On the dependence structure of the trade/no trade sequence of illiquid assets

Abstract

In this paper, we propose to consider the dependence structure of the trade/no trade categorical sequence of individual illiquid stocks returns. The framework considered here is wide as constant and time-varying zero returns probability are allowed. The ability of our approach in highlighting illiquid stock’s features is underlined for a variety of situations. More specifically, we show that long-run effects for the trade/no trade categorical sequence may be spuriously detected in presence of a non-constant zero returns probability. Monte Carlo experiments, and the analysis of stocks taken from the Chilean financial market, illustrate the usefulness of the tools developed in the paper.

Keywords:

Time-varying illiquidity levels; Categorical financial time series; Serial dependence.

JEL Classification: C13; C22; C58.

1 Introduction

In the time series econometrics literature, it is widely documented that neglected non-stationary behaviors can generate misleading assessments. A classical example is given by the spurious regression described in Phillips (1987). Since the seminal papers of Mikosch and Stărică (2004), Stărică and Granger (2005), and Engle and Rangel (2008), a huge amount of papers have explored the possibility that an unconditionally non-constant variance can display spurious long memory features. This led to contributions proposing new tools for a correct assessment of time series dynamics, see Phillips and Xu (2006), Cavaliere and Taylor (2008) or Patilea and Raïssi (2014) among many others. However, at the best of our knowledge, there is no contribution in this spirit on the behavior of the daily zero returns probability of illiquid stocks. In this paper, we aim to investigate the dependence structure of the trade/no trade sequence, i.e the process defined such that if a daily price change is observed at , and 0 if not. It is suggested that long range dependence effects, could possibly be explained by non-constant illiquidity levels in time, i.e., is non-constant. As a consequence, tools for analyzing the dependence structure of the daily trade/no trade structure corrected from the non-stationary probability are developed.

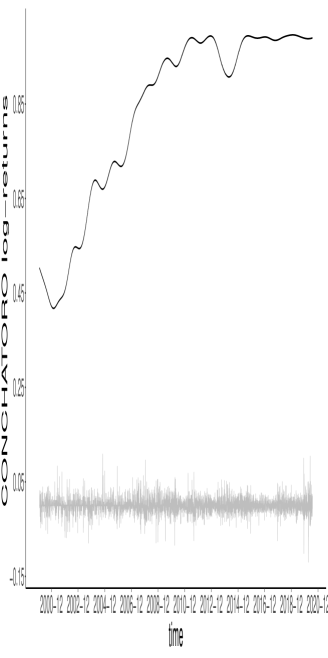

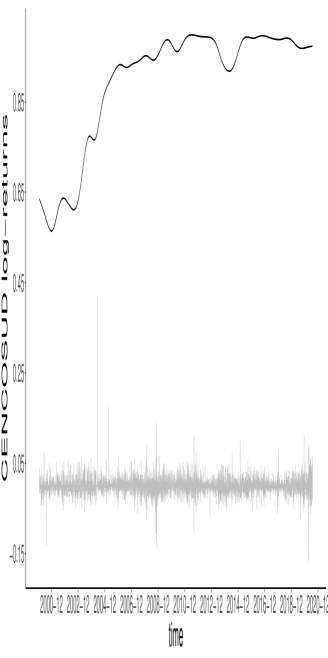

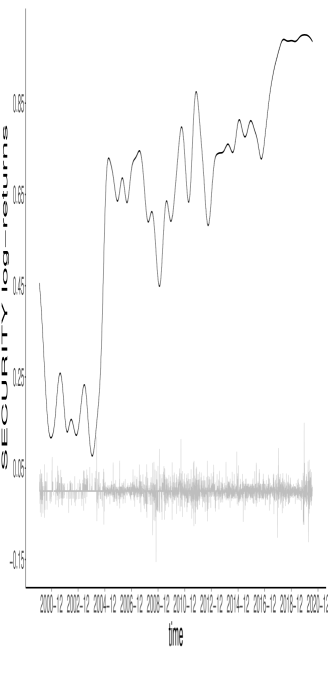

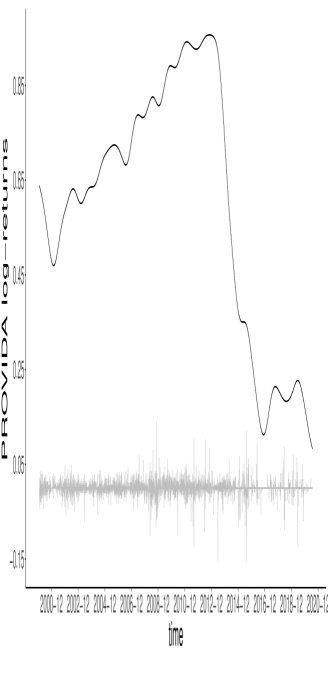

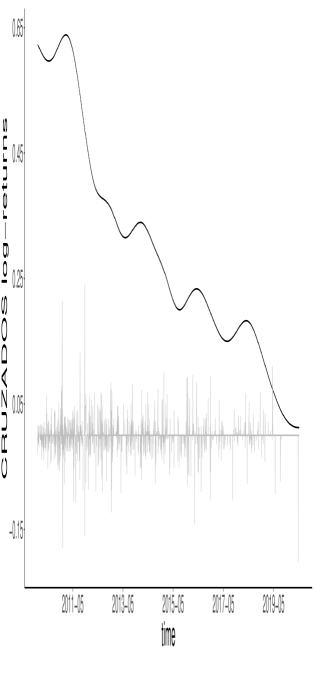

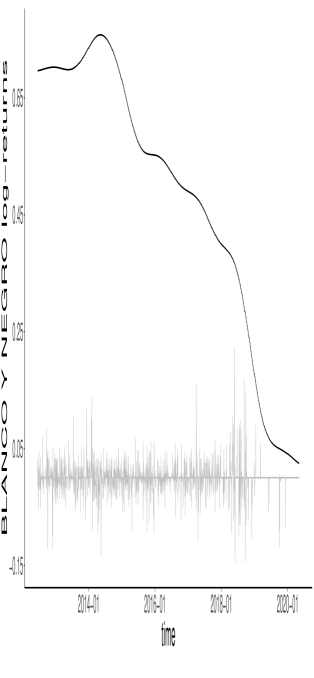

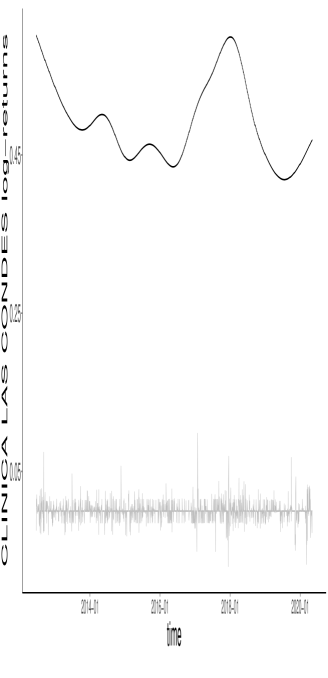

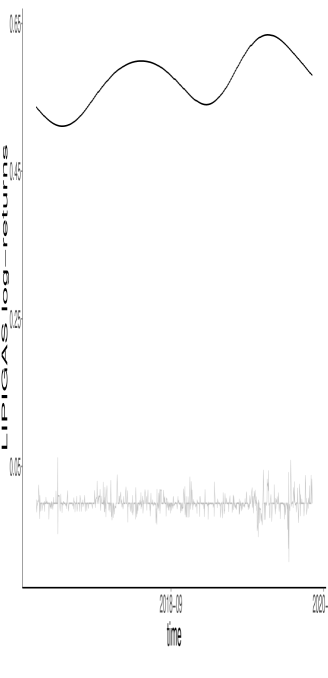

Illiquid stocks exhibiting a large amount of daily zero returns are commonly observed in all markets, see e.g. Lesmond (2005) for emerging markets. In order to motivate the above arguments, examples taken from the chilean stock market (Santiago Stock Exchange, SSE) are provided in Figure 1-4.222The author is grateful to Andres Celedon for research assistance. The main stocks indexes of the SSE are the IPSA (the 30 most liquid stocks) and the IGPA (comprising the 30 stocks of the IPSA, plus other stocks according to some criteria). The stocks presented here are part of the IGPA, but not of the IPSA. The daily returns of the stocks are displayed together with their smoothed . In view of the different panels in Figure 1-3, trends and abrupt breaks can be seen in the daily trade probability. Such behaviors can be backed up by a variety of facts. In Figure 1, the common increasing trends could be explained by a general development of the SSE. Indeed, during the period 2000-2008 the Chilean GDP growth was relatively elevated, which made the SSE reached some kind of maturity. On the other hand, abrupt shifts are often the product of particular events in the company history. For instance, the quick increase of the daily price change probability for the Security bank stock, may be explained by the merger by absorption of the Dresdner Bank Lateinamerika in September 2004. In addition, the Security Bank issued more than 32.8 millions new stocks after the capital increase announced during the extraordinary shareholders meeting by December 29th, 2004. Conversely, the quick decrease of the daily trade probability for the Provida stock seems to be a consequence of the take-over bid of Metlife on Provida during September 2013. As a consequence, we can conclude that a structural break in the zero returns probability, has occurred during the above mentioned period, with some degree of confidence. In Figure 3, long-run decreasing behaviors can be observed. All these observations suggest to allow for a time-varying when analyzing the dependence structure of . Note that investigating the illiquidity sequence dynamics can be useful to understand various facts on the underlying asset. The methodology developed here may be used to identify the relevant past of to consider for modelling financial time series. In a stationary framework, reference can be made to Moysiadis and Fokianos (2014) for predicting , or the GARCH models with covariates considered in Francq and Thieu (2019).

The article is structured as follows. In Section 2, the general framework of the study is presented. We investigate the analysis of the dependence structure of the when is constant in Section 2.1. The consequences of neglecting a time-varying in the dependence structure of the trade/no trade sequence are highlighted in Section 2.2. Then, adaptive tools that adequately take into account a non-constant are developed. Monte Carlo experiments and real data analysis illustrate our theoretical findings in Section 3.

2 The theoretical framework and diagnostic tools

Let us consider a one-period profit-and-loss random variable . It is assumed that are observed, with the sample size. Recall that if , and otherwise. We make the following assumption to describe abrupt or gradual changes in the stock’s illiquidity degree.

Assumption 1 (Non constant probability).

The time-varying probabilities are given by where is a non-constant deterministic function, such that on the interval , and satisfies a piecewise Lipschitz condition on .333For , the function is set constant, that is . Throughout the paper, the piecewise Lipschitz condition means: there exists a positive integer and some mutually disjoint intervals with such that where is a Lipschitz smooth function on respectively.

The rescaling device of Dahlhaus (1997) is often used to describe long run effects (see Cavaliere and Taylor (2007), Xu and Phillips (2008), Patilea and Raïssi (2013) and Wang, Zhao and Li (2019) among others). Note that the double subscript is avoided to simplify the notations.

The specification in Assumption 1 is quite general, as it allows for patterns commonly observed in practice, such as trends or abrupt breaks. As we are interested in testing the independence of , the framework given by Assumption 1 is sufficient, with no need to consider (possibly stochastic) probabilities conditional to some past information. Indeed, as usual a test is built under some null hypothesis, i.e. independent in our case. The tools developed here may be mostly used in an identifying step to some modelling task developed in, e.g. Moysiadis and Fokianos (2014). Our approach is similar to the continuous time series analysis methodology. Indeed, it is usual to study the correlation structure of (respectively powers of ) in a first step. Then, if some correlations are found significant, a model is estimated for the (stochastic) conditional expectation (respectively the volatility) using for instance ARMA (respectively GARCH) models.

2.1 The constant zero returns probability case

In this part, we assume that is strictly stationary, i.e. the particular case where the function is constant. Then, for testing the short run dependence in the sequence, the following hypotheses are considered

vs.

taking a relatively small . The hypothesis suggests the presence of a dependence structure for . Let us introduce

The statistic

can be used for deciding with small . On the other hand, for large , the components of may be plotted to assess some persistency, or long-run effects, in the dependence structure of . From the above, the tools for assessing some serial dependence are built under , that is an iid process. The following proposition gives the asymptotic behavior of in the stationary framework. The convergence in distribution is denoted by .

Proposition 2.1.

Suppose that is iid. Then, as we have,

| (1) |

where stands for the identity matrix of dimension .

The iid assumption is made to detect any short-run dependence structure in the sequence using . On the other hand, persistency or long-run effects may be highlighted plotting together with the confidence intervals obtained from (1). Note that such a plot is similar to an autocorrelation function (ACF) plot. However, as the sequence is categorical, and since we decide that is an independent sequence if all the components of are not significant, we prefer to use the term "dependence plots". For instance, the dependence plots of the stationary Lipigas and CLC stocks in Figure 6, suggest that the sequence is 1-dependent for these two stocks. The reader is referred to Brockwell and Davis (2006), Definition 6.4.3, for the -dependent processes. We end this section by mentioning the ability of the statistic to detect any dependence between daily trade/no trade events. The almost sure convergence is denoted by .

Proposition 2.2.

Suppose that is strictly stationary ergodic, such that holds true. Then, we have , where is a vector of constants with at least a non-zero component.

The proof of Proposition 2.2 is a direct consequence of the Ergodic Theorem (see Francq and Zakoïan (2019), Theorem A.2), and is therefore skipped. The test consists in rejecting , if , where is the th quantile of the distribution.

2.2 The non-constant zero returns probability case

Let us first underline, that the statistics based on the ’s, are not adequate for investigating the dependence structure of the sequence, when is time-varying. Indeed, under Assumption 1, and assuming that is independent, it can be shown that

| (2) |

and using similar arguments to that of the proof of Proposition 2.4 below. If we assume that is non-constant, then in general. As a consequence, the tools introduced in the above section can lead to a spurious detection of a dependence, even for large lags . In view of the stocks considered in this paper, changes in the non-zero returns probabilities are commonly observed in practice for a variety of facts. For this reason, new tools taking into account the framework given by Assumption 1 are proposed.

In this part, we wish to test

vs.

for all , taking small. In a first step, we suppose that the ’s are known. Later, feasible statistics will be proposed. In view of , a cumulative sums (CUSUM) statistic as

| (3) |

should be used, where

and denotes the integer part of a real number. Accordingly to , suppose that is independent, and assume that Assumption 1 holds true. Then we have

| (4) |

as , where , is a standard Brownian motion, and . The proof of the above result is provided in the Appendix. It can be seen that the asymptotic distribution of is non-standard, and have to be approximated using for instance bootstrap methods. Nevertheless, as the supremum is taken, and noting that the time-varying should be estimated nonparametrically to make feasible tools, it can be difficult to control the type I error for finite samples. In addition, noting that the variance of is not constant, the maximum value is more likely to be attained in high variance periods. This could make difficult to detect alternatives for periods where the variance is low.

For all these reasons, tools built using the full sample are considered, although leads to compare and , where . Indeed, this allows to avoid the drawbacks described above, at the cost of a loss of power in the particular case , with . Then, let us introduce

| (5) |

In order to test , , taking small, the test statistic

| (6) |

where

can be used. The following propositions give the asymptotic behavior of .

Proposition 2.3.

Suppose that the sequence is independent, and fulfills Assumption 1. Then as

where , and

In addition, we have

Proposition 2.4.

Suppose that Assumption 1 holds true. Under with , then as , , where is a vector of constants with at least a non-zero component.

In view of , the process is assumed independent but not necessarily identically distributed in Proposition 2.3. In addition, it can be seen that taking the full sample in , we only need to apply a classical Heteroscedasticity Consistent (HC) correction to handle a time-varying . Considering , the usual bounds can be used to assess the dependence horizon of .

For a small , and considering a fixed asymptotic level , the test rejects if , where we recall that is the th quantile of the distribution. Note that the critical values for the statistic based on are standard, on the contrary to the cumulative sums in . If is constant, then , and we retrieve the result of Proposition 2.1. Alternatively, taking a large , a plot of can be examined to analyze persistency or long-run effects in . Proposition 2.4 shows the ability of our tools to detect some dependence for , but provided that .

We now consider a feasible statistic for analyzing the dynamics of the process. Let us introduce first the kernel estimator of the non-constant probability

with , and

where is a kernel function on the real line, and is the bandwidth fulfilling the following conditions.

Assumption 2 (Kernel and bandwidth).

-

(a)

is a continuous kernel function defined on the real line with compact support, such that for some finite real number , and .

-

(b)

As , .

Plugin the above kernel estimator in (7), we get the adaptive dependence structure estimation for the first lags:

| (7) |

where

The following proposition states the asymptotic equivalence between and .

Proposition 2.5.

We are now in position to introduce the following feasible test statistic

| (8) |

where

3 Numerical experiments

In this section, we first study the finite sample behaviors of the different tools introduced in the paper by means of Monte Carlo experiments. Then the real data taken from the Santiago stock exchange will be considered.

3.1 Monte Carlo experiments

3.1.1 Empirical size

We simulated independent trajectories of independent according to the following cases:

-

1-

The probability is constant: .

-

2-

The probability is time-varying: where for , for , and for .

The sample sizes are . The nominal asymptotic level of the tests is . Tables 2 and 3 display the outputs of the and tests. Tables 5 and 6 give the relative frequencies where the components of and are outside its 95% confidence bounds.

From Tables 2 and 5, it can be seen that the adaptive and have similar results to those of the and when is constant and is independent. This can be explained by the fact that all the tools presented in the paper are all valid in the case 1. Nevertheless, from Tables 3 and 6, we can notice that the and do not display satisfactory outputs as the relative rejection frequencies tend to 100% as the sample size is increased. In particular, for large , can spuriously suggest the existence of long memory effects for the trade/no trade sequence. Clearly this is the consequence of the non-constant zero return probability. In contrast, we can see that the adaptive and have a good control of the type I error in general.

3.1.2 Empirical power

We simulated of the following sequence inspired by Romano and Thomb (1996): , where is an iid sequence such that is constant. Note that in view of the empirical size part, the comparison is fair as is constant. For conciseness, we only display the outputs for the and tests in Table 4. The results for the and lead to similar results. When the sample is small, we can note some loss of power of the when compared to the test. This can be explained by the non-parametric estimation of . However, the abilities of detecting a dependence structure are similar for sample sizes commonly encountered in practice.

3.2 Real data analysis

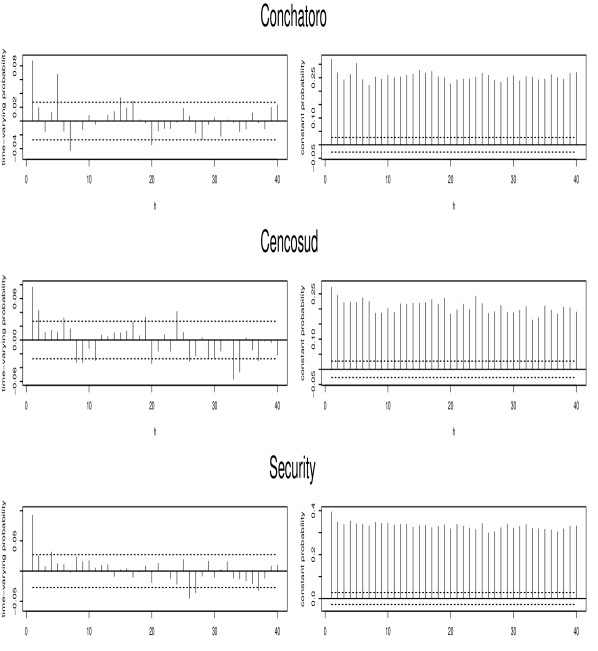

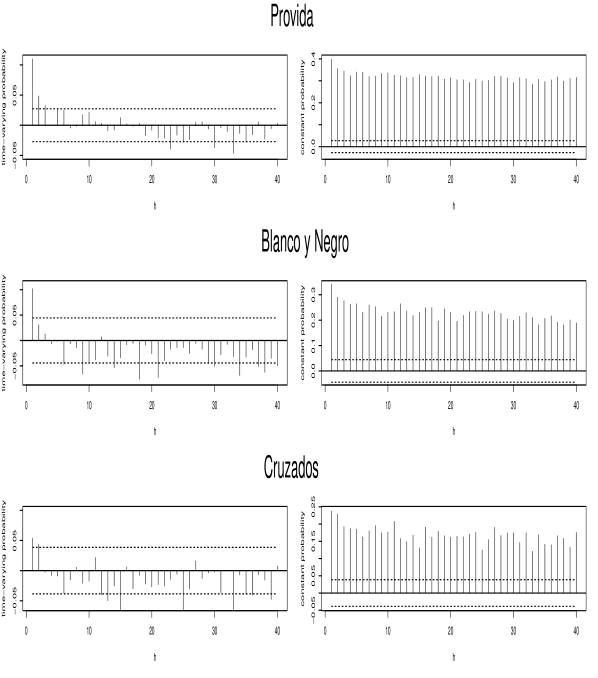

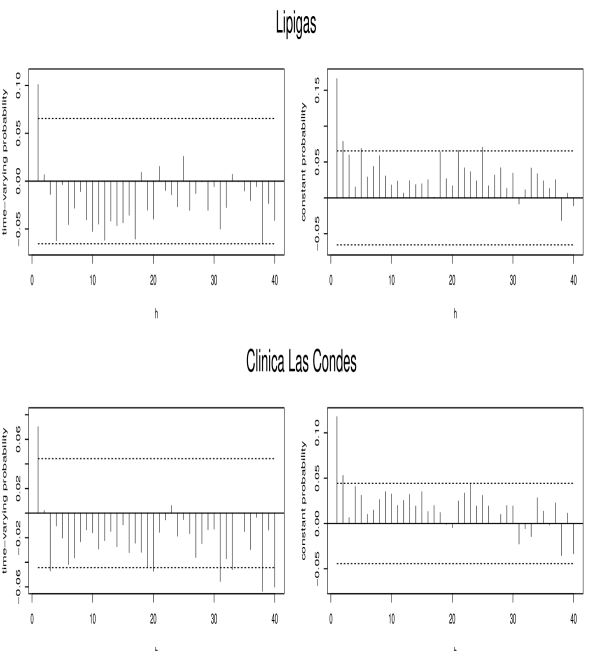

The dependence structure of different stocks taken from the Santiago Stock market are investigated. Recall that the behaviors of for these stocks are described in the Introduction (in particular see Figures 1-4). The sample sizes and the empirical means of the ’s are given in Table 1. The effects of smooth long run changes and abrupt breaks are illustrated considering the Conchatoro, Cencosud, Security, Provida, Cruzados, Blanco y Negro stocks, see Figure 5. The stationary case is studied using the Lipigas and CLC stocks, see Figure 6.

From Figure 5, it can be seen that the lead to detect long-run dependence in the process. Nevertheless, it is likely that such a long-run dependence is spurious as different kinds of non-constant can be observed for these stocks. Conversely, when the time-varying is adequately taken into account by using the , the dependence structure seems only short-run. Let us now study the stationary Lipigas and CLC stocks. From Figure 6, it emerges that when seems constant, the and the lead to the same conclusion: the dependence structure is again short-run. Note that for all the stocks which outputs are displayed in Figures 5 and 6, the rejects the independence hypothesis at the 5% level whether the seems constant or not (not displayed here).

4 Conclusion

Determining the relevant past of the daily price changes/no change categorical sequence may be of interest for financial times series modelling. As an example, note that the sequence shares the clustering properties of the volatility in many cases, see Figures 1-4. Hence, our tools could help to decide if can be used as a covariate in some volatility models, see e.g. Francq and Thieu (2019) for the GARCH-X models. Also, past values of such a series are considered to specify the conditional probability of price changes in Moysiadis and Fokianos (2014). Nevertheless, spurious persistency or long-run effects assessments for the daily price changes/no change sequence may be avoided taking into account a potential non-stationary behavior in the data. It is found that the dependence structure of is short-run in general.

References

-

Brockwell, P.J., and Davis, R.A. (2006) Times Series: Theory and Methods. 2nd edition, Springer, New York.

-

Cavaliere, G., and Taylor, A.M.R. (2007) Time-transformed unit-root tests for models with non-stationary volatility. Journal of Time Series Analysis 29, 300-330.

-

Cavaliere, G., and Taylor, A.M.R. (2008) Bootstrap Unit Root Tests for Time Series with Nonstationary Volatility. Econometric Theory 24, 43-71.

-

Dahlhaus, R. (1997) Fitting time series models to nonstationary processes. Annals of Statistics 25, 1-37.

-

Davidson, J. (1994) Stochastic limit theory. Oxford University Press. New York.

-

Engle, R.F., and Rangel, J.G. (2008) The spline GARCH model for unconditional volatility and its global macroeconomic causes. Review of Financial Studies 21, 1187-1222.

-

Francq, C. and Thieu, L.Q. (2019) QML inference for volatility models with covariates. Econometric Theory 35, 37-72.

-

Francq, C., and Zakoïan, J-M. (2019) GARCH models : structure, statistical inference, and financial applications. Wiley.

-

Hansen, B.E. (1992) Convergence to stochastic integrals for dependent heterogeneous processes. Econometric Theory 8, 489-500.

-

Lesmond, D.A. (2005) Liquidity of emerging markets. Journal of Financial Economics 77, 411–452.

-

Mikosch, T., and Stărică, C. (2004) Nonstationarities in financial time series, the long- range dependence, and the IGARCH effects. Review of Economics and Statistics 86, 378-390.

-

Moysiadis, T., and Fokianos, K. (2014) On binary and categorical time series models with feedback. Journal of Multivariate Analysis 131, 209-228.

-

Patilea, V., and Raïssi, H. (2013) Corrected portmanteau tests for VAR models with time-varying variance. Journal of Multivariate Analysis 116, 190-207.

-

Patilea, V., and Raïssi, H. (2014) Testing second order dynamics for autoregressive processes in presence of time-varying variance. Journal of the American Statistical Association 109, 1099-1111.

-

Phillips, P.C.B. (1987) Time series regression with a unit root. Econometrica 55, 277-301.

-

Phillips, P.C.B., and Xu, K.L. (2006) Inference in autoregression under heteroskedasticity. Journal of Time Series Analysis 27, 289-308.

-

Romano, J. P., and Thombs, L. A. (1996) Inference for autocorrelations under weak assumptions. Journal of the American Statistical Association 91, 590-600.

-

Sen, P. K., and Singer, J. M. (1993) Large Sample Methods In Statistics. Chapman & Hall.

-

Stărică, C., and Granger, C. (2005) Nonstationarities in stock returns. Review of Economics and Statistics 87, 503-522.

-

Wang, S., Zhao, Q., and Li, Y. (2019) Testing for no-cointegration under time-varying variance. Economics Letters 182, 45-49.

-

Xu, K.L., and Phillips, P.C.B. (2008) Adaptive estimation of autoregressive models with time-varying variances. Journal of Econometrics 142, 265-280.

Proofs

Proof of Proposition 2.1.

Firstly, note that we have , so that

where . Let us define . From the Central Limit Theorem (CLT) for martingale difference sequences (see Theorem A.3 in Francq and Zakoïan (2019)), we have

where is a dimensional diagonal matrix, with diagonal component . On the other hand, it is easy to see that . Hence, the result follows from the Slutsky Lemma. ∎

Proof of (4).

Let and

The sequence is a martingale difference, such that , from the Lipschitz condition with a finite number of breaks in Assumption 1. Then from Theorem 2.1 of Hansen (1992), we obtain

The desired result follows from the Continuous Mapping Theorem. ∎

Proof of Proposition 2.3.

Note that . Then using the Central Limit Theorem for independent but heterogeneous sequences, see Davidson (1994), Theorem 23.6, we have

where is obtained using some computations, and since is independent. On the other hand, from the Kolmogorov SLLN for independent but non-identically random variables (see, for instance, Sen and Singer (1993), Theorem 2.3.10), we have

Hence, the first result of Proposition 2.3 follows from the Slutsky Lemma. Now, for the convergence of , using again the Kolmogorov SLLN and some computations, we have

∎

Proof of Proposition 2.4.

From the Kolmogorov SLLN for independent but non identically random variables (see, Sen and Singer (1993), Theorem 2.3.10), and using some computations, we have

from the dominated convergence Theorem, and for any . Hence, under the result follows. ∎

Proof of Proposition 2.5.

In this proof similar arguments to that of the proof of Theorem 2 in Xu and Phillips (2008) are considered. As the break number is finite, we assume that the function is continuous, without a loss of generality. Let us introduce the short notations

and . We can write

From , is an independent process, such that . In addition, from Lemma A(c) in Xu and Phillips (2008), we have . In view of the above arguments, deduce that

Thus, we write

| (9) |

On the other hand, we have

where the last equality is obtained for small enough , and since a compact support is assumed for in Assumption 2(a). Using the Lipschitz condition in Assumption 1, deduce that

| (10) |

Now, writing

Tables and Figures

| n | ||

|---|---|---|

| CONCHATORO | 5188 | 0.83 |

| CENCOSUD | 5198 | 0.89 |

| SECURITY | 5188 | 0.62 |

| PROVIDA | 5179 | 0.59 |

| CRUZADOS | 2584 | 0.29 |

| BN | 1958 | 0.48 |

| LIPIGAS | 896 | 0.57 |

| CLC | 1958 | 0.49 |

| 200 | 400 | 800 | |

|---|---|---|---|

| 4.56 | 4.70 | 4.90 | |

| 4.88 | 4.76 | 4.94 |

| 200 | 400 | 800 | |

|---|---|---|---|

| 81.74 | 98.42 | 100.00 | |

| 4.88 | 5.56 | 5.62 |

| 100 | 200 | 400 | 800 | |

|---|---|---|---|---|

| 85.82 | 99.92 | 100.00 | 100.00 | |

| 75.54 | 99.56 | 100.00 | 100.00 |

| 1 | 2 | 3 | 4 | 5 | 20 | 40 | 60 | ||

|---|---|---|---|---|---|---|---|---|---|

| 4.38 | 4.28 | 4.86 | 4.52 | 4.28 | 4.02 | 2.64 | 1.78 | ||

| 4.64 | 4.24 | 5.08 | 4.64 | 4.48 | 4.16 | 2.90 | 1.88 | ||

| 4.84 | 4.98 | 4.68 | 5.06 | 4.70 | 4.66 | 3.66 | 3.30 | ||

| 5.02 | 5.18 | 4.76 | 5.00 | 4.82 | 4.62 | 3.80 | 3.44 | ||

| 5.06 | 4.62 | 5.18 | 4.88 | 4.80 | 4.70 | 4.32 | 4.08 | ||

| 5.10 | 4.76 | 5.24 | 4.84 | 4.84 | 5.02 | 4.34 | 4.14 |

| 1 | 2 | 3 | 4 | 5 | 20 | 40 | 60 | ||

|---|---|---|---|---|---|---|---|---|---|

| 51.00 | 51.12 | 49.76 | 50.42 | 49.66 | 34.80 | 9.98 | 1.16 | ||

| 5.24 | 4.66 | 4.64 | 4.66 | 4.58 | 3.84 | 3.62 | 2.48 | ||

| 79.02 | 78.80 | 78.00 | 79.52 | 78.16 | 73.28 | 61.78 | 42.16 | ||

| 5.48 | 5.32 | 5.08 | 5.42 | 5.24 | 4.60 | 4.06 | 4.02 | ||

| 97.06 | 97.34 | 97.14 | 97.04 | 97.20 | 96.10 | 95.28 | 92.70 | ||

| 5.44 | 5.42 | 5.40 | 5.34 | 4.82 | 5.14 | 4.92 | 4.88 |