Compensatory model for quantile estimation and application to VaR

Abstract

In contrast to the usual procedure of estimating the distribution of a time series and then obtaining the quantile from the distribution, we develop a compensatory model to improve the quantile estimation under a given distribution estimation. A novel penalty term is introduced in the compensatory model. We prove that the penalty term can control the convergence error of the quantile estimation of a given time series, and obtain an adaptive adjusted quantile estimation. Simulation and empirical analysis indicate that the compensatory model can significantly improve the performance of the value at risk (VaR) under a given distribution estimation.

KEYWORDS: Quantile estimation; VaR; Normal distribution

1 Introduction

For a given time series, the mean, variance, and quantiles are important statistics. In particular, different quantiles can capture different characteristics of the time series. Traditional statistical methods include estimating the distribution behind the time series and using the distribution estimation to calculate the quantile of the time series, that is, the normal distribution, empirical distribution, distribution, or filtered distribution based on regression models.

There are many related works on quantile estimation. Based on a maximum transformation in a two-way layout of the data, Heidelberger and Lewis (1984) proposed a practical scheme to reduce the sample size sufficiently to allow an experimenter to obtain a point estimate of an extreme quantile. Through a combination of extreme or intermediate order statistics, Dekkers and De Hana (1989) investigated a large quantile estimation of a distribution that leads to an asymptotic confidence interval. Francisco and Fuller (1991) considered the estimation of the finite population distribution function, the median, and interquartile range. By solving a simple quadratic programming problem and providing uniform convergence statements, Takeuchi et al. (2006) presented a nonparametric version of a quantile estimator. Mease et al. (2007) studied off-the-shelf boosting for classification at quantiles other than 1/2 and estimation of the conditional class probability function. Further relevant research was conducted by Hosking and Wallis (1987); Koenker and Zhao (1996).

An important application of the quantile is through the value at risk (VaR) that is used to calculate the downside risk of risky assets. VaR was proposed by J.P. Morgan in the 1990s and has become a popular tool to measure downside risk in financial markets. In the Basel Accords I, II, and III, VaR was suggested for measuring the risk of the banking industry, and the countries chose rationality methods to calculate VaR. Duffie and Pan (1997) establish the basic econometric modeling required to estimate VaR, which includes jump diffusions and stochastic volatility.

Many studies have been conduced that evaluate and discuss different models and distribution settings for studying VaR. The reader should refer to the reviews conducted by Kuester et al. (2006), Jorion (2010), Abad et al. (2014), and Zhang and Nadarajah (2017), among others. Using the daily NASDAQ Composite Index, Kuester et al. (2006) concluded an extensive empirical comparison of most models to calculate VaR in terms of their predictive power. By filtering residuals with an autoregressive-generalized autoregressive conditional heteroscedasticity (AR-GARCH) model instead of the original series, the general conclusion of Kuester et al. (2006) is that whatever method is used for VaR modeling, the predictions are always improved. Based on the NASDAQ Composite Index, Kuester et al. (2006) showed that ”conditionally heteroskedastic models yield acceptable forecasts” and that the conditional skewed- (AR-GARCH-St) together with the conditional skewed- coupled with EVT (AR-GARCH-St-EVT) perform best in general. The seminal autoregressive conditional heteroscedastic (ARCH) processes were established in Engle (1982) and Bollerslev (1986). Based on an autoregressive process and estimating the parameters with regression quantiles, Engle and Manganelli (2004) proposed a conditional autoregressive value at risk (CAViaR) model, which has become a very popular time varying quantile model. De Rossi and Harvey (2006, 2009) showed how to fit time-varying quantiles by setting up a state space model and iteratively applying a suitably modified signal extraction algorithm, and determined the conditions under which such quantiles will satisfy the defining property of fixed quantiles in having the appropriate number of observations above and below. Recently, Chen et al. (2019) proposed a new risk measure termed mark to market VaR for settlement being taken daily during the holding period. The usefulness of the asymmetric power GARCH models for VaR was illustrated by simulation results and real data analysis in Wang et al. (2020). Furthermore, there are many related work on portfolios selection under constraints of VaR, such as Zhu et al. (2016); Yiu et al. (2010).

Mean and volatility are two important characteristics of a time series. Many related works have examined the theory and application of mean and volatility uncertainty, such as Avellaneda et al. (1995); Peng (1997); Chen and Epstein (2002); Peng (2004, 2005); Cont (2006); Kerkhof et al. (2010); Epstein and Ji (2013); Peng (2019). The notion of upper expectation was first discussed by Huber (1981) in robust statistics, (see also Walley (1991)), and a systematic nonlinear expectation was established in Peng (2019). Peng et al. (2020); Peng and Yang (2021) introduced a new VaR calculation model, the G-VaR model, and compared it with some distributions under GARCH models to show the performances of the G-VaR model. Recently, Trucíos and Taylor (2020) revisited the procedures of extreme observations, multi-regime, and standard methods in terms of volatility and VaR forecasting. Furthermore, recent cryptocurrency data was evaluated by VaR forecasting performance. Extreme observations and regime changes are two characteristics of cryptocurrency markets, that distinguish them from stock markets and bond markets. See Trucíos (2019); Maciel (2020); Alexander and Dakos (2020); Ardia et al. (2019) and the references therein.

In the present paper, we want to construct a compensatory model that is used to improve the quantile estimation of a given distribution estimation. From the distribution estimation, we can obtain a quantile estimation that minimizes the check function error, such as empirical distribution. However, the convergence error of the counting function still needs to be reduced. Thus, in the compensatory model, we focus on the convergence error of the counting function to improve the quantile estimator of the distribution estimation. Let denote a time series, and assume that satisfies the distribution . Based on historical data, we can obtain a distribution estimation for . For a given quantile level , we can define a counting function that takes when , and takes for other cases, where is the quantile of the estimation function . Thus, when converges to as , we can say that is a ”good” quantile estimation for , where . When we conduct simulation and empirical analysis, we find that it is difficult to obtain a better quantile estimation based on a distribution estimation for , see Figures 1 and 2 with parameter .

To improve the performance of , we introduce a penalty term in the definition of the counting function , which takes when , and takes for other cases, where denotes the control ability of the penalty term . We call the adjusted quantile estimation of . In theory, we prove that for bounded time series with boundary . For the unbounded time series , we take the adjusted quantile estimation as and prove that , where is the uniformly quantile boundary of the time series . We then consider the application of the adjusted quantile estimation for VaR. Based on simulation and empirical analysis, we show that the compensatory model can improve the performance of VaR under a given distribution.

The main contributions of this study are the following:

(i) A new compensatory model is introduced, in which we add a penalty term in the definition of the counting function. The penalty term can deduce the distance between the cumulative sum of the counting function and quantile level.

(ii) Based on the penalty term, an adjusted quantile estimation is constructed and used to regenerate the quantile of a given distribution estimation.

(iii) The simulation and empirical analysis indicate that the adjusted quantile estimation can significantly improve the performance of the quantile of a given distribution estimation.

(iv) The compensatory model is utilized to improve the accuracy of the quantile estimation, and can be easily embedded into the method of quantile estimation based on a distribution estimation.

This paper is organized as follows: In Section 2, two kinds of counting functions are constructed for bounded and unbounded time series. For the bounded time series, we prove that the cumulative sum of the counting functions converges to the interval , . For the unbounded time series, we show that the cumulative sum of the counting functions converges to in probability . In Section 3, we use the compensatory model developed in Section 2 to analyze the benchmark S&P500 Index dataset, and predict VaR by the adjusted quantile estimation. We conclude this study in Section 4.

2 Compensatory Model for Quantile Estimation

For a given sequence , is a random variable on probability space , and is the expectation under probability . Here, can be used to present the return rate of risky assets, or a sample of statistical population. Note that the quantile of a sample is an important statistic that is used to describe the characteristic of the sample. An application of the quantile is to measure the risk of a risky asset. In the following, we introduce the compensatory model for the quantile estimation of the bounded and unbounded time series.

2.1 Bounded time series case

Let the distribution estimation of be , the true distribution of be , . For a given , let be the quantile of the distribution . Based on the historical information , we can obtain and , which minimizes the check function

When the counting function converges to in probability as , then we can say that the is a good quantile estimation of sequence . However, is always far away from . Thus, we add a penalty term in the quantile estimation , and denote it as

| (2.1) |

where

the counting function

| (2.2) |

and

| (2.3) |

Remark 2.1.

Let in (2.1) and be a distribution estimation of . Thus, is the estimator of the quantile of under distribution estimation . Furthermore, when be an independent sequence, the weak law of large numbers indicates that, for any given ,

which indicates that we can use to estimate the quantile of when converges to as .

In general, may not be an independent sequence, and does not converge to as . Thus, we introduce a penalty term in the quantile estimation , which is used to reduce the distance between and . Note that means that the value of quantile estimation is too high; thus we subtract the term in the adjusted quantile , where is used to control the distance between and , as well as for the case . Further details of are given in Remark 2.2.

The main results of this study are the following. We first give the following assumptions for the time series .

Assumption 2.1.

Let be an given sequence and let there exists a positive constant such that

Assumption 2.2.

Proof: For a given , we assume that there exists an integer such that

and thus

From Assumption 2.2, we have

From Assumption 2.1 and the definition of in (2.2), it follows that,

Note that, if

Similar to the above step, we can obtain that . Furthermore, when

we have

decreases with and converges to as . Thus, there exists such that

| (2.5) |

Next, we calculate the distance between and

| (2.6) |

From , we have

Combining inequality (2.5), it follows that

However, if

we can repeat the above process. Thus, we have for ,

Similarly, we can prove that there exists such that when ,

Thus, for , we have

which completes the proof. .

Remark 2.2.

For a given and , Theorem 2.1 shows that the error can be controlled by the term . Thus, the large values of and can reduce the error . For the sequence , based on the distribution estimation , the quantile of is . Theorem 2.1 indicates that we can use to take place , and we consider is the adjustment term of the quantile of . Thus, the term not only can control the convergence error of , but can also help to construct an adaptive quantile estimation .

However, in practice, a large may produce a large check function error. The reason for this is that the rate of the convergence error is . In particular, when , the value may be far away from and lead to a large check function error. To avoid this error, we take

| (2.7) |

where is the total number of time series. In Section 3, we will use the adjusted quantile

to conduct the empirical analysis.

Remark 2.3.

In practice, we only need to consider the bounded time series . Indeed, we can find a constant such that for the given data in the market. However, we establish the related results for the unbounded time series case in the following.

2.2 Unbounded time series case

Now, we consider the case of the unbounded time series and first give the basic assumption.

Assumption 2.3.

For a given quantile level , let be an given sequence, and let there exists a positive constant such that

where is the distribution estimation, is the true distribution of , and is the boundary of quantile of .

We introduce the following adjusted quantile:

| (2.8) |

and the counting function, ,

| (2.9) |

where ,

The difference between in in (2.9) and in (2.2) is that we use the expectation term to take the place of in the definition of .

Similar to the results of Theorem 2.1, we have the following inequality for .

Lemma 2.1.

Let Assumption 2.3 hold. Then, there exists an integer , such that when ,

| (2.10) |

Proof: The proof of this result is similar to that presented in Theorem 2.1. For the reader’s convenience, we present the details here. We assume that there exists an integer such that

From Assumption 2.3,

we can obtain that

Again, from Assumption 2.3 and the definition of in (2.9), it follows that, .

Thus, if

We have . Thus, when

it follows that

decreases with and there exists such that . Thus, there exist such that

| (2.11) |

Next, we calculate the distance between and

| (2.12) |

Note that , we have

From combining inequality (2.11), it follows that

Thus, we have for ,

Similarly, we can prove that there exists such that when ,

Thus, for , we have

which completes the proof. .

Furthermore, we can obtain the weak law of large numbers for sequence .

Lemma 2.2.

We assume that the sequence is uncorrelated. Then, we have for any given ,

| (2.13) |

Proof: Based on the sequence is uncorrelated, we can verify that is a uncorrelated sequence with bounded variance. Then, by Chebyshev’s law of large numbers, we can obtain (2.13).

Theorem 2.2.

Let Assumption 2.3 hold, and we assume that the sequence is uncorrelated. Then, it follows that for any given ,

| (2.14) |

Proof: For any given , Lemma 2.2 shows that

| (2.15) |

From Lemma 2.1, we have concluded that there exists , such that when ,

| (2.16) |

Note that

which deduces that

Thus,

For the arbitrary values of , we complete this proof.

Remark 2.4.

In Theorem 2.2, we show that converges to the interval in probability as , which indicates that there is mean uncertainty of . Furthermore, when taking as a function of and it converges to as , we can show that, for any given ,

Thus, converges to in probability as .

3 Simulation and Empirical Analysis

We now show how to use the compensatory model of Section 2 to estimate the VaR of a risky asset :

(i). For a given risk level and the length of historical data , we first use the data to obtain the distribution estimation of . We can choose the normal distribution, empirical distribution, or distribution as the types of distribution estimation.

(ii). The VaR of under the distribution estimation is given as follows:

which is equal to .

(iii). The adjusted VaR is given as follows:

The counting function is

| (3.1) |

where

and . Here, is the length of historical data that is used to estimate the distribution .

(iv). By equation (2.7) in Remark 2.2, we choose the parameter that satisfies , where is the boundary of sequence . For the given , we repeat steps (i), (ii), (iii), and obtain the adjusted VaR .

To assess the predictive performance of the model, we use the test of the likelihood ratio for a Bernoulli trial and the Christoffersen independence test to verify it. The count numbers of the violations of until time are as follows:

where is the length of historical data and the data are used to estimate the distribution of , that is, ; denotes the count numbers that satisfy the violation conditions. Denoting

and thus

Denoting the likelihood ratio test statistics,

and the Christoffersen independence test statistics,

Applying the well-known asymptotic distribution, the -value of the test is,

| (3.2) |

and independent test of violations point,

| (3.3) |

3.1 Simulation

We assume that satisfies the normal distribution with mean and variance . In the following, we use a different distribution estimation to verify the effect of the compensatory model (2.2).

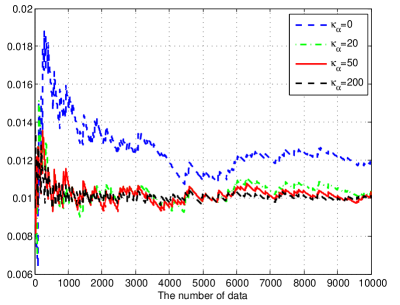

We first determine the value of . By equation (2.7) in Remark 2.2, we obtain that . In Figure 1, we use the normal distribution to approximate and to adjust VaR of , when , is the violation rate of under distribution and the performance of is poor. On the contrary, we can see that the adjustment VaR

performs better with the large value , which coincides with the results of Theorem 2.1.

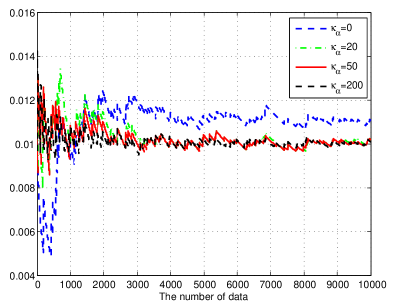

In Figure 2, we use the empirical distribution to approximate , and to adjust VaR of . Similar to the performance of the adjusted VaR in Figure 1, the left and right pictures of Figure 2 indicate that the adjustment VaR performs better with a large value , which verifies the results of Theorem 2.1.

Remark 3.1.

Figure 1 and Figure 2 indicate that we can use the adjusted term to adjust different distributions estimation, that is, the normal distribution and empirical distribution, such that the adjusted VaR has better performance. Furthermore, we can show that the performance of does not depend on the length of historical data .

3.2 Empirical Analysis

Next, we consider the S&P500 stock Index111This dataset was downloaded from https://finance.yahoo.com/lookup.. We denote the log-returns daily data of S&P500 Index as the sequence , which is taken from Mar. 22, 2017 to Dec. 31, 2019, with a total of daily data values.

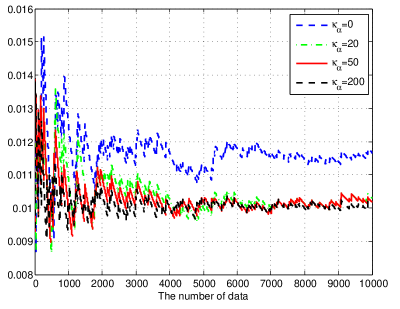

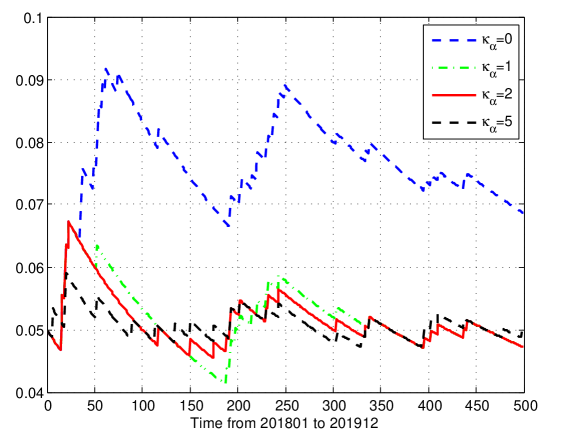

By equation (2.7) in Remark 2.2, we obtain that . In Figure 3, we use the normal distribution to approximate the true distribution of log return of the S&P500 Index at time . We can see that the adjusted VaR performs better with the largest value , which coincides with the results of Theorem 2.1. The value of is stable and nearly at the risk level . Details regarding the testing of are presented in Table 1.

| Model | Time | |||||

|---|---|---|---|---|---|---|

| : | 201801-201912 | 0 | 0.0687 | 0.0125 | 0.0012 | 1.43 |

| 201801-201912 | 1 | 0.0472 | 0.6850 | 0.0994 | 1.62 | |

| 201801-201912 | 2 | 0.0472 | 0.6850 | 0.0994 | 1.72 | |

| 201801-201912 | 5 | 0.0501 | 0.9918 | 0.5157 | 1.84 |

In Table 1, we show at end time , the -value test , the independent test of violations point , and 100 time average values of adjusted VaR under four kinds of values of . When , we can see that the values of testing and are nearly , which indicates that the model (2.2) can significantly improve the performance of VaR under the distribution estimation . However, the value of increases with .

| Model | Time | |||||

|---|---|---|---|---|---|---|

| : | 201801-201912 | 0 | 0.0300 | 0.0000 | 0.0324 | 2.04 |

| 201801-201912 | 1 | 0.0143 | 0.2131 | 0.1094 | 2.83 | |

| 201801-201912 | 2 | 0.0114 | 0.6596 | 0.0542 | 3.20 | |

| 201801-201912 | 5 | 0.0100 | 0.9964 | 1.0000 | 3.12 |

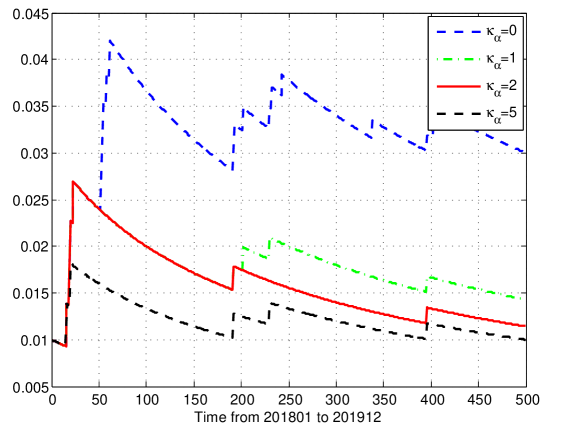

In Table 2, we show at end time , the -value test , the independent test of violations point , and 100 time average value of adjustment VaR under four kinds of values of . When , we can see that the values of testing is improved to comparing to , which indicates that the model (2.2) can significantly improve the performance of VaR under the distribution estimation with different risk levels .

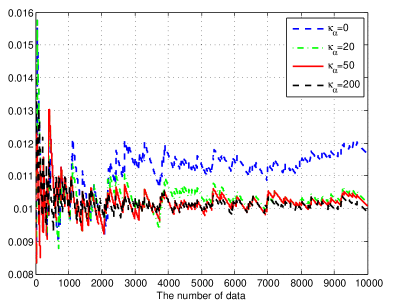

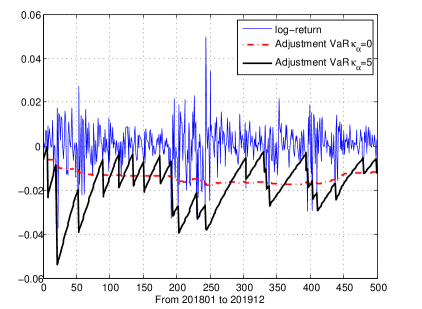

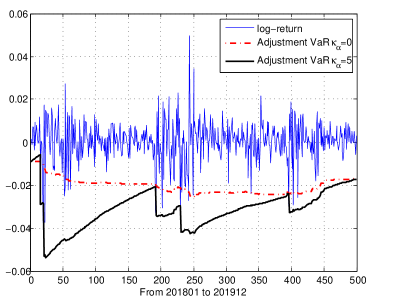

In Figure 5, the left picture indicates that the adjusted VaR with can capture the local changes of the log return of S&P500 for compared with VaR under the normal distribution with . A similar process can be seen in the right image with .

In this section, we show the performances of the adjusted VaR with risk value and under normal distribution estimation . We can see that can improve the performances of VaR under distribution at least for the log return of the Index S&P500. Furthermore, we also use the NASDAQ Index and the CSI300 Index to check the adjusted VaR under the normal and empirical distributions with different values of . In general, we find that can obtain excellent performance with an adaptive .

4 Conclusion

This study developed a compensatory model to improve the quantile estimation of time series under given distribution estimation . Traditional statistical methods include estimating the distribution behind the time series. By introducing a penalty term in the definition of the counting function, this study employs the method of adjusting the quantile of distribution estimation . There is a control ability factor in the penalty term, that is used to control the distance between the cumulative sum of the counting function and quantile level . Thus, the penalty term can adjust and improve the performance of the quantile of . Through simulation and empirical analysis, we showed that the compensatory model can significantly improve the performance of VaR under a given distribution. In particular, the compensatory model is not dependent on the value of quantile level and the length of historical data .

We would like to note that the method developed in this study is not used to estimate the true distribution behind the time series, but to improve the performance of a general distribution estimation. Using the compensatory model presented in this study, we have calculated the adjustment quantile for the S&P500 Index, the NASDAQ Index, and the CSI300 Index under quantile level , which verifies the usefulness of the compensatory model. Therefore, this compensatory model could be used to conduct data analysis for stock markets, bond markets, and cryptocurrency markets.

References

- Abad et al. (2014) P. Abad, S. Benito, and C. López. A comprehensive review of Value at Risk methodologies. The Spanish Review of Financial Economics, 12:1:15–32, 2014.

- Alexander and Dakos (2020) C. Alexander and M. Dakos. A critical investigation of cryptocurrency data and analysis. Quantitative Finance, 20(2):173–188, 2020.

- Ardia et al. (2019) D. Ardia, K. Bluteau, and M. Rüede. Regime changes in Bitcoin GARCH volatility dynamics. Finance Research Letters, 29:266–271, 2019.

- Avellaneda et al. (1995) M. Avellaneda, A. Levy, and A. Parás. Pricing and hedging derivative securities in markets with uncertain volatilities. Applied Mathematical Finance, 2:73–88, 1995.

- Bollerslev (1986) T. Bollerslev. Generalized autoregressive conditional heteroskedasticity. Journal of Econometrics, 31:307–327, 1986.

- Chen et al. (2019) Y. Chen, Z. Wang, and Z. Zhang. Mark to market value at risk. Journal of Econometrics, 208:1:299–321, 2019.

- Chen and Epstein (2002) Z. Chen and L. Epstein. Ambiguity, risk, and asset returns in continuous time. Econometrica, 70(4):1403–1443, 2002.

- Cont (2006) R. Cont. Model uncertainty and its impact on the pricing of derivative instruments. Mathematical Finance, 16:519–547, 2006.

- De Rossi and Harvey (2006) G. De Rossi and A.C. Harvey. Time-varying quantiles. Faculty of Economics, Cambridge:CWPE 0649, 2006.

- De Rossi and Harvey (2009) G. De Rossi and A.C. Harvey. Quantiles, expectiles and splines. Journal of Econometrics, 152:179–185, 2009.

- Dekkers and De Hana (1989) A. L. M. Dekkers and L. De Hana. On the estimation of the extreme-value index and large quantile estimation. The Annals of Statistics, 17(4):1795–1832, 1989.

- Duffie and Pan (1997) D. Duffie and J. Pan. An overview of value at risk. Journal of Derivatives, 4:7–49, 1997.

- Engle (1982) Robert F. Engle. Autoregressive Conditional Heteroskedasticity with Estimates of the Variance of United Kingdom Inflation. Econometrica, 50(4):987–1007, 1982.

- Engle and Manganelli (2004) Robert F. Engle and S. Manganelli. CAViaR: Conditional autoregressive value at risk by regression quantiles. Journal of Business & Economic Statistics, 22:4:367–381, 2004.

- Epstein and Ji (2013) L. G. Epstein and S. Ji. Ambiguous volatility and asset pricing in continuous time. Review of Financial Studies, 26(7):1740–1786, 2013.

- Francisco and Fuller (1991) C. A. Francisco and W. A. Fuller. Quantile estimation with a complex survey design. The Annals of Statistics, 19(1):454–469, 1991.

- Heidelberger and Lewis (1984) P. Heidelberger and P. A. W. Lewis. Quantile estimation in dependent sequences. Operations Research, 32(1):185–209, 1984.

- Hosking and Wallis (1987) J. R.M. Hosking and J. R. Wallis. Parameter and quantile estimation for the generalized pareto distribution. Technometrics, 29(3):339–349, 1987.

- Huber (1981) P. J. Huber. Robust Statistics. Wiley Series in Probability and Mathematical Statistics. John Wiley & Sons, Inc., New York, 3rd edition, 1981.

- Jorion (2010) Ph. Jorion. Risk management. Annual Review of Financial Economics, 2(1):347–365, 2010.

- Kerkhof et al. (2010) J. Kerkhof, B. Melenberg, and H. Schumacher. Model risk and capital reserves. Journal of Banking & Finance, 34:267–279, 2010.

- Koenker and Zhao (1996) R. Koenker and Q. Zhao. Conditional quantile estimation and inference for Arch models. Econometric Theory, 12(5):793–813, 1996.

- Kuester et al. (2006) K. Kuester, S. Mittnik, and M. S. Paolella. Value-at-Risk Prediction: A comparison of alternative strategies. Journal of Financial Econometrics, 4(1):53–89, 2006.

- Maciel (2020) L. Maciel. Cryptocurrencies value-at-risk and expected shortfall: Do regimeswitching volatility models improve forecasting. International Journal of Finance & Economics, pages 1–16, 2020.

- Mease et al. (2007) D. Mease, A. J. Wyner, and A. Buja. Boosted classification trees and class probability quantile estimation. Journal of Machine Learning Research, 8(16):409–439, 2007.

- Peng (1997) S. Peng. Backward SDE and related g-expectation. Backward stochastic differential equations (Paris, 1995-1996) 141-159. Pitman Res. Notes Math. Ser., Longman, Harlow, 1997.

- Peng (2004) S. Peng. Filtration consistent nonlinear expectations and evaluations of contingent claims. Acta Mathematicae Applicatae Sinica, 20:1–24, 2004.

- Peng (2005) S. Peng. Nonlinear expectations and nonlinear Markov chains. Acta Mathematicae Applicatae Sinica, 26B:159–184, 2005.

- Peng (2019) S. Peng. Nonlinear Expectations and Stochastic Calculus under Uncertainty, pages 1–212. Springer, Berlin, Heidelberg, 2019.

- Peng and Yang (2021) S. Peng and S. Yang. Distributional uncertainty of the financial time series measured by g-expectation. Theory of Probability and Its Applications, 66(4):914–928, 2021.

- Peng et al. (2020) S. Peng, S. Yang, and J. Yao. Improving value-at-risk prediction under model uncertainty. Journal of Financial Econometrics, doi:10.1093/jjfinec/nbaa022:1–30, 2020.

- Takeuchi et al. (2006) I. Takeuchi, Q. V. Le, T. D. Sears, and A. J. Smola. Nonparametric quantile estimation. Journal of Machine Learning Research, 7(45):1231–1264, 2006.

- Trucíos (2019) C. Trucíos. Forecasting Bitcoin risk measures: A robust approach. International Journal of Forecasting, 35(3):836–847, 2019.

- Trucíos and Taylor (2020) C. Trucíos and James W. Taylor. Forecasting Value-at-Risk and Expected Shortfall of Cryptocurrencies using Combinations based on Jump-Robust and Regime-Switching Models. DOI: 10.13140/RG.2.2.27175.98728:1–23, 2020.

- Walley (1991) P. Walley. Statistical reasoning with imprecise probabilities. Monographs on Statistics and Applied Probability, 42. Chapman and Hall, Ltd., London, 1991.

- Wang et al. (2020) G. Wang, K. Zhou, G. Li, and W. K. Li. Hybrid quantile estimation for asymmetric power GARCH models. Journal of Econometrics, https://doi.org/10.1016/j.jeconom.2020.05.005:1–22, 2020.

- Yiu et al. (2010) K. Yiu, J. Liu, T. Siu, and W Ching. Optimal portfolios with regime switching and value-at-risk constraint. Automatica, 46:979–989, 2010.

- Zhang and Nadarajah (2017) Y. Zhang and S. Nadarajah. A review of backtesting for value at risk. Communications in Statistics - Theory and Methods, pages 1–24, 2017.

- Zhu et al. (2016) D. Zhu, Y. Xie, W. Ching, and T Siu. Optimal portfolios with maximum value-at-risk constraint under a hidden markovian regime-switching model. Automatica, 74:194–205, 2016.