that is, , and for . This feedback from the death event to the other processes is reflected in Figure 2 by the edges pointing out of . Recall also that

is the filtration generated by the - and -processes. We use a similar notation for other processes and combinations of processes. For example, is the filtration generated by and all three -, -, and -processes. With denoting the -intensity of time of death based on the history of all processes, we assume in this example a Cox model given by

| (7) |

with a deterministic baseline intensity. It is not important that is a Cox model for our general theory, but it allows for certain theoretical computations in this example.

The fact that does not depend upon implies that is also the -intensity, and according to Definition 2.1, is conditionally locally independent of given . This is in agreement with the local independence graphs in Figure 2 where there is no edge in either of them from to .

We will take an interest in the case where is unobserved and test the hypothesis:

is conditionally locally independent of given .

That is, with unobserved we want test if the intensity of time to death given the history of , and depends on . To simplify notation let and – in accordance with the general notation. The -intensity is by the innovation theorem given as

| (8) |

while the -intensity is

| (9) |

and is equivalent to almost surely. Comparing (8) and (9) we see that holds in this example if , and a sufficient condition for this to be the case is

| (10) |

The condition (10) is in concordance with the left graph in Figure 2, see Theorem 2 in Didelez (2008), but not the right, and it implies . We will in Section 6.1 elaborate on condition (10) and give explicit examples.

We recall that can be reformulated as not depending on , and we could investigate the hypothesis via a marginal Cox model

| (11) |

and test if . The Cox model is, however, non-collapsible (Martinussen & Vansteelandt, 2013), and the semi-parametric model (11) is quite likely misspecified. Consequently, the test of is not equivalent to a test of .

Our proposed nonparametric test of does not rely on a specific (semi-)parametric model of . To test we consider the LCM using the additive residual process. Then (6) implies that

By Proposition 2.4, for under , whence conditional local independence implies , and we test by estimating and testing if it is constantly equal to .

Before introducing a general estimator of the LCM in Section 2.3 we outline how to estimate the end point parameter in this example. Due to and the appearance of the indicator in (9),

With i.i.d. observations and (nonparametric) estimates, , based on , we could compute the plug-in estimate

However, we cannot expect the plug-in estimator to have a -rate unless has -rate, which effectively requires parametric model assumptions on the intensity.

Using the definition of in terms of the additive residual process , we also have that

| (12) |

A double machine learning estimator based on the ideas by Chernozhukov et al. (2018) is therefore obtained by plugging in two nonparametric estimators:

To achieve a small bias and a -rate of convergence, we use sample splitting. The nonparametric estimates and are based on one part of the sample only, and are thus independent of the other part of the sample used for testing, see Section 2.3. To obtain a fully efficient estimator, multiple sample splits can be combined, e.g., via cross-fitting, see Section 5.2.

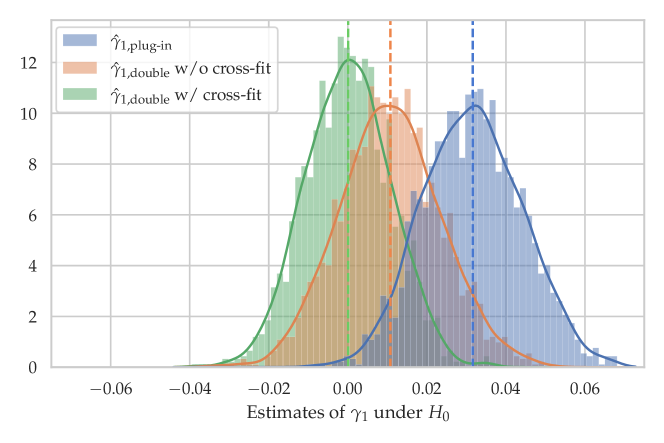

Figure 3 shows the distributions of and for the Cox example with , see Section 6.2 for details on the full model specification. The latter estimator was computed using cross-fitting but also without using any form of sample splitting. The figure illustrates the bias of , which is somewhat diminished by double machine learning without sample splitting and mostly eliminated by double machine learning in combination with cross-fitting.

2.3. Estimating the Local Covariance Measure

To estimate the LCM we assume that we have observed i.i.d. replications of the processes, , where observing signifies that anything adapted to the -th filtration is computable from observations. The process is adapted to , while is not, and denotes the smallest right continuous and complete filtration generated by and .

For each , we consider a sample split corresponding to a partition of the indices into two disjoint sets. We let and be estimates of the intensity and the residualization map, respectively, fitted on data indexed by only. By an estimate, , of we mean a (stochastic) function that can be evaluated on the basis of for , and its value, denoted by , is interpreted as a prediction of . The stochasticity in arises from its dependence on data indexed by , from which its functional form is completely determined. Similarly, is a function that can be evaluated on the basis of for to give a prediction of . In Section 6.1 we illustrate through the Cox example how and are to be computed in practice when we use sample splitting. In Section D we give more examples of such estimation procedures and discuss their statistical properties in greater detail.

To ease notation, we will throughout assume that denotes one additional process and filtration – independent of and with the same distribution as the observed processes. Then the estimated intensity and estimated residual process can be evaluated on , and thus we may write and to denote template copies of and for .

In terms of the estimates and we estimate LCM by the stochastic process given by

| (13) |

where . We can regard as a double machine learning estimator of , with the observations indexed by used to learn models of and , and with observations indexed by used to estimate based on these models. In Section 5.2 we define the more efficient estimator that uses cross-fitting, but it is instructive to study the simpler estimator based on sample splitting first.

In practical applications, we do not directly observe the filtration , but rather samples from the stochastic processes generating the filtration. In accordance with the introductory Cox example, consider and given by and for a third stochastic process , with possibly being multivariate. Within this setup, a general procedure for numerically computing the LCM is described in Algorithm 1. Here, historical regression refers to any method which regresses the outcome at a given time on the history of the regressors up to that time. For example, historical linear regression is discussed in Section 6 and various alternative methods are discussed in Appendix D. The choice of sample split will be discussed further in Section 5.2 in the context of cross-fitting.

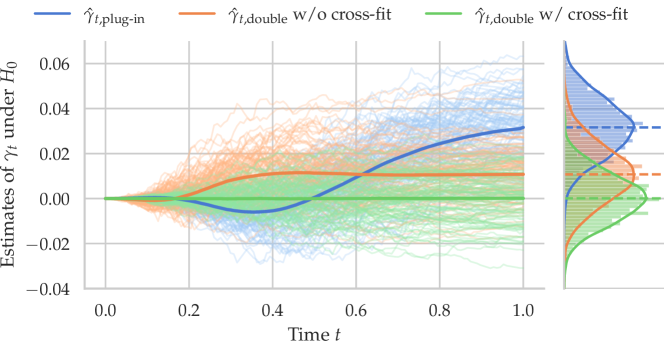

As in Section 2.2 we could suggest estimating the entire function by a simple plug-in estimator of using the representation (6). Figure 4 illustrates the distribution of estimators of the entire time dependent LCM for this plug-in estimator together with the double machine learning estimator with and without using cross-fitting. The figure also shows the distribution of the endpoint being the same distribution shown in Figure 3. The simulation is under , and we see that only the double machine learning estimator with cross-fitting results in estimated sample paths centered around .

3. Interpretations of the LCM estimator

In this section we provide some additional perspectives on and interpretations of the LCM. First we show that the LCM estimator can be seen as a Neyman orthogonalization of the score statistic for a particular one-parameter family. The abstract formulation of the residual process permits that we transform into another -predictable processes. Using this perspective, we may optimize the choice of the process in terms of power.

Next we show that when is independent of time, the test statistic reduces in a survival context to a covariance between -residuals and Cox-Snell-residuals, which we can link to the partial copula between and the survival time.

3.1. Neyman orthogonalization of a score statistic

Consider the one-parameter family of -intensities

for . Within this one-parameter family, the hypothesis of conditional local independence is equivalent to . The normalized log-likelihood with i.i.d. observations in the interval is

Straightforward computations show that

If were known, the score statistic satisfies . Moreover, under we have that is a consistent estimate of the asymptotic variance of the mean zero martingale . The hypothesis of local independence – with known – could thus be tested using the score test statistic .

The nuisance parameter is, however, unknown and we want to avoid restrictive parametric assumptions about . Replacing by the residual process in the score statistic gives a Neyman orthogonalized score

This score is linear in , and it is not difficult to show that it satisfies the Neyman orthogonality condition under , cf. Definition 2.1 in Chernozhukov et al. (2018). Indeed, Neyman orthogonality is implicitly a central part of the asymptotic results for the LCM estimator (in particular Lemma A.7). The Neyman orthogonalized score leads directly to the double machine learning estimator (13), and Neyman orthogonality in combination with sample splitting are key to showing the -rate of convergence for this estimator.

The perspective on the LCM estimator as a Neyman orthogonalized score statistic suggests that a test based on the LCM has most power against alternatives in the one-parameter family . If it happens that the most important alternatives are of the form

for some -predictable process different from , then we should replace by in our test statistic, that is, in the residualization procedure. Examples of processes are:

-

•

transformations, for a function

-

•

time-shifts, for

-

•

linear filters, for a kernel

-

•

non-linear filters, for a kernel and functions and .

Any finite number of such processes could, of course, also be combined into a vector process, and we could, indeed, generalize the LCM estimator (13) to a vector process. The generalization is straightforward.

3.2. Time-independent

A different perspective on the test statistic is obtained if is independent of time. If we consider a survival model where is time of death and , then is a baseline variable and

For , we see that since by assumption. Now is exponentially distributed with mean , thus

Using the additive residual process, the LCM estimator for is

which is simply the (negative) empirical covariance between the residuals and the Cox-Snell residuals .

If we use the quantile residual process , where , the residual is uniformly distributed and independent of provided is continuous. The LCM estimator for is

which is again an empirical covariance, but now between the generalized residuals and the Cox-Snell residuals. This variant of the LCM is closely related to the partial copula between and , which can be estimated as

See Petersen & Hansen (2021) for further details on the partial copula and how this statistic can be used to test the (ordinary) conditional independence . In contrast to the test based on the partial copula, extends to the -indexed estimator

whose asymptotic distribution as a Gaussian martingale follows from the general results of this paper.

4. General asymptotic results

In this section we derive uniform asymptotic results regarding the general LCM estimator as a stochastic process. In Section 5 we discuss how to construct tests of based on the asymptotic results.

We assume that has a -intensity , we let denote the -compensator of and let be the compensated local -martingale. We also recall that denotes the LCM estimator based on sample splitting as defined in Section 2.3. Within this framework we consider the decomposition

| (14) |

where the processes , and are given by

| (15) | ||||

| (16) | ||||

| (17) | ||||

| (18) | ||||

| (19) | ||||

| (20) |

We proceed to show that and each converge in distribution and that the remaining terms converge to the zero-process. This implies that is stochastically bounded in general, so the LCM estimator will asymptotically detect if the LCM is non-zero. Moreover, recall that is a version of under , and hence the processes and are (almost surely) the zero-process in this case. Thus it will follow that drives the asymptotic limit of the LCM estimator under . Based on these general asymptotic results we derive in Section 5 asymptotic error control for tests based on the LCM estimator.

4.1. Asymptotics of the LCM estimator

Our asymptotic results are formulated in terms of uniform stochastic convergence, which has also been discussed extensively in the recent literature on hypothesis testing (Shah & Peters, 2020; Lundborg, Shah & Peters, 2022; Lundborg, Kim, Shah & Samworth, 2022; Scheidegger et al., 2022; Neykov et al., 2021). Uniform convergence allows us to establish uniform asymptotic level of our proposed test, as well as power under local alternatives. We have collected key definitions and results related to uniform convergence in Appendix B.

To state uniform assumptions and asymptotic results we need to indicate a range of possible sampling distributions for which the assumptions apply and the results hold. For this purpose, we extend our setup and allow all data to be parametrized by a fixed parameter set . The set is not a priori assumed to have any structure, and simply indicates that , , , etc. have -dependent distributions. We generally denote evaluation of processes or derived quantities for a specific -value by a superscript, with the LCM, , in particular, depending on . The LCM estimator is likewise written as for to denote its dependence on the sampling distribution. The superscript notation is, however, heavy and unnecessary in many cases and we will suppress the dependency on whenever it is not needed. Any result that does not explicitly involve should be understood as a pointwise result for each .

The parametrization allows us to express convergence in distribution and probability uniformly over , which are denoted by and , respectively. These concepts are defined rigorously in Definition B.2. We note that uniform convergence reduces to classical (pointwise) convergence if is a singleton, which corresponds to fixing the sampling distribution. We also introduce the parameter subset

| (21) |

consisting of all parameter values for which the hypothesis of conditional local independence holds. Correspondingly, we will use and to denote stochastic convergences uniformly over .

We are now ready to formulate the underlying assumptions on the data required for our asymptotic results. See the discussion regarding possible relaxations in Section 7.

Assumption 4.1.

There exist constants , such that for any parameter value

-

i)

The -intensity of is càglàd with almost surely.

-

ii)

The residual process is càglàd with almost surely.

The estimator, , of and the estimator, , of the residual process are assumed to satisfy the same bounds as and . We note that Assumption 4.1 i) implies that is a true -martingale, and by the innovation theorem, . As a consequence, the -intensity inherits the boundedness from the -intensity , and is an -martingale. More generally, we have the following proposition ensuring that stochastic integrals are true martingales, e.g., that is a martingale under .

Proposition 4.1.

Under Assumption 4.1 it holds that each of the processes

are mean zero, square integrable -martingales for any .

To express the asymptotic distribution of we need its variance function.

Definition 4.2.

We define the variance function as

| (22) |

As everything else, the variance function, , is also indexed by the parameter , which we, for notational simplicity, suppress unless explicitly needed.

By taking in Proposition 4.1, Assumption 4.1 implies that for each ,

Moreover, is the variance of , which under is the same as the variance of .

With the assumptions above we can prove the following proposition about the uniform distributional limit of the process in the Skorokhod space , the space of càdlàg functions from to endowed with the Skorokhod topology. A corresponding pointwise result is an application of Rebolledo’s classical martingale CLT. Our generalization to uniform convergence is based on a uniform extension of Rebolledo’s theorem, see Theorem C.4 in Appendix C.

Proposition 4.3.

Under Assumption 4.1 it holds that

in as , where for each , is a mean zero continuous Gaussian martingale on with variance function .

To control the remainder terms in (14) we will bound the estimation errors in terms of the 2-norm, , on , i.e.,

for any process . We will make the following consistency assumptions on and .

Assumption 4.2.

Assume that when and let

Then each of the sequences , , and converge to zero uniformly over as , i.e.,

With this assumption we can establish that the remainder terms also converge uniformly to the zero-process.

To control the asymptotic behavior of the LCM estimator in the alternative we need to control the two terms and .

Proposition 4.5.

We note that might not vanish without an assumption like being the additive residual process, and it is not clear if will even converge in general. We will not pursue an analysis of the asymptotic behavior of in the general case. We note, however, that if we can estimate with a parametric rate, that is, , then it follows from the Cauchy-Schwarz inequality that is stochastically bounded, and still dominates in the alternative where .

We can combine all of the propositions into a single theorem regarding the asymptotics of the LCM estimator, which we consider as our main result.

Theorem 4.6.

Thus we have established the weak asymptotic limit of under . However, the variance function of the limiting Gaussian martingale is unknown and must be estimated from data. We propose to use the empirical version of (22),

| (24) |

for which we have the following consistency result.

We emphasize that is only the asymptotic variance function of the LCM estimator under . It is always the asymptotic variance function of , but in the alternative the asymptotic distribution of also involves the asymptotic distribution of and is thus more complicated.

Tests of conditional local independence can now be constructed in terms of univariate functionals of and that quantify the magnitude of the LCM. The asymptotics of such test statistics under are described in the following corollary, which is essentially an application of the continuous mapping theorem.

Corollary 4.8.

5. The Local Covariance Test

In this section we introduce a practically applicable test based on the LCM estimator. Using the asymptotic distribution of the LCM estimator we show that the asymptotic distribution of our proposed test is independent of the sampling distribution under and has an explicit representation. We show, in addition, uniform asymptotic level of the test, and we give a uniform power result for the additive residual process. Finally, we modify the test to be based on a cross-fitted estimator of the LCM instead of using sample splitting, and we show uniform level of that test.

To construct a test statistic based on the LCM estimator it is beneficial that its distributional limit does not depend on the variance function. As a simple example, consider the endpoint test statistic:

| (26) |

which under converges in distribution to by Corollary 4.8. The distribution of the latter is the standard normal distribution, and in particular it does not depend on .

Any test statistic constructed from should capture deviations of away from . The test statistic in (26) does, however, only consider the endpoint of the process, and since is not necessarily monotone, may deviate more from for other . Thus in order to increase power against such alternatives we consider the test statistic

| (27) |

We refer to as the Local Covariance Test statistic (LCT statistic). We proceed to show that the LCT statistic can be calibrated to obtain a test of with asymptotic level, and which has asymptotic power against any alternative with a non-zero LCM. This is the best we can hope for of any test based on the LCM estimator.

We note that it might be possible to establish similar results for other norms of the LCM, for example, a statistic based on a weighted -norm111such statistics are known as Anderson-Darling type statistics.. However, since other norms of the distributional limit will generally have a distribution with a complicated dependency on , we believe that the LCT statistic is the simplest to calibrate.

To establish uniform asymptotic level via Corollary 4.8 for tests based on test statistics such as (27) we need to assume that the asymptotic variances in are uniformly bounded away from zero.

Assumption 5.1.

There exists a such that for all it holds that .

5.1. Type I and type II error control

We proceed to show that under , the LCT statistic is distributed as , where is a standard Brownian motion. From this point onwards, we let denote a random variable with such a distribution and note that its CDF can be written as:

| (28) |

See, for example, Section 12.2 in Schilling & Partzsch (2012) where the formula is derived from Lévy’s triple law.

The -value for a test of equals , and since the series in (28) converges at an exponential rate, the -value can be computed with high numerical precision by truncating the series. Given a significance level , we also let denote the -quantile of , which exists and is unique since the right-hand side of (28) is strictly increasing and continuous. The Local Covariance Test (LCT) with significance level is then defined by

| (29) |

From Theorem 4.6 we can now deduce the asymptotic properties of the LCT under the hypothesis of conditional local independence. Recall that denotes uniform convergence in distribution under .

Theorem 5.1.

In general, we cannot expect that the test has power against alternatives to for which the LCM is the zero-function. This is analogous to other types of conditional independence tests based on conditional covariances, e.g., GCM (Shah & Peters, 2020). However, we do have the following result that establishes power against local alternatives with decaying at an order of at most .

5.2. Extension to cross-fitting

In Section 4 we considered sample splitting with observations indexed by used to estimate the two models and with observations indexed by used to estimate . Following Chernozhukov et al. (2018), we can improve efficiency by cross-fitting, i.e., by flipping the roles of and to obtain a second equivalent estimator of . Heuristically, the two estimators are approximately independent, and thus their average should be a more efficient estimator. This procedure generalizes directly to a partition of the indices into disjoint folds. The partition is assumed to have a uniform asymptotic density, meaning that as for each .

We estimate and using and subsequently estimate using . Then the -fold Cross-fitted LCM estimator, abbreviated as X-LCM, is defined as the average LCM estimator over the folds, i.e.,

| (30) |

where for each , the processes and are the model predictions of and , respectively, based on training data indexed by . We also define a -fold version of the variance estimator:

| (31) |

Now, similarly to the LCT statistic, the cross-fitted estimator can be used to construct a test statistic,

| (32) |

from which we define the following test of conditional local independence.

Definition 5.3.

We provide a summary of the computation of the X-LCT in Algorithm 2. The asymptotic analysis of generalizes to , but we will refrain from restating all results for the -fold cross-fitted estimator. For simplicity, we focus on the fact that the X-LCT is well calibrated.

Theorem 5.4.

Suppose that Assumption 4.2 is satisfied for every sample split . Under Assumptions 4.1 and 5.1, the X-LCT statistic satisfies

for . In particular, the X-LCT has uniform asymptotic level.

Note that cross-fitting recovers full efficiency in the sense that the scaling factor is rather than , which leads to a more powerful test. Moreover, the asymptotic distribution of does not depend on the number of folds , and any difference between various choices of can thus be attributed to finite sample errors. Larger values of will allocate more data to estimation of and , which intuitively should be the harder estimation problem. Following Remark 3.1 in Chernozhukov et al. (2018), we believe that a default choice of or should be reasonable in practice.

6. Simulation study

In this section we present the results from a simulation study based on the Cox example introduced in Section 2.2. We elaborate in Section 6.1 on the full model specification used for the simulation study – which will also illuminate how and can be modeled and estimated. The results from the simulation study focus on the distribution of the X-LCT statistic and validate the asymptotic level and power of the X-LCT . The latter is also compared to a hazard ratio test based on the marginal Cox model (11). The simulations were implemented in Python and the code is available222https://github.com/AlexanderChristgau/nonparametric-cli-test.

6.1. Cox model continued

Consider the same setup as in Section 2.2. To fully specify the model we need to specify the distribution of the processes , and . We suppose that and can be written in terms of as

| (33) |

where and are two functions defined on the triangle , and where and are two noise processes with mean zero. The processes , and are assumed independent, which implies (10) and thus that is conditionally locally independent of given .

The specific dependency of and on is known as the historical functional linear model in functional data analysis (Malfait & Ramsay, 2003). Within this model,

| (34) |

and on

where . Since

it follows that on ,

| (35) |

where the two baseline terms depending only on time have been merged into .

The computations above suggest how the estimators and could be constructed. That is, could be based on estimates of , and from the observations , and could be based on estimates of from . We would then have

for where denotes the estimate of , and similarly for . Particular choices of estimators and and their theoretical properties are reviewed in Appendix D. Our conclusion from this review is that for the historical functional linear model, sufficient rate results should be possible but have not yet been established rigorously.

More seriously, we found the available implementations limiting. Specifically, the historical linear regression estimator from the scikit-fda library was considered initially, but we found that fitting this model was too computationally expensive for a simulation study with cross-fitting. In principle, in our time-continuous setting, we would like to use a functional estimator of that would utilize the regularity along and . Initial experiments, however, suggested that the simpler historical regression described in Section 6.3 gave similar results as using the scikit-fda library, and we went with the less time consuming implementation.

6.2. Sampling scheme

The actual time-discretized simulations and computations were implemented using an equidistant grid with time points . Inspired by Harezlak et al. (2007), we generated the processes as follows: let and be independent random variables such that and such that , and are identically distributed with

Then the process is determined by

for . The processes and were then given by the historical linear model (33) with kernels and being one of the following four kernels:

To compute and , we evaluated the kernels on and approximated the integrals by Riemann sums. The full intensity for was specified with a Weibull baseline of the form

for and a choice of . To sample we applied the inverse hazard method, which utilizes that is standard exponentially distributed. That is, we sampled and numerically computed as a discretized approximation. For any given parameter setting, the baseline coefficient was chosen sufficiently large to ensure that would occur before time in more that samples.

With this setup, Assumption 4.1 is satisfied if , and were bounded. Since we use the Gaussian distribution, they are technically not bounded, but they could be made bounded by introducing a lower and upper cap. Due to the light tails of the Gaussian distribution such caps would have no noticeable effect on the simulation results, and the results we report are generated without a cap.

6.3. Implementation of estimators and tests

For our proof-of-concept implementation we used two simple off-the-shelf estimators.

To estimate we used the BoXHED2.0 estimator from Pakbin et al. (2021), based on the works of Wang et al. (2020) and Lee et al. (2021). In essence, the estimator is a gradient boosted forest adapted to the setting of hazard estimation with time-dependent covariates. The maximum depth and number of trees were tuned by 5-fold cross-validation over the same grid as in Pakbin et al. (2021). For computational ease, the hyperparameters were tuned once on the entire dataset instead of tuning them on each fold . In principle, this may invalidate the asymptotic properties of since it breaks the independence between and , but we believe that this dependency is negligible.

To estimate the predictable projection , we fitted a series of linear least squares estimators by regressing on for each . To stabilize the estimation error , we added a small -penalty with coefficient fixed across all experiments for simplicity. Since was sampled from a discretized historical linear model, the error should in principle converge with a classical -rate. However, the finite sample error is expected to be large since it accounts for linear regressions with up to predictors.

Based on these estimators, the X-LCT was implemented based on Algorithm 2. Following the recommendation by Chernozhukov et al. (2018, Remark 3.1.), we computed the X-LCT with folds. The associated -value was computed with the series representation of truncated to the first terms.

We compared our results for X-LCT with a hazard ratio test in the possibly misspecified marginal Cox model given by (11). This test was computed using the lifelines library (Davidson-Pilon, 2021), specifically the CoxTimeVaryingFitter model. The model was fitted with an -penalty with a coefficient set to (the default), and as a consequence the hazard ratio test is expected to be conservative.

6.4. Distributions of -values under

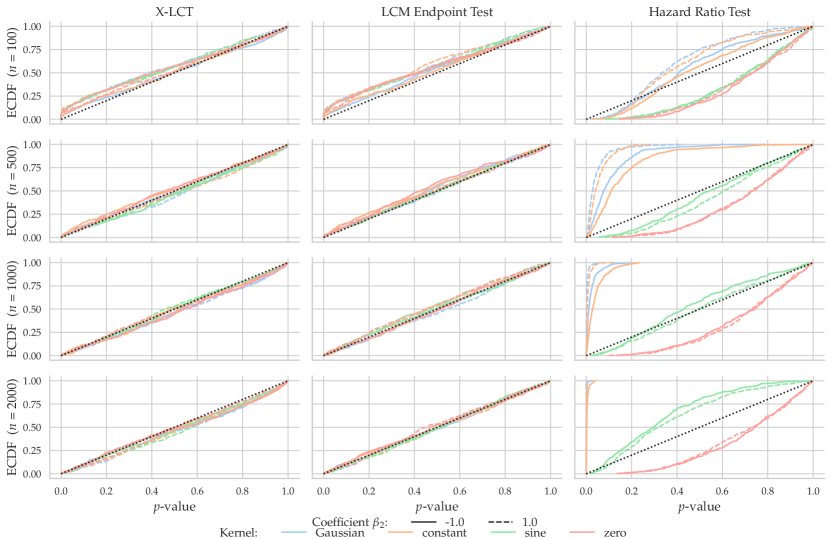

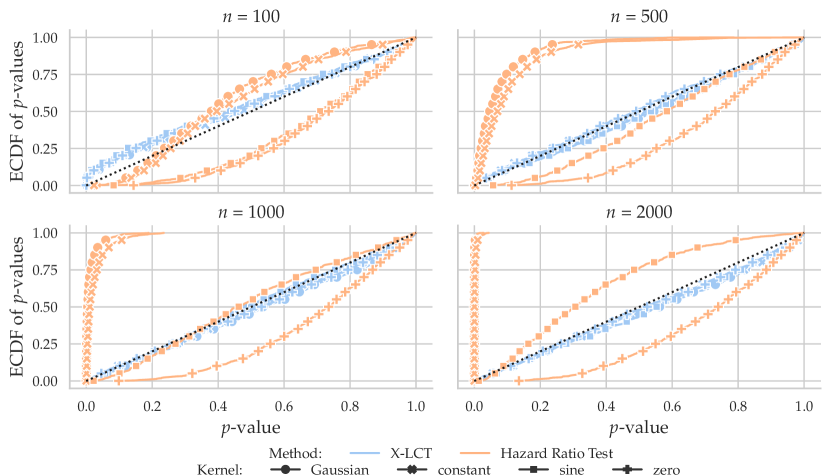

We examine the distributional approximation , cf. Theorem 5.4, by comparing the -values to a uniform distribution. Figure 5 shows the empirical distribution functions of the -values computed from data simulated according to the scheme described in the previous section. The results are aggregated over the two choices of since these two settings were found to be similar. For more detailed results from the experiment, see Figure 9 in Appendix E, which also includes the -values corresponding to the endpoint test statistic.

For the hazard ratio test, Figure 5 shows that the -values are sub-uniform for the zero-kernel. In this case, the marginal Cox model is correct, and the non-uniformity of the -values can be explained by the -penalization. For the constant and Gaussian kernels the hazard ratio test fails completely, whereas for the sine kernel, the mediated effect of on through is more subtle, and the model misspecification only becomes apparent for . Overall, these results are consistent with the reasoning in the Section 2.2: a test based on the misspecified Cox model will wrongly reject the hypothesis of conditional local independence.

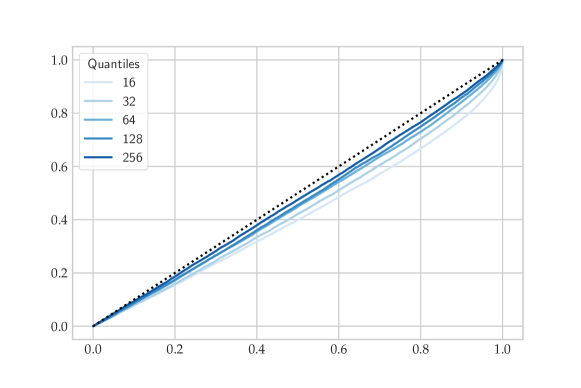

For the proposed X-LCT, Figure 5 shows that the associated -values are slightly anti-conservative for . This is to be expected, and can be explained by the finite sample errors leading to more extreme values of than the approximation by . As increases, these errors become smaller – and for the -values actually seem to be sub-uniform. The sub-uniformity may be explained by the time discretization, since the maximum of the process is taken over rather than . Figure 10 in Appendix E illustrates the asymptotic effect of the time discretization which supports this claim. Another support of this claim is that the endpoint test does not appear to give sub-uniform -values for large , see Figure 9. We finally note that the distributions of the -values for our proposed test is largely unaffected by the kernel used to generate the data.

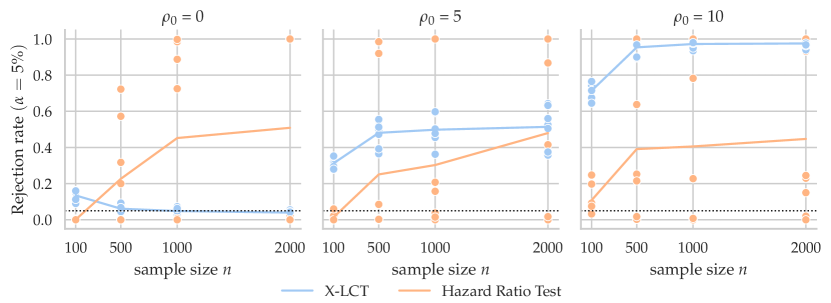

6.5. Power against local alternatives

To investigate the power of the X-LCT we construct local alternatives to in accordance with the right graph in Figure 2 by replacing by the process . That is, for , blood pressure is then directly affected by pension savings, and is no longer conditionally locally independent of given . In terms of the full intensity, these local alternatives are equivalent to

| (36) |

We simulated data for the dependency parameter . Note that corresponds to our previous sampling scheme with conditional local independence. For each of the choices of kernel, , and we ran the tests times and computed the -values. For simplicity, we report the rejection rate at an significance level and the results are shown in Figure 6.

In the leftmost panel, the data was generated under and the plot shows what we noted previously, namely that the X-LCT holds level for large , whereas the hazard ratio test does not.

For the local alternatives, and , we note that the power of the hazard ratio test is quite sensitive to the simulation settings. For some settings it has no power, while for others it has some power.

In contrast, the proposed X-LCT has power against all of the local alternatives. The power increases with initially but stabilizes from around . This is similar to the behavior observed under the null hypothesis and is not surprising. We expect that the sample size needs to be sufficiently large for the nonparametric estimators to work sufficiently well, and we expect the sufficient sample size to be mostly unaffected by the value of . For fixed , we also note that the power of is fairly robust with respect to the choice of and the choice of kernel. Overall, we find that the X-LCT is applicable in these settings with historical effects: it has consistent power against the alternatives while maintaining level for reasonably large.

We now compare the X-LCT, which is based on the uniform norm of the X-LCM, with its endpoint counterpart. More precisely, we consider the test statistic

which is asymptotically standard normal under . With the simulation settings in Section 6.5, the X-LCT turns out to be more or less indistinguishable from the corresponding endpoint test. This is because the alternatives considered have corresponding parameters , which are most extreme towards . Therefore, the supremum and the endpoint behave similarly in these cases.

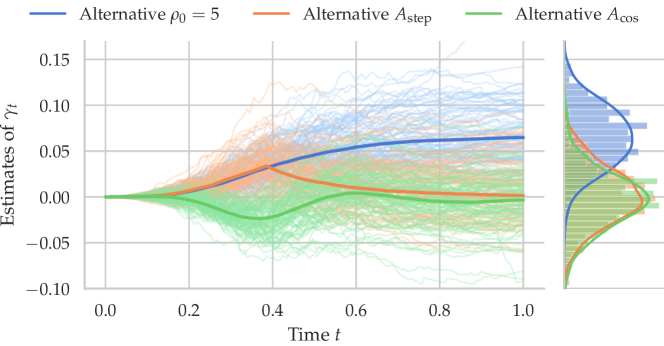

For this reason we consider local alternatives that result in a non-monotonic parameter . Using the same expression for the intensity (36), but with a time-varying , we consider the alternatives

The idea behind the alternative is that should be increasing on and decreasing on . Figure 7 shows sample paths of for data simulated under each of the alternatives , and . The figure illustrates that is, indeed, mostly maximal towards for the alternative , but not for the time-varying alternatives and .

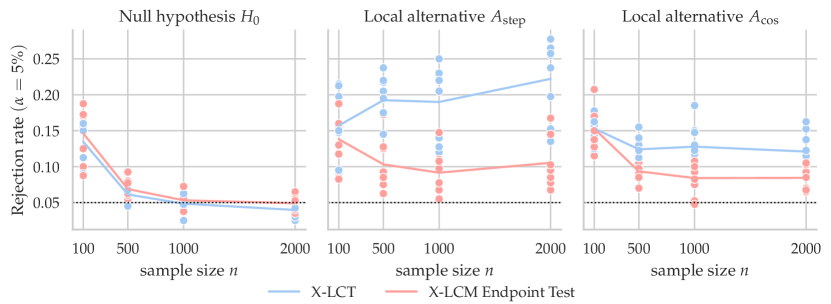

With the same sampling scheme for as in Section 6.2, we conducted an analogous experiment with 400 runs for each setting. Figure 8 shows the rejection rates for the two tests.

Under the hypothesis of conditional local independence, the left plot in Figure 8 shows that the endpoint test behaves similarly to as expected. Both tests have power against the local alternatives, but for the power does not seem to stabilize before . This is different from the previous settings, and can be explained by a slower convergence of the intensity estimator due to the more complex dependency on . For both of the local alternatives, we observe that is more powerful than the endpoint test, with the difference being largest for . In conclusion, these results show that the supremum test dominates the endpoint test in certain situations.

7. Discussion

The LCM was introduced as a functional parameter that quantifies deviations from the hypothesis of conditional local independence. We showed how the parameter may be expressed in several ways, but that it is the representation in terms of the residual process that allows us to estimate the LCM with a -rate under without parametric model assumptions. The residual process was introduced as an abstract model of for each given the history up to time , and we showed that such a residualization could be viewed as a form of orthogonalization. Similar ideas have been used recently for classical conditional independence testing, such as GCM (Shah & Peters, 2020), tests based on the partial copula (Petersen & Hansen, 2021), and GHCM (Lundborg, Shah & Peters, 2022). It is, however, not possible to use any of these to test , which cannot be expressed as a classical conditional independence. Our test based on the LCM is the first nonparametric test of conditional local independence with substantial theoretical support, and we propose to test in practice by using X-LCT based on the cross-fitted estimator of LCM.

Contrary to the tests of conditional independence mentioned above, we need sample splitting – even under – to achieve our asymptotic results. We do not believe that this can be avoided. The standard argument to avoid this uses classical conditional independence in a crucial way, which does not translate into our framework – basically because we condition on information that changes with time. Our simulation study also indicates that sample splitting or cross-fitting is needed in practice for the LCM estimator to be unbiased under .

While our cross-fitted estimator of the LCM, the X-LCM, share some of the general patterns of other double machine learning procedures – including the overall decomposition (14) – our analysis and results required a range of generalizations of known results and some novel ideas. The asymptotic distribution of the leading term, , is also a well known consequence of Rebolledo’s CLT, see, e.g., Section V.4 in (Andersen et al., 1993) for related results in the context of survival analysis. However, we generalized this result to uniform convergence in the Skorokhod space , and we introduced new techniques for handling the remainder terms. These novel techniques are made necessary by the decomposition (14) being a decomposition of stochastic processes indexed by time. We outline below the three most important technical contributions we made.

First, to obtain uniform control of level and power, all asymptotic results in Section 4 are formulated in terms of uniform stochastic convergence. Since this notion of convergence had not previously been considered on general metric spaces, and especially not on the Skorokhod space, we had to develop the necessary theory. This development could be of independent interest, and we have collected the general definitions and main results on uniform stochastic convergence in metric spaces in Appendix B. This framework also allowed us to show a uniform version of Rebolledo’s martingale CLT in Appendix C.

Second, to establish distributional convergence under , we need to control the remainder terms uniformly over . The third term, , is simple to bound, and by exploiting Doob’s submartingale inequality, the second term, , can also be bounded. The most difficult first term, , was controlled using stochastic equicontinuity via an exponential tail bound and the use of the chaining lemma. The necessary general uniform stochastic equicontinuity and chaining arguments are collected in Section B.3 of Appendix B.

Third, to achieve rate results in the alternative, the processes and must be controlled. The process does, like , not involve any estimation, and its distributional convergence follows from a general CLT argument for continuous stochastic processes. The term is more difficult to handle, as it may not have mean zero if is not the additive residual process. However, cancels out in for the additive residual process, which makes the difference -predictable, and can then be bounded similarly to . For a general residual process, it seems possible for to have a bias of order .

Our main result, Theorem 4.6, is stated under two assumptions. The second, Assumption 4.2, is a straightforward generalization to our setup of similar assumptions in the double machine learning literature on rates of convergence for the two estimators used. Both estimation errors are measured using a -norm, and it is plausible that we can relax one norm to a weaker form of convergence if we simultaneously strengthen the other norm. The first assumption, Assumption 4.1, requires uniform bounds on both and . This is a strong assumption but perhaps not particularly problematic from a practical viewpoint. Indeed, is a process we can choose, and we can thus make it bounded if necessary. And though many theoretically interesting counting process models have unbounded intensities, a large cap on the intensity will make no difference in practice. We believe, nevertheless, that it is possible to relax Assumption 4.1 to a weaker form of control on the magnitudes of and as functions of time, e.g., moment bounds uniform in . However, such a generalization will come at the expense of considerably more technical proofs, and we did not pursue this line of research.

A major practical question is whether we can estimate and with sufficient rates, e.g. . In Appendix D we give an overview of some known and some conjectured rate results for specific forms of and . Beyond parametric models we conclude that the existing rate results are scarce, and we regard it is as an independent research project to establish rates for general historical regression methods.

Another question is whether we can replace the counting process by a more general semimartingale. Commenges & Gégout-Petit (2009) define conditional local independence for a class of special semimartingales, and Mogensen et al. (2018) and Mogensen & Hansen (2022) show global Markov properties for local independence graphs of certain Itô processes, which are, in particular, special semimartingales. Thus conditional local independence is well defined beyond counting processes, and we believe that most definitions and results of this paper would generalize beyond being a counting process. Besides some additional technical challenges, the major practical obstacle with such a generalization is that we cannot realistically assume to have completely observed sample paths of Itô processes, say. The discrete time nature of the observations should then be included in the analysis, and this is beyond the scope of the present paper.

Irrespectively of the remaining open problems, the simulation study demonstrated some important properties of our proposed test, the X-LCT. First, it was fairly simple to implement for the specific example considered using some standard estimation techniques that were not tailored to the specific model class. Second, it had good level and power properties and clearly outperformed the test based on the misspecified marginal Cox model. Third, both Neyman orthogonalization as well as cross-fitting were pivotal for achieving the good properties of the test.

Funding

The work was supported by Novo Nordisk Foundation Grant NNF20OC0062897.

References

- (1)

- Aalen (1987) Aalen, O. O. (1987), ‘Dynamic modelling and causality’, Scandinavian Actuarial Journal pp. 177–190.

- Aalen et al. (2012) Aalen, O. O., Røysland, K., Gran, J. M. & Ledergerber, B. (2012), ‘Causality, mediation and time: a dynamic viewpoint’, Journal of the Royal Statistical Society. Series A (Statistics in Society) 175(4), 831–861.

- Achab et al. (2017) Achab, M., Bacry, E., Gaïffas, S., Mastromatteo, I. & Muzy, J.-F. (2017), Uncovering causality from multivariate Hawkes integrated cumulants, in ‘Proceedings of the 34th International Conference on Machine Learning’, Vol. 70, PMLR, pp. 1–10.

- Adler et al. (2007) Adler, R. J., Taylor, J. E. et al. (2007), Random fields and geometry, Vol. 80, Springer.

- Andersen et al. (1993) Andersen, P. K., Borgan, Ø., Gill, R. D. & Keiding, N. (1993), Statistical models based on counting processes, Springer Series in Statistics, Springer-Verlag, New York.

- Bacry et al. (2018) Bacry, E., Bompaire, M., Deegan, P., Gaïffas, S. & Poulsen, S. V. (2018), ‘tick: a Python library for statistical learning, with an emphasis on Hawkes processes and time-dependent models’, Journal of Machine Learning Research 18(214), 1–5.

- Bender et al. (2020) Bender, A., Rügamer, D., Scheipl, F. & Bischl, B. (2020), A general machine learning framework for survival analysis, in ‘Joint European Conference on Machine Learning and Knowledge Discovery in Databases’, Springer, pp. 158–173.

- Bengs & Holzmann (2019) Bengs, V. & Holzmann, H. (2019), ‘Uniform approximation in classical weak convergence theory’, arXiv preprint arXiv:1903.09864 .

- Billingsley (2013) Billingsley, P. (2013), Convergence of probability measures, John Wiley & Sons.

- Boucheron et al. (2013) Boucheron, S., Lugosi, G. & Massart, P. (2013), Concentration inequalities: A nonasymptotic theory of independence, Oxford University Press.

- Brémaud (1981) Brémaud, P. (1981), Point processes and queues, Springer-Verlag, New York.

- Cai et al. (2022) Cai, R., Wu, S., Qiao, J., Hao, Z., Zhang, K. & Zhang, X. (2022), ‘THPs: Topological Hawkes processes for learning causal structure on event sequences’, IEEE Transactions on Neural Networks and Learning Systems pp. 1–15.

- Cai & Yuan (2012) Cai, T. T. & Yuan, M. (2012), ‘Minimax and adaptive prediction for functional linear regression’, Journal of the American Statistical Association 107(499), 1201–1216.

- Chernozhukov et al. (2018) Chernozhukov, V., Chetverikov, D., Demirer, M., Duflo, E., Hansen, C., Newey, W. & Robins, J. (2018), ‘Double/debiased machine learning for treatment and structural parameters’, The Econometrics Journal 21(1), C1–C68.

- Commenges & Gégout-Petit (2009) Commenges, D. & Gégout-Petit, A. (2009), ‘A general dynamical statistical model with causal interpretation’, Journal of the Royal Statistical Society. Series B (Statistical Methodology) 71(3), 719–736.

- Davidson-Pilon (2021) Davidson-Pilon, C. (2021), ‘Lifelines, survival analysis in Python’.

- Didelez (2006) Didelez, V. (2006), ‘Graphical models for composable finite Markov processes’, Scandinavian Journal of Statistics 34(1), 169–185.

- Didelez (2008) Didelez, V. (2008), ‘Graphical models for marked point processes based on local independence’, Journal of the Royal Statistical Society. Series B (Statistical Methodology) 70(1), 245–264.

- Didelez (2015) Didelez, V. (2015), Causal reasoning for events in continuous time: A decision-theoretic approach, in ‘Proceedings of the UAI 2015 Workshop on Advances in Causal Inference’.

- Fleming & Harrington (2011) Fleming, T. R. & Harrington, D. P. (2011), Counting processes and survival analysis, Vol. 169, John Wiley & Sons.

- Granger (1969) Granger, C. W. J. (1969), ‘Investigating causal relations by econometric models and cross-spectral methods’, Econometrica 37(3), 424–438.

- Harezlak et al. (2007) Harezlak, J., Coull, B. A., Laird, N. M., Magari, S. R. & Christiani, D. C. (2007), ‘Penalized solutions to functional regression problems’, Computational statistics & data analysis 51(10), 4911–4925.

- Jiang & Wang (2011) Jiang, C.-R. & Wang, J.-L. (2011), ‘Functional single index models for longitudinal data’, The Annals of Statistics 39(1), 362–388.

- Kallenberg (2021) Kallenberg, O. (2021), Foundations of modern probability, Vol. 3, Springer.

- Kasy (2019) Kasy, M. (2019), ‘Uniformity and the delta method’, Journal of Econometric Methods 8(1).

- Lee et al. (2021) Lee, D. K., Chen, N. & Ishwaran, H. (2021), ‘Boosted nonparametric hazards with time-dependent covariates’, The Annals of statistics 49(4), 2101.

- Lok (2008) Lok, J. J. (2008), ‘Statistical modeling of causal effects in continuous time’, The Annals of Statistics 36(3), 1464–1507.

- Lundborg, Kim, Shah & Samworth (2022) Lundborg, A. R., Kim, I., Shah, R. D. & Samworth, R. J. (2022), ‘The projected covariance measure for assumption-lean variable significance testing’, arXiv preprint arXiv:2211.02039 .

-

Lundborg, Shah & Peters (2022)

Lundborg, A. R., Shah, R. D. & Peters, J. (2022), ‘Conditional independence testing in hilbert spaces

with applications to functional data analysis’, Journal of the Royal

Statistical Society: Series B (Statistical Methodology) 84(5), 1821–1850.

https://rss.onlinelibrary.wiley.com/doi/abs/10.1111/rssb.12544 - Maity (2017) Maity, A. (2017), ‘Nonparametric functional concurrent regression models’, Wiley Interdisciplinary Reviews: Computational Statistics 9(2), e1394.

- Malfait & Ramsay (2003) Malfait, N. & Ramsay, J. O. (2003), ‘The historical functional linear model’, The Canadian Journal of Statistics 31(2), 115–128.

- Manrique (2016) Manrique, T. (2016), Functional linear regression models: application to high-throughput plant phenotyping functional data, PhD thesis, Université de Montpellier.

- Manrique et al. (2018) Manrique, T., Crambes, C. & Hilgert, N. (2018), ‘Ridge regression for the functional concurrent model’, Electronic Journal of Statistics 12(1), 985–1018.

- Martinussen & Vansteelandt (2013) Martinussen, T. & Vansteelandt, S. (2013), ‘On collapsibility and confounding bias in Cox and Aalen regression models’, Lifetime Data Analysis 19(3), 279–296.

- Mogensen & Hansen (2020) Mogensen, S. W. & Hansen, N. R. (2020), ‘Markov equivalence of marginalized local independence graphs’, The Annals of Statistics 48(1), 539–559.

- Mogensen & Hansen (2022) Mogensen, S. W. & Hansen, N. R. (2022), ‘Graphical modeling of stochastic processes driven by correlated noise’, Bernoulli 28(4), 3023–3050.

- Mogensen et al. (2018) Mogensen, S. W., Malinsky, D. & Hansen, N. R. (2018), Causal learning for partially observed stochastic dynamical systems, in ‘Proceedings of the 34th conference on Uncertainty in Artificial Intelligence’, pp. 350–360.

- Newey (1991) Newey, W. K. (1991), ‘Uniform convergence in probability and stochastic equicontinuity’, Econometrica 59(4), 1161–1167.

- Neykov et al. (2021) Neykov, M., Balakrishnan, S. & Wasserman, L. (2021), ‘Minimax optimal conditional independence testing’, The Annals of Statistics 49(4), 2151–2177.

- Pakbin et al. (2021) Pakbin, A., Wang, X., Mortazavi, B. J. & Lee, D. K. (2021), ‘BoXHED2.0: Scalable boosting of dynamic survival analysis’, arXiv preprint arXiv:2103.12591 .

- Petersen & Hansen (2021) Petersen, L. & Hansen, N. R. (2021), ‘Testing conditional independence via quantile regression based partial copulas’, Journal of Machine Learning Research 22(70), 1–47.

- Pollard (1984) Pollard, D. (1984), Convergence of stochastic processes, Springer Series in Statistics, Springer-Verlag, New York.

- Rebolledo (1980) Rebolledo, R. (1980), ‘Central limit theorems for local martingales’, Zeitschrift für Wahrscheinlichkeitstheorie und verwandte Gebiete 51(3), 269–286.

- Revuz & Yor (2013) Revuz, D. & Yor, M. (2013), Continuous martingales and Brownian motion, Vol. 293, Springer Science & Business Media.

- Rogers & Williams (2000) Rogers, L. C. G. & Williams, D. (2000), Diffusions, Markov processes, and martingales, Vol. 2, Cambridge University Press, Cambridge.

- Rytgaard et al. (2022) Rytgaard, H. C., Gerds, T. A. & van der Laan, M. J. (2022), ‘Continuous-time targeted minimum loss-based estimation of intervention-specific mean outcomes’, The Annals of Statistics 50(5), 2469–2491.

- Rytgaard et al. (2021) Rytgaard, H. C. W., Eriksson, F. & van der Laan, M. (2021), ‘Estimation of time-specific intervention effects on continuously distributed time-to-event outcomes by targeted maximum likelihood estimation’, arXiv:2106.11009 .

- saz (2019) saz (2019), ‘Calculating the expecation of the supremum of absolute value of a Brownian motion’, Mathematics Stack Exchange. URL: https://math.stackexchange.com/q/3252132 (version: 2019-06-06).

- Scheidegger et al. (2022) Scheidegger, C., Hörrmann, J. & Bühlmann, P. (2022), ‘The weighted generalised covariance measure’, Journal of Machine Learning Research 23(273), 1–68.

- Schilling (2017) Schilling, R. L. (2017), Measures, integrals and martingales, Cambridge University Press.

- Schilling & Partzsch (2012) Schilling, R. L. & Partzsch, L. (2012), Brownian Motion: An Introduction to Stochastic Processes, De Gruyter.

- Schweder (1970) Schweder, T. (1970), ‘Composable Markov processes’, Journal of Applied Probability 7(2), 400–410.

- Şentürk & Müller (2010) Şentürk, D. & Müller, H.-G. (2010), ‘Functional varying coefficient models for longitudinal data’, Journal of the American Statistical Association 105(491), 1256–1264.

- Shah & Peters (2020) Shah, R. D. & Peters, J. (2020), ‘The hardness of conditional independence testing and the generalised covariance measure’, The Annals of Statistics 48(3), 1514–1538.

- van der Vaart & Wellner (1996) van der Vaart, A. W. & Wellner, J. A. (1996), Weak convergence and empirical processes, Springer Series in Statistics, Springer-Verlag, New York.

- Wang et al. (2020) Wang, X., Pakbin, A., Mortazavi, B., Zhao, H. & Lee, D. (2020), BoXHED: Boosted eXact Hazard Estimator with Dynamic covariates, in ‘International Conference on Machine Learning’, PMLR, pp. 9973–9982.

- Wells (1994) Wells, M. T. (1994), ‘Nonparametric kernel estimation in counting processes with explanatory variables’, Biometrika 81(4), 795–801.

- Xiao et al. (2019) Xiao, S., Yan, J., Farajtabar, M., Song, L., Yang, X. & Zha, H. (2019), ‘Learning time series associated event sequences with recurrent point process networks’, IEEE Transactions on Neural Networks and Learning Systems 30(10), 3124–3136.

- Xu et al. (2016) Xu, H., Farajtabar, M. & Zha, H. (2016), Learning Granger causality for Hawkes processes, in ‘Proceedings of The 33rd International Conference on Machine Learning’, Vol. 48, pp. 1717–1726.

- Yao et al. (2005) Yao, F., Müller, H.-G. & Wang, J.-L. (2005), ‘Functional linear regression analysis for longitudinal data’, The Annals of Statistics 33(6), 2873 – 2903.

- Yuan & Cai (2010) Yuan, M. & Cai, T. T. (2010), ‘A reproducing kernel Hilbert space approach to functional linear regression’, The Annals of Statistics 38(6), 3412–3444.

- Zhou et al. (2013) Zhou, K., Zha, H. & Song, L. (2013), Learning social infectivity in sparse low-rank networks using multi-dimensional Hawkes processes, in ‘Proceedings of the 16th International Conference on Artificial Intelligence and Statistics’.

Supplementary material

In Appendix A, we give the proofs of the results of the paper. In Appendix B, we formulate a general uniform asymptotic theory for metric spaces, whereafter we specialize the theory to the Skorokhod space and chaining of stochastic processes. In Appendix C, we state Rebolledo’s martingale central limit theorem, and then we generalize the result to a uniform version that is used in the proofs. In Appendix D, we discuss estimation of the intensity and the residual process in practice. In particular, we compare known rate results with the rates required in Assumption 4.2. Finally, Appendix E contains additional figures from the simulation study.

Appendix A Proofs

This appendix contains proofs of the results stated in the paper.

A.1. Proof of Proposition 2.4

The process is càglàd and -predictable by assumption, and the process is a stochastic integral of w.r.t. a local -martingale under the hypothesis . It is thus also a local -martingale under . By definition, , and if is a martingale,

A.2. Proof of proposition 2.5

Suppose that is non-negative, càglàd and -predictable, then since is a local -martingale it follows by monotone convergence along a localizing sequence that

| (37) |

for all . We can apply the identity above with the positive and negative part of , respectively, and the integrability assumption ensures that (37) also holds with . It follows that

The latter expectation is indeed a covariance since .

A.3. Proof of Lemma 4.1

Before proving Lemma 4.1, we first state general martingale criteria in the context of counting processes.

Lemma A.1.

Let be a locally bounded -predictable process, let be a counting process with a -intensity , and let .