Impression Allocation and Policy Search

in Display Advertising

Abstract

In online display advertising, guaranteed contracts and real-time bidding (RTB) are two major ways to sell impressions for a publisher. For large publishers, simultaneously selling impressions through both guaranteed contracts and in-house RTB has become a popular choice. Generally speaking, a publisher needs to derive an impression allocation strategy between guaranteed contracts and RTB to maximize its overall outcome (e.g., revenue and/or impression quality). However, deriving the optimal strategy is not a trivial task, e.g., the strategy should encourage incentive compatibility in RTB and tackle common challenges in real-world applications such as unstable traffic patterns (e.g., impression volume and bid landscape changing). In this paper, we formulate impression allocation as an auction problem where each guaranteed contract submits virtual bids for individual impressions. With this formulation, we derive the optimal bidding functions for the guaranteed contracts, which result in the optimal impression allocation. In order to address the unstable traffic pattern challenge and achieve the optimal overall outcome, we propose a multi-agent reinforcement learning method to adjust the bids from each guaranteed contract, which is simple, converging efficiently and scalable. The experiments conducted on real-world datasets demonstrate the effectiveness of our method.

I Introduction

Online display advertising has become one of the most influential business, with $59.8 billion revenue in FY 2019 in US alone [1]. Typically when a user visits a publisher, e.g., a news website, there would be one or more ad impression opportunities generated in real time. Advertisers are able to acquire these opportunities to display their ads at certain cost and these cost eventually become the revenue of the publisher.

For a publisher, there are two major ways to sell impressions. The first one is through guaranteed contracts (also referred as guaranteed delivery [2]). A guaranteed contract is an agreement between an advertiser and a publisher by negotiating directly or by going through a programmatic guaranteed mechanism [3]. The contract usually specifies the contract payment amount, the campaign duration and the desired number of ad impressions. The advertiser typically makes the payment before the ad delivery starts and the publisher guarantees the desired number of ad impressions. The publisher is also responsible for any shortfall in the number of impressions delivered. A penalty is usually incurred based on the volume of under-delivery.

The second way to sell impressions is through real-time bidding (RTB). RTB allows advertisers to bid in real time for impressions and does not guarantee the impression volume for any advertiser [4]. In this paper, we focus on the second price auction [5]. For each impression opportunity, the advertiser who offers the highest bid wins the opportunity to display her ad. The cost of the winner is the second highest bid in the auction.

Despite the increasing popularity of RTB, there is still large amount of the online display advertising revenue generated from guaranteed contracts. For large publishers, simultaneously selling impressions through both guaranteed contracts and in-house RTB has become a popular choice. These publishers need to derive impression allocation strategies between guaranteed contracts and RTB. There are two main considerations when publishers strategically allocate their impressions:

-

1.

Maximizing the overall outcome: The overall outcome we consider in this paper consists of both revenue and contract impression quality (a formal definition can be found in Section II). Revenue represents the short-term value to the publisher. It associates with the revenue from guaranteed contracts, the revenue from RTB, and the contract violation penalties. Impression quality (e.g., click-through rate) of the guaranteed contracts reflects the long-term revenue to the publisher since advertisers of guaranteed contracts are more and more concerned with the impression qualities.

-

2.

Maintaining incentive compatibility in RTB: The publisher also needs to take care of the auction mechanism of its in-house RTB. An incentive compatible auction mechanism111A mechanism is called incentive-compatible if every participant can achieve the best outcome to themselves just by acting according to their true preferences. is essential to facilitate truthful bidding and maximize the efficiency.

Besides the considerations above, what makes it even more challenging is the unstable traffic pattern in real-world applications. Strategies derived based on a known collection of impressions [6, 7, 8] or stochastic arrival models [9, 10, 11, 12] may be inferior in such scenarios. First, the traffic volume is vulnerable to unexpected changes such as holiday sale events. Second, usually concurrent with the traffic volume changes, the market price distribution of the impressions can also deviate from the empirical one. Finally, the unpredictable advertiser behaviors in RTB including modifying budget, bid, and target audience can also make the traffic pattern complicated and dynamic [13].

To derive an optimal impression allocation strategy that takes into account the above-mentioned considerations and challenges, we propose to analyze the problem from another perspective. Since the allocation is non-trivial and the environment is highly dynamic, can the guaranteed contracts also participate in the real-time auctions so that they can also enjoy the liquidity and the impressions can be fully auctioned? More specifically, can each guaranteed contract be treated as a bidding agent which is able to submit bids for individual impressions and the impression allocation is based on the submitted bids from both guaranteed contracts and RTB? We will show that such a setup can actually lead us to the optimal impression allocation strategy. For each impression, the optimal bids of each contract bidding agent are determined by a critical parameter , and the impression can be optimally allocated based on an auction mechanism with the bids from RTB and contract agents. It can be proved that the proposed mechanism results in the theoretically maximum outcome (more details see Section II). Meanwhile, the incentive compatibility, which is important for auction efficiency, is also maintained.

However, although the impressions can be allocated in such scheme, the optimal can only be obtained over a complete impression set. Hence, an adjustment policy is a necessity in real-world application, which aims to continuously adjust to the optimal one under the current state (i.e., indicators about contracts’ fulfillment status and RTB information). Meanwhile, since each agent has its own parameter , and all the agents have a common goal of outcome maximization, it is intuitive to apply multi-agent reinforcement learning (MARL) to model this process. However, MARL method is faced with some common challenges in industrial scenario, such as model complexity, scalability and low converging efficiency. Thus, we carefully design our modeling process and present a simple, scalable, quickly converging MARL method.

To evaluate the effectiveness of our method, we conducted experiments on large-scale real-world datasets. Compared with other methods, we observed substantial improvements on impression allocation results. Meanwhile, the converging efficiency, scalability of our MARL method are also verified empirically. Our main contributions can be summarized as follows:

-

1.

We propose an optimal impression allocation strategy in display advertising with both guaranteed contracts and in-house RTB. The proposed strategy maintains incentive compatibility in RTB.

-

2.

We devise an industrial applicable MARL method to dynamically optimize impression allocation outcome, which is simple, scalable and quickly converging.

-

3.

Empirical studies on real-world industrial dataset demonstrate the scalability and efficiency of our MARL method.

The rest of this paper is organized as follows. The optimal impression allocation strategy is derived associated with optimal bidding function in Section II. In Section III, we present an efficient MARL method to learn the crucial parameter in bidding function. Empirical study is shown in Section IV, followed by the related work in Section V. We conclude the paper in Section VI.

II Optimal Impression Allocation

For the publishers who sell impressions through both guaranteed contracts and in-house RTB, one of their impression allocation motivations is to maximize the total revenue from both contracts and RTB. Meanwhile, the impression quality of the contracts can affect the satisfaction of the contract advertisers and therefore affect the long-term revenue. As illustrated by Fig. 1, the ultimate goal of impression allocation is to maximize the overall outcome, i.e., simultaneously maximize RTB revenue , contract revenue and contract impression quality. Besides, whether the RTB part is incentive compatible is also a critical issue to be considered.

II-A Problem Formulation

Suppose there are impressions indexed by to be allocated by the publisher. On the one hand, suppose that there are guaranteed contracts indexed by to be served. For each contract , let be the demand impression volume and be the unit price of each impression, so the prepaid contract revenue is . Suppose the contract violation penalty of contract for each undelivered impression is , that is, if the number of impressions served to contract is fewer than , the publisher will have to be responsible for the under-delivery and the penalty is for each undelivered impression. On the other hand, for each impression , RTB will also provide a list of bids, of which we are mostly interested in the first and second highest bids and under the second price auction mechanism. If the impression is allocated to RTB, then the publisher will earn . Let be the binary indicator whether an impression is allocated to contract and obviously if then the impression is allocated to RTB. Then we are able to derive revenue from both guaranteed contracts and RTB. Specifically, the revenue from guaranteed contracts is , where is the impression under-delivery amount and the revenue from RTB is . For contract business, a publisher should consider the quality of the impressions allocated to contracts, since the result of poor impression quality (e.g., low CTR) would drastically affect the future investments on contract ads. In industrial application, it is common to introduce a trade-off parameter between the units of impression quality and revenue [6]. Thus, we let be the impression ’s quality for contract and be the quality weight222The quality weight can be also considered as a scaling parameter that converts quality into money., then the total contract impression quality is .

Our goal of impression allocation is to maximize the overall outcome, i.e., the sum of , and quality . One may curious about the reason why we do not consider the quality of the RTB part, this is mainly because the RTB part is fully auctioned and the impression quality is already considered in the bids of each advertiser in RTB, e.g., if an advertiser considers click as the quality of an impression, he or she can only bid with a click price. Hence, we formulate the problem of optimal impression allocation for outcome maximization as the following linear programming problem:

| s.t. | |||||||

II-B The Optimal Allocation Strategy

As demonstrated above, the optimal impression allocation can be obtained by solving (II-A) if the impressions are completely foreseen. However, the impression is unknown until the end of the day and almost impossible to predict since the unstable traffic pattern. Therefore we propose to solve the problem from a different perspective. That is, guaranteed contracts are regarded as bidding agents333Different from the bidding agents in RTB, the contract bidding agents do not have budget, and the delivered bids are only used for the impression allocation., whose bids are decided by the publisher, and participate in the real-time auctions together with the RTB ads. The impression allocation is finally decided by the auction results of RTB and contracts. In this section, we prove that such a setup can actually lead us to the optimal allocation strategy and derive the optimal bidding functions of contract bidding agents.

Theorem 1.

Suppose for each impression , every contract submits a bid . Let . Consider the allocation strategy that allocates impression to contract if and otherwise to RTB. The strategy results in the optimal solution of outcome maximization problem defined by (II-A) if the bid from each contract is:

| (1) |

where is the optimal solution to the dual problem of outcome maximization problem (LP1) and .

Proof.

The maximal revenue from RTB , along with the total payment from contracts can be considered as constants. Then, can be simplified as . Thus, the dual problem of (II-A) is as follows:

| (LP2) | |||||

| s.t. | (2) | ||||

Suppose the optimal solution to (II-A) and (LP2) are and respectively. We denote impression ’s bid of contract as . According to the complementary slackness theorem, we have

| (3) | |||||

| (4) |

:

- •

- •

In summary, for each impression , if we bid with for each contract , and allocate impressions with the strategy demonstrated in Eq. (5), then we achieve the the optimal allocation results of (II-A):

| (5) |

where . ∎

II-C Incentive Compatibility of RTB

Since simultaneously selling impressions through both guaranteed contracts and in-house RTB has become a popular choice for large publishers, the incentive compatibility of RTB should be seriously considered. If the auction mechanism in RTB is incentive compatible, truthful bidding strategy is facilitated for the advertisers who participate in the auction, and it will result in a locally envy-free equilibrium which maximizes the efficiency [5].

According to the allocation strategy presented in Section II-B, for each impression , we simply compare the max bid from contracts with the second highest bid from RTB, and then allocate the impression to the one with the higher bid. From the perspective of any RTB bidder, the social choice function is monotone in every bid submitted by a RTB bidder, i.e., the impression allocation result (True or False) is monotone with respect to her bids, and the critical value (payment) for the winning RTB bidder is still the second highest price . According to the Theorem 9.36 in [14], the optimal allocation strategy introduced in Section II-B will keep the incentive compatibility of RTB.

III A Practical MARL Method

Recall that all the guaranteed contracts are considered as bidders (publisher proxies) to compete with RTB bidders in the auction. The optimal bidding function of contracts is given by Eq. (1), and the remaining problem of impression allocation is the determination of the optimal bidding parameter . Since the traffic pattern is unstable and the impression set is unknown until the end of the day, it is impossible to obtain the optimal by solving the dual problem of (II-A). Thus, in the real-world scenario, we have to adjust the current (not optimal) according to the current state (e.g., contract fulfillment rate, cost per mille in RTB, etc.) to maximize the potential outcome. In this section, we first formulate this adjustment problem as a Markov Game, then we simplify the policy searching process based on an important property in our scenario, last we present an industry-applicable parameter adjustment approach via multi-agent reinforcement learning (MARL).

III-A Formulation as A Markov Game

We formulate the impression allocation process as an Markov Game, where there are contract agents and each agent adjusts its in order to achieve the global outcome maximization. A Markov game is defined by a set of states describing the status of impression allocation, a set of observations indicating the observed information of the current state from the perspective of agent , a set of actions where represents the action space of agent . At each time step , each agent observes and then delivers an action to adjust according to its policy . Then, the state transfers to a next state according to the state transition dynamics where is a collection of probability distributions over . The environment returns an immediate reward to each agent based on a function of current state and all the agents’ actions as . The goal of each agent is to maximize its the total expected return where is a discount factor and is the time horizon. The detailed information can be found as below:

-

:

The observation of agent at time step should in principle reflect the contract status, which mainly includes the following three parts: first, the time information, which tells the agent the current stage of the impression allocation process; second, the contract information, including demand fulfillment status and speed of contract ; third, the context information of other contracts’ fulfillment status, which facilitates the global optimization.

-

:

At time step , each agent delivers action to modify to , typically taking the form of , where is the unit under-delivery penalty of contract .

-

:

Since the goal of impression allocation is to maximize the presented in Section II-A, the reward is defined as the resulting of the auction between time step and . Specifically, let the impression set between time step and be , then .

-

:

We apply a model-free RL method to solve the impression allocation problem, so that the transition dynamics could not be explicitly modeled.

-

:

The reward discount factor is set to 1 since the optimization goal of the impression allocation problem is to maximize the return regardless of time.

Usually, the optimal policies in a Markov game are difficult to learn due to some common challenges such as high model complexity, unstable return (i.e., ) caused by joint agents’ updating in a sequential decision process. Fortunately, as for our problem, there is an important property that can simplify the policy searching process. Next, we first present this important property and then show the details of our method.

III-B The Sub-problem in Impression Allocation

In Theorem 1, we derive the optimal bidding function for the impression allocation problem. At each step, with contracts partially fulfilled, agents would face a sub-problem of impression allocation and are required to take actions based on the current state. We prove that the sub-problem can be formulated in the same form as (II-A) and the optimal action for each agent is shown by the following Theorem 2.

Theorem 2.

For a sub-problem at each time step , the optimal action sequence for each agent is to modify its current to the optimal , and keep it fixed for all its following time steps.

Proof.

At any time step , since contracts may have already won several impressions, the demand of contracts for the subsequent impressions are refreshed. Specifically, let be the impression that contract has won, be the remaining impression set at time step . For impression , the remaining demand of contract can be updated as , the impression under-delivery amount of contract as . Then, the components of can be updated as: , , and . Therefore, the sub-problem can be formulated as the following linear programming, which shares the same form of (II-A):

| s.t. | |||||||

Similarly, the optimal bid can be derived as , where is the optimal parameter of sub-problem at time step . Thus, for the sub-problem of impression allocation, the optimal action is to adjust the current parameter of contract to . After taking the optimal action, for any contract , the would be the optimal one. Thus, the following optimal actions would be keeping the parameters fixed until the end of the episode. ∎

III-C Multi-agent Reinforcement Learning to Impression Allocation (MARLIA)

Based on what has be introduced above, in this section, we present our policy searching method, named Multi-Agent Reinforcement Learning to Impression Allocation (MARLIA). Firstly, we apply an actor-critic reinforcement learning (RL) model [15] as the implementation of our method for its simplicity444Without loss of generality, other actor-critic RL models also can be applied in our scenario.. Secondly, to enhance the scalability and reduce the model complexity, we let all agents share a same model and be differentiated through context information included in each agent observation (e.g., other contracts’ fulfillment status). Thirdly, also most importantly, based on Theorem 2, the learning processes of actors and critics are simplified, which can be interpreted from the following two aspects:

-

•

At time step , the mission of each agent is to make a single optimal decision which adjusts current to and keep it fixed for the following time steps rather than sequentially adjusting it, which significantly reduces the learning difficulty.

-

•

The learning process of the critic is simplified as minimizing the difference between and where is exactly the outcome produced by the fixed parameters over the remaining impression set. Compared with common practice of updating towards (more details see temporal-difference method [15]), more clearly indicates whether the action would leads to a better final outcome. This makes the learning process of easier and, in turn, will boost the policy convergence.

To be more concrete, MARLIA is presented in Algo. 1.

IV Experimental Evaluation

In this section, we first introduce the experimental setup, then we compare MARLIA with existing methods and show its advantages in outcome maximization, last we investigated the converging efficiency and scalability of MARLIA, which is critical in real-world industrial application.

IV-A Experimental Setup

IV-A1 Dataset

The experiment datasets are from a large advertising platform. The datasets consists of two publishers, and for each publisher, the ad serving logs are provided on May 17th-19th and June 17th-19th in 2020, and the contract demands are provided on May 18th-19th and June 18th-19th in 2020. We make each adjacent days of data as a training and testing pair, i.e., the previous day of impression data is used for training under the demand of the latter day, and the latter day of impression data with its demand is used for testing. Therefore there are 4 training sets and 4 test sets for each publisher. In total, the data contains more than 36 millions impressions with the detailed information, including time, market price and predicted click-through rate555Without loss of generality, we consider the click-through rate as impression quality. for each contract bidder.

IV-A2 Evaluation Metrics

The goal of impression allocation is to maximize the overall outcome. Based on the optimal impression allocation formulated by (II-A), the theoretically optimal outcome on the testing dataset can be obtained, denoted by . Let be the actual outcome of the applied policy. The ratio between and , i.e., , is a simple and effective metric to evaluate the policy. For MARL algorithms, the convergence efficiency is also critical for practical effectiveness. It can be measured by converging time.

IV-A3 Implementation Details

The agents take action in every 15 minutes, so the in Algo. 1 is . We use two fully connected neural network, each of them with 2 hidden layers and 32 nodes per layer, to implement the policy and state action value function , respectively. The mini-batch size is set to and the replay memory size is set to . The action range is set to and the action noise is implemented by a normal distribution generator with and . We set the learning rate of actor and critic to and respectively. In our case, the model selection criterion in training process is choosing the best model with initial s from the day before the testing date within 6 hours training time. For practical considerations, for each day, we randomly sample 10% of the data for model training, and use GNU Linear Programming Kit (GLPK) to solve the dual problem of (II-A) to estimate the and . In the evaluation period, we use 100% of the data for testing. All experiments are carried on a Macbook Pro with 2.6 GHz Intel Core i7 and 16 GB 2667 MHz DDR4.

IV-A4 Compared Methods

-

1.

Fixed Parameter (FP): A method that fixes the as the from training data for each contract, and delivers bids according to Eq. (1) in testing period.

-

2.

MSVV: A classical algorithm for online ad allocation [16]. We set the bid for each contract as , where is the the fraction of the bidder’s budget that has been spent so far, and the bid of RTB as .

- 3.

-

4.

MARLIA: The MARL to Impression Allocation method we proposed in this paper.

| publisher1 | publisher2 | |||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Dates | Impressions | Contracts | Demands |

|

|

Impressions | Contracts | Demands |

|

|

||||||||

| 05/17 | 4.34M | - | - | - | - | 2.07M | - | - | - | - | ||||||||

| 05/18 | 4.20M | 45 | 1.62M | -3.5% | 4.8% | 2.01M | 31 | 1.00M | -2.8% | 4.0% | ||||||||

| 05/19 | 4.05M | 49 | 1.72M | -3.5% | 4.3% | 1.95M | 30 | 1.01M | -3.4% | 3.0% | ||||||||

| 06/17 | 4.14M | - | - | - | - | 2.07M | - | - | - | - | ||||||||

| 06/18 | 3.90M | 124 | 2.06M | -5.7% | 4.9% | 1.89M | 72 | 1.20M | -5.2% | 4.4% | ||||||||

| 06/19 | 3.91M | 126 | 2.21M | 0.1% | 5.0% | 1.91M | 79 | 1.41M | 1.2% | 5.4% | ||||||||

| publisher1 | publisher2 | |||||||

|---|---|---|---|---|---|---|---|---|

| Dates | FP | MSVV | PID | MARLIA | FP | MSVV | PID | MARLIA |

| 05/18 | 0.851 | 0.866 | 0.938 | 0.945 | 0.846 | 0.883 | 0.932 | 0.954 |

| 05/19 | 0.909 | 0.849 | 0.923 | 0.949 | 0.928 | 0.878 | 0.929 | 0.953 |

| 06/18 | 0.902 | 0.863 | 0.893 | 0.951 | 0.870 | 0.874 | 0.885 | 0.950 |

| 06/19 | 0.950 | 0.871 | 0.949 | 0.974 | 0.919 | 0.878 | 0.926 | 0.964 |

| Average | 0.903 | 0.862 | 0.926 | 0.955 | 0.891 | 0.878 | 0.918 | 0.955 |

IV-B Evaluation Results

We conduct experiments to compare the performance of FP, MSVV, PID and MARLIA. The initial parameter for Eq. (1) is set as the optimal one of the training data. As stated in Section 1, due to the unstable incoming traffic, the impression volume and market price in the testing data deviate from that of training data. To present the performances of different methods under different traffic patterns, the statistical information is summarized in Table I, and the experimental results based on testing dataset are summarized in Table II. We can see that MARLIA outperforms all methods, and the averaged improvements over FP, MSVV and PID (for publisher 1 / for publisher 2) are %/%, %/% and %/% respectively.

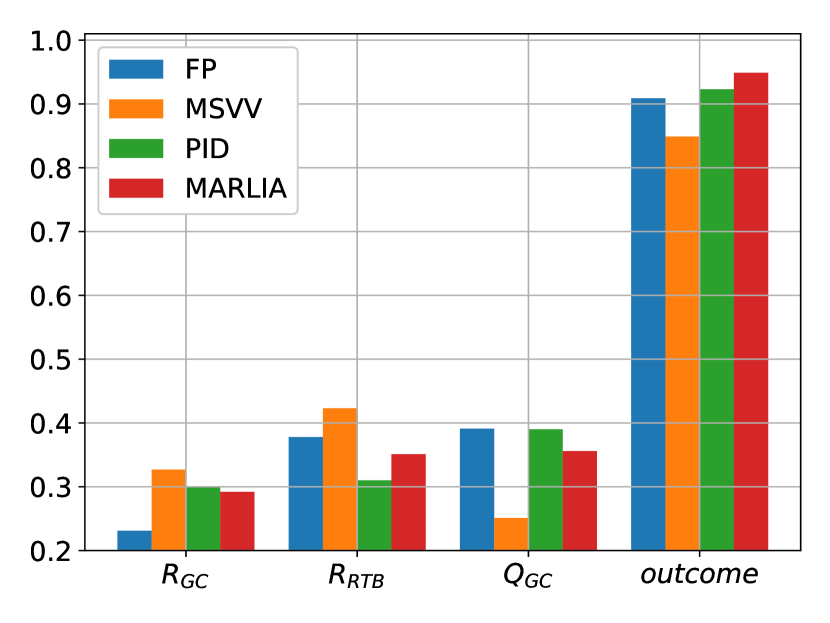

To further investigate the behaviors of all methods, we go deep into the detailed results of all methods of publisher 1 on 2020/05/19. As shown by Fig. 2(a), we illustrate the , , and of all methods.

-

•

FP: FP is a simple strategy and may achieve good results when the environments between training and testing datasets is similar. However, when the bidding competition becomes fiercer or the impression volume has a shortage risk, FP would still bid with the fixed at any time step , which usually makes the bid too low to win sufficient impressions and results in large under-delivery penalty. It can be observed in Fig. 2(a), given the impression difference is -3.5% and the market price difference is 4.3%, although the and is slightly larger than MARLIA, the severe shortage of affects the final outcome.

-

•

MSVV: MSVV takes the RTB revenue into consideration by trading off between the outcome from contracts and that from RTB for each impression arrival. However, since it is unaware of the subsequent impression distribution, it may allocate impressions to contract in early phase of the whole allocation process, resulting in great loss of future . Different from MSVV, MARLIA learns from the training data to make better decisions to maximize the overall outcome. It can be observed in Fig. 2(a), due to such defect, MSVV gains low compared with MARLIA and finally results in low outcome.

-

•

PID: PID tries to adjust to pace impression acquisition, however, it has two drawbacks in our application. First, it is critical for a PID strategy to obtain a proper target, which is the target impression volume to be allocated to the contract at each step. In practice, it is tricky and needs expert knowledge to be continuously optimized. Second, different from MARLIA, PID strategy is usually designed for an individual agent. It is hard to consider global impression allocation between different agents or balance RTB revenue and contract fulfillment. As shown by Fig. 2(a), PID tries to fulfill every contract and results in relatively low , which affects its final outcome.

-

•

MARLIA: Compared with the above methods, MARLIA learns an adjustment policy based on the current state to maximize the future outcome. It can be found in Fig. 2(a) that MARLIA does a good job in balancing different part of outcome.

IV-C Convergence Efficiency and Scalability

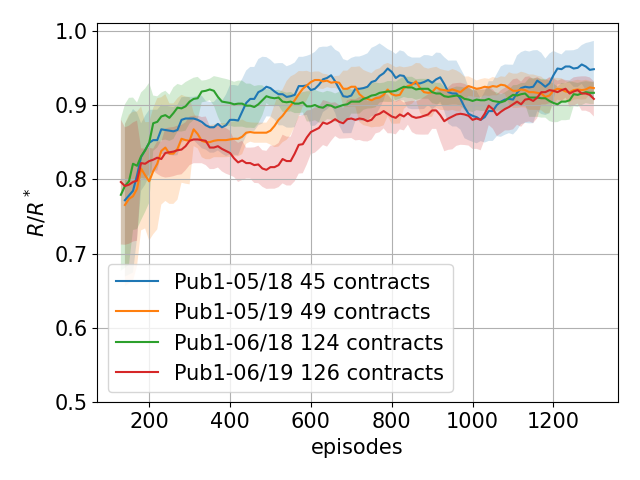

In application, FP, MSVV and PID have little training cost, while complicated methods such as MARL ones commonly suffered from convergence efficiency and scalability challenges. Besides, for an impression allocation task, it is of great necessity to accomplish the training process in an acceptable period of time. In order to show the converging efficiency and scalability of MARL, the training process of MARLIA on the datasets of publisher 1 are illustrated by Fig. 2(b). It can be seen that MARLIA will converge to a satisfying (e.g. greater than ) in episodes ( hours on a laptop) regardless of the contract number. Thus the proposed MARLIA is scalable and applicable in industrial scenario.

V Related Work

Impression allocation for outcome maximization is one of the most important issues to monetize traffic for a publisher. Some algorithms have been proposed to help publishers allocate impressions to contracts without consideration of RTB [18, 19, 20]. [7] is the first work considering contracts as bidders to compete with RTB, but the goal is to maximize the representativeness of contract impressions. [2] proposes a revenue maximization strategy based on allocating and pricing the future contract impressions, which does not involve RTB and the efficiency is not optimized. To maximize the outcome, [6] tries to learn a stochastic policy to deliver reserve price for each impression. However, for a repeated auction model, in any equilibrium, reserve price will make bidders in an ad exchange tend to shade their bids (not incentive compatible) [21]. Besides, the contract first strategy applied in [6] has also been proved not optimal in our experimental evaluations. Recently, a new strategy maximizing the total revenue is proposed in [8]. However, the challenge of unstable traffic patterns is not discussed.

Impression allocation for outcome maximization is one of the most important issues to monetize traffic for a publisher. Some algorithms have been proposed to help publishers allocate impressions to contracts without consideration of RTB[18, 19, 20]. As RTB becomes increasingly important, how to maximize the profit considering both RTB and guaranteed contracts starts to be an open question. [7] was the first work considering contracts as bidders to compete with RTB: the publisher is regarded as a bidder and the impression would be allocated to the bidder with the highest bidd price. However, the goal of [7] was to maximize the representativeness of contract impressions from the advertisers’ perspective. [2] proposed a revenue maximization strategy based on allocating and pricing the future contract impressions, but the allocation was determined in advance rather than through RTB. To maximize the outcome, [6] tries to learn a stochastic policy to deliver reserve price for each impression. However, it is known that, for a repeated auction model, in any equilibrium, reserve price will make bidders in an ad exchange tend to shade their bids (not incentive compatible) [21]. Besides, the contract first strategy applied in [6] has also been proved not optimal in our experimental evaluations. Recently, a new strategy maximizing the total revenue was proposed in [8]. However, the challenge of unstable traffic patterns was not discussed or addressed.

Reinforcement learning (RL) has been applied to solve a wide range of problems. Specifically in the computational advertising domain [22, 23, 24], RL has been leveraged to optimize bidding strategies [25, 13]. Traditional reinforcement learning approaches achieved a huge success in single agent settings, but delivered poor performance in MARL [26]. One issue is that simply considering other agents as a part of the environment often breaks the convergence guarantee and makes the learning process unstable [27]. Nash equilibrium algorithms have been proposed to address this problem [28]. However, the computational complexity of directly solving Nash equilibrium confines such algorithms within handful agents and prohibits them from real-world applications. Following this direction, [29] tries to improve the scalability via leveraging action information from neighboring agents, while the concept of neighborhood is hard to be defined in the advertising context.

VI Conclusion

In online display advertising, guaranteed contracts and real-time bidding (RTB) are two major ways to sell impressions for a publisher, especially for those large publishers with in-house RTB. In this paper, we proposed a strategy to maximize the outcome of a publisher by allocating impressions between guaranteed contracts and RTB. We proposed the outcome maximization strategy by deriving the optimal bidding function when contracts are treated as bidders. Meanwhile, the impression allocation strategy can also keep the incentive compatibility of RTB, making truthful bidding still the dominant strategy. In order to implement the strategy with the practical challenges such as unstable traffic patterns, we proposed an efficient MARL method, MARLIA, to adjust the critical parameter for contract . Meanwhile, based on the important property of the impression allocation problem, the learning efficiency is significantly boosted, and making the deploy of our method in industrial scenario is feasible. Experimental evaluations on large-scale real-world datasets demonstrate that MARLIA outperforms other baselines in outcome maximization. Meanwhile, empirical studies also show that MARLIA converges quickly regardless of the contract amount, which is important in industrial application.

References

- [1] IAB, “Full-year 2019 internet advertising revenue report and coronavirus impact on ad pricing report in q1 2020,” https://www.iab.com/video/full-year-2019-internet-advertising-revenue-report-and-coronavirus-impact-on-ad-pricing-report-in-q1-2020/, 2020.

- [2] B. Chen, S. Yuan, and J. Wang, “A dynamic pricing model for unifying programmatic guarantee and real-time bidding in display advertising,” in Proceedings of the Eighth International Workshop on Data Mining for Online Advertising. ACM, 2014, pp. 1–9.

- [3] B. Chen, J. Huang, Y. Huang, S. Kollias, and S. Yue, “Combining guaranteed and spot markets in display advertising: selling guaranteed page views with stochastic demand.”

- [4] S. Yuan, J. Wang, and X. Zhao, “Real-time bidding for online advertising: measurement and analysis,” in Proceedings of the Seventh International Workshop on Data Mining for Online Advertising. ACM, 2013, p. 3.

- [5] B. Edelman, M. Ostrovsky, and M. Schwarz, “Internet advertising and the generalized second-price auction: Selling billions of dollars worth of keywords,” American economic review, vol. 97, no. 1, pp. 242–259, 2007.

- [6] S. R. Balseiro, J. Feldman, V. Mirrokni, and S. Muthukrishnan, “Yield optimization of display advertising with ad exchange,” Management Science, vol. 60, no. 12, pp. 2886–2907, 2014.

- [7] A. Ghosh, P. McAfee, K. Papineni, and S. Vassilvitskii, “Bidding for representative allocations for display advertising,” in International Workshop on Internet and Network Economics. Springer, 2009, pp. 208–219.

- [8] G. Jauvion and N. Grislain, “Optimal allocation of real-time-bidding and direct campaigns,” in Proceedings of the 24th ACM SIGKDD International Conference on Knowledge Discovery & Data Mining. ACM, 2018, pp. 416–424.

- [9] E. Vee, S. Vassilvitskii, and J. Shanmugasundaram, “Optimal online assignment with forecasts,” in Proceedings of the 11th ACM conference on Electronic commerce. ACM, 2010, pp. 109–118.

- [10] J. Feldman, M. Henzinger, N. Korula, V. S. Mirrokni, and C. Stein, “Online stochastic packing applied to display ad allocation,” in European Symposium on Algorithms. Springer, 2010, pp. 182–194.

- [11] N. R. Devanur and T. P. Hayes, “The adwords problem: online keyword matching with budgeted bidders under random permutations,” in Proceedings of the 10th ACM conference on Electronic commerce. ACM, 2009, pp. 71–78.

- [12] N. R. Devanur, K. Jain, B. Sivan, and C. A. Wilkens, “Near optimal online algorithms and fast approximation algorithms for resource allocation problems,” in Proceedings of the 12th ACM conference on Electronic commerce. ACM, 2011, pp. 29–38.

- [13] D. Wu, X. Chen, X. Yang, H. Wang, Q. Tan, X. Zhang, J. Xu, and K. Gai, “Budget constrained bidding by model-free reinforcement learning in display advertising,” in Proceedings of the 27th ACM International Conference on Information and Knowledge Management, 2018, pp. 1443–1451.

- [14] N. Nisan, T. Roughgarden, E. Tardos, and V. V. Vazirani, Algorithmic game theory. Cambridge University Press, 2007.

- [15] R. S. Sutton and A. G. Barto, Reinforcement learning: An introduction. MIT press, 2018.

- [16] A. Mehta, A. Saberi, U. Vazirani, and V. Vazirani, “Adwords and generalized on-line matching,” in 46th Annual IEEE Symposium on Foundations of Computer Science (FOCS’05). IEEE, 2005, pp. 264–273.

- [17] X. Yang, Y. Li, H. Wang, D. Wu, Q. Tan, J. Xu, and K. Gai, “Bid optimization by multivariable control in display advertising,” arXiv preprint arXiv:1905.10928, 2019.

- [18] V. Bharadwaj, W. Ma, M. Schwarz, J. Shanmugasundaram, E. Vee, J. Xie, and J. Yang, “Pricing guaranteed contracts in online display advertising,” in Proceedings of the 19th ACM international conference on Information and knowledge management, ser. CIKM ’10. ACM, 2010, pp. 399–408.

- [19] V. Bharadwaj, P. Chen, W. Ma, C. Nagarajan, J. Tomlin, S. Vassilvitskii, E. Vee, and J. Yang, “Shale: an efficient algorithm for allocation of guaranteed display advertising,” in Proceedings of the 18th ACM SIGKDD international conference on Knowledge discovery and data mining. ACM, 2012, pp. 1195–1203.

- [20] J. Zhang, Z. Wang, Q. Li, J. Zhang, Y. Lan, Q. Li, and X. Sun, “Efficient delivery policy to minimize user traffic consumption in guaranteed advertising,” in Proceedings of the Thirty-First AAAI Conference on Artificial Intelligence, ser. AAAI ’17. AAAI, 2017.

- [21] O. Carare, “Reserve prices in repeated auctions,” Review of Industrial Organization, vol. 40, no. 3, pp. 225–247, 2012.

- [22] S. Yuan and J. Wang, “Sequential selection of correlated ads by pomdps,” in Proceedings of the 21st ACM international conference on Information and knowledge management. ACM, 2012, pp. 515–524.

- [23] K. Amin, M. Kearns, P. Key, and A. Schwaighofer, “Budget optimization for sponsored search: Censored learning in mdps,” arXiv preprint arXiv:1210.4847, 2012.

- [24] J. Jin, C. Song, H. Li, K. Gai, J. Wang, and W. Zhang, “Real-time bidding with multi-agent reinforcement learning in display advertising,” in Proceedings of the 27th ACM International Conference on Information and Knowledge Management. ACM, 2018, pp. 2193–2201.

- [25] H. Cai, K. Ren, W. Zhang, K. Malialis, J. Wang, Y. Yu, and D. Guo, “Real-time bidding by reinforcement learning in display advertising,” in Proceedings of the Tenth ACM International Conference on Web Search and Data Mining. ACM, 2017, pp. 661–670.

- [26] L. Matignon, G. J. Laurent, and N. Le Fort-Piat, “Independent reinforcement learners in cooperative markov games: a survey regarding coordination problems,” The Knowledge Engineering Review, vol. 27, no. 1, pp. 1–31, 2012.

- [27] M. K. Colby, S. Kharaghani, C. HolmesParker, and K. Tumer, “Counterfactual exploration for improving multiagent learning,” in Proceedings of the 2015 International Conference on Autonomous Agents and Multiagent Systems. International Foundation for Autonomous Agents and Multiagent Systems, 2015, pp. 171–179.

- [28] E. M. De Cote and M. L. Littman, “A polynomial-time nash equilibrium algorithm for repeated stochastic games,” arXiv preprint arXiv:1206.3277, 2012.

- [29] Y. Yang, R. Luo, M. Li, M. Zhou, W. Zhang, and J. Wang, “Mean field multi-agent reinforcement learning,” arXiv preprint arXiv:1802.05438, 2018.