Fissler & Pesenti

Sensitivity Measures Based on Scoring Functions

Sensitivity Measures Based on Scoring Functions

Tobias Fissler \AFFInstitute for Statistics and Mathematics, Vienna University of Economics and Business (WU), Vienna, Austria††thanks: \EMAILtobias.fissler@wu.ac.at \AUTHORSilvana M. Pesenti \AFFDepartment of Statistical Sciences, University of Toronto, Toronto, Canada††thanks: \EMAILsilvana.pesenti@utoronto.ca

We propose a holistic framework for constructing sensitivity measures for any elicitable functional of a response variable. The sensitivity measures, termed score-based sensitivities, are constructed via scoring functions that are (strictly) consistent for . These score-based sensitivities quantify the relative improvement in predictive accuracy when available information, e.g., from explanatory variables, is used ideally. We establish intuitive and desirable properties of these sensitivities and discuss advantageous choices of scoring functions leading to scale-invariant sensitivities.

Since elicitable functionals typically possess rich classes of (strictly) consistent scoring functions, we demonstrate how Murphy diagrams can provide a picture of all score-based sensitivity measures. We discuss the family of score-based sensitivities for the mean functional (of which the Sobol indices are a special case) and risk functionals such as Value-at-Risk, and the pair Value-at-Risk and Expected Shortfall. The sensitivity measures are illustrated using numerous examples, including the Ishigami–Homma test function. In a simulation study, estimation of score-based sensitivities for a non-linear insurance portfolio is performed using neural nets.

Consistency; Elicitability; Expected Shortfall; Information value; Value-at-Risk

1 Introduction

We consider the context of quantitative risk management where describes a random variable of interest, e.g., an (insurance) portfolio. The vector , , describes the risk factors or risk factor changes which determine via a mapping or aggregation function , such that , see e.g. McNeil et al. (2015). Typical in applications is that not all risk factors are observable, e.g., only functions of are observable, or their observation is costly. In such situations, the available information may be expressed via a random vector , , and in the absence of knowing what factors determine , may contain information irrelevant for modelling .

The key question we aim to address is: How sensitive is with respect to ? Or more specifically: What is the information value of for ? This can be made more precise by assessing by how much the uncertainty of is reduced when knowing/learning . We will see that this latter question can be equivalently rephrased as: What is the gain in predictive accuracy for when knowing ? To answer these questions one needs to first clarify some imminent ones. How is uncertainty of measured? And what is the predictive target? As for the latter, one distinguishes between probabilistic predictions, that is, specifying the full conditional distribution of given , and point predictions. For point predictions the conditional distribution of given is summarised by a functional such as the mean or a law-determined risk measure, e.g., Value-at-Risk (VaR) or Expected Shortfall (ES). Then, truthful prediction amounts to specifying the correct conditional distribution or a functional thereof, .

The above raised question is typically addressed using sensitivity analysis, and in particular, via sensitivity measures or importance measures (Saltelli et al. 2008). Sensitivity measures associate the uncertainty in with the uncertainties in the risk factors in a way that allows for e.g., importance ranking of risk factors. Such an importance ranking may inform where to direct scarce resources to collect more data. Besides, it may lead to model simplifications when a factor is deemed to have irrelevant explanatory power. The literature on sensitivity measures is vast and we refer to Borgonovo and Plischke (2016) and Razavi et al. (2021) for an extensive review. Examples of sensitivity measures include variance-based (Saltelli and Tarantola 2002), moment-independent (Borgonovo 2007), and quantile-based sensitivities (Browne et al. 2017). Alternative approaches include those based on divergence measures (Gamboa et al. 2018, Pesenti et al. 2019, Fort et al. 2021, Pesenti 2021) and differential sensitivity measures, see Tsanakas and Millossovich (2016) and Pesenti et al. (2021) in a risk management context. However, as argued in Borgonovo et al. (2021), the choice of a sensitivity measure should be intimately tied to the functional of interest via the notion of strictly consistent scoring functions and moreover reflect the information value of risk factors.

A scoring function or scoring rule maps the tuple , consisting of a prediction and an observation of , to the non-negative real number with the convention that smaller values of reflect more accurate predictions of . Here, the prediction may be a point prediction, an interval, or the entire probability distribution or density of . As forcefully argued in Murphy and Daan (1985), Engelberg et al. (2009), and Gneiting (2011), a score should be strictly consistent for a functional . A strictly consistent score incentivises truthful predictions in the sense that the expected score is strictly minimised by the target at hand, which in our setup is the conditional distribution or a functional thereof, . Examples for strictly consistent scoring functions are the squared loss for the mean functional and the negative log-likelihood or the continuous ranked probability score for the conditional distribution (Gneiting and Raftery 2007). If a functional admits a strictly consistent scoring function it is called elicitable (Lambert et al. 2008). Many functionals of interest are elicitable, e.g. the mean via the squared loss and the median via the absolute loss . As for risk measures, entropic risk measures, VaR, and expectiles are elicitable, while the variance, standard deviation, and ES fail to be elicitable (Osband 1985, Weber 2006, Gneiting 2011). However, the pair consisting of the mean and variance (or standard deviation) and the pair VaR and ES admit strictly consistent scoring functions (Fissler and Ziegel 2016).

If the functional of interest is elicitable, the information value of for can be measured by the potential reduction of uncertainty when knowing – expressed by a strictly consistent scoring function – that is by ; a notion first proposed in the sensitivity literature by Borgonovo et al. (2021). We build on their suggestion by defining for a strictly consistent scoring function the score-based sensitivity measure of to information as

see Definition 2.2 for a precise statement of the involved assumptions. By construction, the score-based sensitivity measure attains values in and is unitless, which allows for comparison of sensitivities to risk factors that live on different scales. Sensitivity measures constructed via strictly consistent scoring functions include the Sobol indices (and extensions thereof), corresponding to the mean functional and the squared loss (Borgonovo et al. 2021), and the contrast index studied in Maume-Deschamps and Niang (2018), corresponding to the pinball loss and the VaR functional. Fort et al. (2016) consider a related concept using contrast functions in the machine learning literature. Sensitivity concepts that reflect value of information (which typically are intimately connected to scoring functions) have been studied by Felli and Hazen (1998) and more recently by Borgonovo and Cillo (2017) in the context of probability safety assessment, and by Straub et al. (2021) in applications to reliability analysis.

In this paper, we provide a comprehensive framework for constructing score-based sensitivity measures for any elicitable functional . Moreover, we establish universal properties of score-based sensitivity measures that are inherited by any elicitable functional with any strictly consistent scoring function. In particular, we argue that sensitivity measures should possess the zero information gain property, a property significantly weaker than Borgonovo et al. (2021)’s nullity-implies-independence property. Indeed, while the nullity-implies-independence property means that a zero sensitivity implies that and are independent, we only require that a sensitivity of zero is equivalent to being irrelevant for modelling . Furthermore, we show that a score-based sensitivity measure is equal to 1 if and only if contains all relevant information to model . We additionally define an interaction sensitivity measure – termed interaction information – that quantifies the information value of interactions of risk factors. In the special case of the squared loss scoring function we recover the well-known Sobol interaction terms.

One imminent challenge of score-based sensitivity measures is the choice of scoring function. An elicitable functionals typically admits infinitely many strictly consistent scoring functions. Furthermore, as we illustrate in examples, different scoring functions may lead to sensitivity measures that rank information, and thus risk factors, differently. To overcome these difficulties, we advocate for scoring functions that lead to scale-invariant sensitivities. We moreover promote and illustrate the usage of Murphy diagrams, which has been impressively demonstrated in the context of scoring functions in Ehm et al. (2016). Another challenge is the estimation of the score-based sensitivity, in particular the term . One way to address this is with neural nets from machine learning, which we do in Section 5.

This paper is organised as follows. Section 2 motivates and defines score-based sensitivity measures. In Section 3 we discuss their universal properties and introduce a sensitivity that quantifies the value of information of interactions of risk factors; termed interaction information. Section 4 discusses the choice of strictly consistent scoring functions and defines score-based Murphy diagrams for sensitivity measures. We illustrate the score-based sensitivities on the Ishigami–Homma test function and a non-linear insurance portfolio in Section 5.

2 From Scoring Functions to Sensitivity Measures

Let be a complete probability space on which we identify random elements which almost surely coincide. Moreover, if not stated explicitly, all events such as equalities, inequalities, etc., are to be understood in an almost sure sense. We use the decision-theoretic setup and notation of Gneiting (2011) and Fissler et al. (2021a). For this let be the class of all Borel probability measures on and let be two sub-classes. We equip with the -algebra generated by the family of evaluation maps given by , which map . We moreover identify any probability measure with its cumulative distribution function , . Further, let be an action domain – in our context, this is typically the interval , , or – equipped with with the Borel -algebra. The predictive goal is then described by the measurable functional and we refer to Fissler and Holzmann (2022) for measurability results for functionals of interest such as the mean, expectiles, Value-at-Risk (VaR), and Expected Shortfall (ES).

For a random variable in some class we denote its cumulative distribution function by . For a sub--algebra – often referred to as information set – we denote by a regular version of the conditional distribution of given . (Recall that is a measurable map from to (Fissler and Holzmann 2022).) If and (almost surely, which will be suppressed in the sequel), we can consider the (measurable) random variables and . If is generated by some random vector , i.e. , then we simply write and use the shorthand .

Definition 2.1 (Consistency & Elicitability)

A scoring function (or score) is a measurable map . For a functional and a sub-class the scoring function may satisfy the following properties:

-

is -consistent for , if for all and for all

(1) -

is strictly -consistent for , if it is -consistent for and if the inequality in (1) is strict for all .

-

is elicitable on , if there exists a strictly -consistent scoring function for .

Elicitability of a functional is equivalent to the fact that it is a Bayes act or the minimiser of an expected score (Gneiting 2011).

We will work with the following set of assumptions throughout the rest of the paper.

Let be an -consistent scoring function for and . Suppose that for all and that for all .111For , the point measure is a probability measure such that for any , if and otherwise. Note that is a random probability measure on . Let the following hold:

-

for all .

-

for all , .

-

For all , .

-

For all , .

Assumption 2 part (ii) amounts to strict consistency for on the class of point measures . Part (i) is a normalisation condition and can be achieved under (ii) by considering the normalised score . The finiteness in (iii) is implied if is strictly -consistent. Indeed, if , it cannot be strictly smaller than for . Condition (iv) usually holds if is strictly -consistent and is not constant almost surely.

It is well-known that consistent scoring functions respect increasing information sets (Holzmann and Eulert 2014, Theorem 1). This means that if is -consistent for and if are two sub--algebras such that , then

| (2) |

If is strictly -consistent for , then equality in (2) holds only if . (The main argument behind this result is an application of the definition of (strict) consistency in combination with the tower property for the conditional expectation.) This provides a motivation for considering, for , the term

| (3) |

which corresponds to the resolution term of the score decomposition in Pohle (2020), the discrimination in Gneiting and Resin (2021), and it is a special instance for a score divergence (Thorarinsdottir et al. 2013, Gneiting and Raftery 2007, Dawid 2007), which is related to the cost of uncertainty discussed in Frankel and Kamenica (2019). The resolution term (3) quantifies how helpful the information is to improve the correct baseline model , when used ideally. This improvement is naturally measured in terms of a consistent score (Gneiting 2011). The next definition quantifies this improvement relative to the so-called oracle improvement of full information

where equality follows from Assumption 2 (i) and the fact that and strict positivity from Assumption 2 (iv).

The resolution term normalised by the oracle improvement motivates to consider the following notion of sensitivity measure. The sensitivity measure is inspired by Borgonovo et al. (2021) who introduced sensitivity measures based on scoring functions to the sensitivity literature.

Definition 2.2 (Sensitivities based on scoring functions)

Let be an -consistent scoring function for with satisfying Assumption 2, a random variable, and an information set with . Then the sensitivity of to based on is given by

| (4) |

The larger the value of , the larger is the information value of , measured by the scoring function . While Borgonovo et al. (2021) consider sensitivity measures based solely on the numerator of (4), our proposed sensitivity measure is normalised to lie between 0 and 1; see Theorem 3.1 for details. This normalisation is achieved by the division with the oracle improvement ; a quantity called uncertainty in the forecasting literature (Gneiting and Resin 2021). is a generalisation of the variance which arises when is the squared loss. Our sensitivity measures closely resemble the universal coefficient of determination which was recently introduced by Gneiting and Resin (2021) and which generalises the classical coefficient of determination R2. The subtle difference is that in this work, the term in (4) is conditionally calibrated with respect to the information , whereas Gneiting and Resin (2021) require the notion of a “conditionally -calibrated forecast”, which is generally a weaker assumption. Moreover, (4) is a special instance of a skill score due to Murphy (1973); see also Gneiting and Raftery (2007) for a discussion.

Exploiting the consistency of for in Definition 2.2, we could replace by and by , where the latter minimum is taken over all -measurable random variables . Thus, the score-based sensitivity only depends on the functional through its consistent score.

In the sequel, we shall use the shorthand to indicate the sensitivity of with respect to the information generated by a random vector .

3 Properties of Score-based Sensitivities

Theorem 3.1 provides the core properties of our score-based sensitivities.

Theorem 3.1

Let be an -consistent scoring function for with satisfying Assumption 2, a random variable, and an information set with . Then, satisfies the following properties.

-

(a)

Normalisation: .

-

(b)

Zero information gain: implies . If is strictly -consistent then only if .

-

(c)

Full information gain: implies that . If is strictly -consistent then only if .

-

(d)

Monotonicity with respect to nested information: For any information set with and it holds that . If is strictly -consistent then only if .

Proof of Theorem 3.1. The normalisation follows from the non-negativity of the resolution term (3). The remaining assertions are a corollary of Theorem 1 in Holzmann and Eulert (2014). \Halmos

The normalisation of the proposed sensitivity has the obvious advantage of rendering the sensitivity unitless. This facilitates comparison of sensitivities to risk factors that live on different scales in a straightforward manner. In the subsequent subsections we discuss the properties of the proposed sensitivity measures, including the ones established in Theorem 3.1, and provide illustrating examples. Interestingly, these properties (almost) correspond to four of the five axioms stipulated in Griessenberger et al. (2022) for a dependence measure between and , which yields an alternative angle on our sensitivity measures.

3.1 Zero Information Gain

We first start with an obvious, yet important, corollary of the zero information gain property stated in Theorem 3.1 (b).

Corollary 3.2

Under the assumptions of Theorem 3.1, if and are independent, then .

Corollary 3.2 follows from Theorem 3.1 since independence of and is equivalent to , which implies that .

Clearly, if and are stochastically independent, does not contain any information about . The perspective of the zero information gain property, however, is more nuanced than independence. Assume that contains information about , i.e., they are not independent, but the information is not relevant for modelling , i.e., , then the score-based sensitivity measure is equal to 0. Thus, the sensitivity measure being equal to 0 implies that contains no relevant information for modelling . Examples 3.3 and 3.4 below illustrate such situations. For the mean functional , the identity is also known as mean independence (Wooldridge 2013, p. 25) which is weaker than independence but stronger than uncorrelatedness. Following this terminology can be called -independence of from .

Borgonovo et al. (2021) advocate that sensitivity measures should satisfy the so-called nullity-implies-independence (n.i.i.) property, see Definition 4 in Borgonovo et al. (2021); a property inspired by Rény’s postulate D for measures of dependence (Rényi 1959). A (sensitivity) measure satisfies the n.i.i. property – Rény’s postulate D – if the measure is zero if and only if and are independent. While Rényi considers measures of dependence between any two random variables, a sensitivity measure in our manuscript (and the extant literature) is a measure between the unconditional distribution and the conditional distribution of the output . Therefore, in our context, the n.i.i. property means that the sensitivity measure is 0 if and only if and coincide (almost surely). Since the conditional distribution enters the sensitivity measure (4) only via the functional , one cannot hope for the n.i.i. property unless is the identity functional. If a modeller is interested in the information value of for only, the n.i.i. property needs to be replaced by an achievable desideratum which is the zero information gain property. In this spirit, we may call the zero information gain property the “nullity-implies--independence”, which we illustrate in Examples 3.3 and 3.4. We emphasise that for the special case of probabilistic predictions, i.e. when is the identity map, the zero information gain property coincides with the n.i.i. property; see Proposition 6 in Borgonovo et al. (2021).

Example 3.3

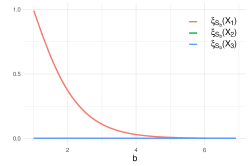

Consider the output , where are independent and non-deterministic, , and . Clearly, and are dependent. For the mean functional, we obtain that . Thus, knowing does not help to make a mean-model more precise. Therefore, for any consistent scoring function for the mean functional.

For the next example, we recall the definition of Value-at-Risk (VaR) of a random variable at level which is given by

corresponding to the left-continuous -quantile of the distribution of . Since VaR is a law-determined functional, we may write .

Example 3.4

Let be independent, has a Bernoulli distribution with , and almost surely for a constant . The output may be viewed as an insurance portfolio consisting of small claims – smaller than – which occur with probability , and large claims – larger than – occurring with probability . Then,

Moreover,

Thus, knowing does not improve the modelling of the functional even though and are dependent. The reason is that only affects the distribution of in the left tail below the -quantile. As a consequence, for any consistent score for it holds .

3.2 Full Information Gain

The counterpart of zero information gain is full information gain. We start with a straightforward and important observation.

Corollary 3.5

Under the assumptions of Theorem 3.1, if is -measurable, then .

Again, the proof of Corollary 3.5 is simple. If is -measurable, the conditional distribution of given reduces to a random point measure in , that is . This in turn implies that and therefore by Assumption 2(i).

Corollary 3.5 for example applies if is generated by a real-valued random variable such that the pair is co- or countermonotonic. Another example of being -measurable is if is generated by all risk factors, i.e., and . Similar comments about the relevance of information with respect to only can be made corresponding to the ones in Subsection 3.1. In particular, the below example shows that we can obtain a sensitivity of 1, i.e. we have all relevant information for , even if itself cannot be fully explained by .

Example 3.6 (Example 3.4 continued)

We consider independent, Bernoulli distributed with , and almost surely, for some constant , where has finite mean. Then, the output is not measurable with respect to . However, for the functional , we have that . By part c) of Theorem 3.1, for any consistent scoring function for we get that . Example 3.6 shows that knowing fully explains , which implies that , however, is not measurable with respect to .

3.3 Monotonicity with respect to Nested Information

It is difficult to compare arbitrary sets of information. Put mathematically, there is no canonical total order on the class of all sub--algebras of . However, the subset relation is a sensible partial order on this class and Theorem 3.1 (d) asserts that our sensitivities are monotone with respect to this partial order. Some direct consequences are immediate, for example in regard to transformations of explanatory variables.

Corollary 3.7

The proof follows by invoking that . The inclusion becomes an equality if is an injection.

Corollary 3.7 implies that injective transformations of risk factors do not affect the sensitivities. Examples include affine transformations or (component-wise) logarithmic scaling of explanatory variables. If the transformation is not injective, then the transformation may induce a loss of information, e.g., a projection to components of (reduction of dimensionality) implies that , for any subvector of .

Again, we stress that monotonicity with respect to nested information sets only takes relevant information for modelling into account. We illustrate this with the following example.

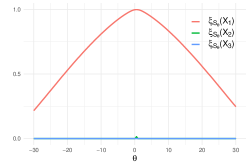

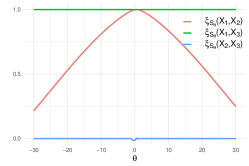

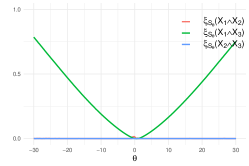

Example 3.8

Let , where are independent standard normal. The target functional is the mean and and the squared loss. Then, we obtain that

Next, we consider the transformation , then . Using part (b) of Theorem 3.1, the sensitivity to , , are

This also constitutes another example for Theorem 3.1 (b), where the information is not independent of but irrelevant for prediction purposes.

3.4 Interaction Information

Important in sensitivity analysis, particularly for non-additive models, is the calculation of interaction indices, which quantify the effects that multiple risk factors have jointly on the functional of interest minus their individual effects, see e.g. Chapter 4 in Saltelli et al. (2008). In an information value setting, the relevant question that quantifies interaction information between two information sets and is: “How much do we learn from knowing both jointly, once we already know and individually”. We formalise this in the next definition.

Definition 3.9 (Interaction Information)

The sensitivity of with respect to the interaction information of based on is given by

where is the smallest -algebra which contains all elements of and , i.e., .

Remark 3.10

The sensitivity with respect to the interaction information does generally not coincide with the sensitivity with respect to the intersection of the two information sets, .222For example, consider the probability space , where is the Borel -algebra on and is the measure of a standard normal distribution on . For define the random variables and . Then are two independent standard normal random variables and is the trivial -algebra . If is a linear combination of and such that and are not perfectly correlated, then is still trivial.

Example 3.11 (Variance-based Interactions)

For variance-based sensitivity measures, that is, when is the mean and the squared loss, we recover the Sobol interaction term if the information sets and are independent. Indeed, the sensitivity of with respect to the interaction information of and is

| (5) |

The first summand in (5) is the normalised joint effect of and , while the second and third term are the normalised first-order effects to and , respectively; see e.g., Saltelli and Tarantola (2002).

While for the special case of Sobol indices the interaction terms are always non-negative, this need not be the case for general scoring functions and prediction functionals, as is illustrated in the next proposition and example.

Proposition 3.12 (Information is Not Additive)

Sensitivities are generally neither subadditive nor superadditive, in the sense that the term can generally take any sign.

Proposition 3.12 follows from the following example.

Example 3.13

Let , where are jointly normal with means 0, variances 1 and correlation . The target functional is the mean and we consider the scoring function . Moreover, let , . In this context . On the other hand,

Interestingly, we obtain additivity in Example 3.13 for the case when and are independent, i.e., if . The following modification of Example 3.3 shows, however, that independence of and does not imply additivity.

Example 3.14

4 Choice of Score-based Sensitivities

So far we did not discuss the choice of (strictly) consistent scoring function for a functional to compute score-based sensitivities. This is, however, an important issue since almost all elicitable functionals possess rich classes of (strictly) consistent scoring functions each of which could lead to a different score-based sensitivity measure. In this section, we discuss potential choices of scoring function and their implication on the corresponding score-based sensitivities. We first discuss scale-invariant score-based sensitivity measures which leads to the subclass of homogeneous scores (Section 4.1). We further introduce score-based Murphy diagrams which allow for graphical illustrations of score-based sensitivities (Sections 4.2 and 4.3).

Throughout this section, the concepts are illustrated on the mean functional and the -quantile (or ). For this, we first recall their family of consistent scoring functions in the next proposition, referring to Gneiting (2011). For an overview of characterisation results of other important functionals such as entropic risk measures, expectiles, the mode, the pairs (mean, variance), (, ), and Range Value-at-Risk (RVaR) together with its VaR-components, we refer to Appendix 7.

Proposition 4.1 (Gneiting (2011))

-

Let be the class of distributions with finite mean. If is (strictly) convex with subgradient , then

(6) is (strictly) -consistent for the mean, if for all . Moreover, on the class of compactly supported measures, any (strictly) consistent scoring function for the mean which is continuously differentiable in its first argument and which satisfies is necessarily of the form (6).

-

If is increasing, the score

(7) is -consistent for if for all . If is strictly increasing and if for all , for all , then (7) is strictly -consistent. Moreover, on the class of compactly supported measures, any consistent scoring function for which is continuous in its first argument, which admits a continuous derivative for all and which satisfies is necessarily of the form (7).

Scoring functions of the form (6) are called Bregman scores and the scores in (7) are termed generalised piecewise linear scores. Almost all different choices of in (6) and in (7) lead to different score-based sensitivity measures for the mean and VaR, respectively. Indeed, the next proposition states the family of score-based sensitivity measures for the mean and VaR arising from their scoring functions given in Proposition 4.1. To that end, recall the definition of the Expected Shortfall (ES) of a random variable at level (Acerbi 2002)

| (8) | ||||

Since ES is law-determined, we may write instead of .

Proposition 4.2

-

For any strictly convex function and any random variable such that is integrable and such that , the score-based sensitivity for induced by the Bregman score (6) is

(9) -

For any strictly increasing function and any random variable such that is integrable and such that , the score-based sensitivity for the -quantile, , induced by the generalised piecewise linear score (7) is

(10)

Proof of Proposition 4.2. First, we prove (9). For this, let , then

which shows (9). To prove (10), let , and note that since is strictly increasing . Next, we use the second identity in (8) to obtain

Similarly,

Inserting the above into the formula for the sensitivity measures completes the proof. \Halmos

Obviously, scaling the scoring function leaves the value of the sensitivity measure unaffected, i.e., , for any . But otherwise, different choices of scoring functions lead to different sensitivities. In particular, these different sensitivities may induce different rankings of information value, see Example 4.15 in Section 4.3 for an illustration. Proposition 4.2, however, offers some further insight on the ordering of sensitivity measures for the mean and quantile. Specifically, for the mean functional, Proposition 4.2 (case i)) states an if and only if condition for the ordering of sensitivities. Indeed, , if and only if, for convex and two (not necessarily nested) information sets , , see also Theorem 3.1 in Krüger and Ziegel (2021). This condition thus establishes monotonicity of the sensitivity measure for the mean functional for situations beyond nested information sets. An Example of interest is , where are independent and normally distributed with mean 0 and variances , respectively. Then it holds for all convex functions that , if and only if, , see also Example 3.2. in Krüger and Ziegel (2021). A similar argument can be made for the quantile, i.e. part ii) of Proposition 4.2. Indeed the sensitivities for the are ordered , if and only if, , for increasing and two not necessarily nested information sets , . For further discussion, we refer the interested reader to Theorem C.1 in the online appendix of Krüger and Ziegel (2021).

There are many ways to choose a scoring function. One can use a scoring function motivated by tradition and interpretability. For the mean functional, for example, the traditional choice is the squared loss which results in the Sobol indices. We would like to promote two alternative choices. First, in Subsection 4.1 we consider scale-invariant sensitivities, i.e., sensitivities that are unaffected by scaling , which are induced by the important subclass of positively homogeneous scores. Second, in Subsection 4.2, we use Murphy diagrams to illustrate score-based sensitivities simultaneously for basically the entire class of consistent scoring functions for a functional. Subsection 4.3 combines the ideas of its two previous subsections and promotes a way to assess sensitivities simultaneously for all positively homogeneous scores.

4.1 Scale-invariant Sensitivities

Baucells and Borgonovo (2013) introduce and advocate for the use of sensitivities which are invariant under (strictly) monotone transformations of the output . A sensitivity based on is invariant under monotone transformations if for any random variable and any information set

for all strictly increasing functions . The only score-based sensitivity reported in Table 6 of Borgonovo et al. (2021) which is invariant under monotone transformations of the output is based on the log-score, where is a predictive density. The log-score is a strictly proper scoring rule which is tailored to evaluate probabilistic predictions (corresponding to the situation where is the identity map). To the best of our knowledge, we are not aware of any other score-based sensitivity, in particular also for point predictions, which is invariant under monotone transformations of the output . There are, however, examples of sensitivity measures that, while not score-based sensitivities, are transformation invariant under monotone transformation of the output random variables. We refer the interested reader to Plischke and Borgonovo (2019) and Baucells and Borgonovo (2013).

We suggest to consider a weaker, but still very relevant, invariance criterion.

Definition 4.3 (Scale-invariance)

A sensitivity based on is scale-invariant if for any random variable and any information set

A scale-invariant sensitivity measure is a sensitivity measure that takes on the same value, independent of the units in which is reported. We will see that a score-based sensitivity measure is scale-invariant if the employed scoring function is homogeneous, which in turn implies that the considered functional is homogeneous of degree 1. Thus, to discuss scale-invariant score-based sensitivity measures, we first define positive homogeneity for scoring functions.

Definition 4.4 (Homogeneity)

Let be the positive half-line, the negative half-line or the whole . A scoring function is positively homogeneous of degree , if for all and for all . We call a scoring function positively homogeneous if there exists a such that it is positively homogeneous of degree .

Next, we establish a sufficient condition for an elicitable functional to be homogeneous of degree 1.

Proposition 4.5 (Homogeneous Elicitable Functionals)

Let be the positive half-line, the negative half-line, or the whole . If there is a positively homogeneous score which is strictly -consistent for , then is positively homogeneous of degree 1.

Proof of Proposition 4.5. The assertion is a special instance of Lemma 4.3 in Fissler and Ziegel (2019). For completeness, we provide a short proof. Let be strictly -consistent for and positively homogeneous of degree . Then, for all with and for all , it holds that if , then setting implies that , and we obtain that

Many functionals of interests such as monetary risk measures, which include the entropic risk measures, VaR, ES, and RVaR, are by definition homogeneous of degree 1 (scale-equivariant), i.e., for all . Moreover, these elicitable functional possess homogeneous scores. Note that positive homogeneity of implies that for any information set . The next proposition provides a sufficient condition for a score-based sensitivity to be scale-invariant.

Proposition 4.6

Let be the positive half-line, the negative half-line, or the whole . If there is a positively homogeneous score which is strictly -consistent for , then, the score-based sensitivity is scale-invariant.

The proof of Proposition 4.6 is a direct consequence of Proposition 4.5 and that , for all and . \Halmos

The above proposition implies that if scale-invariance is a desired property a homogeneous score should be chosen for the score-based sensitivity measures. Many elicitable and positively homogeneous functionals admit positively homogeneous scoring functions, which enables to build scale-invariant score-based sensitivities. We recall the family of homogeneous scoring functions for the mean and VaR functional from the literature.

Proposition 4.7 (Homogeneous Scores for the Mean (Nolde and Ziegel 2017, Patton 2011))

The class of strictly consistent and -homogeneous scores for the mean satisfying are given by any positive multiple of a member of the Patton family

| (11) |

where we require that .

Note that homogeneous scores of a given degree are unique up to positive scaling and that scaling a score does not affect the sensitivity. The positively homogeneous scores in (11) arise from (6) upon choosing the strictly convex functions for , for , and for . Note that in (11) we require to be strictly positive. There are no strictly consistent and -homogeneous scores for the mean on , since there are no convex and -homogeneous functions on for . For , however, one may choose

for positive constants . We refer to the supplement of Nolde and Ziegel (2017) which contains the characterisation results of positively homogeneous and consistent scoring functions for the -expectile; for which the mean arises for . Moreover, this supplement contains similar characterisation results for VaR and the pair consisting of VaR and ES. We state the former.

Proposition 4.8 (Homogeneous Scores for VaR (Nolde and Ziegel 2017))

The class of strictly consistent and -homogeneous scores for satisfying are given by any positive multiple of

where

for a positive constant .

Again, if , homogeneous scores of a certain degree are unique up to positive scaling. We could also consider transformations other than scaling, such as e.g., translations. Then, if the score is invariant and the functional is equivariant for that transformation, we directly retrieve the corresponding invariance of the score-based sensitivity for that transformation. If we consider transformations with respect to which the functional of interest is not equivariant or the score is not invariant, we do not obtain an invariance property of the resulting sensitivity measure . In case of the mean and the coefficient of determination, R2, this fact is very well known and described in standard Econometrics textbooks.333E.g. Wooldridge (2013, p. 194) writes “…it is not legitimate to compare -squareds from models where is the dependent variable in one case and is the dependent variable in the other. These measures explain variations in different variables.” (The emphasis in the quote is original.) We further illustrate this in the following example.

Example 4.9

Let , where are independent and standard normally distributed. Consider the mean functional with the squared loss score. Then the sensitivity of with respect to is

In contrast, the sensitivity of with respect to based on the squared loss is

We emphasise that for a function , the sensitivity of with respect to is in general not equal to the sensitivity of with respect to if is not affine.

4.2 Murphy Diagrams Based on Elementary Scores

In contrast to Subsection 4.1, where we discuss the choice of score-based sensitivity measure by imposing additional restrictions on the scoring functions, here, we pursue a different strategy. Since different choices of scoring functions may lead to different rankings of information in terms of score-based sensitivities, we suggest to simultaneously consider (ideally) all sensitivity measures that arise by (strictly) consistent scoring functions. While there are many characterisation results for consistent scoring functions available in the spirit of Proposition 4.1, these classes are typically indexed by an infinite dimensional parameter space, e.g., the space of convex functions for the mean or the space of increasing functions for the quantile. This fact renders a computation and comparison of all score-based sensitivities practically infeasible at first glance.

Ehm et al. (2016) establish so-called mixture representations of classes of all consistent scoring functions for the mean444And more generally also the -expectile. and the -quantile; subject to mild regularity conditions. That is, they show that is a consistent scoring function for the mean (or the -quantile) if and only if there is a non-negative and -finite measure on such that

| (12) |

where the class consists of co-called elementary scores, which are consistent scores for the mean (or the -quantile). Moreover, the measure is uniquely determined by . We recall the formal statements.

Proposition 4.10 (Elementary Scores for the Mean and VaR (Ehm et al. 2016))

These mixture representations of Proposition 4.10 open the door to assess prediction dominance with respect to almost any Bregman score or generalised piecewise linear score. I.e., for any (possibly random) forecasts , we obtain that for all Bregman scores (6) with left-continuous subgradient , if and only if, for all elementary scores in (13). Ehm et al. (2016) demonstrate that this equivalence can be used to establish forecast dominance by inspecting the so called Murphy diagrams.

Definition 4.11 (Murphy Diagrams; Ehm et al. (2016))

Let be a class of scoring functions indexed by . For an observation and two (possibly random) forecasts , the Murphy diagram of the score difference with respect to is the map

Clearly, in applications one can approximate the Murphy diagram with the corresponding empirical counterparts of the expectations. The following result shows that we can apply a similar rationale in our context of score-based sensitivities and therefore introduce Murphy diagrams for score-based sensitivity measures.

Proposition 4.12 (Ordering of Score-based Sensitivities)

Suppose is a class of consistent scoring functions for a functional and a subclass of such that for any there exists a non-negative -finite measure on such that

| (14) |

Then, for any response and any information sets and , the following are equivalent:

-

;

-

.

Proof of Proposition 4.12. The implication “ ” is obvious since by assumption for all . For the other direction, suppose that holds. Then, for all it holds that if and only if . Hence, implies that for any and any

| (15) |

(15) in turn is equivalent to . Finally, (15), the construction of the integral (14), and Fubini’s Theorem imply . \Halmos

Proposition 4.12 implies that if we want to check whether information is more important for modelling than with respect to all score-based sensitivities, it suffice to establish this ranking with respect to all elementary score-based sensitivities. This motivates to consider the following Murphy diagrams for score-based sensitivities.

Definition 4.13 (Murphy Diagrams for Sensitivities)

Let be a class of scoring functions indexed by . The sensitivity of to based on is given by the Murphy diagram for sensitivities

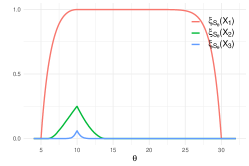

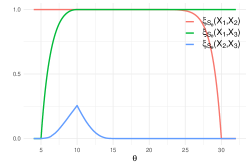

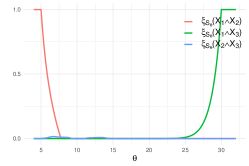

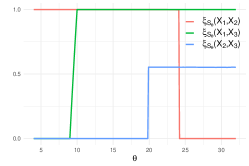

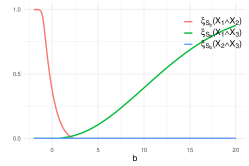

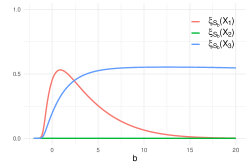

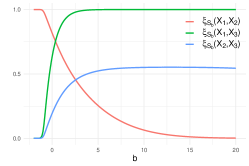

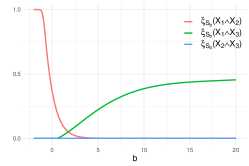

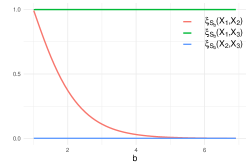

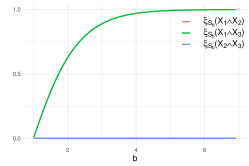

Example 4.14 (Example 3.4 Continued)

Let be independent, Bernoulli distributed with , and almost surely, for , and consider the output . We further choose , , uniformly distributed on , and , where has a Gamma distribution with mean 20 and variance 10.

Table 1 contains the conditional functionals for one and two risk factors for the mean functional and the used for calculating the score-based sensitivities. Figure 1 displays the corresponding Murphy diagrams of the elementary score-based sensitivities for the mean functional and the . All plots are based on simulations. We observe that the sensitivities of the mean to one risk factor are ordered, that is for all , see top left panel of Figure 1. This implies that the sensitivities to one risk factor are ordered for all strictly consistent scoring functions. This is in contrast to the sensitivity for . Comparing the mean functional with the , we observe that has a large sensitivity for both functionals, the sensitivity to is larger for the mean compared for the , and the sensitivity to is larger for the compared for the mean. This reflects that influences the mean of while influences the tail, hence the of .

4.3 Murphy Diagrams for Homogeneous Scores

In Subsection 4.1 we have seen that a positively 1-homogeneous functional combined with a positively homogeneous scoring function renders the corresponding score-based sensitivity measure scale-invariant. Moreover, known characterisation results for positively homogeneous scores (Propositions 4.7, 4.8) state that, at least when is positive, the -homogeneous and strictly consistent scoring functions for the mean and the VaR are unique up to scaling. Since scaling the scores leaves the sensitivities unaffected, this means that for and for the mean and the VaR, there is only a one-dimensional family of scores – the -homogeneous ones – which render the sensitivity scale-invariant.

We propose to evaluate all of them jointly, making use of the Murphy diagram introduced in Definition 4.13. The difference to the Murphy diagrams for elementary scores is that here the diagram is considered with respect to the parameter , indicating the degree of homogeneity of the scoring function. That is

We illustrate the homogeneous score-based Murphy diagrams for the mean and functional in the next example. For comparison with the Murphy diagrams for elementary scoring function, we illustrate the homogeneous score-based Murphy diagrams on the same Example 4.14.

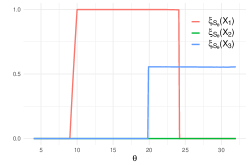

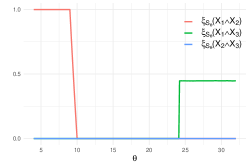

Example 4.15 (Example 4.14 Continued)

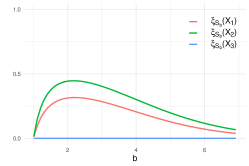

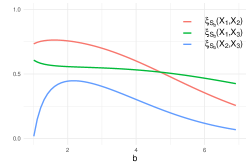

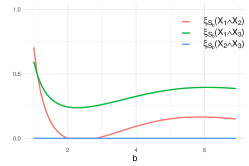

Figure 2 displays the Murphy diagrams of the homogeneous score-based sensitivities. Comparing with the elementary score-based Murphy diagrams in Figure 1, we observe a similar picture in that has a large sensitivity for both functionals, the sensitivity to is zero for the , and the sensitivity to is zero for the mean but large for the . The interaction sensitivities, right panels of Figure 2, show that the interaction between and are non-negligible for both functionals. This is informative, as the sensitivity to for the mean is equal to zero for all choices of homogeneous scoring functions. We obtain the Socol indices for .

The sensitivities for the mean to one risk factor (top left panel in Figure 2) are ordered: . This is in contrast to the sensitivities for the based on the homogeneous scores to one risk factor (bottom left panel in Figure 2). Indeed, for the sensitivities of to , , and are respectively , , and . For , the sensitivities of to is equal to 0.32, the sensitivities of to is , and to is equal to . Thus, different choices of strictly consistent scoring function for can lead to different rankings of risk factors.

Finally, we point out that the mixture representations of Proposition 4.10 hold for the corresponding elementary scores, but not for the positively homogeneous scores of Propositions 4.7 and 4.8. Hence, while it is the case that an ordering of the sensitivities with respect to all elementary scores implies an ordering with respect to all positively homogeneous scores, the reverse does not hold.

5 Applications

In this section we illustrate the score-based sensitivities on the well-known Ishigami–Homma test function in sensitivity analysis and a non-linear insurance portfolio.

The main challenge when calculating score-based sensitivities is the estimation of the conditional functionals , for a risk factor . For the Ishigami–Homma test function the conditional mean functionals, i.e., the conditional expectations, are available in closed form for all risk factors of interest. Thus, estimating Murphy diagrams for elementary and homogeneous score-based sensitivities may be conducted straightforwardly using Monte Carlo approximations of the expectations. In the non-linear insurance portfolio, however, closed form conditional functionals are not available. Thus, we use neural nets to estimate the conditional VaR and ES.

5.1 The Ishigami–Homma Test Function

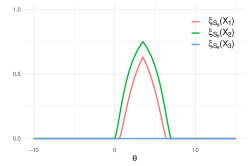

In this section we consider the Ishigami–Homma function given by (Ishigami and Homma 1990)

where are independent uniform random variables on . We consider the mean functional for comparison with the literature.

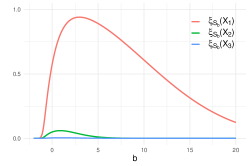

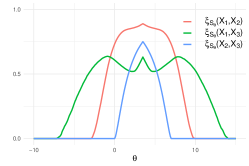

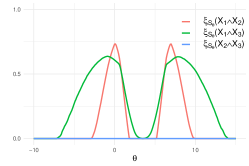

Figure 3 displays the score-based Murphy diagrams for the mean functional and for the choices and . The top panels correspond to the Murphy diagrams using the elementary scoring functions and the bottom panels correspond to homogeneous scoring functions. Both the homogeneous and elementary Murphy diagrams describe a similar pattern. Indeed, we observe that risk factor is most influential and and are non-influential with a sensitivity for all elementary and homogeneous scores close to zero. The interaction term of and , however, is equal to 1 for all scoring functions, reflecting the findings in Saltelli et al. (2008). Note that the sensitivity for the homogeneous score with are equal to the Sobol indices. We obtain that the Sobol indices of to , , is equal to . Similarly, and . We refer to Saltelli et al. (2008), Equation (4.34), for the analytical derivation of the Sobol indices of the Ishigami–Homma function, and to Pianosi and Wagener (2015) and Baroni and Francke (2020) for a recent discussion on the Ishigami–Homma function.

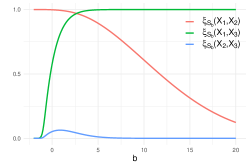

Next, we consider the Ishigami–Homma function with parameters and as in Marrel et al. (2009). The elementary and homogeneous score-based sensitivities for the mean functional are displayed in Figure 4. We observe that for these choices of and , the sensitivity to is larger than the sensitivity to for all strictly consistent scoring functions, see left panels in Figure 4. The estimated Sobol indices for , , and are , , and , respectively. The fact that the sensitivity to is larger than that to is in contrast to the choice and , for which the sensitivity to is negligible. The sensitivity to is zero for both sets of parameters and . For and , the sensitivity to knowing two components, i.e. , , or , strongly depends on the choice of the scoring function, as depicted in the right panels of Figure 4.

It is well-known that for the Sobol indices, the interaction of and is non-zero, see Figures 3 and 4 bottom right panel. Interestingly, for the choice and , this is the only interaction which is non-zero for all elementary scoring functions, see Figure 3. For homogeneous scores, however, the interaction between and becomes positive for large and small values of . Thus, considering Murphy diagrams reveals a more wholesome picture on the individual sensitivities and their interactions.

5.2 Non-linear Insurance Portfolio

In this section we consider an insurance company with three different lines of business whose losses are , and that are subject to a multiplicative factor , e.g., inflation. The insurance company has a reinsurance contract on the first two lines of business, , with deductible and limit . Thus, the insurance company’s total loss is given by

where denotes the positive part. The distributional assumptions are presented in Table 2 and we set the deductible to and the limit to . Furthermore, we assume the factors are dependent through a Gaussian copula with correlation matrix

| Risk factor | Distribution | Mean | Std |

|---|---|---|---|

| Log-Normal | 150 | 35.0 | |

| Log-Normal | 150 | 35.0 | |

| Gamma | 100 | 10.0 | |

| Log-Normal | 1 | 0.1 |

First, we calculate the score-based sensitivity for the at level . For simplicity, we choose the pinball loss

| (16) |

obtained with in (7).

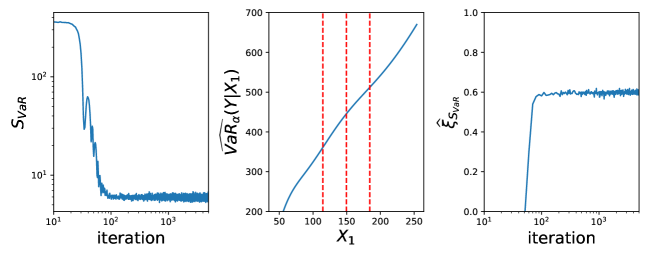

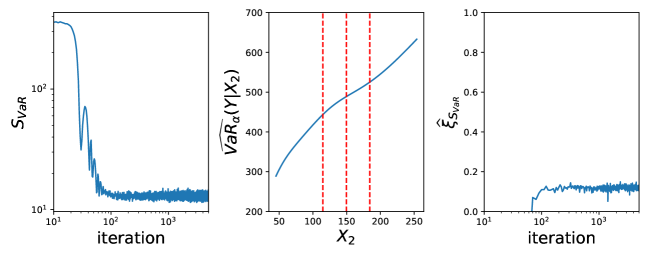

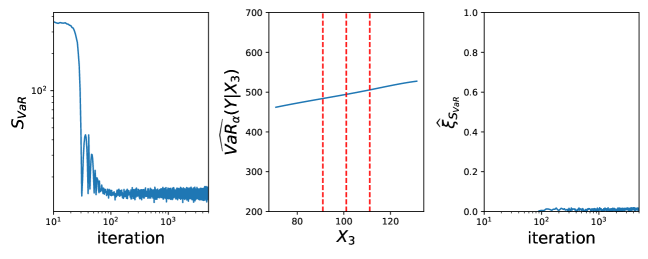

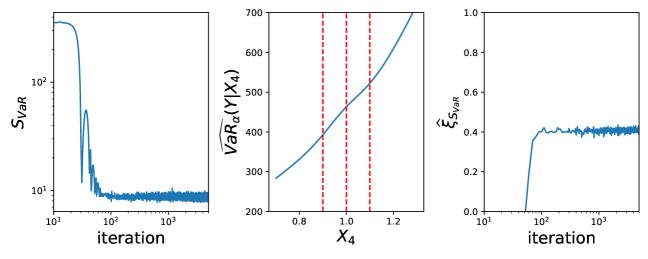

We calculate the score-based sensitivities to risk factors , where and is an index set of cardinality one or two such that is an at most two-dimensional subvector of . For this, we first calculate the conditional of the aggregate portfolio loss given , i.e., . Denote by , , the conditional quantile of given viewed, for fixed , as a function of . For each choice of , we approximate the function via a neural network (NN) denoted by , where are the network parameters. For relevant literature on estimating conditional VaR via NN – albeit in a different context – we refer the reader to Fissler et al. (2021b). The network parameters are learnt by iteratively minimising the expected score (16)

| (17) |

over independently simulated mini-batches , . That is, for each iteration we independently simulate a mini-batch of i.i.d. samples of . We denote the learnt NN by . After learning the NN, we estimate the sensitivity to out-of-sample, that is, using an independent sample , , of , via

| (18) |

where is the sample quantile of .

For each choice of , the NN structure consists of 6 hidden layers with 20 neurons per layer and SiLU activation functions apart from the last layer. The networks are learnt via independently simulated mini-batches of size , i.e. every single iteration uses an independently simulated i.i.d. samples of of size . Figure 5 displays the learning of the NN and the score-based sensitivities to single risk factors from (top row) to (bottom row), with . The left panel displays the average score for each mini-batch (Equation (17) with per mini-batch) against the iterations of learning the NN. The right panel displays the out-of-sample estimates of the score-based sensitivity (Equation (18) with ) against the iterations of learning the model. The middle panels display the learnt NN, , that is an estimate of as a function of , for from top to bottom. The red dotted lines correspond to the mean of and the first standard deviations from its mean. We observe that risk factor has the largest sensitivity. The sensitivity to is significantly larger than that to , even though and have the same distribution and the aggregate portfolio loss is symmetric in and . Thus, the difference in the sensitivities solely stems from the dependence structure of the portfolio; recall that is independent of while is highly correlated with . Moreover, the sensitivity to (the independent business line) is negligible, while, the sensitivity to , the multiplicative factor, is the second largest sensitivity.

Next, we estimate the score-based sensitivities to two risk factors, i.e., , for . We proceed similarly to estimating the score-based sensitivities to one risk factor in that we learn for each with , a NN using Equation (17) and independently simulated mini-batches. The corresponding sensitivities to are estimated using the learnt NN out-of-sample via Equation (18) with . The estimates of the sensitivities to one and two risk factors for the with level are reported in Table 3. We observe that the sensitivities with are close to the sensitivity to , thus knowing and then learning an additional risk factor does not considerably increase the sensitivity. This is in contrast to the sensitivity to the pair which is equal to 0.740, providing a sensitivity that is substantially larger than the sum of the sensitivities to and to .

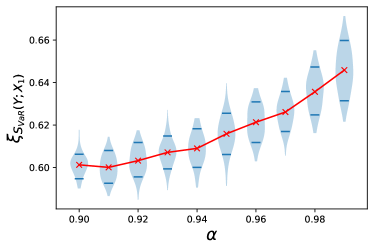

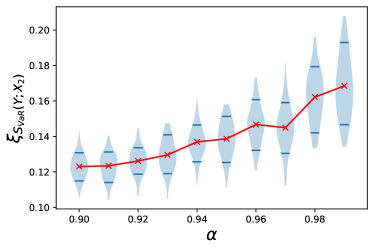

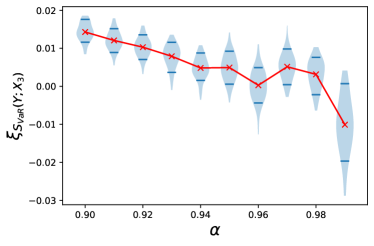

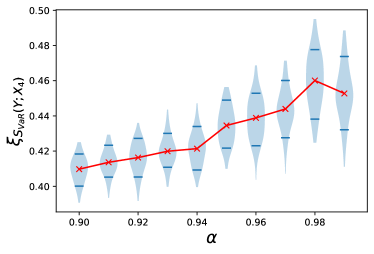

In Figure 6 we compare the score-based sensitivities to single risk factors for different levels of , that is from to . Specifically, we learn for each and risk factor a NN using the procedure prescribed above. Figure 6 displays violin plots of for and calculated using the learnt NNs. We observe that the sensitivities to , and are increasing in , whereas the sensitivity to is decreasing. The bottom left panel, depicting the sensitivity to , contains negative values for the sensitivities. These stem from statistical errors, as the sensitivities by definition should be non-negative. Note, however, that zero is contained in all 90% confidence intervals (displayed via the blue lines).

Next, we calculate the sensitivity of the insurance portfolio for the pair . Recall that is not elicitable on its own, but is jointly elicitable with (Fissler and Ziegel 2016). We consider the 0-homogeneous strictly consistent scoring function given by

| (19) |

which arises from the general family of scores in (22) with and . (Note that all risk factors and also are positive almost surely.) We proceed similarly to estimating the score-based sensitivities for , in that we use NNs to estimate the conditional functionals. Let be a sub-vector of the risk factors with dimension 1 or 2, and denote by and the conditional VaR and ES, viewed, for fixed , as a function of . Then, we jointly estimate and via two neural nets and , respectively. The network parameters are learnt by iteratively minimising the score (19)

| (20) |

over independently simulated mini-batches , , of . We denote the learnt NNs by and , respectively, and estimate the sensitivity to using the learnt NNs out-of-sample, that is using an independent sample , , of , by

| (21) |

where and are the sample quantile and sample ES of , respectively.

Since for all it holds that , we require that , for all . Thus, we define the NN for estimating the conditional ES by , where is constrained to be non-negative for all ; modelled using a softplus activation function on the last node. For each choice of , we choose a NN structure consists of 6 hidden layers with 20 neurons per layer. The activation functions are SiLU for each layer apart from the last layer which uses a softplus activation function.

The estimates of the score-based sensitivities for are reported in Table 4. We observe that the sensitivities are similar in magnitude to the sensitivities for the , see also Table 3. Moreover, the ranking of the risk factors stays the same.

6 Conclusion

This paper provides a comprehensive framework for constructing sensitivity measures induced by strictly consistent scoring functions for any elicitable target functional . These score-based sensitivities naturally quantify the relative information gain – when using available information ideally – to model the target functional. Theorem 3.1 establishes intuitive and desirable properties for these score-based sensitivities such as zero information gain and full information gain. Following Griessenberger et al. (2022), these properties suggest that the sensitivities can also be considered as a dependence measure between an output and an information set . We further define a sensitivity called interaction information, which quantifies the information gain when learning the interaction of risk factors. We show that sensitivities based on a positively homogeneous score are scale-invariant, making them attractive in applications. Using Murphy diagrams for score-based sensitivities, we illustrate how to inspect entire classes of sensitivities, thus providing a holistic impression and revealing yet unknown model characteristics.

We emphasise that our approach is general and works for sensitivities which focus on any elicitable functional. In particular, we discuss the entire family of score-based sensitivity measures for the mean functional (of which the Sobol indices are one special case) and construct sensitivities for the pair consisting of VaR and ES; both, to the authors’ best knowledge, novel endeavours to the literature.

Acknowledgements

The authors thank Johanna Ziegel and Timo Dimitriadis for stimulating discussions about the topic as well as three anonymous referees whose comments helped to substantially improve the paper. SP would like to acknowledge support from the Natural Sciences and Engineering Research Council of Canada (grants DGECR-2020-00333 and RGPIN-2020-04289).

7 Scoring Functions of Risk Functionals

This appendix provides an overview of known characterisation results of (strictly) consistent scoring functions for popular functionals. For precise technical conditions and statements see original references.

7.1 Entropic Risk Measures

Entropic risk measures, also called exponential premium principle in insurance, (Gerber 1974) are defined for a random variable and parameter by

Invoking the revelation principle (Osband 1985, Gneiting 2011), we can exploit the characterisation result (6) and obtain that, subject to mild regularity conditions, any (strictly) consistent score satisfying is of the form

where is (strictly) convex with subgradient such that for all .

7.2 Expectiles

For , the -expectile of a probability distribution is the unique solution of the equation

Gneiting (2011) characterises the class of (strictly) -consistent scoring functions for the -expectile satisfying as

where is (strictly) convex with subgradient such that for all .

7.3 Mode

The mode is generally not elicitable on classes of absolutely continuous distributions (Heinrich 2014, Heinrich-Mertsching and Fissler 2021). However, on distributions with countably many outcomes, the mode is elicitable. Gneiting (2017) showed that the zero-one loss is basically the only strictly consistent score such that . This yields the score-based sensitivity

where is the maximum of the counting density of and is the maximum of the conditional counting density of given .

7.4 Mean and Variance

We can again invoke the revelation principle to characterise the class of (strictly) -consistent scoring functions for the pair (mean, variance) satisfying Assumption 2 (i), such that . Following Fissler and Ziegel (2019) they take the form

where is (strictly) convex with subgradient , interpreted as a row vector, such that for all .

7.5 VaR and ES

ES generally fails to be elicitable (Osband 1985, Gneiting 2011, Weber 2006). However, the pair together with , at the same probability level , is elicitable, subject to mild conditions (Acerbi and Szekely 2014, Fissler and Ziegel 2016). Note that different sign conventions are used in the literature. Upon using the one introduced in 8, the (strictly) -consistent scoring functions for satisfying Assumption 2 (i) such that are of the form

| (22) | ||||

where , is (strictly) convex with subgradient and is such that for all

is (strictly) increasing. One convenient way to achieve this latter condition is to choose such that and to be increasing.

7.6 RVaR together with two VaR components

The Range Value-at-Risk (RVaR) at levels for a random variable has been introduced by Cont et al. (2010) and is defined as

RVaR fails to be elicitable on its own in general (Wang and Wei 2020). However, Fissler and Ziegel (2021) show that the triplet is elicitable subject to mild conditions. The (strictly) -consistent scoring functions satisfying Assumption 2 (i) such that are of the form

where for , is (strictly) convex with subgradient and are such that for all the functions

are (strictly) increasing. We refer to Fissler and Ziegel (2021) for examples of such scores as well as to the detailed conditions on .

References

- Acerbi (2002) Acerbi C (2002) Spectral measures of risk: A coherent representation of subjective risk aversion. Journal of Banking & Finance 26(7):1505–1518, URL https://doi.org/10.1016/S0378-4266(02)00281-9.

- Acerbi and Szekely (2014) Acerbi C, Szekely B (2014) Backtesting Expected Shortfall. Risk Magazine URL https://www.msci.com/documents/10199/22aa9922-f874-4060-b77a-0f0e267a489b.

- Baroni and Francke (2020) Baroni G, Francke T (2020) An effective strategy for combining variance-and distribution-based global sensitivity analysis. Environmental Modelling & Software 134:104851, URL https://doi.org/10.1016/j.envsoft.2020.104851.

- Baucells and Borgonovo (2013) Baucells M, Borgonovo E (2013) Invariant probabilistic sensitivity analysis. Management Science 59(11):2536–2549, URL http://dx.doi.org/10.1287/mnsc.2013.1719.

- Borgonovo (2007) Borgonovo E (2007) A new uncertainty importance measure. Reliability Engineering & System Safety 92(6):771–784, URL https://doi.org/10.1016/j.ress.2006.04.015.

- Borgonovo and Cillo (2017) Borgonovo E, Cillo A (2017) Deciding with thresholds: Importance measures and value of information. Risk Analysis 37(10):1828–1848, URL https://doi.org/10.1111/risa.12732.

- Borgonovo et al. (2021) Borgonovo E, Hazen GB, Jose VRR, Plischke E (2021) Probabilistic sensitivity measures as information value. European Journal of Operational Research 289(2):595–610, URL https://doi.org/10.1016/j.ejor.2020.07.010.

- Borgonovo and Plischke (2016) Borgonovo E, Plischke E (2016) Sensitivity analysis: a review of recent advances. European Journal of Operational Research 248(3):869–887, URL https://doi.org/10.1016/j.ejor.2015.06.032.

- Browne et al. (2017) Browne T, Fort JC, Iooss B, Le Gratiet L (2017) Estimate of quantile-oriented sensitivity indices. Preprint URL https://hal.archives-ouvertes.fr/hal-01450891.

- Cont et al. (2010) Cont R, Deguest R, Scandolo G (2010) Robustness and sensitivity analysis of risk measurement procedures. Quantitative Finance 10(6):593–606, URL https://doi.org/10.1080/14697681003685597.

- Dawid (2007) Dawid AP (2007) The geometry of proper scoring rules. Annals of the Institute of Statistical Mathematics 59(1):77–93, URL https://doi.org/10.1007/s10463-006-0099-8.

- Ehm et al. (2016) Ehm W, Gneiting T, Jordan A, Krüger F (2016) Of quantiles and expectiles: consistent scoring functions, Choquet representations and forecast rankings. Journal of the Royal Statistical Society Series B (Statistical Methodology) 78(3):505–562, URL https://doi.org/10.1111/rssb.12154.

- Engelberg et al. (2009) Engelberg J, Manski CF, Williams J (2009) Comparing the point predictions and subjective probability distributions of professional forecasters. Journal of Business & Economic Statistics 27(1):30–41, URL https://www.jstor.org/stable/27639017.

- Felli and Hazen (1998) Felli JC, Hazen GB (1998) Sensitivity analysis and the expected value of perfect information. Medical Decision Making 18(1):95–109, URL https://doi.org/10.1177/0272989X9801800117.

- Fissler et al. (2021a) Fissler T, Frongillo R, Hlavinová J, Rudloff B (2021a) Forecast evaluation of quantiles, prediction intervals, and other set-valued functionals. Electronic Journal of Statistics 15(1):1034–1084, URL http://dx.doi.org/10.1214/21-EJS1808.

- Fissler and Holzmann (2022) Fissler T, Holzmann H (2022) Measurability of functionals and of ideal point forecasts. Preprint URL https://doi.org/10.48550/arXiv.2203.08635.

- Fissler et al. (2021b) Fissler T, Merz M, Wüthrich MV (2021b) Deep quantile and deep composite model regression. arXiv preprint arXiv:2112.03075 .

- Fissler and Ziegel (2016) Fissler T, Ziegel JF (2016) Higher order elicitability and Osband’s principle. Annals of Statistics 44(4):1680–1707, URL https://doi.org/10.1214/16-AOS1439.

- Fissler and Ziegel (2019) Fissler T, Ziegel JF (2019) Order-sensitivity and equivariance of scoring functions. Electronic Journal of Statistics 13(1):1166–1211, URL https://doi.org/10.1214/19-EJS1552.

- Fissler and Ziegel (2021) Fissler T, Ziegel JF (2021) On the elicitability of range value at risk. Statistics & Risk Modeling 38(1-2):25–46, URL https://doi.org/10.1515/strm-2020-0037.

- Fort et al. (2021) Fort JC, Klein T, Lagnoux A (2021) Global sensitivity analysis and wasserstein spaces. SIAM/ASA Journal on Uncertainty Quantification 9(2):880–921, URL https://doi.org/10.1137/20M1354957.

- Fort et al. (2016) Fort JC, Klein T, Rachdi N (2016) New sensitivity analysis subordinated to a contrast. Communications in Statistics-Theory and Methods 45(15):4349–4364, URL https://doi.org/10.1080/03610926.2014.901369.

- Frankel and Kamenica (2019) Frankel A, Kamenica E (2019) Quantifying information and uncertainty. American Economic Review 109(10):3650–3680, URL https://doi.org/10.1257/aer.20181897.

- Gamboa et al. (2018) Gamboa F, Klein T, Lagnoux A (2018) Sensitivity analysis based on Cramér–von Mises distance. SIAM/ASA Journal on Uncertainty Quantification 6(2):522–548, URL https://doi.org/10.1137/15M1025621.

- Gerber (1974) Gerber HU (1974) On additive premium calculation principles. ASTIN Bulletin: The Journal of the IAA 7(3):215–222, URL https://doi.org/10.1017/S0515036100006061.

- Gneiting (2011) Gneiting T (2011) Making and Evaluating Point Forecasts. Journal of the American Statistical Association 106(494):746–762, URL https://www.jstor.org/stable/41416407.

- Gneiting (2017) Gneiting T (2017) When is the mode functional the bayes classifier? Stat 6(1):204–206, URL https://doi.org/10.1002/sta4.148.

- Gneiting and Raftery (2007) Gneiting T, Raftery A (2007) Strictly Proper Scoring Rules, Prediction, and Estimation. Journal of the American Statistical Association 102(477):359–378, URL https://doi.org/10.1198/016214506000001437.

- Gneiting and Resin (2021) Gneiting T, Resin J (2021) Regression diagnostics meets forecast evaluation: Conditional calibration, reliability diagrams, and coefficient of determination. Preprint URL https://arxiv.org/abs/2108.03210.

- Griessenberger et al. (2022) Griessenberger F, Junker RR, Trutschnig W (2022) On a multivariate copula-based dependence measure and its estimation. Electronic Journal of Statistics 16(1):2206–2251, URL https://doi.org/10.1214/22-EJS2005.

- Heinrich (2014) Heinrich C (2014) The mode functional is not elicitable. Biometrika 101(1):245–251, URL https://doi.org/10.1093/biomet/ast048.

- Heinrich-Mertsching and Fissler (2021) Heinrich-Mertsching C, Fissler T (2021) Is the mode elicitable relative to unimodal distributions? Biometrika URL https://doi.org/10.1093/biomet/asab065.

- Holzmann and Eulert (2014) Holzmann H, Eulert M (2014) The role of the information set for forecasting – with applications to risk management. Annals of Applied Statistics 8(1):79–83, URL https://doi.org/10.1214/13-AOAS709.

- Ishigami and Homma (1990) Ishigami T, Homma T (1990) An importance quantification technique in uncertainty analysis for computer models. [1990] Proceedings. First International Symposium on Uncertainty Modeling and Analysis, 398–403 (IEEE), URL https://doi.org/10.1109/ISUMA.1990.151285.

- Krüger and Ziegel (2021) Krüger F, Ziegel JF (2021) Generic conditions for forecast dominance. Journal of Business & Economic Statistics 39(4):972–983, URL http://dx.doi.org/10.1080/07350015.2020.1741376.

- Lambert et al. (2008) Lambert N, Pennock DM, Shoham Y (2008) Eliciting properties of probability distributions. EC ’08: ACM Conference on Electronic Commerce, Chicago II, USA, 129–138 (New York, USA: Association for Computing Machinery), URL https://doi.org/10.1145/1386790.1386813.

- Marrel et al. (2009) Marrel A, Iooss B, Laurent B, Roustant O (2009) Calculations of sobol indices for the gaussian process metamodel. Reliability Engineering & System Safety 94(3):742–751, URL https://doi.org/10.1016/j.ress.2008.07.008.

- Maume-Deschamps and Niang (2018) Maume-Deschamps V, Niang I (2018) Estimation of quantile oriented sensitivity indices. Statistics & Probability Letters 134:122–127, URL https://doi.org/10.1016/j.spl.2017.10.019.

- McNeil et al. (2015) McNeil AJ, Frey R, Embrechts P (2015) Quantitative Risk Management: Concepts, Techniques and Tools. Princeton Series in Finance (Princeton University Press), revised edition edition.

- Murphy (1973) Murphy AH (1973) Hedging and skill scores for probability forecasts. Journal of Applied Meteorology 12(1):215–223, URL https://doi.org/10.1175/1520-0450(1973)012<0215:HASSFP>2.0.CO;2.

- Murphy and Daan (1985) Murphy AH, Daan H (1985) Forecast Evaluation. Murphy AH, Katz RW, eds., Probability, Statistics and Decision Making in the Atmospheric Sciences, 379–437 (Westview Press, Boulder, Colorado).

- Nolde and Ziegel (2017) Nolde N, Ziegel JF (2017) Elicitability and backtesting: Perspectives for banking regulation. Annals of Applied Statistics 11(4):1833–1874, URL https://doi.org/10.1214/17-AOAS1041.

- Osband (1985) Osband KH (1985) Providing Incentives for Better Cost Forecasting. Ph.D. thesis, University of California, Berkeley, URL https://doi.org/10.5281/zenodo.4355667.

- Patton (2011) Patton AJ (2011) Data-based ranking of realised volatility estimators. Journal of Econometrics 161(2):284–303, URL https://doi.org/10.1016/j.jeconom.2010.12.010.

- Pesenti (2021) Pesenti SM (2021) Reverse sensitivity analysis for risk modelling. Preprint URL https://arxiv.org/abs/2107.01065.

- Pesenti et al. (2019) Pesenti SM, Millossovich P, Tsanakas A (2019) Reverse sensitivity testing: What does it take to break the model? European Journal of Operational Research 274(2):654–670, URL https://doi.org/10.1016/j.ejor.2018.10.003.

- Pesenti et al. (2021) Pesenti SM, Millossovich P, Tsanakas A (2021) Cascade sensitivity measures. Risk Analysis 31(12):2392–2414, URL https://doi.org/10.1111/risa.13758.

- Pianosi and Wagener (2015) Pianosi F, Wagener T (2015) A simple and efficient method for global sensitivity analysis based on cumulative distribution functions. Environmental Modelling & Software 67:1–11, URL https://doi.org/10.1016/j.envsoft.2015.01.004.

- Plischke and Borgonovo (2019) Plischke E, Borgonovo E (2019) Copula theory and probabilistic sensitivity analysis: Is there a connection? European Journal of Operational Research 277(3):1046–1059.

- Pohle (2020) Pohle MO (2020) The Murphy decomposition and the calibration-resolution principle: A new perspective on forecast evaluation. Preprint URL https://arxiv.org/abs/2005.01835.

- Razavi et al. (2021) Razavi S, Jakeman A, Saltelli A, Prieur C, Iooss B, Borgonovo E, Plischke E, Piano SL, Iwanaga T, Becker W, et al. (2021) The future of sensitivity analysis: An essential discipline for systems modeling and policy support. Environmental Modelling & Software 137:104954, URL https://doi.org/10.1016/j.envsoft.2020.104954.

- Rényi (1959) Rényi A (1959) On measures of dependence. Acta Mathematica Academiae Scientiarum Hungaricae (10):441–451.

- Saltelli et al. (2008) Saltelli A, Ratto M, Andres T, Campolongo F, Cariboni J, Gatelli D, Saisana M, Tarantola S (2008) Global sensitivity analysis: the primer (John Wiley & Sons).

- Saltelli and Tarantola (2002) Saltelli A, Tarantola S (2002) On the relative importance of input factors in mathematical models: safety assessment for nuclear waste disposal. Journal of the American Statistical Association 97(459):702–709, URL https://doi.org/10.1198/016214502388618447.

- Straub et al. (2021) Straub D, Ehre M, Papaioannou I (2021) Decision-theoretic reliability sensitivity. Reliability Engineering & System Safety 108215, URL https://doi.org/10.1016/j.ress.2021.108215.

- Thorarinsdottir et al. (2013) Thorarinsdottir TL, Gneiting T, Gissibl N (2013) Using proper divergence functions to evaluate climate models. SIAM/ASA Journal on Uncertainty Quantification 1(1):522–534, URL https://doi.org/10.1137/130907550.

- Tsanakas and Millossovich (2016) Tsanakas A, Millossovich P (2016) Sensitivity analysis using risk measures. Risk Analysis 36(1):30–48, URL https://doi.org/10.1111/risa.12434.

- Wang and Wei (2020) Wang R, Wei Y (2020) Risk functionals with convex level sets. Mathematical Finance 30(4):1337–1367, URL https://doi.org/10.1111/mafi.12270.

- Weber (2006) Weber S (2006) Distribution-Invariant Risk Measures, Information, and Dynamic Consistency. Mathematical Finance 16(2):419–441, URL https://doi.org/10.1111/j.1467-9965.2006.00277.x.

- Wooldridge (2013) Wooldridge JM (2013) Introductory Econometrics: A Modern Approach (South-Western, Cengage Learning), 5th edition.