The Evolution of U.S. Retail Concentration††thanks: This paper is conditionally accepted at American Economic Journal: Macroeconomics.

Any views expressed are those of the authors and not those of the U.S. Census Bureau.

The Census Bureau’s Disclosure Review Board and Disclosure Avoidance Officers have reviewed this information product for unauthorized disclosure of confidential information and have approved the disclosure avoidance practices applied to this release. This research was performed at a Federal Statistical Research Data Center under FSRDC Project Numbers 1179 and 1975 (CBDRB-FY19-P1179-R7207, CBDRB-FY20-P1975-R8604 and CBDRB-FY23-P1975-R10585).

We gratefully acknowledge advice from Thomas Holmes, Teresa Fort, Amil Petrin, Joel Waldfogel, Emek Basker, Brian Adams, Fatih Guvenen, Juan Herreño, Gueorgui Kambourov, Burhan Kuruscu, Rory McGee, Emily Moschini, Martin O’Connell, Jane Olmstead-Rumsey, Pascual Restrepo, Jeff Thurk, and Nicholas Trachter.

We are also indebted to an anonymous referee for constructive comments.

We also thank participants of seminars at various institutions as well as participants at the 2021 NBER SI CRIW, 2021 CEA, 2021 IIOC, and 2019 SED meetings and the 2018 FSRDC conference.

This paper is based upon work supported by the Doctoral Dissertation Fellowship at the University of Minnesota.

Abstract

Increases in national concentration have been a salient feature of industry dynamics in the U.S. and have contributed to concerns about increasing market power. Yet, local trends may be more informative about market power, particularly in the retail sector where consumers have traditionally shopped at nearby stores. We find that local concentration has increased almost in parallel with national concentration using novel Census data on product-level revenue for all U.S. retail stores between 1992 and 2012. The increases in concentration are broad based, affecting most markets, products, and retail industries. We show that the expansion of multi-market firms into new markets explains most of the increase in national retail concentration, with consolidation via increases in local market shares increasing in importance between 1997 and 2007, and single-market firms playing a negligible role. Finally, we find that increases in local concentration can explain one-quarter to one-third of the observed rise in retail gross margins.

JEL: D4, L8, R1

Keywords: Retail, Local Markets, Concentration, Herfindahl-Hirschman Index

1 Introduction

There is an economy-wide trend toward greater ownership concentration and an increase in the dominance of large, established firms. These trends have been accompanied by rising markups, which raises concerns about increasing market power.111 See Autor, Dorn, Katz, Patterson, and Van Reenen ((2020) for evidence of increased concentration in retail and other sectors, and Decker, Haltiwanger, Jarmin, and Miranda ((2014, 2020) for the dominance of large firms. De Loecker, Eeckhout, and Unger ((2020) and Hall ((2018) document increasing markups. The increase in concentration has been particularly strong in the retail sector, which accounts for 11 percent of U.S. employment and 6 percent of U.S. GDP. Both the share of sales going to the largest firms and the national Herfindahl-Hirschman Index (HHI) have been increasing for decades across retail industries ((Autor, Dorn, Katz, Patterson, and Van Reenen, 2020; Hortaçsu and Syverson, 2015). These changes potentially reflect a decrease in retail competition.

However, local concentration is more informative than national concentration about the degree of competition and the evolution of retail markups, because consumers in the retail sector primarily choose among local stores. Retail firms also compete within and across industries, as firms from different industries often sell identical products. This raises the need for new measures of retail firm concentration that reflect the evolution of local retail markets at the product and industry levels.

In this paper, we use novel U.S. Census data covering all retail establishments to show that both national and local firm concentration have increased. The data come from the Census of Retail Trade (CRT) and span 1992 to 2012, allowing us to measure changes in local and national concentration over 20 years. Our data allow us not only to measure industry-based concentration, but also to construct sales by product for individual retail stores with which we compute new measures of concentration for local product markets, handling retailers that sell multiple products by assigning their sales to the appropriate markets. We consistently find increases across these measures.

Our data show that the national and local HHI increased almost in parallel between 1992 and 2012. We show that the HHI measures the probability that two dollars spent at random are spent at the same firm. We use this fact to interpret changes in the HHI. The national product HHI increased from 1.3 to 4.3 between 1992 and 2012, indicating that the probability that two random dollars spent on a product anywhere in the U.S. are spent at the same firm has increased by 3 percentage points. Local (commuting zone) concentration in product markets increased by 2.2 percentage points, from 6.4 to 8.6. Moreover, we find that the increases in local retail concentration hold and are often larger when looking at an extended sample dating back to 1982, when changing the geographical definition of local markets, or when concentration is measured using the sales share of the largest firms.

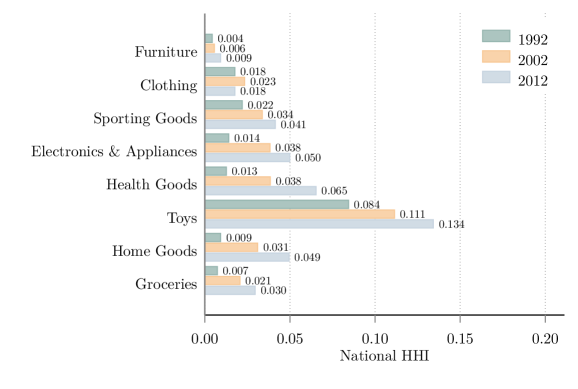

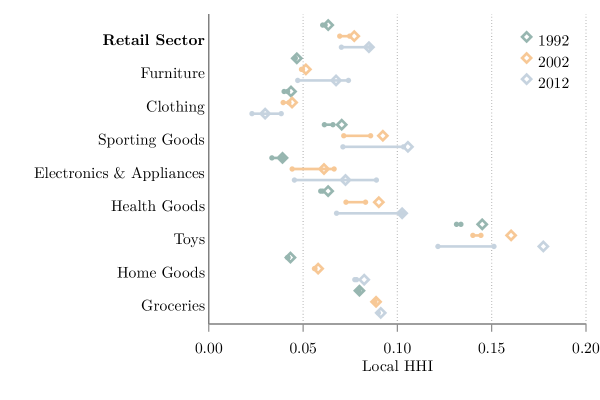

We find that the increases in local concentration were widespread, with a majority of markets and product categories experiencing increasing concentration. The local HHI increased in 72 percent of commuting zones between 1992 and 2012, with markets with increasing concentration accounting for 66 percent of retail sales in 2012. Moreover, the increases in concentration were substantial, with 40 percent of markets presenting increases of more than 5 percentage points (well above the thresholds in the merger guidelines of the Department of Justice and Federal Trade Commission, 2010). Concentration also increased for seven of the eight major product categories in retail between 1992 and 2012, with Clothing being the exception.222 The eight major product categories are Clothing, Furniture, Sporting Goods, Electronics & Appliances, Health Goods, Toys, Home Goods, and Groceries. These categories account for 94 percent of retail sales. For comparison, the eight largest (out of 61) six-digit NAICS codes in retail account for two-thirds of sales.

We examine how online and other non-store retailers affect local concentration and find they have a small effect because they account for less than 10 percent of CRT sales throughout our sample. Establishing the exact effect of non-store retailers on local concentration is challenging because the CRT does not contain the location of sales for non-store retailers. Nevertheless, we obtain bounds for the effect of non-store retailers by assigning their national sales to local markets using a range of assumptions on how concentrated their local sales are. Including non-store retailers implies smaller increases in national and local concentration under most assumptions.

We also measure local and national retail concentration in six-digit NAICS industries and compare them to our product-based results. We find that industry-based measures exhibit a stronger increase in concentration than product-based measures. Commuting zone concentration increased by 12.6 percentage points between 1992 and 2012, an increase six times greater than the increase in local product concentration. Local concentration increased within all eight three-digit NAICS subsectors, led by a 28 percentage point increase in the industries that make up the General Merchandising subsector.

The main difference between product- and industry-based measures of concentration is the type of competition that they emphasize. Product-based measures emphasize competition in the sale of goods, while industry-based measures emphasize competition in retail services. This difference is made clear in the treatment of general merchandisers and other multi-product retailers, which, by definition, sell the same products as retailers in other industries, but offer a different service precisely by offering a wider range of products.333 For example, Walmart is in the general merchandising subsector (three-digit NAICS 452) but competes with grocery, clothing, and toy stores. However, a retailer in a clothing industry is likely to carry a large number of clothing items, while a general merchandiser like Walmart carries other products in addition to a smaller selection of clothing. Walmart reports SIC code 5331 to the Security and Exchange Commission, which corresponds to NAICS 452990 ((Securities and Exchange Commission, 2020). References to specific firms are based on public information and do not imply the company is present in the confidential data. In fact, general merchandisers account for more than 20 percent of sales in Electronics & Appliances, Groceries, and Clothing, and their expansion has been linked to the closure of grocery stores ((Arcidiacono, Bayer, Blevins, and Ellickson, 2016), showing that competition across industries is a relevant feature of retail markets. The same pattern arises in more detailed industries, as we show in Section 2 and Appendix C.

Having established the increase in both national and local retail concentration, we investigate the relationship between these two trends. We find that the two trends are linked by the expansion and consolidation of multi-market retailers, with the expansion of large retailers across markets accounting for 89 percent of the increase in national retail concentration between 1992 and 2012. In this way, concentration has increased as consumers in different markets increasingly buy from the same firms, adding to the findings of previous papers such as Cao, Hyatt, Mukoyama, and Sager ((2019), Hsieh and Rossi-Hansberg ((2023), and Rossi-Hansberg, Sarte, and Trachter ((2021) on the role of the expansion of large firms in explaining changes in the U.S. economy.444 The expansion of large retail firms has led to the closing of small stores ((Jia, 2008; Haltiwanger, Jarmin, and Krizan, 2010) and grocery chains ((Arcidiacono et al., 2016), as well as higher retail employment in local labor markets ((Basker, 2005) and increased welfare for consumers ((Leung and Li, 2022, 2023).

Our findings also reveal that single-market firms operating in local product markets have a negligible effect in the evolution of national concentration. This is because the distribution of retail sales across locations in the U.S. implies that even the largest retail markets in the U.S. are too small to affect national trends. By contrast, the national market share of retail firms present in at least 50 commuting zones increased from 34 to 58 percent between 1992 and 2012, despite there being fewer than 350 of these firms in the U.S. (or less than 0.1 percent of retail firms). All this while their average local market share barely increased from 3.2 to 3.4 percent.

We end the paper with a discussion of the implications of our findings. Under Cournot competition there is a direct link between local concentration and firms’ margins. This link implies increases in retailers’ margins of 1.6 percentage points from the overall increase in local product market concentration. Taking into account differences in concentration trends and retailers’ margins across products increases the estimate to 2.1 percentage points.555 Many of the concerns about concentration leading to higher markups (Hall, 2018; Traina, 2018; Edmond, Midrigan, and Xu, 2019; De Loecker et al., 2020) would operate through local markets, particularly in labor and retail markets. For instance, higher local employment concentration has been shown to negatively impact wages ((Jarosch, Nimczik, and Sorkin, 2020; Azar, Berry, and Marinescu, 2019; Rinz, 2020; Berger, Herkenhoff, and Mongey, 2022), and has been associated with the presence of large publicly traded firms that are increasingly owned by common investors ((Azar, Qiu, and Sojourner, 2022). These changes in margins are meaningful, accounting for one-fourth to one-third of the 6.0 percentage points increase in retailers gross margins between 1993 and 2012 from the Annual Retail Trade Survey (ARTS). We also discuss the importance of multi-market pricing and the growth of online retailers. These trends imply that retailers may increasingly set prices based on their average market power across markets, attenuating the impacts of increasing local concentration on retailer margins.

Comparison to Previous Concentration Results

Our finding of parallel increases in local and national concentration complements work documenting increasing concentration across the U.S. economy.666 See Basker, Klimek, and Van ((2012); Foster, Haltiwanger, Klimek, Krizan, and Ohlmacher ((2016); Hortaçsu and Syverson ((2015); Grullon, Larkin, and Michaely ((2019); Ganapati ((2021). In particular, our product-based measures complement work finding increasing national concentration at the industry level using the Census of Retail Trade ((Autor et al., 2020). The increases in local concentration in the retail sector that we document are in line with the findings of Rinz ((2020) and Lipsius ((2018), who study local labor markets using the Longitudinal Business Database (LBD), another U.S. Census dataset, and contrast with the decreasing trends in local concentration that they and Rossi-Hansberg et al. ((2021) find outside of retail. We provide more evidence that retail is the only sector with consistently increasing local concentration.

We provide new series of concentration by product categories, which better reflect the nature of competition in retail, as well as series by industry at different levels of geographic aggregation. Our results differ from the industry-based results in Rossi-Hansberg et al. ((2021) and studies of consumer purchasing decisions by Neiman and Vavra ((2020) and Benkard, Yurukoglu, and Zhang ((2021), that find decreasing concentration.

Rossi-Hansberg et al. ((2021) base their results on data from the National Establishment Time Series (NETS), a private dataset, that does not contain sales by product categories, preventing them from addressing cross-industry competition. Moreover, the NETS includes restaurants in the retail sector while the CRT does not, which explains part of the difference between the two studies ((Trachter, 2021).777 The NETS also has issues tracking establishments and imputing sales of retailers ((see, Crane and Decker, 2020; Decker, 2020). There are also methodological differences between our studies. We consider a range of methods to calculate the local HHI to make our studies more comparable. We find increases in local concentration with all but one, with changes in local industry concentration between -1.5 and 12.6 percentage points. The baseline estimate in Rossi-Hansberg et al. that local retail concentration decreased by 17 percentage points falls significantly outside this range. Half of the remaining difference is due to data source as we show in Section 3.4 and Appendix E.

On the other hand, Benkard et al. ((2021) study the ownership of the brands of goods and services that consumers purchase, finding that both national and local concentration among the producers of these products decrease over time, while Neiman and Vavra ((2020) use scanner data to show that aggregate concentration in household UPC purchases of groceries has fallen. We calculate firm-level concentration among the retailers that sell those (and other) goods using data covering all retail sales. Taken together, our results are complementary as they speak to different aspects of the retail sector. On aggregate, consumers are simultaneously purchasing a wider variety of brands as they buy those products from a smaller set of retail firms. In this way, increasing retail concentration could cause retail firms to have both more market power with consumers and better negotiating power with suppliers.

Finally, we show how the consolidation and expansion of single- and multi-market firms has shaped the relationship between local and national concentration trends. Our results extend previous work documenting the expansion of individual retail firms ((Basker, 2005, 2007; Holmes, 2011) and national chains ((Miranda, Klimek, and Jarmin, 2004; Foster, Haltiwanger, and Krizan, 2006; Foster, Haltiwanger, Klimek, Krizan, and Ohlmacher, 2016) in the 1980s and 1990s. We further contribute by showing that this expansion was followed by within consolidation of large retailers that explains 40 percent of the increase in national concentration between 1997 and 2007.

The rest of the paper proceeds as follows. Section 2 describes the data and how we construct store-level sales by product. Section 3 measures retail concentration and documents its evolution. Section 4 decomposes national concentration into local and cross-market concentration. Section 5 discusses implications for retailers’ market power.

2 Data: Retailer Revenue for All U.S. Stores

This section describes the creation of new data on store-level revenue for 18 product categories for all stores with at least one employee in the U.S. retail sector. These data allow us to construct detailed measures of concentration that take into account competition between stores selling similar products in specific geographical areas.

2.1 Data Description

We use confidential U.S. Census Bureau microdata that cover 1992 to 2012 ((U.S. Census Bureau, 1992-2012). The data source is the Census of Retail Trade (CRT), which provides revenue by product type for retail stores (establishments) in years ending in 2 and 7. We compile CRT data on product-level revenue and information on each store’s location to define which stores compete with each other. Importantly, a store’s local competition will include stores in many different industries inside the retail sector because stores of different industries can sell similar products. This is particularly relevant for stores in the general merchandising subsector, but it also affects stores across more detailed industries (e.g., family clothing stores, women’s clothing stores, and men’s clothing stores). The data we create here are uniquely equipped to deal with cross-industry competition.

We combine the CRT data with the Longitudinal Business Database (LBD) ((Jarmin and Miranda, 2002), which contains data on each store’s employment and allows us to track stores over time. The LBD’s firm identifiers allow us to determine which stores are owned or controlled by the same entity.888 See https://www.census.gov/econ/esp/definitions.html This definition of firms combines stores with different names if they are subsidiaries of the same firm. It also combines the stores of entities that merge into one firm.999 The effect of mergers on concentration depends on whether the stores that merge sell the same products, are in the same industries, and are located in the same geographical markets. We calculate all concentration measures at the firm level by combining store sales of a firm in each market.

2.2 Sample Construction

The retail sector is defined based on the North American Industrial Classification System (NAICS) as stores with a two-digit code of 44 or 45. As such, it includes stores that sell final goods to consumers without performing any transformation of materials. We use the NAICS codes available from the CRT as the industry of each store. The sample includes all stores with positive sales and valid geographic information that appear in official CRT and County Business Patterns (CBP) statistics that sell one of the product categories used in this study.101010 We exclude sales of gasoline and other fuels, autos and automotive parts, and non-retail products because franchising makes it difficult to identify firms. In our main results we exclude non-store retailers because sales from these stores are typically shipped to different markets than their physical location. We explore the implications of this assumption in Section 3.3.

Table 1 shows summary statistics for our sample. Even though the number of establishments and firms fluctuates over time, there is an overall decrease in both counts between 1992 and 2012. Notably, the decrease in firms is double the decrease of establishments. This trend is consistent with the growing importance of multi-market firms in rising cross-market concentration that we show in Section 4. Despite these trends, employment increases over time, representing about 9 percent of nonfarm U.S. employment over the whole sample period.111111 U.S. employment numbers come from Total Nonfarm Employees in the Current Employment Statistics ((Bureau of Labor Statistics, 2019).

| 1992 | 1997 | 2002 | 2007 | 2012 | |

| Establishments | 908 | 942 | 913 | 912 | 877 |

| Firms | 593 | 605 | 589 | 566 | 523 |

| Sales | 1,004 | 1,368 | 1,657 | 2,062 | 2,195 |

| Employment | 9.91 | 11.60 | 11.89 | 12.78 | 12.31 |

-

•

Notes: Establishment and firm numbers are expressed in thousands. Sales and employment numbers are expressed in millions. The numbers are based on calculations from the Census of Retail Trade and the Longitudinal Business Database. (CBDRB-FY20-P1975-R8604)

2.3 Creation of Product-Level Revenue

We construct product-level revenue data for all U.S. stores, allowing us to assign a store in a given location to markets based on the types of products it carries. To do this, we exploit the CRT’s store-level data on revenue by product line (e.g., men’s footwear, women’s pants, diamond jewelry). We then aggregate product line codes into 18 categories such that stores in industries outside of general merchandise and non-store retailers sell primarily one type of product.121212 Table B.2 lists all the product categories. Unless otherwise stated, we use data from all products for our aggregate results. In Section 3.2 we focus on the eight “main” product categories that account for 94 percent of store sales in our sample for results for individual product categories. The remaining categories are individually small and have not been released due to disclosure limitations. For instance, stores in industries beginning with 448 (clothing and clothing accessory stores) primarily report sales in products such as women’s dress pants, men’s suits, and footwear, which are grouped into a Clothing category.

The product-level data we construct opens up the possibility to study product markets covering all of retail. Alternative data sources, such as the NielsenIQ Homescan Consumer Panel and the Nielsen Scanner Data, provide more detailed product descriptions but lack the representativeness of our sample, focusing mostly on grocery and health products for a limited sample of people or retailers, making them less useful for computing concentration at the firm level.131313 Firm level concentration is the relevant measure of concentration for antitrust in retail. However, detailed product concentration is informative about consumer behavior and retailers upstream market power with their suppliers ((Benkard et al., 2021; Neiman and Vavra, 2020). Our definition of product categories implies slightly higher levels of aggregation than six-digit NAICS industry codes while dealing with cross-industry competition (see Appendix C). It also addresses the fact that several product lines are consistently sold together, as is the case for men’s wear (product line code—plc—20200), women’s juniors’ and misses’ wear (plc 20220), and footwear products (pcl 20260), or for major household appliances (plc 20300) and TVs (plc 20320).

Aggregating product lines into categories allows us to accurately impute revenue by category for stores that do not report product-level data. The CRT asks for sales by product lines from all stores of large firms and a sample of stores of small firms. For the remainder, store-level revenue estimates are constructed from administrative data using store characteristics (e.g., industry and multi-unit status). These revenue estimates are constructed for stores that account for about 20 percent of sales in each year. Appendix B provides the details of this procedure.

Our product-level revenue data also accounts for the presence of multi-product stores. When a store sells products in more than one category, we assign the store’s sales in each category to its respective product market. Consequently, a given store faces competition from stores in other industries. For example, an identical box of cereal can be purchased from Walmart (NAICS 452), the local grocery store (NAICS 448), or online (NAICS 454).141414 The authors found a 10.8 oz box of Honey Nut Cheerios at Walmart, Giant Eagle, and Amazon.com on June 22, 2020.

Table 2 shows that cross-industry competition is pervasive in retail. On average, the main subsector for each product accounts for just over half of the product’s sales. The remaining sales are accounted for by multi-product stores, particularly from the general merchandise and non-store retailer industries, which are included in the appropriate product markets based on their reported sales. The high sales shares of these multi-product stores makes industry classifications problematic when studying competition. Table D.1 reports the composition of sales for each product category, further distinguishing between general merchandisers and other multi-product retailers.

Moreover, even stores in detailed industries (six-digit NAICS) sell the same products. For example, men’s clothes are available at Men’s clothing stores (448110), and family clothing stores (448140), in addition to department stores (452111) and discount department stores (452112), see Table C.4 in Appendix C. Although the shopping experience may differ between stores in different industries a consumer looking to buy a new pair of jeans might consider stores in more than four different NAICS industries.

| 1992 | 2002 | 2012 | |

|---|---|---|---|

| Avg. Main Subsector Share | 55.8 | 53.2 | 50.0 |

| Max Main Subsector Share | 79.8 | 73.1 | 72.4 |

| Min Main Subsector Share | 30.3 | 27.6 | 22.0 |

-

•

Notes: The numbers are based on calculations from the Census of Retail Trade. The average is the arithmetic mean across the eight main product categories of the share of sales accounted by establishments in the product’s associated subsector. Shares are multiplied by 100.

2.4 Definition of Local Markets

We use the 722 commuting zones that partition the contiguous U.S. as our definition of local markets. Commuting zones are defined by the U.S. Department of Agriculture such that the majority of individuals work and live inside the same zone, and they provide a good approximation for the retail markets in which stores compete. If individuals live and work in a commuting zone, they likely do most of their shopping in that region.

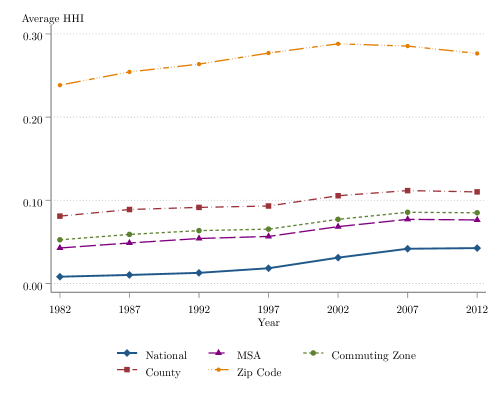

Our results regarding the increasing trends in local concentration and the role of local trends for national concentration are robust to changes in the definition of retail markets. Choosing a larger geographical unit when defining retail markets, such as commuting zones, typically increases the contribution of local concentration to national concentration relative to smaller geographical units such as counties or zip codes. Larger geographical units also tend to have lower levels of concentration than smaller units. However, despite differences in levels of concentration, measures at the zip code, county, commuting zone, and Metropolitan Statistical Area (MSA) levels lead to the same conclusions about the trend in local concentration, even in an extended sample dating back to 1982 (see Appendix D.2).

3 Changes in Retail Concentration

In this section, we use the detailed microdata described in Section 2 to measure national and local concentration in the U.S. retail sector. We find that local concentration has increased almost in parallel with national concentration. The increases in concentration are broad based, affecting most markets, product categories, and retail industries.

Our primary measure of concentration is the firm Herfindahl-Hirschman Index (HHI) for a given product category. We denote by an individual firm and by a product so that represents the sales share of firm in product at time . More generally, we define subscripts and superscripts such that is the share OF IN . The national HHI in a year is defined as the sum of the product-level HHIs weighted by the share of product ’s sales in total retail sales, :

| (1) |

while the HHI of location and product in year is calculated as

| (2) |

The HHI for product measures the probability that two dollars, and , chosen at random, are spent at the same firm. This probabilistic interpretation of the HHI provides a direct way to understand its level and changes.

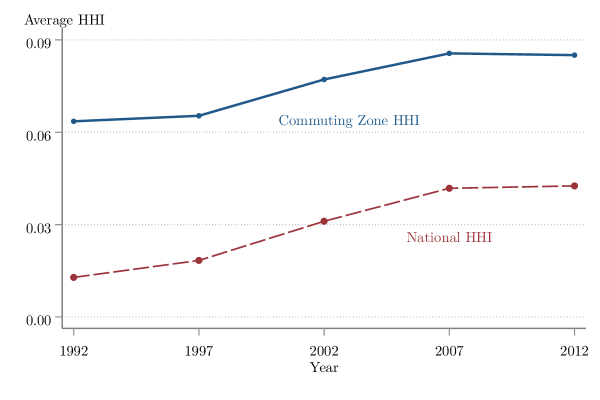

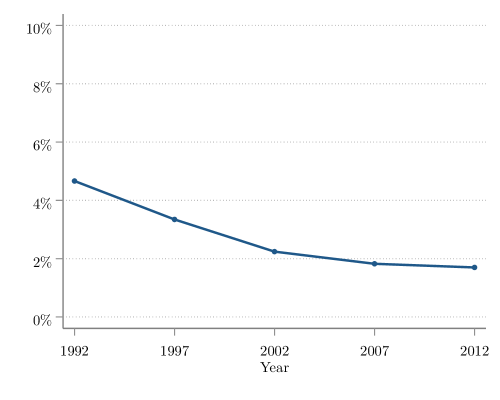

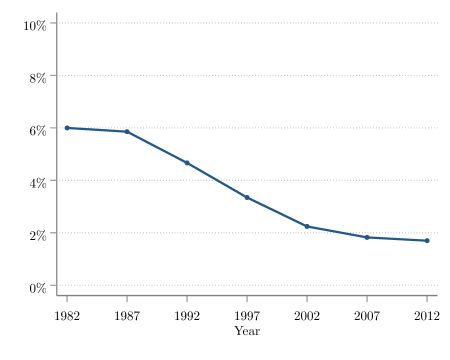

Figure 1 plots national and local concentration in the U.S. retail sector as measured by the HHI. Between 1992 and 2012, both national and local concentration increased at a similar pace. National concentration more than tripled from 0.013 to 0.043. That is, the probability that two dollars are spent in the same firm in the U.S. goes from 1.3 percent in 1992 to 4.3 percent in 2012. Local concentration, measured by the commuting zone HHI, increased by 34 percent from 6.4 percent to 8.6 percent, a similar increase to that of the national HHI.

We extend these results back to 1982 and consider additional measures of local concentration measures at the zip code, county, and MSA level (Appendix D.2). We find no change in the increasing trends for national and local concentration. Most of this increase occurred between 1997 and 2007, after which all concentration measures plateau. In fact, the national HHI was low and grew at a low rate before 1997. National concentration increased by 1 percentage point in the 15 years between 1982 and 1997; by contrast, it increased 2.3 percentage points in the 10 years between 1997 and 2007. We also show that increases in local concentration are found with other definitions of local markets and that these changes are broad based across products and geographic areas.

The national concentration results are consistent with previous industry-level work using sales and employment for various sectors, including retail ((Basker et al., 2012; Foster et al., 2016; Lipsius, 2018; Autor et al., 2020; Rinz, 2020; Rossi-Hansberg et al., 2021). The local concentration results are also consistent with studies on labor market concentration that find increasing local concentration in retail but decreasing local concentration in other sectors ((Rinz, 2020; Lipsius, 2018). We show that industry-based measures of sales concentration also rise at both the national and local level in Section 3.4 and contrast these results with those of Rossi-Hansberg et al. ((2021) who report decreasing local concentration.

3.1 Changes in Concentration across Markets

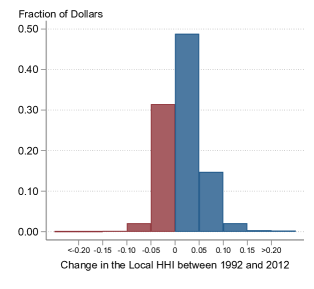

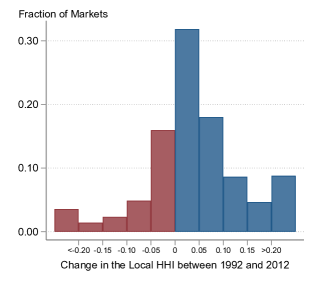

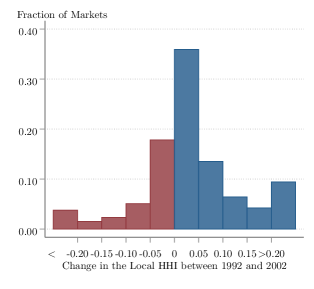

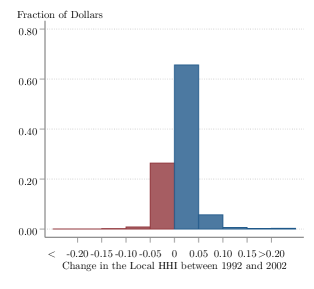

We now turn to the distribution of changes in concentration across markets. We find that the increases in concentration have been broad based. Sixty-six percent of dollars spent in 2012 are spent in markets that have increased concentration since 1992 (Figure 2(a)). In 20 years, 40 percent of markets accounting for 17 percent of spending have increases in concentration of over 5 percentage points (Figure 2(b)). These changes are significant. For comparison, the Department of Justice considers a 2 percentage point increase in the local HHI potential grounds for challenging a proposed merger ((Department of Justice and Federal Trade Commission, 2010). On the other side, only 12 percent of markets accounting for 2 percent of spending experienced decreases in the local HHI at at least 5 percentage points.

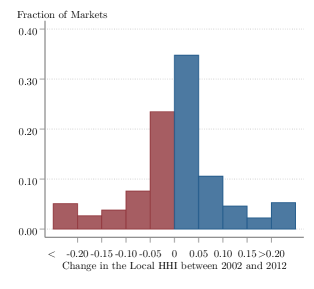

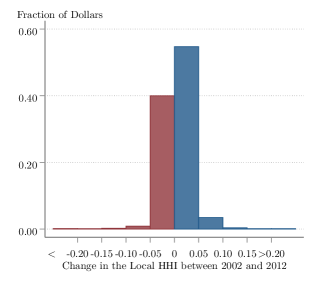

Even though local retail concentration has sustainably increased between 1992 and 2012, the changes in concentration were more widespread between 1992 and 2002, when concentration increased in almost 70 percent of markets. The share of markets with increasing concentration was lower in the following decade with just under 60 percent of markets increasing their concentration. We explore these patterns in in Appendix D.5 where we present changes in concentration by decade.

3.2 Changes in Concentration across Products

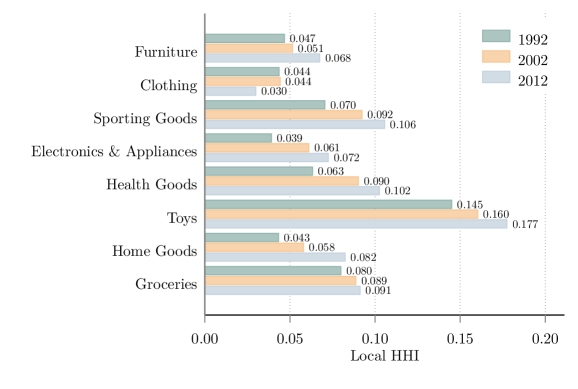

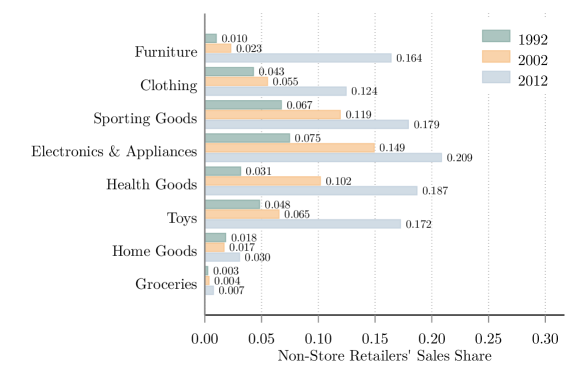

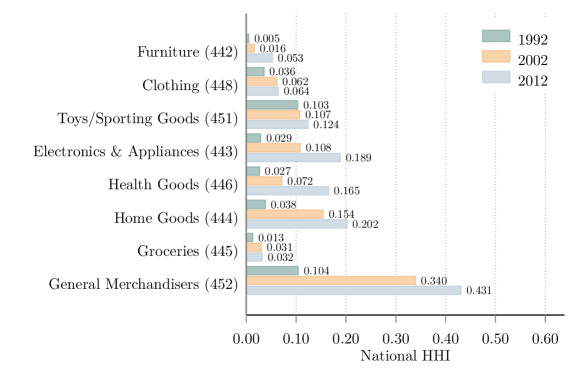

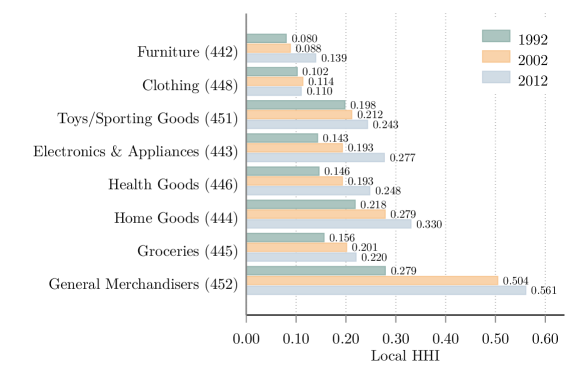

Between 1992 and 2012, both local and national concentration increased for seven of the eight major product categories, Clothing being the exception. Figure 3(a) shows that these increases were large for many products. Six of the eight categories had an increase in HHI between 3 and 4 percentage points. Despite this common trend, the changes in concentration vary substantially across product categories. Local concentration in Groceries increased by only 1.1 percentage points and decreased in Clothing by 2012, while it almost doubled in Home Goods and Electronics & Appliances.

Figure 3(b) shows the levels of national concentration for each product category between 1992 and 2012. The increases in national concentration are widespread and significant. Six of the categories have larger absolute changes in national concentration relative to local concentration even though the levels of national concentration are markedly lower than those of local concentration.

Finally, comparing Figures 3(a) and 3(b) shows that not all product markets evolved in the same way between 1992 and 2012. The markets for Furniture and Clothing changed very little, and both have relatively low levels of both local and national concentration. On the other hand, local markets for Groceries and Health Goods became slightly more concentrated, while at the national level, concentration has increased more than fourfold.

3.3 Impact of Online and Other Non-Store Retailers

The previous results calculated local concentration using only brick-and-mortar retailers. In what follows, we consider the potential impact of online and other non-store retailers on local concentration. The market share of non-store retailers has more than tripled between 1992 and 2012. However, the overall importance of non-store retailers remained limited through 2012. The initial sales share of non-store retailers is low, just 2.7 percent in 1992. This low share reflects both the absence of online retailers and the limited role of other retailers that rely on mail order and telephone sales. The sales share of non-store retailers had risen to 9.5 percent by 2012, driven by an increase in online sales. The increase was uneven across product categories. Non-store retailers had significant market share in product categories, such as Furniture, Clothing, and Sporting Goods, but have almost no market share in Groceries and Home Goods (see Appendix D.3).

The effect of online and other non-store retailers on local concentration depends on how their sales are distributed across and within markets. Unfortunately, the CRT does not record the location in which non-store retailers sell their products, making it impossible to determine the exact effect of these retailers on local concentration. Nevertheless, we can generate bounds for the effect of non-store retailers while being consistent with their behavior at the national level. To do this, we assume that the share of retail spending that goes to non-store retailers is constant across markets within a product category and is equal to the national sales share of non-store retailers in that category.151515 It is possible for brick-and-mortar retailers to sell online becoming mixed channel retail firms. The CRT assigns these transactions to the establishment that fulfills them. Transactions shipped from a brick and mortar establishment are typically included in the sales of that establishment and are thus already accounted for in our concentration calculations. Transactions shipped from a dedicated fulfillment center are assigned to an establishment of the same firm in a non-store retailer industry. We have studied multiple ways of assigning the sales of mixed channel retailers and found that they have limited effects through 2012 because their sales are relatively low.

Having distributed the sales of non-store retailers across markets, we can construct a lower and upper bound for the local HHI. The total effect on concentration depends on the total market share of non-store retailers and how concentrated they are. The lower bound assumes that non-store retailers are atomistic, with the sales share of each non-store retailer equal to zero. The lower bound is

| (3) |

where corresponds to the sales share of non-store retailers and to the HHI of brick-and-mortar stores. In this case, non-store retailers decrease concentration by reducing the sales share of brick-and-mortar stores. The size of this decrease depends on the sales shares of non-store retailers in the product category. The upper bound assumes that all the sales of non-store retailers belong to a single stand-in firm. The upper bound is

| (4) |

This is an upper bound on concentration under the assumption that firms do not have both brick-and-mortar and non-store establishments, which is consistent with the data.

Figure 4 shows the bounds we construct for local concentration across product categories in the retail sector. As expected, including non-store retailers for categories like Home Goods or Groceries hardly affects the level of concentration because the market share of non-store retailers remains low throughout. The effects are larger for the other categories, especially for 2012. Accounting for non-store retailers reduces concentration in most categories because of the decrease in market share among brick-and-mortar stores. For most product categories, the bounds for local concentration lie below the estimated HHI for brick-and-mortar stores (marked by the diamonds in the figure). It is only in Electronics & Appliances, and to a lesser extent in Clothing, that the market share of non-store retailers is large enough for their inclusion to potentially increase concentration.

When non-store retailers are included, there is still a clear increase in local concentration between 1992 and 2002, although the levels are slightly lower. Moving from 2002 to 2012, the story becomes ambiguous, especially for product categories with a significant share of their sales going to non-store retailers. In many cases, the bounds for 2012 contain the bounds for 2002, indicating local concentration could either be increasing or decreasing depending on the concentration among non-store sales. At a national level, non-store retailers were not highly concentrated during this time period ((Hortaçsu and Syverson, 2015), and thus the increasing importance of non-store retailers is potentially limiting the increase in local market concentration between 2002 and 2012. In Table D.2 of Appendix D.3, we show that national concentration is unaffected by non-store retailers until 2002 and does reduce its increase afterwards.

3.4 Comparing Industry- and Product-Based Results

We now document the evolution of industry-based concentration measures. These measures capture the variation in retail services offered by different industries. For instance, general merchandisers offer a variety of products, and consumers value the ability to buy multiple products in one location ((Seo, 2019). In this sense, industry based measures focus on a different dimension of competition between retail stores than the product-based measures we have presented.

We find larger increases in both national and local concentration at the industry level than at the product level. We study industry-based measures of concentration defined at the six-digit NAICS level, the most disaggregated industries available in the data. We aggregate these results to the three-digit NAICS level using a sales-weighted average. Table 3 shows that national industry-based concentration increases by 8.7 percentage points, 5.7 percentage points more than with product-based measures. Commuting zone concentration goes up by 12.6 percentage points between 1992 and 2012 when measured at the industry level, 10.4 percentage points more than the product-based measure. The same patterns arise when defining markets at the zip code level and show that the large increase in industry-based local concentration is not a feature of the geographical aggregation of markets.

A significant portion of the increase in industry concentration comes from six-digit industries within the general merchandise subsector (NAICS 452), where local concentration increased by 28.2 percentage points (see Figure D.5 in Appendix D.6). This change is at least partially due to general merchandisers selling an increasing number of products and may not reflect increasing market power.

| National Concentration | |||||

| 1992 | 1997 | 2002 | 2007 | 2012 | |

| Product Based | 0.013 | 0.018 | 0.031 | 0.042 | 0.043 |

| Industry Based | 0.029 | 0.046 | 0.085 | 0.105 | 0.116 |

| Commuting Zone Concentration | |||||

| Product Based | 0.064 | 0.065 | 0.077 | 0.086 | 0.085 |

| Industry Based | 0.177 | 0.199 | 0.263 | 0.287 | 0.302 |

| Zip Code Concentration | |||||

| Product Based | 0.264 | 0.277 | 0.288 | 0.286 | 0.277 |

| Industry Based | 0.530 | 0.552 | 0.602 | 0.611 | 0.615 |

-

•

Notes: The numbers come from the Census of Retail Trade and are the level of concentration in a given year with markets defined according to the noted geography. All local measures of concentration use the establishments included in the sample for the product-based results. Industry concentration uses six-digit NAICS codes. (CBDRB-FY20-P1975-R8604, CBDRB-FY19-P1179-R7207)

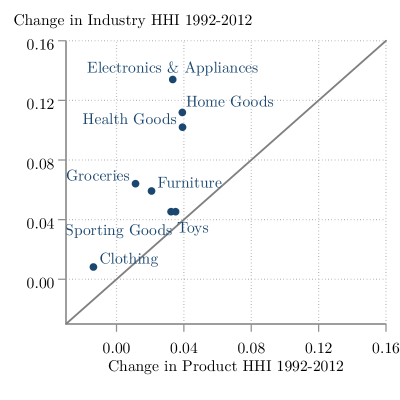

We match each product to the subsector that primarily sells that product (e.g., Clothing and NAICS 448: Clothing and Clothing Accessory Stores) and plot the changes in concentration in Figure 5. The figure shows a positive correlation between industry and product concentration despite the differences in market definition. However, the increases in concentration are larger when measured at the industry level, which explains the larger increases in overall retail concentration shown in Table 3. Appendix D.6 complements these results by reporting the levels of local and national concentration for the industries corresponding to our main product categories and general merchandisers.

The picture that emerges from our data differs from Rossi-Hansberg et al. ((2021), who find a decrease in industrial retail concentration at the zip code level of 17 percentage points between 1992 and 2012. Our studies differ in both data and methodology.

Rossi-Hansberg et al. use U.S. National Establishment Time Series (NETS) data, a private dataset, to calculate concentration using sales and employment for multiple sectors.161616 Crane and Decker ((2020) show that the NETS has issues tracking establishments over time, making it problematic for measuring trends and Decker ((2020) argues that NETS sales are typically imputed from employment, making studies with NETS most comparable to studies of employment concentration. The NETS defines the retail sector using Standard Industrial Classification (SIC) codes, while the CRT uses NAICS. The main difference is that SIC includes restaurants in retail while the NAICS does not, making it so that our results are not directly comparable ((Trachter, 2021).

We also differ in the aggregation methodology for local concentration. The methodology in Rossi-Hansberg et al. places more weight on markets with declining concentration because it uses each market’s final share of employment and markets become less concentrated as they grow. Weighting markets using their average share of employment over time or their initial share always implies increasing local concentration.

We replicate the methodology of Rossi-Hansberg et al. in our data and find a 1.5 percentage point decrease in local industrial concentration at the zip code level. The remaining 15.5 percentage points between our results are equally due to differences in market definition and data sources. For their baseline result, Rossi-Hansberg et al. define markets based on eight-digit SIC codes, while we use six-digit NAICS codes in our industry measures.171717 Eight-digit SIC codes may be overly detailed for retail markets because many retailers will sell multiple types of goods. For example, concentration in eggs and poultry (54999902) would miss the fact that many eggs and poultry are sold by chain grocery stores (54119904) and discount department stores (53119901). Rossi-Hansberg et al. show that moving from eight- to four-digit SIC codes in NETS implies a decline in concentration of 8 percent, explaining about half of the difference between our results. Four-digit SIC codes are comparable to the six-digit NAICS available in the CRT. The change from NETS data to CRT data explains the other half of the difference. We provide full details of these exercises in Appendix E.

All other concentration measures we calculate for the retail sector—varying the level of geographical aggregation, aggregation methodology, and definition of markets by product or industry—imply an increase in local concentration between 1992 and 2012. Taken together, we find robust evidence for increases in local retail concentration.

4 The Relationship Between National and Local HHIs

We now turn to the relationship between national and local concentration, and the role of single- and multi-market firms in shaping this relationship. National concentration can increase as single- and multi-market firms consolidate in local markets and increase local concentration. But concentration can also increase as multi-market firms expand across markets, capturing a larger share of national sales without necessarily increasing local concentration. This expansion makes it so that consumers in different markets increasingly buy from the same firms. We refer to this as cross-market concentration.

We disentangle the contribution of consolidation and expansion of single- and multi-market retailers in increasing national concentration in three steps. First, we show that the contribution of single-market firms is negligible. Then, we establish that this is necessarily the case given the distribution of economic activity in the U.S. retail sector. Finally, we conduct a counterfactual exercise to separate the impact of consolidation and expansion in the growth of national concentration. We find that expansion plays a prominent role between 1992–2002 explaining about 89 percent of the increase in national concentration, with consolidation increasing in importance in the 1997–2007 period.

4.1 The Contribution of Single-Market Firms to Concentration

Single-market firms can only affect national trends through local concentration as they do not affect cross-market concentration. To quantify their role, we consider a counterfactual where all firms are single-market firms by breaking up multi-market firms into separate firms in each commuting zone. This counterfactual gives us an upper bound on the role of single-market firms in explaining national trends, while keeping the level and evolution of local concentration unchanged.

If all firms operated as single-market firms, the national HHI would have been 0.06 percent in 1992 and 0.07 percent in 2012. These counterfactual levels are 95-98 percent smaller than the actual national HHI, showing that the increase in local concentration coming from single-market firms cannot explain the evolution of U.S. retail concentration.181818 Similar patterns arise for individual product markets. The level of the product HHI in the counterfactual varies between 0.03 and 0.14 percent and remain flat between 1992 and 2012.

This exercise further implies that, in the U.S., national retail trends must be due to changes in cross-market concentration and therefore to the behavior of multi-market firms. We make this precise by decomposing the national HHI into the role of local and cross-market concentration. Recall that the HHI for product measures the probability that two dollars, and , chosen at random, are spent at the same firm. Using the Law of Total Probability we decompose the national HHI based on whether the two dollars are spent in the same or different markets:191919 The same principle also applies in other settings. We can use the law of total probability to decompose the HHI into any set of mutually exclusive components. These can be the urban or rural markets, or markets with different demographic characteristics. We provide a detailed description of the decomposition in Appendix A.

| (5) |

where is the firm at which dollar is spent and is the location of the market in which dollar is spent, and likewise for .

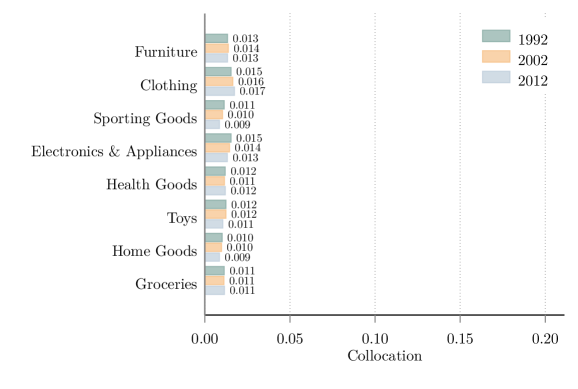

Equation (5) has three components. The first component, , which we term collocation, captures the probability that two dollars are spent in the same location. The second component, , is an aggregate index of local concentration, with local concentration measured as in equation (2). This captures the extent to which consumers in a local market shop at the same firm. The third component, , captures cross-market concentration, the probability that a dollar spent in different markets is spent at the same firm.

The decomposition shows that 98 percent of the level of national concentration comes from the cross-market term. The reason for this is that, in the U.S., even the largest markets represent only a small fraction of total retail sales, resulting in a low collocation term. This limits the impact that concentration on local markets on its own can have on national trends.202020 The collocation term is where is the share of location in national sales. Our estimates of the collocation term for the retail sector using confidential data are about 0.012. See figures A.1 and A.2 in Appendix A. For national and local concentration to increase as we observe, it must be that the increase in local concentration is accompanied by cross-market concentration, with consumers in different locations increasingly shopping at the same (large) firms. This can only happen via the consolidation and expansion of multi-market firms.

4.2 The Contribution of Multi-Market Firms to Concentration

The previous results show that the increase in national retail concentration reflects the activity of multi-market firms, particularly that of the largest retailers, that affect cross-market concentration through their expansion and consolidation across markets. Take, for instance, the behavior of firms present in at least 50 commuting zones. Table 4 shows that their share of national sales increased from 34 percent to 58 percent between 1992 and 2012, despite there being no more than 350 of these firms in the U.S.. By contrast, their average local share increased only slightly from 3.2 to 3.4 percent. This suggests that the increase in U.S. retail concentration is mostly due to the expansion of multi-market retailers into new markets, rather than consolidation in the markets they were already present in.212121 In fact, large retailers went from being present in 139 commuting zones on average in 1992 to 163 commuting zones in 2012, an increase of 27 percent. This adds to the findings of Cao et al. ((2019), Hsieh and Rossi-Hansberg ((2023), and Rossi-Hansberg et al. ((2021), who also highlight the role of firm expansion.

| 1992 | 2002 | 2012 | |

|---|---|---|---|

| Commuting Zones per firm | 131.5 | 154.7 | 169.2 |

| Establishments per firm | 616.2 | 686.7 | 814.9 |

| National market share | 0.388 | 0.533 | 0.581 |

| Local market share | 0.032 | 0.033 | 0.034 |

-

•

Notes: The numbers come from the Census of Retail Trade and report averages across retailers with establishments in at least 50 commuting zones in a given year. National market share is the total sales of establishments of these firms in sales of product categories in our sample divided by total sales of product categories in sample. The local market share is a simple average across commuting zones, product categories, and firms of the market share of firms active in a given product category and commuting zone in a given year. (CBDRB-FY23-P1975-R10585)

We find that most of the increase in U.S. retail concentration comes from the expansion of multi-market retailers, with consolidation in markets they are already in playing a minor role. We do this by taking into account the behavior of all U.S. retailers and conducting an additional counterfactual exercise that allows us to isolate the changes in national concentration coming from higher concentration at the local level (consolidation) from those coming from the expansion of firms across markets, all while being consistent with the observed evolution of local concentration.

To isolate the contribution of within-market consolidation, we generate a counterfactual economy where the rank of firms is preserved across time.222222 We thank an anonymous referee for suggesting this exercise. This means that the identity of the leader in each market is counterfactually preserved, as is the identity of the rth largest firm in the market at time , and they are assigned the sales share of the corresponding rth largest firm in the market at time . In this way, the counterfactual economy assigns the increases in local market shares to consolidation of existing firms (the previous leaders) and not to changes induced by the expansion of firms into new markets. The counterfactual preserves the local market structure of time and replicates the changes in local concentration by construction.

Formally, for each product , we consider all firms active at some time in each location and record their rank . These ranks capture the market structure at time in each local product market. We then consider a future time and assign to each firm active at time the share of the firm with the same rank operating in time : , where gives the identity of the largest firm selling product , in location at time and if . So that the counterfactual matches the evolution of local concentration, we first assign market shares to the firms operating at time and then assign any remaining market shares to entrants (in order of rank in ). Having completed this process, we aggregate the counterfactual shares at the national level, and compute the national HHI as in (1).

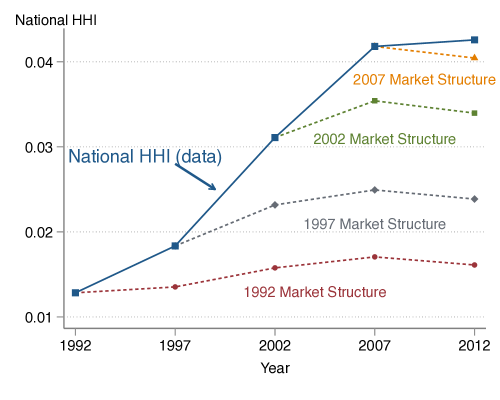

We conduct the counterfactual taking the market structure of each census year and present the results in Figure 6. Without the expansion of retailers across markets the national HHI would have only increased 0.33 percentage points between 1992 and 2012, this is just 11 percent of the observed change in concentration. The share of the increase in concentration accounted for within-market consolidation does rise when we start from the 1997 or 2002 market structure. Consolidation explains up to 40 percent of the increase in the 1997–2007 period, the years when national concentration increased the most. Nevertheless, the message is clear. The majority of the increase in U.S. retail concentration comes from the increase in the market share of multi-market retailers as they expand into new markets.

The same pattern of low but increasing importance of consolidation holds when we look at the evolution of concentration across product categories. Take, for example, the largest product category, groceries. Where expansion accounts for 92 percent of the change in national concentration between 1992 and 2002, falling to 80 percent between 2002 and 2012. These results align with the behavior of large general merchandisers like Walmart, that expanded into new markets during the 1980s and 1990s ((Holmes, 2011, Fig. 2, pg. 255) and went from not selling groceries to being the largest grocer in the U.S. ((Basker, 2007). We extend these results and show that within-market consolidation plays a larger role in the period after 1997. Our data indicates that this was part of a broader phenomena across multiple product categories. However, there are two categories that stand as outliers. Consolidation captures less than 2 percent of the increase in concentration in Clothing between 1992 and 2002, while it accounts for 60 percent of the increase in concentration in Sporting Goods between 1992 and 2002, and 84 percent between 2002 and 2012.

5 Local Retail Concentration and Retailers’ Margins

The previous sections document increases in product- and industry-based measures of local retail concentration that are broad based and follow the overall trend of higher national concentration in Retail and other sectors. These trends in concentration can imply higher markups and ultimately affect consumer prices. However, studying this relationship is challenging because long series on prices or costs for U.S. retailers are unavailable. We now provide a discussion of the magnitude of these effects in light of the observed increases in retailers’ gross margins.

To get a sense of the potential effect of concentration on markups and deal with data limitations, we use the relationship between market profitability and market concentration as measured by the HHI that arises under Cournot competition ((e.g., Tirole, 1988, pg. 221-223). The gross margins in a local product or industry market satisfy232323 The relationship above applies when goods are homogeneous, however, we generalize it to the case in which goods are differentiated and preferences are homothetic in Appendix F. Then, the gross-margin is approximately given by . This is the same relationship between gross margins and concentration in models of oligopolistic competition like Atkeson and Burstein ((2008) and Grassi ((2017).

| (6) |

where is the elasticity of demand. This relationship gives us a measure of the effect of the change in local concentration on retailers’ margins coming from the increased market power of retailers in the local markets they operate in.

| Products | Industry | |||||

|---|---|---|---|---|---|---|

| Commuting Zone | 1.59 | 0.75 | 0.37 | 11.89 | 4.95 | 2.27 |

| Zip Code | 1.27 | 0.52 | 0.23 | 14.87 | 4.34 | 1.74 |

We use our measures of the local HHI for product and industry markets to get the changes in firms’ margins between 1992 and 2012 implied by equation (6). We do this for different values of the elasticity of demand based on the range of estimates in Brand ((2020, fig. 3). As shown in Table 5, the change in local product concentration implies an increase in margins of 1.6 percentage points for a low value of , but the number is cut almost by half for larger values of the elasticity of demand. The changes implied by industry concentration are much larger, reflecting the findings of Section 3.4 documenting that the increases in concentration are larger at the industry than at the product level. Industry concentration implies increases in markups between 14.9 and 1.7 percentage points. However, these magnitudes can be misleading as they do not take into account cross-industry competition taking place in retail.

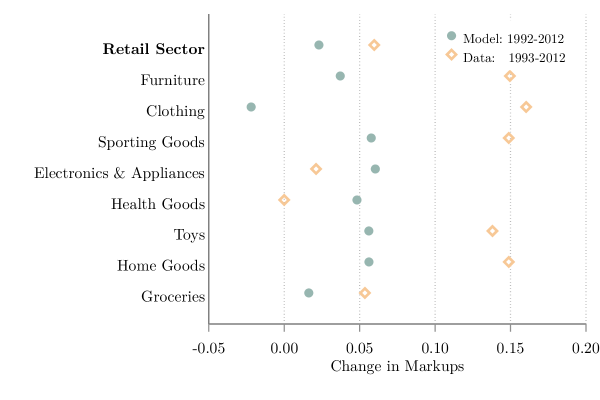

The change in margins in product markets implied by local product concentration is meaningful and accounts for about one-fourth of the observed changes in retailers gross margins from the Annual Retail Trade Survey (ARTS).242424 The changes in markups implied by local concentration as well as the changes in retailers gross margins from the ARTS are significantly lower than those found for retail by De Loecker et al. ((2020, fig. VI). The ARTS data show an increase in retailers’ margins of 6.0 percentage points between 1993 and 2012 ((U.S. Census Bureau, 1993-2012). Moreover, taking into account the differences in concentration trends and elasticities of demand across products implies a larger increase in margins. In Appendix G, we estimate a model of oligopolistic competition in local product markets based on Atkeson and Burstein ((2008) and find that average product markups increase by 2.1 percentage points between 1992 and 2012, or about one-third of the increase in margins reported in the ARTS.

Looking forward, the growth of multi-market and online retail presents new challenges for understanding retail markets. There is evidence that multi-market firms charge uniform prices across locations ((Adams and Williams, 2019; Dellavigna and Gentzkow, 2019). This practice initially leads to lower markups because larger (less concentrated) markets have more weight in the pricing decisions of multi-market retailers (Appendix G.6). Simultaneously, the growth of e-commerce has led to new options for consumers in all markets, but much of this growth is due to a few large firms and may have caused the closing of brick-and-mortar retailers.

6 Conclusion

Consumers have traditionally chosen between nearby stores selling a given product when purchasing goods. This fact makes local market conditions relevant for assessing the competitive environment in the retail sector. Accordingly, we measure concentration on local product markets using novel Census data on all U.S. retailers. We find increases in concentration covering the majority of markets which hold for product- and industry-based measures of concentration, even after taking into account the role of online and other non-store retailers. These trends match that of national retail concentration that also rises strongly between 1992 and 2012.

Further, we show that the trends of increasing national and local concentration are linked through the expansion and consolidation of multi-market firms, with single-market firms playing no role in the increase of national concentration. We find that the observed increases in national concentration between 1992 and 2002 are due mostly to the expansion of multi-market firms into new markets, with consolidation of these firms in the markets they operate in increasing in importance in the 2002-2007 period.

The increases in local concentration that we document can account for one-quarter to one-third of the rise in retailers’ gross margins observed in the retail sector by increasing retailers’ local market power. This can reflect an increase in markups that can potentially hurt consumers. However, if increases in concentration are caused by low-cost multi-market firms increasing their market share, prices may fall despite increases in markups ((Bresnahan, 1989). In fact, the 1.6 percentage point increase in markups due to local concentration is small relative to the 34 percent decrease in relative retail prices observed in the same period. These cost advantages may be due to direct foreign sourcing ((Smith, 2019), negotiating power with suppliers ((Benkard et al., 2021), or investments in information and communication technologies ((Hsieh and Rossi-Hansberg, 2023). Moreover, increases in e-commerce penetration since 2012 may have tempered the increasing trends in local concentration.

References

- Adams and Williams ((2019) Adams, Brian and Kevin R. Williams, 2019. “Zone Pricing in Retail Oligopoly.” American Economic Journal: Microeconomics 11(1):124–56, https://dx.doi.org/10.1257/mic.20170130.

- Arcidiacono et al. ((2016) Arcidiacono, Peter, Patrick Bayer, Jason R Blevins, and Paul B Ellickson, 2016. “Estimation of Dynamic Discrete Choice Models in Continuous Time with an Application to Retail Competition.” Review of Economic Studies 83(3):889–931, https://dx.doi.org/10.1093/restud/rdw012.

- Atkeson and Burstein ((2008) Atkeson, Andrew and Ariel Burstein, 2008. “Pricing-to-Market, Trade Costs, and International Relative Prices.” American Economic Review 98(5):1998–2031, https://dx.doi.org/10.1257/aer.98.5.1998.

- Autor et al. ((2020) Autor, David H., David Dorn, Lawrence F. Katz, Christina Patterson, and John Van Reenen, 2020. “The Fall of the Labor Share and the Rise of Superstar Firms.” The Quarterly Journal of Economics 135(2):645–709, https://dx.doi.org/10.1093/qje/qjaa004.

- Azar et al. ((2019) Azar, José, Steven T. Berry, and Ioana Elena Marinescu, 2019. “Estimating Labor Market Power.” https://dx.doi.org/10.2139/ssrn.3456277 (accessed 2020-03-20).

- Azar et al. ((2022) Azar, José, Yue Qiu, and Aaron Sojourner, 2022. “Common Ownership in Labor Markets.” Upjohn Institute Working Paper Series No 22-368, https://dx.doi.org/0.17848/wp22-368.

- Barnatchez et al. ((2017) Barnatchez, Keith, Leland Dod Crane, and Ryan A. Decker, 2017. “An Assessment of the National Establishment Time Series (Nets) Database.” Board of Governors of the Federal Reserve System: Finance and Economics Discussion Series No. 2017-1, https://dx.doi.org/10.17016/FEDS.2017.110.

- Basker ((2005) Basker, Emek, 2005. “Job Creation or Destruction? Labor Market Effects of Wal-Mart Expansion.” The Review of Economics and Statistics 87(1):174–183, https://dx.doi.org/10.1162/0034653053327568.

- Basker ((2007) Basker, Emek, 2007. “The Causes and Consequences of Wal-Mart’s Growth.” Journal of Economic Perspectives 21(3):177–198, https://dx.doi.org/10.1257/jep.21.3.177.

- Basker et al. ((2012) Basker, Emek, Shawn D Klimek, and Pham Hoang Van, 2012. “Supersize It: The Growth of Retail Chains and the Rise of the ”Big-Box” Store.” Journal of Economics and Management Strategy 21(3):541–582, https://dx.doi.org/10.1111/j.1530-9134.2012.00339.x.

- Benkard et al. ((2021) Benkard, C. Lanier, Ali Yurukoglu, and Anthony Lee Zhang, 2021. “Concentration in Product Markets.” National Bureau of Economic Research Working Paper Series No. 28745, https://dx.doi.org/10.3386/w28745.

- Berger et al. ((2022) Berger, David, Kyle Herkenhoff, and Simon Mongey, 2022. “Labor Market Power.” American Economic Review 112(4):1147–93, https://dx.doi.org/10.1257/aer.20191521.

- Bornstein ((2018) Bornstein, Gideon, 2018. “Entry and Profits in an Aging Economy: The Role of Consumer Inertia.” https://www.dropbox.com/s/8ud1oukigjqd9i6/JMP_Bornstein.pdf (accessed 2020-12-15).

- Brand ((2020) Brand, James, 2020. “Differences in Differentiation: Rising Variety and Markups in Retail Food Stores.” https://www.jamesbrandecon.com/s/Brand_JMP_Oct10.pdf (accessed 2020-12-15).

- Bresnahan ((1989) Bresnahan, Timothy F., 1989. “Empirical studies of industries with market power.” Handbook of Industrial Organization pp. 1011–1057, ch 17, vol. 2, https://dx.doi.org/10.1016/S1573-448X(89)02005-4.

- Bureau of Labor Statistics ((2019) Bureau of Labor Statistics, 2019. “Current Employment Statistics.” https://www.bls.gov/ces/ (accessed 2020-03-20).

- Cao et al. ((2019) Cao, Dan, Henry R. Hyatt, Toshihiko Mukoyama, and Erick Sager, 2019. “Firm Growth Through New Establishments.” https://dx.doi.org/10.2139/ssrn.3361451 (accessed 2019-09-23).

- Crane and Decker ((2020) Crane, Leland Dod and Ryan A. Decker, 2020. “Research with private sector business microdata: The case of NETS/D&B.” https://conference.nber.org/conf_papers/f142811.pdf (accessed 2020-01-04).

- De Loecker et al. ((2020) De Loecker, Jan, Jan Eeckhout, and Gabriel Unger, 2020. “The Rise of Market Power and the Macroeconomic Implications.” The Quarterly Journal of Economics 135(2):561–644, https://dx.doi.org/10.1093/qje/qjz041.

- Decker ((2020) Decker, Ryan, 2020. “Discussion of “Diverging Trends in National and Local Concentration”.” https://rdeckernet.github.io/website/2020ASSA_discussion_RST.pdf.

- Decker et al. ((2014) Decker, Ryan A., John C Haltiwanger, Ron S. Jarmin, and Javier Miranda, 2014. “The Role of Entrepreneurship in US Job Creation and Economic Dynamism.” Journal of Economic Perspectives 28(3):3–24, https://dx.doi.org/10.1257/jep.28.3.3.

- Decker et al. ((2020) Decker, Ryan A., John C Haltiwanger, Ron S. Jarmin, and Javier Miranda, 2020. “Changing Business Dynamism and Productivity: Shocks vs. Responsiveness.” American Economic Review 110(12):3952–90, https://dx.doi.org/10.1257/aer.20190680.

- Dellavigna and Gentzkow ((2019) Dellavigna, Stefano and Matthew Gentzkow, 2019. “Uniform Pricing in U.S. Retail Chains.” The Quarterly Journal of Economics 134(4):2011–2084, https://dx.doi.org/10.1093/qje/qjz019.

- Department of Justice and Federal Trade Commission ((2010) Department of Justice and Federal Trade Commission, 2010. “Horizontal Merger Guidelines.” Tech. rep., Department of Justice, Federal Trade Commission. https://www.justice.gov/atr/file/810276/download (accessed 2019-09-23).

- Edmond et al. ((2019) Edmond, Chris, Virgiliu Midrigan, and Daniel Yi Xu, 2019. “How Costly Are Markups?” http://www.virgiliumidrigan.com/uploads/1/3/9/8/13982648/how-costly-markups-01-14-19.pdf (accessed 2019-09-23).

- Fort and Klimek ((2018) Fort, Teresa C and Shawn D Klimek, 2018. “The Effects of Industry Classification Changes on US Employment Composition.” U.S. Census Bureau Center for Economic Studies Working Papers No. 18-28, https://www.census.gov/library/working-papers/2018/adrm/ces-wp-18-28.html.

- Foster et al. ((2006) Foster, Lucia, John Haltiwanger, and C. J Krizan, 2006. “Market Selection, Reallocation, and Restructuring in the U.S. Retail Trade Sector in the 1990s.” Review of Economics and Statistics 88(4):748–758, https://dx.doi.org/10.1162/rest.88.4.748.

- Foster et al. ((2016) Foster, Lucia, John C Haltiwanger, Shawn D Klimek, C.J. Krizan, and Scott Ohlmacher, 2016. “The Evolution of National Retail Chains: How We Got Here.” Handbook on the Economics of Retailing and Distribution pp. 7–37, ch 1, https://dx.doi.org/10.4337/9781783477388.

- Ganapati ((2021) Ganapati, Sharat, 2021. “Growing Oligopolies, Prices, Output, and Productivity.” American Economic Journal: Microeconomics 13(3):309–27, https://dx.doi.org/10.1257/mic.20190029.

- Grassi ((2017) Grassi, Basile, 2017. “IO in I-O: Size, Industrial Organization, and the Input-Output Network Make a Firm Structurally Important.” https://sites.google.com/site/grassibasile/home/research/job-market-paper (accessed 2020-04-23).

- Grullon et al. ((2019) Grullon, Gustavo, Yelena Larkin, and Roni Michaely, 2019. “Are US Industries Becoming More Concentrated?” Review of Finance 23(4):697–743, https://dx.doi.org/10.1093/rof/rfz007.

- Hall ((2018) Hall, Robert E, 2018. “New Evidence of the Markup of Prices Over Marginal Costs and the Role of Mega-Firms in the US Economy.” National Bureau of Economic Research Working Paper Series No. 24574, https://dx.doi.org/10.3386/w24574.

- Haltiwanger et al. ((2010) Haltiwanger, John C, Ron S. Jarmin, and C. J. Krizan, 2010. “Mom-and-Pop Meet Big-Box: Complements or Substitutes?” Journal of Urban Economics 67(1):116–134, https://doi.org/10.1016/j.jue.2009.09.003.

- Holmes ((2011) Holmes, Thomas J., 2011. “The Diffusion of Wal-Mart and Economies of Density.” Econometrica 79(1):253–302, https://dx.doi.org/https://doi.org/10.3982/ECTA7699.

- Hortaçsu and Syverson ((2015) Hortaçsu, Ali and Chad Syverson, 2015. “The Ongoing Evolution of US Retail: A Format Tug-of-War.” Journal of Economic Perspectives 29(4):89–112, https://dx.doi.org/10.1257/jep.29.4.89.

- Hsieh and Rossi-Hansberg ((2023) Hsieh, Chang-Tai and Esteban Rossi-Hansberg, 2023. “The Industrial Revolution in Services.” Journal of Political Economy Macroeconomics 1(1):3–42, https://dx.doi.org/10.1086/723009.

- Jarmin and Miranda ((2002) Jarmin, Ron S. and Javier Miranda, 2002. “Data for: The Longitudinal Business Database (1976-2012).” https://www2.census.gov/library/working-papers/2002/adrm/ces-wp-02-17.pdf (accessed 2020-03-01).

- Jarosch et al. ((2020) Jarosch, Gregor, Jan Sebastian Nimczik, and Isaac Sorkin, 2020. “Granular Search, Market Structure, and Wages.” National Bureau of Economic Research Working Paper Series No. 26239, https://dx.doi.org/10.3386/w26239.

- Jia ((2008) Jia, Panle, 2008. “What Happens When Wal-Mart Comes to Town: An Empirical Analysis of the Discount Retailing Industry.” Econometrica 76(6):1263–1316, https://dx.doi.org/10.3982/ECTA6649.

- Leung and Li ((2022) Leung, Justin and Zhonglin Li, 2022. “Big-Box Store Expansion and Consumer Welfare.” https://drive.google.com/file/d/1qXZHcAwREzDlsZNp5w3EVsOZnqjBnEA1.

- Leung and Li ((2023) Leung, Justin and Zhonglin Li, 2023. “Rising Retail Concentration: Superstar Firms and Household Demand.” https://drive.google.com/file/d/1LfmztMkSl7nKJYgzR3wjxk9P90Y072Vx.

- Lipsius ((2018) Lipsius, Ben, 2018. “Labor Market Concentration Does Not Explain the Falling Labor Share.” https://ideas.repec.org/p/jmp/jm2018/pli1202.html (accessed 2019-09-23).

- Miranda et al. ((2004) Miranda, Javier, Shawn D. Klimek, and R. Jarmin, 2004. “Firm Entry and Exit in the U.S. Retail Sector, 1977-1997.” Center for Economic Studies, Discussion Papers 04-17, U.S. Census Bureau. https://www2.census.gov/ces/wp/2004/CES-WP-04-17.pdf.

- Neiman and Vavra ((2020) Neiman, Brent and Joseph S. Vavra, 2020. “The Rise of Niche Consumption.” National Bureau of Economic Research Working Paper Series No 26134, https://dx.doi.org/10.3386/w26134.

- Rinz ((2020) Rinz, Kevin, 2020. “Labor Market Concentration, Earnings, and Inequality.” Journal of Human Resources https://dx.doi.org/10.3368/jhr.monopsony.0219-10025R1.

- Rossi-Hansberg et al. ((2021) Rossi-Hansberg, Esteban, Pierre-Daniel Sarte, and Nicholas Trachter, 2021. “Diverging trends in national and local concentration.” NBER Macroeconomics Annual 35(1):115–150, https://dx.doi.org/10.1086/712317.

- Securities and Exchange Commission ((2020) Securities and Exchange Commission, 2020. “Walmart Inc. EDGAR Results.” https://www.sec.gov/cgi-bin/browse-edgar?action=getcompany&CIK=0000104169&owner=exclude&count=40&hidefilings=0 (accessed 2020-01-31).

- Seo ((2019) Seo, Boyoung, 2019. “Firm Scope and the Value of One-Stop Shopping in Washington State’s Deregulated Liquor Market.” http://doi.wiley.com/10.1002/cbm.1988 (accessed 2021-09).

- Smith ((2019) Smith, Dominic, 2019. “Concentration and Foreign Sourcing in the U.S. Retail Sector.” https://dominic-smith.com/smith_jmp2.pdf (accessed 2021-03).

- Tirole ((1988) Tirole, Jean, 1988. “The Theory of Industrial Organization.” https://mitpress.mit.edu/9780262200714/the-theory-of-industrial-organization/.

- Trachter ((2021) Trachter, Nicholas, 2021. “Discussion of ”The Evolution of U.S. Retail Concentration”.” NBER CRIW Summer Institute.

- Traina ((2018) Traina, James, 2018. “Is Aggregate Market Power Increasing? Production Trends Using Financial Statements.” Stigler Center for the Study of the Economy and the State: New Working Paper Series No. 17, https://research.chicagobooth.edu/-/media/research/stigler/pdfs/workingpapers/17isaggregatemarketpowerincreasing.pdf.

- U.S. Bureau of Labor Statistics ((1982-2012) U.S. Bureau of Labor Statistics, 1982-2012. “Consumer Price Index Deflators.” https://www.bls.gov/cpi/ (accessed 2020-01-01).

- U.S. Census Bureau ((1992-2012) U.S. Census Bureau, 1992-2012. “Census of Retail Trade - Base and Lines Files.” https://www.census.gov/programs-surveys/ces/data/restricted-use-data/economic-data.html (accessed 2020-03-01). Federal Statistical Research Data Center [distributor].

- U.S. Census Bureau ((1993-2012) U.S. Census Bureau, 1993-2012. “Annual Retail Trade Survey.” https://www.census.gov/programs-surveys/arts/data/tables.html (accessed 2020-03-01).

- U.S. Census Bureau ((2002) U.S. Census Bureau, 2002. “Census of Retail Trade - Public Files.” https://www.census.gov/library/publications/2002/econ/census/retail-trade.html (accessed 2020-04-01).

Online Appendix

The Evolution of U.S. Retail Concentration111Any views expressed are those of the authors and not those of the U.S. Census Bureau. The Census Bureau’s Disclosure Review Board and Disclosure Avoidance Officers have reviewed this information product for unauthorized disclosure of confidential information and have approved the disclosure avoidance practices applied to this release. This research was performed at a Federal Statistical Research Data Center under FSRDC Project Numbers 1179 and 1975 (CBDRB-FY19-P1179-R7207, CBDRB-FY20-P1975-R8604 and CBDRB-FY23-P1975-R10585).

Dominic A. Smith222Bureau of Labor Statistics; Email: smith.dominic@bls.gov; Web: https://www.bls.gov/pir/authors/smith.htm. & Sergio Ocampo333University of Western Ontario; Email: socampod@uwo.ca; Web: https://sites.google.com/site/sergiocampod/.

Appendix A Concentration Decomposition

We calculate the HHI for the retail sector at a time , as the sales-weighted average of the product-HHIs:

| (A.1) |

The HHI for a given product , , can be decomposed into the contribution of local and cross-market concentration. The decomposition starts from the probability that two dollars spent on a product during some time period are spent at the same firm , which gives the HHI at the national level:

| (A.2) |

where is the share of firm in product during period . This probability can be divided into two terms by conditioning on the dollars being spent in the same location, :

| (A.3) | ||||

When we report contribution of local and cross-market concentration for the retail sector, we report the sales-weighted average of these two terms across products.

The collocation probability is calculated as:

| (A.4) |

When we report the collocation for the retail sector, we report the sales-weighted average of collocation across products: .

The first component, , is an aggregate index of local concentration, with local concentration measured as in equation (2).444 In the decomposition, each local market is weighted by the conditional probability that the two dollars are spent in location given that they are spent in the same location: . These weights give more importance to larger markets than the more usual weights —the share of sales (of product ) accounted for by location (at time ). We present aggregated series for local concentration in Section 3 that use the latter weights. Appendix A derives these results in detail. This captures the extent to which consumers in a local market shop at the same firm. Local concentration is calculated as:

| (A.5) |

In the main text, when we report the local HHI for individual product categories we also report the retail sector’s average local HHI using sales weights instead of the weights implied by the decomposition to facilitate comparison to other research:

| (A.6) |

The third component, , which we call cross-market concentration, captures the probability that a dollar spent in different markets is spent at the same firm:

| (A.7) |

The cross-market concentration between two markets (say and ) is given by the product of the shares of the firms in each location (the probability that two dollars spent in different locations are spent in the same firm). The pairs of markets are then weighted by their share of sales and are summed.

The cross-market term as a whole is calculated as: