Linear Laws of Markov Chains with an Application for Anomaly Detection in Bitcoin Prices

Abstract

The goals of this paper are twofold: (1) to present a new method that is able to find linear laws governing the time evolution of Markov chains and (2) to apply this method for anomaly detection in Bitcoin prices. To accomplish these goals, first, the linear laws of Markov chains are derived by using the time embedding of their (categorical) autocorrelation function. Then, a binary series is generated from the first difference of Bitcoin exchange rate (against the United States Dollar). Finally, the minimum number of parameters describing the linear laws of this series is identified through stepped time windows. Based on the results, linear laws typically became more complex (containing an additional third parameter that indicates hidden Markov property) in two periods: before the crash of cryptocurrency markets inducted by the COVID-19 pandemic (12 March 2020), and before the record-breaking surge in the price of Bitcoin (Q4 2020 – Q1 2021). In addition, the locally high values of this third parameter are often related to short-term price peaks, which suggests price manipulation.

keywords:

Markov chain, Linear law, Anomaly detection, Bitcoin, CryptocurrencyIntroduction

The hidden Markov model [1, 2, 3, 4] is a stochastic approach that captures hidden information from observable random variables. As an extension of Markov models, it can be characterized by two stochastic processes: an unobserved Markov chain and an observed sequence that depends only on the current state of the aforementioned Markovian (memoryless) process [5]. Its objective is to estimate the hidden sequence of states that provides the best statistical explanation of the observed data [4]. The concept of hidden Markov models has been successfully employed in a variety of areas such as speech [6, 7, 8], gesture [9, 10, 11], and text recognition [12, 13, 14], bioinformatics [15, 16, 17, 18, 19, 20], signal processing [21, 22, 23], and finance [24, 25, 26, 27].

Among the recent financial applications, hidden Markov models have been used to understand the behavior of the decentralized, loosely regulated [28], and highly speculative [29] market of cryptocurrencies. From these studies, Giudici and Abu Hashish (2020) [30] investigated how the prices of Bitcoin [31] switch between “bear,” “stable,” and “bull” regimes. Koki et al. (2022) [32] modeled the return series of the three highest capitalization cryptocurrencies, Bitcoin, Ether[33] and Ripple [34]. Similarly to the results of Giudici and Abu Hashish (2020) [30], they found that the hidden Markov framework distinguished "bear", "stable" and "bull" regimes for the Bitcoin series, while, in the case of the Ether and Ripple, it separated periods with different profit and risk magnitudes. Finally, Kim et al. (2021) [35] used the hidden Markov model to examine how cryptocurrency markets behave and react to social sentiment under various regimes.

Similar to the behavior of the crypto market, increasing attention has been paid to detecting and understanding its anomalies. Some of these works were focused on the anomalies of the underlying blockchain transaction network [36, 37, 38, 39, 40, 41]. Others employed social media data [42, 43, 44, 45, 46] or directly investigated the price anomalies of various cryptocurrencies [47]. A common cause of these anomalies is the so-called pump-and-dump price manipulation, in which scammers lure traders to buy a cryptocurrency at an artificially inflated price (pump), then quickly sell their previous holdings to profit (dump) [46]. According to Li et al. (2021)[48], pump-and-dump activities lead to short-term bubbles featuring dramatic increases in prices, volume, and volatility. Prices peak within minutes, followed by quick reversals. In contrast with Li et al. (2021)[48], Hamrick et al. (2021)[49] investigated long-term (so-called target-based) pump-and-dump schemes, in which pump signals do not reach a buy target until days or even weeks.

In this paper, (1) we present a new method that is able to find linear laws governing the time evolution of Markov chains, then (2) we apply this method for anomaly detection in Bitcoin prices. To this end, we first derive the linear laws of Markov chains by using the time embedding of their (categorical) autocorrelation function. At this point, we rely on Jakovác’s (2020, 2021)[50, 51] ideas on linear laws as well as the time-delay embedding method proposed by Takens (1981)[52] and used in various fields, such as dimensional causality analysis[53, 54, 55, 56, 57] and anomaly detection[58]. As a next step, we generate a binary series from the first difference of Bitcoin exchange rate (against the United States Dollar). Finally, we identify the minimum number of parameters describing the linear laws of this series through stepped time windows. Based on our results, linear laws typically became more complex (containing an additional third parameter that indicates hidden Markov property) in two periods: before the crash of cryptocurrency markets inducted by the COVID-19 pandemic (12 March 2020), and before the record-breaking surge in the price of Bitcoin (Q4 2020 – Q1 2021). In addition, the locally high values of this third parameter are often related to short-term price peaks, which suggests price manipulation.

The paper is organized as follows. The linear laws of Markov chains are formulated in the Methods section. This is followed by the Results and Discussions section, which first demonstrates how linear laws are able to indicate the hidden Markov property of a series. Then, it presents and discusses the results of anomaly detection in Bitcoin prices. The paper ends with the Conclusions and Future Work section, which provides the conclusions and suggests future research directions.

Methods

Finding linear laws in Markov chains

Markov chains are random processes, where the next element depends only on the present one, and not on the previous ones. Let us denote by the conditional probability to find in the -th step , where is a vector space, and is some condition. In a causal process, the condition can be all the history, but in Markov processes it simplifies:

| (1) |

This can be treated as a matrix if the range in is discrete. In the following we assume that there is no dependence (time translation symmetry), and we denote . The matrix is used to call the transfer matrix. means the probability of the transfer .

Since the elements of are probabilities, must be true. Moreover, from the state we arrive to some state with probability one, thus we find:

| (2) |

the sum of each column is one. This means that the vector is a left eigenvector with eigenvalue one, . Because the spectrum is the same for left and right eigenvectors, there is a eigenvalue in the spectrum.

If we know the probability distribution after the -th step to be , then the probability distribution after the -th step is:

| (3) |

This follows, after generalization:

| (4) |

Equilibrium distribution, denoted simply by is invariant under the time translation, i.e.:

| (5) |

it is the right eigenvector of the transfer matrix with eigenvalue.

With the help of the transfer matrix we can calculate the expected value of any function as (assume ):

| (6) |

We remark that this formula in the continuous case is called path integral.

In particular, we may consider the expected value of a function of two variables:

| (7) |

where means trace and the matrix reads:

| (8) |

As we see, for the two-variable case, the and dependence factorizes. We will consider long-time behavior, where is the equilibrium distribution. The result is independent of , so we may omit this variable.

After we diagonalized the transfer matrix:

| (9) |

We find for :

| (10) |

where:

| (11) |

This means that is in general a sum of geometric series, and the number of terms is equal to the number of possible states.

For this special class of series we may look for a linear law in the form:

| (12) |

This is possible if:

| (13) |

Therefore we need:

| (14) |

i.e., we seek those polynomials, whose roots are the eigenvalues of the transfer matrix. But we know such a polynomial, the equation which determines the eigenvalues, i.e., the characteristic equation for the transfer matrix:

| (15) |

This means that the expected value of any function of two variables, , satisfies a linear law for Markov processes. The coefficients of the linear law (defined by Eq. (14)) are equal to the coefficients of the characteristic polynomial of the transfer matrix, while its roots are the eigenvalues of the transfer matrix. This means that by inspecting the embedding of function we can also determine the eigenvalues of the transfer matrix.

We emphasize that the above conclusion is true for arbitrary function of two variables. In particular we may use , where is the first component of the vector. Put another way, if we observe only a subprocess, we can determine the eigenvalues of the transfer matrix of the complete process.

Case of binary Markov chains

The simplest case is the binary Markov chain, where . The transfer matrix is a matrix. Since the sum of all columns is one, thus it contains two parameters:

| (16) |

Here is the probability of , is the probability of . The equilibrium distribution:

| (17) |

The characteristic polynomial of is:

| (20) | |||

| (21) |

The two eigenvalues are and . Both are real, but not necessarily positive. The corresponding right eigenvectors are:

| (22) |

The left eigenvectors are:

| (23) |

We find:

| (24) |

As an example we may consider the function, i.e., we count the cases where . This is the most appropriate choice for categorical variables. We find:

| (25) |

therefore:

| (26) |

The characteristic polynomial of the transfer matrix is:

| (27) |

Thus, as it is easy to check also directly, our expression satisfies the linear law:

| (28) |

In a real system we observe , and produce the matrix:

| (29) |

We seek that satisfies:

| (30) |

Multiplying this with we get:

| (31) |

This means exactly that , which is a matrix, has a zero eigenvalue. Then is the corresponding eigenvector.

We remark that the 2-state Markov chain can be written in a Langevin equation form as:

| (32) |

where with uniform distribution, and "int" means integer part. As it is easy to check, the above formula yields if it was true for , and the transfer matrix is exactly the same as shown in the Eq. (16).

Results and Discussion

Detection of Hidden Markov Property

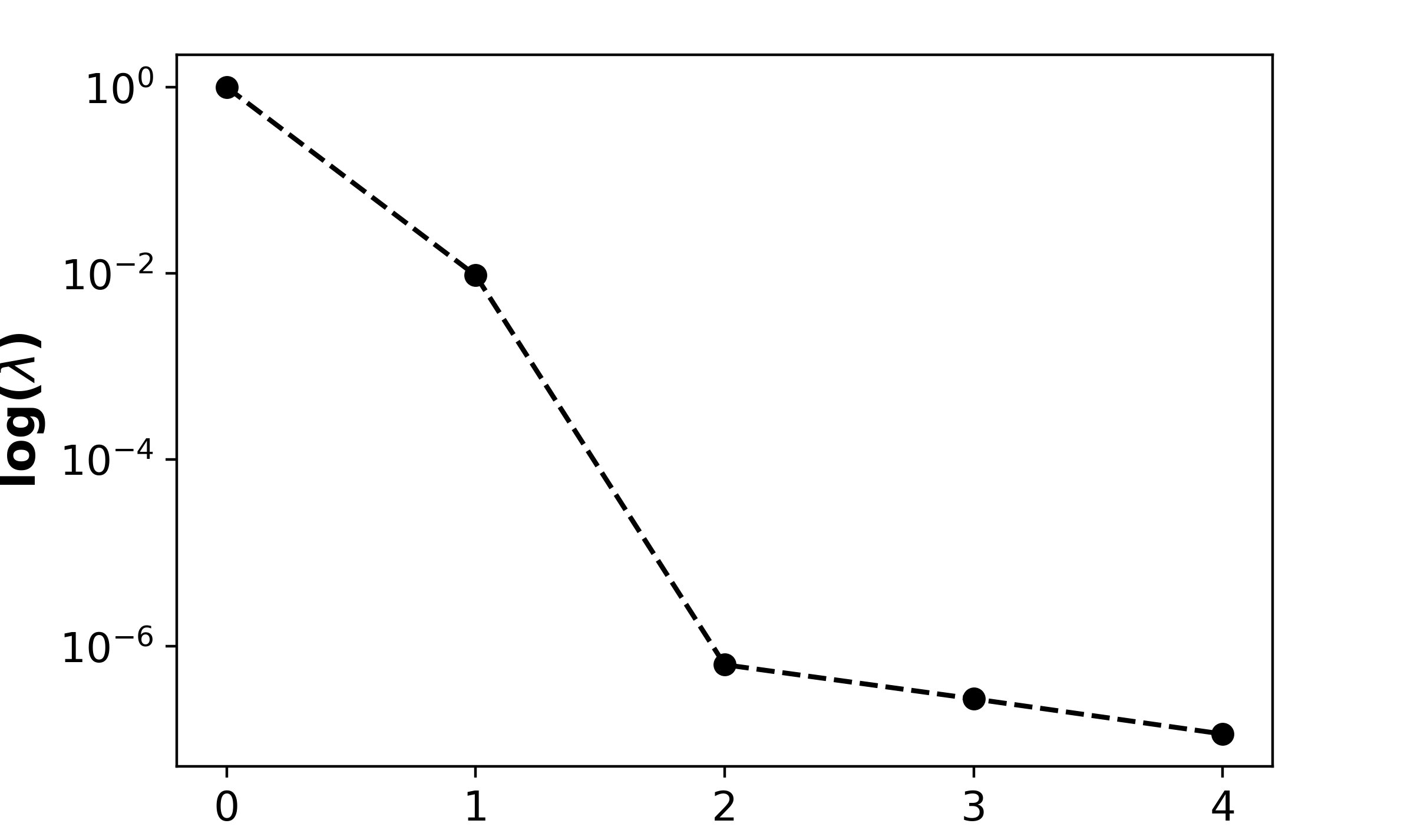

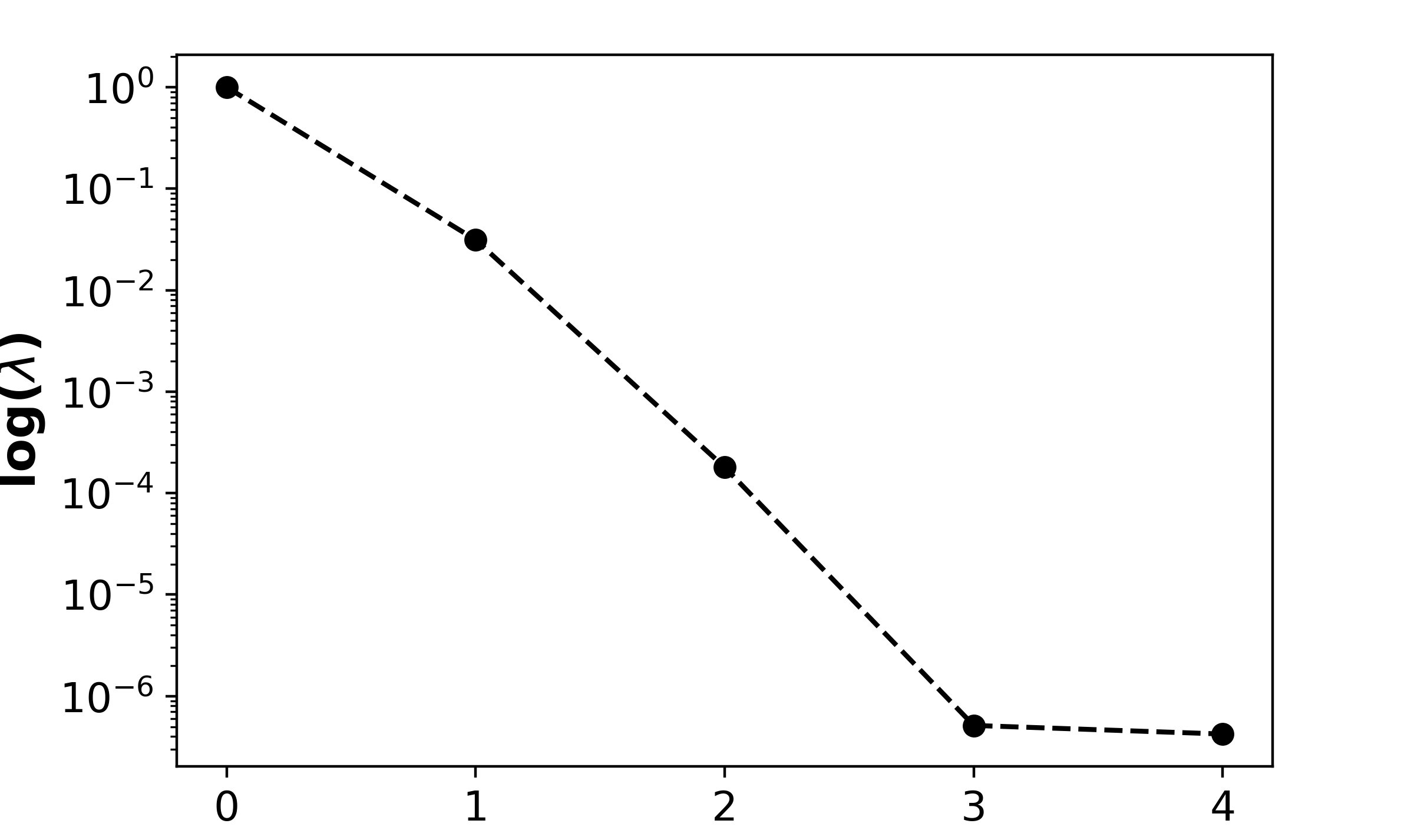

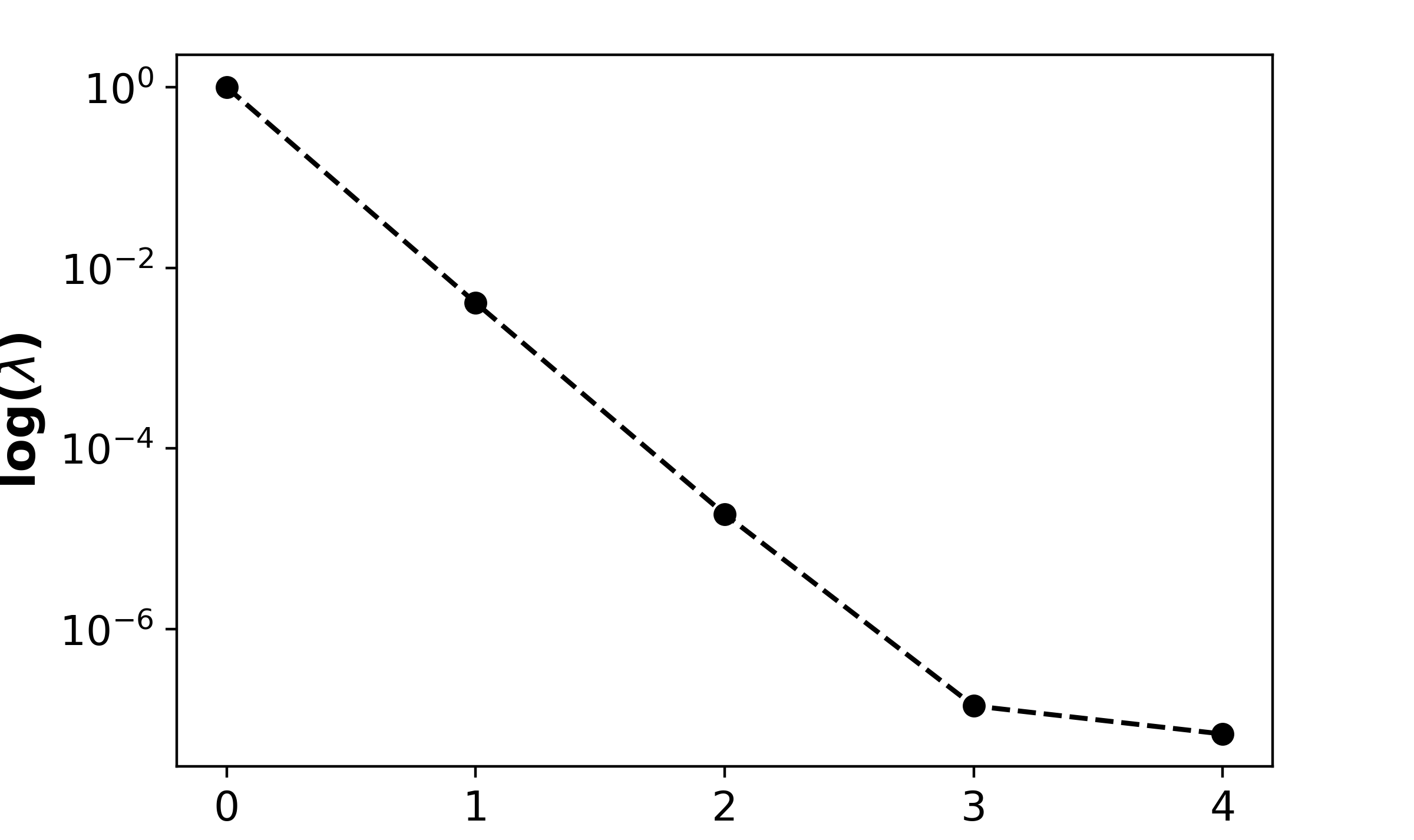

In this subsection, we demonstrate how the proposed method reveals the hidden Markov property of a simulated process, through the example of three simulated series. First, a -length binary Markov chain () is simulated by using the following (randomly generated) transfer matrix ():

| (33) |

and as initial state. Then, we generate an other -length Markov process () with states based on the following (random) transfer matrix ():

| (34) |

and initial state. The left bit of this process forms a separate binary series () with initial state. Applying Eqs. (16) – (31) to , , and , the eigenvalues of the given matrices are determined. These eigenvalues (contained by , , and ) are illustrated in Fig. 1.

The difference between and suggests that although both and are binary processes (), unlike , cannot be characterized by two parameters (see and in Eq. (16)). In other words, it is only the part of the Markov process of similar complexity (cf. and in Fig. 1). This phenomenon refers to the hidden Markov property of the series.

Anomaly detection in Bitcoin prices

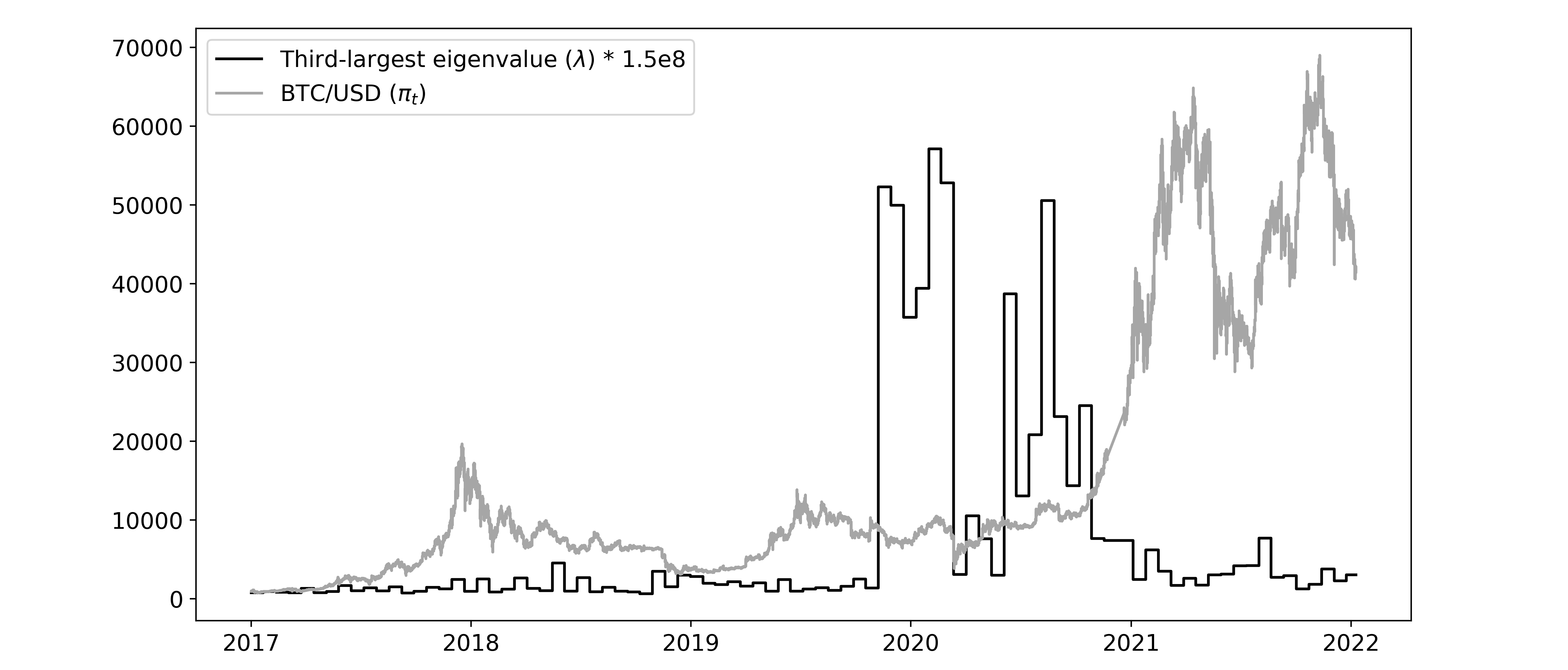

We first generate a binary series () from the first difference of Bitcoin exchange rate (against the United States Dollar) as follows:

| (35) |

where is the closing price of Bitcoin in time . Similar to Phaladisailoed and Numnonda (2018)[59], Kavitha et al. (2020)[60], and Passalis et al. (2021)[61], we use the 1-minute interval price data of Bitstamp (collected from: https://www.cryptodatadownload.com/, retrieved: 9 January 2022) during the calculations. The employed dataset contains price data (at a missing value rate of ) between 1 January 2017 00:01:00 GMT and 9 January 2022 07:16:00 GMT ().

As a next step, the studied time horizon is divided into 30 000-width time windows (i.e., the first time window contains price data from to ). Then, by applying Eqs. (16) – (31) to , the eigenvalues of matrices are determined for each time window. As discussed in the previous section, the magnitude of the third-largest eigenvalue can indicate that two parameters (see and in Eq. (16)) are not sufficient to describe the observed binary series. Following this logic, Fig. 2 illustrates the third-largest eigenvalues determined in each time window.

Based on the results, the examined eigenvalues are remarkably high in two periods: before the crash of cryptocurrency markets inducted by the COVID-19 pandemic (12 March 2020), and before the record-breaking surge in the price of Bitcoin (Q4 2020 – Q1 2021). Although it is difficult to determine the reasons for this phenomenon, it is striking that most of the locally high eigenvalues are related to a short-term price peak. Thus, a possible explanation is that intensive pump-and-dump activities artificially manipulate Bitcoin prices and permanently change its evolution over time. This is also supported by the fact that the anomaly disappeared immediately after the collapse of Bitcoin prices (12 March 2020), and reappeared only after the uncertainty caused by COVID-19 decreased (June 2020).

Conclusions and Future Work

This paper presented a new method that is able to find linear laws governing the time evolution of Markov chains by using the time embedding of their (categorical) autocorrelation function. As an application, we investigated the linear laws of the 1-minute interval price data of Bitcoin between 1 January 2017 00:01:00 GMT and 9 January 2022 07:16:00 GMT. To this, first, a binary Markov series was generated from the first difference of the exchange rate of Bitcoin (against the United States Dollar). Then, the minimum number of parameters describing the linear laws of this series was identified through stepped time windows.

Our investigation demonstrated promising results on the detection of Bitcoin anomalies. Based on our findings, linear laws typically became more complex (containing an additional third parameter that indicates hidden Markov property) in two periods: before the crash of cryptocurrency markets inducted by the COVID-19 pandemic (12 March 2020), and before the record-breaking surge in the price of Bitcoin (Q4 2020 – Q1 2021). In addition, the locally high values of this third parameter are often related to short-term price peaks, which suggests price manipulation.

In our future work, we will examine the linear laws in exchange rates of other cryptocurrencies, as well as stock prices and the prices of oil and other commodities. Although due to the theory of efficient market hypothesis[62], financial data typically fit well with the concept of Markov chains, we also plan to investigate electroencephalograms (EEGs) record neural activity to detect epilepsy.

References

- [1] Baum, L. E. & Petrie, T. Statistical inference for probabilistic functions of finite state markov chains. \JournalTitleThe annals of mathematical statistics 37, 1554–1563 (1966).

- [2] Baum, L. E., Petrie, T., Soules, G. & Weiss, N. A maximization technique occurring in the statistical analysis of probabilistic functions of markov chains. \JournalTitleThe annals of mathematical statistics 41, 164–171 (1970).

- [3] Baum, L. E. et al. An inequality and associated maximization technique in statistical estimation for probabilistic functions of markov processes. \JournalTitleInequalities 3, 1–8 (1972).

- [4] Rabiner, L. R. A tutorial on hidden markov models and selected applications in speech recognition. \JournalTitleProceedings of the IEEE 77, 257–286 (1989).

- [5] Danisman, O. & Kocer, U. U. Hidden markov models with binary dependence. \JournalTitlePhysica A: Statistical Mechanics and its Applications 567, 125668 (2021).

- [6] Kayte, S., Mundada, M. & Gujrathi, J. Hidden markov model based speech synthesis: A review. \JournalTitleInternational Journal of Computer Applications 130, 35–39 (2015).

- [7] Muhammad, H. Z., Nasrun, M., Setianingsih, C. & Murti, M. A. Speech recognition for english to indonesian translator using hidden markov model. In 2018 International Conference on Signals and Systems (ICSigSys), 255–260 (IEEE, 2018).

- [8] Mustafa, M. K., Allen, T. & Appiah, K. A comparative review of dynamic neural networks and hidden markov model methods for mobile on-device speech recognition. \JournalTitleNeural Computing and applications 31, 891–899 (2019).

- [9] Presti, L. L., La Cascia, M., Sclaroff, S. & Camps, O. Gesture modeling by hanklet-based hidden markov model. In Asian Conference on Computer Vision, 529–546 (Springer, 2014).

- [10] Sagayam, K. M. & Hemanth, D. J. Abc algorithm based optimization of 1-d hidden markov model for hand gesture recognition applications. \JournalTitleComputers in Industry 99, 313–323 (2018).

- [11] Sagayam, K. M. & Hemanth, D. J. A probabilistic model for state sequence analysis in hidden markov model for hand gesture recognition. \JournalTitleComputational Intelligence 35, 59–81 (2019).

- [12] Du, J., Wang, Z.-R., Zhai, J.-F. & Hu, J.-S. Deep neural network based hidden markov model for offline handwritten chinese text recognition. In 2016 23rd International Conference on Pattern Recognition (ICPR), 3428–3433 (IEEE, 2016).

- [13] Wang, Z.-R., Du, J., Wang, W.-C., Zhai, J.-F. & Hu, J.-S. A comprehensive study of hybrid neural network hidden markov model for offline handwritten chinese text recognition. \JournalTitleInternational Journal on Document Analysis and Recognition (IJDAR) 21, 241–251 (2018).

- [14] Shen, V. R., Chiou, G.-J., Lin, Y.-N. & Jhan, J.-Y. Novel text recognition based on modified k-clustering and hidden markov models. \JournalTitleWireless Personal Communications 111, 1453–1474 (2020).

- [15] Marco, E. et al. Multi-scale chromatin state annotation using a hierarchical hidden markov model. \JournalTitleNature communications 8, 1–9 (2017).

- [16] Manogaran, G. et al. Machine learning based big data processing framework for cancer diagnosis using hidden markov model and gm clustering. \JournalTitleWireless personal communications 102, 2099–2116 (2018).

- [17] Benelli, M. et al. Charting differentially methylated regions in cancer with rocker-meth. \JournalTitleCommunications biology 4, 1–15 (2021).

- [18] Emdadi, A. & Eslahchi, C. Auto-hmm-lmf: feature selection based method for prediction of drug response via autoencoder and hidden markov model. \JournalTitleBMC bioinformatics 22, 1–22 (2021).

- [19] Porter, T. M. & Hajibabaei, M. Profile hidden markov model sequence analysis can help remove putative pseudogenes from dna barcoding and metabarcoding datasets. \JournalTitleBMC bioinformatics 22, 1–20 (2021).

- [20] Tang, Y. et al. Quantifying information accumulation encoded in the dynamics of biochemical signaling. \JournalTitleNature communications 12, 1–10 (2021).

- [21] Zhou, H., Chen, J., Dong, G. & Wang, R. Detection and diagnosis of bearing faults using shift-invariant dictionary learning and hidden markov model. \JournalTitleMechanical systems and signal processing 72, 65–79 (2016).

- [22] Yuwono, M. et al. Automatic bearing fault diagnosis using particle swarm clustering and hidden markov model. \JournalTitleEngineering Applications of Artificial Intelligence 47, 88–100 (2016).

- [23] Cai, Y., Shi, X., Shao, H., Wang, R. & Liao, S. Energy efficiency state identification in milling processes based on information reasoning and hidden markov model. \JournalTitleJournal of Cleaner Production 193, 397–413 (2018).

- [24] Cao, Y., Li, Y., Coleman, S., Belatreche, A. & McGinnity, T. M. Adaptive hidden markov model with anomaly states for price manipulation detection. \JournalTitleIEEE transactions on neural networks and learning systems 26, 318–330 (2014).

- [25] Nguyen, N. Hidden markov model for stock trading. \JournalTitleInternational Journal of Financial Studies 6, 36 (2018).

- [26] Zhang, M., Jiang, X., Fang, Z., Zeng, Y. & Xu, K. High-order hidden markov model for trend prediction in financial time series. \JournalTitlePhysica A: Statistical Mechanics and its Applications 517, 1–12 (2019).

- [27] Zheng, K., Li, Y. & Xu, W. Regime switching model estimation: spectral clustering hidden markov model. \JournalTitleAnnals of Operations Research 303, 297–319 (2021).

- [28] La Morgia, M., Mei, A., Sassi, F. & Stefa, J. The doge of wall street: Analysis and detection of pump and dump cryptocurrency manipulations. \JournalTitlearXiv preprint arXiv:2105.00733 (2021).

- [29] Malladi, R. K. & Dheeriya, P. L. Time series analysis of cryptocurrency returns and volatilities. \JournalTitleJournal of Economics and Finance 45, 75–94 (2021).

- [30] Giudici, P. & Abu Hashish, I. A hidden markov model to detect regime changes in cryptoasset markets. \JournalTitleQuality and Reliability Engineering International 36, 2057–2065 (2020).

- [31] Nakamoto, S. Bitcoin: A peer-to-peer electronic cash system. \JournalTitleDecentralized Business Review 21260 (2008).

- [32] Koki, C., Leonardos, S. & Piliouras, G. Exploring the predictability of cryptocurrencies via bayesian hidden markov models. \JournalTitleResearch in International Business and Finance 59, 101554 (2022).

- [33] Buterin, V. et al. Ethereum white paper. \JournalTitleGitHub repository 1, 22–23 (2013).

- [34] Schwartz, D., Youngs, N., Britto, A. et al. The ripple protocol consensus algorithm. \JournalTitleRipple Labs Inc White Paper 5, 151 (2014).

- [35] Kim, K., Lee, S.-Y. T. & Assar, S. The dynamics of cryptocurrency market behavior: sentiment analysis using markov chains. \JournalTitleIndustrial Management & Data Systems (2021).

- [36] Monamo, P., Marivate, V. & Twala, B. Unsupervised learning for robust bitcoin fraud detection. In 2016 Information Security for South Africa (ISSA), 129–134 (IEEE, 2016).

- [37] Dixon, M. F., Akcora, C. G., Gel, Y. R. & Kantarcioglu, M. Blockchain analytics for intraday financial risk modeling. \JournalTitleDigital Finance 1, 67–89 (2019).

- [38] Akcora, C. G., Li, Y., Gel, Y. R. & Kantarcioglu, M. Bitcoinheist: Topological data analysis for ransomware prediction on the bitcoin blockchain. In Proceedings of the twenty-ninth international joint conference on artificial intelligence (2020).

- [39] Li, Y. et al. Dissecting ethereum blockchain analytics: What we learn from topology and geometry of the ethereum graph? In Proceedings of the 2020 SIAM International Conference on Data Mining, 523–531 (SIAM, 2020).

- [40] Hassan, M. U., Rehmani, M. H. & Chen, J. Anomaly detection in blockchain networks: A comprehensive survey. \JournalTitlearXiv preprint arXiv:2112.06089 (2021).

- [41] Ofori-Boateng, D., Dominguez, I. S., Kantarcioglu, M., Akcora, C. G. & Gel, Y. R. Topological anomaly detection in dynamic multilayer blockchain networks. \JournalTitlearXiv preprint arXiv:2106.01806 (2021).

- [42] Phillips, R. C. & Gorse, D. Predicting cryptocurrency price bubbles using social media data and epidemic modelling. In 2017 IEEE symposium series on computational intelligence (SSCI), 1–7 (IEEE, 2017).

- [43] Victor, F. & Hagemann, T. Cryptocurrency pump and dump schemes: Quantification and detection. In 2019 International Conference on Data Mining Workshops (ICDMW), 244–251 (IEEE, 2019).

- [44] Nizzoli, L. et al. Charting the landscape of online cryptocurrency manipulation. \JournalTitleIEEE Access 8, 113230–113245 (2020).

- [45] Mirtaheri, M., Abu-El-Haija, S., Morstatter, F., Ver Steeg, G. & Galstyan, A. Identifying and analyzing cryptocurrency manipulations in social media. \JournalTitleIEEE Transactions on Computational Social Systems 8, 607–617 (2021).

- [46] Nghiem, H., Muric, G., Morstatter, F. & Ferrara, E. Detecting cryptocurrency pump-and-dump frauds using market and social signals. \JournalTitleExpert Systems with Applications 115284 (2021).

- [47] Kamps, J. & Kleinberg, B. To the moon: defining and detecting cryptocurrency pump-and-dumps. \JournalTitleCrime Science 7, 1–18 (2018).

- [48] Li, T., Shin, D. & Wang, B. Cryptocurrency pump-and-dump schemes. \JournalTitleAvailable at SSRN 3267041 (2021).

- [49] Hamrick, J. et al. Analyzing target-based cryptocurrency pump and dump schemes. In Proceedings of the 2021 ACM CCS Workshop on Decentralized Finance and Security, 21–27 (2021).

- [50] Jakovac, A., Berenyi, D. & Posfay, P. Understanding understanding: a renormalization group inspired model of (artificial) intelligence. \JournalTitlearXiv preprint arXiv:2010.13482 (2020).

- [51] Jakovac, A. Time series analysis with dynamic law exploration. \JournalTitlearXiv preprint arXiv:2104.10970 (2021).

- [52] Takens, F. Dynamical systems and turbulence, eds. rand, da & young, l.-s. \JournalTitleLecture Notes in Mathematics 898, 366 (1981).

- [53] Benko, Z. et al. Exact inference of causal relations in dynamical systems. \JournalTitlearXiv preprint arXiv:1808.10806 (2018).

- [54] Benkő, Z. et al. Inferring causal relations between neurophysiological signals with dimensional causality. \JournalTitleIBRO Reports 6, S135 (2019).

- [55] Benkő, Z. et al. Causal relationship between local field potential and intrinsic optical signal in epileptiform activity in vitro. \JournalTitleScientific reports 9, 1–12 (2019).

- [56] Zlatniczki, Á., Stippinger, M., Benkő, Z., Somogyvári, Z. & Telcs, A. Relaxation of some confusions about confounders. \JournalTitleEntropy 23, 1450 (2021).

- [57] Benkő, Z. et al. Manifold-adaptive dimension estimation revisited. \JournalTitlePeerJ Computer Science 8, e790 (2022).

- [58] Benkő, Z., Bábel, T. & Somogyvári, Z. Model-free detection of unique events in time series. \JournalTitleScientific reports 12, 1–17 (2022).

- [59] Phaladisailoed, T. & Numnonda, T. Machine learning models comparison for bitcoin price prediction. In 2018 10th International Conference on Information Technology and Electrical Engineering (ICITEE), 506–511 (IEEE, 2018).

- [60] Kavitha, H., Sinha, U. K. & Jain, S. S. Performance evaluation of machine learning algorithms for bitcoin price prediction. In 2020 Fourth International Conference on Inventive Systems and Control (ICISC), 110–114 (IEEE, 2020).

- [61] Passalis, N., Kanniainen, J., Gabbouj, M., Iosifidis, A. & Tefas, A. Forecasting financial time series using robust deep adaptive input normalization. \JournalTitleJournal of Signal Processing Systems 1–17 (2021).

- [62] Fama, E. F. Efficient capital markets: A review of theory and empirical work. \JournalTitleThe Journal of Finance 25, 383–417 (1970).

Acknowledgements

The authors would like to thank András Telcs (Wigner Research Centre for Physics, Budapest) and Zoltán Somogyvári (Wigner Research Centre for Physics, Budapest) for their valuable comments and suggestions. The authors thank the support of Eötvös Loránd Research Network. The research was supported by the Ministry of Innovation and Technology NRDI Office within the framework of the MILAB Artificial Intelligence National Laboratory Program. A.J. had a support from the Hungarian Research Fund NKFIH (OTKA) under contract No. K123815.

Author contributions statement

A.J., P.P., and M.T.K. conceptualized the work and contributed to the writing and editing of the manuscript. M.T.K. acquired the data and conducted the analysis. A.J. supervised the research.

Competing interests

The authors declare no competing interests.