Multivariate Analysis for Multiple Network Data via Semi-Symmetric Tensor PCA

Abstract

Network data are commonly collected in a variety of applications, representing either directly measured or statistically inferred connections between features of interest. In an increasing number of domains, these networks are collected over time, such as interactions between users of a social media platform on different days, or across multiple subjects, such as in multi-subject studies of brain connectivity. When analyzing multiple large networks, dimensionality reduction techniques are often used to embed networks in a more tractable low-dimensional space. To this end, we develop a framework for principal components analysis (PCA) on collections of networks via a specialized tensor decomposition we term Semi-Symmetric Tensor PCA or SS-TPCA. We derive computationally efficient algorithms for computing our proposed SS-TPCA decomposition and establish statistical efficiency of our approach under a standard low-rank signal plus noise model. Remarkably, we show that SS-TPCA achieves the same estimation accuracy as classical matrix PCA, with error proportional to the square root of the number of vertices in the network and not the number of edges as might be expected. Our framework inherits many of the strengths of classical PCA and is suitable for a wide range of unsupervised learning tasks, including identifying principal networks, isolating meaningful changepoints or outlying observations, and for characterizing the “variability network” of the most varying edges. Finally, we demonstrate the effectiveness of our proposal on simulated data and on an example from empirical legal studies. The techniques used to establish our main consistency results are surprisingly straightforward and may find use in a variety of other network analysis problems.

Keywords: Principal components analysis, network analysis, tensor decomposition, semi-symmetric tensor, CP factorization, regularized PCA

1 Introduction

Principal Components Analysis (PCA) is a fundamental tool for the analysis of multivariate data, enabling a wide range of dimension reduction, pattern recognition, and visualization strategies. Originally introduced by [55] and [32] for investigating low-dimensional data in a Euclidean space, PCA has been generalized to much more general contexts, including data taking values in general inner product spaces [18], (possibly infinite-dimensional) function spaces [59], discrete and compositional spaces [44], and shape spaces [37]. In this work, we analyze PCA-type decompositions for network data: that is, given a collection of undirected networks on a common set of nodes, we seek to identify common patterns in the form of one or more “principal networks” that capture most of the variation in our data. Our main technical tool is a tensor decomposition on so-called semi-symmetric tensors, for which we provide an efficient computational algorithm and rigorous statistical guarantees, in the form of a general finite sample consistency result. As we show below, our approach achieves the same convergence rates as classical (Euclidean) PCA up to a logarithmic factor, with error proportional to the square root of the number of vertices rather than the number of edges, providing significant improvements when analyzing networks of even moderate size.

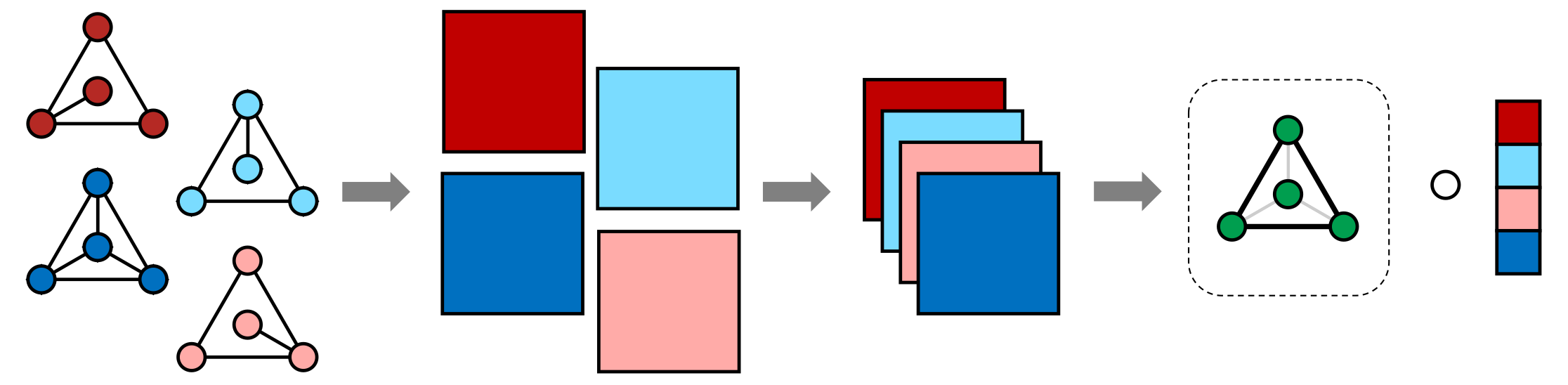

Network-valued data are of increasing importance in analyzing modern structured data sets. In many situations, multiple networks are observed in conjunction with the same phenomenon, typically when independent replicates are observed over time (“network series”) or when different network representations of the same underlying dynamics can be observed [38]. Notable examples of this type of data can be found in neuroscience [78], group social dynamics [17], international development [25], and transportation studies [12]. Because these undirected (weighted) networks are observed on a common known set of nodes, they can each be represented as symmetric matrices and these symmetric matrices can be stacked into a third-order semi-symmetric tensor, i.e., a tensor each slice of which is a symmetric matrix. In this paper, we study the decomposition depicted in Figure 1: that is, decomposing a semi-symmetric tensor into a “principal network” term as well as a loading vector. More details of this decomposition follow in Section 2.

In this paper, we focus on scenarios where networks are directly observed and the structure of the networks is of primary interest. We distinguish this from closely related problems arising in the analysis of network-structured signals, i.e., graph signal processing [58], or in estimating network structure from observed multivariate data, i.e., structure learning of probabilistic graphical models [47, Part III].

1.1 Selected Background and Related Work

We take the “canonical polyadic” or “CP” tensor decomposition framework as our starting point. The CP decomposition approximates a tensor by a sum of rank-1 components, which are typically estimated using an alternating least squares approach [92, Section 3]. The CP decomposition has been applied as the basis for various forms of tensor PCA, where it is preferred over Tucker-type decompositions because it provides interpretable and ordered components, similar to those resulting from classical (matrix) PCA [75]. For scalar data arranged in a tensor, CP-based tensor PCA exhibits strong performance and has been fruitfully extended to sparse and high-dimensional settings with efficient algorithms [82, 81], but it is less ideal for network settings. Specifically, CP-based approaches decompose a tensor into rank-1 components, but realistic networks essentially never have exact rank-1 structure, as this would imply a uniform connectivity pattern across all nodes. This problem—developing an efficient tensor decomposition and PCA framework which captures meaningful network structure—motivates the “semi-symmetric tensor PCA” (SS-TPCA) decomposition at the heart of this paper.

While computational theory for tensor decompositions is well-established, comprehensive statistical theory remains an active area of research in the statistics and machine learning communities. [5] give a general analysis of statistical estimation under CP-type models, developing incoherence conditions that allow recovery of multiple CP factors. Extending their analysis to the sparse CP framework of [81], [60] establish consistency and sparse recovery under additional sparsity and incoherence assumptions. Consistency results have also been established for tensor decompositions using the Tucker [77, 76] and Tensor-Train [54, 80] frameworks. A recent paper by [28] considers general estimation problems under a low Tucker-rank assumption and establishes convergence guarantees for a wide range of problems, including low-rank approximation, tensor completion, and tensor regression. For tensors with symmetric structure, Anandkumar and co-authors [4, 34] analyze decompositions of fully-symmetric tensors, such as those arising in certain method-of-moments estimation schemes. The fully-symmetric case imposes additional computational concerns not present in the general case: [40] discusses these issues and reviews related work in more detail. The tensor statistical estimation literature is too large to be comprehensively described here and we refer the reader to the recent survey by [9] for additional references.

While we are the first to provide rigorous statistical theory for semi-symmetric tensor decompositions, these techniques have already found wide use in the literature. In particular, our SS-TPCA builds upon the Network Tensor PCA proposal of [78] who apply tensor techniques to brain connectivity in order to find connectomic structures correlated with a variety of interesting behavioral traits. [71] extend this approach to matrices of allow for graphs of different granularity, yielding an approach which is robust to the particular brain parcellation used. [68] use a different semi-symmetric decomposition to perform Independent Components Analysis on spectroscopy data. Despite the empirical successes of these approaches, this work is the first to provide rigorous theoretical guarantees of the type presented in Theorem 1 below.

Separately, the task of finding common low-rank subspace representations of multiple graphs has been well-studied in the network science community. The recent work of [69] is particularly closely related to our work: both papers consider a tensor decomposition approach to learning common features among a set of graphs. Our results significantly improve upon their findings, as we are able to give finite-sample results on the quality of both the estimated principal components and the loading vector under a general “low-rank” model, while they only give an asymptotic consistency result for the principal component under a particular rank-1 variant of the Erdős-Rényi model. Similarly, the COSIE proposal of [6] develops a spectral embedding approach for multiple graphs, but does so leveraging techniques from distributed estimation rather than tensor decompositions and under a different probabilistic model than we consider below.

Our approach is motivated by the statistical analysis of multiple networks, an area of much recent activity. In addition to the embedding analysis described above, we highlight several recent advances in this space including: spectral clustering of network-valued data [51]; model-based clustering of network valued data [49];probabilistic models and Bayesian estimators for network series [57, 23, 16]; factor models for matrix time series [13]; two-sample testing [22]; and scalar-on-network regression [7, 24]. We expect that a robust Network PCA framework, such as that associated with our approach, can lead to advances in many of these objectives.

1.2 Notation

Notation used in this paper follows that of [92] with two minor modifications: firstly, in the tensor-matrix product, , we omit a transpose implicitly used by [92]: for two matrices we have while they have . Consequently, we have rather than . In general, the appropriate axes on which to multiply are clear from context. Secondly, while denotes the general outer product, we also adopt the convention that when it is applied to two matrices of equivalent size, it denotes a matrix product with its transpose, not a higher order product: that is, if , , a matrix, not a tensor. Unless otherwise noted, inner products and norms refer to the Frobenius norm and associated inner product ( and ). We denote the (compact) Stiefel manifold by . We will make frequent use of the fact that, for any , is a rank- matrix of size .

Semi-symmetric tensors are third-order tensors, i.e., three dimensional arrays, each slice of which along a fixed axis yields a (real) symmetric matrix. By convention, we take the first two dimensions to be the axes of symmetry, so is a semi-symmetric tensor if is a symmetric matrix for all . We introduce several notations for non-standard tensor operations which arise naturally in the semi-symmetric context: for a semi-symmetric tensor and a matrix , we define the trace-product as the -vector whose element is given by . For a symmetric matrix , denotes the -vector formed from the upper triangle of ; denotes the inverse vector-to-symmetric matrix mapping. Finally, the operator norm of a symmetric matrix is given by the absolute value of the largest magnitude eigenvalue and the rank- operator norm of a semi-symmetric tensor is defined as , where is the unit ball in . In general, the semi-symmetric tensor operator norm is difficult to compute, but Proposition 1 in Section 3 gives a tractable upper bound in terms of the operator norm of the individual slices of .

1.3 Our Contributions

Our contributions are threefold: firstly, building on a proposal of [78], we develop a computationally efficient flexible tensor PCA framework that is able to characterize networks arising from a large class of random graph models; secondly, we establish statistical consistency of the SS-TPCA procedure under fairly weak and general assumptions, centered on a tensor analogue of the low-rank mean model; finally, we establish a novel connection between multilayer network analysis and regularized -estimation that is of significant independent theoretical interest.

The remainder of this paper is organized as follows: Section 2 introduces the “Semi-Symmetric Tensor PCA” decomposition (SS-TPCA) and proposes an efficient algorithm for computing the SS-TPCA solution; in this section, we also discuss several useful aspects of the SS-TPCA framework, including procedures for computing multiple principal components and an extension to a functional PCA-type setting. Section 3 further examines the theoretical properties of the SS-TPCA via a simple, yet novel, analytical framework we expect may find use in other contexts; Section 3.1 connects these results to the wider literature on regularized Principal Components Analysis and shows how the technical tools we develop can be used for other -estimation problems arising from network-valued data. Section 4 demonstrates the usefulness and flexibility of the SS-TPCA framework, both in simulation studies and in an extended case study from empirical legal studies. Finally, Section 5 concludes the paper and discusses several possible future directions for investigation.

2 Semi-Symmetric Tensor Principal Components Analysis

Our goal is to develop a tensor PCA framework which is able to capture realistic network structures in its output. While real-world networks have a variety of structures, we focus here on networks which are (approximately) low-rank, as these are most well-suited for PCA-type analyses. Many network models are approximately low-rank in expectation, most notably, the random dot-product graph family [8], which includes both latent position and stochastic block models as special cases. These models have found use in a wide range of contexts, including analysis of social media networks, brain connectivity networks, and genomic networks [61, 45].

With these low-rank models in mind, we introduce our “Semi-Symmetric Tensor PCA” (SS-TPCA) factorization, which approximates a semi-symmetric tensor by a rank- “principal component” and a loading vector for the final mode, which we typically take to represent independent replicates observed over time. As seen in the sequel, it is natural in many applications to interpret these as a “principal network” and a “time factor,” but this viewpoint is not essential for the technical developments of this section.

The single-factor rank- SS-TPCA approximates as

where is a unit-norm -vector, is a scale factor, and is an orthogonal matrix satisfying . When and is a unit vector, this coincides with the Network PCA approach of [78]. This decomposition is related to the standard -term CP decomposition:

with the additional restrictions and for all as well as to ensure orthogonality. These constraints restrict the number of free parameters from to , which significantly improves both computational performance and estimation accuracy, as will be described in more detail below.

A more general SS-TPCA, which we denote as the -SS-TPCA, may be defined by

where, as before, each is a unit-norm -vector, are positive scale factors, and are orthogonal matrices used to construct the low-rank principal networks. We emphasize that the terms need not be of the same dimension, allowing our model to flexibly capture principal components of differing rank. The general SS-TPCA model inherits properties of both the popular CP and Tucker decompositions: it approximates by the sum of multiple simple components like the CP decomposition but allows for orthogonal low-rank factors like the Tucker decomposition.

To compute the single-factor SS-TPCA, we seek the best approximation of in the tensor Frobenius norm:

It is easily seen that solving this problem is equivalent to minimizing the inner product:

While this problem is difficult to optimize jointly in and , closed-form global solutions are available both for with held constant and for with held constant. This motivates an alternating minimization (block coordinate descent) strategy comprised of alternating and updates. Specifically, holding constant, the optimal value of is simply the principal eigenvalues of and, holding constant, the optimal value of is a unit vector in the direction of . Note that, for the single factor rank-1 SS-TPCA, the -update simplifies to . Putting these steps together, we obtain the following algorithm for the single-factor rank- SS-TPCA decomposition:

-

•

Input: ,

-

•

Initialize:

-

•

Repeat until convergence:

-

(i)

-

(ii)

-

(iii)

-

(i)

-

•

Return , , , and .

where and denotes the first eigenvectors of . When has both positive and negative eigenvalues, denotes those eigenvectors whose eigenvalues have the largest magnitudes. Convergence of Algorithm 1 follows from the general block coordinate analysis of [64] or from a minor extension of the results of [39], noting that the use of an eigendecomposition allows the -update to be solved to global optimality. In Section 3.1 below, we outline an alternate convergence proof based on recent developments in the theory of regularized (matrix) PCA.

We note here that we consider the case where is a projection matrix, i.e. one with all eigenvalues either 0 or 1. This simplifies the derivation above and the theoretical analysis presented in the next section, but is not necessary for our approach. In situations where the eigenvalues of are allowed to vary, the -update in Algorithm 1 can be replaced by where is the matrix with the leading eigenvalues of on the diagonal. Standard eigensolvers return elements of alongside the eigenvectors so this approach does not change the complexity of our approach. For the theory given in Section 3, can be taken to be the th eigenvalue of with minor modification.

2.1 Deflation and Orthogonality

While Algorithm 1 provides an efficient approach for estimating a single SS-TPCA factor, the multi-factor case is more difficult. The difficulty of the multi-factor case is a general characteristic of CP-type decompositions, posing significant computational and theoretical challenges, discussed at length by [29] among others. To avoid these difficulties, we adapt a standard greedy (deflation) algorithm to the SS-TPCA setting; this sequential deflation approach to CP-type decompositions builds on well-known properties of the matrix power method and has been adapted to tensors independently by several authors, including [42] and [81]. While this approach was originally applied heuristically, [50] and [21] have shown conditions under which the deflation approach is able to recover an optimal solution. In our case, extending [32]’s \citeyearparlinkHotelling:1933 orginal approach to the tensor context yields the following successive deflation scheme:

-

•

Initialize:

-

•

For :

-

(i)

Run Algorithm 1 on for rank to obtain ()

-

(ii)

Deflate to obtain

-

(i)

-

•

Return

As [93] notes, classical (Hotelling) deflation fails to provide orthogonality guarantees when approximate eigenvectors are used, such as those arising from regularized variants of PCA. To address this, he proposes several additional deflation schemes with superior statistical properties. We discuss these alternate schemes in detail in Section A of the Supplementary Materials.

We note that the Algorithm 1 is only guaranteed to reduce the norm of the residuals and may not reduce the tensor rank at each iteration: in fact, in some circumstances, the tensor rank may actually be increased by our approach. We believe this is not a weakness of our approach: as signal is removed from a data tensor, the remaining residuals should increasingly resemble pure noise, which has high tensor rank almost surely [92, Section 3.1]. Similarly, as we remove estimated signal, the unexplained residual variance should decrease. While classical PCA does reduce the rank of the residual matrix at each iteration, this is an attractive but incidental property of linear algebra and not an essential statistical characteristic.

2.2 Algorithmic Concerns

The computational cost of Algorithm 1 is dominated by the eigendecomposition appearing in the -update. Standard algorithms scale with complexity , which can be reduced to since we only need leading eigenvectors. Computation of the trace product is similarly expensive with complexity but can be trivially parallelized across slices of . Taken together, these give an overall per iteration complexity of when processing units are used. In practice, we have found the cost of the eigendecomposition to dominate in our experiments. As our theory below suggests, only a relatively small number of iterations, , are required to achieve statistical convergence with growing logarithmically in the signal-to-noise ratio of the problem.

Algorithm 1 given above closely parallels the classical power method for computing singular value decompositions. As such, many techniques from that literature can be used to improve the performance of our approach or to adapt it to reflect additional computational constraints. While a full review of this literature is beyond the scope of this paper, we highlight the use of sketching techniques for particularly large data, one-pass techniques for streaming data, and distributed techniques [26, 62, 63, 43]. When applied in the context of networks, it is particularly advantageous to take advantage of sparsity in in both the eigendecomposition and tensor algebra steps [56].

2.3 Regularized SS-TPCA

While the restriction to a rank- factor provides a powerful regularization effect as we will explore in the next section, it may sometimes be useful to regularize the term as well. For networks observed over time, a functional (smoothing) variant of SS-TPCA can be derived using the framework of [33]. Specifically, applying their smoothing perspective to the -update of Algorithm 1, the -constraint becomes for some smoothing matrix yielding a modified -update step:

where the norm is defined by . A similar approach was considered by [82] and [27] have recently established consistency of a related model. Alternatively, structured-sparsity in the factor can be achieved using a soft- or hard-thresholding step in the -update, as discussed by [74] and [46] respectively, or the -based techniques considered by [72]. [3] discussed the possibility of simultaneously imposing smoothing and sparsity on estimated singular vectors and the core ideas of their approach could be applied to the vector as well, though we do not do so here.

3 Consistency of SS-TPCA

Having introduced the SS-TPCA methodology, we now present a key consistency result for this decomposition. We analyze SS-TPCA under a tensor analogue of the spiked covariance model popularized by [35] or the low-rank mean model of [31]. Specifically, we consider data generated with signal corresponding a rank- principal component for some fixed and a loading vector and noise drawn from a semi-symmetric sub-Gaussian tensor, :

| (1) |

Here is a measure of signal strength, roughly analogous to the square root of the leading eigenvalue of the spiked covariance model. In this scenario, we have the following consistency result:

Theorem 1.

Suppose is generated from the semi-symmetric model described above (1) with elements of each independently -sub-Gaussian, subject to symmetry constraints. Suppose further that the initialization satisfies

for some arbitrary . Finally, assume . Then, the output of Algorithm 1 applied to satisfies the following

with high probability. Here denotes an inequality holding up to a universal constant and denotes an inequality holding up to a universal constant factor and a term scaling as .

A similar result holds for the -factor:

Theorem 2.

We highlight that these results are first-order comparable to those for classical PCA attained by [52], though with more strenuous conditions on the initialization. (The results of the matrix power method almost surely do not depend on the choice of initialization, but this property is unique to the classical (unregularized) eigenproblem and does not hold in general.) A full proof of these results appears in the Supplementary Materials to this paper, but we provide a sketch of our approach in Section 3.2 below. A highlight of our approach is that it relies only on the Davis-Kahan theorem and standard concentration inequalities. While [52] uses sophisticated matrix perturbation results to establish higher-order consistency, we derive similar bounds for classical PCA using only the Davis-Kahan theorem in Section B of the Supplementary Materials. The fact that comparable results are obtained for the matrix and semi-symmetric tensor cases suggests that our results are essentially the best that can be obtained for this problem using elementary non-asymptotic techniques.

The initialization condition of Theorem 1 essentially assumes initialization within of the true factor, with additional accuracy needed to deal with higher-noise scenarios. In low-dimensions, this condition is easily satisfied, but it becomes more strenuous in the the large setting. We believe this condition to be, in part, an artifact of our proof technique: our experiments in Section 4 suggest that initialization in the correct orthant is typically sufficient. This is particularly compelling in the network setting, where it is reasonable to assume that all elements of are positive, i.e., that the network does not swap a large number of edges simultaneously, flipping the loading on the principal network. In situations where cannot be assumed positive, our approach is computationally efficient enough to allow for repeated random initializations.

We note that our results are stated for root mean squared error under sub-Gaussian noise for analytical simplicity, but that our approach could be used more broadly. In particular, if one assumes iid Bernoulli noise, corresponding to randomly corrupted edge indicators in the network setting, the results of [65] lead to significantly tighter bounds. In certain high-dimensional problems, elementwise error bounds on and may be more useful than an overall RMSE bound and could be derived using the eigenvector perturbation results of [20] or [14]. Finally, we note that because our analysis leverages Davis-Kahan (uniform) bounds, we do not assume any cancellation among elements of , allowing our proofs to be applied in a dynamic adversarial setting, so long as remains bounded at each iteration. Replacing the uniform Davis-Kahan bounds with high-probability bounds such as those of [53] could lead to tighter bounds or less stringent initialization and signal conditions.

3.1 Connection with Regularized PCA

At this point, the reader may wonder about the connection between traditional PCA and SS-TPCA: after all, our approach endows the space of semi-symmetric tensors with a real inner product, treating it as essentially Euclidean, and achieves the same estimation error as classical PCA under the appropriate rank-one model. As we now discuss, there is an equivalence between SS-TPCA and a certain form of regularized matrix PCA not previously considered in the literature. The regularization implicit in this equivalence is key to understanding how our method can perform well on large graphs and avoid the pitfalls of standard PCA in high-dimensional settings [36].

In order to express a -dimensional semi-symmetric tensor as a matrix, it is natural to form a data matrix by vectorizing one triangle of each tensor slice and combining the vectorized slices as rows of a matrix. For a given semi-symmetric tensor, , let us denote the corresponding data matrix as where denotes tensor matricization of the upper triangle of each slice preserving the th mode, i.e. . Performing classical PCA on this matrix will have estimation error proportional to , which can be significantly worse than the rate attained by SS-TPCA for graphs having rank . Furthermore, classical PCA imposes no requirements on the estimated principal component and does not imply that the principal network given by has a low-rank structure.

| Method | Data Dimension | Aligned RMSE | |

|---|---|---|---|

| -Factor | -Factor | ||

| Classical PCA | |||

| Matricization + Classical PCA | |||

| SS-TPCA (rank ) | |||

| SS-TPCA (rank ) | |||

Low-rank structure of the principal network can be reimposed by adding an additional constraint on the right-singular vector: that is, by solving the regularized singular value problem

Finally, note that standard reformulation of the singular value problem as an eigenproblem via Hermitian dilation yields an equivalent regularized eigenvalue problem:

While these formulations are much more unwieldy than the tensor formulation, they reveal connections between our approach and the rich literature on sparse PCA. Specifically, our SS-TPCA Algorithm 1 can be interpreted as a variant of the truncated power method considered by [74] and [46], with the truncation to a -sparse vector being replaced by truncation to a matrix with only non-zero eigenvalues. In this form, it is clear to see that [74]’s \citeyearparlinkYuan:2013 convergence analysis of the Truncated Power Method can be applied to give an alternate proof of the convergence of Algorithm 1.

While we do not consider minimax optimality in this paper, we note that substantially similar approaches have been shown to be minimax under comparable assumptions. In particular, [10] show that classical PCA is rate-optimal under a dense signal model and that [46]’s \citeyearparlinkMa:2013 version of the truncated power method is optimal under a sparse signal model. Relatedly, [15] establish optimality of a soft-thresholded SVD under the matrix version of the “signal plus noise” model. Because our method attains comparable convergence rates, we conjecture that SS-TPCA is minimax rate-optimal up to a logarithmic factor under conditions substantially similar to those of Theorem 1.

This “rank-unvec” constraint appearing above has not previously appeared in the literature, but arises naturally from the low-rank structure random dot-product graphs. A similar constraint is implicit in certain unrelaxed formulations of the linear matrix sensing problem, but typically not analyzed as such [11]. Despite the non-convexity of this constraint, it is both computationally and theoretically tractable due to the nice properties of low-rank projections. We believe that this type of constraint can be applied more broadly in the analysis of network data, e.g., a variant of the network classification scheme considered by [7] with the coefficient matrix representing a low-rank graph rather than a sparse set of edges.

3.2 Sketch of Proof of Theorems 1 and 2

In this section, we outline the proof of Theorems 1 and 2. Full proofs of both results can be found in Section C of the Supplementary Materials. Our analysis is of a tensor analogue of the classical power method for matrix decomposition; [88] give an analysis of the matrix case that may provide useful background to our approach.

We first establish the following tail bound on the size of the noise tensor in terms of its semi-symmetric rank- operator norm:

Proposition 1.

The semi-symmetric operator norm, can be deterministically bounded above by . Furthermore, if the elements of are independently -sub-Gaussian, subject to symmetry constraints, we have

with probability at least , for some absolute constant .

The deterministic claim follows by bounding the elements of separately as and applying the standard result that for any . The probabilistic claim follows from standard bounds on the maximum eigenvalue of sub-Gaussian matrices and a union bound.

We combine the above result with a deterministic bound on the accuracy of Algorithm 1 for fixed :

Proposition 2.

Suppose for a unit-norm -vector , a orthogonal matrix satisfying , , and a semi-symmetric tensor. Then the result of Algorithm 1 applied to satisfies the following:

so long as and

for some arbitrary .

We establish Proposition 2 using an iterative analysis of Algorithm 1 which controls the error in in terms of and repeats this to convergence. Applying [100]’s \citeyearparlinkYu:2015 variant of the Davis-Kahan theorem to the -update, we find

Similarly, applying the Davis-Kahan theorem to the -update yields

Due to the non-linear function, this is not as simple as the -update and requires applying the Davis-Kahan theorem to the matrix pair and , where is the pre-normalized iterate. Because is an eigenvector of by construction, the eigenvector bound provided by Davis-Kahan is exactly what is needed to control .

With these two bounds in hand, we can bound the sine of the -angle in terms of the cosine of the -angle and vice versa. To connect these, it suffices to assume we are in the range of angles such that or . In order to ensure a substantial contraction at each step, we make the slightly stronger assumption that

for all and for some fixed . From here, we iterate our - and -update bounds to show that the error in the -iterates is bounded above by

where . Taking the limit, this gives the error bound for the final estimate . Finally, we note that given the geometric series structure of the above bound, only a logarithmically small number of iterations are required for the iterates to converge up to the noise bound of the data.

An important technical element of our proof is to ensure that the iterates remain within the strict -contraction region for all . While this follows immediately for the noiseless case, the noisy case is more subtle, requiring us to balance the non-expansive error from our initialization with the effect of the noise which recurs at each iteration. To ensure this, we need our iterates to be bounded away from the boundary of the contraction region so that the sequence of “contract + add noise” does not increase the total error at any iterate. We term this non-expansive region the “stable interior” of the contraction region. Simple algebra shows that assuming assuming is in the stable interior, i.e.,

implies that is in the stable interior so it suffices to make this stronger assumption on the initialization only. This style of algorithm-structured analysis has recently found use in the analysis of non-convex problems: notable examples include recent work by [19], [60] and [79]. In particular, the contraction assumptions above parallel the Restricted Correlated Gradient condition of [28]’s \citeyearparlinkHan:2022 low Tucker-rank framework. Compared with those papers, our result holds under much more general assumptions, only requiring bounds on the signal-to-noise ratio of the problem and a loose bound on initialization. Specifically, we do not require standard high-dimensional assumptions of sparsity, restricted strong convexity, or incoherence.

4 Empirical Results

4.1 Simulation Studies

In this section, we demonstrate the effectiveness of SS-TPCA under various conditions and give empirical evidence to support the theoretical claims of the previous two sections. Specifically, we seek to demonstrate the following four claims empirically: i) SS-TPCA outperforms classical PCA methods and generic tensor decompositions in the analysis of network valued data; ii) SS-TPCA exhibits rapid computational convergence to a region surrounding the true parameter value; iii) SS-TPCA exhibits classical statistical convergence rates as and vary; and iv) SS-TPCA is robust to the choice of initialization, .

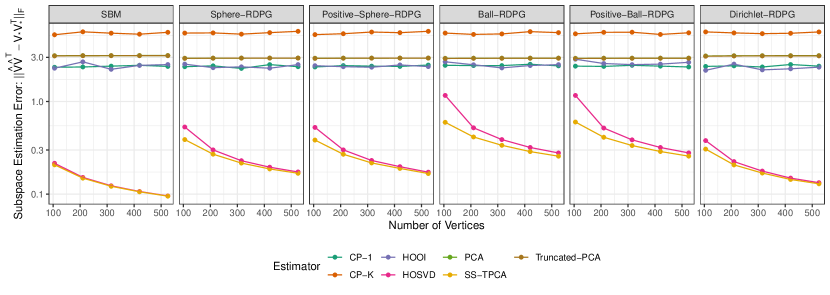

Simulation I - Methods Comparison:

We generate using iid samples from different variants of the Random Dot Product Graph framework, including a stochastic block model and latent position graphs on the simplex, unit sphere, and unit ball. In each case, we simulate graphs with a rank-5 structure, but vary the number of nodes from 105 to 525. We compare SS-TPCA with several potential competitors, including classical (vectorized) PCA, classical PCA followed by a low-rank truncation step, a rank-1 CP decomposition, a rank-5 CP decomposition, and a Tucker decomposition of order (5, 5, 1). The CP decompositions are estimated using alternating least squares, while we consider both the Higher-Order SVD (HOSVD) and the Higher-Order Orthogonal Iterations (HOOI) approaches to estimating Tucker decompositions. See [92] for additional background. Our results appear in Figure 2, where we report the subspace estimation error for each method. (We do not report estimation error for the -factor as it is uninteresting for iid samples, but all methods estimate both terms.) SS-TPCA consistently outperforms other estimators, with the HOSVD-estimated Tucker decomposition also performing well.

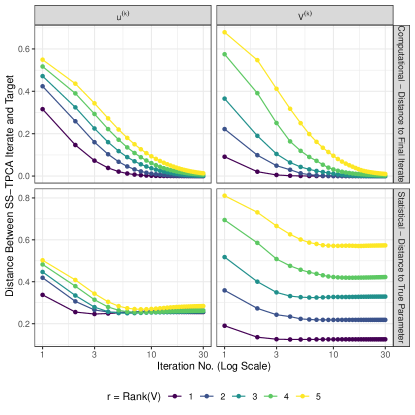

Simulation II - Computational and Statistical Convergence:

We generate from the model from the model , with observations and vertices. Because our main theorems do not place any restrictions on , we draw uniformly at random from the rank- Stiefel manifold. We fix and initialize Algorithm 1 with drawn randomly from the set of positive unit vectors. Finally, we generate such that each slice of is an independent draw from the Gaussian orthogonal ensemble (GOE): that is, the off-diagonal elements are drawn from independent standard normal distributions and the diagonal elements are independent samples from a distribution. We vary the signal strength to preserve a signal to noise ratio of slightly more than one (note ). Figure 3 depicts the convergence of the iterates of Algorithm 1 under this regime. It is clear that the iterates of Algorithm 1 achieve statistical convergence, in the sense of non-decreasing estimation error, in approximately one tenth the iterations needed to achieve computational convergence.

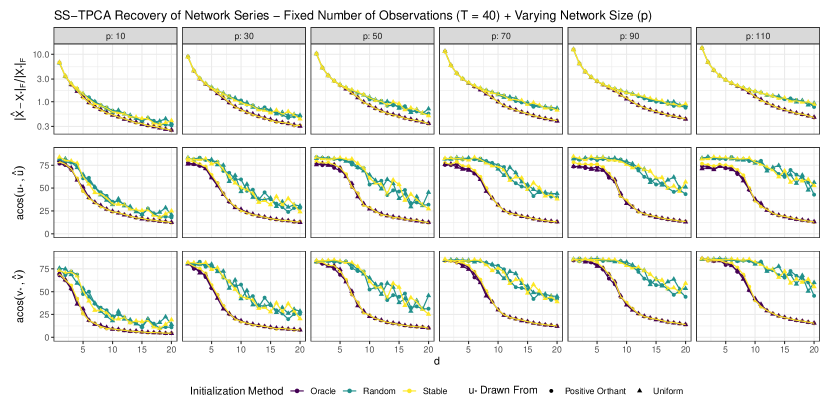

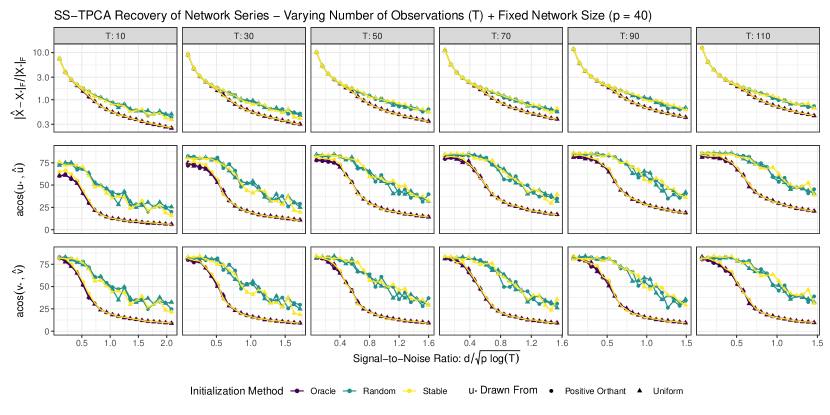

Simulation III - Convergence Rates and Initialization Robustness:

We generate as before, but fix so is drawn uniformly at random from the rank-1 Stiefel manifold, i.e., the unit sphere. We now also let be generated randomly under two different mechanisms: drawn uniformly at random from the unit sphere and drawn uniformly at random from the portion of the unit sphere in the first (positive) orthant, i.e., non-negative unit vectors. As before, each slice of is independently drawn from the GOE. From well-known bounds on the GOE, we have , giving an effective signal-to-noise ratio of for all experiments. We consider three approaches to initialize Algorithm 1: i) oracle initialization - ; ii) random initialization where is drawn at random from the unit sphere; and iii) “stable” initialization with .

Figure 4 shows the results of our study in the case of fixed (number of samples) and varying (network size) from 10 to 110. We present three measures of accuracy: i) the normalized reconstruction error between and the signal tensor ; ii) the angle between and ; and iii) the angle between the subspaces spanned by and , calculated as , where denotes the last (non-zero) singular value. Note that, for very accurate recovery, the used in computing the angle introduces a non-linear artifact: Figures 2 and 3, as well as , depict the expected parametric () convergence rate. Consistent with Theorems 1 and 2, we observe errors that decay rapidly in for all three measures under all generative and initialization schemes. Comparing the case with from the positive orthant or the entire unit sphere, we observe that random initialization does well in both cases, with accuracy only slightly worse than oracle initialization, and that stable initialization achieves essentially the same performance as oracle initialization for positive .

Figure 5 presents similar results taking the network size of nodes fixed and varying , though here with the effective signal-to-noise ratio as the ordinate (-axis) rather than the scale factor . As in Figure 4, the results of Theorems 1 and 2 are confirmed, with error decaying quickly and accurate recovery even at signal-to-noise ratios of approximately 1, and with both random and stable initializations being qualitative competitive with oracle initialization and with the stable initialization being essentially indistinguishable from the oracle scheme for positive . Taken together, these two experiments demonstrate that Algorithm 1 is robust to the initialization scheme and consistently performs well, even in situations where the initialization and signal strength requirements of our theorems are violated.

4.2 Case Study: Voting Patterns of the Supreme Court of the United States

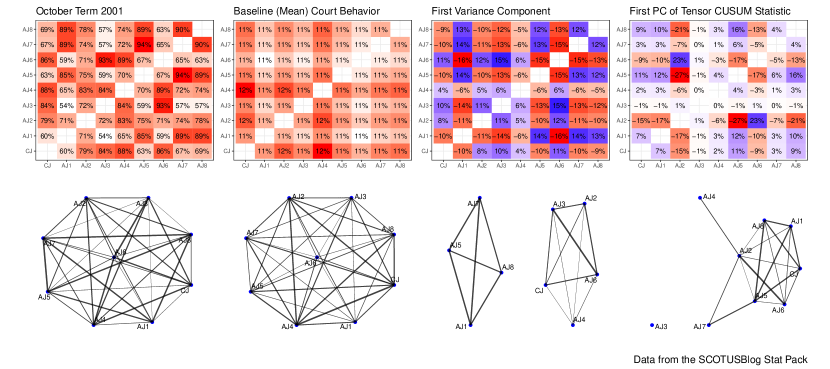

Finally, we apply SS-TPCA to analyze voting patterns of the justices of the Supreme Court of the United States (scotus) from a period from October 1995 to June 2021. Specifically, we construct a series of networks with nodes corresponding to each “seat” on the court: that is, a justice and her successor are assigned to the same node even if they have substantially different judicial philosophies, e.g., Ruth Bader Ginsberg and Amy Coney Barrett. Edge weights for each network are given by the fraction of cases in which the pair of justices agree in the specific judgement of the court: we ignore additional subtleties that arise when two justices agree on the outcome, but disagree on the legal reasoning used to reach that conclusion. We repeat this process for 25 year-long terms beginning in October 1995 (“October Term 1995” or “OT 1995”) to the term ending in June 2021 (“OT 2020”). Our results are presented in Figure 6.

We begin by finding the principal (mean) network from this data by applying Algorithm 1 to directly. This yields a rank-1 principal component with or, equivalently, , where is the all-ones matrix. This suggests that the baseline behavior of scotus is a broad-based consensus, typified by unanimous or nearly unanimous decisions. While this is somewhat at odds with the popular perception of scotus and news coverage highlighting controversial decisions, it is consistent with the fact that the majority of scotus cases are focused on rather narrow questions of legal and procedural arcana on which the justices can find broad agreement. We also note that the justices have discretion over the majority of their docket and may choose to favor cases where unanimity is likely.

We next apply SS-TPCA to the residuals from the mean analysis in order to identify the typical patterns of agreement after removing the unanimity factor. In this case, we find a principal network with two clear components of 5 and 4 vertices: a closer examination of this split reveals a stereotypical conservative (5) - liberal (4) split, where justices tend to vote in agreement with other justices nominated by a president from the same political party. This factor thus clearly identifies the partisan divide highlighted in media coverage and popular perceptions of scotus. We note, that the signal of the first factor () is much stronger than the signal of the second factor () suggesting that public perception is driven by a small number of high-profile and divisive cases.

Finally, we note that SS-TPCA techniques can be used to identify change points in a time-ordered network series under a rank- mean-shift model. Specifically, we adapt a proposal of [70] to the network setting and perform SS-TPCA on the Cumulative Sum Control Chart (“cusum”) tensor given by

By construction, inherits the semi-symmetric structure of and so can be used as input to Algorithm 1 with rank . The resulting “time factor,” , can then be used for change point analysis with being the most likely change point. A combination of Theorem 1 and standard change point detection theory implies that this approach correctly identifies a change point from data generated with mean to with probability inversely proportional to the effective signal-to-noise ratio

where and are the number of observations before and after the change point directly. This compares well with optimal rates for the univariate cusum model [66] and with recent work on network change point detection [67], specializing the latter results to the low-dimensional (non-sparse) regime.

We apply this cusum type analysis to identify major changes in the voting patterns of scotus justices. The results of this analysis suggest that the most important change, estimated by the largest element of , occurred in OT 2005 and was driven by the replacement of Justice Sandra Day O’Connor, a moderate conservative who would occasionally vote with her more liberal colleague Justice Souter, by Justice Samuel Alito, a firm conservative who almost always votes in agreement with fellow conservative Justice Thomas. The importance of this shift is commonly noted by legal commentators. We note that, while the replacement of Justice Ruth Bader Ginsberg by Justice Amy Coney Barett is likely to be even more important in the overall history of the court, Justice Barrett only served for one scotus term in our sample and hence cannot be identified by change point analyses. Further, we also note that cusum analysis suggests essentially no change in voting behavior when Justice Neil Gorsuch replaced Justice Antonin Scalia, consistent with their similar judicial philisophies and Justice Gorsuch’s adherence to judicial philisophy originally expounded by Justice Scalia.

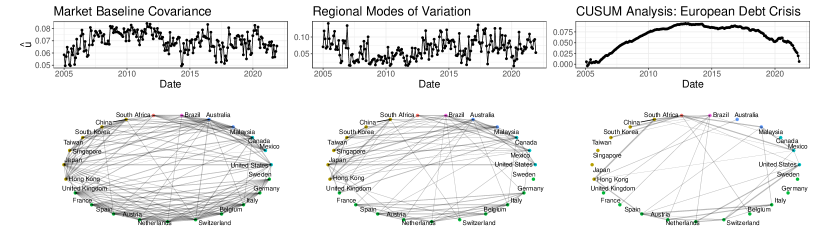

Note that the networks in this case study are quite small, with only nine vertices, and barely cross into the high-dimensional regime with distinct edges for observations. In this case, classical PCA on edge weights obtains results that are qualitatively similar to those presented here, as the effect of low-rank regularization is minimal. An additional case study in Section D of the Supplementary Materials analyzes correlation networks of international stock markets.

5 Discussion

We have presented a novel framework for multivariate analysis of network-valued data based on a semi-symmetric tensor decomposition we term SS-TPCA. Our major contribution is a theoretical analysis of SS-TPCA, where we show that SS-TPCA achieves estimation accuracy comparable to classical PCA, despite the significantly higher dimensionality of the tensor problem. We also highlight connections between SS-TPCA and a novel form of regularized PCA, based on a “rank-unvec” constraint. This constraint naturally captures a wide range of random graph models and can be applied in other supervised and unsupervised learning problems. Our analysis has three attractive properties: i) it relies only on elementary tools of matrix perturbation theory; ii) it establishes consistency under a very general noise model, allowing for the possibility of adversarial noise; and iii) by analyzing a specific computational approach, it avoids considerations of global versus local optimality. Given this combination of ease and power, we expect that our analytic approach will find use elsewhere. Finally, we demonstrate through simulation that our method is robust to choice of initialization and outperforms other methods in low- and high-signal regimes.

We expect several extensions of our work to be of particular interest: given the large scale of much network data, streaming, parallel, and approximate versions of Algorithm 1 will broaden the applicability of SS-TPCA. Network time series also are typically highly autocorrelated and regularization of the -term reflecting this fact may significantly improve performance. While the low-rank model at the heart of SS-TPCA captures a wide range of useful graph models, analogues of our work for directed, preferential attachment, multi-edge, and other graph structures would also be quite helpful in certain application domains. Robust versions of SS-TPCA, building on similar techniques for matrix PCA, are also of interest. Finally, we have assumed that the set of vertices is fixed and consistent node labels are available: unfortunately, this is rarely the case for large-scale networks arising from social media, telecommunications, or other important domains. Node sets change from one day to the next as users create and delete accounts and, despite recent progress, the graph alignment problems resulting from unlabeled nodes remain computationally prohibitive. Recent development in the theory of graphons suggests the use of continuous (functional) representations of graphs of different sizes and we are excited to pursue this avenue in future work.

Acknowledgements

MW’s research is supported by an appointment to the Intelligence Community Postdoctoral Research Fellowship Program at the University of Florida Informatics Institute, administered by Oak Ridge Institute for Science and Education through an interagency agreement between the U.S. Department of Energy and the Office of the Director of National Intelligence. GM’s research is supported by NSF/DMS grant 1821220.

References

- [1] Genevera I. Allen “Sparse Higher-Order Principal Components Analysis” In AISTATS 2012: Proceedings of the 15th International Conference on Artificial Intelligence and Statistics 22 Canary Islands, Spain: PMLR, 2012, pp. 27–36 URL: http://proceedings.mlr.press/v22/allen12.html

- [2] Genevera I. Allen “Multi-way functional principal components analysis” In CAMSAP 2013: Proceedings of the 5th IEEE International Workshop on Computational Advances in Multi-Sensor Adaptive Processing St. Martin, France: IEEE, 2013, pp. 220–223 DOI: 10.1109/CAMSAP.2013.6714047

- [3] Genevera I. Allen and Michael Weylandt “Sparse and Functional Principal Components Analysis” In DSW 2019: Proceedings of the 2nd IEEE Data Science Workshop Minneapolis, Minnesota: IEEE, 2019, pp. 11–16 DOI: 10.1109/DSW.2019.8755778

- [4] Animashree Anandkumar, Rong Ge, Daniel Hsu, Sham M. Kakade and Matus Telgarsky “Tensor Decompositions for Learning Latent Variable Models” In Journal of Machine Learning Research 15.80, 2014, pp. 2773–2832 URL: https://jmlr.org/papers/v15/anandkumar14b.html

- [5] Animashree Anandkumar, Rong Ge and Majid Janzamin “Guaranteed Non-Orthogonal Tensor Decomposition via Alternating Rank-1 Updates” In ArXiv Pre-Print 1402.5180, 2014 DOI: 10.48550/arXiv.1402.5180

- [6] Jesús Arroyo, Avanti Athreya, Joshua Cape, Guodong Chen, Carey E. Priebe and Joshua T. Vogelstein “Inference for Multiple Heterogeneous Networks with a Common Invariant Subspace” In Journal of Machine Learning Research 22.142, 2021, pp. 1–49 URL: https://jmlr.org/papers/v22/19-558.html

- [7] Jesús D. Arroyo Relión, Daniel Kessler, Elizaveta Levina and Stephan F. Taylor “Network Classification with Applications to Brain Connectomics” In Annals of Applied Statistics 13.3, 2019, pp. 1648–1677 DOI: 10.1214/19-AOAS1252

- [8] Avanti Athreya, Donniell E. Fishkind, Minh Tang, Carey E. Priebe, Youngser Park, Joshua T. Vogelstein, Keith Levin, Vince Lyzinski, Yichen Qin and Daniel L Sussman “Statistical Inference on Random Dot Product Graphs: a Survey” In Journal of Machine Learning Research 18.226, 2018, pp. 1–92 URL: http://jmlr.org/papers/v18/17-448.html

- [9] Xuan Bi, Xiwei Tang, Yubai Yuan, Yanqing Zhang and Annie Qu “Tensors in Statistics” In Annual Review of Statistics and Its Application 8, 2021, pp. 345–368 DOI: 10.1146/annurev-statistics-042720-020816

- [10] Aharon Birnbaum, Iain M. Johnstone, Boaz Nadler and Debashis Paul “Minimax bounds for sparse PCA with noisy high-dimensional data” In Annals of Statistics 41.3, 2013, pp. 1055–1084 DOI: 10.1214/12-AOS1014

- [11] Emmanuel J. Candès and Yaniv Plan “Tight Oracle Inequalities for Low-Rank Matrix Recovery From a Minimal Number of Noisy Random Measurements” In IEEE Transactions on Information Theory 57.4, 2011, pp. 2342–2359 DOI: 10.1109/TIT.2011.2111771

- [12] Alessia Cardillo, Jesús Gómez-Gardeñes, Massimiliano Zanin, Miguel Romance, David Paop, Francisco Pozo and Stefano Boccaletti “Emergence of Network Features from Multiplexity” In Scientific Reports 3.1344, 2013 DOI: 10.1038/srep01344

- [13] Rong Chen, Dan Yang and Cun-Hui Zhang “Factor Models for High-Dimensional Tensor Time Series (with discussion and rejoinder)” In Journal of the American Statistical Association 117.537, 2022, pp. 94–116 DOI: 10.1080/01621459.2021.1912757

- [14] Anil Damle and Yuekai Sun “Uniform Bounds for Invariant Subspace Pertubations” In SIAM Journal on Matrix Analysis and Applications 41.3, 2020, pp. 1208–1236 DOI: 10.1137/19M1262760

- [15] David Donoho and Matan Gavish “Minimax risk of matrix denoising by singular value thresholding” In Annals of Statistics 42.6, 2014, pp. 2413–2440 DOI: 10.1214/14-AOS1257

- [16] Daniele Durante, David B. Dunson and Joshua T. Vogelstein “Nonparametric Bayes Modeling of Populations of Networks” In Journal of the American Statistical Association 112.520, 2017, pp. 1516–1530 DOI: 10.1080/01621459.2016.1219260

- [17] Nathan Eagle, Alex Pentland and David Lazer “Inferring friendship network structure by using mobile phone data” In Proceedings of the National Academy of Sciences 106.36, 2009, pp. 15274–15278 DOI: 10.1073/pnas.0900282106

- [18] Morris L. Eaton “Multivariate Statistics: A Vector Space Approach”, Lecture Notes-Monograph Series 53 Beachwood, Ohio, USA: Institute of Mathematical Sciences, 2007 URL: https://projecteuclid.org/euclid.lnms/1196285102

- [19] Jianqing Fan, Han Liu, Qiang Sun and Tong Zhang “I-LAMM for sparse learning: Simultaneous control of algorithmic complexity and statistical error” In Annals of Statistics 46.2, 2018, pp. 814–841 DOI: 10.1214/17-AOS1568

- [20] Jianqing Fan, Weichen Wang and Yiqiao Zhong “An Eigenvector Pertubatiotn Bound and Its Application to Robust Covariance Estimation” In Journal of Machine Learning Research 18.207, 2018, pp. 1–42 URL: https://jmlr.org/papers/v18/16-140.html

- [21] Rong Ge, Yunwei Ren, Xiang Wang and Mo Zhou “Understanding Deflation Process in Over-parametrized Tensor Decomposition” In NeurIPS 2021: Advances in Neural Information Processing Systems 34 34, 2021 URL: https://proceedings.neurips.cc/paper/2021/hash/09a630e07af043e4cae879dd60db1cac-Abstract.html

- [22] Debarghya Ghoshdastidar, Maurilio Gutzeit, Alexandra Carpentier and Ulrike Luxburg “Two-sample hypothesis testing for inhomogeneous random graphs” In Annals of Statistics 48.4, 2020, pp. 2208–2229 DOI: 10.1214/19-AOS1884

- [23] Isabella Gollini and Thomas Brendan Murphy “Joint Modeling of Multiple Network Views” In Journal of Computational and Graphical Statistics 25.1, 2016, pp. 246–265 DOI: 10.1080/10618600.2014.978006

- [24] Sharmistha Guha and Abel Rodriguez “Bayesian Regression with Undirected Network Predictors with an Application to Brain Connectome Data” In Journal of the American Statistical Association 116.534, 2021, pp. 581–593 DOI: 10.1080/01621459.2020.1772079

- [25] Emilie M. Hafner-Burton, Miles Kahler and Alexander H. Montgomery “Network Analysis for International Relations” In International Organization 63.3, 2009, pp. 559–592 DOI: 10.1017/S0020818309090195

- [26] Nathan Halko, Per-Gunnar Martinsson and Joel A. Tropp “Finding Structure with Randomness: Probabilistic Algorithms for Constructing Approximate Matrix Decompositions” In SIAM Review 53.2, 2011, pp. 217–288 DOI: 10.1137/090771806

- [27] Rungang Han, Pixu Shi and Anru R. Zhang “Guaranteed Functional Tensor Singular Value Decomposition” In ArXiv Pre-Print 2108.04201, 2021 DOI: 10.48550/arXiv.2108.04201

- [28] Rungang Han, Rebecca Willett and Anru R. Zhang “An optimal statistical and computational framework for generalized tensor estimation” In Annals of Statistics 50.1, 2022, pp. 1–29 DOI: 10.1214/21-AOS2061

- [29] Yuefeng Han, Cun-Hui Zhang and Rong Chen “CP Factor Model for Dynamic Tensors” In ArXiv Pre-Print 2110.15517, 2021 DOI: 10.48550/arXiv.2110.15517

- [30] Moritz Hardt and Eric Price “The Noisy Power Method: A Meta Algorithm with Applications” In NIPS 2014: Advances in Neural Information Processing Systems 27 Montréal, Canada: Curran Associates, Inc., 2014 URL: https://proceedings.neurips.cc/paper/2014/hash/729c68884bd359ade15d5f163166738a-Abstract.html

- [31] Peter D Hoff “Model Averaging and Dimension Selection for the Singular Value Decomposition” In Journal of the American Statistical Association 102.478, 2007, pp. 674–685 DOI: 10.1198/016214506000001310

- [32] Harold Hotelling “Analysis of a Complex of Statistical Variables into Principal Components” In Journal of Educational Psychology 24.6, 1933, pp. 417–441 DOI: 10.1037/h0071325

- [33] Jianhua Z. Huang, Haipeng Shen and Andreas Buja “The Analysis of Two-Way Functional Data Using Two-Way Regularized Singular Value Decompositions” In Journal of the American Statistical Association 104.488, 2009, pp. 1609–1620 DOI: 10.1198/jasa.2009.tm08024

- [34] Majid Janzamin, Rong Ge, Jean Kossaifi and Anima Anandkumar “Spectral Learning on Matrices and Tensors” In Foundations and Trends® in Machine Learning 12.5-6, 2019, pp. 393–536 DOI: 10.1561/2200000057

- [35] Iain M. Johnstone “On the distribution of the largest eigenvalue in principal components analysis” In Annals of Statistics 29.2, 2001, pp. 295–327 DOI: 10.1214/aos/1009210544

- [36] Iain M. Johnstone and Arthur Yu Lu “On Consistency and Sparsity for Principal Components Analysis in High Dimensions” In Journal of the American Statistical Association 104.486, 2009, pp. 682–693 DOI: 10.1198/jasa.2009.0121

- [37] Sungkyu Jung, Ian L. Dryden and J.. Marron “Analysis of principal nested spheres” In Biometrika 99.3, 2012, pp. 551–568 DOI: 10.1093/biomet/ass022

- [38] Mikko Kivlä, Alex Arenas, Marc Barthelemy, James P. Glesson, Yamir Moreno and Mason A. Porter “Multilayer Networks” In Journal of Complex Networks 2.3, 2014, pp. 203–271 DOI: 10.1093/comnet/cnu016

- [39] Eleftherios Kofidis and Phillip A. Regalia “On the Best Rank-1 Approximation of Higher-Order Supersymmetric Tensors” In SIAM Journal on Matrix Analysis and Applications 23.3, 2002, pp. 863–884 DOI: 10.1137/S0895479801387413

- [40] Tamara G. Kolda “Numerical optimization for symmetric tensor decomposition” In Mathematical Programming 151, 2015, pp. 225–248 DOI: 10.1007/s10107-015-0895-0

- [41] Tamara G. Kolda and Brett W. Bader “Tensor Decompositions and Applications” In SIAM Review 51.3, 2009, pp. 455–500 DOI: 10.1137/07070111X

- [42] Tamara G. Kolda, Brett W. Bader and Joseph P. Kenny “Higher-order Web link analysis using multilinear algebra” In ICDM 2005: Proceedings of the IEEE International Conference on Data Mining 2005, 2005 DOI: 10.1109/ICDM.2005.77

- [43] Xiang Li, Shusen Wang, Kun Chen and Zhihua Zhang “Communication-Efficient Distributed SVD via Local Power Iterations” In ICML 2021: Proceedings of the 38th International Conference on Machine Learning Virtual: PMLR, 2021, pp. 6504–6514 URL: http://proceedings.mlr.press/v139/li21u.html

- [44] Lydia T. Liu, Edgar Dobriban and Amit Singer “ePCA: High-Dimensional Exponential Family PCA” In Annals of Applied Statistics 12.4, 2018, pp. 2121–2150 DOI: 10.1214/18-AOAS1146

- [45] Vince Lyzinski, Minh Tang, Avanti Athreya, Youngser Park and Carey E. Priebe “Community Detection and Classification in Hierarchical Stochastic Blockmodels” In IEEE Transactions on Network Science and Engineering 4.1, 2016, pp. 13–26 DOI: 10.1109/TNSE.2016.2634322

- [46] Zongming Ma “Sparse Principal Component Analysis and Iterative Thresholding” In Annals of Statistics 41.2, 2013, pp. 772–801 DOI: 10.1214/13-AOS1097

- [47] “Handbook of Graphical Models”, Chapman & Hall/CRC Handbooks of Modern Statistical Methods CRC Press, 2018 DOI: 10.1201/9780429463976

- [48] Lester Mackey “Deflation Methods for Sparse PCA” In NIPS 2008: Advances in Neural Information Processing Systems 21, 2008, pp. 1017–1024 URL: https://papers.nips.cc/paper/3575-deflation-methods-for-sparse-pca

- [49] Catherine Matias and Vincent Miele “Statistical Clustering of Temporal Networks Through a Dynamic Stochastic Block Model” In Journal of the Royal Statistical Society, Series B: Statistical Methodology 79.4, 2017, pp. 1119–1141 DOI: 10.1111/rssb.12200

- [50] Cun Mu, Daniel Hsu and Donald Goldfarb “Successive Rank-One Approximations for Nearly Orthogonally Decomposable Symmetric Tensors” In SIAM Journal on Matrix Analysis and Applications 36.4, 2015 DOI: 10.1137/15M1010890

- [51] Soumendu Sundar Mukherjee, Purnamrita Sarkar and Lizhen Lin “On Clustering Network-Valued Data” In NIPS 2017: Advances in Neural Information Processing Systems 30, 2017 URL: https://proceedings.neurips.cc/paper/2017/hash/018dd1e07a2de4a08e6612341bf2323e-Abstract.html

- [52] Boaz Nadler “Finite sample approximation results for principal component analysis: A matrix perturbation approach” In Annals of Statistics 36.6, 2008, pp. 2791–2817 DOI: 10.1214/08-AOS618

- [53] Sean O’Rourke, Van Vu and Ke Wang “Random perturbation of low rank matrices: Improving classical bounds” In Linear Algebra and its Applications 540, 2018, pp. 26–59 DOI: 10.1016/j.laa.2017.11.014

- [54] I.. Oseledets “Tensor-train decomposition” In SIAM Journal on Scientific Computing 33.5, 2011, pp. 2295–2317 DOI: 10.1137/090752286

- [55] Karl Pearson “On Lines and Planes of Closest Fit to Systems of Points in Space” In Philosophical Magazine 2.11, 1901, pp. 559–572 DOI: 10.1080/14786440109462720

- [56] Eric T. Phipps and Tamara G. Kolda “Software for Sparse Tensor Decomposition on Emerging Computing Architectures” In SIAM Journal on Scientific Computing 41.3, 2019, pp. C269–290 DOI: 10.1137/18M1210691

- [57] Daniel K. Sewell and Yuguo Chen “Latent Space Models for Dynamic Networks” In Journal of the American Statistical Association 110.512, 2015, pp. 1646–1657 DOI: 10.1080/01621459.2014.988214

- [58] David I. Shuman, Sunil K. Narang, Pascal Frossard, Antonio Ortega and Pierre Vandergheynst “The emerging field of signal processing on graphs: Extending high-dimensional data analysis to networks and other irregular domains” In IEEE Signal Processing Magazine 30.3, 2013, pp. 83–98 DOI: 10.1109/MSP.2012.2235192

- [59] Bernard W. Silverman “Smoothed Functional Principal Components Analysis by Choice of Norm” In Annals of Statistics 24.1, 1996, pp. 1–24 DOI: 10.1214/aos/1033066196

- [60] Will Wei Sun, Junwei Lu, Han Liu and Guang Cheng “Provable Sparse Tensor Decomposition” In Journal of the Royal Statistical Society, Series B: Statistical Methodology 79.3, 2016, pp. 899–916 DOI: 10.1111/rssb.12190

- [61] Daniel L. Sussman, Minh Tang and Carey E. Priebe “Consistent Latent Position Estimation and Vertex Classification for Random Dot Product Graphs” In IEEE Transactions on Pattern Analysis and Machine Intelligence 36.1, 2014, pp. 48–57 DOI: 10.1109/TPAMI.2013.135

- [62] Joel A. Tropp, Alp Yurtsever, Madeleine Udell and Volkan Cevher “Practical Sketching Algorithms for Low-Rank Matrix Approximation” In SIAM Journal on Matrix Analysis and Applications 38.4, 2017, pp. 1454–1485 DOI: 10.1137/17M1111590

- [63] Joel A. Tropp, Alp Yurtsever, Madeleine Udell and Volkan Cevher “Streaming Low-Rank Matrix Approximation with an Application to Scientific Simulation” In SIAM Journal on Scientific Computing 41.4, 2019, pp. A2430–A2463 DOI: 10.1137/18M1201068

- [64] Paul Tseng “Convergence of a Block Coordinate Descent Method for Nondifferentiable Minimization” In Journal of Optimization Theory and Applications 109.3, 2001, pp. 475–494 DOI: 10.1023/A:1017501703105

- [65] Van Vu “Singular vectors under random perturbation” In Random Structures and Algorithms 39.4, 2011, pp. 526–538 DOI: 10.1002/rsa.20367

- [66] Daren Wang, Yi Yu and Alessandro Rinaldo “Univariate mean change point detection: Penalization, CUSUM and optimality” In Electronic Journal of Statistics 14, 2020, pp. 1917–1961 DOI: 10.1214/20-EJS1710

- [67] Daren Wang, Yi Yu and Alessandro Rinaldo “Optimal change point detection and localization in sparse dynamic networks” In Annals of Statistics 49.1, 2021, pp. 203–232 DOI: 10.1214/20-AOS1953

- [68] Lu Wang, Laurent Albera, Amar Kachenoura, Huazhong Shu and Lotfi Senhadji “Canonical polyadic decomposition of third-order semi-nonnegative semi-symmetric tensors using LU and QR matrix factorizations” In EURASIP Journal on Advances in Signal PRocessing, 2014 DOI: 10.1186/1687-6180-2014-150

- [69] Shangsi Wang, Jesús Arroyo, Joshua T. Vogelstein and Carey E. Priebe “Joint Embedding of Graphs” In IEEE Transactions on Pattern Analysis and Machine Intelligence 43.4, 2021, pp. 1324–1336 DOI: 10.1109/TPAMI.2019.2948619

- [70] Tengyao Wang and Richard J. Samworth “High Dimensional Change Point Estimation via Sparse Projection” In Journal of the Royal Statistical Society, Series B: Statistical Methodology 80.1, 2018, pp. 57–83 DOI: 10.1111/rssb.12243

- [71] Steven Winter, Zhengwu Zhang and David Dunson “Multi-scale graph principal component analysis for connectomics” In ArXiv Pre-Print, 2020 DOI: 10.48550/arXiv.2010.02332

- [72] Daniela M. Witten, Robert Tibshirani and Trevor Hastie “A Penalized Matrix Decomposition, with Applications to Sparse Principal Components and Canonical Correlation Analysis” In Biostatistics 10.3, 2009, pp. 515–534 DOI: 10.1093/biostatistics/kxp008

- [73] Yi Yu, Tengyao Wang and Richard J. Samworth “A useful variant of the Davis–Kahan theorem for statisticians” In Biometrika 102.2, 2015, pp. 315–323 DOI: 10.1093/biomet/asv008

- [74] Xiao-Tong Yuan and Tong Zhang “Truncated Power Method for Sparse Eigenvalue Problems” In Journal of Machine Learning Research 14.Apr, 2013, pp. 899–925 URL: http://www.jmlr.org/papers/v14/yuan13a.html

- [75] Ali Zare, Alp Ozdemir, Mark A. Iwen and Selin Aviyente “Extension of PCA to Higher Order Data Structures: An Introduction to Tensors, Tensor Decompositions, and Tensor PCA” In Proceedings of the IEEE 106.8, 2018, pp. 1341–1358 DOI: 10.1109/JPROC.2018.2848209

- [76] Anru Zhang and Rungang Han “Optimal Sparse Singular Value Decomposition for High-Dimensional High-Order Data”, 2019, pp. 1708–1725 DOI: 10.1080/01621459.2018.1527227

- [77] Anru Zhang and Dong Xia “Tensor SVD: Statistical and Computational Limits” In IEEE Transactions on Information Theory 64.11, 2018, pp. 7311–7338 DOI: 10.1109/TIT.2018.2841377

- [78] Zhengwu Zhang, Genevera I. Allen, Hongtu Zhu and David Dunson “Tensor network factorizations: Relationships between brain structural connectomes and traits” In NeuroImage 197, 2019, pp. 330–343 DOI: 10.1016/j.neuroimage.2019.04.027

- [79] Tuo Zhao, Han Liu and Tong Zhang “Pathwise Coordinate Optimization for Sparse Learning: Algorithm and Theory” In Annals of Statistics 46.1, 2018, pp. 180–218 DOI: 10.12.14/17-AOS1547

- [80] Yuchen Zhou, Anru R. Zhang, Lili Zheng and Yazhen Wang “Optimal High-Order Tensor SVD via Tensor-Train Orthogonal Iteration” In IEEE Transactions on Information Theory 68.6, 2022, pp. 3991–4019 DOI: 10.1109/TIT.2022.3152733

References

- [81] Genevera I. Allen “Sparse Higher-Order Principal Components Analysis” In AISTATS 2012: Proceedings of the 15th International Conference on Artificial Intelligence and Statistics 22 Canary Islands, Spain: PMLR, 2012, pp. 27–36 URL: http://proceedings.mlr.press/v22/allen12.html

- [82] Genevera I. Allen “Multi-way functional principal components analysis” In CAMSAP 2013: Proceedings of the 5th IEEE International Workshop on Computational Advances in Multi-Sensor Adaptive Processing St. Martin, France: IEEE, 2013, pp. 220–223 DOI: 10.1109/CAMSAP.2013.6714047

- [83] Zhidong Bai, Kwok Pui Choi and Yasunori Fujikoshi “Consistency of AIC and BIC in estimating the number of significant components in high-dimensional principal component analysis” In Annals of Statistics 46.3, 2018, pp. 1050–1076 DOI: 10.1214/17-AOS1577

- [84] Raymond B. Cattell “The Scree Test For The Number Of Factors” In Multivariate Behavioral Research 1.2, 1966, pp. 245–276 DOI: 10.1207/s15327906mbr0102_10

- [85] Yunjin Choi, Jonathan Taylor and Robert Tibshirani “Selecting the number of principal components: Estimation of the true rank of a noisy matrix” In Annals of Statistics 45.6, 2017, pp. 2590–2617 DOI: 10.1214/16-AOS1536

- [86] Chandler Davis and W.. Kahan “The Rotation of Eigenvectors by a Perturbation III” In SIAM Journal on Numerical Analysis 7.1, 1970, pp. 1–46 DOI: 10.1137/0707001

- [87] Eugene F. Fama and Kenneth R. French “The Capital Asset Pricing Model: Theory and Evidence” In Journal of Economic Perspectives 18.3, 2004, pp. 25–46 DOI: 10.1257/0895330042162430

- [88] Moritz Hardt and Eric Price “The Noisy Power Method: A Meta Algorithm with Applications” In NIPS 2014: Advances in Neural Information Processing Systems 27 Montréal, Canada: Curran Associates, Inc., 2014 URL: https://proceedings.neurips.cc/paper/2014/hash/729c68884bd359ade15d5f163166738a-Abstract.html

- [89] Julie Josse and François Husson “Selecting the number of components in principal component analysis using cross-validation approximations” In Computational Statistics & Data Analysis 56.6, 2012, pp. 1869–1879 DOI: 10.1016/j.csda.2011.11.012

- [90] Michel Journée, Yurii Nesterov, Peter Richtárik and Rodolphe Sepulchre “Generalized Power Method for Sparse Principal Component Analysis” In Journal of Machine Learning Research 11, 2010, pp. 517–553 URL: http://www.jmlr.org/papers/v11/journee10a.html

- [91] Yuhi Kawakami and Mahito Sugiyama “Investigating Overparameterization for Non-Negative Matrix Factorization in Collaborative Filtering” In RecSys 21: Proceedings of the Fifteenth ACM Conference on Recommender Systems, 2021, pp. 685–690 DOI: 10.1145/3460231.3478854

- [92] Tamara G. Kolda and Brett W. Bader “Tensor Decompositions and Applications” In SIAM Review 51.3, 2009, pp. 455–500 DOI: 10.1137/07070111X

- [93] Lester Mackey “Deflation Methods for Sparse PCA” In NIPS 2008: Advances in Neural Information Processing Systems 21, 2008, pp. 1017–1024 URL: https://papers.nips.cc/paper/3575-deflation-methods-for-sparse-pca

- [94] Art B. Owen and Patrick O. Perry “Bi-Cross-Validation of the SVD and the Nonnegative Matrix Factorization” In Annals of Applied Statistics 3.2, 2009, pp. 564–594 DOI: 10.1214/08-AOAS227

- [95] Farnaz Sedighin, Andrzej Cichocki and Anh-Huy Phan “Adaptive Rank Selection for Tensor Ring Decomposition” In IEEE Journal of Selected Topics in Signal Processing 15.3, 2021, pp. 454–463 DOI: 10.1109/JSTSP.2021.3051503

- [96] Roman Vershynin “High-Dimensional Probability: An Introduction with Applications in Data Science”, Cambridge Series in Statistical and Probabilistic Mathematics Cambridge University Press, 2018

- [97] Martin J. Wainwright “High-Dimensional Statistics: A Non-Asymptotic Viewpoint”, Cambridge Series in Statistical and Probabilistic Mathematics Cambridge University Press, 2019

- [98] Per-Åke Wedin “Perturbation bounds in connection with singular value decomposition” In BIT Numerical Mathematics 12, 1972, pp. 99–111 DOI: 10.1007/BF01932678

- [99] Michael Weylandt “Multi-Rank Sparse and Functional PCA: Manifold Optimization and Iterative Deflation Techniques” In CAMSAP 2019: Proceedings of the 8th IEEE Workshop on Computational Advances in Multi-Sensor Adaptive Processing, 2019, pp. 500–504 DOI: 10.1109/CAMSAP45676.2019.9022486

- [100] Yi Yu, Tengyao Wang and Richard J. Samworth “A useful variant of the Davis–Kahan theorem for statisticians” In Biometrika 102.2, 2015, pp. 315–323 DOI: 10.1093/biomet/asv008

centerSupplementary Materials

Appendix A Additional Discussion for Subsection 2.1 - Deflation and Orthogonality

As [93] notes, classical (Hotelling) deflation fails to provide orthogonality guarantees when approximate eigenvectors are used, such as those arising from regularized variants of PCA. To address this shortcoming, he proposes “projection deflation” and “Schur deflation” techniques which provide stronger orthogonality guarantees and consequently improve the estimation of subsequent components. Because we cannot treat the SS-TPCA components estimated by Algorithm 1 as true eigenvectors, we propose three distinct tensor deflation schemes, each providing distinct degrees of orthogonality:

| (HD) | ||||

| (PD) | ||||

| (SD) | ||||

The Hotelling deflation (HD) and projection deflation (PD) schemes are tensor extensions of the analogous results for non-symmetric matrix decompositions given by [99]. The Schur deflation scheme (SD) requires more explanation: matrix Schur deflation is given by

for a target matrix and estimated left- and right-singular vectors respectively. Naïve extension of this formula to the tensor case would require defining the inverse of the quantity ; this sort of tensor inverse, however, is not well-defined. Rather than constructing a suitable notion of tensor inverse, we instead apply Schur deflation to each slice of separately, yielding the Schur deflation scheme given above.

Using these deflation schemes, we obtain the following general algorithm for the -SS-TPCA problem:

-

•

Initialize:

- •

-

•

Return

The factors estimated by Algorithm 3 have the following attractive orthogonality properties:

Theorem A.1.

For arbitrary semi-symmetric , the decomposition estimated by Algorithm 2 satisfies:

-

•

Two-way orthogonality, , at each iteration for all deflation schemes;

-

•

One-way orthogonality for the -factor () when either projection or Schur deflation is used;

-

•

One-way orthogonality for the -factor ( for ) when either projection or Schur deflation is used; and

-

•

Subsequent orthogonality for the -factor ( for and ) when Schur deflation is used.

The residual tensors have decreasing norm at each iteration under Hotelling’s deflation (HD) and projection deflation (PD): that is, for each . Schur deflation (SD) also guarantees decreasing norm so long as remains slicewise positive semi-definite at all .

The terminology of “two-way,” “one-way,” and “subsequent” orthogonality is due to [99], though we believe this is the first time these techniques have been applied in the tensor context. Proofs of these claims are given in Section A of the Supplemental Materials. We emphasize that these results hold without any assumptions on or without any assumptions of the quality of solution identified by Algorithm 1 and can be used in other tensor decomposition contexts with minor modification.

For convenience of the reader, we summarize the key claims of Theorem A.1 here:

| Orthogonality | Deflation Scheme | ||

|---|---|---|---|

| Hotelling (HD) | Projection (PD) | Schur (SD) | |

| Two-Way: | ✓ | ✓ | ✓ |

| One-Way (-factor): | ✗ | ✓ | ✓ |

| One-Way (-factor): () | ✗ | ✓ | ✓ |

| Subsequent (-factor): (; ) | ✗ | ✗ | ✓ |

| True Deflation | ✓ | ✓ | ✓ |

| Under additional conditions that can be checked at run-time. | |||

Proofs of these results are straightforward, if cumbersome, multilinear algebra: the reader is referred to the proofs of these results in Section A.2 of the paper by [99] to see the key ideas of each construction in a simpler (matrix) setting. As he notes, subsequent deflation, in particular is useful for encouraging approximate orthogonality of greedily estimated factors: if the target of the next SS-TPCA iteration is orthogonal to previous , the next estimated terms, which explain that target, are also likely to be nearly orthogonal. Conversely, we have also noted that imposing these additional restrictions may propose unexpected estimation difficulties, most notably decreasing cumulative percent of variance explained : we speculate this may be a useful diagnostic when selecting the number of factors, , but these issues are subtle and best left for future work.

Proof of Theorem A.1.

We first prove two-way orthogonality at each step for Hotelling’s deflation:

Recalling that , cf. Algorithm 1, this implies as desired.

Next, we prove one-way orthogonality for the factor under projection deflation:

where and are the all-zero -vector and matrix respectively. From this, two-way orthogonality is immediate:

A similar argument gives one-way orthogonality for the factor under projection deflation. Here, we establish orthogonality along the first axis, but the same argument applies for the second axis as well.

Recall that we here use a different convention for tensor-matrix multiplication () than [92] which satisfies the convention for suitably sized square matrices . The convention used by [92] has ; if their convention is used, the second term in the second line of the above would be , which again simplifies to . As before, one-way orthogonality immediately implies two-way orthogonality.

Finally, we establish the orthogonality properties of Schur deflation: one-way orthogonality for the -factor follows essentially the same argument as above:

recalling that is the tensor formed by Schur deflating each slice of by separately:

Similarly, for the factor, we note that

Here, each slice of is given by

implying and hence . The same argument holds along the second axis of .

We can take this as a base case to inductively establish subsequent orthogonality for the factor: assuming , we consider :

where is a semi-symmetric tensor, each slice of which is given by

Under the inductive hypothesis, we note that

and hence so for all .

We first show that Hotelling’s deflation gives a true deflation directly:

Recalling that , the desired result follows immediately from the fact that .111This can always be ensured by replacing with as needed.

For projection and Schur deflation, a different analysis is needed: we first note that for any real matrix and any unit vector .222Note that while . This last term is minimized when is the trailing eigenvector of , so , clearly giving the desired result. Here we use the convention to order the singular values of a matrix. Applying this result separately to each slice of a tensor and recalling that the Frobenius norm adds in quadrature across the slices, we have for any and unit vector . For projection deflation, we note that

for each slice separately by essentially the same argument as above. Hence, we have

as desired. For Schur deflation, we note that for any positive semi-definite matrix and orthogonal matrix and apply this slicewise in a similar fashion. ∎

We note that the assumption of slicewise positive semi-definitness is only used in the proof of decreasing norm and is not required for the orthogonality results.