Spectral clustering with variance information for group structure estimation in panel data ††thanks: We are grateful to professors H.J. Wang and Y. Zhang for sending us the code for their simulations in Zhang et al. (2019a) . We thank Professor D. Millimet for kindly sharing this data with us. The data we use here is the same as in Millimet et al. (2003). We also thank the AE and anonymous referees for constructive comments on an earlier version of this manuscript that motivated us to consider the local analysis in section 2.2 and resulted in a greatly improved manuscript.

Abstract

Consider a panel data setting where repeated observations on individuals are available. Often it is reasonable to assume that there exist groups of individuals that share similar effects of observed characteristics, but the grouping is typically unknown in advance. We first conduct a local analysis which reveals that the variances of the individual coefficient estimates contain useful information for the estimation of group structure. We then propose a method to estimate unobserved groupings for general panal data models that explicitly accounts for the variance information. Our proposed method remains computationally feasible with a large number of individuals and/or repeated measurements on each individual. The developed ideas can also be applied even when individual-level data are not available and only parameter estimates together with some quantification of estimation uncertainty are given to the researcher. A thorough simulation study demonstrates superior performance of our method than existing methods and we apply the method to two empirical applications.

Keywords: group structure estimation, spectral clustering, panel data models

1 Introduction

Panel data models are a standard empirical tool in statistics, economics, marketing, and financial research. The conventional modeling approach is to assume that all individual heterogeneity can be summarized by an individual specific intercept, often known as the fixed effects, while assuming all covariates have a common effect among all the individuals, such that information can be pooled across individuals to gain efficiency for estimating these common parameters. However, heterogeneous responses towards observed control variables are often better supported by empirical evidence, especially as detailed individual level data becomes more available.

An increasingly popular approach to model unobserved heterogeneity in the effects of covariates on individual responses is to assume the existence of a finite number of homogeneous groups. Here, parameters in a potentially non-linear model111Examples include quantile regression and discrete outcome models. are assumed to take common values within groups but differ across groups. The main challenge is to learn the unobserved group structure from observed data. An alternative way to model unobserved heterogeneity is through latent factors (e.g., Bai (2009)). This approach also has discrete heterogeneity in the sense that a small number of unobserved factors drive the co-movement of a large number of time series. Both group pattern and factor structure are useful empirical tools, but they have different interpretations. In this paper, we focus on group patterns.

The existing literature can be roughly categorized into three categories. Methods from the first category rely on minimizing a loss function that incorporates different coefficients for all individuals combined with a penalty which encourages the coefficient estimates to be similar. Su et al. (2016) propose the classifier-LASSO (C-LASSO) approach, which is applicable to both linear and nonlinear models. Differences among individual parameters are penalized through a LASSO type penalty, and consistent grouping can be achieved if the penalty parameter is chosen properly. Wang et al. (2018) propose a Panel-CARDS penalty which extends the idea of homogeneity pursuit in Ke et al. (2015) from cross-sectional models to panel data models. Gu and Volgushev (2019) propose to use the convex clustering penalty of Hocking et al. (2011) in panel data quantile regression models with grouped individual intercepts and common slope parameters.

An alternative approach is to relate the group structure estimation problem to clustering; here clusters in the coefficient vectors correspond to latent groups of individuals. Estimating clusters has a long history in statistics and economics. Among the many clustering algorithms, the -mean algorithm by MacQueen et al. (1967) is one of the most popular and commonly used methods. However, instead of directly applying -mean methods on the estimated individual parameters, Lin and Ng (2012) and Bonhomme and Manresa (2015) propose to incorporate the regression loss function and re-estimate the group-specific coefficients in an iterative fashion. Originally proposed for linear regression models, this approach has also been extended to quantile regression models by Zhang et al. (2019a) and Leng et al. (2023). Further advancement of this literature has considered time varying group membership, for example Miao et al. (2020), Okui and Wang (2021) and Lumsdaine et al. (2023).

Both the penalization-based and clustering-based approaches described above require the repeated fitting of large regression models which involve all individuals and all individual-specific parameters in a large-scale minimization problem. This can be computationally costly especially for large scale datasets, which become more and more common in practice. In addition, the extensions of the -means approach discussed above rely on iterative algorithms with random initialization which require repeated application with many different starting points. Motivated by those computational challenges, Chetverikov and Manresa (2022) propose an estimator for linear panel data models with grouped intercepts and common slope. Their approach is shown to guarantee the same theoretical properties as Bonhomme and Manresa (2015) but is computationally much faster. It should be pointed out however that their approach seems to be difficult to extend to non-linear panels. Wang and Su (2021) propose to use ordered individual-specific regression estimators to convert the grouping problem into a change-point detection setting and apply binary segmentation to learn the underlying group structure. This approach can be applied to both linear and nonlinear panel data models. It is computationally efficient because the individual-specific regressions only need to be estimated once rather than in an iterative fashion. They further show that by considering the spectral decomposition of an outer product of the individual parameter estimates and then applying binary segmentation on the leading eigenvectors can lead to improved group estimation.

In the present paper, we propose a novel approach that retains the computational advantages of working with individual-specific regressions but explicitly takes into account the uncertainty in the corresponding estimates. This information is particularly important in settings where different entries of a coefficient vector are estimated with different degrees of precision and hence carry varying amounts of information about the underlying population coefficients. To motivate the specific form of reweighting we use, we first conduct a simplified analysis in a local alternative framework. In the simplest case where there are only two groups in the population, we study the probability of classifying an individual to one of two groups when the separation between group centers tends to zero at a certain rate. This analysis targets a simplified iteration step which is the key ingredient of most existing iterative procedures for estimating group membership.

This local analysis motivates us to weigh the differences between coefficient estimates of different individuals by an estimated variance-covariance matrix. The resulting weighted differences can not be interpreted as a Euclidean distance. This renders many classical clustering approaches such as the vanilla -means algorithm or extensions of homogeneity pursuit and binary segmentation inapplicable. We handle this challenge by interpreting the weighted distances as a quantification of dissimilarity between individuals. With this interpretation, we can apply any clustering approach that works with general measures of dissimilarity. We consider two popular approaches: k-medoids Schubert and Rousseeuw (2019) and spectral clustering Ng et al. (2002). In simulation studies, we find that both approaches outperform existing proposals. In finite samples, the spectral clustering approach works better than the k-medoids approach and we provide high level assumptions which guarantee consistent group structure recovery asymptotically.

The remaining paper is organized as follows. In Section 2.2 we present the simple local analysis motivates our approach. Section 2.3 contains a detailed description of the proposed estimation procedure and illustrates it on several specific models that were previously considered in the literature. Section 3.1 contains theoretical guarantees on correct group estimation under high-level conditions. Those conditions are verified for several examples in Section 3.2. A simulation study is presented in Section 4. An empirical illustration analyzing the heterogeneous relationship between income and pollution level among different states using data from the United States is given in Section 5. We also apply our approach to the commuting zone summary statistics provided by Chetty and Hendren (2018) to analyze group patterns of intergenerational income mobility. Section 6 concludes. All proofs and some additional plots are deferred to the supplementary material.

2 Setting and proposed methodology

2.1 General setting

Assume that we have repeated observations from individuals . Our goal is to assign the individuals into groups such that individuals in the same group share a set of characteristics. For now, let be given, a data-driven choice of will be discussed at a later point.

Specifically, assume that the characteristics of individual are described by a vector of parameters and that we are interested in grouping individuals according to sub-vectors of . For instance, can be coefficients in a non-linear model linking the response to the covariates and can be the full vector , a sub-vector thereof, or simply the intercept term in a regression model. Specific examples are provided in Section 2.4.

A popular approach to such problems, pioneered by Lin and Ng (2012) and Bonhomme and Manresa (2015), is to interpret this as a clustering problem and apply an iterative approach in the spirit of Lloyd’s k-means clustering algorithm. For concreteness, assume that we only have two groups and that the coefficient vectors 222since the will be left unrestricted, they correspond to the individual specific effects can be estimated by minimizing a loss function via

Roughly speaking, procedures in the spirit of Lin and Ng (2012); Bonhomme and Manresa (2015) consist of an initialization step where individuals are assigned to groups in a randomized fashion, followed by iterative re-assignments until convergence. In the k’th iteration step, denote the group centers from step by . Now individual is assigned to group iff333Bonhomme and Manresa (2015) consider linear least squares models where the individual-specific intercepts can be differenced out. The method presented here is a canonical generalization of their approach to non-linear models where differencing out individual effects may not be possible.

| (1) |

This approach has been adopted to quantile regression by Zhang et al. (2019a). In practice, it has two potential drawbacks. First, for large the cost of each iteration step can be expensive. Second and more importantly, if only initial estimators but not individual level data are available, this approach is infeasible to implement.

Assuming that we only have access to estimators and covariance estimates for , a natural alternative to the iteration step is to assign individual to group iff

| (2) |

For a motivation, note that the problem of assigning individual to group or reduces to classifying an individual into one of two classes. The rule in (2) can now be viewed as an approximate Bayes rule in classification: if are fixed and and the population parameters satisfy , (2) reduces to the Bayes rule which is known to be optimal for minimizing classification error.

2.2 Loss functions versus weighted distances of estimators: a local analysis

To keep the presentation focused and notation simple, consider a single individual and drop the index throughout this section. Assume that the true parameter that generated the data is and that we want to decide based on observations whether the data are generated from parameter or where are given and are unspecified. Let denote the parameter space and define

Denote by a consistent estimator of the asymptotic variance of . Define

and

We also consider a more general approach for a general weight matrix that can depend on the sample size and on the available data

This includes the case of no weighting by setting to be the identity matrix. We will now compare those rules in a local alternative regime where . Assume that the loss function has the following properties.

Assumption 2.1.

-

Assume that are i.i.d. and that further

-

(i)

The map is twice continuously differentiable in a neighbourhood of with symmetric Hessian matrix of full rank.

-

(ii)

The map is differentiable at on a set such that and there exists a measurable function such that almost surely for all in a neighborhood of and .

-

(iii)

For any in a neighbourhood of the function has a well separated (uniformly in ) global minimizer , i.e. for every we have

-

(iv)

The value is in the interior of the parameter space . Either the parameter space is compact or the parameter space is convex and the function is convex almost surely.

It is routine to verify that all of the above conditions hold for two important examples that we will discuss throughout this paper: quantile regression and logistic regression. More generally, parts (i) and (ii) of the assumptions are fairly mild and standard conditions for establishing asymptotic normality and expansions for m-estimators, see for instance Theorem 5.23 and the discussion around it in Van der Vaart (2000). Conditions (iii) and (iv) are added because the proof relies not only on expansions for the original estimator but also for the minimizer of the perturbed objective where . We have opted for simple to state and verify conditions rather than the most general possible ones. The proof of Theorem 2.1 reveals that it is the expansions (25)–(28) in the proof rather than the specific conditions we state above that are needed to establish this result. Such expansions can also be established for data with serial dependence but we do not pursue this direction here as it does not add any insights to our main message.

To state the next result introduce some additional notation. For square matrices of dimension consider the following block structures

with .

Theorem 2.1.

A similar result under even weaker conditions continues to hold if there is no individual-specific and all parameters are estimated globally. The proof of this result is similar in spirit but even simpler and we omit the details for the sake of brevity.

Note that when is a correctly specified negative log-likelihood function, standard regularity conditions yield which further implies by the block matrix inversion formula. In this case so the asymptotic probabilities for rules (1) and (2) selecting the correct center are equal for any . Correct specification of is sufficient but not necessarry. The equality continues to hold in the case where is a scalar multiple of which is the case in least squares or quantile regression with homoscedastic errors, for instance. However, in general models such as quantile regression or ordinary least squares estimation with heteroscedasticity or in the presence of temporal dependence, is not a scalar multiple of in general and thus also . Since rule (2) is always at least as good as (1) asymptotically, this suggests that (2) would be preferable whenever the asymptotic covariance matrix can be estimated consistently, even when (1) is feasible.

The second statement of Theorem 2.1 implies that the proposed scaling with is asymptotically optimal among all possible choices of scale matrix that converge to a fixed matrix.

Although the results presented above only work in a very idealized setting and can not be directly utilized to analyze the performance of rules (1) and (2) when applied inside an iterative procedure, the findings strongly suggest that using the objective function in iteration for group centers might not be optimal from a statistical perspective. Instead, using information on the (asymptotic) variance of the estimators can lead to more efficient procedures. This motivates the ideas in the following section.

Remark 2.1.

The key to proving the first statement of Theorem 2.1 is an asymptotic expansion for the probabilities appearing in (3). Specifically, we derive the following limits

in equation (30) and

in equation (31) in the proof of Theorem 2.1. This is where the matrix comes into play. Given those expansions, (3) follows by an application of the Cauchy-Schwarz inequality as follows

This inequality is strict unless is a scalar multiple of .

2.3 Proposed methodology through the lens of clustering

The discussion up to this point focused on variants of the k-means algorithm for grouping individuals. However, k-means is not the only clustering method which is available and other approaches have been observed to have superior performance in certain settings. Many methods of this type work with general measures of dissimilarity between units and attempt to cluster units that are most similar to each other. Given the developments in the previous sections, a natural measure of dissimilarity is given by

| (4) |

where typically and estimates the variance of . Note that for consistent estimators , will typically converge to zero. This measure of dissimilarity can be computed based on summary statistics and variance estimates and does not require individual level data. The importance of taking variance information into account was illustrated in a simplified setting in Theorem 2.1 and is also confirmed in our simulations. As pointed out by the Associate Editor, using covariance estimates or diagonal versions thereof for has the added benefit of making the procedure scale invariant.

Two popular clustering approaches in the literature that work with general measures of dissimilarity are -medoids Schubert and Rousseeuw (2019) and spectral clustering Ng et al. (2002); Chung and Graham (1997); Von Luxburg (2007). Similarly to -means clustering, the -medoids problem is NP-hard to solve exactly. In practice, approximate solutions to this problem are obtained by employing the algorithm Partitioning Around Medoids (PAM) Reynolds et al. (2006); Schubert and Rousseeuw (2019); Kaufman and Rousseeuw (2005). We refer to (Kaufman and Rousseeuw, 2005, Section 4.1, Chapter 2) for more details about the PAM algorithm. As we observe in simulations, using the PAM algorithm with dissimilarity measure (4) can already lead to substantial gains relative to the iterative k-means style approaches of Lin and Ng (2012); Bonhomme and Manresa (2015); Zhang et al. (2019a). However, extensive simulations showed that in all settings considered spectral clustering leads to even more accurate group estimation than PAM, and hence we focus on spectral clustering in the theoretical developments that follow. Simulation evidence for the superiority of spectral clustering over to PAM is presented in Section 4.

Since there are many variations of spectral clustering that are available in the literature, a detailed description of the specific version we use is given in Algorithm 1444We do not claim any novel contributions to this specific algorithm, the details and explanation are presented here for the reader’s convenience..

Input: Number of clusters , dissimilarity matrix computed in (4).

Output: Clusters .

To intuitively understand the motivation behind the above algorithm observe that the dissimilarities can be expected to be large if individuals are from different groups. In the limit those distances will tend to infinity, and thus whenever are from different groups. Similarly, can be expected to be bounded when are in the group, and thus will usually be bounded away from zero for such pairs. Thus after rearranging the order of individuals we see that will be approximately block diagonal with non-zero entries in the blocks. It is now straightforward to see that will have exactly zero eigenvalues if there are such blocks and all other eigenvalues will be strictly positive. Moreover, the eigen-space corresponding to zero eigenvalues will have an orthogonal basis consisting of vectors that have non-zero entries in the exact components corresponding to different groups, see also the discussion surrounding equation (32) and Lemma 9.1 in the supplementary material. For a more detailed discussion of the intuition and alternative formulations of the spectral clustering algorithm see Von Luxburg (2007) and the literature cited therein. Although the last step of the algorithm uses the standard -means algorithm, we note that it is applied on the rows of which is a standard clustering problem with data points in Euclidean space. No refitting of models on individual level or large scale models as in Bonhomme and Manresa (2015) is required.

Some additional comments on specific choices that we made in Algorithm 1 are in order. First, in step (1), we apply an exponential kernel to the dissimilarity matrix. Other monotone transformations can be used, for instance the Gaussian kernel is another popular choice. Our simulation exercise confirms that both the exponential kernel and the Gaussian kernel perform similarly. Second, in step (3), we apply a normalization to the graph Laplacian for the spectral clustering analysis. A line of seminal works (Von Luxburg et al. (2004) and Von Luxburg et al. (2008)) investigate the convergence of the normalized and unnormalized versions of the popular spectral clustering algorithm. They demonstrate that the normalized spectral clustering converges under very general conditions, while the unnormalized spectral clustering is only consistent under strong additional assumptions, which are not always satisfied in real data. These works give strong evidence for the superiority of normalized spectral clustering.

Remark 2.2.

Wang and Su (2021) also observe that the spectral decomposition of a certain matrix that is derived from individual-specific estimators contains information on the latent group structure. However, there are several crucial differences between their and our approach. Most importantly, we explicitly take into account the uncertainty that is associated with individual-specific estimators while Wang and Su (2021) work directly with raw estimators. Moreover, Wang and Su (2021) do not apply spectral clustering directly but rather use certain eigenvectors as input to a binary segmentation algorithm. For a simulation-based comparison with that method, see section 4.1.

The idea to use spectral clustering for grouping different entities also appeared in van Delft and Dette (2021). The setting in the latter paper is very different from ours since van Delft and Dette (2021) consider grouping locally stationary functional time series and do not take into account estimation uncertainty when constructing their dissimilarity measure between observations. Still, some parts of our theoretical analysis under high-level assumptions are related to theirs, additional comments on this can be found in Remark 3.1.

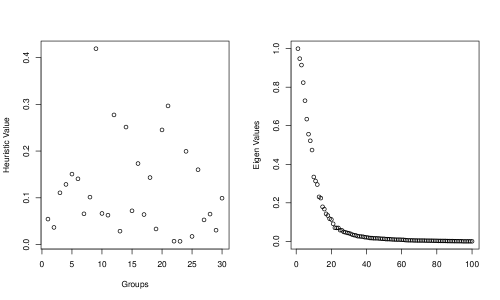

So far we discussed an algorithm for assigning individuals to groups for any given . In some settings, will be chosen based on domain knowledge about the problem at hand. If no such knowledge is available, we propose to select the that maximizes the relative eigen–gap (Von Luxburg (2007)) of a modified graph Laplacian More precisely, consider the scaled dissimilarity Use as input to Algorithm 1 and obtain as output from step 3 of that algorithm. Consider the values with denoting the ordered eigenvalues of . The estimated number of groups is

| (5) |

The motivation for using the scaling in is that, under technical assumptions made later, this scaling ensures for all in the same group. Without this scaling, the heuristic tends to have a small probability of not selecting a correct number of groups as increases.

Similar heuristic eigen-gap methods for estimating the number of groups can also be found in van Delft and Dette (2021); John et al. (2020); Little et al. (2020), among many others.

Remark 2.3.

There are at least two other popular approaches to selecting the number of groups or equivalently the number of clusters. The first type of method combines cross-validation with the idea that “true” cluster assignment should be stable under small perturbations of the data. This idea was exploited in Wang (2010) for selecting the number of clusters in a general setting and adapted by Zhang et al. (2019a) to selecting the number of groups for panel data quantile regression. However, as pointed out in Ben-David et al. (2006), methods that select the number of clusters based on stability can fail for certain cluster configurations. One such example will be given in the simulation section, see Model 2 in section 3.2.2 . The second drawback of such methods is that clustering stability can only be defined when there are at least two clusters. Hence, by construction, stability methods always select at least two clusters and fail if there is only a single cluster in the data.

The second method uses information criteria which select the number of clusters that maximize a sum of objective function plus penalty, see for instance Su et al. (2016); Gu and Volgushev (2019); Wang and Su (2021) among many others. The main drawback of such approaches is that information criteria need to be derived case by case as they differ depending on the specific form of the objective function making them difficult to use for applied researchers. We note that this is different from the classical setting involving AIC and BIC in a maximum likelihood framework where only the number of parameters in the model matters. Moreover, computation of such information criteria typically requires access to raw data which might not always be available as in our second application. The information criteria method also involves the heaviest computation burden because to construct the information criteria statistics, all candidate models with varying values of need to be estimated which can be costly (See computation time comparison in Section 4.1).

2.4 Examples

The setting above is generic and so far we did not assume anything about the specific structure of the estimators. In the remainder of this section, we provide several illustrative examples of model specifications that were considered previously and show how those examples fit into the proposed framework.

Example 2.1 (Logistic regression regression with individual-specific intercepts and grouping on slopes).

Consider binary responses and assume that

where and . We leave the unrestricted and assume that certain sub-vectors of have a group structure.

Su et al. (2016) considers a similar model; they assume a Gaussian link function for the binary response. Ando et al. (2022) also considers the logit model with individual specific slope coefficients and a factor structure on the individual fixed effects. Their way of modeling unobserved heterogeneity is different from ours as we focus on group patterns.

Example 2.2 (Quantile regression with individual-specific intercepts and grouping on slopes).

Given the observations are assume that the conditional quantile function of the response given covariates for individual satisfies

where are unrestricted and we search for a group structure on .

This setting was also considered in Zhang et al. (2019a), Leng et al. (2023). Zhang et al. (2019a) propose an iterative algorithm based on the -mean algorithm in Bonhomme and Manresa (2015) to learn group structure. Leng et al. (2023) use a -means type of iterative algorithm, but allow for time fixed effect while grouping both the individual fixed effects and the slope coefficients. This model will be considered in Section 5 where coefficients of the panel quantile regression model will be utilized to analyze heterogeneous relationship between income and pollution level among different states in the US.

Example 2.3 (Quantile regression with joint slope and grouping on intercepts).

Assume that the conditional quantile function of response given covariates for individual is

where the vector of slope coefficients is assumed to be the same across individuals.

This model was first considered in Koenker (2004), who proposed to regularize the individual fixed effects via penalization. Lamarche (2010) considers the optimal choice of the penalty parameters in this approach. There has been an active literature on panel data quantile regression, mainly focusing on estimation of the common parameters (e.g., Kato et al. (2012), Galvao and Kato (2016), Harding and Lamarche (2017) and Galvao et al. (2020)). Zhang et al. (2019b) and Gu and Volgushev (2019) consider group structure on .

3 Theoretical Analysis

3.1 Generic spectral clustering results

In this section, we provide high-level conditions on the estimators and which ensure that the correct group structure is recovered with probability tending to one as tend to infinity. Formally, assume that the true coefficients take different values, say and the true group membership is given by

where denote the true underlying groups. Naturally, we assume for . We begin by providing an analytical non-asymptotic result which guarantees perfect classification in terms of certain abstract quantities. More precisely, define

Theorem 3.1.

A sufficient condition for perfect classification is

| (6) |

Theorem 3.1 holds for fixed and is proved in a purely analytic way. The result does not assume anything about temporal or cross–sectional dependence. On a high level, this result corresponds to intuition as the inequality in (6) becomes more difficult to satisfy for a larger number of groups or when groups have more unbalanced sizes leading to a larger ratio . Having more individuals (larger ) also intuitively makes the problem harder. In order to achieve perfect classification, a large minimal dissimilarity between individuals from different groups, i.e. a small , relative to , is required. The ratio describes the spread of similarity measures among individuals that belong to the same group. Having a large spread here makes the problem harder, which again corresponds to intuition. Note that this is only a sufficient condition, and sharper results might be possible. However, we are not aware of any necessary and sufficient conditions guaranteeing the success of spectral clustering or sharp expansions for the proportion of correctly grouped units.

Remark 3.1.

The proof relies on the type of arguments that appeared in earlier work on spectral clustering, in particular Ng et al. (2002), Von Luxburg (2007) and van Delft and Dette (2021). However, the setting we consider is different from any of the works mentioned above and the arguments need to be modified accordingly. The work of van Delft and Dette (2021) is closest in spirit, but our analysis is complicated by the fact that we allow the number of individuals to diverge while the number of entities to be clustered was fixed in van Delft and Dette (2021). In order to deal with this complication, we leverage the fact that our construction of the similarity matrix gives rise to the different order for the diagonal blocks and off-diagonal blocks of the empirical Laplacian matrix. Taking advantage of this difference in order together with spectral information contained in the diagonal blocks of the empirical Laplacian matrix allows us to handle a diverging number of individuals.

Below, we will provide more specific assumptions on the minimal separation of group centers and quality of initial estimators which guarantee that the probability of the events in (6) tend to one. In the assumptions below, we allow for data from triangular arrays where the values of and change with . To keep the presentation simple this is not emphasized in the notation. We also allow the number of groups to grow with .

Assumption 3.1.

The estimators are uniformly consistent with rate , i.e.

Assumption 3.2.

There exists a sequence and matrices (which may depend on ) such that

where denotes the spectral norm. Moreover, assume

| (7) |

with some fixed constants that do not depend on .

Assumptions 3.1 and 3.2 impose minimal restrictions on the quality of the initial estimates and . We emphasize that the matrices in Assumption 3.2 are not required to be equal to the true asymptotic covariance matrices of for the theory to work. This is a useful result because in some environments researchers only have access to individual estimates and the associated coordinate-by-coordinate standard deviation, but the covariances estimate are missing. In such cases, our method can still be used by setting the off-diagonal elements of to zero. Assumption 3.2 will hold provided that the variance estimators on the diagonal converge to non-negative values. While setting off-diagonal entries to zero might not be optimal in the asymptotic setting of Theorem 2.1, simulations indicate that in finite samples the performance can be close to using consistent estimates of the covariance. When covariances are difficult to estimate, using only the diagonal entries can even enhance finite sample performance as we will see in Section 4.1. Similarly, this assumption can be satisfied if there is dependence across individuals but this dependence is ignored when estimating the covariance of . Again, ignoring this dependence will not lead to procedures with best possible performance but might work reasonably well if the dependence across individuals is mild.

In all examples we consider later the individuals will be assumed independent and the estimators will satisfy By independence among individuals, the weak convergence above holds jointly for any given pair of individuals and the corresponding limits will be independent. In this case, we will set , , where will be consistent estimators of .

The bound in is uniform over a potentially growing number of individuals and typically be of the form where the additional factor is to ensure uniformity.

We now have the following result

Theorem 3.2.

In order to achieve perfect classification with probability going to one, Theorem 3.2 requires lower bounds on the minimal separation which is required to grow faster than the uniform estimation error and than . In the special setting discussed above the Theorem where , this corresponds to assuming that . For groups with fixed separation across centers where is a constant, this leads to the requirement which allows the number of individuals to grow very quickly with . If the minimal separation tends to zero, the requirements on relative to become more stringent.

Given the non-asymptotic bound in (6), it would also be possible to conduct a more detailed analysis in the case where the orders of and match but is sufficiently large so as to dominate a constant multiple of with a certain probability. Such an analysis would reveal more nuanced view on the role of and but does not lead to any specific insights except that large and imbalanced groups make the problem harder.

3.2 Verification of high level conditions for specific examples

In this section, we provide specific conditions in Example 2.1–Example 2.2 which guarantee that the high-level conditions 3.1 and 3.2 are satisfied. The set of examples that we consider is by no means exhaustive for the possible applications of our methodology. Rather, it is intended as a demonstration that our high-level conditions can be verified in several different settings including the presence of individual-specific and joint parameters, binary outcomes, and non-smooth objective functions.

3.2.1 Logistic regression with individual-specific intercepts and grouping on the slopes (Example 2.1)

The coefficient vector is estimated via maximum likelihood, i.e.

The exact form of the asymptotic variance differs depending on whether the data exhibit temporal dependence. We begin by discussing the case that the observations are i.i.d. across and independent across and discuss the case with temporal dependence across later in this section. Throughout, the values of are allowed to depend on .

Recall that in the i.i.d. case under standard assumptions the estimator is asymptotically normal with asymptotic variance given by

The canonical plug-in estimator of takes the form

Denote by the lower sub-matrix of . Then we set

| (9) |

Consider the following assumptions.

Assumption 3.3.

Assume that for a constant independent of

and there exists independent of such that .

Assumption 3.4.

Assume a.s. for a constant that does not depend on .

Assumption 3.3 places mild restrictions on the design matrix. The boundedness condition in Assumption 3.4 is made for the sake of simplicity; it can be relaxed to designs with bounded moments at the cost of additional technicalities in the proofs.

Theorem 3.3.

Theorem 3.3 implies that Assumptions 3.1 and 3.2 hold with , and corresponding to the scaled asymptotic variance matrix of . In particular, (8) is satisfied provided that .

Note that the results directly imply that Assumptions 3.1 and 3.2 continue to hold for any sub-vectors of . This covers settings where we want to leave some coefficients individual-specific and only perform grouping on a part of the full coefficient vector.

We now proceed to consider the case of temporal dependence.

Assumption 3.5.

For each , the process is strictly stationary and -mixing. Let denote the -mixing coefficient of the process . Assume that there exist constants independent of such that

where

Such exponential mixing assumptions are often made in the literature, see for instance Kato et al. (2012) and Galvao et al. (2020) in the context of quantile regression.

The available data are an observed stretch from the strictly stationary process . Under this assumption, the asymptotic variance of the estimator is of the form

with

where . A possible sandwich estimator of the asymptotic variance takes the form

where

and denotes the bandwidth parameter tending to be infinity as goes to infinity. Denote by the lower sub-matrix of . Then we set

| (12) |

Theorem 3.4.

Let Assumptions 3.3, 3.4 and 3.5 hold.

Assume grows at most polynomially in and . Assume that the smallest and largest eigenvalues of are bounded away from zero an infinity uniformly in .

(i) It holds that

| (13) |

(ii) In addition, if as and , the estimators satisfy

| (14) |

where denotes the lower submatrix of . Furthermore satisfy (7) .

3.2.2 Quantile regression with individual-specific intercepts and grouping on the slopes (Example 2.2)

Consider the quantile regression panel data model

where is the conditional - quantile of given

We will first assume that are i.i.d. across for each and independent across . An extension to temporal dependence as in Assumption 3.5 will be considered below. The distribution of and the values of are allowed to vary with .

Consider the quantile regression estimator

where denotes the check function.

Under mild regularity assumptions (in particular, this is true under Assumptions 3.6–3.8 given below) this estimator is asymptotically normal with asymptotic covariance matrix of the form where

| (15) |

with as the density function of the conditional distribution

A common way to estimate uses the Hendricks-Koenker sandwich covariance matrix estimator (Hendricks and Koenker (1992)) which takes the following form

| (16) |

Here denotes a smoothing parameter that should converge to zero at an appropriate rate. Let denote the lower submatrix of and set

| (17) |

Assumption 3.6.

Assume that , and that holds uniformly in for some fixed constants and that are independent of .

Assumption 3.7.

Define .The conditional distribution is twice differentiable w.r.t. , with the corresponding derivatives and . Assume that

where are independent of .

Assumption 3.8.

Denote by an open neighborhood of . Assume that uniformly across , there exists a constant independent of such that

Assumption 3.9.

Assume that , as and

Assumptions 3.6-3.9 are fairly standard in the quantile regression literature and have been imposed in Kato et al. (2012) and Galvao et al. (2020) among many others.

Theorem 3.5.

Let Assumptions 3.6-3.8 hold.

Assume and . Assume that the data are i.i.d. across and independent across .

(i) It holds that

In particular, Assumption 3.1 holds with provided that .

(ii)

If in addition to the above Assumption 3.9 holds, then Assumption 3.2 is also satisfied with , denoting the lower sub-matrix of and defined in (20).

Theorem 3.3 implies that Assumptions 3.1 and 3.2 hold with , and corresponding to the scaled asymptotic variance matrix of .

Similarly to the discussion in Section 3.2.1, the results directly imply that Assumptions 3.1 and 3.2 continue to hold for any sub-vectors of .

We now consider the dependent case. Since we need to account for the temporal dependence structure, the asymptotic covariance matrix for the estimator is now of the form where the matrix is defined in (15) as in the independent case, whereas the matrix is defined in the following way incorporating the dependence

with This motivates the following generalized version of the Hendricks-Koenker sandwich covariance matrix estimator

| (18) |

where is defined in the same way as in the independent case and the estimator is defined via

Here, denotes the bandwidth parameter tending to be infinity as goes to infinity, and

To establish the asymptotic consistency of the covariance estimator, we need following additional assumptions.

Assumption 3.10.

For each and , the random vector has a density conditional on and this density is bounded uniformly across and .

A similar assumption was made in Kato et al. (2012).

Assumption 3.11.

Assume that and as , and

This assumption is similar to Assumption 3.9 and imposes a restriction on the relative growth of the time dimension compared to the number of individuals.

Theorem 3.6.

Let Assumptions 3.6-3.8, and 3.5-3.10 hold.

Assume grow at most polynomial in , , and . Assume that the smallest and largest eigenvalues of are bounded away from zero and infinity uniformly in .

(i) It holds that

| (19) |

In particular, Assumption 3.1 holds with .

(ii) If in addition to the above Assumption 3.11 holds, then Assumption 3.2 is also satisfied with , denoting the lower sub-matrix of and denoting the lower submatrix of

| (20) |

3.2.3 Quantile regression with common slope and grouping on the intercepts (Example 2.3)

Consider the quantile regression panel data model

where denotes the conditional - quantile of given In contrast to the setting in Section 3.2.2, we assume that the slope coefficient is common across individuals and are only interested in grouping the intercepts. This model was considered in Gu and Volgushev (2019), who used a lasso-type penalty to enforce grouping on the intercepts . The latter paper also demonstrated that putting this kind of regularization on can result in improved estimation of compared to leaving unrestricted.

Assume that are i.i.d. across for each and independent across . Since only intercepts contain the grouping information, we aim to use the estimates for and their variance estimates to construct the similarity matrix. At this point, there are two possibilities for estimating : (1) run individual-specific quantile regressions ignoring the fact that is common across individuals or (2) put all individuals into a single large model in order to borrow information across individuals to improve the efficiency in estimating the joint coefficient vector .

Approach (1) has computational advantages, especially if is large, but can also result in a loss of efficiency. The theoretical treatment of (1) easily follows from minor modifications of the results in Section 3.2.2, and we hence focus on the second approach. Define

| (21) |

In what follows, we assume that which is the more relevant case for group structure detection. In this case, it is possible to obtain simplified estimators for the asymptotic variance of . Those estimators will be motivated next.

The main insight is that under the estimation of has a negligible effect of the asymptotic variance of since is estimated at a faster rate due to borrowing information across individuals. Further observe that, defining , we have

| (22) |

Thus is approximately the sample quantile of , which should be close to the sample quantile of where .

If this idea can be formalized by applying a modification of Lemma 7 in Galvao et al. (2020) (after noting that the proof of the latter result can be modified to weaken the assumption made in there). Denoting the sample quantile of by , the latter result implies

Observing that by the proof of Theorem 3.2 in Kato et al. (2012) we have when (note that this part of their result does not require the restrictive growth assumption on which is needed for unbiased asymptotic normality of ), this implies uniformly over and thus the asymptotic distributions of and coincide. Now classical results on the distribution of sample quantiles imply that the asymptotic variance of is

| (23) |

where denote the (unconditional) density and quantile function of , respectively.

This motivates the following version of : for a bandwidth parameter define

and compute

| (24) |

Theorem 3.7.

We next consider the case of temporal dependence. Under Assumptions 3.5–3.10 the asymptotic variance takes he form

This can be estimated consistently by

where denotes the bandwidth parameter tending to be infinity as goes to infinity, and

Theorem 3.8.

Let Assumptions 3.6-3.8, and 3.5-3.10 with hold.

Assume grows at most polynomially in , , and .

(i) It holds that

where is defied in (22).

In particular, Assumption 3.1 holds with .

(ii)

If in addition to the above Assumption 3.11 holds, then Assumption 3.2 is also satisfied with , where are defined in (23), and defined in (24).

4 Numerical experiments

In Section 4.1 and Section 4.2, we report the performance of different algorithms in terms of assigning individuals to groups when the true number of groups is specified. We consider two performance metrics: perfect matching, which corresponds to the proportion of times that the exact group assignment is found, and average matching. The latter is computed as follows. Define the true cluster assignment as a set where denotes the -th group to which the individual belongs. Define the set of permutations of the labels Define the estimated membership as a set where denotes the estimated group number of the -th individual. We define the average percentage of correct classification of the estimated membership as

A similar approach was taken in Su et al. (2016); Gu and Volgushev (2019); Leng et al. (2023). The performance of the heuristic (5) for selecting the number of groups is considered in Section 4.1.2 for logistic regression and in Section 4.3 for quantile regression. Additional models and simulation settings are discussed in the supplement.

4.1 Logistic regression

In this section, we consider logistic regression with individual-specific intercepts and groupings on the slopes specified as

where follows a logistic distribution, for all and with equal proportions, and . Moreover,

We consider two different data generating processes for the covariates . For Model 1,

where and and

Here, the data generating process is constructed such that the coefficient of is not informative on the group structure while at the same time it is estimated less precisely. On the contrary, the coefficient of is informative on group structure and also precisely estimated.

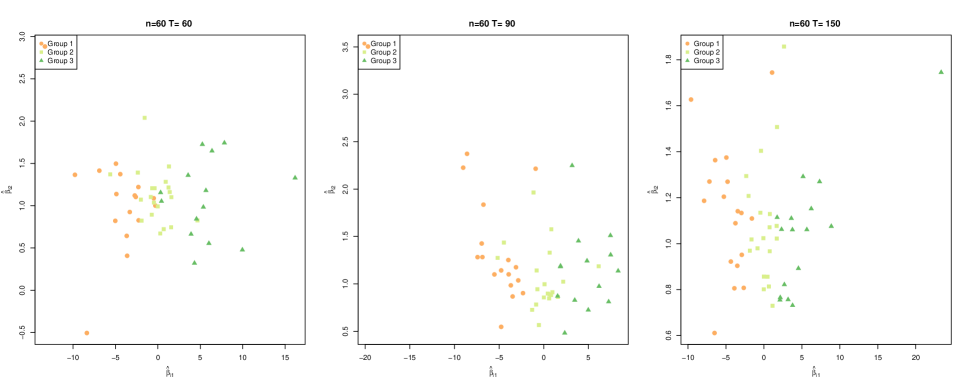

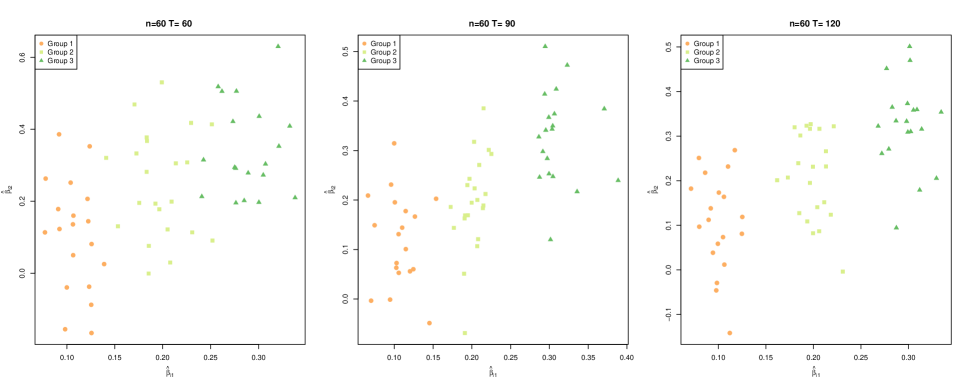

For model 2, we switch the labels of and . This is a more challenging DGP because the coordinate of that contains group information is estimated with a lot of noise; see the scatter plot of in Figure 1 for a data realization from Model 1 versus Model 2.

4.1.1 Clustering with a known number of groups

We first compare our method with the C-LASSO proposed by Su et al. (2016). The C-LASSO approach proposed in Su et al. (2016) considers minimizing the following objective:

This itself is not a convex optimization, but at each , we can focus on only the -th element in the product term in the penalty, resulting in a convex program. For details of the implementation, we refer to our supplement or Su et al. (2016). In addition, we also consider an interative -means approach in the spirit of Bonhomme and Manresa (2015). In particular, in each iterative step, we re-estimate group membership based on the logit likelihood function, and then refit the model until coefficients converge. We also compare to the Sequential Binary Segmentation Algorithm (SBSA) in Wang and Su (2021) (labeled as SBSA in Table 1. The SBSA method applies the binary segmentation algorithm to detect break-points in eigenvectors from the spectral decomposition of the outer product of that corresponds to the largest eigenvalues where is the number of covariates.

| Model 1 | |||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Perfect Match | Average Match | ||||||||||||||||||||||

| n | T | S | PAM | S-Diag | S-Iden | C-LASSO | -means | SBSA | S | PAM | S-Diag | S-Iden | C-LASSO | -means | SBSA | ||||||||

| Model 2 | |||||||||||||||||||||||

| Perfect Match | Average Match | ||||||||||||||||||||||

| n | T | S | PAM | S-Diag | S-Iden | C-LASSO | -means | SBSA | S | PAM | S-Diag | S-Iden | C-LASSO | -means | SBSA | ||||||||

The first few rows in Table 1 report the performance of four different grouping methods for several combinations of and based on Model 1. We evaluate the performance by the proportion of perfect matches out of 100 simulation repetitions and the average matches described at the beginning of Section 4. The spectral clustering method works consistently better than the PAM approach (labeled PAM).

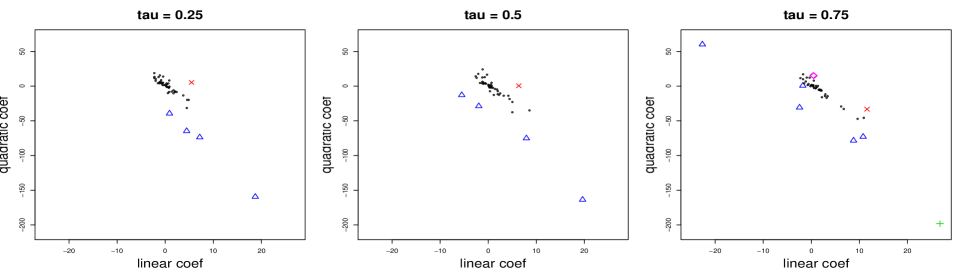

From local analysis in Section 2.2, one might expect that PAM and the iterative k-mean method should perform similarly. However, that analysis is asymptotic and inspecting the scatter plot of in Figure 1 suggests that the coefficient estimates are not yet approximately Gaussian around their true values. Hence the asymptotic analysis may not provide a sufficiently accurate description of finite sample performance at the sample sizes considered in this simulation. We also note that there are non-convergence issues with the iterative k-means method. For , in of the cases none of the random initialization lead to convergence after iterations and in of all cases the initialization that led to the best likelihood function did not correspond to convergence after 100 iterations.

In addition, the non-Gaussian shape of the point clouds may also provide an explanation for the superior performance of the spectral clustering method over PAM, since spectral clustering is known to have an advantage for clusters with non-elliptical shapes.

For small , using the diagonalized estimated variance-covariance matrix (labeled S-Diag) actually performs slightly better than using the full estimated variance-covariance matrix (labeled S). In finite samples, the off-diagonal terms of the variance-covariance matrix can be poorly estimated and using just the diagonal variance information seems to provide a small margin of better performance. However, discarding variance information completely (labeled S-Iden) clearly shows much worse performance. The iterative -mean method performs much worse than spectral clustering with variance information in terms of perfect match. Its average match performance is in fact better than the spectral method when the variance information is not accounted for. This shows that spectral clustering needs to be applied together with variance information for good performance. We also note that the iteration k-means method sometimes does not converge after 100 iterations, which may explain why performance is not improving monotonically as increases. The SBSA approach in Wang and Su (2021) has better performance than the k-mean method for perfect match proportion in Model 1, but is still inferior to CLASSO, PAM, and spectral clustering with variance information.

For C-LASSO, the penalty tuning parameter is set at as recommended by the authors with a few different values of specified in the caption of Table 1. We see that the C-LASSO can perform very well for a suitably chosen constant, and our method matches that or overperforms sometimes. However, it can perform poorly if the tuning parameter constant is not chosen carefully. This imposes challenges for its practical usage.

Performance for Model 2 is reported in the last few rows in Table 1. We clearly see that this is a much more challenging DGP with almost all methods failing to recover perfect match for group membership. In terms of average matches, our method still performs comparable or sometimes better than all other methods for all combinations of and .

4.1.2 Estimating the number of groups

Simulation results in Table 1 assume the researchers know the correct number of groups . We report in Table 2 the performance of the proposed method for estimation of . The comparison is made with the information criteria proposed in Su et al. (2016). For Model 1, both methods work very well while for Model 2, the information criteria of Su et al. (2016) works much better across most combinations of . The information criteria relies on the whole sample to estimate while our heuristic approach only requires information on individual based estimates.

| Model 1 | |||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Heuristic | IC-CLASSO | ||||||||||||

| n | T | 1 | 2 | 3 | 4 | 5 | 1 | 2 | 3 | 4 | 5 | ||

| 0.89 | 0.98 | ||||||||||||

| 0.98 | 0.99 | ||||||||||||

| 1.00 | 0.94 | ||||||||||||

| 0.98 | 1.00 | ||||||||||||

| 1.00 | 1.00 | ||||||||||||

| 1.00 | 0.94 | ||||||||||||

| Model 2 | |||||||||||||

| Heuristic | IC-CLASSO | ||||||||||||

| n | T | 1 | 2 | 3 | 4 | 5 | 1 | 2 | 3 | 4 | 5 | ||

| 0.00 | 0.15 | ||||||||||||

| 0.04 | 0.20 | ||||||||||||

| 0.22 | 0.40 | ||||||||||||

| 0.00 | 0.01 | ||||||||||||

| 0.02 | 0.08 | ||||||||||||

| 0.36 | 0.36 | ||||||||||||

4.1.3 Computation times

In what follows, Table 3 reports the computation times for our method versus C-LASSO, the iterative k-means method which requires iteration with the whole sample as well as SBSA proposed in Wang and Su (2021). The run time of SBSA is very similar to our proposed method because it also only required the use of individual coefficients. For C-LASSO the reported times are based on maximum 20 iterations for optimization. The final estimates are obtained when the objective function differs less than 0.001 and when the norm of the estimates group centers differ by less than or when the maximum iterations are reached. For the iterative k-mean method, we take 20 random start of group membership and pick the best estimates that minimizes the loss function criteria. For each random starting, the maximum number of iteration is 100. With known , our method and the SBSA method has the least computational time while the iterative k-means has the largest. This is because quite often the k-mean algorithm does not converge before the maximum 100 iterations is reached. Our algorithm spends most of its computation time on individual based estimates. For the C-LASSO method, the individual estimates are computed as initial estimates before applying a re-optimization with the penalty terms for group center estimates. Because the optimization problem is only convex for optimizing over one group center while fixing the others, it has to optimize group by group, which increases computation times. The iterative k-means method takes the most computation time, as it requires individual loops to decide group membership until convergence as well as refitting to obtain group center estimates. In practice, we observe that it may take a very large number of iterations to converge. When is not known, the computation time of our method does not increase because the heuristic method recycles already computed similarity measures to estimate . The SBSA method uses a IC criteria to estimate . Because grouping is obtained very fast for each candidate model and the IC criteria just needs to evaluate the likelihood of each estimated candidate model, the increase in computation time is also very minimal. Both the C-LASSO and k-means rely on information criteria to estimate which requires fitting of all candidate models with varying . Hence computation times grow at least linearly with the number of candidate models. The reported times in Table 3 are based on candidate models with .

| Known G | Estimate G | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| n | T | Spectral | C-LASSO | Kmeans | SBSA | Spectral | C-LASSO | Kmeans | SBSA | |

| 30 | 60 | 0.32 | 5.88 | 13.23 | 0.38 | 0.32 | 31.75 | 86.27 | 0.44 | |

| 30 | 90 | 0.38 | 6.55 | 24.76 | 0.44 | 0.38 | 39.94 | 122.75 | 0.50 | |

| 30 | 150 | 0.42 | 6.87 | 52.69 | 0.43 | 0.43 | 48.09 | 245.97 | 0.52 | |

| 60 | 60 | 1.26 | 10.15 | 48.27 | 0.77 | 1.28 | 59.48 | 445.17 | 0.94 | |

| 60 | 90 | 1.47 | 11.10 | 197.70 | 0.80 | 1.52 | 79.38 | 742.79 | 1.12 | |

| 60 | 150 | 1.61 | 12.30 | 225.92 | 0.85 | 1.61 | 123.48 | 801.23 | 1.34 | |

4.2 Quantile regression

In this section, we consider quantile regression with individual-specific intercepts and grouping on the slopes as in Example 2.2, and with joint slope and grouping of intercepts from Example 2.3. We focus on the clustering performance with a given (correctly specified) number of groups, the performance of the proposed heuristic, and several other methods for selecting the number of groups is considered in Section 4.3.

4.2.1 Quantile regression individual–specific intercepts and grouping on slopes

Recall the model specification in Example 2.2: This setting was also considered in Zhang et al. (2019a) and we will compare the performance of the proposed method with theirs. Simulations are done in the quantreg package in R. Covariance estimates are computed using the function summary.rq() with option se="nid" and default bandwidth choice hs=true.

We consider three models. Model 1 corresponds to Model 3 from Zhang et al. (2019a).

Model 1:

where

Set

and

Results for are reported in Table 4. We considered the PAM method as well as several variants of spectral clustering. In particular, refers to spectral clustering when we apply the Gaussian kernel instead of the exponential kernel in Algorithm 1. S-Diag is spectral clustering when we use only the diagonal entries in the variance-covariance matrix and sets the off–diagonal entries to zero. S-Iden is spectral clustering when we do not use the variance covariance information of the coefficient estimates. k- applies the k-mean clustering algorithm on and ZWZ19 is the method in Zhang et al. (2019a) which adapts the iterative method of Bonhomme and Manresa (2015) to the quantile regression case.

Spectral clustering shows uniformly best performance in terms of average and perfect matching across all settings considered. The approach of Zhang et al. (2019a) comes close in terms of average matching and is better than both methods which ignore variance information (S-Iden and k-) but is slightly worse than PAM and the spectral method. This agrees with the theoretical analysis in Section 2.2 which suggests that for a heteroscedastic model as in Model 1, the loss function based approach implicitly takes into account variance information, but is not as efficient as using the dissimilarity measure as in Algorithm 1. Surprisingly, Zhang et al. (2019a) shows much worse performance in terms of perfect matching. A closer look at the results revealed that in this model the method of Zhang et al. (2019a) often assigns one individual to the wrong group, resulting in good average matching but inferior perfect matching performance. Despite our best efforts at varying various parameters of Zhang et al. (2019a) (e.g. criteria for termination and number of random starting points), we were not able to alleviate this issue. Among spectral methods, using the Gaussian kernel to transform the dissimilarity measure does not lead to improvements in terms of performance. Using just the diagonal of the variance-covariance matrix also yields almost identical performance than using the estimated full variance-covariance matrix. We do note that the PAM method is slightly worse than the corresponding spectral clustering method. This seems to be a persistent phenomenon we observe in all the simulations for quantile regression. Moreover, we provide the scatter plot of in the online Appendix (Section 8 Figure 5) for a data realization where the proposed method achieves perfect matching but all the other methods fail. The figure suggests that there seems to be clear separation along the first coordinate, but not in the second coordinate of , which is driven by the fact that the second coordinate is estimated with more noise. However, this information is not available to the researcher. Accounting for the variance information improves the performance compared to methods that do not account for this. The loss function based method of Zhang et al. (2019a) implicitly accounts for this to some extent, but less well than reweighting.

The simulation findings suggest that the main improvements in our proposal are due to using variance information, while using spectral clustering instead of PAM only leads to modest additional gains. The results here are also consistent with the local analysis in Theorem 2.1 since this is a model with heteroscedastic errors.

The second model we consider has four groups, with pairs of group centres being close together. Both entries of the coefficient vector carry information about the group structure, but one of them is estimated more precisely than the other one.

Model 2:

where

Set

and set

Results for are reported in Table 5. The results are fairly similar to those of Model 1, the proposed method has the best performance with respect to perfect and average match. The design of this DGP is also used later for estimation of to demonstrate the drawback of stability based method proposed in Wang (2010). Again, the main performance boost comes from using reweighting and using spectral clustering instead of PAM only leads to small additional accuracy gains.

| n | T | Perfect Match | Average Match | ||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| S | PAM | S-Diag | S-Iden | - | ZWZ19 | S | PAM | S-Diag | S-Iden | - | ZWZ19 | ||||||

| n | T | Perfect Match | Average Match | ||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| S | PAM | S-Diag | S-Iden | - | ZWZ19 | S | PAM | S-Diag | S-Iden | - | ZWZ19 | ||||||

Model 3: The last model we consider has the same specification as Model 1, except that we allow individuals to have varying time period lengths and individuals with shorter panel length are expected to be estimated with larger standard error. This resembles many macroeconomic settings where individual units have varying panel length and hence individual based estimates are of very different quality. In the simulation, the panel lengths are a random draw from with equal probabilities. Results are summarized in Table 6. The overall performance deteriorates in comparison to Table 4 since some individuals with shorter panel length are estimated with more noise. The spectral clustering methods ( and S) perform comparably. Using just the diagonal information of the covariance matrix yields equally good performance, but not using the covariance information at all clearly performs worse. The vanilla k-means method again performs very similarly to spectral clustering without accounting for variance information. The method proposed by Zhang et al. (2019a) is competitive, improves upon estimates not using variance information, but is slightly inferior to PAM and our proposed spectral clustering methods.

| n | Perfect Match | Average Match | ||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| S | PAM | S-Diag | S-Iden | - | ZWZ19 | S | PAM | S-Diag | S-Iden | - | ZWZ19 | |||||

4.2.2 Quantile regression with joint slope and grouping on intercepts

In this section, we consider the setting in Example 2.3. The spectral clustering approach is based on the estimators for the slopes and variances described in Section 3.2.3. More precisely, recall the definition of in (21) and defined in (24). The variation matrix which we use as input to the spectral clustering algorithm is given by For comparison, we also consider spectral clustering setting all variance estimators set to be equal, the naive -means approach on estimated from (21), and the convex clustering procedure of Gu and Volgushev (2019). Tuning parameters for Gu and Volgushev (2019) were set as described in the latter paper. The following model corresponds to DGP1 location scale shift model in Gu and Volgushev (2019).

Model 4:

where and where and are independent and identically distributed from standard normal distribution over , respectively.

Tables 7 summarizes the proportion of perfect classification and the average of the percentage of correct classification based on the proposed method with both exponential and the Gaussian kernel (denoted as S and respectively). Spectral clustering ignoring variance information is denoted as S-Iden, and -means clustering on is denoted as - along with the PAM method for clustering. The procedure from Gu and Volgushev (2019) is denoted as GV.

In this model, including variance information is not helpful (S versus S-Iden). A possible explanation for variance information not being useful in this model is that the are one-dimensional and there are no directions of larger or smaller variation in their estimates. The PAM and vanilla k-means performs identical in this model. The key difference is that PAM picks a representative point as the center of a group while k-means will take a cluster based average, this does not materialize any differences for grouping estimation in this Model. The method proposed in Gu and Volgushev (2019), which uses convex clustering method to group the intercept shows slightly inferior performance for smaller , but is otherwise comparable for larger .

| n | T | Perfect Match | Average Match | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| S | S-Iden | PAM | - | GV | S | S-Iden | PAM | - | GV | ||||||

| , | |||||||||||||||

| , | |||||||||||||||

4.3 Determining the Number of Groups

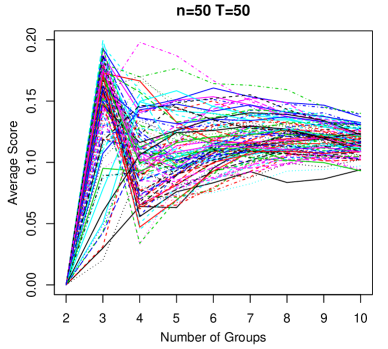

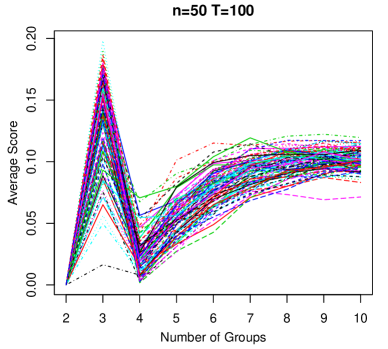

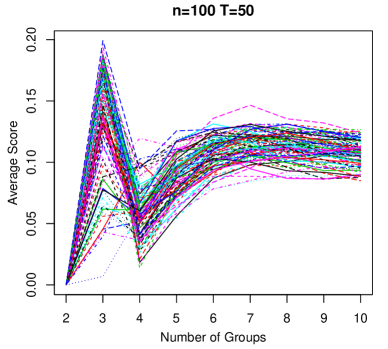

In this section, we compare the proposed heuristic in (5) for selecting the number of groups with other proposals from the literature. A general principle for determining the number of clusters using cross-validation (CV) in combination with the stability of cluster assignments was proposed by Wang (2010) and adapted to quantile regression with grouping on the slopes in Zhang et al. (2019a). The underlying idea is directly applicable to any clustering algorithm, and hence we consider two versions: CV-kmeans corresponding to the proposal of Zhang et al. (2019a), and CV-Spectral which uses spectral clustering as proposed in the present paper as the underlying clustering algorithm. The maximum numbers of clusters to consider, denoted by , is set to throughout. Results for Model 1 are presented in Table 8 and those for Model 2 are summarized in Table 9. All results reported in this section are based on 500 simulation repetitions.

For Model 1, the proposed heuristic has the best performance for all settings except for errors with where the CV–Spectral outperforms slightly. CV–Spectral shows better performance than CV–kmeans consistently. We note that Model 1 is perfectly symmetric with an odd number of groups, this corresponds to a setting that is favorable for stability–based methods. Model 2 demonstrates a situation where stability based method performs badly.

Model 2 corresponds to an even number of groups, and both CV methods fail in this setting because they always pick groups. In light of the findings in Ben-David et al. (2006), this is not surprising; see also Von Luxburg (2010). The issue is that a wrong grouping with two groups corresponding to coefficients in one group and in the other is very stable under variations of the data which leads to confusion of the stability–based methods. In the online appendix, we plot the paths of cross-validated stability scores for different combinations and different realizations of the data (Section 8 Figure 6). For larger there is a local minimum at the true number of groups , but the global minima are always at . The proposed heuristic works reasonably well and is able to pick up the correct number of groups as increases.

Model 4 corresponds to common slopes and group structure on the intercept (see also Example 2.3). Since this setting was also considered in Gu and Volgushev (2019), we consider the information criterion proposed in there. Results are presented in Table 10. We also include cross–validation with spectral clustering, denoted by CV-spectral, for comparison. Note that CV–kmeans is not applicable in this setting.

For , the best performing method is Gu and Volgushev (2019) with about a advantage over the other two methods which show comparable performance. In all other settings, CV-Spectral is the best or close to best (within ) performer. The heuristic method performs better or is similar to Gu and Volgushev (2019) for most cases with while the results between those two are mixed in other settings.

In conclusion, there is no clear winner that performs best across all models and settings. This is not surprising because selecting the number of clusters is a very difficult problem in general. This also explains why there exists no unifying approach for selecting the number of groups. Our proposed eigenvalue heuristic is competitive in most cases considered, and clearly the best on some. Stability–based methods have two major limitations: they cannot select one group by construction, and they can fail for models with stable clusters for the wrong number of groups. The information criterion in Gu and Volgushev (2019) can select one group and performs well when are smaller but falls behind when is large. No information criterion is known for quantile regression models with unrestricted intercepts and grouping on the slopes. Such a criterion could potentially be derived, but it would only be valid in this specific setting and we refrained from taking this route since we aimed to propose a method that is applicable in more generality.

| n | T | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| 1 | 2 | 3 | 4 | 5 | 1 | 2 | 3 | 4 | 5 | ||

| CV-Spectral, | |||||||||||

| 30 | 60 | – | 0.05 | 0.84 | 0.09 | 0.02 | – | 0.08 | 0.72 | 0.15 | 0.05 |

| 30 | 90 | – | 0.01 | 0.98 | 0.01 | 0.00 | – | 0.03 | 0.91 | 0.06 | 0.00 |

| 30 | 120 | – | 0.01 | 0.99 | 0.00 | 0.00 | – | 0.01 | 0.98 | 0.01 | 0.00 |

| 60 | 60 | – | 0.01 | 0.98 | 0.01 | 0.00 | – | 0.01 | 0.95 | 0.02 | 0.02 |

| 60 | 90 | – | 0.00 | 1.00 | 0.00 | 0.00 | – | 0.00 | 0.99 | 0.01 | 0.00 |

| 60 | 120 | – | 0.00 | 1.00 | 0.00 | 0.00 | – | 0.00 | 1.00 | 0.00 | 0.00 |

| CV-kmeans, | |||||||||||

| 30 | 60 | – | 0.29 | 0.40 | 0.17 | 0.14 | – | 0.34 | 0.32 | 0.17 | 0.17 |

| 30 | 90 | – | 0.13 | 0.69 | 0.12 | 0.06 | – | 0.19 | 0.58 | 0.16 | 0.07 |

| 30 | 120 | – | 0.13 | 0.80 | 0.06 | 0.01 | – | 0.13 | 0.72 | 0.11 | 0.04 |

| 60 | 60 | – | 0.09 | 0.39 | 0.25 | 0.27 | – | 0.13 | 0.27 | 0.16 | 0.44 |

| 60 | 90 | – | 0.06 | 0.74 | 0.15 | 0.05 | – | 0.07 | 0.63 | 0.18 | 0.12 |

| 60 | 120 | – | 0.05 | 0.85 | 0.08 | 0.02 | – | 0.03 | 0.78 | 0.15 | 0.04 |

| Heuristic, | |||||||||||

| 30 | 60 | 0.00 | 0.07 | 0.91 | 0.02 | 0.00 | 0.05 | 0.25 | 0.69 | 0.01 | 0.00 |

| 30 | 90 | 0.00 | 0.00 | 1.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.98 | 0.02 | 0.00 |

| 30 | 120 | 0.00 | 0.00 | 1.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.99 | 0.01 | 0.00 |

| 60 | 60 | 0.01 | 0.00 | 0.98 | 0.01 | 0.00 | 0.09 | 0.07 | 0.84 | 0.00 | 0.00 |

| 60 | 90 | 0.00 | 0.00 | 1.00 | 0.00 | 0.00 | 0.00 | 0.00 | 1.00 | 0.00 | 0.00 |

| 60 | 120 | 0.00 | 0.00 | 1.00 | 0.00 | 0.00 | 0.00 | 0.00 | 1.00 | 0.00 | 0.00 |

| n | T | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| 1 | 2 | 3 | 4 | 5 | 1 | 2 | 3 | 4 | 5 | ||

| CV-Spectral, | |||||||||||

| 40 | 40 | – | 1.00 | 0.00 | 0.00 | 0.00 | – | 1.00 | 0.00 | 0.00 | 0.00 |

| 40 | 80 | – | 1.00 | 0.00 | 0.00 | 0.00 | – | 1.00 | 0.00 | 0.00 | 0.00 |

| 40 | 160 | – | 1.00 | 0.00 | 0.00 | 0.00 | – | 1.00 | 0.00 | 0.00 | 0.00 |

| 60 | 40 | – | 1.00 | 0.00 | 0.00 | 0.00 | – | 1.00 | 0.00 | 0.00 | 0.00 |

| 60 | 80 | – | 1.00 | 0.00 | 0.00 | 0.00 | – | 1.00 | 0.00 | 0.00 | 0.00 |

| 60 | 160 | – | 1.00 | 0.00 | 0.00 | 0.00 | – | 1.00 | 0.00 | 0.00 | 0.00 |

| CV-kmeans, | |||||||||||

| 40 | 40 | – | 1.00 | 0.00 | 0.00 | 0.00 | – | 1.00 | 0.00 | 0.00 | 0.00 |

| 40 | 80 | – | 1.00 | 0.00 | 0.00 | 0.00 | – | 1.00 | 0.00 | 0.00 | 0.00 |

| 40 | 160 | – | 1.00 | 0.00 | 0.00 | 0.00 | – | 1.00 | 0.00 | 0.00 | 0.00 |

| 60 | 40 | – | 1.00 | 0.00 | 0.00 | 0.00 | – | 1.00 | 0.00 | 0.00 | 0.00 |

| 60 | 80 | – | 1.00 | 0.00 | 0.00 | 0.00 | – | 1.00 | 0.00 | 0.00 | 0.00 |

| 60 | 160 | – | 1.00 | 0.00 | 0.00 | 0.00 | – | 1.00 | 0.00 | 0.00 | 0.00 |

| Heuristic, | |||||||||||

| 40 | 40 | 0.00 | 0.70 | 0.00 | 0.30 | 0.00 | 0.00 | 0.92 | 0.00 | 0.08 | 0.00 |

| 40 | 80 | 0.00 | 0.00 | 0.00 | 0.99 | 0.01 | 0.00 | 0.02 | 0.00 | 0.97 | 0.01 |

| 40 | 160 | 0.00 | 0.00 | 0.00 | 0.99 | 0.01 | 0.00 | 0.00 | 0.00 | 1.00 | 0.00 |

| 60 | 40 | 0.00 | 0.49 | 0.00 | 0.51 | 0.00 | 0.00 | 0.91 | 0.00 | 0.09 | 0.00 |

| 60 | 80 | 0.00 | 0.00 | 0.00 | 1.00 | 0.00 | 0.00 | 0.01 | 0.00 | 0.99 | 0.00 |

| 60 | 160 | 0.00 | 0.00 | 0.00 | 1.00 | 0.00 | 0.00 | 0.00 | 0.00 | 1.00 | 0.00 |

| n | T | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| 1 | 2 | 3 | 4 | 5 | 1 | 2 | 3 | 4 | 5 | ||

| CV-Spectral, | |||||||||||

| 30 | 15 | – | 0.35 | 0.43 | 0.09 | 0.13 | – | 0.45 | 0.31 | 0.09 | 0.15 |

| 30 | 30 | – | 0.04 | 0.92 | 0.03 | 0.01 | – | 0.11 | 0.79 | 0.07 | 0.03 |

| 30 | 60 | – | 0.00 | 1.00 | 0.00 | 0.00 | – | 0.01 | 0.99 | 0.00 | 0.00 |

| 60 | 15 | – | 0.13 | 0.63 | 0.02 | 0.22 | – | 0.20 | 0.44 | 0.01 | 0.35 |

| 60 | 30 | – | 0.00 | 1.00 | 0.00 | 0.00 | – | 0.01 | 0.97 | 0.01 | 0.01 |

| 60 | 60 | – | 0.00 | 1.00 | 0.00 | 0.00 | – | 0.00 | 1.00 | 0.00 | 0.00 |

| 90 | 15 | – | 0.09 | 0.79 | 0.00 | 0.12 | – | 0.18 | 0.61 | 0.01 | 0.20 |

| 90 | 30 | – | 0.00 | 1.00 | 0.00 | 0.00 | – | 0.00 | 1.00 | 0.00 | 0.00 |

| 90 | 60 | – | 0.00 | 1.00 | 0.00 | 0.00 | – | 0.00 | 1.00 | 0.00 | 0.00 |

| Heuristic, | |||||||||||

| 30 | 15 | 0.05 | 0.40 | 0.45 | 0.06 | 0.04 | 0.10 | 0.49 | 0.31 | 0.06 | 0.04 |

| 30 | 30 | 0.01 | 0.04 | 0.92 | 0.02 | 0.01 | 0.00 | 0.15 | 0.79 | 0.03 | 0.03 |

| 30 | 60 | 0.00 | 0.00 | 0.99 | 0.00 | 0.01 | 0.00 | 0.00 | 1.00 | 0.00 | 0.00 |

| 60 | 15 | 0.18 | 0.37 | 0.44 | 0.00 | 0.01 | 0.50 | 0.28 | 0.22 | 0.00 | 0.00 |

| 60 | 30 | 0.00 | 0.01 | 0.99 | 0.00 | 0.00 | 0.00 | 0.04 | 0.95 | 0.00 | 0.01 |

| 60 | 60 | 0.00 | 0.00 | 1.00 | 0.00 | 0.00 | 0.00 | 0.00 | 1.00 | 0.00 | 0.00 |

| 90 | 15 | 0.02 | 0.31 | 0.64 | 0.01 | 0.02 | 0.12 | 0.40 | 0.46 | 0.00 | 0.02 |

| 90 | 30 | 0.00 | 0.00 | 1.00 | 0.00 | 0.00 | 0.00 | 0.02 | 0.98 | 0.00 | 0.00 |

| 90 | 60 | 0.00 | 0.00 | 1.00 | 0.00 | 0.00 | 0.00 | 0.00 | 1.00 | 0.00 | 0.00 |

| GV, | |||||||||||

| 0.51 | 0.50 | ||||||||||

| 0.81 | 0.76 | ||||||||||

| 0.98 | 0.96 | ||||||||||

| 0.52 | 0.44 | ||||||||||

| 0.86 | 0.78 | ||||||||||

| 0.99 | 0.98 | ||||||||||

| 0.51 | 0.37 | ||||||||||

| 0.88 | 0.79 | ||||||||||

| 0.99 | 0.98 | ||||||||||

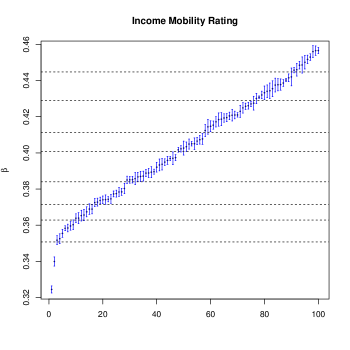

5 Empirical Applications

5.1 Heterogeneity in environmental Kuznet curves