Lorenz map, inequality ordering and curves based on multidimensional rearrangements

Abstract.

We propose a multivariate extension of the Lorenz curve based on multivariate rearrangements of optimal transport theory. We define a vector Lorenz map as the integral of the vector quantile map associated to a multivariate resource allocation. Each component of the Lorenz map is the cumulative share of each resource, as in the traditional univariate case. The pointwise ordering of such Lorenz maps defines a new multivariate majorization order. We define a multi-attribute Gini index and complete ordering based on the Lorenz map. We formulate income egalitarianism and show that the class of egalitarian allocations is maximal with respect to our inequality ordering over a large class of allocations. We propose the level sets of an Inverse Lorenz Function as a practical tool to visualize and compare inequality in two dimensions, and apply it to income-wealth inequality in the United States between 1989 and 2019.

Keywords: Multidimensional inequality, multidimensional egalitarianism, Lorenz curve, Gini index, vector quantiles, optimal transport, majorization

Introduction

The Lorenz curve, first proposed in Lorenz (1905), is a compelling visual and simple quantification tool for the analysis of dispersion in univariate distributions. It allows easy visualization of dispersion from the curvature of a convex curve and its distance from the diagonal. The diagonal itself is the Lorenz curve of a degenerate distribution– an egalitarian allocation where all individuals have the same amount of resource. This visualization property is further enhanced by the relation between majorization and the pointwise ordering of Lorenz curves, which provides a way to visualize inequality comparisons between populations and within a given population between time periods. It also enables quick computations, reading off the curve, as it were, of the share of a resource held by the top or bottom of the allocation distribution for that resource. These features of the Lorenz curve account for much of its enduring appeal among practitioners, policy analysts and policy makers. This appeal is further enhanced by the relation between majorization and the pointwise ordering of Lorenz curves, which provides a way to visualize inequality comparisons between populations and within a given population between time periods. Comprehensive accounts are given in Marshall et al. (2011) and Arnold and Sarabia (2018).

The appealing properties of the Lorenz curve are well captured by the formulation given in Gastwirth (1971). In that formulation, the Lorenz curve is the graph of the Lorenz map, and the latter is the cumulative share of individuals below a given rank in the distribution, i.e., the normalized integral of the quantile function. The relation to majorization and the convex order follows immediately, as shown in section C of Marshall et al. (2011). As pointed out by Arnold (2008), this makes the Lorenz ordering an uncontroversial partial inequality ordering of univariate distributions, and most open questions concern the higher dimensional case.

Dispersion in multivariate distributions is not adequately described by the Lorenz curve of each marginal, and a genuinely multidimensional approach is needed. Even for utilitarian welfare inequality, Atkinson and Bourguignon (1982) motivate the need for the multidimensional approach initiated by Fisher (1956). More generally, the literature on multidimensional inequality of outcomes and its measurement is vast, as evidenced by many recent surveys, see for instance Decancq and Lugo (2012), Aaberge and Brandolini (2014), Andreoli and Zoli (2020). We only discuss it insofar as it relates to the Lorenz curve.

Multivariate extensions have been proposed for the Lorenz curve, most notably Taguchi (1972a, 1972b), Arnold (1983), and Koshevoy and Mosler (1996, 1999). They are reviewed in Marshall et al. (2011) and Sarabia and Jorda (2014) and discussed in more details in the next subsection. We contribute to this literature with a vector version of the Gastwirth (1971) formulation of the Lorenz map, based on a multivariate reordering of the data, with optimal transport rearrangement theory. With this reordering, we emulate the features of the Lorenz curve that most contributed to its success: we derive a tool to compute the share of each resource held by the subset of the population below any given rank, and we provide tools to visualize and compare inequality in multivariate distributions.

The solution of quadratic optimal transport problems, see Villani (2003, 2009), can be seen as rearrangements of random vectors. For a given random vector , interpreted as the resource allocation in the population, under mild regularity conditions, there is a uniform random vector and a gradient of a convex function such that . The vector can be interpreted as a vector of multivariate ranks of individuals in the population, and the Lorenz map at can be defined as the cumulative vector share of resources held by individuals with vector ranks below , componentwise. Equivalently, we define the Lorenz map as the integral of the vector quantile of Chernozhukov et al. (2017). Correspondingly, we define a Lorenz ordering from the pointwise dominance of Lorenz maps. The Lorenz map and Lorenz ordering defined here reduce to the traditional Lorenz map and ordering in the univariate case. Our multivariate Lorenz map also shares two important properties with the traditional Lorenz map. First, it characterizes the distribution of the random vector it is constructed from. Second, we define a multi-attribute notion of egalitarian allocation and we show that such egalitarian allocations have maximal Lorenz maps in a large class of allocations.

Since the multivariate Lorenz map is an integrated quantile map, the Lorenz ordering based on pointwise dominance of Lorenz maps is a multivariate majorization ordering, based on optimal transport reorderings. We show that the Lorenz ordering is able to rank two allocations, when one is a monotone mean preserving spread of the other. The notion of monotone mean preserving spread is a multivariate extension of the univariate monotone mean preserving spread of Quiggin (1992), also called Bickel-Lehmann increases in dispersion (Bickel and Lehmann (1976)). It captures increases in inequality in the marginals, as well as increases in correlation. We show that our Lorenz ordering can rank two allocations, where one is the result of a correlation increasing transfer of the other, that existing multivariate Lorenz orderings are unable to rank (see section 2.3). We also construct a multivariate Gini index based on the distance to the Lorenz map of an egalitarian allocation where all individuals have identical endowments. This Gini index preserves the Lorenz ordering and also reduces to the traditional Gini in the univariate case.

For our visualization device, we define an Inverse Lorenz Function at a given vector of resource shares as the share of the population that cumulatively holds those shares. It is characterized by the cumulative distribution function of the image of a uniform random vector by the Lorenz map. Hence, it is a cumulative distribution function by construction, like the univariate inverse Lorenz function. In two dimensions, the -level sets of this cumulative distribution function, which we call -Lorenz curves, are non crossing downward sloping curves that shift to the south-west when inequality increases, as defined by the Lorenz ordering. Because this compelling visual tool for the comparison of multi-attribute inequality is one of the major objectives we pursue with this work, we report all our results in the bivariate case, and propose an illustration to the analysis of income-wealth inequality in the United States between 1989 and 2019.

Closely related work

The original definition of the Lorenz curve is implicit. Denote the cumulative distribution function of random variable . The Lorenz curve of allocation is defined by and where denotes the indicator function. In the multivariate case, denote the cumulative distribution of random vector and let be the cumulative distribution of the -th marginal. Arnold (1983) extends the implicit formulation to multiple univariate ranks and , and defines a scalar-valued Lorenz map . Koshevoy and Mosler (1996) keep for random vector , but extend univariate shares to vector shares. The Lorenz zonoid of Koshevoy and Mosler (1996) relates any proportion of the population to its share of each of the resources. The Lorenz zonoid is difficult to compute in general. We discuss the relation between our Lorenz map, the Lorenz surface of Taguchi (1972a, 1972b) and the Lorenz zonoid of Koshevoy and Mosler (1996) in section 1 after equation (1.5). Koshevoy and Mosler (1999) propose an Inverse Lorenz Function that can be interpreted as the maximum share of the population that holds a given vector share of resources, but it is the solution of a complex optimization problem. Grothe et al. (2021) define an Inverse Lorenz Function as the probability that for each , a share of resource is collectively held by individuals whose rank in the distribution of resource is below . They characterize this Inverse Lorenz Function with a coupling argument. Multivariate Lorenz dominance is defined and discussed in Koshevoy (1995), Koshevoy and Mosler (2007), Banerjee (2010). See Arnold and Sarabia (2018) for a comprehensive account. Gajdos and Weymark (2005) discuss multivariate versions of the Gini index based exclusively on functionals of individually reordered marginals, as opposed to the multivariate reorderings proposed here. Koshevoy and Mosler (1997), Banerjee (2016), Grothe et al. (2021), Mosler (2013), Sarabia and Jorda (2020) also propose multivariate Gini indices based on multivariate Lorenz curve proposals. Finally, optimal transport rearrangements are used to define multivariate comonotonicity and quantiles in Ekeland et al. (2012), Galichon and Henry (2012) and Puccetti and Scarsini (2010). More recently, subsequent to our work, Hallin and Mordant (2022) also adopt a transportation approach to the definition of multi-attribute Lorenz curves. They adopt a center-outward approach, which is better suited to define notions of middle class.

Notation

All random elements are defined on the same complete probability space. Let be the uniform distribution on . The indicator function takes value if and zeo otherwise. We call the set , where denotes the componentwise inequality. We denote a random vector on . Let stand for the distribution of the random vector . Following Villani (2003), we let denote the image measure (or push-forward) of a measure by a measurable map . Explicitly, for any Borel set , . The generalized inverse of a function is denoted . The symbol denotes the gradient, and the Jacobian. The convex conjugate of a convex lower semicontinuous function is denoted . We use the standard convention of calling weak monotonicity non-decreasing or non-increasing, as the case may be.

1. Vector Lorenz Maps and Curves

We propose a method to compare, measure and visualize inequality of allocations of two resources. A resource allocation is modeled as a random vector with support . The distribution of is assumed to have unit mean, to avoid issues of normalization or change of units of measurement. Most of the definitions and properties we present here are valid in higher dimensions. However, the crucial visualization aspect is lost, so we don’t pursue a greater level of generality.

1.1. Lorenz map

The Gastwirth (1971) formulation of the Lorenz curve for a scalar allocation relies on the quantile function. Let be a scalar allocation with mean and cumulative distribution function . Then is the rank of individuals in the distribution. The value at rank of the Lorenz curve associated with allocation is the cumulative share of individuals with rank . Hence

| (1.2) |

To analyze inequality in allocation , we can first look at inequality in each marginal allocation and , using the Lorenz curves and . However, this strategy disregards the effect of dependence. The latter is relevant to inequality, as can be trivially illustrated by the fact that for given wealth and income marginal allocations, the co-monotonic allocation (the wealthier individuals have higher incomes) is more unequal than the admittedly unrealistic counter-monotonic allocation (the wealthier individuals have lower income). In section 2.3, we discuss an example of such a comparison. In this example, an allocation where the first half of the population holds all the resources is compared with an allocation where the first half of the population holds the totality of the first resource, while the second half of the population holds the totality of the second resource.

To take dependence into account, we propose to emulate the Gastwirth (1971) formulation by measuring cumulative shares of both resources for all individuals, whose vector rank is below . The vector rank we adopt is a uniform random vector on . It is obtained from the vector allocation via a unique transformation analogous to the probability integral transform in the scalar case described above. Its associated vector quantile, inverse of the vector rank, is guaranteed when has independent marginals to simply be the vector of univariate quantile functions. This multivariate quantile function can then be integrated over to obtain a vector analogue of the Gastwirth (1971) formulation of the Lorenz curve.

We adopt the vector quantile and rank notions proposed in Chernozhukov et al. (2017), based on optimal transport theory. The vector quantile of random vector is defined, to emulate the traditional quantile function, as the unique cyclically monotone function that pushes the uniform distribution on into the distribution of random vector . Existence and uniqueness follow from Theorem 1 in McCann (1995), which extends the Brenier (1991) polar factorization theorem (see also Rachev and Rüschendorf (1990)) beyond finite second moments. We give a brief review of the theory of vector ranks and quantiles, and the underlying notions in optimal transport theory, in appendix A.1. Here we only give the elements required to define our vector Lorenz map.

Definition 1 (Vector quantiles).

Let be the uniform distribution on , and let be the distribution of a random vector on . There exists a convex function such that . The function exists and is unique, -almost everywhere. We define the vector quantile of as the function , and we call the function a potential of , following the optimal transport literature.

Existence and uniqueness in definition 1 follow from proposition 3 in appendix A.1. In case , gradients of convex functions are nondecreasing functions, hence the vector quantile of definition 1 reduces to the classical quantile function.

By construction, if a random vector has uniform distribution on , then the random vector has distribution . Take any point . The proportion of the resources held by individuals ranked below is the cumulative integral of the vector quantile, as in the scalar case.

Definition 2 (Lorenz map).

Let . The Lorenz map of an allocation is the vector-valued function defined by

| (1.4) |

As stated in proposition 3 in appendix A.1, when has absolutely continuous distribution , its quantile function is -almost everywhere invertible with inverse , where is the convex conjugate of (see the introduction for notation and definitions from convex analysis). In that case, the transformation is the vector analogue of the probability integral transform discussed above. The random vector is the vector rank of the individual with endowment , in the terminology of Chernozhukov et al. (2017). In this case, the Lorenz map of definition 2 can be rewritten:

| (1.5) |

This clarifies the interpretation of as the cumulative endowment of all individuals with vector rank below .

Relation with other multivariate Lorenz concepts

Expression (1.5) also clarifies the relation with the Lorenz surface of Taguchi (1972a,1972b) and the Lorenz zonoid of Koshevoy and Mosler (1996). With a bivariate allocation, its Lorenz zonoid (Koshevoy and Mosler (1996)) relates any function to the vector

| (1.6) |

Hence, to a proportion of the population , it associates their share of each of the resources. The Lorenz surface of Taguchi (1972a,1972b) is a subset of the Lorenz zonoid, obtained with the choice of functions , all . Both Taguchi (1972a,1972b) and Koshevoy and Mosler (1996) relate univariate population proportions to share proportions. Our proposal differs substantially from these in that it directly relates a specific subset of the population, namely individuals with multivariate rank below to their share of both resources. Beyond this major difference, under the conditions for equation (1.5), we can make a direct connection. If, in (1.6), we use the class of functions , for each rank , where is the vector rank defined in section 1, we obtain the surface , which is therefore a subset of the Lorenz zonoid. This subset is different from the Taguchi (1972a,1972b) Lorenz surface, since in general.

Examples

We now explore special endowments and compute the corresponding Lorenz maps. First, we consider the case, where all individuals are endowed with the same quantity of resources.

Example 1 (Identical allocations).

If almost surely, then for all , and . The image of is the diagonal in .

Second, we check that our definition is compatible with scalar definitions when both resources are independently distributed.

Example 2 (Independent Resources).

Let the components and of be independent with univariate Lorenz curves and respectively. Then, the Lorenz map is . This expression of the Lorenz map has the following interpretation. Consider the first component . The share of resource held by people with multivariate rank in is the marginal share, equal to the univariate Lorenz function. Since the two resources are independent, this share is uniformly distributed along the other dimension, so that people with ranks in command a share . The other component is interpreted analogously. When , the Lorenz map takes values . That is, the image of under is the Lorenz curve of the second resource (and symmetrically when ).

Third, we derive the Lorenz map in the case of endowments with the same components, i.e., almost surely.

Example 3 (Comonotonic Resources).

Let the components and of the endowment be almost surely equal. Then, and have identical distributions. The optimal transport map from the uniform distribution on to the distribution of is then , where is the optimal map from to the distribution of , where , which has density on given by . Each component of the Lorenz curve is then given by

In case and are uniformly distributed on , the optimal transport map for is given by , so that . We then have,

when , and

when . The image of this Lorenz map is once again the diagonal in .

1.2. Inverse Lorenz Function and -Lorenz Curves

In the scalar case discussed above, inverting the Lorenz curve defined in (1.2) yields the inverse Lorenz curve

| (1.8) |

The scalar inverse Lorenz curve at is therefore shown in (1.8) to be equal to the maximum proportion of the population with cumulative share of the resource equal to . In the vector case, the right-hand side of (1.8) becomes

| (1.9) |

where , inequality is understood component-wise, and the probability is taken with respect to the uniform random vector on . The expression above is no longer the inverse of the Lorenz map , but it can still be interpreted as the share of the population with cumulative shares of both resources equal to . This motivates the following definition.

Definition 3 (Inverse Lorenz Function).

(1) The Inverse Lorenz Function (ILF) of a bivariate random vector is the function defined by (1.9). (2) We call -Lorenz curves the curves for each .

The -Lorenz curves are the objects involved in our proposed multivariate inequality visualization technique. We will see how to compare the inequality of different endowments based on the shape and relative positions of their respective -Lorenz curves. First, we revisit the three special cases of the previous section.

-

Example 1 continued

[Identical allocations] The ILF of the endowment is when and

By definition, the -Lorenz curves are right angles defined by .

-

Example 2 continued

[Independent Resources] The ILF of endowment with independent components is

where is the univariate inverse Lorenz curve of .

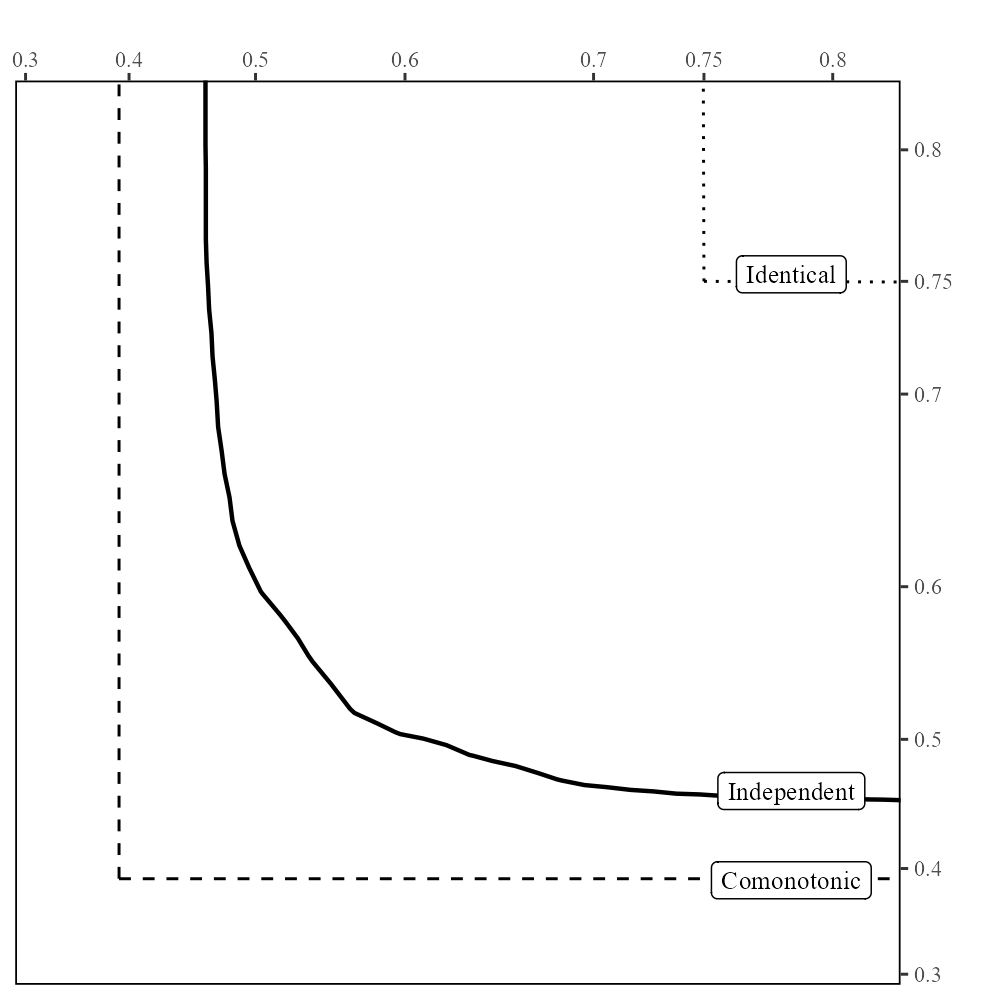

Figure 1 shows the -Lorenz curve of the identical allocation compared to the comonotonic and independent cases with . We use lognormal marginal distributions as it is traditionally found in the literature and convenient for tuning inequality by selecting the scale parameter ; see Arnold and Sarabia (2018).

1.3. Properties of Lorenz maps, and -Lorenz curves

The traditional scalar Lorenz curve enjoys many well-known properties that justify its interpretation as an inequality measurement, comparison and visualization tool. We emulate many of these properties and provide new ones to justify the interpretation of our Lorenz map, Inverse Lorenz Function and -Lorenz curves as multi-attribute inequality measurement, comparison and visualization tools.

First, the Lorenz map characterizes the distribution of the endowment it is associated with.

Property 1.

The Lorenz map characterizes the distribution of in the sense that and are identically distributed if and only if .

The Lorenz map is a map from to . Hence, unlike the traditional scalar Lorenz curve, it cannot be a cdf. However, the Inverse Lorenz Function trivially is a cdf by construction.

Property 2.

The Inverse Lorenz Function is the cumulative distribution function of a random vector on .

In the univariate case, the Lorenz curve of the identical endowment almost surely, is , which is sometimes called the egalitarian line. The Lorenz curve of any other endowment is below the egalitarian line, i.e., , for all . For the identical allocation of example 1 is a direct extension of the univariate notion of egalitarian. We show here that the Lorenz map and Inverse Lorenz Function of the identical allocation provide similar bounds in the multi-attribute case. For this, we require endowments with components that display a form of positive association defined in assumption 1. We will argue in section 3 that defining egalitarianism solely by identical allocations is too restrictive in the case of multiple resources, and we will show that a much larger class of allocations have Lorenz maps dominated by an egalitarian allocation from definition 9, which includes the identical allocation.

Assumption 1.

The vector quantile of is such that

are monotonically increasing as functions of and , respectively, where the vector is uniformly distributed on .

This assumption imposes a type of positive dependence between and through their ranks. More precisely, assumption 1 imposes a form of positive regression dependence, as in Lehmann (1966), between one resource and the other’s rank. A sufficient condition for assumption 1 is supermodularity of the potential function of endowment , as shown in lemma 1 below. We also show in lemma 1, that supermodularity of the potential function also implies positive quadrant dependence of the two components and of i.e., , for all , see Lehmann (1966).

Lemma 1 (Supermodular potential).

Suppose has a supermodular potential function, i.e., , with . Then, assumption 1 holds, and and are positive quadrant dependent.

For endowments satisfying assumption 1, we show that Lorenz map and Inverse Lorenz Function of the identical allocation serve as upper and lower bounds, respectively.

Property 3.

Without assumption 1, some allocations may have a Lorenz map that is component-wise larger than the Lorenz map of the identical allocation for some ranks. To illustrate the point, consider the potential . It corresponds to an endowment , whose distribution is supported on the line . Calculating the Lorenz map, we obtain

Notice, in particular, that in the region where . If the implicit relative price of resource is , endowment is an egalitarian endowment, since all individuals have equal budgets. However, this endowment does not satisfy assumption 1 and its Lorenz map is not dominated by as we have shown. This apparent departure from properties of the scalar Lorenz curve is due to the fact that an endowment with a.s. can also be considered egalitarian, as we discuss in section 3.

Visually, inequality can be assessed by the departure of -Lorenz curves from those of the identical allocation. This visual comparison is facilitated by the fact that they are shaped like indifference curves.

Property 4.

(i) The -Lorenz curves are the level curves of a bivariate cdf, hence they are downward sloping, non decreasing in and they do not cross. In addition, (ii) The -Lorenz curves are convex if

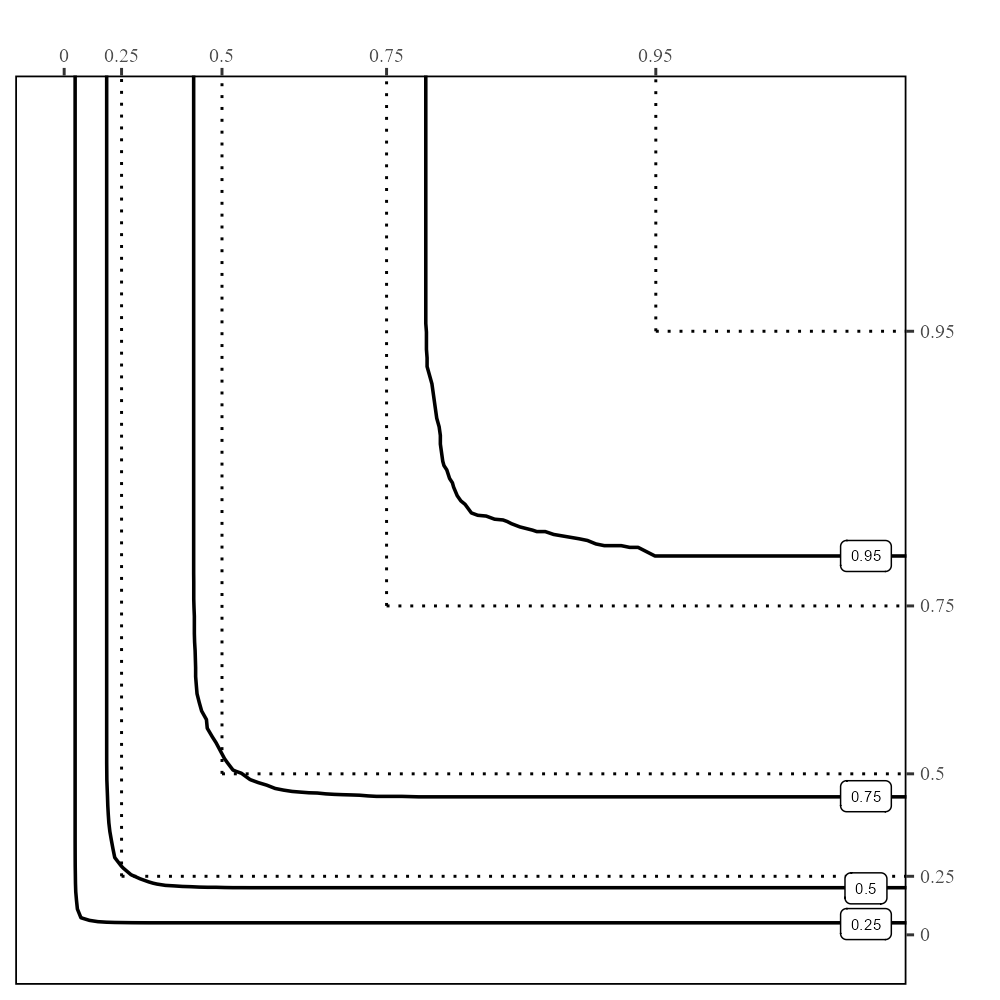

Figure 2 shows -Lorenz curves for allocations with lognormally distributed marginals and Plackett copulas with dependence parameter , for , and . Plackett copulas were used in Bonhomme and Robin (2009) in their model of earnings dynamics and they exhibit symmetric upper- and lower-tail dependence making them suitable in this context. The markings on the horizontal and vertical scales indicate the level of the -Lorenz curves of the identical allocation for comparison. This allocation exhibits positive association by construction and the diagram indicates it has ILF that dominates the ILF of the identical allocation.

2. Inequality orderings

2.1. Lorenz ordering

Consider two allocations and , with respective Lorenz maps and . If for some vector rank , the same proportion of the population with vector ranks below commands a larger share of both resources in allocation than in allocation . If this is true for any vector rank in , then, we say that allocation is more unequal than allocation .

Definition 4.

An allocation is said to be more unequal in the Lorenz order than an allocation if for all . We denote this as .

As a partial ordering based on cumulative sums of vector quantiles, the relation is a multivariate extension of the concept of majorization of Hardy et al. (1934). It is different from existing multivariate notions of majorization reviewed in Marshall et al. (2011) and Arnold and Sarabia (2018), in that it relies on a multivariate reordering of the random vector allocation. The relation is equivalent to stochastic dominance of the random vector , with , over (see Section 3.8 of Müller and Stoyan (2002)). As in the scalar case, it is a partial ordering. Under assumption 1, the maximal element of is the identical allocation by property 3.

We can also define an increasing inequality order based on the Inverse Lorenz Functions. Consider two allocations and , with respective Inverse Lorenz Functions and . If for some vector of shares , a larger proportion of the population commands the same share of resources in allocation than in allocation . If this is true for any vector of resource shares in , then, we say that allocation is more unequal than allocation .

Definition 5.

An allocation is said to be more unequal in the weak Lorenz order than an allocation if for all . We denote this as .

The relation is equivalent to lower orthant dominance of the random vector , with , over (see Section 3.8 of Müller and Stoyan (2002)). In the scalar case, the orderings of definitions 4 and 5 both coincide with the traditional Lorenz ordering. In higher dimensions, however, the equivalence doesn’t hold. Nonetheless, as the name indicates, the weak Lorenz inequality order of definition 5 is weaker than the Lorenz order of definition 4, as we show in the following proposition.

Proposition 1.

This inequality dominance of definition 5 can be visualized on through the relative positions of -Lorenz curves. Indeed, the -Lorenz curves are, by definition, curves with equation . In other words,

Suppose is less unequal in the Lorenz order than . For any , by definition of the Lorenz order, . So with . This can be visualized as a shift to the north-east of the -Lorenz curves of the less unequal allocation relative to the -Lorenz curves of the less unequal allocation .

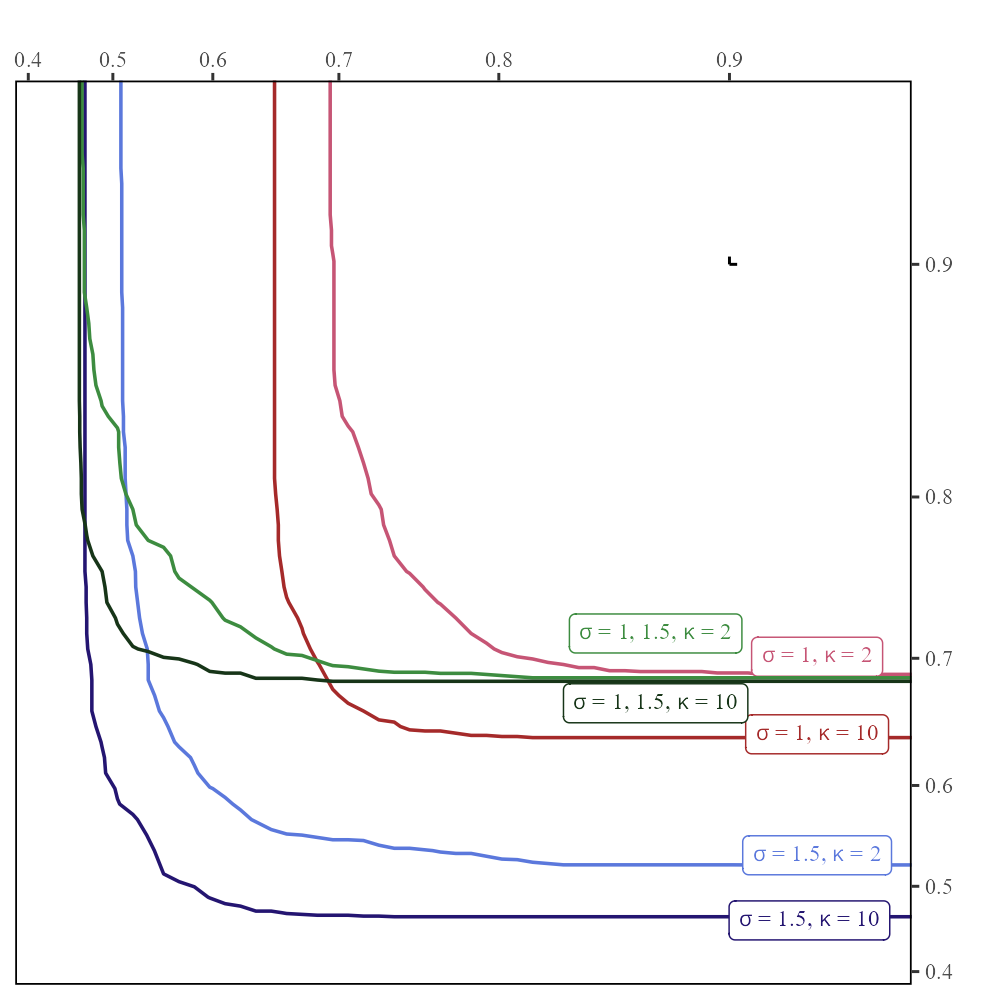

Figure 3 compares -Lorenz curves of different allocations with lognormally distributed marginals and Plackett copulas, for . The coefficient of the lognormal distributions takes value or , whereas the dependence parameter of the Plackett copula takes value (lower dependence) or (higher dependence). In case of marginals with different , the asymmetry is reflected in the -Lorenz curves. Moreover, other things equal, inequality increases with , which measures inequality in the marginals, and with , which measures dependence of the copula.

2.2. Increasing marginal inequality and increasing correlation

A desirable feature of the Lorenz inequality ordering of definition 4 is its ability to rank two allocations and , when the latter is obtained from the former through a transfer that increases inequality of the marginals or that increases the degree of dependence between the marginals. We formalize this feature with a specific type of multivariate transfer called monotone mean preserving spread, using the terminology of Quiggin (1992) in univariate risk analysis. Such transfers involve ultramodular functions, which were introduced in Marinacci and Montrucchio (2005) and applied to multidimensional inequality and risk analysis in Müller and Scarsini (2012), and which we now define.

Definition 6 (Ultramodular functions).

We call a function ultramodular, if it is

-

()

supermodular, i.e., for all and in , where and denote the componentwise maximum and minimum respectively,

-

()

separately convex, i.e., and are convex for all .

By definition, the gradient of a differentiable ultramodular function satisfies non decreasing, for and . Therefore, if the gradient of an ultramodular function , with , is added to an allocation with multivariate gradient , it corresponds to a transfer with the following property: the amount of the transfer of each resource is non decreasing (component-wise) in the multivariate rank of the individual. In other words, individuals richer in resource receive more of both resources, for . We call such an unequivocally inequality increasing transfer monotone mean preserving spread.

Definition 7 (Monotone Mean Preserving Spread, MMPS).

A distribution with multivariate quantile is said to be more dispersed than a distribution with multivariate quantile if there is an ultramodular function such that for all ,

| (2.1) |

In the univariate case, equation (2.1) states that the difference between the quantile function of and that of is a non decreasing function. Such a difference is a monotone mean preserving spread (Quiggin (1992)), also called Bickel-Lehmann increase in dispersion (Bickel and Lehmann (1976)). A related extension in the theory of multivariate risks was proposed in Charpentier et al. (2016).

As in the univariate case, the relation “ is an MMPS of ” is a transitive relation, hence defines a partial order of increasing inequality. The following lemma states that a monotone mean preserving spread is also an increase in inequality according to our Lorenz order in definition 4.

Lemma 2 (Monotonicity in MMPS).

If is an MMPS of , then .

The multivariate Lorenz order of definition 4 therefore ranks an allocation as more unequal if a marginal is more unequal, as defined by univariate monotone mean preserving spreads. It also ranks an allocation as more unequal if the marginal resource allocations are more correlated. The former point is immediate from lemma 2 and definition 7. The latter point requires more explanation. Lemma 1 shows that allocations with a supermodular potential are positive quadrant dependent. When an allocation is an MMPS of , the potential of is more supermodular than the potential of , in the sense that

| (2.2) |

for all . Relation (2.2) is the basis of a partial order of increasing dependence.

2.3. Detection of correlation increasing transfers

Consider two endowments with identical marginal distributions but radically different joint distributions. Call Allocation the random vector that equals and with equal probabilities. Hence, every member of the first half of the population holds an equal endowment of the first resource, while every member of the second half of the population holds an equal endowment of the second resource. Compare it with Allocation , which is the random vector that equals and with equal probabilities. Hence, every member of the first half of the population holds an equal endowment of the both resources, while the second half of the population holds nothing.

The multivariate quantile of is the map

The two regions and of have probability each and are such that the map minimizes the sum of squared distances between and . Similarly, the multivariate quantile of is the map

Integrating the vector quantiles over , the Lorenz map is given by

and the corresponding Lorenz map is given by

The difference between the two multivariate Lorenz maps is

which is non negative, since . The transfer from endowment to endowment is an egregious increase in inequality, since it gives all resources of both goods to the same half of the population. It is therefore a desirable feature of our Lorenz inequality ordering that . This differentiates our proposal from the partial order of Lorenz zonoid inclusion in Koshevoy (1995), Koshevoy and Mosler(1996; 2007), as discussed in Andreoli and Zoli (2020).

2.4. Multivariate Gini Index

Lorenz ordering is a partial ordering of multivariate distributions. For a complete inequality ordering, we also propose an extension of the classical Gini index to compare inequality in multi-attribute allocations.

The univariate Gini index can be interpreted as the average deviation from the egalitarian allocation, the univariate version of our identical allocation. We emulate this interpretation and define a multivariate Gini based on an average deviation from the the Lorenz map . The deviation measure we propose is

| (2.5) |

where, as before, and are the first and second components of , respectively. Note that the expression can be extended to allow for weights to reflect relative importance of the two resources, without changing the analysis below. After normalization, (2.5) becomes

| (2.6) |

which yields the following definition.

Definition 8 (Gini Index).

(2.6) defines the Gini index of allocation .

The traditional Gini index of a univariate allocation can also be characterized as a weighted sum of outcomes, where the weights are increasing linearly in the rank of the individual in the population. Hence, the negative of the Gini, seen as a social evaluation function displays inequality aversion by giving more weight to the outcomes of lower ranked individuals than to those of higher ranked ones. We show in the appendix that the same interpretation is valid for our multivariate Gini, which takes the form

| (2.7) |

In expression (2.7), is the sum of the two resource allocations of the individual in the population with vector rank . Hence, the Gini index is indeed a weighted sum of outcomes, with weights increasing with the vector ranks . It is a genuinely multivariate extension in that the weighting scheme, hence the social evaluation of inequality, depends on multivariate ranks of individuals.

-

Examples 2 and 3 continued

We compare Gini indices in the independent case with the perfect comonotonicity case, where and have the same (uniform on ) marginal distributions. We verify (analytically for and numerically using Wolfram for ) that is smaller in the comonotonic case, than in the independent case. Hence the Gini index (and the measure of inequality) is larger in the comonotonic case.

Example 4 (Countermonotone Resources).

If we have a.s., then for almost all , and we obtain , so that, in particular, the Gini index in the countermonotone case is the same as in the case of the identical allocation, i.e., equal to , and both are smaller than the Gini of the allocation with independent resources. This is consistent with the fact that these allocations are considered egalitarian according to definition 9.

The Gini index of definition 8 is in under assumption 1. It equals for the identical allocation. It tends to , when the Lorenz map tends to (extreme inequality). The Gini index of an allocation with independent components reduces to the average of classical scalar Ginis of both components. Like the classical scalar Gini index, it satisfies a set of desirable properties for an inequality index. First, it doesn’t depend on labeling of individuals in the population, only on the allocation distribution. This property is referred to as anonymity. Second, the Gini index of definition 8 preserves the Lorenz inequality ordering, in the sense that higher inequality according to implies a larger value of the Gini index. In other words, implies . We refer to this property as monotonicity. Finally, it satisfies a multivariate extension of comonotonic independence proposed in Galichon and Henry (2012), as a generalization of the scalar requirement in Weymark (1981). If individuals are ranked identically in endowments and , and is more unequal than , then, adding to both and a third endowment cannot reverse the inequality ordering, if ranks individuals as and do. Details and proofs are given in appendix B.

3. Egalitarian multi-attribute allocations

The identical allocation with Lorenz map is a very special instance of egalitarian allocation. We extend this narrow notion of egalitarian allocation to include income egalitarianism, in the terminology of Kolm (1977). In the special case where the two resources are transferable with relative price of the second resource, then an allocation is deemed egalitarian if all agents have the same budget endowment, i.e., if (where the constant value is derived from the normalization ). In the general case of non (or imperfectly) transferable resources, we call egalitarian the allocations with equalized shadow budgets.

Definition 9 (Egalitarian allocation).

An allocation such that a.s., for some , is called egalitarian.

Another way to interpret egalitarianism of such an allocation, beyond shadow budget equality, is through the perfect compensation of inequality in the marginal resource allocations by perfect negative correlation between resource allocations. The vector quantile and Lorenz map of egalitarian allocations can be characterized in the following way.

Proposition 2.

Let be a random vector with distribution . An egalitarian allocation such that , admits potential for some convex function such that and allocation is equal in distribution to ; The Lorenz map is given by

If, in addition, denotes the quantile function (generalized inverse) of , then

where is the cdf of the random variable ; see appendix D for an explicit expression for .

We see in proposition 2 that the distribution of the allocation is entirely determined by the convex function , which is itself determined by the distribution of one of the marginals of . This follows from the deterministic linear relationship between the two resource allocations. The perfect negative correlation compensates any inequality in the marginal allocations.

With this definition of egalitarian allocations, we show that a large class of allocations are dominated in the Lorenz order by egalitarian allocations, and that egalitarian allocations are maximal in the Lorenz order of definition 4.

Assumption 2.

For some , the potential of allocation satisfies for all :

Before stating the main result of this section, which is an extension of property 3, we discuss sufficient conditions for assumption 2 and examples of classes of allocations that satisfy assumption 2. The following lemma provides sets of sufficient conditions based on a suitable choice of .

Lemma 3 (Sufficient condition for assumption 2).

An allocation with potential satisfies assumption 2 if any of the following conditions hold.

-

The potential is supermodular.

-

The potential satisfies:

(3.2) -

The function

is positive and constant equal to over and, for all , the Hessian of is constant over .

The first sufficient condition in lemma 3, i.e. supermodularity of the potential , imposes a form of positive dependence between the two resources, which implies assumption 2 (and 1). However, assumption 2 also accommodates allocations that do not satisfy positive dependence. For instance, the mixture of an egalitarian allocation with a positively dependent one satisfies assumption 2.

Example 5.

An allocation with potential , with convex, and ultramodular, satisfies assumption 2. It mixes a perfectly negatively correlated allocation with a positively dependent one.

Sufficient condition (2) in lemma 3 also show that positive dependence is not required for assumption 2. Indeed, a special case of condition (2) in lemma 3 is the case, where is a quadratic function, hence has a constant Hessian. Indeed, in that case, convexity of immediately yields (3.2).

Example 6.

All allocations with quadratic potential with , i.e., allocations of the form , with , satisfy assumption 2

Sufficient condition (2) in lemma 3 can also be used to show that allocations where the two marginal resource allocations are independent also satisfy assumption 2. More generally, a large class of allocations defined as deviations from independence satisfy assumption 2 as formalized in the following example.

Example 7.

An allocation with potential satisfies assumption 2 if and , and with . The case is the case of independent marginal allocations.

Assumption 2 is not satisfied, however, in case and are perfectly negatively correlated, i.e., with increasing , when is nonlinear.

Under assumption 2, we can complement property 3 and emulate the traditional property of Lorenz curves, which are maximal at perfect equality. Here we show that egalitarian allocations dominate all allocations that satisfy assumption 2, and are themselves undominated thereby forming a class of distributions that are maximal under the Lorenz order.

4. Empirical Illustration

In this section, we propose estimators for the Lorenz map, Inverse Lorenz Function, -Lorenz curves and Gini index and how to calculate them. We then apply these to the analysis of wealth-income inequality in the U.S. with data from the Survey of Consumer Finances (SCF) between the years 1989-2019.

4.1. Estimation of the Lorenz map, Inverse Lorenz Function, and Gini

Suppose we have a sample from a probability distribution with sampling weights such that and normalized to have sample mean one. Let be the empirical distribution relative to the weighted sample and let be the Lebesgue measure over .

Vector Quantiles and Lorenz maps. Let be an estimator for the population vector quantile of Definition 1. The empirical Lorenz map is defined as the plug-in estimator

| (4.1) |

One natural estimator for the vector quantile is the solution to the transport problem between the rank space and the data. By Proposition 3 in Appendix A.1, there exists a convex function such that . The function exists and is unique, -almost everywhere. Since pushes forward to , it takes a.e. finitely many values in . Hence, is a piecewise affine convex function, and there exists a unique (up to scalar addition) such that

and is the solution of a convex optimization problem; see for instance Proposition 6 of Ekeland et al. (2012). The resulting estimator induces a cell decomposition of the domain into convex polytopes, one for each observation in the sample, and each with area equal to the value of the corresponding sample weight . This partitioning is called a power diagram; see Aurenhammer (1987).

Viewing the transport problem as solving for the power diagram of with weights has computational advantages. This is exploited in Aurenhammer et al. (1998) where they connect solving for the optimal weight vector to an unconstrained convex optimization problem. This allows for efficient (damped) Newton or quasi-Netwon methods as in Mérigot (2011) and Kitagawa et al. (2019) for which the gradient and Hessian of the objective function are easily computed, see Lévy (2015) 111Implementations for these methods are available in the Geogram and CGAL libraries. To start, see https://github.com/BrunoLevy/geogram..

The cells of the resulting power diagram are defined by

We can therefore rewrite the estimator of the Lorenz map (4.1) as

where and are the components of and the Lebesgue measure is simply the ordinary area of the convex polytope formed by the intersection of the cell and the rectangle .

Inverse Lorenz Function. The estimator can then be used to generate a pseudo sample , where is a uniform random sample from . The Inverse Lorenz function can then be estimated with the empirical distribution of this pseudo-sample:

| (4.2) |

and the -Lorenz curves are given by the level sets of .

Gini Index. Finally, the Gini index is estimated directly from the plug-in of the empirical Lorenz map:

where and are the two components of individual ’s endowment in the sample and the weights are

which sum to one over .

Calculation of our Gini index can be done using Monte Carlo integration techniques. One way is to take an average of a sample of empirical Lorenz maps evaluated from uniform random sample of ranks to estimate (2.6). Another is to bypass the Lorenz map entirely and estimate the partition of ranks then apply Monte Carlo integration to approximate (4.1) for each . In what follows we use the former since we are already calculating the empirical Lorenz map for the SCF example.

4.2. Data and descriptive statistics

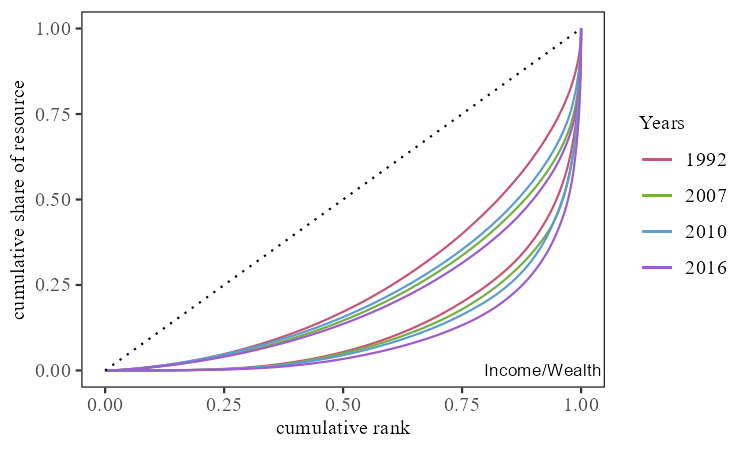

The data is sourced from the public version of the Survey of Consumer Finances (SCF) between the years 1989-2019. It is (normally) a triennial cross-sectional survey that collects micro-level data of U.S families including income, balance sheets, pensions, assets, debts, and expenditures. We combine all assets, including financial, in our wealth variable. The latter and the income variable observed in all waves of the survey between 1989 and 2019 form our data set. The survey over-samples higher income families who are likely to be wealthy. This is intended to counteract low survey response from high income and wealthy households. Consequently we estimate the vector quantile function for a weighted sample. Details of the sampling technique and a discussion of specific features and issues with the data set are given in appendix C. We refer to inequality in the marginal distribution of income as income inequality and inequality in the marginal distribution of wealth as wealth inequality. We refer to inequality displayed by -Lorenz curves as overall inequality. Figure 6 shows univariate Lorenz curves for income and for wealth for the years 1992, 2007, 2010 and 2016. Univariate inequality in both income and wealth is highest in 2016 and lowest in 1992. For the years 2007 and 2010 the evidence is mixed. The bend of the clusters of curves suggests wealth inequality is worse than income inequality across all years.

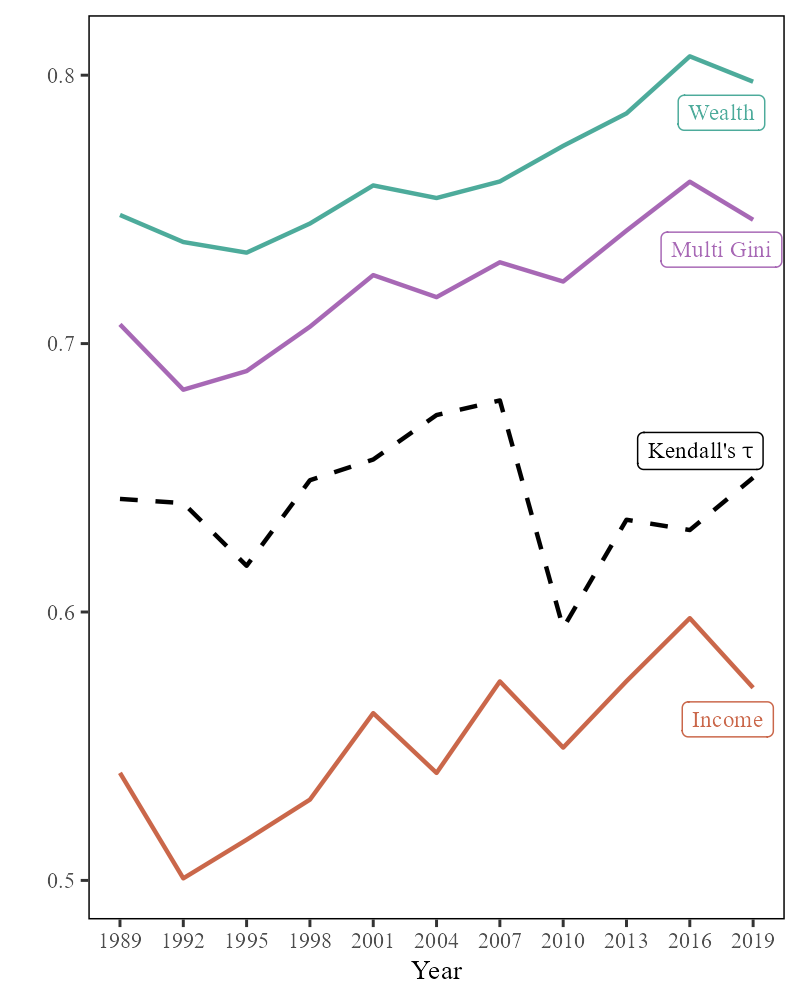

Figure 7 displays univariate Gini indices for income and for wealth, the multivariate Gini index, as well as Kendall’s for the dependence between income and wealth over time. Contrary to the inconclusive evidence from univariate Lorenz curves, the multivariate Gini shows improved overall inequality between 2007 to 2010. More specifically the decreased correlation and income inequality was sufficient to offset the rise in wealth inequality. As another example, in 1992 and 1995, the drop in wealth inequality and correlation is offset by the increased income inequality, apparently increasing the multivariate Gini.

4.3. Discussion of -Lorenz curves for the SCF data

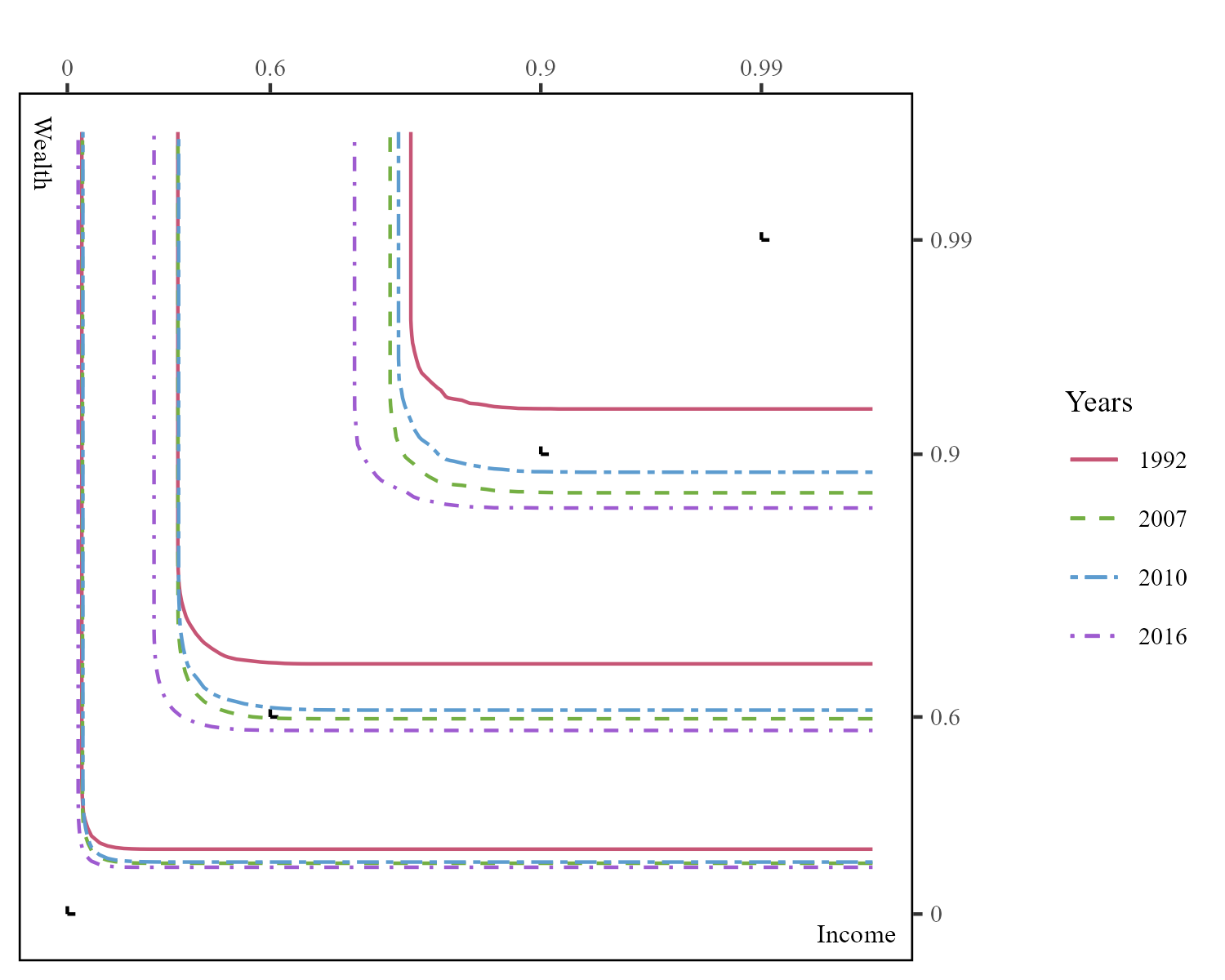

Figure 8 display the -, - and -Lorenz curves for the SCF data for the years 1992, 2007, 2010 and 2016 as well as the corresponding identical allocation curves. A common property for all clusters of curves is that they are disproportionately pulled towards the wealth axis and further away from the egalitarian curves indicating that wealth inequality is more pronounced than income inequality. For each year we see the effect on the curves of positive dependency through the curvature– the more curvature on the curve, the less positive dependence there is between the marginals. For example, for each -level the year 2016 has the most curvature and this intuition is supported by the Kendall’s in Figure 7 being the smallest value among these years.

Visually there is a departure from the univariate Lorenz curves inconclusiveness in comparing overall inequality between 2007 and 2010. The -Lorenz curves suggest that overall inequality was higher in 2007 than in 2010 since the curves of 2010 are further shifted to the north-east. Therefore we have some suggestive evidence that the income-wealth allocation of 2007 is more unequal in the weak Lorenz order than the allocation in 2010. Overall, the ranking looks consistent with .

Appendix A Additional Details and Results

A.1. Vector ranks and quantiles

Proposition 3 below, a seminal result in the theory of measure transportation, states essential uniqueness of the gradient of a convex function (hence cyclically monotone map) that pushes the uniform distribution on into the distribution of an allocation .

Proposition 3 (McCann 1995).

Let and be two distributions on . () If is absolutely continuous with respect to the Lebesgue measure on , with support contained in a convex set , the following statements hold: there exists a convex function such that . The function exists and is unique, -almost everywhere. () If, in addition, is absolutely continuous on with support contained in a convex set , the following holds: there exists a convex function such that . The function exists, is unique and equal to , -almost everywhere.

Proposition 3 is an extension of Brenier (1991) (see also Rachev and Rüschendorf (1990)). It removes the finite variance requirement, which is undesirable in our context. Proposition 3 is the basis for the definition of vector quantiles and ranks in Chernozhukov et al. (2017). In our context, it is applied with uniform reference measure.222This vector quantile notion was introduced in Galichon and Henry (2012) and Ekeland et al. (2012) and called -quantile.

In case , gradients of convex functions are nondecreasing functions, hence vector quantiles and ranks reduce to classical quantile and cumulative distribution functions. As the notation indicates, the function of proposition 3 is the convex conjugate of . In case of absolutely continuous distributions on with finite variance, the vector rank function solves a quadratic optimal transport problem, i.e., vector rank minimizes, among all functions such that is uniform on , the quantity , where .

Appendix B Properties of the Gini coefficient

The Gini index of definition 8 is in under assumption 1. It satisfies a set desirable properties for an inequality index. The first two are explained in the main text and repeated here:

Property G1 (Anonymity). The Gini index of allocation is a function of the distribution of .

Property G2 (Monotonicity). The Gini index is non decreasing in the Lorenz increasing inequality ordering. In other words, implies .

It also satisfies a multivariate extension of comonotonic independence proposed in Galichon and Henry (2012), as a generalization of the scalar requirement in Weymark (1981). Two scalar endowments and are comonotonic if they are both increasing transformations of the same uniform random variable on . Suppose and have respective cdfs and . Then and are comonotonic if they have the same ranks .

Now, in case of random vectors and , comonotonicity is defined in the same way by the fact that and have the same vector ranks. The following definition is due to Galichon and Henry (2012) and Ekeland et al. (2012), where it is called -comonotonicity333A related notion, namely -comonotonicity, was proposed by Puccetti and Scarsini (2010)..

Definition 10 (Vector comonotonicity).

Random vectors on are said to be comonotonic if there exists a uniform random vector on such that almost surely, where is the vector quantile of definition 1 associated with the distribution of , for each .

The following property states that mixing two equally comonotonic endowments with the same third endowment, comonotonic with the first two, does not change the inequality ordering.

Property G3 (Comonotonic Independence). If , and are comonotonic allocations, and , then, for all , .

The interpretation of property G3 is very compelling for an inequality index. If individuals are ranked identically in endowments and , and is more unequal than , then, adding to both and a third endowment cannot reverse the inequality ordering, if ranks individuals as and do.

We bring these statements together in the following lemma:

Proposition 4.

The Gini index of definition 8 satisfies properties G1 to G3.

Proposition 4 is not a characterization of our proposed Gini index, even when we extend the definition to allow for different weights given to the different resources. In other words, there may be other inequality indices that also satisfy properties G1–3.

Property G2 is the preservation of the multivariate majorization order we introduce, based on multivariate rearrangements. Our multivariate Gini index preserves this majorization order, but not the traditional multivariate majorization of Kolm (1977). An example of multivariate Gini that satisfies properties G1, G3 and preserves the multivariate majorization order of Kolm (1977) is , proposed in Galichon and Henry (2012), where the expectation is taken with respect to . However, is unsuitable as an inequality index in our context as can be seen with the following two observations. First, the following expression shows that only depends on , hence, on very specific features of the dependence between the two components and of allocation .

| (B.1) |

Second, and more troubling still, for any given fixed marginals for and , is maximized when the two components and of endowment are independent, which runs against the intuition that increased dependence can increase inequality444Note that we are considering inequality over outcomes, not welfare inequality. Hence, the point made in Atkinson and Bourguignon (1982), that increased correlation may decrease utilitarian welfare inequality when resources are complements, doesn’t apply here..

| (B.2) |

where and denote the classical scalar Gini index of components and respectively.

Appendix C Specific features and issues with the data source

We review some known issues with the data set that impact our analysis. See Hanna et al. (2018) more a more in-depth account.

C.1. Sampling strategy

The over sampling of high income and wealthy households is achieved by applying two distinct sampling techniques. The first sample is the core representative sample selected by a standard multi-stage area-probability design. The second is the high income supplement from statistical records derived from tax data by the Statistics of Income (SOI) division of the Internal Revenue Service of the U.S. The stages sample disproportionately– usually one-third of the final sample is from the high income supplement. Sampling in this way retains characteristic information of the population while also addressing the known selection biases of the wealthy not responding to surveys. In order to represent the population with this sample, weights must be constructed for each unit of observation. For more details on the construction of weights and their implications on the distribution of wealth, see Kennickell and Woodburn (1999).

C.2. Unit of observation and timing of interviews

The observations in this data set are not households, but rather a subset called the primary economic unit (PEU) that may be individuals or couples and their financial dependents. For example in the 2016 data set 13% of PEUs were in a household that contained one or more members not in their PEU. Additionally, the respondent is not necessarily the head of the household, so special care must be taken if analyzing attitudes in relation to some demographic characteristics such as age. The interviews start in May of the survey year, after most income taxes are filed and usually finish by the end of the calendar year, see Kennickell (2017b) for challenges at the end of the interview period. Questions also may change over time so it is important to review the codebook each year when making comparisons across time.

C.3. Multiple Imputation

During interviews, respondents may omit answers or provide a range of values for which their response belongs. This missing data impacts analysis and so the SCF contains 5 imputed values for each PEU, creating a sample 5 times larger than the actual number of respondents and forms 5 data sets called implicates. Imputation is done by the Federal Reserve Imputation Technique Zeta model (FRITZ), details can be found in Kennickell (2017a) based upon the ideas of Little and Rubin (2019). Multiple imputation for missing data provide multiple probable values. Each of these form a data set from which sample statistics can be found. The technique of Repeated Imputation Inference (RII) is applied in our analysis. For each implicate , the empirical ILF is calculated using the appropriate quantile map estimator taking into account sample weights. Then the repeated-imputation estimate of is

Calculation of the Gini index follows a similar procedure. Accounting for the multiple imputation in the calculation of standard errors is an important issue, but is not revelant to our visualization technique. For more information on multiple imputation and inference with imputed values, see Rubin (1996).

C.4. Computational issues

At times within the data, values can be repeated (e.g. many zeros), which have been found to pose issues calculating the quantile maps required for our Lorenz curves. Typically if this happens a few empty cells will be produced, which implies that the solution is invalid. A work-around for this is to introduce some noise to separate the data points. We added a random number between 0 and 10 for most implicates and added a random number between 0 and 200 to the data in 2007 and 2016. These numbers are too small to affect disparity when income and wealth are well over the tens of thousands in most of the stratum of the population so the visuals will not be influenced by this correction.

C.5. Definition of Wealth

In the literature, there is no consensus on what factors should be included in wealth measurement. Wolff (2021) defines wealth as marketable weath, which is the sum of marketable or fungible assets less the current value of all debts. Bricker et al. (2017) define wealth as net worth including those assets which are not readily transformed into consumption: properties, vehicles, etc. In our analysis we consider all assets, including financial, as our wealth variable.

Appendix D Proofs of results in the main text

In this section, we omit the subscript of for notational compactness.

D.1. Proofs for section 1.3

Proof of property 1.

The off diagonal elements of the Jacobian of are and . From the latter, by differentiation, we can recover . The result then follows from the fact that characterizes , see for instance Chernozhukov et al. (2017). ∎

Proof of lemma 1.

Let . Let , . Then is distributed identically to . Since is monotonically increasing in , we have . Hence

Under the stated assumption, is increasing in and . Since , we have

where denotes the cumulative distribution function of conditional on . Now is increasing in , since

Similarly is increasing in . We conclude that , see e.g. Joe (1997). ∎

Proof of property 3.

We only need to show for one component of the Lorenz map and the second follows with similar reasoning. We have for the first component

Now define . is monotone increasing by assumption, so is convex. Therefore, . Note that as an integral over a degenerate interval, and , as this is the mean of the normalized . So and so , as desired. ∎

D.2. Proofs for section 2

Proof of proposition 1.

is equivalent to first order stochastic dominance of over , where (see Section 6.B page 266 of Shaked and Shanthikumar (2007)). Hence, implies for any lower set , so that implies , given that the sets are lower sets. ∎

Proof of lemma 2.

Suppose is an MMPS of , so that there is an ultramodular function , such that (2.1) holds, with (since by assumption). We want to see if , i.e., . Consider the first component:

by convexity. We then show that

for all . Since , the latter holds if is convex, i.e., if

which holds by supermodularity of . A similar reasoning applies to the second component and the result follows. ∎

Proof of proposition 4.

Property G1 is automatically satisfied since is defined as a function of the allocation’s distribution. Property G2 follows immediately from equation 2.6. We now show that Property G3 is satisfied. Take . Let , and be comonotonic according to definition 10, and assume , i.e., . We have

where the second and last equalities hold by lemma 4. The result follows. ∎

Lemma 4 (Galichon and Henry (2012)).

If and with respective vector quantiles and are comonotonic, then, for any , the vector quantile of is .

Proof of (B.1).

Let be uniformly distributed on . Note that

Now,

where the last equality follows from interchangeability of the order of integration and is the first component of the Lorenz map.

Note that

and

Therefore

Similarly, we have , as desired. ∎

Proof of (B.2).

because and . The second inequality follows from and . We now prove the latter. Letting be the vector quantile function of , note that since pushes uniform measure on forward to law, we can write

where is the quantile of the random variable . Note that the area of the domain of integration must be . On the other hand,

is an integral of the same function over a region with the same area. Writing , we have , where and and the union is disjoint. Similarly, where . Note that the areas of and must be the same, , and throughout while throughout . We have

Note that this inequality holds for any dependence structure between and . ∎

Lemma 5.

For non negative bivariate random vectors with , we have

where .

Proof of lemma 5.

This is seen by applying integration by parts a few times. Start with

Then

and

Combining these,

It is a similar line of reasoning for the second component. ∎

D.3. Proofs for section 3

Proof of proposition 2.

The potential of an egalitarian allocation satisfies . Solutions are of the form

Convexity of implies convexity of . The normalization

implies

The latter, in turn, implies

Call the cdf of , where . Call the cdf of , which is the first marginal of allocation . Then

Now

Hence

as desired. ∎

Lemma 6 (Explicit formula for ).

The cumulative distribution function of with is given by the following.

Proof of lemma 3.

A sufficient condition for assumption 2 is

If we choose the optimal value of , i.e.,

we get the sufficient inequality

as desired. ∎

Proof of example 1.

Let , with convex and twice continuously differentiable, and ultramodular. We have, for

Also,

Therefore

∎

Proof of “property 3 continued”.

Define

Under assumption 2,

Hence is an ultramodular function. Applying the proof of property 3, we find that for all ,

Hence

where as desired.

We now show that egalitarian allocations do not dominate each other. Suppose an egalitarian allocation with potential dominates an allocation with potential . Then

Hence, for all ,

so that both allocations have the same Lorenz map, hence are equally distributed. ∎

References

- Aaberge and Brandolini [2014] R. Aaberge and A. Brandolini. Multidimensional poverty and inequality. Discussion Papers, No. 792, Statistics Norway, Research Department, Oslo, 2014.

- Andreoli and Zoli [2020] F. Andreoli and C. Zoli. From unidimensional to multidimensional inequality: a review. Metron, 78:5–42, 2020.

- Arnold [2008] B. Arnold. The Lorenz curve: Evergreen after 110 years. In Advances on Income Inequality and Concentration Measures. Routledge, 2008.

- Arnold [1983] B. C. Arnold. Pareto Distributions. International Co-operative Publishing House, 1983.

- Arnold and Sarabia [2018] B. C. Arnold and J. M. Sarabia. Majorization and the Lorenz order with applications in applied mathematics and economics. Springer, 2018.

- Atkinson and Bourguignon [1982] A. Atkinson and F. Bourguignon. The comparison of multi-dimensioned distributions of economic status. Review of Economic Studies, 49:183–201, 1982.

- Aurenhammer [1987] F. Aurenhammer. Power diagrams: properties, algorithms and applications. SIAM Journal on Computing, 16:78–96, 1987.

- Aurenhammer et al. [1998] F. Aurenhammer, F. Hoffmann, and B. Aronov. Minkowski-type theorems and least-squares clustering. Algorithmica, 20:61–76, 1998.

- Banerjee [2010] A. Banerjee. Multidimensional Gini index. Mathematical Social Sciences, 60:87–93, 2010.

- Banerjee [2016] A. Banerjee. Multidimensional Lorenz dominance: a definition and an example. Keio Economic Studies, 52:65–80, 2016.

- Bickel and Lehmann [1976] P. Bickel and E. Lehmann. Descriptive statistics for nonparametric models, iii. dispersion. Annals of Statistics, 4:1139–1158, 1976.

- Bonhomme and Robin [2009] S. Bonhomme and J.-M. Robin. Assessing the equalizing force of mobility using short panels: France, 1990–2000. Review of Economic Studies, 76:63–92, 2009.

- Brenier [1991] Y. Brenier. Polar factorization and monotone rearrangement of vector‐valued functions. Communications on Pure and Applied Mathematics, 4:375–417, 1991.

- Bricker et al. [2017] J. Bricker, L. J. Dettling, A. Henriques, J. W. Hsu, L. Jacobs, K. B. Moore, S. Pack, J. Sabelhaus, J. Thompson, and R. A. Windle. Changes in US family finances from 2013 to 2016: Evidence from the survey of consumer finances. Fed. Res. Bull., 103:1, 2017.

- Brock and Thomson [1966] W. Brock and R. Thomson. Convex solutions of implicit relations. Mathematics Magazine, 39:208–111, 1966.

- Charpentier et al. [2016] A. Charpentier, A. Galichon, and M. Henry. Local utility and multivariate risk aversion. Mathematics of Operations Research, 41:266–276, 2016.

- Chernozhukov et al. [2017] V. Chernozhukov, A. Galichon, M. Hallin, and M. Henry. Monge-Kantorovich depth, quantiles, ranks and signs. Annals of Statistics, 45:223–256, 2017.

- Decancq and Lugo [2012] K. Decancq and M. Lugo. Inequality of wellbeing: A multidimensional approach. Economica, 79:721–746, 2012.

- Ekeland et al. [2012] I. Ekeland, A. Galichon, and M. Henry. Comonotone measures of multivariate risks. Mathematical Finance, 22:109–132, 2012.

- Fisher [1956] F. Fisher. Income distribution, value judgments and welfare. Quarterly Journal of Economics, 70:380–424, 1956.

- Gajdos and Weymark [2005] T. Gajdos and J. Weymark. Multidimensional generalized Gini indices. Economic Theory, 26:471–496, 2005.

- Galichon and Henry [2012] A. Galichon and M. Henry. Dual theory of choice under multivariate risks. Journal of Economic Theory, 147:1501–1516, 2012.

- Gastwirth [1971] J. L. Gastwirth. A general definition of the Lorenz curve. Econometrica, 39:1037–1039, 1971.

- Grothe et al. [2021] O. Grothe, F. Kächele, and F. Schmid. A multivariate extension of the Lorenz curve based on copulas and a related multivariate gini coefficient. arXiv preprint arXiv:2101.04748, 2021.

- Hallin and Mordant [2022] M. Hallin and G. Mordant. Center-outward multiple-output lorenz curves and gini indices a measure transportation approach. Unpublished manuscript, 2022.

- Hanna et al. [2018] S. D. Hanna, K. T. Kim, and S. Lindamood. Behind the numbers: Understanding the survey of consumer finances. Journal of Financial Counseling and Planning, 29:410–418, 2018.

- Hardy et al. [1934] G. Hardy, J. Littlewood, and G. Pólya. Inequalities. Cambridge University Press, 1934.

- Joe [1997] H. Joe. Multivariate Models and Multivariate Dependence Concepts. Chapman and Hall, 1997.

- Kennickell [2017a] A. Kennickell. Multiple imputation in the survey of consumer finances. Statistical Journal of the IAOS, 33:143–151, 2017a.

- Kennickell [2017b] A. B. Kennickell. The bitter end? the close of the 2007 SCF field period. Statistical Journal of the IAOS, 33:93–99, 2017b.

- Kennickell and Woodburn [1999] A. B. Kennickell and R. L. Woodburn. Consistent weight design for the 1989, 1992 and 1995 SCFs, and the distribution of wealth. Review of Income and Wealth, 45:193–215, 1999.

- Kitagawa et al. [2019] J. Kitagawa, Q. Mérigot, and B. Thibert. Convergence of a newton algorithm for semi-discrete optimal transport. Journal of the European Mathematical Society, 21:2603–2651, 2019.

- Kolm [1977] S.-C. Kolm. Multidimensional egalitarianisms. The Quarterly Journal of Economics, 91:1–13, 1977.

- Koshevoy [1995] G. Koshevoy. Multivariate Lorenz majorization. Social Choice and Welfare, 12:93–102, 1995.

- Koshevoy and Mosler [1996] G. Koshevoy and K. Mosler. The Lorenz zonoid of a multivariate distribution. Journal of the American Statistical Association, 91:873–882, 1996.

- Koshevoy and Mosler [1997] G. Koshevoy and K. Mosler. Multivariate Gini indices. Journal of Multivariate Analysis, 60:252–276, 1997.

- Koshevoy and Mosler [1999] G. Koshevoy and K. Mosler. Price majorization and the inverse Lorenz function. Discussion Papers in Statistics and Econometrics 3/99, University of Cologne, 1999.

- Koshevoy and Mosler [2007] G. Koshevoy and K. Mosler. Multivariate Lorenz dominance based on zonoids. AStA, 91:57–76, 2007.

- Lehmann [1966] E. L. Lehmann. Some concepts of dependence. The Annals of Mathematical Statistics, 37:1137–1153, 1966.

- Lévy [2015] B. Lévy. A numerical algorithm for L2 semi-discrete optimal transport in 3D. ESAIM: Mathematical Modelling and Numerical Analysis, 49:1693–1715, 2015.

- Little and Rubin [2019] R. J. Little and D. B. Rubin. Statistical analysis with missing data, volume 793. John Wiley & Sons, 2019.

- Lorenz [1905] M. Lorenz. Methods of measuring the concentration of wealth. Publication of the American Statistical Association, 9:209–219, 1905.

- Marinacci and Montrucchio [2005] M. Marinacci and L. Montrucchio. Ultramodular functions. Mathematics of Operations Research, 30:311–332, 2005.

- Marshall et al. [2011] A. W. Marshall, I. Olkin, and B. C. Arnold. Inequalities: Theory of Majorization and Its Applications. Springer, 2nd edition, 2011.

- McCann [1995] R. J. McCann. Existence and uniqueness of monotone measure-preserving maps. Duke Mathematical Journal, 80:309–323, 1995.

- Mérigot [2011] Q. Mérigot. A multiscale approach to optimal transport. Computer Graphics Forum, 30:1583–1592, 2011.

- Mosler [2013] K. Mosler. Representative endowments and uniform Gini orderings of multi-attribute inequality. arXiv preprint arXiv:2103.17030, 2013.

- Müller and Scarsini [2012] A. Müller and M. Scarsini. Fear of loss, inframodularity, and transfers. Journal of Economic Theory, 147:1490–1500, 2012.

- Müller and Stoyan [2002] A. Müller and D. Stoyan. Comparison Methods for Stochastic Models and Risks. Wiley, 2002.

- Puccetti and Scarsini [2010] G. Puccetti and M. Scarsini. Multivariate comonotonicity. Journal of Multivariate Analysis, 101:291–304, 2010.

- Quiggin [1992] J. Quiggin. Increasing risk: another definition. In A. Chikan, editor, Progress in Decision, Utility and Risk Theory, pages 239–248. Kluwer: Dordrecht, 1992.

- Rachev and Rüschendorf [1990] S. Rachev and L. Rüschendorf. A characterization of random variables with minimal L2 distance. Journal of Multivariate Analysis, 32:48–54, 1990.

- Rubin [1996] D. B. Rubin. Multiple imputation after 18+ years. Journal of the American Statistical Association, 91:473–489, 1996.

- Sarabia and Jorda [2014] J.-M. Sarabia and V. Jorda. Bivariate Lorenz curves: a review of recent proposals. In XXII Jornadas de ASEPUMA, 2014.

- Sarabia and Jorda [2020] J.-M. Sarabia and V. Jorda. Lorenz surfaces based on the Sarmanov–Lee distribution with applications to multidimensional inequality in well-being. Mathematics, 8:1–17, 2020.

- Shaked and Shanthikumar [2007] M. Shaked and J. G. Shanthikumar. Stochastic orders. Springer, 2007.

- Taguchi [1972a] T. Taguchi. On the two-dimensional concentration surface and extensions of concentration coefficient and Pareto distribution to the two-dimensional case-i. Annals of the Institute of Statistical Mathematics, 24:355–382, 1972a.

- Taguchi [1972b] T. Taguchi. On the two-dimensional concentration surface and extensions of concentration coefficient and Pareto distribution to the two-dimensional case-ii. Annals of the Institute of Statistical Mathematics, 24:599–619, 1972b.

- Villani [2003] C. Villani. Topics in Optimal Tranportation. American Mathematical Society, 2003.

- Villani [2009] C. Villani. Optimal Transport: Old and New. Springer, 2009.

- Weymark [1981] J. Weymark. Generalized Gini inequality indices. Mathematical Social Sciences, 1:409–430, 1981.

- Wolff [2021] E. N. Wolff. Household wealth trends in the United States, 1962 to 2019: Median wealth rebounds… but not enough. Working paper, National Bureau of Economic Research, 2021.