Forgiving Debt in Financial Network Games

University of Essex, UK)

Abstract

A financial system is represented by a network, where nodes correspond to banks, and directed labeled edges correspond to debt contracts between banks. Once a payment schedule has been defined, where we assume that a bank cannot refuse a payment towards one of its lenders if it has sufficient funds, the liquidity of the system is defined as the sum of total payments made in the network. Maximizing systemic liquidity is a natural objective of any financial authority, so, we study the setting where the financial authority offers bailout money to some bank(s) or forgives the debts of others in order to maximize liquidity, and examine efficient ways to achieve this. We investigate the approximation ratio provided by the greedy bailout policy compared to the optimal one, and we study the computational hardness of finding the optimal debt-removal and budget-constrained optimal bailout policy, respectively.

We also study financial systems from a game-theoretic standpoint. We observe that the removal of some incoming debt might be in the best interest of a bank, if that helps one of its borrowers remain solvent and avoid costs related to default. Assuming that a bank’s well-being (i.e., utility) is aligned with the incoming payments they receive from the network, we define and analyze a game among banks who want to maximize their utility by strategically giving up some incoming payments. In addition, we extend the previous game by considering bailout payments. After formally defining the above games, we prove results about the existence and quality of pure Nash equilibria, as well as the computational complexity of finding such equilibria.

1 Introduction

A financial system comprises a set of institutions, such as banks, that engage in financial transactions. The interconnections showing the liabilities (financial obligations or debts) among the banks can be represented by a network, where the nodes correspond to banks and the edges correspond to liability relations. Each bank has a fixed amount of external assets (not affected by the network) which are measured in the same currency as the liabilities. A bank’s total assets comprise its external assets and its incoming payments, and may be used for (outgoing) payments to its lenders. If a bank’s assets are not enough to cover its liabilities, that bank will be in default and the value of its assets will be decreased (e.g., by liquidation); the extent of this decrease is captured by default costs and essentially implies that the corresponding bank will have only a part of its total assets available for making payments.

On the liquidation day (also known as clearing), each bank in the system has to pay its debts in accordance with the following three principles of bankruptcy law (see, e.g., (Eisenberg and Noe, 2001)): i) absolute priority, i.e., banks with sufficient assets pay their liabilities in full, ii) limited liability, i.e., banks with insufficient assets to pay their liabilities are in default and pay all of their assets to lenders, subject to default costs, and iii) proportionality, i.e., in case of default, payments to lenders are made in proportion to the respective liability. Payments that satisfy the above properties are called clearing payments and (perhaps surprisingly) these payments are not uniquely defined for a given financial system. However, maximal clearing payments, i.e., ones that point-wise maximize all corresponding payments, are known to exist and can be efficiently computed (Rogers and Veraart, 2013).

The total liquidity of a financial system is measured by the sum of payments made at clearing, and is a natural metric for the well-being of the system. Financial authorities, e.g., governments or other regulators, wish to keep the systemic liquidity as high as possible and they might interfere, if their involvement is necessary and would considerably benefit the system. For example, in the not so far past, the Greek government (among others) took loans in order to bailout banks that were in danger of defaulting, to avert collapse. In this work, we study the possibility of a financial regulating authority performing cash injections (i.e., bailouts) to selected bank(s) and/or forgiving debts selectively, with the aim of maximizing the total liquidity of the system (total money flow). Similarly to cash injections, it is a fact that debt removal can have a positive effect on systemic liquidity. Indeed, the existence of default costs can lead to the counter-intuitive phenomenon whereby removing a debt/edge from the financial network might result in increased money flow, e.g., if the corresponding borrower avoids default costs because of the removal.

Even more surprising than the increase of liquidity by the removal of debts, is the fact that the removal of an edge from borrower to lender might result in receiving more incoming payments, e.g., if avoids default costs and there is an alternative path in the network where money can flow from to . This motivates the definition of an edge-removal game on financial networks, where banks act as strategic agents who wish to maximize their total assets and might intentionally give-up a part of their due incoming payments towards this goal. As implied earlier, removing an incoming debt could rescue the borrower from financial default, thereby avoiding the activation of default cost, and potentially increasing the lender’s utility (total assets). This strategic consideration is meaningful both in the context where a financial authority performs cash injections or not. We consider the existence, quality, and computation of equilibria that arise in such games.

1.1 Our contribution

We consider computational problems related to maximizing systemic liquidity, when a financial authority can modify the network by appropriately removing debt, or by injecting cash into selected agents. We also consider financial network games where agents can choose to forgive incoming debts.

We show how to compute the optimal cash injection policy in polynomial time when there are no default costs, by solving a linear program; the problem is NP-hard when non-trivial default costs apply. As our LP-based algorithm requires knowledge of the available budget and leads to non-monotone payments, we study the approximation ratio of a greedy cash injection policy. Regarding debt removal, we prove that finding the set of liabilities whose removal maximizes systemic liquidity is NP-hard, and so are relevant optimization problems.

Regarding edge-removal games, with or without bailout, we study the existence and the quality of Nash equilibria, while also addressing computational complexity questions. Apart from arguing about well-established notions, such as the Price of Anarchy and the Price of Stability, we introduce the notion of the Effect of Anarchy (Stability, respectively) as a new measure on the quality of equilibria in this setting.

1.2 Related work

Our model is based on the seminal work of Eisenberg and Noe (2001) who introduced a widely adopted model for financial networks, assuming debt-only contracts and proportional payments. This was later extended by Rogers and Veraart (2013) to allow for default costs. Additional features have been since introduced, see e.g., (Schuldenzucker et al., 2020) and (Papp and Wattenhofer, 2020). We follow the model of Eisenberg and Noe and consider proportional payments; we note that a recent series of papers introduced different payment schemes (Bertschinger et al., 2020; Papp and Wattenhofer, 2020; Kanellopoulos et al., 2021).

When the financial regulator has available funds to bailout each bank of the network, Jackson and Pernoud (2020) characterize the minimum bailout budget needed to ensure systemic solvency and prove that computing it is an NP-hard problem. When the financial authority has limited bailout budget, Demange (2018) proposes the threat index as a means to determine which banks should receive cash during a default episode and suggests a greedy algorithm for this process. Egressy and Wattenhofer (2021) focus on how central banks should decide which insolvent banks to bailout and formulate corresponding optimization problems. Dong et al. (2021) introduce an efficient greedy-based clearing algorithm for an extension of the Eisenberg-Noe model, while also studying bailout policies when banks in default have no assets to distribute. We note that the problem of injecting cash (as subsidies) in financial networks has been studied (in a different context) in microfinance markets (Irfan and Ortiz, 2018).

Further work includes (Schuldenzucker and Seuken, 2020) that considers the incentives banks might have to approve the removal of a set of liabilities forming a directed cycle in the financial network, while (Schuldenzucker et al., 2017) considers the complexity of finding clearing payments when CDS contracts are allowed. In a similar spirit, (Ioannidis et al., 2021) studies the clearing problem from the point of view of irrationality and approximation strength, while (Papp and Wattenhofer, 2021) studies which banks are in default, and how much of their liabilities these defaulting banks can pay.

2 Preliminaries

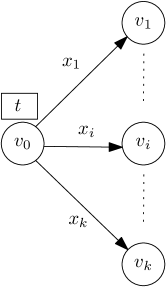

A financial network consists of a set of banks, where each bank initially has some non-negative external assets corresponding to income received from entities outside the financial system. Banks have payment obligations, i.e., liabilities, among themselves. In particular, a debt contract creates a liability of bank (the borrower) to bank (the lender); we assume that and . Note that and may both hold simultaneously. Also, let be the total liabilities of bank . Banks with sufficient funds to pay their obligations in full are called solvent banks, while ones that cannot are in default. Then, the relative liability matrix is defined by

Let denote the actual payment111Note that the actual payment need not equal the liability, i.e., the payment obligation. from to ; we assume that . These payments define a payment matrix with , where by we denote the set of integers . We denote by the total outgoing payments of bank . A bank in default may need to liquidate its external assets or make payments to entities outside the financial system (e.g., to pay wages). This is modeled using default costs defined by values . A bank in default can only use an fraction of its external assets and a fraction of its incoming payments (the case without default costs is captured by ). The absolute priority and limited liability regulatory principles, discussed in the introduction, imply that a solvent bank must repay all its obligations to all its lenders, while a bank in default must repay as much of its debt as possible, taking default costs also into account. Summarizing, it must hold that and, furthermore, , where

Payments that satisfy these constraints are called clearing payments. Proportional payments have been frequently studied in the financial literature (e.g., in (Demange, 2018; Eisenberg and Noe, 2001; Rogers and Veraart, 2013)). Given clearing payments , in order to satisfy proportionality, each must also satisfy when is solvent, and , when is in default.

Given clearing payments , the total assets of bank are defined as the sum of external assets plus incoming payments, i.e.,

Maximal clearing payments, i.e., ones that point-wise maximize all corresponding payments (and hence total assets), are known to exist (Eisenberg and Noe, 2001; Rogers and Veraart, 2013) and can be computed in polynomial time.

We measure the total liquidity of the system (also refered to as systemic liquidity) as the sum of payments traversing through the network, i.e.

We assume that there exists a financial authority (a regulator) who aims to maximize the systemic liquidity.In particular, the regulator can decide to remove certain debts (edges) from the network or inject cash to some bank(s). In the latter case, we assume the regulator has a total budget available in order to perform cash injections to individual banks. We sometimes refer to the total increased liquidity, , (as opposed to total liquidity) which measures the difference in the systemic liquidity before and after the cash injections. 222This is necessary as in some cases, like the proof of the approximability of the greedy algorithm in Theorem 2, we cannot argue about the total liquidity but we can argue about the total increased liquidity. A cash injection policy is a sequence of pairs of banks and associated transfers , such that the regulator gives capital to bank , to bank , etc. These actions naturally define two corresponding optimization problems on the total (increased) liquidity, i.e., optimal cash injection and optimal debt removal.

We will also find useful the notion of the threat index333The term threat index aims to capture the “threat” posed to the network by a decrease in a bank’s cash-flow or even the bank’s default; this index can be thought of as counting all the defaulting creditors that would follow a potential default of the said bank., , of bank , which captures how many units of total increased liquidity will be realized if the financial authority injects one unit of cash into bank ’s external assets (Demange, 2018); a unit of cash represents a small enough amount of money so that the set of banks in default would not change after the cash injection. We remark that for the maximum total increased liquidity it holds , where is the maximum threat index. Naturally, the threat index of solvent banks is , while the threat index of banks in default will be at least . Formally, the threat index is defined as

where is the set of banks who are in default.444In matrix form, the threat index for banks who are in default can be computed by . This is a homogeneous linear equation system where is the relative liability matrix only involving in the banks in set ; and represent the dimension identity matrix and the dimension identity vector, respectively, while is the vector of threat indices for banks in default.

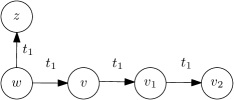

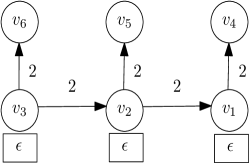

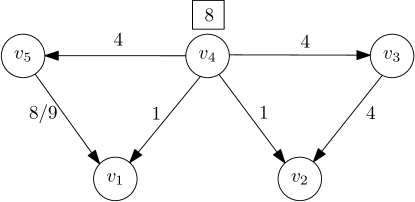

An example. Figure 1 provides an example of a financial network, inspired by an example in (Demange, 2018). The clearing payments are as follows: , , and , implying that banks and are in default. We assume that there are no default costs, i.e., . The threat indexes are computed as follows: , , , and , implying that , , while .

Additional definitions are deferred to the corresponding sections they are used for ease of exposition. Most importantly, we introduce (in Section 4) two novel notions, namely the Effect of Anarchy/Stability, that measure the effect strategic behavior has on the original network.

3 Computing and approximating optimal outcomes

In this section we present algorithmic and complexity results regarding the problems of computing optimal cash injection (see Section 3.1) and debt removal (Section 3.2) policies. Note that we omit referring to default costs in our statements for those results that hold when .

3.1 Optimal cash injections

We begin with a positive result about computing the optimal cash injection policy when default costs do not apply.

Theorem 1.

Computing the optimal cash injection policy can be solved in polynomial time.

Proof.

The proof follows by solving a linear program that computes the optimal cash injections and accompanying payments.

We denote by the cash injection to bank and by the payment from to . We aim to maximize the total liquidity, i.e., the total payments, subject to satisfying the limited liability and absolute priority principles. Recall that is the budget, is the liability of to , is the external assets of bank , and is the total liabilities of .

The first constraint corresponds to the budget constraint, while the second and third sets of constraints guarantee that no bank pays more than her total assets or more than a given liability; hence, the limited liability principle is satisfied. It remains to argue about the absolute priority principle, i.e., a bank can pay strictly less than her total assets only if she fully repays all outstanding liabilities.

Consider the optimal solution corresponding to a vector of cash injections and payments ; we will show that this solution satisfies the absolute priority principle as well. We distinguish between two cases depending on whether a bank is solvent or in default. In the first case, consider a solvent bank , i.e., , for which for some bank . By replacing with , we obtain another feasible solution that strictly increases the objective function; a contradiction to the optimality of the starting solution. Similarly, consider a bank with for which . Then, there necessarily exists a bank for which and it suffices to replace with to obtain another feasible solution that, again, strictly increases the objective function. Hence, we have proven that the optimal solution to the linear program satisfies the absolute priority principle and the claim follows by providing each bank a cash injection of . ∎

Note that the optimal policy does not satisfy certain desirable properties. In particular, as observed in (Demange, 2018), cash injections are not monotone with respect to the budget. To see that, consider the financial network in Figure 1 and note that when , the optimal policy would give all available budget to bank , while under an increased budget of , the entire budget would be allocated to , hence would get nothing. Furthermore, our LP-based algorithm crucially relies on knowledge of the available budget.

In an attempt to alleviate these undesirable properties, we turn our attention to efficiently approximating the optimal cash injection policy by a natural and intuitive greedy algorithm, and we compute its approximation ratio under a limited budget, when we care about the total increased liquidity.

Definition 1 (Greedy and its approximation ratio).

According to Greedy (the Greedy cash injection policy), banks receive their cash injections in sequence, so that , for , is the bank with the highest threat index after the cash injection at round (round is defined to be the starting configuration), while is the minimum amount that would cause a change in the vector of threat indexes at the time it is transferred (it would lead to some previously defaulting bank to become solvent).555Without loss of generality we assume ties are broken in favor of the smallest index. This process is repeated until the budget runs out.

The approximation ratio of Greedy shows how smaller the total increased liquidity (or money flow) can be, compared to the optimal total increased liquidity, and is computed as

where the minimum is computed over all possible networks and budgets.

Let us revisit the example in Figure 1, assuming a budget . Initially banks and have the highest threat index of compared to , and . We can assume666This is consistent to our tie breaking assumption that favors the least index. that bank would receive the first cash injection () and in fact this will be equal to . Indeed, a cash injection of to will result in becoming solvent (notice that receives from ), while a smaller cash injection would not impose any change on the threat index vector. At this stage, the threat index of each bank is as follows and . At this round, would receive the remaining budget of . Hence, the total increased liquidity achieved by Greedy at this instance is ( will traverse edges and , while will traverse edge ). However, the optimal cash injection policy is to inject the entire budget to bank resulting in . Therefore, this instance reveals .

Theorem 2.

Greedy’s approximation ratio is at most . For inputs satisfying , this ratio is tight.

Proof.

The upper bound follows from the instance in Figure 1 and the discussion above; in the following, we argue about the lower bound when the total budget satisfies the condition in the statement. We consider the following properties and claim that the worst approximation ratio of Greedy is achieved at networks that satisfy both properties. To prove this claim we will show that starting from an arbitrary network on which Greedy approximates the optimal total increased liquidity by a factor of , we can create a new network that satisfies properties (P1) and (P2), such that Greedy approximates the optimal total increased liquidity in the new network by a factor of at most . We can then bound the approximation ratio of Greedy on the set of networks that satisfy these properties.

-

(P1)

The total increased liquidity achieved by Greedy is exactly .

-

(P2)

The optimal total increased liquidity is exactly .

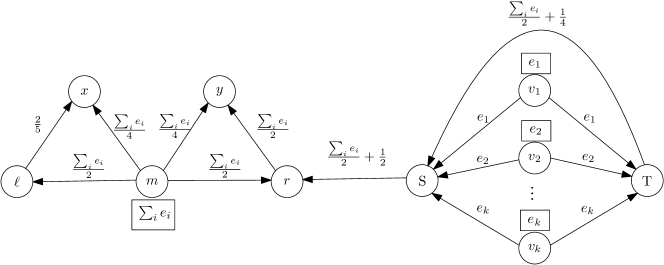

Let the bank with the highest threat index in be and let be that threat index. If or then the claim is true (Greedy trivially achieves an approximation ratio of ), so we henceforth assume that and . We create (see Figures 2 and 3) as follows. To formally describe our construction it is convenient to express the highest threat index as for some that satisfy and a fixed integer. If is an integer, then we set (which implies and ), while if is not an integer, we set and . Our network comprises nodes, i.e., and , for . There is a directed path of length , including the following nodes in sequence and , for , where the first edges have liability . The remaining edge(s) on that path has/have liability and there is an edge with liability . Moreover, there are edges and such that and . Note that the liabilities of the two outgoing edges of are selected so that and both have the highest threat index in ; indeed, the threat index of in is , and the threat index of in is , where . Immediate consequences of our construction are (i) and (ii) which will be useful later.

To see that satisfies property (P1), it suffices to consider that in the first step, Greedy offers a cash injection of to in ; is then the only node in default and has threat index equal to . The total increased liquidity achieved by Greedy in is exactly , while Greedy achieves at least that total increased liquidity in since each node in default has threat index at least equal to . Assume now that the regulator offers the entire budget to node in ; this would result to total increased liquidity of as required by (P2), and since, by construction is the maximum total increased liquidity in , it holds that is an upper bound on the optimal total increased liquidity in the original network too. We can conclude that it is without loss of generality to restrict attention to networks that satisfy properties (P1) and (P2) when proving a lower bound on the approximation ratio of Greedy.

Overall, it holds that the approximation ratio of Greedy is lower bounded by

where the minimum ranges over the set of networks satisfying properties (P1) and (P2). Straightforward calculations after substituting which holds by construction, leads to

where the second inequality holds by assumption that and since, by construction , while the third inequality holds since is a global minimum of function . ∎

We conclude this section with some hardness results.

Theorem 3.

The following problems are NP-hard:

-

a)

Compute the optimal cash injection policy under the constraint of integer payments.

-

b)

Compute the optimal cash injection policy with default costs and .

-

c)

Compute the minimum budget so that a given agent becomes solvent, with default costs and .

Proof.

We begin with the case where all proportional payments need to be integers, and then prove the cases where default costs apply.

Hardness of computing the optimal cash injection policy under integer payments. We warm-up with a rather simple reduction from Exact Cover by 3-Sets (X3C), a well-known NP-complete problem. An instance of X3C consists of a set of elements together with a collection of size-3 subsets of . The question is whether there exists a subset of size such that each element in appears exactly once in .

We build an instance of our problem as follows. We add an agent for each and an agent for each element ; we also add agent . There are no external assets and the liabilities are as follows. Each agent , corresponding to where are elements in , has liability to each of the three agents . Furthermore, each agent has liability of to agent , while we assume that the budget equals .

Due to the integrality constraint and the fact that payments are proportional, a yes-instance for X3C, admitting a solution , leads to a solution of liquidity , by injecting a payment of to each corresponding to the set .

On the other direction, we argue that any solution with liquidity at least leads to a solution for the instance of X3C. Indeed, any such solution must necessarily lead to liquidity of at least to the edges from the agents to the agents. Since the budget equals this implies that exactly of the agents must receive a payment of and these agents should cover the entire set of the agents.

Hardness of computing the optimal cash injection policy with default costs. Our proof follows by a reduction from the Partition problem, a well-known NP-complete problem. Recall that in Partition, an instance consists of a set of positive integers and the question is whether there exists a subset of such that .

The reduction works as follows. Starting from , we build an instance by adding an agent for each element and allocating an external asset of to ; we also include three additional agents and . Each agent has liability equal to to and equal to to , while has liability to ; see also Figure 4. We assume the presence of default costs , and , while the budget is ; clearly, the reduction requires polynomial-time.

We first show that if is a yes-instance for Partition, then the total liquidity is . Indeed, consider a solution for instance satisfying , and let the set contain agents where . Then, since , we choose to inject an amount of to any agent . The total assets of agent are then

and, hence, is solvent. The total liquidity in this case is

as desired.

We now show that any cash injection policy that leads to a total liquidity of at least leads to a solution for instance of Partition. Assume any such cash injection policy and let be the set of agents that become solvent by it. Denote by the liquidity arising solely from the payments made by the agents , for , to their direct neighbors, and we denote by the amount of cash injected to , we get that

| (1) |

It also holds that

| (2) |

since, by assumption, the policy under consideration leads to a total liquidity of at least and the payment from to can be at most .

Combining Inequalities (3.1) and (2), we get that

which is equivalent to for . Moreover, note that each agent needs (at least) an extra to become solvent and, hence, it must be , due to the budget constraint. We can conclude that and, hence, we can obtain a solution to instance of Partition, as desired.

Hardness of computing the minimum budget that makes an agent solvent. The proof follows by the same reduction as in the previous case. We will prove that computing the minimum budget necessary to make agent solvent corresponds to solving an instance from Partition. As before, whenever instance admits a solution , we inject an amount of to each agent such that , and, as in the previous case, we obtain that a budget of suffices to make solvent. We now argue that any cash injection policy with a budget of that can make agent solvent leads to a solution for instance when the default costs are .

Let be the cash injected at agent and let be the cash injected directly at agent ; clearly, . As before, let be the set of agents that become solvent by the cash injection policy. Clearly, if , we immediately obtain a solution to the Partition instance. Otherwise, and the total assets of are

| (3) | ||||

where the second equality holds due to the budget constraint and the strict inequality holds since and ; the claim follows. ∎

3.2 Optimal debt removal

In this section, we focus on maximizing systemic liquidity by appropriately removing edges/debts. As an example, consider again Figure 1, where the central authority can increase systemic liquidity by removing the edge between and .

Theorem 4.

The problem of computing an edge set whose removal maximizes systemic liquidity is NP-hard.

Proof.

The proof relies on a reduction from the NP-complete problem RXC3 (Gonzalez, 1985), a variant of Exact Cover by 3-Sets (X3C). In RXC3, we are given an element set , with for an integer , and a collection of subsets of where each such subset contains exactly three elements. Furthermore, each element in appears in exactly three subsets in , that is . The question is if there exists a subset of size that contains each element of exactly once. Given an instance of RXC3, we construct an instance as follows. We add an agent for each element of and an agent for each subset in , as well as two additional agents, and . Each , corresponding to set , has external assets and liability to the three agents corresponding to the three elements . Furthermore, each has liability to agent , where is a large integer. Finally, each agent has liability to agent ; see also Figure 5. Note that this construction requires polynomial time.

When instance is a yes-instance with a solution , we claim that admits a solution with systemic liquidity . Indeed, it suffices to remove all edges from the agents, with , towards . Then, the liquidity due to agents , with , equals , while each of the agents whose edge towards was preserved generates a liquidity of .

It suffices to show that any solution that generates liquidity at least can lead to a solution for instance . First, observe that it is never strictly better for the financial authority to remove an edge from some agent towards an agent . Let and be the subsets of agents whose edges towards are kept and removed, respectively, and let . The liquidity traveling from agents in towards their direct neighbors is exactly , while the liquidity traveling from agents in towards their direct neighbors is exactly . The maximum liquidity traveling from agents towards is at most . We conclude that the maximum liquidity is bounded by .

Note that, whenever , then the maximum liquidity is at bounded by . Similarly, whenever and since is arbitrarily large, the maximum liquidity is bounded by . It remains to show that whenever , a liquidity of at least necessarily leads to a solution in . Indeed, by the discussion above, any such solution must have liquidity equal to traveling from agents towards , i.e., all these liabilities are fully repaid. This, in turn, can only happen if each of the agents receives a payment of at least from the agents. Using the assumptions that i) , ii) is arbitrarily large, iii) payments are proportional to liabilities, and iv) each has exactly three neighboring agents, this property holds only when the neighbors of the agents in are disjoint. This directly translates to a solution for instance and the RXC3 problem. ∎

We note that the objective of systemic solvency, i.e., guaranteeing that all agents are solvent, can be trivially achieved by removing all edges. However, adding a liquidity target, makes this problem more challenging.

Theorem 5.

In networks with default costs, the following problems are NP-hard:

-

a)

Compute an edge set whose removal ensures systemic solvency and maximizes systemic liquidity.

-

b)

Compute an edge set whose removal ensures systemic solvency and minimizes the amount of deleted liabilities.

-

c)

Compute an edge set whose removal guarantees that a given agent is no longer in default and minimizes the amount of deleted liabilities.

Proof.

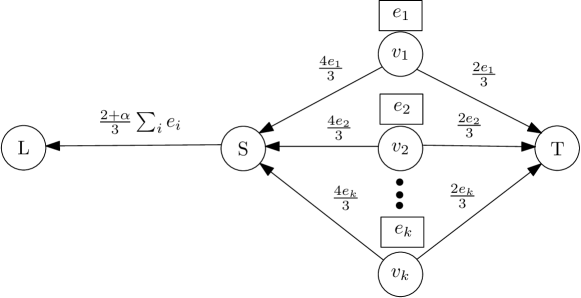

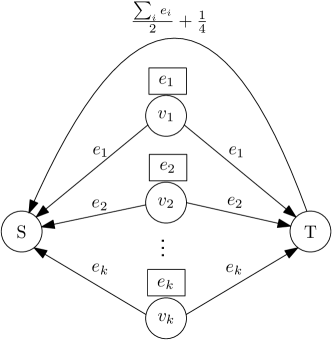

The proof for all these claims relies on a reduction from the Subset Sum problem, where the input consists of a set of integers and a target and the question is whether there exists a subset such that . Given an instance of Subset Sum, we construct an instance by adding an agent for each integer , adding an extra agent having and setting the liability of to to be equal to ; see also Figure 6.

Since is in default, the goal becomes to remove an edge set so that the remaining liability of is at most . Whenever instance is a yes-instance for Subset Sum admitting a solution , we remove edges from to agents corresponding to integers not in . Then, is solvent and the systemic liquidity equals . Otherwise, if is a no-instance, no edge set removal that leaves solvent can lead to systemic liquidity of (at least) . ∎

4 The edge-removal game

In this section, we consider the case of strategic agents who have the option to forgive debt.

Edge-removal games and the Effect of Anarchy/Stability. Consider a financial network of banks who act strategically. The strategy set of a bank is the power set of its incoming edges and a strategy denotes which of its incoming edges that bank will remove, thus erasing the corresponding debt owed to itself. The edge-removal game can be defined with and without cash-injections. A given strategy vector will result in realized payments through maximal clearing payments including possible cash injections through a predetermined cash injection policy. Our results hold for both the optimal policy and Greedy.

A bank is assumed to strategize over its incoming edges in order to maximize its utility, i.e., its total assets, where we remark that a possible cash injection can be seen as increasing one’s external assets. The objective of the financial authority is to maximize the total liquidity of the system, i.e., the social welfare is the sum of money flows that traverse the network.

We consider the central notion of Nash equilibrium strategy profile, under which no bank can unilaterally increase its utility by changing strategy. The inefficiency of Nash equilibria in terms of liquidity is measured by the Price of Anarchy (Stability, respectively) which is equal to optimal systemic liquidity over that of the worst (best, respectively) pure Nash equilibrium. Note that the optimal systemic liquidity corresponds to the maximal one when the financial authority can dictate everyone’s actions (edge-removals).

The Price of Anarchy/Stability notions provide indications regarding the extent to which the individual objectives of the banks and the objective of the regulator are (not) aligned. We, here, introduce a new notion that we use to measure the discrepancy between the systemic liquidity of the original network (no edge removal) and that of worst (best) Nash equilibrium. We call this the Effect of Anarchy, (Stability, respectively) and define it as follows.

We investigate properties of Nash equilibria in the edge-removal game with respect to their existence and quality, while we also address computational complexity questions under different assumptions on whether default costs and/or cash injections apply. Our results on the Effect of Anarchy of edge removal games imply that, rather surprisingly, in the presence of default costs even the worst Nash equilibrium can be arbitrarily better than the original network in terms of liquidity. However, the situation is reversed in the absence of default costs, where we observe that the original network can be considerably better in terms of liquidity than the worst equilibrium; in line with similar Price of Anarchy results. We begin with some results for the basic case, that is, without default costs; recall that we do not refer to default costs in the statements for results holding for .

Theorem 6.

Edge-removal games without cash injections always admit Nash equilibria. In particular, the strategy profile where all edges are preserved is a Nash equilibrium.

Proof.

We claim that it is a Nash equilibrium if no bank removes an incoming edge. Indeed, consider a financial network and an arbitrary debt relation in that network represented by an edge from to . Since there are no default costs, removing and keeping everything else unchanged, will result in instantly having additional assets to pay to its lenders (excluding ). This, however can lead to at most additional assets to reach through indirect paths starting from so it can not lead to more total payments from to .777This wouldn’t be true if additional money was inserted to the network in the form of a cash injection. Hence, is better off not removing . Since is an arbitrary bank and represents an arbitrary edge, our proof is complete. ∎

Theorem 7.

In edge-removal games without cash injections, the Effect of Anarchy is unbounded and the Effect of Stability is at most .

Proof.

The result on the Effect of Stability follows as a corollary of Theorem 6. For the Effect of Anarchy, consider a simple network with two banks, each having a liability of to the other. In the original network, the total liquidity is , while it is not hard to see that the network with both edges removed is a Nash equilibrium with a total liquidity of zero. ∎

Our next result shows that Nash equilibria may not exist once we allow for cash injections.

Theorem 8.

In edge-removal games with cash injections, Nash equilibria are not guaranteed to exist.

Proof.

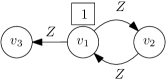

Consider the network shown in Figure 7, and a budget equal to , where is an arbitrarily small constant.

We begin by observing that and will never remove their incoming edges, since each of these agents has a single incoming edge, originating from some agent with positive externals. Hence, it suffices to consider the strategic actions of banks and regarding the possible removal of edges and , respectively. There are four possible cases:

-

A)

both edges are present. In this case, has the highest threat index, i.e., and, thus receives the entire budget; it is not hard to verify that this is the optimal policy as well. The payments are, then, , resulting in total assets .

-

B)

is present, is removed. In this case, receives the budget and the following payments are realized . This leads to total assets and .

-

C)

both edges are removed. In this case, there is a tie on the maximum threat index ( and have threat index ), so, assuming that the banks with lower index are prioritized, receives all the budget; again, it is not hard to verify that this is an optimal policy as well. This results to payments and with .

-

D)

is removed, is present. In this case, receives the budget. The payments are and (due to the removal), which implies and respectively.

One can now easily check that the best response dynamics cycle, as starting from Case A, has an incentive to remove its incoming edge and we reach Case B. Then, has an incentive to remove its incoming edge (we are now in Case C), which leads to have an incentive to reinstate its incoming edge (thus, reaching Case D). Finally, in Case D, has an incentive to reinstate , leading to Case A again. ∎

Theorem 9.

The Price of Stability in edge-removal games (with or without cash injections) is unbounded.

Proof.

We present the proof for the case without cash injections and note that the proof carries over for the case of limited budget regardless of who receives it. Moreover, note that the proof does not assume default costs but the result immediately applies to that (more general) case as well, i.e., is a special case of default costs.

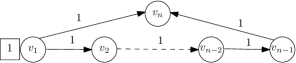

Consider the network shown in Figure 8, where is an arbitrary large constant. Since each bank has exactly one incoming edge, no edge removals occur at the unique Nash equilibrium. By the proportionality principle it holds that the three payments have to be equal (to ), that is , which results in the systemic liquidity of . However, systemic liquidity of can be achieved when removes its incoming edge. Indeed, then each remaining payment can be equal to . We conclude that , so the price of stability can be arbitrarily large for appropriately large values of , as desired. ∎

Theorem 10.

The Effect of Anarchy in edge-removal games with cash injections is at least .

Proof.

Consider the network shown in Figure 9 and assume a budget . If there are no edge removals, then bank will receive the entire budget, thus achieving total liquidity equal to . However, we claim that the state where every bank except removes their incoming edge is an equilibrium with total liquidity . Indeed, in this case receives the budget and this leads to total assets . Under the assumption that ties are broken in favor of the lowest index, the only edge addition that would change the recipient of the cash injection is if decides to reinstate edge , however, this will lead to exactly the same total assets for since will receive the budget. Clearly, does not have an incentive to remove its incoming edge. The proof is complete.

∎

Theorem 11.

The Effect of Stability in edge-removal games with cash injections is .

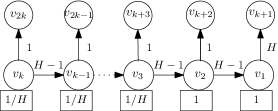

Proof.

Consider the network in Figure 10 where the budget , and is arbitrarily larger than .

We start by noticing that , while for , it holds that , for sufficiently large ; all other banks are solvent. Hence, the optimal total liquidity is achieved when receives the entire budget of as a cash injection, and is roughly , when is sufficiently large.

We now claim that under any Nash equilibrium, will receive the budget and all edges for are removed. This would complete the proof, as the total liquidity would be at most . We now prove this claim. Consider any equilibrium and observe that , for , must have their unique incoming edge present. Now, assume for a contradiction that some bank with gets a cash injection; this implies that the edge is present as, otherwise, the result holds trivially. Then, bank has total assets , but can increase them to by strategically removing its incoming edge. So, under any Nash equilibrium, either or receives a cash injection. In the former case, where edge is present, , while the assets of would be if it removed its incoming edge and received the cash injection.

So far, we have proven that gets the cash injection and it remains to show no other edge for exists in a Nash equilibrium. Now, observe that if such an edge exists, then neighboring edges on the horizontal path cannot exist as that would contradict that gets the cash injection. Then, when , bank would have an incentive to add edge , thus, making bank the recipient of the budget (for both optimal and greedy) and strictly increase its own total assets. The cases can be easily ruled out as well. Our proof is complete. ∎

We now present a series of results for the case where default costs exist, but cash injections are not allowed. Contrary to the case with neither default costs nor cash injections, we show that a Nash equilibrium is no longer guaranteed to exist; the next result is complementary to Theorem 8.

Theorem 12.

Edge-removal games with default costs but without cash injections may not admit Nash equilibria.

Proof.

We present the proof for the case without cash injections and note that the proof carries over for the case of limited budget regardless of who receives it, as a sufficiently small budget will not alter the players incentives.

Consider the financial network in Figure 11 and assume that default costs are applied.

We begin by claiming that (and, by symmetry ) will never remove its incoming edge. Indeed, since has positive external assets, then will receive a positive payment from if the edge between them remains, however will have zero incoming payments if the corresponding edge is removed. Similarly, (and, by symmetry ) will never remove the edge from (respectively ). Therefore, it suffices to consider the possible removal of edges and . We will prove that none of the following states are at equilibrium: A) no edge is removed, B) is removed but remains, C) both edges are removed, and D) remains but is removed.

Note that in Case A is in default, hence, due to the default costs, its payments are broken down as . But then, and are also in default, and in this case. So, the utility of both and is . By removing in Case A, and moving to Case B, would increase its utility to . Indeed, in this case, , while and , so the utility of is and the utility of is . But, then, it is beneficial for to remove ). In this case (Case C), is now solvent and all existing debts are paid for, thus giving utility to and utility to . However, if then decides to reinstate its incoming edge , its utility in this case (Case D) is increased to , while ’s utility is , since , and . Finally, prefers its utility in Case A to its utility in Case D so will decide to reinstate when in Case D, thus defining a cycle between the four possible states. ∎

For some restricted topologies, however, the existence of Nash equilibria is guaranteed; in particular, keeping all edges is a Nash equilibrium.

Theorem 13.

Edge-removal games with default costs but without cash injections always admit Nash equilibria if the financial network is a tree or a cycle.

Proof.

We present the proof for the case without cash injections and note that the proof carries over for the case of limited budget regardless of who receives it.

Consider a financial network that is a tree (similar argument works in case of a directed cycle) and an arbitrary debt relation in that network represented by a directed edge . By definition of the tree structure, it holds that there is no other path in the network from to . Hence, cannot benefit by removing that edge, even if the removal affects (increases) ’s available assets. ∎

The following result demonstrates that the positive impact of (individually benefiting) edge removals dominates the negative impact of reducing the number of edges through which money can flow, hence, edge removals are in line with the regulator’s best interest too.

Lemma 1.

Edge-removal games with default costs but no cash injections satisfy the following: given any network and any strategy profile, any unilateral removal of any edge(s) that weakly improves the total assets of the corresponding bank, also weakly improves the total assets of every other bank in the network. Consequently, the total liquidity of the system is increased.

Proof.

Consider a network and a strategy profile , under which banks have total assets according to . Fix a bank and let be the strategy profile that is derived by if bank changes its strategy from to , where is derived by by the removal of an edge (the argument can be applied repeatedly to prove the claim for more than one edge removals). By assumption, the total assets of bank under , , satisfy . It holds that any bank reachable by or (the two endpoints of the edge that was removed) through a directed path will have at least the same total assets under than with , since there will be at least the same amount of money available to leave and and traverse these paths. The assets of banks not reachable by or will, clearly, not be affected by the removal of . Hence, the assets of each bank in are weakly higher under than under . The increase in the total liquidity follows since the total assets, by definition, equal external assets plus payments. ∎

In fact, the systemic liquidity of even the worst Nash equilibrium can be arbitrarily higher than at the original network. To see this, consider the network in the proof of Theorem 14, which admits a unique Nash equilibrium with arbitrarily higher total liquidity than that of the original network.

Theorem 14.

When default costs apply but there are no cash injections, the Effect of Stability is arbitrarily close to .

Proof.

Consider the network in Figure 12 where default costs are for some arbitrary small positive constant . If no edge is removed, then all banks except are in default and the following payments are realized: and The systemic liquidity is then .

On the other hand, the unique Nash equilibrium is achieved when removes the edge pointing from to itself. The systemic liquidity in this case is , and the proof follows. ∎

We conclude with our results on computational complexity for the setting with default costs.

Theorem 15.

In edge-removal games with default costs, the following problems are NP-hard:

-

a)

Decide whether a Nash equilibrium exists or not.

-

b)

Compute a Nash equilibrium, when it is guaranteed to exist.

-

c)

Compute a best-response strategy.

-

d)

Compute a strategy profile that maximizes systemic liquidity.

Proof.

We begin by proving that the problem of computing a Nash equilibrium (even when its existence is guaranteed) is NP-hard.

Hardness of computing a Nash equilibrium. Our proof follows by a reduction from the Partition problem. Recall that in Partition, an instance consists of a set of positive integers and the question is whether there exists a subset of such that .

The reduction works as follows. Starting from , we build an instance by adding an agent for each element and allocating an external asset of to ; we also include two additional agents and . Each agent has liability equal to to each of and , while has liability to ; see also Figure 13. We furthermore set default costs ; clearly, the reduction requires polynomial-time.

Observe that, in any Nash equilibrium, agent keeps all its incoming edges. Indeed, removing an edge from agent will decrease ’s total assets, as there is no alternative path for payments originating at to reach . Similarly, agent keeps its incoming edge from at any Nash equilibrium, as deleting it will reduce ’s total assets. Therefore, the only strategic choice in this financial networks is by agent about which edges from agents to keep and which to remove. We denote by and the set of agents whose edges towards are kept and removed, respectively, and observe that agents in are in default while agents in are not. Clearly, as is essentially the only strategic agent, any best-response strategy by forms a Nash equilibrium. This guarantees the existence of a Nash equilibrium in . We will show that in instance , agent can compute her best response, and hence we can compute a Nash equilibrium, if and only if instance of Partition is a yes-instance.

We first show that if is a yes-instance for Partition, then agent has total assets . Indeed, consider the subset in with and let contain agents where , while agents with . Note that obtains total assets

and is therefore solvent, while obtains

We will now show that if is a no-instance, then ’s total assets in are strictly less than ; this suffices to prove the claim. Consider any subset in and the corresponding strategy profile in where keeps incoming edges from agents in while removes edges from agents in . Let and observe that, as elements in are integers, it holds either or .

In the first case, when , we claim that is in default. Indeed, collects a total payment of from the agents in and a total payment of from the agents in . So,

i.e., less than ’s liability to ; the first inequality follows by the assumption on . Therefore, can collect from the agents in and strictly less than from . We conclude that in this case.

In the second case, when , obtains a total payment of from agents in and a payment of at most from , i.e., again.

Since in any case, a no-instance for Partition leads to an instance where , the claim follows, as we cannot compute a best-response strategy for , and, by the discussion above, a Nash equilibrium.

Hardness of computing a best-response strategy. The proof was given in the previous case.

Hardness of maximizing systemic liquidity. The proof follows by the reduction from Partition described in the previous case by adding a path of agents as shown in Figure 14. By the discussion above, starting from a yes-instance in Partition, we have , and as well as any agent are solvent. On the contrary, starting from a no-instance for Partition, agent is in default and the payments traveling to the agents get reduced by a factor of at each edge. By selecting to be large enough, the claim follows.

Hardness of deciding the existence of Nash equilibria. Again, the proof follows by the reduction from Partition used in Theorem 15b by adding five agents, and with liabilities and external assets are show in Figure 15. Recall that the default costs are and, without loss of generality, we assume that .

As argued earlier, always keeps all its incoming edges, while always keeps the edge from . Similarly, agents and always keep their incoming edges, as by removing any incoming edge their total assets strictly decrease. As agents and do not have incoming edges, the only strategic agents are (with respect to the edges originating from ) and (with respect to edges from the agents). We first show that, if instance of Partition is a yes-instance, then there is a Nash equilibrium. Indeed, we argued earlier that in this case and, hence, is solvent. So, is solvent as well and, therefore, always keeps the edge from as the liability from is always fully paid. This implies that is necessarily in default and agent should keep the edge from as well. To conclude, the strategy profile where keep all edges is a Nash equilibrium.

On the other hand, when instance is a no-instance, we have shown that is in default. Then, collects a payment of from and is, hence, necessarily in default. When both and keep their edges from , their total assets are and . When removes the edge and keeps it, it is and , i.e., improves compared to the previous case. When they both remove these edges, we have and , i.e., improves compared to the previous case. Similarly, when keeps the edge and removes it, the total assets are and , i.e., improves compared to the previous case. The claim follows by observing that, in the last case, improves by keeping the edge. ∎

5 Conclusions

We considered problems arising in financial networks, when a financial authority wishes to maximize the total liquidity either by injecting cash or by removing debt. We also studied the setting where banks are rational strategic agents that might prefer to forgive some debt if this leads to greater utility, and we analyzed the corresponding games with respect to properties of Nash equilibria. In that context, we also introduced the notion of the Effect of Anarchy (Stability, respectively) that compares the liquidity in the initial network to that of the worst (best, respectively) Nash equilibrium.

Our work leaves some interesting problems unresolved. Given the computational hardness of some of the optimization problems, it makes sense to consider approximation algorithms. From the game-theoretic point of view, one can also consider the problems from a mechanism design angle, i.e., to design incentive-compatible policies where banks weakly prefer to keep all incoming liabilities.

References

- Bertschinger et al. [2020] Nils Bertschinger, Martin Hoefer, and Daniel Schmand. Strategic payments in financial networks. In Proceedings ofthe 11th Conference on Innovations in Theoretical Computer Science (ITCS), pages 46:1–46:16, 2020.

- Demange [2018] Gabrielle Demange. Contagion in financial networks: a threat index. Management Science, 64(2):955–970, 2018.

- Dong et al. [2021] Zhi-Long Dong, Jiming Peng, Fengmin Xu, and Yu-Hong Dai. On some extended mixed integer optimization models of the Eisenberg-Noe model in systemic risk management. International Transactions in Operational Research, 28(6):3014–3037, 2021.

- Egressy and Wattenhofer [2021] Beni Egressy and Roger Wattenhofer. Bailouts in financial networks. arXiv:2106.12315, 2021.

- Eisenberg and Noe [2001] Larry Eisenberg and Thomas H. Noe. Systemic risk in financial systems. Management Science, 47(2):236–249, 2001.

- Gonzalez [1985] Teofilo F. Gonzalez. Clustering to minimize the maximum interclusted distance. Theoretical Computer Science, 38:293–306, 1985.

- Ioannidis et al. [2021] Stavros D. Ioannidis, Bart de Keijzer, and Carmine Ventre. Strong approximations and irrationality in financial networks with financial derivatives. arXiV, abs/2109.06608, 2021.

- Irfan and Ortiz [2018] Mohammad T. Irfan and Luis E. Ortiz. Causal strategic inference in a game-theoretic model of multiplayer networked microfinance markets. ACM Transactions on Economics and Computation, 6(2), 2018.

- Jackson and Pernoud [2020] Matthew O. Jackson and Agathe Pernoud. Credit freezes, equilibrium multiplicity, and optimal bailouts in financial networks. arXiv:2012.12861, 2020.

- Kanellopoulos et al. [2021] Panagiotis Kanellopoulos, Maria Kyropoulou, and Hao Zhou. Financial network games. In Proceedings of the 2nd ACM International Conference on Finance in AI (ICAIF), 2021.

- Papp and Wattenhofer [2020] Pál András Papp and Roger Wattenhofer. Network-aware strategies in financial systems. In Proceedings of the 47th International Colloquium on Automata, Languages, and Programming (ICALP), pages 91:1–91:17, 2020.

- Papp and Wattenhofer [2021] Pál András Papp and Roger Wattenhofer. Default ambiguity: finding the best solution to the clearing problem. In Proceedings of the 17th Conference on Web and Internet Economics (WINE), 2021.

- Rogers and Veraart [2013] Leonard CG Rogers and Luitgard Anna Maria Veraart. Failure and rescue in an interbank network. Management Science, 59(4):882–898, 2013.

- Schuldenzucker and Seuken [2020] Steffen Schuldenzucker and Sven Seuken. Portfolio compression in financial networks: Incentives and systemic risk. In Proceedings of the 21st ACM Conference on Economics and Computation (EC), page 79, 2020.

- Schuldenzucker et al. [2017] Steffen Schuldenzucker, Sven Seuken, and Stefano Battiston. Finding clearing payments in financial networks with credit default swaps is PPAD-complete. In Proceedings of the 8th Innovations in Theoretical Computer Science Conference (ITCS), pages 32:1–32:20, 2017.

- Schuldenzucker et al. [2020] Steffen Schuldenzucker, Sven Seuken, and Stefano Battiston. Default ambiguity: Credit default swaps create new systemic risks in financial networks. Management Science, 66(5):1981–1998, 2020.