Monitoring Model Deterioration with Explainable Uncertainty Estimation via Non-parametric Bootstrap

Abstract

Monitoring machine learning models once they are deployed is challenging. It is even more challenging to decide when to retrain models in real-case scenarios when labeled data is beyond reach, and monitoring performance metrics becomes unfeasible. In this work, we use non-parametric bootstrapped uncertainty estimates and SHAP values to provide explainable uncertainty estimation as a technique that aims to monitor the deterioration of machine learning models in deployment environments, as well as determine the source of model deterioration when target labels are not available. Classical methods are purely aimed at detecting distribution shift, which can lead to false positives in the sense that the model has not deteriorated despite a shift in the data distribution. To estimate model uncertainty we construct prediction intervals using a novel bootstrap method, which improves upon the work of Kumar and Srivastava (2012). We show that both our model deterioration detection system as well as our uncertainty estimation method achieve better performance than the current state-of-the-art. Finally, we use explainable AI techniques to gain an understanding of the drivers of model deterioration. We release an open source Python package, doubt, which implements our proposed methods, as well as the code used to reproduce our experiments.

Introduction

Monitoring machine learning models in production is not an easy task. There are situations when the true label of the deployment data is available, and performance metrics can be monitored. But there are cases where it is not, and performance metrics are not so trivial to calculate once the model has been deployed. Model monitoring aims to ensure that a machine learning application in a production environment displays consistent behavior over time.

Being able to explain or remain accountable for the performance or the deterioration of a deployed model is crucial, as a drop in model performance can affect the whole business process (Mougan, Kanellos, and Gottron 2021), potentially having catastrophic consequences111The Zillow case is an example of consequences of model performance degradation in an unsupervised monitoring scenario, see https://edition.cnn.com/2021/11/09/tech/zillow-ibuying-home-zestimate/index.html (Online accessed January 26, 2022).. Once a deployed model has deteriorated, models are retrained using previous and new input data in order to maintain high performance. This process is called continual learning (Diethe et al. 2019) and it can be computationally expensive and put high demands on the software engineering system. Deciding when to retrain machine learning models is paramount in many situations.

Traditional machine learning systems assume that training data has been generated from a stationary source, but data is not static, it evolves. This problem can be seen as a distribution shift, where the data distributions of the training set and the test set differ. Detecting distribution shifts has been a longstanding problem in the machine learning (ML) research community (Shimodaira 2000; Sugiyama, Krauledat, and Müller 2007; Sugiyama and Müller 2005; Tasche 2017; Zadrozny 2004; Stolzenberg and Relles 1997; Heckman 1990; Cortes et al. 2008; Huang et al. 2006; He et al. 2014), as it is one of the main sources of model performance deterioration (Quiñonero-Candela et al. 2008). Furthermore, data scientists in machine learning competitions claim that finding the train/validation split that better resembles the test (evaluation) distribution is paramount to winning a Kaggle competition (Guschin et al. 2018).

However, despite the fact that a shift in data distribution can be a source of model deterioration, the two are not identical. Indeed, if we shift a random noise feature we have caused a change in the data distribution, but we should not expect the performance of a model to decline when evaluated on this shifted dataset. Thus, we emphasize here that our focus is on model deterioration and not distribution shift, despite the correlation between the two.

Established ways of monitoring distribution shift when the real target distribution is not available are based on statistical changes either the input data (Diethe et al. 2019; Rabanser, Günnemann, and Lipton 2019) or on the model output (Garg et al. 2021). These statistical tests correctly detect univariate changes in the distribution but are completely independent of the model performance and can therefore be too sensitive, indicating a change in the covariates but without any degradation in the model performance. This can result in false positives, leading to unnecessary model retraining. It is worth noting that several authors have stated the clear need to identify how non-stationary environments affect the behavior of models (Diethe et al. 2019).

Aside from merely indicating that a model has deteriorated, it can in some circumstances be beneficial to identify the cause of the model deterioration by detecting and explaining the lack of knowledge in the prediction of a model. Such explainability techniques can provide algorithmic transparency to stakeholders and to the ML engineering team (Mougan, Kanellos, and Gottron 2021; Bhatt et al. 2021; Koh and Liang 2017; Ribeiro, Singh, and Guestrin 2016; Sundararajan, Taly, and Yan 2017).

This paper’s primary focus is on non-deep learning models and small to medium-sized tabular datasets, a size of data that is very common in the average industry, where, non-deep learning-based models achieve state-of-the-art results (Grinsztajn, Oyallon, and Varoquaux 2022; Borisov et al. 2021; Elsayed et al. 2021).

Our contributions are the following:

-

1.

We develop a novel method that produces prediction intervals using bootstrapping with theoretical guarantees, which achieves better coverage than previous methods on eight real-life regression datasets from the UCI repository (Dua and Graff 2017).

-

2.

We use this non-parametric uncertainty estimation method to develop a machine learning monitoring system for regression models, which outperforms previous monitoring methods in terms of detecting deterioration of model performance.

-

3.

We use explainable AI techniques to identify the source of model deterioration for both entire distributions as a whole as well as for individual samples, where classical statistical indicators can only determine distribution differences.

-

4.

We release an open source Python package, doubt, which implements our uncertainty estimation method and is compatible with all scikit-learn models (Pedregosa et al. 2011).

Related Work

Model Monitoring

Model monitoring techniques help to detect unwanted changes in the behavior of a machine learning application in a production environment. One of the biggest challenges in model monitoring is distribution shift, which is also one of the main sources of model degradation (Quiñonero-Candela et al. 2008; Diethe et al. 2019).

Diverse types of model monitoring scenarios require different supervision techniques. We can distinguish two main groups: Supervised learning and unsupervised learning. Supervised learning is the appealing one from a monitoring perspective, where performance metrics can easily be tracked. Whilst attractive, these techniques are often unfeasible as they rely either on having ground truth labeled data available or maintaining a hold-out set, which leaves the challenge of how to monitor ML models to the realm of unsupervised learning (Diethe et al. 2019). Popular unsupervised methods that are used in this respect are the Population Stability Index (PSI) and the Kolmogorov-Smirnov test (K-S), all of which measure how much the distribution of the covariates in the new samples differs from the covariate distribution within the training samples. These methods are often limited to real-valued data, low dimensions, and require certain probabilistic assumptions (Diethe et al. 2019; Malinin et al. 2021).

Another approach suggested by Lundberg et al. (2020b) is to monitor the SHAP value contribution of input features over time together with decomposing the loss function across input features in order to identify possible bugs in the pipeline as well as distribution shift. This technique can account for previously unaccounted bugs in the machine learning production pipeline but fails to monitor the model degradation.

Is worth noting that prior work (Garg et al. 2021; Jiang et al. 2021) has focused on monitoring models either on out-of-distribution data or in-distribution data (Neyshabur et al. 2017, 2019). Such a task, even if challenging, does not accurately represent the different types of data a model encounters in the wild. In a production environment, a model can encounter previously seen data (training data), unseen data with the same distribution (test data), and statistically new and unseen data (out-of-distribution data). That is why we focus our work on finding an unsupervised estimator that replicates the behavior of the model performance.

The idea of mixing uncertainty with dataset shift was introduced by Ovadia et al. (2019). Our work differs from theirs, in that they evaluate uncertainty by shifting the distributions of their dataset, where we aim to detect model deterioration under dataset shift using uncertainty estimation. Their work is also focused on deep learning classification problems, while we estimate uncertainty using model agnostic regression techniques. Further, our contribution allows us to pinpoint the features/dimensions that are main causes of the model degradation.

Garg et al. (2021) introduces a monitoring system for classification models, based on imposing thresholds on the softmax values of the model. Our method differs from theirs in that we work with regression models and not classification models, and that our method utilizes external uncertainty estimation methods, rather than relying on the model’s own “confidence” (i.e., the outputted logits and associated softmax values).

Rabanser, Günnemann, and Lipton (2019), presents a comprehensive empirical investigation of dataset shift, examining how dimensionality reduction and two-sample testing might be combined to produce a practical pipeline for detecting distribution shift in a real-life machine learning system. They show that the two-sample-testing-based approach performs best. This serves as a baseline comparison within our models, even if their idea is more focused on binary classification, whereas our works focus on building a regression indicator.

Uncertainty

Uncertainty estimation is being developed at a fast pace. Model averaging (Kumar and Srivastava 2012; Gal and Ghahramani 2016; Lakshminarayanan, Pritzel, and Blundell 2017; Arnez et al. 2020) has emerged as the most common approach to uncertainty estimation. Ensemble and sampling-based uncertainty estimates have been successfully applied to many use cases such as detecting misclassifications (Lakshminarayanan 2021), out-of-distribution inputs (D’Angelo and Henning 2021), adversarial attacks (Carlini and Wagner 2017; Smith and Gal 2018), automatic language assessments (Malinin 2019) and active learning (Kirsch, Van Amersfoort, and Gal 2019). In our work, we apply uncertainty to detect and explain model performance for seen data (train), unseen and identically distributed data (test), and statistically new and unseen data (out-of-distribution).

Kumar and Srivastava (2012) introduced a non-parametric method to compute prediction intervals for any ML model using a bootstrap estimate, with theoretical guarantees. Our work is an extension of their work, where we take into account the model’s variance in the construction of the prediction intervals. The result, as we will see in the experiments section, is that such intervals have better coverage in such high-variance scenarios.

Barber et al. (2021) recently introduced a new non-parametric method of creating prediction intervals, using the Jackknife+. Our method differs from theirs in that we are using general bootstrapped samples for our estimates, rather than leave-one-out estimates. In the experimental, we will see that the two methods perform similarly, but that our method is again more accurate in a high-variance scenario.

Methodology

Evaluation of deterioration detection systems

The problem we are tackling in this paper is evaluating and accounting for model predictive performance deterioration. To do this, we simulate a distribution shift scenario in which we have access to the true labels, which we can use to measure the model deterioration and thus evaluate the monitoring system. A naive simulation in which we simply manually shift a chosen feature of a dataset would not be representative, as the associated true labels could have changed if such a shift happened ”in the wild”.

Therefore, we propose the following alternative approach. Starting from a real-life dataset and a numerical feature of , we sort the data samples of by the value of , and split the sorted in three equally sized sections: . The model is then fitted to the middle section () and evaluated on all of . The goal of the monitoring system is to input the model, the labeled data segment and a sample of unlabelled data , and output a “monitoring value” which behaves like the model’s performance on . Such a prediction will thus have to take into account the training performance, generalization performance as well as the out-of-distribution performance of the model.

In the experimental section, we compare our monitoring technique to several other such systems. To enable comparison between the different monitoring systems, we standardize all monitoring values as well as the performance metrics of the model. From these standardized values, we can now directly measure the goodness-of-fit of the model monitoring system by computing the absolute difference between its (standardized) monitoring values and the (standardized) ground truth model performance metrics. Our chosen evaluation method is very similar to the one used by Garg et al. (2021). They focus on classification models and their systems output estimates of the model’s accuracy on the dataset. They evaluate these systems by computing the absolute difference between the system’s accuracy estimate and the actual accuracy that the model achieves on the dataset.

As we are working with regression models in this paper, we will only operate with a single model performance metric: mean squared error. We will introduce our monitoring system, which is based on an uncertainty measure, and will compare our monitoring system against statistical tests based on input data or prediction data. In that section, we will also compare our uncertainty estimation method to current state-of-art uncertainty estimation methods.

Uncertainty estimation

In order to estimate uncertainty in a general way for all machine learning models, we use a non-parametric regression technique, which is an improvement of the technique introduced by (Kumar and Srivastava 2012). This method aims at determining prediction intervals for outputs of general non-parametric regression models using bootstrap methods.

Setting to be the dimension of the feature space, we assume that the true model is of the form , where is a deterministic and continuously differentiable function, and the observation noise is a uniform random field such that are iid for any , have zero mean and finite variance. We will assume that we have a data sample of size , as well as a convergent estimator of , meaning the following:

Definition 1

Let be a function for every . We then say that is a convergent estimator of a function if:

-

1.

is deterministic and continuous, for all .

-

2.

There is a function such that converges pointwise to as .

We define an associated bias function . Note that in Kumar and Srivastava (2012) they assumed that for , effectively meaning that the candidate model would be able to perfectly model the underlying distribution given enough data. It turns out that their method does not require this assumption, as we will see below. Aside from removing this assumption, the primary difference between our approach and Kumar and Srivastava (2012) is that our approach extends the latter by maintaining good coverage in a high-variance situation, as we will also see below. We start by rewriting the equation for the true model as follows:

| (1) | ||||

| (2) |

where is the model variance noise. Note that

| (3) |

To produce correct prediction intervals we thus need to estimate the distribution of the observation noise, bias and model variance noise.

Estimating Model Variance Noise

To estimate the model variance noise term we adapt the technique in Kumar and Srivastava (2012) to our scenario, using a bootstrap estimate. Concretely, we bootstrap our dataset times, fitting our model on each of the bootstrapped samples and generating bootstrapped estimates for every . Centering the bootstrapped predictions as , we have that

| (4) | ||||

| (5) | ||||

| (6) |

as , giving us our estimate of the model variance noise.

Estimating Bias and Observation Noise

We next have to estimate the bias and the observation noise . By rewriting (1) we get that that

| (7) |

so since we already have an estimate for , it remains to estimate the residual . In Kumar and Srivastava (2012) this was estimated purely using the training residuals without using any bootstrapping, whereas our approach will estimate the expected value of this residual via a bootstrap estimate, by using bootstrapped validation residuals , where is not in the ’th bootstrap sample . Concretely, we have that

| (8) | |||

| (9) |

as . An initial estimate is thus

| (10) | ||||

| (11) |

Denote (11) by . The problem with this approach is that the resulting prediction intervals arising from these validation errors are going to be too wide, as the bootstrap samples only contain on average 63.2% of the samples in the original dataset (Friedman et al. 2001), causing the model to have artificially large validation residuals. To fix this, we follow the approach in Friedman et al. (2001) and use the 0.632+ bootstrap estimate instead, defined as follows. We start by defining the no-information error rate

| (12) |

corresponding to the mean-squared error if the inputs and outputs were independent. Next, define the associated training residuals as:

| (13) |

Combining these two, we set the relative overfitting rate to be:

| (14) |

This gives us a convenient number between and , denoting how much our model is overfitting the dataset. From this, we define the validation weight as:

| (15) |

which denotes how much we should weigh the validation error over the training error. In case of no overfitting, we get that and this reduces to the standard bootstrap estimate (Friedman et al. 2001), whereas in case of severe overfitting the weight becomes and thus only prioritizes the validation error.

Our final estimate of is thus

| (16) |

where

Note that this estimate is only an aggregate and is not specific to any specific value of , as opposed to the model variance estimate in equation (4).

Prediction Interval Construction

Calculating the estimate of the prediction interval is then a matter of joining the results from the section of model variance noise and bias observation noise, in the same way as in Kumar and Srivastava (2012). As the estimate of does not depend on any new sample, we can pre-compute this in advance by bootstrapping samples , fit our model to each and calculate the using Equation (16). Now, given a new data point and , we can estimate an prediction interval around as follows. We again bootstrap samples , fit our model to each and calculate the values. Next, we form the set , and our interval is then , where

| (17) | |||

| (18) |

with being the ’th quantile of .

Detecting the source of uncertainty/model deterioration

Using uncertainty as a method to monitor the performance of an ML model does not provide any information on what features are the cause of the model degradation, only a goodness-of-fit to the model performance. We propose to solve this issue with the use of Shapley values.

We start by fitting a model to the training data, . We next shift the test data by five standard deviations (call the shifted data ) and compute uncertainty estimates of on . We next fit a second model on to predict the uncertainty estimate , and compute the associated Shapley values (Lundberg et al. 2020b) of . These Shapley values thus signify which features are the ones contributing the most to the uncertainty values. With the correlation between uncertainty values and model deterioration that we hope to conclude from the experiment described in the experimental section, this thus also provides us with a plausible cause of the model deterioration, if deterioration has taken place. Particularly, this methodology can be extended to large-scale datasets and deep learning-based models.

Experiments

Our experiments have been organized into three main groups: Firstly, we compare our non-parametric bootstrapped estimation method with the previous state-of-the-art, Kumar and Srivastava (2012) and Barber et al. (2021). Secondly, we assess the performance of our proposed uncertainty method for monitoring the performance of a machine learning model. And then, we evaluate the usability of the explainable uncertainty for identifying the features that are driving model degradation in local and global scenarios. In the main body of the paper, we present the results over several real-world datasets in the appendix we provide the experiments on synthetic datasets that exhibits, non-linear and linear behavior.

Uncertainty method comparison

To demonstrate the accuracy of our prediction intervals introduced in the uncertainty estimation section, we compare the coverage of the intervals with the NASA method from Kumar and Srivastava (2012) on eight regression datasets from the UCI repository (Dua and Graff 2017). The statistics of these datasets can be seen in Table 1.

| Dataset | # Samples | # Features |

|---|---|---|

| Airfoil Self-Noise | 1,503 | 5 |

| Bike Sharing | 17,379 | 16 |

| Concrete Compressive Strength | 1,030 | 8 |

| QSAR Fish Toxicity | 908 | 6 |

| Forest Fires | 517 | 12 |

| Parkinsons | 5,875 | 22 |

| Power Plant | 9,568 | 4 |

| Protein | 45,730 | 9 |

We split each of the eight datasets into a 90/10 train/test split, uniformly at random. Next, we fit a linear regression, a decision tree, and a gradient boosting decision tree on the training split. We chose these three models to have an example of a model with large bias (the linear regression model), a model with large variance (the decision tree model), and an intermediate model that achieves state-of-the-art performance in many tasks, the gradient boosting model. We will use the xgboost (Chen and Guestrin 2016) implementation of the gradient boosting model. After fitting the three models we compute -prediction intervals for , using our “Doubt” prediction intervals, the “NASA” prediction intervals from (Kumar and Srivastava 2012) as well as the “MAPIE” prediction intervals from (Barber et al. 2021), the latter implemented with the MAPIE package222https://github.com/scikit-learn-contrib/MAPIE. We can then compare the coverage of the three methods on the eight test sets.

As the goal of an prediction interval is to have a coverage of , we can measure the performance of a prediction interval system by reporting the absolute difference between the actual coverage of the interval and this ideal coverage . In Table 2 we report the mean and standard deviations of these absolute differences, for each of the three model architectures. We have performed pairwise two-tailed paired t-tests on all absolute differences, and the best-performing prediction interval methods are marked in bold for each model architecture.

We see (cf. Table 2) that there is no significant difference between the three methods in the high bias case with the linear regression model. In the case of the XGBoost model, a model with higher variance, both the MAPIE and Doubt methods outperform the NASA method, but there is no significant difference between the MAPIE method and the Doubt method in this case. In the high-variance scenario with the decision tree, however, the Doubt intervals achieve significantly better coverage than both of the other two methods.

| Model | Linear Regression | XGBoost | Decision Tree |

|---|---|---|---|

| NASA | |||

| MAPIE | |||

| Doubt |

Evaluating model deterioration

The scenario we are addressing is characterized by regression data sets that have statistically seen data (train data), iid statistically unseen data (test data), and out-of-distribution data. Following the open data for reproducible research guidelines described in Arnold et al. (2019) and for measuring the performance of the proposed methods, we have used eight open-source datasets (cf. Table 1) for an empirical comparison coming from the UCI repository (Dua and Graff 2017). As described in the methodology, in order to benchmark our algorithm we, for each feature in each dataset , sort according to and split into three equally sized sections . We then train the model on and test the performance of all of . In this way we obtain a mixture of train, test, and out-of-distribution data, allowing us to evaluate our monitoring techniques in all three scenarios.

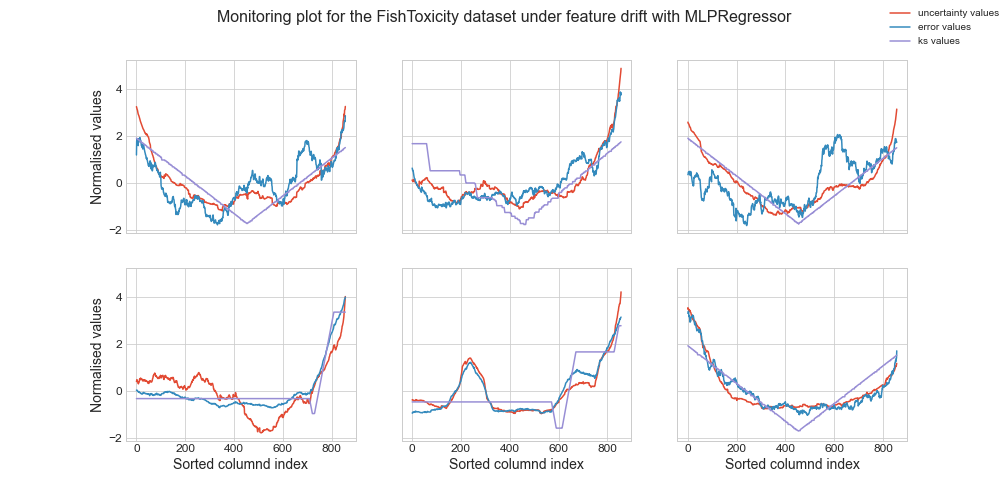

In evaluating a monitoring system we need to make a concrete choice of the sampling method to get the unlabelled data . We are here using a rolling window of fifty samples, which has the added benefit of giving insight into the performance of the monitoring system on each of the three sections , and (cf. Figure 1).

We compare our monitoring system using the uncertainty estimation method against: two classical statistical methods on input data: the Kolmogorov-Smirnov test statistic (K-S) and the Population-Stability Index (PSI) (Diethe et al. 2019), a Kolmogorov-Smirnov statistical test on the predictions between train and test (Garg et al. 2021) that we denominate prediction shift and the previous state-of-the-art uncertainty estimate MAPIE. We evaluate the monitoring systems on a variety of model architectures: generalized linear models, tree-based models as well as neural networks.

The average performance across all datasets can be found in Table 3.333See the appendix for a more detailed table. From these we can see that our methods outperform K-S and PSI in all cases except for the Random Forest case, where our method is still on par with the best method, in that case, K-S. We have included a table with each dataset and all the estimators (cf. Table 6 in the appendix), where it can be seen that both K-S and PSI easily identify a shift in the distribution but fail to detect when the model performance degrades, giving too many false positives.

| Method | Linear Regression | Poisson | Decision Tree | Random Forest | Gradient Boosting | MLP |

|---|---|---|---|---|---|---|

| PSI | ||||||

| K-S | ||||||

| Prediction Shift | ||||||

| MAPIE | ||||||

| Doubt |

Detecting the source of uncertainty

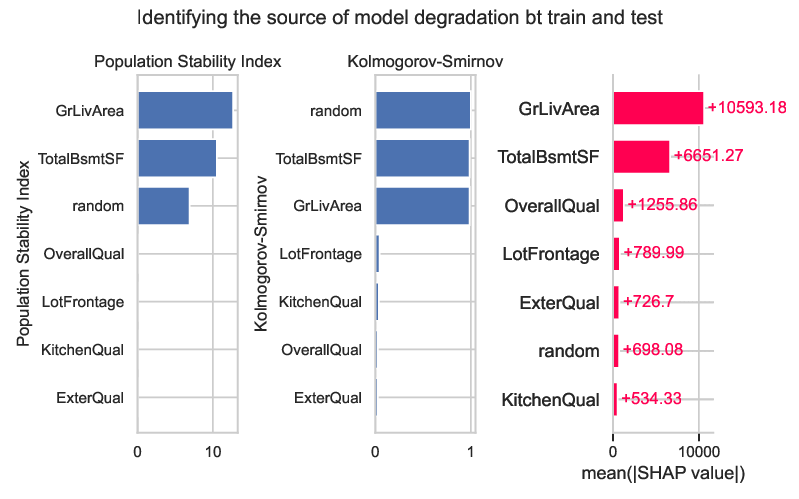

For this experiment, we make use of two datasets: the synthetic one (on the Appendix) and the popular and intuitive House Prices regression dataset444https://www.kaggle.com/c/house-prices-advanced-regression-techniques, whose goal is to predict the selling price of a given property. We select two of the features that are the most correlated with the target, GrLivArea and TotalBsmtSF, being the size of the living and base areas in square feet, respectively. We also create a new feature of random noise, to have an example of a feature with minimum correlation with the target. A model deterioration system should therefore highlight the GrLivArea and TotalBsmtSF features, and not highlight the random features.

Concretely, we compute an estimation of the Shapley values using TreeSHAP, which is an efficient estimation approach values for tree-based models (Lundberg et al. 2020b), that allows for this second model to identify the features that are the source of the uncertainty, and thus also provide an indicator for what features might be causing the model deterioration.

We fitted an MLP on the training dataset, which achieved a value of on the validation set. We then shifted all three features by five standard deviations and trained a gradient boosting model on the uncertainty values of the MLP on the validation set, which achieves a good fit (an value of on the hold-out set of the validation). We then compare the SHAP values of the gradient boosting model with the PSI and K-S statistics for the individual features.

In Figure 2, classical statistics and SHAP values to detect the source of the model deterioration are compared. We see that the PSI and K-S value correctly capture the shift in each of the three features (including the random noise). On the other hand, our SHAP method highlights the two substantial features (GrLivArea and TotalBsmtSF) and correctly does not assign a large value to the random feature, despite the distribution shift.

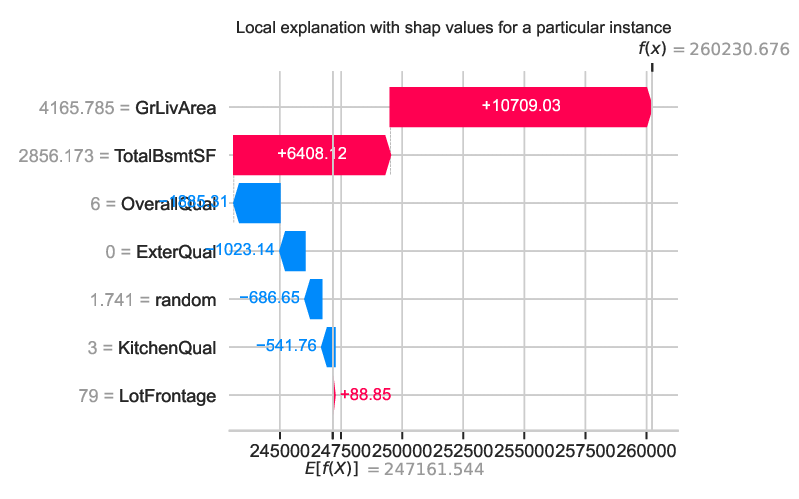

Figure 3 shows features contributing to pushing the model output from the base value to the model output. Features pushing the uncertainty prediction higher are shown in red, and those pushing the uncertainty prediction lower are in blue (Lundberg et al. 2018, 2020a; Lundberg and Lee 2017). From these values, we can, at a local level, also identify the two features (GrLivArea and TotalBsmtSF) causing the model deterioration in this case.

Conclusion

In this work, we have provided methods and experiments to monitor and identify machine learning model deterioration via non-parametric bootstrapped uncertainty estimation methods, and use explainability techniques to explain the source of the model deterioration.

Our monitoring system is based on a novel uncertainty estimation method, which produces prediction intervals with theoretical guarantees and which achieves better coverage than the current state-of-the-art. The resulting monitoring system was shown to more accurately detect model deterioration than methods using classical statistics. Finally, we used SHAP values in conjunction with these uncertainty estimates to identify the features that are driving the model deterioration at both a global and local level and qualitatively showed that these more accurately detect the source of the model deterioration compared to classical statistical methods.

Limitations:We emphasize here that due to computationally limitations, we have only benchmarked on datasets of relatively small to medium size (cf. Table 1), and further work needs to be done to see if these results are also valid for datasets of significantly larger size. This work also focused on tabular data and non-deep learning models.

Reproducibility Statement

To ensure reproducibility of our results, we make the data, data preparation routines, code repositories, and methods publicly available555https://github.com/cmougan/MonitoringUncertainty. Our novel uncertainty methods are included in the open-source Python package doubt666https://github.com/saattrupdan/doubt.. We describe the system requirements and software dependencies of our experiments. Our experiments were run on an 8 vCPU server with 60 GB RAM.

Acknowledgements

This work has received funding by the European Union’s Horizon 2020 research and innovation programme under the Marie Skłodowska-Curie Actions (grant agreement number 860630) for the project : ”NoBIAS - Artificial Intelligence without Bias”. Furthermore, this work reflects only the authors’ view and the European Research Executive Agency (REA) is not responsible for any use that may be made of the information it contains.

References

- Arnez et al. (2020) Arnez, F.; Espinoza, H.; Radermacher, A.; and Terrier, F. 2020. A Comparison of Uncertainty Estimation Approaches in Deep Learning Components for Autonomous Vehicle Applications. In Espinoza, H.; McDermid, J. A.; Huang, X.; Castillo-Effen, M.; Chen, X. C.; Hernández-Orallo, J.; hÉigeartaigh, S. Ó.; and Mallah, R., eds., Proceedings of the Workshop on Artificial Intelligence Safety 2020 co-located with the 29th International Joint Conference on Artificial Intelligence and the 17th Pacific Rim International Conference on Artificial Intelligence (IJCAI-PRICAI 2020), Yokohama, Japan, January, 2021, volume 2640 of CEUR Workshop Proceedings. CEUR-WS.org.

- Arnold et al. (2019) Arnold, B.; Bowler, L.; Gibson, S.; Herterich, P.; Higman, R.; Krystalli, A.; Morley, A.; O’Reilly, M.; Whitaker, K.; et al. 2019. The turing Way: a handbook for reproducible data science. Zenodo.

- Barber et al. (2021) Barber, R. F.; Candes, E. J.; Ramdas, A.; and Tibshirani, R. J. 2021. Predictive inference with the jackknife+. The Annals of Statistics, 49(1): 486–507.

- Bhatt et al. (2021) Bhatt, U.; Antorán, J.; Zhang, Y.; Liao, Q. V.; Sattigeri, P.; Fogliato, R.; Melançon, G.; Krishnan, R.; Stanley, J.; Tickoo, O.; et al. 2021. Uncertainty as a form of transparency: Measuring, communicating, and using uncertainty. In Proceedings of the 2021 AAAI/ACM Conference on AI, Ethics, and Society, 401–413.

- Borisov et al. (2021) Borisov, V.; Leemann, T.; Seßler, K.; Haug, J.; Pawelczyk, M.; and Kasneci, G. 2021. Deep Neural Networks and Tabular Data: A Survey. CoRR, abs/2110.01889.

- Carlini and Wagner (2017) Carlini, N.; and Wagner, D. 2017. Adversarial examples are not easily detected: Bypassing ten detection methods. In Proceedings of the 10th ACM workshop on artificial intelligence and security, 3–14.

- Chen et al. (2020) Chen, H.; Janizek, J. D.; Lundberg, S. M.; and Lee, S. 2020. True to the Model or True to the Data? CoRR, abs/2006.16234.

- Chen and Guestrin (2016) Chen, T.; and Guestrin, C. 2016. Xgboost: A scalable tree boosting system. In Proceedings of the 22nd acm sigkdd international conference on knowledge discovery and data mining, 785–794.

- Cortes et al. (2008) Cortes, C.; Mohri, M.; Riley, M.; and Rostamizadeh, A. 2008. Sample selection bias correction theory. In International conference on algorithmic learning theory, 38–53. Springer.

- D’Angelo and Henning (2021) D’Angelo, F.; and Henning, C. 2021. Uncertainty-based out-of-distribution detection requires suitable function space priors. arXiv preprint arXiv:2110.06020.

- Diethe et al. (2019) Diethe, T.; Borchert, T.; Thereska, E.; Balle, B.; and Lawrence, N. 2019. Continual Learning in Practice. stat, 1050: 18.

- Dua and Graff (2017) Dua, D.; and Graff, C. 2017. UCI Machine Learning Repository. University of California, Irvine, School of Information and Computer Sciences, http://archive.ics.uci.edu/ml.

- Elsayed et al. (2021) Elsayed, S.; Thyssens, D.; Rashed, A.; Schmidt-Thieme, L.; and Jomaa, H. S. 2021. Do We Really Need Deep Learning Models for Time Series Forecasting? CoRR, abs/2101.02118.

- Friedman et al. (2001) Friedman, J.; Hastie, T.; Tibshirani, R.; et al. 2001. The elements of statistical learning, volume 1.10. Springer series in statistics New York.

- Gal and Ghahramani (2016) Gal, Y.; and Ghahramani, Z. 2016. Dropout as a bayesian approximation: Representing model uncertainty in deep learning. In international conference on machine learning, 1050–1059. PMLR.

- Garg et al. (2021) Garg, S.; Balakrishnan, S.; Lipton, Z. C.; Neyshabur, B.; and Sedghi, H. 2021. Leveraging Unlabeled Data to Predict Out-of-Distribution Performance. In NeurIPS 2021 Workshop on Distribution Shifts: Connecting Methods and Applications.

- Grinsztajn, Oyallon, and Varoquaux (2022) Grinsztajn, L.; Oyallon, E.; and Varoquaux, G. 2022. Why do tree-based models still outperform deep learning on tabular data? Working paper or preprint.

- Guschin et al. (2018) Guschin, A.; Ulyanov, D.; Trofimov, M.; Altukhov, D.; and Michaidilis, M. 2018. How to Win a Data Science Competition: Learn from Top Kagglers - National Research University Higher School of Economics. https://www.coursera.org/lecture/competitive-data-science/categorical-and-ordinal-features-qu1TF. Accessed 02/11/20.

- He et al. (2014) He, X.; Pan, J.; Jin, O.; Xu, T.; Liu, B.; Xu, T.; Shi, Y.; Atallah, A.; Herbrich, R.; Bowers, S.; et al. 2014. Practical lessons from predicting clicks on ads at facebook. In Proceedings of the Eighth International Workshop on Data Mining for Online Advertising, 1–9.

- Heckman (1990) Heckman, J. 1990. Varieties of selection bias. The American Economic Review, 80(2): 313–318.

- Huang et al. (2006) Huang, J.; Gretton, A.; Borgwardt, K.; Schölkopf, B.; and Smola, A. 2006. Correcting sample selection bias by unlabeled data. Advances in neural information processing systems, 19: 601–608.

- Jiang et al. (2021) Jiang, Y.; Nagarajan, V.; Baek, C.; and Kolter, J. Z. 2021. Assessing generalization of sgd via disagreement. arXiv preprint arXiv:2106.13799.

- Kirsch, Van Amersfoort, and Gal (2019) Kirsch, A.; Van Amersfoort, J.; and Gal, Y. 2019. Batchbald: Efficient and diverse batch acquisition for deep bayesian active learning. Advances in neural information processing systems, 32: 7026–7037.

- Koh and Liang (2017) Koh, P. W.; and Liang, P. 2017. Understanding black-box predictions via influence functions. In International Conference on Machine Learning, 1885–1894. PMLR.

- Kumar and Srivastava (2012) Kumar, S.; and Srivastava, A. 2012. Bootstrap prediction intervals in non-parametric regression with applications to anomaly detection. In Proc. 18th ACM SIGKDD Conf. Knowl. Discovery Data Mining.

- Lakshminarayanan (2021) Lakshminarayanan, B. 2021. Uncertainty and Out-of-Distribution Robustness in Deep Learning.

- Lakshminarayanan, Pritzel, and Blundell (2017) Lakshminarayanan, B.; Pritzel, A.; and Blundell, C. 2017. Simple and Scalable Predictive Uncertainty Estimation using Deep Ensembles. Advances in Neural Information Processing Systems, 30.

- Lundberg et al. (2020a) Lundberg, S. M.; Erion, G.; Chen, H.; DeGrave, A.; Prutkin, J. M.; Nair, B.; Katz, R.; Himmelfarb, J.; Bansal, N.; and Lee, S.-I. 2020a. From local explanations to global understanding with explainable AI for trees. Nature machine intelligence, 2(1): 56–67.

- Lundberg et al. (2020b) Lundberg, S. M.; Erion, G. G.; Chen, H.; DeGrave, A. J.; Prutkin, J. M.; Nair, B.; Katz, R.; Himmelfarb, J.; Bansal, N.; and Lee, S. 2020b. From local explanations to global understanding with explainable AI for trees. Nat. Mach. Intell., 2(1): 56–67.

- Lundberg and Lee (2017) Lundberg, S. M.; and Lee, S.-I. 2017. A unified approach to interpreting model predictions. In Proceedings of the 31st international conference on neural information processing systems, 4768–4777.

- Lundberg et al. (2018) Lundberg, S. M.; Nair, B.; Vavilala, M. S.; Horibe, M.; Eisses, M. J.; Adams, T.; Liston, D. E.; Low, D. K.-W.; Newman, S.-F.; Kim, J.; et al. 2018. Explainable machine-learning predictions for the prevention of hypoxaemia during surgery. Nature biomedical engineering, 2(10): 749–760.

- Malinin (2019) Malinin, A. 2019. Uncertainty estimation in deep learning with application to spoken language assessment. Ph.D. thesis, University of Cambridge.

- Malinin et al. (2021) Malinin, A.; Band, N.; Gal, Y.; Gales, M.; Ganshin, A.; Chesnokov, G.; Noskov, A.; Ploskonosov, A.; Prokhorenkova, L.; Provilkov, I.; et al. 2021. Shifts: A Dataset of Real Distributional Shift Across Multiple Large-Scale Tasks. In Thirty-fifth Conference on Neural Information Processing Systems Datasets and Benchmarks Track (Round 2).

- Mougan, Kanellos, and Gottron (2021) Mougan, C.; Kanellos, G.; and Gottron, T. 2021. Desiderata for Explainable AI in Statistical Production Systems of the European Central Bank. In Machine Learning and Principles and Practice of Knowledge Discovery in Databases - International Workshops of ECML PKDD 2021, Virtual Event, September 13-17, 2021, Proceedings, Part I, volume 1524 of Communications in Computer and Information Science, 575–590. Springer.

- Neyshabur et al. (2017) Neyshabur, B.; Bhojanapalli, S.; Mcallester, D.; and Srebro, N. 2017. Exploring Generalization in Deep Learning. Advances in Neural Information Processing Systems, 30: 5947–5956.

- Neyshabur et al. (2019) Neyshabur, B.; Li, Z.; Bhojanapalli, S.; LeCun, Y.; and Srebro, N. 2019. Towards Understanding the Role of Over-Parametrization in Generalization of Neural Networks. In International Conference on Learning Representations (ICLR).

- Ovadia et al. (2019) Ovadia, Y.; Fertig, E.; Ren, J.; Nado, Z.; Sculley, D.; Nowozin, S.; Dillon, J. V.; Lakshminarayanan, B.; and Snoek, J. 2019. Can You Trust Your Model’s Uncertainty? Evaluating Predictive Uncertainty Under Dataset Shift. stat, 1050: 17.

- Pedregosa et al. (2011) Pedregosa, F.; Varoquaux, G.; Gramfort, A.; Michel, V.; Thirion, B.; Grisel, O.; Blondel, M.; Prettenhofer, P.; Weiss, R.; Dubourg, V.; et al. 2011. Scikit-learn: Machine learning in Python. the Journal of machine Learning research, 12: 2825–2830.

- Quiñonero-Candela et al. (2008) Quiñonero-Candela, J.; Sugiyama, M.; Schwaighofer, A.; and Lawrence, N. D. 2008. Dataset shift in machine learning. Mit Press.

- Rabanser, Günnemann, and Lipton (2019) Rabanser, S.; Günnemann, S.; and Lipton, Z. C. 2019. Failing Loudly: An Empirical Study of Methods for Detecting Dataset Shift. In Wallach, H. M.; Larochelle, H.; Beygelzimer, A.; d’Alché-Buc, F.; Fox, E. B.; and Garnett, R., eds., Advances in Neural Information Processing Systems 32: Annual Conference on Neural Information Processing Systems 2019, NeurIPS 2019, December 8-14, 2019, Vancouver, BC, Canada, 1394–1406.

- Ribeiro, Singh, and Guestrin (2016) Ribeiro, M. T.; Singh, S.; and Guestrin, C. 2016. ” Why should i trust you?” Explaining the predictions of any classifier. In Proceedings of the 22nd ACM SIGKDD international conference on knowledge discovery and data mining, 1135–1144.

- Shimodaira (2000) Shimodaira, H. 2000. Improving predictive inference under covariate shift by weighting the log-likelihood function. Journal of statistical planning and inference, 90(2): 227–244.

- Smith and Gal (2018) Smith, L.; and Gal, Y. 2018. Understanding Measures of Uncertainty for Adversarial Example Detection. In Globerson, A.; and Silva, R., eds., Proceedings of the Thirty-Fourth Conference on Uncertainty in Artificial Intelligence, UAI 2018, Monterey, California, USA, August 6-10, 2018, 560–569. AUAI Press.

- Stolzenberg and Relles (1997) Stolzenberg, R. M.; and Relles, D. A. 1997. Tools for intuition about sample selection bias and its correction. American sociological review, 494–507.

- Sugiyama, Krauledat, and Müller (2007) Sugiyama, M.; Krauledat, M.; and Müller, K.-R. 2007. Covariate shift adaptation by importance weighted cross validation. Journal of Machine Learning Research, 8(5).

- Sugiyama and Müller (2005) Sugiyama, M.; and Müller, K.-R. 2005. Input-dependent estimation of generalization error under covariate shift. .

- Sundararajan, Taly, and Yan (2017) Sundararajan, M.; Taly, A.; and Yan, Q. 2017. Axiomatic attribution for deep networks. In International Conference on Machine Learning, 3319–3328. PMLR.

- Tasche (2017) Tasche, D. 2017. Fisher consistency for prior probability shift. The Journal of Machine Learning Research, 18(1): 3338–3369.

- Zadrozny (2004) Zadrozny, B. 2004. Learning and evaluating classifiers under sample selection bias. In Proceedings of the twenty-first international conference on Machine learning, 114.

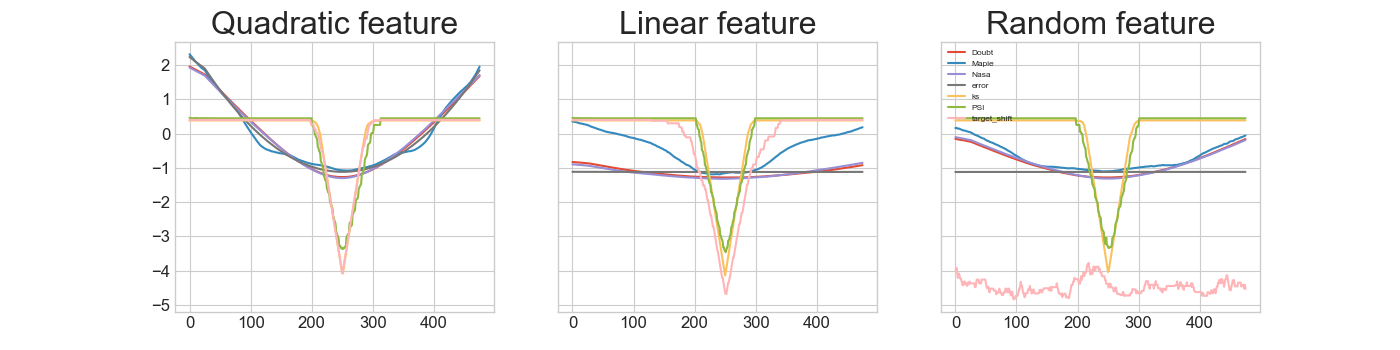

Synthetic data experiments

In this section we apply our model monitoring method to synthetic data to demonstrate main differences between our approach, methods from classical statistics and other model agnostic uncertainty approaches.

We sample data from a three-variate normal distribution with being an identity matrix of order 3. We construct the target variable as , with being random noise. We thus have a non-linear feature , a linear feature and a feature which is not used, all of them being independent among each other. We draw random samples for both training and test data, yielding the training set and the test set and train a linear model .

Evaluating model deterioration

In this experiment we aim to compare indicators of model deterioration by replacing the value of each feature, , with a continuous vector with evenly spaced numbers over a specified range

| Notation | Meaning |

|---|---|

| True label/model. | |

| Dimension of the feature space. | |

| Deterministic component of . | |

| Observation noise component of . | |

| Our data sample. | |

| Size of . | |

| Finite sample estimate of . | |

| The bias function. | |

| Model variance noise. | |

| Number of bootstrap samples. | |

| The index of a particular bootstrap sample. | |

| Bootstrap estimate of . | |

| Centered bootstrap estimate of . | |

| Expected value of . | |

| Distribution function (CDF) of . | |

| The ’th quantile of . |

| Doubt | NASA | MAPIE | KS | PSI | Prediction Shift | |

|---|---|---|---|---|---|---|

| Quadratic feature | 0.09 | 0.11 | 0.09 | 0.96 | 0.95 | 0.94 |

| Linear feature | 0.11 | 0.12 | 0.70 | 0.35 | 1.39 | 1.46 |

| Random feature | 0.34 | 0.35 | 0.42 | 1.39 | 1.46 | 5.58 |

| Mean | 0.18 | 0.20 | 0.40 | 1.24 | 1.29 | 2.69 |

In Figure 5 and Table 5 we can see what is the impact of the synthetic distribution shift is in terms of model mean squared error. We see that our uncertainty method follows a better goodness-of-fit than both the Kolmogorov-Smirnov test and the Population Stability Index on the input data and and target data. The latter two methods have identical values for the linear and random features since they are independent of the target values.

Detecting the source of uncertainty/model deterioration

For this example, we simulate out-of-distribution data by shifting by 10; i.e., for . We train a linear regression model on and use Doubt to get uncertainty estimates on both and . We then train another linear model on to predict . The coefficients of are . Since the features are independent and we are dealing with linear regression, the interventional conditional expectation Shapley values can be computed as (Chen et al. 2020), where is the mean of the training data . So for the data point , the Shapley values are , where the most relevant shifted feature in the model is the one that receives the highest Shapley value. In this experiment with synthetic data, statistical testing on the input data would have flagged the three feature distributions as equally shifted. With our proposed method, we can identify the more meaningful features towards identifying the source of model predictive performance deterioration. It is worth noting that this explainable AI uncertainty approach can be used with other uncertainty estimation techniques.

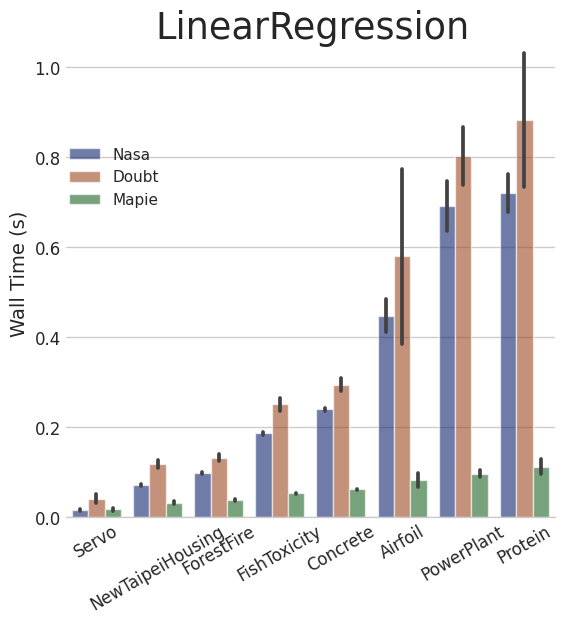

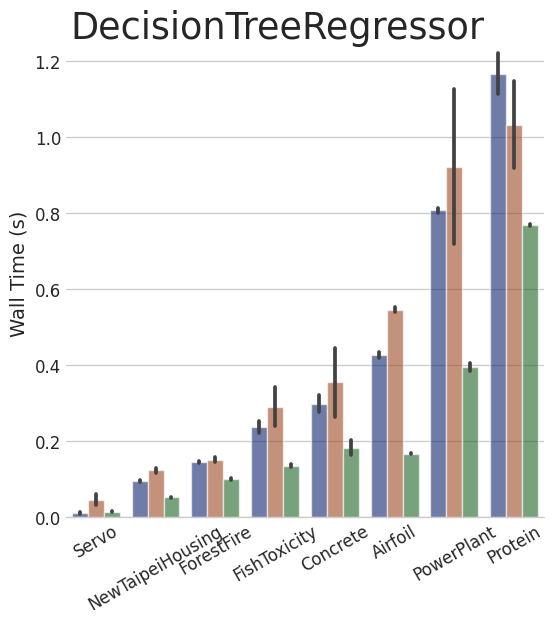

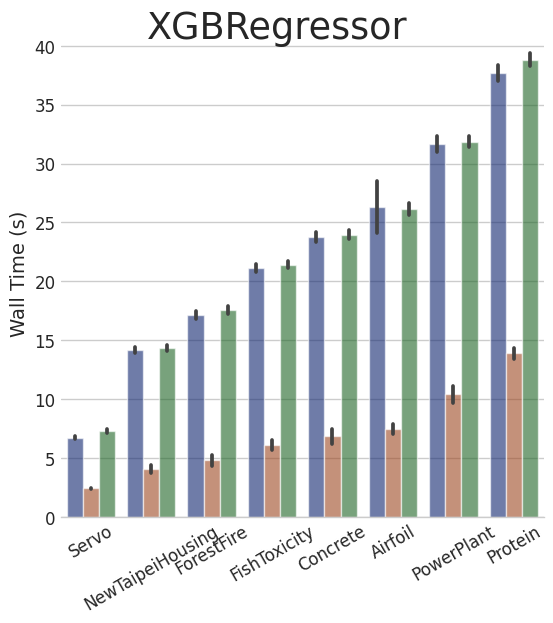

Computational performance comparison

In this section we compare the wall clock time of the NASA method (Kumar and Srivastava 2012), MAPIE (Barber et al. 2021) and Doubt with three estimators: linear regression, decision tree and gradient boosting decision tree, over the range of dataset previously used. We set the number of model bootstraps in the Doubt method to be equal to the number of cross-validation splits in the MAPIE method; namely, the square root of the total number of samples in the dataset. The experiment are performed on a virtual machine with 8 vCPUs and 60 GB RAM.

See the results in Figure 6. We see here that the MAPIE approach is significantly faster than the NASA and Doubt methods in the cases where the model used is a linear regression model or a decision tree. However, interestingly, in the case where the model is an XGBoost model, the Doubt method is significantly faster than the other two.

| Airfoil | Concrete | ForestFire | Parkinsons | PowerPlant | Protein | Bike | FishToxicity | Mean | Std | ||

|---|---|---|---|---|---|---|---|---|---|---|---|

| Linear Regression | Uncertainty | 0.67 | 0.59 | 0.6 | 0.6 | 1.0 | 0.72 | 0.86 | 0.64 | 0.71 | 0.14 |

| MAPIE | 0.72 | 0.79 | 0.71 | 0.62 | 0.85 | 0.74 | 0.79 | 0.94 | 0.77 | 0.09 | |

| K-S | 0.78 | 0.67 | 0.81 | 0.92 | 0.8 | 0.99 | 0.85 | 0.71 | 0.81 | 0.10 | |

| PSI | 1.02 | 0.9 | 0.78 | 0.83 | 0.93 | 0.79 | 0.91 | 0.81 | 0.87 | 0.08 | |

| Target | 0.94 | 0.68 | 0.7 | 0.84 | 0.8 | 0.97 | 0.97 | 1.0 | 0.86 | 0.12 | |

| Poisson Regressor | Uncertainty | 0.81 | 0.49 | 0.93 | 0.82 | 0.97 | 0.83 | 0.79 | 0.71 | 0.79 | 0.14 |

| MAPIE | 0.84 | 0.55 | 0.89 | 0.86 | 0.87 | 0.91 | 0.61 | 1.1 | 0.82 | 0.17 | |

| K-S | 0.83 | 0.68 | 1.08 | 1.08 | 0.8 | 1.16 | 1.16 | 0.79 | 0.94 | 0.19 | |

| PSI | 1.01 | 0.9 | 1.04 | 1.04 | 0.94 | 0.85 | 0.85 | 0.86 | 0.93 | 0.08 | |

| Target | 1.02 | 0.75 | 1.15 | 1.15 | 0.79 | 1.1 | 1.1 | 0.95 | 1.00 | 0.15 | |

| Decision Tree (20) | Uncertainty | 0.48 | 0.44 | 0.74 | 0.51 | 0.45 | 0.44 | 0.46 | 0.47 | 0.49 | 0.10 |

| MAPIE | 0.59 | 0.52 | 0.96 | 0.61 | 0.61 | 0.51 | 0.49 | 0.45 | 0.59 | 0.15 | |

| K-S | 0.49 | 0.56 | 0.66 | 0.49 | 0.3 | 0.49 | 0.68 | 0.5 | 0.52 | 0.11 | |

| PSI | 1.14 | 1.08 | 1.02 | 0.9 | 0.92 | 0.9 | 0.86 | 0.95 | 0.97 | 0.09 | |

| Target | 0.96 | 0.77 | 0.81 | 0.9 | 0.64 | 0.54 | 0.94 | 0.79 | 0.79 | 0.14 | |

| Random Forest Regressor | Uncertainty | 0.57 | 0.577 | 0.93 | 0.5 | 0.8 | 0.92 | 0.67 | 0.98 | 0.74 | 0.18 |

| MAPIE | 0.76 | 0.91 | 0.95 | 0.58 | 0.99 | 1.0 | 0.75 | 0.98 | 0.86 | 0.15 | |

| K-S | 0.48 | 0.51 | 0.74 | 0.41 | 0.41 | 0.41 | 0.62 | 0.45 | 0.50 | 0.11 | |

| PSI | 1.11 | 1.02 | 1.0 | 0.89 | 0.92 | 0.92 | 0.85 | 0.93 | 0.95 | 0.08 | |

| Target | 0.95 | 0.7 | 0.7 | 0.87 | 0.61 | 0.38 | 0.89 | 0.8 | 0.73 | 0.18 | |

| Gradient Boosting Regressor | Uncertainty | 0.48 | 0.49 | 1.0 | 0.45 | 0.45 | 0.32 | 0.57 | 0.88 | 0.58 | 0.23 |

| MAPIE | 0.66 | 0.86 | 0.94 | 0.55 | 0.67 | 0.51 | 0.64 | 1.03 | 0.73 | 0.18 | |

| K-S | 0.45 | 0.47 | 0.65 | 0.9 | 0.9 | 0.42 | 0.64 | 0.48 | 0.61 | 0.19 | |

| PSI | 1.11 | 1.01 | 0.99 | 0.91 | 0.92 | 0.9 | 0.85 | 0.98 | 0.95 | 0.08 | |

| Target | 1.05 | 0.73 | 0.54 | 0.92 | 0.65 | 0.46 | 0.88 | 0.8 | 0.75 | 0.19 | |

| MultiLayer-Perceptron | Uncertainty | 1.5 | 0.93 | 0.81 | 0.43 | 0.43 | 0.42 | 0.52 | 0.41 | 0.68 | 0.38 |

| MAPIE | 1.6 | 0.85 | 0.95 | 0.49 | 0.58 | 0.42 | 0.55 | 0.55 | 0.74 | 0.38 | |

| K-S | 1.03 | 0.72 | 1.18 | 0.61 | 0.62 | 0.64 | 0.62 | 0.62 | 0.75 | 0.22 | |

| PSI | 1.1 | 0.75 | 1.08 | 0.76 | 0.88 | 0.79 | 0.74 | 0.66 | 0.84 | 0.16 | |

| Target | 0.63 | 0.8 | 1.24 | 0.6 | 0.59 | 0.54 | 0.73 | 0.78 | 0.73 | 0.22 |