Combining Evidence

Abstract

The problem of combining the evidence concerning an unknown, contained in each of Bayesian inference bases, is discussed. This can be considered as a generalization of the problem of pooling priors to determine a consensus prior. The linear opinion pool of Stone (1961) is seen to have the most appropriate properties for this role. In particular, linear pooling preserves a consensus with respect to the evidence and other rules do not. While linear pooling does not preserve prior independence, it is shown that it still behaves appropriately with respect to the expression of evidence in such a context. For the general problem of combining evidence, Jeffrey conditionalization plays a key role.

Keywords and phrases: combining priors, statistical evidence, preserving consensus, Jeffrey conditionalization, ancillarity.

1 Introduction

Suppose that different experts choose models and priors for a statistical analysis concerning a common quantity of interest which is a parameter or a future value. A problem then arises as to how the resulting statistical analyses should be combined so that the inferences presented can serve as a consensus inference. If all the models are the same, then this is the well-known problem of combining priors and this is covered by our discussion here. Even for the problem of combining priors, however, a somewhat different point-of-view is taken. A particular measure of evidence is adopted, as discussed in Section 3, such that the data set, sampling model and prior leads to either evidence in favor of or against each possible value of . The purpose then is to determine a consensus on what the evidence indicates. So, even for the combining priors problem, the motivation here is combining the evidence rather than combining prior beliefs. Since the primary goal of a statistical analysis is to express what the evidence says, this seems appropriate. Also, it is perfectly reasonable that some analyses express evidence against while others express evidence in favor but the combined expression of the evidence is one way or the other, see Section 2.

Before discussing the combination approach, however, it is necessary to be more precise about the problem and distinguish between somewhat different contexts where the problem can arise. It will be supposed here that is a parameter of interest but prediction problems are easily handled by a slight modification, see Example 3. Let denote a generic statistical model and where is onto and to save notation the function and its range have the same symbol.

Context I. Suppose there is a single statistical model for the data and distinct priors so there are inference bases for It is assumed that the conditional priors on the nuisance parameters are all the same, as is satisfied when This situation arises when there is a group of analysts who agree on and perhaps use a default prior for the nuisance parameters, while each member puts forward a prior for

Context II. Suppose there are data sets, models, and priors as given by the inference bases for and there is a common characteristic of interest with the true value of being the same for each model, as will occur when corresponds to some real world quantity.

Note that references some real-world quantity so in Context II the set of possible values and its true value is the same for each model even though formally the function may differ between models but we suppress this in the notation.

It is a necessary part of any statistical analysis that a model be checked to see whether or not it is contradicted by the data, namely, determining if it is the case that the data lies in the tails of each distribution in the model. So in any situation where there is a lack of model fit, it is necessary to modify that component of the inference base. Similarly, each prior needs to be checked for prior-data conflict, namely, is there an indication that the true value lies in the tails of the prior, see Evans and Moshonov (2006), Nott et al. (2020). If such a conflict is found, then the prior needs to be modified, see Evans and Jang (2011). It is assumed hereafter that all the models and priors have passed such checks. A salutary effect of a lack of prior-data conflict is that it rules out the possibility of trying to combine priors which have little overlap in terms of where they place their mass.

Given an inference base and interest in a Bayesian analysis has a consistency property. In particular, this inference base is equivalent to the inference base for inference about where is the marginal prior on and with the prior predictive density of the data obtained by integrating out the nuisance parameters via the conditional prior for given So, for example, the posterior for obtained via these two inference bases is the same and moreover the evidence about is also the same. This result has implications for the combination strategy as it is really the inference bases that are relevant in Context I and it is the inference bases that are relevant in Context II, namely, nuisance parameters are always integrated out before combining.

Perhaps the simplest step away from Context I is when the data sets differ but all the models are based on the same basic set of candidates for the true probability measure and with the same conditional prior on the nuisance parameters. In such a context it seems obviously correct to simply combine the data sets and use the common model for the combined data set which places the problem within Context I. The result would not necessarily be the same if the data sets were not combined, so it is necessary that the following rule be applied first to the set of inference bases in general.

Combining inference bases rule: all data sets that are assumed to arise from the same set of basic distributions are combined so that separate data sets are associated with truly distinct models.

This rule ensures that any combination reflects true differences among the beliefs concerning where the truth lies as there is agreement on the other ingredients. It is assumed hereafter that this is applied before the inference bases are determined. Note too that, even if the basic model is the same for each when the conditional priors on the nuisance parameters differ, then this is Context II.

In Section 2 a general family of rules for combining priors with given weights is presented. In Section 3 the problem of combining evidence for Context I is analyzed, with given weights for the respective priors, and the linear pooling combination rule is seen to have appropriate properties with respect to evidence. In Section 4 the problem of determining appropriate weights is considered. In Section 5 the problem for Context II is discussed and a proposal is made for a rule that generalizes the rule for Context I. The rule for Context I possesses a natural consistency property as the combined evidence is the same whether considered as a mixture of the evidence arising from each inference base or obtained directly from the combined prior and the corresponding posterior. In particular, it is Bayesian in this generalized sense which differs from being externally Bayesian as discussed in Genest (1984), see Section 3. This is not the case for Context II, however, because of ambiguities in the definition of the likelihood, but Jeffrey conditionalization provides a meaningful interpretation, at least when all the inference bases contain the same data.

The problem of combining priors has an extensive literature. Winkler (1968) is a basic reference and reviews can be found in Genest and Zidek (1986), Clemen and Winkler (1999), O’Hagan et al. (2006) and French (2011). Farr et al. (2018) is a significant recent application. Broadly speaking there are mathematical approaches and behavioral approaches. The mathematical approach provides a formal rule, as in Section 2, while the behavioral approach provides methodology for a group of proposers to work towards a consensus through mutual interaction. For example, Burgman et al. (2011) consider the elicitation procedure where quantities concerning the object of interest are elicited by each member of a group and then the average elicited values are used to choose the prior. Albert et al. (2012) adopt a supra-Bayesian approach where the data generated during the elicitation process is conditioned on in a formal Bayesian analysis to choose a prior in a family on which an initial prior has been placed. Yager and Alajlan (2015) present an iterative methodology for a group of proposers to work towards a consensus prior based upon each proposer seeing how far their proposal deviated from a current grouped proposal. While the behavioral approach has a number of attractive features, there are also reservations as indicated by Kahneman in Goodman (2021).

The focus in this paper is on presenting a consensus assessment of the evidence via a combination of the evidence that each analyst obtains. In particular, the priors need not arise via the same elicitation procedure and the proposers may not be aware of other proposals although the approach does not rule this out. Also, utility functions, necessary for decisions, are not part of the development as these may indeed lead to conflicts with what the evidence indicates and they are not generally checkable against the data as with models and priors. The assessment of statistical evidence as the primary driver of statistical methodology is a theme that many authors have pursued, for example, Birnbaum(1962), Royall (1997), Evans (2015), Gelman and O’Rourke (2017) and Vieland and Chang (2019).

2 Combining Priors with Given Prior Weights

Let the -dimensional simplex for some and, for now, suppose that is given. While general combination rules could be considered, attention is restricted here to the power means of densities

where and, for any and sequence of nonnegative functions defined on then is the relevant normalizing constant. Note that and do not depend on

For each the mean is nondecreasing in see Steele (2004), and two of the means are equal everywhere iff all priors are the same. Since this implies that is finite for all whenever If is to be considered, then it is necessary to check on the integrability of the mean so that a proper prior is obtained and this will be assumed to hold whenever the case is referenced. When is finite, this is not an issue.

The following result characterizes how the posterior behaves in terms of a combination of the individual posteriors. Let denote the -th prior predictive density based on prior and denote the prior predictive density obtained using the prior.

Proposition 1. For Context I, the posterior based on equals

and when

Proof: The expressions for for are obvious and

so the factor cancels giving the result. Finally,

and this is bounded above (below) by when which gives the inequality.

So the posterior is always proportional to a power mean of the individual posteriors of the same degree as the power mean of the priors but, excepting the case, the weights have changed and when or the prior and posterior do not depend on The posterior resulting when is

| (1) |

and so is a linear combination of the individual posteriors but with different weights than the prior. The case is called the linear opinion pool, see Stone (1961), and when it is called the logarithmic opinion pool.

The weights staying constant from a priori to a posteriori property for or even independence from the weights, may seem like an appealing property but, as discussed in Section 3, these combination rules have properties that make them inappropriate for combining evidence. A combination rule is said to be externally Bayesian when the rule for combining the posteriors is the same as the rule for combining the priors. As shown in Genest (1984a,b), logarithmic pooling is characterized by being externally Bayesian while linear pooling only satisfies this when there is a dictatorship, namely, for some as otherwise the weights differ. Proposition 2 (iii) shows, however, that there is a sense in which linear pooling can be considered as Bayesian.

Linear pooling has a number of appealing properties.

Proposition 2. For Context I, linear pooling satisfies the following:

(i) the prior probability measure satisfies the same combination rule as the densities, namely, and similarly for the posterior,

(ii) marginal priors obtained from are equal to the same combination of the marginal priors obtained from the , and this is effectively the only rule with this property among all possible combination rules,

(iii) if is given joint prior distribution with density , then the posterior density of is given by (1) and the weight is the posterior probability of the index .

Proof: The proof of (i) is obvious while (ii) is proved in McConway (1981) and holds here with no further conditions. For (iii), note that is the conditional prior of given and is the conditional density of given Once is observed the posterior of is then given by which implies that the marginal posterior of is (1) and the posterior probability of is .

The significance of (i) is that the other combination rules considered here do not exhibit such simplicity and require more computation to get the measures. Property (ii) implies that integrating out nuisance parameters before or after combining does not affect inferences about a marginal parameter in Context I as the marginal models for are all the same. Genest (1984c) proves a similar result allowing for negative . Property (iii) shows that both the prior and the posterior can be seen to arise via valid probability calculations when is known. A possible interpretation of this is that represents the combiner’s prior belief in how well the -th prior represents appropriate beliefs concerning the true value of relative to the other priors. The posterior weight is then the appropriate modified belief after seeing the data, as the factor reflects how well the -th inference has done at predicting the observed data relative to the other inference bases. This is a somewhat different interpretation than that taken by Bunn (1981) where represents the combiner’s prior belief that the -th inference base is the true one which, in this context, doesn’t really apply.

One commonly cited negative property of linear pooling, see Ladagga (1977), is that if and are independent events for each then generally It is also to be noted that if also one of or is constant in then independence is preserved and this will be seen to play a role in linear pooling behaving appropriately when considering statistical evidence, see Proposition 4 (ii) and the discussion thereafter

3 Combining Measures of Evidence with Given Prior Weights

The criterion for choosing an appropriate combination should depend on how statistical evidence is characterized, as using the evidence to determine inferences is the ultimate purpose of a statistical analysis. The underlying idea concerning evidence used here is the principle of evidence which says that there is evidence in favor of the value if there is evidence against the value if and no evidence either way if So, if the data has caused belief in the value being true to go up, then there is evidence in favor of this value, etc. The principle of evidence does not require that a specific numerical measure of evidence be chosen only that any measure used be consistent with this principle, namely, that there is a cut-off such that the numerical value greater than (less than) the cut-off corresponds to evidence in favor of (against) as indicated by the principle. The relative belief ratio the ratio of the posterior to the prior, with the necessary cut-off 1, is used here as it has a number of good properties, see Evans (2015), and it is particularly appropriate for the combination of the evidence as easily interpretable formulas result.

The next result examines the behavior of the combination rules of Section 2 with respect to evidence and is stated initially for the full model parameter .

Proposition 3. For Context I, the relative belief ratio for based on the prior equals

| (2) |

Proof: Using and then

This result shows the value of using the relative belief ratio to express evidence since the combination rule, at least for power means, is quite simple and natural. Notice too that if there are only distinct priors, then the combination rules for the priors, posteriors and relative belief ratios are really only based on these distinct priors and the weights change only by summing the that correspond to common priors.

The result in Proposition 3 is another indication that the correct way to combine priors, from the point of view of measuring evidence, is via linear pooling as is always proportional to The constant multiplying in (2) suggests that finding that minimizes , leads to the power mean prior that maximizes the amount of mass the prior places at see Proposition 7 (iv) . But there is a significant reason for preferring over the other possibilities. For suppose that for all or for all Then it is clear that in the first case and in the second case. In the first case there is a consensus that there is evidence against being the true value and in the second case there is a consensus that there is evidence in favor of being the true value. In other words is consensus preserving and this seems like a necessary property for any approach to combining evidence.

A formal definition is now provided which takes into account that sometimes indicating that there is no evidence either way and the -th inference base is agnostic about whether or not is the true value.

Definition A rule for combining evidence about a parameter is called consensus preserving if, whenever at least one of the inference bases indicates evidence in favor of (against) a value of the parameter and the remaining inference bases do not give evidence against (in favor), then the rule gives evidence in favor of (against) the value and if no inference base indicates evidence one way or the other then neither does the combination.

The following property is immediately obtained for linear pooling.

Proposition 4. For Context I, whenever for all then (i) is consensus preserving and (ii) whenever for all then iff for all .

The property of preserving consensus is similar to the unanimity principle for priors, see Clemen and Winkler (1999), which says that if all the priors are the same, then the combination rule must give back that prior.

Proposition 4 (ii) indicates that linear pooling deals correctly with independent events at least with respect to evidence. For note that, for probability measure and events and satisfying then and are statistically independent iff and independence is equivalent to saying that the occurrence of provides no evidence concerning the truth or falsity of Now consider the statistical context and suppose and further suppose that all the probabilities are discrete. This implies that which implies the joint prior density at factors as and so the events and are statistically independent in the -th inference base. If this holds for each then is constant in and so indeed implies that these events are independent when the prior is the linear pool. With a continuous prior then can also happen, but typically this event has prior probability 0.

It is of interest to determine whether or not any of the other rules based on the means are consensus preserving. The inequality in Proposition 1 and Proposition 3 imply that, when then and since with the inequality typically strict when this suggests that might even contradict the consensus of evidence in favor. A similar argument holds for The following example shows that generally the combination rules based on power means of priors aren’t consensus preserving.

Example 1. Power means of priors aren’t generally consensus preserving.

Suppose and is observed. There are two priors given by and Then so both inference bases give evidence against when and when so no evidence either way is obtained from the data when a statistician is categorical in their beliefs. Note being categorical in your beliefs is a possible choice provided it doesn’t lead to prior-data conflict. When so the two priors are being given equal weight, then and

When so statistician 2 is categorical in their beliefs, then and so there is evidence against.

Now consider given by So and when then and so

and so indicates no evidence either way. Therefore, the case is not consensus preserving.

Next consider the case so When then and so which implies that

So also the case is not consensus preserving.

If there is evidence against (in favor of) an event, then a property of the relative belief ratio gives that there is evidence in favor of (against) its complement and, if there is no evidence either way for an event, then there is no evidence either way for its complement, see Evans (2015), Proposition 4.2.3 (i). So in this example the priors and also do not preserve consensus with respect to

So far no case has been found where a combination based on a power mean actually reverses a consensus and it is a reasonable conjecture, based on many examples, that this will never happen but a proof is not obvious. It is still disturbing, however, that, as Example 1 illustrates, the inference bases can be equally weighted with none giving evidence in favor and at least one giving evidence against but the determination is that no evidence is obtained either way. It can be argued that a rule that behaves like this is not reflecting what the overall conclusion should be about the evidence.

There is another interesting consequence of Proposition 3 which is relevant when the goal is to estimate The natural estimate is the relative belief estimate and the accuracy of this estimate is assessed by the plausible region the set of values for which there is evidence in favor. For example, the ”size” of and its posterior content together provide an a posteriori indication of how accurate is. Ideally we want ”small” and its posterior content high. Note that it is easy to show in general that so provided is not 1 for all which only occurs when the data indicates nothing about the true value.

Corollary 5. Whenever is not 1 for all and for all then

So the estimate of based on maximizing the evidence is always determined by linear pooling. It is not the case, however, that the plausible region is independent of because of the constant

The following underscores the role of linear pooling in preserving consensus.

Corollary 6. The set for all and

So the set of where there is a consensus that there is evidence in favor is always contained in the plausible region determined by linear pooling. A similar comment applies to the implausible region which is the set of all values where there is evidence against. While it might be tempting to quote the region there is no guarantee that any of the relative belief estimates will be in this set, whether determined by or any of the

The situation with respect to the assessment of the hypothesis is a bit different. Clearly, if for all so there is a consensus that there is evidence in favor of (against) then preserves this consensus. In general, if one assesses the evidence for via a relative belief ratio then the posterior probability can be taken as a measure of the strength of the evidence, see Evans (2015). In the context under discussion here, it follows from (2) that the event for all Of course, the posterior probability of this event will depend on but linear pooling completely determines the event.

Now suppose that interest is in the quantity and the assumptions of Context I hold so that prior beliefs only differ concerning the value of which implies that the inference bases only differ with respect to the priors on This situation may arise when the analysts all agree to use a common default prior on the nuisance parameters. Then we can treat as the model parameter for the common model and the relevant linear pooling rule is

| (3) |

and all the results derived for apply.

In general it can be expected that some inference bases will indicate evidence in favor of being the true value and some will indicate evidence against, but will indicate evidence one way or the other. This depends on the values assumed by the as well as the weights It is to be noted, however, that there is nothing paradoxical about this as it is possible that there is evidence in favor of a set and contrary evidence for a set even though This situation is discussed in Corollary 4.2.1 of Evans (2015) and it is shown there that, when the prior probabilities are taken into account, the apparent paradox disappears. For example, if the prior probability of is a small relative to the prior probability of then such a reversal can occur and so the evidence measures disagreeing is not paradoxical. As an example of this, if there is evidence that a small subgroup of a population has extreme views on an issue, this is not evidence favoring the whole population having such extreme views and, on balance, the evidence could well indicate otherwise depending on the relative size of the subgroup. In essence, measuring evidence is quite different than measuring beliefs via probability as it is the change in belief from a priori to a posteriori that informs us about the evidence the data is expressing.

Consider now the context where is an sample. The following result gives the consistency of this approach when the basic sample space for the and the model parameter space are finite. Such results will hold more generally but require some mathematical constraints on densities and this is not pursued further here. Let be the relative belief estimate of based on linear pooling. All the convergence results are almost everywhere as with the proof in the Appendix.

Proposition 7. For Context I, suppose is an sample from a distribution in a

model having a finite parameter space and each prior for is

everywhere positive on Then

(i) and

(ii) and

(iii)

(iv)

Noting that when then Proposition 7 (i) says that the evidence in favor of (against) based on the combination, goes to categorical when is true (false). Part (ii) says that the relative belief estimate based on the combination is consistent. Part (iii) implies that, when the priors are equally weighted, then the inference base whose prior gives the largest value to the true value will inevitably have the largest weight in determining the combined evidence.

Overall, the conclusion reached here is that linear pooling is the most natural way to combine evidence at least among the power means. As such, attention is restricted to this case hereafter. Various authors, when discussing the combination of priors, have come to a similar conclusion. For example, O’Hagan et al. (2006), when considering the full spectrum of methods for combining priors, write the following, ”In general, it seems that a simple, equally weighted, linear opinion pool is hard to beat in practice.” The results developed here support such a conclusion when considering evidence.

4 Determining the Prior Weights

The discussion so far has assumed that is known. So arguments or methodologies for choosing need to be considered. There are several possible approaches to determining a suitable choice of the prior weights and nothing novel is proposed here. As previously mentioned, the can represent the combiner’s beliefs concerning how well the -th prior represents appropriate beliefs about The combiner’s beliefs should of course be based upon experience or knowledge concerning the various proposers of the priors. In absence of such knowledge then uniform weights, namely, seem reasonable. Genest and McConway (1990) provides a good survey of various approaches to choosing . Also, DeGroot (1974) and Lehrer and Wagner (1981) present a novel iterative approach to determining a consensus among the proposers.

In Context I notice that the weights only depend on the data through some function of the value of the minimal sufficient statistic (mss) for the model. So, for example, if the priors are distinct and equally weighted via then the weight of the -th prior is and so more weight is given to those inference bases that do a better job, relatively speaking, of predicting a priori the observed value of this function of the mss). Since it is only the observed value of the mss that is relevant for inference, this seems sensible. There is the possibility, however, to weight some priors more than others for a variety of reasons.

A prior can also be placed on the results examined for a number different choices of and summarized in a way that addresses the issue of whether or not the inferences are sensitive to For example, suppose the goal is to determine if there is evidence for or against the hypothesis For a given weighting the evidence for or against will be determined by the value Accordingly, a Dirichlet prior with mode at and with some degree of concentration around this point could be used to assess the robustness of the combination inferences. In particular, for each generated value of from the prior, one can record whether evidence in favor of or against was obtained together with the strength of the evidence. If a great proportion of the results gave results similar to those obtained with the weights then this would provide some assurance that the conclusions drawn are robust to deviations. A similar approach can be taken to estimation problems where the relative belief estimate is given by When is 1-dimensional then a histogram of the estimates obtained in the simulation and histograms of the prior and posterior contents of will provide an indication of the dependence on

5 The General Problem

The general Context II is more complicated and an overall solution is not proposed here rather a special case is considered when there is a common data set Since Context II covers Context I, it is necessary that any rule proposed for such situations agrees with what is determined for Context I when that applies.

While the prior on can be taken to be the mixture the overall posterior does not have a clear definition as it is not obvious how to form the likelihood. For example, the model parameters may not be comparable even if the parameter of interest always references the same real-world object as is assumed here. In some contexts there may be good arguments for a specific definition of the likelihood but this issue is not addressed further as our focus is on combining the evidence as characterized by the individual inference bases.

The simplest approach to characterizing the evidence in Context II is to use the obvious expression

| (4) |

where again and arise from the -th inference base and . This will agree with the answer obtained in Context I when it applies, but generally is not the ratio of the posterior of to its prior and as such it cannot be claimed that it is a valid characterization of the evidence as is in Context I.

One approach to defining a posterior in Context II is to use the argument known as Jeffrey conditionalization, see Diaconis and Zabell (1982). This involves considering the probabilities on the partition given by completely separately from the probabilities on given In this scenario the probabilities on the partition elements are updated differently than the probabilities given a partition element. This makes some sense here because one can think of the as being the combiner’s prior probabilities concerning the relevance of the -th inference base to inference about and these are separate from the individual analyst’s beliefs expressed about the true value of For example, some of the inference bases could be formed by teams with much more relevant experience than some of the others and so be more heavily weighted. As in Proposition 2 (iii), can be thought of as the prior probability of so, after observing the posterior probability of is again given by and given the posterior of is Both of these arise via regular (Bayesian) conditionalization but with priors on different objects. Using the Jeffrey’s conditionalization argument, the overall posterior of is

| (5) |

It is not the case, however, that in general (4) results as the relative belief ratio formed from (5) and the prior although (5) will be used to determine probabilities like the content of the plausible region determined by (4). One reason for not using and to determine the evidence is that this does not lead to a linear pooling of the characterizations of the evidence via the individual relative belief ratios and so the nice properties of linear pooling are lost, see Example 3. Notice that (4) will satisfy all the properties of linear pooling established for Context I with the exception of Proposition 2 (iii) and Jeffreys conditionalization is then used to justify the mixture. In particular, will preserve a consensus about evidence in favor or against.

The following result characterizes what happens as sample size grows and is proved in the Appendix.

Proposition 8. Suppose is an sample from a distribution in at least one of

the models and each of the parameter spaces is finite with the

prior everywhere positive on Denoting the set of indices

corresponding to the models containing the true distribution by then as

(i) and

(ii) which is greater than when

(iii)

So Proposition 8 shows that and provide consistent inferences and the weights converge to appropriate values.

There is another significant difference between (4) and (3). In Context I the weights all depended on the data through the same function of a constant mss for the full common model. Furthermore, if is an ancillary statistic for the full model, then it is seen that the -th weight satisfies This implies that the weights are comparable as they are all concerned with predicting essentially the same data and moreover they are not concerned with predicting aspects of the data that have no relation to the quantity of interest. In Context II this is not the case which raises the question of whether or not the weights are comparable.

It is not obvious how to deal with this issue in general, but in some contexts the structure of the models is such that where has fixed dimension and is ancillary for each model. For example, if all the models are location models, then where is a column of 1’s, and is ancillary. In such a case it is desirable to determine the weights based on how well the inference bases predict the value of and not To take account of this it is necessary that Jeffrey conditionalization be modified so that the -th weight is now proportional to where is the -th prior predictive of the data given Examples 4 and 5 illustrate this modification.

While Proposition 8 does not apply with the conditional weights, a similar result can be proved and for this some assumptions are imposed to simplify the proof. Let the basic sample space be such that there is a finite ancillary partition applicable to each of the models, and for any the ancillary is given by where records the number of values in the sample that lie in Then the probability distribution of for the -th model is given by the multinomial where the are fixed and independent of the model parameter and denote this probability function at the observed data by where Suppose that each parameter space is finite with the prior everywhere positive. Let for and denote the set of indices containing the true distribution. Calling these requirements condition the following is proved in the Appendix.

Proposition 9. If condition holds, then and

Proposition 9 provides the desirable consistency result as the only thing that is affected here are the weights which have been shown to have the correct asymptotic property.

Of course, this result needs to be generalized to handle even a situation like the location model. For this some conditions on the models and priors are undoubtedly required but this is not pursued further here. One key component of the proof is the existence of the ancillary partition and such a structural element seems necessary generally to get comparability of the weights. In group-based models, like linear regression and many others, such a structure exists via the usual ancillaries, see Example 5. As an approximation, a finite ancillary partition can be constructed via the ancillary statistic in question and so Proposition 9 is applicable. It should also be noted that, if the original model is replaced by the conditional model given the ancillary, then (4) gives the same answer as this modification as the values of are unaffected by the conditioning.

6 Examples

Some examples are now considered and initially a very simple context is considered where understanding of what is going on is enhanced by the availability of closed form expressions for relevant quantities.

Example 2. Location-normal model with normal priors.

Suppose is a sample from a distribution where the mean is unknown but the variance is known. It might be more appropriate to model this with an unknown variance but this situation will suffice for illustrative purposes. The model is then given by, after reducing to a mss, the collection of distributions and so this is Context I. Suppose there are three analysts and they express their priors for as distributions for so the posteriors are and these determine the relative belief ratios. For combining, the prior predictives are also needed and the -th prior predictive density for is the density. Suppose the inference bases are equally weighted so the posterior weight of the -th analysis relative to the others is determined by how well the observed value fits the distribution. Note, however, that even if there is a perfect fit, in the sense that the weight still depends on the quantity For example, if the are all equal and there is a perfect fit, then the -th weight is proportional to and this weight goes to 0 as with the other prior variances constant and goes to its biggest value when This suggests that making a prior quite diffuse leads to reducing the impact such a prior has in the combined analysis.

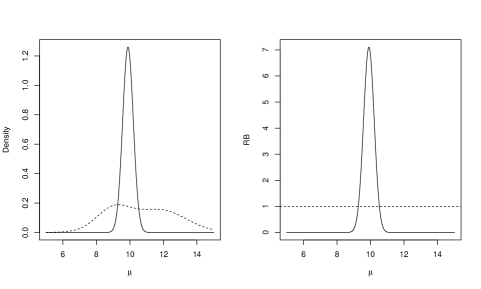

As a specific data example, suppose the true value of with and consider the results for several sample sizes Data were generated from the true distribution obtaining the values respectively. For the priors consider with the priors weighted equally. Figure 1 plots the combined prior, posterior and relative belief ratio for the case. Table 1 records the estimates of the plausible regions together with the posterior and prior contents of these intervals for each inference base and linear pooling. Note that in this case, because the model is the same for each inference base and is the model parameter, the estimates are all equal to the MLE of but the plausible intervals and their posterior contents differ.

| est. | comb. | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

|

|

|

|

|

||||||||||

|

|

|

|

|

||||||||||

|

|

|

|

|

||||||||||

|

|

|

|

|

Consider now prediction which produces the interesting consequence that Context II now obtains even when all the models are same.

Example 3. Prediction.

Consider Context I but suppose interest is in predicting a future value whose distribution is conditionally independent of the observed data given and has model where with The first step in solving this problem is to determine the relevant inference bases and this is done by integrating out the nuisance parameter which in this case is So the -th inference base is given by where is the density of the -th prior for namely, and is the conditional density of given Note that unconditionally and are not independent and now the collection of possible distributions for is indexed by The -th posterior density of is then

The models are now not all the same so this is Context II. It is assumed, as is typically the case, that the mss for these models is constant in so the weights are comparable. Applying (4), with the single data set leads to

with and (5) leads to posterior Note that in this case the posterior of given is well-defined via Bayesian conditioning and equals so there is no need to invoke Jeffrey’s conditionalization for the posterior. It is notable, however, that if the relative belief ratio for is computed using this posterior and the prior then this equals

| (6) |

which does not equal Given that the weights in (6) depend on the object of interest this does not correspond to linear pooling of the evidence and this is because the model is not constant. There is no reason to suppose that (6) will retain the good properties of linear pooling and experience with it suggests that it is not the correct way to combine. As such, the recommended approach is via (4) based on Jeffrey’s conditionization and which retains the good properties of linear pooling.

Suppose now the context is as discussed in Example 2 but the goal is to make a prediction concerning a future independent value So the -th prior is given by and the -th posterior is Table 2 gives the results for predicting using the data in Example 2. The final row indicates what happens as and note that the weights converge as well with the -th limiting weight proportional to which depends on the relative accuracy of the -th prior with respect to the true mean When all the prior variances are the same the prior which has its mean closest to the true value will give the heaviest weight. Also, as the -th weight goes to 0. Note that the limiting plausible intervals are dependent on the prior and the interval does not shrink to a point because is random. The limiting posterior content of these intervals is the probability content given by the true distribution of

For the limiting plausible intervals for to still be dependent on the prior is different than the situation when making inference about a parameter as, in that case, the plausible intervals shrink to the true value as the amount of data increases. The difference is that there is not a ”true” value for The limiting plausible interval does not allow for all possible values for and the effect of the prior is to disallow some possible values because belief in such a value is less than that specified by the prior of As can be seen from Table 2 this effect is not great unless the prior, as with here, puts little mass near the true value. However, such an occurrence also reduces the limiting weight for such a component.

| pred. | comb. | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

|

|

|

|

|

||||||||||

|

|

|

|

|

||||||||||

|

|

|

|

|

||||||||||

|

|

|

|

|

||||||||||

|

|

|

|

|

Consider now an example where the weights require adjustment.

Example 4. Location-normal models with different variances.

Suppose a situation similar to Example 2 but now with three distinct models so this is Context II. Here the -th statistician assumes that the true distribution is where the are known but is unknown and interest is in Again three priors are assumed. So the statisticians disagree about the ”known” variance of the sampling distribution and an ancillary needs to play a role to make the weights comparable.

In this case is ancillary for each model and is independently distributed from the common mss and Therefore, with equal weights for the priors, and taking the ancillaries into account, the -th weight satisfies

From this it is seen that the assumed variances and the prior both play a role in determining how much weight a given analysis should have. Note that as or , and all other parameters are fixed, then the weight of the -th analysis goes to 0 as it should as, in the limit, no information is being provided about the true value of Proposition 8 tell us that when and the -th variance is correct and the others are not, then the -th inference base will dominate.

Consider now an example where the models are truly different.

Example 5. Location with quite different models.

Consider now the context of Example 2 and suppose that one of the models, say the one in is a (Cauchy) location model, while the other models and all the priors are as previously specified. For all three inference bases is ancillary. To insure that has the same interpretation across all inference bases, the density is rescaled by so that the interval contains of the probability for all 3 distributions. This implies and, with the first model is where To obtain the corresponding weight the following expression needs to be evaluated numerically,

When applied to the data of Example 2 very similar results are obtained. Table 3 contains the weights for the inference bases for this situation.

Consider now a common context for applications.

Example 6. Linear regression.

Suppose that the data is for and there are two analysts where both propose a simple regression model where with and and unknown and is a sample from for analyst 1 and is a sample from a distribution for analyst 2 for some value In both models is the variance of a Letting be the least squares estimate of and then where and is ancillary for both models. Further suppose that the quantity of inferential interest is the slope parameter Denoting the relevant density of a by the joint density of given is proportional to

The posterior density of can be worked out in closed-form when is the density but generally it will require numerical integration to determine the posterior density and the posterior weights for the combination.

For the prior suppose both analysts agree on and gamma Note that the zero mean for may entail subtracting a known, fixed constant vector from so this, and the assumption that may entail some preprocessing of the data. The prior distribution of the quantity of interest is then where denotes the distribution on degrees of freedom.

To obtain the hyperparameters of the prior requires elicitation and this can be carried out using the following method as described in Evans and Tomal (2018). Suppose that it is known with virtual certainty, based on our knowledge of the measurements being taken, that will lie in the interval for some for all a compact set centered at 0 and contained in on account of the standardization. The phrase ‘virtual certainty’ is interpreted here as a probability greater than or equal to where is some large probability like Therefore, the prior on must satisfy for all which implies

| (7) |

where with equality when An interval that will contain a response value with virtual certainty, given predictor value is Suppose that we have lower and upper bounds and on the half-length of this interval so that or, equivalently,

| (8) |

holds with virtual certainty. Combining (8) with (7) implies To obtain the relevant values of and let denote the cdf of the gamma distribution and note that Therefore, the interval for implied by (8) contains with virtual certainty, when satisfy or equivalently

| (9) | ||||

| (10) |

It is a simple matter to solve these equations for For this choose an initial value for and, using (9), find such that which implies If the left-side of (10) is less (greater) than then decrease (increase) the value of and repeat step 1. Continue iterating this process until satisfactory convergence is attained.

Consider now a numerical example drawn from Zellner (1996) where the response variable is income in U.S. dollars per capita (deflated), and the predictor variable is investment in dollars per capita (deflated) for the United States for the years 1922–1941. The data are provided in Table 4. The data vector was replaced by as this centered the observations about 0. Taking leads to the values The following prior is then used for both models,

Table 5 presents the weights that result when different error distributions are considered to be combined with the results from a error assumption. Presumably this arises when one analyst is concerned that tails longer than the normal are appropriate. As can be seen the normal error assumption dominates except for when the inferences don’t differ by much in any case. This is not surprising as various residual plots don’t indicate any issue with the normality assumption for these data. These weights were computed using importance sampling and were found to be robust to the prior by repeating the computations after making small changes to the hyperparameters.

The approach taken in this example is easily generalized to more general linear regression models including situations where the priors change.

Year Income Investment Year Income Investment

7 Conclusions

The problem of how to combine evidence has been considered for a Bayesian context where each analyst proposes a model and prior for the same data. Linear opinion pooling is seen as the natural way to make such a combination at least when the inference bases only differ in the priors on the parameter of interest. This has been shown to have appropriate properties such as preserving a consensus with respect to the evidence and, when combining evidence is considered as opposed to just combining priors, behaves appropriately when considering independent events. In certain contexts the idea can be extended in a logical way based on the idea underlying Jeffrey conditionalization. There are restrictions as in the end the posterior weights have to be seen to be comparable and focused on that aspect of the data which is relevant for inference about the unknowns. Asymptotically the approach has been shown to behave correctly.

Certainly this does not cover all contexts where one might want to combine evidence as when there are different data sets and different models. If the models are all for the same response variable, then one possibility is to simply combine data sets and proceed as we have done here. More generally it may be that the only aspect in common among the models is the characteristic of interest and then it is not clear how we should combine and this warrants further investigation.

8 Appendix

Proof of Proposition 7

Parts (i) and (ii) are established in Evans (2015), Section 4.7 for a general prior and so can be applied with the prior For part (iii) we have

and by the SLLN where is the Kullback-Leibler divergence. Since and 0 iff this completes the result. Part (iv) is established similarly.

Proof of Proposition 8

Suppose initially that only one of the proposed models contains the true distribution and wlog it is given by Following the proof of Proposition 7 (iii) then

If two of the models contain the true distribution, say given by then

This line of reasoning proves (i).

Now note that

which implies If then the -ith term in converges to 0 as it has been shown that the -th weight does. If then which proves the first part of (ii). Now note that proving the second part.

Now is bounded so it is only necessary to the limit when and in that case and the result follows.

Proof of Proposition 9

As in the proof of Proposition 7, suppose that the true distribution is contained in only one of the models, say

Now noting that

the result is obtained. The remainder of the proof is as in Proposition 8.

9 References

Albert, I., Donnet, S., Guihenneuc-Jouyaux, C., Low-Choy S., Mengersen, K. and Rousseau, J. (2012) Combining expert opinions in prior elicitation. Bayesian Analysis, 7, 3, 503-532.

Birnbaum, A. (1962) On the foundations of statistical inference. J. of the American Statistical Association, 57, 298, 269-306.

Bunn, D. K. (1981) Two methodologies for the linear combination of forecasts. J. of the Operational Research Society, 32, 213-222.

Burgman, M. A., McBride , M., Ashton, R., Speirs-Bridge, A., Flander, L., Wintle, B, Rumpff, L. and Twardy, C. (2011) Expert status and performance. PLoS ONE, 6, e22998, doi:10.1371/journal.pone.0022998.

Clemen, R. T. and Winkler, R. L. (1999) Combining probability distributions from experts in risk analysis. Risk Analysis, 19 (2), 187-203.

Cooke, R. M. (1991) Experts in Uncertainty: Opinion and Subjective Probability in Science. Oxford University Press.

DeGroot, M. H. (1974) Reaching a consensus. J. of the American Statistical Association, 69, 118-121.

Diaconis, P. and Zabell, S. (1982) Updating subjective probability. Journal of the American Statistical Association, 77, 380, 822-820

Evans, M. (2015) Measuring Statistical Evidence Using Relative Belief. Monographs on Statistics and Applied Probability 144, CRC Press, Taylor & Francis Group.

Evans, M. and Jang, G-H. (2011). Weak informativity and the information in one prior relative to another. Statistical Science, 26, 3, 423-439.

Evans, M. and Moshonov, H. (2006) Checking for prior-data conflict. Bayesian Analysis, 1, 4, 893-914.

Evans, M. and Tomal, J. (2018) Multiple testing via relative belief ratios. FACETS, 3: 563-583, doi: 10.1139/facets-2017-0121.

Farr, C., Ruggeri F. and Mengersen, K. (2018) Prior and posterior linear pooling for combining expert opinions: uses and impact on Bayesian networks—the case of the wayfinding model. Entropy , 20, 209. doi:10.3390/e20030209

French, S. (2011) Aggregating expert judgement. Revista de la Real Academia de Ciencias Exactas, Físicas y Naturales. Serie A, Matemáticas, 03, 105 (1), 181-206, Springer.

Gelman, A. and O’Rourke, K. (2017) Attitudes towards amalgamating evidence in statistics. Manuscript.

Genest, C. (1984a) A characterization theorem for externally Bayesian groups. Annals of Statistics, 12, 2, 1100-1105.

Genest, C. (1984b) A conflict between two axioms for combining subjective distributions. J. of the Royal Statistical Society. Series B, 46 (3), 403-405.

Genest, C. (1984c) Pooling operators with the marginalization property. Canadian Journal of Statistics, 12, 2, 153-163.

Genest, C. and McConway, K. J. (1990) Allocating the weights in the linear opinion pool. J. of Forecasting, 9, 53-73.

Genest, C. and Zidek, J.V. (1986) Combining probability distributions: a critique and an annotated bibliography. Statistical Science, 1, 114-135.

Goodman, B. (2021) Daniel Kahneman says noise is wrecking your judgment. Here’s why, and what to do about it. Barrons, Economics Q&A, May 28, 2021.

Ladagga, R. (1977) Lehrer and the consensus proposal. Synthese, 36, 473-477.

Lehrer, K. and Wagner, C. (1981) Rational Consensus in Science and Society. D. Reidel Publishing Co.

McConway, K. J. (1981) Marginalization and linear opinion pools. J. of the American Stat. Assoc., 76:374, 410-414. doi: 10.1080/01621459.1981.10477661

Nott,D., Wang, X., Evans, M., and Englert, B-G. (2020) Checking for prior-data conflict using prior to posterior divergences. Statistical Science, 35, 2, 234-253.

O’Hagan A., Buck C. E., Daneshkhah A., Eiser J. R., Garthwaite, P. H., Jenkinson, D. J., Oakley, J. E. and Rakow, T. (2006) Uncertain Judgements:Eliciting Experts’ Probabilities. John Wiley & Sons Ltd.

Royall, R. (1997) Statistical Evidence: A Likelihood Paradigm. Monographs on Statistics and Applied Probability 71, CRC Press, Taylor & Francis Group.

Stone, M. (1961) The opinion pool. Annals of Mathematical Statistics, 32,1339-1342.

Vieland, V.J. and Chang, H. (2019) No evidence amalgamation without evidence measurement. Synthese, 196:3139–3161. https://doi.org/10.1007/s11229-017-1666-7

Winkler, R. L. (1968) The consensus of subjective probability distributions. Management Science, 15, 2, B-61-B-75.

Yager, R., Alajlan, N. (2015) An intelligent interactive approach to group aggregation of subjective probabilities. Knowledge-based systems, 83 (1), 170-175.

Zellner, A. (1996) An Introduction to Bayesian Inference in Econometrics. Wiley Classics.