A Unified Framework for Generalized Moment Problems: a Novel Primal-Dual Approach

Jiayi Guo, Simai He, Bo Jiang, Zhen Wang \AFFSchool of Information Management and Engineering, Shanghai University of Finance and Economics, China, 200433, guo.jiayi@sufe.edu.cn, simaihe@mail.shufe.edu.cn, isyebojiang@gmail.com, zhenwang@163.sufe.edu.cn

Generalized moment problems optimize functional expectation over a class of distributions with generalized moment constraints, i.e., the function in the moment can be any measurable function. These problems have recently attracted growing interest due to their great flexibility in representing nonstandard moment constraints, such as geometry-mean constraints, entropy constraints, and exponential-type moment constraints. Despite the increasing research interest, analytical solutions are mostly missing for these problems, and researchers have to settle for nontight bounds or numerical approaches that are either suboptimal or only applicable to some special cases. In addition, the techniques used to develop closed-form solutions to the standard moment problems are tailored for specific problem structures. In this paper, we propose a framework that provides a unified treatment for any moment problem. The key ingredient of the framework is a novel primal-dual optimality condition. This optimality condition enables us to reduce the original infinite dimensional problem to a nonlinear equation system with a finite number of variables. In solving three specific moment problems, the framework demonstrates a clear path for identifying the analytical solution if one is available, otherwise, it produces semi-analytical solutions that lead to efficient numerical algorithms. Finally, through numerical experiments, we provide further evidence regarding the performance of the resulting algorithms by solving a moment problem and a distributionally robust newsvendor problem. \KEYWORDSDistributionally robust optimization, Generalized moment problem, Newsvendor, Primal-dual

1 Introduction

The generalized moment problem (see, e.g., Bertsimas and Popescu, 2005) aims to optimize the expectation of a measurable function with general distributional moment information for , where can be any measurable function. The study of this problem dates back to the pioneering work of Chebyshev, (1874) and Markov, (1884) on the standard moment problem (i.e., ). Despite the long history, the research on this fundamental problem is still active today in modern probability theory (Smith, 1995, Bertsimas and Popescu, 2005, He et al., 2010). Moreover, the generalized moment problem is viewed as an important building block for distributionally robust optimization, with wide applications in inventory control (Scarf, 1958, Perakis and Roels, 2008, Natarajan et al., 2018, Das et al., 2021), portfolio optimization (Ghaoui et al., 2003, Bertsimas et al., 2010, Delage and Ye, 2010, Zymler et al., 2013, Rujeerapaiboon et al., 2016), and statistical learning (Lanckriet et al., 2002, Mehrotra and Zhang, 2014, Fathony et al., 2018).

For the standard moment problem, the classic numerical algorithm comes from Bertsimas and Popescu, (2005), who formulate the dual of the problem as a polynomial-time solvable semidefinite program (SDP). For certain more structured problems, the relative entropy formulation (see, e.g., Das et al., 2021) can be applied to further accelerate this solving process. However, methods that can yield closed-form solutions and provide management insights are often preferred. A classic example of such methods is due to Scarf, (1958), who obtains an analytical solution for the robust newsvendor problem, given the first two moments. Following this approach, a large volume of literature has discovered more closed-form decisions for some variants of Scarf’s model by considering the asymmetry of demands (Natarajan et al., 2018), heavy-tailed distributed demands (Das et al., 2021), risk-averse objectives (Han et al., 2014), etc. The study of closed-form solutions is also prevalent in probability theory (Bertsimas and Popescu, 2005, He et al., 2010, Roos et al., 2021) and portfolio selection (Ghaoui et al., 2003, Zuluaga et al., 2009, Natarajan et al., 2010, Chen et al., 2011, Li, 2018). However, the techniques that have been used in the literature to develop these closed forms are mathematically different and are only tailored for specific problems. In particular, much effort has been devoted to verifying the optimality of analytical solution candidates that are provided without much explanation. However, discussion of how to come up with such analytical forms in the first place is largely missing. Thus, there is an urgent need for a unified framework that can systematically derive the closed-form solution for a given moment problem.

The generalized moment problem has recently attracted growing interest due to its great flexibility in representing nonstandard moments,111In this paper, we call a moment nonstandard if it cannot be represented as the expectation of some piece-wise polynomial function. such as geometry-mean constraints (i.e., ) in the pricing problem (Tamuz, 2013, Elmachtoub et al., 2021), entropy constraints (Chen et al., 2019), and exponential-type moment constraints (i.e., ) including moment-generating constraints and sub-Gaussian distribution constraints (Honorio and Jaakkola, 2014). Such exponential-type moment information is known to be crucial for establishing sharp tail estimations with large deviations when a distribution has light tails. In contrast, geometry-mean constraints are useful for estimating tail bounds with small deviations, especially when the distribution has a heavy tail. However, to the best of our knowledge, the literature lacks an efficient algorithm that can exactly solve the generalized moment problem. The existing solution methods are either suboptimal (Smith, 1995) or restricted to special cases (Popescu, 2007, Chen et al., 2019).

1.1 Our Contributions

To address the two issues raised above, we propose a unified framework for solving the generalized moment problem, which is our main contribution. The merits of this framework can be summarized as follows:

-

1.

It provides a unified treatment for any generalized moment problem. Such treatment proves useful in identifying an analytical solution of the problem if one is available. Even when a closed-form solution is unavailable, this framework can quickly reduce the problem to a system of equations with a small number of variables that include only the optimal supporting points. For certain structured problems, this system of equations can lead to numerical methods that are even more efficient than the SDP approach shown in our numerical experiments.

-

2.

The framework has great flexibility for accommodating nonstandard moment constraints/objective functions. It complements the current literature by providing an approach for finding the exact solutions of generalized moment problems. As an illustration, in Section 5 we demonstrate how to solve an exponential moment constrained problem with this framework.

-

3.

The framework provides a novel viewpoint for generalized moment problems and lends alternative insights even for some well-studied models. For instance, we manage to obtain an exact semi-closed-form solution for the st and -th moment problem, which tightens the semi-closed-form bounds given in Das et al., (2021), Proposition 3.4, under the same condition. It also enables us to find infinitely many optimal solutions in a degenerate case for the moment problem with the upper partial moment objective and constraint in Han et al., (2014).

Apart from the framework, we also propose a novel optimality condition for the generalized moment problem by incorporating the primal feasible condition, the complementary slackness condition, and a tangent condition. To the best of our knowledge, the tangent condition has not been systematically treated as an optimality condition prior to our work, even though it has been implicitly used in the derivation of theoretical results (see, e.g., Smith, 1995, Popescu, 2007, Zuluaga et al., 2009). In fact, our optimality condition is equivalent to a sizeable nonlinear system with an equal number of variables and equations, which paves the way for the analytical solution and efficient numerical algorithms for the problem.

1.2 Related Literature

Due to the popularity of closed-form solutions, in this subsection, we first review the vast literature on the analytical solutions of the standard moment problems in the fields of inventory control, finance, and probability theory. The moment problems in inventory control theory are mostly discussed in the literature on the distributionally robust newsvendor model. The previously mentioned seminal work of Scarf, (1958) has been criticized for its over-conservative behavior, and several variants have been proposed and studied to address this issue. For instance, Yue et al., (2006) derive analytical bounds on the min-max regret objective with mean-variance moment constraints. Han et al., (2014) extend Scarf’s closed-form formula to the risk- and ambiguity-averse newsvendor problem. Natarajan et al., (2018) provide a closed-form expression for the worst-case newsvendor profit with mean, variance, and semivariance information, and they show that the worst case occurs in a three-point distribution. Recently, Das et al., (2021) have considered the problem with the first and -th moment constraints that capture the heavy-tailed behavior of the demand, and they manage to derive a closed-form worst-case distribution when the order quantities are below a certain value.

Regarding the research on analytically solving the moment problems in finance, Ghaoui et al., (2003) consider the distributionally robust single-period portfolio selection and obtain closed-form solutions of the worst-case value at risk over a mean-variance constraint. Chen et al., (2011) extend this result to the disutility function in the form of a conditional value at risk (CVaR), or the form of lower partial moments. Under the same moment constraint, Natarajan et al., (2010) and Li, (2018) identify closed-form solutions for the optimized certainty equivalent risk measure in Ben-Tal and Teboulle, (2007) and the law-invariant risk measure that is the most important extension of CVaR, respectively. Zuluaga et al., (2009) analytically find the worst-case payoff of the European call option using up to the third-order moment, which characterizes the skewness of the asset return.

In probability theory, moment problems have been applied to derive tight closed-form tail probability bounds, given the first three moments (Bertsimas and Popescu, 2005). Subsequently, He et al., (2010) extend this result to the problem with first-, second-, and fourth-order moments. Recently, Roos et al., (2021) provide alternative tight lower and upper bounds on the tail probability under a bounded support, given the mean and mean absolute deviation of the random variable.

In contrast to the fruitful research on the standard moment problems, studies of nonstandard moment problems are quite limited, and they all focus on the numerical approaches. Smith, (1995) applies an approximate procedure to reduce the dimension of the sample space of the problem by grid search. Unfortunately, the efficiency of this approach has not been supported by theoretical foundations or by extensive numerical experiments. For the moment problem with entropy constraints that can be characterized by tractable conic inequalities, Chen et al., (2019) propose a greedy improvement procedure that sequentially optimizes tractable relaxed subproblems. If we relax the objective to be the so-called one- or two-point support functions while restricting the constraint to be the first two moments, Popescu, (2007) successfully reduces this problem to a deterministic parametric quadratic program.

In this paper, we focus on providing a unified treatment for various moment problems, including nonstandard ones, and on identifying the analytical solution when it is available. We note that, even for the standard moment problems, to the best of our knowledge, a similar framework has not yet been proposed, as the methods described above for obtaining the analytical solutions are problem-dependent. There are also other framework-like methods that can solve a wide class of moment problems have been proposed (Smith, 1995, Bertsimas and Popescu, 2005). However, the classical SDP method (Bertsimas and Popescu, 2005) is a numerical approach, and it only works for standard moment problems, while Smith, (1995)’s method can be applied to generalized moment problems, but, as noted above, its efficiency has not been theoretically or numerically justified. For these reasons, our work is an excellent complement to the existing literature.

1.3 Outline and Notations

The remainder of the paper is organized as follows. In Section 2, we present a novel primal-dual optimality condition for the generalized moment problems and propose a three-step unified framework for these problems. In the subsequent sections, we analyze three concrete moment problems with our framework. In Section 3, we consider the st and -th moment problem that was proposed in Das et al., (2021), and we obtain the same analytical solution under the same condition. In cases where an analytic solution is unavailable, our framework also provides a semi-analytical form of the optimal solution. The merit of this form is that it relies on only one parameter that is a root of a nonlinear equation. Section 4 is devoted to the problem of minimizing nd-order upper partial moments with the st-order upper partial moment constraint. Not only do we obtain the same explicit optimal value as Han et al., (2014), but we also identify more analytical solutions for a degenerate case (see Lemma 4.6). To demonstrate our framework’s ability to handle nonpolynomial moments, we consider an exponential moment constrained problem in Section 5. Similar to Section 3, we obtain an analytical solution and a semi-analytical solution for two scenarios that are defined by the range of the moment parameters. By solving those three moment problems, we show that our framework is capable of finding the closed-form solution if one exists. In addition, when a closed-form solution is not available, our framework leads to some efficient numerical algorithms. In Section 6, we apply those algorithms to the st and -th moment problem and the distributionally robust newsvendor problem with an exponential moment ambiguity set as two illustrative examples. We show that the resulting algorithms indeed solve the two problems efficiently and thus demonstrate the benefit of our framework.

Throughout this paper, we denote vectors and matrices by boldface lowercase letters and capital letters, respectively. For probability distributions, we use to denote the set of all Borel probability distributions on the support , and we use to denote a discrete distribution with support and probability vector such that for . Finally, we use to represent the positive function .

2 The Unified Framework for the Generalized Moment Problem

2.1 The Generalized Moment Problem and the Optimality Condition

We consider the generalized moment problem in the following form:

| (GMP) | ||||

| s.t. | ||||

with and . In contrast to the standard moment problem, where the moment constraints are defined by the expectations of certain piece-wise polynomial functions, the function in (GMP) can be any measurable function with respect to for . Note that problem (GMP) can be viewed as a semi-infinite linear program with constraints. According to Smith, (1995) and Bertsimas and Popescu, (2005), there exists an optimal distribution of (GMP) with at most mass points. Therefore, we consider an optimal distribution with finite support and probability vector . Then the moment constraints in (GMP) can be rewritten as

| (PriCond) |

To study (GMP) from an alternative perspective, we consider the dual problem:

| (DGMP) | ||||

Let be a moment vector. The strong duality () holds if lies in the interior of the set of all moment vectors that make problem (GMP) feasible (Bertsimas and Popescu, 2005). It is well known that a primal feasible distribution and a dual feasible solution are optimal if and only if the complementary slackness condition holds (Smith, 1995), i.e., for . Since , we further have for , which is equivalent to:

| (SlackCond) |

The equations above together with the dual feasibility imply that are global minimizers of the problem . Furthermore, if is the differentiable interior point, i.e., the differentiable point of lying in the interior of , for some , then according to the first-order optimality condition, we have

Without loss of generality, we assume that with are the differentiable interior points. The above equality leads to the so-called tangent condition:

| (TagntCond) |

Consequently, we formally propose the three systems of equations (PriCond), (SlackCond), and (TagntCond) as an optimality condition for problem (GMP) in the following theorem.

Theorem 2.1

Proof 2.2

The necessity of the optimality condition follows directly from the discussion immediately preceding this theorem. To prove the sufficiency of the condition, suppose that there exist a distribution with and a vector satisfying for all such that (PriCond), (SlackCond), and (TagntCond) hold. Then is a feasible solution to the primal problem (GMP), due to and condition (PriCond), and is also a feasible solution to the dual problem (DGMP), as for all . Moreover, the complementary slackness is guaranteed by (SlackCond). Therefore, and are optimal solutions to (GMP) and (DGMP), respectively.

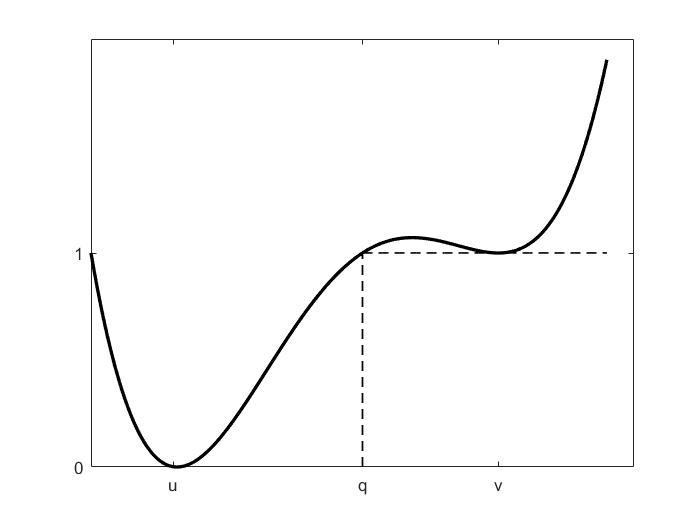

We remark that (PriCond) and (SlackCond) are standard conditions that are used to characterize the optimal solution. However, to the best of our knowledge, (TagntCond) has not been formally proposed as an optimality condition, although it has been implicitly used in the literature for the analysis of some structured moment problems (see, e.g., Smith, 1995, Popescu, 2007, Zuluaga et al., 2009). In fact, condition (TagntCond) has a very clear geometric explanation, which is that and share the same tangent plane at the points , while it is possible that such a tangent property does not hold for other intersecting points with , as illustrated in Figure 1. Specifically, the instance in Figure 1 is taken from the dual problem of upper bounding the probability under the first, second, and fourth moments (He et al., 2010). In this case, is a quartic function, and for some given constant is an indicator function. From the figure, we can see that is tangent to at and , where condition (TagntCond) holds, while the two functions intersect but are not tangent at point , as is not differentiable at this point.

2.2 The Unified Framework

In accordance with the optimality conditions (PriCond), (SlackCond), and (TagntCond) stated in Theorem 2.1, we propose the following three-step unified framework for solving the GMP.

The Unified Framework for Solving the GMP: 1. Identify the rough structure of the support of the optimal distribution. 2. Provide the possible (semi-)analytical form of the optimal supporting points. 3. Solve and verify the optimal distribution.

The rough structure in Step 1 of the framework means the cardinality of the optimal support and the description of how the associated supporting points are distributed among differentiable pieces.222For the instance in Figure 1, there are two differential pieces, and . Therefore, the two tangent points can possibly be allocated in those two pieces in three ways: , and . Each piece is defined as the interval connecting two consecutive non-differentiable points of the function , with being treated as non-differentiable points. The rough structure can be identified by (SlackCond), (TagntCond), and the dual feasibility condition. It is worth mentioning that the optimal support derived from our approach is often sparse compared to the number of moment constraints , which is the dimension of the dual variable . Intuitively, this is because (SlackCond) and (TagntCond) combined together can be viewed as a linear system on , and every supporting point with contributes one equation in (SlackCond) and one more equation if it appears in (TagntCond). can therefore be determined by far fewer supporting points than its dimension, i.e., . Our observation is also consistent with the previous results (see, e.g., Popescu, 2007, Zuluaga et al., 2009, He et al., 2010, Natarajan et al., 2018, Das et al., 2021), where the cardinality of the optimal support is often less than .

Note that the information about the optimal solution that is provided by the rough structure in Step 1 is still limited. To proceed, in Step 2 we define several scenarios where the rough structure exhibits a more explicit expression, and then derive the possible (semi-)analytical form of the optimal supporting points for each scenario. This is achieved by treating (PriCond), (SlackCond), and (TagntCond) as a large nonlinear system of equations in , , and with a total of variables and an equal number of equations, and working intensively on the nonlinear system. Since this system is linear in and for any given , we can represent and with by solving the linear system and further plugging the expression into the large nonlinear system to eliminate and . As a result, we obtain a much smaller nonlinear system regarding only with variables and an equal number of equations. For instance, in the proofs of Lemma 3.10 and Lemma 5.6 we obtain two nonlinear equations involving only that are derived from the original nonlinear system with respect to , , and . For more general cases, we can resort to classical methods such as the Gauss-Newton, trust region, and Levenberg-Marquardt methods (see, e.g., More, 1978, Dennis and Schnabel, 1983, Kelley, 1995) to solve such nonlinear systems.

The purpose of Step 3 is to compute the distribution according to the (semi-)analytical forms of the supporting points given in Step 2 and further verify the optimality of the constructed distribution. Since the (semi-)analytical forms are often derived by (PriCond), (SlackCond), and (TagntCond), Theorem 2.1 shows that it remains to verify the primal feasibility and the dual feasibility for all .

We remark that the main effort in Step 3 is devoted to verifying the optimality of a given distribution, which plays a similar role to most analyses conducted in the literature to obtain the closed-form solution of a moment problem. However, an explanation of how to systematically provide such a distribution is largely missing in the extant research, while Step 1 together with Step 2 of our framework serve the purpose of finding one such distribution, thus complementing the extant literature. Moreover, any analytical solution of (GMP) must satisfy the large nonlinear system of equations jointly defined by (PriCond), (SlackCond), and (TagntCond) in Step 2, as this is a necessary optimality condition according to Theorem 2.1. Therefore, our approach can find any analytical optimal distribution as long as such a nonlinear system can be solved analytically, which has a good chance of occurring because the system has an equal number of variables and equations.

In what follows, we analyze three concrete moment problems with our unified framework: the st and -th moment problem, the moment problem with an upper partial moment objective and constraint, and the exponential moment problem. To analyze each problem, we supplement our framework with detailed technical lemmas. Specifically, the task of each step is accomplished by one or two of these lemmas, as summarized in Table 1 for the reader’s convenience.

| st and -th moment problem | upper partial moment problem | st and exponential moment problem | |

|---|---|---|---|

| Step | Lemma 3.4 | Lemma 4.2 | Lemma 5.3 |

| Step | Lemma 3.6, 3.10 | Lemma 4.3, 4.5 | Lemma 5.4, 5.6 |

| Step | Lemma 3.8, 3.12 | Lemma 4.4, 4.6 | Lemma 5.5, 5.7 |

3 The st and -th moment problem in the newsvendor model

3.1 Problem formulation and main results

In this section, we consider the moment problem that originated from a distributional robust newsvendor model proposed in Das et al., (2021) and demonstrate how to apply our framework to solve this problem. In particular, the problem is given as follows:

| (MP1t) |

where is the order quantity in the newsvendor model and is the cumulative distribution function of random variable . We also require that the distribution satisfies the following moment constraint given in Das et al., (2021):

where and are the st and -th moment parameters satisfying , with . In fact, Das et al., (2021) showed that is capable of capturing more light-tailed () or heavy-tailed behavior () of the underlying distribution than the classical constraint in Scarf, (1958)’s model. To analyze the moment problem (MP1t), we also consider the following dual problem:

| (DMP1t) | ||||||

| subject to |

Note that for any random variable with mean , we can always perform a variable transformation by letting such that

and work on instead. Therefore, without loss of generality, we assume that in the remaining part of this section. In this case, any single-point feasible distribution includes only the point in the support, and the -th moment of this distribution is also equal to . Thus, we further assume that to exclude the trivial cases of single-point feasible distributions. With our unified framework, we obtain the following main theorem of this section, which provides a characterization of the optimal value of problem (MP1t).

Theorem 3.1

Suppose that , with . Then the optimal value of problem (MP1t) is given by

where and is any root of the following equation:

| (1) |

When , the optimal value stated in Theorem 3.1 is consistent with the optimal value in Das et al., (2021), Proposition 3.1. However, when , the problem (MP1t) cannot be solved analytically. In particular, upper and lower bounds for the optimal value are derived in Das et al., (2021), Propositions 3.3 and 3.4, while our Theorem 3.1 provides a semi-closed form, which is probably the best one can hope for. One implication of the semi-closed form solution is that the optimal value essentially depends on only one parameter that can be any root of a prespecified function, and one such root always exists and can be found efficiently by the bisection method presented in the next subsection.

3.2 The bisection algorithm

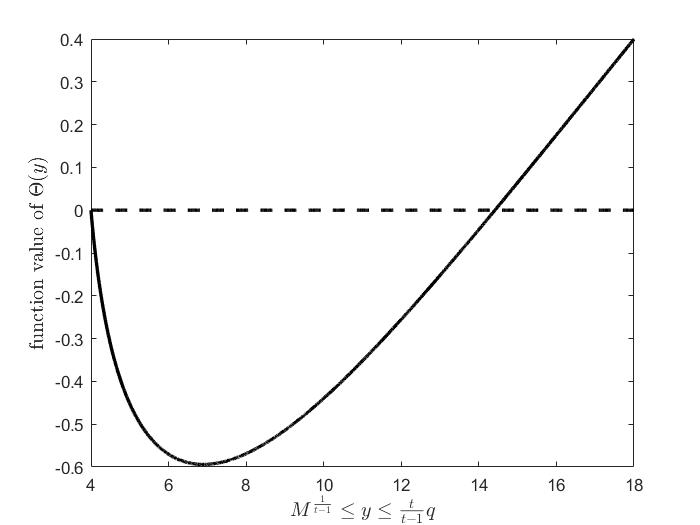

In this subsection, we propose in Algorithm 1 a variant of the bisection method that can find a root of the function defined in (1) in Theorem 3.1 and thus solve the moment problem (MP1t) when .

Note that there are some subtle differences between Algorithm 1 and the standard bisection method. Specifically, Algorithm 1 aims to find a root of a function in an open interval and allows the left starting point itself to be a root of the function, which is exactly the case for the function . In Figure 2 we plot one concrete instance of to illustrate this situation. In the following proposition, we formally state that Algorithm 1 is indeed able to find a root of . The proof is given in the appendix.

Proposition 3.2

To end this subsection, we remark that the iteration complexity of Algorithm 1 is independent of the value of , while the classical SDP approach works only if is a rational number, and its dimension depends on both the denominator and numerator of .

3.3 Proof of Theorem 3.1

This subsection is dedicated to the proof of Theorem 3.1, which follows the three steps in our framework.

3.3.1 Identify the rough structure of the optimal support.

To implement the first step of our framework, we shall show that the optimal solution of (MP1t) is a two-point distribution, and characterize how the two supporting points could be allocated. We first present the following lemma as preparation, relegating its proof to the appendix.

Lemma 3.3

Suppose that for all , where is a convex function with a strictly increasing derivative and is a two-piece linear function such that

Then (i) there is at most one point or if is continuous at such that , and (ii) there is at most one point such that .

We are now ready to provide the rough structure of the optimal support in the following lemma.

Lemma 3.4 (The rough structure of the optimal support)

The optimal solution of (MP1t) is a two-point distribution with support such that .

Proof 3.5

Since we are assuming that , the optimal support cannot be a singleton. Let be the optimal solution of the dual problem (DMP1t), and consider the dual constraint:

According to the complementary slackness condition (SlackCond), the dual constraint must be tight at the points in the support of the primal optimal distribution. Therefore, in what follows we shall identify the optimal support by searching the points where the dual constraint could be tight. We first note that , since otherwise for sufficiently large as , which contradicts the feasibility of . Now we consider the easy case of , where the dual constraint reduces to

which gives us and . As minimizes in the objective and , we obtain and . Consequently, only when . That is, the optimal solution of (MP1t) is a single-point distribution with support , contradicting the first sentence of the proof. Thus, we must have , and the function is convex in and has a strictly increasing derivative. Moreover, since is a two-piece linear function and is continuous at the break point , Lemma 3.3 implies that there are at most one point and at most one point such that . In other words, the optimal distribution of (MP1t) has two support points, one in the interval and one in the interval . Moreover, we have , for otherwise and are both included in either or or the optimal distribution is supported by a single point, which leads to a contradiction. Therefore, the two support points satisfy .

To make the structure of the optimal support in Lemma 3.4 more explicit, we shall continue our analysis with two scenarios, one in which the supporting point equals and one in which it is strictly greater than .

3.3.2 Analysis under the support with .

We start with the boundary case and provide the analytical form of the optimal support as follows.

Lemma 3.6 (Analytical form of the supporting points)

Suppose that , with , and the optimal solution of (MP1t) is a two-point distribution with support such that . Then we must have and .

Proof 3.7

Suppose that the optimal distribution of (MP1t) is supported by with probabilities and , respectively, and that is an optimal solution of the dual problem (DMP1t). Let

| (2) |

In this case, condition (TagntCond) gives . According to Theorem 2.1, and satisfy conditions (PriCond), (SlackCond), and (TagntCond), which are equivalent to

| (3) |

Solving the above equations gives

| (4) |

In addition, the second system of equations in (3) indicates that . By invoking the dual feasibility of , we have

That is, for arbitrarily small . Therefore, , which combined with (4) guarantees that .

Given the analytical form of the optimal support, we can solve and verify the optimal distribution for this case.

Lemma 3.8 (Analytical form of the optimal distribution)

Suppose that , with and . Then the optimal distribution for problem (MP1t) can be characterized as

| (5) |

Proof 3.9

We first construct and in accordance with (4), where and correspond to the probabilities associated with and in the support of the distribution described in (5). We shall show that and are the optimal solutions for the primal problem (MP1t) and the dual problem (DMP1t), respectively. Recalling that , , and thus is a primal feasible solution. Next, we verify the dual feasibility of , i.e., for any with defined as in (2). According to (4) and , we have , , and , and hence for any . When , is convex, as in this case,

In addition, we have , as is the solution to the second set of equations in (3), and is the unique root of . Then the global minimizer of on is taken either at the point or at the end point , where we already have shown that . Therefore, holds when , and is a feasible solution for the dual problem (DMP1t). In addition, also satisfies the complementary slackness condition due to the second set of equations in (3), and thus we conclude that is an optimal primal-dual solution pair such that the distribution defined in (5) is optimal for (MP1t).

3.3.3 Analysis under the support with .

We now consider the case where and provide the semi-analytical form of the optimal support.

Lemma 3.10 (Semi-analytical form of the supporting points)

Proof 3.11

Suppose that the optimal distribution of (MP1t) is supported by with probabilities and , respectively, and that is an optimal solution of the dual problem (DMP1t). Recalling that is defined in (2) and according to Theorem 2.1, we have and . Therefore, and satisfy the conditions (PriCond), (SlackCond), and (TagntCond), which are equivalent to

| (6) |

The first system of equations in (6) has a solution if and only if

That is,

| (8) |

By a similar argument, the second set of equations in (6) has a solution if and only if

| (20) | |||||

| (26) |

which is precisely , or equivalently,

| (27) |

Consequently, we have

where the last equality is due to (8). Therefore, we can represent as , and substitute in , which is a reformulation of (8). Consequently, is a root of . In addition, we have further estimations of the range of . In particular, due to our assumption that and the validity of the -th moment constraint, we have and . Combining those two inequalities yields , or equivalently, . Equation (27) also implies that , and thus we conclude that . As the upper bound must exceed the lower bound , we have .

.

Finally, the semi-analytical form of the optimal support enables us to identify the optimal distribution as follows.

Lemma 3.12 (Semi-analytical form of the optimal distribution)

Proof 3.13

Suppose that is any root of and construct . We first want to show that , or equivalently, that the function at point . Since when , is a strictly decreasing function on , which combined with implies

Therefore, holds and the construction

is well defined, and and are the solutions of the two linear equations in (DMP1t). Therefore, to confirm the primal feasibility, all that remains is to show that , or equivalently, , due to the construction of . We first observe that , as . Next we consider the function , and a straightforward computation shows that

Therefore, as long as , , and thus is a strictly increasing function. Recall that we have already proved that and holds by (8). Then we must have , as desired, for is strictly increasing on and cannot have the same value at and . Next, we verify the dual feasibility of . Recalling that is defined as in (2), the second equation in (6) indicates that

| (29) |

Moreover, since we have shown that , and when . Therefore, is convex on and , which combined with and (29) implies that

Since is continuous at , we conclude that for all and is a dual feasible solution. Observe that the complementary slackness condition is already implied by , and hence is indeed an optimal primal-dual solution such that the distribution defined in (28) is optimal for (MP1t).

3.3.4 Proof of Theorem 3.1.

4 Minimizing the upper partial moment with the 1st-order upper partial moment constraint

4.1 Problem formulation and the main results

In this section, we consider the following moment constraint defined by the 1st-order upper partial moment:

where and are the st moment, nd moment, and st-order upper partial moment, respectively. Given such a constraint, we want to minimize the nd-order upper partial moment given as follows:

This problem appears in (EC.4) of Han et al., (2014), and it is the key to deriving the analytical results for the risk-averse and ambiguity-averse newsvendor problem in Theorem 1 therein. Adopting the normalization idea given in Han et al., (2014), we assume that and for some without loss of generality. Therefore, the corresponding moment problem is given by

| (MP) |

and the associated dual formulation is given by

| (DMP) | ||||||

| subject to |

By applying our unified framework, we get the same optimal value for problem (MP) as that provided in Han et al., (2014), in the following theorem. Moreover, our framework is able to discover a degenerate case with infinitely many optimal supporting points (Lemma 4.5) and to identify infinitely many optimal solutions (Lemma 4.6) that are not mentioned in Han et al., (2014).

Theorem 4.1

In the rest of this section, we shall only highlight the major flow of our analysis. Specifically, we present the contents of the key technical lemmas that correspond to the three steps in our framework, but relegate the proofs to the appendix.

4.2 Sketch of Proof for Theorem 4.1

We first provide the rough structure of the optimal support that realizes the goal of the first step in our framework.

Lemma 4.2 (The rough structure of the optimal support)

Note that the support obtained in part ii) of Lemma 4.2 is a special case of i). Our discussion in the remainder of this section will therefore consider only the expressions of the support described in parts i) and iii).

4.2.1 Results under the support with .

We start with the case where the optimal support includes only two points and provide the following analytical form of the support.

Lemma 4.3 (Analytical form of the support )

Given the analytical form in Lemma 4.3, we can solve and verify the optimal distribution in this case.

4.2.2 Results under the support .

Now we consider the degenerate case in which the optimal support includes infinitely many points and provide the following analytical form for the three-point optimal support.

Lemma 4.5 (Analytical form of the support )

Suppose that , , and the optimal solution of (MP) has the support . Then we have , and any feasible support with for all has the same objective value and thus is an optimal support. Moreover, any three-point optimal support has the form , with .

The analytical form in the preceding lemma enables us to find the optimal distribution in the following lemma.

4.2.3 Proof of Theorem 4.1.

5 The st and exponential moment problem in the newsvendor model

5.1 Problem formulation and main results

In this section, we further demonstrate the capability of our framework by solving a problem with an exponential moment constraint that cannot be handled by the SDP or by the relative entropy approach in Das et al., (2021). Moreover, as it will be shown in a numerical experiment, the model with this moment information is prone to capture the features of the light tailed distribution. Specifically, the moment constraint that we consider is given by

where is fixed, and and are the st and exponential moment parameters satisfying such that is not empty. Moreover, as only holds for single-point distributions, we assume that to exclude this trivial case. The moment problem that we consider is thus

| (MP1e) |

where is the order quantity in the newsvendor model. The dual of (MP1e) is

| (DMP1e) | ||||||

| subject to |

Without loss of generality, in the rest of this section we assume that . This is because when , we can construct such that

and work on (MP1e) with by replacing with . Our unified framework allows us to arrive at the following main theorem of this section, which provides a characterization of the optimal value for problem (MP1e).

Theorem 5.1

Suppose that , and define

| (33) |

with the Lambert W function . The optimal value for problem (MP1e) is given by

| (34) |

where and is any root of the equation

| (35) |

The above theorem states that the problem (MP1e) has a closed-form optimal value when , while in the opposite case where , the following proposition states that Algorithm 1 can find a root of the function defined in (35), and thus solve problem (MP1e) efficiently.

Proposition 5.2

5.2 Sketch of Proof for Theorem 5.1

To implement the first step of our framework, we show that the optimal solution of (MP1t) is a two-point distribution and indicate where the two supporting points could possibly be allocated.

Lemma 5.3 (The rough structure of the optimal support)

The optimal solution of (MP1e) is a two-point distribution with support such that .

To make the support set in the lemma above more explicit, we shall continue our discussion with two scenarios, one in which the supporting point equals and one in which it is strictly greater than .

5.2.1 Results under the support with .

We start with the boundary case of u = 0 and provide the analytical form of the optimal support as follows.

Lemma 5.4 (Analytical form of the support )

Given the analytical form of the optimal support, we can solve and verify the optimal distribution in this case.

5.2.2 Results under the support with .

Next, we discuss the case where and provide the following semi-analytical form of the optimal support.

Lemma 5.6 (Semi-analytical form of the support )

Finally, the semi-analytical form of the optimal support enables us to identify the optimal distribution as shown below.

5.2.3 The proof of Theorem 5.1.

6 Numerical Experiments

In this section, we show that the semi-analytical solutions derived in the previous sections can also be used to numerically solve moment problems and distributionally robust problems under the newsvendor model, which provides further evidence for the capability of our proposed framework. Since our unified framework is more of theoretical interest, the two numerical examples provided in this section are only for illustrative purposes. We leave a deeper investigation of efficient computational approaches for general moment problems for future work. All of the numerical experiments in this section were performed using Matlab R2017a running on a 2.9GHz i7-7820HQ PC with 16GB memory.

6.1 The st and -th moment problem in the newsvendor model

We first consider the st and -th moment problem (MP1t) in Section 3 for a given (the order quantity in the newsvendor model). According to Theorem 3.1, this problem has a closed-form solution if . Otherwise, the problem cannot be solved analytically. In this case, a semi-analytical solution is presented in Theorem 3.1 such that the optimal value is determined by a parameter that can be any root of the equation defined in (1) and can be found using the bisection method presented in Algorithm 1. In the following, we summarize this procedure for solving problem (MP1t) in Algorithm 2, where BM is the bisection method defined in Algorithm 1.

There are two other approaches that can solve the dual problem (DMP1t) of (MP1t). The first one is the classical SDP approach introduced by Bertsimas and Popescu, (2005). However, this approach works only if is a rational number, and its dimension also depends on , which could possibly lead to a high computational cost. The second approach solves the dual problem (DMP1t) with the relative entropy (RE) formulation due to Das et al., (2021). Since both the SDP formulation and the RE formulation are convex, we can resort to an off-the-shelf convex optimization solver such as SDPT3 (version 4.0) for an exact solution.

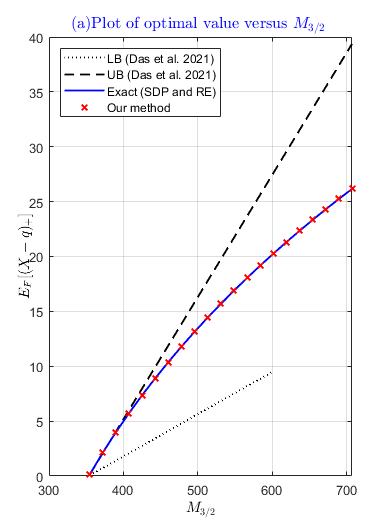

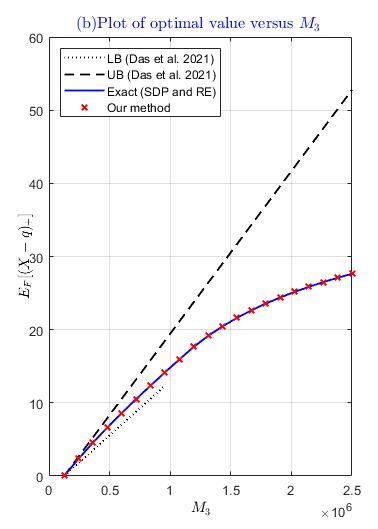

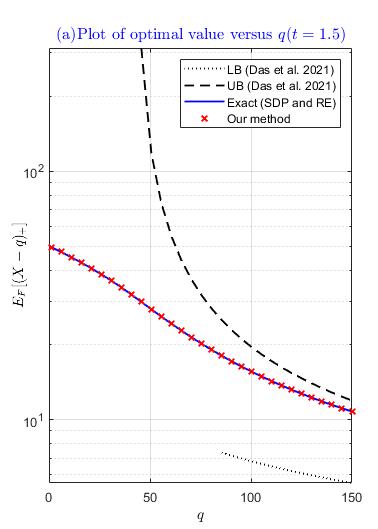

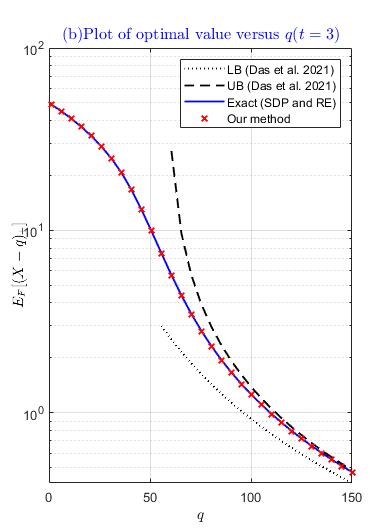

In the numerical experiment, we apply our Algorithm 2, the SDP approach, and the RE approach to solve the st and -th moment problem (MP1t) with and , and compare the optimal values computed by the three algorithms with the upper and lower bounds (abbreviated as UB and LB) from Das et al., (2021). We set the order quantity and mean demand , and we visualize the optimal value as a function of in Figure 3. Then we set , , and , and we plot the optimal value as a function of in Figure 4. Both figures indicate that the value obtained by our method is strictly larger than the lower bound and less than the upper bound by a significant margin. Note that the curves of the upper and lower bounds fail to span the entire horizontal axis, as those bounds are only valid within certain ranges of and . Moreover, the two figures show that the curve obtained by our approach coincides with the curves of the SDP and RE approaches. This confirms that our method can solve the moment problem (MP1t) exactly.

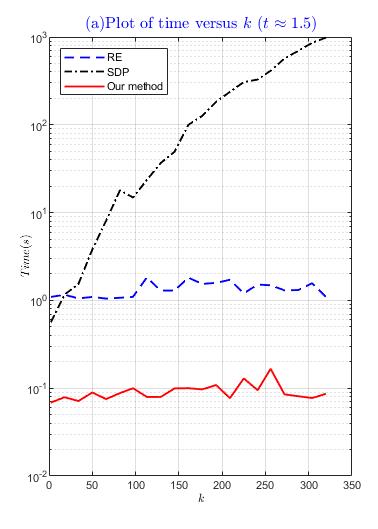

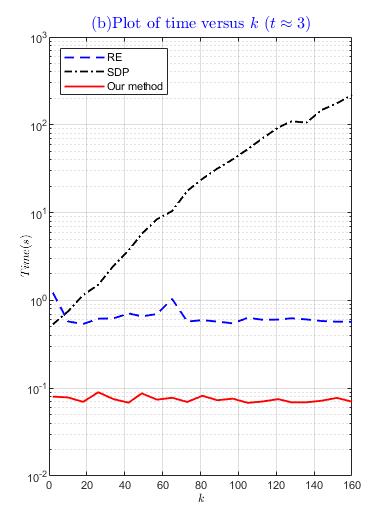

Since there are three algorithms that can solve problem (MP1t), we further report their running time in Figure 5 for and . We plot the running time as a function of with for Plot(a) and for Plot(b). In this figure, it can been seen that the running time of our method and of the RE approach remain almost constant regardless of the value of , while the SDP approach consumes much more time as the value of increases. This is because the dimension of the SDP is dependent on the numerator of , and our choices of make such a phenomenon noticeable.

6.2 The distributionally robust newsvendor model with a st and exponential moment ambiguity set

In this subsection, we further demonstrate the potential of our framework by solving a distributionally robust newsvendor problem that cannot be tackled by either the SDP or the RE approach. Recall that in the newsvendor model, the number of items needs to be ordered before the random demand is realized. Suppose that the unit revenue and unit purchase cost for this item are and , respectively, with . Given a cumulative distribution function of , we want to decide on the order quantity that will maximize the total expected profit:

where we assume that unsold units have zero salvage value. In practice, the exact demand distribution is often unknown, so here we assume that it lies in the following ambiguity set defined by the st and exponential moment:

| (38) |

In this subsection, we consider the distributional robust newsvendor problem that maximizes the worst-case expected profit with respect to the ambiguity set :

Using the relation , this problem is equivalent to

| (39) |

where denotes the critical ratio. Our approach to problem (39) is based on the observation that the objective function is convex in , as it is the maximum of a collection of convex functions having the form and the convexity is preserved under the maximum operator. Therefore, to globally minimize , we can resort to the golden section search method, which requires knowledge of the function value in each step of the search procedure. Furthermore, evaluating the function value for some given point is exactly the moment problem (MP1e) subject to the st and exponential moment constraints. According to Theorem 5.1, such a problem has a closed-form solution if , with . For other cases, a semi-closed form solution is presented in Theorem 3.1, where the optimal value is determined by a parameter that can be any root of the equation defined in (35). Similar to Algorithm 2, we use the bisection method BM defined in Algorithm 1 to find one root of (35) and thus solve the moment problem (MP1e) in Algorithm 3.

Letting EM be the operator for calling Algorithm 3, we present the golden section search method to solve the distributionally robust newsvendor problem (39) in Algorithm 4. We first input an interval with and , where can be found by repeatedly doubling its value until the inequality holds. Since is convex and the optimal solution , this procedure ensures that is included in . Then, in each step of the while loop in Algorithm 4, two points and are computed based on the golden ratio. These two points divide the search interval into three subintervals. We evaluate the function values at and by calling the operator EM, and drop the rightmost or leftmost subinterval based on a comparison of their values. If the length of the remaining interval is less than , the algorithm terminates and returns an -optimal order quantity.

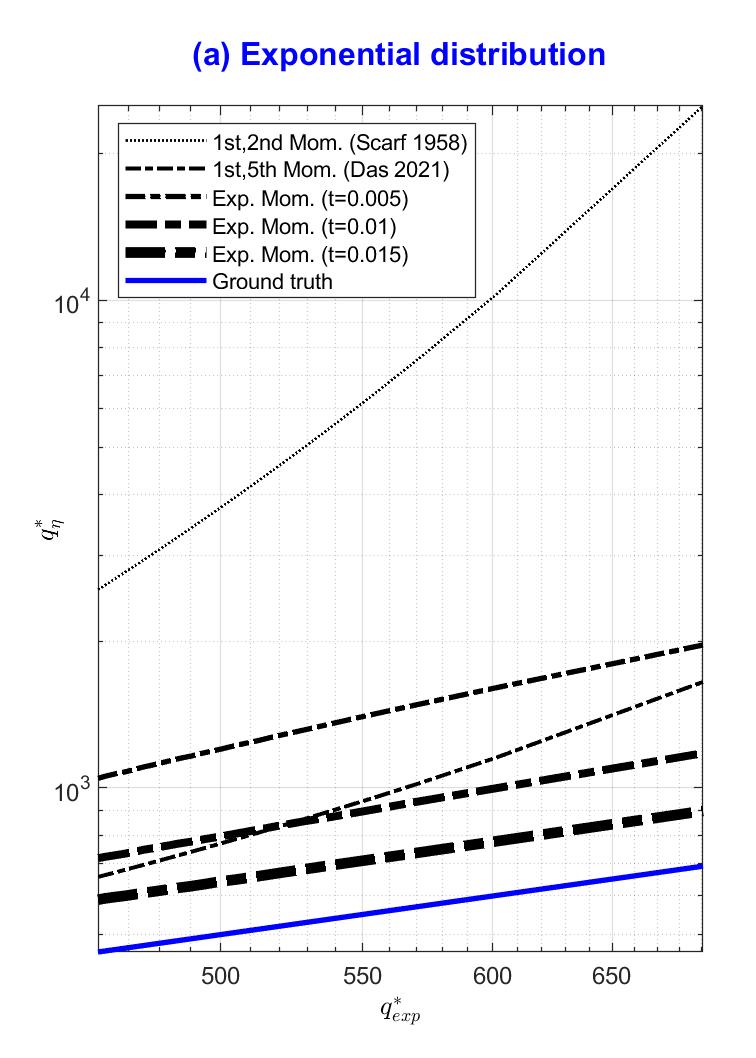

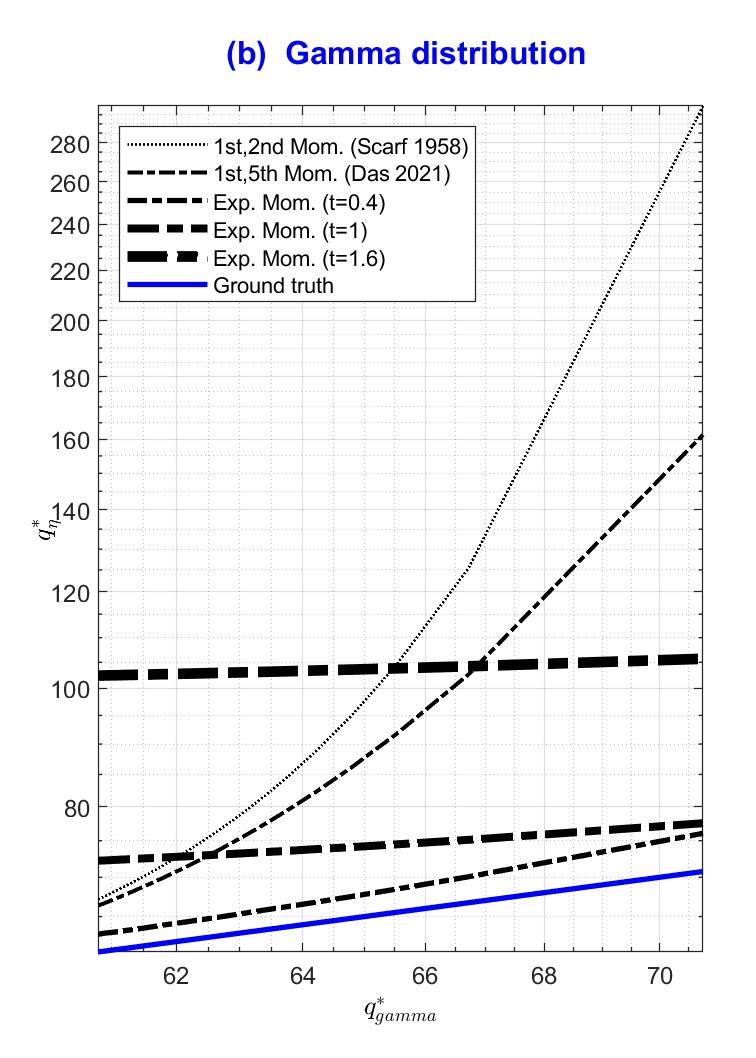

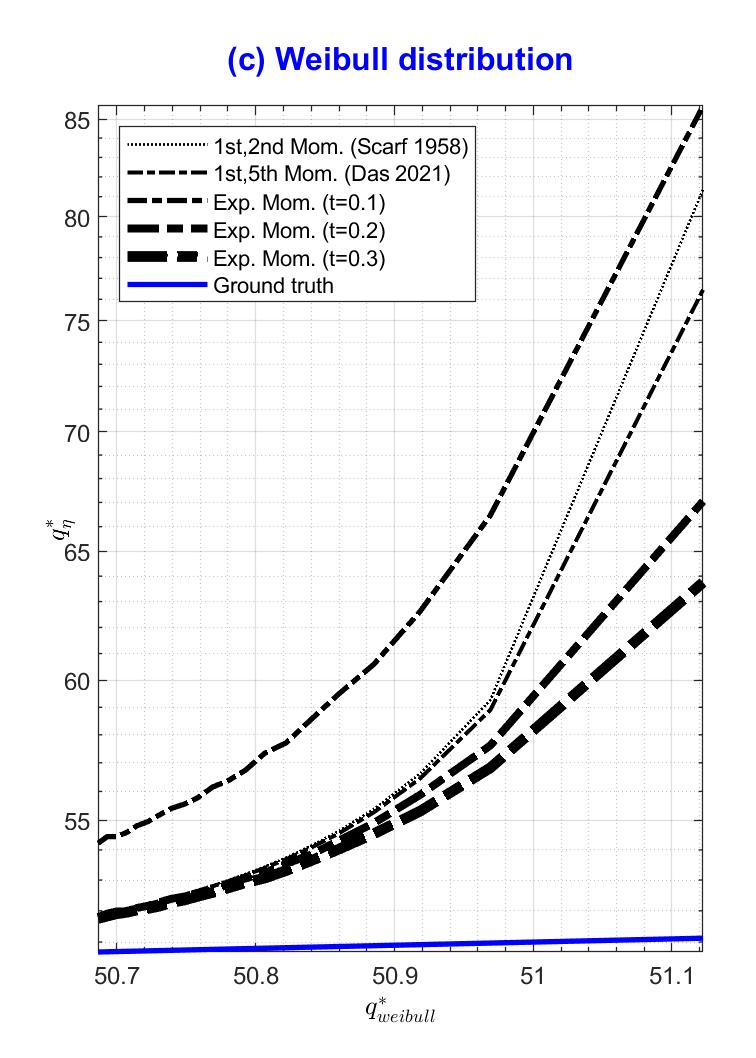

In the following experiment, we consider a classical newsvendor problem where a random demand follows a predetermined distribution that is unknown to the decision maker. We use robust models to hedge against the ambiguity in the distribution. In particular, we apply Algorithm 4 to solve the distributionally robust newsvendor model (39) and compare its optimal order quantity with two other distributionally robust models. The ambiguity sets of these two models are defined by the first two moments (Scarf’s model) and by the st and -th moments (the model in Das et al., 2021).

We further set as in Das et al., (2021), as the authors found that the st and th moments make the robust model less conservative and closer to the ground truth model than other settings in terms of the optimal order quantity. In addition, we provide the optimal order quantity for the ground truth model as a benchmark. Regarding the demand distribution of the ground truth model, we consider the following three distributions, which admit different types of light tailed behavior:

-

•

Exponential random variable (density function for ) with ;

-

•

Gamma random variable (density function for ) with and ;

-

•

Weibull random variable (density function for ) with and .

The parameters for the three distributions are deliberately chosen such that they are all light tailed and all moments of finite order exist, while the exponential moment in (38) exists only when

In Figure 6, we present the log-log plots of the optimal order quantities for the three distributionally robust newsvendor models, where the ground truth demand follows an exponential, gamma, or Weibull distribution. The horizontal-axis value and the vertical-axis value of every point in the subplots of Figure 6 represent, respectively, the optimal order quantities of the ground truth model and a specific distributionally robust model under the same critical ratio . Moreover, the critical ratio varies within the range for the exponential distribution, and within for the gamma and Weibull distributions. In Figure 6, it can been seen that Algorithm 4 solves the distributionally robust newsvendor problem (39) well, as it provides reasonable order quantities that are closer to the ground truth than the st and th moment model and Scarf’s model for most instances when the critical ratio is large. This also indicates that incorporating exponential moment information in the model has a better chance of capturing the light tailed behavior of the underlying distribution.

7 Conclusion

To summarize, we propose a framework that is built on a novel primal-dual optimality condition and provides a unified treatment for generalized moment problems. Through solving three concrete moment problems, we show that this framework not only reproduces some known analytical results, but also demonstrates great potential for accommodating nonstandard moments. Even for these well-studied models, our framework provides new insights. Therefore, it would be interesting to see whether there is any improvement when our framework is applied to other existing models. It is worth mentioning that our framework can also solve moment problems with shape constraints (Popescu, 2005, Perakis and Roels, 2008, Van Parys et al., 2016) that include symmetry, unimodality, convexity, and more. This is done by first using Choquet theory (Phelps, 2001, Popescu, 2005) to transform these problems into problems without shape constraints and then applying the framework. However, there are some related problems that our framework cannot handle. These problems include non-convex-shaped moment problems (Chen et al., 2021) and discrete moment problems (Ninh and Prékopa, 2013, Prékopa et al., 2016, Ninh et al., 2019). This is due to their inherent nonconvex natures (see, e.g., Chen et al., 2021) and the nonsmoothness of the functions in the dual constraints (see, e.g., Prékopa et al., 2016), which we leave for future work. Another possible research direction is to extend the current framework from the univariate case to the multivariate case, as the moment problem with multidimensional random variables has more meaningful applications. One thought that immediately comes to mind is to replace the derivatives in condition (TagntCond) with directional derivatives in the multivariate setting. Then, combining the optimality conditions (PriCond), (SlackCond), and (TagntCond) will lead to a more complicated nonlinear system, which we also leave for further study.

Acknowledgments

S. He is supported by the National Natural Science Foundation of China [Grants 71771141,71825003 and 72192832] and the Program for Innovative Research Team of Shanghai University of Finance and Economics. B. Jiang’s research is supported by the National Natural Science Foundation of China [Grants 72171141, 72150001 and 11831002], and Program for Innovative Research Team of Shanghai University of Finance and Economics. Jiayi Guo is supported by the National Natural Science Foundation of China [Grant 72101139], Shanghai Sailing Program [Grant 20YF1412200], and the Fundamental Research Funds for the Central Universities.

References

- Ben-Tal and Teboulle, (2007) Ben-Tal, A. and Teboulle, M. (2007). An old-new concept of convex risk measures: The optimized certainty equivalent. Mathematical Finance, 17(3):449–476.

- Bertsimas et al., (2010) Bertsimas, D., Doan, X. V., Natarajan, K., and Teo, C.-P. (2010). Models for minimax stochastic linear optimization problems with risk aversion. Mathematics of Operations Research, 35(3):580–602.

- Bertsimas and Popescu, (2005) Bertsimas, D. and Popescu, I. (2005). Optimal inequalities in probability theory: A convex optimization approach. SIAM Journal on Optimization, 15(3):780–804.

- Chebyshev, (1874) Chebyshev, P. L. (1874). Sur les valeurs limites des intégrales. Imprimerie de Gauthier-Villars.

- Chen et al., (2011) Chen, L., He, S., and Zhang, S. (2011). Tight bounds for some risk measures, with applications to robust portfolio selection. Operations Research, 59(4):847–865.

- Chen et al., (2021) Chen, X., He, S., Jiang, B., Ryan, C. T., and Zhang, T. (2021). The discrete moment problem with nonconvex shape constraints. Operations Research, 69(1):279–296.

- Chen et al., (2019) Chen, Z., Sim, M., and Xu, H. (2019). Distributionally robust optimization with infinitely constrained ambiguity sets. Operations Research, 67(5):1328–1344.

- Das et al., (2021) Das, B., Dhara, A., and Natarajan, K. (2021). On the heavy-tail behavior of the distributionally robust newsvendor. Operations Research, 69(4):1077–1099.

- Delage and Ye, (2010) Delage, E. and Ye, Y. (2010). Distributionally robust optimization under moment uncertainty with application to data-driven problems. Operations Research, 58(3):595–612.

- Dennis and Schnabel, (1983) Dennis, J. E. and Schnabel, R. B. (1983). Numerical methods for unconstrained optimization and nonlinear equations. Prentice-Hall, Englewood Cliffs.

- Elmachtoub et al., (2021) Elmachtoub, A. N., Gupta, V., and Hamilton, M. L. (2021). The value of personalized pricing. Management Science, 67(10):6055–6070.

- Fathony et al., (2018) Fathony, R., Rezaei, A., Bashiri, M. A., Zhang, X., and Ziebart, B. D. (2018). Distributionally robust graphical models. In Proceedings of the 32nd International Conference on Neural Information Processing Systems, pages 8354–8365.

- Ghaoui et al., (2003) Ghaoui, L. E., Oks, M., and Oustry, F. (2003). Worst-case value-at-risk and robust portfolio optimization: A conic programming approach. Operations Research, 51(4):543–556.

- Han et al., (2014) Han, Q., Du, D., and Zuluaga, L. F. (2014). A risk-and ambiguity-averse extension of the max-min newsvendor order formula. Operations Research, 62(3):535–542.

- He et al., (2010) He, S., Zhang, J., and Zhang, S. (2010). Bounding probability of small deviation: A fourth moment approach. Mathematics of Operations Research, 35(1):208–232.

- Honorio and Jaakkola, (2014) Honorio, J. and Jaakkola, T. (2014). Tight bounds for the expected risk of linear classifiers and Pac-Bayes finite-sample guarantees. In Artificial Intelligence and Statistics, pages 384–392. PMLR.

- Kelley, (1995) Kelley, C. T. (1995). Iterative methods for linear and nonlinear equations. In Frontiers in Applied Mathematics 16. SIAM.

- Lanckriet et al., (2002) Lanckriet, G. R., Ghaoui, L. E., Bhattacharyya, C., and Jordan, M. I. (2002). A robust minimax approach to classification. Journal of Machine Learning Research, 3(Dec):555–582.

- Li, (2018) Li, J. Y.-M. (2018). Closed-form solutions for worst-case law invariant risk measures with application to robust portfolio optimization. Operations Research, 66(6):1533–1541.

- Markov, (1884) Markov, A. (1884). On certain applications of algebraic continued fractions. Unpublished Ph. D. thesis, St Petersburg.

- Mehrotra and Zhang, (2014) Mehrotra, S. and Zhang, H. (2014). Models and algorithms for distributionally robust least squares problems. Mathematical Programming, 146(1):123–141.

- More, (1978) More, J. J. (1978). The Levenberg-Marquardt algorithm: Implementation and theory. In Lecture Notes in Mathematics 630: Numerical Analysis, pages 105–116. Springer-Verlag.

- Natarajan et al., (2010) Natarajan, K., Sim, M., and Uichanco, J. (2010). Tractable robust expected utility and risk models for portfolio optimization. Mathematical Finance: An International Journal of Mathematics, Statistics and Financial Economics, 20(4):695–731.

- Natarajan et al., (2018) Natarajan, K., Sim, M., and Uichanco, J. (2018). Asymmetry and ambiguity in newsvendor models. Management Science, 64(7):3146–3167.

- Ninh et al., (2019) Ninh, A., Hu, H., and Allen, D. (2019). Robust newsvendor problems: Effect of discrete demands. Annals of Operations Research, 275(2):607–621.

- Ninh and Prékopa, (2013) Ninh, A. and Prékopa, A. (2013). The discrete moment problem with fractional moments. Operations Research Letters, 41(6):715–718.

- Perakis and Roels, (2008) Perakis, G. and Roels, G. (2008). Regret in the newsvendor model with partial information. Operations Research, 56(1):188–203.

- Phelps, (2001) Phelps, R. R. (2001). Lectures on Choquet’s theorem. Springer Science & Business Media.

- Popescu, (2005) Popescu, I. (2005). A semidefinite programming approach to optimal-moment bounds for convex classes of distributions. Mathematics of Operations Research, 30(3):632–657.

- Popescu, (2007) Popescu, I. (2007). Robust mean-covariance solutions for stochastic optimization. Operations Research, 55(1):98–112.

- Prékopa et al., (2016) Prékopa, A., Ninh, A., and Alexe, G. (2016). On the relationship between the discrete and continuous bounding moment problems and their numerical solutions. Annals of Operations Research, 238(1-2):521–575.

- Roos et al., (2021) Roos, E., Brekelmans, R., van Eekelen, W., den Hertog, D., and van Leeuwaarden, J. S. (2021). Tight tail probability bounds for distribution-free decision making. European Journal of Operational Research.

- Rujeerapaiboon et al., (2016) Rujeerapaiboon, N., Kuhn, D., and Wiesemann, W. (2016). Robust growth-optimal portfolios. Management Science, 62(7):2090–2109.

- Scarf, (1958) Scarf, H. (1958). A min-max solution of an inventory problem. Studies In The Mathematical Theory of Inventory and Production, (201–209).

- Smith, (1995) Smith, J. E. (1995). Generalized Chebychev inequalities: Theory and applications in decision analysis. Operations Research, 43(5):807–825.

- Tamuz, (2013) Tamuz, O. (2013). A lower bound on seller revenue in single buyer monopoly auctions. Operations Research Letters, 41(5):474–476.

- Van Parys et al., (2016) Van Parys, B. P., Goulart, P. J., and Kuhn, D. (2016). Generalized Gauss inequalities via semidefinite programming. Mathematical Programming, 156(1-2):271–302.

- Yue et al., (2006) Yue, J., Chen, B., and Wang, M.-C. (2006). Expected value of distribution information for the newsvendor problem. Operations Research, 54(6):1128–1136.

- Zuluaga et al., (2009) Zuluaga, L. F., Peña, J., and Du, D. (2009). Third-order extensions of Lo’s semiparametric bound for European call options. European Journal of Operational Research, 198(2):557–570.

- Zymler et al., (2013) Zymler, S., Kuhn, D., and Rustem, B. (2013). Worst-case value at risk of nonlinear portfolios. Management Science, 59(1):172–188.

Proofs

8 Proofs for Section 3

8.1 Proof of Proposition 3.2

Proof 8.1

Since and , we have . A straightforward calculation shows that

and statement i) follows.

When , we let , which is equivalent to . We can express the quantity as

Next we define the function , and we have . Then is increasing whenever and decreasing whenever . Therefore, for all . In particular, for , we have , which completes the proof of statement ii).

When , it is easy to verify that . Then it remains to calculate . To this end, we introduce two functions and such that . Since , and , we obtain

with the last inequality due to our assumption that . Therefore, statement iii) is also valid.

Based on the above results, we are able to apply the bisection method in Algorithm 1 to the function in the interval with a given precision . In particular, when , the left end point is , and we have and . Then, similar to the standard bisection method, Algorithm 1 can find a root of equation (1) within iterations. On the other hand, when , the left end point is , and we have with and . Therefore, there exists such that for any . Hence, the updated interval after each iteration can still include at least one root of , and Algorithm 1 can still terminate within iterations and return a root of equation (1).

8.2 Proof of Lemma 3.3

Proof 8.2

Suppose that there are two points such that . Since is convex in , we have, for any with , . Thus, we have when , which has a constant derivative and contradicts the assumption of a strictly increasing derivative of . Hence, there must be at most one root of in . Finally, by a similar argument, the other case (i.e., is continuous at ) of conclusion (i) as well as conclusion (ii) follow.

9 Proofs for Section 4

9.1 Proof of Lemma 4.2

Proof 9.1

Since with , the optimal support cannot be a singleton. Now consider the following dual constraint:

associated with the dual optimal solution . It is obvious that , for otherwise the coefficient of the quadratic term is for and thus for sufficiently large , which violates the dual constraint.

According to the complementary slackness condition, the dual constraint must be tight at the supporting points of the primal optimal distribution. Therefore, in the following we shall identify the optimal support by searching areas where the dual constraint could be tight.

If , is concave quadratic whenever or , so has at most one root in , for otherwise, there would exist two roots and with such that for . Then we would have when , which violates the dual constraint for . Since is also concave quadratic whenever , a similar argument shows that has at most one root in . Suppose that and are the two roots of in and , respectively. Then we must have , for otherwise and are both included in either or or the optimal distribution is single-point supported, which is a contradiction. Therefore, we have support with , and prove statement i).

If , is convex quadratic whenever and concave quadratic whenever . Then, by a similar argument for that i), has at most one root in . Since is convex quadratic in , there exist at most two roots and , with , such that . Then we must have , for otherwise in or in , which violates the dual constraint for . Therefore, , and with are the only possible roots of , and cannot both be roots, as has at most one root in . In addition, cannot constitute all of the roots, for otherwise the support , which contradicts our assumption that . Therefore, with are the only roots of . That is, , and statement ii) follows.

If , then for all . In this case we must have , and hence is decreasing for . Consequently, we have for as long as is nonpositive at the left end point, i.e., . In the other case where , we have . Thus, for is ensured by and . Since maximizes with in the objective function, the aforementioned three inequalities on should be tight, i.e.,

| (40) |

That is, and for any . Therefore, the support , and statement iii) is proved.

9.2 Proof of Lemma 4.3

9.3 Proof of Lemma 4.4

Proof 9.3

We first construct in accordance with (41) such that and are respectively the probabilities of and in the support of the distribution defined in (31). Therefore, satisfy and from (41), which gives us . Turning to the ranges of and , we note from Lemma EC.1 in Han et al., (2014) that the feasibility of problem (MP) implies that , and thus

| (43) |

where the first inequality is due to the assumption that . Moreover, this assumption together with the argument at the end of Lemma 4.3 guarantees that (42) holds, which combined with (43) yields that . In addition, we also have , as

| (44) |

Therefore, , and as well. That is, is a primal feasible solution of (MP). Next we construct the dual solution satisfying

| (45) |

which is the solution to the linear system

| (46) |

from (SlackCond) and (TagntCond). To verify the dual feasibility of , recalling that we have proved , we must have , for otherwise holds, which contradicts the assumption that . In addition, the assumption implies that . Those facts together with (46) indicate the following dual constraint function:

Moreover, the expression of in (45) gives us

where the last inequality is due to (44). Therefore, for all , and is a dual feasible solution. In addition, also satisfies the complementary slackness condition due to (46), and thus we conclude that is an optimal primal-dual solution pair such that the distribution defined in (31) is optimal for (MP).

9.4 Proof of Lemma 4.5

Proof 9.4

For any feasible support of problem (MP) with for all , let be the probability of and be the probability of in the support. Then the following hold:

Therefore, the associated objective value is

which is a constant. Since the optimal support , we conclude that any feasible support with for all has the same objective and thus is optimal. In addition, a straightforward computation shows that

The equality holds only when , by the Cauchy-Schwarz inequality, and so the support reduces to with , which is the case discussed in Lemma 4.3. Therefore, we consider the optimal support to include three points: , with probabilities , , and , respectively. We solve the equation

| (47) |

In this case, we must have and , which is equivalent to . As a result, we obtain , which completes the proof.

9.5 Proof of Lemma 4.6

Proof 9.5

We construct in accordance with (47), such that , , and are respectively the probabilities of , , and in the support of the distribution defined in (32). Since we have proved that and in Lemma 4.3, we have . Moreover, an equivalent reformulation of shows that

which together with implies that as well. Therefore, is a primal feasible solution of (MP). Next, we construct by solving (40) and letting . The associated dual function is

Consequently, is a dual feasible solution. In addition, recall that , and observe that , as . Therefore, , and the complementary slackness condition (SlackCond) holds. As a result, is an optimal primal-dual pair such that the distribution defined in (32) is optimal for (MP).

10 Proofs for Section 5

10.1 Proof of Proposition 5.2

Proof 10.1

We start with definition (33) of , which can be rewritten as . According to the definition of the Lambert W function, we have , and with some simplification we obtain the equivalent formulation

| (48) |

Noting that , as we assume and , we obtain

| (49) |

Then the strictly increasing property of implies . Consequently,

| (50) |

due to the Lambert W function being strictly decreasing in . Therefore, we have

where the last inequality is due to being a decreasing function in and the assumption that . This proves statement i).

Now we consider the case , for which we have

Since is a strictly increasing function for , we have , which implies that . Therefore, is well defined. To further prove , it suffices to show that

| (51) |

We first note that , as

is strictly increasing for .

Multiplying both sides of this inequality by and recalling that , we conclude that

, which further implies

. Therefore, (51) follows from the observation that is a strictly increasing function when , and hence statement ii) is proved.

Turning to the case , since , we have

which completes the proof of statement iii).

Therefore, the function has opposite signs at the two end points of the interval , and the bisection method can find a root of within iterations for a given precision .

10.2 Proof of Lemma 5.3

Proof 10.2

First, the optimal distribution of (MP1e) cannot be supported by a single point, as we assume that . Then the rest of the proof is similar to the proof of Lemma 3.4, except that the dual constraint is changed to

| (52) |

where is the optimal solution of the dual problem (DMP1e). We still have , for otherwise for sufficiently large , contradicting the feasibility of . When , the dual constraint is identical to that of (DMP1t) with , and hence the proof in Lemma 3.4 can be applied. Moreover, when , the function is still convex in and has a strictly positive derivative. Therefore, the conclusion follows by an argument similar to Lemma 3.4 for the case .

10.3 Proof of Lemma 5.4

Proof 10.3

Suppose that the optimal distribution of (MP1e) is supported by with probabilities and , respectively, and that is an optimal solution of the dual problem (DMP1e) with the constraint function defined in (52). In this case, the condition (TagntCond) gives us . According to Theorem 2.1, and satisfy conditions (PriCond), (SlackCond), and (TagntCond), which together are equivalent to

| (53) |

Solving the above equations gives us

| (54) |

Note that the first equality above is equivalent to and that

so or , where and are the two branches of the Lambert W function. As our assumption indicates that , we must have , i.e., (33) holds. In addition, as the second system of equations in (53) implies , the dual feasibility of requires . Note that the denominator

| (55) |

as and is a strictly increasing function for . Therefore, implies , or equivalently

10.4 Proof of Lemma 5.5

Proof 10.4

We construct and in accordance with (54), where and correspond to the probabilities associated with the support points and of the distribution described in (36). We need to show that is the optimal primal-dual solution pair for problems (MP1e) and (DMP1e). First, we observe that due to the assumption . Since the function is strictly increasing whenever , we conclude that and is a primal feasible solution. Next, we verify the dual feasibility of . According to the expression of in (54) and the inequality (55), we have and that defined in (52) is convex in and in , as for any and . Moreover, we have by the assumption that and the argument at the end of Lemma 5.4. We also note by the second system of equations in (53). It follows that

where we use the fact from (49). Furthermore, since is a continuous function, as well, and thus is a feasible solution for the dual problem (DMP1e). In addition, also satisfies the complementary slackness condition due to the second system of equations in (53), and thus we conclude that is an optimal primal-dual solution pair.

10.5 Proof of Lemma 5.6

Proof 10.5

Suppose that the optimal distribution of (MP1e) is supported by with probabilities and , respectively, and that is an optimal solution of the dual problem (DMP1e). In this case, the condition (TagntCond) gives us and . According to Theorem 2.1, and satisfy the conditions (PriCond), (SlackCond), and (TagntCond), which together are equivalent to

| (56) |

The first system of equations in (56) has a solution if and only if

As a result,

| (58) |

By a similar argument, the feasibility of the second system of equations in (56) gives us

| (70) | |||||

| (76) |

which further implies that , or equivalently

| (77) |

Consequently, we have

Therefore, , and we can substitute this expression of in =0, which is a reformulation of (58). Consequently, is a root of . Finally, we want to show that

| (78) |

and the key is to prove that the middle inequality holds. To this end, we consider the function , and for it is easy to verify that

Hence, is strictly increasing with respect to if , and consequently . Moreover, is increasing with respect to on , as when . Therefore, it remains to show that , which gives

and the middle inequality in (78) holds. Hence, we construct the functions

| (79) |

Noting that is decreasing on since , we have

Therefore, is a strictly increasing function, and . As a result, we have

Since is strictly increasing when , the above equality implies that .

10.6 Proof of Lemma 5.7

Proof 10.6

Suppose that is any root of equation (35), and construct . Since and defined in (79) is strictly decreasing, we have , which yields . Moreover, recalling that , we have and the following construction

is well defined, where and are the solutions of the two linear equations in (56). Therefore, to confirm the primal feasibility, all that remains is to show that , or equivalently, , due to the construction of . Recall that the function defined in (79) is strictly increasing on . Since and , we must have , for otherwise, cannot have the same value at and . Next we verify the dual feasibility of . The second system of equations in (56) indicates that

| (80) |

In addition, since we showed at the very beginning of the proof that , it follows that and when . Therefore, is convex in and , which combined with (80) gives us

Since is continuous at , we conclude that for all , and thus is a dual feasible solution. Observing that the complementary slackness condition is already implied by , we conclude that is indeed an optimal primal-dual solution pair, as desired.