Using Joint Random Partition Models for Flexible Change Point Analysis in Multivariate Processes

Abstract

Change point analyses are concerned with identifying positions of an ordered stochastic process that undergo abrupt local changes of some underlying distribution. When multiple processes are observed, it is often the case that information regarding the change point positions is shared across the different processes. This work describes a method that takes advantage of this type of information. Since the number and position of change points can be described through a partition with contiguous clusters, our approach develops a joint model for these types of partitions. We describe computational strategies associated with our approach and illustrate improved performance in detecting change points through a small simulation study. We then apply our method to a financial data set of emerging markets in Latin America and highlight interesting insights discovered due to the correlation between change point locations among these economies.

Key words: correlated random partitions, multiple change point analysis, multivariate time series.

1 Introduction

Change point analyses identify times or positions of an ordered stochastic process that undergo abrupt local changes. These abrupt changes are typically seen as shifts in expectation, variability, or shape of an underlying distribution (or some combination of the three). Methods that detect change points have been employed in a variety of fields, including finance (Wood et al., 2021), climatology (Gupta et al., 2021), and ecology (Jones et al., 2021) to name a few. Due to this, many change point methods have been proposed in the statistical literature both in a univariate (see for example Arellano-Valle et al., 2013) and a multivariate setting (see Truong et al., 2020, for a comprehensive review).

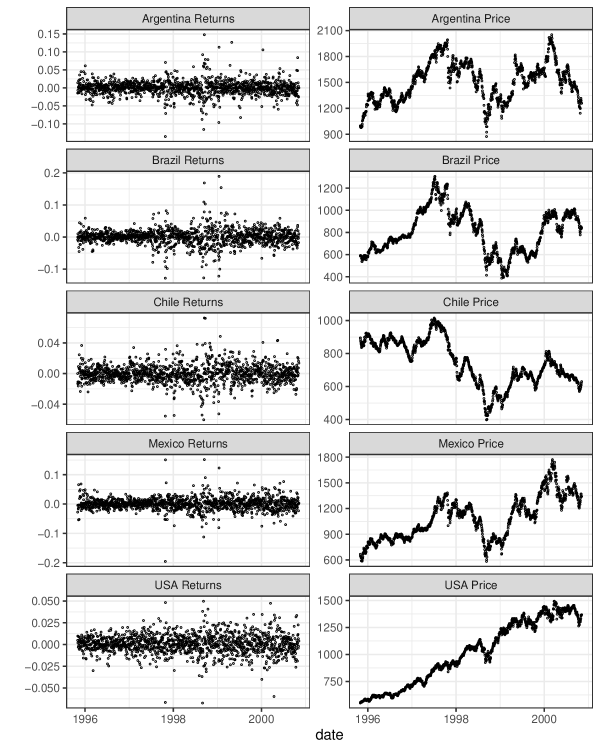

The phenomenon that motivates our research is the so-called financial contagion or simply contagion. This phenomenon can be understood as the spread of financial crises from one country to another (see for example Lowell et al., 1998; Valdés, 2000; de P. Filleti et al., 2008, among others). To illustrate contagion consider the price and returns of the five markets displayed in Figure 1. Note that the overall trend of the price in the Latin American markets (Argentina, Brazil, Chile, and Mexico) seem to coincide. However, the USA market (Dow Jones index) presents a different trend during the same observation period (1995 to 2001). It is important to note that, in the second half of 1998, Dow Jones suffered a slight crash (a change in volatility according to Figure 1, left column) due to the Russian financial crisis and the Long Term Capital Management episode. Consequently, we hypothesize that a change point in a mature market such as the US could produce change points in emerging markets such as those from Latin American, or simply, the financial contagion between the US market and Latin American markets could increase the chance of change points occurring in the later markets when they occur in the former. Consequently, the method we develop will incorporate dependence between change point probabilities across multiple processes which could potentially improve the ability of detecting a change point compared to an independent model.

One commonly used approach in the statistical literature for detecting time-series change points is based on product partition models (PPM). These models, which were introduced by Barry and Hartigan (1992), assume that (a) the number and positions of change points are random and, (b) observations within the same block are assumed to follow the same distribution. Thus, the inferential problem reduces to identifying a partition where each cluster is a collection of consecutive data points and then estimate parameters associated with each cluster’s assumed data model. From a Bayesian viewpoint, a prior distribution on the space of partitions, which are restricted to be contiguous, is needed. Barry and Hartigan (1992) use a prior for which prior change point probabilities are based on the so-called cohesion function studied in Yao (1984). Since Barry and Hartigan (1992) many other PPM type approaches to change point analysis have be developed (see, for example Loschi and Cruz, 2002; Loschi et al., 2003; Loschi and Cruz, 2005; Loschi et al., 2005, 2010; Martínez and Mena, 2014; García and Gutiérrez-Peña, 2019; Pedroso et al., 2021).

Most of the existing approaches based on PPMs for detecting change points in time series treat the series individually. However, in the presence of contagion, the information available from several series could improve the accuracy of the change point detection mechanism compared to when series are treated individually. In general, the strategies for detecting change points in the multivariate context focus on detecting changes in the joint distribution of the coordinates of a multivariate process across time. For example, Cheon and Kim (2010) developed a Bayesian model for detecting changes in the mean and variance when data follow a multivariate normal distribution. Their approach considers a latent vector that identifies change point positions for partitioning the observations. Nyamundanda et al. (2015) proposed a Bayesian latent variable PPM, the so-called product partition latent variable model (PPLVM), providing a flexible framework for detecting multiple change point detection in multivariate data. The key feature of the PPLVM is that it can be used to detect distributional changes in the mean and covariance of the series, even in high-dimensional settings. Recently, Jin et al. (2021) developed a hierarchical Bayesian model for changes in the mean process were the prior distribution for change point configurations arises from a Poisson-Dirichlet process, restricted to contiguous partitions (see Martínez and Mena, 2014, for more details).

In contrast to the approaches described above, there are models that do not introduce explicitly a distribution for partitions of contiguous clusters. For example, Killick et al. (2012) considered a procedure for detecting change points by minimizing a cost function, which detects the optimal number and location of change points with a linear computational complexity under mild conditions. Tveten et al. (2021) also minimize a cost function when searching for change points in cross-correlated processes. Matteson and James (2014) proposed a robust nonparametric method using a divergence measure based on Euclidean distances. With this method, the authors showed that it is possible to detect any distributional change within an independent sequence of random variables without making any distributional assumption beyond the existence of the -th absolute moment, for some . Padilla et al. (2021) proposed a novel change point detection algorithm based on the Kolmogorov–Smirnov statistic and showed that it is nearly minimax rate optimal under suitable conditions.

Other approaches for detecting changes in a multivariate process that is more inline with what we proposed assume that each process has its own change point structure. Harlé et al. (2016) introduce a set of independent binary vectors whose entries indicate which coordinate of the multivariate process changes. They do this using a composite marginal likelihood based on Wilcoxon’s rank-sum test and a suitable prior for the binary vectors. Their approach allows us to include dependence among change points between different coordinates. Moreover, Fan and Mackey (2017) introduce a set of change point indicator variables for each coordinate and time such that the prior change point probabilities for all coordinates at a fixed time are the same but change through time.

Our approach, which is motivated by the contagion phenomena, considers simultaneous changes in all parameters associated with a particular process dealing with multiple univariate time series (not all of which are necessarily the same type of response). Thus, each series has its change point structure where the change points between them may or may not coincide in time. We base our approach on elements from the method described in Fan and Mackey (2017) combined with a novel multivariate extension of the PPM approach of Barry and Hartigan (1992). The resulting method takes advantage of the existing correlation in change point locations between series. This strategy requires specifying a joint prior distribution for a collection of partitions. Constructing these types of dependent partition models over a series of partitions has only very recently been considered in the literature by, for instance, Zanini et al. (2019); Page et al. (2021). The method we present is the first work that we are aware of that considers jointly modeling contiguous partitions.

The remainder of the article is organized as follows. Section 2 provides notation and background to the change point PPM. In Section 3 we describe our approach of incorporating dependence between change point probabilities, provide some theoretical properties and details with regards to computation. Section 4 describes a numerical experiment designed to study our method’s ability to detect change points, and in Section 5 we apply our approach to the finance data concerning stock market returns of five countries. We close the paper with some concluding remarks in Section 6.

2 Background and Preliminaries

To make the paper self-contained, we start this section with a background related to PPMs, introducing some notation we will use throughout the paper.

2.1 Partition Definition and Notation

Without loss of generality, consider time series , each of length . Change points occur when the behavior of undergoes sudden changes at unknown times. These times of sudden changes partition into contiguous sets, say , for some . Here, is the th block and is the number of blocks in . The space of these types of partitions will be denoted by .

An alternative, and commonly used, way to denote a partition is through a collection of cluster labels , such that if . Due to the contiguous structure of the that we consider, the cluster labels that define necessarily are such that and , for all . Therefore, change point locations can be identified using . Letting and for all , we have that and the set identifies the locations at which change points in occur.

In a change point setting there is another way to represent that will prove to be very useful for our approach. It is based on a set of change point indicators , such that if time is a change point in , and otherwise. Note that and have a one-to-one correspondence through the relation , for all , where by construction. The number of change points can be identified using by noticing that . In what follows, we will use , and interchangeably. With the necessary notation introduced, we next describe the change point PPM.

2.2 Change Point Product Partition Models

For the -th sequence, the PPM is a discrete distribution on space such that

where is referred to as a cohesion function and measures the a priori belief that elements in co-cluster. The change point PPM as described in Barry and Hartigan (1992), Loschi et al. (2003), and others, uses Yao (1984)’s cohesion function to assign probabilities to each element in . Yao (1984)’s cohesion function applied to contiguous results in

| (1) |

for some such that . Based on this cohesion we have that

Thus, the change point PPM takes on the following form

Once the partition model has been specified, the key idea behind change point modeling from a partition perspective is that observations within the same block are assumed to follow a common distribution, whereas different distributions are assumed between blocks. Following Barry and Hartigan (1992)’s approach, given , the joint density of is written as a product of data factors, also known as marginal likelihoods, which measure the similarity of observations within each block. More precisely,

| (2) | ||||

where and is a likelihood function indexed by the set of parameters which are block-specific, and a collection of parameters that are common to all blocks. Further, is a suitable prior for . The data generating mechanism (2) along with prior distributions for and (if applicable) completely specify the Bayesian change point PPM.

It is common to select and such that they form a conjugate pair which results in being available in closed form. That said, the choices for and in (2) can be quite general, depending on the nature of and . Examples of this are data that follow an Ornstein-Uhlenbeck process with a Normal-Gamma prior for mean-precision parameters (Martínez and Mena, 2014) (here, is a case dependency parameter with a prior) and independent data belonging to the exponential family with a conjugate prior for the natural parameters (Loschi and Cruz, 2005) (in this case, there is no ). The types of marginal likelihoods just described (and others not listed) are easily applied using our method. Even so, in what follows, we will focus on the following specification (which is suitable for changes in mean and variance for data supported on ). Let and

| (3) | ||||

Here, and are fixed hyperparameters, denotes a normal density with mean and variance , and denotes an inverse Gamma density with shape and scale . It is well known that the th data factor induced by (3) is given by

| (4) |

where is the cardinality of , is the vector with entries equal 1, is the identity matrix and is the matrix with all entries equal 1. Also, is the -dimensional Student’s -density with degrees of freedom , location vector and scale matrix , where denotes the space of positive-definite matrices.

The set of hyperparameters , ,, play a crucial role in determining what constitutes a change point. For example, setting close to one will result in (4) having thick tails so that a change point would necessarily need to be far from the center. Conversely, with a large value of (4) approximates a normal distribution and points not far from the center can still be change points. Consequently, thought must be dedicated to assigning values to the marginal likelihood parameters. In Section 3.2 we discuss an empirical Bayes method that produces reasonable values for them in absence of prior information.

3 The Joint Prior Distribution on a Collection of Partitions

We now describe our approach of formulating a joint model for a sequence of partitions. As mentioned, the partition for the -th time series has a one-to-one correspondence with . Thus, any prior distribution for , say , uniquely determines a prior for . We start by describing our joint model as an extension of the change point PPM and then we connect it to , which is what we ultimately use in our approach as it facilitates computation.

In our setup, rather than consider a single probability parameter for the -th series, we define with and extend the cohesion in (1) to

| (5) |

Using the cohesion (5) for contiguous partitions still results in Therefore, the partition probabilities become

where . Including all partitions, the joint partition model becomes

It is important to stress that our extension (i.e., introducing ) provides more flexibility for modeling simultaneous change point configurations by allowing us to correlate probabilities of a change point at each time point. As a consequence, the change point indicators are assumed conditionally independent with their own probability of detecting a change .

Let be a -dimensional vector of probabilities supported on the space . To specify a multivariate distribution for , we consider the bijective transformation which is defined on the Euclidean space , and model it with a multivariate Student’s- distribution. The reason for selecting a Student’s- distribution instead of, for example, a multivariate normal distribution is that extreme probabilities (near 0 or 1) are more achievable due to the thicker tails of the Student’s-. In summary, the proposed model for partitions can be formulated using the following hierarchical structure:

| (6) |

with , In what follows, we will refer to the model comprised of (3), (5), and (6) as the correlated change point product partition model or simply, CCP-PPM.

Note that, specifying adequate values for , and in (6) must be done with caution as are not invariant to their selection. In the absence of information regarding these parameters, we provide an interesting approach for selecting them in Section 3.2.

3.1 Properties of the Joint Model on Partitions

In this section, we provide some interesting properties that are consequences of modeling the change point indicators with (6). The proofs of all propositions are provided in the Appendix.

Proposition 1.

Under the assumptions in (6), each of the follows a change point PPM based on Yao’s cohesion with probability parameter

| (7) |

A consequence of Proposition 1 is that the correlation in the change point probabilities from our model only exists across the series for a fixed . Within a series, the probability of a change point at time is independent of time .

The next proposition provides an interesting result regarding the number of expected change points based on the CCP-PPM.

Proposition 2.

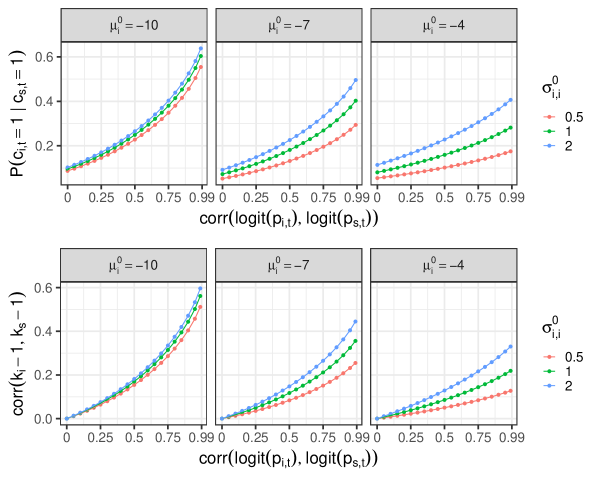

Note that easily follows from Proposition 2. For the values of and considered in Figure 2, the expected number of change points in each series ranges between 6.19 and 12.29 a priori. The bottom row of Figure 2 provides values for based on a numerical approximation of . As expected the number of change points in two series with high correlation between and will be similar.

The last proposition derives the conditional probabilities of change point indicators. These are of particular interest as they illustrate how the probability of a change point across series varies as one series experiences a change point.

Proposition 3.

The top row of Figure 2 provides values for . The integral in was approximated using the statistical software R (R Core Team 2021). As expected, the higher the correlation between and the higher the conditional probabilities a priori, for the values of and considered.

3.2 Selection of tuning parameters

Like most change point methods, the posterior probability of classifying a point as a change point can be sensitive to marginal likelihood specification and prior parameter selection. We refer to these parameters as tuning parameters. In some cases, the practitioner can inform the procedure regarding a change point, which guides tuning parameter selection. Without this information, it is appealing to have a procedure that produces default values for the tuning parameters. Therefore, we describe an empirical Bayes approach to selecting values for , , , . The approach we describe is geared towards situations in which the magnitudes of change points are relatively small.

First note that from (4) we have

for all and . Under the scenario of no change points, is equal to the upper bound , which is constant as a function of . Thus, a value for could be empirically selected using . This correlation can be estimated by inspecting the empirical -lag autocorrelation for , say , and choosing the smallest such that . Then set . From there, the maximum likelihood estimators of the parameters in the Student’s -distribution given in (4) based on the entire can be used to provide values for , , and . Let , and . Then, we set , and where denote the maximum likelihood estimates of .

Now, we focus on . Although and do not exist in a closed form, a first-order Taylor expansion provides approximations to them. If , then

After choosing prior guesses for and , say and respectively, we set

We recommend setting , which is the least integer such that the approximations described above exist. In the case that no prior information is available to guide specifying and , the following empirical approach can be used. Set . For , a compound symmetry covariance matrix can be used, where and .

3.3 Posterior Sampling

The joint posterior distribution of and is not analytically tractable. Therefore we resort to sampling from it using Markov Chain Monte Carlo (MCMC) methods. The MCMC algorithm we construct is very straightforward to implement and is an extension of the Gibbs sampler described in Loschi et al. (2003) with the main difference being that we employ Metropolis updates when conditional conjugacy is not available. Before model fitting, we recommend scaling each series to have mean zero and standard deviation one. The full conditional distributions we need in our algorithm are described next.

-

•

For each and update according to its full conditional density , which is proportional to

Here, is the indicator function of the set . To update , we employ a random walk Metropolis step with a normal centered at the previous iteration’s value as a candidate density. The standard deviation of the normal candidate density is set to 0.005 which produces an acceptance rate in the general range of 0.2 and 0.5

-

•

For each , and , define the set of change point indicators such that

Using , we construct the corresponding set of cluster labels . Then, after computing

where , can be updated using a Bernoulli distribution with probability parameter

Now, an MCMC algorithm can be obtained by cycling through each of the full conditionals individually. If a model is proposed so that is available, it is relatively straightforward to update in the Gibbs sampler using a Metropolis step. The update is based on the following full conditional of for each

where is a prior density for .

4 Simulation Study

We conduct a small numerical experiment to study the CCP-PPM’s ability to detect multiple change points. The experiment is based on generating data sets containing change points whose times are dependent across series, mimicking the contagion idea. We consider change points that result from simultaneous changes in the mean and variance of a normal distribution. Data sets are generated using three scenarios, with each one producing data sets containing series of observations. The scenarios are detailed next.

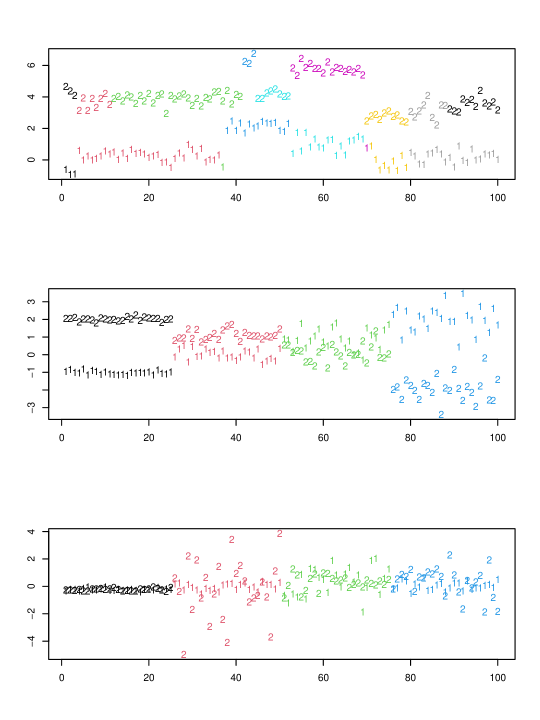

The first scenario referred as data type 1 uses the CCP-PPM as a data generating mechanism. We set , , and to a compound symmetric matrix with variance 10 and correlation 0.9. Based on these values, (6) is used to create partitions. Once partitions are formed, we use a to generate cluster specific means for one series and a for the other. Cluster specific variances were all generated using an distribution. Once cluster specific parameters were generated, observations were generated using a . An example of this type of data is displayed in the top row of Figure 3.

The following two scenarios set change point locations in both series at 25, 50, and 75. As a result, the change points of the two series are highly dependent. Under this setting, four clusters of 25 observations for both series are obtained. Given this type of partition, we produce observations in two ways. The first one, which we refer to as data type 2, generates observations using a normal distribution with the following cluster-specific means and variances:

-

-

and ,

-

-

and .

The second scenario, which we refer to as data type 3, generates observations using a normal distribution and cluster-specific means and variances given by:

-

-

and ,

-

-

and .

This scenario is included because it provides insight to how the CCP-PPM approach performs for data similar to that which we consider in Section 5. Examples of synthetic data sets created from these two scenarios are provided in the second and third rows of Figure 3. It is important to note that in the scenario data type 2, the means are the primary driver of change points, while in the scenario data type 3 the variances, or volatility, is the primary driver of change points.

We simulated one hundred data sets for each scenario. Then, we fit the CCP-PPM by collecting 2000 MCMC iterates after discarding the initial 10,000 as burn-in and thinning by 10 all of which was carried out using the ppmSuite (Page and Quinlan 2022) R package that is available on CRAN. In addition, we also consider the following controls for detecting change points:

-

•

The PPM-based method of Wang and Emerson (2015). Since this approach does not analyze multiple series, we fit it to each series independently instead. The bcp package (Erdman and Emerson, 2007) found in the R statistical software (R Core Team, 2021) is used to implement this method. We referred to this method as the Wang method.

- •

- •

The tuning parameters used for the CCP-PPM are the following. For the marginal likelihood we use . These same values are used for the Loschi method. For the prior on , we use the same values that were used to generate the data type 1. For the Loschi method there is a single for each series and we used . Default values of the bcp and ecp R-packages were considered for the Wang and Matteson methods, respectively.

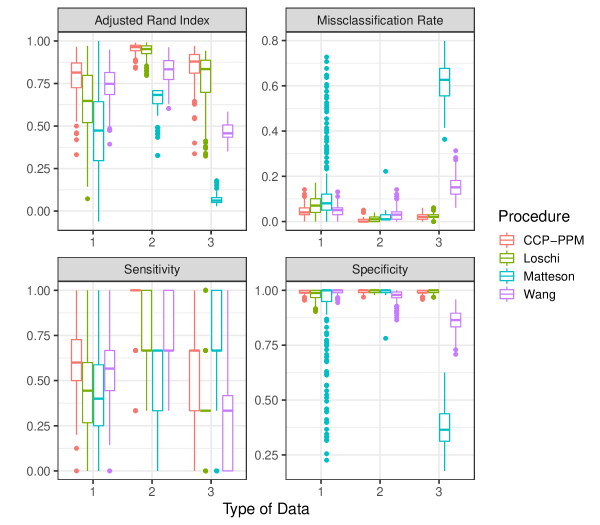

After considering the methods described above in each scenario, we classify any point as a change if its posterior probability of being a change is greater than 0.5. Then, we compute the overall misclassification rate, sensitivity (true positive rate), and specificity (true negative rate) of classifying points as change points. These metrics give us information on the accuracy of identifying points as change points. In addition, we calculate the adjusted Rand index (Rand, 1971) (ARI) between the estimated partition based on change points and the true partition. This metric illustrates how well each method does at recovering the true partition of contiguous clusters.

The results of the simulation study are provided in Figure 4. Note that the CCP-PPM outperforms all the considered methods at recovering the true partition according to the adjusted Rand index regardless of the type of data. In terms of the overall misclassification rate, our method performs better than the Loschi and Matteson methods. The Wang method performs comparably way to our approach in the scenario 1 (data type 1), but in scenario 3 (data type 3) this method performs poorly. Regarding the sensitivity, our approach outperforms the other three methods in the first and second scenarios (data type 1 and data type 2, respectively). Nonetheless, in the third scenario (data type 3) Matteson has the highest sensitivity but at the cost of very low specificity. In summary, it appears that the CCP-PPM overall performs the best at detecting the correct number and location of change points.

5 Finance Data Application

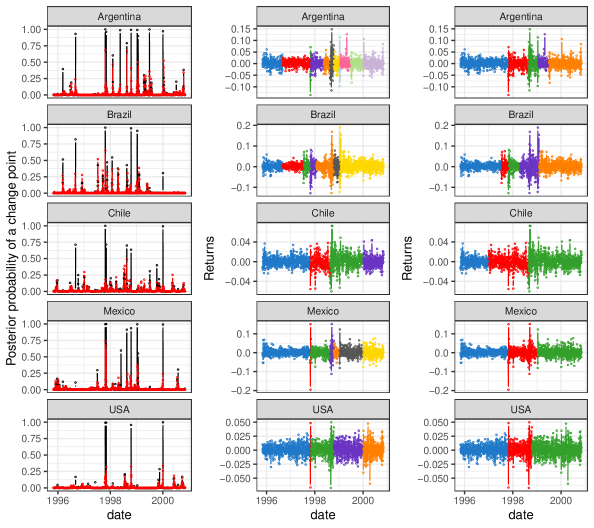

We now turn our attention to the application that motivated our proposal. As is commonly done in financial applications, we analyze returns rather than prices. Returns are defined as for , where is the daily price. When analyzing the data set, we consider contagion both between mature markets and emerging ones and also between emerging markets. We analyzed the most important Latin American markets (emerging markets), namely Argentinean, Brazilian, Chilean and Mexican markets, including the USA market in the analysis (mature market). Consequently, we fit the CCP-PPM and the change point PPM of Loschi or simply Loschi method (which is perhaps our method’s most natural competitor, treating each series independently).

We considered the return series of their main stock indexes, namely, the MERVAL (Índice de Mercado de Valores de Buenos Aires) of Argentina, the IBOVESPA (Índice da Bolsa de Valores do Estado de São Paulo) of Brazil, the IPSA (Índice de Precios Selectivos de Acciones) of Chile, the IPyC (Índice de Precios y Cotizaciones) of Mexico, and the Dow Jones (Dow Jones Industrial Average) of USA. The stock returns were recorded daily from October 31, 1995 to October 31, 2000.

We employ the procedure described in Section 3.2 to produce values for the tuning parameters in (4) and (6). This resulted in values for that are listed in Table 1. These tuning parameter values were used for both the CCP-PPM and that of Loschi method.

| Series | ||||

|---|---|---|---|---|

| USA | 0.009 | 188.924 | 2.212 | 1.233 |

| Mexico | -0.014 | 9.075 | 1.596 | 0.574 |

| Argentina | 0.009 | 10.186 | 1.328 | 0.402 |

| Chile | -0.022 | 2.533 | 1.864 | 0.656 |

| Brazil | 0.022 | 11.010 | 1.349 | 0.423 |

To specify values for and , we first set (in the application ) and used a compound symmetry matrix for with variance and correlation . This resulted in and being a compound symmetric matrix with variance and correlation . We set . For the Loschi method and we set and . These values were selected based on setting the mean number of clusters a priori to 3.5 with a variance of 2.5. Both methods were fit by collecting 1000 MCMC samples after discarding the first 10,000 as burn-in and thinning by 5 (i.e., 15,000 total samples were collected). Both the CCP-PPM and Loschi’s method were fit using the ccp_ppm and icp_ppm functions that are available in the ppmSuite-package that can be found on CRAN.

There are two approaches that could used to estimate change points. The first classifies points as change points if their posterior probability of being a change point is greater than some pre-specified value. The second classifies points as change points based on a partition estimate. We report both as both require input from the user (pre-specified probability cut-off for the first approach and a loss function in the second approach).

We first explore the a posteriori dependence between partitions from the five markets. To do this, at each MCMC iteration we computed the ARI for all possible pairs of partitions (which is 10 in this application). The CCP-PPM produced slightly more similar partitions across countries than the Loschi method. The overall average pairwise ARI for CCP-PPM turned out to be 0.51 compared to 0.48 from the Loschi method.

Next we explore the posterior change point probabilities which are displayed in the first column of Figure 5. The black points correspond to the CCP-PPM and the red to Loschi. For both, change point probabilities were estimated using the posterior means of . It seems that there is a general agreement between the two methods regarding the location of potential change points. However, the CCP-PPM seems to produce probabilities that are closer to one for these points compared to the Loschi method. In fact, the Loschi method never records a change point probability greater than 0.75. Similarly, both methods agree on the general location of points that have a small chance of being a change point, although the CCP-PPM seems to push these probabilities closer to zero compared to the Loschi method.

Figure 5, second and third columns, shows the partition estimates under the CCP-PPM (second column) and Loschi method (third column). Partition estimates were obtained using the salso (Dahl et al., 2021b) R package and the generalization of the Variation of Information loss function (Meilǎ, 2007). Since in our case it seems natural to penalize change point false positives more than false negatives, we set the false positive penalty parameter of the salso function to (see Dahl et al., 2021a, for more details). We note briefly that setting was driven primarily by Loschi’s method. If , then Loschi’s method tended to smooth over some change points and for it tended to produce more change points than what would be desired. However, the CCP-PPM was reasonably robust to ’s value. This is a consequence of the change point probabilities from the the Loschi method being more central (i.e., closer to 0.5) than those from the CCP-PPM.

Apparent differences between the estimated partitions exist, and they illustrate how the CCP-PPM takes into account the dependency between the index series or the contagion phenomenon. For example, the CCP-PPM method identifies a shared partition for Brazil, Chile, Mexico, and the USA at the end of 1997. It is important to stress that in July 1997, the Thai government ran out of foreign currency, forcing it to float the Thai baht which is a factor in starting the 1997 Asian financial crisis, or Asian Flu. This crisis spread internationally, affecting some Asian stock markets such as Indonesia, South Korea, Hong Kong, Laos, Malaysia, Philippines, Brunei, mainland China, Singapore, Taiwan, and Vietnam. According to Harrigan (2000), the Asian crises’ overall effect on the United States were small. However, as mentioned by Stallings (1998), the Asian Flu hit the Latin American markets in October 1997, when bone spreads widened abruptly implying more risk. In the Argentinean market, our approach identified a first partition at the end of 1996. Note that, at the end of 1995, the (real) gross domestic product (GDP) in this country fell by 2.5 percent. However, by the end of 1996, it rebounded by 5.5 percent (International Monetary Found, 2003), possibly affecting the performance of the MERVAL index.

Another cluster or change point our method identifies is related to the Russian crisis or Russian Cold in August 1998. This crisis started when the Russian government and the Russian Central Bank devalued the ruble and defaulted on its debt. It is important to stress that although most countries experienced changes in their stock market returns series at the end of 1998, the Argentinean market experienced a change in mid-1998. Moreover, the IBOVESPA index (Brazil) experienced a change at the beginning of 1999, just after the Russian crisis. This crisis was known as the Samba effect and was produced when the Minas Gerais State Governor, Itamar Franco, stopped paying Minas Gerais debt to other states, generating unleashing capital flights. Note that a small cluster is detected by the CCP-PPM in the indexes of Argentina, Mexico, and USA towards the end of 1998, but something the Loschi method misses. These clusters provide some evidence that the contagion phenomena from a mature market to emerging ones is being captured by the CCP-PPM, which includes dependency between partitions.

Finally, the CCP-PPM also detected a cluster after the year 2000. The corresponding change point can be explained by the dot-com bubble, caused by excessive speculation of some internet companies in the late 1990s. On January 14, 2000, the Dow Jones Industrial Average reached its dot-com bubble peak. This partition is observed in the Argentinean, Chilean, Mexican, and USA markets. Possibly, the dot-com bubble may have affected other economies over the Latin American region, evidencing some contagion effect. In this case, Loschi method did not detect a change point at or near the above-mentioned date.

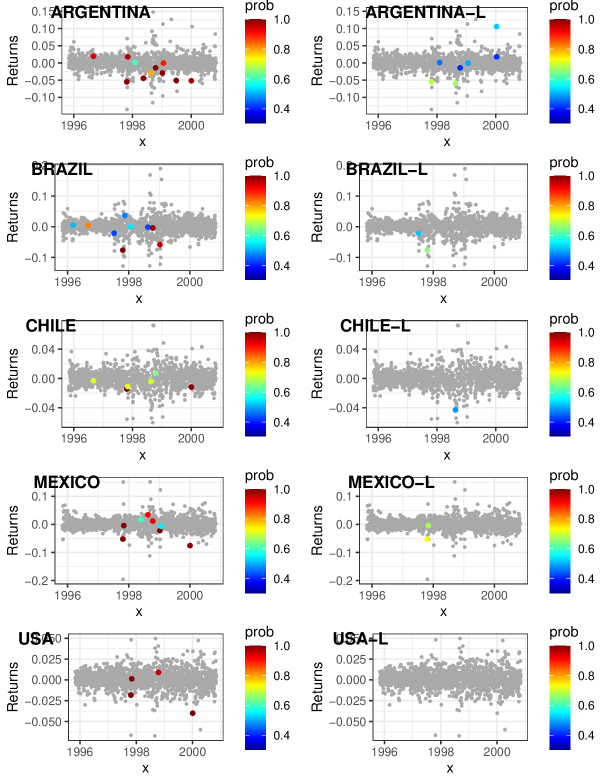

As mentioned, the estimated partitions in Figure 5 depend on the value . To show a more complete picture of both methods performance, we provide Figure 6. In this figure, all points with a posterior probability of being a change point less than 0.4 are colored gray. The left column corresponds to the CCP-PPM fit while the right the Loschi method. The CCP-PPM fit has more power in detecting change points compared to Loschi method, without inflating the false-positive rate. The points highlighted by the CCP-PPM fit are at least plausibly change points, and those associated with more pronounced volatility generally have a larger probability of being a change point, which is a desirable characteristic.

6 Discussion

In this paper we developed a new change point detection model for time series with observations in an arbitrary space, which undergo sudden changes in their distributional parameters. By making dependent the vector of latent change point probabilities at a specific time , the corresponding partitions with contiguous clusters are encouraged to be correlated. We provide some theoretical results that help to better understand the main features of our model, a useful procedure to guide the specification of all parameters that are involved in, and simple pseudo-code to perform posterior inference via MCMC methods. Through a small simulation study, we compared the ability of our model with other compelling approaches to detect highly dependent changes under different scenarios, showing an improvement in detecting change points. Additionally, we applied our method to the returns of emerging Latin American and US markets, obtaining exciting results about possible contagion effect between the economies of these countries based on the dependence between change point locations.

In terms of extending the proposed model with the aim of making it more flexible, several directions can be pursued. For instance, the assumption that the vectors of change point probabilities are independent and identically distributed through time can be relaxed. One possible approach would be to model with a stationary process in . Another interesting direction would be to incorporate time-dependent covariates in the marginal likelihood function to describe abrupt changes in a regression curve. A similar situation, but more complex, is to incorporate covariates in the distribution for contiguous partitions. Finally, the computational cost involved in the MCMC algorithm for posterior inference increases rapidly as the length and number of time series grow. It would be appealing to develop strategies that mitigate the so-called “curse of dimensionality”. These are all topics of future research.

Acknowledgements

José J. Quinlan gratefully recognizes the financial support provided by the Agencia Nacional de Investigación y Desarrollo de Chile (ANID) through Fondecyt Grant 3190324.

7 Appendix

Appendix A Proofs of Propositions

Proofs of the propositions depend on a well known result of the multivariate . For the sake of completeness, we include it here.

Result 1 (Ding (2016)).

Let be a non-empty subset of . If , then , where is the cardinality of , and . When , set , and .

Proof of Proposition 1.

A direct consequence of (6) and Result 1 is that

Invoking the Change of Variables theorem, the marginal distribution for is given by

where

Keeping in mind that ,

From the last expression, the result follows.

Proof of Proposition 2.

From the proof of Proposition 1, we saw that are independent random variables. From this observation, it follows that

As for the distribution of , given the random variables and are conditionally independent Poisson’s Binomial with corresponding parameters and . The mixture distribution follows since

for all . Now, by the Law of Total Covariance

Due to (6) and Result 1 with its respective notation,

where . By the Change of Variables theorem and the previous observation, we have that

where

Finally,

Proof of Proposition 3.

Consider two disjoint non-empty subsets of and set for any non-empty subset of . Then,

Using the Change of Variables theorem,

where . Using Result 1 and the notation therein, it follows that

Similar expression applies for . Therefore,

As for the conditional probability , take and .

References

- Arellano-Valle et al. (2013) Arellano-Valle, R., Castro, L. M., and Loschi, R. (2013), “Change point detection in the skew-normal model parameters,” Communications in Statistics. Theory and Methods, 42, 603–618.

- Barry and Hartigan (1992) Barry, D. and Hartigan, J. A. (1992), “Product partition models for change point problems,” Ann. Statist., 20, 260–279.

- Cheon and Kim (2010) Cheon, S. and Kim, J. (2010), “Multiple Change-Point Detection of Multivariate Mean Vectors with the Bayesian Approach,” Comput. Stat. Data Anal., 54, 406––415.

- Dahl et al. (2021a) Dahl, D. B., Johnson, D. J., and Mueller, P. (2021a), “Search Algorithms and Loss Functions for Bayesian Clustering,” arXiv:2105.04451v1.

- Dahl et al. (2021b) Dahl, D. B., Johnson, D. J., and Müller, P. (2021b), salso: Search Algorithms and Loss Functions for Bayesian Clustering, r package version 0.2.23.

- de P. Filleti et al. (2008) de P. Filleti, J., Hotta, L. K., and Zevallos, M. (2008), “Analysis of contagion in emerging markets,” Journal of Data Science, 6, 601–626.

- Ding (2016) Ding, P. (2016), “On the Conditional Distribution of the Multivariate t Distribution,” The American Statistician, 70, 293–295.

- Erdman and Emerson (2007) Erdman, C. and Emerson, J. W. (2007), “bcp: An R Package for Performing a Bayesian Analysis of Change Point Problems,” Journal of Statistical Software, 23, 1–13.

- Fan and Mackey (2017) Fan, Z. and Mackey, L. (2017), “Empirical Bayesian Analysis of Simultaneous Changepoints in Multiple Data Sequences,” Annals of Applied Statistics, 11, 2200–2221.

- García and Gutiérrez-Peña (2019) García, E. C. and Gutiérrez-Peña, E. (2019), “Nonparametric product partition models for multiple change-points analysis,” Communications in Statistics - Simulation and Computation, 48, 1922–1947.

- Gupta et al. (2021) Gupta, S. K., Gupta, N., and Singh, V. P. (2021), “Variable-Sized Cluster Analysis for 3D Pattern Characterization of Trends in Precipitation and Change-Point Detection,” Journal of Hydrologic Engineering, 26, 04020056.

- Harlé et al. (2016) Harlé, F., Chatelain, F., Gouy-Pailler, C., and Achard, S. (2016), “Bayesian Model for Multiple Change-Points Detection in Multivariate Time Series,” IEEE Transactions on Signal Processing, 64, 4351–4362.

- Harrigan (2000) Harrigan, J. (2000), “The impact of the Asia crisis on U.S industry: An almost-free lunch?” Federal Reserve Bank of New York, Economic Policy Review.

- International Monetary Found (2003) International Monetary Found (2003), “El papel del FMI en la Argentina, 1991-2002,” .

- James et al. (2019) James, N. A., Zhang, W., and Matteson, D. S. (2019), “ecp: An R Package for Nonparametric Multiple Change Point Analysis of Multivariate Data. R package version 3.1.2,” .

- Jin et al. (2021) Jin, H., Yin, G., Yuan, B., and Jiang, F. (2021), “Bayesian Hierarchical Model for Change Point Detection in Multivariate Sequences,” Technometrics, 0, 1–30.

- Jones et al. (2021) Jones, C., Clayton, S., Ribalet, F., Armbrust, E. V., and Harchaoui, Z. (2021), “A kernel-based change detection method to map shifts in phytoplankton communities measured by flow cytometry,” Methods in Ecology and Evolution, 12, 1687–1698.

- Killick et al. (2012) Killick, R., Fearnhead, P., and Eckley, I. A. (2012), “Optimal Detection of Changepoints With a Linear Computational Cost,” Journal of the American Statistical Association, 107, 1590–1598.

- Loschi and Cruz (2002) Loschi, R. and Cruz, F. (2002), “Analysis of the influence of some prior specifications in the identification of change points via product partition model,” Computational Statistics & Data Analysis, 39, 477–501.

- Loschi and Cruz (2005) — (2005), “Extension to the product partition model: computing the probability of a change,” Computational Statistics & Data Analysis, 48, 255–268.

- Loschi et al. (2005) Loschi, R., Cruz, F., and Arellano-Valle, R. (2005), “Multiple change point analysis for the regular exponential family using the product partition model,” Journal of Data Science, 3, 305–330.

- Loschi et al. (2003) Loschi, R., Cruz, F., Iglesias, P., and Arellano-Valle, R. (2003), “A Gibbs sampling scheme to product partition model: An application to change-point problems,” Computers & Operations Research, 30, 463–482.

- Loschi et al. (2010) Loschi, R., Pontel, J., and Cruz, F. (2010), “Multiple change-point analysis for linear regression models,” Chilean Journal of Statistics, 1, 93–112.

- Lowell et al. (1998) Lowell, J. F., Neu, C. R., and Tong, D. (1998), Financial Crises and Contagion in Emerging Market Countries, Santa Monica, CA: RAND Corporation.

- Martínez and Mena (2014) Martínez, A. F. and Mena, R. H. (2014), “On a Nonparametric Change Point Detection Model in Markovian Regimes,” Bayesian Analysis, 9, 823–858.

- Matteson and James (2014) Matteson, D. and James, N. (2014), “A Nonparametric Approach for Multiple Change Point Analysis of Multivariate Data,” Journal of the American Statistical Association, 109, 334–345.

- Meilǎ (2007) Meilǎ, M. (2007), “Comparing clusterings-an information based distance,” Journal of Multivariate Analysis, 98, 873–895.

- Nyamundanda et al. (2015) Nyamundanda, G., Hegarty, A., and Hayes, K. (2015), “Product partition latent variable model for multiple change-point detection in multivariate data,” Journal of Applied Statistics, 42, 2321–2334.

- Padilla et al. (2021) Padilla, O. H. M., Yu, Y., Wang, D., and Rinaldo, A. (2021), “Optimal nonparametric change point analysis,” Electronic Journal of Statistics, 15, 1154–1201.

- Page and Quinlan (2022) Page, G. L. and Quinlan, J. J. (2022), ppmSuite: A Collection of Models that Employ a Product Parition Prior Distribution on Partitions, r package version 0.2.1.

- Page et al. (2021) Page, G. L., Quintana, F. A., and Dahl, D. B. (2021), “Dependent Modeling of Temporal Sequences of Random Partitions,” Journal of Computational and Graphical Statistics, 0, 1–29.

- Pedroso et al. (2021) Pedroso, R. C., Loschi, R. H., and Quintana, F. A. (2021), “Multipartition model for multiple change point identification,” arXiv:2107.11456v2.

- R Core Team (2021) R Core Team (2021), R: A Language and Environment for Statistical Computing, R Foundation for Statistical Computing, Vienna, Austria.

- Rand (1971) Rand, W. M. (1971), “Objective Criteria for the Evaluation of Clustering Methods,” Journal of the American Statistical Association, 66, 846–850.

- Stallings (1998) Stallings, B. (1998), “Impact of th Asian crisis on Latin America,” United Nations Economic Commission for Latin America and the Caribbean.

- Truong et al. (2020) Truong, C., Oudre, L., and Vayatis, N. (2020), “Selective review of offline change point detection methods,” Signal Processing, 167, 107299.

- Tveten et al. (2021) Tveten, M., Eckley, I. A., and Fearnhead, P. (2021), “Scalable changepoint and anomaly detection in cross-correlated data with an application to condition monitoring,” arXiv:2010.06937v2.

- Valdés (2000) Valdés, R. (2000), “Emerging markets contagion: evidence and theory,” Available at SSRN: https://ssrn.com/abstract=69093 or http://dx.doi.org/10.2139/ssrn.69093.

- Wang and Emerson (2015) Wang, X. and Emerson, J. W. (2015), “Bayesian Change Point Analysis of Linear Models on Graphs,” arXiv:1509.00817.

- Wang (1993) Wang, Y. H. (1993), “On the Number of Successes in Independent Trials,” Statistica Sinica, 3, 295–312.

- Wood et al. (2021) Wood, K., Roberts, S., and Zohren, S. (2021), “Slow Momentum with Fast Reversion: A Trading Strategy Using Deep Learning and Changepoint Detection,” The Journal of Financial Data Science, jfds.2021.1.081.

- Yao (1984) Yao, Y.-C. (1984), “Estimation of a noisy discrete-time step function: Bayes and empirical Bayes approaches,” Ann. Statist., 12, 1434–1447.

- Zanini et al. (2019) Zanini, C. T. P., Müller, P., Ji, Y., and Quintana, F. A. (2019), “A Bayesian Random Partition Model for Sequential Refinement and Coagulation,” Biometrics, 75, 988–999.