Predicting Value at Risk for Cryptocurrencies With Generalized Random Forests

Abstract

We study the prediction of Value at Risk (VaR) for cryptocurrencies. In contrast to classic assets, returns of cryptocurrencies are often highly volatile and characterized by large fluctuations around single events. Analyzing a comprehensive set of 105 major cryptocurrencies, we show that Generalized Random Forests (GRF) (Athey et al., 2019) adapted to quantile prediction have superior performance over other established methods such as quantile regression, GARCH-type and CAViaR models. This advantage is especially pronounced in unstable times and for classes of highly-volatile cryptocurrencies. Furthermore, we identify important predictors during such times and show their influence on forecasting over time. Moreover, a comprehensive simulation study also indicates that the GRF methodology is at least on par with existing methods in VaR predictions for standard types of financial returns and clearly superior in the cryptocurrency setup.

Keywords: Generalized Random Forests, Value at Risk, Quantile Prediction, Backtesting, Cryptocurrencies, Conditional Predictive Ability.

JEL Classification: C58,G17,C22

1 Introduction

Cryptocurrencies are an important and rising part of today’s digital economy. Currently, the market capitalization of the top 10 cryptocurrencies in the world is close to $2 trillion and growing111See e.g. https://coinmarketcap.com/charts/; accessed at 22nd March 2022.. The use of cryptocurrencies in terms of daily volume exploded from 2016 to 2018††footnotemark: , which not only attracts individuals but also business users such as hedge funds or merchants as well as long-term investors such as crypto-focused and traditional investment funds (Vigliotti and Jones, 2020). The crypto asset market, however, remains highly volatile where e.g. an investment in Bitcoin in 2013 would have seen a return of roughly in 2017, but an investment in 2017 would have led to a performance of -75% in 2019††footnotemark: . Consequently, there is a need to predict and monitor the risks associated with cryptocurrencies. To address this, we find that classic approaches such as historical simulation, GARCH-type, or CaViaR methods are too restrictive. More general non-linear methods provide more flexibility to account for such non-standard time series behaviour that might be attributed to a large extend to speculators.

In this paper, we propose a novel flexible way for out-of-sample prediction of the Value at Risk for cryptocurrencies. We use a quantile version of Generalized Random Forests (GRF, see Athey et al., 2019), which builds upon mean random forests (Breiman, 2001) now tailored to quantiles. This framework shows to be especially promising when dealing with more volatile classes of cryptocurrencies due to the non-linear structure of their returns. In a comprehensive out-of-sample scenario using more than 100 of the largest cryptocurrencies, GRF outperforms other established methods such as CAViaR (Engle and Manganelli, 2004), quantile regression (Koenker and Hallock, 2001) or GARCH-models (Bollerslev, 1986; Glosten et al., 1993) over a rolling window, particularly in unstable times. This can be attributed to the non-parametric approach of random forests that is flexible and adaptable considering important factors and non-linearity. We further analyze performance in different important subperiods, consider different classes of cryptocurrencies, and employ different sets of covariates with the forest-based methods and the benchmark procedures.

Previous studies have confirmed that there exist speculative bubbles (Cheah and Fry, 2015; Hafner, 2020), and we find that our approach assesses risks especially well during such times. Moreover, we account for a large number of covariates that describe volatility, liquidity, and supply (Liu and Tsyvinski, 2020). It can be seen that variable importance differs substantially depending on time, where long-term measures of standard deviation, that are an important predictor in stable times, are not relevant predictors for VaR in unstable, volatile times. Furthermore, only few of the additional covariates beside lagged standard deviations and lagged returns are relevant. We find that for other, less volatile classes of cryptocurrencies such as stablecoins, especially GJR-GARCH models and quantile regression can compete with GRF. A simulation study also highlights that the proposed GRF methodology is at least on par in prediction of VaR also for standard-type financial returns with clear advantages in the crypto-currency type case.

Our paper contributes to the growing literature on cryptocurrencies. Analyses performed in the past include GARCH models (Chu et al., 2017) as well as ARMA-GARCH models (Platanakis and Urquhart, 2019), approaches using RiskMetrics (Pafka and Kondor, 2001) and GAS-models (Liu et al., 2020), application of extreme value theory (Gkillas and Katsiampa, 2018), vine copula-based approaches (Trucios et al., 2020), Markov-Switching GARCH models (Maciel, 2020), non-causal autoregressive models (Hencic and Gouriéroux, 2015) and also some machine learning-based approaches (see e.g. Takeda and Sugiyama, 2008). Additionally, cryptocurrencies can be used for diversification in investment strategies with other, traditional assets (see e.g. Trimborn et al., 2020; Petukhina et al., 2021), as the correlation between them and more established assets tends to be low (Elendner et al., 2017; Platanakis and Urquhart, 2019). This again poses the question of assessing the risks of cryptocurrencies, where new methods of addressing the above mentioned challenges need to be explored.

The paper is structured as follows. Section 2 presents the underlying data and cryptocurrencies with descriptive statistics and standard Box-Jenkins time-series checks. In Section 3, we introduce the main random forest-type techniques for conditional quantiles and present the employed evaluation tests and framework. The comprehensive simulation study in Section 4 demonstrates the performance of the different methods under various data generating processes. The empirical results are contained in Section 5, where we present aggregate prediction results for all currencies in coverage performance (Section 5.1.1) as well as in pairwise comparison tests (Section 5.1.2). In Section 5.2, we analyze representative important currencies in detail and study the importance of specific factors. Finally, we conclude in Section 6.

2 Data

We use daily log-returns of 105 of the largest cryptocurrencies222The data was obtained on 23rd March 2022 from https://docs.coinmetrics.io/ using the community data set, which can be downloaded from a public Github repository at https://github.com/coinmetrics/data/. from coinmetrics by market capitalization333All currencies have a maximum market capitalization of more than 15 million USD each. in US-Dollar (USD) at time of retrieval, in the period from 07/2010 to 03/2022. The coinmetrics data includes spot-market information from 30 different exchanges, such as Binance, ZB.COM, FTX, OKX, Coinbase, KuCoin, or Kraken444See https://docs.coinmetrics.io/exchanges/all-exchanges for an overview of all exchanges included.. Depending on the currency (i.e. the first trade date on the exchanges), the number of available observations varies between 261 and 4264. The data is summarized in Table 1. We see that there are some very negative and positive returns in the data, as well as high excess-kurtosis confirming the observations in the depicted quantiles. Furthermore, there are some assets with a high skewness, both positive and negative, indicating asymmetry in the distribution of returns.

We do not detect any stochastic non-stationarities in the data, which is supported by Augmented Dickey-Fuller (ADF) tests and Kwiatkowski-Phillips-Schmidt-Shin (KPSS) tests (Kwiatkowski et al., 1992). With Alpha Finance Lab (alpha), Polymath (poly), and Synthetix (snx), KPSS tests against level stationarity seem slightly significant, while trend KPSS tests and ADF tests suggest stationarity. With Algorand (algo), Binance Coin (bnb), Curve DAO Token (crv), FTX Token (ftt), Internet Computer (icp), Aave (lend), OMG Network (omg), SushiSwap (sushi), and Monero (xmr), KPSS tests against trend stationarity are slightly significant, while ADF tests and level KPSS tests again suggest stationarity. All results of the stationarity tests can be found in Table 10 in the appendix.

| Min | 1% | 5% | Median | 95% | 99% | Max | Skewness | Excess-Kurtosis | Standard Deviation | Observations | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Min% | -1.264 | -0.308 | -0.168 | -0.006 | 0.001 | 0.002 | 0.006 | -3.556 | 1.671 | 0.001 | 261.000 |

| 1% | -1.120 | -0.268 | -0.158 | -0.006 | 0.001 | 0.002 | 0.006 | -2.691 | 1.965 | 0.001 | 314.960 |

| 5% | -0.830 | -0.243 | -0.139 | -0.004 | 0.002 | 0.006 | 0.016 | -1.195 | 3.043 | 0.002 | 526.200 |

| 25% | -0.576 | -0.199 | -0.114 | -0.001 | 0.089 | 0.170 | 0.342 | -0.190 | 6.482 | 0.060 | 717.000 |

| 50% | -0.492 | -0.181 | -0.104 | 0.000 | 0.109 | 0.209 | 0.461 | 0.298 | 10.708 | 0.073 | 1354.000 |

| 75% | -0.362 | -0.160 | -0.086 | 0.001 | 0.120 | 0.239 | 0.704 | 1.030 | 23.164 | 0.080 | 1669.000 |

| 95% | -0.022 | -0.006 | -0.002 | 0.002 | 0.153 | 0.318 | 1.258 | 2.241 | 75.697 | 0.101 | 2851.800 |

| 99% | -0.006 | -0.002 | -0.001 | 0.003 | 0.197 | 0.412 | 1.431 | 3.472 | 160.129 | 0.117 | 3264.120 |

| Max% | -0.005 | -0.002 | -0.001 | 0.003 | 0.201 | 0.539 | 1.462 | 3.753 | 216.567 | 0.136 | 4264.000 |

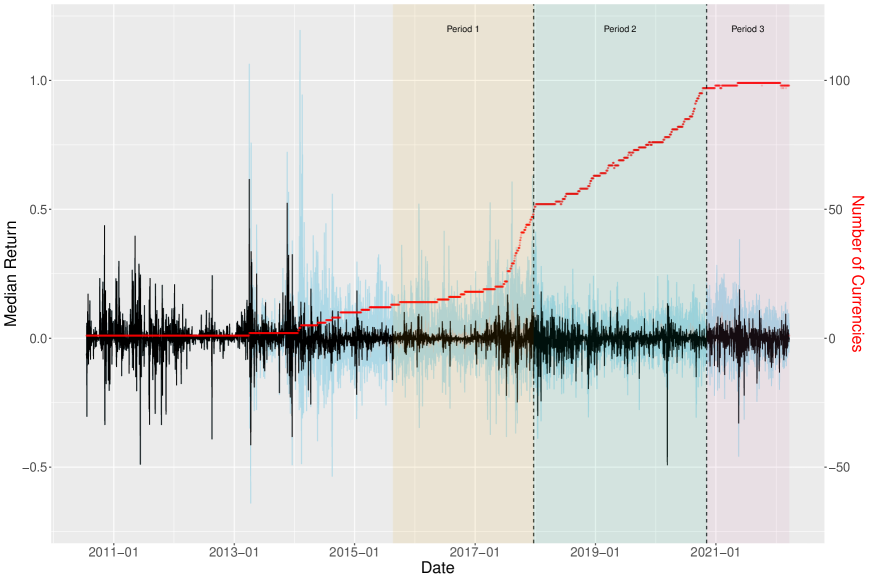

For the cryptocurrencies, Figure 1 illustrates the median returns (black) over all cryptocurrencies by date. We can see that in the beginning of the time period, only one currency, namely Bitcoin, was present in the data set. From 2014, we see an incremental increase (red line), while there is a jump up in 2017 and an consecutively faster increase in available cryptocurrencies. We also see that the returns are very different between currencies from 2014 to 2018 (blue), which marks a period of hype leading to a crash in the beginning of 2018. Later, there are large negative spikes corresponding to the many waves of the Covid-19 pandemic. Based on these observations, we divide our data into three periods. The first period ranges from August 2015 (2015-08-22) to the end of 2017 (2017-12-21), while the second period subsequently lasts until November 2020 (2020-11-05). The last period then covers the rest of our data (until 2022-03-20)555The specific dates account for the training periods of currencies and creation of new assets to make sure that we capture a maximum number of cryptocurrencies in each time period..

Since we are in a time series setup, we include classic covariates based on lagged return in our analysis. Additionally, we employ information specific to each cryptocurrency in 7 external covariates. The five time-series based covariates consist of the one-day lagged return and the lagged 3,7,30, and 60 day return standard deviation. The external covariates are the number of unique active daily addresses (Active_Users), the number of unique addresses that hold any amount of native units of that currency or at least 10 or 100 USD equivalent (Total_Users, Total_Users_USD10,Total_Users_USD100), the supply equality ratio (SER), i.e. the ratio of supply held by addresses with less than of the current supply to the top 1% of addresses with the highest current supply, the number of initiated transactions (Transactions), and the velocity of supply in the current year (Velocity), which describes the the ratio of current supply to the sum of the value transferred in the last year. See also Table 12 in the appendix for details on the covariates.

| Quantile | Ret | Active_Users | Total_Users | Total_Users_USD100 | Total_Users_USD10 | SER | Transactions | Velocity | sd_3 | sd_7 | sd_30 | sd_60 | CapMrktCurMUSD |

| Period 1: 5 Currencies | |||||||||||||

| 5% | -0.094 | 7691 | 233361 | 7768 | 32688 | 0.001 | 3304 | 9.321 | 0.007 | 0.014 | 0.022 | 0.026 | 17 |

| Median | -0.001 | 127679 | 2579591 | 297029 | 615602 | 0.013 | 49170 | 33.708 | 0.036 | 0.044 | 0.051 | 0.055 | 2611 |

| 95% | 0.104 | 324662 | 9697275 | 3562101 | 5930594 | 0.031 | 110698 | 109.281 | 0.137 | 0.134 | 0.123 | 0.124 | 185407 |

| Period 2: 15 Currencies | |||||||||||||

| 5% | -0.085 | 3592 | 95320 | 5271 | 16960 | 0.001 | 16618 | 4.668 | 0.008 | 0.015 | 0.024 | 0.027 | 70 |

| Median | -0.001 | 66921 | 2629309 | 233835 | 540993 | 0.008 | 128481 | 16.244 | 0.034 | 0.041 | 0.047 | 0.049 | 5008 |

| 95% | 0.094 | 179852 | 8601014 | 2135275 | 4469914 | 0.018 | 655221 | 67.849 | 0.122 | 0.119 | 0.111 | 0.109 | 99979 |

| Period 3: 77 Currencies | |||||||||||||

| 5% | -0.082 | 2138 | 533215 | 15647 | 41396 | 0.002 | 25250 | 5.255 | 0.008 | 0.017 | 0.026 | 0.030 | 233 |

| Median | -0.000 | 19371 | 1218761 | 80236 | 215034 | 0.007 | 137082 | 15.325 | 0.035 | 0.041 | 0.047 | 0.049 | 1794 |

| 95% | 0.086 | 76081 | 2793940 | 565048 | 1195791 | 0.012 | 424953 | 53.743 | 0.111 | 0.105 | 0.101 | 0.096 | 26105 |

| Full Data: 105 Currencies | |||||||||||||

| 5% | -0.089 | 1857 | 559862 | 16964 | 44887 | 0.002 | 19135 | 5.626 | 0.009 | 0.019 | 0.028 | 0.033 | 461 |

| Median | -0.000 | 15406 | 1095198 | 72651 | 186751 | 0.006 | 106286 | 14.371 | 0.038 | 0.045 | 0.051 | 0.054 | 2367 |

| 95% | 0.095 | 62448 | 2389786 | 434200 | 917576 | 0.010 | 339294 | 44.627 | 0.120 | 0.113 | 0.108 | 0.102 | 21085 |

Table 2 gives an overview of the employed covariates and their values in the different time periods. We can see that in Period 1, we have the most extreme returns on average as well as the most extreme lagged standard deviations. This is not surprising looking at the first period (853 days), which arguably marks the most volatile period, with many new currencies being created, as well as the second longest period. In the following period (1050 days), the average median market cap reaches a high as well as the number of users invested in the currencies, indicating that the market is growing while stabilizing more. This is followed by a sharp drop in the market cap for the last, shortest period (500 days), which starts at the beginning of the Covid-19 pandemic. There, the number of active users as well as the SER decreases, indicating that more smaller addresses are pushed off the market, while it is the period with the most currencies.

Given this hugely dynamic cryptocurrency market evolution we distinguish between the three systematically different periods in terms of actively traded currencies and market capitalization. The first one is characterized by a few, rapidly changing currencies and extreme returns and volatilities, while the second period is less extreme and more characterized by a strong increase in median market caps with a few dozens of market components. The third period, in the end, is very short but contains more than five times the number of currencies in comparison to the second period.

3 Methodology

For the prediction of cryptocurrencies, we advocate the use of non-linear machine learning based techniques. In this way, we intend to accommodate the documented large share of speculation (Ghysels and Nguyen, 2019; Baur et al., 2018; Selmi et al., 2018; Glaser et al., 2014) and resulting frequent changes in unconditional volatility which make predictions in this market peculiar. In particular, we focus on generalized random forest methods that are tailored for conditional quantiles of returns and thus allow to forecast the VaR. The flexible but interpretable non-linearity of the approach allows for a direct comparison to standard linear and (G)ARCH-type models. We also argue that the difference in forecasting performance can moreover be employed to detect periods of bubbles and extensive speculation.

Recall that for daily log returns the at level conditional on some covariates is defined as

| (1) |

where marks the distribution of conditional on . Generally, the conditioning variables could consist of past lagged returns, standard deviations, but also of external (market) information or other assets. We employ these as covariates that are explained in Section 2.

We propose the use of two different types of random forest-based techniques which directly model the conditional VaR in (1). Both build on the classic random forest (Breiman, 2001) which is an ensemble of (decorrelated) decision trees (see e.g. Hastie et al., 2009) for the mean of . In a decision tree, each outcome is sorted into leafs of the tree by binary splits. These splits are performed based on different components falling above or below specific adaptive threshold values that need to be calculated, for example by the Gini Impurity or MSE-splitting in Classification and Regression Trees (CART) (Breiman et al., 1984), or using other criteria. Finally, the prediction for a new is a weighted version of each tree prediction.

In the proposed method that we employ, the generalized random forest (GRF) from on Athey et al. (2019), the random forest split criterion is adapted to mimic the task of quantile regression rather than minimizing a standard mean squared loss criterion for mean regression tasks. Intuitively, the splits in each leaf are conducted by minimizing the Gini-loss, which separates the returns as best as possible at different quantiles. To transform the minimizing problem in the splits into a classification task, the response variable is transformed in each split to obtain pseudo-outcomes , where describe a set of pilot-quantiles of in the parent node. These quantiles with levels are then used to calibrate the split666We use the tuning parameters and , i.e. the level of VaR we are analyzing, in this classification pre-step.. In Athey et al. (2019), this is formally motivated by moment conditions and gradient approximations, but practically, is relabeled to a nominal scale depending on the largest quantile it does not exceed. In a final step, the optimal split on a variable component of and observations in the parent node is then based on minimizing the above-mentioned Gini impurity criterion for classification. For a separation into two possible leaf sets , the Gini impurity for one leaf is , where is the proportion of in group with value . The full loss is then an average weighted by leaf size, yielding

| (2) |

We choose the Gini-loss since it is fast and, for certain configurations, produces purer nodes than for example using entropy as a splitting criterion (see e.g Breiman, 1996). This can be particularly helpful when dealing with changing variance (and thus time-varying quantiles) of returns, where we would like to detect single extreme events. For our specific case of , this implies that values larger than in the parent node are given the value , while others are . Algorithm 1 briefly summarizes the tree building algorithm from Athey et al. (2019) for the quantile version of GRF, where the main differences with regard to the splitting regime in comparison to a classic CART occur in every step the tree is grown.

In addition to that, the outcome that is predicted is not the mean but the -quantile (i.e. ), which is done in a way that you do not calculate a weighted average of but a weighted average of the empirical CDF . Intuitively, log returns that have similar in comparison to a new observation receive higher weight in the empirical CDF. Similarity weights are measured as the relative frequency on how often falls in the same terminal leaf as , for , and averaged over all trees for each . This last step was originally introduced by Meinshausen (2006) for random forests.

As a benchmark, we employ the quantile regression forest (QRF) based on Meinshausen (2006). This random forest, however, uses the same splitting regime as the original CART random forest and therefore does not account explicitly for situations where the variance and therefore the quantile changes, as splits are conducted based on a mean-squared error criterion. Since such volatility changes are to be expected for cryptocurrencies in our data, we expect GRF to perform better than QRF, but still include both in the analysis to see potential differences in predictions. Furthermore, GRF uses so-called “honest” trees, meaning that different data (usually the subsampled data for each tree is split again in half) is used for building and “filling” each of the trees with values.

As benchmarks we further include two types of standard time series methods. We use the CAViaR (CAV) methodology by Engle and Manganelli (2004) and standard quantile regression (Koenker and Hallock, 2001). Both make use of quantile regression (QR) techniques (Koenker and Bassett, 1978) that do not minimize the squared error as in ordinary regression, but use the check function to minimize . For CAV, we use a symmetric absolute value (SAV) component for , i.e , and for the quantile regression. In contrast to the former methods, they can only capture parametric (non)-linear effects which limits their flexibility.

For comparison, we use a GJR-GARCH(1,1) model (Glosten et al., 1993), a GARCH(1,1) (Bollerslev, 1986) model, a simple historical simulation (Hist), meaning that we predict at level as the sample -quantile of the preceding returns in a window of length , i.e. , and one that fits a normal distribution to the sample data and uses the theoretical fitted -quantile as the prediction for (NormFit). We do not expect the latter to perform well as we have high skewness and excess-kurtosis in the data (see Table 1 in Section 2).

For the proposed random forest-type and all benchmark procedures that allow for additional covariates (GRF, QRF, QR) we include lagged standard deviations (SD) in addition to the lagged level in the model. We expect these to capture the strongly varying levels of unconditional volatility in particular for the cryptocurrencies in the non-linear structure. Additionally, we also employ the above methods and the GARCH(1,1) model using both the latter covariates as well as the 7 external covariates described in Section 2. These methods are GRF-X, QRF-X, QR-X, and GARCH-X. To establish a fair common ground in used model complexity for the QR, QRF, GARCH-X, and GRF, we select a common set of different SD lags as covariates from an additional Monte-Carlo study. In this, we use the simple SAV-model from Section 4 as a baseline of which the respective specification is tailored to regime changes in the unconditional volatilities as observed form the cryptocurrencies. The model is essentially linear autoregressive of order 1 in the VaR and thus directly yields the VaR as outputs. With this, it is possible to use a MSE-minimizing criterion and select the MSE-minimizing variables for the subsequent simulations and data analysis. Table 3 summarizes the results of this short simulation study, which is why we use 3, 7, 30, and 60 day lagged SD as covariates.

| Lagged SD (in days) | 3 | 7 | 30 | 3 and 7 | 3 and 30 | 7 and 30 | 3, 7 and 30 | 3, 7, 30, and 60 |

|---|---|---|---|---|---|---|---|---|

| GRF-MSE | 0.124 | 0.095 | 0.089 | 0.075 | 0.070 | 0.069 | 0.059 | 0.057 |

To compare the performance of the above methods, we use two types of evaluation approaches. First, we test how well each model predicts the conditional -VaR over the entire out-of-sample horizon using three different sets of evaluation techniques. The simplest way of checking whether a model predicts correctly over a time horizon is to look at its coverage meaning the number of times is smaller than the predicted . Ideally, this should be exactly times. This measure is called Actual over Expected Exceedances (AoE) and is computed as . To test this intuition formally, we employ three tests, the DQ-test777We use the implementation from the GAS-package in R (Ardia et al., 2019) including 4 lagged Hit-values, a constant, the VaR-forecast, and the squared lagged (log-)return in the regression model. from Engle and Manganelli (2004), the Christoffersen-test (Christoffersen, 1998) and the Kupiec-test (Kupiec, 1995). All three tests assume that the forecasts have correct coverage under the null hypothesis. The Kupiec-test is simply the formalization of the above intuition, the Christoffersen-test is robust against serial correlation by assuming that , and the DQ-test additionally accounts for problems with conditional coverage due to clustering of the hits exceedance sequences with a regression-based approach. In the empirical analysis, we only report the values of the DQ-test, which is the strictest of the tests, for reasons of clarity. Results for the other tests do not differ substantially and are available upon request from the authors.

Secondly, for comparing the forecast performance of two models 1 and 2 directly, we implement the one-step ahead test for conditional predictive ability (CPA) from Giacomini and White (2006), Theorem 1, that assumes under the null hypothesis that forecasts of model 1 and model 2 have on average equal predictive ability conditional on previous information. As suggested by Giacomini and Komunjer (2005), we use the quantile loss function for the test. This tests assumes under the null hypothesis that and that this loss difference is a martingale difference sequence, where contains all information up to time and and are two competing forecasts. The test statistic is computed using a Wald-type test with a set of factors that can possibly predict the loss difference and is -distributed under . More specifically, we choose (i.e. ), i.e. using the lagged loss difference and an intercept as predictors in a linear regression with parameter for the simulation and application.

4 Simulation

In this section, we study the finite sample forecast performance in quantiles for true DGPs of standard stock-type dynamics as well as for set-ups of cryptocurrency type. Overall, we find that, as expected, GRF performs best in all settings, in particular in settings which are designed to mimic the cryptocurrency behaviour over time but also in those similar to stock index behaviour. For QRF, the performance is entirely different, at least for the chosen parsimonious model specification and the relatively short estimation intervals.

We study two different types of DGPs. The first one is a standard GARCH(1,1) process, i.e

| (3) | ||||

| (4) |

where the parameters are estimated on the full Bitcoin data to mimic the behavior of cryptocurrencies (with ). We denote this setting as sim GARCH Bitcoin fit. Moreover, we also consider the specification with , , and (sim GARCH) and with as -distributed (sim GARCH t), which corresponds to standard stock index data. Secondly, for the Sim SAV-Model setting, we fit a symmetric absolute value (SAV) model to normal returns, i.e.

| (5) |

with and , where new draws of are only taken every 100 observations, keeping constant meanwhile. We then generate the final return as from the fitted SAV-model, where is the quantile function of a standard normal variable. We do this to obtain returns that have exactly the VaR that we obtained from the SAV model before.

| Rolling Window | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| DQ | Kupiec | Christoffersen | AoE | DQ | Kupiec | Christoffersen | AoE | ||

| Sim GARCH Normal | |||||||||

| QRF | 1.185 | 1.148 | |||||||

| GRF | 1.040 | 1.030 | |||||||

| QR | 1.095 | 1.042 | |||||||

| Hist | 1.047 | 1.030 | |||||||

| NormFit | 1.006 | 1.001 | |||||||

| CAV | 1.073 | 1.032 | |||||||

| GARCH(1,1) | 1.046 | 1.028 | |||||||

| Sim GARCH t | |||||||||

| QRF | 1.188 | 1.162 | |||||||

| GRF | 1.029 | 1.022 | |||||||

| QR | 1.109 | 1.049 | |||||||

| Hist | 1.036 | 1.016 | |||||||

| NormFit | 0.839 | 0.817 | |||||||

| CAV | 1.059 | 1.032 | |||||||

| GARCH(1,1) | 0.893 | 0.862 | |||||||

| Sim SAV-Model | |||||||||

| QRF | 1.187 | 1.158 | |||||||

| GRF | 1.047 | 1.048 | |||||||

| QR | 1.102 | 1.064 | |||||||

| Hist | 1.047 | 1.048 | |||||||

| NormFit | 0.994 | 0.999 | |||||||

| CAV | 1.067 | 1.038 | |||||||

| GARCH(1,1) | 1.021 | 1.018 | |||||||

| Sim GARCH Bitcoin fit | |||||||||

| QRF | 1.185 | 1.148 | |||||||

| GRF | 1.040 | 1.030 | |||||||

| QR | 1.095 | 1.042 | |||||||

| Hist | 1.047 | 1.030 | |||||||

| NormFit | 1.006 | 1.001 | |||||||

| CAV | 0.814 | 0.791 | |||||||

| GARCH(1,1) | 1.054 | 1.032 | |||||||

For all settings, we generate 2000 return observations and forecast the one-step ahead VaR over the different rolling window lengths . We repeat this generation process 200 times for and . For comparison of the different methods described in Section 3, we use the DQ-test, the Kupiec test, the Christoffersen-test, and the AoE. Note that for all tests, we present aggregate results from two-sided t-tests of the empirical versus the nominal coverage. The results are therefore rejection rates of t-tests against the nominal level of 5%. Therefore, a lower rejection rate and higher mean p-values (in parentheses) indicate better performance. For GRF, QRF, and QR, we use a common set of lagged covariates as described at the end of Section 3.

Table 4 summarizes the results of the simulation for the 5% . According to the more advanced - and Christoffersen-tests for evaluation, GRF consistently outperforms the other methods in almost all cases, indicating superior predictive quality. This is very much in contrast to the QRF which is consistently dominated by the other models. For the Sim GARCH and Sim GARCH t cases which mimic standard stock indices, the performances of GRF, CAV and QR appear in a similar range with mostly advantages for GRF in particular for smaller sample sizes. This holds generally for normally distributed as well as heavy tailed innovations which lead to similar results also in magnitude of the rejection rates. As expected, forecasting performance increases throughout all models with larger estimation windows, though with CAV often profiting the most from the larger sample sizes. For these settings with GARCH as the true DGP, the performance of the GARCH model serves as an oracle reference. In the t-innovation case, it has coverage problems and GRF is even able to outperform it in Christoffersen-tests.

For the Sim SAV Model and the Sim GARCH Bitcoin fit the situation, however, differs substantially. In these cryptocurrency-like cases, the GRF clearly dominates the QR and CAV particularly strongly in the small 500 observations setting. Considering our application where only a relatively small time span is available, this seems crucial. Moreover, CAV runs into coverage problems according to the AoE results which even deteriorate for larger sample sizes for Sim GARCH Bitcoin fit. In the latter case, the GRF rejection rates are close to the GARCH benchmark while the strong conditional dependence structure in the tails of the Sim SAV Model setting shows that for such extreme cases, the unconditional coverage of GRF is still excellent, but the conditional coverage measured by the DQ-test is only average among all models for the larger estimation samples and even below for the smaller ones. These relative findings generally prevail for the 1% VaR forecasts, but absolute performance is generally worse for all methods, especially with a smaller rolling window of 500 (see Table 16 in the appendix.). Intuitively, this finding is reasonable, since relevant observations for the 1% level should in theory only occur in 5 of the 500 observations, making it harder for the data-driven methods to predict such unlikely events.

Additionally, we conduct direct pairwise comparison tests between the superior random forest type method GRF against the best performing non-oracle other parametric methods via CPA-tests for each scenario. The respective results are reported in Table 5. In the majority of cases, GRF outperforms its competitors on average, however, mean p-values are mostly not significant. For example, GRF has a smaller loss (i.e. quantile loss) than QR in about 90% of the forecasts (aggregated over all runs) but a mean p-value of 0.298, which would not qualify as a significant out-performance (on average). This of course does not mean that the test never rejects but is likely be caused by high variances in the p-values over different simulation runs. Furthermore, the competing methods are also slightly improving with window length, which further implies that GRF can deal better with a smaller training time frame.

| Rolling Window | |||||||

|---|---|---|---|---|---|---|---|

| GRF vs: | QR | Hist | CAV | QR | Hist | CAV | |

| Sim GARCH Normal | |||||||

| Mean P-Value | |||||||

| No. P-Values | |||||||

| GRF-Performance | |||||||

| Sim GARCH t | |||||||

| Mean P-Value | |||||||

| No. P-Values | |||||||

| GRF-Performance | |||||||

| Sim SAV-Model | |||||||

| Mean P-Value | |||||||

| No. P-Values | |||||||

| GRF-Performance | |||||||

| Sim GARCH Bitcoin fit | |||||||

| Mean P-Value | |||||||

| No. P-Values | |||||||

| GRF-Performance | |||||||

5 Results

In this section, we highlight the advantages from using non-linear machine learning-based methods for forecasting the VaR of cryptocurrencies. In particular, we show for a large cross-section of more than 100 cryptocurrencies that the proposed random forest method GRF yields superior performance across a wide range of different types of cryptocurrencies and different time periods. Investigating the underlying drivers, we illustrate that the non-linear model predictions excel especially for assets that are frequently traded by a large amount of different users, and for more volatile assets and times.

More specifically, we predict the as a key quantity in risk management for our comprehensive set of cryptocurrencies. In an extensive out-of-sample forecasting study, we compare the random forest-based machine learning methods to standard linear time series and GARCH-type models including approaches with exogenous asset information in covariates. The prediction performance is assessed with the DQ-test to obtain an overall aggregate picture on the realized coverages as well as pairwise CPA-tests across different time periods and types of cryptocurrencies. Based on these findings, we focus our analysis on three important selected currencies comprising Bitcoin (btc) as the largest currency by far regarding market cap, Tether (usdt) as a stablecoin with lower volatility, and Cardano (ada) as a currency specifically allowing for smart contracts. For these we also consider predicted loss series by CPA-tests and variable importance measures to uncover important drivers. We furthermore identify single events that majorly affect the predictive ability of the procedures.

5.1 Aggregated Forecasting Performance

In this section, we provide results on aggregate forecast performance of the different modeling approaches over all cryptocurrencies.

5.1.1 Backtesting

| Period | GRF | QRF | QR | CAV | GJR-GARCH | Hist | GRF-X | QRF-X | QR-X | GARCH-X |

|---|---|---|---|---|---|---|---|---|---|---|

| 1 | 0.16 | 0.29 | 0.08 | 0.06 | 0.03 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| 2 | 0.27 | 0.09 | 0.06 | 0.27 | 0.17 | 0.08 | 0.13 | 0.06 | 0.00 | 0.00 |

| 3 | 0.18 | 0.05 | 0.07 | 0.03 | 0.30 | 0.01 | 0.20 | 0.10 | 0.00 | 0.03 |

| Group | GRF | QRF | QR | CAV | GJR-GARCH | Hist | GRF-X | QRF-X | QR-X | GARCH-X |

|---|---|---|---|---|---|---|---|---|---|---|

| Period 1 | ||||||||||

| High | 0.16 | 0.92 | 0.00 | 0.00 | 0.12 | 0.00 | 0.01 | 0.00 | 0.00 | 0.00 |

| Low | 0.13 | 0.28 | 0.10 | 0.10 | 0.02 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| Period 2 | ||||||||||

| High | 0.16 | 0.08 | 0.20 | 0.19 | 0.11 | 0.08 | 0.13 | 0.07 | 0.00 | 0.00 |

| Low | 0.29 | 0.10 | 0.06 | 0.31 | 0.25 | 0.10 | 0.32 | 0.06 | 0.00 | 0.09 |

| Period 3 | ||||||||||

| High | 0.47 | 0.05 | 0.22 | 0.11 | 0.21 | 0.01 | 0.51 | 0.12 | 0.00 | 0.00 |

| Low | 0.07 | 0.04 | 0.03 | 0.02 | 0.32 | 0.00 | 0.18 | 0.07 | 0.00 | 0.06 |

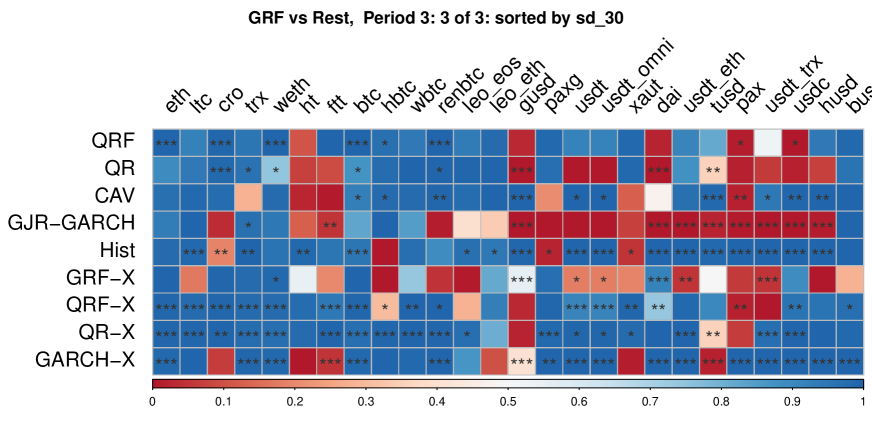

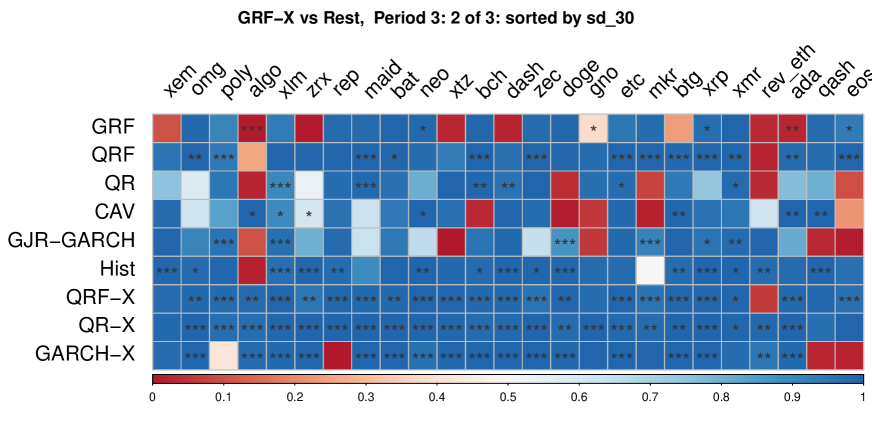

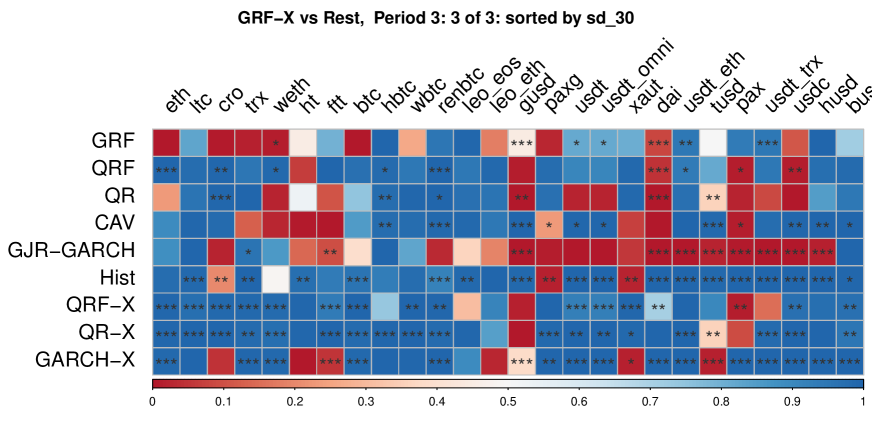

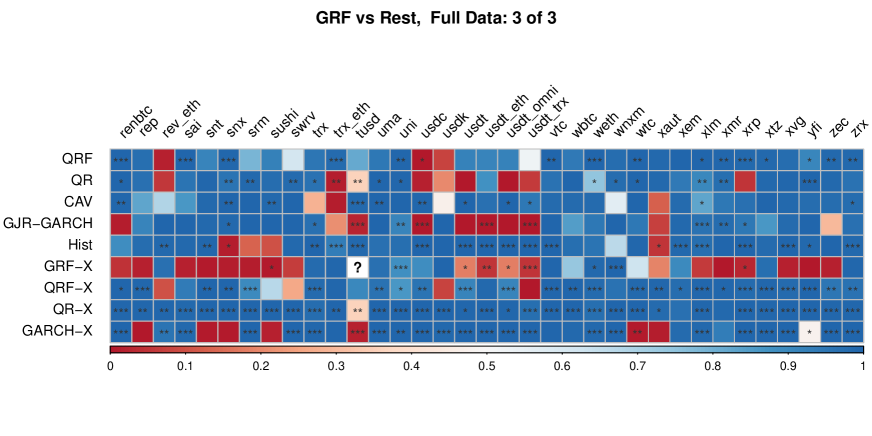

We analyze the three fundamentally distinct periods 08/2015–12/2017, 01/2018–11/2020, and 12/2020–03/2022 of the cryptocurrency market which differ according to the number of actively traded currencies, the market capitalization and the overall market situation (see Section 2). We thus analyze each period separately, with a focus on the last period 3 in the aggregate, where the number of available currencies is relatively high. Given the largely different market situations, we refrain from reporting results for the full time period. We assess the performance of VaR forecasts by their conditional coverage and the dependence structure of exceedances, which we test with the DQ-test (see Section 3 for details). This test is the most strict of all backtests, conditioning on past information, and therefore most accurately captures the coverage abilities of the procedures888Detailed results for the other tests are omitted here for reasons of clarity, do not differ qualitatively, and are available upon request from the authors.. The results over the different time periods for the 5% VaR-predictions are shown in Table 6. We can see that depending on the time period, the median p-values vary strongly, which is not surprising giving the different characteristics of each period and the increasing number of cryptocurrencies in the later periods. In general, GRF is the only method with median values consistently over the 10% level, indicating that it is the most consistently calibrated forecasting method. The QRF performs extremely well in the first time period, but rejects the test often in the third period. Adding external covariates as listed in Table 2 does not improve performance and in general leads to substantially lower p-values especially for the QR. Only in the final third period, adding external covariates increases the p-values slightly for the GRF and substantially for the QRF (GRF-X, QRF-X). This indicates that those extra covariates are not necessarily predictive for extreme returns, or rather that the existing measures such as lagged returns and SD comprise the information already quite well. Compared to its non-forest counterparts, only CAV and GJR-GARCH can partly keep up with GRF. GJR-GARCH has higher median p-values than GRF in the third period, which is the shortest and which contains the most currencies. It is also marked by less extreme returns and a large reduction in active users (see Table 2), which could indicate that the forest methods excel in particular in highly volatile periods, when large shifts in the market are present. On the other hand, CAV has a similar, slightly worse performance in the second period while performing much worse than GRF in the other periods. This highlights the inability of the parametric methods to adapt to rapidly changing situations such as in Period 1 and 3. QR, Hist, and GARCH-X are all fully dominated by GRF throughout the three time periods as expected, as QR can only incorporate changes linearly, and GARCH-X and Hist serve as simple baselines. Additionally, when checking the unconditional (median) coverage represented as the ratio of exceedances relative to the expected ones, random forest-type methods also show superior performance over standard GARCH-type methods, which have quite low coverage in all (GARCH-X) or the first period (GJR-GARCH)999Detailed results are available on request..

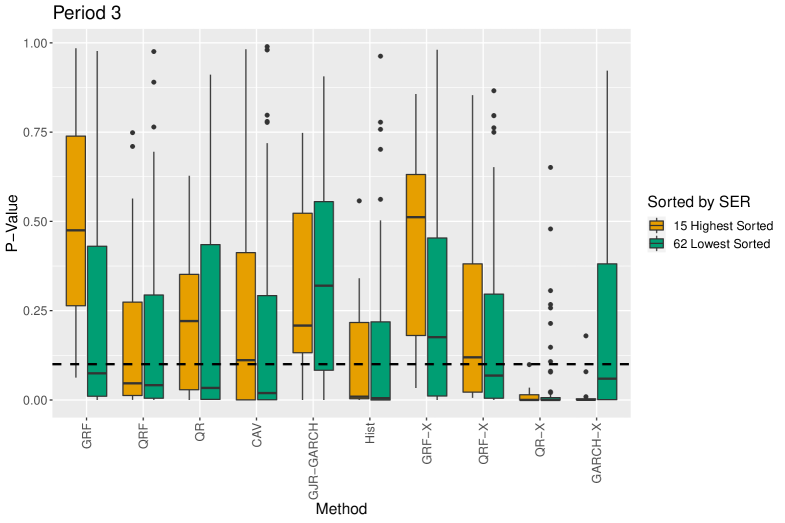

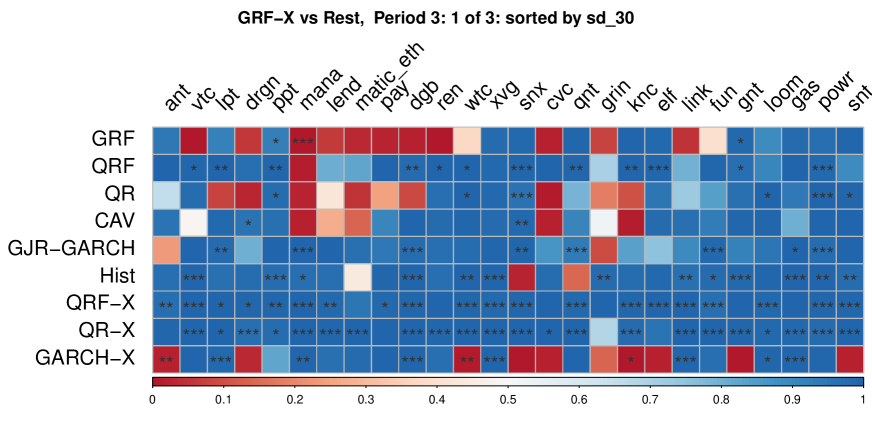

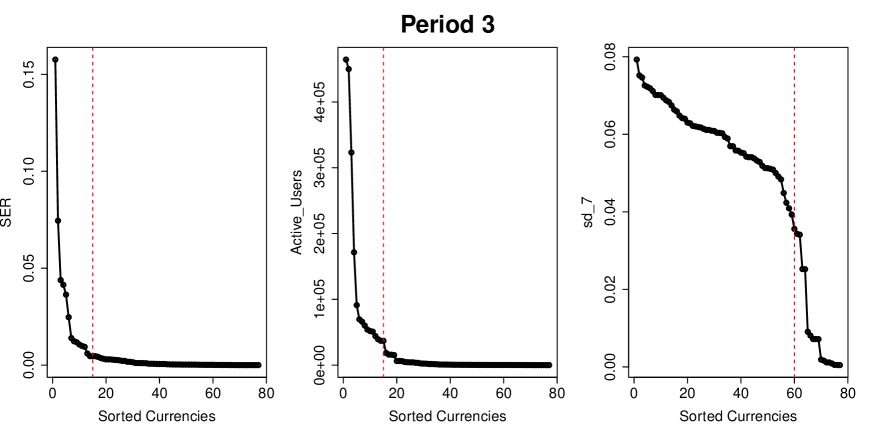

We investigate Period 3, which contains 77 cryptocurrencies, more in detail, especially with regard to how conditional coverage is characterized by external information. For this, we split the currencies into two groups101010Split points are plotted in Figure 10 in the appendix and correspond to obtaining two groups with mean SER values as homogeneous as possible. They are therefore separated around their steepest decay. depending on the value of the SER, which characterizes the concentration of supply to users. A low SER consequently implies that most supply is concentrated on a few, large users, often indicating a more stable currency. Figure 2 depicts boxplots over p-values of DQ-tests for each group and procedure in Period 3. GRF(-X) performs particularly well for the groups with a high SER, which arguably are more prone to speculations during hype/bubble periods due to the large amount of supply held by many small addresses. For the (arguably) more stable addresses with a smaller SER, GJR-GARCH has higher p-values, followed by GRF-X, which has the most consistent performance in this period. This is in contrast to CAV, QR, or QRF, which are always outperformed by GRF(-X), as well as the simple baselines Hist and GARCH-X. For details on all time periods and groups according to the different observable factors active users and lagged standard deviation, see Table 13 in the appendix.

5.1.2 Direct Pairwise Forecast Comparisons

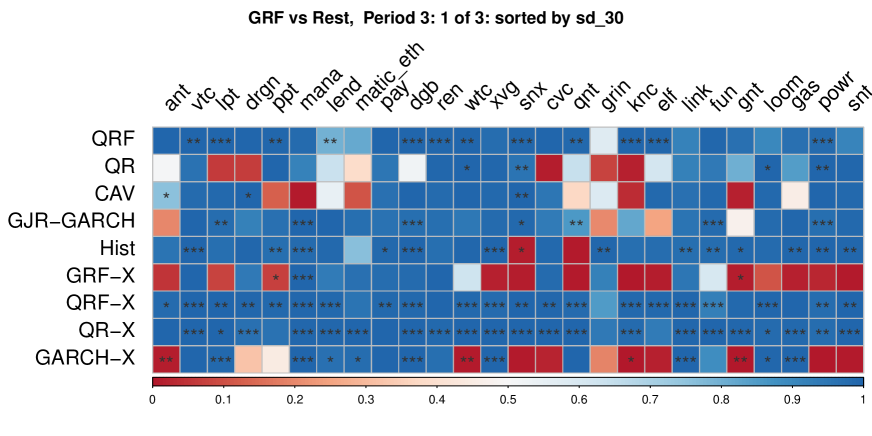

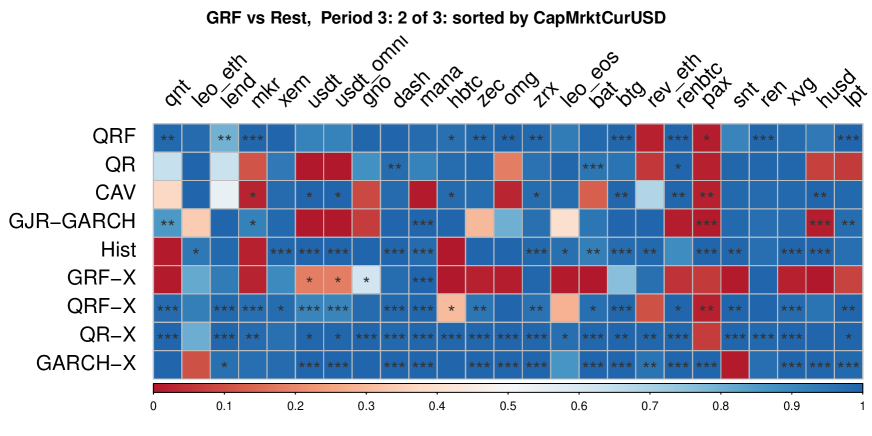

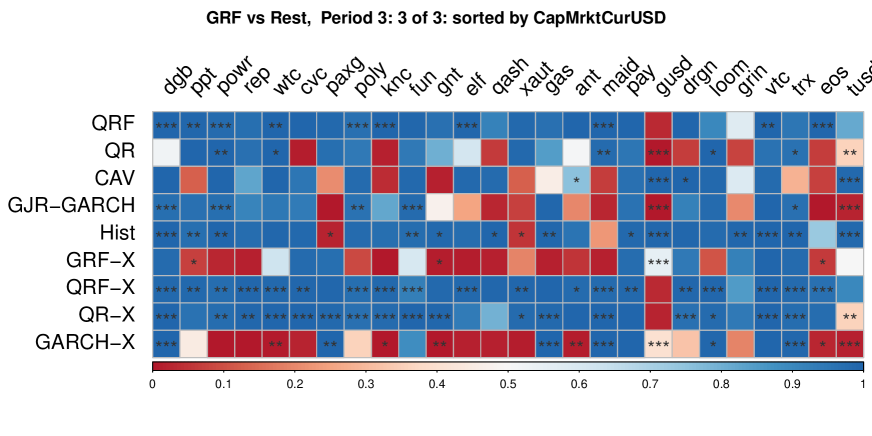

In addition to assessing the coverage performance, we conduct pairwise CPA-tests for all considered methods in the three different specified time periods over all cryptocurrencies. The results of the tests are contained in Table 8 and Figure 4. Note that the CPA-tests require the rolling window length to be smaller than the out-of-sample forecast window to produce valid results. Therefore the results from the shortest period Period 3, where both window sizes are equal to 500 might have less power. Thus by construction, for the only recently introduced cryptocurrencies in period 3, the out-of-sample size is too low for the CPA-tests to have high power. Therefore, we additionally look at the direct comparisons of predicted losses (as suggested by Giacomini and White (2006), Section 4)111111We use the lagged loss difference and an intercept for loss prediction in an autoregressive setup since these are the main drivers of the test statistic in the CPA test., where we compare in the loss series how often GRF is better, i.e. has a smaller loss, than its competitors (GRF-Performance). Note that a value of one thus indicates that GRF has a smaller predicted loss over the full loss series.

In general, GRF performs better than its competitors for a majority of crypotocurrencies over all time periods. Table 8 summarizes the results. We can see that QRF is almost always outperformed, and for around 50% of cryptocurrencies, losses are even significantly smaller. This is not surprising, as QRF has a similar structure to GRF while not being tuned to predict the quantiles directly. Thus, we expect it to be less sensitive to changes that only affect the quantile of the return distribution, for example large shock events. The same holds for the GARCH-X and Hist, which are clearly outperformed by the GRF, as well as the QR-X and QRF-X. Adding exogenous information in covariates as part of the non-linear GRF (i.e. GRF-X) is better especially in later periods (see Figure 9 in the appendix). This is interesting, since the other methods cannot benefit as much as GRF from additional covariates. Generally, for cryptocurrencies, the non-parametric form of the GRF helps to extract information from exogenous covariates in contrast to standard parametric methods such as QR and GARCH. As GRF accounts specifically for the quantiles in the random forest splitting function, this helps to also favorably integrate additional covariates in contrast to QRF. Overall, however, both GRF-procedures seem to perform very similarly, especially in pairwise comparisons. For full results of the GRF-X, see Table 14 and Figure 9 in the appendix. While CAV, QR, and GJR-GARCH are outperformed over the majority of cryptocurrencies, only 20% to 50% of these out-performances reach significance. In subsection 5.2, we will focus on specific cryptocurrencies for a more in-depth understanding.

| GRF vs.: | QRF | QR | CAV | GJR-GARCH | Hist | GRF-X | QRF-X | QR-X | GARCH-X |

|---|---|---|---|---|---|---|---|---|---|

| Share of GRF With Better Performance | |||||||||

| Period 1 | 1.00 | 0.80 | 0.80 | 1.00 | 1.00 | 0.60 | 1.00 | 1.00 | 1.00 |

| Period 2 | 1.00 | 0.73 | 0.87 | 0.80 | 0.93 | 0.40 | 1.00 | 1.00 | 1.00 |

| Period 3 | 0.92 | 0.68 | 0.71 | 0.64 | 0.90 | 0.44 | 0.92 | 0.96 | 0.70 |

| Full Data | 0.91 | 0.74 | 0.75 | 0.71 | 0.82 | 0.44 | 0.90 | 0.97 | 0.72 |

| Share of GRF With Significantly Better Performance | |||||||||

| Period 1 | 0.40 | 0.40 | 0.20 | 0.20 | 1.00 | 0.00 | 1.00 | 1.00 | 0.60 |

| Period 2 | 0.53 | 0.33 | 0.27 | 0.33 | 0.73 | 0.00 | 1.00 | 0.87 | 0.67 |

| Period 3 | 0.43 | 0.21 | 0.23 | 0.19 | 0.51 | 0.09 | 0.74 | 0.78 | 0.53 |

| Full Data | 0.41 | 0.31 | 0.24 | 0.18 | 0.41 | 0.12 | 0.69 | 0.83 | 0.54 |

![[Uncaptioned image]](/html/2203.08224/assets/x3.png)

![[Uncaptioned image]](/html/2203.08224/assets/x4.png)

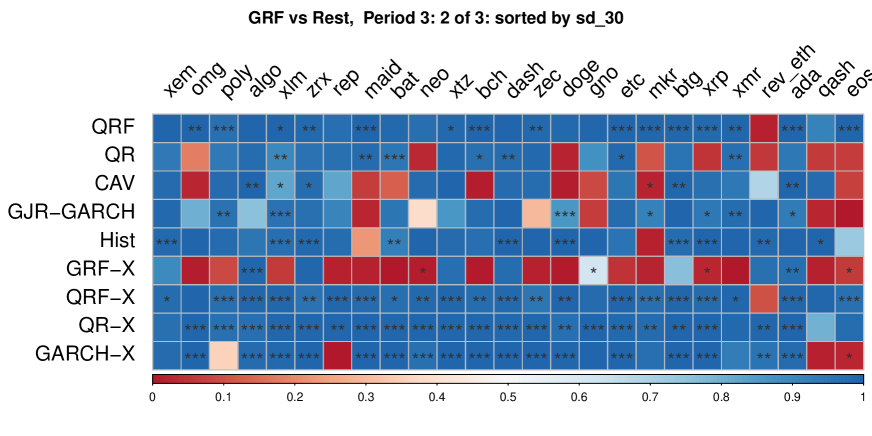

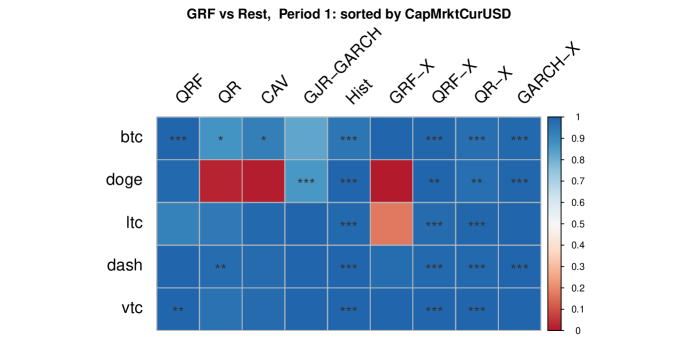

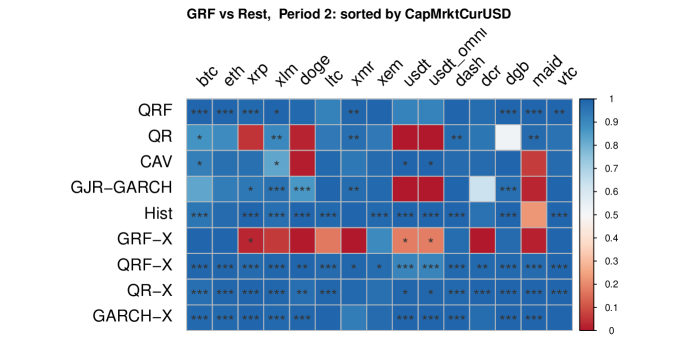

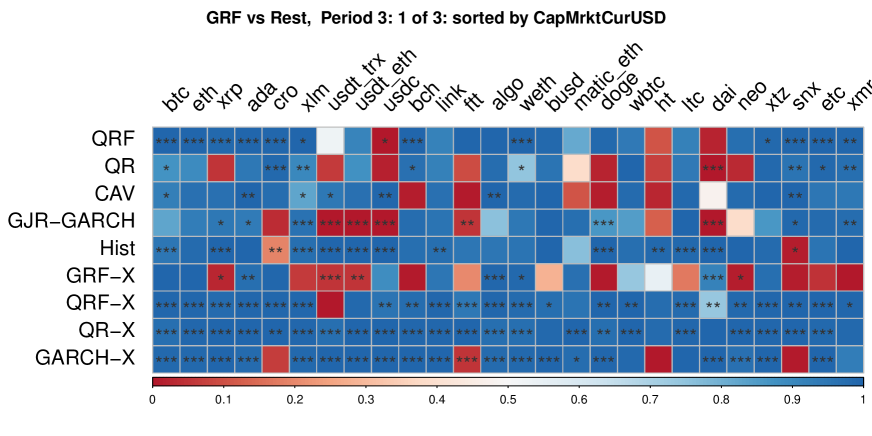

When considering the single time periods, it is notable how for Period 1 and 2 (bottom part of Table 8), GRF(-X) is constantly outperforming the other methods for most cryptocurrencies, and only has somewhat worse performance for doge and the stablecoins, although these are insignificant (see below). For the first two periods, QR is maybe the most competitive of the other methods, while there is a general tendency for the classic methods to perform worse with higher volatility of returns, which can be seen in Table 8 for Period 2 where the currencies are ordered from highest 30 day lagged SD on the left to the lowest on the right. This becomes more apparent in Period 3, where we deal with much more cryptocurrencies (77) and a much shorter time horizon (500 out-of-sample observations). Here, methods such as GJR-GARCH and QR are on par with GRF or even better when looking at low-volatility (partly regulated) stablecoins such as pax, gusd, tusd, dai, and usdt with its derivatives (e.g. usdt_eth,usdt_trx). CAV, on the other hand, is only rarely better here (as indicated by CPA tests), while being significantly outperformed for important and large assets such as btc, ada, xlm, and most stablecoins where the QR and GJR-GARCH performed well.

To highlight the specific properties of currencies where GRF outperforms the other methods, we split the assets into two groups. The first group (Group_low) contains assets where GRF performance is low in comparison to the three other methods that were able to compete in some cases with GRF, namely QR, CAV, and GJR-GARCH. We add an asset into that group when at least two of the methods outperform GRF (in terms of loss difference) for that asset, separately for each time period. All other assets are sorted into the second group (Group_high), indicating high performance of GRF. Table 9 summarizes the results over these groups for each time period and covariate. In each group, we take the mean over all cryptocurrencies of median values for each covariate. We then divide Group_low by Group_high. For example, An SER of 0.15 in Period 3 indicates that cryptocurrencies in Group_low have, on average, a median SER that is only 15% to that of Group_high, or in other words, the median SER for Group_high is around times higher than that of Group_low on average. We see that covariates of cryptocurrencies for which GRF performs better have much higher volatility (especially for the second and third period), a much higher SER121212Apart from the first period where the only currency belonging to Group_low is doge., indicating a larger concentration of supply at a lot of small addresses, a higher market capitalization, a lower rate of turnover (Velocity), and more active and total users. To summarize, this confirms the observation that GRF performs better for assets with highly varying returns that are traded by a large amount of users, which could thus also be prone to speculation. On the other side, methods such as QR or GJR-GARCH are better with more stable currencies that are used more as a hedging device (e.g. stablecoins). This confirms our findings from the backtests in Section 5.1.1, where GRF excels in particular for currencies with high SER values, high volatility, and a large number of active users.

| Period 1 | Period 2 | Period 3 | Full Data | |

|---|---|---|---|---|

| Ret | 1.20 | 0.16 | 1.05 | 0.92 |

| Active_Users | 0.34 | 0.15 | 0.26 | 0.34 |

| Total_Users | 0.79 | 0.18 | 0.13 | 0.15 |

| Total_Users_USD100 | 0.22 | 0.17 | 0.27 | 0.35 |

| Total_Users_USD10 | 0.41 | 0.17 | 0.19 | 0.25 |

| CapMrktCurUSD | 0.08 | 0.11 | 0.37 | 0.33 |

| SER | 1.07 | 0.50 | 0.15 | 0.21 |

| Transactions | 0.42 | 0.04 | 1.20 | 1.53 |

| VelCur1yr | 4.68 | 3.11 | 1.48 | 1.43 |

| sd_3 | 0.89 | 0.52 | 0.59 | 0.58 |

| sd_7 | 0.91 | 0.54 | 0.59 | 0.57 |

| sd_30 | 0.90 | 0.52 | 0.59 | 0.58 |

| sd_60 | 0.91 | 0.54 | 0.58 | 0.57 |

5.2 Extension: In-Depth Analysis of Specific Classes of Assets

To identify which specific events drive the performance of these methods, we analyze the predicted loss series of CPA tests over the full horizon of availability for the three cryptocurrencies Bitcoin, Cardano, and Tether separately. We furthermore show which covariates are important over the full data and specific time periods using variable importance measures of GRF-X.

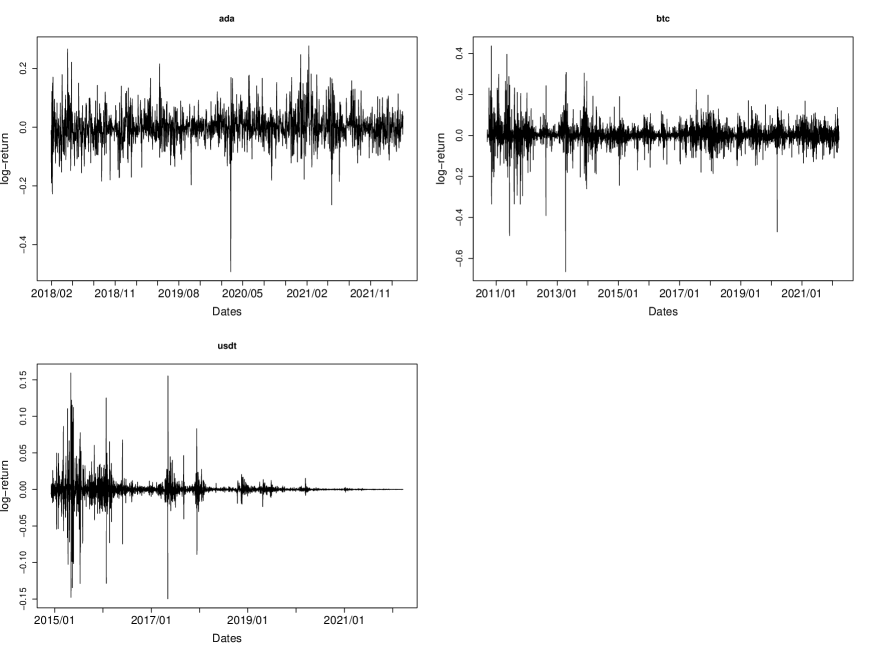

We choose Bitcoin since it is the largest currency by market cap, with the longest data availability, Tether as the largest stablecoin by daily volume and market cap, and Cardano as a fairly new (i.e. fewer observations), however large currency (again by market cap), which can be used for smart contracts, identity verification, or supply chain tracking131313See e.g. https://cardano.org/enterprise/, accessed 19/05/2022.. Since we deal with VaR-predictions, the initial loss function is the quantile loss with a quantile .

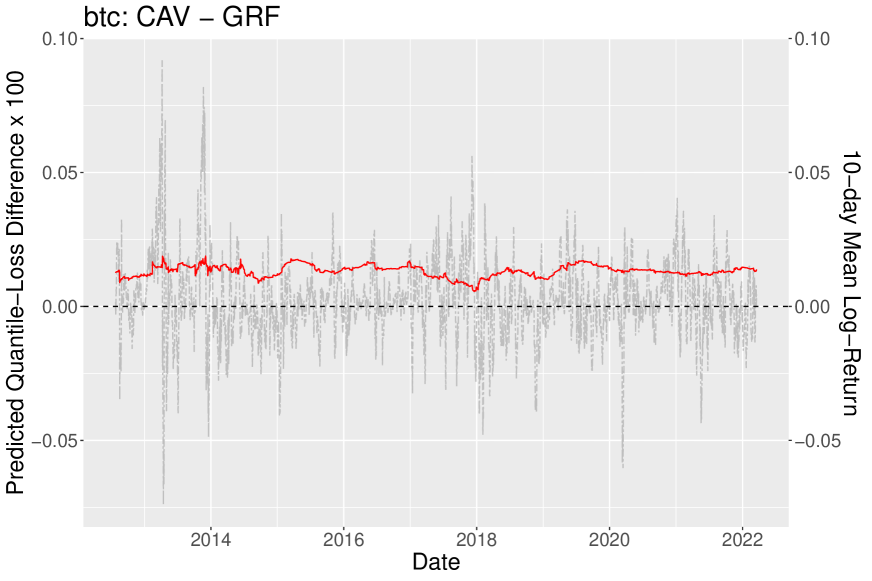

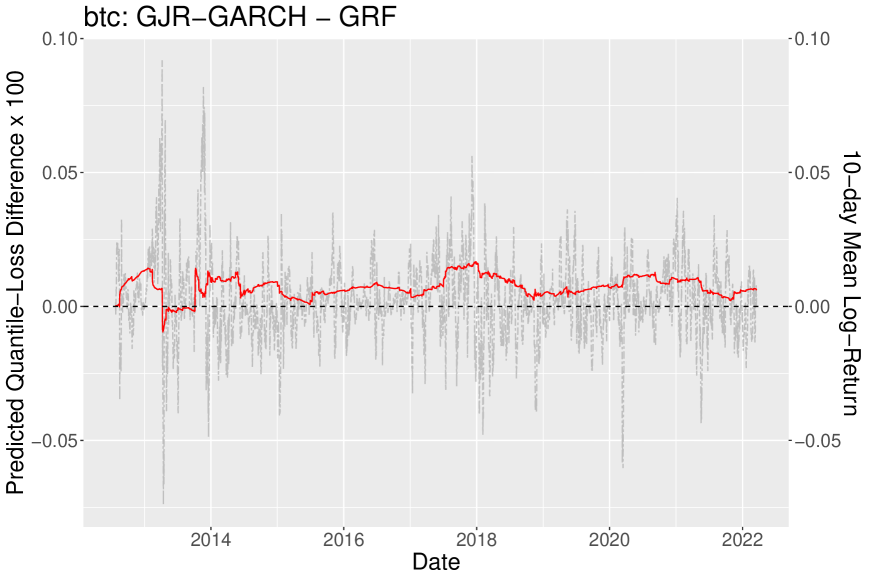

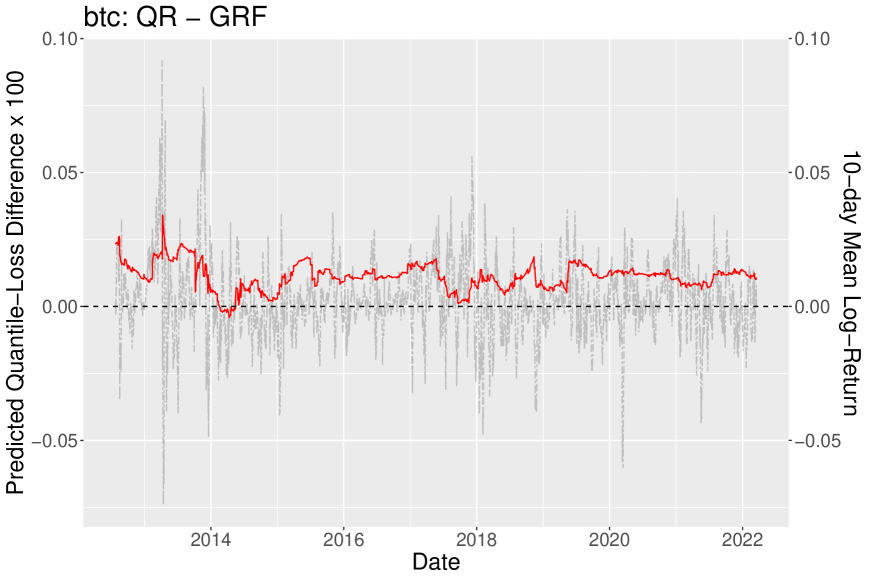

First, we look at Bitcoin (btc), the largest and most popular currency, where GRF largely outperforms QR, CAV, and GJR-GARCH in the CPA-tests. Figure 5 shows the predicted loss difference for each of the different methods. GRF outperforms the other methods consistently for most time frames. This is most likely due to the specific tailoring of the methodology to quantiles, as it outperforms QRF (not plotted) consistently here. For the parametric methods GJR-GARCH and QR, there are two short time periods where they have a smaller loss. For GJR-GARCH, this happens in the very beginning of the out-of-sample periods in April 2013, where btc crashed with negative log-returns of up to . Since this was the first drop of that magnitude for btc, GRF, as a forest based-method, had never seen such an extreme event, therefore could have technically not predicted it. GJR-GARCH, on the other hand, as a parametric method, has no range restriction in that regard. In the following crashes, GRF correctly predicts these extreme events better than GJR-GARCH, which is visible from the loss series. For QR, the short time frame is only caused by the predictions of the CPA test itself, while actual losses are smaller for GRF141414It might indicate, however, that the methods perform quite equally during that specific time, since there is no predictable difference..

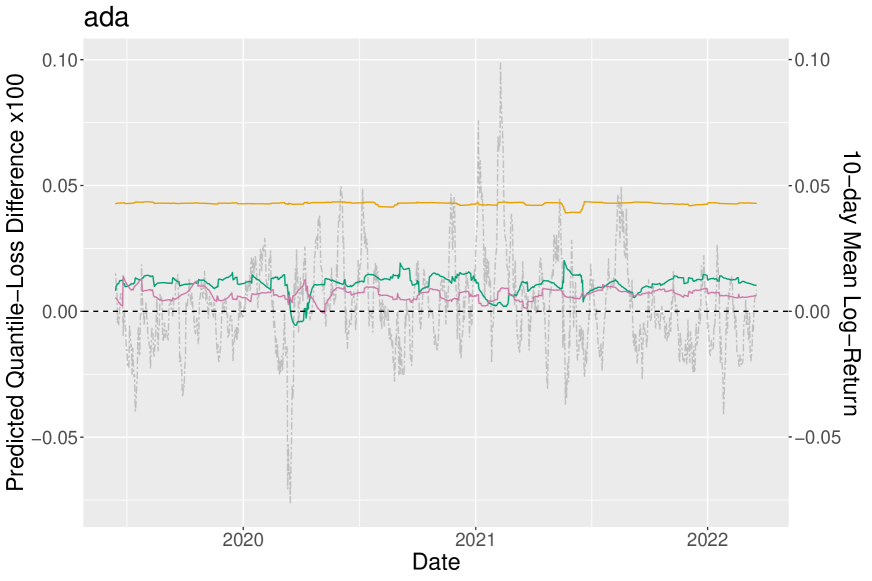

Secondly, as summarized on the left in Figure 6, we look at Cardano (ada), a large and fairly new currency offering e.g. smart contracts or supply chain tracking. There, GRF is significantly outperforming GJR-GARCH and CAV, while being slightly better than QR, although not reaching a significant level. This lack of power for QR is likely due to the small out-of-sample size (roughly 1000) for the fairly new asset compared to the training window of . Again, we can see that around the most extreme spike in March 2020, GJR-GARCH is slightly better, as GRF has not yet seen such an extreme event, therefore is not able to correctly predict the size of the loss. One normal solution would be to increase the training length, which is not possible in this case with a fairly new currency. Interestingly, in the later extreme events in May 2022, GRF increases in performance compared to GJR-GARCH, confirming the challenge with lacking training data.

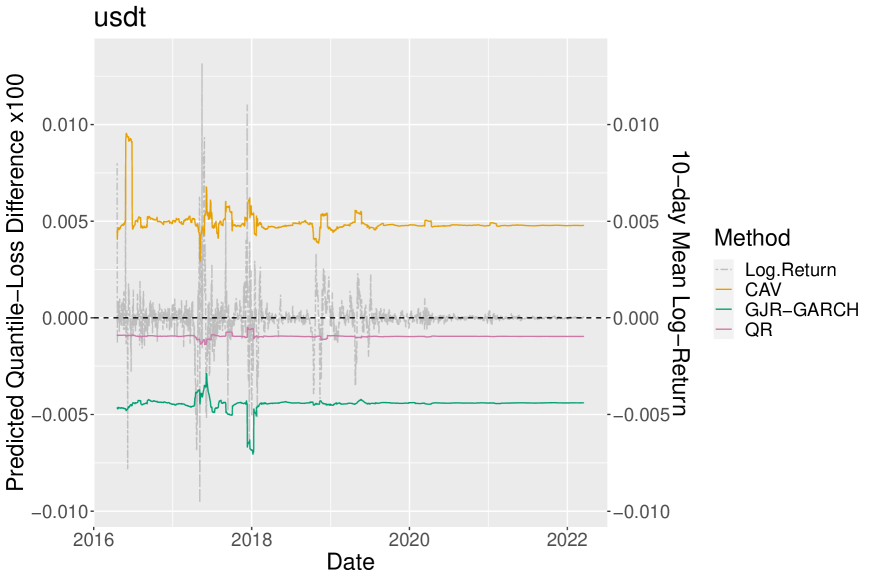

Finally, we also look more closely at Tether (usdt) as the largest stablecoin that is roughly bound to the USD151515As it is backed by USD cash reserves, see https://tether.to/en/.. The right part of Figure 6 shows the 30-day rolling means of the predicted loss differences. Notably, the rolling loss difference and rolling mean-return are already around 10 times smaller than those of btc or ada, indicating that usdt substantially differs from the other two currencies. While the losses of QR are very similar to those of GRF, CAV is significantly worse. Only GJR-GARCH consistently has lower predicted losses than GRF, although they are deemed not significant by the CPA tests (see Figure 13 in the appendix for detailed results for the full time frame). We can see, however, that for the relatively rare tail events in 2017, which are still not too extreme, there is some variation in the predicted loss difference. For the first event that is quite extreme, GJR-GARCH reacts too late, and only the second event is correctly detected by GJR-GARCH, as there is some limited information of anticipation. In general, GRF tends too overshoot less in these situations, which is also reflected in the DQ-tests, where GRF tends to be better for assets that are more prone to speculative bubbles.

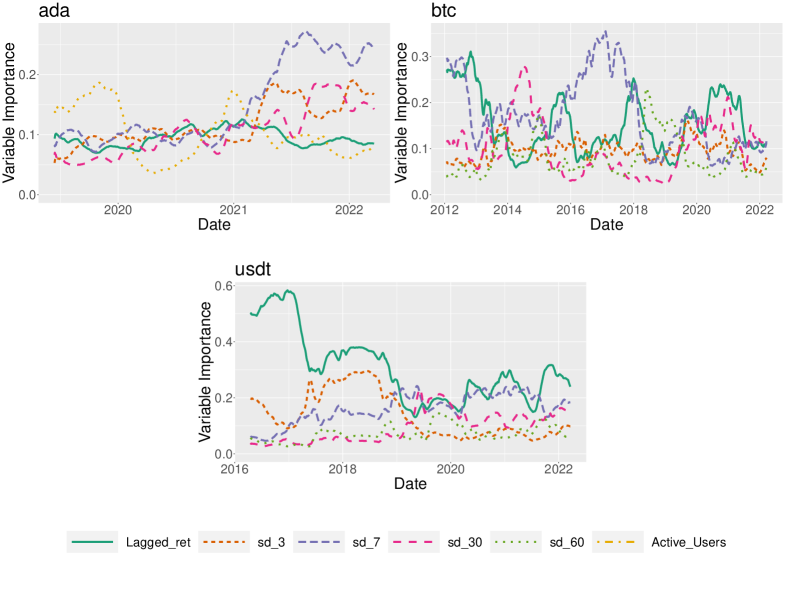

To further understand the drivers of the GRF performance, we obtain variable importance measures that depict the frequency of inclusion in splits of the forest. The variable importance of a covariate is measured as the proportion of splits on relative to all splits in a respective layer (over all trees in a trained forest), weighted by layer 161616We use a maximum depth of corresponding to the number of covariates and a weight decay of 2, meaning a split further down in each tree receives less weight in the final frequency as it is less important for the three specific currencies analyzed in the previous section. Specifically, for layer , .. In Figure 7, the importance difference of certain covariates over time for the three currencies is clearly visible.

Overall, the lagged return is very important for predicting VaR when returns are quite extreme relative to all returns in a specific asset, in the case of btc in times of hypes and crashes. Intuitively, this finding seems reasonable as in times of bubbles, when the volatility is driven by some short, bubble-like events and returns are highly variable, volatility lagged over a longer time horizon is less predictive for VaR and predictions are driven by events happening shortly before the prediction. In rather unstable times, but not in extreme cases, the lagged SD-measures gain importance, while the extra covariates only play a role for assets with relatively small volumes, e.g. when new currencies are created. This also explains why GRF-X performs much better for new, low-market-cap assets in Period 3 (see e.g. Figure 12 in the appendix).

Starting with ada, we see that it is the only asset of the three where the number of active addresses plays an important role, where for the other two assets, the 60-day lagged standard deviation is more important. The importance of variables can be split into two periods. The period until the beginning of 2021 is largely dominated by measures that somehow account for trading activity (Active_Users,Total_Users/_USD100/_USD10, Transactions). For reasons of clarity, we only plot the most important one of these measures, Active_Users. The spike of the latter in importance at the beginning of 2021 is likely caused by the massive increase in price and market cap during that time, representing a period of hype with many actively trading users171717See also Figure 14 in the appendix for an overview of the log-returns of the three currencies.. For the rest of the time period, lagged SD, mostly 3-day lagged SD, followed by 30-day and 60-day SD, is dominating the predictions of GRF. This change of importance seems reasonable as the structure of the asset fundamentally changes with the price increasing tenfold and the volume increasing strongly at the same time.

For btc, we have much more data covering 10 years, which is why the important variables change frequently in different periods. Lagged return is naturally important in phases of extreme hype and crashes that are characterized by large positive and negative returns, e.g. in the very beginning (where the price was still quite low), at the end of 2013 (the first time btc had a price of USD 1000), at the end of 2017 (with a price over USD 19,000), and from mid 2020 to the mid 2021, where there were multiple hypes and crashes during the Covid-19 pandemic. Between these hype periods, the lagged SDs are most important. In 2014-2015 and from the end of 2019 to mid 2021 , 30-day SD is contributing most to the GRF-predictions, followed by 7-day SD in 2016-2018 and 60-day SD 20 from 2018 to the end of 2019. This changing scheme is interesting, as 30-day SD seems to be a good predictor especially in very unstable times (return-wise), while 7-day and 60-day SD are more important in relatively stable times.

Finally, the stablecoin usdt is an exception, being largely dominated by the lagged return. Given that by construction usdt is essentially bound to the US dollar, its dynamic properties also largely correspond to those of standard currencies. From mid 2019, the prices and returns are rather stable and the volume increases strongly, and the influence lagged 7-day SD increases slightly, while still being less important than lagged return. This is not surprising, as usdt is quite stable in comparison to btc and ada.

6 Conclusion

In this paper, we show that random forests can significantly improve the forecasting performance for VaR-predictions when tailored to conditional quantiles. In both simulations and analyzing return data of 105 of the largest cryptocurrencies, the proposed GRF-type random forest shows superior prediction performance. In particular, the adaptive non-linear form of GRF appears to capture time-variations of volatility and spike-behavior in cryptocurrency returns especially well in contrast to more conventional financial econometric methods. We further show that the GRF is better in assessing the tail risk of cryptocurrencies in times where volatility in returns is high which often coincides with increased speculation in the market. In such periods, standard time-series based procedures, even when augmented with external factors, are substantially inferior in VaR predictions suggesting that a comparison of predicted losses could serve as an easy, empirical pre-screening device to detect such speculative bubbles.

Our findings are highly relevant for the risk assessment of cryptocurrencies where we show that classic methods might lead to a miss-quantification of associated risks. Such results directly impact investment and hedging decisions for respective assets. Specifically, we detect superior performance of GRF especially for highly volatile cryptocurrencies that have a high number of active users and could thus be potentially prone to speculation and hypes. On the other hand, for the class of stablecoins that are usually tied to some large, classic currency such as the USD, and which are usually dominated by a smaller number of large accounts, other classic methods such as GJR-GARCH or quantile regression are more on par with GRF. This corresponds also to the simulation results mimicking the behavior of conventional assets such as as stock returns where the advantage of GRF decreases. Major gains of GRF, however, occur the more cryptocurrency-like the set-up becomes.

The proposed random forest methodology allows identifying important external factors despite the non-linearity of the methodology. We show that such factors are time-varying and changing particularly in unstable times. For future research, this set of covariates could even be further augmented with other potentially driving real-time factors, such as for example properly extracted and filtered social media information. The relevance of such factors might also provide additional guidance for relevant exogenous information to be included in standard parametric models such as CAViaR.

References

- Ardia et al. (2019) Ardia, D., K. Boudt, and L. Catania (2019): “Generalized autoregressive score models in R: The GAS package,” Journal of Statistical Software, 88.

- Athey et al. (2019) Athey, S., J. Tibshirani, and S. Wager (2019): “Generalized random forests,” Annals of Statistics, 47, 1179–1203.

- Baur et al. (2018) Baur, D. G., K. H. Hong, and A. D. Lee (2018): “Bitcoin: Medium of exchange or speculative assets?” Journal of International Financial Markets, Institutions and Money, 54, 177–189.

- Bollerslev (1986) Bollerslev, T. (1986): “Generalized autoregressive conditional heteroskedasticity,” Journal of Econometrics, 31, 307–327.

- Breiman (1996) Breiman, L. (1996): “Some properties of splitting criteria,” Machine Learning, 24, 41–47.

- Breiman (2001) ——— (2001): “Random Forests,” Machine Learning, 45, 5–32.

- Breiman et al. (1984) Breiman, L., J. Friedman, C. J. Stone, and R. A. Olshen (1984): Classification and regression trees, CRC press.

- Cheah and Fry (2015) Cheah, E. T. and J. Fry (2015): “Speculative bubbles in Bitcoin markets? An empirical investigation into the fundamental value of Bitcoin,” Economics Letters, 130, 32–36.

- Christoffersen (1998) Christoffersen, P. F. (1998): “Evaluating Interval Forecasts,” International Economic Review, 39, 841.

- Chu et al. (2017) Chu, J., S. Chan, S. Nadarajah, and J. Osterrieder (2017): “GARCH Modelling of Cryptocurrencies,” Journal of Risk and Financial Management, 10, 17.

- Elendner et al. (2017) Elendner, H., S. Trimborn, B. Ong, and T. M. Lee (2017): “The Cross-Section of Crypto-Currencies as Financial Assets: Investing in Crypto-Currencies Beyond Bitcoin,” in Handbook of Blockchain, Digital Finance, and Inclusion, Volume 1: Cryptocurrency, FinTech, InsurTech, and Regulation, Elsevier, 145–173.

- Engle and Manganelli (2004) Engle, R. F. and S. Manganelli (2004): “CAViaR: Conditional autoregressive value at risk by regression quantiles,” Journal of Business and Economic Statistics, 22, 367–381.

- Ghysels and Nguyen (2019) Ghysels, E. and G. Nguyen (2019): “Price Discovery of a Speculative Asset: Evidence from a Bitcoin Exchange,” Journal of Risk and Financial Management, 12, 164.

- Giacomini and Komunjer (2005) Giacomini, R. and I. Komunjer (2005): “Evaluation and combination of conditional quantile forecasts,” Journal of Business and Economic Statistics, 23, 416–431.

- Giacomini and White (2006) Giacomini, R. and H. White (2006): “Tests of conditional predictive ability,” Econometrica, 74, 1545–1578.

- Gkillas and Katsiampa (2018) Gkillas, K. and P. Katsiampa (2018): “An application of extreme value theory to cryptocurrencies,” Economics Letters, 164, 109–111.

- Glaser et al. (2014) Glaser, F., K. Zimmermann, M. Haferkorn, M. C. Weber, and M. Siering (2014): “Bitcoin - Asset or currency? Revealing users’ hidden intentions,” ECIS 2014 Proceedings - 22nd European Conference on Information Systems, 1–14.

- Glosten et al. (1993) Glosten, L. R., R. Jagannathan, and D. E. Runkle (1993): “On the Relation between the Expected Value and the Volatility of the Nominal Excess Return on Stocks,” The Journal of Finance, 48, 1779–1801.

- Hafner (2020) Hafner, C. M. (2020): “Testing for Bubbles in Cryptocurrencies with Time-Varying Volatility,” Journal of Financial Econometrics, 18, 233–249.

- Hastie et al. (2009) Hastie, T., R. Tibshirani, and J. Friedman (2009): The Elements of Statistical Learning, Springer, second ed.

- Hencic and Gouriéroux (2015) Hencic, A. and C. Gouriéroux (2015): “Noncausal autoregressive model in application to bitcoin/USD exchange rates,” in Studies in Computational Intelligence, Springer, vol. 583, 17–40.

- Koenker and Bassett (1978) Koenker, R. and G. Bassett (1978): “Regression Quantiles,” Econometrica, 46, 33.

- Koenker and Hallock (2001) Koenker, R. and K. F. Hallock (2001): “Quantile regression,” Journal of economic perspectives, 15, 143–156.

- Kupiec (1995) Kupiec, P. H. (1995): “Techniques for Verifying the Accuracy of Risk Measurement Models,” The Journal of Derivatives, 3, 73–84.

- Kwiatkowski et al. (1992) Kwiatkowski, D., P. C. Phillips, P. Schmidt, and Y. Shin (1992): “Testing the null hypothesis of stationarity against the alternative of a unit root. How sure are we that economic time series have a unit root?” Journal of Econometrics, 54, 159–178.

- Liu et al. (2020) Liu, W., A. Semeyutin, C. K. M. Lau, and G. Gozgor (2020): “Forecasting Value-at-Risk of Cryptocurrencies with RiskMetrics type models,” Research in International Business and Finance, 54, 101259.

- Liu and Tsyvinski (2020) Liu, Y. and A. Tsyvinski (2020): “Risks and Returns of Cryptocurrency,” The Review of Financial Studies, 34, 2689–2727.

- Maciel (2020) Maciel, L. (2020): “Cryptocurrencies value-at-risk and expected shortfall: Do regime-switching volatility models improve forecasting?” International Journal of Finance & Economics.

- Meinshausen (2006) Meinshausen, N. (2006): “Quantile Regression Forests,” Journal of Machine Learning Research, 7, 983–999.

- Pafka and Kondor (2001) Pafka, S. and I. Kondor (2001): “Evaluating the RiskMetrics methodology in measuring volatility and Value-at-Risk in financial markets,” Physica A: Statistical Mechanics and its Applications, 299, 305–310.

- Petukhina et al. (2021) Petukhina, A., S. Trimborn, W. K. Härdle, and H. Elendner (2021): “Investing with cryptocurrencies – evaluating their potential for portfolio allocation strategies,” Quantitative Finance, 0, 1–29.

- Platanakis and Urquhart (2019) Platanakis, E. and A. Urquhart (2019): “Portfolio management with cryptocurrencies: The role of estimation risk,” Economics Letters, 177, 76–80.

- Selmi et al. (2018) Selmi, R., A. Tiwari, and S. Hammoudeh (2018): “Efficiency or speculation? A dynamic analysis of the Bitcoin market,” Economics Bulletin, 38, 2037–2046.

- Takeda and Sugiyama (2008) Takeda, A. and M. Sugiyama (2008): “N-Support Vector Machine As Conditional Value-At-Risk Minimization,” Proceedings of the 25th International Conference on Machine Learning, 1056–1063.

- Trimborn et al. (2020) Trimborn, S., M. Li, and W. K. Härdle (2020): “Investing with Cryptocurrencies - A Liquidity Constrained Investment Approach,” Journal of Financial Econometrics, 18, 280–306.

- Trucios et al. (2020) Trucios, C., A. K. Tiwari, and F. Alqahtani (2020): “Value-at-risk and expected shortfall in cryptocurrencies’ portfolio: A vine copula–based approach,” Applied Economics, 52, 2580–2593.

- Vigliotti and Jones (2020) Vigliotti, M. G. and H. Jones (2020): “The Rise and Rise of Cryptocurrencies,” in The Executive Guide to Blockchain, Springer, 71–91.

Appendix A Appendix

| KPSS_level | KPSS_trend | ADF | |

|---|---|---|---|

| algo | 0.09 | 0.02 | 0.01 |

| alpha | 0.02 | 0.10 | 0.01 |

| bnb | 0.06 | 0.05 | 0.01 |

| bnb_eth | 0.06 | 0.05 | 0.01 |

| btc | 0.05 | 0.10 | 0.01 |

| crv | 0.10 | 0.03 | 0.01 |

| dash | 0.07 | 0.10 | 0.01 |

| dcr | 0.10 | 0.08 | 0.01 |

| dot | 0.10 | 0.10 | 0.01 |

| eth | 0.10 | 0.08 | 0.01 |

| ftt | 0.10 | 0.04 | 0.01 |

| gno | 0.10 | 0.10 | 0.01 |

| gnt | 0.10 | 0.04 | 0.01 |

| icp | 0.10 | 0.02 | 0.01 |

| lend | 0.10 | 0.02 | 0.01 |

| loom | 0.05 | 0.10 | 0.01 |

| neo | 0.10 | 0.08 | 0.01 |

| omg | 0.10 | 0.02 | 0.01 |

| poly | 0.04 | 0.10 | 0.01 |

| ppt | 0.10 | 0.07 | 0.01 |

| snx | 0.02 | 0.10 | 0.01 |

| sushi | 0.10 | 0.01 | 0.01 |

| uni | 0.10 | 0.08 | 0.01 |

| weth | 0.05 | 0.10 | 0.01 |

| wtc | 0.10 | 0.09 | 0.01 |

| xem | 0.07 | 0.10 | 0.01 |

| xmr | 0.10 | 0.04 | 0.01 |

| xtz | 0.10 | 0.09 | 0.01 |

| yfi | 0.08 | 0.10 | 0.01 |

| id | Asset | Start-Date | End-Date | Obs. | X | Time Periods | id | Asset | Start-Date | End-Date | Obs. | X | Time Periods |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1inch | 1inch | 2020-12-26 | 2022-03-21 | 451 | 7 | eos | EOS | 2018-06-09 | 2022-03-21 | 1382 | 2 | 3 | |

| aave | Aave | 2020-10-10 | 2022-03-21 | 528 | 7 | eos_eth | EOS ETH | 2017-06-29 | 2018-06-02 | 339 | 7 | ||

| ada | Cardano | 2017-12-01 | 2022-03-21 | 1572 | 7 | 3 | etc | Ethereum Classic | 2016-07-25 | 2022-03-21 | 2066 | 9 | 3 |

| algo | Algorand | 2019-06-22 | 2022-03-21 | 1004 | 7 | 3 | eth | Ethereum | 2015-08-08 | 2022-03-21 | 2418 | 9 | 2,3 |

| alpha | Alpha Finance Lab | 2020-10-11 | 2022-03-21 | 527 | 7 | ftt | FTX Token | 2019-08-20 | 2022-03-21 | 945 | 7 | 3 | |

| ant | Aragon | 2017-08-29 | 2022-03-21 | 1666 | 7 | 3 | fun | FunFair | 2017-09-02 | 2022-03-21 | 1662 | 7 | 3 |

| bal | Balancer | 2020-06-25 | 2022-03-21 | 635 | 7 | fxc | Flexacoin | 2019-07-17 | 2021-01-25 | 559 | 6 | ||

| bat | Basic Attention Token | 2017-10-06 | 2022-03-21 | 1628 | 7 | 3 | gas | Gas | 2017-08-08 | 2022-03-21 | 1687 | 7 | 3 |

| bch | Bitcoin Cash | 2017-08-01 | 2022-03-21 | 1694 | 8 | 3 | gno | Gnosis | 2017-05-02 | 2022-03-21 | 1785 | 7 | 3 |

| bnb | Binance Coin | 2017-07-15 | 2019-04-22 | 647 | 7 | gnt | Golem (gnt) | 2017-02-19 | 2022-03-21 | 1857 | 7 | 3 | |

| bnb_eth | bnb_eth | 2017-07-15 | 2019-04-22 | 647 | 7 | grin | Grin | 2019-01-29 | 2022-03-21 | 1148 | 2 | 3 | |

| bsv | Bitcoin SV | 2018-11-15 | 2022-03-21 | 1220 | 8 | gusd | Gemini Dollar | 2018-09-16 | 2022-03-21 | 1283 | 7 | 3 | |

| btc | Bitcoin | 2010-07-18 | 2022-03-21 | 4265 | 9 | 1,2,3 | hbtc | Huobi Bitcoin | 2019-12-09 | 2022-03-21 | 834 | 5 | 3 |

| btg | Bitcoin Gold | 2017-10-25 | 2022-03-21 | 1609 | 7 | 3 | hedg | HedgeTrade | 2019-11-02 | 2022-01-27 | 818 | 7 | |

| busd | Binance USD | 2019-09-20 | 2022-03-21 | 914 | 7 | 3 | ht | Huobi Token | 2019-03-06 | 2022-03-21 | 1112 | 7 | 3 |

| comp | Compound | 2020-06-18 | 2022-03-21 | 642 | 7 | husd | HUSD | 2019-07-20 | 2022-03-21 | 976 | 7 | 3 | |

| cro | Crypto.com Coin | 2019-03-20 | 2022-03-21 | 1098 | 7 | 3 | icp | Internet Computer | 2021-05-11 | 2022-03-21 | 315 | 7 | |

| crv | Curve DAO Token | 2020-08-15 | 2022-03-21 | 584 | 7 | kcs | KuCoin Token | 2020-04-04 | 2022-03-22 | 718 | 0 | ||

| cvc | Civic | 2017-09-11 | 2022-03-21 | 1653 | 7 | 3 | knc | Kyber Network | 2017-09-27 | 2022-03-21 | 1637 | 7 | 3 |

| dai | Dai | 2019-11-20 | 2022-03-21 | 853 | 7 | 3 | lend | Aave (lend) | 2017-12-09 | 2022-03-21 | 1564 | 7 | 3 |

| dash | Dash | 2014-02-08 | 2022-03-21 | 2964 | 8 | 1,2,3 | leo_eos | UNUS SED LEO EOS | 2019-05-21 | 2022-03-21 | 1036 | 3 | 3 |

| dcr | Decred | 2016-05-17 | 2022-03-21 | 2133 | 8 | 2 | leo_eth | UNUS SED LEO ETH | 2019-05-21 | 2022-03-21 | 1036 | 7 | 3 |

| dgb | DigiByte | 2015-02-10 | 2022-03-21 | 2597 | 8 | 2,3 | link | Chainlink | 2017-09-29 | 2022-03-21 | 1635 | 7 | 3 |

| doge | Dogecoin | 2014-01-23 | 2022-03-21 | 2980 | 8 | 1,2,3 | loom | Loom Network | 2018-05-03 | 2022-03-21 | 1419 | 7 | 3 |

| dot | Polkadot | 2020-08-20 | 2022-03-21 | 579 | 7 | lpt | Livepeer | 2018-12-20 | 2022-03-21 | 1182 | 7 | 3 | |

| drgn | Dragonchain | 2018-01-03 | 2022-03-21 | 1539 | 7 | 3 | ltc | Litecoin | 2013-04-01 | 2022-03-21 | 3277 | 8 | 1,2,3 |

| elf | aelf | 2017-12-22 | 2022-03-21 | 1551 | 7 | 3 | maid | MaidSafeCoin | 2014-07-10 | 2022-03-21 | 2812 | 7 | 2,3 |

| id | Asset | Start-Date | End-Date | Obs. | X | Time Periods | id | Asset | Start-Date | End-Date | Obs. | X | Time Periods |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| mana | Decentraland | 2017-08-25 | 2022-03-21 | 1670 | 7 | 3 | tusd | TrueUSD | 2018-07-06 | 2022-03-21 | 1355 | 0 | 3 |

| matic_eth | matic_eth | 2019-04-27 | 2022-03-21 | 1060 | 7 | 3 | uma | UMA | 2020-09-08 | 2022-03-21 | 560 | 7 | |

| mkr | Maker | 2017-12-26 | 2022-03-21 | 1547 | 7 | 3 | uni | Uniswap | 2020-09-18 | 2022-03-21 | 550 | 7 | |

| neo | Neo | 2017-07-15 | 2022-03-21 | 1711 | 7 | 3 | usdc | USD Coin | 2018-09-28 | 2022-03-21 | 1271 | 7 | 3 |

| nxm | Nexus Mutual | 2020-08-26 | 2022-03-21 | 573 | 7 | usdk | USDK | 2020-06-13 | 2022-03-21 | 647 | 7 | ||

| omg | OMG Network | 2017-07-15 | 2022-03-21 | 1711 | 7 | 3 | usdt | Tether | 2014-10-06 | 2022-03-21 | 2724 | 7 | 2,3 |

| pax | Paxos Standard | 2018-11-30 | 2022-03-21 | 1208 | 7 | 3 | usdt_eth | TetherETH | 2017-11-28 | 2022-03-21 | 1575 | 7 | 3 |

| paxg | PAX Gold | 2020-02-15 | 2022-03-21 | 766 | 7 | 3 | usdt_omni | usdt_omni | 2014-10-06 | 2022-03-21 | 2724 | 7 | 2,3 |

| pay | TenX | 2017-10-03 | 2022-03-21 | 1631 | 7 | 3 | usdt_trx | TetherTRON | 2019-04-16 | 2022-03-21 | 1071 | 7 | 3 |

| perp | Perpetual Protocol | 2021-02-04 | 2022-03-21 | 411 | 7 | vtc | Vertcoin | 2014-01-29 | 2022-03-21 | 2974 | 8 | 1,2,3 | |

| poly | Polymath | 2018-06-15 | 2022-03-21 | 1376 | 7 | 3 | wbtc | Wrapped Bitcoin | 2018-11-27 | 2022-03-21 | 1211 | 7 | 3 |

| powr | Power Ledger | 2017-11-02 | 2022-03-21 | 1601 | 7 | 3 | weth | Wrapped Ether | 2017-12-18 | 2022-03-21 | 1555 | 7 | 3 |

| ppt | Populous | 2017-09-20 | 2022-03-21 | 1644 | 7 | 3 | wnxm | Wrapped NXM | 2020-08-26 | 2022-03-21 | 573 | 7 | |

| qash | QASH | 2017-11-06 | 2022-03-21 | 1597 | 7 | 3 | wtc | Waltonchain | 2017-08-28 | 2022-03-21 | 1667 | 7 | 3 |

| qnt | Quant | 2019-03-16 | 2022-03-21 | 1102 | 7 | 3 | xaut | Tether Gold | 2020-02-24 | 2022-03-21 | 757 | 7 | 3 |

| ren | Ren | 2018-12-07 | 2022-03-21 | 1201 | 7 | 3 | xem | NEM | 2015-04-01 | 2022-03-21 | 2547 | 2 | 2,3 |

| renbtc | renBTC | 2020-05-13 | 2022-03-21 | 678 | 7 | 3 | xlm | Stellar | 2015-09-30 | 2022-03-21 | 2365 | 7 | 2,3 |

| rep | Augur | 2016-10-04 | 2022-03-21 | 1995 | 7 | 3 | xmr | Monero | 2014-05-20 | 2022-03-21 | 2863 | 3 | 2,3 |

| rev_eth | rev_eth | 2020-03-26 | 2022-03-21 | 726 | 7 | 3 | xrp | XRP | 2014-08-15 | 2022-03-21 | 2776 | 7 | 2,3 |

| sai | Sai | 2017-12-23 | 2019-11-30 | 708 | 7 | xtz | Tezos | 2018-06-30 | 2022-03-21 | 1361 | 7 | 3 | |

| snt | Status | 2017-06-20 | 2022-03-21 | 1736 | 7 | 3 | xvg | Verge | 2017-09-30 | 2022-03-21 | 1634 | 8 | 3 |

| snx | Synthetix | 2020-04-09 | 2022-03-21 | 712 | 7 | 3 | yfi | yearn.finance | 2020-07-25 | 2022-03-21 | 605 | 7 | |

| srm | Serum | 2020-08-11 | 2022-03-21 | 588 | 7 | zec | Zcash | 2016-10-29 | 2022-03-21 | 1970 | 8 | 3 | |

| sushi | SushiSwap | 2020-09-01 | 2022-03-21 | 567 | 7 | zrx | 0x | 2017-08-11 | 2022-03-21 | 1684 | 7 | 3 | |

| swrv | Swerve | 2020-09-22 | 2022-03-21 | 546 | 7 | ||||||||

| trx | TRON | 2018-06-25 | 2022-03-21 | 1366 | 2 | 3 | |||||||

| trx_eth | TronETH | 2017-10-07 | 2018-06-25 | 262 | 7 |

| Variable Name | Coding Coinmetrics | Description |

|---|---|---|

| Active_Users | AdrActCnt | The number of unique active daily addresses |

| Total_Users | AdrBalCnt | The number of unique addresses that hold any amount of native units of that currency |

| Total_Users_USD100 | AdrBalUSD100Cnt | The number of unique addresses that hold at least 100 USD of native units of that currency |

| Total_Users_USD10 | AdrBalUSD10Cnt | The number of unique addresses that hold at least 10 USD of native units of that currency |

| SER | SER | The supply equality ratio, i.e. the ratio of supply held by addresses with less than 1 over 10 millionth of the current supply to the top one percent of addresses with the highest current supply |

| Transactions | TxCnt | The number of daily initiated transactions |

| Velocity | VelCur1yr | The velocity of supply in the current year, which describes the the ratio of current supply to the sum of the value transferred in the last year |

| Period | Sorting | GRF | QRF | QR | CAV | GJR-GARCH | Hist | GRF-X | QRF-X | QR-X | GARCH-X |

|---|---|---|---|---|---|---|---|---|---|---|---|

| High Group | |||||||||||

| SER | |||||||||||

| 1 | 1 Highest | 0.16 | 0.92 | 0.00 | 0.00 | 0.12 | 0.00 | 0.01 | 0.00 | 0.00 | 0.00 |

| 2 | 5 Highest | 0.16 | 0.08 | 0.20 | 0.19 | 0.11 | 0.08 | 0.13 | 0.07 | 0.00 | 0.00 |

| 3 | 15 Highest | 0.47 | 0.05 | 0.22 | 0.11 | 0.21 | 0.01 | 0.51 | 0.12 | 0.00 | 0.00 |

| Number of Active Users | |||||||||||

| 1 | 1 Highest | 0.16 | 0.92 | 0.00 | 0.00 | 0.12 | 0.00 | 0.01 | 0.00 | 0.00 | 0.00 |

| 2 | 5 Highest | 0.16 | 0.09 | 0.40 | 0.19 | 0.11 | 0.08 | 0.13 | 0.07 | 0.00 | 0.00 |

| 3 | 15 Highest | 0.38 | 0.06 | 0.05 | 0.01 | 0.21 | 0.00 | 0.17 | 0.18 | 0.00 | 0.00 |

| 7-Day Lagged Standard Deviation | |||||||||||

| 1 | 1 Highest | 0.16 | 0.02 | 0.03 | 0.00 | 0.01 | 0.00 | 0.00 | 0.00 | 0.00 | 0.02 |

| 2 | 12 Highest | 0.29 | 0.06 | 0.23 | 0.21 | 0.20 | 0.12 | 0.16 | 0.05 | 0.00 | 0.00 |

| 3 | 60 Highest | 0.19 | 0.02 | 0.03 | 0.01 | 0.23 | 0.01 | 0.21 | 0.05 | 0.00 | 0.04 |

| Low Group | |||||||||||

| SER | |||||||||||

| 1 | 4 Lowest | 0.13 | 0.28 | 0.10 | 0.10 | 0.02 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| 2 | 10 Lowest | 0.29 | 0.10 | 0.06 | 0.31 | 0.25 | 0.10 | 0.32 | 0.06 | 0.00 | 0.09 |

| 3 | 62 Lowest | 0.07 | 0.04 | 0.03 | 0.02 | 0.32 | 0.00 | 0.18 | 0.07 | 0.00 | 0.06 |

| Number of Active Users | |||||||||||

| 1 | 4 Lowest | 0.13 | 0.28 | 0.10 | 0.10 | 0.02 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| 2 | 10 Lowest | 0.42 | 0.09 | 0.06 | 0.31 | 0.20 | 0.10 | 0.26 | 0.06 | 0.00 | 0.09 |

| 3 | 62 Lowest | 0.13 | 0.04 | 0.07 | 0.03 | 0.32 | 0.01 | 0.21 | 0.07 | 0.00 | 0.07 |

| 7-Day Lagged Standard Deviation | |||||||||||

| 1 | 4 Lowest | 0.13 | 0.42 | 0.10 | 0.10 | 0.07 | 0.00 | 0.01 | 0.00 | 0.00 | 0.00 |

| 2 | 3 Lowest | 0.00 | 0.11 | 0.00 | 0.32 | 0.00 | 0.00 | 0.00 | 0.06 | 0.00 | 0.00 |

| 3 | 17 Lowest | 0.06 | 0.47 | 0.24 | 0.30 | 0.60 | 0.00 | 0.15 | 0.45 | 0.00 | 0.00 |

| GRF-X vs.: | GRF | QRF | QR | CAV | GJR-GARCH | Hist | QRF-X | QR-X | GARCH-X |

|---|---|---|---|---|---|---|---|---|---|

| Share of GRF With Better Performance | |||||||||

| Period 1 | 0.40 | 1.00 | 0.80 | 0.60 | 0.80 | 1.00 | 1.00 | 1.00 | 1.00 |

| Period 2 | 0.60 | 1.00 | 0.67 | 0.87 | 0.80 | 1.00 | 1.00 | 1.00 | 1.00 |

| Period 3 | 0.55 | 0.90 | 0.66 | 0.75 | 0.66 | 0.90 | 0.94 | 0.96 | 0.73 |

| Full Data | 0.54 | 0.89 | 0.72 | 0.76 | 0.73 | 0.83 | 0.92 | 0.97 | 0.76 |

| Share of GRF With Significantly Better Performance | |||||||||

| Period 1 | 0.00 | 0.20 | 0.20 | 0.00 | 0.20 | 1.00 | 1.00 | 1.00 | 0.60 |