Stochastic Approximation Based Confidence Regions for Stochastic Variational Inequalities 111The work is supported by National Natural Science Foundation of China #11971090.

Wuwenqing Yan and Yongchao Liu

School of Mathematical Sciences, Dalian University of Technology, Dalian, 116024, China (ywwq@mail.dlut.edu.cn (Yan), lyc@dlut.edu.cn (Liu)).

Abstract. The sample average approximation (SAA) and the stochastic approximation (SA) are two popular schemes for solving the stochastic variational inequalities problem (SVIP). In the past decades, theories on the consistency of the SAA solutions and SA solutions have been well studied. More recently, the asymptotic confidence regions of the true solution to SVIP have been constructed when the SAA scheme is implemented. It is of fundamental interest to develop confidence regions of the true solution to the SVIP when the SA scheme is employed. In this paper, we discuss the framework of constructing asymptotic confidence regions for the true solution of SVIP with a focus on stochastic dual average method. We first establish the asymptotic normality of the SA solutions both in ergodic sense and non-ergodic sense. Then the online methods of estimating the covariance matrices in the normal distributions are studied. Finally, practical procedures of building the asymptotic confidence regions of solutions to SVIP with numerical simulations are presented.

Key words. Stochastic variational inequalities, confidence regions, stochastic approximation, statistical inference

1 Introduction

For the given convex set and a mapping , the variational inequalities problem (VIP) is to find a vector such that

VIP has many applications in engineering, economics, game theory and has been well studied in theories, algorithms, see the monograph by Facchinei and Pang [1]. In order to describe decision making problems which involve future uncertainty, the stochastic version of variational inequalities problem (SVIP) has been proposed. Different approaches to incorporate the uncertainty into VIP induce different SVIP models, such as, expected residual minimization-SVIP (ERM-SVIP) model [2], expected value-SVIP (EV-SVIP) [3], -SVIP model [4], two-stage SVIP model [5] and multi-stage SVIP model [6].

In this paper, we focus on the EV-SVIP model (for simplicity, we refer the EV-SVIP as SVIP): find such that

| (1.1) |

where , is a convex set, is a random vector defined on probability space with support set , is measurable function from to and denotes the expected value with respect to the distribution . Indeed, (1.1) is deterministic VIP if has a closed form representation. However, in most problems of interest obtaining a closed form of or computing its value numerically is usually difficult either due to the unavailability of distribution of or multiple integration involved. In general, it is more realistic to obtain a sample of the random vector either from past data or from computer simulation. Depending on how sampling is incorporated with the algorithm, solution methods for SVIP can be classified into two basic categories: sample average approximation (SAA) based and stochastic approximation (SA) based.

SAA method is also known under different names such as Monte Carlo method, sample path optimization, and has been well studied in stochastic programming. Suppose there is independent and identically distributed (iid) sample , SAA method replaces the in (1.1) with

Then algorithms for VIP are employed to solve (1.1) and return the SAA solutions. Since SAA method does not depend on the algorithms, it is an ‘exterior’ approach. SAA method is known to be consistent [3], that is, the SAA solutions converge to the true counterpart with probability one. A natural question to ask is how well the SAA solutions approximate the true solution. Very recently, Lu et al. [7, 8, 9, 10, 11] study the confidence regions of true solutions to SVIP based on SAA solutions, where the normal map approach is proposed. The idea of the normal map approach is to build the confidence region of solution to ,222The normal map induced by function and convex set reads as: therefore, the confidence region of solution to SVIP (1.1) can be obtained through the relations between the solutions to SVIP (1.1) and . See [7, 12] for the application of normal map approach on least absolute shrinkage and selection operator (lasso) and sparse penalized regression. Motivated by the normal map approach, Liu et al. [13, 14] propose the so-called error bound approach to build the confidence regions of SVIP by the SAA solutions. The road-map of error bound approach is that characterizing the distance between the SAA solutions and the true solution by error bound conditions first, then statistical tools such as central limit theorem and Owen’s empirical likelihood theorem are used to build the confidence regions.

On the other hand, the SA scheme always depends on the structure of the algorithm, then it is an ‘interior’ approach. The development of stochastic approximation scheme goes back to the work of Robbins and Monro [15], where the stochastic root-finding problems are studied. Research on asymptotic normality results for the SA based algorithm can be traced to the works in the 1950s [16, 17]. In particular, Polyak and Juditsky [18] show that the averaged SA iterates is asymptotically normal with optimal covariance matrix for strongly convex stochastic optimization problem. In [19], Hsieh and Glynn establish the asymptotically normality of Robbins-Monro algorithm [15] and construct confidence regions of true solutions through simulating multiple independent replications of the stochastic approximation procedure. More recently, Lei and Shanbhag [20] provide a unified frame work to show the asymptotically normality of variance-reduced accelerated stochastic first-order methods, where the confidence regions of the true solutions are constructed through simulation method [19]. The first SA based method for SVIP is proposed by Jiang and Xu [21]. Since it is easy to implement and needs less memory, researches on SA based methods for SVIP have been well developed, for examples, SA based extragradient method [22], SA based incremental constraint projection methods [23], SA based backward-forward methods [24] and SA based mirror-proximal algorithm [25]. As far as we known, all the results on the SA based methods for SVIP focus on the consistency, that is, under some moderate conditions, the SA solutions converge to the true counterpart. It is of fundamental interest to use SA based solutions to develop confidence regions of prescribed level of significance for the true solution.

In this paper, we discuss the framework of constructing asymptotic confidence regions of the true solution to SVIP (1.1) when stochastic approximation based method is implemented. The two seminal papers on stochastic approximation [26, 27] motivate and guide much of our work. Similar to the normal map approach [8, 28, 11], we need to establish the asymptotic normality of SA solutions first. Indeed, Duchi and Ruan [26] have established the asymptotic normality of Polyak-Ruppert averaged iterates of a variant of stochastic dual average algorithm (SDA) [29] for solving constrained optimization problems. This motivates us to employ SDA to solve the SVIP (1.1) and study the asymptotic normality of averaged SA solutions (Theorem 2.1). On the other hand, compared with the last iterate of SDA, the average of iterates may deviate from the solution if the initial point of SDA is far away from the solution and the iteration is not large enough. Then we also establish the asymptotic normality of the last iterate of SDA for SVIP (1.1) (Theorem 2.3).

With the asymptotic normality of SDA solutions, the following task is to estimate the corresponding covariance matrices. The standard covariance matrix estimator employs the sample average approximation, where the history data of SDA is needed. This requirement loses the advantage of stochastic approximation scheme in terms of data storage. More recently, the seminal work [27] provides two online methods plug-in and batch-means to estimate the covariance matrix when vanilla SGD method is implemented on unconstrained stochastic optimization problems. They show the consistency of the both methods with the convergence rate for plug-in method and for batch-means method in expectation sense, where is the number of iterates. We extend the plug-in and batch-means methods to stochastic dual averaging algorithm for SVIP (1.1). Due to the existence of constraints, we only obtain the almost sure convergence of the plug-in estimator and convergence in distribution of batch-means estimator. Specifically, Theorems 3.1 and 3.2 present the almost sure convergence of plug-in estimators for the covariance matrices in ergodic and non-ergodic asymptotic normality respectively. Theorem 3.3 shows that batch-means estimator of covariance matrix in ergodic asymptotic normality is convergent in distribution. These results enable us to build confidence regions of the true solution through the iterates of SDA.

The rest of paper is organized as follows. Section 2 establishes the asymptotic distribution results of SDA in ergodic and non-ergodic senses. Section 3 discusses the plug-in method and batch-means method for estimating the corresponding covariance matrices. Finally, practical procedures of building the asymptotic confidence regions of solutions to SVIP with numerical simulations are presented in Section 4.

Throughout the paper, is the largest integer less than or equal to . denotes the identity matrix, denotes Moore-Penrose inverse of matrix and denotes the trace of a square matrix . is the vector of all 0s. For any sequences and of positive numbers, we write if , if holds for all large enough and some constant if holds, and if and . We denote if holds for all large enough and some positive random variable almost surely. For a sequence of random vectors and a random vector , denotes the convergence in distribution and denotes the covariance matrix of random vector . ‘a.s.’ is short for almost surely.

2 Asymptotic normality

Asymptotic normality plays a significant role in stochastic approximation and its history can be traced to 1950s [16, 17]. In this section, we study the asymptotic normality of iterates when SDA is implemented on SVIP (1.1). The dual averaging algorithm is proposed by Nesterov [29] and further studied by many authors [26, 30, 31, 32]. We focus on the stochastic variant of dual averaging algorithm proposed in [26], which for SVIP (1.1) reads as following.

Input , and step-size .

| (2.2) |

In what follows, we focus on the case that the set in SVIP (1.1) is polyhedral, that is,

where and . Let be a solution to SVIP (1.1). Without loss of generality, we assume and , that is, is the active constraints at the solution .

We next record the assumptions that will be used to analyze the asymptotic normality of SDA, which are variations of the standard conditions on optimization problem in [26].

Assumption 2.1.

Let be the unique solution to SVIP (1.1).

-

(i)

There exists measurable variable such that for some and

(2.3) There exist constants and such that for

(2.4) - (ii)

-

(iii)

There exists such that for any ,

where is the critical tangent set to at , that is,

(2.5) -

(iv)

The covariance matrix is finite.

Condition (2.3) in Assumption 2.1 is the calmness of at point relative to , which implies the calmness of at point , that is,

where . Condition (2.4) in Assumption 2.1 ensures the boundedness of linear approximation error of . Condition (ii) of Assumption 2.1 is a constraint qualification which ensures the stability of the system of optimality conditions. Condition (iii) of Assumption 2.1 means the positive definiteness of relative to subspace .

Theorem 2.1.

Proof.

The asymptotic normality of SDA for optimization problem has been studied in [26, Theorem 4]. We just need to verify the conditions of [26, Theorem 4]([26, Assumption A-D]). Indeed, Assumption 2.1 (i)-(iii) are variants of the conditions in [26, Assumption A-C]. Combining Assumption 2.1 (i) and (iv), we verify the condition of [26, Assumption D]. The proof is complete. ∎

Theorem 2.1 shows the asymptotic normality of Polyak-Ruppert averaged SDA for SVIP (1.1), which paves the way to construct the confidence regions of the true solution to SVIP (1.1) by the average of the iterates of SDA. However, if the initial point of SDA is far away from the solution and the iteration is not large enough, the average of the iterates may deviate from the true solution. This motivates us to study the asymptotic normality of last iterate of SDA for SVIP (1.1). For ease of presentation, we assume the boundedness of set .

Assumption 2.2.

The set is bounded.

If is strictly monotone on and Assumption 2.1 holds, Assumption 2.2 is not necessary. Specifically, the solution of SVIP (1.1) must be the unique solution to the new SVIP where is replaced by a bounded convex set such that [1, Theorem 2.3.3].

The following theorem analyzes the convergence rate of last iterate to solution , which plays a key role in asymptotic normality of last iterate of SDA for SVIP (1.1).

Theorem 2.2.

Proof.

We employ Lemma 5.1 in Appendix to study (2.7). We reformulate the recursion (2.2) of Algorithm 1 into the form of iteration (5.50) in Lemma 5.1 first.

Considering the KKT (Karush-Kuhn-Tucker) conditions of problem (2.2) at -th iteration and let and be the corresponding lagrange multipliers. It is easy to show that

Then

| (2.8) |

Denote

| (2.9) |

We may reformulate the recursion (2.8) as

| (2.10) |

Let , (2.10) can be rewritten as

| (2.11) |

Dividing on both sides of equation (2.11),

| (2.12) | ||||

where

| (2.13) |

By the definitions of in (2.9) and the fact

which induce

Then (2.12) can be rewritten as

| (2.14) |

Let be the orthogonal matrix with the set of eigenvectors associated with projection matrix , and being the associated diagonal matrix of eigenvalues, be a -matrix composed of first row vectors of and be the -order leading principle submatrix of . Denote

| (2.15) |

Then by [32, Lemma 4], (2.14) can be rewritten as

| (2.16) |

Obviously, it is sufficient to focus on the nonzero part of (2.16),

| (2.17) |

Setting

In what follows, we verify the conditions of Lemma 5.1. Firstly, we show that converges to a stable matrix 333All the eigenvalues of the matrix have strictly negative real part.. Recall the definition (2.13), the first two terms in

as Moreover, for large enough , the third term of satisfies

where the inequality follows from the definition of and (2.4). Then almost surely as almost surely [26, Theorem 2]. Combining the fact that is the -order leading principle submatrix of , converges to the -order leading principle submatrix of , which is a positive definite matrix by [32, Lemma 4]. Then, the limit of is stable.

Next, we show almost surely. Recall the definition of ,

By [26, Theorem 3], when is large enough as and Then almost surely.

We verify

Denote

Define the filtration

| (2.18) |

where is the -algebra generated by . Obviously, is a martingale difference sequence as is. Then,

| (2.19) | ||||

where the second inequality follows from

Define and . Obviously,

Moreover, Assumption 2.1 (i) implies

and Assumption 2.2 implies

| (2.20) |

Then, (2.19) is finite. Since

the convergence theorem of martingale difference sequences [34, Appendix B.6, Theorem B 6.1] ensures that

which implies

Subsequently, Lemma 5.1 implies almost surely. By the definition of in (2.15), almost surely. The proof is complete. ∎

We are ready to study the asymptotic normality of the last iterate of SDA for SVIP (1.1).

Theorem 2.3.

Suppose that (i) Assumptions 2.1 and 2.2 hold, (ii) step-size and , (iii) is the orthogonal matrix with the set of eigenvectors associated with projection matrix , and is the associated diagonal matrix of eigenvalues. Then

| (2.21) |

where

| (2.22) |

is composed by first row vectors of is the r-order leading principle submatrix of and .

Proof.

We mimic the proof of [32, Theorem 3] to study (2.21). We employ Lemma 5.2 in Appendix to prove (2.21). We first reformulate into the form of formula (5.51) in Lemma 5.2.

Left multiplying on both side of (2.10), we have by [32, Lemma 4] that

| (2.23) |

where is the -order leading principle submatrix of ,

Obviously, it is sufficient to focus on the nonzero part of (2.23),

| (2.24) |

Setting

Next, we verify the conditions of Lemma 5.2. By the setting of step-size , which implies condition (i) of Lemma 5.2. By the definition of , is stable, condition (ii) of Lemma 5.2 holds. In what follows, we verify condition (iii) of Lemma 5.2. We first show that almost surely.

By [26, Theorem 3], almost surely for large enough and then almost surely for large enough. By the definition of ,

where the inequality follows from Assumption 2.1 (i) and the last equality follows from Theorem 2.2. Therefore,

as we may choose . By mimicking the proof of [32, (57)-(61)], the conditions (5.52-5.54) in Lemma 5.2 hold.

Theorem 2.3 presents the asymptotic normality of the last iterate of SDA for SVIP (1.1) with the rate . Note that step-size , the convergence rate of the asymptotic normality of the last iterate can not arrive at . Similarly, Theorem 2.3 ensure us to construct the confidence regions of the true solution to SVIP (1.1) by the last iterate of SDA.

3 Estimator for the covariance matrix

Inference is a core topic in statistics and the confidence region has been widely used to quantify the uncertainty in the estimation of model parameters. The asymptotic normality of SDA is the first step of building the confidence regions of the true solutions for SVIP (1.1). Next, we have to provide estimators of the asymptotic covariance matrices in the limit normal distributions. In the seminal work [27], Chen et al. propose two online methods plug-in and batch-means to estimate the covariance matrix when vanilla SGD is implemented to solve unconstrained stochastic optimization problems. We extend the plug-in and batch-means methods to SDA algorithm for SVIP (1.1).

3.1 Plug-in method

Recall the normal distribution in Theorem 2.1,

The idea of the plug-in method [27] is to separately estimate , and by some , and . However, as the Moore-Penrose inverse of matrix is not continuous, it is difficult to show the convergence of to . This motivates us to reformulate the above normal distribution through linear transformation first.

Let be the orthogonal matrix with the set of eigenvectors associated with projection matrix , and being the associated diagonal matrix of eigenvalues, be a -matrix composed of first row vectors of . Left multiplying on (2.6), we have

By some calculations and the fact [26],

Note also that could identify the subspace [26, Theorem 3], (2.6) can be rewritten as

with , where

Then the plug-in method is to estimate , and separately. Denote as the matrix with respect to active constraint on ,

and

Let be the orthogonal matrix with the set of eigenvectors associated with projection matrix , and being the associated diagonal matrix of eigenvalues, be a -matrix composed of first row vectors of . Then ,

are the estimators of respectively.

The consistency of the plug-in estimator can be established under the following conditions.

Assumption 3.1.

-

(i)

There exists measurable variable such that and

-

(ii)

There exists a constant such that almost surely.

Assumption 3.1 (i) is the calmness of at point relative to . Assumption 3.1 (ii) holds if is continuous in and is compact.

Proof.

Following [26, Theorem 3], SDA could identify the subspace , which implies

for sufficiently large . As and are the orthogonal matrices to eigendecomposition of and with diagonal matrix and respectively, then

| (3.25) |

for sufficiently large . Subsequently,

Note that , and are bounded and (3.25) holds, we only need to study the consistency of .

Obviously,

Note that and are finite, it is sufficient to show and converge to zero almost surely. By the definition of ,

| (3.26) | |||||

As is iid sample, the strong law of large numbers ensures the first term on the right hand of (3.26) converges to zero almost surely. By Assumption 3.1 (i), the second term on the right hand of (3.26)

which converges to zero as almost surely [26, Theorem 2]. By the consistency of and (3.25), is nonsingular for sufficiently large , that is, . Then almost surely as almost surely.

Next, we study the convergence of . By the definition of and ,

Therefore, it is sufficient to show almost surely. For easy of notation, we denote

then,

| (3.27) | ||||

Again, the strong law of large numbers implies the first term on the right hand of (3.27) tends to zero almost surely. By Assumptions 2.1 (i) and 3.1 (ii), the last four terms on the right hand of (3.27)

Then, almost surely. The proof is complete. ∎

Next, we study the consistency of plug-in method for estimating the covariance matrix in the limit normal distribution of last iterate of SDA (Theorem 2.3). Let be defined as above and be the -order leading principle submatrix of . Then and

are the plug-in estimators of and in (2.22) respectively. 444We may use sample average approximation method to calculate the integration in .

Theorem 3.2.

Proof.

By (3.25) and the definitions of and ,

for sufficiently large . Note that and are bounded, it is sufficient to show that converges to zero.

We employ the sensitivity of solution for Lyapunov equation [35, Theorem 2.1] to study the convergence of . Denote

we have

which means is the solution of Lyapunov equation

where is defined in Theorem 2.3. By the similar analysis, is the solution of Lyapunov equation

where

and is the -order leading principle submatrix of . Denote

we have

By Assumption 2.1 (iii),

Moreover, is stable. Then, by the sensitivity of solution to Lyapunov equation [35, Page 327, last inequality],

Mimicking the proof of Theorem 3.1, it is easy to show and almost surely. Then tends to zero almost surely. The proof is complete. ∎

3.2 Batch-means method

Different with plug-in method, batch-means method only uses the iterates from SDA without requiring computation of any additional quantities. Let be a sequence of iterates of SDA, we define the strictly increasing integer-valued sequence with and for some constant . Then we split the iterates into batches with the starting index of -th batch. The batch-means estimator [36, (5)] of covariance matrix in (2.6) is given as follows:

| (3.28) |

where is determined by the sequence through when , , .

Although the batch-means estimator is the same as the batch-means estimator for SGD [36], the proof of convergence of (3.28) is not straightforward at all. If we follow [36, Theorem 3.3] to explore the consistency of batch-means estimator in expectation, the required convergence rate of the iterates to the true solution is not reachable. On the other hand, if we follow Theorems 3.1-3.2 to study almost sure convergence of the batch-means estimator, we are unable to show the convergence of the indispensable auxiliary sequence (see the following formula (3.29)) to the true covariance matrix. Therefore, we have to establish the consistency of batch-means estimator through the techniques both for convergence in expectation and almost sure convergence. Following the idea of [36, Theorem 3.3], we investigate the consistency of (3.28) by the following three steps.

- Step 1.

- Step 2.

-

Step 3.

[Theorem 3.3] Combine the convergence in expectation in the first step and convergence in distribution in the second step,

We begin by starting some technical lemmas where the convergence of the fourth moment of and the convergence rate of are studied.

Lemma 3.1.

Proof.

Lemma 3.2.

Proof.

Define the seminorm

where if By the definition (3.29), . Recall the filtration defined in (2.18). Then, there exists a constant such that

where the first inequality follows from (2.20), the second follows from Assumptions 2.1 (iii) and 2.2. Then the rest of proof is same as the proof of [27, Lemma B.3]. ∎

Lemma 3.3.

Proof.

The proof is similar to Theorem 2.2. ∎

We are ready for the Step 1.

Lemma 3.4.

Proof.

By the triangle inequality,

| (3.32) | ||||

Then, we may finish the proof by studying the convergence of the three terms on the right hand of (3.32).

We first focus on the first term on the right hand of (3.32). Denote the following matrices sequences,

| (3.33) |

the recursion of (3.29) can be rewritten as

where is defined in (2.9). Then we have

where

| (3.34) |

Subsequently, the first term on the right hand of (3.32)

| (3.35) | ||||

Next, we mimic the proof of [36, Lemma B.2.] to show , which implies the first term on the right hand of (3.35) tends to zero. Denote and , we have

| (3.36) |

By the definition of and the fact is iid, . can be expanded into two parts,

where

and

Then, the first term on the right hand of (3.36)

| (3.37) |

We first focus on the first term on the right hand of (3.37). Consider two cases, one is when and are in the same block,

and the other is when and are in different blocks,

Then, we have

Under Assumption 3.1 (ii), is bounded by constant . Following [36, (48)],

The fact implies . Then, the first term on the right hand of (3.37) tends to zero. Based on Assumption 3.1 (ii), is still bounded by constant for any , . By [36, (45-46)], the second term on the right hand of (3.37)

Next, we study the convergence of the second term on the right hand of (3.36). Denote , we have

| (3.38) |

Apply Cauchy’s inequality

Note that is a martingale difference sequence,

| (3.39) | ||||

Following Assumption 2.1 (i),

then (3.39) tends to zero by Lemma 3.1. Combining (3.37) and (3.38), the first term on the right hand of (3.35) tends to zero.

On the other hand, by mimicking the analysis on [36, (63)-(67)] with Lemma 3.2, the second term on the right hand of (3.35)

Using Cauchy’s inequality,

Combining the fact is bounded, Slutsky’s Theorem implies the last term on the right hand of (3.35) tends to zero. Summarizing above, the first term on the right hand of (3.32) converges to zero.

Next, we focus on second term on the right hand of (3.32). Note that , then

| (3.40) | ||||

[36, (76)-(77)] and Lemma 3.1 imply (3.40) tends to zero. Then, we only need the last term on the right hand of (3.32) tends to zero. By Cauchy’s inequality,

| (3.41) | ||||

The left term of (3.41) is bound by (3.35), Slutsky’s Theorem implies the last term on the right hand of (3.32) tends to zero. The proof is complete. ∎

Next, we move to Step 2.

Lemma 3.5.

Proof.

By the definition of and ,

| (3.42) | ||||

where the inequality follows from Young’s inequality.

Using Cauchy’s inequality, we have

| (3.43) | ||||

Claim that the left term of (3.43) is bounded by Lemma 3.4, we only need to show the second term on the right hand of (3.42) tends to zero. By triangle inequality,

| (3.44) | ||||

Next, we focus on the first term on the right hand of (LABEL:eq:rho). By the definition of , and in (3.31), (3.33) and (3.34) respectively,

Then,

| (3.45) | ||||

where the first inequality follows from triangle inequality and the second inequality follows from Cauchy-Schwartz inequality. According to [36, Lemma A.2.], On the other hand, Lemma 3.3 implies

Following from [36, Lemma A.2.], and following from [26, Theorem 3], almost surely for sufficiently large . Then,

Subsequently,

Note that , , and , the first term on the right hand of (LABEL:eq:rho)

| (3.46) |

On the other hand, by the definition of ,

From [36, (77)], , where , the second term on the right hand of (LABEL:eq:rho)

| (3.47) |

Combining (3.46) and (3.47), (LABEL:eq:rho) converges to zero in distribution.

The proof is complete. ∎

4 Numerical test

In this section, we report some preliminary numerical results on the confidence regions of the solution for SVIP (1.1). Following the asymptotic distribution given in Theorem 2.1,

defines an approximate confidence region for the solution to SVIP, where , , is defined to be the number that satisfies for a random variable with degrees of freedom. Similarly, the approximate confidence region for the asymptotic distribution given in Theorem 2.3 is

where is defined in (2.22).

Compared with confidence regions, the individual confidence intervals of the solution induce a measure of the uncertainty in each individual component of an estimated solution. Then it is able to assess the uncertainty in an individual component, which thereby allows us to focus on parameters of specific component of our interest. Under Theorem 2.1, the approximate confidence interval for -th component of solution is

where and are the -th and -th components of and respectively, satisfies for the standard normal random variable . Similarly, the approximate individual confidence interval for -th component of solution under Theorem 2.3 is

We report the empirical performance of the proposed methods on two examples from [8] and [7], where the first example is a stochastic linear complementarity problem with simulated data and the second example is a linear regression problem with real data [37, Prostate cancer].

4.1 Stochastic linear complementarity problem

We first consider a stochastic linear complementarity problem [8]:

| (4.48) |

where

and follows uniform distribution over the box

Obviously, the unique true solution and the true covariance matrices in Theorem 2.2 and Theorem 2.3 are

respectively.

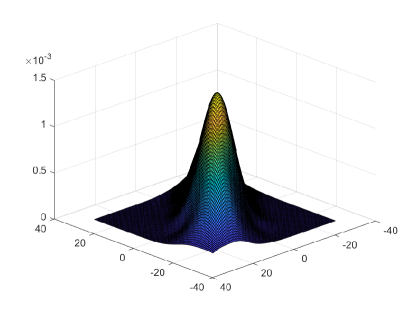

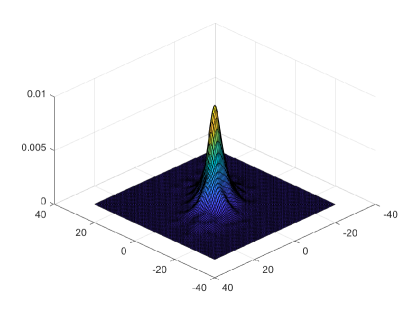

In implementing of Algorithm 1, the step-size and the initial point . We first test the asymptotic normality of iterates of SDA in Theorems 2.1 and 2.3. We do 1000 Monte-Carlo simulations of running SDA 1000 iterates and record the estimated density in Figure 1. Figure 1 (a) and Figure 1 (b) depict the estimated densities of the average of iterates SDA and the last iterate of SDA respectively. Figure 1 seems to confirm Theorems 2.1 and 2.3 since we can see that the estimated density is close to the density of a normal distribution and is also confirmed by a Kolmogorov-Smirnov test.

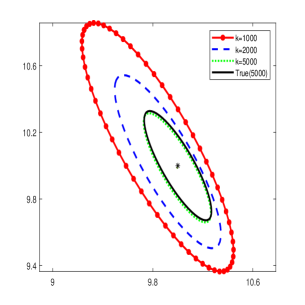

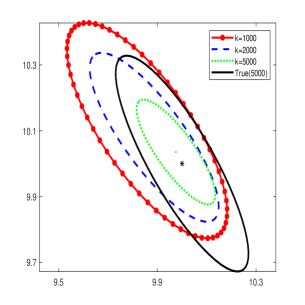

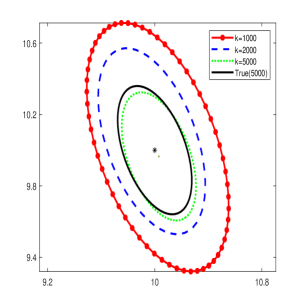

Next, we record the confidence regions with number of iterates , and respectively. For the stability, we do 50 Monte-Carlo simulations and report the results with the average covariance matrix and the average of iterates. In batch-means method, the sequence is chosen in the form with . Figure 2 depicts the asymptotic confidence regions of the solution to complementarity problem (4.48), where the red circle ellipse, blue dashed ellipse, green dot ellipse and black solid ellipse denote the confidence regions for number of iterates , , and the true one respectively. As we can observe from Figure 2 (a), the asymptotic confidence region based on plug-in method at almost coincides with true confidence region, which indicates the consistency of plug-in method in Theorem 3.1. Compared with Figure 2 (a), the asymptotic confidence region based on batch-means methods is reported in Figure 2 (b), where the asymptotic confidence region at is small than the true one. The underlying reason may be that the plug-in method employs more information such as gradient of functions and batch-means method uses iterates of SDA only. On the other hand, the batch-means estimator tends to underestimate the variance due to the correlation between batches. Figure 2 (c) verifies the consistency of plug-in method in building the asymptotic confidence regions based on the last iterate of SDA.

We record the diagonal elements of covariance matrices for number of iterates , , and the true one respectively in Table 1-2, which characterize the individual confidence intervals of the solution to complementarity problem (4.48). Similar to Figure 2, we can conclude that the plug-in estimators are consistent.

| Plug-in | Batch-means | TRUE | |||||

|---|---|---|---|---|---|---|---|

| Iterations | 1000 | 2000 | 5000 | 1000 | 2000 | 5000 | |

| 114.07 | 111.65 | 112.05 | 23.25 | 29.68 | 27.61 | 111.78 | |

| 86.52 | 83.99 | 83.15 | 22.87 | 28.61 | 27.57 | 83.56 | |

| Iterations | 1000 | 2000 | 5000 | TRUE |

|---|---|---|---|---|

| 30.63 | 30.36 | 30.42 | 30.31 | |

| 52.84 | 51.53 | 50.94 | 51.06 |

We report the coverage probability of confidence regions in Table 3. We estimate the coverage probability by 1000 replications. From Table 3, we can observe that the coverage probabilities of the plug-in methods are getting closer to the nominal level when the number of iterates grows larger. However, the coverage probabilities of the batch-means method is only . The underestimation problem of the batch-means method is because it neglects the correlation between batches. One possible way to handle this problem is to do Monte-Carlo simulation as in Figure 2.

| iterations | 1000 | 2000 | 5000 |

|---|---|---|---|

| Plug-in | 82 | 84 | 88 |

| Batch-means | 14 | 14 | 20 |

| Plug-in (Non-ergodic) | 83 | 83 | 86 |

4.2 Lasso

Least absolute shrinkage and selection operator (Lasso) is a regression analysis method that performs both variable selection and regularization in order to enhance the prediction accuracy and interpretability of the resulting statistical model. We consider lasso on the prostate cancer example [7],

| (4.49) |

where is the random input vector and is the response variable. The feasible set of problem (4.49) is given by

Similar to [7], we first standardize the predictors to have unit variance and split observations into two parts. One part consists of 67 observations, which are the training set in [37]. We use only these 67 observations in our computation. In implementing of Algorithm 1, we use the same setting of the step-size and initial point in the former example, that is, and . Moreover, the maximum number of iterates is .

| Ave-Est | PI CI | BM CI | Last-Est | Non-PI CI | |

|---|---|---|---|---|---|

| 0.57 | [0.55,0.60] | [0.56,0.59] | 0.54 | [0.44,0.65] | |

| 0.17 | [0.13,0.20] | [0.14,0.20] | 0.18 | [0.09,0.27] | |

| 0 | [0,0.04] | [0,0.01] | 0 | [0,0.10] | |

| 0.01 | [0.01,0.01] | [0,0.03] | 0 | [0,0] | |

| 0.09 | [0.09,0.09] | [0.07,0.10] | 0.08 | [0.08,0.08] | |

| 0 | [0,0] | [0,0] | 0 | [0,0] | |

| 0 | [0,0] | [0,0] | 0 | [0,0] | |

| 0 | [0,0] | [0,0] | 0 | [0,0] |

| Ave-Est | PI CI | BM CI | Last-Est | Non-PI CI | |

|---|---|---|---|---|---|

| 0.21 | [0.14,0.28] | [0.18,0.24] | 0.17 | [0.03,0.31] | |

| 0 | [0,0] | [0,0] | 0 | [0,0] | |

| 0 | [0,0] | [0,0] | 0 | [0,0] | |

| 0 | [0,0] | [0,0.01] | 0 | [0,0] | |

| 0 | [0,0] | [0,0.02] | 0 | [0,0] | |

| 0 | [0,0] | [0,0.01] | 0 | [0,0] | |

| 0 | [0,0] | [0,0.01] | 0 | [0,0] | |

| 0 | [0,0] | [0,0.01] | 0 | [0,0] |

Tables 4-5 record the individual confidence intervals for lasso parameters with penalty terms and respectively. We only report the confidence regions of as is the intercept. Similar to [7], we can conclude the importance of predictors in predicting the response and the impact of penalty term in sparseness of predictors to problem (4.49). Specifically, for , the individual confidence intervals of and do not contain zero and the variances related to and are zero. Moreover, the individual confidence intervals of all other variables include zero in them. As and are close to zero, we may claim that the first two predictors are the most useful ones in predicting the response. On the other hand, for , only the individual confidence interval of does not contain zero, which indicates that the first predictor is more important than the second one. We can also observe from Tables 4-5 that lasso shrinks the regression coefficients by imposing a penalty parameter on their size.

References

- [1] F. Facchinei and J. Pang, Finite-Dimensional Variational Inequalities and Complementarity Problems. Springer New York, 2003.

- [2] X. Chen and M. Fukushima, “Expected residual minimization method for stochastic linear complementarity problems,” Mathematics of Operations Research, vol. 30, pp. 1022–1038, 2005.

- [3] G. Gürkan, A. Y. Demir, and S. Robinson, “Sample-path solution of stochastic variational inequalities,” Mathematical Programming, vol. 84, pp. 313–333, 1999.

- [4] J. Gwinner, “A class of random variational inequalities and simple random unilateral boundary value problems - existence, discretization, finite element approximation,” Stochastic Analysis and Applications, vol. 18, pp. 967–993, 2000.

- [5] X. Chen, T. K. Pong, and R. J. Wets, “Two-stage stochastic variational inequalities: an erm-solutioin procedure,” Mathematical Programming, vol. 165, pp. 71–112, 2017.

- [6] R. T. Rockafellar and R. J. Wets, “Stochastic variational inequalities: Single-stage to multistage,” Mathematical Programming, vol. 165, pp. 331–360, 2017.

- [7] S. Lu, Y. Liu, L. Yin, and K. Zhang, “Confidence intervals and regions for the lasso by using stochastic variational inequality techniques in optimization,” Journal of the Royal Statistical Society: Series B (Statistical Methodology), vol. 79, pp. 589–611, 2017.

- [8] S. Lu and A. Budhiraja, “Confidence regions for stochastic variational inequalities,” Mathematics of Operations Research, vol. 38, pp. 545–568, 2013.

- [9] M. Lamm and S. Lu, “Generalized conditioning based approaches to computing confidence intervals for solutions to stochastic variational inequalities,” Mathematical Programming, vol. 174, pp. 99–127, 2019.

- [10] S. Lu, “A new method to build confidence regions for solutions of stochastic variational inequalities,” Optimization, vol. 63, pp. 1431–1443, 2014.

- [11] S. Lu, “Symmetric confidence regions and confidence intervals for normal map formulations of stochastic variational inequalities,” SIAM Journal on Optimization, vol. 24, pp. 1458–1484, 2014.

- [12] G. Yu, L. Yin, S. Lu, and Y. Liu, “Confidence intervals for sparse penalized regression with random designs,” Journal of the American Statistical Association, 2019.

- [13] Y. Liu and J. Zhang, “Confidence regions of stochastic variational inequalities: Error bound approach,” Optimization, 2020. to appear.

- [14] Y. Liu, W. Yan, and S. Zhao, “Confidence regions of two‐stage stochastic linear complementarity problems,” International Transactions in Operational Research, vol. 29, pp. 48–62, 2022.

- [15] H. Robbins and S. Monro, “A stochastic approximation method,” Annals of Mathematical Statistics, vol. 22, pp. 400–407, 1951.

- [16] K. Chung, “On a stochastic approximation method,” Annals of Mathematical Statistics, vol. 25, pp. 463–483, 1954.

- [17] V. Fabian, “On asymptotic normality in stochastic approximation,” Annals of Mathematical Statistics, vol. 39, pp. 1327–1332, 1968.

- [18] B. T. Polyak and A. B. Juditsky, “Acceleration of stochastic approximation by averaging,” SIAM journal on control and optimization, vol. 30, no. 4, pp. 838–855, 1992.

- [19] M.-h. Hsieh and P. Glynn, “Recent advances in simulation optimization: confidence regions for stochastic approximation algorithms.,” in Proceedings of the 34th conference on Winter simulation: exploring new frontiers, pp. 370–376, 01 2002.

- [20] J. Lei and U. V. Shanbhag, “Variance-reduced accelerated first-order methods: Central limit theorems and confidence statements,” arXiv preprint arXiv:2006.07769, 2020.

- [21] H. Jiang and H. Xu, “Stochastic approximation approaches to the stochastic variational inequality problem,” IEEE Transactions on Automatic Control, vol. 53, pp. 1462 – 1475, 2008.

- [22] A. Iusem, A. Jofre, R. Oliveira, and P. Thompson, “Variance-based stochastic extragradient methods with linear search for stochastic variational inequalities,” SIAM Journal on Optimization, vol. 29, pp. 175–206, 2019.

- [23] M. Wang and D. Bertsekas, “Incremental constraint projection methods for variational inequalities,” Mathematical Programming, vol. 150, pp. 321–363, 2015.

- [24] S. Cui and U. Shanbhag, “On the analysis of reflected gradient and splitting methods for monotone stochastic variational inequality problems,” in 2016 IEEE 55th Conference on Decision and Control, pp. 4510–4515, 2016.

- [25] F. Yousefian, A. Nedic, and U. Shanbhag, “On stochastic mirror-prox algorithms for stochastic cartesian variational inequalities: Randomized block coordinate and optimal averaging schemes,” Set-Valued and Variational Analysis, vol. 26, pp. 789–819, 2018.

- [26] J. Duchi and F. Ruan, “Asymptotic optimality in stochastic optimization,” The Annals of Statistics, vol. 49, pp. 21–49, 2021.

- [27] X. Chen, J. Lee, X. Tong, and Y. Zhang, “Statistical inference for model parameters in stochastic gradient descent,” The Annals of Statistics, vol. 48, pp. 251–273, 2020.

- [28] M. Lamm, S. Lu, and A. Budhiraja, “Individual confidence intervals for solutions to expected value formulations of stochastic variational inequalities,” Mathematical Programming, vol. 165, pp. 151–196, 2017.

- [29] Y. Nesterov, “Primal-dual subgradient methods for convex problems,” Mathematical Programming, vol. 120, pp. 221–259, 2009.

- [30] S. Lee and S. J. Wright, “Manifold identification in dual averaging for regularized stochastic online learning,” Journal of Machine Learning Research, vol. 13, pp. 1705–1744, 2012.

- [31] L. Xiao, “Dual averaging methods for regularized stochastic learning and online optimization,” Journal of Machine Learning Research, vol. 11, pp. 2543–2596, 2010.

- [32] S. Zhao, X. Chen, and Y. Liu, “Asymptotic properties of dual averaging algorithm for constrained distributed stochastic optimization,” 2020. manuscript.

- [33] R. T. Rockafellar and R. Wets, Variational Analysis. Springer, 1998.

- [34] H. Chen, Stochastic Approximation and Its Applications. Springer US, 2003.

- [35] G. Hewer and C. Kenney, “The sensitivity of the stable lyapunov equation,” SIAM Journal on Control and Optimization, vol. 26, pp. 321–344, 1988.

- [36] W. Zhu, X. Chen, and W. B. Wu, “Online covariance matrix estimation in stochastic gradient descent,” Journal of the American Statistical Association, pp. 1–12, 2021.

- [37] T. Hastie, R. Tibshirani, and J. Friedman, The Elements of Statistical Learning: Data Mining, Inference, and Prediction. Springer New York, 2009.

5 Appendix

Lemma 5.1.

[34, Lemma 3.1.1] Suppose -dimension matrix , is a stable matrix, that is, every eigenvalue of has strictly negative real part. If step-size satisfies as , and -dimension vectors satisfy the following conditions

then defined by the following recursion with arbitrary initial value tends to zero:

| (5.50) |

Lemma 5.2.

[34, Theorem 3.3.1] Let be given by the following recursion with an arbitrarily given initial value:

| (5.51) |

Assume the following conditions hold:

-

(i)

as , and

-

(ii)

and is stable;

-

(iii)

where are constant matrices with and is a martingale difference sequence of -dimension satisfying the following conditions

(5.52) (5.53) and

(5.54) Then is asymptotically normal:

where