Asymptotic normality in linear regression with approximately sparse structure

-

1

Institute of Applied Mathematics, Faculty of Mathematics and Informatics,

Vilnius University, Naugarduko 24, Vilnius LT-03225, Lithuania

Abstract

In this paper we study the asymptotic normality in high-dimensional linear regression. We focus on the case where the covariance matrix of the regression variables has a KMS structure, in asymptotic settings where the number of predictors, , is proportional to the number of observations, . The main result of the paper is the derivation of the exact asymptotic distribution for the suitably centered and normalized squared norm of the product between predictor matrix, , and outcome variable, , i.e. the statistic . Additionally, we consider a specific case of approximate sparsity of the model parameter vector and perform a Monte-Carlo simulation study. The simulation results suggest that the statistic approaches the limiting distribution fairly quickly even under high variable multi-correlation and relatively small number of observations, suggesting possible applications to the construction of statistical testing procedures for the real-world data and related problems.

MSC: 60F05, 62E20, 62J99

Keywords: linear regression, sparsity, asymptotic normality, variance-gamma distribution

1 Introduction

Consider a linear regression model

| (1.1) |

where are observations of outcome and are -dimensional predictors with being i.i.d. random vectors , which are normally distributed with zero mean and covariance matrix , denoted . We assume that the covariance matrix has a form

| (1.6) |

if , and if (here and below denotes the identity matrix). This matrix is often called the Kac–Murdock–Szegö (KMS) matrix, originally introduced in Kac et al. (1953). As the autocorrelation matrix of corresponding causal AR(1) processes, KMS matrix is positive definite and is considered due to the wide array of applications in the literature and its’ well known spectral properties (see, e.g., Fikioris (2018) for a thorough literature review). Further, are unobserved i.i.d. errors with , , and is an unknown -dimensional parameter. In practice, the assumption that can be untenable and it may be appropriate to add an intercept to the linear model (1.1), however, for simplicity, throughout this paper we will assume that the intercept is known and the variables are centered.

This paper is concerned with the derivation of the exact asymptotic distribution for the suitably centered and normalized squared norm under the assumption of the KMS type covariance structure in (1.6), where and are assumed large. Throughout the paper we assume that and . We are particularly interested in cases where . Statistics of such form arise in various applications in the context of high-dimensional linear regression, and under normality assumptions, general results can be derived using random matrix theory through Wishart distributions (see, e.g., Dicker (2014)). In our paper we approach the problem following an observation by Gaunt (2013), that the distribution of product of Gaussian random variables admits a variance-gamma distribution, resulting in a set of attractive properties. In addition to the -norm statistic, we find that the obtained results can be easily extended towards alternative forms of the statistic, e.g., by using a different norm, which would reduce the problem to manipulating variance-gamma distribution, thus suggesting possible further research cases and useful extensions.

Additionally, we examine a specific case of parameter by considering , . Similar structures of the vector are often found in the literature when approximate sparsity of the coefficients in the linear regression model (1.1) is assumed. See, e.g., Ing (2020) and Cha et al. (2021) for a broader view towards sparsity requirements and its’ implications to specific high-dimensional algorithms; Shibata (1980) and Ing (2007) for model selection problems in autoregressive time series models; or Belloni et al. (2012), Javanmard and Montanari (2014), Zhang and Zhang (2014), Caner and Kock (2018), Belloni et al. (2018), Gold et al. (2020), Ning et al. (2020), Guo et al. (2021) for applications on inference of high-dimensional models and high-dimensional instrumental variable (IV) regression models. Performing Monte Carlo simulations, we find that the empirical distributions of the corresponding statistic approach the limiting distribution reasonably quickly even for large values of and , suggesting that the assumption of sparse structure can be included in the applications and statistical tests.

In this paper, , and denote the equality of distributions, convergence of distributions and convergence in probability, respectively. stands for a generic positive constant which may assume different values at various locations. denotes the indicator function of a set .

The structure of the paper is as follows. In Section 2 we present the main results of the paper. In Section 3 we present useful properties of variance-gamma distribution, which are used in Section 4 in order to prove some auxiliary results. In Section 5 we present the proof of the main result. Finally, in Section 6 we provide an example of the main result under imposed approximate sparsity assumption for the parameter of the model (1.1). Technical results are presented in Appendix A, while, for brevity, some straightforward yet tedious proofs are presented in the Supplementary material.

2 Main results

In this section we formulate the main results on the normality of statistic . Introduce the notations:

| (2.1) | |||||

| (2.2) | |||||

| (2.3) |

It is easy to see that, under , there exist limits

Obviously, . Moreover, since is positive semi-definite, , . Indeed, , thus it suffices to take for and for .

Our first main result is the following theorem.

Theorem 2.1.

Our second main result deals with the case where the centering sequence in (2.6) is modified to include the limiting values of , .

Theorem 2.2.

Let the assumptions of Theorem 2.1 hold. In addition, assume that and with . Then,

| (2.8) |

The proofs of these theorems are given in Section 5.

Remark 2.1.

For alternative expressions of , and , see Lemma 5.2 below.

Define

The following corollary deals with the case when , i.e., . The result easily follows from Theorem 2.2, noting that in this case , .

3 Properties of the variance-gamma distribution

In this section we provide some properties of the variance-gamma distribution, which will be used in the following proofs.

Recall that the variance-gamma distribution with parameters , , and has density

where , is the modified Bessel function of the second kind. For a random variable with density (3) we write . Let , , , denote the gamma distribution with density

It holds that

| (3.2) |

where , , and are independent. The characteristic function of has a form (see, e.g., Madan et al. (1998), Kotz et al. (2001))

| (3.3) |

We note the following properties of the variance-gamma distribution.

-

(i)

If and are independent random variables then

-

(ii)

If , then for any

The following proposition is crucial for our purposes.

Proposition 3.1.

(i) If , where , then

(ii) If , are i.i.d. random vectors with common distribution , then

and

where and are independent random variables.

(iii) Assume that , , are i.i.d. copies of and let , , , , . Then

where , with

| (3.5) |

Proof.

Lemma 3.1.

Assume that has distribution and let , , , , . Then

where , is, independent of , zero mean normal vector with covariances in (3.5).

4 Some auxiliary lemmas

In this section we establish some auxiliary results that will be used in the proofs of Theorems 2.1 and 2.2. Here and throughout the paper we remove the upper indices when working with triangular schemes of random variables, e.g., , whenever it is clear from the context.

Lemma 4.1.

Let , where is positive definite covariance matrix and , . Then

| (4.1) |

If, in addition, , then

| (4.2) |

Proof.

Remark 4.1.

Lemma 4.2.

Assume that are i.i.d. random variables. For any define

| (4.6) |

where , are positive scalars, and , , are real scalars, such that

| (4.7) | |||||

| (4.8) |

with Then, as ,

| (4.9) |

Proof.

The proof uses the method of cumulants and is structured as follows:

-

(i)

we establish the moment-generating function of , , and ;

-

(ii)

we find which corresponds to the cumulant generating function of the sum ;

-

(iii)

we find , which corresponds to the cumulant generating function of the left hand side of (4.9);

-

(iv)

finally, in order to prove (4.9), we show that the cumulants , generated by , satisfy , and , as .

Step 1. First, rewrite

| (4.10) |

Here, has a noncentral chi-squared distribution with the following moment-generating function:

| (4.11) |

Therefore, by (4.10) and (4.11),

for , and

Step 2. Since are independent, we have that

Step 3. It is straightforward to see that

where , , and for ,

| (4.12) |

Step 4. In order to prove that (4.9) holds, it remains to show that, as , for all . By (4.12), it is equivalent to showing that for any fixed , as ,

| (4.13) | |||||

| (4.14) |

In order to prove (4.13) we use induction. The case for holds by assumption. Assuming that (4.13) holds for fixed , we have

concluding that (4.13) holds for all . The proof for (4.14) is analogous: the case for holds by assumption, thus, we repeat the same arguments as with (4.13) and conclude that (4.14) holds for all . This concludes the proof of the lemma. ∎

5 Proof of the main results

In this section we give the proofs of theorems 2.1 and 2.2. Throughout the proofs, we express corresponding constants in terms of and , , introduced in (2.1)–(2.3). Recall that , and, by Remark 5.1, , for .

Proof of Theorem 2.1.

Applying Proposition 3.1(iii) with , , and , , , where , we obtain that

where and with defined as (see (3.5)):

| (5.1) |

By expanding the square we can write

By further rearranging the right-hand side, we have

| (5.2) |

where

| (5.3) | |||||

| (5.4) | |||||

| (5.5) | |||||

| (5.6) |

We will show that, as , , the term , while the terms and are asymptotically normal. More precisely, we will show that and , where and are given by (5.12) and (5.30) below. Here, since and are mutually independent for each , it follows that . Finally, the term defines the mean of the statistic, i.e.

| (5.7) |

Thus, we will conclude by establishing that , while , as in the statement of the theorem.

First, consider defined in (5.3). We will show that . Denote

| (5.8) |

It is clear that and . Recall that, by CLT,

| (5.9) |

Therefore,

| (5.10) |

Second, consider , defined in (5.4). We will show that

| (5.11) |

with given by

| (5.12) |

Rewrite

| (5.13) |

Applying (5.8) and (5.9) for the outer term of (5.13), we obtain

We will show that the inner term of (5.13) approaches . Since , by (5.8) and assumption it suffices to prove the convergence

| (5.14) |

Denote matrix

| (5.15) |

To prove (5.14) we apply Lemma 4.1 with , , and . Obviously, the conditions of Lemma 4.1 will hold if and , as . Observe, that

| (5.16) | |||||

since , and . Here we used (5.8) and the observation that

| (5.17) |

Next, consider , defined by (5.5). We will show that

| (5.18) |

with defined in (5.30). Write

where , is defined by (5.15), and

Observe that due to the Law of Large Numbers. Thus, since and are independent for any and , it follows that

| (5.19) |

First, we consider the inner term of (5.19) and show, that, as ,

| (5.20) |

Recall, that , . Further, let . Clearly, one has that , where denotes the symmetric square root of . By the Spectral Theorem, we construct , where and is an orthogonal matrix that diagonalizes , such, that , with comprised of the eigenvalues of . Then,

| (5.21) | |||||

where , and

| (5.22) |

Clearly, and . Therefore, proving the result (5.20) is equivalent to showing:

| (5.23) |

where

| (5.24) |

We prove (5.23) by applying Lemma 4.2 with as the eigenvalues of and . By the conditions of Lemma 4.2, we need to show that the following holds

| (5.25) |

First, observe that . Indeed, we have that , since

| (5.26) | |||||

Next, by (5.16), we find that . Indeed, by (5.16), we have

| (5.27) | |||||

Thus, by (5.26) and (5.27), it follows that and condition (5.25) reduces to:

| (5.28) |

We show that (5.28) holds. For the first term of (5.28), we have

| (5.29) | |||||

where the last equality follows from Lemma A.5. For the second term of (5.28), observe, that by Hölder’s inequality and (5.29),

This concludes with (5.28), ensuring that the conditions of Lemma 4.2 hold.

Now we can establish the expression for . By (5.8), (5.24), (5.26) and (5.27),

| (5.30) | |||||

By (5.12) and (5.30), recalling that , we have that

| (5.31) |

Finally, consider , defined by (5.6). Since , we have that

| (5.32) |

Before proceeding with the proof of Theorem 2.2, we establish the following lemma that ensures convergence rate for and , appearing in Theorem 2.1, under additional restrictions for the parameters .

Lemma 5.1.

Assume that and , , and . Then,

-

(i)

-

(ii)

Proof.

For the proof see Appendix S1. ∎

Proof of Theorem 2.2.

We end this section by deriving two supporting results that allows us to derive convenient alternative expressions for the terms and . For this, we introduce functions and by Definition 5.1 below, which, under the assumptions of Theorem 2.1 and a given structure of ’s, requires only to evaluate the terms and . Then, due to Lemma 5.2 below, the expressions for , and easily follow.

Definition 5.1.

Note, that, by the rules of differentiation of power series, the functions (5.36)–(5.39) are well defined.

Lemma 5.2.

Proof.

See the proof in Appendix A.2. ∎

Remark 5.1.

6 Approximate sparsity: an example

In this section we study the case when coefficients decay hyperbolically, i.e., . This assumption is analogous to the assumption of approximate sparsity, as defined by Belloni et al. (2012). The authors of the aforementioned paper note, that for approximately sparse models the regression function can be well approximated by a linear combination of relatively few important regressors, which is one of the reasons of popularity of variable selection approaches such as LASSO (Tibshirani (1996)) and it’s modifications (see, e.g., Zou (2006), Meinshausen (2007), Belloni et al. (2011)). At the same time, approximate sparsity allows all coefficients to be nonzero, which is a more plausible assumption in many real world settings.

In order to derive the quantities in Theorem 2.2, we apply the results of Lemma 5.2. For this, we establish the expressions for the quantities in Definition 5.1.

Define the real dilogarithm function (see, e.g., Morris (1979)):

| (6.1) |

(Here and below, if .) For the real dilogarithm has a series representation,

| (6.2) |

Then,

Additionally, we have

| (6.3) |

Thus, by (5.36) and (6.3), we establish

Next, note that

| (6.4) | |||||

where we have used identities

and (6.1). Then, by (5.37), (6.3) and (6.4),

whereas by (5.39),

Further, note that

| (6.5) | |||||

where the last equality follows from Lemma A.1. Next, by (5.37), (6.3) and (6.5) we have

Thus, we can apply Lemma 5.2(i) and arrive at the following expression for :

| (6.6) |

Similarly, for , by collecting and simplifying the terms, by Lemma 5.2(ii) and Lemma A.1, we have

| (6.7) | |||||

Lastly, for , by Lemma 5.2(iii), through simplification of terms, we get

| (6.8) | |||||

This allows us to apply Theorem 2.2 under the considered specification of the parameter , and conclude with the following corollary.

Corollary 6.1.

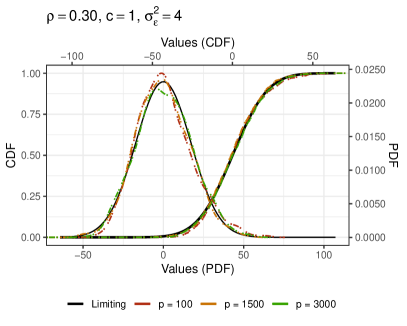

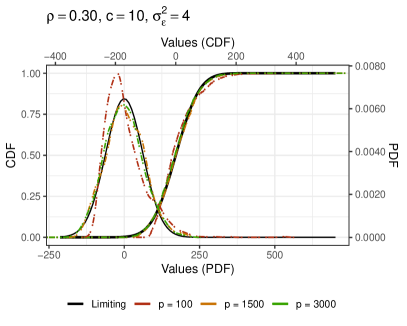

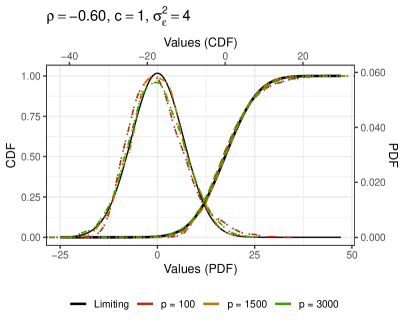

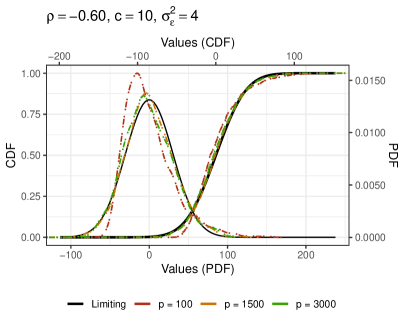

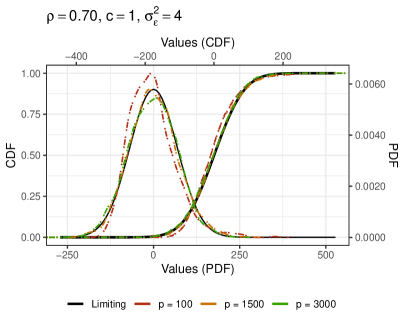

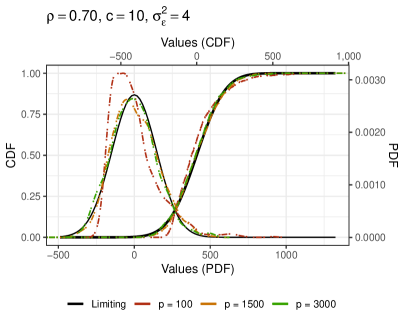

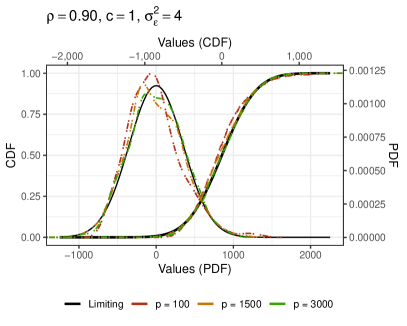

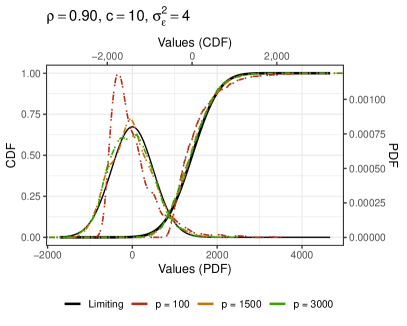

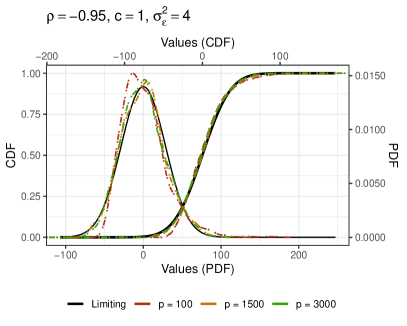

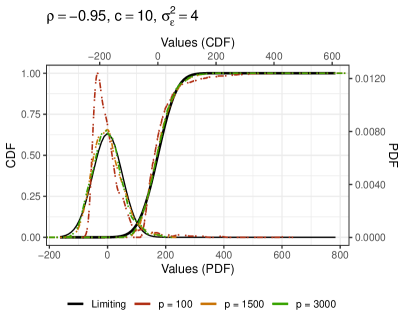

In order to illustrate the results of Corollary 6.1, we end this section with a Monte Carlo simulation study, where we generate 1000 independent replications of the statistic . The data is generated following the assumptions of Corollary 6.1 for varying sets of parameters . The results are presented in Figures 1–5. Figures show the empirical cumulative distribution function (CDF) and the empirical probability density function (PDF), together with the limiting CDF and PDF of for different parameter combinations. We notice that for relatively small values of , the distribution is fairly close to the limiting distribution even for small values of . On the other hand, slightly slower convergence is evident for (see Figure 1 for simulation results with ). However, it can be noted that for large values of the effect of term is greatly reduced, resulting in very similar distributions when comparing, e.g., against .

Appendix A Appendix

Throughout the proofs we use the notation to mark generic constants, the specific values of which can change from line to line.

A.1 Technical lemmas

Lemma A.1.

Assume that . Then,

where denotes the real dilogarithm function. (Recall, that for , by we denote .)

Proof.

Write,

By (6.1), we have

| (A.1) |

It remains to show that

| (A.2) |

Indeed, by substitution , we have

| (A.3) | |||||

Further, by substitution , we have

| (A.4) | |||||

| (A.5) |

where for (A.4)–(A.5) we apply the easily verifiable identities (see, e.g., Maximon (2003)):

Thus, (A.3) and (A.5) imply (A.2), which concludes the proof. ∎

Lemma A.2.

Assume that and . Then, the following inequalities hold:

-

(i)

-

(ii)

-

(iii)

-

(iv)

Proof.

See the proof in Supplementary material, Section S2. ∎

Lemma A.3.

Assume that , and that . Then,

Proof.

We have

Here we used the fact that . Thus,

| (A.6) |

∎

Remark A.1.

Obviously, the assumption , for , implies that :

Lemma A.4.

Assume that the assumptions of Theorem 2.1 hold. Then,

Lemma A.5.

Assume that and . Define . Then,

| (A.8) |

Proof.

See the proof in Supplementary material, Section S3. ∎

A.2 Proof of Lemma 5.2

Here and throughout the proof we employ the notation as in Definition 5.1.

References

- Belloni et al. (2012) Belloni, A., D. Chen, V. Chernozhukov, and C. Hansen (2012). Sparse models and methods for optimal instruments with an application to eminent domain. Econometrica 80(6), 2369–2429.

- Belloni et al. (2018) Belloni, A., V. Chernozhukov, D. Chetverikov, C. Hansen, and K. Kato (2018). High-dimensional econometrics and regularized GMM. ArXiv preprint arXiv:1806.01888.

- Belloni et al. (2011) Belloni, A., V. Chernozhuv, and L. Wang (2011). Square-root lasso: pivotal recovery of sparse signals via conic programming. Biometrika 98(4), 791–806.

- Caner and Kock (2018) Caner, M. and A. B. Kock (2018). Asymptotically honest confidence regions for high dimensional parameters by the desparsified conservative Lasso. Journal of Econometrics 203(1), 143–168.

- Cha et al. (2021) Cha, J., H. D. Chiang, and Y. Sasaki (2021). Inference in high-dimensional regression models without the exact or sparsity. ArXiv preprint arXiv:2108.09520.

- Dicker (2014) Dicker, L. H. (2014, 03). Variance estimation in high-dimensional linear models. Biometrika 101(2), 269–284.

- Fikioris (2018) Fikioris, G. (2018). Spectral properties of Kac–Murdock–Szegö matrices with a complex parameter. Linear Algebra and its Applications 553, 182–210.

- Gaunt (2013) Gaunt, R. (2013, 03). Rates of Convergence of Variance-Gamma Approximations via Stein’s Method. Ph. D. thesis, The Queen’s College, University of Oxford.

- Gaunt (2019) Gaunt, R. E. (2019, May). A note on the distribution of the product of zero-mean correlated normal random variables. Statistica Neerlandica 73(2), 176–179.

- Gold et al. (2020) Gold, D., J. Lederer, and J. Tao (2020). Inference for high-dimensional instrumental variables regression. Journal of Econometrics 217(1), 79–111.

- Guo et al. (2021) Guo, Z., D. Ćevid, and P. Bühlmann (2021). Doubly Debiased Lasso: high-dimensional inference under hidden confounding. ArXiv preprint arXiv:2004.03758.

- Ing (2007) Ing, C.-K. (2007). Accumulated prediction errors, information criteria and optimal forecasting for autoregressive time series. The Annals of Statistics 35(3), 1238–1277.

- Ing (2020) Ing, C.-K. (2020). Model selection for high-dimensional linear regression with dependent observations. The Annals of Statistics 48(4), 1959–1980.

- Javanmard and Montanari (2014) Javanmard, A. and A. Montanari (2014). Confidence intervals and hypothesis testing for high-dimensional regression. The Journal of Machine Learning Research 15(1), 2869–2909.

- Kac et al. (1953) Kac, M., W. Murdock, and G. Szegő (1953). On the eigen-values of certain Hermitian forms. Journal of Linear Rational Mechanics and Analysis 2, 767–800.

- Kotz et al. (2001) Kotz, S., T. Kozubowski, and K. Podgórski (2001). The Laplace Distribution and Generalizations: A Revisit with Applications to Communications, Economics, Engineering, and Finance. Boston: Birkhäuser.

- Madan et al. (1998) Madan, D. B., P. P. Carr, and E. C. Chang (1998). The variance gamma process and option pricing. Review of Finance 2(1), 79–105.

- Maximon (2003) Maximon, L. C. (2003). The dilogarithm function for complex argument. Proceedings of the Royal Society of London. Series A: Mathematical, Physical and Engineering Sciences 459(2039), 2807–2819.

- Meinshausen (2007) Meinshausen, N. (2007). Relaxed Lasso. Computational Statistics & Data Analysis 52(1), 374–393.

- Morris (1979) Morris, R. (1979). The dilogarithm function of a real argument. Mathematics of Computation 33(146), 778–787.

- Ning et al. (2020) Ning, Y., S. Peng, and J. Tao (2020). Doubly robust semiparametric difference-in-differences estimators with high-dimensional data. ArXiv preprint arXiv:2009.03151.

- Shibata (1980) Shibata, R. (1980). Asymptotically efficient selection of the order of the model for estimating parameters of a linear process. The Annals of Statistics, 147–164.

- Tibshirani (1996) Tibshirani, R. (1996). Regression shrinkage and selection via the lasso. Journal of the Royal Statistical Society: Series B (Methodological) 58(1), 267–288.

- Zhang and Zhang (2014) Zhang, C.-H. and S. S. Zhang (2014). Confidence intervals for low dimensional parameters in high dimensional linear models. Journal of the Royal Statistical Society: Series B (Statistical Methodology) 76(1), 217–242.

- Zou (2006) Zou, H. (2006). The adaptive lasso and its oracle properties. Journal of the American Statistical Association 101(476), 1418–1429.

Supplementary material

S1 Proof of Lemma 5.1

Part (ii). Write

| (S1) | |||||

We have

Thus,

by Lemma A.2(ii)–(iv). For the term we have

Thus, by Lemma A.2(ii)-(iii),

For the term we have

Thus,

since and due to Hölder’s inequality. Further, for the term we have

by Lemma A.3. Finally, for write

For the first summand, we have

| (S2) | |||||

where . Similarly,

| (S5) | |||||

For (S5), write

Thus, by Lemma A.2(i), we have

for . Next, for (S5), write

It follows from Lemma A.2(ii) that

for . Finally, for (S5), we have

Thus, by Lemma A.2(i),

Hence, (S2) and the estimates for (S5)–(S5) yield

Equality (S1) and estimates , , complete the proof of part (ii).

S2 Proof of Lemma A.2

Proof.

For inequality (i), we have that

For inequality (ii), note that

For (iii), see that

where the last inequality follows from (S10).

The proof of (iv) follow the same steps as that of (iii). ∎

S3 Proof of Lemma A.5

Proof.

First, note, that by (5.8), Lemma 5.2 and Remark 5.1, it holds that

| (S6) |

Then, we have that

In order to show (A.8), it suffices to show that the following results hold, since the remaining cases will be symmetric:

-

(i)

-

(ii)

-

(iii)

-

(iv)

Case (i). We have

where

| (S7) |

and

so that

Case (ii). We have,

Observe, that by (S6), we have . Additionally,

We use (S7) and note that

Thus, it follows that

Case (iv). By (S6),

Thus, this concludes the proof of (A.8). ∎

S4 Proof of result (A.9) of Lemma 5.2(ii)

Proof.

Denote

Then, we can write

| (S8) |

First, note that

Then, using the notation by Definition 5.1, it follows by the Dominated Convergence Theorem (DCT) that

Next, consider , . It’s straightforward to see that,

By simplifying, it follows that

therefore, using the notation of Definition 5.1, we rewrite

which concludes the proof of (A.9). ∎

S5 Proof of results (A.13)–(A.14) of Lemma 5.2(iii)

Proof.

First, we establish the following observation:

| (S9) | |||||

Consider in (A.11). By (S9), write,

Observe, that

| (S10) | |||||

Hence,

| (S11) | |||||

Similarly,

The first term can be rewritten,

We get

| (S12) | |||||

Similarly,

where due to (S10),

| (S13) | |||||

Finally, observe that

where due to (S10), it remains to see that, as ,

| (S14) |

Finally, by collecting the terms of (S12), (S13) and (S14) and simplifying, we get

Therefore, from (S11), (S12), (S13) and (S14),

which concludes the proof of (A.13).

Next, consider in (A.12). According to the arrangement of indices , we have 9 cases:

-

1.

,

-

2.

, ,

-

3.

, ,

-

4.

, ,

-

5.

,

-

6.

, ,

-

7.

, ,

-

8.

, ,

-

9.

.

Case 1:

Case 2:

Case 3:

Case 4:

Case 5:

Case 6:

Case 7:

Case 8: We have

Case 9: We have

Observe, that

| (S15) | |||||

The two summands of (S15) are symmetric, therefore due to brevity we consider only the first term. The proof for the second term will be analogous. Note,

| (S16) |

where

holds due to . It remains to note that

since and . Thus, by (S15) and (S16), it follows that

| (S17) |