On randomized sketching algorithms and the Tracy-Widom law

Abstract

There is an increasing body of work exploring the integration of random projection into algorithms for numerical linear algebra. The primary motivation is to reduce the overall computational cost of processing large datasets. A suitably chosen random projection can be used to embed the original dataset in a lower-dimensional space such that key properties of the original dataset are retained. These algorithms are often referred to as sketching algorithms, as the projected dataset can be used as a compressed representation of the full dataset. We show that random matrix theory, in particular the Tracy-Widom law, is useful for describing the operating characteristics of sketching algorithms in the tall-data regime when . Asymptotic large sample results are of particular interest as this is the regime where sketching is most useful for data compression. In particular, we develop asymptotic approximations for the success rate in generating random subspace embeddings and the convergence probability of iterative sketching algorithms. We test a number of sketching algorithms on real large high-dimensional datasets and find that the asymptotic expressions give accurate predictions of the empirical performance.

1 Introduction

Sketching is a probabilistic data compression technique that makes use of random projection (Cormode, 2011; Mahoney, 2011; Woodruff, 2014). Suppose interest lies in a dataset . When and or are large, typical data analysis tasks will involve a heavy numerical computing load. This computational burden can be a practical obstacle for statistical learning with Big Data. When the sample size is the computational bottleneck, sketching algorithms use a linear random projection to create a smaller sketched dataset of size , where . The random projection can be represented as a random matrix , and the sketched dataset is generated through the linear embedding . The smaller sketched dataset is used as a surrogate for the full dataset within numerical routines. Through a judicious choice of the distribution on the random sketching matrix , it is often possible to bound the error that is introduced stochastically into calculations given the use of the randomized approximation in place of

The selected distribution of the random sketching matrix can be divided into two categories, data-oblivious sketches, where the distribution is not a function of the source data , and data-aware sketches, where the distribution is a function of . The majority of data-aware sketches perform weighted sampling with replacement, and are closely connected to finite population survey sampling methods (Ma et al., 2015; Quiroz et al., 2018). The analysis of data-oblivious sketches requires different methods to data-aware sketches, as there are no clear ties to finite-population subsampling. In general, data-oblivious sketches generate a dataset of pseudo-observations, where each instance in the compressed representation has no exact counterpart in the original source dataset .

Three important data-oblivious sketches are the Gaussian sketch, the Hadamard sketch and the Clarkson-Woodruff sketch. The Gaussian sketch is the simplest of these, where each element in the matrix is an independent sample from a distribution. The Hadamard sketch uses structured elements for fast matrix multiplication, and the Clarkson-Woodruff uses sparsity in for efficient computation of the sketched dataset. The comparative performance between distributions on is of interest, as there is a trade-off between the computational cost of calculating and the fidelity of the approximation with respect to original when choosing the type of sketch. Our results help to establish guidelines for selecting the sketching distribution.

Sketching algorithms are typically framed using stochastic error bounds, where the algorithm is shown to attain accuracy with probability at least (Woodruff, 2014). These notions are made more precise in Section 2. Existing bounds are typically developed from a worst-case non-asymptotic viewpoint (Mahoney, 2011; Woodruff, 2014; Tropp, 2011). We take a different approach, and use random matrix theory to develop asymptotic approximations to the success probability given the sketching distortion factor .

Our main result is an asymptotic expression for the probability that a Gaussian based sketching algorithm satisfies general probabilistic error bounds in terms of the Tracy-Widom law (Theorem 1), which describes the distribution of the extreme eigenvalues of large random matrices (Tracy and Widom, 1994; Johnstone, 2001). We then identify regularity conditions where other data-oblivious projections are expected to demonstrate the same limiting behavior (Theorem 3). If the motivation for using a sketching algorithm is data compression due to large , the asymptotic approximations are of particular interest as they become more accurate as the computational benefits afforded by the use of a sketching algorithm increase in tandem. Empirical work has found that the quality of results can be consistent across the choice of random projections (Venkatasubramanian and Wang, 2011; Le et al., 2013; Dahiya et al., 2018), and our results shed some light on this issue. An application is to determine the convergence probability when sketching is used in iterative least-squares optimisation. We test the asymptotic theory and find good agreement on datasets with large sample sizes . Our theoretical and empirical results show that random matrix theory has an important role in the analysis of data-oblivious sketching algorithms for data compression.

2 Sketching

2.1 Data-oblivious sketches

As mentioned, a key component in a sketching algorithm is the distribution on . Four important random linear maps are:

-

•

The uniform sketch implements subsampling uniformly with replacement followed by a rescaling step. The Uniform projection can be represented as . The random matrix subsamples rows of with replacement. Element if observation in the source dataset is selected in the th subsampling round . The uniform sketch can be implemented in time.

-

•

A Gaussian sketch is formed by independently sampling each element of from a distribution. Computation of the sketched data is .

-

•

The Hadamard sketch is a structured random matrix (Ailon and Chazelle, 2009). The sketching matrix is formed as , where is a matrix and and are both matrices. The fixed matrix is a Hadamard matrix of order . A Hadamard matrix is a square matrix with elements that are either or and orthogonal rows. Hadamard matrices do not exist for all integers , the source dataset can be padded with zeroes so that a conformable Hadamard matrix is available. The random matrix is a diagonal matrix where each of the diagonal entries is an independent Rademacher random variable. The random matrix subsamples rows of with replacement. The structure of the Hadamard sketch allows for fast matrix multiplication, reducing calculation of the sketched dataset to operations.

-

•

The Clarkson-Woodruff sketch is a sparse random matrix (Clarkson and Woodruff, 2013). The projection can be represented as the product of two independent random matrices, , where is a random matrix and is a random matrix. The matrix is initialized as a matrix of zeros. In each column, independently, one entry is selected and set to . The matrix is a diagonal matrix where each of the diagonal entries is an independent Rademacher random variable. This results in a sparse , where there is only one nonzero entry per column. The sparsity of the Clarkson-Woodruff sketch speeds up matrix multiplication, dropping the complexity of generating the sketched dataset to .

The Gaussian sketch was central to early work on sketching algorithms (Sarlos, 2006). The drawback of the Gaussian sketch is that computation of the sketched data is quite demanding, taking operations. As such, there has been work on designing more computationally efficient random projections.

Sketch quality is commonly measured using -subspace embeddings (Woodruff (2014, Chapter 2), Meng and Mahoney (2013), Yang et al. (2015)). These are defined below.

Definition 1.

-subspace embedding

For a given matrix , we call a matrix an -subspace embedding for , if for all vectors

An -subspace preserves the linear structure of the original dataset up to a multiplicative factor. Broadly speaking, the covariance matrix of the sketched dataset is similar to the covariance matrix of the source dataset if is small. Mathematical arguments show that the sketched dataset is a good surrogate for many linear statistical methods if the sketching matrix is an -subspace embedding for the original dataset, with sufficiently small (Woodruff, 2014). Suitable ranges for depend on the task of interest and structural properties of the source dataset (Mahoney and Drineas, 2016).

The Gaussian, Hadamard and Clarkson-Woodruff projections are popular data-oblivious projections as it is possible to argue that they produce -subspace embeddings with high probability for an arbitrary data matrix . It is considerably more difficult to establish universal worst case bounds for the uniform projection (Drineas et al., 2006; Ma et al., 2015). We include the uniform projection in our discussion as it is a useful baseline.

| Sketch | Sketching time | Required sketch size | |

|---|---|---|---|

| Gaussian | |||

| Hadamard | |||

| Clarkson-Woodruff | |||

| Uniform |

2.2 Sketching algorithms

Sketching algorithms have been proposed for key linear statistical methods such as low rank matrix approximation, principal components analysis, linear discriminant analysis and ordinary least squares regression (Mahoney, 2011; Woodruff, 2014; Erichson et al., 2016; Falcone et al., 2021). Sketching has also been investigated for Bayesian posterior approximation (Bardenet and Maillard, 2015; Geppert et al., 2017). A common thread throughout these works is the reliance on the generation of an -subspace embedding. In general, serves an approximation tolerance parameter, with smaller guaranteeing higher fidelity to exact calculation with respect to some divergence measure.

An example application of sketching is ordinary least squares regression (Sarlos, 2006). The sketched responses and predictors are defined as . Let , and . It is possible to establish the concrete bounds, that if is an -subspace embedding for (Sarlos, 2006), then

where represents the smallest singular value of the design matrix . If is very small, then is a good approximation to .

Given the central role of -subspace embeddings (Definition 1), the success probability,

| (1) |

is thus an important descriptive measure of the uncertainty attached to the randomized algorithm. The probability statement is over the random sketching matrix with the dataset treated as fixed. The embedding probability is difficult to characterize precisely using existing theory (Venkatasubramanian and Wang, 2011). The bounds in Table 1 only give qualitative guidance about the embedding probability. Users will benefit from more prescriptive results in order to choose the sketch size , and the type of sketch for applications (Grellmann et al., 2016; Geppert et al., 2017; Ahfock et al., 2020; Falcone et al., 2021).

Another use for sketching is in iterative solvers for ordinary least squares regression. A sketch can be used to generate a random preconditioner, , that is then applied to the normal equations . Given some initial value , the iteration is defined as

| (2) |

If the iteration will converge in a single step. The degree of noise in the preconditioner will be influenced by the sketch size . A sufficient condition for convergence of the iteration (2) is that is an -subspace embedding for with (Pilanci and Wainwright, 2016). As is typical with randomized algorithms, we accept some failure probability in order to relax the computational demands. It is of interest to develop expressions for the failure probability of the algorithm as a function of the sketch size , as this can give useful guidelines in practice. It is possible to establish worst case bounds using the results in Table 1, however we will aim to give a point estimate of the probability. Although it is possible to improve on the iteration (2) using acceleration methods (Meng et al., 2014; Dahiya et al., 2018; Lacotte et al., 2020), we focus on the basic iteration to introduce our asymptotic techniques.

2.3 Operating characteristics

Let the singular value decomposition of the source dataset be given by . Let and denote the minimum and maximum singular values respectively, of a matrix . Likewise, let and denote the minimum and maximum eigenvalues of a matrix . It is possible to show

| (3) |

where is the matrix of left singular vectors of the source data matrix (Woodruff, 2014). Now as

| (4) |

the extreme eigenvalues of are the critical factor in generating -subspace embeddings. The convergence behavior of the basic iteration (2) is also tied to the eigenvalues of where . Providing that is of rank , the maximum eigenvalue satisfies

From standard results on iterative solvers (Hageman and Young, 2012), a necessary and sufficient condition for the iteration to converge is if and only if . The probability of convergence can then be expressed as

| (5) |

Most existing results on the probabilities (3) and (5) are finite sample lower bounds (Tropp, 2011; Nelson and Nguyên, 2013; Meng, 2014). Worst case bounds can be conservative in practice, and there is value in developing other methods to characterize the performance of randomized algorithms (Halko et al., 2011; Raskutti and Mahoney, 2014; Lopes et al., 2018; Dobriban and Liu, 2018). The embedding probability (3) and the convergence probability (5) are related to the extreme eigenvalues of . In Section 3 we study this distribution for the Gaussian sketch and develop a Tracy-Widom approximation. The approximation is then extended to the Clarkson-Woodruff and Hadamard sketches in Section 4.

3 Gaussian sketch

3.1 Exact representations

Meng (2014, Section 2.3) notes that when using a Gaussian sketch, it is instructive to consider directly the distribution of the random variable to study the embedding probability (3). Consider an arbitrary data matrix . As is a matrix of independent Gaussians with mean zero and variance , it is possible to show that

as . The key term is in some sense a pivotal quantity, as its distribution is invariant to the actual values of the data matrix . When using a Gaussian sketch, the probability of obtaining an -subspace embedding has no dependence on the number of original observations , or on the values in the data matrix . This is a useful property for a data-oblivious sketch, as it is possible to develop universal performance guarantees that will hold for any possible source dataset. This invariance property is also noted in Meng (2014), although the derivation is different.

Let us define the random matrix . The success probability of interest can then be expressed in terms of the extreme eigenvalues of the Wishart distribution The embedding probability of interest has the representation:

| (6) |

where we have made use of the expression for the maximum singular value (4).

It is difficult to obtain a mathematically tractable expression for the embedding probability as it involves the joint distribution of the extreme eigenvalues (Chiani, 2017). Meng forms a lower bound on the probability (6) using concentration results on the eigenvalues of the Wishart distribution.

The convergence probability (5), can also be related to the eigenvalues of the Wishart distribution. Assuming , the matrix has full rank with probability one. As such, using the same pivotal quantity as before,

| (7) |

where . The convergence probability (7) has no dependence on the specific response vector or design matrix under consideration. Problem invariance is a highly desirable property for a randomized iterative solver (Roosta-Khorasani and Mahoney, 2016; Lacotte et al., 2020). Both the embedding probability and the convergence probability are related to the extreme eigenvalues of the Wishart distribution. The extreme eigenvalues of Wishart random matrices are a well studied topic in random matrix theory (Edelman, 1988), and we can make use of existing results to analyse the operating characteristics of sketching algorithms. In the following section we develop approximations to the embedding probability and the convergence probability in the asymptotic regime:

| (8) |

The limit is asymptotic in , and , with the constraint that the number of variables to sketch size tends to a constant . This can be interpreted as a type of Big Data asymptotic, where we consider tall and wide datasets through the limit in and , and increasing sketch sizes to cope with the expanding number of variables . Although there is no explicit dependence on for the finite sample expressions (3) and (7) for the Gaussian sketch, the asymptotic limit in is still used to emphasize that we are taking limits in the tall-data setting.

Dobriban and Liu (2018) analyse the mean squared error of single-pass sketching algorithms for linear regression in this asymptotic framework under the assumption of a generative model. Our analysis is different as we are concerned with the embedding and convergence probabilities ((3) and (5)), rather than the accuracy of population parameter estimates. In independent work, Lacotte et al. (2020) study the limiting empirical spectral distribution of Hadamard sketch in the asymptotic regime (8). Here we are concerned with the fluctuations of the extreme eigenvalues rather than the bulk of the spectrum.

3.2 Random matrix theory

Random matrix theory involves the analysis of large random matrices (Bai and Silverstein, 2010). The Tracy-Widom law is an important result in the study of the extreme eigenvalue statistics (Tracy and Widom, 1994). Johnstone (2001) showed that Tracy-Widom law gives the asymptotic distribution of the maximum eigenvalue of a matrix after appropriate centering and scaling. In subsequent work Ma (2012) showed that the rate of convergence could be improved from to by using different centering and scaling constants than in Johnstone (2001). We build from the convergence result given by Ma.

The R package RMTstat contains a number of functions for working with the Tracy-Widom distribution (Johnstone et al., 2014). The main application of the Tracy-Widom law to statistical inference has been its use in hypothesis testing in high-dimensional statistical models (Johnstone, 2006; Bai and Silverstein, 2010). To the best of our knowledge, the connection to sketching algorithms has not been explored in great depth. The Tracy-Widom law can be used to approximate the embedding probability (3).

Theorem 1.

Suppose we have an arbitrary data matrix where and is of rank . Furthermore assume we take a Gaussian sketch of size . Consider the limit in and , such that with . Define centering and scaling constants and as

Set where is the Tracy-Widom distribution. Let give the exact embedding probability and let give the asymptotic approximation to the embedding probability:

Then asymptotically in and , for any ,

Furthermore, for even , .

The proof is given in the supplementary material.

The convergence probability of the iterative algorithm (5) can also be approximated using the Tracy-Widom law.

Theorem 2.

Suppose we have an arbitrary data matrix where and is of rank . Furthermore, assume we take a Gaussian sketch of size . Consider the limit in and , such that with . Set

and define the following centering and scaling constants . Set , where is the Tracy-Widom distribution. Let give the exact convergence probability, and give the asymptotic approximation to the convergence probability:

Then for all starting values , asymptotically in and ,

Furthermore, for even , .

The proof is given in the supplementary material.

The embedding probability for the Gaussian sketch can be estimated by simulating and using the empirical distribution of the random variable . To assess the accuracy of the approximation in Theorem 1, we generated random Wishart matrices . For each simulated matrix we computed the distortion factor for . The simulated distortion factors were used to give a Monte Carlo estimate of the embedding probability:

| (9) |

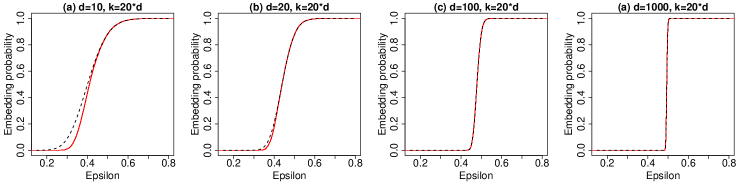

We used the ARPACK library (Lehoucq et al., 1998) to compute the maximum singular values . The estimated embedding probabilities are displayed in Figure 1 for different dimensions . The sketch size to variables ratio, , was held fixed at 20. The solid red line shows the empirical probability of obtaining an -subspace embedding. The dashed black line gives the Tracy-Widom approximation given in Theorem 1. The agreement is consistently good over dimensions , and the range of sketch sizes that were considered.

4 Computationally efficient sketches

4.1 Asymptotics

Asymptotic methods are useful to analyse data-oblivious sketches that do not admit interpretable finite sample distributions (Li et al., 2006; Ahfock et al., 2020; Lacotte et al., 2020). Here we describe the limiting behavior of the sketched algorithms for fixed and as the number of source observations increases.

Under an assumption on the limiting leverage scores of the source data matrix, we can establish a limit theorem for the Hadmard and Clarkson-Woodruff sketches. The leverage scores are an important structural property in sketching algorithms (Mahoney and Drineas, 2016).

Assumption 1.

Define the singular value decomposition of the source dataset as . Let give the th row in . Assume that the maximum leverage score tends to zero, that is

The asymptotic probability of obtaining an -subspace embedding for the Hadamard and Clarkson-Woodruff sketches can be related to the Wishart distribution.

Theorem 3.

Consider a sequence of arbitrary data matrices , where each data matrix is of rank , and is fixed. Let represent the singular value decomposition of . Let be a Hadamard or Clarkson-Woodruff sketching matrix where is also fixed. Suppose that Assumption 1 is satisfied. Then as tends to infinity with and fixed,

where .

The proof is given in the supplementary material.

Theorem 3 states the the embedding probability for the Hadamard and Clarkson-Woodruff sketches converges to that of the Gaussian sketch as . Therefore, Theorem 1 can also be used to approximate the embedding probability. Empirical studies have shown that the Hadamard and Clarkson-Woodruff sketches can give similar quality results to the Gaussian projection (Venkatasubramanian and Wang, 2011; Le et al., 2013; Dahiya et al., 2018). Theorem 3 helps to characterize situations where this phenomenon is expected to be observed.

Remark 1.

The same line of proof used in Theorem 3 can be used to show that the convergence probability of (2) using the Hadamard and Clarkson-Woodruff projections converges to that of the Gaussian sketch under Assumption 1. Theorem 2 also gives an asymptotic approximation for the Hadamard and Clarkson-Woodruff sketches.

It remains to establish a formal limit theorem in terms of the Tracy-Widom distribution for the Hadamard and Clarkson-Woodruff sketches. The proof of Theorem 3 treats and as fixed, with only being taken to infinity. It is possible that Assumption 1 on the leverage scores will remain sufficient in the expanding dimension scenario. For any , the maximum leverage score must be greater than the average leverage score,

If we maintain that Assumption 1 holds on the leverage scores as , this implies that . As we have assumed that our primary motivation for sketching is data compression when , we feel that analysis in the asymptotic regime is reasonable for this use-case setting. The asymptotic approximations developed here are recommended for applications of sketching in tall-data problems .

The key result is that the Hadamard and Clarkson-Woodruff sketches behave like the Gaussian projection for large , with and fixed. If the Tracy-Widom approximation in Theorem 1 is good for finite and with the Gaussian sketch, it should hold well for the Hadamard and Clarkson-Woodruff projections for sufficiently large.

4.2 Uniform sketch

It is considerably more difficult to approximate the embedding probability for the uniform sketch compared to the other data-oblivious projections. Vershynin (2010) provides a bound for the uniform sketch that is useful for comparative purposes.

Theorem 4 (Vershynin (2010), Theorem 5.1).

Consider an matrix such that . Let represent the -th row in for . Let give an upper bound on the leverage scores, so

Let be a uniform sketch of size . Then for every , with probability at least one has

Theorem 4 can be used to give a lower bound on the probability of obtaining an -subspace embedding. Both Theorem 4 and Theorem 3 involve the maximum leverage score. Holding and fixed, in order for the bound in Theorem 4 to remain controlled as the sample size increases, the maximum leverage score must decrease at a sufficient rate. In contrast, Assumption 1 does not enforce a rate of decay on the maximum leverage score, only that it eventually tends to zero as . This suggests that the uniform projection could be more sensitive to the maximum leverage score than the Gaussian, Hadamard and Clarkson-Woodruff projections. As mentioned earlier, it is very difficult to give a general expression for the embedding probability (3) when using the uniform sketch as it will be a complicated function of the source dataset . An advantage of the Gaussian, Hadamard and Clarkson-Woodruff projections is that a Tracy-Widom approximation can be motivated under mild regularity conditions.

5 Data application

5.1 -subspace embedding

We tested the theory on a large genetic dataset of European ancestry participants in UK Biobank. The covariate data consists of genotypes at genetic variants in the Protein Kinase C Epsilon (PKC) gene on subjects. Variants were filtered to have minor allele frequency of greater than one percent. The response variable was haemoglobin concentration adjusted for age, sex and technical covariates. The region was chosen as many associations with haemoglobin concentration were discovered in a genome-wide scan using univariable models; these associations were with variants with different allele frequencies, suggesting multiple distinct causal variants in the region. We also considered a subset of this dataset with representative markers identified by hierarchical clustering. When including the intercept and response, the PKC subset has , and the full PKC dataset has .

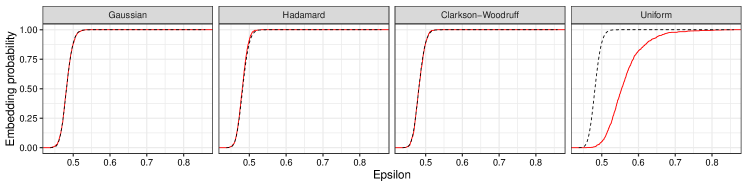

The full PKC dataset is of moderate size, so it was feasible to take the singular value decomposition of the full dataset . Given the singular value decomposition we ran an oracle procedure to estimate the exact embedding probability. We generated sketching matrices . These were used to compute for and give an estimated embedding probability as in (9). When working with the full PKC dataset we simulated directly from the matrix normal distribution for the Gaussian sketch, rather than computing the matrix multiplication . We took sketches of the PKC subset, and sketches of the full PKC dataset using the uniform, Gaussian, Hadamard and Clarkson-Woodruff projections, with .

Figure 2 shows the empirical and theoretical embedding probabilities for the PKC subset for each type of sketch. The observed and theoretical curves match well for the Gaussian, Hadamard and Clarkson-Woodruff projection. The uniform projection performs worse than the other data-oblivious random projections, as larger values of indicate weaker approximation bounds. The uniform projection does not satisfy a central limit theorem for fixed , so we do not necessarily expect the Tracy-Widom law to give a good approximation for the uniform projection.

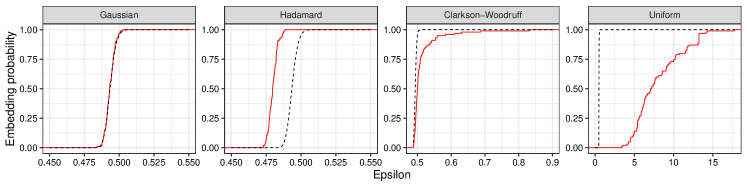

Figure 3 shows the empirical and theoretical embedding probabilities for the full PKC dataset for each type of sketch. The Tracy-Widom approximation is accurate for the Gaussian sketch, but there are some deviations for the Hadamard and the Clarkson-Woodruff sketch. Interestingly, the empirical cdf for the Hadamard sketch (red) is to the left of the theoretical value (black), indicating smaller values of than predicted. The distribution of has a longer right tail under the Clarkson-Woodruff sketch than is predicted by the Tracy-Widom law.

The deviation from the Tracy-Widom limit in Figure 3 could be because the finite sample approximation is poor. Theorem 3 suggests that the Hadamard and Clarkson-Woodruff projections behave like the Gaussian sketch for sufficiently large with respect to . To test this we bootstrapped the full PKC dataset to be ten times its original size. The bootstrapped PKC dataset has . We took one thousand sketches of size using the Clarkson-Woodruff projection and ran the oracle procedure of computing for each sketch. Figure 4 compares the distribution of using Clarkson-Woodruff projection on the original dataset and on the large bootstrapped dataset. As increases we expect the quality of the Tracy-Widom approximation to improve. Panel (a) of Figure 4 compares the theoretical to the simulation results on the original dataset. The Clarkson-Woodruff projection shows greater variance than expected. Panel (b) compares the theoretical to the simulation results on the bootstrapped dataset. In (b) there is very good agreement between the empirical distribution and the theoretical distribution. It seems that for this dataset is not big enough for the large sample asymptotics to kick in. At million the Tracy-Widom approximation is very good. As mentioned earlier, our motivation for using a sketching algorithm is to perform data compression with tall datasets . This example highlights that the asymptotic approximations become more accurate as the sample size grows while the computational incentives for using sketching increase in parallel.

| Projection | Subset | Full |

|---|---|---|

| Gaussian | 769 | - |

| Hadamard | 17.2 | 156 |

| Clarkson-Woodruff | 1.33 | 21 |

| Uniform | 0.03 | 2.8 |

5.2 Iterative optimisation

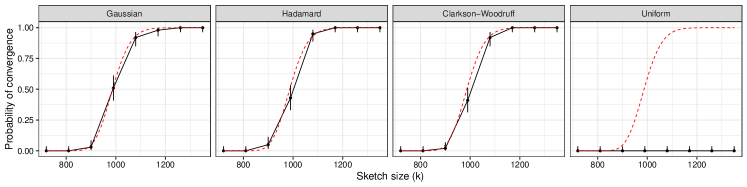

We considered iterative least-squares optimisation using the song year dataset available from the UCI machine learning repository. The dataset has observations, covariates, and year of song release as the response. We assessed the convergence probability by running the iteration (2) with the sketched preconditioner. The initial parameter estimate was a vector of zeros. The iteration was run for 2000 steps, with convergence being declared if the gradient norm condition was satisfied any time step . This convergence criterion was used instead of as will not be known in practice. This was repeated one hundred times for each of the random projections discussed in Section 2.1 using different sketch sizes . Figure 5 compares the empirical (black solid points) and theoretical convergence probabilities (dashed red line) against the sketch size . The point-ranges represent 95% confidence intervals. The Gaussian, Hadamard and Clarkson-Woodruff show near identical behavior, and the empirical convergence probabilities closely match the theoretical predictions using Theorem 2. The uniform sketch was much less successful in generating preconditioners, the algorithm did not show convergence in any replication at each sketch size . In this example, the additional computational cost of the Gaussian, Hadamard and Clarkson-Woodruff sketches compared to the Uniform subsampling has clear benefits.

6 Conclusion

The analysis of the asymptotic behavior of common data-oblivious random projections revealed an important connection to the Tracy-Widom law. The probability of attaining an -subspace embedding (Definition 1) is an integral descriptive measure for many sketching algorithms. The asymptotic embedding probability can approximated using the Tracy-Widom law for the Gaussian, Hadamard and Clarkson-Woodruff sketches. The Tracy-Widom law can also be used to estimate the convergence probability for iterative schemes with a sketched preconditioner. We have tested the predictions empirically and seen close agreement. The majority of existing results for sketching algorithms have been established using non-asymptotic tools. Asymptotic results are a useful complement that can provide answers to important questions that are difficult to address concretely in a finite dimensional framework.

There was a stark contrast between the performance of the basic uniform projection and the other data-oblivious projections (Gaussian, Hadamard and Clarkson-Woddruff) in the data application. The Hadmard and Clarkson-Woodruff projections are expected to behave like the Gaussian projection under mild regularity conditions on the maximum leverage score. We observed this phenomenon when was large, as is required by Theorem 3. The Hadamard and Clarkson-Woodruff projections are substantially more computationally efficient than the Gaussian projection (recall Table 1), so their universal limiting behavior implies that the trade-off between computation time and performance guarantees is asymptotically negligible in the regime (8).

The Tracy-Widom law has found many applications in high-dimensional statistics and probability (Edelman and Wang, 2013), and we have shown that it useful for describing the asymptotic behavior of sketching algorithms. The asymptotic behaviour with respect to large is of practical interest, as this is the regime where sketching is attractive as a data compression technique. The universal behavior of high-dimensional random matrices has practical and theoretical consequences for randomized algorithms that use linear dimension reduction (Dobriban and Liu, 2018; Lacotte et al., 2020).

References

- Ahfock et al. (2020) Ahfock, D.C., Astle, W.J., Richardson, S.: Statistical properties of sketching algorithms. Biometrika 108(2), 283–297 (2020)

- Ailon and Chazelle (2009) Ailon, N., Chazelle, B.: The fast Johnson Lindenstrauss transform and approximate nearest neighbors. SIAM Journal on Computing 39(1), 302–322 (2009)

- Bai and Silverstein (2010) Bai, Z., Silverstein, J.W.: Spectral Analysis of Large Dimensional Random Matrices. Springer, New York, 2nd ed. (2010)

- Bardenet and Maillard (2015) Bardenet, R., Maillard, O.A.: A note on replacing uniform subsampling by random projections in MCMC for linear regression of tall datasets. HAL preprint 01248841 (2015)

- Bhatia (1996) Bhatia, R.: Matrix Analysis. Springer (1996)

- Billingsley (1999) Billingsley, P.: Convergence of Probability Measures. Wiley Series in Probability and Statistics. Wiley, New York, 2nd ed. (1999)

- Chiani (2017) Chiani, M.: On the probability that all eigenvalues of Gaussian, Wishart, and double Wishart random matrices lie within an interval. IEEE Transactions on Information Theory 63(7), 4521–4531 (2017)

- Clarkson and Woodruff (2013) Clarkson, K.L., Woodruff, D.P.: Low rank approximation and regression in input sparsity time. In: Proceedings of the forty-fifth annual ACM symposium on Theory of Computing, pp. 81–90. ACM (2013)

- Cormode (2011) Cormode, G.: Sketch techniques for approximate query processing. Foundations and Trends in Databases (2011)

- Dahiya et al. (2018) Dahiya, Y., Konomis, D., Woodruff, D.P.: An empirical evaluation of sketching for numerical linear algebra. In: Proceedings of the 24th ACM SIGKDD International Conference on Knowledge Discovery & Data Mining, pp. 1292–1300. ACM (2018)

- Dobriban and Liu (2018) Dobriban, E., Liu, S.: A new theory for sketching in linear regression. arXiv preprint arXiv:1810.06089 (2018)

- Drineas et al. (2006) Drineas, P., Mahoney, M.W., Muthukrishnan, S.: Sampling algorithms for l2 regression and applications. In: Proceedings of the seventeenth annual ACM-SIAM symposium on Discrete algorithms, pp. 1127–1136. Society for Industrial and Applied Mathematics (2006)

- Edelman (1988) Edelman, A.: Eigenvalues and condition numbers of random matrices. SIAM Journal on Matrix Analysis and Applications 9(4), 543–560 (1988)

- Edelman and Wang (2013) Edelman, A., Wang, Y.: Random matrix theory and its innovative applications. In: Advances in Applied Mathematics, Modeling, and Computational Science, pp. 91–116. Springer (2013)

- Erichson et al. (2016) Erichson, N.B., Voronin, S., Brunton, S.L., Kutz, J.N.: Randomized Matrix Decompositions using R. arXiv preprint p. arXiv:1608.02148 (2016)

- Falcone et al. (2021) Falcone, R., Anderlucci, L., Montanari, A.: Matrix sketching for supervised classification with imbalanced classes. Data Mining and Knowledge Discovery pp. 1–35 (2021)

- Geman (1980) Geman, S.: A limit theorem for the norm of random matrices. The Annals of Probability 8(2), 252–261 (1980)

- Geppert et al. (2017) Geppert, L.N., Ickstadt, K., Munteanu, A., Quedenfeld, J., Sohler, C.: Random projections for Bayesian regression. Statistics and Computing 27(1), 79–101 (2017)

- Grellmann et al. (2016) Grellmann, C., Neumann, J., Bitzer, S., Kovacs, P., Tönjes, A., Westlye, L.T., Andreassen, O.A., Stumvoll, M., Villringer, A., Horstmann, A.: Random Projection for Fast and Efficient Multivariate Correlation Analysis of High-Dimensional Data: A New Approach. Frontiers in Genetics 7, 102 (2016)

- Hageman and Young (2012) Hageman, L., Young, D.: Applied Iterative Methods. Dover Books on Mathematics. Dover Publications (2012)

- Halko et al. (2011) Halko, N., Martinsson, P.G., Tropp, J.A.: Finding structure with randomness: Probabilistic algorithms for constructing approximate matrix decompositions. SIAM Review 53(2), 217–288 (2011)

- Johnstone (2001) Johnstone, I.M.: On the distribution of the largest eigenvalue in principal components analysis. Annals of Statistics pp. 295–327 (2001)

- Johnstone (2006) Johnstone, I.M.: High dimensional statistical inference and random matrices. arXiv preprint arXiv:0611589 (2006)

- Johnstone et al. (2014) Johnstone, I.M., Ma, Z., Perry, P.O., Shahram, M.: RMTstat: Distributions, Statistics and Tests derived from Random Matrix Theory (2014). R package version 0.3

- Lacotte et al. (2020) Lacotte, J., Liu, S., Dobriban, E., Pilanci, M.: Limiting spectrum of randomized Hadamard transform and optimal iterative sketching methods. arXiv preprint arXiv:2002.00864 (2020)

- Le et al. (2013) Le, Q., Sarlós, T., Smola, A.: Fastfood-computing hilbert space expansions in loglinear time. In: International Conference on Machine Learning, pp. 244–252 (2013)

- Lehoucq et al. (1998) Lehoucq, R.B., Sorensen, D.C., Yang, C.: ARPACK users’ guide: solution of large-scale eigenvalue problems with implicitly restarted Arnoldi methods, vol. 6. SIAM (1998)

- Li et al. (2006) Li, P., Hastie, T.J., Church, K.W.: Very sparse random projections. In: Proceedings of the 12th ACM SIGKDD international conference on Knowledge discovery and data mining, pp. 287–296. ACM (2006)

- Lopes et al. (2018) Lopes, M.E., Wang, S., Mahoney, M.W.: Error Estimation for Randomized Least-Squares Algorithms via the Bootstrap. arXiv preprint arXiv:1803.08021 (2018)

- Ma et al. (2015) Ma, P., Mahoney, M.W., Yu, B.: A statistical perspective on algorithmic leveraging. Journal of Machine Learning Research 16(1), 861–911 (2015)

- Ma (2012) Ma, Z.: Accuracy of the Tracy–Widom limits for the extreme eigenvalues in white Wishart matrices. Bernoulli 18(1), 322–359 (2012)

- Mahoney (2011) Mahoney, M.: Randomized algorithms for matrices and data. Foundations and Trends in Machine Learning 3(2), 123–224 (2011)

- Mahoney and Drineas (2016) Mahoney, M., Drineas, P.: Structural properties underlying high-quality Randomized Numerical Linear Algebra algorithms. In: Buhlmann, P., Drineas, P., Kane, M., van de Laan, M. (eds.) Handbook of Big Data, pp. 137–154. Chapman and Hall (2016)

- Meng (2014) Meng, X.: Randomized Algorithms for Large-scale Strongly Over-determined Linear Regression Problems. Ph.D. thesis, Stanford University, Stanford, California, United States (2014)

- Meng and Mahoney (2013) Meng, X., Mahoney, M.M.: Low-distortion Subspace Embeddings in Input-sparsity Time and Applications to Robust Linear Regression. In: Proceedings of the forty-fifth annual ACM symposium on Theory of computing, pp. 91–100. ACM (2013)

- Meng et al. (2014) Meng, X., Saunders, M.A., Mahoney, M.W.: Lsrn: A parallel iterative solver for strongly over-or underdetermined systems. SIAM Journal on Scientific Computing 36(2), C95–C118 (2014)

- Nelson and Nguyên (2013) Nelson, J., Nguyên, H.L.: Osnap: Faster numerical linear algebra algorithms via sparser subspace embeddings. In: 54th Annual IEEE Symposium on the Foundations of Computer Science, pp. 117–126. IEEE (2013)

- Pilanci and Wainwright (2016) Pilanci, M., Wainwright, M.J.: Iterative Hessian sketch: Fast and accurate solution approximation for constrained least-squares. Journal of Machine Learning Research 17(1), 1842–1879 (2016)

- Quiroz et al. (2018) Quiroz, M., Villani, M., Kohn, R., Tran, M.N., Dang, K.D.: Subsampling MCMC-an introduction for the survey statistician. Sankhya A 80(1), 33–69 (2018)

- Raskutti and Mahoney (2014) Raskutti, G., Mahoney, M.: A Statistical Perspective on Randomized Sketching for Ordinary Least-Squares. arXiv preprint arXiv:1406.5986 (2014)

- Roosta-Khorasani and Mahoney (2016) Roosta-Khorasani, F., Mahoney, M.W.: Sub-Sampled Newton Methods I: Globally Convergent Algorithms. arXiv preprint arXiv:1601.04737 (2016)

- Sarlos (2006) Sarlos, T.: Improved approximation algorithms for large matrices via random projections. In: 47th Annual IEEE Symposium on Foundations of Computer Science, pp. 143–152. IEEE (2006)

- Silverstein (1985) Silverstein, J.W.: The smallest eigenvalue of a large dimensional wishart matrix. The Annals of Probability 13(4), 1364–1368 (1985)

- Tracy and Widom (1994) Tracy, C.A., Widom, H.: Level-spacing distributions and the airy kernel. Communications in Mathematical Physics 159(1), 151–174 (1994)

- Tropp (2011) Tropp, J.A.: Improved analysis of the subsampled randomized Hadamard transform. Advances in Adaptive Data Analysis 3(01n02), 115–126 (2011)

- Van Der Vaart (1998) Van Der Vaart, A.: Asymptotic Statistics. Cambridge Series in Statistical and Probabilistic Mathematics, 3. Cambridge University Press (1998)

- Venkatasubramanian and Wang (2011) Venkatasubramanian, S., Wang, Q.: The Johnson-Lindenstrauss transform: an empirical study. In: 2011 Proceedings of the Thirteenth Workshop on Algorithm Engineering and Experiments, pp. 164–173. SIAM (2011)

- Vershynin (2010) Vershynin, R.: Introduction to the non-asymptotic analysis of random matrices. arXiv preprint arXiv:1011.3027 (2010)

- Woodruff (2014) Woodruff, D.P.: Sketching as a tool for numerical linear algebra. Foundations and Trends in Theoretical Computer Science 10(1-2), 1–157 (2014)

- Yang et al. (2015) Yang, J., Meng, X., Mahoney, M.W.: Implementing randomized matrix algorithms in parallel and distributed environments. arXiv preprint arXiv:1502.03032 (2015)

Supplementary Material

S1.1 Weak convergence

Our asymptotic arguments concern the convergence of sequences of probability measures. Billingsley (1999) is an authoritative reference on the topic. We now recap some useful foundational theory, as is presented in Van Der Vaart (1998, Chapter 2). The Portmanteau lemma gives a number of useful equivalent definitions of convergence in distribution (weak convergence).

Lemma S.1 (Portmanteau).

Let denote a sequence of random vectors of fixed dimension, and denote another random vector of the same dimension. The following statements are equivalent, where limits are being taken in :

-

(a)

at all continuity points of the cumulative distribution function .

-

(b)

for all Borel sets with , where denotes the boundary of the set . The boundary is defined as the closure of the set minus the interior of , so .

Lemma S.2 (Uniform convergence).

Suppose that converges in distribution to a random vector with a continuous distribution function. Then

Proofs for these results are given in Chapter 2 of Van Der Vaart (1998).

S1.2 Random Matrix Theory

Definition S.2.

A random variable has a Tracy-Widom distribution , when the cumulative distribution function is given by

Where satisfies the nonlinear differential equation , subject to the asymptotic boundary condition, . The function denotes the Airy function, defined as .

Theorem S.5.

(Ma, 2012)

Consider a sequence of random matrices where and with . Let denote the maximum eigenvalue of the random matrix. Define the centering and scaling constants as

Then with and is the Tracy-Widom distribution.

A limit theorem for the minimum eigenvalue is best expressed in terms of the logarithm of the minimum eigenvalue as this gives higher order accuracy (Ma, 2012).

Theorem S.6.

(Ma, 2012)

Consider a sequence of random matrices where and with . Let denote the minimum eigenvalue of the random matrix. Set

and define the following centering and scaling constants . Then where and is the Tracy-Widom distribution,

S1.3 Proof of Theorem 1

Proof.

The extreme eigenvalues of a Wishart random matrix converge in probability to fixed values as both the dimension and degrees of freedom expand. The result for the largest eigenvalue is due to Geman (1980) and the result for the smallest eigenvalue is due to Silverstein (1985).

Theorem S.7.

(Geman, 1980; Silverstein, 1985)

Consider a sequence of random matrices where the degrees of freedom and dimension are both taken to infinity. Suppose that the variables to samples ratio converges to a constant , where . Then the extreme eigenvalues of the random matrix, and converge in probability to the limits

| (S.10) | |||

| (S.11) |

Theorem S.7 and the continuous mapping theorem can be used to determine the asymptotic embedding probability for the Gaussian sketch.

Lemma S.3.

Suppose we have an arbitrary data matrix where and is of rank . Assume we take a Gaussian sketch of size . Then asymptotically in and , with where ,

Proof.

Let , and let and denote the minimum and maximum eigenvalues of respectively. Using Slutsky’s theorem and the continuous mapping theorem we have the joint convergence result

| (S.12) |

where the equality uses the fact that . For large and , the maximum eigenvalue is expected to show greater deviation from one than the minimum eigenvalue . Over the interval it holds that

Applying the continuous mapping theorem to the random vector in (S.12),

yields . Now as is greater than one for all , the absolute value sign can be removed in the limit giving the equivalent statement . Recalling that , we establish convergence of the limiting singular value

| (S.13) |

As convergence in probability to a constant implies convergence in distribution, the Portmanteau lemma then gives the probabilistic statement

As is a discontinuity point of the limiting distribution function we do not make a statement about the case . We have the equality in limits

giving the final result. ∎

Given Lemma S.3, we can move on to the proof of Theorem 1. Let , and let and denote the minimum and maximum eigenvalues of respectively. The majority of the proof comes down to showing that controls the embedding probability. Using the Portmanteau lemma (Lemma S.1) we will show that

Recall the key expression

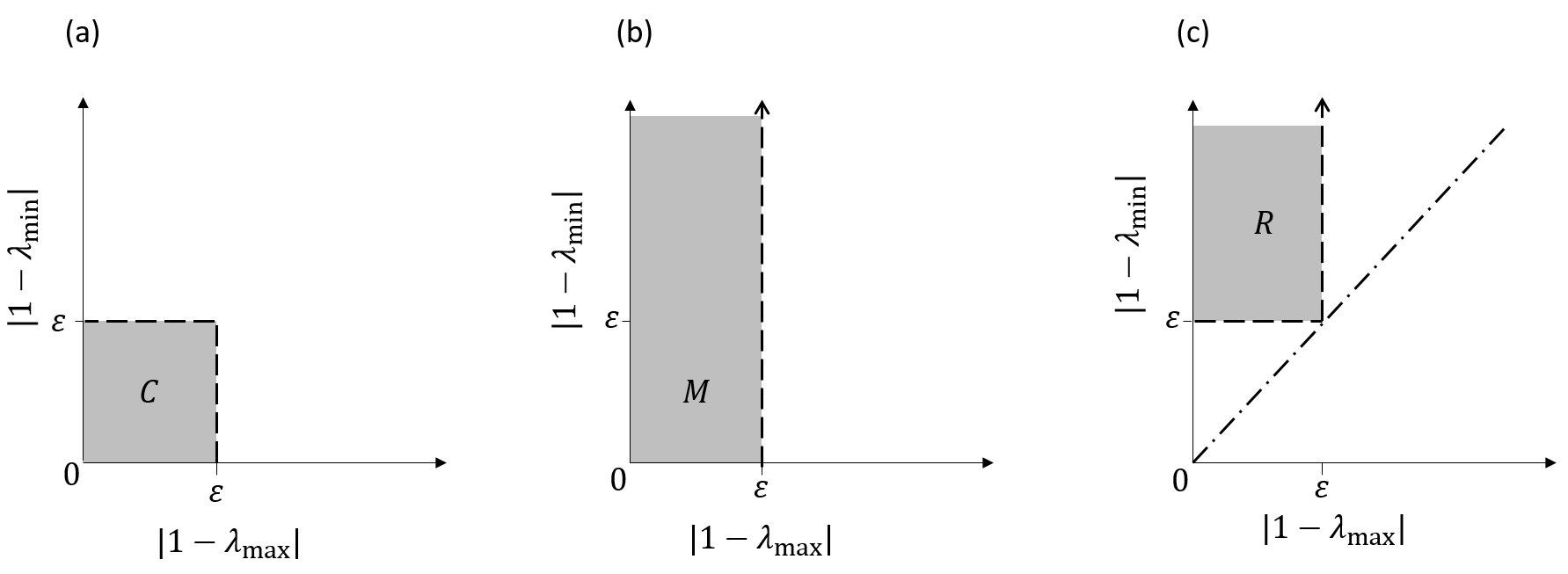

The Tracy-Widom law describes the marginal distributions of and . We would like to avoid working with the joint distribution of the extreme eigenvalues, and instead restrict attention to the distribution of the maximum. Let denote the random vector . Figure S6 presents some diagrams that will be useful. We wish to know the probability that lies in the shaded region in panel (a). For every we have that . The region can be expressed as where and are the shaded regions in panels (b) and (c) respectively. The probability represents the marginal probability that . The probability represents the probability of the joint event that . We have that

In panel (c) the dot-dash line gives the identity line where . From the first part of the proof of Lemma S.3 we know that as tends to infinity converges in distribution to the constant vector . As such, asymptotically with probability one. Referring to panel , the random vector takes values in the region below the dot-dash line with probability one. The limiting random vector thus satisfies and . As , Property (b) of the Portmanteau lemma (Lemma S.1) gives that . The limiting probability is then

| (S.14) |

We have now isolated the maximum eigenvalue as the determining factor in obtaining an -subspace embedding. We make another application of the Portmanteau lemma to arrive at the final result. From here we can write

| (S.15) |

From Theorem S.7 we know that converges in distribution to the constant random variable , where we have assumed . Let denote the interval . The limiting random variable satisfies and . As such using property b of the Portmanteau lemma, . Now for any . We can then conclude that for any . Asymptotically, the term drops out of the expression for the embedding probability. Taking limits over (S.15),

The asymptotic embedding probability is then related to the asymptotic distribution of . The inequality can be manipulated to include the centering and scaling constants that appear in Theorem S.5,

Let be a random variable with Tracy-Widom distribution . Now using Theorem S.5 in the main text we have that for any fixed and , it must hold that for any fixed ,

| (S.16) | ||||

As converges in distribution to the continuous random variable , where , it follows from Lemma S.2 that

Now by the squeeze theorem, it holds that for all ,

From Theorem 1 of Ma (2012), the error in the approximation (S.16) is for even . As discussed in Ma (2012), it is difficult to give a rigorous error bound for odd , however simulations suggest the bound still holds. ∎

S1.4 Proof of Theorem 2

Proof.

Let and let denote the minimum eigenvalue of . The probability of convergence can be expressed as

| (S.17) |

Let be a random variable with Tracy-Widom distribution . Now from Theorem S.6, converges in distribution to the continuous random variable , where is distributed according to the Tracy-Widom distribution . For any fixed and , it must hold that for any fixed ,

| (S.18) | ||||

| (S.19) | ||||

From Lemma S.2 it must hold that

Now by the squeeze theorem, for all ,

Rearranging

and using the identity (S.17) gives the the final result,

∎

S1.5 Proof of Theorem 3

Proof.

Assumption 1 on the leverage scores is sufficient to establish a central limit theorem for the data-oblivious sketches.

Theorem S.8 (Ahfock et al. (2020)).

Consider a sequence of arbitrary data matrices , where is fixed. Let

represent the singular value decomposition of . Let be a Hadamard or Clarkson-Woodruff sketching matrix where is also fixed. Suppose that Assumption 1 on the maximum leverage score is satisfied. Then as tends to infinity

As we only need to consider the sequence of orthonormal matrices to determine the embedding probability, we can use Theorem S.8 with and set to the identity matrix. As such we conclude that . By the continuous mapping theorem it holds that for fixed and , asymptotically with , . Another application of the continuous mapping theorem gives

where . We can use the continuous mapping theorem as the limiting Wishart matrix has rank with probability one. The maximum singular value function is continuous over the range where has full rank (Bhatia, 1996). By the Portmanteau lemma it then holds that

Now as

we have the final result. ∎