An Algorithmic Framework for Bias Bounties

Abstract

We propose and analyze an algorithmic framework for “bias bounties” — events in which external participants are invited to propose improvements to a trained model, akin to bug bounty events in software and security. Our framework allows participants to submit arbitrary subgroup improvements, which are then algorithmically incorporated into an updated model. Our algorithm has the property that there is no tension between overall and subgroup accuracies, nor between different subgroup accuracies, and it enjoys provable convergence to either the Bayes optimal model or a state in which no further improvements can be found by the participants. We provide formal analyses of our framework, experimental evaluation, and findings from a preliminary bias bounty event.111The most up-to-date version of this paper may be found at https://arxiv.org/abs/2201.10408

1 Introduction

Modern machine learning (ML) is well known for its powerful applications, and more recently, for its potential to train discriminatory models. As organizations become more aware of these negative consequences, many are instituting partial remedies such as responsible AI teams, auditing practices, and model cards (Mitchell et al., 2019) and data sheets (Gebru et al., 2021) that document ML workflows.

Such practices are likely to remain insufficient for at least two reasons. First, even an organization that diligently audits its models on carefully curated datasets cannot anticipate all possible downstream use cases. A face recognition system designed and tested for use in well-lit, front-facing conditions may be applied by a customer in less ideal conditions, leading to degradation in performance overall and on particular subgroups. Second, we live in an era of AI activism, in which teams of researchers, journalists, and other external parties can independently audit models with commercial or open source APIs, and publish their findings in both the research community and mainstream media. In the absence of more stringent regulation of AI and ML, this activism is one of the strongest forces pushing for change on organizations developing ML models and tools. It has the ability to leverage distributed teams of researchers searching for a wide variety of kinds of problems in deployed models and systems.

Unfortunately, the dynamic between ML developers and their critics currently has a somewhat adversarial tone. An external audit will often be conducted privately, and its results aired publicly, without prior consultation with the organization that built the model and system. That organization may endure criticism, and attempt internally to fix the identified biases or problems, but typically there is little or no direct interaction with external auditors.

Over time, the software and security communities have developed “bug bounties” in an attempt to turn similar dynamics between system developers and their critics (or hackers) towards more interactive and productive ends. The hope is that by deliberately inviting external parties to find software or hardware bugs in their systems, and often providing monetary incentives for doing so, a healthier and more rapidly responding ecosystem will evolve.

It is natural for the ML community to consider a similar “bias bounty” approach to the timely discovery and repair of models and systems with bias or other undesirable behaviors. Rather than finding bugs in software, external parties are invited to find biases — for instance, (demographic or other) subgroups of inputs on which a trained model underperforms — and are rewarded for doing so. Indeed, we are already starting to see early field experiments in such events (Chowdhury and Williams, 2021).

In this work, we propose and analyze a principled algorithmic framework for conducting bias bounties against an existing trained model . Our framework has the following properties and features:

-

•

“Bias hunters” audit by submitting pairs of models — a model identifying a subset of inputs to that performs poorly on, and a proposed model which improves on this subset. Requiring participants to identify not just a group but an improved model ensures that improvement on the group is in fact possible (as opposed to identifying a fundamentally hard subgroup, such as images of occluded faces in a face recognition task).

-

•

The proposed groups do not need to be identified in advance, and the improving models do not need to be chosen from predetermined parametric classes; indeed, both groups and improving models can be arbitrarily complex. This is in contrast to most fair ML frameworks, in which training is formulated as a constrained optimization problem over a fixed parametric family of models, with fairness constraints over fixed demographic subgroups.

-

•

Given a proposed group and model pair, our algorithm validates the proposed improvement on a holdout set, using techniques from adaptive data analysis to circumvent the potential for overfitting due to the potentially unlimited complexity of the submitted pair.

-

•

If the improvement is validated, our algorithm has a simple mechanism for automatically incorporating the improvement into an update of in a way that reduces both the overall error and the error on the proposed subgroup. Indeed, our algorithm has the further property that once a subgroup improvement has been accepted, the error on that subgroup will never increase (much) due to subsequent subgroup introductions. Thus there is no tradeoff between overall and subgroup errors, or between different subgroups. This is again in contrast to constrained optimization approaches, where there is necessarily tension between fairness and accuracy. Our algorithm achieves this through the use of a new model class called pointer decision lists.

-

•

Our algorithm provably and monotonically converges quickly to one of two possible outcomes: either we reach the Bayes optimal model, or we reach a model that cannot be distinguished from the Bayes optimal, in the sense that the bias hunters can find no further improvements. If payments are made to the bias hunters in proportion to the scale of the improvement (the product of the size of the group they improve on and the magnitude of the improvement on that group), we guarantee that the total payments made to the bias hunters can be bounded in advance.

-

•

We can alternatively view our framework as an entirely algorithmic approach to training (minimax) fair and accurate models, by replacing the bias hunters with automated mechanisms for finding improving pairs. We propose and analyze two such mechanisms: one based on a reduction to cost-sensitive classification, and an expectation-maximization style approach that alternates between finding the optimal model for a given subgroup and optimizing the subgroup for a given model.

Our contributions include the introduction of the bias bounty framework; proofs of the convergence, generalization and monotonicity properties of our algorithm; experimental results on census-derived Folktables datasets (Ding et al., 2021); and preliminary findings from an initial bias bounty event held in an undergraduate class at the University of Pennsylvania.

1.1 Limitations and Open Questions

The primary limitation of our proposed framework is that it can only identify and correct sub-optimal performance on groups as measured on the data distribution for which we have training data. It does not solve either of the following related problems:

-

1.

Our model appears to perform well on every group only because in gathering data, we have failed to sample representative members of that group.

-

2.

The model that we have cannot be improved on some group only because we have failed to gather the features that are most predictive on that group, and the performance would be improvable if only we had gathered better features.

That is, our framework can be used to find and correct biases as measured on the data distribution from which we have data, but cannot be used to find and correct biases that come from having gathered the wrong dataset. In both cases, one primary obstacle to extending our framework is the need to be able to efficiently validate proposed fixes. For example, because we restrict attention to a single data distribution, given a proposed pair , we can check on a holdout set whether in fact has improved performance compared to our model, on examples from group . This is important to disambiguate distributional improvements compared to subsets of examples that amount to cherrypicking. How can we approach this problem when proposed improvements include evaluations on new datasets, for which we by definition do not have held out data? Compelling solutions to this problem seem to us to be of high interest. We remark that a bias bounty program held under our proposed framework would at least serve to highlight where new data collection efforts are needed, by disambiguating failures of training from failures for the data to properly represent a population: if a group continues to have persistently high error even in the presence of a large population of auditors in our framework, this is evidence that in order to obtain improved error on that group, we need to focus on better representing them within our data.

1.2 Related Work

There are several strands of the algorithmic fairness literature that are closely related to our work. Most popular notions of algorithmic fairness (e.g. those that propose to equalize notions of error across protected groups as in e.g. (Hardt et al., 2016; Agarwal et al., 2018; Kearns et al., 2018; Zafar et al., 2017), or those that aim to “treat similar individuals similarly” as in e.g. (Dwork et al., 2012; Ilvento, 2020; Yona and Rothblum, 2018; Jung et al., 2019)) involve tradeoffs, in that asking for “fairness” involves settling for reduced accuracy. Several papers (Blum and Stangl, 2019; Dutta et al., 2020) show that fairness constraints of these types need not involve tradeoffs (or can even be accuracy improving) on test data if the training data has been corrupted by some bias model and is not representative of the test data. In cases like this, fairness constraints can act as corrections to undo the errors that have been introduced in the data. These kinds of results leverage differences between the training and evaluation data, and unlike our work, do not avoid tradeoffs between fairness and accuracy in settings in which the training data is representative of the true distribution.

A notable exception to the rule that fairness and accuracy must involve tradeoffs is the literature on multicalibration initiated by Hébert-Johnson et al. (Hébert-Johnson et al., 2018; Kim et al., 2019; Jung et al., 2021; Gupta et al., 2021; Dwork et al., 2021) that asks that a model’s predictions be calibrated not just overall, but also when restricted to a large number of protected subgroups . Hébert-Johnson et al. (Hébert-Johnson et al., 2018) and Kim, Ghorbani, and Zou (Kim et al., 2019) show that an arbitrary model can be postprocessed to satisfy multicalibration (and the related notion of “multi-accuracy”) without sacrificing (much) in terms of model accuracy. Our aim is to achieve something similar, but for predictive error, rather than model calibration. There are two things driving the “no tradeoff” result for multicalibration, from which we take inspiration: 1) the fairness notion that they ask for is satisfied by the Bayes-optimal model, and 2) they do not optimize over a fixed model class, but rather a model class defined in terms of the groups that define their fairness notion. These two things will be true for us as well.

The notion of fairness that we ask for in this paper was studied in an online setting (in which the data, rather than the protected groups arrive online) by Blum and Lykouris (Blum and Lykouris, 2020) and generalized by Rothblum and Yona (Rothblum and Yona, 2021) as “multigroup agnostic learnability.” Noarov, Pai, and Roth (Noarov et al., 2021) show how to obtain it in an online setting as part of the same unified framework of algorithms that can obtain multicalibrated predictions. The algorithmic results in these papers lead to complex models — in contrast, our algorithm produces “simple” predictors in the form of a decision list. In contrast to these prior works, we do not view the set of groups that we wish to offer guarantees to as fixed up front, but instead as something that can be discovered online, after models are deployed. Our focus is on fast algorithms to update existing models when new groups on which our model is performing poorly are discovered.

Concurrently and independently of our paper, Tosh and Hsu (Tosh and Hsu, 2021) study algorithms and sample complexity for multi-group agnostic learnability and give an algorithm (“Prepend”) that is equivalent to our Algorithm 1 (“ListUpdate”). Their focus is on sample complexity of batch optimization, however — in contrast to our focus on the discovery of groups on which our model is performing poorly online (e.g. as part of a “bias bounty program”). They also are not concerned with the details of the optimization that needs to be solved to produce an update — we give practical algorithms based on reductions to cost sensitive classification and empirical evaluation. Tosh and Hsu (Tosh and Hsu, 2021) also contains additional results, including algorithms producing more complex hypotheses but with improved sample complexity (again in the setting in which the groups are fixed up front).

The multigroup notion of fairness we employ (Blum and Lykouris, 2020; Rothblum and Yona, 2021) aims to perform optimally on each subgroup , rather than equalizing the performance across subgroups. This is similar in motivation to minimax fairness, studied in (Martinez et al., 2020; Diana et al., 2021b, a), which aim to minimize the error on the maximum error sub-group. Both of these notions of fairness have the merit that they produce models that pareto-dominate equal error solutions, in the sense that in a minimax (or multigroup) optimal solution, every group has weakly lower error than they would have in any equal error solution. However, optimizing for minimax error over a fixed hypothesis class still results in tradeoffs in the sense that it results in higher error than the error optimal model in the same class, and that adding more groups to the guarantee makes the tradeoff more severe. Our approach avoids tradeoffs by optimizing over a class that is dynamically expanded as the set of groups to be protected expands.

The idea of a “bias bug bounty” program dates back at least to a 2018 editorial of Amit Elazari Bar On (On, 2018), and Twitter ran a version of a bounty program in 2021 to find bias issues in its image cropping algorithm (Chowdhury and Williams, 2021). These programs are generally envisioned to be quite different than what we propose here. On the one hand, we are proposing to automatically audit models and award bounties for the discovery of a narrow form of technical bias — sub-optimal error on well defined subgroups — whereas the bounty program run by Twitter was open ended, with human judges and written submissions. On the other hand, the method we propose could underly a long-running program that could automatically correct the bias issues discovered in production systems at scale, whereas Twitter’s bounty program was a labor intensive event that ran over the course of a week.

2 Preliminaries

We consider a supervised learning problem defined over labelled examples . This can represent (for example) a binary classification problem if , a discrete multiclass classification problem if , or a regression problem if . We write to denote a joint probability distribution over labelled examples: . We will write to denote a dataset consisting of labelled examples sampled i.i.d. from . Our goal is to learn some model represented as a function which aims to predict the label of an example from its features, and we will evaluate the performance of our model with a loss function , where represents the “cost” of mistakenly labelling an example that has true label with the prediction . We will be interested in the performance of models not just overall on the underlying distribution, but also on particular subgroups of interest. A subgroup corresponds to an arbitrary subset of the feature space , which we will model using an indicator function:

Definition 1 (Subgroups).

A subgroup of the feature space will be represented as an indicator function . We say that is in group if and is not in group otherwise. Given a group , we write to denote its measure under the probability distribution :

We write to denote the corresponding empirical measure under , which results from viewing as the uniform distribution over its elements.

We can now define the loss of a model both overall and on different subgroups:

Definition 2 (Model Loss).

Given a model We write to denote the average loss of on distribution :

We write to denote the loss on conditional on membership in :

Given a dataset , we write and to denote the corresponding empirical losses on , which result from viewing as the uniform distribution over its elements.

The best we can ever hope to do in any prediction problem (fixing the loss function and the distribution) is to make predictions that are as accurate as those of a Bayes optimal model:

Definition 3.

A Bayes Optimal model with respect to a loss function and a distribution satisfies:

where can be defined arbitrarily for any that is not in the support of .

The Bayes optimal model is pointwise optimal, and hence has the lowest loss of any possible model, not just overall, but simultaneously on every subgroup. In fact, its easy to see that this is a characterization of Bayes optimality.

Observation 4.

Fixing a loss function and a distribution , is a Bayes optimal model if and only if for every group and every alternative model :

The above characterization states that a model is Bayes optimal if and only if it induces loss that is as exactly as low as that of any possible model , when restricted to any possible group . It will also be useful to refer to approximate notions of Bayes optimality, in which the exactness is relaxed, as well as possibly the class of comparison models , and the class of groups . We call this -Bayes optimality to highlight the connection to (exact) Bayes Optimality, but it is identical to what Rothblum and Yona (Rothblum and Yona, 2021) call a “multigroup agnostic PAC solution” with respect to and . Related notions were also studied in (Blum and Lykouris, 2020; Noarov et al., 2021).

Definition 5.

A model is -Bayes optimal with respect to a collection of (group, model) pairs if for each , the performance of on is within of the performance of on . In other words, for every :

When is a product set , then we call “-Bayes Optimal” and the condition is equivalent to requiring that for every , has performance on that is within of the best model on . When and represent the set of all groups and models respectively, we call -Bayes optimal.

Remark 6.

We have chosen to define approximate Bayes optimality by letting the approximation term scale proportionately to the inverse probability of the group , similar to how notions of multigroup fairness are defined in (Kearns et al., 2018; Jung et al., 2021; Gupta et al., 2021). An alternative (slightly weaker) option would be to require error that is uniformly bounded by for all groups, but to only make promises for groups that have probability larger than some threshold, as is done in (Hébert-Johnson et al., 2018). Some relaxation of this sort is necessary to provide guarantees on an unknown distribution based only on a finite sample from it, since we will necessarily have less statistical certainty about smaller subsets of our data.

Note that -Bayes optimality is identical to Bayes optimality when and when and represent the classes of all possible groups and models respectively, and that it becomes an increasingly stronger condition as and grow in expressivity.

3 Certificates of Sub-Optimality and Update Algorithms

Recall that “bias hunters” submit a group that our existing model performs poorly on and an improvement on that group. We need to formulate what our requirements for accepting their proposed improvement would be, and develop a method to incorporate these fixes into our model without retraining it. Formally, suppose we have an existing model , and we find that it is performing sub-optimally on some group . By Observation 4, it must be that is not Bayes optimal, and this will be witnessed by some model such that:

We call such a pair a certificate of sub-optimality. Note that by Observation 4, such a certificate will exist if and only if is not Bayes optimal. We can define a quantitative version of these certificates:

Definition 7.

A group indicator function together with a model form a -certificate of sub-optimality for a model under distribution if:

-

1.

Group has probability mass at least under : , and

-

2.

improves on the performance of on group by at least :

We say that form a certificate of sub-optimality for if they form a -certificate of optimality for for any constants .

The core of our algorithmic updating framework will rely on a close quantitative connection between certificates of sub-optimality and approximate Bayes optimality. The following theorem can be viewed as a quantitative version of Observation 4.

Theorem 8.

Fix any , and any collection of (group,model) pairs . There exists a -certificate of sub-optimality for if and only if is not -Bayes optimal for .

Proof.

We need to prove two directions. First, we will assume that is -Bayes optimal, and show that in this case there do not exist any pairs such that form a -certificate of sub-optimality with . Fix a pair . Without loss of generality, we can take (and if we are done, so we can also assume that ). Since is -Bayes optimal, by definition we have that:

Solving, we get that as desired.

Next, we prove the other direction: We assume that there exists a pair that form an -certificate of sub-optimality, and show that is not -Bayes optimal for any . Without loss of generality we can take and conclude:

which falsifies -Bayes optimality for any as desired. ∎

Theorem 8 tells us that if we are looking for evidence that a model fails to be Bayes Optimal (or more generally, fails to be -Bayes optimal), then without loss of generality, we can restrict our attention to certificates of sub-optimality with large parameters — these exist if and only if is significantly far from Bayes optimal. But it does not tell us what to do if we find such a certificate. Can we use a certificate of sub-optimality for to easily update to a new model that both corrects the suboptimality witnessed by and makes measurable progress towards Bayes Optimality? It turns out that the answer is yes, and we can do this with an exceedingly simple update algorithm, which we analyze next. The update algorithm (Algorithm 1) takes as input a model together with a certificate of sub-optimality for , , and outputs an improved model based on the following intuitive update rule: If an example is in group (i.e. if ), then we will classify using ; otherwise we will classify using .

Theorem 9.

Algorithm 1 (ListUpdate) has the following properties. If form a -certificate of sub-optimality for , and then:

-

1.

The new model matches the performance of on group : , and

-

2.

The overall performance of the model is improved by at least : .

Proof.

It is immediate from the definition of that , since for any such that , . It remains to verify the 2nd condition. Because we also have that for every such that , , we can calculate:

∎

We can use Algorithm 1 as an iterative update algorithm: If we have a model , and then discover a certificate of sub-optimality for , we can update our model to a new model . If we then find a new certificate of sub-optimality , we can once again use Algorithm 1 to update our model to a new model, , and so on. The result is that at time , we have a model in the form of a decision list in which the internal nodes branch on the group indicator functions and the leaves invoke the models or the initial model . See Figure 1. Note that to evaluate such a decision list on a point , although we might need to evaluate for every group indicator used to define the list, we only need to evaluate a single model . Moreover, as we will show next in Theorem 10, when the decision list is constructed iteratively in this manner, it cannot grow very long. Thus, evaluation can be fast even if the models used to construct it are complex.The fact that each update makes progress towards Bayes Optimality (in fact, optimal progress, given Theorem 8) means that this updating process cannot go on for too long:

Theorem 10.

Fix any . For any initial model with loss and any sequence of models , such that and each pair forms a -certificate of suboptimality for for some such that , the length of the update sequence must be at most .

Proof.

By assumption . Because each is a -certificate of suboptimality of with , we know from Theorem 9 that for each , . Hence . But loss is non-negative: . Thus it must be that as desired. ∎

What can we do with such an update algorithm? Given a model , we can search for certificates of sub-optimality, and if we find them, we can make quantitative progress towards improving our model. We can then repeat the process. The guarantee of Theorem 10 is that this process of searching and updating cannot go on for very many rounds before we arrive at a model that our search process is unable to demonstrate is not Bayes Optimal. How interesting this is depends on what our search process is.

Suppose, for example, that we have an optimization algorithm that for some class of (group,model) pairs can find a certificate of sub-optimality whenever one exists. Paired with our update algorithm, we obtain an algorithm which quickly converges to an -Bayes Optimal model. We give such an algorithm in Section 4.2 .

Suppose alternately that we open the search for certificates of sub-optimality to a large and motivated population: for example, to machine learning engineers, regulators and the general public, incentivized by possibly large monetary rewards. In this case, the guarantee of Theorem 10 is that the process of iteratively opening our models up to scrutiny and updating whenever certificates of suboptimality are found cannot go on for too many rounds: at convergence, it must be either that our deployed model is -Bayes optimal, or that if not, at least nobody can find any evidence to contradict this hypothesis. Since in general it is not possible to falsify Bayes optimality given only a polynomial amount of data and computation, this is in a strong sense the best we can hope for. We give a procedure for checking large numbers of arbitrarily complex submitted proposals for certificates of sub-optimality (e.g. that arrive as part of a bias bounty program) in Section 4.1. There are two remaining obstacles, which we address in the next sections:

-

1.

Our analysis so far is predicated on our update algorithm being given certificates of sub-optimality . But and are defined with respect to the distribution , and we will not have direct access to — we will only have samples drawn from . So how can we find certificates of sub-optimality and check their parameters? In an algorithmic application in which we search for certificates within a restricted class , we can appeal to uniform convergence bounds, but the bias bounty application poses additional challenges. In this case, the certificates are not constrained to come from any fixed class, and so we cannot appeal to uniform convergence results. If we are opening up the search for certificates of sub-optimality to the public (with large monetary incentives), we also need to be prepared to handle a very large number of submissions. In Section 4.1 we show how to use techniques from adaptive data analysis to re-use a small holdout set to check a very large number of submissions, while maintaining strong worst case guarantees (Dwork et al., 2015a, b, c; Blum and Hardt, 2015; Bassily et al., 2021; Jung et al., 2020).

-

2.

Theorem 9 gives us a guarantee that whenever we are given a certificate of sub-optimality , our new model makes improvements both with respect to its error on , and with respect to overall error. But it does not promise that the update does not increase error for some other previously identified group for . This would be particularly undesirable in a “bias bounty” application, and would represent the kind of tradeoff that our framework aims to circumvent. However, we show in Section 4.1.1 that (up to small additive terms that come from statistical estimation error), our updates can be made to be groupwise monotonically error improving, in the sense that the update at time does not increase the error for any group identified at any time .

4 Obtaining Certificates of Suboptimality

In this section we show how to find and verify proposed certificates of sub-optimality given only a finite sample of data . We consider two important cases:

In Section 4.1, we consider the “bias bounty” application in which the discovery of certificates of sub-optimality is crowd-sourced (aided perhaps with API access to the model and a training dataset). In this case, we face two main difficulties:

-

1.

The submitted certificates might be arbitrary (and in particular, not guaranteed to come from a class of bounded complexity or expressivity), and

-

2.

We expect to receive a very large number of submitted certificates, all of which need to be checked.

The first of these difficulties means that we cannot appeal to uniform convergence arguments to obtain rigorous bounds on the sub-optimality parameters and . The second of these difficulties means that we cannot naively rely on estimates from a (single, re-used) holdout set to obtain rigorous bounds on and .

In Section 4.2 we consider the algorithmic application in which the discovery of certificates is treated as an optimization problem over , for particular classes . In this case we give two algorithms for finding -Bayes optimal models via efficient reductions to cost sensitive classification problems over an appropriately defined class, solved over a polynomially sized dataset sampled from the underlying distribution.

4.1 Unrestricted Certificates and Bias Bounties

In this section we develop a procedure to re-use a holdout set to check the validity of a very large number of proposed certificates of sub-optimality with rigorous guarantees. Here we make no assumptions at all about the structure or complexity of either the groups or models , or the process by which they are generated. This allows us the flexibility to model e.g. a public bias bounty, in which a large collection of human competitors use arbitrary methods to find and propose certificates of sub-optimality, potentially adaptively as a function of all of the information that they have available. We use simple description length techniques developed in the adaptive data analysis literature (Dwork et al., 2015b; Blum and Hardt, 2015). Somewhat more sophisticated techniques which employ noise addition (Dwork et al., 2015a, c; Bassily et al., 2021; Jung et al., 2020) could also be directly used here to improve the sample complexity bound in Theorems 11 and 12 by a factor, but we elide this for clarity of exposition. First we give a simple algorithm (Algorithm 2) that takes as input a stream of arbitrary adaptively chosen triples , and checks if each form a certificate of sub-optimality for . We then use this as a sub-routine in Algorithm 3 which maintains a sequence of models produced by ListUpdate (Algorithm 1) and takes as input a sequence of proposed certificates which claim to be certificates of sub-optimality for the current model : it updates the current model whenever such a proposed certificate is verified.

Theorem 11.

Let be any distribution over labelled examples, and let be a holdout dataset consisting of i.i.d. samples from . Suppose:

Let be the output stream generated by CertificateChecker (Algorithm 2). Then for any possibly adaptive process generating a stream of up to submissions as a function of the output stream , with probability over the randomness of :

-

1.

For every round such that (the submission is rejected), we have that is not a certificate of sub-optimality for for any with . And:

-

2.

For every round such that (the submission is accepted), we have that is a -certificate of sub-optimality for for .

The high level idea of the proof is as follows: For any fixed (i.e. non-adaptively chosen) sequence of submissions, a Chernoff bound and a union bound are enough to argue that the estimate of the product of the parameters and on the holdout set is with high probability close to their expected value on the underlying distribution. We then observe that submissions depend on the holdout set only through the transcript , and so are able to union bound over all possible transcripts . Since contains only instances in which the submission is accepted, the number of such transcripts grows only polynomially in rather than exponentially, and so we can union bound over all transcripts with only a logarithmic dependence in .

Proof.

We first consider any fixed triple of functions . Observe that we can write:

Since each is drawn independently from , each term in the sum is an independent random variable taking value in the range . Thus is the average of independent bounded random variables and we can apply a Chernoff bound to conclude that for any value of :

Solving for we have that with probability , we have if:

This analysis was for a fixed triple of functions , but these triples can be chosen arbitrarily as a function of the transcript . We therefore need to count how many transcripts might arise. By construction, has length at most and has at most indices such that . Thus the number of transcripts that can arise is at most: , and each transcript results in some sequence of triples . Thus for any mechanism for generating triples from transcript prefixes, there are at most triples that can ever arise. We can complete the proof by union bounding over this set. Taking and plugging into our Chernoff bound above, we obtain that with probability over the choice of , for any method of generating a sequence of triples from transcripts , we have that: so long as:

Finally, note that whenever this event obtains, the conclusions of the theorem hold, because we have that exactly when . In this case, as desired. Similarly, whenever , we have that as desired. ∎

We conclude this section by showing that we can use CertificateChecker (Algorithm 2) to run an algorithm FalsifyAndUpdate (Algorithm 3) which:

-

1.

Persistently maintains a current model publicly, and elicits a stream of submissions attempting to falsify the hypothesis that the current model is approximately Bayes optimal,

-

2.

With high probability does not reject any submissions that falsify the assertion that is -Bayes optimal,

-

3.

With high probability does not accept any submissions that do not falsify the assertion that is -Bayes optimal,

-

4.

Whenever it accepts a submission , it updates the current model and outputs a new model such that and such that no longer falsifies the sub-optimality of , and

-

5.

With high probability does not halt until receiving submissions.

Theorem 12.

Fix any . Let be any distribution over labelled examples, and let be a holdout dataset consisting of i.i.d. samples from . Suppose:

Then for any (possibly adaptive) process generating a sequence of at most submissions , with probability at least , we have that FalsifyAndUpdate satisfies:

-

1.

If is rejected, then is not a -certificate of sub-optimality for , where is the current model at the time of submission , for any such that .

-

2.

If is accepted, then is a -certificate of sub-optimality for , where is the current model at the time of submission , for some such that . Moreover, the new model output satisfies and .

-

3.

FalsifyAndUpdate does not halt before receiving all submissions.

At a high level, this proof reduces to the guarantees of CertificateChecker and ListUpdate. Note that the models produced in the run of this algorithm depend on the holdout set only through the transcript produced by certificate checker — i.e. given the stream of submissions and the output of CertificateChecker, one can reproduce the decision lists output by FalsifyAndUpdate. Thus we inherit the sample complexity bounds proven for CertificateChecker.

Proof.

This theorem follows straightforwardly from the properties of Algorithm 1 and Algorithm 2. From Theorem 11, we have that with probability , every submission accepted by CertificateChecker (and hence by FalsifyandUpdate) is a -certificate of sub-optimality for with and every submission rejected is not a -certificate of sub-optimality for any with .

Whenever this event obtains, then for every call that FalsifyAndUpdate makes to is such that is a -certificate of sub-optimality for for . Therefore by Theorem 9, we have that and . Finally, by Theorem 10, if each invocation of the iteration is such that is a -certificate of sub-optimality for with , then there can be at most such invocations. Since FalsifyAndUpdate makes one such invocation for every submission that is accepted, this means there can be at most submissions accepted in total. But CertificateChecker has only two halting conditions: it halts when either more than submissions are accepted, or when submissions have been made in total. Because with probability at least no more than submissions are accepted, it must be that with probability , FalsifyAndUpdate does not halt until all submissions have been received. ∎

Remark 13.

Note that FalsifyAndUpdate has sample complexity scaling only logarithmically with the total number of submissions that we can accept, and no dependence on the complexity of the submissions. This means that a relatively small holdout dataset is sufficient to run an extremely long-running bias bounty program (i.e. handling a number of submissions that is exponentially large in the size of the holdout set) that automatically updates the current model whenever submissions are accepted and bounties are awarded.

4.1.1 Guaranteeing Groupwise Monotone Improvements

FalsifyAndUpdate (Algorithm 3) has the property that whenever it accepts a submission falsifying that its current model is -Bayes optimal, it produces a new model that has overall loss that has decreased by at least . It also promises that has strictly lower loss than on group . However, because the groups can have arbitrary intersections, this does not imply that has error that is lower than that of on groups that were previously identified. Specifically, let denote the set of at most groups that make up the internal nodes of decision list — i.e. the set of groups corresponding to submissions that were previously accepted and incorporated into model . It might be that for some , . This kind of non-monotonic behavior is extremely undesirable in the context of a bias bug bounty program, because it means that previous instances of sub-optimal behavior on a group that were explicitly identified and corrected for can be undone by future updates. Note that simply repeating the update when this occurs does not solve the problem — this would return the performance of the model on to what it was at the time that it was originally introduced — but since the model’s performance on might have improved in the mean time, it would not guarantee groupwise error monotonicity.

There is a simple fix, however: whenever a new proposed certificate of sub-optimality for a model is accepted and a new model is generated, add the proposed certificates to the front of the stream of submissions, for each pair of and . Updates resulting from these submissions (which we call repairs) might themselves generate new non-monotonicities, but repeating this process recursively is sufficient to guarantee approximate groupwise monotonicity — and because we know from Theorem 10 that the total number of updates cannot exceed , this process never adds more than submissions to the existing stream, and thus affects the sample complexity bound only by low order terms. This is because for each of the at most updates, there are at most proposed certificates that can be generated in this way. Moreover, if any of these constructed submissions trigger a model update, these updates too count towards the limit of updates that can ever occur — and so do not increase the maximum length of the decision list that is ultimately output.The procedure, which we call MonotoneFalsifyAndUpdate, is described as Algorithm 4. Here we state its guarantee:

Theorem 14.

Fix any . Let be any distribution over labelled examples, and let be a holdout dataset consisting of i.i.d. samples from . Suppose:

Then for any (possibly adaptive) process generating a sequence of at most submissions , with probability at least , we have that MonotoneFalsifyAndUpdate satisfies all of the properties proven in Theorem 12 for FalsifyAndUpdate, and additionally satisfies the following error monotonicity property. Consider any model that is output, and any group . Then:

Proof.

The proof that MonotoneFalsifyAndUpdate satisfies the first two conclusions of Theorem 12:

-

1.

If is rejected, then is not a -certificate of sub-optimality for , where is the current model at the time of submission , for any such that .

-

2.

If is accepted, then is a -certificate of sub-optimality for , where is the current model at the time of submission , for some such that . Moreover, the new model output satisfies .

are identical and we do not repeat them here. We must show that with probability , CertificateChecker (and hence MonotoneFalsifyAndUpdate) does not halt before processing all submissions. Note that MonotoneFalsifyAndUpdate initializes an instance of CertificateChecker that will not halt before receiving many submissions. Thus it remains to verify that our algorithm does not produce more than many submissions to CertificateChecker in its monotonicity update process. But this will be the case, because by Theorem 10, , and so after each call to ListUpdate, we generate at most many submissions to CertificateChecker. Since there can be at most such calls to ListUpdate, the claim follows.

To see that the monotonicity property holds, assume for sake of contradiction that it does not — i.e. that there is a model , a group , and a model with such that:

In this case, the pair would form a -certificate of sub-optimality for with . But if , then this certificate must have been rejected, which we have already established is an event that occurs with probability at most . ∎

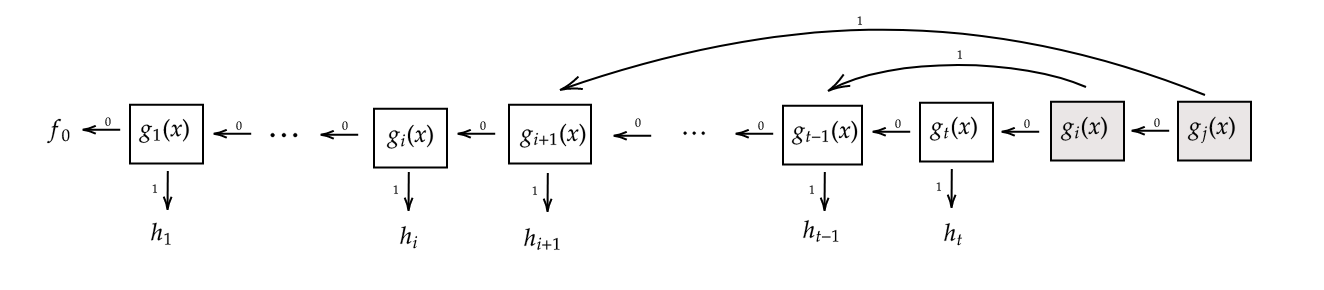

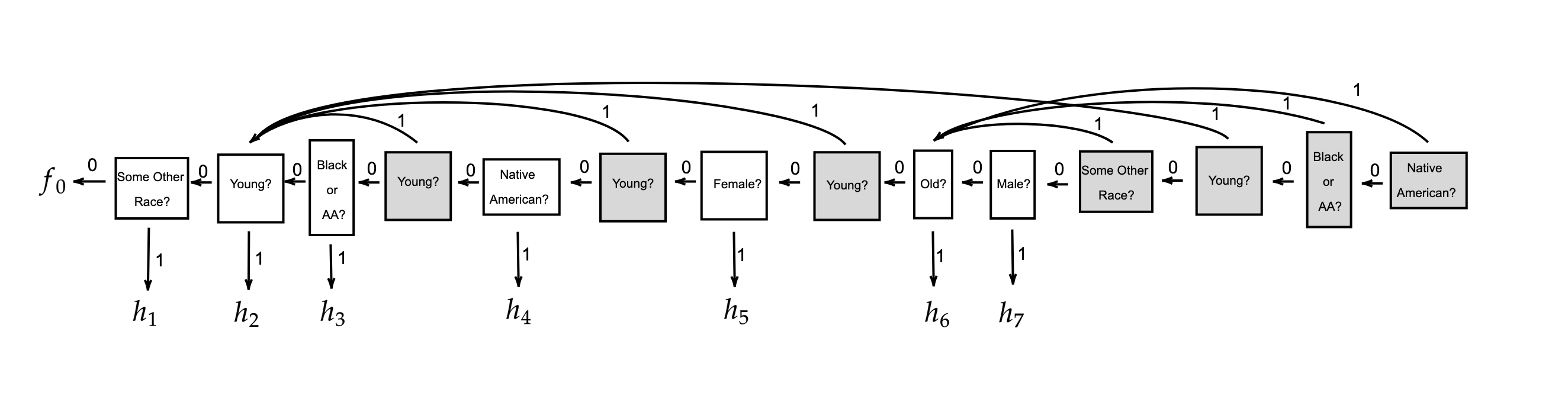

Algorithm 4 introduces updates of the form , where is a decision list previously generated by ListUpdate. We might worry that these updates could produce a very large model, since on such an update, the new model at the first leaf of the new decision list entirely replicates some previous decision list . However, note that for any such update, is a prefix of . Therefore, rather than replicating , we can introduce a backpointer to level of our existing decision list, without increasing our model’s size. We call such a model a pointer decision list, as shown in Figure 2. We call the pointer nodes that are introduced to repair non-monotonicities introduced by previous updates repair nodes of our pointer decision list. These are the nodes that are shaded in our illustration in Figure 2.

4.2 Certificates of Bounded Complexity and Algorithmic Optimization

In this section we show how to use our ListUpdate method as part of an algorithm for explicitly computing -Bayes optimal models from data sampled i.i.d. from the underlying distribution . First, we must show that if we find certificates of sub-optimality on our dataset, that we can be assured that they are certificates of sub-optimality on the underlying distribution. Here, we invoke uniform convergence bounds that depend on being a class of bounded complexity. Next, we must describe an algorithmic method for finding certificates of sub-optimality that maximize . Here we give two approaches. The first approach is a reduction to cost sensitive (ternary) classification: the result of the reduction is that the ability to solve weighted multi-class classification problems over some class of models gives us the ability to find certificates of sub-optimality over a related class whenever they exist. The second approach takes an “EM” style alternating maximization approach over and in turn, where each alternating maximization step can be reduced to a binary classification problem. It is only guaranteed to converge to a local optimum (or saddlepoint) of its objective — i.e. to find a certificate of sub-optimality that cannot be improved by changing either or unilaterally — but has the merit that it requires only standard binary classification algorithms for a class and to search for certificates of sub-optimality in . For simplicity of exposition, in this section we restrict attention to the binary classification problem, where the labels are binary ) and our loss function corresponds to classification error — but the approach readily extends to more general label sets (replacing VC-dimension with the appropriate notion of combinatorial dimension as necessary).

The algorithmic problem we need to solve at each round is, given an existing model , find a -certificate of optimality for that maximizes as computed on the empirical data — i.e. to solve:

| (1) |

We defer for now the algorithmic problem of finding these certificates, and describe a generic algorithm that can be invoked with any method for finding such certificates. First, we state a useful sample complexity bound proven in (Kearns et al., 2018) in a related context of multi-group fairness — we here state the adaptation to our setting.

Lemma 15 (Adapted from (Kearns et al., 2018)).

Let denote a class of group indicator functions with VC-dimension and denote a class of binary models with VC-dimension . Let be an arbitrary binary model. Then if:

we have that with probability over the draw of a dataset , for every and :

With our sample complexity lemma in hand we are ready to present our generic reduction from training an -Bayes optimal model to the optimization problem over given in (1).

Theorem 16.

Fix an arbitrary distribution over , a class of group indicator functions of VC-dimension and a class of binary models of VC-dimension . Let and be arbitrary. If:

and , then with probability , TrainByOpt (Algorithm 5) returns a model that is -Bayes optimal, using at most calls to a sub-routine for solving the optimization problem over given in (1).

Proof.

Each of the partitioned datasets has size at least and is selected independently of and so we can invoke Lemma 15 with and to conclude that with probability , for every round :

For the rest of the argument we will assume this condition obtains. By assumption, at every round the models exactly maximize amongst all models , and so in combination with the above uniform convergence bound, they are -approximate maximizers of . Therefore, if at any round the algorithm outputs a model , it must be because:

Equivalently, for every , it must be that:

By definition, such a model is -Bayes optimal.

Similarly, if at any round we do not output , then it must be that forms a -certificate of sub-optimality for and such that . By Theorem 10 we have that for any sequence of models such that and forms a -certificate of sub-optimalty for with , it must be that . Therefore, it must be that if our algorithm outputs model , then must be -Bayes optimal. If this were not the case, then by Theorem 8, there would exist a -certificate of sub-optimality for with , which we could use to extend the sequence by setting — but that would contradict Theorem 10. Since -Bayes optimality is strictly stronger than -Bayes optimality, this completes the proof. ∎

Algorithm 5 is an efficient algorithm for training an -Bayes optimal model whenever we can solve optimization problem (1) efficiently. We now turn to this optimization problem. In Section 4.2.1 we show that the ability to solve cost sensitive classification problems over a ternary class gives us the ability to solve optimization problem 1 over a related class . In Section 4.2.2 we show that the ability to solve standard empirical risk minimization problems over classes and respectively give us the ability to run iterative updates of an alternating-maximization (“EM style”) approach to finding certificates .

4.2.1 Finding Certificates via a Reduction to Cost-Sensitive Ternary Classification

For this approach, we start with an arbitrary class of ternary valued functions . It will be instructive to think of the label “” as representing the decision to “defer” on an example, leaving the classification outcome to another model. We will identify such a ternary-valued function with a pair of binary valued functions representing a group indicator function and a binary model that might form a certificate of sub-optimality . They are defined as follows:

Definition 17.

Given a ternary valued function , the -derived group and model are defined as:

In other words, interpreting as the decision for to “defer” on , defines exactly the group of examples that does not defer on, and is the model that makes the same prediction as on every example that does not defer on. Given a class of ternary functions , let the -derived certificates denote the set of pairs that can be so derived from some : . Similarly let and denote the class of group indicator functions and models derived from respectively.

Given a model Our goal is to reduce the problem of solving optimization problem (1) over to the problem of solving a ternary cost-sensitive classification problem over :

Definition 18.

A cost-sensitive classification problem is defined by a model class consisting of functions , where is some finite label set, a distribution over , and a set of real valued costs for each pair in the support of and each label . A solution to the cost-sensitive classification problem is given by:

i.e. the model that minimizes the expected costs for the labels it assigns to points drawn from .

The reduction will make use of the following induced costs:

Definition 19.

Given a binary model , the induced costs of are defined as follows:

Intuitively, it costs nothing to defer a decision to the existing model — or equivalently, to make the same decision as . On the other hand, making the wrong decision on an example costs when would have made the right decision, and making the right decision “earns” when would not have.

Theorem 20.

Fix an arbitrary distribution over , let be a class of ternary valued functions, and let be any binary valued model. Let be a solution to the cost-sensitive classification problem , where are the induced costs of . We have that:

In other words, when is the empirical distribution over , form a solution to optimization problem (1).

Proof.

For any model , we can calculate its expected cost under the induced costs of :

Thus minimizing is equivalent to maximizing over . ∎

In other words, in order to be able to efficiently implement algorithm 5 for the class , it suffices to be able to solve a ternary cost sensitive classification problem over . The up-shot is that if we can efficiently solve weighted multi-class classification problems (for which we have many algorithms which form good heuristics) over , then we can find approximately -Bayes optimal models as well.

4.2.2 Finding Certificates Using Alternating Maximization

The reduction from optimization problem (1) that we gave in Section 4.2.1 to ternary cost sensitive classification starts with a ternary class and then finds certificates of sub-optimality over a derived class . What if we want to start with a pre-defined class of group indicator functions and models , and find certificates of sub-optimality ? In this section we give an alternating maximization method that attempts to solve optimization problem 1 by alternating between maximizing over (holding fixed), and maximizing over (holding fixed):

| (2) |

| (3) |

We show that each of these alternating maximization steps can be reduced to solving a standard (unweighted) empirical risk minimization problem over and respectively. Thus, each can be solved for any heuristic for standard machine learning problems — we do not even require support for weighted examples, as we do in the cost sensitive classification approach from Section 4.2.1. This alternating maximization approach quickly converges to a local optimum or saddle point of the optimization objective from from (1) — i.e. a solution that cannot be improved by either a unilateral change of either or .

We begin with the minimization problem (3) over , holding fixed, and show that it reduces to an empirical risk minimization problem over .

Lemma 21.

Fix any and dataset . Let be the subset of consisting of members of group . Let . Then is a solution to optimization problem 3.

Proof.

We observe that only the final term of the optimization objective in (3) has any dependence on when is held fixed. Therefore:

∎

Next we consider the minimization problem (2) over , holding fixed and show that it reduces to an empirical risk minimization problem over . The intuition behind the below construction is that the only points that matter in optimizing our objective are those on which the models and disagree. Amongst these points on which the two models disagree, we want to have if correctly predicts the label, and not otherwise.

Proof.

For each , we partition the set of points such that according to how they are labelled by and :

i.e. amongst the points in group , consists of the points that both and classify correctly, consists of the points that both classify incorrectly, and and consist of points that and disagree on: are those points that classifies correctly, and are those points that classifies correctly. Write:

to denote the corresponding proportions of each of the sets within .

With these two components in hand, we can describe our alternating maximization algorithm for finding certificates of sub-optimality for a model (Algorithm 6):

We have the following theorem:

Theorem 23.

Let be an arbitrary dataset, be an arbitrary model, and be arbitrary group and model classes, and . Then after solving at most empirical risk minimization problems over each of and , AltMinCertificateFinder (Algorithm 6) returns a -certificate of sub-optimality for that is an -approximate local optimum (or saddle point) in the sense that:

-

1.

For every , is not a certificate of sub-optimality for for any , and

-

2.

For every , is not a certificate of sub-optimality for for any

Proof.

By the halting condition of the While loop, every iteration of the While loop increases by at least . Since this quantity is bounded in , there cannot be more than iterations. Each iteration solves a single empirical risk minimization problem over each of and .

5 Experiments

We next provide an experimental illustration and evaluation of our main algorithm MonotoneFalsifyAndUpdate (Algorithm 4), as well as our optimization approach (Algorithm 5) paired with our reduction to ternary cost sensitive classification. We report findings on a number of different datasets and classification tasks from the recently published Folktables package (Ding et al., 2021), which provides extensive U.S. census-derived Public Use Microdata Samples (PUMS). These granular and large datasets are well-suited to experimental evaluations of algorithmic fairness, as they include a number of demographic or protected features including race categories, age, disability status, and binary sex categories. We refer to (Ding et al., 2021) for details of the datasets examined below.

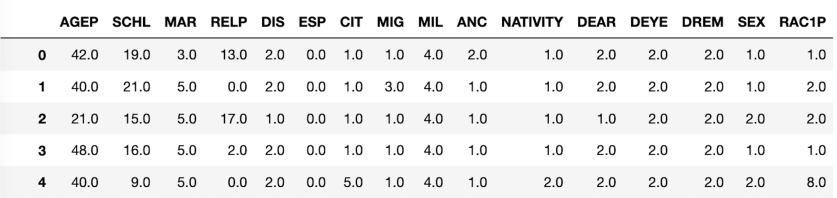

We implemented Algorithm 4 and divided each dataset examined into 80% for training pairs as proposed certificates of sub-optimality for the algorithm’s current model, and 20% for use by the certificate checker to validate improvements. In order to clearly illustrate the gradual subgroup and overall error improvements, we train a deliberately simple initial model (a decision stump). In the first set of experiments, the sequence of subgroups is 11 different demographic groups given by features common to all of the Folktables datasets. We consider four different datasets corresponding to four different states and prediction tasks, all for the year 2018 (the most recent available). Table 1 and its caption detail the states and tasks, the total dataset sizes, and the definitions and counts of each demographic subgroup considered. Figure 3 shows a sample fragment and the full feature set for one of the prediction tasks.

| Dataset | Total | White | Black | Asian | Native | Other | Two+ | Male | Female | Young | Middle | Old |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| NY Employment | 196966 | 138473 | 24024 | 17030 | 10964 | 5646 | 829 | 95162 | 101804 | 68163 | 47469 | 81334 |

| Oregon Income | 21918 | 18937 | 311 | 923 | 552 | 823 | 372 | 11454 | 10464 | 5041 | 9124 | 7753 |

| Texas Coverage | 98927 | 72881 | 11192 | 4844 | 6660 | 2555 | 795 | 42128 | 56799 | 42048 | 31300 | 25579 |

| Florida Travel | 88070 | 70627 | 10118 | 2629 | 2499 | 1907 | 290 | 45324 | 42746 | 16710 | 35151 | 36209 |

In our first experiments, these 11 subgroups were introduced to Algorithm 4 in some order, and for each a depth 10 decision tree was trained on just the training data falling into that subgroup. These pairs are then given to the certificate checker, and if improves the holdout set error for , the improvement is accepted and incorporated into the model, and any needed monotonicity repairs of previously introduced groups are made. Otherwise the pair is rejected and we proceed to the next subgroup.

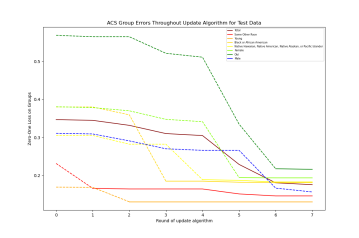

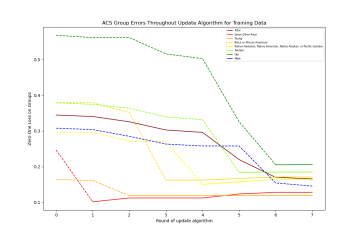

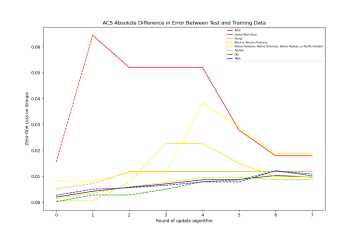

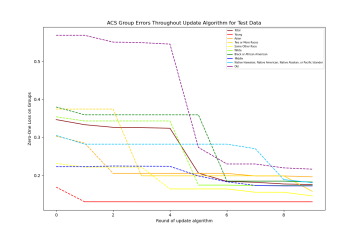

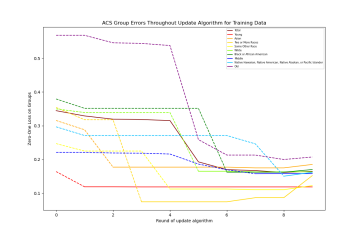

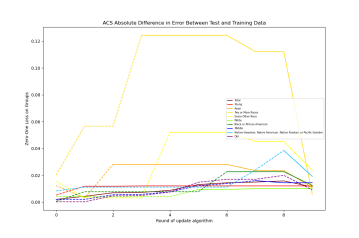

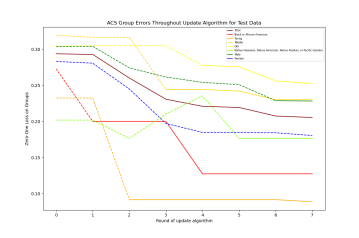

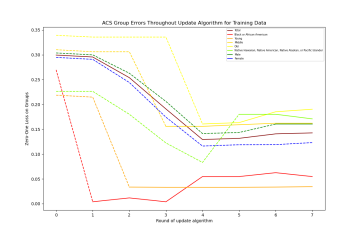

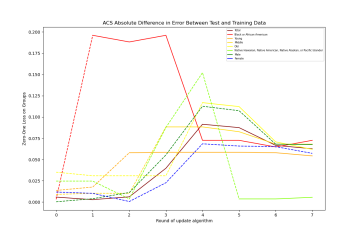

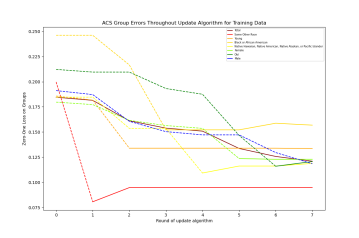

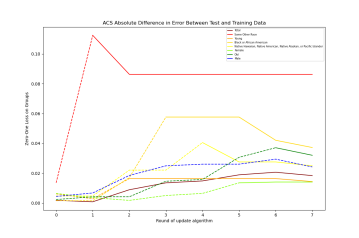

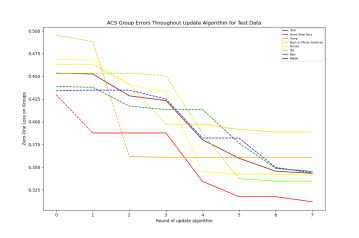

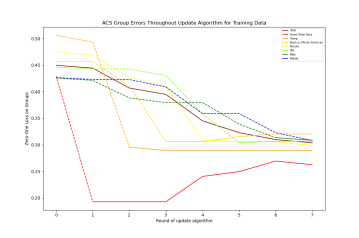

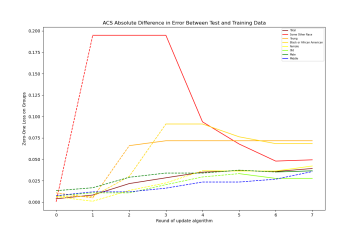

Each of the five rows of Figure 4 shows the results of one experiment of this type, with the left panel in each row showing the test error of each subgroup and overall; the middle panel showing the training error of each subgroup and overall; and the right panel showing the absolute difference of train and test errors. The axis corresponds to the rounds of Algorithm 4. Since the subgroups are introduced in some sequential order (given in the legends), we plot the subgroup errors using dashed lines up until the round at which the group is introduced, and solid lines thereafter for visual clarity. Subgroups whose trained decision tree was rejected by the certificate checker are not shown at all. In Figure 5, a depiction of the decision list generated by the employment task in row 1 of Figure 4 is given.

A number of overarching observations are in order. First, as promised by Theorem 14, the overall and subgroup test errors (left panels) are all monotonically non-increasing after the introduction of the subgroup, and generally enjoy significant improvement as the algorithm proceeds. Note that even prior to the introduction of a subgroup (dashed lines), the test errors are generally non-increasing. Although this is not guaranteed by the theory, it is not necessarily surprising, since before groups are introduced they often start from a high baseline error. However, this is not always the case — for example, on the Oregon income prediction task (third row) the test error for the Native subgroup (light green) increases significantly with the introduction of the subgroups for young and middle-aged at rounds 3 and 4 before it has been introduced.

We also note that, as shown in Figure 5, the need for repair backpointers for previously introduced groups upon introduction of a new group is rather common on these datasets, which demonstrates that this is a crucial feature of our algorithm for guaranteeing group monotonicity. Note that this is not in opposition to our observation that we often have monotonic improvement for groups before they are introduced, since after a group is introduced, the model performs well on them, and so it is more likely for changes in group performance to increase error.

Turning next to the subgroup and overall training errors (middle panels), we observe that while they are generally non-increasing, they are not exclusively non-increasing, and this is not guaranteed by the theory — indeed, the entire purpose of the certificate checker enforcing monotonicity on the test set is to validate proposed improvements from training. Examining the differences between train and test errors (right panels): as expected, the gaps tend to be larger for smaller subgroups since overfitting is more likely. Nevertheless, by the final rounds, train and test errors are generally close, almost always less than 0.1 and often less than 0.05. Second, while volatile, the train-test gaps generally increase with rounds of the algorithm. This is because the algorithm’s model increases in complexity with rounds, thus training errors underestimate test errors more as the algorithm proceeds.

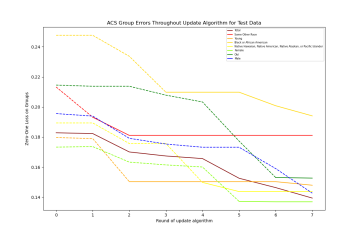

The first two rows of plots in Figure 4 correspond to experiments on the same dataset (New York employment task), with the only difference being the order in which the demographic subgroups are introduced to Algorithm 4. This ordering can have qualitative effects on the behavior of the algorithm, including which subgroup improvements are accepted. For example, the male and female subgroups appear in the first row but are absent in the second due to their proposed improvements being rejected, while the Asian, 2 or more races, white, and middle-age subgroups appear in the second row but not the first. While the evolution of errors for the subgroups common to both rows is also quite different, in general both the overall and all 11 subgroup test errors end up being quite similar for both orderings at their final round, with the differences generally being in the second or third decimal place, as shown by Table 2.

| Total | White | Black | Asian | Native | Other | Two+ | Male | Female | Young | Middle | Old |

| 0.0004 | 0.016 | 0.065 | 0.023 | 0.0367 | 0.020 | 0.033 | 0.016 | 0.008 | 0.040 | 0.045 | 0.030 |

Examining the actual pointer decision list produced in one of these experiments is also enlightening — see Figure 5. We note a couple of things. First, observing the repairs for the group “Young”, we see that via the sequence of repairs, any “young” individual will always be classified by the model introduced at round 2 together with the group “young”. This is in contrast to the other groups, whose members are split across a number of different models by the pointer decision list. This indicates that being in the group “young” is more salient than being in any of the racial or gender groups in this task from the point of view of accurate classification. Second, we note that unlike for the group “young”, repairs for other groups do not necessarily point back to the round at which they were introduced. For example, the right-most repairs for “Native American”, “Black or AA”, and “Some Other Race” point back to round 6, at which the group “Old” was introduced. This indicates that the pointer decision list at round 6 is more accurate for each of these groups then the decision trees and that were introduced along with these groups, despite the fact that these decision trees were trained only on examples from their corresponding groups.

The experiments described so far apply our framework and algorithm to a setting in which the groups considered are simple demographic groups, introduced in a fixed ordering. We finish with a brief experimental investigation of the approach described in Section 4.2, in which the discovery of updates is posed as an optimization problem. Specifically, we implemented the ternary CSC approach of Section 4.2.1. In our implementation, following the approach taken in (Agarwal et al., 2018; Kearns et al., 2019), we learn a ternary classifier by first learning two separate depth 7 decision tree regression functions for the costs of predicting 0 and 1, while the cost of predicting ”?” is always 0 as per Section 4.2.1. Our final ternary classifier chooses the prediction that minimizes the costs predicted by the regression functions.

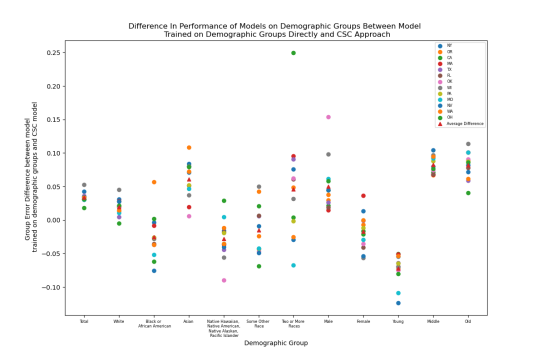

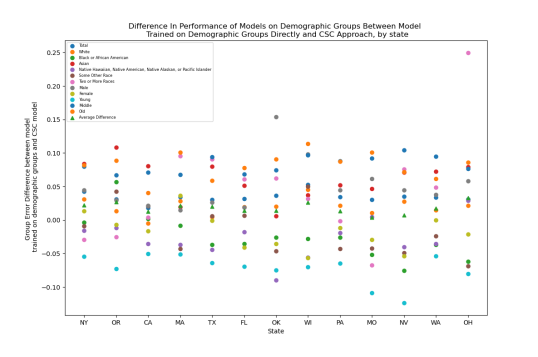

We applied the CSC approach to the ACS income task using Folktables datasets for thirteen different states in the year 2016. One interesting empirical phenomenon is the speed with which this approach converges, generally stopping after two to five rounds and not finding any further subgroup improvements to the current model. While the subgroups identified by the algorithm are not especially simple or interpretable (being defined by the minimum over two depth 7 regression trees), one way of understanding behavior and performance is by direct comparison of the test errors on the 11 basic demographic subgroups, which are available as features (along with various non-demographic features) to the regression trees. In Figure 6, we compare these subgroup test errors to those obtained by the simple sequential introduction of those subgroups discussed earlier. In the left panel, the axis represents each of the 11 subgroups, and the color coding of the points represents which of the 13 state datasets is considered. The values of the points measure the signed difference of the test errors of the CSC approach and the simple sequential approach (using a fixed ordering), with positive values being a win for sequential and negative values a win for CSC. The right panel visualizes the same data, but now grouped by states on the axis and with color coding for the groups.

The overarching message of the figure is that though CSC does not directly consider these subgroups, and instead optimizes for the complex subgroup giving the best weighted improvement to the overall error, it is nevertheless quite competitive on the simple subgroups, with the mass of points above and below being approximately the same. More specifically, averaged over all 143 state-group pairs, the average difference is 0.018, only a slight win for the sequential approach; and for 5 of the 11 groups (Black or African American, some other race, Native, female and young) the CSC averages are better. Combined with the very rapid convergence of CSC, we can thus view it as an approach that seeks rich subgroup optimization while providing strong basic demographic group performance “for free”. Further, combining the two approaches (e.g. running the CSC approach then sequentially introducing the basic groups) should only yield further improvement.

6 A Preliminary Deployment

We conclude by informally reporting findings from a preliminary deployment of our bias bounty framework to a group of 83 students divided into 36 teams in an undergraduate class on ethical algorithm design at the University of Pennsylvania in the Spring of 2022. In order to expedite this deployment in a limited time window, we made a few departures from the formal framework. First, we did not implement the adaptive data analysis mechanisms to prevent overfitting to the holdout set, but instead reported errors on the holdout set regardless of whether a proposed update is accepted or not. Second, in order to avoid the systems overhead of implementing a full client-server architecture and its potential security mechanisms, each team was instead given a self-contained notebook implementing both tools for finding pairs and the functionality for accepting updates and incorporating them into a revised decision list. Each notebook contained access to one of two Folktables datasets and classification tasks, which were divided roughly evenly between the teams. Students were told there were absolutely no constraints on the approaches they could take to finding improving pairs — they could do so by human intuition, manual exploratory data analysis, or they could entirely automate the process using ML or other techniques. They were generally encouraged to find as many accepted updates as they could during the duration of the deployment.

Despite the very preliminary nature of this exercise, a number of informal and high-level observations can nevertheless be made. First, despite wide variations in the quantitative backgrounds of the students (the only prerequisite to the course being exposure to introductory programming), virtually all of the most successful teams adopted hybrid approaches that involved some combination of manual or data-driven discovery of groups along with more automated means of finding , followed by training of on .

For instance, many groups automatically scanned through the feature space by column, or combinations of a small number of columns, to identify which values for each feature the current model performed poorly on, and then trained models on these subsets of the data. Note this has an advantage of interpretability over the groups generated by the algorithmic approaches developed in Section 4.2, as the groups are always explicit functions of categorical values over a small number of features (e.g. “Native American Women” or “Young Men”). However, this method is also restricted to tabular data that has a nicely structured feature space: if instead students were tasked with bias hunting over a collection of images, given only the input pixel matrix, such a strategy would not be sufficient.

Another notable feature of the exercise is that the purely algorithmic approaches appeared insufficient: groups who employed a combination of manual data analytics and algorithmic methods were able to bring errors down better than groups who employed purely algorithmic approaches similar to those in Section 4.2. This emphasizes the fact that there is really an advantage to doing a true deployment of such a system within a community, as opposed to attempting to automatically identify all issues.

Some detail on the efforts of one of the most successful teams is provided in Table 3, where for each successive pair accepted, we show an English description of the group, and indication of whether it was discovered by (A)utomated or (M)anual techniques, as well as the pre- and post-update group errors, the group weight, and the overall model error after each update. A number of observations are in order. First, in general the earlier groups discovered are simpler and often manually discovered, whereas the later ones tend to be more complex and automated. Indeed, the final group accepted is not even defined by features of the dataset at all, but rather is trained on the errors of the overall model. Second, echoing the increasing complexity and specificity of successive groups, we see that there are generally diminishing marginal returns in both the group weights and the reduction of overall model error. We might expect both increasing group complexity and diminishing returns to be general features of bias bounty events conducted under our particular algorithmic framework.

| Round | Group Description | Group Error Pre Update | Group Error Post Update | Group Error Improvement | Group Weight | Overall Model Error |

| 0 | 1.0000 | 0.2796 | ||||

| 1 | male sex (M) | 0.2866 | 0.1734 | 0.1133 | 0.5238 | 0.2203 |

| 2 | female sex (M) | 0.2719 | 0.1658 | 0.1061 | 0.4762 | 0.1698 |

| 3 | ages 17 to 24 and non-white (M) | 0.0447 | 0.0414 | 0.0032 | 0.0526 | 0.1696 |

| 4 | over the age of 30 working without pay in a family business (A) | 0.2258 | 0.1452 | 0.0806 | 0.0021 | 0.1694 |

| 5 | self-employed in own not incorporated business, professional practice, or farm (A) | 0.2255 | 0.2205 | 0.0050 | 0.0884 | 0.1690 |

| 6 | over the age of 62 (retired) (M) | 0.2322 | 0.2291 | 0.0031 | 0.1193 | 0.1686 |

| 7 | First-line supervisors of office and administrative support workers (A) | 0.3073 | 0.2661 | 0.0413 | 0.0074 | 0.1683 |

| 8 | real estate brokers and sales agents (A) | 0.3154 | 0.2905 | 0.0249 | 0.0082 | 0.1681 |

| 9 | first-line supervisors of retail sales workers (A) | 0.2583 | 0.2494 | 0.0088 | 0.0154 | 0.1680 |

| 10 | office clerks, general (A) | 0.2135 | 0.1842 | 0.0292 | 0.0117 | 0.1676 |

| 11 | paint, coating, and adhesive manufacturing (A) | 0.1713 | 0.1657 | 0.0055 | 0.0185 | 0.1675 |

| 12 | those born in California, Mexico, or Southeast Asia generally working as medical technicians (M) | 0.2126 | 0.2032 | 0.0094 | 0.0255 | 0.1671 |

| 13 | accountants/Auditors who work 40 hour work weeks (A) | 0.2883 | 0.2793 | 0.0090 | 0.0076 | 0.1671 |

| 14 | female sex secretaries and administrative assistants, except legal, medical, and executive (A) | 0.2586 | 0.2533 | 0.0053 | 0.0129 | 0.1670 |

| 15 | machine learning classifier over errors on current model (A) | 0.5600 | 0.3200 | 0.2400 | 0.0009 | 0.1668 |

Acknowledgements

We give warm thanks to Peter Hallinan, Pietro Perona and Alex Tolbert for many enlightening conversations at an early stage of this work, and to Bri Cervantes and Declan Harrison for providing details of their class bias bounty efforts, and permission to include them here.

References

- Agarwal et al. [2018] Alekh Agarwal, Alina Beygelzimer, Miroslav Dudík, John Langford, and Hanna Wallach. A reductions approach to fair classification. In International Conference on Machine Learning, pages 60–69. PMLR, 2018.

- Bassily et al. [2021] Raef Bassily, Kobbi Nissim, Adam Smith, Thomas Steinke, Uri Stemmer, and Jonathan Ullman. Algorithmic stability for adaptive data analysis. SIAM Journal on Computing, (0):STOC16–377, 2021.

- Blum and Hardt [2015] Avrim Blum and Moritz Hardt. The ladder: A reliable leaderboard for machine learning competitions. In International Conference on Machine Learning, pages 1006–1014. PMLR, 2015.

- Blum and Lykouris [2020] Avrim Blum and Thodoris Lykouris. Advancing subgroup fairness via sleeping experts. In Innovations in Theoretical Computer Science Conference (ITCS), volume 11, 2020.

- Blum and Stangl [2019] Avrim Blum and Kevin Stangl. Recovering from biased data: Can fairness constraints improve accuracy? arXiv preprint arXiv:1912.01094, 2019.

- Chowdhury and Williams [2021] Rumman Chowdhury and Jutta Williams. Introducing twitter’s first algorithmic bias bounty challenge. https://blog.twitter.com/engineering/en_us/ topics/insights/2021/algorithmic-bias-bounty-challenge, 2021.

- Diana et al. [2021a] Emily Diana, Wesley Gill, Ira Globus-Harris, Michael Kearns, Aaron Roth, and Saeed Sharifi-Malvajerdi. Lexicographically fair learning: Algorithms and generalization. In 2nd Symposium on Foundations of Responsible Computing (FORC 2021). Schloss Dagstuhl-Leibniz-Zentrum für Informatik, 2021a.

- Diana et al. [2021b] Emily Diana, Wesley Gill, Michael Kearns, Krishnaram Kenthapadi, and Aaron Roth. Minimax group fairness: Algorithms and experiments. In Proceedings of the 2021 AAAI/ACM Conference on AI, Ethics, and Society, pages 66–76, 2021b.

- Ding et al. [2021] Frances Ding, Moritz Hardt, John Miller, and Ludwig Schmidt. Retiring adult: New datasets for fair machine learning. arXiv preprint arXiv:2108.04884, 2021.

- Dutta et al. [2020] Sanghamitra Dutta, Dennis Wei, Hazar Yueksel, Pin-Yu Chen, Sijia Liu, and Kush Varshney. Is there a trade-off between fairness and accuracy? a perspective using mismatched hypothesis testing. In International Conference on Machine Learning, pages 2803–2813. PMLR, 2020.

- Dwork et al. [2012] Cynthia Dwork, Moritz Hardt, Toniann Pitassi, Omer Reingold, and Richard Zemel. Fairness through awareness. In Proceedings of the 3rd innovations in theoretical computer science conference, pages 214–226, 2012.

- Dwork et al. [2015a] Cynthia Dwork, Vitaly Feldman, Moritz Hardt, Toniann Pitassi, Omer Reingold, and Aaron Roth. The reusable holdout: Preserving validity in adaptive data analysis. Science, 349(6248):636–638, 2015a.

- Dwork et al. [2015b] Cynthia Dwork, Vitaly Feldman, Moritz Hardt, Toniann Pitassi, Omer Reingold, and Aaron Roth. Generalization in adaptive data analysis and holdout reuse. In NIPS, 2015b.

- Dwork et al. [2015c] Cynthia Dwork, Vitaly Feldman, Moritz Hardt, Toniann Pitassi, Omer Reingold, and Aaron Leon Roth. Preserving statistical validity in adaptive data analysis. In Proceedings of the forty-seventh annual ACM symposium on Theory of computing, pages 117–126, 2015c.

- Dwork et al. [2021] Cynthia Dwork, Michael P Kim, Omer Reingold, Guy N Rothblum, and Gal Yona. Outcome indistinguishability. In Proceedings of the 53rd Annual ACM SIGACT Symposium on Theory of Computing, pages 1095–1108, 2021.

- Gebru et al. [2021] Timnit Gebru, Jamie Morgenstern, Briana Vecchione, Jennifer Wortman Vaughan, Hanna Wallach, Hal Daumé Iii, and Kate Crawford. Datasheets for datasets. Communications of the ACM, 64(12):86–92, 2021.

- Gupta et al. [2021] Varun Gupta, Christopher Jung, Georgy Noarov, Mallesh M Pai, and Aaron Roth. Online multivalid learning: Means, moments, and prediction intervals. arXiv preprint arXiv:2101.01739, 2021.

- Hardt et al. [2016] Moritz Hardt, Eric Price, and Nati Srebro. Equality of opportunity in supervised learning. Advances in neural information processing systems, 29:3315–3323, 2016.

- Hébert-Johnson et al. [2018] Ursula Hébert-Johnson, Michael Kim, Omer Reingold, and Guy Rothblum. Multicalibration: Calibration for the (computationally-identifiable) masses. In International Conference on Machine Learning, pages 1939–1948. PMLR, 2018.

- Ilvento [2020] Christina Ilvento. Metric learning for individual fairness. In 1st Symposium on Foundations of Responsible Computing (FORC 2020). Schloss Dagstuhl-Leibniz-Zentrum für Informatik, 2020.

- Jung et al. [2019] Christopher Jung, Michael Kearns, Seth Neel, Aaron Roth, Logan Stapleton, and Zhiwei Steven Wu. An algorithmic framework for fairness elicitation. arXiv e-prints, pages arXiv–1905, 2019.