[ style=section, level=2, indent=0pt, beforeskip=-3.25ex plus -1ex minus -.2ex, afterskip=1.5ex plus .2ex, tocstyle=subsection, tocindent=1.5em, tocnumwidth=2.3em, font=\usekomafontsubsection, counterwithin=section ]theorysubsection \DeclareNewSectionCommand[ style=section, level=2, indent=0pt, beforeskip=-3.25ex plus -1ex minus -.2ex, afterskip=1.5ex plus .2ex, tocstyle=subsection, tocindent=1.5em, tocnumwidth=2.3em, font=\usekomafontsubsection, counterwithin=section ]insightsubsection \DeclareNewSectionCommand[ style=section, level=2, indent=0pt, beforeskip=-3.25ex plus -1ex minus -.2ex, afterskip=1.5ex plus .2ex, tocstyle=subsection, tocindent=1.5em, tocnumwidth=2.3em, font=\usekomafontsubsection, counterwithin=section ]examplesubsection

Model Comparison and Calibration Assessment

Working Group “Data Science”

Swiss Association of Actuaries SAV

Version of March 8, 2024)

Abstract

One of the main tasks of actuaries and data scientists is to build good predictive models for certain phenomena such as the claim size or the number of claims in insurance.

These models ideally exploit given feature information to enhance the accuracy of prediction.

This user guide revisits and clarifies statistical techniques to assess the calibration or adequacy of a model on the one hand, and to compare and rank different models on the other hand.

In doing so, it emphasises the importance of specifying the prediction target functional at hand a priori (e.g. the mean or a quantile) and of choosing the scoring function in model comparison in line with this target functional.

Guidance for the practical choice of the scoring function is provided.

Striving to bridge the gap between science and daily practice in application, it focuses mainly on the pedagogical presentation of existing results and of best practice.

The results are accompanied and illustrated by two real data case studies on workers’ compensation and customer churn.

keywords: actuarial science, backtesting, calibration, classification, consistency, data science, identification functions, machine learning, model comparison, predictive performance, propriety, scoring functions, scoring rules, supervised learning

1 Introduction

This study has been carried out for the working group “Data Science” of the Swiss Association of Actuaries SAV, see

https://www.actuarialdatascience.org

The purpose of this user guide is to provide an overview of point forecast evaluation, theory and examples hand in hand. For better readability and distinction of theory and example sections, we mark them as follows:

dispositionTheory \faInfoCircle \usekomafontdispositionPracticalities \faFlask \usekomafontdispositionExample

Nowadays, validating and comparing the predictive performance of statistical models has become ubiquitous by means like cross-validation, testing on a hold-out data set and machine learning (ML) competitions. In the light of these developments, this article strives to provide the methodology to answer two key questions:

In finance, these two tasks are customarily subsumed under the umbrella term backtesting. Intuitively, calibration means that the predictions produced by a model are in line with the observations of the response variable. It is a generalisation of unbiasedness, sometimes referred to as balance property in actuarial science. Calibration can be checked by means of identification functions, also known as moment functions. For the latter quest, predictive accuracy is commonly assessed in terms of loss or scoring functions, sometimes also called metrics. Roughly speaking, they measure the distance between a prediction and the observation of the quantity of interest. Crucially, for both tasks, the evaluation methodology should be “designed such that truth telling […] is an optimal strategy in expectation” [29]. But what does truth amount to in this setting? In the most general and informative form, it is the true (conditional) probability distribution of the response (given the information contained in the features), called probabilistic prediction [27]. Alternatively, when the model outputs point predictions, it is a pre-specified summary measure, a property, or a functional of the true (conditional) probability distribution of the response, such as the (conditional) mean or a (conditional) quantile. For the situation of point predictions, the identification and scoring functions used must be chosen to fit to the target functional, i.e. they need to be strictly consistent. Interestingly, strictly consistent scoring functions then simultaneously assess calibration and discrimination ability of the model predictions.

In this user guide, we summarise the theoretical background and give illustrative examples. As a shortcut, just follow Figure 1 and Theory Short Form.

Theory Short Form

Outline

The present user guide starts with a short overview of supervised learning in Section 2 at the end of which a data set for a regression modelling example is introduced. Section 3 continues with the core of supervised learning: loss functions and the statistical risk. It introduces the concept of overfitting and the necessity of a train–test split for model comparison. In the example part, several models are trained, among them generalised linear models and gradient boosted trees. How to assess model calibration is then presented in Section 4. It defines identification functions and different notions of calibration which are then assessed and visualised in detail. The following Section 5 lays out the theory of scoring functions, which is an alternative name for loss functions.111Conventions in the literature are different and sometimes loss functions are required to be non-negative. We do not impose this condition. Our convention is to speak of loss functions in the context of learning and of scoring functions in the context of evaluation. A central property of scoring functions is (strict) consistency, and general forms of consistent scoring functions for the most common target functionals are provided. Furthermore, it is shown that scoring functions simultaneously assess calibration and potential discriminative power of a given model. After practical considerations on how to choose a particular scoring function, the example part illustrates model comparison and concludes which model performs best on the given data set. Section 6 sheds light on the peculiarities of probabilistic binary classification and demonstrates them on a classification data set. Finally, the user guide concludes with Section 7.

Configuration

All R code was run on the following system.

-

•

Processor: Intel(R) Core(TM) i7-8650U CPU @ 1.90GHz, 2112 Mhz, 4 Core(s)

-

•

R version: 4.0.4

The complete R code can be found at https://github.com/JSchelldorfer/ActuarialDataScience. Note: Since version 3.6.0, R uses a different random number generator. Results are not reproducible under older versions.

2 Supervised Learning

[nonumber=false, tocentry=Theory, reference=Theory]Theory

According to Wikipedia222https://en.wikipedia.org/wiki/Supervised_learning as of 06.01.2021. “supervised learning is the machine learning task of learning a function that maps an input to an output based on example input-output pairs.” [67] Using standard notation, we call the input features, also called covariates, regressors or explanatory variables, , taking values in some possibly high dimensional feature space such as , and the output , which is the response or target variable, and which takes values in some space , which we assume to be a subset of . Observations of input-output pairs are denoted by , . The presence of the observable outputs is the reason for the term supervised. In statistical learning theory, we consider both and to be random variables with joint probability distribution . To ease the exposition, we dispense with a discussion of a time series framework and solely focus on cross-sectional data. That is, we assume that each sample of data is a random sample, meaning the data at hand , , is independent and identically distributed (i.i.d.).333It is also possible to allow for serial dependence and some non-stationarity in the data. However, this would dilute the main message of the paper and distract from our main goals.

The first key point we would like to stress is: It is in general illusive to hope that the input features can fully explain the behaviour of in that is a deterministic function of the features, . There is a remaining degree of uncertainty, which can be expressed in terms of the conditional distribution of , given , denoted by . The most informative prediction approach is probabilistic, aiming at specifying the full conditional distribution . Often, one is content with point predictions,444In this tutorial, we will use the terms “prediction” and “forecast” interchangeably, possibly ignoring the temporal connotation of the latter. modelling only a certain property or summary measure of the conditional distribution. Strictly speaking, such a summary measure is a statistical functional, mapping a distribution to a real number, such as the mean or a quantile. Then the ideal point prediction takes the form , which we will denote by for convenience. If is the mean functional, we obtain , or if is the -quantile, we get . It is also possible to combine different functionals to a vector, e.g., when interested in two quantiles at different levels or in the mean and variance of given . For the sake of simplicity, we will mostly stick to one dimensional functionals in this article, though.

The ideal goal of supervised learning is then to find a model which approximates the actual underlying regression function . Since the search space of all (measurable) functions is clearly not tractable, one needs to come up with a suitable model class of such functions. For our purpose, we will require that contains models of different complexity (also called model capacity) and always contains the trivial model, i.e. constant model (also called null model or intercept model). While the model complexity can theoretically be defined by the Vapnik–Chervonenkis dimension or the Rademacher complexity, cf. [70, 52, 3] and references therein, we give some vivid examples:

-

•

Most classically, for the class of linear models, complexity can be measured by the number of estimable parameters, also known as degrees of freedom (df). This amounts to including and excluding features as well as adding interaction terms and quadratic and higher order polynomial terms such as splines.

-

•

For penalised linear models (with fixed input features), such as ridge or lasso regression, the penalty parameter is a—reciprocal—measure of complexity.

-

•

Non-parametric approaches often impose smoothness or shape constraints on the models, with the most prominent case of isotonic models.555There is some (partial) order on and implies that . Then the degree of smoothness, for example, can be taken as a measure of complexity.

-

•

For decision trees, it can be the number of leaves or the maximal tree depth.

-

•

For ensemble models like gradient boosted trees, it can be a combination of the single tree complexity and the number of fitted trees.

-

•

For neural nets, where the model class is implicitly given by the architecture of the net, it can be the combination of the number of weights, early stopping and weight penalisation.

Using a training data sample , , one then fits (or trains or estimates) a model . The fitted model commonly has two purposes: On the one hand, it should be interpretable, describing the connection of and in terms of (which is often easier if is small, e.g., for linear models). On the other hand, should produce predictions which should be as accurate as possible. That is, when using a new feature point (not necessarily contained in the training sample), should be close to the ideal .

[nonumber=false, tocentry=Example, reference=Example]Example: Mean Regression for Workers’ Compensation.

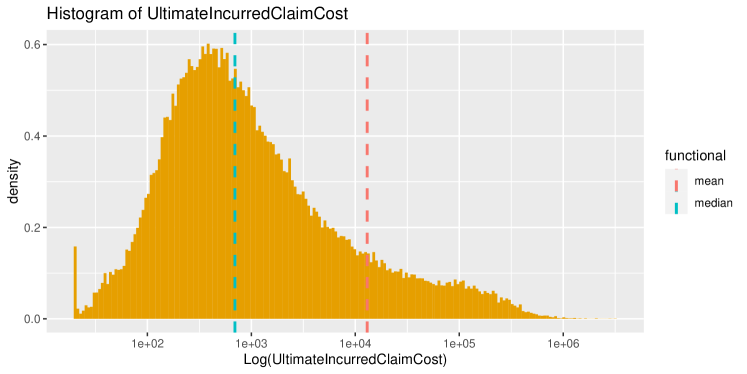

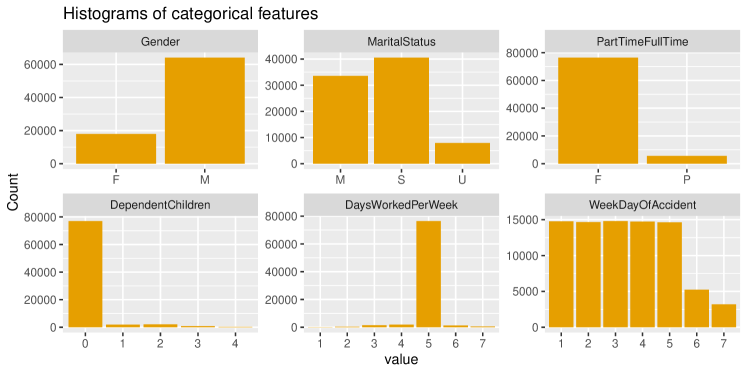

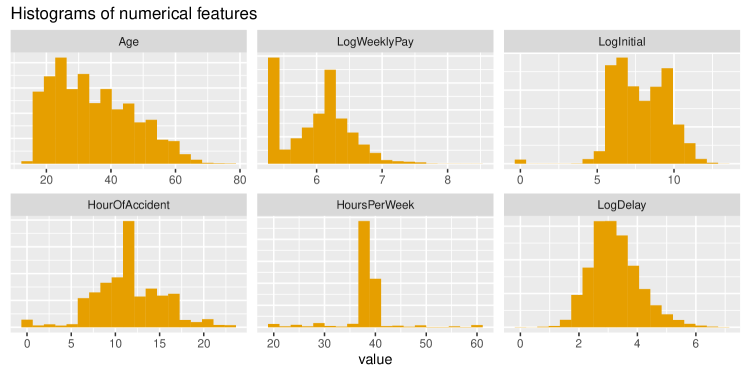

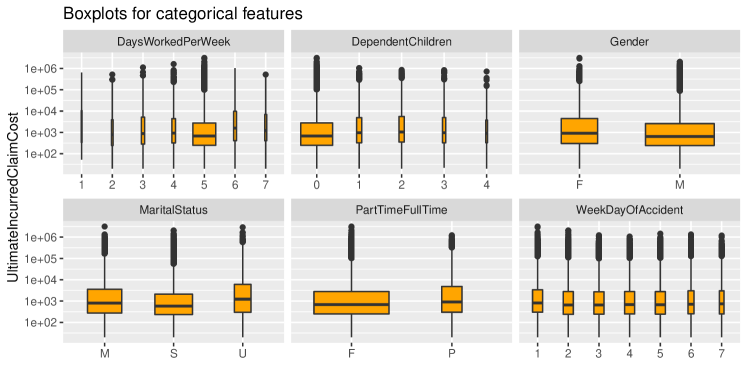

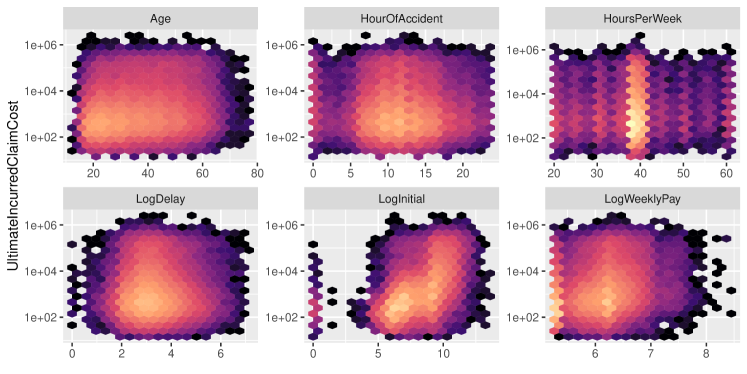

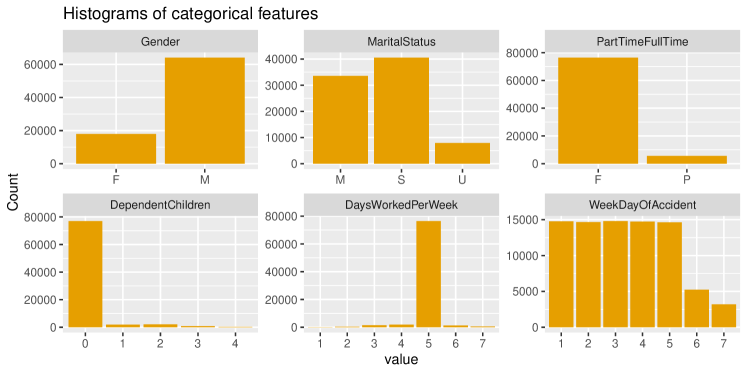

Throughout this user guide, we illustrate the theoretical results on the Workers’ Compensation data set,666https://www.openml.org/d/42876 which consists of rows, each representing a single insurance claim caused by injury or death from accidents or occupational disease while a worker is on the job. Due to possible data inconsistencies, we filter out all rows with and . This leaves us with rows, see Listing 1.

The response variable is with explanatory features represented by the remaining columns listed in x_vars. As a summary measure , we choose to model the conditional expectation of given . It is the most common target functional in machine learning. In actuarial science, it informs about adequate pricing of policies. Moreover, the tower property of the conditional expectation777That is, . facilitates to compute an estimate of the unconditional expectation of as for claims (or policies) , i.e. the expected value for a whole portfolio of claims (or policies).

Listing 2 shows the first ten rows of the data.

In Figure 2, the empirical, marginal distribution of is visualised. As the large difference between mean and median indicates, the distribution seems to be very asymmetric, right-skewed, even heavy tailed. (Mind the logarithmic scale of the -axis.) For further exploratory data analysis, we refer to Subsection A.1.

3 Statistical Learning Theory

[nonumber=false, tocentry=Theory, reference=Theory]Theory

To provide a complete picture, we shortly outline the basics of statistical learning theory. This will explain the difference between model estimation on the one hand and model validation and selection on the other hand. We start by introducing a loss function , , that measures the accuracy of predictions from a model for observations of the response —with the convention the smaller the better. The leading example is the squared error, . The loss function should be chosen in line with the directive in that it should be (strictly) consistent for ; see Definition 4 in Section 5. For a model and a loss , the statistical risk, also known as generalisation error, is defined as

| (1) |

where the expectation is taken with respect to the joint distribution of and . The goal of statistical learning is to find the ideal model minimising the corresponding statistical risk (1). Supposed a solution exists, this amounts to the Bayes rule,

The tower property of the conditional expectation yields the representation

If there is some model minimising the conditional statistical risk

| (2) |

for almost all ,888That means it holds for all in some subset such that with probability one. then clearly minimises the unconditional risk and .

In the absence of knowing the distribution of on the population level, we cannot calculate the statistical risk , and therefore generally also fail to determine the ideal model . We need to resort to an approximation of on a sample level. Employing a random sample , we can easily compute the empirical risk

The so called M-estimator999Where the “M” is for minimisation and is due to Huber [41]; see also [42] for a good textbook. is defined as the empirical risk minimiser

| (3) |

over a training sample . Since estimating is based on the empirical risk, which is only an approximation of the statistical risk, it suffers from sampling uncertainty and is thus prone to estimation error. In particular, inherently depends on the particular training sample at hand. If another training sample had been chosen, then generally . This sampling variability leads us directly to the keyword of overfitting which we will formally introduce in Definition 1. A common practice to reduce this variability is to add an additional penalty term, , such that (3) turns into

Often, represents model complexity, see Section 2. For example, it can be a norm of the underlying parameter vector , employed in ridge or lasso regression. The penalisation strength is a tuning parameter, or hyperparameter. It should asymptotically vanish with increasing sample size, which is necessary to obtain a consistent estimate of the statistical risk and thus of the ideal model . Still, this is only an asymptotic result, and in finite samples, is to be expected.

This fact necessitates a reliable evaluation of the predictive accuracy of , quantifying how well it generalises to unseen data points, . Furthermore, it calls for a meaningful comparison of different estimators of which will be the main subject of Section 5. These estimators could stem from different samples or from different choices of the penalty term . The first possibility that comes to mind to estimate the statistical risk of is to use the same again in the empirical risk, i.e. to use the in-sample performance, in-sample risk, or training loss, . Having used the training sample twice, it is generally a biased performance measure. Since any estimator is tailored to fit the training sample involved in the estimation process,101010For instance, the OLS estimator is constructed as to minimise the in-sample squared error. It approximates the conditional mean perfectly on the training sample in so far as the sum of residuals is 0 by construction. the in-sample risk is usually an overly optimistic performance measure that underestimates the statistical risk of .111111To be precise, the bias is caused by the dependence between the fitted model and the data used to estimate the risk. For squared error and zero-one loss, it can be shown that, in expectation, this bias stems indeed from and is called expected optimism, see Chapter 7.4 in [35] or Theorem 2.2 in [48]. Roughly speaking, the amount of “optimism” of the in-sample risk amounts to too high a sensitivity of the training of the model w.r.t. changes of the response values in the training sample. This is connected to the notion of overfitting.

As the term overfitting is often used heuristically, we make it more precise by defining overfitting in a relative sense, cf. [54]:

Definition 1

Model overfits (w.r.t. model complexity given by ) the training data if there exists another model with such that , but .

Clearly, this definition of overfitting is only relevant on model classes containing models of different complexity. The left side of Figure 3, denoted by “classical regime”, provides an illustration of over- and underfitting with the typical U-shape of the statistical risk and a monotonically decreasing in-sample risk.

Intuitively, overfitting appears as soon as a model starts to learn the training set by heart, indicated by point . The behaviour of this regime is often explained by the bias-variance trade-off [26, 35]: At low complexity, the model is not able to capture the data structure, leading to a high bias. With larger complexity, the bias is reduced, but the variance, i.e. the estimation error, grows.

The interpolating regime on the right side of Figure 3 is an area of recent research, initiated by investigating the success of deep neural nets—models with an enormously huge amount of parameters—[59, 79]. The point where a model starts to interpolate the data, i.e. for all training data , has a very high statistical risk.121212Here, we implicitly assume that the target functional satisfies for any , where is a point mass in . But as the model gets even more overparametrised, the statistical risk decreases again, while the in-sample risk remains constant (and minimal). Therefore, the terms interpolation and overparameterisation are more appropriate in this regime than the notion of overfitting. The overall shape of the statistical risk has been called “double descent” and has been confirmed for several model classes [5]. Analytical results are available for linear models [6, 36, 2]. Whether there is a point in the interpolating regime with a smaller statistical risk than the local minimum in the classical regime denoted by depends on the model class as well as the distribution of the data, see [12] for a review.

Another possible way for dealing with the bias of the in-sample risk besides making use of an independent test data set is to use alternative in-sample measures like Akaike’s information criterion (AIC) or the Bayesian information criterion (BIC), see [35] and references therein. They measure the in-sample risk including a penalty term accounting for model complexity.

The following decomposition of the statistical risk of a model 131313Due to Daniel Hsu’s slides https://www.cs.columbia.edu/~djhsu/tripodsbootcamp/overview.slides.pdf. illustrates the constituent parts of the learning procedure:

| inherent unpredictability | (4) | |||||

| approximation error | ||||||

| estimation error I | ||||||

| optimisation error | ||||||

| estimation error II |

Note that while the approximation and optimisation errors are always non-negative, the two estimation errors can have any sign.141414Figure 7.2 in [35] illustrates a similar decomposition. Equation (17) in Section 5 provides an alternative decomposition of statistical risk (there named expected score) with an emphasis on evaluation rather than learning.

[nonumber=false, tocentry=Practicalities, reference=Practicalities]Practicalities

3.2.1 Train–Validation–Test split

In actuarial practice and machine learning, one often enjoys the situation of having a large amount of data,151515Interestingly, the amount of data available to actuaries varies a lot depending on insurance sector and country, from (almost) no data for newly invented insurance coverages to usually very good amounts of data for motor insurance. both for fitting and for model evaluation and comparison. Then, a crucial rule is to divide the data set into mutually exclusive subsets. Terminology and usage patterns for those data samples vary in the literature. We give the following definition, cf. [35, Chapter 7.2], [78, Chapter 7.2.3], [65]:

-

•

Training set for model fitting, typically the largest set.

-

•

Validation set for model comparison and model selection.

Typically, this set is used to tune a model of a given model class while building (fitting) models on the training set. Examples are variable selection and specification of terms for linear models, finding optimal architecture and early stopping for neural nets, hyperparameter tuning of boosted trees. This way, the validation set is heavily used and therefore does not provide an unbiased performance estimate anymore. The result is a “final” model for the given model class that is often refit on the joint training and validation sets. -

•

Test set for assessment and comparison of final models.

Once the model building phase is finished, this set is used to calculate an unbiased estimate of the statistical risk. It may be used to pick the best one of the (few) final models. -

•

Application set.

This is the data the model is used for in production. It consists of feature variables only. If the observations of the response become known after a certain time delay, it can serve to monitor the performance of the model.

In practise, the usage of the terms “validation set” and “test set” is often not clearly distinguished.

A golden rule is: Never ever look at the test set while still training models. Any data leakage from the test to the training set might invalidate the results, i.e. it will likely render evaluation results on the test set too optimistic. Also be aware that the more you use the test or validation data set, the less reliable your results become.161616Assume 1000 random forests, each trained with a different random seed. Now, we evaluate on the validation set which one performs best and choose it as our final tuned model. We will pick the one that, by chance, optimised the validation set. If we finally look at the performance of the picked model on an independent test set, we might likely see a worse performance than on the validation set. This can be seen as an instance of the survivorship bias. For the validation set, this risk can be mitigated to some degree by methods like cross-validation, see below.

Data points of a hold-out set, i.e. validation and test set, should be independently drawn from the same distribution as the training set, ensuring that the evaluation is representative on the one hand and preventing overly optimistic results on the other hand.171717Beware of distributions of response or feature variables that change over time. Take the trend to improved motorway safety in Switzerland as an example. A model for insurance claims frequency fitted in the year 2000 and evaluated on test data from 2015–2020 will show that it is not a good fit for today’s situation, but might have been a good model at its time. Below, we review and discuss some examples of data with dependencies.

3.2.2 Data with dependencies

Real life data sets often contain dependent rows. Taking the dependence structure into account is essential to create independent data sets, cf. [66].

-

•

Data rows with the same policy number or customer ID are likely correlated. In this case, the same number or ID should only go in either training or test set, but not in both. This is called grouped sampling and is a form of a blocking strategy [66]. In practice, this can be a hidden dependency, e.g., if the ID is unknown.

-

•

If the data at hand is a time series [43], the usual assumption is that the dependence decreases with larger time difference. Therefore, choosing a split time such that all training samples are older than the test set is a good strategy, called out-of-time [71] or forward-validation scheme [69]. The specific validation scheme depends on different aspects, for instance how the models are to be applied. For more details, we refer to the overview and references of [69].

Failing to account for important dependencies is information leakage between test and train set and will often lead to too optimistic results.

3.2.3 Data splitting ensuring identical distributions

The second aspect next to independence of the split data sets is to ensure that they are identically distributed. Differently distributed features or response variables will typically lead to different estimates of the statistical risk. This time, however, the direction is unclear: the result on the test set can be clearly better or worse than on the training set. Ensuring identically distributed sets makes results comparable.

-

•

The data at hand might be ordered in some way. A simple random shuffled split then helps to create similarly distributed data sets. This procedure, however, does not mitigate possible dependence in the data.

-

•

To ensure identically distributed response variables, one can employ stratified sampling. It can be combined with the previous point and is then called stratified random sampling. Stratification is often applied in classification problems, as do we in Subsubsection 3.2.4. Interestingly, stratification may induce some degree of dependence between the test and the training set, underpinning that there is no silver bullet in statistics.

3.2.4 Cross-Validation

A statistically more robust and less wasteful alternative to the above strategy of using a validation set to evaluate and compare models is -fold cross-validation (CV) [35, 1]. There, the full data set available for training and validation is first split into partitions or folds, where is often a value between five and ten. For each fold, a model is trained on the remaining folds and a validation score is calculated from the hold-out fold. The validation scores are then summarised to an average CV score that can be supplemented by its standard error or a confidence interval.181818Note, however, that CV in fact estimates the statistical risk for different models, each trained on a different fold permutation, meaning on different but dependent training sets. Thus, the averaged loss value over all folds may be seen as measuring the fit algorithm rather than as estimate of the statistical risk of a single—fitted—model, see [4]. After all decisions are made, the final model is retrained on all folds, i.e., on the full data set (besides a possible test data set). In practice, different variants to standard -fold CV exist, e.g., repeated or nested CV, see references above.

[nonumber=false, tocentry=Example, reference=Example]Example: Mean Regression for Workers’ Compensation.

Before we start modelling, we need to make a train–test split. It could be the case that the same person has several claims represented by different rows in the data. These rows would then likely be correlated. As we do not have that information in our data, we assume no ordering, and we use a random shuffled split which helps to create similarly distributed sets.

For inspection of this point, we list the mean as well as several quantiles of the response variable in Table 1.

| Mean | Quantile | ||||||

|---|---|---|---|---|---|---|---|

| Set | |||||||

| train | |||||||

| test | |||||||

For large quantiles, we observe a certain discrepancy, but otherwise this looks acceptable.

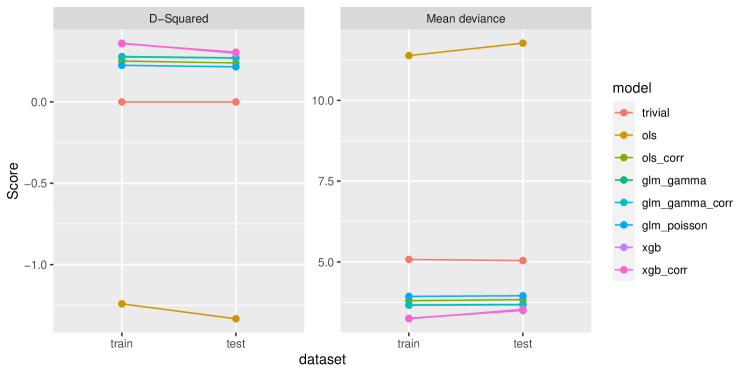

Later on, we will evaluate and compare the models using the Gamma deviance, see Table 8. Therefore, we mainly focus on models that minimise this loss function. We train four different models:

-

•

Trivial model: It will always predict the mean UltimateIncurredClaimCost of the training set, that is, .

-

•

Ordinary least squares (OLS) on : As the response is very skewed, but always positive, we fit an OLS model on the log transformed response.

form <- reformulate(x_vars, y_var)fit_ols_log <- lm(update(form, log(UltimateIncurredClaimCost) ~ .),data = train)corr_fact <- mean(y_train) / mean(exp(fitted(fit_ols_log)))Note that the backtransformation for predicting on the untransformed response, , introduces a bias. We mitigate this by a multiplicative correction factor corr_fact_ols = 6.644697; see listing above.

-

•

Gamma generalised linear model (GLM) with log link: Note that, while the log link gives us positive predictions, it is not the canonical link of the Gamma GLM, and therefore introduces a slight bias (see discussion around Equation (9) for this bias and the balance property). As for the OLS in log-space, we account for that with the multiplicative correction factor corr_fact_glm = 1.11445, which is much smaller than the factor for the OLS.

library(glm2)# glm2 is more stable.fit_glm_gamma <- glm2(reformulate(x_vars, y_var), data = train,family = Gamma(link = "log"))glm_gamma_predict <- function(X) {predict(fit_glm_gamma, X, type = "response")}corr_fact_glm <- mean(y_train) / mean(glm_gamma_predict(train))glm_gamma_corr_predict <- function(X){corr_fact_glm * predict(fit_glm_gamma, X, type = "response")} -

•

Poisson GLM: We keep the log link, but now use a Poisson distribution because this gives us a GLM with canonical link with good calibration properties. For instance, we do not need a correction factor.

- •

Instead of a multiplicative correction factor, we could have corrected the models by adding a constant. An additive constant, however, has the disadvantage that it could render some predictions negative. A multiplicative correction is better suited for models with a log link and models fit on the log transformed response as it is just an additive constant in link-space. For the Gamma GLM, it corresponds to adjusting the intercept term.

For this user guide the above five models are sufficient. Further models or improvements could consist in a separate large claim handling, e.g., shown in [22], more feature engineering with larger model pipelines, usage of other model types like neural nets, stacking of models, and many more.

4 Calibration and Identification Functions

[nonumber=false, tocentry=Theory, reference=Theory]Theory

Once a certain model has been fitted, important questions arise: “Is the model fit for its purpose?” Or similarly: “Does the model produce predictions which are in line with the observations?” To answer these questions, the statistical notion of calibration is adequate, which was coined in [13] and further examined in [60].

4.1.1 Conditional calibration and auto-calibration

To introduce a formal definition of calibration, recall that exactly predicting using a feature vector is illusive. In almost all applications, does not describe entirely in the sense that is a deterministic function of . That means given is stochastic, and we summerise this stochasticity in terms of a functional . Our definitions of calibration follow [60, 49].

Definition 2

Given a feature–response pair , the model is conditionally calibrated for the functional if

The model is auto-calibrated for if

In other words, a conditionally calibrated model uses the entire feature information ideally in the prediction task. It describes the oracle regression function . On the other hand, auto-calibration merely says that the information in the model is used ideally to predict in terms of . Clearly, the one-dimensional is less informative than the feature itself. In the extreme case when is a constant model, it contains no information. Being auto-calibrated then simply means that the model equals the unconditional functional value .191919In an insurance context, this would amount to assessing the risk of each client of a car insurance with the very same number, no matter what age, health conditions and experience they have, or if they have ever been involved in a car accident before. For the rich class of identifiable functionals so called moment or identification functions are a tool to assess conditional calibration and auto-calibration.

Definition 3

Let be a class of probability distributions where the functional is defined on. A strict -identification function for is a function in a forecast and an observation such that

| (5) |

If only the implication in (5) holds, then is just called an -identification function for . If admits a strict -identification function, it is identifiable on .

| Functional | Strict Identification Function | Domain of , |

|---|---|---|

| expectation | ||

| -expectile | ||

| median | ||

| -quantile |

Table 2 displays the most common strict identification functions for the mean and median as well as their generalisations, -quantiles for the latter and -expectiles for former.202020We use the indicator function When is the mean functional, (conditional) calibration boils down to (conditional) unbiasedness. Not all functionals are identifiable. Most prominently, the variance, the expected shortfall (an important quantitative risk measure) and the mode (the point with highest density) fail to be identifiable [61, 27, 72, 38]. Strict identification functions are not unique: If is a strict -identification function for , so is , where for all .212121It is actually also possible to show that all strict identification functions must be of this form, see Theorem S.1 in [16].

The connection between calibration and identification functions is as follows: Let be any strict -identification function for and suppose further that contains the conditional distributions for almost all . Then, an application of (5) to these conditional distributions yields that if and only if . This shows that is conditionally calibrated for if and only if

| (6) |

Similarly, if the conditional distributions are in for almost all , then is auto-calibrated for if and only if

| (7) |

Hence, for identifiable functionals with a sufficiently rich class , the tower property of the conditional expectation yields that a conditionally calibrated model is necessarily auto-calibrated.222222This implication does not necessarily hold for non-identifiable functionals. Consider the variance functional, let be standard normal and consider the single feature . Clearly, fully describes . Hence, . The zero model is conditionally calibrated. On the other hand, it provides no information about at all. Consequently, conditioning on it has no effect. Since , the zero model is not auto-calibrated. The reverse implication generally does not hold as can be seen, e.g., with constant models.

4.1.2 Unconditional calibration

Besides conditional calibration and auto-calibration, one can also find the notion of unconditional calibration in the literature on identifiable functionals. If is a strict identification function for , then we say that is unconditionally calibrated for relative to if . Unless is constant, and in stark contrast to conditional calibration and auto-calibration, the notion of unconditional calibration depends on the choice of the identification function used. Moreover, there is no definition solely in terms of and as in Definition 2, unless the model is constant such that the notions of unconditional calibration and auto-calibration coincide. As pointed out in [60], non-constant models that are not conditionally calibrated (or auto-calibrated) can still be unconditionally calibrated. The different notions of calibration are summarised in Table 3. For a more detailed discussion, we refer to [63] and [31].

| Notion | Definition | Check |

|---|---|---|

| conditional calibration | ||

| auto-calibration | ||

| unconditional calibration |

4.1.3 Assessment of calibration

On a sample , unconditional calibration can be empirically tested by checking whether is close to 0. This property justifies the term generalised residuals for the quantities . Next to pure diagnostics, this can also be accompanied with a Wald test in an asymptotic regime. To check conditional calibration, one needs to assess (6) on a sample level. The presence of the conditional expectation in (6) complicates this check. Formally, (6) is equivalent to

| (8) |

Clearly, implementing (8) in practice is usually not feasible.232323An important instance where this is possible is when the features are categorical only such that . Then (6) is equivalent to for all . One needs to choose a finite number of test functions and check whether for all , which can be done with a Wald test. On the other hand, (6) can be assessed visually with appropriate plots. or by checking suitable plots. The choice of the specific test functions and the overall number of test functions can greatly influence the power of the corresponding Wald test. On the population level, the more test functions, the higher the power of the test. But in the practically relevant situation of finite samples, increasing the number of test functions also increases the overall estimation error. Hence, one faces a trade-off. In many situations, one is left with practically testing a broader, i.e. less informative, null hypothesis than (6). So if the Wald test fails to reject the null for all , one cannot be sure if (6) actually holds.242424On top of that, recall the general limitations in statistical tests that it is not possible to establish a null hypothesis by not rejecting it. It might thus be the case that a model is deemed conditionally calibrated even if it does not make ideal use of the information contained in .

The counterpart of (8) for testing auto-calibration is

This time is a univariate function of only, which greatly simplifies the practical implementation. The notion of auto-calibration and its assessment become important when the feature vector is unknown in the evaluation process, but only the model (prediction) along with the response are reported, thus adhering to the weak prequential principle of [14].

Calibration gives us only a very limited possibility to actually compare two models. What if both of them are (auto-)calibrated, but one is more precise in that it incorporates strictly more information than the other one? What about two miscalibrated models?252525This is particularly relevant under model-misspecification. That means that the model class is too narrow such that there is no with . This can arise, e.g., when a monotone model is used to capture a relation with a clear saturation point. This can be observed, for instance, when is a driver’s age and is the probability of having a car accident (), given that age. The effect of age on the accident probability is often bathtub-like: young drivers have more accidents, then become safer drivers over time until the risk of accident increases again. And how should we think of the situation where we have a calibrated, but uninformative model (e.g., making use of only one covariate) versus a very informative one, which is, however, slightly uncalibrated? On the one hand, such comparisons can be made by the expert at hand, say, the actuary, taking into regard the economic relevance of these differences.262626For example, is a more discriminative price policy (say, based on age, health, sex, race etc.) practically implementable, or legal at all? If not, then a less informative but well calibrated model might be more adequate. On the other hand, we shall introduce the notion of consistent scoring functions in Section 5. Assessing conditional calibration and resolution (a measure of the information content used in the model or its discrimination ability) simultaneously, they constitute an adequate tool to overall quantify prediction performance, and to ultimately compare and rank different models.

[nonumber=false, tocentry=Practicalities, reference=Practicalities]Practicalities

4.2.1 Best practice recommendations

-

•

Check for calibration on the training as well as on the test set. On the training set, this yields insights on further modelling improvements, such as including an important omitted feature or excluding a less informative one. (One should, however, mind the overfitting trap when working on the training set.) Once training is finished, assessing calibration on the test set provides a more unbiased view of the calibration and indications whether there is severe bias in the model or whether the model is fit for predictive usage.

-

•

Quantify calibration by making a choice for the test function and report . For practical and diagnostic purposes, we recommend to consider at least as well as all projections to single components of the feature vector (supposed we do not have too many feature components) in addition with the (fitted) model , where the latter explicitly assesses auto-calibration. Moreover, the test functions can be chosen to bin continuous feature variables; see [21] for more details.272727If, e.g., a numerical feature variable income is reported, we can bin it in, say, three categories low, middle, and high, defined through two thresholds, say and . Then we can consider the test functions , , and .

-

•

Assess calibration visually: For a test function , plot the generalised residuals versus for the above choices of test functions . Check whether the average of the generalised residuals is around 0 for all values of the test function. Another possibility is to plot the values of for different , for instance projections to single feature columns; see [21] for more details.

In addition, auto-calibration can be visually assessed by means of a reliability diagram: a graph of the mapping , see [31]. For identifiable , can be estimated by isotonic regression of against as shown in [45]. For an auto-calibrated model, the graph is the diagonal line. Note that due to the estimation error of the graph usually shows some deviation from the diagonal even for an auto-calibrated model. In Figure 10, an example is given for binary classification where is called conditional event probability.

4.2.2 GLMs with canonical link

By construction, a fitted GLM with canonical link fulfils the simplified score equations

| (9) |

on the training set.282828Often in the GLM context, is written as . This means that (8) is satisfied on the training set for all projections to single features. By incorporating a constant feature to account for the intercept, (9) yields the so called balance property [78], , which amounts to unconditional calibration on the training set. Moreover, dummy coding and (9) ensure that this balance property also holds on all labels of categorical features. Note that (8) is not necessarily fulfilled for other choices of on the training set, nor is it clear that (8) holds on the test set in the presence of an estimation error.

[nonumber=false, tocentry=Example, reference=Example]Example: Mean Regression for Workers’ Compensation.

As we are modelling the expectation, we use the identification function , corresponding to the bias or negative residual. This immediately leads to the well-known analysis of residuals.

4.3.1 Unconditional calibration

Checking for unconditional calibration amounts to checking for the average bias . Normalising with the sample size ensures that results on training and test set are directly comparable despite having different sizes.

| -value of -test | ||||

|---|---|---|---|---|

| Model | train | test | ||

| Trivial | ||||

| OLS | ||||

| OLS corr | ||||

| GLM Gamma | ||||

| GLM Gamma corr | ||||

| GLM Poisson | ||||

| XGBoost | ||||

| XGBoost corr | ||||

From the numbers in Table 4, we confirm that the correction factor eliminated the bias over the whole training set, while there is some bias on the test set. The bias on the test set might be due to estimation error on the training set on the one hand or to sampling error of the test set on the other hand. As expected, the Poisson GLM is unbiased on the training set out of the box as a consequence of the balance property for GLMs with canonical link. This, however, no longer holds on the test set, where the corrected XGBoost is the best one apart from the trivial model.

Table 4 additionally provides -values for the two-sided -tests with null hypotheses for the respective models . The advantage of -values lies in a scale free representation of the statistic within the range and the meaning: the larger the better calibrated.

4.3.2 Auto-Calibration

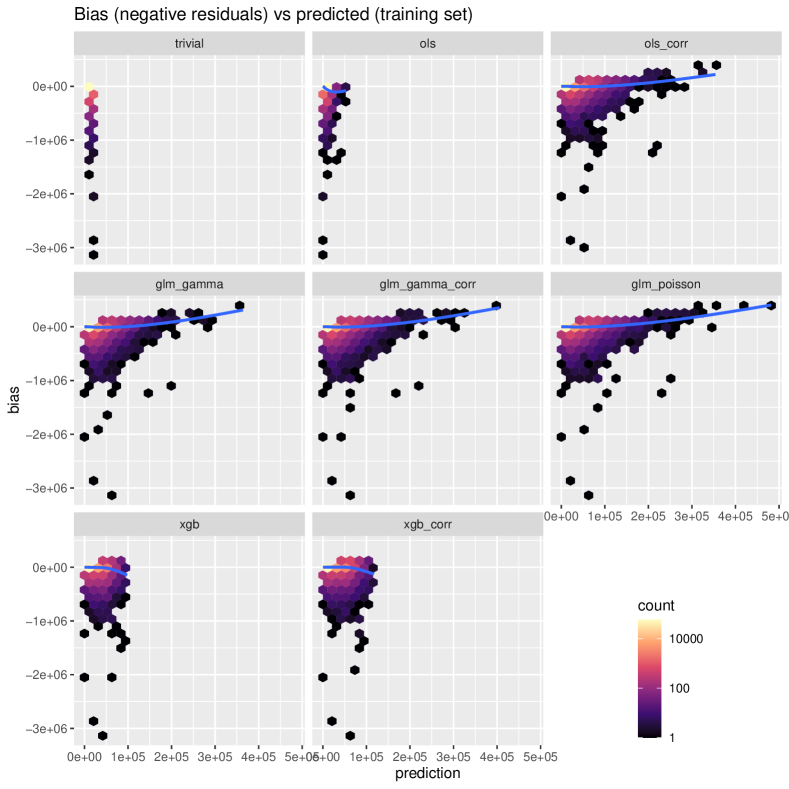

We analyse auto-calibration by visualising bias versus predicted values. On the training set, this is a vertically flipped version of the well-known residual versus fitted plot.

The smoothed lines in Figure 4 are an estimate of the average bias per prediction. We observe large differences in the range of predictions among the models. The three GLMs and the corrected OLS model show a wide range of predicted values with the Poisson GLM having the largest range with the largest predicted value, while the OLS has the smallest range and also the smallest predicted value—neglecting the trivial model. These peculiarities of the OLS are due to the backtransformation after modelling on the log-scale. By comparing the bias term with maximum absolute value, we get another valuable information. The OLS model has the bias term with largest absolute value, on the training set () as well as on the test set (), the corrected Gamma GLM has the smallest such value on the training set (), the corrected XGBoost exhibits the smallest one on the test set (). For the three GLMs and the corrected OLS model, the bias tends to increase with increasing prediction. On the other hand, both XGBoost models show the opposite behaviour. Both phenomena might be due to the fact that there are only a few observations of features leading to large predictions such that the estimation error might be relatively high for such feature constellations.

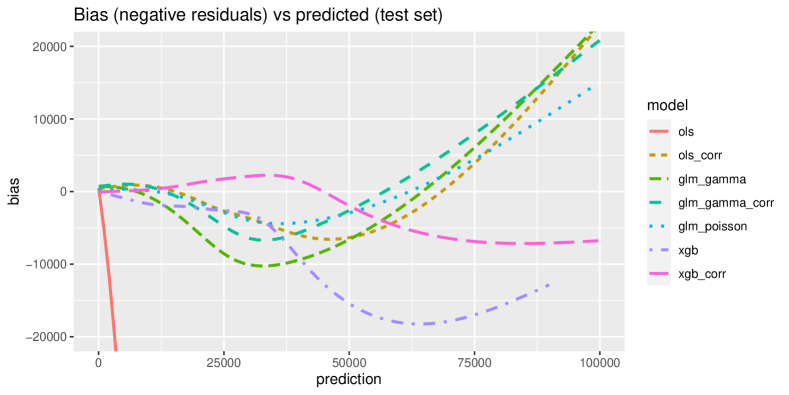

For a better view on the range with most exposure, we draw the smoothed lines only on the restricted range , but this time on the test set, see Figure 5. Here, it becomes visible that the corrected XGBoost model seems to have the best auto-calibration in that range.

| Model | ||

|---|---|---|

| Trivial | ||

| OLS | ||

| OLS corr | ||

| GLM Gamma | ||

| GLM Gamma corr | ||

| GLM Poisson | ||

| XGBoost | ||

| XGBoost corr | ||

The next step is to evaluate different test functions. We list the values of for the test function in Table 5. The results are similar in quality to the ones concerning unconditional calibration. Among the non-trivial models, it is again the calibrated XGBoost model that is best in class on the test set.

4.3.3 Calibration conditional on Gender

We now have a look at the categorical variable Gender. Therefore, we evaluate for the two projection test functions and .

| train | test | |||

|---|---|---|---|---|

| Model | bias F | bias M | bias F | bias M |

| Trivial | ||||

| OLS | ||||

| OLS corr | ||||

| GLM Gamma | ||||

| GLM Gamma corr | ||||

| GLM Poisson | ||||

| XGBoost | ||||

| XGBoost corr | ||||

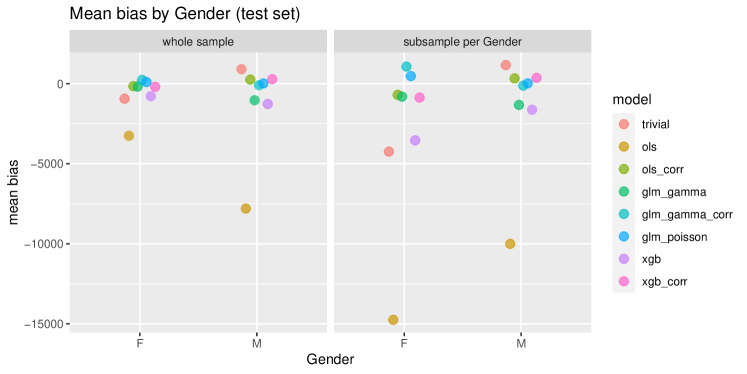

From the bare numbers in Table 6 as well as from the implied bar plot on the left-hand side of Figure 6, we observe again the perfect calibration of the Poisson GLM on the training set due to the balance property (9). This time, this carries over to the test set to a considerable degree. Interestingly, only the Poisson and the corrected Gamma GLM have a positive mean bias for on the test set. These two models seem to have the best out-of-sample calibration conditional on Gender.

A different perspective arises if, instead of evaluating on the whole training or test sample, we evaluate the mean bias on the two projected subsamples with and separately. This corresponds to a different normalisation of the averaging step such that one obtains a mean bias per categorical level—a valuable information about possible discrimination. It can be seen from the right-hand side of Figure 6 that the bias for “F” is larger than for “M”, in particular the opposite of the left plot.

Remarkably, it turns out that the models with correction factor are not only better unconditionally calibrated than the uncorrected ones, but they are also better conditionally calibrated on Gender, in-sample as well as out-of-sample. If we were to place great importance on calibration, we could exclude the three model variants without correction factor, OLS, Gamma GLM and XGBoost, from further analysis as they persistently show worse calibration than their counterparts with calibration factor.

We could go on and investigate interactions with other features, for instance, use .

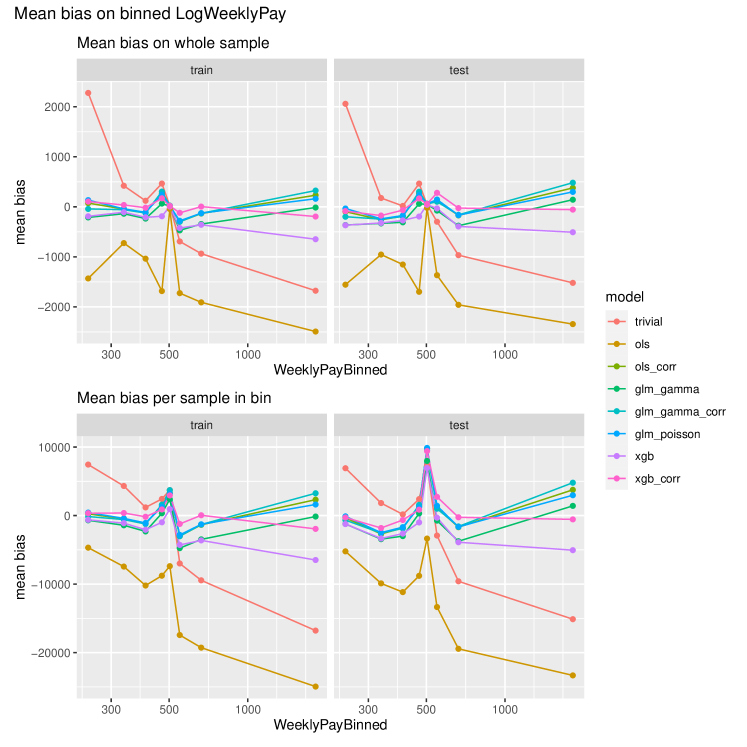

4.3.4 Calibration conditional on LogWeeklyPay

In order to assess the calibration conditional on the continuous variable LogWeeklyPay, we bin it on the whole data set into intervals of evenly distributed quantiles (, , , …, ). Since the lowest value occurs in over of the data rows, we end up with only 8 unique bins. Then we compute

-

•

for the projection test functions for all bins ; and

-

•

the average bias per bin.

To plot the bins on the -axis, we choose the midpoint of each bin. While it is the logarithm of WeeklyPay that enters the models, we display the results in Figure 7 on the original scale. It is obvious that the OLS model without correction is very biased as a consequence of the backtransformation after modelling on the log scale of . We rate the corrected XGBoost model as the most unbiased one, conditional on LogWeeklyPay.

| Model | ||

|---|---|---|

| Trivial | ||

| OLS | ||

| OLS corr | ||

| GLM Gamma | ||

| GLM Gamma corr | ||

| GLM Poisson | ||

| XGBoost | ||

| XGBoost corr | ||

Similar to what we have done for assessing auto-calibration, we also check with the test function . This leads to computing , see Table 7. We see that the Poisson GLM passes this check perfectly on the training set which is a result of the score equation Eq. (9). On the test set, the corrected XGBoost has again the smallest value, which confirms our earlier findings: overall, the corrected XGBoost seems to be the best calibrated model.

5 Model Comparison and Selection with Consistent Scoring Functions

[nonumber=false, tocentry=Theory, reference=Theory]Theory

| Functional | Scoring Function | Formula | Domain |

|---|---|---|---|

| expectation | squared error | ||

| Poisson deviance | |||

| Gamma deviance | |||

| Tweedie deviance | |||

| for | |||

| homogeneous score | |||

| log loss | |||

| -expectile | APQSF | ||

| median | absolute error | ||

| -quantile | pinball loss |

For more details about the Tweedie deviance, see Appendix B. The homogeneous score arises from Eq. (13) with . Note that homogeneous score and Tweedie deviance coincide on the common domains, up to a multiplicative constant. The terms in the second line of the log loss render it non-negative for all , but are zero for , see Section 6. APQSF stands for asymmetric piecewise quadratic scoring function. The pinball loss is also known as asymmetric piecewise linear scoring function.

Suppose we have two models and we would like to compare and rank their accuracy or predictive performance. Here, we are agnostic about how one has come up with these models. They might be the result of a statistically sound parametric estimation procedure, the yield of fitting the same model with different loss functions, the output of black box algorithms (which is often the case in Machine Learning), or they might be based on expert opinion (or an aggregate of different opinions), underlying physical models or pure gut guess. Since we ignore how the models have been produced, particularly if and what training sample might have been used, we only care about out-of-sample performance.

5.1.1 Model comparison

So suppose we have a random test sample . The standard tool to assess prediction accuracy are scoring functions , which is an alternative name for loss functions frequently used in the forecasting literature; see Footnote 1 for further comments. Just like identification functions, they are functions of the prediction and the observed response . In a sense, they measure the distance between a forecast and the observation , with the standard examples being the squared and the absolute prediction error, and , such that smaller scores are preferable. We estimate the expected score , earlier called statistical risk, as

| (10) |

which we called empirical risk before. Model is deemed to have an inferior predictive performance than model in terms of the score (and on the sample ) if

| (11) |

This pure assessment can be accompanied by a testing procedure to take into account the estimation error of the empirical risk. Hence, we can test for superiority of by formally testing (and rejecting) the null hypothesis . Similarly, one can also test the composite null that , or test the null hypothesis of equal predictive performance via the two-sided null . In a cross-sectional framework, these null hypotheses can all be addressed with a -test which provides asymptotically valid results. In the context of predictive performance comparisons, such -tests are also known as Diebold–Mariano tests, [15].292929For more details about hypothesis testing with scoring functions, we refer to Chapter 3 of [29]. Serial correlation as in time-series needs to be accounted for in the estimation of the variance of the score difference. For correction in a cross-validation setting, see [58, 7]. Finally, we hint at recent developments for e-values, see [39].

5.1.2 Consistency and elicitability

An important question in this model ranking procedure is the choice of the scoring function . At first glance, there is a multitude of scores to choose from. To get some guidance, let us first ignore the presence of features and consider only constant models. Then, the constant model is correctly specified if . To ensure that the correctly specified model outperforms any misspecified model on average if evaluated according to (11), one needs to impose the following consistency criterion on the score , which was coined in [55] and is discussed in detail in [27].

Definition 4

Let be a class of probability distributions where the functional is defined on. A scoring function is a function in a forecast and an observation . It is -consistent for if

| (12) |

The score is strictly -consistent for if it is -consistent for and if equality in (12) implies that . If admits a strictly -consistent scoring function, it is elicitable on .

If the functional of interest is possibly set-valued (e.g. in the case of quantiles), the usual modification of (12) is that any value in the correctly specified functional should outperform a forecast in expectation. Roughly speaking, strict consistency acts as a “truth serum”, encouraging to report correct forecasts.

As can be seen in Table 8, quantiles and expectiles (and therefore the median and mean) are not only identifiable, but also elicitable, subject to mild conditions. Indeed, it can be shown that under some richness assumptions on the class and continuity assumptions on , identifiability and elicitability are equivalent for one-dimensional functionals, see [72]. In line with this, variance and expected shortfall fail to be elicitable [61, 27]. An important exception from this rule is the mode. If is categorical, then the mode is elicitable with the zero-one loss, but no strict identification function is known. For continuous response variables, the mode generally fails to be elicitable or identifiable [38].

5.1.3 Characterisation results

(Strictly) consistent scoring functions for a functional are generally not unique. One obvious fact is that if is (strictly) consistent for , then is also (strictly) consistent for if . But the flexibility is usually much higher: For example, under richness conditions on and smoothness assumptions on the score, any (strictly) -consistent score for the mean takes the form of a Bregman function

| (13) |

where is (strictly) convex and is some function only depending on the observation . For and , this nests the usual squared error; see Table 8 for some examples. Note also that deviances of the exponential dispersion family are Bregman functions, see [68] and Eq. (2.2.7) of [78]. An example of this fact is given in Appendix B for the Tweedie familiy. For the -quantile, under similar conditions, any (strictly) -consistent score takes the form

| (14) |

called generalised piecewise linear, where is (strictly) increasing [27]. The standard choice arises when is the identity. Then (14) is often called piecewise linear loss, tick loss, or pinball loss.

There is an intimate link between strictly consistent scoring functions and strict identification functions, called Osband’s principle [61, 27, 24]. For any strictly -consistent score and strict -identification function there exists a function such that

| (15) |

Using the standard identification functions for the mean and the quantile, Osband’s principle (15) applied to (13) yields that , and applied to (14) it yields ; see Table 8 for some specific examples. Again, the mode functional constitutes an important exception. Here, for categorical , any strictly consistent score is of the form

| (16) |

see [28].

5.1.4 Score decompositions

So far, we have motivated consistency in the setup without any feature information. In the presence of feature information, however, [40] showed that a conditionally calibrated model outperforms a conditionally calibrated model , where the latter one is based only on a subvector of . This led to the observation that consistent scoring functions assess the information contained in a model and how accurately it is used simultaneously. It can be formalised in the following two versions of the calibration–resolution decomposition due to [63]:

| (17) | ||||

The term expresses the degree of conditional miscalibration of with respect to the information contained in the full feature vector . If the score is -consistent and assuming that the conditional distribution is in almost surely, this term is non-negative. Under strict -consistency, it is if and only if almost surely.303030This follows from an application of the definition of (strict) consistency (12) using the conditional distribution . Then, the expected score amounts to the conditional risk defined in (2). The second term, , called conditional resolution or conditional discrimination, expresses the potential of a calibrated and informed prediction with respect to a calibrated, but uninformative prediction . Using the tower property of the conditional expectation and consistency, it is non-negative (see also [40]). Under strict consistency, it is if and only if almost surely. Finally, quantifies the inherent uncertainty of when predicting in terms of . It is also called entropy or Bayes risk in the literature [30]. The second identity in (17) constitutes a similar score decomposition, but now with respect to the auto-calibration. Here, one is more modest in terms of the information set which is used. It is generated by the model itself (hence the term “auto”). This contains generally less information than itself.313131As an example, consider a linear model where is high dimensional, but the model is only one-dimensional. Therefore, the first term , called auto-miscalibration, assesses the deviation from perfect auto-calibration, while the second term , called auto-resolution or auto-discrimination, is still a resolution term, quantifying the potential improvement in reducing uncertainty if the information in the model had been used ideally. This second decomposition reflects the general trade-off a modeller faces when deciding whether to incorporate an additional feature into the model in terms of out-of-sample performance. On the one hand, including additional feature information increases the auto-resolution, but on the other hand, correctly fitting the model will become more difficult making it prone to a potential increase in auto-miscalibration. The two decompositions (17) inform that minimising the expected score in the model amounts to simultaneously improving calibration and maximising resolution [63].

To make the calibration–resolution decomposition (17) tangible, we provide it for the squared error:

| (18) |

The intuitive link between the conditional miscalibration term or the auto-miscalibration term on the one hand and the characterisation of conditional calibration (6) or auto-calibration (7) on the other hand can be made as follows: Invoking the close connection between scoring functions and identification functions via Osband’s principle (15), the respective miscalibration terms can be regarded as the antiderivative of the expected identification function in , with an additive term such that this antiderivative is non-negative and if and only if the corresponding calibration property holds. (Of course, formally this reasoning only holds for the case of constant models and for auto-calibration / unconditional calibration.)

Practical estimation of and therefore of the auto variant of the decomposition can often be performed, see [31] or Figure 10, while the estimation of the ultimate goal can be harder. Hence, estimation of the miscalibration and resolution terms in the decompositions (17) are challenging. In any case, the score decompositions yield beneficial conceptional insights. For practical checks of calibration, one should usually resort to the methods pointed out in Section 4. However, since the unconditional functional and hence the uncertainty are relatively easy to estimate, a simplified decomposition consisting of miscalibration minus resolution / discrimination on the one hand and uncertainty on the other hand is feasible to estimate. Therefore, [31] have promoted the ratio of these two constituents of the simplified score decomposition as a universal coefficient of determination (tacitly assuming that the scores are non-negative). As an in-sample version, it generalises the classical coefficient of determination, , from OLS estimation. The out-of-sample version of this universal coefficient of determination is often referred to as skill score.323232More generally, the skill score for model and scoring function is defined as relative improvement over a reference model as where for a suitable choice of the constant , see [30]. It has therefore a reversed orientation, meaning larger values are better, and the optimal model achieves .

We close the discussion by commenting on the differences of the calibration–resolution decomposition (17) from the decomposition of the statistical risk in (4). Upon identifying the loss function with the score , the terms which are decomposed are the same: . The two main differences are, however, that first the decomposition (4) is concerned with estimation of the risk on a sample level while the decomposition (17) stays on a population level. Second, the baseline in (17) is the entropy , which corresponds to the smallest risk in the class of trivial models . In contrast, the baseline in (4) is , which corresponds to the term in (17).

5.1.5 Further topics

The following five topics also have potential relevance in applications:

-

•

When aiming at estimating the expectation functional, often the root mean squared error is reported and used for comparisons instead of the mean squared error (MSE) in order to have a score on the same unit as the response variable. Since taking the square root is a monotone transformation, RMSE and MSE induce the same model ranking.

-

•

Absolute percentage error (APE) and relative error (RE) , , are two frequently used scores, in particular because they have no unit and can be reported as percentages. According to [27], Theorem 5 (Theorem 2.7 in arxiv version), they both are strictly consistent scoring functions for the -median with for the APE and for the RE. The -median of a distribution with density is defined as the median of the re-weighted distribution with density proportional to .

-

•

One could be interested in a whole vector of different point predictions, resulting in a vector of functionals . Scoring functions for such pairs have been studied, e.g., in [24]. Even though variance and expected shortfall fail to be elicitable, the pair of expected shortfall and the quantile at the same probability level admit strictly consistent scores, see [24] for details. Similarly, the pair (mean, variance) is elicitable. Scores of this pair are provided in [25] Eq. (4.13). One particular example derived from the squared loss and the Poisson deviance is

with predicted mean and predicted standard deviation . Note that this is a homogeneous function of degree two, see (20), and .

It might also be interesting to consider pairs of functionals which are elicitable on their own. Two quantiles at different levels induce a prediction interval with nominal coverage of . Scores for two quantiles can easily be obtained as the sum of two generalised linear losses (14). For the case of a central -prediction interval, i.e. when predicting two quantiles at levels and , denoted (lower) and (upper), a standard interval score [30] arises as

The first term penalises large intervals (corresponding to bad discrimination), the other terms penalise samples outside the predicted interval (corresponding to miscalibration). For more details on evaluating prediction intervals, we refer to [8, 23].

-

•

If the goal is a probabilistic prediction, i.e. to predict the whole conditional distribution , then one uses scoring rules to evaluate the predictions, see [30, 29]. They are maps of the predictive distribution or density and the observation. Here, (strict) consistency is often termed (strict) propriety. It arises in (12) upon considering the identity functional, . Standard examples are the logarithmic scoring rule and the continuously ranked probability score.

-

•

The notion of consistency in Definition 4 has its justification in a large sample situation, relying on a Law of Large Numbers argument to approximate expected scores. In a small sample setting it depends on how scores are used. If modellers are rewarded for their prediction accuracy according to the average score their models achieve, consistency still has its justification in a repeated setting. If, on the other hand, the average score is only a tool to establish a ranking of different models, such that there is a winner-takes-it-all reward, one should care about the probability of achieving a smaller score than competitor models, . This probability is not directly linked to the expected score and such schemes do generally not incentivise truthful forecasting [77]. Hence, it provides an example where a criterion other than consistency is justified. While this field is still subject to ongoing research, the following Subsubsection 5.1.6 provides some links between winner-takes-it-all rewards and efficiency considerations in Diebold–Mariano tests.

5.1.6 Role of data generating process for efficiency

As discussed in Subsubsection 5.1.1, Diebold–Mariano tests for superior predictive performance of model over model formally test the null hypothesis for a scoring function . Without any further distributional assumptions on , one needs to invoke asymptotic normality of the average score differences and uses a - or a -test. With this normal approximation, the power of such a test, i.e. the probability for rejecting under the alternative, is the higher the smaller the ratio

is. This ratio clearly depends on the true joint distribution of and on the choice of . While we are unaware of any clear theoretical results which maximises this efficiency, the simulation study in Appendix C and the following arguments provide evidence that scores derived from the negative log-likelihood of the underlying distribution behave advantageously. The rationale is deeply inspired by the exposition of Section 3.3 in [50] highlighting the role of the classical Neyman–Person Lemma.

To facilitate the presentation, we omit the presence of features for a moment such that we only need to care about the distribution of . Hence, the null simplifies to for two reals . Suppose follows some parametric distribution with density , . Moreover, assume that on this family, the parameter corresponds to the target functional , i.e. for all . For example, could be the family of normal densities with mean and variance 1. Then one could also consider the simple test of the null against the simple alternative . The Neyman–Pearson Lemma then asserts that—under independence—the most powerful test at level is based on the likelihood ratio and it rejects if this ratio exceeds some critical level , which is determined such that the probability of false rejection is exactly under .

Suppose there exists a strictly consistent scoring function for such that for some function it holds that for all , ,

| (19) |

For the above example for normally distributed densities, could be half of the squared error. Hence, the likelihood ratio exceeds if and only if the log of the likelihood ratio, which corresponds to

exceeds . As a matter of fact, the decision based on the likelihood ratio is equivalent to a decision based on the empirical score difference, or equivalently on the average thereof.

Advantageously, this is not an asymptotic argument, but holds for any finite sample size . On the other hand, the Neyman–Pearson Lemma is only applicable if the level of the test is exactly achieved under the null. The correct critical value can, however, only be calculated when exactly knowing and . And it is not clear per se if the test has the correct size under the broader null .

[nonumber=false, tocentry=Practicalities, reference=Practicalities]Practicalities

5.2.1 Which scoring function to choose?

In the presence of a clear purpose for a model, be it business, scientific or anything else, accompanied by an intrinsically meaningful loss function to assess the accuracy of this model, one should just use this very loss function for model ranking and selection.333333E.g. the owner of a windmill might be interested in predictions for windspeed. Windspeed is directly linked to the production capability of electricity for the windmill. The owner uses this capability to enter a short-term contract on the electricity marked with explicit costs for over- or undersupply, resulting in an explicit economic loss for inaccurate forecasts. In the absence of knowing such a specific cost function, but still knowing the modelling target , one should clearly use a strictly consistent scoring function for the functional .

But out of the (usually) infinitely many consistent scoring functions, which one to choose? We see four different directions which might help in selecting a single one:

-

•

Different scoring functions have different domains for forecasts and observations . For instance, the Poisson deviance can only be used for non-negative and positive . This might at least exclude some of the choices.

-

•

Scoring functions can exhibit beneficial invariance or equivariance properties. One of the most relevant ones is positive homogeneity. This describes the scaling behaviour of a function if all its arguments are multiplied by the same positive number. The degree of homogeneity of the score is defined as the number that fulfils

(20) Up to a multiplicative constant, the Tweedie deviances, see Table 8 and Appendix B, are essentially the only homogeneous scoring functions that are strictly consistent for the expectation functional. The Tweedie deviance with power parameter has degree , the Gaussian deviance (corresponding to the squared error) has , the Poisson deviance , the Gamma deviance and the inverse Gaussian deviance . This reflects the well-known fact that the squared error penalises large deviations of its arguments quadratically more than small ones. On the other hand, the Poisson deviance scales linearly with its arguments and preserves the unit. For instance, if and are amounts in some currency like CHF, the unit of Poisson deviance is CHF, too. The scale-invariant Gamma deviance only measures relative differences and has no notion of scales or units. As a 0-homogeneous score it can downgrade the (conditional) heteroskedasticity in the data (volatility clusters etc.). Lastly, larger values of the Tweedie power correspond to heavier-tailed distributions (still, all moments are finite). The larger the Tweedie power, the smaller the degree of homogeneity of the corresponding deviance, which puts less and less emphasis on the deviation of large values and more and more weight on deviations of small values.343434Consider the inverse Gaussian deviance with and degree of homogeneity , . The score is ten times larger than the score .

-

•

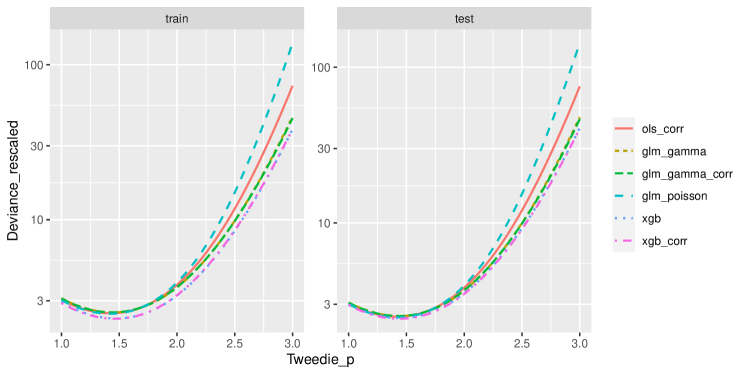

Another aspect in the choice of the scoring function is the efficiency in test decisions for predictive dominance, see Subsubsection 5.1.6. Scoring functions based on the negative log-likelihood of the conditional distribution of given appear to be beneficial. E.g. if this distribution is a certain Tweedie distribution, the corresponding Tweedie deviance given in Table 8 is appropriate. See Appendix C for a corresponding simulation study.

- •

5.2.2 Sample weights and scoring functions

For model fitting, a priori known sample weights , also known as case weights and—in the actuarial literature—exposure or volume, are a way to account for heteroskedasticity and to improve the speed of convergence of the estimation. A simple example is given by the weighted least squares estimation in comparison to OLS estimation. More generally, estimating the conditional expectation via maximum likelihood with a member of the exponential dispersion family amounts to minimising the weighted score

for scoring functions of the Bregman form, see (13) and comments thereafter.

For fitting as well as for model validation, it is noteworthy that using weights often changes the response variable. Take as an example the actuarial task of modelling the average claim size, called severity. Let denote the number of claims of a policy with features , where is given in the feature vector, which happened in a certain amount of time, and denotes the corresponding sum of claim amounts. We define the severity as . Then, the response modelled and predicted by is and not , with the important assumption that .353535This can be seen as follows. We use the -–parametrisation of the Gamma distribution, such that has and upon setting . A typical assumption is that is a sum of independent -distributed claim amounts each with mean and variance , such that . Then, the severity is also Gamma distributed, , with mean and variance .

Back to our main purpose of estimating the expected score based on an i.i.d. test sample . We assume that for some constant and heteroskedasticity in the form of a conditional variance for some and some positive and measurable function . Again, consider the weighted score average

Here, each weight is a function of the feature . For the case that all weights are the same, one simply retrieves the average score . Just like , the weighted average is an unbiased estimate of the expected score. (This is achieved by the normalisation. Simply consider .) Thanks to the total variance formula,363636It asserts that . we can calculate the variance of as

| (21) |

Minimising (21) with respect to the weights yields that any solution can be written as for some constant .373737This can be easiest derived by a constraint optimisation with the Lagrange method, where (21) is minimised subject to for some constant .)

The major drawback with this re-weighting approach in practice is that the conditional variance of the scores is usually unknown. Even if the conditional variance of the response variable is known or assumed, as in maximum likelihood estimation, the authors are not aware of a general link to the level of the score. Whether weighted averages with weights accounting for heteroskedasticity of the response provide more efficient estimates for the expected score seems to be an open question. That being said, weighted averages of scores are nonetheless unbiased.

[nonumber=false, tocentry=Example, reference=Example]Example: Mean Regression for Workers’ Compensation.

5.3.1 Model comparison with Gamma deviance

As stated in the Subsubsection 3.2.4, we evaluate our models with the Gamma deviance, see Table 8 and Equation (10). The reasons for this choice follow the discussion of Subsubsection 5.2.1:

-

•

The target functional is the expectation and the Gamma deviance is strictly consistent for it.

-

•