MS-0001-1922.65

Convex Surrogate Loss Functions for Contextual Pricing with Transaction Data

Convex Surrogate Loss Functions for Contextual Pricing with Transaction Data

Max Biggs \AFFDarden School of Business, University of Virginia, Charlottesville, VA 22902, \EMAILbiggsm@darden.virginia.edu

We study an off-policy contextual pricing problem where the seller has access to samples of prices that customers were previously offered, whether they purchased at that price, and auxiliary features describing the customer and/or item being sold. This is in contrast to the well-studied setting in which samples of the customer’s valuation (willingness to pay) are observed. In our setting, the observed data is influenced by the previous pricing policy, and we do not know how customers would have responded to alternative prices. We introduce suitable loss functions for this setting that can be directly optimized to find an effective pricing policy with expected revenue guarantees, without the need for estimation of an intermediate demand function. We focus on convex loss functions. This is particularly relevant when linear pricing policies are desired for interpretability reasons, resulting in a tractable convex revenue optimization problem. We propose generalized hinge and quantile pricing loss functions that price at a multiplicative factor of the conditional expected valuation or a particular quantile of the prices which sold, despite the valuation data not being observed. We prove expected revenue bounds for these pricing policies respectively when the valuation distribution is log-concave, and we provide generalization bounds for the finite sample case. Finally, we conduct simulations on both synthetic and real-world data to demonstrate that this approach is competitive with, and in some settings outperforms, state-of-the-art methods in contextual pricing.

Machine learning, Pricing, Revenue Management, Off-Policy Learning

1 Introduction

There is an increasing amount of data being collected and stored on customers and sales histories. This has led to the development of more targeted pricing algorithms, in which firms try to increase revenues by offering customers contextual prices that depend on the attributes of the customer and/or product. There has been interest in utilizing abundant historical, posted-price data on whether each customer purchased a particular item at the price they were offered. As an example, we explore offering customers personalized prices for grocery items, based only on previous transaction data and demographic information from their participation in a loyalty program. Using such observational data can be less costly than running randomized trials (Dubé and Misra 2017), or online algorithms that balance exploration and exploitation over time (Den Boer 2015), either of which can lead to a significant loss of revenue in the short term. Our observational posted-price setting has received less attention than the setting where the seller has access to customer valuation (willingness to pay) samples or distribution information (Mohri and Medina 2014, Dhangwatnotai et al. 2015, Devanur et al. 2016, Medina and Vassilvitskii 2017, Huang et al. 2018, Babaioff et al. 2018, Daskalakis and Zampetakis 2020, Allouah et al. 2021, Beyhaghi et al. 2021). A challenge in the posted-price setting is that we do not observe counterfactual data on whether customers would have purchased if offered different prices, an instance of the fundamental problem of causal inference (Holland 1986). Furthermore, the observed data is influenced by the previous pricing policy, which can make it difficult to estimate how customers will respond to uncommon prices (Shalit et al. 2017).

A popular approach in practice is the predict then optimize, or direct method, whereby an intermediate contextual demand function is estimated to predict the probability of a customer purchasing at a given price, and then optimized to maximize revenue (Chen et al. 2015, Ferreira et al. 2016, Dubé and Misra 2017, Alley et al. 2019, Baardman et al. 2020, Biggs et al. 2021b). In practice, often sellers do not know the functional form of demand, leading to a model selection problem. Although advances in machine learning have introduced new models that can capture the complexities of contextual demand more accurately, these models can result in complex revenue maximization problems. Note that this is a consequence of the choice of the demand model used, rather than the inherent properties of the true demand. For example, although tree ensemble or neural network models can result in accurate demand estimation (Ferreira et al. 2016, Mišic 2017, Chen and Mišić 2021, Feldman et al. 2021), both are highly nonlinear functions of their inputs, resulting in a nonlinear estimated revenue surface when the price is optimized. This holds even when considering simple pricing policies, such as linear functions. Furthermore, it is unclear if there exist bounds on expected revenue from optimizing such complex demand functions.

A more direct approach is to formulate a loss function for the pricing setting and optimize such a loss directly through empirical risk minimization without estimating demand first. At a high level, a loss function provides a way to measure how well a policy performs directly from data. Unlike in typical supervised learning settings, we do not observe the ideal price to charge each customer (their valuation or willingness to pay), which could potentially be considered the labels we are trying to learn. As such, it is not clear how to use the distance from this label as our criteria, as is often done in regression. In the classification setting, a surrogate loss function is often justified through desirable properties of the prediction function that minimizes it, such as Bayes consistency (predict 1 if otherwise, which is the optimal classification policy (Bartlett et al. 2006)). It is less clear how to define and determine desirable properties of a loss function in our posted price setting. We propose convex pricing loss functions where the pricing policy obtained from optimizing the loss function has attractive expected revenue bounds. However, unlike the classification setting, we show that there is no convex loss function that can always find the optimal pricing policy, so there is always some gap in expected revenue.

2 Contributions

We propose loss functions for contextual pricing with observational posted price data, whereby customers are offered a price as a function of the customer and/or product attributes, which address the aforementioned issues.

-

•

Computational efficiency: We propose loss functions that are convex, so they can be optimized in a computationally efficient manner. This is particularly relevant when implementing linear pricing policies, which are often desirable for interpretability and generalizability, as this results in a convex revenue optimization problem. The importance of interpretable pricing is documented in Amram et al. (2020) and Biggs et al. (2021b). Transparency lets sellers understand how the algorithm is pricing items, verify this matches their intuition, and ensure the algorithm satisfies regulatory requirements.

-

•

Characterization of pricing policies: We propose two loss functions for the pricing setting, where the behavior of the pricing policy that results from optimizing the loss function can be characterized and understood. This is in contrast to existing loss functions for pricing where the behavior of the optimal policy is unclear (e.g., Ye et al. (2018)). The first function we propose is a hinge pricing loss function, which shares similarities with the classification hinge loss function but is adapted to the posted-price setting. We show that despite not observing valuation data, the resulting pricing policy prices at the scaled conditional expected value of the valuation distribution. The second is a quantile pricing loss function, which prescribes prices at a chosen quantile of prices at which similar customers purchased. Since both of these approaches are dependent on a scaling parameter, we show how this can be chosen in a robust manner to maximize revenue against an adversarial valuation distribution.

-

•

Expected revenue guarantees: The loss functions we propose have bounds on the expected revenue relative to the optimal revenue achievable from the optimal contextual pricing policy that has access to the customer valuation distribution. Assuming the complementary cumulative distribution function (survival function) of customer valuations is log-concave, we prove revenue bounds of 0.772 for the hinge pricing policy and 0.749 for the quantile pricing policy against an adversarially chosen valuation function. These bounds are stronger than 0.5 bounds proved in Chen et al. (2021) in a setting that is closely related but restricted to uniform historical pricing policies.

-

•

Finite-sample bounds: In addition to the expected performance, we also show generalization bounds for a finite sample of observations for a class of linear policies that satisfies the computational efficiency requirements discussed above.

-

•

Competitive empirical performance: Finally, we provide simulations on both synthetic and real-world data to demonstrate that this approach is competitive with, and in some settings outperforms, state-of-the-art methods in contextual pricing, which may work well in practice but do not have known expected revenue guarantees. In particular, we empirically show that using machine learning functions such as gradient-boosted trees to estimate demand often results in poor pricing policies due to the difficulty of optimizing a non-convex function, while simpler functions such as logistic regression often do not capture the non-linear interactions in demand, resulting in sub-optimal performance relative to the convex surrogates pricing loss functions.

3 Other related literature

A significant body of literature focuses on the online pricing setting, where the seller chooses prices to balance learning and earning over time (Kleinberg and Leighton 2003, Gallego et al. 2006, Feng 2010, Broder and Rusmevichientong 2012, Harrison et al. 2012, Cheung et al. 2017, Besbes et al. 2018, Den Boer and Keskin 2020, Calmon et al. 2021, Keskin et al. 2021). Within this area, there has also been a focus on incorporating contextual data to offer more targeted prices (Javanmard and Nazerzadeh 2016, Qiang and Bayati 2016, Bertsimas and Vayanos 2017, Cohen et al. 2018, Nambiar et al. 2019, Cohen et al. 2020, Ban and Keskin 2020, Zhang et al. 2021, Chen and Gallego 2021, Liu et al. 2021). Of particular relevance are Amin et al. (2014), and Cohen et al. (2020), who study online contextual pricing with access to similar data where they observe whether a sale occurred at the price offered. Amin et al. (2014) study a setting where the customers’ valuations are deterministic (no noise) around an unknown linear function. Cohen et al. (2020) consider a noisy setting where a linear valuation with an unknown mean is perturbed by an error term that has a known distribution. The distribution of the error term is used in optimizing prices. In contrast, we study a noisy setting where the distribution of the error is unknown, but comes from a log-concave distribution. A comprehensive review of earlier work in dynamic pricing can be found in Den Boer (2015). As experimentation can be costly, we focus on a setting where we want to maximize revenue in the short term, using only existing observational data.

An important differentiating feature in the pricing literature is how much information the seller has access to. There is a substantial body of work that focuses on a seller with limited samples of valuation data (Dhangwatnotai et al. 2015, Huang et al. 2018, Babaioff et al. 2018, Daskalakis and Zampetakis 2020, Derakhshan et al. 2020, Allouah et al. 2021), including contextual side information (Mohri and Medina 2014, Devanur et al. 2016, Medina and Vassilvitskii 2017). In the setting with a single valuation sample and no contextual data, assuming the valuation distribution is regular, Dhangwatnotai et al. (2015) prove expected revenue bounds of by setting the next customer’s price equal to the valuation of the first customer. Huang et al. (2018) improve the revenue bound to by pricing at a multiplicative factor of the valuation observed, provided the valuation distribution is log-concave. Daskalakis and Zampetakis (2020) study the case with two samples and prove bounds of for regular distributions, while Allouah et al. (2021) improve to and also provide upper and lower bounds for any number of samples in the regular and log-concave valuation distribution setting, using a dynamic programming approach. Huang et al. (2018) also study a data-rich regime, showing that in order to find a optimal price from valuation data, the sample complexity scales polynomially in .

Algorithms also exist under alternative knowledge about the valuation distribution. Cohen et al. (2015) provide bounds when only the support of the valuation distribution is known; Azar et al. (2013) and Chen et al. (2019) use the mean and variance of the valuation distribution; Elmachtoub et al. (2020) uses the coefficient of deviation of the valuation distribution; Bergemann and Schlag (2011) use a neighborhood containing the true valuation distribution. In contrast to all this work, we have posted-price samples on whether the item sells or not at the price consumers were given, rather than samples or other knowledge of the valuation distribution. Hence, the observed posted-price sales samples are affected by the previous pricing policy, while the valuation samples are not. This needs to be accounted for in any pricing algorithm. Some of this work also focuses on the “value of price discrimination” rather than practical algorithms for pricing that can be solved tractably.

Closest to our work are efforts to formulate contextual pricing loss functions that can be optimized directly to find pricing policies. Mohri and Medina (2014) propose a loss function when setting reserve prices for a second price auction, while assuming valuation samples (the maximum each customer is willing to pay) are available. The surrogate functions they propose are continuous but non-convex, hence still challenging to optimize. Huchette et al. (2020) provide strong Mixed Integer Programming (MIP) formulations for this loss function, which allows the global optimal solution for small problem instances to be found. They also provide linear relaxations. Similar to our setting, Biggs et al. (2021a) propose pricing loss functions for the observational posted-price setting when prices are restricted to a discrete price ladder. Here we focus on continuous prices. In the same setting we study, Ye et al. (2018) propose a customized -insensitive loss, used for contextual pricing at Airbnb, which is related to the functions we study. We further discuss this function in detail in Section 5. Another very related paper is Chen et al. (2021), which offers model-free pricing for assortments. While Chen et al. (2021) do not consider contextual pricing for the single-item case they observe the price that the product is purchased. As such, the setting for their revenue bounds is very similar to ours; these settings are further compared in section 5.3.

A potential approach to pricing using observational data is to use methods from the off-policy learning literature such as inverse propensity scoring (IPS) (Rosenbaum and Rubin 1983, Beygelzimer and Langford 2009, Li et al. 2011). Although IPS methods are typically used when the treatment is binary, there have been extensions to continuous treatments (Austin and Stuart 2015, Kallus and Zhou 2018), which better model pricing. In Kallus and Zhou (2018), the reward is estimated using a weighted average according to how far the given treatment in the historical data is from the proposed policy, as evaluated by a kernel. The approach of Kallus and Zhou (2018), however, leads to non-convex optimization problems for most practical choices of the kernel. There is a recent stream of literature that applies some ideas from off-policy learning to pricing problems with censored demand, which occurs due to a lack of inventory (Ban 2020, Bu et al. 2022, Qi et al. 2022). In contrast, our model doesn’t incorporate inventory effects but focuses on the different setting where the observed purchase outcomes are binary, as may occur in a personalized pricing setting.

4 Model

We study a fundamental contextual pricing problem of a monopolist selling a single product with no inventory constraints. The monopolist wants to set prices based on historical data to maximize sales in the short term. Each customer is described by features and has an unobserved valuation , which is the maximum amount they are willing to pay, both drawn from a joint distribution. The customer is offered the realization of a stochastic price from a historical pricing policy that follows a known conditional distribution with density . This assumption supposes that the practitioners know or have recorded the pricing policy used in the past. One setting where this is likely satisfied is when the firm is already doing algorithmic pricing. We observe whether the customer purchases , depending on whether the price is above or below their valuation. Specifically,

| (1) |

We do not observe the counterfactual outcomes associated with the customer being given a different price from what was assigned by the previous pricing policy, nor do we observe the valuation of each customer. As such, we have access to an i.i.d. dataset of samples . For identifiability (Swaminathan and Joachims 2015), we assume overlap and ignorability.

(Overlap)

(Ignorability)

The overlap assumption requires that each price has a nonzero probability of being offered to each customer. The known impossibility result of counterfactual evaluation also applies when it is not satisfied (Langford et al. 2008). The ignorability assumption requires that there be no hidden confounding variables influencing the pricing decision and the customers’ purchasing decision. It is commonly satisfied as long as the factors that drove historical pricing decisions are available in the observed data (Bertsimas and Kallus 2020). For clarity of exposition, we also assume that all customers have a positive valuation, meaning all customers will purchase if given the product for free, , and that the complementary CDF (survival function) , is log-concave. Recall that a function is log-concave if its domain is a convex set and it satisfies

The log-concavity assumption encompasses a broad range of valuation distributions including commonly used distributions such as normal, exponential, and uniform (Bagnoli and Bergstrom 2005). Furthermore, it is known that if the density function is log-concave, then so is the complementary CDF (Bagnoli and Bergstrom 2005). Log-concavity also implies that the hazard rate is monotone, a common assumption in pricing (Cole and Roughgarden 2015, Huang et al. 2018, Allouah et al. 2021). Without log-concavity, there are simple examples showing that the revenue gap may be unbounded (Cole and Roughgarden 2015).

Our goal is to find a pricing policy, , which prescribes a price for each customer. The expected revenue obtained from a policy conditioned on is:

| (2) |

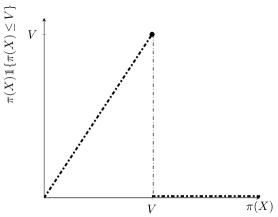

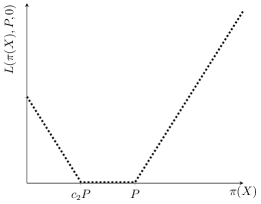

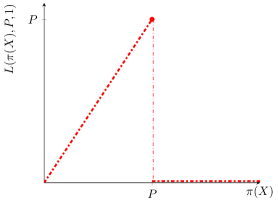

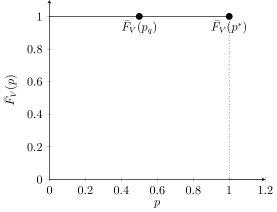

That is, if the price offered is less than the customer’s valuation , the item sells and the revenue obtained is the price offered, while if the price is above the customer’s valuation the revenue is zero. Unfortunately, it is not possible to directly optimize because the distribution of customer valuations is not known and samples are not observed. If valuation samples are observed, a pricing policy could be found by optimizing an empirical version (Mohri and Medina 2014):

This is visualized in Figure 1. However, optimizing this function, which is non-convex and discontinuous, is challenging (Mohri and Medina 2014, Huchette et al. 2020). Instead, we need to find a loss function that provides good prices when optimized using the samples we observe , rather than valuations .

4.1 Convex relaxations

In particular, we aim to find loss functions that are convex, so they can be optimized efficiently, yet still have provable guarantees on expected revenue, relative to the optimal contextual pricing policy which has access to the valuation distribution, , where the dependence on is henceforth omitted for notational clarity. We start by showing an impossibility result, which states that there is no loss function with access only to posted price data that is able to recover the optimal price for all valuation distributions. This Proposition is a minor extension of Theorem 2 of Mohri and Medina (2014), which proves that there is no convex surrogate for which the global minimum price is obtained in the case with access to valuation data. We denote a loss function using observational posted-price data as .

Proposition 4.1

There is no nonconstant function , left continuous in and with convex with respect to its first argument, such that for any distribution on satisfying Equation 1, there exists a nonnegative optimal price , satisfying .

The requirement of left continuity of the expected loss is a minor technical requirement that follows from a left continuity assumption in Mohri and Medina (2014). This impossibility result contrasts with the well-studied classification setting, where there are convex surrogates for the loss that can recover the optimal classification policy, a property known as Bayes consistency or classification calibration (Bartlett et al. 2006). Huchette et al. (2020) also show that optimizing the function is NP-Hard in the setting where valuation samples are available with a linear policy class. For convenience, we provide commonly used notations in Table 1.

| Notation | Description |

|---|---|

| Valuation of the customer (unobserved) | |

| Whether the customer purchased the item | |

| Price posted in the past | |

| Contextual features describing the customer and or product | |

| Conditional historical probability density of a price being offered to a customer | |

| Contextual pricing policy (decision) | |

| Expected conditional revenue | |

| Optimal price | |

| Parameter the seller can set for hinge pricing loss | |

| Parameter the seller can set for quantile pricing loss | |

| Price set by the hinge pricing loss function | |

| Price set by the quantile pricing loss function |

5 Pricing hinge loss function

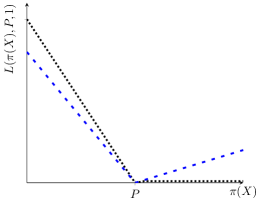

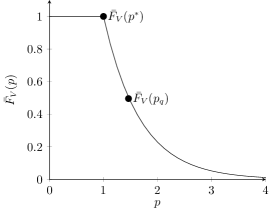

Since it is not possible to find a convex loss function that recovers the optimal pricing policy, we focus on loss functions that are capable of achieving a high proportion of the optimal revenue. We propose the hinge pricing loss function, which has similarities to the hinge loss function used for classification tasks. This loss function is defined in Definition 5.1 and visualized in Figure 2.

Definition 5.1

The hinge pricing loss function is given by

Where is a parameter chosen by the seller, which we will discuss how to choose later in this section. When , this loss function penalizes prices that are below the listed price when the item was sold and penalizes prices that are above the listed price when the item wasn’t sold, giving the loss function the characteristic “hinge” shape. This is reasonable since if an item sold, the customer’s valuation is likely higher than the listed price, so pricing above the listed price is more attractive. Conversely, if an item did not sell, then the customer’s valuation is likely below the listed price, so pricing below this price should be encouraged. The parameter controls how aggressive the pricing policy is. For , when the item sells, there is a reduced penalty for pricing below the sale price and even a small penalty for pricing above the sale price. The penalty remains the same for pricing above the price offered when there is no sale, as shown in Figure 2.

Similar to inverse propensity scoring methods (Rosenbaum and Rubin 1983), each observation is scaled by a weight that is inversely proportional to the probability of receiving the price, , to counteract the imbalance due to the historical pricing policy. In practice, a pricing policy from a sample can be found using empirical loss minimization, which is further discussed in Section 9:

5.1 Comparison with Ye et al. (2018)

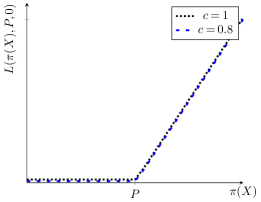

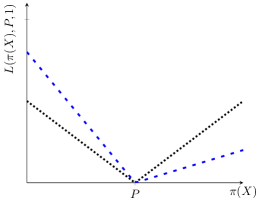

The hinge pricing loss shares a similar motivation to the loss function from Ye et al. (2018), and in certain settings for extreme parameter choices, the loss functions are the same. Ye et al. (2018) proposes a customized -insensitive loss used for contextual pricing at Airbnb:

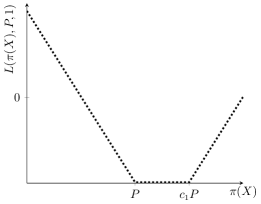

This loss function is shown in Figure 3. Similar to the pricing hinge loss, this captures the intuition that if the item sold, then the customer’s valuation is likely higher than the price the customer was offered, and the future price offered should be raised. However, the loss function from Ye et al. (2018) additionally introduces the idea that the price shouldn’t be raised too much, since eventually the customer will not purchase if the price gets too high. This is reflected in the function where there is no loss between and , but an increasing loss incurred above , where . This gives the loss function a characteristic “U” shape (the authors highlight the similarity with -insensitive regression), compared to the hinge shape of the loss function we propose. Likewise, for the items that don’t sell, both loss functions incur a loss for pricing above the listed price at which no sale occurred, pressuring the price downward. However, the loss function from Ye et al. (2018) additionally incurs a loss for prices that are below , where . The intuition is that if the price is far below the customers’ valuation, there will be potentially unrealized revenue.

While this approach from Ye et al. (2018) is intuitive and has been shown to perform well in practice, there are no guarantees on what the expected revenue is for the resulting policy. Furthermore, the behavior of the pricing policy is unclear, as the policy obtained by optimizing this loss function is not characterized. Finally, there is little theoretical justification for the choices on and , which are left to the user to choose. Due to these drawbacks, it is unclear whether the additional arms that differentiate the Ye et al. (2018) loss and hinge loss are justified.

Another key distinction is that the loss from Ye et al. (2018) does not take into account the historical pricing policy, whereas the hinge loss divides by the propensity score to counteract the imbalance. As such, unless the historical pricing policy is uniform (such as would arise from a randomized trial), this is likely to affect the perfromance of this policy.

However, due to the similarities between the two loss functions, we are able to provide revenue guarantees for the loss function from Ye et al. (2018), for a restricted class of settings. In particular, when the parameters in Ye et al. (2018) are set to and , and the historical pricing policy is uniform, then the loss proposed in Ye et al. (2018) is the same as the hinge pricing loss function for . In this case, our bounds and insights apply to Ye et al. (2018).

5.2 Characterization of the pricing policy

We can characterize the behavior of the policy that results from using the hinge pricing loss function. When we minimize the conditional expectation of this loss function, we end up pricing at the conditional expected valuation for each customer, scaled by a parameter , despite not observing the valuation data. This is proved in Lemma 5.2. As mentioned previously, the parameter controls how aggressive the pricing policy is, with resulting in prices less than the expected valuation and resulting in prices above the expected valuation. We focus on , as this results in stronger revenue bounds. We provide guidance on how to choose robustly following our analysis. If we condition on and for notational simplicity denote , we can prove Lemma 5.2.

Lemma 5.2

(Hinge pricing loss optimality condition): Let be the minimizer of the hinge pricing loss function, then

Proof 5.3

Proof of Lemma 5.2:

Applying the Leibniz rule to find the optimality conditions:

Where the third equality follows since from Equation 1. Therefore, at optimality. \Halmos

This simple result is important since it provides clarity about the behavior of the pricing policy that results from minimizing the pricing hinge loss function. This is not clear in previous loss functions used for pricing, such as Ye et al. (2018). We also note that this is a different minimizer than that of the standard hinge loss function used in binary classification, which predicts 1 if and if (Bartlett et al. 2006).

This result implicitly assumes that there are no model misspecification issues that may prevent this minimizer from being reached. In this respect, the result is similar to Bayes consistency, which depends on the underlying distributions rather than model-specific bounds for the policy class considered. Model-specific bounds are studied for the case of linear policies in Section 9. In the next section, we will show the expected revenue bounds that can be achieved by following this pricing policy.

5.3 Expected revenue bounds

For the expected hinge pricing policy, we can find bounds on the optimal expected revenue, relative to the best pricing policy that has access to the conditional valuation distribution and solves . Furthermore, these bounds are robust in the sense that this holds across all valuation distributions that satisfy the log-concave assumption, including an adversarially chosen distribution. Note these bounds hold in expectation and do not address what happens for a finite sample or a particular policy class, which is addressed in Section 9.

Theorem 5.4

For :

To prove this bound we need to examine two cases: the case where the prescribed price is below the optimal price for the adversarial distribution (), and the case where it is above (). Which case is relevant depends on the chosen parameter of . If a lower value of is chosen (i.e., much below the expected valuation), the adversary will choose a valuation distribution where , which is characterized by many high-valued customers that the lower price doesn’t fully exploit. Conversely, if a higher value of is chosen, the adversary will choose a distribution where , which will be characterized by a long tail where the selling probability at is low, relative to a significantly higher selling probability at the slightly lower price . This is explored more in Section 7, and the worst-case valuation distributions are characterized in Figure 7. We prove Lemmas that give revenue bounds in each case, and prove they are tight. We start with the case where .

Lemma 5.5

Consider a pricing policy that prescribes a price such that and , then:

The proof can be found in Appendix 12 and follows from manipulations of log-concave distributions. We note that the condition in Lemma 5.5, , is satisfied by the optimality conditions for the hinge pricing loss function with equality. While the bound is relatively opaque, it simplifies significantly for lower values of . In this case, the hinge pricing policy receives a constant fraction of the revenue.

Corollary 5.6

for

The proof is in Appendix 12. For , the adversarial distribution is simple and puts a point mass at , so and the hinge price gets a fraction of the revenue. This distribution is shown in Figure 7c. The worst-case distribution is more involved for .

We prove an expected revenue bound for the case where the prescribed price is greater than the optimal price in Lemma 5.7.

Lemma 5.7

If there exists a pricing rule satisfying optimality conditions from Lemma 5.2 and , then:

| (3) |

An important special case of this occurs when when the hinge pricing function prices at the conditional expected valuation . In this case, the bound from Lemma 5.7 simplifies significantly.

Corollary 5.8

for .

Lemma 5.7 is a generalization of Lemma 5.4 in Lovász and Vempala (2007), who proved a similar result for the case when . Furthermore, the case where is also an application of Grünbaum’s Theorem (Grünbaum 1960). We also note that for , a closed-form solution can also be found for the minimizer of the bound.

Corollary 5.9

For ,

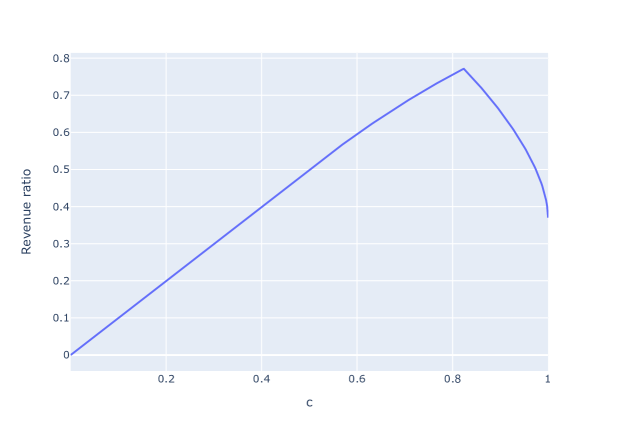

Theorem 5.4 follows from applying the optimality conditions in Lemma 5.2, and combining the worst-case from bounds in Lemma 5.5 and 5.7. These expressions are difficult to evaluate, but it is possible to do so using simulation. It can be shown that for the range , . Furthermore, for , and . As a result, the bound is never the minimum for any value for , leading to its exclusion in the bound presented in Theorem 5.4. Furthermore, simulated evaluation of the expressions in Theorem 5.4 leads to the following characterization of the worst-case revenue:

Corollary 5.10

, which occurs at .

These bounds can be compared to the bounds in Chen et al. (2021), who study a similar setting. In their single item setting, Chen et al. (2021) study pricing from transaction data with observations of the price of purchases. In the more restricted case of a uniform historical pricing policy, they are able to show that their pricing policy achieves a 0.5 fraction of the optimal revenue, under a similar but not identical assumption on the failure rate of the valuation distribution. The comparison with Chen et al. (2021) is explored in more detail in Section 6.1, as their approach relates closely to the next loss function we propose.

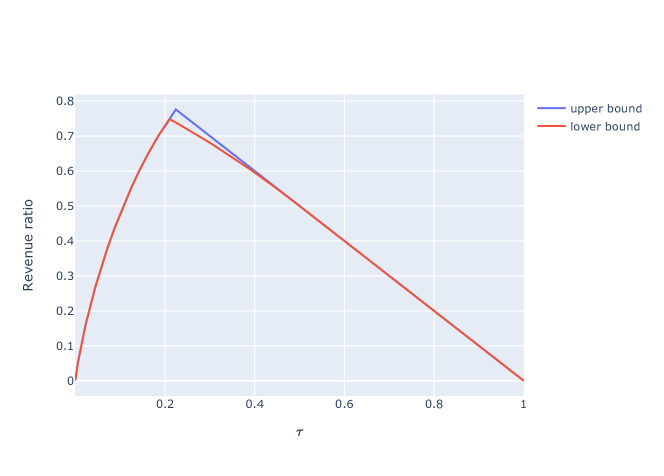

This result provides the pricing practitioner with guidance on how to select in a robust manner by balancing the risk that the valuation distribution is concentrated at high or low values. In particular, this suggests pricing at , which is the point at which the two bounds are equal and the adversary is ambivalent about choosing a distribution with an optimal price above or below . The revenue bounds as a function of are shown in Figure 4. We note that the revenue bounds decrease more rapidly when rather than if , which suggests selecting above this point might be a riskier choice. We also note that the decrease in revenue for is approximately linear, which is an extension of Corollary 5.6. The fact that the optimal parameter is less than 1 captures the intuition that it is better to price below the customer’s expected valuation than above it. Indeed, if the price is above the customer’s valuation, there will not be a sale and no revenue will be gained, whereas if the price is below the customer’s valuation, there will still be a sale and some revenue gained, albeit less than could optimally be achieved.

The hinge pricing loss can also be used to adapt the results from Medina and Vassilvitskii (2017) to this setting. Medina and Vassilvitskii (2017) provide pricing algorithms based on access to an estimate of the valuation, such as that obtained by regressing on valuation samples. Lemma 5.2 shows that using the hinge pricing loss function, for example using , will provide an estimate of the expected value of the valuation distribution that can be used in their algorithm. However, their approach is based on forming clusters of customers with similar valuations and setting a price for each, so it does not result in the interpretable linear policies we desire.

6 Quantile pricing loss function

We also propose an alternative loss function that is able to achieve similar, albeit slightly lower, worst-case pricing bounds but outperforms the pricing hinge loss in some experimental situations. Furthermore, it can be used in settings where the no-purchase decision is not observed, which is often the case with transaction data (e.g., Chen et al. (2021)). The quantile loss is visualized in Figure 5.

Definition 6.1

The quantile pricing loss function is given by

This can be considered as a weighted quantile loss function for price, using only data for which the product sold. As such, when this loss function is minimized, prices are prescribed at a given quantile of the historical prices of items that sold. The quantile priced at depends on , and the strategies for picking a suitable for pricing are discussed later in this section. While to the best of our knowledge, this loss function is not currently used in practice, it does bear resemblance to some commonly used ad hoc contextual pricing strategies, whereby the price is set to be close to similar products that have recently sold. If the product doesn’t sell, there is no contribution to the loss. Similar to the hinge pricing loss, the quantile pricing loss is weighted by a weight inversely proportional to the probability of the product receiving each price , to counteract the imbalance due to the historical pricing policy.

6.1 Comparison with Chen et al. (2021)

The quantile loss has similarities to the loss function from Chen et al. (2021). While Chen et al. (2021) focuses on multi-product assortments and does not focus on convexity or contextual information, they study a similar problem setting of pricing from transaction data with observations of the price of purchases. In particular, for the single product setting, they propose maximizing the following function to obtain a pricing policy:111Since Chen et al. (2021) do not study contextual setting, there is no dependence on for the pricing policy , which we introduce. We also note that Figure 6 assumes the historical pricing policy is uniform.

This is visualized in Figures 6a and 6b. The rationale is that if the customer purchased at price , they will purchase at any price below , but Chen et al. (2021) take a conservative approach and assume there will be no sale above . They study a setting with transaction data where only purchases are observed, but not no-purchase outcomes. As such, they implicitly assume there is no contribution from the no-purchase decisions as shown in Figure 6b.

The loss function from Chen et al. (2021) can be transformed from a maximization to a minimization through multiplication by -1, and translated by a constant , to result in the loss function in Figure 6e. Neither of these transformations will affect the minimizer of the function. It is clear that this loss function is non-convex, and therefore potentially difficult to optimize in the contextual setting. The quantile pricing loss function can be thought of as a convex relaxation of this function, in the sense that rather than having a discontinuity at , there is a linear penalty associated with increasing the price above this price, as shown in Figure 6e. This maintains the convexity of the loss function. This relaxation does not assume all revenue is lost above , so it can be considered less conservative than Chen et al. (2021), although this also depends on the choice of . In addition, the loss function in Chen et al. (2021) does not adjust for the historical pricing policy, and as such, revenue guarantees are only able to be obtained only for the case of uniform pricing policies.

6.2 Comparison with Inverse Propensity Scoring

We also note the similarity between the quantile loss and an Inverse Propensity Scoring (IPS) approach (Rosenbaum and Rubin 1983, Beygelzimer and Langford 2009, Li et al. 2011). In a setting where the price is discrete, the IPS estimator is:

Here there is a contribution to the reward proportional to only if the proposed price is equal to the price that was given to the customer in the observed data. Thus the reward obtained from a customer can be considered as a point mass at . This is shown in Figures 6c and 6d. Similarly, this can be transformed by multiplying by -1, and shifting by as shown in Figure 6e. We note that rather than having a point mass, the quantile reward function has a linear penalty for prices above or below the point .

6.3 Characterization of the pricing policy

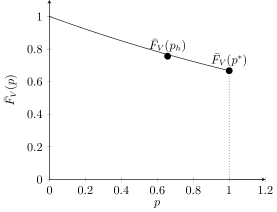

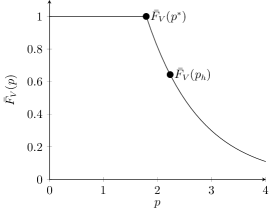

We can characterize the pricing policy that results from minimizing the expected conditional quantile pricing loss function in Lemma 6.2. This shows that when this loss function is optimized, the price is set such that there is a fixed ratio between the total area under the valuation complementary CDF and the area below the complementary CDF and to the left of the price. This is useful for proving revenue bounds, since the total area under the complementary CDF is the maximum expected revenue achievable from a clairvoyant seller who knows the customers’ valuations exactly in advance. As we will show, pricing using the quantile pricing loss function ensures we get a constant fraction of this revenue. If we condition on and for notational simplicity denote we can prove Lemma 6.2.

Lemma 6.2

(Quantile optimality condition): Let be the minimizer of the expected quantile pricing loss function, then

Proof 6.3

Lemma 6.2:

Where the second equality follows since from Equation 1. Applying the first-order optimality condition, and the Leibniz integral rule:

| (4) | ||||

| (5) | ||||

| (6) |

It is also important to differentiate this from the standard quantile loss function applied to the (unobserved) valuation data. If we applied quantile regression here, we would get an estimator of the fraction of the area under the valuation PDF, , resulting in a policy where . As a result, this pricing policy is clearly different.

6.4 Expected revenue bounds

When we optimize the quantile pricing loss function, we can find bounds on the optimal revenue, relative to the best contextual pricing policy that has access to the valuation distribution.

Theorem 6.4

Similar to the hinge pricing loss function, the proof for Theorem 6.4 requires exploring two cases, one where the price chosen by minimizing the quantile pricing loss is above the optimal price and one where it is below. We start by bounding the case where the price obtained by minimizing the quantile pricing loss function is greater than the optimal price.

Lemma 6.5

If there exists a pricing rule satisfying optimality conditions from Lemma 6.2 and , then:

This again follows nontrivially from the properties of log-concavity and is proven in Appendix 12. To help parse this bound, it can be lower bounded by the following function with only a minor loss of accuracy.

Corollary 6.6

This bound helps understand the relationship with the parameter and clearly shows that increasing from 0 toward 0.5 improves the bound. Furthermore, it can be observed from Figure 8, which visualizes the revenue bound, this bound is well approximated by a quadratic.

For the case where , we can apply the bound from Lemma 5.5 again. Lemma 5.5 shows that a constant fraction of revenue can be achieved under a condition where the price prescribed is at least a fixed constant of the revenue achievable by a clairvoyant, . We show that the optimality condition for the quantile loss function implies this condition.

Corollary 6.7

If there exists a pricing rule satisfying optimality conditions from Lemma 6.2 and

Proof 6.8

As a result, a version of Corollary 5.6 also holds for the quantile pricing loss function, whereby the revenue ratio can be very simply lower bounded by for the range . As shown in Section 7, this bound is actually tight.

Corollary 6.9

for

Theorem 6.4 follows from combining the bounds in Lemma 6.5 and Corollary 6.7. Similar to the hinge pricing loss, the bound from Theorem 6.4 is difficult to simplify further. However, since Theorem 6.4 only has parameters , , , it is possible to find the best revenue bound across all valuation distributions with simulation:

Corollary 6.10

, which occurs at .

This gives practical guidance on how to choose . In particular, with the best worst-case guarantee corresponds to setting the price to approximately the percentile of the items that sold. The complete relationship between the revenue bounds and is shown in Figure 8, which gives practitioners an idea of the worst-case revenue for different choices of .

While this bound is marginally weaker than the bound for the hinge pricing loss function, it is applicable in the setting where only sale outcomes are observed. In this respect, the bound for the quantile pricing loss is perhaps more directly comparable with the 0.5 bound from Chen et al. (2021) than the hinge pricing loss.

7 Tightness of bounds

In this section, we examine the tightness of the bounds from Sections 5.3 and 6.4. This is achieved by finding valuation distributions that obtain the revenue given by the bounds. Since the worst-case distribution is different for different pricing rules, these distributions are parameterized by and respectively. Figure 7 illustrates the worst-case distributions.

Lemma 7.1

As a corollary of Lemma 7.1, the bounds for the hinge pricing loss function given in Theorem 5.4 are tight, while those for the quantile pricing loss function given in Theorem 6.4 are very close to being tight. This occurs because the revenue bounds from Lemma 5.5 are satisfied by the distribution from Figure 7c for the range , but not for . As a result, it is unclear whether there exists an alternative valuation distribution that satisfies the bound for the range , or whether it is possible to improve the bound for this range. The relative difference between the upper bound given by the distribution in Figure 7c and the lower bound from Lemma 5.5 is shown in Figure 8. We note that the difference is at most , so the bound is very close to being tight. More practically, there is minimal effect on the optimal choice for a robust . For the hinge pricing loss, there are no such issues, as valuation distributions can be found that satisfy bounds from Lemma 5.5 and 5.7 and cover the range of .

The worst-case distributions from Figure 8 also provide practical insight into the difficulties in choosing a parameter or . If is chosen to be small so that the price is a small fraction of the expected valuation, then the worst-case valuation distribution is similar to Figure 7a but perhaps more easily understood from Figure 7c (when c¡0.5, this is the worst case bound for the hinge loss too). In this case, most customers have a valuation close to the expected value, which is approximately equal to the optimal price . This results in a complementary CDF that is relatively flat (most customers will purchase at prices below the optimal price), followed by a sharp drop as no customers will purchase above the optimal price. From this example, it is clear why the hinge pricing loss gets close to a fraction of optimal revenue. However, as increases, the worst-case distribution changes to one where . In this alternative regime where is larger, the worst-case valuation distribution is similar to Figure 7b wherein the selling probability rapidly (exponentially) declines after the optimal price. However, since the is a fraction of the expected valuation, there must be some customers with a higher valuation. Combined with the log-concavity assumption, which limits how quickly the selling probability changes, this prevents from being too low, so it is still possible to achieve a fraction of the optimal revenue. The behavior for the quantile pricing loss is similar and shown in Figures 7c and 7d.

8 Cross-validation for parameter selection

The parameters and can be chosen to robustly maximize revenue across all valuation distributions, as per Corollary 5.10 or 6.10. However, this is often too conservative in practice. We can utilize the pricing practitioner’s partial knowledge of the valuation distribution or demand to set these parameters. We present a simple heuristic for choosing and for the specific valuation distribution encountered, based on ideas from cross-validation. To evaluate the effectiveness of the model parameters, we propose using a demand model estimated from the available data. Specifically, for each parameter value in a discretized set of size , we find an optimal policy by optimizing the corresponding hinge or quantile loss function. We then estimate the revenue obtained from this pricing policy using the estimated demand model and pick the parameter that corresponds to the highest estimated revenue. This approach allows us to utilize an accurate nonparametric demand model (such as a tree ensemble or neural network), without being concerned about the difficulty of optimizing such a non-convex model.

9 Linear policies and generalization bounds

An important class of pricing policies is the class of linear functions, where . This class of functions is valued for its simplicity and interpretability and is well-studied in the pricing literature (e.g., Besbes and Zeevi 2015). Also, when using a linear policy class, the empirical risk minimization problem of finding the best policy by optimizing the hinge and quantile pricing loss functions is convex. This is not necessarily true for nonlinear policy classes.

The bounds introduced in previous sections apply when optimizing the expected loss function which is often not possible in practice. It is of interest to study how the solution will generalize when it is optimized using a finite sample of data to form generalization bounds. To achieve these bounds, we use regularized loss minimization, in which we jointly minimize the empirical risk and a regularization function that penalizes large values of .

Generalization bounds are well studied for regularized convex loss functions that are -Lipshitz (e.g., Shalev-Shwartz and Ben-David 2014). In Lemma 9.1 we show that the quantile and hinge pricing loss functions are -Lipshitz. For these results, we will assume that the price range is bounded, , so that the historical probability of assigning a price can be bounded away from 0 by a constant.

Lemma 9.1

Assume there exists for all , . Then and are -Lipshitz, with .

This simple result follows from taking the maximum absolute gradient of each loss function. This allows us to apply known generalization bounds to this setting. First, denote .

Lemma 9.2

For either or , let . For any training set of size ,

In particular, if , and , then .

The result follows from Corollary 13.9 in Shalev-Shwartz and Ben-David (2014). An advantage of this bound is that it doesn’t explicitly depend on the dimension of the covariate space , although there is a dependence on since we require . Therefore, it is still possible to get good bounds when the covariate space is high-dimensional yet sparse. This bound suggests that a large sample size is needed for small , which occurs when there are some prices that have a very low probability of being assigned . This happens when the pricing policy is unbalanced. This unbalanced data issue is well known in the off-policy learning community and affects inverse propensity weighting methods because to account for observations at uncommon prices, large weights must be used, leading to high variance estimates. Approaches including normalization via re-weighting (Lunceford and Davidian 2004, Austin and Stuart 2015) and trimming of the weights to reduce the variance of the estimates (Elliott 2008, Ionides 2008) have been shown to help mitigate this problem. It is also possible to apply generalization bounds to nonlinear function classes, although this may result in a non-convex revenue optimization problem, which may be challenging to solve.

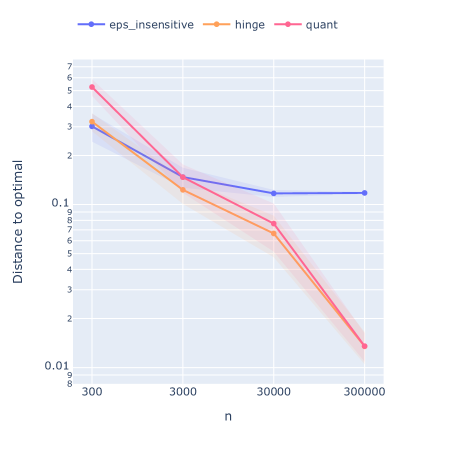

10 Numerical experiments

We test the proposed loss functions using synthetic and real-world datasets. We benchmark against commonly used direct method approaches that first estimate demand using logistic regression (dm_log, e.g., Chen et al. 2015) and a tree ensemble model (dm_lgbm, e.g., Mišic 2017), then optimize estimated revenue to find a pricing policy. In particular, we adopt the logistic regression model implemented in sci-kit learn (Pedregosa et al. 2011), and the lightgbm gradient boosted tree package (Ke et al. 2017) with default parameters in each case. We also benchmark against an Inverse Propensity Weighting approach (kern_ipw) adapted to the continuous action setting (Kallus and Zhou 2018), whereby revenue is estimated using a weighted average according to how far the historical price is from the proposed policy as evaluated by a kernel. We use a Gaussian kernel with a 0.2 bandwidth, a value that worked well in our setting. We benchmark against the model-free assortment approach from Section 6.1 (Chen et al. 2021, model_free) and the -insensitive regression approach from Section 5.1 (Ye et al. 2018, eps_insensitive). The hinge and quantile pricing loss functions (denoted hinge and quant respectively) are optimized using the cross-validation technique from Section 8 to find the parameters ( and ), with 10 rounds of cross-validation. We use the lightgbm model to evaluate the reward in this procedure. Likewise, to find the parameters and for eps_insensitive, we use the same cross-validation procedure. In all experiments, we restrict the pricing policy to be a linear function of the covariates with no intercept term. In all algorithms, the optimal policy is found using the popular BFGS nonlinear optimization algorithm (Nocedal and Wright 2006), implemented in scipy (Virtanen et al. 2020). This can handle non-differentiable demand functions such as tree-based ensemble methods.

10.1 Synthetic data

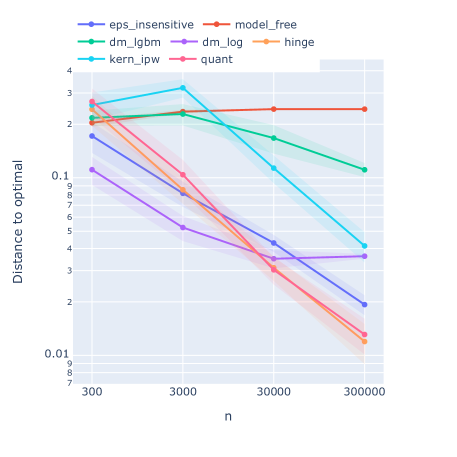

Synthetic experiments are important in this setting due to the lack of publicly available pricing data with counterfactual outcomes on whether a customer would have purchased if a different price had been offered. As a result, estimating the revenue of different pricing policies from historical data is challenging. However, with synthetic data, the underlying probability distributions that govern customer behavior are known, so pricing policies can be evaluated.

In our synthetic experiments, we propose a number of different data-generating scenarios to test the algorithms under varied demand settings. In one set of experiments, the valuation distribution is uniformly distributed. The average valuation depends on the customer features through a function , such that , , and where the historical pricing policy is uniform . We study a linear function and a step function, , where . As described in Section 4, we do not observe , but only as generated by Equation 1, depending on whether the valuation is greater than the price offered. In another set of experiments, we generate valuations according to a shifted exponential distribution , with , also with the linear and step dependence on .

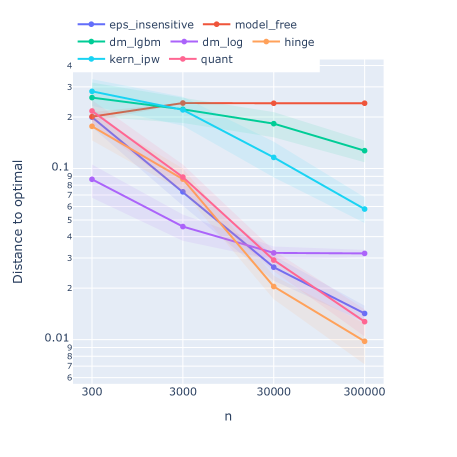

We compare the pricing policies generated to the optimal policy in each scenario, found by minimizing the valuation loss function (Equation 2), although this valuation data isn’t available to the other algorithms. We report the distance from the proposed pricing policy to the optimal solution , . We vary the dataset size . To initialize the BFGS optimizer, we use an initial solution , for . We repeat each simulation 20 times and report the average with plus/minus one standard error, shown shaded in Figure 9.

10.1.1 Discussion:

We observe that the hinge and quantile pricing loss functions are competitive with and in some cases, outperform state-of-the-art benchmarks. In general, for larger datasets or skewed valuation distributions, the convex pricing loss functions (quant, hinge, eps_insensitive) tend to perform best. While there is little to differentiate the convex pricing loss functions when the historical pricing policy is uniform, we show in the next section that the eps_insensitive approach from Ye et al. (2018) can perform poorly when the historical pricing policy is imbalanced.

For small datasets with uniform valuation distributions, the logistic regression direct method performs well. This is potentially due to the low model complexity of logistic regression, which can have lower variance than more complex estimators such as gradient-boosted trees. While not convex, the estimated logistic regression revenue function is quasi-convex, and empirically the BFGS optimizer is often able to find a price close to the optimal. This is not the case for the boosted tree or kernel models, which are in general highly nonlinear and are unable to find good prices with small data samples. We note that none of the approaches we benchmark against except eps_insensitive result in a convex policy optimization problem, so it is possible that any approach could get stuck at a local minimum, an issue that the hinge and quantile pricing loss functions do not have.

For larger datasets , we observe that the kernel IPW and gradient-boosted tree methods both improve, while the logistic regression does not improve as much. This is likely due to the relatively larger bias of the logistic regression approach, which doesn’t decrease with the sample size. Even in the linear setting, the logistic function is not able to exactly model the uniform or exponential complementary CDF. We empirically observe that it seems like the logistic function can better approximate the uniform CDF than the exponential CDF, which is more asymmetrical. Furthermore, as the number of samples increases, we empirically observe that the demand of the kernel IPW becomes smoother, so the optimizer is more likely to find a good solution.

The convex pricing loss functions (quant, hinge, eps_insensitive) often find the best prices for larger datasets. We hypothesize that this is because the gradient-boosted tree model used in the cross-validation becomes more accurate with more samples. However, we also observe that the hinge and quantile pricing models tend to choose better policies than the boosted tree model itself. This is likely because optimizing the boosted tree is very challenging due to non-convexity, whereas for each parameter instance in the cross-validation, the hinge and quantile regressions are convex. Furthermore, we emphasize that the hinge and quantile pricing loss algorithms have guarantees on expected revenue, whereas the algorithms we benchmark against do not.

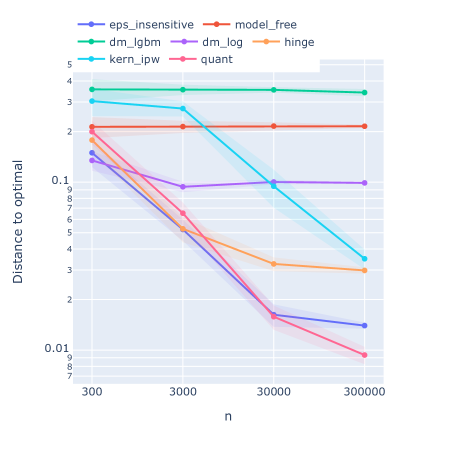

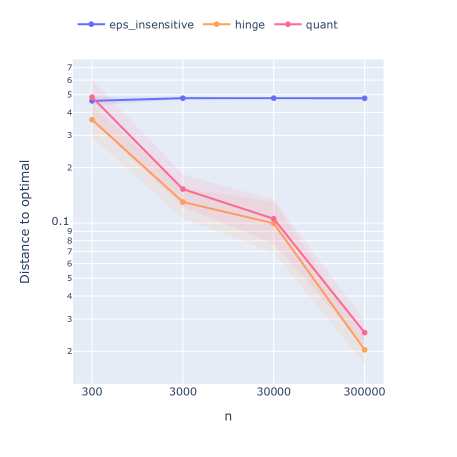

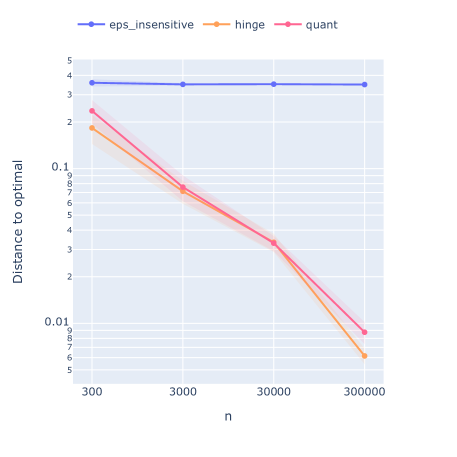

10.2 Imbalanced historical pricing policies

To better understand the difference between the eps_insensitive approach from Ye et al. (2018) and the hinge/quantile loss functions, we ran some additional experiments with an unbalanced historical pricing policy. Historical pricing policies that are not uniform are common in practice where firms are targeting prices to customers to maximize revenue. We repeated the experiments from Section 10.1, focusing on the convex pricing loss functions that performed similarly when the historical pricing policy is uniform. For the experiments with a uniform valuation distribution, we update the historical pricing policy to a policy that is skewed toward high prices, , where the parameters are (lowest value, mode, highest value). For experiments with an exponential valuation distribution, we use , which is skewed towards lower prices. We observe the results in Figure 10.

We observe that the eps_insensitive approach from Ye et al. (2018) performs significantly worse than the hinge or quantile pricing loss functions when the historical pricing policy is not balanced. In particular, in Figures 10c and 10d when the valuation and historical pricing policies are both exponential, eps_insensitive is badly biased and the pricing policy does not improve with sample size. This difference is at least partially due to the propensity score adjustments that the hinge and quantile pricing policies use.

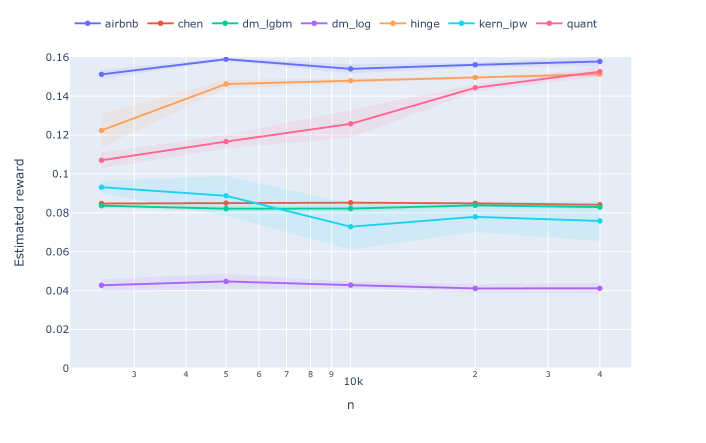

10.3 Case study: personalized prices for groceries

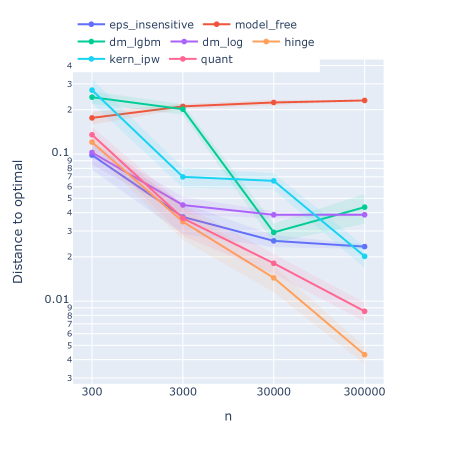

We also test the proposed approaches on a real-world dataset involving personalized pricing for grocery products. The data we have tracks individual customers and whether they purchased strawberries from a chain of grocery stores at the posted price. In addition, demographic data is collected on the individual customers based on enrollment in a loyalty program, specifically, income, age, gender, marital status, home ownership, size of household, and whether the customer has children. Using this data, Amram et al. (2020) and Biggs et al. (2021b) have studied the potential of offering personalized prices to customers based on these features to maximize revenue, using interpretable tree-based models. This data was originally collected by the analytics firm Dunnhumby, and we use the cleaned and processed version of the data from Amram et al. (2020), who provide a detailed description of the data. The data size is rows, corresponding to unique customer trips to the supermarket, with of trips resulting in a sale of strawberries. Once the features described above have been one-hot encoded, it results in a dataset with dimension . Unlike the setting studied in this paper, the historical pricing policy is not known. However, based on the available data, a distribution of historical prices offered is estimated using a log-normal distribution. This pricing policy has no dependence on customer features since the grocery is not currently using personalized pricing.

To evaluate the pricing policies, we use the approach used in Biggs et al. (2021b). Specifically, since the data doesn’t show the counterfactual sales outcomes associated with different pricing policies, we used a model-based approach to estimate the contextual selling probabilities. These probabilities are estimated using a model trained on a held-out dataset, to avoid bias due to a finite data sample. To achieve this, the data is initially split into a prescription dataset and an evaluation dataset. All models used to prescribe prices (including estimating demand if necessary) are trained on the prescription set. A predictive model is trained on the evaluation dataset, which can estimate the revenue of any given pricing policy. Following Biggs et al. (2021b), we use a lightgbm boosted tree model, as the evaluator model as it had the highest out-of-sample accuracy of the methods we tested (81% AUC, compared 71% for logistic regression).

In Figure 11, we show the estimated revenue of different policies, as evaluated by the out-of-sample lightgbm model. We repeat the experiment 10 times for each prescription dataset of size . The remaining data is used as the evaluation set. The standard error of the average reward is shown in the shaded area. We omitted 2 trials where the dm_lgbm and kern_IPW did not converge to a solution.

We observe that the convex pricing loss functions perform better than the other benchmarks on this dataset. In particular, eps_insensitive pricing loss function performs the best across all dataset sizes, with the hinge and quantile pricing loss functions improving to comparable performance for larger datasets. This suggests there are practical advantages to the loss function from Ye et al. (2018), and further understanding the theoretical revenue guarantees for this function is a worthwhile avenue for future work. Interestingly, we observe that the eps_insensitive, hinge, and quantile pricing loss functions outperform the dm_lgbm method, even though the lightgbm model is used to evaluate the estimated revenue. As in the synthetic experiments, this is likely due to the difficulty of optimizing the highly nonlinear estimated revenue curve produced by the boosted tree and is also perhaps why there is no significant improvement as the data size increases. The kernel IPW function has a very high variance and is unreliable, while the logistic regression model does not perform well, possibly due to its inability to capture nonlinear relationships between covariates in the data.

11 Conclusion

We have proposed methods to address the problem of contextual pricing using observational posted-price data rather than the well-studied setting where willingness to pay (valuation) data is available. We have focused on pricing algorithms that can achieve bounds on expected revenue and can also be computed tractably. In particular, we have proposed two loss functions, the quantile and hinge pricing loss functions, which are convex and can be easily optimized. We have also shown how to choose the relevant parameters to optimize bounds on expected revenue according to an adversarially chosen valuation distribution, and how to heuristically choose parameter values when the seller has access to an estimated demand model that is accurate but challenging to optimize, such as a neural network or tree ensemble. Using both real-world and synthetic data, we have shown that the proposed loss functions are competitive against commonly used contextual pricing approaches, which are known to work well in practice, but do not have theoretical expected revenue bounds and may be unpredictable due to non-convexity.

References

- Alley et al. (2019) Alley M, Biggs M, Hariss R, Herrmann C, Li M, Perakis G (2019) Pricing for heterogeneous products: Analytics for ticket reselling. Available at SSRN 3360622 .

- Allouah et al. (2021) Allouah A, Bahamou A, Besbes O (2021) Revenue maximization from finite samples. Proceedings of the 22nd ACM Conference on Economics and Computation, 51–51.

- Amin et al. (2014) Amin K, Rostamizadeh A, Syed U (2014) Repeated contextual auctions with strategic buyers. Advances in Neural Information Processing Systems 27.

- Amram et al. (2020) Amram M, Dunn J, Zhuo YD (2020) Optimal policy trees. arXiv preprint arXiv:2012.02279 .

- Apostol (1991) Apostol TM (1991) Calculus, Volume 1 (John Wiley & Sons).

- Austin and Stuart (2015) Austin PC, Stuart EA (2015) Moving towards best practice when using inverse probability of treatment weighting (iptw) using the propensity score to estimate causal treatment effects in observational studies. Statistics in medicine 34(28):3661–3679.

- Azar et al. (2013) Azar P, Micali S, Daskalakis C, Weinberg SM (2013) Optimal and efficient parametric auctions. Proceedings of the twenty-fourth annual ACM-SIAM symposium on Discrete algorithms, 596–604 (SIAM).

- Baardman et al. (2020) Baardman L, Boroujeni SB, Cohen-Hillel T, Panchamgam K, Perakis G (2020) Detecting customer trends for optimal promotion targeting. Manufacturing & Service Operations Management .

- Babaioff et al. (2018) Babaioff M, Gonczarowski YA, Mansour Y, Moran S (2018) Are two (samples) really better than one? Proceedings of the 2018 ACM Conference on Economics and Computation, 175–175.

- Bagnoli and Bergstrom (2005) Bagnoli M, Bergstrom T (2005) Log-concave probability and its applications. Economic theory 26(2):445–469.

- Ban (2020) Ban GY (2020) Confidence intervals for data-driven inventory policies with demand censoring. Operations Research 68(2):309–326.

- Ban and Keskin (2020) Ban GY, Keskin NB (2020) Personalized dynamic pricing with machine learning: High dimensional features and heterogeneous elasticity. Available at SSRN 2972985 .

- Bartlett et al. (2006) Bartlett PL, Jordan MI, McAuliffe JD (2006) Convexity, classification, and risk bounds. Journal of the American Statistical Association 101(473):138–156.

- Bergemann and Schlag (2011) Bergemann D, Schlag K (2011) Robust monopoly pricing. Journal of Economic Theory 146(6):2527–2543.

- Bertsimas and Kallus (2020) Bertsimas D, Kallus N (2020) From predictive to prescriptive analytics. Management Science 66(3):1025–1044.

- Bertsimas and Vayanos (2017) Bertsimas D, Vayanos P (2017) Data-driven learning in dynamic pricing using adaptive optimization. Optimization Online 20.

- Besbes et al. (2018) Besbes O, Iancu DA, Trichakis N (2018) Dynamic pricing under debt: Spiraling distortions and efficiency losses. Management Science 64(10):4572–4589.

- Besbes and Zeevi (2015) Besbes O, Zeevi A (2015) On the (surprising) sufficiency of linear models for dynamic pricing with demand learning. Management Science 61(4):723–739.

- Beygelzimer and Langford (2009) Beygelzimer A, Langford J (2009) The offset tree for learning with partial labels. Proceedings of the 15th ACM SIGKDD international conference on Knowledge discovery and data mining, 129–138.

- Beyhaghi et al. (2021) Beyhaghi H, Golrezaei N, Leme RP, Pál M, Sivan B (2021) Improved revenue bounds for posted-price and second-price mechanisms. Operations Research 69(6):1805–1822.

- Biggs et al. (2021a) Biggs M, Gao R, Sun W (2021a) Loss functions for discrete contextual pricing with observational data. arXiv preprint arXiv:2111.09933 .

- Biggs et al. (2021b) Biggs M, Sun W, Ettl M (2021b) Model distillation for revenue optimization: Interpretable personalized pricing. International Conference on Machine Learning, 946–956 (PMLR).

- Boyd and Vandenberghe (2004) Boyd S, Vandenberghe L (2004) Convex optimization (Cambridge university press).

- Broder and Rusmevichientong (2012) Broder J, Rusmevichientong P (2012) Dynamic pricing under a general parametric choice model. Operations Research 60(4):965–980.

- Bu et al. (2022) Bu J, Simchi-Levi D, Wang L (2022) Offline pricing and demand learning with censored data. Management Science .

- Calmon et al. (2021) Calmon AP, Ciocan FD, Romero G (2021) Revenue management with repeated customer interactions. Management Science 67(5):2944–2963.

- Chen et al. (2019) Chen H, Hu M, Perakis G (2019) Distribution-free pricing. Available at SSRN 3090002 .

- Chen et al. (2021) Chen N, Cire A, Hu M, Lagzi S (2021) Model-free assortment pricing with transaction data. arXiv preprint arXiv:2101.02251 .

- Chen and Gallego (2021) Chen N, Gallego G (2021) Nonparametric pricing analytics with customer covariates. Operations Research .

- Chen et al. (2015) Chen X, Owen Z, Pixton C, Simchi-Levi D (2015) A statistical learning approach to personalization in revenue management. Available at SSRN 2579462 .

- Chen and Mišić (2021) Chen YC, Mišić V (2021) Assortment optimization under the decision forest model. Available at SSRN 3812654 .

- Cheung et al. (2017) Cheung WC, Simchi-Levi D, Wang H (2017) Dynamic pricing and demand learning with limited price experimentation. Operations Research 65(6):1722–1731.

- Cohen et al. (2020) Cohen MC, Lobel I, Paes Leme R (2020) Feature-based dynamic pricing. Management Science 66(11):4921–4943.

- Cohen et al. (2018) Cohen MC, Lobel R, Perakis G (2018) Dynamic pricing through data sampling. Production and Operations Management 27(6):1074–1088.

- Cohen et al. (2015) Cohen MC, Perakis G, Pindyck RS (2015) Pricing with limited knowledge of demand. Technical report, National Bureau of Economic Research.

- Cole and Roughgarden (2015) Cole R, Roughgarden T (2015) The sample complexity of revenue maximization.

- Daskalakis and Zampetakis (2020) Daskalakis C, Zampetakis M (2020) More revenue from two samples via factor revealing sdps. Proceedings of the 21st ACM Conference on Economics and Computation, 257–272.

- Den Boer (2015) Den Boer AV (2015) Dynamic pricing and learning: historical origins, current research, and new directions. Surveys in operations research and management science 20(1):1–18.

- Den Boer and Keskin (2020) Den Boer AV, Keskin NB (2020) Discontinuous demand functions: estimation and pricing. Management Science 66(10):4516–4534.

- Derakhshan et al. (2020) Derakhshan M, Golrezaei N, Leme RP (2020) Data-driven optimization of personalized reserve prices .

- Devanur et al. (2016) Devanur NR, Huang Z, Psomas CA (2016) The sample complexity of auctions with side information. Proceedings of the forty-eighth annual ACM symposium on Theory of Computing, 426–439.

- Dhangwatnotai et al. (2015) Dhangwatnotai P, Roughgarden T, Yan Q (2015) Revenue maximization with a single sample. Games and Economic Behavior 91:318–333.

- Dubé and Misra (2017) Dubé JP, Misra S (2017) Scalable price targeting. Technical report, National Bureau of Economic Research.

- Elliott (2008) Elliott MR (2008) Model averaging methods for weight trimming. Journal of official statistics 24(4):517.

- Elmachtoub et al. (2020) Elmachtoub AN, Liang JCN, McNellis R (2020) Decision trees for decision-making under the predict-then-optimize framework.

- Feldman et al. (2021) Feldman J, Zhang DJ, Liu X, Zhang N (2021) Customer choice models vs. machine learning: Finding optimal product displays on alibaba. Operations Research .

- Feng (2010) Feng Q (2010) Integrating dynamic pricing and replenishment decisions under supply capacity uncertainty. Management Science 56(12):2154–2172.

- Ferreira et al. (2016) Ferreira KJ, Lee BHA, Simchi-Levi D (2016) Analytics for an online retailer: Demand forecasting and price optimization. Manufacturing & Service Operations Management 18(1):69–88.

- Gallego et al. (2006) Gallego G, Krishnamoorthy S, Phillips R (2006) Dynamic revenue management games with forward and spot markets. Journal of Revenue and Pricing Management 5(1):10–31.

- Grünbaum (1960) Grünbaum B (1960) Partitions of mass-distributions and of convex bodies by hyperplanes. Pacific Journal of Mathematics 10(4):1257–1261.

- Harrison et al. (2012) Harrison JM, Keskin NB, Zeevi A (2012) Bayesian dynamic pricing policies: Learning and earning under a binary prior distribution. Management Science 58(3):570–586.

- Holland (1986) Holland PW (1986) Statistics and causal inference. Journal of the American statistical Association 81(396):945–960.

- Huang et al. (2018) Huang Z, Mansour Y, Roughgarden T (2018) Making the most of your samples. SIAM Journal on Computing 47(3):651–674.

- Huchette et al. (2020) Huchette J, Lu H, Esfandiari H, Mirrokni V (2020) Contextual reserve price optimization in auctions via mixed integer programming. Advances in Neural Information Processing Systems 33:1287–1297.

- Ionides (2008) Ionides EL (2008) Truncated importance sampling. Journal of Computational and Graphical Statistics 17(2):295–311.

- Javanmard and Nazerzadeh (2016) Javanmard A, Nazerzadeh H (2016) Dynamic pricing in high-dimensions. arXiv preprint arXiv:1609.07574 .

- Kallus and Zhou (2018) Kallus N, Zhou A (2018) Policy evaluation and optimization with continuous treatments.

- Ke et al. (2017) Ke G, Meng Q, Finley T, Wang T, Chen W, Ma W, Ye Q, Liu TY (2017) Lightgbm: A highly efficient gradient boosting decision tree. Advances in neural information processing systems, 3146–3154.

- Keskin et al. (2021) Keskin NB, Li Y, Song JSJ (2021) Data-driven dynamic pricing and ordering with perishable inventory in a changing environment. Management Science, forthcoming .

- Kleinberg and Leighton (2003) Kleinberg R, Leighton T (2003) The value of knowing a demand curve: Bounds on regret for online posted-price auctions. 44th Annual IEEE Symposium on Foundations of Computer Science, 2003. Proceedings., 594–605 (IEEE).

- Langford et al. (2008) Langford J, Strehl A, Wortman J (2008) Exploration scavenging. Proceedings of the 25th international conference on Machine learning, 528–535.

- Li et al. (2011) Li L, Chu W, Langford J, Wang X (2011) Unbiased offline evaluation of contextual-bandit-based news article recommendation algorithms. Proceedings of the fourth ACM international conference on Web search and data mining, 297–306.

- Liu et al. (2021) Liu A, Leme RP, Schneider J (2021) Optimal contextual pricing and extensions. Proceedings of the 2021 ACM-SIAM Symposium on Discrete Algorithms (SODA), 1059–1078 (SIAM).

- Lovász and Vempala (2007) Lovász L, Vempala S (2007) The geometry of logconcave functions and sampling algorithms. Random Structures & Algorithms 30(3):307–358.

- Lunceford and Davidian (2004) Lunceford JK, Davidian M (2004) Stratification and weighting via the propensity score in estimation of causal treatment effects: a comparative study. Statistics in medicine 23(19):2937–2960.

- Medina and Vassilvitskii (2017) Medina AM, Vassilvitskii S (2017) Revenue optimization with approximate bid predictions. arXiv preprint arXiv:1706.04732 .

- Mišic (2017) Mišic VV (2017) Optimization of tree ensembles. arXiv preprint arXiv:1705.10883 .

- Mohri and Medina (2014) Mohri M, Medina AM (2014) Learning theory and algorithms for revenue optimization in second price auctions with reserve. International Conference on Machine Learning, 262–270 (PMLR).

- Nambiar et al. (2019) Nambiar M, Simchi-Levi D, Wang H (2019) Dynamic learning and pricing with model misspecification. Management Science 65(11):4980–5000.

- Nocedal and Wright (2006) Nocedal J, Wright S (2006) Numerical optimization (Springer Science & Business Media).

- Pedregosa et al. (2011) Pedregosa F, Varoquaux G, Gramfort A, Michel V, Thirion B, Grisel O, Blondel M, Prettenhofer P, Weiss R, Dubourg V, Vanderplas J, Passos A, Cournapeau D, Brucher M, Perrot M, Duchesnay E (2011) Scikit-learn: Machine learning in Python. Journal of Machine Learning Research 12:2825–2830.

- Qi et al. (2022) Qi Z, Tang J, Fang E, Shi C (2022) Offline personalized pricing with censored demand. Available at SSRN .

- Qiang and Bayati (2016) Qiang S, Bayati M (2016) Dynamic pricing with demand covariates. Available at SSRN 2765257 .

- Rosenbaum and Rubin (1983) Rosenbaum PR, Rubin DB (1983) The central role of the propensity score in observational studies for causal effects. Biometrika 70(1):41–55.

- Shalev-Shwartz and Ben-David (2014) Shalev-Shwartz S, Ben-David S (2014) Understanding machine learning: From theory to algorithms (Cambridge university press).

- Shalit et al. (2017) Shalit U, Johansson FD, Sontag D (2017) Estimating individual treatment effect: generalization bounds and algorithms. International Conference on Machine Learning, 3076–3085.

- Swaminathan and Joachims (2015) Swaminathan A, Joachims T (2015) Counterfactual risk minimization: Learning from logged bandit feedback. International Conference on Machine Learning, 814–823 (PMLR).

- Virtanen et al. (2020) Virtanen P, Gommers R, Oliphant TE, Haberland M, Reddy T, Cournapeau D, Burovski E, Peterson P, Weckesser W, Bright J, van der Walt SJ, Brett M, Wilson J, Millman KJ, Mayorov N, Nelson ARJ, Jones E, Kern R, Larson E, Carey CJ, Polat İ, Feng Y, Moore EW, VanderPlas J, Laxalde D, Perktold J, Cimrman R, Henriksen I, Quintero EA, Harris CR, Archibald AM, Ribeiro AH, Pedregosa F, van Mulbregt P, SciPy 10 Contributors (2020) SciPy 1.0: Fundamental Algorithms for Scientific Computing in Python. Nature Methods 17:261–272, URL http://dx.doi.org/10.1038/s41592-019-0686-2.

- Ye et al. (2018) Ye P, Qian J, Chen J, Wu Ch, Zhou Y, De Mars S, Yang F, Zhang L (2018) Customized regression model for airbnb dynamic pricing. Proceedings of the 24th ACM SIGKDD International Conference on Knowledge Discovery & Data Mining, 932–940.

- Zhang et al. (2021) Zhang M, Ahn HS, Uichanco J (2021) Data-driven pricing for a new product. Available at SSRN 3545574 .

12 Proofs