Risk-Sensitive Optimal Execution via a Conditional Value-at-Risk Objective††thanks: The authors wish to thank Carlos Gomez Gascon and Paul Glasserman for helpful discussions.

Abstract

We consider a liquidation problem in which a risk-averse trader tries to liquidate a fixed quantity of an asset in the presence of market impact and random price fluctuations. When deciding the liquidation strategy, the trader encounters a trade-off between the transaction costs incurred due to market impact and the volatility risk of holding the position. Our formulation begins with a continuous-time and infinite horizon variation of the seminal model of Almgren and Chriss [2000], but we define as the objective the conditional value-at-risk (CVaR) of the implementation shortfall, and allow for dynamic (adaptive) trading strategies. In this setting, remarkably, we are able to derive closed-form expressions for the optimal liquidation strategy and its value function.

Our results yield a number of important practical insights. We are able to quantify the benefit of adaptive policies over optimized static (pre-committed) policies. The relevant improvement depends only on the level of risk aversion, and grows without bound as the trader becomes more risk neutral. For moderate levels of risk aversion, the optimal dynamic policy outperforms the optimal static policy by 5–15%, and outperforms the optimal volume weighted average price (VWAP) policy by 15–25%. This improvement is achieved through dynamic policies that exhibit ‘‘aggressiveness-in-the-money’’: trading is accelerated when price movements are favorable (to minimize risk), and is slowed when price movements are unfavorable (to minimize transaction costs). Overall, the optimal dynamic policies exhibit much better performance in the right tail of worst outcomes, relative to optimal static policies.

From a mathematical perspective, our analysis exploits the dual representation of CVaR to convert the problem to a continuous-time, zero sum dynamic game. In this setting, we leverage the idea of the state-space augmentation, recently applied to certain discrete-time Markov decision processes with a CVaR objective. We obtain a partial differential equation describing the optimal value function, which is separable and a special instance of the Emden–Fowler equation. This leads to a closed-form solution. As our problem is a special case of a continuous-time linear-quadratic-Gaussian control problem with a CVaR objective, these results may be interesting in broader settings.

PRELIMINARY VERSION — DO NOT DISTRIBUTE

1 Introduction

Optimal execution is a problem of significant importance for algorithmic traders in modern financial markets. Here, a trader must decide an optimal trading strategy to buy (or sell) a fixed quantity of an asset. Typically, there is a trade-off between trading quickly, which minimizes the risk of adverse price movements, and trading slowly, which minimizes transaction costs. In their seminal paper, Almgren and Chriss [2000] framed this liquidation problem as a mean-variance optimization problem, that optimizes a combination of the average cost (i.e., the expected implementation shortfall) and the variability of the cost (i.e., the variance of the implementation shortfall). In that setting, they explicitly derive the optimal liquidation schedule, which is parameterized by the risk-aversion level of the trader. Their framework and suggested solution have become standards in this area, serving as a starting point for more complicated models and trading strategies, both in the academic literature and among practitioners.

However, the Almgren and Chriss [2000] analysis is restricted to static strategies: they only considered deterministic schedules under which the trader pre-commits to a fixed trading schedule, i.e., algorithms that do not adapt to changing market conditions such as the price of the asset. This restriction makes the analysis considerably more straightforward and tractable, and allows for closed-form solutions. This leaves open possible additional benefit from dynamic, adaptive trading strategies, however. Indeed, most practitioners utilize adaptive strategies. This is often done through ad hoc or heuristic means, such as model predictive control (MPC), where the trader periodically resolves for a new deterministic policy as time evolves.

Indeed, it has been an important objective to incorporate dynamic strategies into the Almgren-Chriss framework, but in a more principled way. Some practitioners such as Kissell and Malamut [2005] have suggested a series of heuristics that are price-adaptive in a particular way: they liquidate more aggressively when the price moves in a favorable direction, and liquidate more slowly when the price moves in an adverse direction. Lorenz and Almgren [2007] observed that this ‘‘aggressiveness in-the-money’’ (AIM) behavior can strictly improve on the optimal deterministic strategy in the mean-variance criterion. In a subsequent work, Lorenz and Almgren [2011] develop a dynamic programming technique by which approximate solutions can be numerically obtained, and show that such approximate solutions exhibit AIM, despite the lack of an analytic solution. See also Forsyth [2011] for the continuous-time version of this analysis.

Another stream of work (including the present paper) introduces alternative risk criteria other than the mean-variance objective, so as to formulate the problem into a more tractable form. For example, Schied and Schöneborn [2009] formulate the problem as an expected utility maximization problem, and derive a Hamilton-Jacobi-Bellman (HJB) equation that characterizes the optimal adaptive strategy. They find that the optimal strategy is either aggressive- or passive-in-the-money, respectively, if and only if the utility function displays increasing or decreasing risk aversion, respectively, but an analytic solution is not available. Gatheral and Schied [2011] propose an alternative risk criterion that utilizes the time-averaged risk exposure to the price change driven by the geometric Brownian motion (more precisely, the risk term is formulated as the time integration of the position value process, i.e., the product of the position process and the price process), and explicitly solve for the optimal strategy that is shown to exhibit the AIM behavior. However, their proposed risk criteria is ad hoc, and may encourage, for example, negative positions to reduce risk. Hence, the resulting optimal policies are not ‘‘liquidate-only’’: they may trade in both directions (buying and selling) in excess of what is strictly necessary to reduce the position to zero. Forsyth et al. [2012] investigate the use of the quadratic variation of the position value process as a risk criteria, and observe that the classic static solution of Almgren and Chriss [2000] is again optimal when the price process is driven by the arithmetic Brownian motion. The authors also consider the geometric Brownian motion, under which the optimal solution is numerically determined and shown to be price-adaptive, and they report its AIM behavior through numerical examples. Lin et al. [2015] introduces a composite dynamic coherent risk measures and derive the optimal solution that is tractable but static. One can also consider an entropic risk measure introduced such as that of Glasserman and Xu [2013], but it can be shown that the resulting strategy is also not price-adaptive.

To summarize, the prior work in this area either (i) yields only approximate numerical solutions; (ii) incorporates only ad hoc risk criteria; (iii) yields policies that are not liquidate-only and trade in both directions; or (iv) illustrates no benefit from dynamic policies over static policies. In contrast, our work simultaneously addresses all of these issues, and, to our knowledge, is the first paper to do so.

In this paper, we consider the conditional value-at-risk (CVaR; also known as average value-at-risk, tail conditional expectation, or expected shortfall) as an objective. CVaR is a risk measure that quantifies the tail risk. Given a quantile value and a random variable that represents the cost, the CVaR value at level is defined as the average of the worst -fraction of the outcomes, i.e., the tail average beyond the quantile of the cost distribution. Smaller values of focus on performance in the worst cases, i.e., the trader is more risk averse, while , on the other hand, corresponds to a risk neutral trader. Starting from the pioneering work of Artzner et al. [1999], CVaR has received much attention for its intuitive definition and for nice mathematical properties as a convex and coherent risk measure.

From the point of view of using CVaR as an optimization objective, the (static) optimization of the CVaR value for a single period can be done efficiently, by utilizing its primal variational representation [Rockafellar and Uryasev, 2002]. In the multi-period setting of a Markov decision problem (MDP), however, the dynamic optimization of the CVaR value of the total cost is challenging. To begin, this objective is time-inconsistent. Moreover, as observed by Artzner et al. [2007] and Shapiro [2009], the optimal action at a point in time may not be completely determined by the current state of the MDP, but may depend on the entire history, and therefore the conventional dynamic programming techniques may not work.

More recent work has adopted the idea of state augmentation to overcome this issue: by introducing an extra state variable, an optimal policy can be sufficiently characterized as a Markov process defined on this augmented state space. Broadly speaking, these studies develop CVaR MDP frameworks using two kinds of state augmentation. The first kind introduces an extra state variable that represents the running cost, and derives the dynamic programming principle from the primal variational representation of CVaR, i.e., [see Rockafellar and Uryasev, 2002]. This state augmentation scheme is adopted in, for example, Bäuerle and Ott [2011], Huang and Guo [2016], Miller and Yang [2017], Chow et al. [2018], Backhoff-Veraguas and Tangpi [2020]. The second kind of state augmentation introduces an extra state variable that represents the quantile value, and derives the dynamic programming principle from the dual variational representation of CVaR, i.e., [see Artzner et al., 1999]. The work of Pflug and Pichler [2016], Chow et al. [2015], Chapman et al. [2018], Li et al. [2020] belongs to this category.

This paper. In this paper, we seek an adaptive liquidation strategy that minimizes the CVaR value of the implementation shortfall in a continuous-time, infinite-horizon variation of the classical Almgren-Chriss framework. We adopt the second kind of state augmentation described above. More specifically, we consider an augmented state space represented as , where is the current remaining position size of the trader, and is a quantile value that represents the current level of risk neutrality. We observe that the dynamic optimization of the CVaR objective can be represented as a (continuous-time) stochastic game between the trader who controls the position process and the adversary who controls the quantile process . By analyzing the Nash equilibrium of this game, we can identify the minimal CVaR value that the trader can achieve, and specify the trader’s optimal policy and the adversary’s optimal policy, which are formulated as time-stationary Markov policies on .

Practical contributions. Using our approach, we can express the optimal dynamic liquidation strategy in an analytic closed-form. This allows us to characterize properties of the optimal strategy, and yields a number of insights consistent with how optimal execution algorithms are widely employed in practice.

First, we show that the optimal strategy is liquidate-only, i.e., trades in only one direction and it keeps liquidating until it completes the execution. This is intuitive since, in practice, traders typically do not want to increase their positions or establish new positions during the liquidation process. We also observe that the optimal trading strategy becomes more aggressive and trades more quickly as the level of risk aversion increases. This is also intuitive since price risk can be minimized by trading quickly.

Second, and more interestingly, we show that the optimal trading strategy is dynamic and responds to stochastic fluctuations in the price process in a way that accelerates trading (to minimize price risk) when price movements are favorable, and slows trading (to minimize transaction costs) when price movements are unfavorable — in other words, it exhibits aggressiveness-in-the-money (AIM). The intuition behind the optimality of AIM is as follows:

Recall that the CVaR measure is the tail average beyond the quantile — the CVaR objective is not impacted by cost realizations below this threshold but only requires the average cost above this threshold to be minimized. As an extreme case, imagine a situation when the price movements have been so favorable that the trader has earned a large profit from the holding positions and the current cumulative cost is far below the quantile threshold. The CVaR objective of a trader in this scenario is not impacted by the cost (so long as it remains below the threshold) and the trader should thus be willing to pay a large, deterministic transaction cost (up to the gap between the current cumulative cost and the threshold) so as to complete the execution quickly and minimize the risk of the total cost exceeding the threshold. In the opposite case, imagine a scenario where the current cumulative cost is far above the threshold. Since the total cost is very likely to ultimately exceed the threshold, the CVaR objective of the trader becomes the expected cost and is approximately risk neutral. The trader is thus encouraged to slow down trading so as to minimize (deterministic) transaction costs thereafter. As illustrated in these two extreme cases, the optimal strategy responds asymmetrically to price changes, in the way that it becomes more aggressive in an adverse situation, due to the intrinsic asymmetry of the CVaR measure.

Our stochastic game interpretation of this dynamic CVaR optimization problem provides an alternative (and more formal) justification of AIM. On the augmented state space, the adversary’s quantile process represents the current level of risk neutrality (starting at value ), and is coupled with the price process. In particular, the adversary’s optimal quantile process represents the probability that the current sample path is among the -fraction of worst outcomes for the trader, and hence, increases when the price moves in an unfavorable direction. When increases, consequently, the trader becomes more risk-neutral and is encouraged to trade slowly, which is consistent with AIM.

Third, we are also able to quantify the benefit of dynamic trading by comparing the optimal dynamic policy to two benchmark static policies: the optimal static policy and an optimized version of a policy that trades at a constant rate. The later policy is meant to be representative of volume weighted average price (VWAP) polices that are popular in practice. The relative improvement of the optimal dynamic policy depends on the problem parameters only through the risk aversion , and can be characterized analytically. For moderate levels of risk aversion, the optimal dynamic policy outperforms the optimal static policy by 5–15%, and outperforms the optimal VWAP policy by 15–25%. Moreover, relative improvement is increasing in and grows without bound as , i.e., as the investor becomes more risk neutral. Since most traders using optimal execution algorithms are large investors trading a small portion of their overall portfolio over a short time horizon, their utility functions are nearly linear from the perspective of the optimal execution problem, hence the nearly risk neutral regime (), where the relative benefits of dynamic trading are greatest, is also the most practically relevant regime.

Last, numerical experiments yield insight to some useful features of the dynamic optimal policy. Namely, this policy effectively controls the worst outcomes in the (right) tail of the cost distribution, resulting in a cost distribution is very distinguished from the ones induced by deterministic policies. This feature may appeal to the practitioners who are not particularly interested in optimizing the CVaR value. For example, we observe that the class of CVaR-optimal dynamic policies achieves better median performance and better tail probabilities than the class of deterministic policies. See Figure 10 and the accompanying discussion for further details.

Mathematical contributions. We introduce a novel and technically sound approach to developing the CVaR MDP framework in the continuous-time setting. To sketch our approach briefly, we first introduce a scaled version of CVaR that allows us to avoid the ambiguity of CVaR in the corner case (i.e., when ) and inherently induces the concavity of the objective (Proposition 1). We then utilize the martingale representation theorem, by which we can rewrite the CVaR objective as a maximization problem for an adversary who controls the quantile process against the decision maker (Theorem 1), and the problem can be translated into a continuous-time stochastic game between the decision maker and the adversary who are competing over the expected value of the risk-adjusted outcome (Theorem 2). After this step, the objective now decomposes over time, hence we can develop a CVaR dynamic programming principle (Theorem 3). This naturally leads to the Hamilton-Jacobi-Bellman (HJB) partial differential equations that characterize the optimal solution. The HJB equation is separable across the state variables, and hence admits a closed form solution for the value function.

From the HJB equation, we are able to define candidate optimal control policies for the trader and adversary. Unfortunately, we are not able to show that these policies as feasible. Instead, we construct a series of feasible policies that converge pointwise to the candidate optimal policy and in value to the optimal value function (see Theorem 6 and the accompanying discussion).

Our approach leverages the idea of state augmentation that incorporates the quantile value as an extra state variable, which has been suggested and utilized in prior work [Pflug and Pichler, 2016, Chow et al., 2015, Chapman et al., 2018, Li et al., 2020], but in exclusively discrete-time settings. To our knowledge, our work is the first to apply this in continuous-time, which introduces new technical challenges. We clearly take advantage of the continuous-time setting: the martingale representation theorem, which is intrinsically continuous-time, is fundamental in our analysis as it allows us to parameterize the adversary’s control policy with a real-valued stochastic process that can be tractably optimized. Moreover, the choice of continuous-time is critical in this application, since the optimization of an analogous discrete-time model would involve a Bellman equation that is not separable, and hence is unlikely to admit an analytic solution (see the discussion at the end of §3.1).

As our problem is a special case of a continuous-time linear-quadratic-Gaussian control problem with a CVaR objective, these technical results may be interesting in broader settings, and feed into the broader emerging literature of continuous-time differential games.

Organization of paper. In §2, we introduce the notation and formally describe the model and the problem. In §3, we develop the CVaR MDP framework for which we sequentially introduce a martingale representation of the CVaR objective, the game-theoretic representation of the problem, and the Markov policies defined on the augmented state space. In §4, we derive the HJB equation, identify its solution, and characterize the optimal liquidation strategy. In §5, we compare the optimal adaptive strategy with two deterministic strategies: the optimal deterministic strategy and the optimized VWAP strategy. In §6, we provide simulation results that illustrate the optimal strategy. In the appendix, we provide the proofs that are deferred from §2–§5.

2 Problem

We consider a filtered probability space , where is a natural filtration of a Brownian motion that satisfies the usual conditions. We denote by (or simply by ) the set of –measurable random variables such that . Given a sequence of random variables , it is said that if . The time index set is denoted by . We also define to be the set of progressively measurable stochastic processes in this filtered probability space. We denote and .

2.1 Model

We consider a continuous-time and infinite-horizon version of the setting of Almgren and Chriss [2000]. We postulate a trader who wants to liquidate units of an asset over an infinite-time horizon.111The choice of an infinite-horizon setting is important since as it will allow an analytical solution of the problem. In particular, in an infinite-horizon setting, the optimal policy is stationary over time, and hence time can be eliminated as a state variable. As we will see in subsequent sections, this results in a simpler Hamilton-Jacobi-Bellman (HJB) equation that can be solved analytically. Beyond this, in some sense the infinite-horizon setting is more elegant from a modeling perspective since it endogenizes the effective time horizon of the trader dynamically as a function of risk aversion. That said, the optimal policy for a finite-horizon variation of our setting could be obtained via a numerical solution of the HJB equation, and we expect the qualitative insights to be no different. Here, can be negative if the trader wants to acquire the asset. We define , where is an arbitrary large number222We require that the position size be bounded in order to resolve technical difficulties (see Remark 1). that represents the largest possible position size that the trader is allowed to own.

Liquidation strategy. The trader’s liquidation policy is represented with a real-valued continuous-time stochastic process , where specifies the liquidation rate at time . Given an initial position size and a liquidation strategy , the trader’s position process is determined by

| (1) |

i.e., the trader liquidates units of the asset per unit time (or acquires units of the asset per unit time if ). While deferring a formal statement to the end of this subsection, we will restrict our attention to the policies under which the trader’s position varies continuously over time (i.e., involves no impulse trades) and vanishes eventually (i.e., converges to zero as goes to infinity).

Liquidation cost. Following the framework of Almgren and Chriss [2000], we define the cost process (or loss process) as

| (2) |

The first term represents the (cumulative) transaction cost incurred by the temporary price impact, where the coefficient reflects the illiquidity of the asset. The second term represents the (cumulative) loss incurred by the random fluctuation of the market price, where is the volatility of the price process and is the standard Brownian motion. The total cost (i.e., total implementation shortfall) is a random variable of interest that we want to minimize via a CVaR objective.

Note that we do not consider permanent price impact in our formulation. Within the continuous-time Almgren–Chriss framework, it is well known that the contribution of permanent linear price impact to the implementation shortfall is path-independent; i.e., it does not depend on the liquidation strategy as long as the strategy clears all the positions eventually.333 Suppose that liquidating the asset at rate permanently shifts the market price at rate , i.e., permanent linear price impact. Given a feasible policy , the associated transaction costs can be expressed , which is always equal to , independent of the policy, given that . Therefore, without loss of generality, we can ignore the presence of permanent impact since it does not make any difference in the trader’s decision making. See Almgren and Chriss [2000] for details.

Admissible strategies. We now formally define the set of admissible policies as

| (3) |

An admissible policy can be dynamic and so it can adjust the trading rate adaptively to the price changes. By this definition, impulse trades are not allowed by the constraint , and a non-vanishing position is also not allowed by the constraint . These conditions are to guarantee that the limit is an integrable random variable: individual terms in (2) converge in as , and therefore for some .

Remark 1.

The last condition is seemingly restrictive, but enforcing boundedness of the position path is merely a technical condition necessary for our later analysis. In particular, we will see that under the optimal policy, the position size will be monotonically decreasing towards zero over time. Therefore, we need only choose so that the initial position size is feasible, i.e., . Beyond this, the choice of will not be a binding constraint: it will neither influence the optimal policy nor the optimal value function.

2.2 Scaled Conditional Value-at-Risk

The conditional value-at-risk (CVaR) at a quantile level is a mapping from to . While there exist several definitions of CVaR in the literature, we consider the one based on its dual representation as a coherent risk measure [Artzner et al., 1999, Shapiro, 2009]: given a random variable ,

| (4) |

i.e., it is defined as a maximization over a random variable that has bounded support and an expected value of one (or equivalently, a maximization over a probability measure such that it is absolutely continuous with respect to and its Radon–Nikodyn derivative with respect to is upper bounded by almost surely).

We introduce a scaled version of the CVaR measure, which surprisingly simplifies our analysis.

Definition 1 (Scaled Conditional Value-at-Risk).

Given a random variable and a quantile , the scaled conditional value-at-risk (S-CVaR) at level is

| (5) |

where represents the risk envelope:

| (6) |

The S-CVaR measure is obtained by simply scaling the risk envelope of CVaR by . As a result, is also given by for . Nevertheless, it naturally incorporates the case into its definition, for which CVaR is not well defined.444 When , is typically defined as the essential supremum of , which can be infinite if the loss distribution has an unbounded support. We have defined the S-CVaR measure using the dual representation of CVaR so that we can effectively avoid the ambiguity at . It further has the following useful properties:

Proposition 1 (Properties of S-CVaR).

For any random variable , satisfies the following properties:

-

(i)

, for any .

-

(ii)

and .

-

(iii)

and for any .

-

(iv)

The mapping is concave and continuous on .

-

(v)

Suppose that is a continuous random variable whose distribution is atomless. Then,

(7) where is the inverse distribution function of , and .

The proof can be found in Appendix B. Properties (i)–(iii) provide basic characterizations of S-CVaR. The property (v) provides an interpretation of S-CVaR as a truncated average as opposed to the interpretation of CVaR as a conditional average. We particularly highlight property (iv) that shows the concavity and continuity of the S-CVaR value with respect to , which is a crucial property that will be exploited in our analysis.

One can interpret the definition (5) as a maximization problem for an adversary. This adversary selects a set of scenarios so as to maximize the average cost within the selected scenario, given a constraint that the total measure of the selected scenarios should be . Informally,555When the loss distribution has an atom at the quantile, the extremal random variable may take a fractional value. the optimized random variable is an indicator random variable such that if the scenario is among the worst -fraction of the scenarios, and otherwise.

2.3 Risk-sensitive Execution with a CVaR Objective

We now introduce the CVaR risk criterion into the setting described in §2.1. In particular, we seek an adaptive strategy that minimizes the CVaR value of the implementation shortfall, given an initial position and a target quantile . Without loss of generality, we formulate this optimization problem via an S-CVaR objective and define the value function as

| () |

Note that the above formulation includes the case . By Proposition 1, the value function is well-defined at , and the minimal CVaR value is simply given by for any . We aim to identify the optimal value function as well as its corresponding optimal liquidation strategy .

Recall that the objective concerns the worst -fraction of outcomes. When , the problem reduces to a risk-neutral liquidation problem. When takes a smaller value, the problem is equivalent to considering a more risk-averse trader who concerns a smaller fraction of worst cases, being wary of more extreme cases. We anticipate that the trader uses this quantile value as an input to our algorithm so as to control the level of risk-aversion that he wants to achieve. In practice, we do not expect the traders to use an extremely small quantile value such as or : since they encounter this sort of liquidation task often, possibly on a daily basis, it would be too conservative for them to optimize their performance in the worst or of cases at a cost of sacrificing their performance in the normal or of cases.

3 CVaR Dynamic Programming Principle

Using the definition of the S-CVaR measure (5), the risk-sensitive optimal execution problem ( ‣ 2.3) can be formulated as

| (8) |

As discussed in §2.2, we can think of an adversary who optimizes a random variable so as to select the worst -fraction of sample paths against the trader who employs a liquidation policy . In this section, we reformulate the adversary’s optimization problem as an optimization over a real-valued continuous-time stochastic process rather than a random variable, and interpret the risk-sensitive optimal control problem as a continuous-time stochastic game between the trader and the adversary. To this end, we develop a continuous-time dynamic programming principle by exploiting the recursive structure of this game.

3.1 Martingale Representation of CVaR Objective

We consider an arbitrary random variable and derive an alternative representation of . The results in this subsection are valid not only in the context of the liquidation problem, but also in any filtered probability space generated by a Brownian motion.

We define the adversary’s policy as a real-valued continuous-time stochastic process , which determines the adversary’s quantile process :

| (9) |

where is the Brownian motion that drives the random price fluctuation. We sometimes call the quantile diffusion rate by analogy to the liquidation rate .

The set of admissible adversary’s policies is defined as

| (10) |

Given an admissible adversary’s policy , its corresponding quantile process is a (local) martingale starting at whose diffusion term is governed by . In particular, the quantile process is required to take values within and, as a result, it has the following properties (the proof is provided in Appendix C):

Proposition 2 (Properties of the adversary’s quantile process ).

For any ,

-

(i)

is a continuous and bounded martingale taking values in , and hence for any stopping time .

-

(ii)

exists in almost surely, and also .

-

(iii)

Once hits or , it never escapes thereafter.

By the martingale representation theorem, any random variable in the risk envelope can be represented as the limit of a quantile process for some , and vice versa:

Lemma 1.

For any , .

Proof.

Consider an arbitrary , and Doob martingale generated by , i.e., for each (we have and ). By the martingale representation theorem [Protter, 2015, Thm. 43 in Chap. IV], there exists a predictable process such that . Since for any , we have an admissible adversary’s policy and therefore and .

Now consider an arbitrary and let . Trivially, and . Therefore, , and hence . ∎

This alternative representation of the risk envelope immediately leads to the following representation of the S-CVaR value, under which the adversary optimizes over the set of stochastic processes instead of the set of random variables:

Theorem 1 (Martingale representation of the CVaR objective).

For any given random variable and , we have

| (11) |

To better understand this adversary’s optimization problem, consider a discrete-time setting with two periods, six sample paths and , as illustrated in Figure 1. The adversary is asked to assign the quantile values on the individual nodes so as to maximize the objective, , given a constraint that the resulting quantile process needs to be a martingale.

It is easy to see that the adversary’s optimal solution is to select the worst -fraction of sample paths, i.e., to assign the quantile value to the -fraction of terminal nodes with the largest realized cost and assign the quantile value to the rest of terminal nodes. The quantile values of the non-terminal nodes are sequentially determined via backward induction (from to ) by averaging the quantile values of subsequent nodes. Here, the quantile value at each node means how likely the current sample path ends at one of the terminal nodes selected by the adversary.666 Consider the optimal martingale that solves (11), and recall that the random variable indicates whether the sample path is among the worst -fraction of scenarios. As a Doob martingale, the quantile process is its running estizmate at time , i.e., the likelihood that the current sample path will end up with one of the worst scenarios.

We can alternatively interpret this optimization problem as a sequential decision-making problem that the adversary assigns the quantile values in a forward direction (from to ). It begins with assigning the quantile value to the root node. Starting from the root node, the adversary is asked to allocate quantile values to the subsequent nodes given a budget constraint that the average of the quantile values assigned to these nodes should equal the quantile value at the current node. This is repeated until all terminal nodes get assigned their quantile values. Here, the quantile value at each node means how much fraction of sample paths can be selected thereafter, and the budget constraint guarantees the resulting quantile process be a martingale.

The latter interpretation is closed related to Theorem 1. Indeed, for example, can consider a binomial tree model as a discrete-time approximation of the underlying Brownian motion, in which every node has two branches representing the events of price moving up or down by a small amount. In this binomial approximation, the quantile value allocation problem that the adversary solves at each node involves only one decision variable: given the current quantile value , the allocation of next quantile values is of the form , where is the real-valued decision variable. Here, determining the value of is effectively equivalent to determining the diffusion rate of , which is in fact the adversary’s policy in our formulation.

We highlight that this martingale representation greatly simplifies the adversary’s optimization problem and is only available in a continuous-time setting. In the discrete-time setting investigated in Pflug and Pichler [2016], Chow et al. [2015], Chapman et al. [2018], Li et al. [2020], for example, the adversary in each period needs to solve a much more complicated optimization that may involve many decision variables (if there are possible random outcomes at a state, the quantile value allocation problem involves real-valued decision variables). It may not easy in such cases to solve the adversary’s optimization problem even numerically.

3.2 Risk-sensitive Liquidation as a Continuous-time Stochastic Game

We now return to the liquidation problem, and define an outcome function as a function of the trader’s policy and the adversary’s policy at each and :

| (12) |

By Theorem 1, the value function ( ‣ 2.3) can be formulated as

| (13) |

The following theorem characterizes this value function as an equilibrium outcome of a continuous-time stochastic game between the trader and the adversary.

Theorem 2 (CVaR optimization as a continuous-time stochastic game).

The value function is the outcome at the Nash equilibrium of the zero-sum game in which the trader and the adversary compete over the outcome ,

| (14) |

where an optimal solution must exist for each maximization.

Theorem 2 states that the minimax solution equals the maximin solution. This means that the value function is, as a saddle point, the equilibrium outcome at which each player simultaneously plays the best response against the other player’s strategy. This may not always hold true for a general class of risk-sensitive control problems: the convexity of the outcome function with respect to the trader’s policy and the convexity of the policy space are required in our proof (Appendix C.1) in order to apply Sion’s minimax theorem [Sion, 1958].

The following remark provides an alternative interpretation of this game based on the Girsanov theorem.

Remark 2.

Recall that the dual representation of the CVaR objective (4) involves a multiplication with a random variable , which corresponds to an absolutely continuous change of measure with Radon-Nikodym derivative . In terms of the adversary’s quantile process , this change of measure can by written as . By the Girsanov theorem, the price process has a drift under this new measure, and is given by

where is a Brownian motion under the new measure. In other words, the trader’s optimization problem given the adversary’s policy is can also be viewed as a risk-neutral liquidation problem under altered price dynamics in the presence of adversary who can introduce drift into the price process.

3.3 CVaR Dynamic Programming Principle

In this subsection, we develop a continuous-time dynamic programming principle. We first state a proposition that characterizes a temporal structure of the game.

Proposition 3 (Time decomposition).

Fix and . For any trader’s policy , adversary’s policy , and stopping time , we have

| (15) |

Proof.

Observe that is -measurable and since is a martingale. Utilizing the tower property, we obtain . ∎

Note that represents the cost realized after time . Proposition 3 states that the final outcome can be decomposed into two terms: one term describes the subgame before time , and the other term describes the subgame after time .

Observe that, in the subgame after time , the trader is liquidating shares and the adversary is selecting a -fraction of the future scenarios realized thereafter. This time decomposition naturally leads to the following dynamic programming principle:

Theorem 3 (CVaR dynamic programming principle).

For any , , and a stopping time with , we have

| (16) |

Theorem 3 provides the optimality principle in the form of Bellman’s equation: at the equilibrium, the outcome after time can be sufficiently described by the subgame equilibrium . The trader is minimizing the (risk-adjusted) cost up to time in a consideration of his future state , while the adversary is simultaneously maximizing the (risk-adjusted) cost up to time in a consideration of his future state , and the subgame starts at those future states. Like Theorem 2, Theorem 3 relies on the saddle-point characterization of the equilibrium; i.e., it does not matter which player commits his policy first in the subgame. The formal proof can be found in Appendix C.3.

3.4 -Markov Policies

Theorem 3 implies that the augmented state space is sufficient to describe the remaining subgame at time . Therefore, if a policy is reasonable, its action at time ( or ) should be determined by the current position size and the current quantile value . To formalize this idea, we introduce time-stationary Markov policies running on this augmented state space:

Definition 2 ( -Markov policies ).

We say that a trader’s policy is an -Markov policy coupled with if

| (17) |

for some measurable function .

Similarly, an adversary’s policy is an -Markov policy coupled with if

| (18) |

for some measurable function .

An -Markov policy is characterized by a function defined on the augmented state space. The function or specifies the liquidation rate or the quantile diffusion rate when the current position size is and the current quantile level is . Recall that we have defined a policy, or , as a continuous-time stochastic process adapted to the Brownian motion, i.e., as a (progressively measurable) mapping . Strictly speaking, the function or does not completely determine one player’s policy unless the other player’s policy is specified. To avoid this ambiguity, when we describe an -Markov policy, we specify the other player’s policy that is coupled with it.

To better understand, consider the policies and that are mutually coupled -Markov policies induced by functions and . Under and , the system is completely described by the coupled processes on the augmented state space, whose dynamics are given by the following stochastic differential equations:

| (19) |

with the initial states and . Even if is not an -Markov policy, we can still consider an -Markov policy that is induced by and coupled with , and then the position process will be given by .

4 Optimal Solution

In this section, we utilize the CVaR dynamic programming principle (Theorem 3) to derive a Hamilton–Jacobi–Bellman (HJB) equation for the risk-sensitive optimal execution problem, and identify the functional form of the value function and the optimal policies by solving this HJB equation. For all propositions/theorems stated in this section, we defer their proofs to Appendix D.

4.1 Minimal CVaR Cost

We first state Dynkin’s formula that we can apply to the right-hand side of (16) in Theorem 3 so as to represent it as a time-integration.

Proposition 4 (Dynkin’s formula).

Consider a function such that . For any , , and stopping time , we have

| (20) | ||||

| (21) | ||||

| (22) |

where and .

For the sake of argument, suppose that the value function can be plugged into Proposition 4 in the place of . When considering an infinitesimal time interval (i.e., ), we have

| (23) | ||||

| (24) | ||||

| (25) |

Observe that the terms associated with the trader’s policy and the terms associated with the adversary’s policy can be separated. This informal argument suggests that the value function has to satisfy the following HJB equation:

| (26) |

In the following theorem, we make this argument more formally and identify the sufficient conditions to be the optimal value function.

Theorem 4 (Verification theorem).

Consider a function satisfying

-

(i)

, and, for any and , it satisfies

(27) where and .

-

(ii)

for all , and for all .

-

(iii)

for all and , and is increasing in on .

-

(iv)

is increasing in on for each , and decreasing in on for each .

-

(v)

is decreasing in on .

Then, for all and .

In Theorem 4, conditions (i) and (ii) specify the HJB equation and the boundary conditions that the value function has to satisfy. In fact, the value function can be uniquely determined by these two conditions. However, the other conditions, (iii)–(v), are also necessary to show that this value is indeed achievable within our definition of the admissible policies, and . More specifically, condition (iii) asserts the symmetry and the monotonicity of the value function with respect to position size , and conditions (iv) and (v) assert certain behaviors of the optimal policies that are implied from the HJB equation (e.g., the optimal liquidation strategy should trade more aggressively when liquidating a larger quantity). While these properties of the value function are natural given the problem structure, they serve as regularity conditions in our proof to resolve technical issues arising in the convergence analysis.

Observe that the optimization terms in the HJB equation (27) are separated and each of them is a trivial quadratic optimization problem. By solving these optimizations explicitly, the HJB equation can be translated into the following partial differential equation:

| (28) |

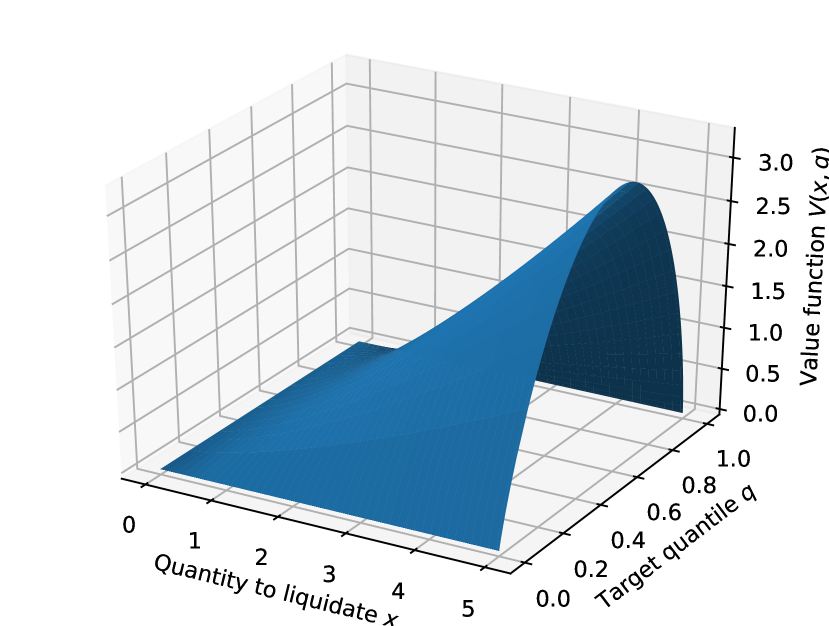

It turns out that this differential equation with the boundary condition (ii) admits a separable solution. The value function can be represented as a product of a function of and a function of , as identified in the following theorem.

Theorem 5 (Value function).

Consider a function defined as

| (29) |

where is the solution in to the following differential equation:

| (30) |

Then, satisfies the conditions of Theorem 4, and hence for all and .

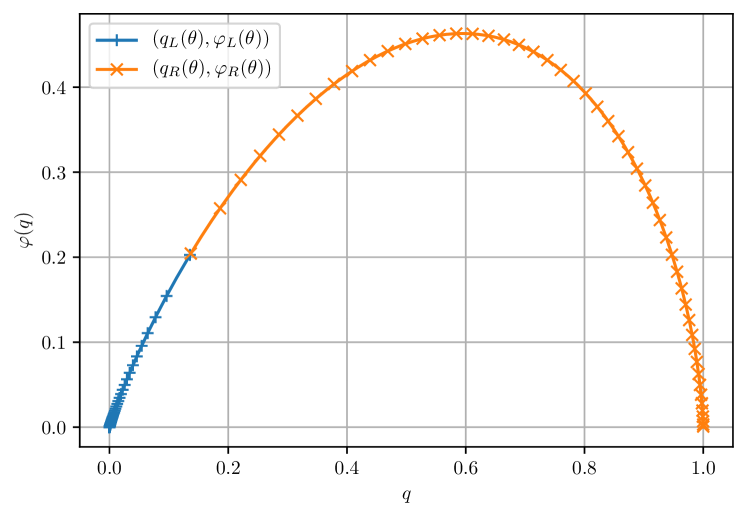

The differential equation of form (30) is known as the Emden-Fowler equation [Polyanin and Zaitsev, 2003, 2.3.27], and its solution can be expressed in parametric form as follows:

Proposition 5 (Parametric representation of ).

The function can be represented in a parametric form that admits a closed-form expression. Define

| (31) |

where and are the first and second kinds of Bessel functions, and is the second kind of modified Bessel function. Further define

| (32) |

Then, the curve is parameterized as

| (33) |

where777The values of and are not defined when . However, the limit points (e.g., , ) do exist, and our parametric representation includes those limit points.

| (34) |

and

| (35) |

4.2 Optimal Adaptive Liquidation Strategy

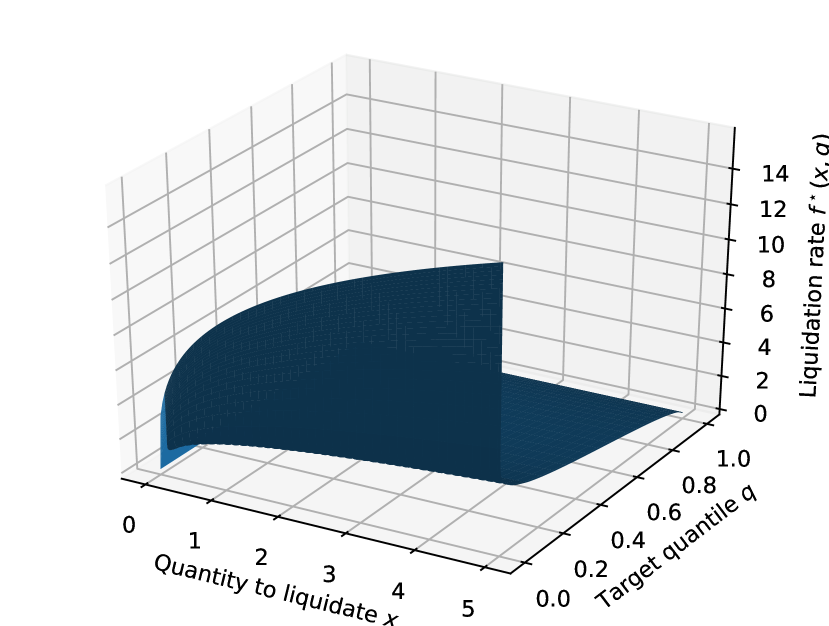

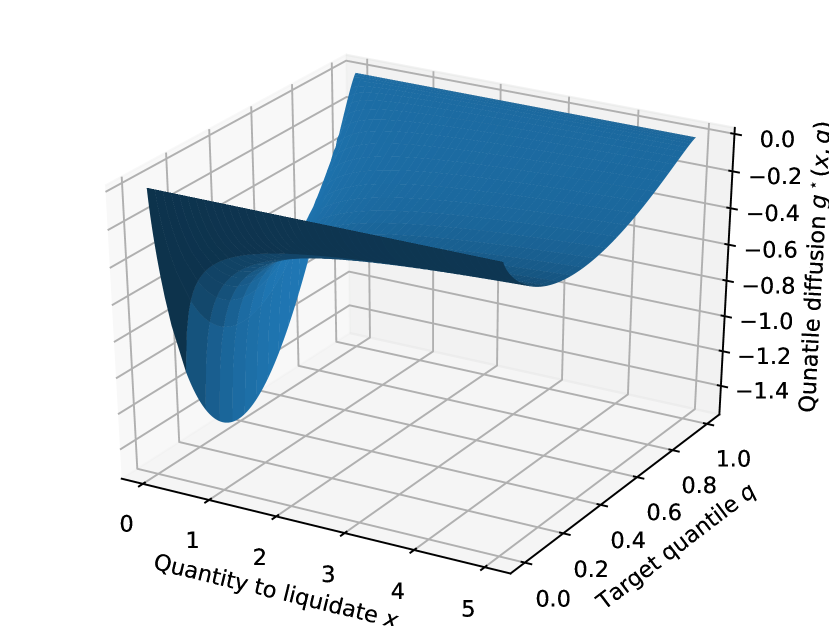

Let and be, respectively, the minimizer and the maximizer of the optimization terms in the HJB equation (27), i.e.,

| (36) | ||||||

| (37) |

where we define for . The function specifies the trader’s optimal liquidation rate when the current position size is and the current quantile level is , and similarly, the function specifies the adversary’s optimal quantile diffusion rate in that situation. We can naturally postulate mutually coupled -Markov policies and induced by these functions and , which are characterizing the equilibrium of the stochastic game.888 This does not mean that the policy is optimal against any adversary’s policy , nor an -Markov policy induced by and coupled with is the best response against . It merely means that is the best response against only, and vice versa. In order to obtain a best response against an arbitrary adversary’s policy , we may need to characterize the best possible performance against , e.g., , and derive and solve the HJB equation associated with it. Nevertheless, the policy is the optimal liquidation strategy that minimizes the CVaR value of implementation shortfall. Under policies and , the system is described by the following stochastic differential equations:

| (38) |

with and .

However, we cannot directly show that the policies and satisfy the admissibility conditions introduced in (3) and (10), because the functions and exhibit extreme behaviors near the boundaries, as shown in Figure 3. For example, if , the liquidation rate may increase unboundedly since , and thus may violate the condition . If , on the other hand, the liquidation rate may vanish since , and thus may violate the condition .

We instead prove that the optimal value function can be achieved ‘‘asymptotically’’ by a sequence of admissible policies that approximate and .

Theorem 6 (Policy optimality).

There exists a sequence of function pairs with and such that

| (39) |

and it satisfies the following properties for any and :

-

(a)

For any given , let be an -Markov trader’s policy induced by and coupled with . Then, is admissible and

(40) -

(b)

For any given , let be an -Markov adversary’s policy induced by and coupled with . Then, is admissible and

(41) -

(c)

Let be a mutually coupled -Markov policy pair induced by . Then, and are admissible and

(42)

Theorem 6 shows that we can construct a sequence of functions that converges to pointwise except at the boundaries, and further induces -Markov policies that are admissible and asymptotically optimal. More precisely, against any adversary’s policy , the sequence of functions induces a sequence of admissible policies for the trader, and in the limit, the trader achieves an outcome that is no worse than the equilibrium outcome. And vice versa, against any trader’s policy , the sequence of functions induces a sequence of admissible policies for the adversary, and in the limit, the adversary achieves an outcome that is no worse than the equilibrium outcome. As a combination, the sequence of function pairs induces a sequence of mutually admissible policy pairs that yields the equilibrium outcome asymptotically.

The construction of such a sequence of function pairs is straightforward. We consider a vanishing subset of the augmented state space that contains the boundaries, i.e., , and obtain and by suppressing the extreme behaviors of and arising in this subset. Roughly speaking, the liquidation strategy induced by mimics the optimal strategy until it clears almost all positions (i.e., ) or it becomes almost risk-neutral (i.e., ) or extremely risk-averse (i.e., ), and then liquidates according to a deterministic schedule thereafter. We can show that the gap between the outcome of this approximated strategy and the theoretical equilibrium outcome is diminishing as goes to infinity. We refer the readers to Appendix D for the details.

Aggressiveness-in-the-money. Despite that the admissibility of the optimal liquidation policy is not guaranteed, we can still characterize its behaviors by inspecting the stochastic differential equations (38). Without loss of generality, let us consider the task of liquidation (i.e., ).

First, we observe that the optimal policy liquidates only (i.e., ), until it completes the execution999 We are not sure if the completion time is almost surely finite even though the position will be vanishing eventually (i.e., ). In particular, when , the optimal policy trades very slowly () and the position process may never hit zero. We believe that the completion time is finite with a probability of at least . (i.e., ). Note that we have not imposed any constraint on the trading direction. This formally shows that winding back the position during the liquidation process will never be helpful in reducing the CVaR loss.

Second, when the trader becomes more risk-averse (i.e., ), the optimal policy trades more aggressively (i.e., ). The opposite also holds true. This is because, by liquidating the position more quickly, it can reduce the risk exposure to the changes in price more effectively. Even though it will be more costly in terms of market impact, it can make sure that the transactions will be made at a certain level, which is more beneficial to a risk-averse trader than a risk-neutral trader. We can also understand this behavior based on the alternative interpretation of the problem discussed in Remark 2: when the risk-averse liquidation problem is cast as a risk-neutral execution problem that involves an adverse price drift, being more risk-averse is equivalent to facing a more adverse price drift, which encourages the risk-neutral trader to trade more aggressively.

Most interestingly, we observe that when the price moves in a favorable direction toward in-the-money (i.e., ), the policy becomes more risk-averse (i.e., since ) and hence it trades more aggressively. This formally characterizes aggressiveness-in-the-money, which has been observed by Lorenz and Almgren [2007, 2011], Gatheral and Schied [2011], Forsyth et al. [2012]. Intuitively, if the trader has made some ‘‘free’’ money due to the price change, he would have an additional incentive to complete the liquidation early so as to secure his current profit, and thus he would be willing to pay an additional deterministic cost for aggressive execution.

This behavior can also be understood in the context of a more general risk-sensitive optimal control problem. Recall that the optimal adversary’s martingale represents the likelihood that the current sample path leads to one of the worst -fraction of outcomes. When something favorable happens, it becomes less likely that the sample path is in the worst quantile, and therefore decreases. This means that the trader will need to pay attention to a smaller fraction of adverse scenarios; i.e., he will become more risk-averse.

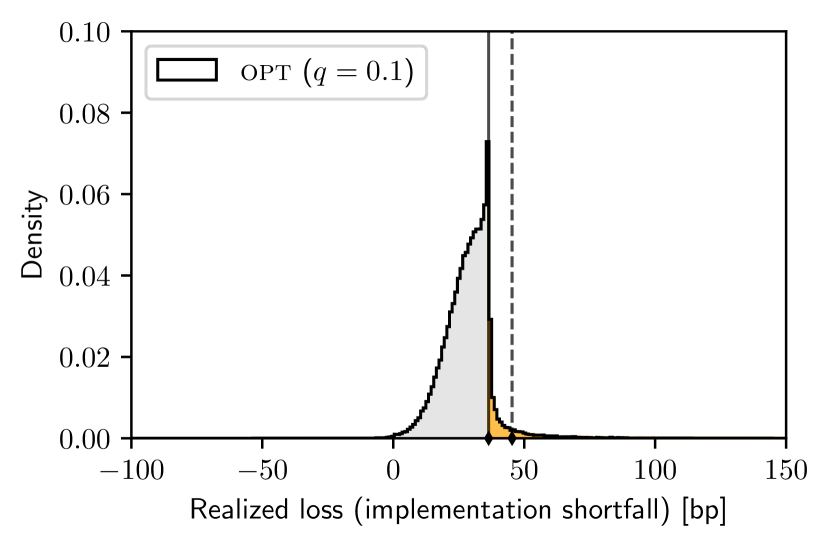

Threshold behavior. While we do not have a formal characterization here, we observe that the optimal strategy exhibits some threshold behavior, particularly near the end of the liquidation. We observe that the policy trades aggressively when the cumulative cost is below some threshold, and it trades passively when the cumulative cost is above the threshold. Near the end of the liquidation, such a threshold corresponds to (the value-at-risk, i.e., the quantile of the loss distribution), and the liquidation rate sharply changes around . This behavior is related to an alternative representation of CVaR [Rockafellar and Uryasev, 2002]: , where the maximizer is in fact , and only concerns the cases where .

To better illustrate, suppose that the trader is currently left with a small amount of position to liquidate. If , the trader is willing to pay a large transaction cost (up to ) to complete the execution as soon as possible, thereby making sure that the total loss won’t exceed the threshold . If , the trader may believe that the total loss will inevitably exceed the threshold , and then tries to minimize the expected future cost by slowing down the liquidation. One can make a connection with aggressiveness-in-the-money, since having implies that the price has moved in a favorable direction.

We believe that the threshold value is a function of remaining position size such that it increases as the position size decreases and converges to as the position vanishes. Moreover, the change in the aggressiveness around the threshold also depends on the remaining position size. To formalize this behavior, one may adopt an alternative formulation of the problem with an extra state variable representing the cost realized so far (i.e., a Markov policy defined on the augmented state space ), which is in fact the approach suggested by Bäuerle and Ott [2011] for a general class of control problems with a CVaR objective. This might be a topic of future research.

5 Cost Analysis: Adaptive vs. Deterministic Strategy

In this section, we provide a comparison between the optimal adaptive strategy derived in §4 and the (optimized) deterministic schedules under which the liquidation is executed according to a deterministic schedule committed at the beginning of the liquidation process.

5.1 Optimized Deterministic Schedules

First observe that any deterministic schedule will yield a normally distributed implementation shortfall; i.e., given a deterministic schedule , the total implementation shortfall follows a normal distribution with mean and variance given by

| (43) |

To understand the performance of deterministic schedules, therefore, it suffices consider the CVaR value of a normal distribution.

Given a normal random variable , it is easy to verify that

| (44) |

where

| (45) |

and and are the p.d.f. and the c.d.f. of a standard normal distribution, respectively. Thus,

| (46) |

for any deterministic schedule .

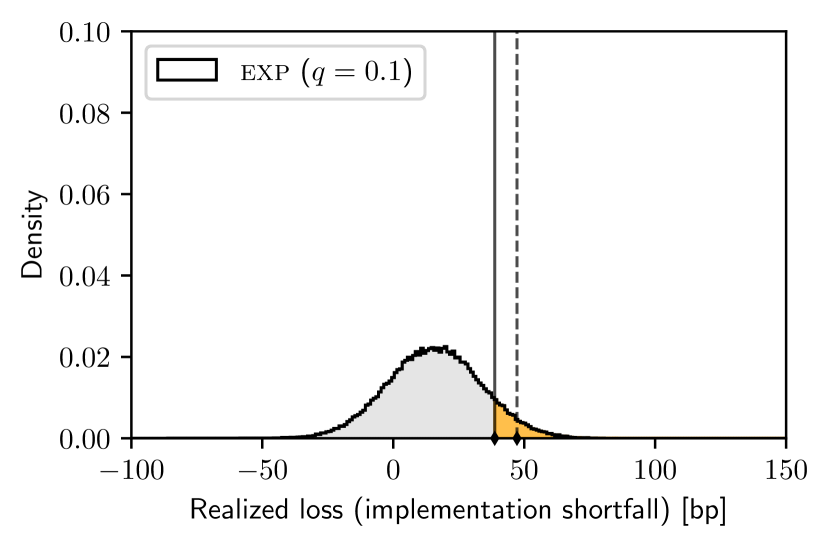

We first focus on the set of all deterministic schedules and find the optimal one that minimizes the CVaR cost. The next proposition shows that such an optimal schedule has the form of an exponential schedule under which the trader’s position decays exponentially over time (i.e., the liquidation rate is proportional to the current position size).

Proposition 6 (Optimized deterministic schedule).

Given an initial position and a target quantile , the optimal deterministic schedule is given by an exponential schedule where the optimal time constant is given by

| (47) |

Let exp be this optimized exponential schedule. Then, its performance is given by

| (48) |

While the proof is provided in Appendix A, we remark that the optimality of the exponential schedule can be directly inferred from the result of Almgren and Chriss [2000]: it was shown that, given a finite time-horizon of length , a mean-variance optimization results in a trajectory for some constant . As , we can observe that the optimized trajectory converges to an exponential schedule .

We next examine the volume-weighted average price (VWAP) schedules, under which the trader liquidates the asset at a constant rate until completion so that the trader’s position decreases linearly over time.101010 A VWAP schedule typically refers to a liquidation schedule that is proportional to the average market volume profile, aiming to make its average transaction price close to the market volume-weighted average price. As we assume a time-stationary market in this paper, the VWAP schedule is equivalent to a constant liquidation rate schedule (also known as a TWAP schedule). The next proposition identifies the optimized VWAP schedule (see Appendix A for the proof).

Proposition 7 (Optimized VWAP schedule).

Given an initial position and a target quantile , the best VWAP schedule is given by , where the optimal execution period is as follows:

| (49) |

Let vwap be this optimized VWAP schedule. Then, its performance is given by

| (50) |

5.2 Cost Analysis

We now compare three liquidation strategies: the optimal adaptive strategy (opt) derived in §4, the optimized deterministic strategy (exp), and the optimized VWAP strategy (vwap). We have derived closed-form expressions (29), (48), and (50) that represent their S-CVaR performance , , and , respectively. Given that by their definitions, we particularly consider the following ratios that are useful for pairwise comparison:

| (51) |

Note that these ratios do not change even if we compare performance instead of performance since is merely a scaled version of (see Remark 1(i)).

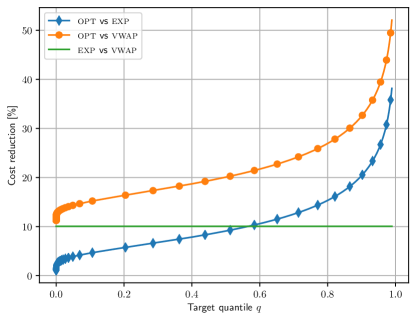

These ratios can be expressed in closed form, and we observe the following. First, all the ratios depend only on the quantile , but not on the other problem parameters such as the quantity to liquidate , the price volatility , and the market impact factor . Figure 4 plots these ratios as functions of . Second, the optimal deterministic schedule always outperforms to the best VWAP schedule by , irrespective of the value of . Finally, in a moderate range of , from to , the adaptive strategy outperforms the optimal deterministic strategy by to , and outperforms the optimized VWAP strategy by to . This gap increases as increases (i.e., becomes more risk-neutral). More specifically, it explodes as approaches one, and vanishes as approaches zero.111111 The absolute performance (i.e., the CVaR cost) of all three policies converges to zero as , and diverges to infinity as . Note that most traders using optimal execution algorithms are large investors trading a small portion of their overall portfolio over a short time horizon. Thus, from the perspective of optimal decision making, their utility functions are nearly linear, hence the nearly risk neutral regime (), where the relative benefits of dynamic trading are greatest, is also the most practically relevant regime. See also §6.2 for a more illustrative comparison between the adaptive strategy and the deterministic strategies.

6 Numerical Simulations

Throughout this section, we denote the optimal adaptive strategy by opt, the optimized deterministic schedule by exp, and the optimized VWAP schedule by vwap.

6.1 Illustration of Optimal Adaptive Strategy

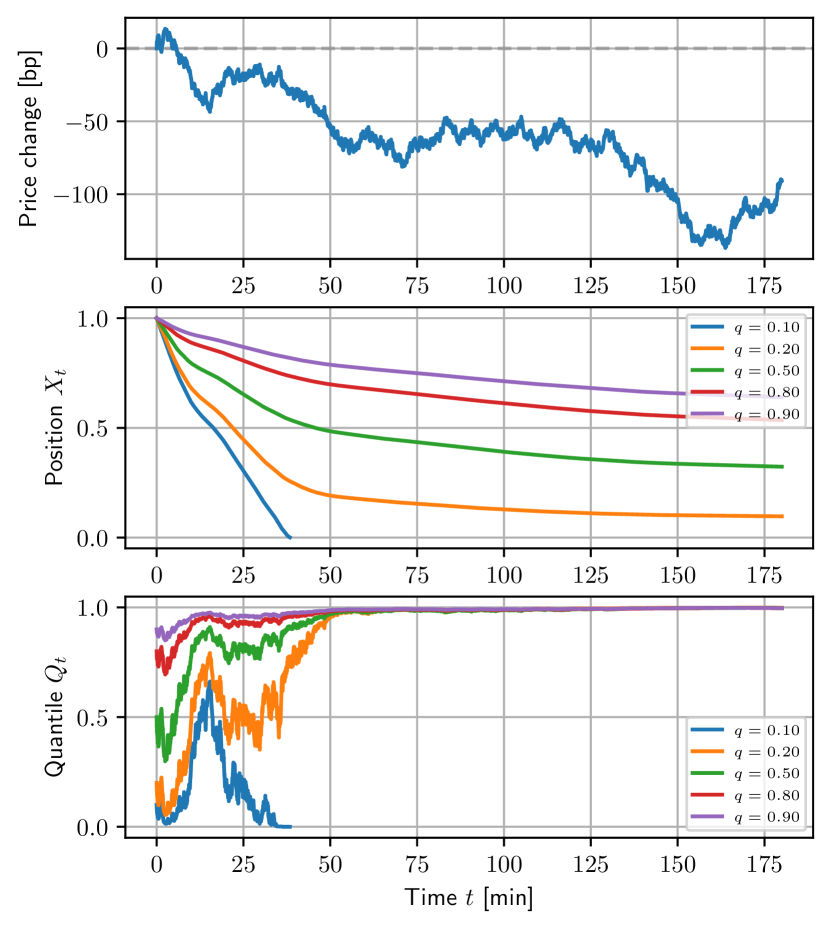

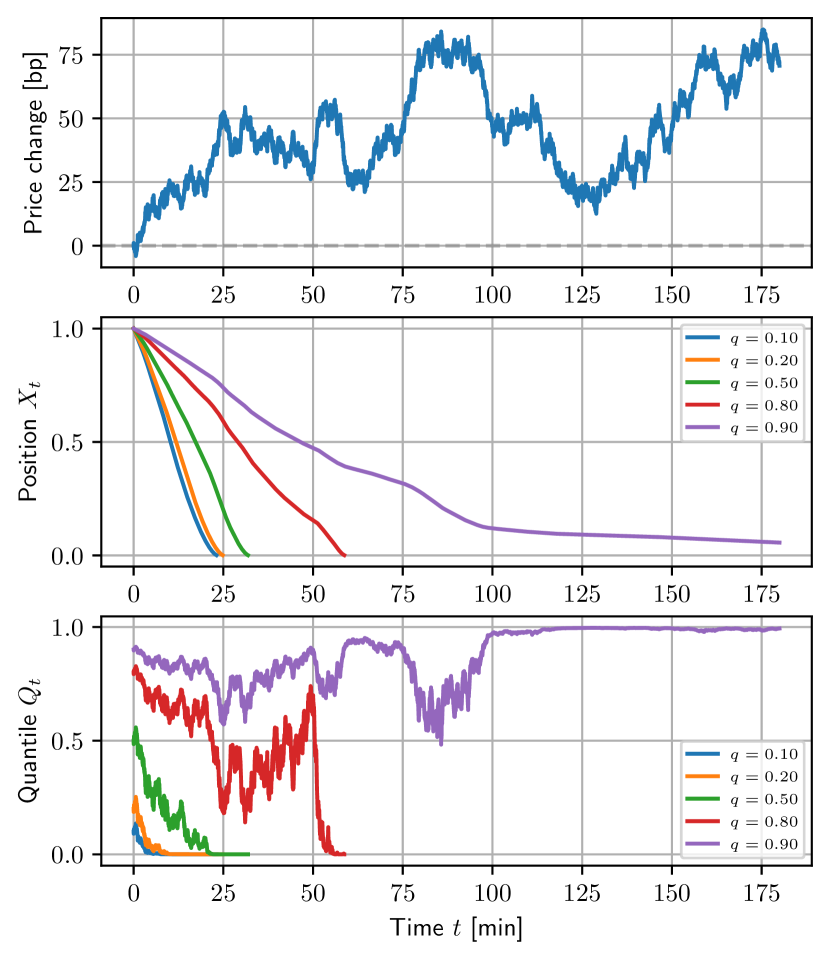

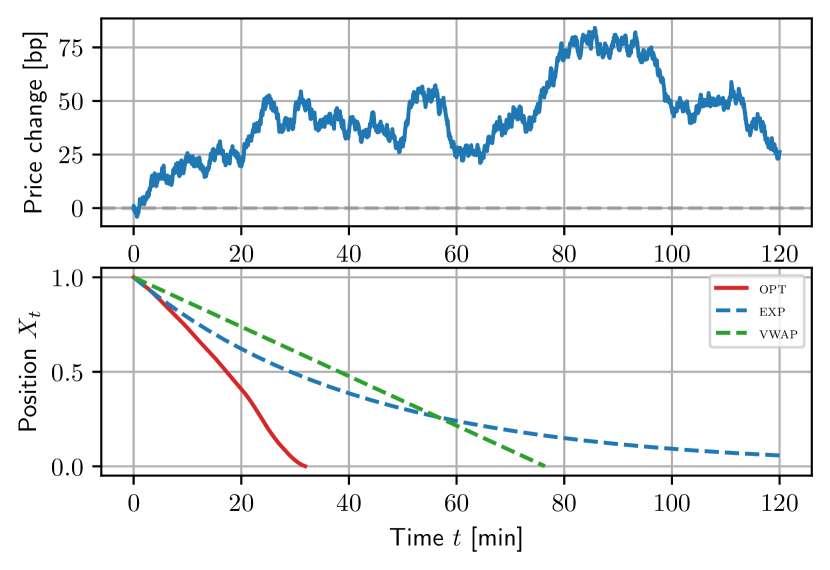

We consider a situation where the trader wants to liquidate unit of an asset given the volatility basis points per minute ( per day), the market impact factor (liquidating one unit over a day at a constant rate incurs basis points loss in average), and the target quantile varying from to .

We simulate the optimal policy opt as follows. We first discretize the time horizon into subintervals of equal length , and generate a sample path of the standard Brownian motion . Starting from and , at each time , we compute the liquidation rate and the quantile diffusion rate and then update the position size and the quantile accordingly, where . The expressions for and are given in (36) and (37), and the value of can be computed using linear interpolation based on its parametric representation derived in Proposition 5. In order to prevent numerical instability, we keep the value of quantile process between and via truncation (we take ); i.e., if or , it is set to or , respectively. This procedure is repeated until the remaining position size becomes smaller than .

Figure 5 illustrates the sample paths of the price process , the position process , and the quantile process under opt for different values of target quantile in the following two scenarios: when the price moves in an adverse direction (left), and when the price moves in a favorable direction (right). From these results, we confirm the behaviors of the optimal strategy characterized in §4.2. In every case, the position monotonically decreases over time; i.e., the optimal policy keeps trading in one direction. Also observe that the policy liquidates the position more aggressively as we take a smaller value for (i.e., as the policy becomes more risk-averse). In a comparison between two scenarios (left vs. right), we observe ‘‘aggressiveness-in-the-money’’; i.e., the policy trades more aggressively when the price moves in a favorable direction (right). This behavior can also be observed within each sample path: during the execution process, the quantile process decreases when the price moves upward and the policy trades more aggressively. In addition, the quantile process converges to either zero or one, indicating whether the realized price process is among the worst -fraction of the scenarios. While not reported here, we observe that converges to one in the -fraction of simulations and converges to zero in the other -fraction of simulations (recall that is a martingale starting at ).

6.2 Comparison with Deterministic Strategies

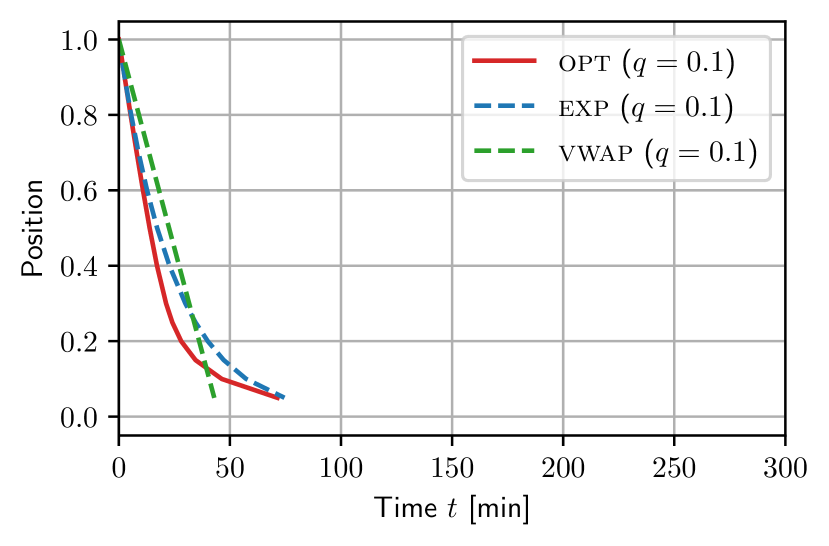

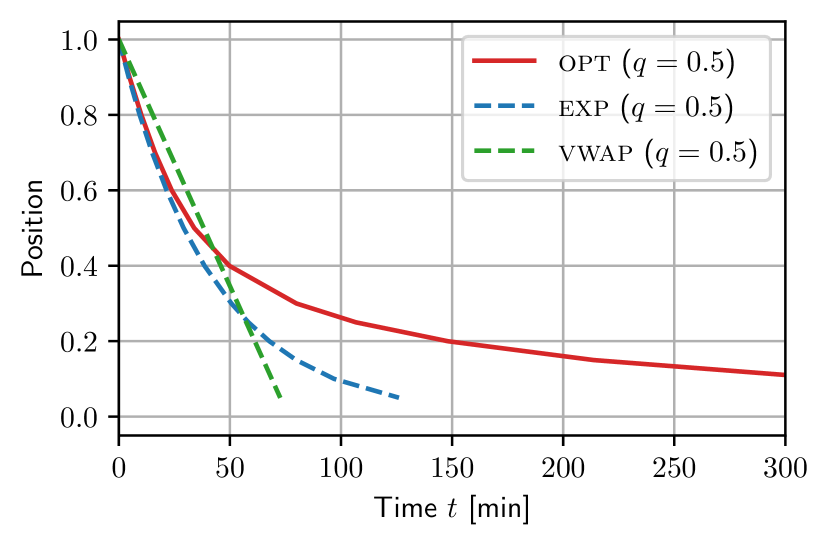

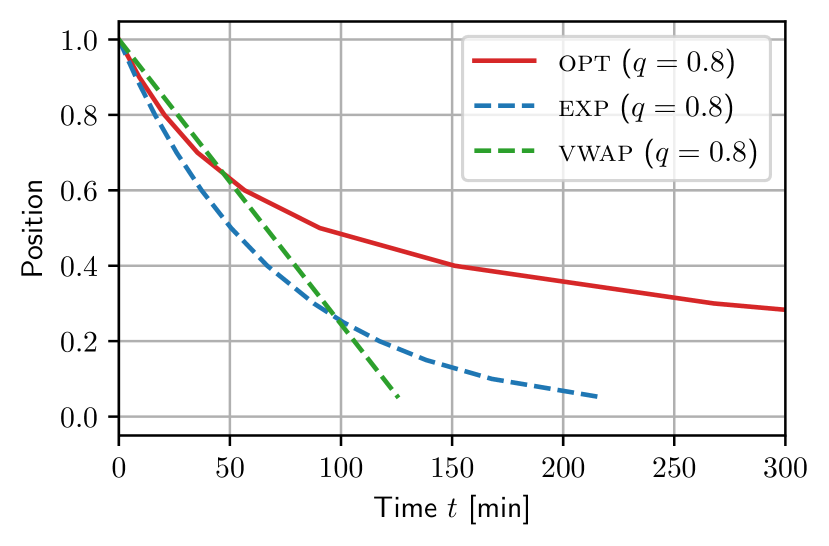

We provide the detailed simulation results of the optimal adaptive strategy (opt) in a comparison with those of the deterministic strategies (exp, vwap) introduced in §5.1.

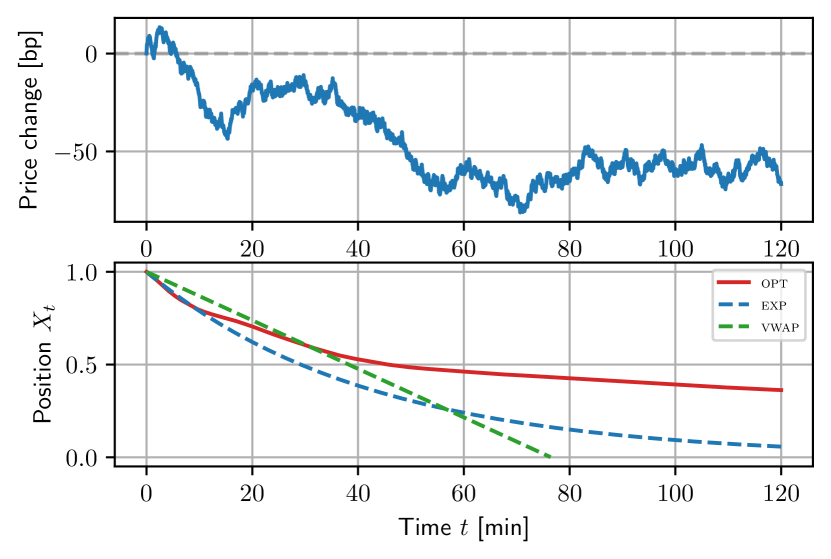

Figure 6 illustrates the position process trajectories under these three strategies with target quantile in the two scenarios as in Figure 5. One can immediately observe that the deterministic strategies are not adaptive to the price changes. The optimal adaptive strategy opt liquidates at a similar rate to the exponential schedule exp during the initial periods, but it deviates as soon as it adjusts its aggressiveness adaptively to the price changes. In particular, it slows down when the price moves in the adverse direction (i.e., the quantile process moves toward one). Figure 7 shows the average position trajectories under these three strategies given the target quantile , aggregated across 100,000 runs of simulations. Similarly to the above, we observe that opt trades more aggressively than exp when the target quantile is small and less aggressively when the target quantile is large.

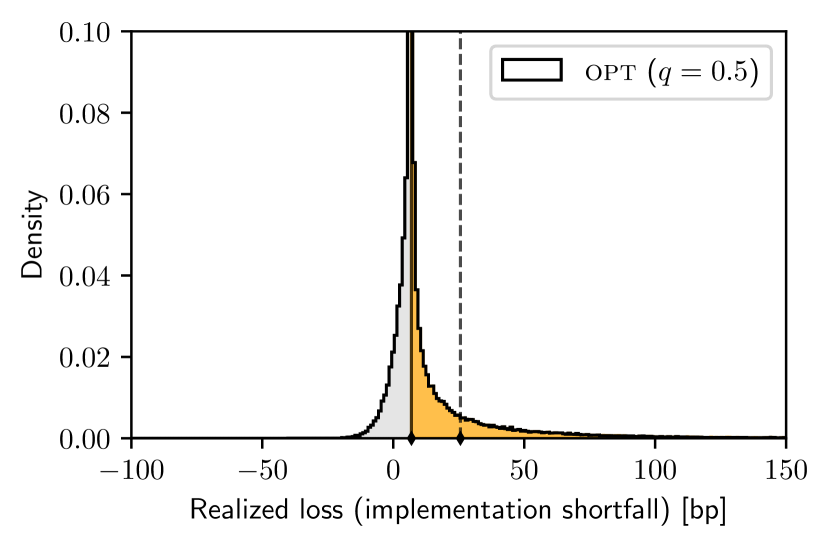

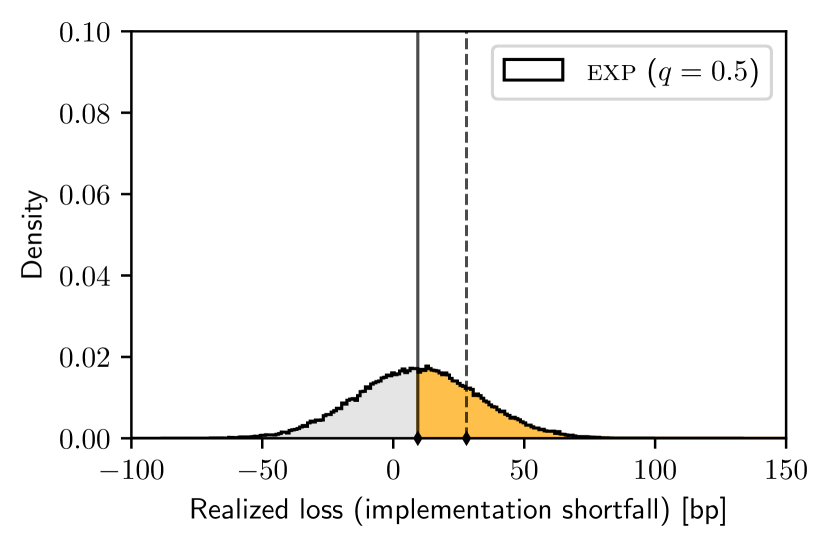

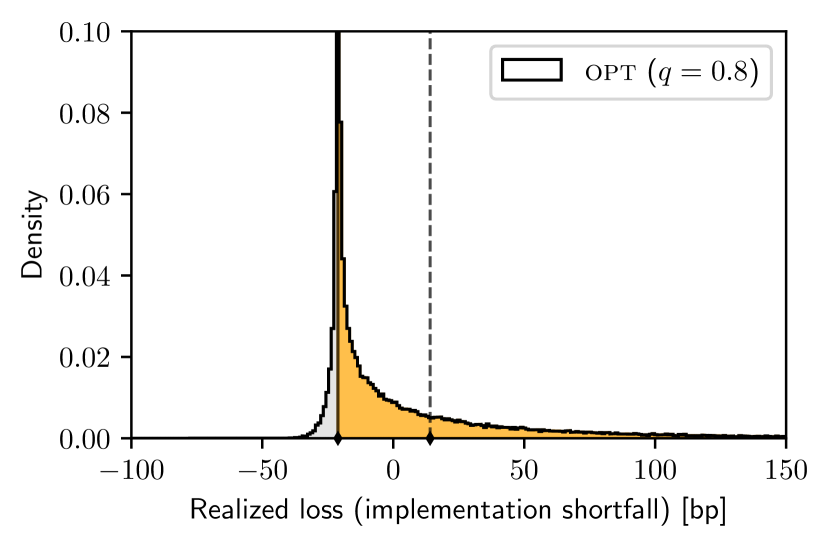

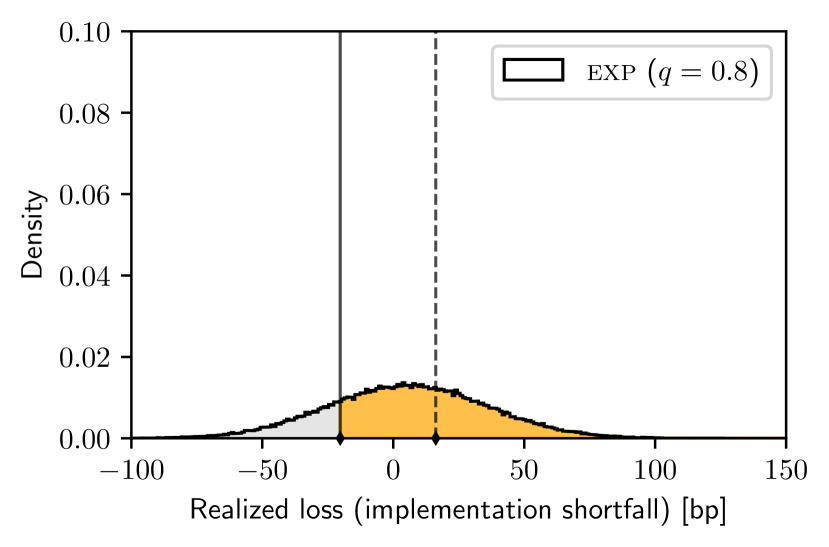

Figure 8 shows the implementation shortfall distributions (i.e., the histograms of ) resulting from opt (top) and exp (bottom) with different values of the target quantile . These histograms are obtained from simulation trials, where all the strategies see the same price process realization per simulation. The resulting distributions are visually very different: exp yields a normal distribution whereas opt yields a distribution that has a sharp peak at the quantile. Such a sharp peak can be explained by the threshold behavior of the optimal adaptive strategy, discussed at the end of §4.2. Figure 9 visualizes these distributions for a wider range of target quantiles . We observe that the implementation shortfall distribution induced by opt is more concentrated than the ones induced by exp and vwap when the target quantile is small, and it is the opposite when the target quantile is large (roughly speaking, it has a longer right tail, visually similar to an exponential distribution).

Table 1 reports in detail the summary statistics of those implementation shortfall distributions. We first confirm that the simulation results are consistent with our theoretic predictions, i.e., the measured CVaR values match with the values calculated from the expressions (29), (48), and (50). We also see that the optimal adaptive strategy does not make an improvement over the deterministic strategies in terms of the average nor the variance as it specifically targets to minimize the CVaR value at a given target quantile. But, it significantly improves the median value particularly in the risk-neutral regime (when ). See also a discussion on Figure 10 below.

| Target quantile | Policy | CVaR (theo.) | VaR | Average | Median | Std. dev. | 50% time | 95% time |

| opt | () | |||||||

| exp | () | |||||||

| vwap | () | |||||||

| opt | () | |||||||

| exp | () | |||||||

| vwap | () | |||||||

| opt | () | |||||||

| exp | () | |||||||

| vwap | () | |||||||

| opt | () | |||||||

| exp | () | |||||||

| vwap | () | |||||||

| opt | () | |||||||

| exp | () | |||||||

| vwap | () | |||||||

| opt | () | |||||||

| exp | () | |||||||

| vwap | () | |||||||

| opt | () | |||||||

| exp | () | |||||||

| vwap | () | |||||||

| opt | () | |||||||

| exp | () | |||||||

| vwap | () | |||||||

| opt | () | |||||||

| exp | () | |||||||

| vwap | () | |||||||

| opt | () | |||||||

| exp | () | |||||||

| vwap | () | |||||||

| opt | () | |||||||

| exp | () | |||||||

| vwap | () |

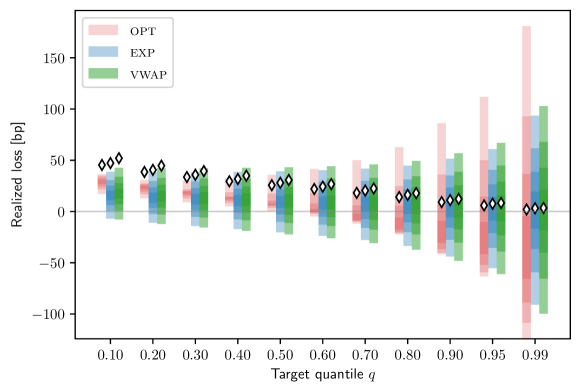

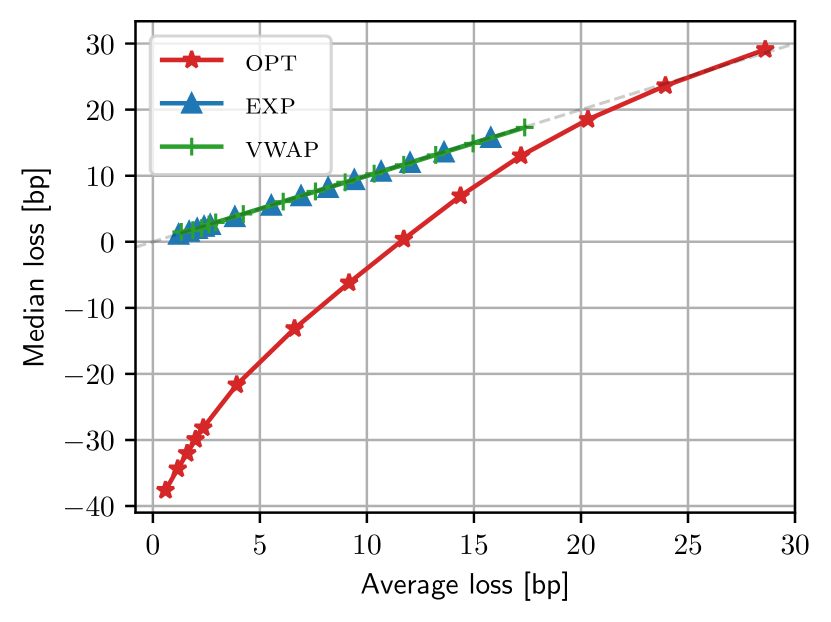

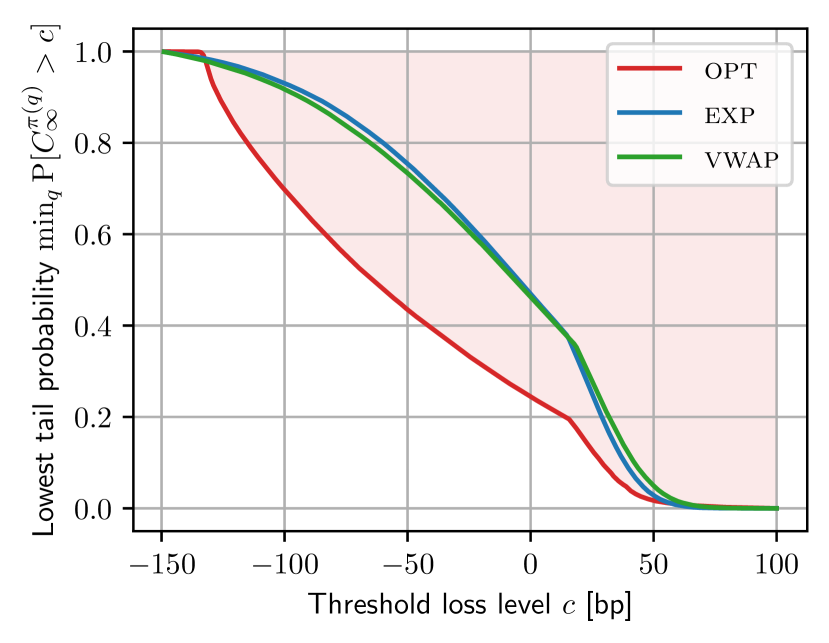

Figure 10 demonstrates some additional advantages of the adaptive strategy other than minimizing the CVaR value. Here, the target quantile is considered as a control parameter to the strategies on the behalf of a trader who may not be particularly interested in minimizing the CVaR value, and we compare three families of strategies (opt, exp, and vwap with the target quantile ranging from to ) in terms of the mean, the median, and the tail probability of the resulting implementation shortfall distributions. It is shown in the left plot that, by implementing the adaptive strategy opt with a suitably chosen target quantile, it can achieve a smaller median value than any of deterministic strategies that yield the same average loss value. Similarly, it is shown in the right plot that a smaller tail probability can be achieved by opt for a given target threshold level: for example, when wanting to avoid the event that the implementation shortfall exceeds 25 basis points, the trader can implement opt with the target quantile so that such event takes place with probability 12.9%, whereas the probability is 25.3% under the best deterministic schedule (exp with ).

References

- Almgren and Chriss [2000] Robert Almgren and Neil Chriss. Optimal execution of portfolio transactions. 2000.

- Artzner et al. [1999] Philippe Artzner, Freddy Delbaen, Jean-Mark Eber, and David Heath. Coherent measures of risk. Mathematical Finance, 9(3):203–228, 1999.

- Artzner et al. [2007] Philippe Artzner, Freddy Delbaen, Jean-Marc Eber, David Heath, and Hyejin Ku. Coherent multiperiod risk adjusted values and Bellman’s principle. Annals of Operations Research, 152:5–22, 2007.

- Backhoff-Veraguas and Tangpi [2020] Julio Backhoff-Veraguas and Ludovic Tangpi. On the dynamic representation of some time-inconsistent risk measures in a Brownian filtration. Mathematics and Financial Economics, 14:433–460, 2020.

- Barbu and Precupanu [2012] Viorel Barbu and Teodor Precupanu. Convexity and Optimization in Banach Spaces. Springer, 4th edition, 2012.

- Bäuerle and Ott [2011] Nicole Bäuerle and Jonathan Ott. Markov decision processes with average-value-at-risk criteria. Mathematical Methods of Operational Research, 74(4):361–379, 2011.

- Chapman et al. [2018] Margaret P. Chapman, Jonathan P. Lacotte, Kevin M. Smith, Insoon Yang, Yuxi Han, Marco Pavone, and Claire J. Tomlin. Risk-sensitive safety specifications for stochastic system using conditional value-at-risk. 2018.

- Chow et al. [2015] Yinlam Chow, Aviv Tamar, Shie Mannor, and Marco Pavone. Risk-sensitive and robust decision-making: a CVaR optimization approach. Advances in Neural Information Processing Systems 28 (NIPS 2015), 2015.

- Chow et al. [2018] Yinlam Chow, Mohammad Ghavamzadeh, Lucas Janson, and Marco Pavone. Risk-constrained reinforcement learning with percentile risk criteria. Journal of Machine Learning Research, 18:1–51, 2018.

- Courant and Hilbert [1953] R. Courant and D. Hilbert. Methods of Mathematical Physics, volume I. New York and London (Interscience Publishers), 1953.

- Durrett [2010] Rick Durrett. Probability: Theory and Examples. Cambridge University Press, 4th edition, 2010.

- Forsyth [2011] Peter A. Forsyth. A Hamilton–Jacobi–Bellman approach to optimal trade execution. Applied Numerical Mathematics, 61:241–265, 2011.

- Forsyth et al. [2012] Peter A. Forsyth, Shannon Kennedy, Shu Tong Tse, and Heath Windcliff. Optimal trade execution: A mean quadratic variation approach. Journal of Economic Dynamics & Control, 36:1971–1991, 2012.

- Gatheral and Schied [2011] Jim Gatheral and Alexander Schied. Optimal trade execution under geometric Brownian motion in the Almgren and Chriss framework. International Journal of Theoretical and Applied Finance, 14(3):353–368, 2011.

- Glasserman and Xu [2013] Paul Glasserman and Xingbo Xu. Robust portfolio control with stochastic factor dynamics. Operations Research, 61(4):874–893, 2013.

- Huang and Guo [2016] Yonghui Huang and Xianping Guo. Minimum average value-at-risk for finite horizon semi-Markov decision processes in continuous time. SIAM Journal on Optimization, 26(1):1–28, 2016.

- Kissell and Malamut [2005] Robert Kissell and Roberto Malamut. Understanding the profit and loss distribution of trading algorithms. In B. R. Bruce, editor, Algorithmic Trading, pages 41–49. Institutional Investor, 2005.

- Li et al. [2020] Xiaocheng Li, Huaiyang Zhong, and Margaret L. Brandeau. Quantile Markov decision processes. 2020.

- Lin et al. [2015] Qihang Lin, Xi Chen, and Javier Peña. A trade execution model under a composite dynamic coherent risk measure. Operations Research Letters, 43:52–58, 2015.

- Lorenz and Almgren [2007] Julian Lorenz and Robert Almgren. Adaptive arrival price. In B. R. Bruce, editor, Algorithmic Trading III, pages 59–66. Institutional Investor, 2007.

- Lorenz and Almgren [2011] Julian Lorenz and Robert Almgren. Mean-variance optimal adaptive execution. Applied Mathematical Finance, 18(5):395–422, 2011.

- Miller and Yang [2017] Christopher W. Miller and Insoon Yang. Optimal control of conditional value-at-risk in continuous time. SIAM Journal on Control and Optimization, 55(2):856–884, 2017.

- Pflug and Pichler [2016] Georg Ch. Pflug and Alois Pichler. Time-inconsistent multistage stochastic programs: Martingale bounds. European Journal of Operational Research, 249:155–163, 2016.

- Polyanin and Zaitsev [2003] Andrei D. Polyanin and Valentin F. Zaitsev. Handbook of Exact Solutions for Ordinary Differential Equations. Chapman & Hall/CRC Press, 2003.

- Protter [2015] Philip Protter. Stochastic Integration and Differential Equations. Springer, 2015.

- Rockafellar and Uryasev [2002] R. Tyrrell Rockafellar and Stanislav Uryasev. Conditional value-at-risk for general loss distributions. Journal of Banking & Finance, 26:1443–1471, 2002.

- Schied and Schöneborn [2009] Alexander Schied and Torsten Schöneborn. Risk aversion and the dynamics of optimal liquidation strategies in illiquid markets. Finance and Stochastics, 13(2):181–204, 2009.

- Shapiro [2009] Alexander Shapiro. On a time consistency concept in risk averse multistage stochastic programming. Operations Research Letters, 37:143–147, 2009.

- Sion [1958] Maurice Sion. On general minimax theorems. Pacific Journal of Mathematics, 8(1):171–176, 1958.

Organization of appendix. The appendix is organized as follows. In Appendix A, we identify the optimal deterministic strategy and its performance for §5.1. The CVaR performance of the optimal deterministic strategy is utilized as an upper bound on the CVaR performance of the optimal adaptive strategy. In Appendix B, we provide the basic characterizations of S-CVaR measure introduced in §2. In Appendix C, we provide the preliminary characterizations of the value function, and by applying Sion’s minimax theorem, we prove Theorem 2 and Theorem 3 stated in §3. The main challenge here is to verify the conditions of Sion’s minimax theorem. In Appendix D, we provide proofs for §4. We first state and prove Theorem 7 from which Theorem 4 and Theorem 6 follow almost immediately. Proposition 4, Proposition 5 and Theorem 5 are proven separately.

Appendix A Optimal Deterministic Schedules

Lemma 2.

For any ,

| (52) |

Proof.

Let . Since , the equation has a unique solution at . ∎

Proof of Proposition 6.

We prove the optimality of exponential schedules and identify the optimal decaying rate.

First we consider a mean-variance optimization problem:

| (53) |

where is the set of all deterministic policies and is a penalty for variance term. Applying (44), this is equivalent to an optimization over the deterministic trajectories of :

| (54) |

where . By applying standard calculus of variations arguments [Courant and Hilbert, 1953], we deduce that the optimal schedule has to satisfy the Euler-Lagrange equation at each time , with boundary conditions and . The solution is uniquely given by an exponential schedule

| (55) |

with the decay rate , and such a schedule yields

| (56) |

In other words, the efficient frontier of the range of mean and variance achievable by deterministic schedules, , is given by and is attained by exponential schedules.

Let us now consider the achievable range of mean and standard deviation, . Observe that its efficient frontier is still characterized by . Therefore, the optimal solution of the following mean-standard deviation optimization problem

| (57) |

is also given by an exponential schedule, for any given .

Proof of Proposition 7.

With some calculation, it can be easily shown that a VWAP schedule yields

| (60) |

Therefore, the optimal execution horizon is given by

| (61) |

∎

We state the following lemma that identifies the boundary values of , which is useful to characterize the optimal value function.

Lemma 3.

The function given in (45) satisfies

| (62) |

Proof.

Recall that . Since for any , we have . Also note that since and . Therefore, it suffices to show that .

We have the following tail bounds of standard normal distribution [Durrett, 2010, Theorem 1.2.3]: for any ,

| (63) |

Define , and then we have

| (64) |

for large enough (such that ) since . Observe that and thus . We further deduce that, since ,

| (65) |

Therefore, . ∎

Appendix B Preliminary Characterizations of

We begin with a technical lemma:

Lemma 4.

The risk envelope is a non-empty, convex, and weak-* compact subset of .

Proof.

It is non-empty because is always feasible.

Consider and for some . Since , we have , and by the linearity of expectation, . Therefore, and thus is convex.

Finally, note that is a closed subset of the unit ball in . Given that is the dual space of , it is weak-* compact by Banach-Alaoglu theorem. ∎

Proof of Proposition 1.

Proof of claim (i) and (v). Claim (i) immediately follows from our definition of CVaR. Claim (v) follows from the following identity [Shapiro, 2009, Theorem 6.2]:

| (66) |

Proof of claim (ii). When , the risk envelope has a single element , and hence, . When , the risk envelope also has a single element , and hence, .

Proof of claim (iii). For any , we have since almost surely, and therefore, . Furthermore, contains , and therefore, .

Appendix C Proofs for §3

From now on, we characterize as a mapping from to . This can be done without loss generality since we have for any feasible policy . This is to utilize the fact that is reflexive so that its weak-* topology coincides with its weak topology.

Lemma 5.

The risk envelope is a weakly compact subset of .

Proof.

As stated in the proof of Lemma 4, is a closed subset of the unit ball in , which is a subset of . By Banach–Alaoglu theorem, it is weak-* compact in and hence weakly compact since is reflexive. ∎

Proof of Proposition 2.

Proof of claim (i). Note that is a continuous local martingale since it is a stochastic integral of a progressively measurable process with respect to Brownian motion [Protter, 2015, Theorem 33 in Chap. III]. Since for any by the definition of , it is a bounded local martingale, which is indeed a martingale [Protter, 2015, Thm. 51 in Chap. I].

Proof of claim (ii). The limit exists due to martingale convergence theorem [Protter, 2015, Theorem 10 in Chap. I].

Proof of claim (iii). Recall that is a martingale taking values in . Define a stopping time . Then, for any , we have and therefore almost surely (otherwise, we would have ). In words, once hits zero, it never escapes thereafter, and the same argument holds for the other boundary. ∎

C.1 Proof of Theorem 2

Within this subsection, we characterize the trader’s policy with its position process rather than dealing with the liquidation rate process : the set of admissible policies is represented as

| (69) |

where we require that each sample path is differentiable so that we can define . Then, . Accordingly, we represent the loss process as

| (70) |

so that we have if and .

We aim to prove Theorem 2 by utilizing Sion’s minimax theorem:

Lemma 6 (Sion’s minimax theorem [Sion, 1958]).