Multi-fidelity methods for uncertainty propagation in kinetic equations

Résumé

The construction of efficient methods for uncertainty quantification in kinetic equations represents a challenge due to the high dimensionality of the models: often the computational costs involved become prohibitive. On the other hand, precisely because of the curse of dimensionality, the construction of simplified models capable of providing approximate solutions at a computationally reduced cost has always represented one of the main research strands in the field of kinetic equations. Approximations based on suitable closures of the moment equations or on simplified collisional models have been studied by many authors. In the context of uncertainty quantification, it is therefore natural to take advantage of such models in a multi-fidelity setting where the original kinetic equation represents the high-fidelity model, and the simplified models define the low-fidelity surrogate models. The scope of this article is to survey some recent results about multi-fidelity methods for kinetic equations that are able to accelerate the solution of the uncertainty quantification process by combining high-fidelity and low-fidelity model evaluations with particular attention to the case of compressible and incompressible hydrodynamic limits. We will focus essentially on two classes of strategies: multi-fidelity control variates methods and bi-fidelity stochastic collocation methods. The various approaches considered are analyzed in light of the different surrogate models used and the different numerical techniques adopted. Given the relevance of the specific choice of the surrogate model, an application-oriented approach has been chosen in the presentation.

keywords:

Kinetic equations, Boltzmann equation, uncertainty quantification, moment methods, hydrodynamical limits, multi-fidelity methods, surrogate modelsLa construction de méthodes rapides pour la quantification de l’incertitude dans les équations cinétiques représente un défi en raison de la grande dimensionnalité des modèles qui impliquent souvent des coûts de calcul prohibitifs. D’autre part, précisément à cause de fléau de la dimension, la construction de modèles simplifiés capables de fournir des solutions approchées à un coût de calcul réduit a toujours représenté l’un des principaux axes de recherche dans le domaine des équations cinétiques. Des approximations basées sur des fermetures appropriées des équations des moments ou sur des modèles collisionnels simplifiés ont été étudiées par de nombreux auteurs. Dans le cadre de la quantification de l’incertitude, il est donc naturel utiliser tels modèles dans un cadre multi-fidélité où l’équation cinétique d’origine représente le modèle haute fidélité, et les modèles simplifiés définissent les modèles à basse fidélité. Ce travail passe en revue quelques résultats récents sur les méthodes multi-fidélité pour les équations cinétiques qui accélèrent la résolution du processus de quantification des incertitudes en combinant des évaluations de modèles haute fidélité et basse fidélité avec une attention particulière au cas des limites hydrodynamiques compressibles et incompressibles. Nous nous concentrerons essentiellement sur deux classes de stratégies : les méthodes des variables de contrôle multi-fidélité et les méthodes de collocation stochastique bi-fidélité. Les différentes approches sont analysées à la lumière des différents modèles simplifiés utilisés et des différentes techniques numériques adoptées. Compte tenu de la pertinence du choix spécifique du modèle de substitution simplifié, une approche orientée aux applications a été choisie dans la présentation.

1 Introduction

The Boltzmann equation is used to model a very large number of different phenomena ranging from rarefied gas flows such as those found in hypersonic aerodynamics, gases in vacuum technologies, or fluids inside microelectromechanical devices [15, 16], to the description of social and biological phenomena [74, 64]. For these reasons, the development of efficient and accurate numerical methods for solving kinetic equations and in particular the Boltzmann equation has experienced great commitment in the past to which contributed many researchers working in different fields [9, 65, 42, 43, 31, 104, 72, 70, 13]. We refer to [20, 22, 72, 71, 88] for recent monographs, collections and surveys.

In spite of the vast amount of existing research on the approximation of Boltzmann and related equations, the study of kinetic equations with stochastic terms has been considered only in recent years [87, 78, 41, 45, 92, 108, 53, 30, 86, 84]. See in particular the recent collection [46] and the survey [69]. We refer also to [57, 83, 87, 67, 87] for related researches in computational fluid dynamics and hyperbolic conservation laws.

On the other hand, these uncertainties arise naturally in many problems where these models are frequently used. In particular, incomplete knowledge of the interaction mechanism between the particles, imprecise measurements of the initial and boundary data, and unknown details of the domain geometry or forcing terms represent problems that are nearly impossible to overcome in a fully deterministic environment. At the same time, modeling the impact of these uncertainties in the solution is critical to providing reliable results for decision and design processes in applications.

Most of the literature on quantification of uncertainties in kinetic equations is based on the use of Stochastic-Galerkin methods built via generalized Polynomial Chaos (gPC) expansions [40, 108, 53, 45, 92, 19, 101]. Only recently these problems have been analyzed in the framework of statistical sampling methods based on Monte Carlo (MC) techniques [33, 23, 24, 26, 41]. We also cite a related research direction where Monte Carlo sampling has been used in the physical space while the random space is still approximated through gPC expansions [14, 78, 3, 85].

In particular, when dealing with kinetic equations, non-intrusive sampling methods, such as MC sampling, have several advantages over an intrusive gPC approach, as they allow to be used in combination with existing deterministic numerical solvers designed to satisfy certain relevant physical properties [22, 20]. This permits also to use implementations via fast algorithms and parallelization techniques which are essential to reduce the computational complexity [21]. Furthermore, Monte Carlo methods are very effective when the probability distribution of the random inputs is not known analytically or lacks of regularity while the approaches based on stochastic orthogonal polynomials may be impossible to use or may produce low accurate results [33, 60, 102].

One of the challenges central to uncertainty quantification for kinetic equations is the simulation cost. Most of the existing algorithms are mainly developed based on the direct resolution of the main reference model, the so-called high-fidelity model. For many complex systems, in particular, the kinetic equations with multidimensional random inputs, an accurate high-fidelity deterministic simulation can be so time-consuming and memory demanding that only a few high-fidelity simulations can be afforded. Many stochastic algorithms require repetitive implementations of the deterministic solver, the overall accurate stochastic simulation can be difficult and even computationally infeasible. However, there usually exist some approximate, less complex low-fidelity models which compared to the high-fidelity models, usually contain simplified physics and/or are simulated on a coarser physical mesh, and consequently, own a cheaper computational cost. Although their accuracy may not be high, the low-fidelity models are designed in such a way that they can resolve or capture certain important features of the underlying problem and produce reliable and qualitative predictions. Recently, there has been a surging interest in developing efficient uncertainty quantification algorithms by leveraging the strengths of multiple models where costs and fidelity, to be intended as the capacity of correctly describing the problem under consideration, vary. This approach is known in the literature as the multi-fidelity method [80, 27, 79].

In this work, we precisely survey several recent results about multi-fidelity methods for kinetic equations that accelerate the solution of the uncertainty quantification process based on stochastic samples by combining high-fidelity and low-fidelity model evaluations. This will be done through the introduction of multi-fidelity control variates techniques and bi-fidelity stochastic collocation approaches. The first class of methods uses the knowledge of the space spanned by one or more inexpensive low-fidelity models to improve the accuracy of the Monte Carlo solution at the high-fidelity level [23, 24, 25]. The choice of the low fidelity models follows the classical legacy of kinetic equations based on developing a hierarchy of reduced order models through suitable fluid-dynamics and diffusive scalings. Note that this requires the adoption of a suitable asymptotic-preserving solver for the high-fidelity model in order to take full advantage of the multiscale control variate [22].

However, the choice of the samples for the high fidelity solver remains arbitrary. The second methodology, is based on a simpler bi-fidelity setting where a single low-fidelity model is used to effectively inform the selection of representative points in the parameter space and then employ this information to construct accurate approximations to high-fidelity solutions [106, 105, 107, 63, 55, 32]. As a result, it does not necessarily require that the low-fidelity and high-fidelity to reside in the same physical space.

Consistent with the discussion above, the remainder of this survey is divided into two main parts. The first part addresses the construction of multi-fidelity Monte Carlo methods based on single or multiple control variates. The focus of this part will be primarily on the Boltzmann equation of rarefied gas dynamics [23, 24, 15]. The concepts will then be extended to the case of kinetic equations in the social and economic sciences where we also discuss how to couple the approach with direct simulation Monte Carlo solvers in the physical space [74, 76]. The second part will cover bi-fidelity approximations based on an appropriate choice of collocation nodes. Initially, the Boltzmann equation of rarefied gas dynamics will still be discussed. Subsequently, the bi-fidelity approach will be extended to linear transport kinetic equations in the diffusive limit, both in the classical case of neutron transport [54, 49] and in the context of epidemiology [1, 6]. Some final remarks conclude this review.

2 Fidelity spectrum of kinetic models

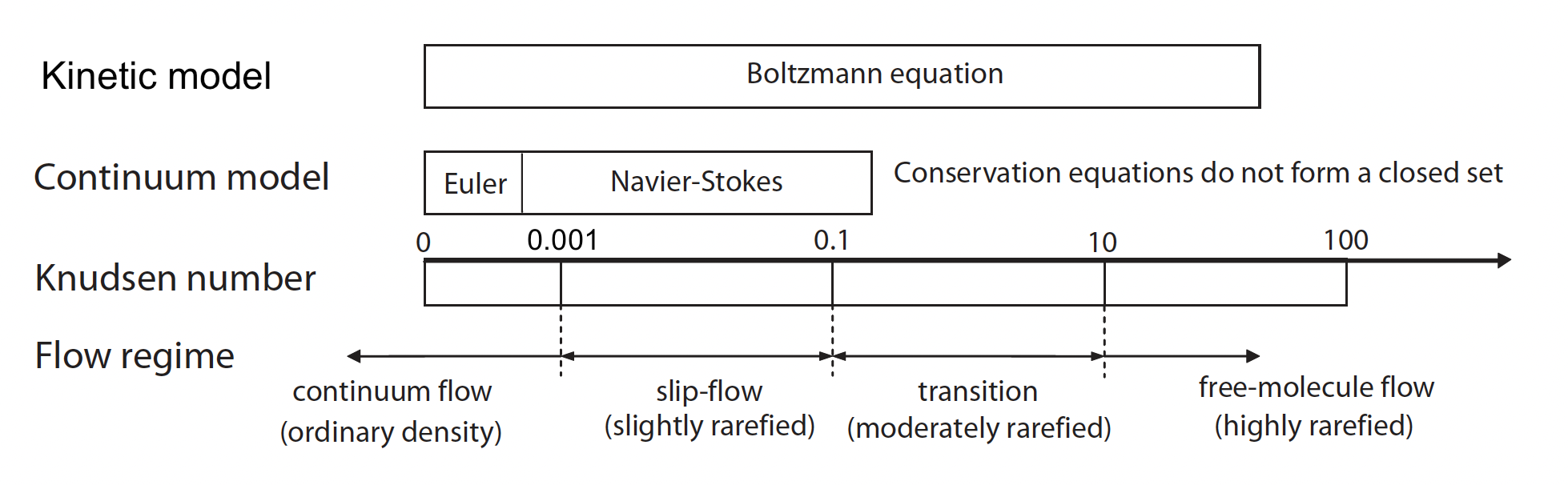

The fidelity of the kinetic models can vary along a broad spectrum between low- and high-fidelity. This sections provide examples of kinetic models across the fidelity spectrum, while defining the benefits and limitations of each model. We first focus on the Boltzmann equation of rarefied gas dynamics (RGD), including in our discussion the related moment equations, their possible closures, and the Bhatnagar-Gross-Krook (BGK) approximation. We next illustrate the quasi-invariant limit for some homogeneous Boltzmann equation of interest in the socio-economic sciences. Finally, we consider kinetic equations of linear transport in the diffusion limit both in the case of classical neutron transport and in recent applications in epidemiology. In Table 1 we summarized the various low- and high-fidelity models.

| High-fidelity | Low-fidelity | Application |

|---|---|---|

| Homogeneous Boltzmann | - Maxwellian steady state | Trend to equilibrium |

| - Homogeneous BGK | ||

| Full Boltzmann | - Euler equations | Rarefied gas dynamics |

| - Navier-Stokes equations | ||

| - Full BGK | ||

| Boltzmann-type models | - Mean-field steady state | Socio-economy |

| - Mean-field limit | ||

| Linear transport | - Diffusion limit | Neutron transport |

| - Goldstein-Taylor model | ||

| Compartmental transport | - Reaction-diffusion limit | Epidemiology |

| - Two-velocity models |

2.1 The Boltzmann equation of rarefied gas dynamics

We consider kinetic equations of the general form [15, 23]

| (1) |

where , , , , , and , , is a random variable. In (1) the parameter is the Knudsen number and the particular structure of the interaction term depends on the kinetic model considered. The most famous example is represented by the nonlinear Boltzmann equation of rarefied gas dynamics

| (2) |

where and

| (3) |

We consider the variable hard sphere (VHS) case with

| (4) |

The Boltzmann operator is such that the local conservation properties are satisfied, i.e.

| (5) |

where are the collision invariants. In addition, the operator satisfies the entropy inequality

| (6) |

As a consequence, the functions such that are local Maxwellian equilibrium functions

| (7) |

where , , are the density, mean velocity and temperature of the gas in the -position and at time defined as

| (8) |

Integrating now (1) against the collision invariants in the velocity space leads to the following set of non closed conservations laws

| (9) |

Close to fluid regimes, the mean free path between collisions, and therefore the Knudsen number, is very small (see Figure 1). In this situation, passing to the limit we formally obtain from (1) and so . Thus, at least formally, we recover the closed hyperbolic system of compressible Euler equations

| (10) |

with and

where is the identity matrix. For small but non zero values of the Knudsen number, the evolution equation for the moments can be derived by the so-called Chapman-Enskog expansion [15]. This originates the compressible Navier-Stokes equations as a second order approximation with respect to to the solution of the Boltzmann equation

| (11) |

with

| (15) | |||

| (16) |

with the viscosity and the thermal conductivity defined according to the Boltzmann operator [15]. The Prandtl number in this setting is defined as the ratio .

A simplified kinetic model is obtained by replacing (2) by a relaxation operator towards the local Maxwellian state. This model is usually referred to as BGK model since its introduction by Bhatnagar, Gross and Krook [8]

| (17) |

In (17) the function is the local Maxwellian and , in general, is proportional to the density and depends on the temperature . For instance, a frequently used law is given by , where is a constant and is the exponent of the viscosity law of the gas [58]. Conservation of mass, momentum and energy as well as Boltzmann’s H-theorem are readily satisfied and the equilibrium solutions are Maxwellians. Furthermore, the model has the correct fluid dynamic limit, since as formally the moments , , and satisfy the compressible Euler equations (10). However, this model exhibits some unphysical features, such as an unrealistic Prandtl number . The correct Navier-Stokes limit (11) can be recovered using more sophisticated BGK models such as the Ellipsoidal Statistical BGK (ES-BGK) models [39].

The Boltzmann equation (1) and its low-fidelity counterparts such as the BGK equation (17) and the compressible Euler (10) and Navier-Stokes (11) systems will be employed as leading examples both for the development of the control variate multi-fidelity methods in Section 3 as well as in the case of the stochastic collocation bi-fidelity approach in Section 4.

2.2 Kinetic models for the social sciences

Recently, Boltzmann-type models have also become quite popular for describing binary dynamics between agents, representing individuals interacting in a society (see [74] for an introduction to the topic). In presence of uncertainties, the pair of interacting agents is characterized by the pre-interaction states and the post-interaction states obtained as follows [26, 76]

| (18) |

where is a given constant, , are suitable interaction functions depending on a random variable . Furthermore, and are i.i.d. random variables with zero mean and variance . The function defines the local relevance of the diffusion.

Introducing the distribution function , its evolution is given in terms of the Boltzmann-type equation

| (19) |

being any observable quantity which may be expressed as a function of the microscopic state of the agents. The symbol denotes the expectation with respect to . Taking is easily seen that the number of agents is conserved in time.

In contrast to the classical Boltzmann case (1), the equilibrium states of the socio-economic Boltzmann models like (19) are often unknown. A way to achieve some insight into the long time behavior of such systems is to consider the quasi-invariant interaction limit [74, 73, 99]. To that aim, given a small parameter , let us introduce the scaling

| (20) |

and denote by the scaled distribution. Thus, small values of correspond to the case in which elementary interactions (18) produce minimal modification of and and, at the same time, the frequency of such interactions increases like . Then, the distribution is solution to

| (21) |

Now, for small values of using a Taylor expansion of the interactions it can be shown that in the limit , converges, up to subsequences, to a distribution function which is weak solution to the following Fokker-Planck equation

| (22) |

where

provided that suitable boundary conditions are taken for .

We shortly present now two socio-economic models used in the rest of the survey as examples for developing our multi-fidelity Monte Carlo methods. The first is an opinion formation model where we set and the binary interaction rules read [74, 2, 75]

| (23) | ||||

where the function weights the compromise tendency with respect to the relative opinion . In the quasi-invariant limit, the following model is obtained

If in (23), , and we consider uncertainties in the initial distribution, the steady state distribution of the Fokker-Planck model reads

| (24) |

where is a normalization factor such that . Other form of equilibrium distribution can be determined as well [75].

For example the choice produce a Beta-type steady state of the form

| (25) |

where is the Beta function. We refer to [75] for a detailed discussion.

The second example, known as the Cordier-Pareschi-Toscani (CPT) model [74, 18] for wealth exchanges between agents composing a simple economy. The wealth variable is here allowed to take values on the positive half line therefore . The binary interactions with reference to (18) are such that and with . We also consider . The uncertain parameter determines the proportion of wealth that a single agents wants to invest, the quantity is the so-called saving propensity. Thus, the binary scheme for wealth exchanges reads

| (26) |

The corresponding mean field model reads

If we assume that there is no uncertainty in the initial conditions, following [74] the equilibrium state can be computed and reads

| (27) |

where denotes the Gamma function and . We refer to Section 3.6 for applications of control variate strategies based on the mean-field equilibrium states (24) and (27) or on the full mean-field system (22).

2.3 Linear transport equations

Another class of kinetic models that will be considered in the sequel are the linear transport equation under diffusive scaling and with random parameters [49, 54, 45]. Let be the probability density distribution of particles at time , position , and with the cosine of the angle between the particle velocity and its position. In particular, we consider in our discussion the case of random scattering coefficients with a random vector. The time evolution of the distribution function is governed by the following linear transport equation under diffusive scaling

| (28) |

where is the Knudsen number. In order to shed light on the link between the kinetic equation and its diffusive limit, we first split (28) into two equations for

| (29) |

where we omitted for brevity the dependence from in the kinetic density. By using now the so-called even-odd decomposition [48], we introduce then the relative even and odd parities

| (30) |

Thanks to the above reformulation, the system (29) can then be recast in the following form:

| (31) |

where

| (32) |

Now the formal passage to the limit is easily obtained. In fact, as , the system (31) yields

Substituting back this limit it into the same system (31) and integrating over , one gets the limiting diffusion equation [49, 4]

| (33) |

The neutron transport equation (28) and its low-fidelity diffusive limit (33) are employed in Section 2.3 to design efficient bi-fidelity approximations, together with a different low-fidelity models given by the Goldstein-Taylor model [74, 54].

2.4 Kinetic models in epidemiology

We consider the development of hyperbolic transport models for the propagation in space of an epidemic phenomenon described by a classical compartmental dynamics [5, 10, 1]. The model is based on a kinetic description with discrete velocities of the spatial movement and interactions of a population of susceptible, infected and recovered individuals. The model is constructed in such a way that a diffusive behavior of the spread can be recovered in a suitable limit similar to the one described in Section 2.3. In the considered framework, the distributions of individuals at position at time moving with velocity are then denoted by

These quantities represent, respectively, the fraction of susceptible individuals (who may be infected by the disease), the fraction of infected individuals (who may transmit the disease) and removed individuals (healed or died due to the disease). We assume to have a population without an a-priori immunity and we neglect the vital dynamics represented by births and deaths due to the time scale considered. The densities for , and are given by

| (34) | |||||

In this setting, the distribution functions satisfy the epidemic transport equations

| (35) | |||||

where , , with take into account the heterogeneities of geographical areas, thus are chosen dependent on the spatial location. The quantity is the recovery rate of infected, and the transmission of infection is governed by an incidence function modeling the transmission of the disease [38]

| (36) |

with the classic bi-linear case corresponding to , . Finally, represent the relaxation frequencies playing the role of the Knudsen number introduced in Section 2.3 when discussing the linear transport equation in the diffusive scaling. In this model, the reproduction number for the system (35) is given by

| (37) |

This quantity describes the space averaged instantaneous variation of the number of infected individuals at time . Now, with the scope of deriving a possible surrogate/low-fidelity model approaching the high fidelity model described by system (35), we introduce the flux functions

| (38) |

We integrate then the system (35) over and obtain the following equations for the macroscopic densities

| (39) | |||||

The above system is not closed since the flux functions depend upon the distribution functions values. However, by introducing now the so-called diffusion coefficients that characterize the diffusive transport mechanism of susceptible, infected and removed

| (40) |

one can pass to the limit while keeping the diffusive coefficients finite. This permits to get the following diffusion system characterizing a possible low fidelity model for the spread of a disease

| (41) | |||||

In Section 4.4 we will discuss strategies for quantifying uncertainty for the above model while also introducing an alternative low-fidelity model based on a simpler two-velocity dynamic [7, 6].

3 Multi-fidelity control variate methods

This part introduces the multi-fidelity control variate methods for the Boltzmann equation of gas dynamic introduced in Section 2.1 and then discusses its extension to the kinetic models in the social sciences presented in Section 2.2.

3.1 Some notations and definitions

First we introduce some notations and assumptions that will be used in the sequel of the section. If is distributed as we denote the expected value of any quantity of interest expressed as a functional by

| (42) |

and its variance by

| (43) |

As quantity of interest, in addition to , another natural choice is represented by , the moments of the distribution function. In the latter case the dependence on is dropped in the previous definitions.

We also introduce the following -norm with polynomial weight [82, 90]

| (44) |

Next, for a random variable taking values in , we define

| (45) |

The above norm, in general, differs from a more classical norm used in the context of uncertainty quantification for hyperbolic conservation laws. This latter often reads

| (46) |

which has been used for example in [60]. Note, in particular that by Jensen inequality [89], we have

| (47) |

Let also observe that for the two norms (45) and (46) coincide. In the sequel, we will consider in our analysis the norm (45) with . The extension of the results shown about the control variate approach to norm (46) for typically requires to be compactly supported (see [60, 23, 59] for further details).

We assume that the model (1) is solved in the phase-space by means of deterministic methods and that the following estimate is satisfied (see [90, 22, 93, 23, 61])

| (48) |

with a positive constant which depends on time and on the initial data, and the computed approximation of the deterministic solution at time on the mesh and . The positive integers and characterize the accuracy of the discretizations in the phase-space and, for simplicity, we ignored the errors due to the time discretization and to the truncation of the velocity domain in the deterministic solver. We refer to [22] for details about the numerical discretization of a kinetic equation of the form (1). In the sequel, if not otherwise stated, in the numerical examples we will make use of the fast spectral method [61, 29] combined with finite volumes WENO solvers in space [44]. The time discretization is performed by suitable asymptotic-preserving techniques [22].

3.2 Monte Carlo sampling method.

Before discussing the multi-fidelity approach, we first recall the standard Monte Carlo method for the estimation of the uncertainties when computing the solution of a kinetic equation of the type (1) with random initial data . To avoid unnecessary difficulties, we will mainly restrict to the case of a one-dimensional random input distributed as , the extension to multidimensional setting being straightforward.

The simplest Monte Carlo (MC) sampling method for UQ is described in Algorithm 3.1.

-

1.

Sampling: Sample independent identically distributed (i.i.d.) initial data , from the random initial data and approximate these over the grid.

-

2.

Solving: For each realization , the underlying kinetic equation (1) is solved numerically by a deterministic solver. We denote the solutions at time by , , where and characterizes the discretizations in and .

-

3.

Estimating: Estimate the expected value of the random solution field with the sample mean of the approximate solution

(49)

Similarly to the case of the expectation, higher order statistical moments can be computed as well. The above algorithm present several advantages:

-

i)

Straightforward to implement in any existing deterministic or stochastic solver for the particular kinetic equation.

-

ii)

It operates in a post-processing setting, the only data interaction between different samples is in step , when ensemble averages are computed.

-

iii)

It is non-intrusive and easily parallelizable.

Concerning the error analysis, starting from the fundamental estimate [12, 56]

| (50) |

one can obtain the typical error bound which is summarized by the following proposition (see [60, 59, 23] for more details).

Proposition 3.1.

Once an error estimate is given, it is possible to equilibrate the discretization and the sampling errors in the a-priori estimate taking and . This means that in order to have comparable errors the number of samples should be extremely large, especially when dealing with high order deterministic discretizations. As a consequence, the Monte Carlo approach may result very expensive in practical applications.

3.3 Multi-Scale Control Variate (MSCV) method

We survey here the MSCV approach recently introduced in [23]. The main idea of the method is to reduce the variance of standard Monte Carlo estimators using as control variate different low-fidelity models at the various scales introduced by the Knudsen number. In the following we will refer to this type of approach that uses a high-fidelity model and a single low-fidelity model as the bi-fidelity case.

3.3.1 The space homogeneous case

For sake of clarity, we first illustrate the method when applied to the solution of a kinetic equation of the type (1) with deterministic interaction operator and random initial data in a homogeneous setting

| (52) |

where . Let observe that without loss of generality, we have fixed here , since in the space homogeneous case the only temporal scale is the collisional one. Under suitable assumptions, one can show that exponentially decays [99, 98, 97, 96] to the unique steady state such that which satisfies

| (53) |

The error of the standard Monte Carlo estimator reads now

| (54) |

Thus, a first variance reduction strategy is obtained by splitting the expected value of the solution as

| (55) |

and exploiting the fact that can be evaluated with arbitrary accuracy at a negligible cost (for example using a very fine grid of samples) since it does not depend on the solution computed at each time step. Now, if we use (55) and estimate

| (56) |

we obtain an error of the type

Since the non equilibrium part goes to zero in time exponentially fast, then also its variance goes to zero, which means that for long times estimate (56) becomes exact and depends only on the accuracy of the evaluation of .

The above argument can be generalized by considering a time dependent approximation of the solution , whose evaluation is significantly cheaper than computing , such that for some moments and that as . For example, one can consider to use the BGK approximation (17) which in this simple case can be exactly solved giving the following expression

| (57) |

Then we have

| (58) |

where and or accurate approximations of the same quantities.

Using the same estimator (56)

| (59) |

gives the following estimate for the error

where even in this case, as .

Let now observe that a general variance reduction technique can be obtained by introducing the following control variate estimator [23]

| (60) |

In particular, for we recover the standard MC estimator , whereas for we have the estimator corresponding to (59). The following result holds true

Lemma 3.1.

The control variate estimator (60) is unbiased and consistent for any .

Démonstration.

If we now consider a new the random variable depending on

we have that the expectation for this new random variable is such that , , i.e. it shares the same expectation of the distribution function in terms of the random variable. Moreover, we can quantify its variance as

| (61) |

and we can prove the following result [23]

Theorem 3.1.

The quantity

| (62) |

minimizes the variance of at the point and gives

| (63) |

where is the correlation coefficient between and . In addition, we have

| (64) |

Démonstration.

Equation (62) is readily found by direct differentiation of (61) with respect to and then observing that is the unique stationary point. The fact that is a minimum follows from the positivity of the second derivative . Then, by substitution in (61) of the optimal value one finds (63) where

In addition, since as we have , asymptotically and independently of . ∎

The above result permits in combination with a deterministic solver satisfying (48) to get the following error estimate [23, 60]

| (65) |

where , and depends on the final time and on the initial data. Let observe that in the above estimate, we ignored the statistical errors due to the approximation of the control variate expectation and the error in the estimate of . Note finally that, since as the statistical error will vanish for large times.

Remark 3.2.

In practice, appearing in is not known and has to be estimated. Starting from the samples we have the following unbiased estimators

| (66) | |||||

| (67) |

which allow to estimate

| (68) |

It can be verified easily that as .

The resulting multi-scale control variate method based on a low-fidelity model is summarized in Algorithm 3.2.

-

1.

Sampling: Sample i.i.d. initial data , from the random initial data and approximate these over the grid.

- 2.

-

3.

Estimating:

-

(a)

Estimate the optimal value of as

-

(b)

Compute the expectation of the random solution with the control variate estimator

(69)

-

(a)

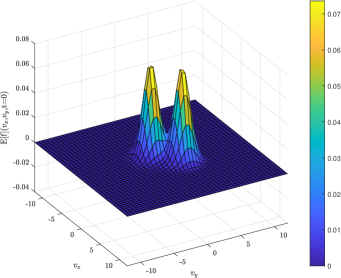

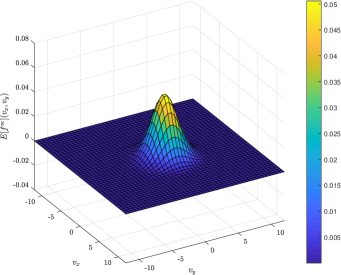

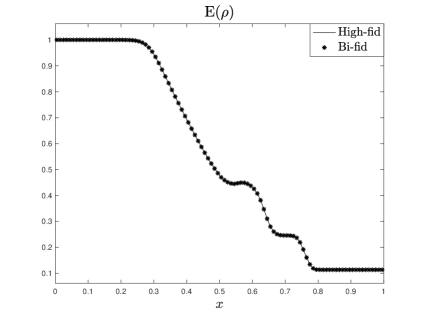

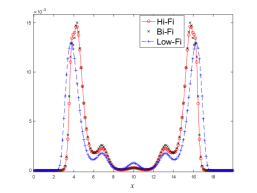

In Figure 2, we show some results of the MSCV method in the space homogeneous case in comparison with standard MC approaches. In this test, we solve the homogeneous Boltzmann equation with Maxwellian kernel, i.e. equation (4) with , for through the fast spectral method [62] using and modes in each direction. The initial condition is a two bumps problem with uncertainty

| (70) |

with , , and uniform in . The figure shows the expectation of the distribution function together with the error of the expected value of the solution.

The gain in accuracy obtained with the MSCV methods is of several orders of magnitudes larger with respect to standard Monte Carlo.

3.3.2 The space non homogeneous case

We focus now on the full space non homogeneous problem (1). Generalizing the space homogeneous method based on the local equilibrium as control variate, we consider here the Euler closure. If we denote by the solution of the fluid model (10), for the same initial data, the corresponding equilibrium state can be used as low fidelity model. In this case, the control variate estimate based on i.i.d. samples reads

| (71) |

where is an accurate approximation of . Consistency and unbiasedness of (71) for any follows again from Lemma 3.1. The fundamental difference is that now the variance of

will not vanish asymptotically in time since , unless the kinetic equation is close to the fluid regime, namely for small values of the Knudsen number. We can state the following

Theorem 3.2.

If the quantity

| (72) |

minimizes the variance of at the point and gives

| (73) |

where is the correlation coefficient between and . In addition, we have

| (74) |

The proof follows the same lines of Theorem 64. Note that, since as we formally have which implies and , from (72) and (73) we obtain (74).

Similarly to the homogeneous case, the generalization to an improved control variate based on a suitable approximation of the kinetic solution by a low fidelity model can be done with the aid of a more accurate fluid approximation, like the compressible Navier-Stokes system, or a simplified kinetic model. In the latter case, we can solve a BGK model (17) for the same initial data and use its solution as control variate. More precisely, given i.i.d. samples of the solution and of the control variate we define the new estimator

| (75) |

where is an accurate approximation of . As for the case of the compressible Euler equations in the space non homogeneous case the variance of

will not vanish asymptotically in time since , unless the two solutions are very close together, such as in the fluid regime. Thus, while the first part of Theorem 64 is still valid, the optimal value

| (76) |

and the variance

| (77) |

now satisfy a different condition relating the low fidelity and the high fidelity models. In fact, one can prove that

| (78) |

In fact, since as from (1) we formally have which implies and , from (76) and (77) we obtain (78).

Let notice now that even if simulating the control variate system is cheaper than the full model, however its computational cost is no more negligible and thus we cannot ignore it. In this respect, we assume then that the control variate model is computed over a fine grid of samples. At the same time, we replace the exact computation of the expectation of the low fidelity BGK model with the approximation

in the estimator (75) which we will denote now by . This replacement has an impact on the optimal value of . In fact, using the independence of and by the central limit theorem [56, 37] we have

Thus, minimizing the variance now leads to the optimal value

| (79) |

with given by (76). As can be easily seen from the above formula, this correction may be relevant only in the cases when and do not differ too much. In many practical cases and in the simulations shown after, however, so that and we consequently assume .

Using the optimal value (76) for the control variate variable and a deterministic solver which satisfies (48), we obtain the error estimate [23, 60]

| (80) | |||

with , and with a constant depending on the final time and on the initial data.

Remark 3.3.

For space non homogeneous simulations, one is typically interested in the evolution of the moments instead that on the evolution of the shape of the distribution function. More in general, one can compute the optimal value of with respect to any quantity of interest as

| (81) |

In particular, in the case , we have . Note that, using (81) all estimates in this section for translates into estimates for . This is particularly relevant when compressible Euler or Navier-Stokes equations are used as the low-fidelity model.

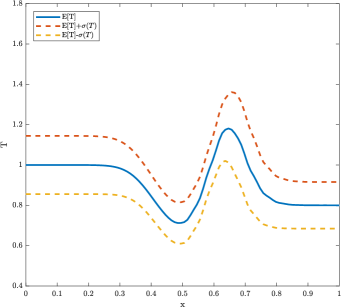

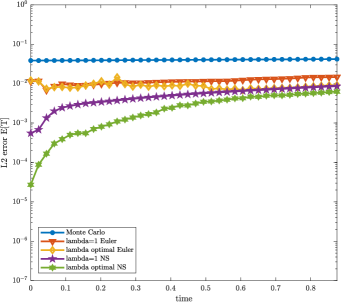

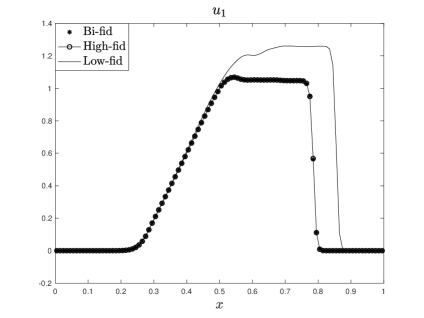

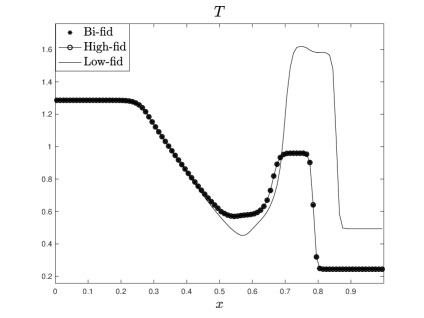

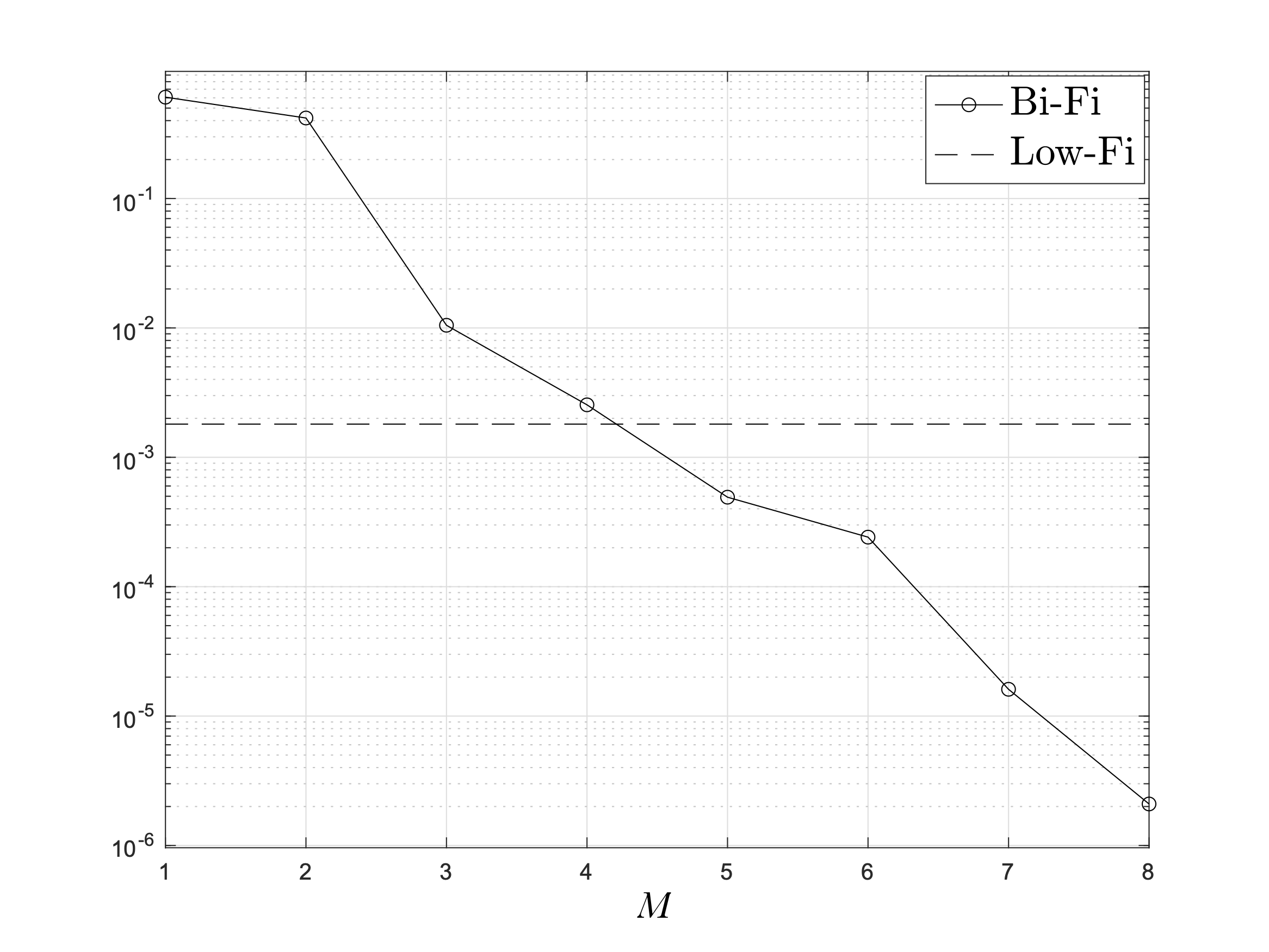

In Figure 3, we show the results of the MSCV method where the BGK or the compressible Euler equations are used as low fidelity models. The Boltzmann equation is solved for , , and in (4). The fast spectral method [61] for with modes in each direction is used combined with a fifth order WENO method [91] in space for with grid points.. The initial conditions are given by Sod problem with uncertain temperature

with , uniformly distributed in and equilibrium initial distribution given by

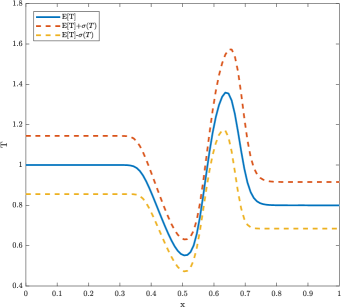

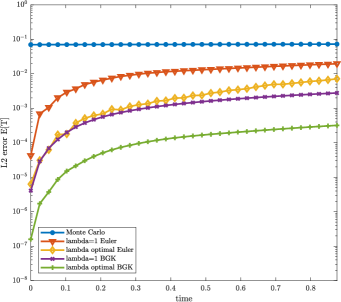

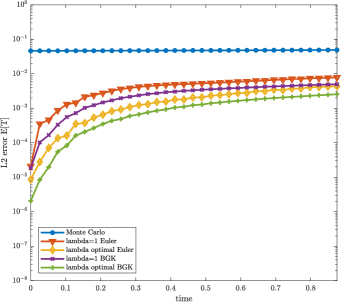

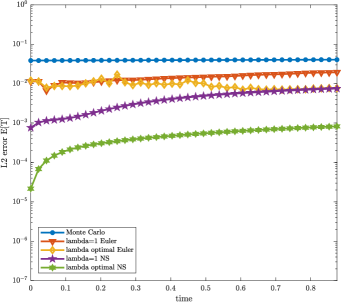

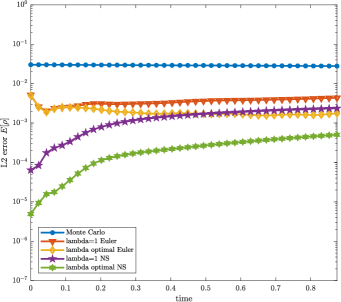

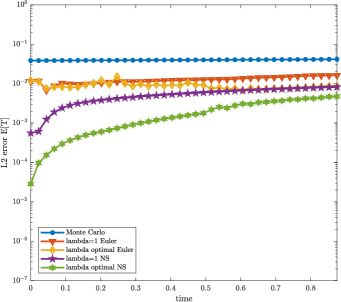

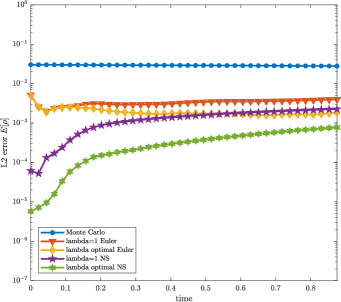

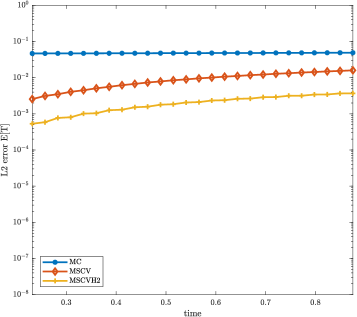

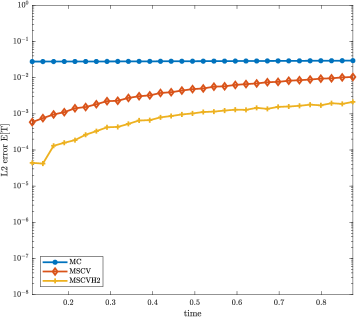

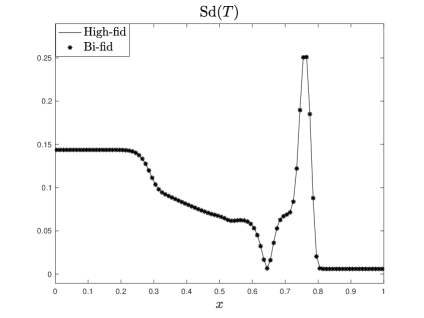

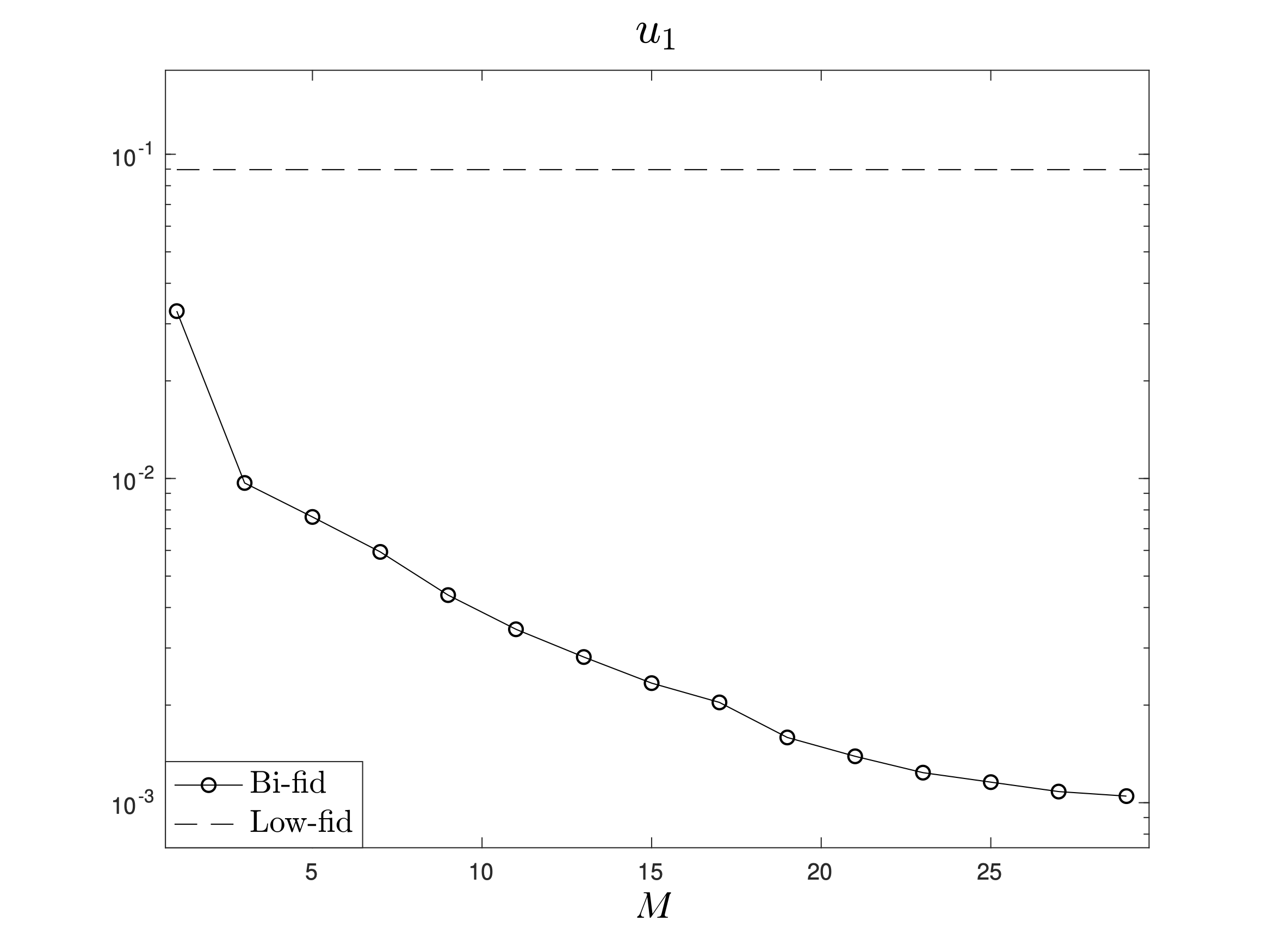

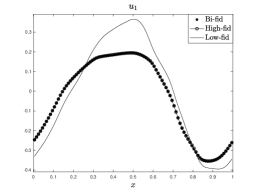

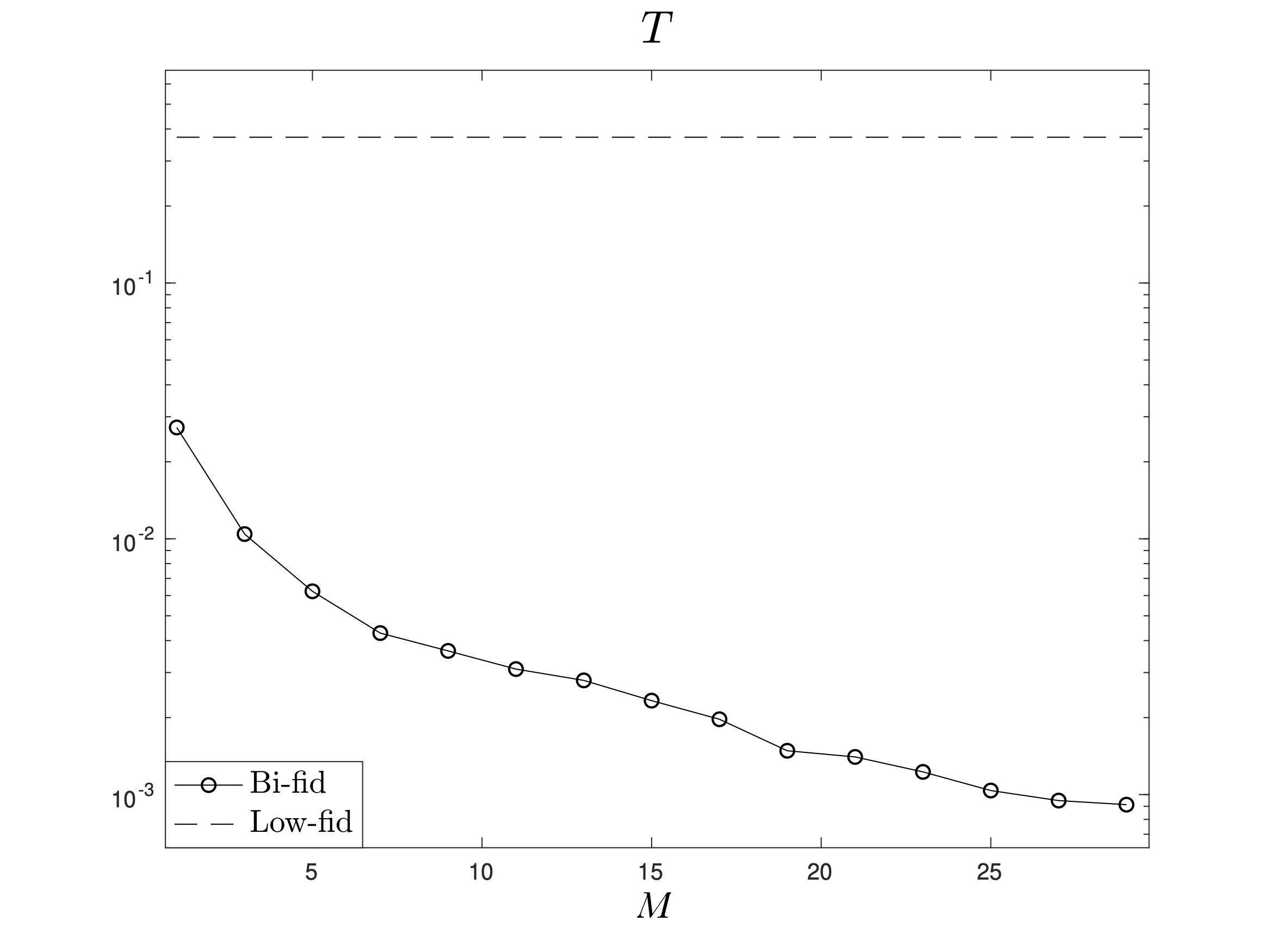

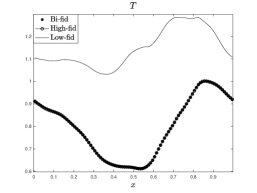

We report the results for two different regimes, namely and . The images show on the top the expectation of the temperature at the final time together with the confidence bands with the standard deviation. On the bottom, we report the various errors for the expected value of the temperature as a function of time. The number of samples used to compute the expected value of the solution is while the number of samples used to compute the control variate is . The optimal values of have been computed with respect to the temperature.

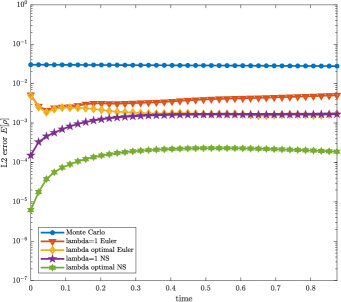

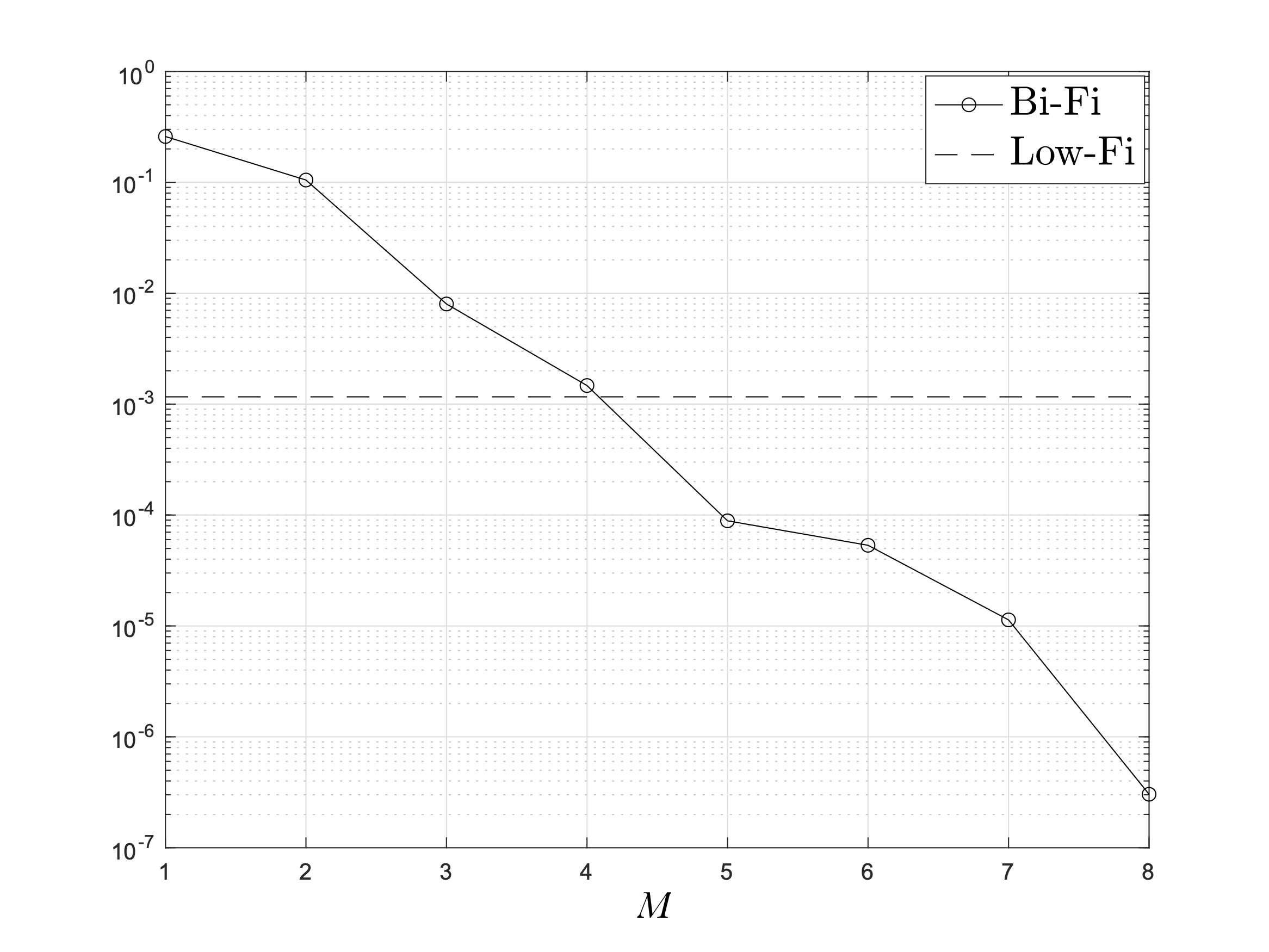

In Figure 4 we show the results of the same MSCV approach where the Navier-Stokes equations (11) are used as low fidelity model. The setting is similar to the one shown in Figure 3 where now, however, uncertainty is also present in the initial density. We then have

the other discretization parameters remaining unchanged. In this case, the optimal values of have been computed both with respect to the density (left images) as well as with respect to the temperature (right images). We stress that the computation of the optimal values is done through an offline procedure. This employs, irrespectively of the quantity of interest, the same results of the deterministic simulations for the low and high fidelity models. These results are then combined to improve the estimation of the expectation of respectively the density and the temperature. For all situations reported the Navier-Stokes control variate approach improves the result of the compressible Euler case, especially when far from the thermodynamical equilibrium.

3.4 Multi-fidelity MSCV methods

3.4.1 The space homogeneous case.

In this section we extend the control variate strategy to the case in which several low-fidelity models are employed to accelerate the statistical convergence. We start again from the space homogeneous equation (52) for sake of clarity. Let us consider approximations of furnished by a set of low fidelity models whose properties will be discussed later. We can then define a new random variable as

| (84) |

Clearly (84) is such that while the variance of this new variable is given by

| (85) | |||||

The above quantity can be rewritten in a more compact form by introducing the following notations

giving then

| (86) |

where , is the symmetric covariance matrix. Following the same path of the bi-fidelity case, one can now try to find the set minimizing the variance of the new variable . This is obtained thanks to the following Theorem (see [24] for a proof):

Theorem 3.3.

Assuming the covariance matrix is not singular, the vector

| (87) |

minimizes the variance of at the point and gives

| (88) |

Having the above result in mind, one can then introduce the control variate estimator based on (84) which takes the form

| (89) |

where is an accurate approximation of . In the above formula, we also assumed to have at disposal i.i.d. samples from the solution and from the control variate functions for . Moreover, in practice, as done for the bi-fidelity case, to estimate the value of the vector we can use directly the Monte Carlo samples as in the bi-fidelity case. The resulting multi-fidelity MSCV method is summarized in Algorithm 3.3.

-

1.

Sampling: Sample i.i.d. initial data from the random initial data and approximate these over the grid . Denote these samples by , .

-

2.

Solving:

-

(a)

For each control variate and for each realization of the random input data , , the resulting control variate model is solved with mesh width . We denote the resulting ensemble of deterministic solutions for at time by

-

(b)

For each realization , the underlying kinetic equation (52) is solved with mesh width . We denote the solution at time by , .

-

(a)

-

3.

Estimating:

-

(a)

Estimate the optimal vector of values solving

(90) where and .

-

(b)

Compute the expectation of the random solution with the control variate estimator

(91)

-

(a)

An interesting result is obtained introducing the vector , such that . This gives , and equation (84) reads

| (92) |

This permits to conclude that the variance of is reduced to zero if is in the span of the set of functions . Using now Gram–Schmidt orthogonalization and observing that

we can also construct the vector , with orthogonal components, for , as follows [35]

| (93) |

and define , such that , . Then, we may try to minimize the variance of the random variable

| (94) |

which now using the orthogonality property reads

Given the above arguments, one can prove the following result [24]:

Theorem 3.4.

If the control variate vector in (94) has orthogonal components, for , then if the vector with components

| (95) |

minimizes the variance of at the point and gives

| (96) |

where is the correlation coefficient between and .

3.4.2 A leading example: two control variates

To better exemplify the multi-fidelity approach, here we give the details of the method in the case , where , the initial data, and , the stationary state. In this case we know that is in the span of the control variates at and as . A straightforward computation shows that the optimal values and are given by

where . Using samples for both control variates, the optimal estimator reads

Now, at since we clearly have and so that the estimator (LABEL:eq:nest2b) is exact

Moreover, by the same arguments as in Theorem 64, for large times since from (LABEL:eq:l12) we get

and thus, the variance of the estimator vanishes asymptotically in time

We want now to emphasize the relation between this last example and the bi-fidelity case based on the BGK model discussed in (60). This latter can be rewritten in the form (LABEL:eq:nest2b)

where

Therefore, the single control variate based on the BGK model can be understood as a suboptimal solution to the minimization problem for the control variates and . In particular, if the solution has the form (57), namely the full model is the BGK model, then it is in the span generated by and and we obtain and .

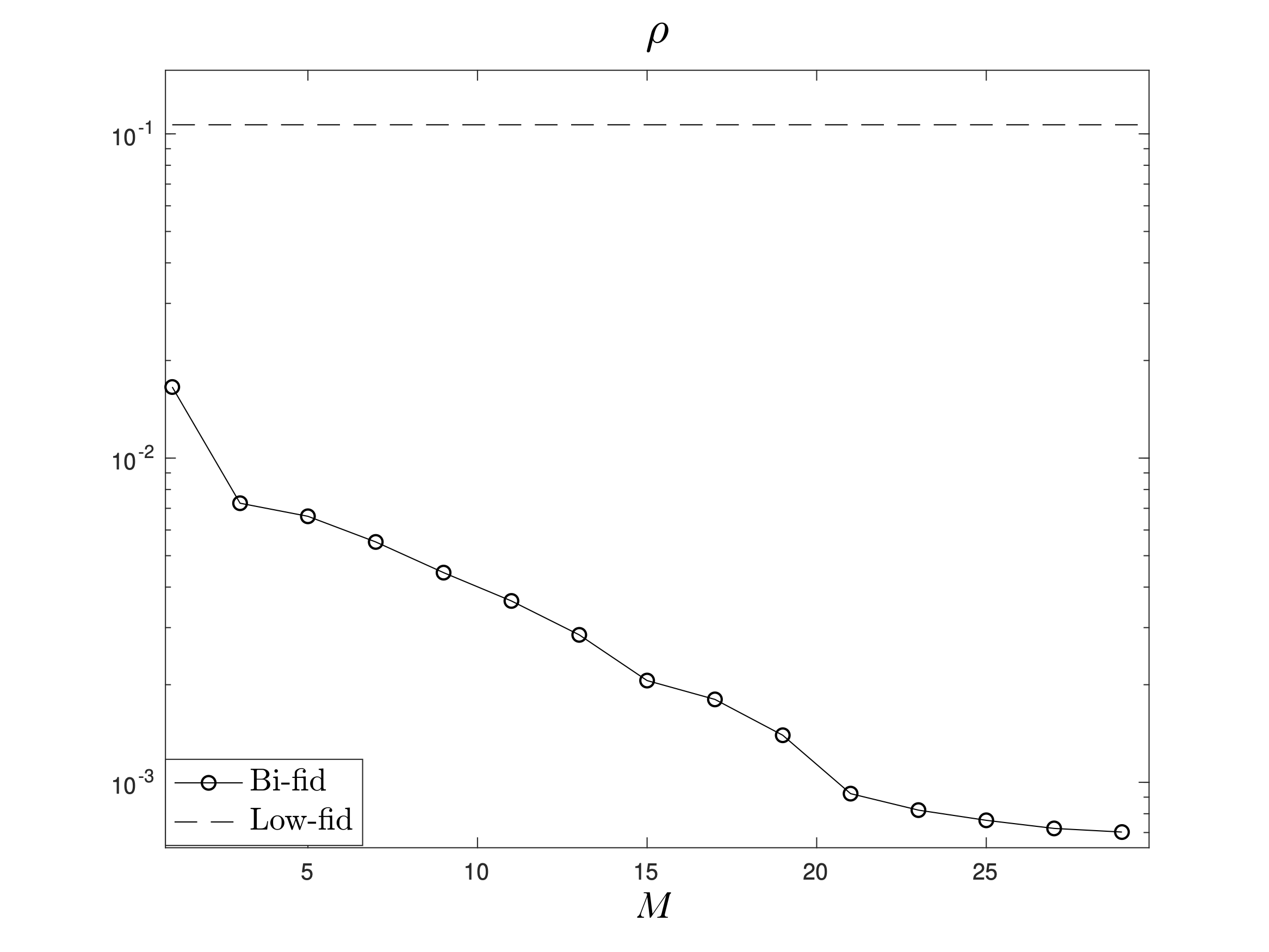

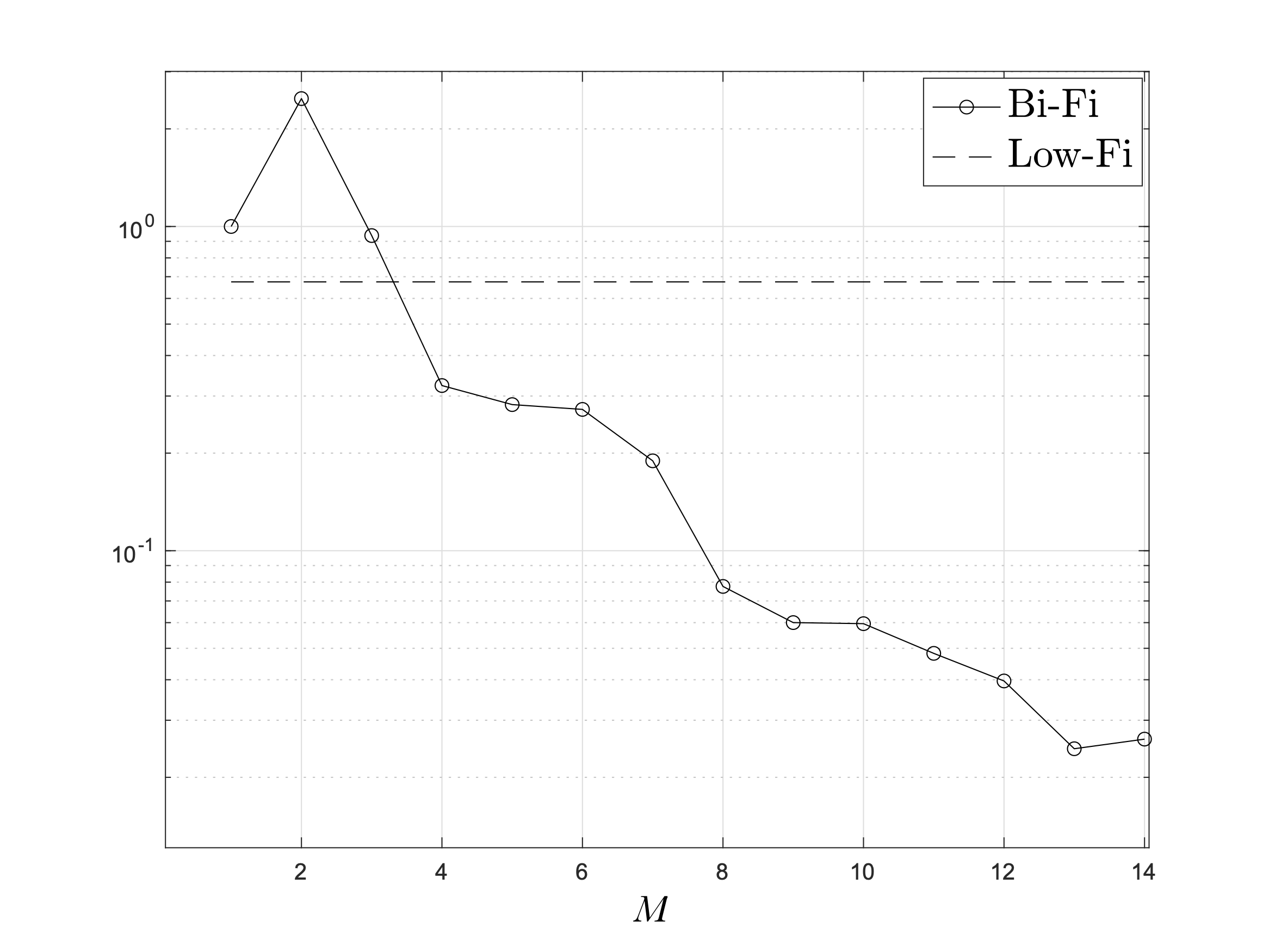

We now compare the case of the single control variate given by the BGK model discussed in 3.3 with the case of the two control variate approach discussed here. The number of samples used to compute the expected solution for the Boltzmann equation is while the expected values of the control variates can be evaluated offline as in the BGK case. The initial condition is the two bumps problem with uncertainty (70) and the same discretization parameters as in Figure 2 have been used. In Figure 5, we report the error with respect to the random variable in the computation of the expected value for the distribution function for the different methods. We observe that the multi-fidelity method with two control variates permits to gain one order of accuracy with respect to the standard bi-fidelity approach.

3.4.3 The space non homogeneous case.

For non homogeneous problems, as in the bi-fidelity case summarized in Section 3.3.2, we cannot assume to know offline the expectation of the control variate. Therefore, the control variates have a non-negligible computational cost. Each control variate, in fact, acts at a certain scale and requires the numerical solution of a suitable time dependent model in the phase space. The multi-fidelity MSCV estimator (89), based on the multi fidelity control variates , , for the solution to the space non homogeneous problem (1), reads

where samples have been used to estimate the expectations of the control variates . As in the bi-fidelity case, minimization of the variance of (LABEL:eq:mscvgh), leads to the optimal values

| (102) |

with given by (87). In the sequel we assume so that .

We can apply the Gram–Schmidt orthogonalization (93) and estimate

with the optimal vector of values defined by (95). For the estimator (LABEL:eq:mscvg2ih) we have the following generalization of the error estimate (98).

Proposition 3.3.

Consider a deterministic scheme which satisfies (48) for problem (1) with random and sufficiently regular initial data . Then, the multi-fidelity MSCV estimate defined in (LABEL:eq:mscvg2ih) with the optimal values given by (95) satisfies the error bound

| (104) | |||

with

and depends on the final time and on the initial data.

3.5 Hierarchical multi-fidelity MSCV methods

3.5.1 The space homogeneous case

We formulate in this part a recursive construction of the multiple control variate estimator (89) based on the use of several low-fidelity models.

To this aim, let us assume that the control variates represent kinetic models with an increasing level of fidelity. Under this assumption the control variate represents the less accurate model whereas the control variate is the closer model to the high fidelity model .

To start with, we estimate with samples using as control variate

Next, to estimate of we use samples and consider as control variate

Similarly, in a recursive way we can construct estimators for the remaining expectations of the control variates using respectively samples until

and we stop with the final estimate

with . By combining the estimators of each stage together we obtain the hierarchical MSCV estimator

Now, if we compute the optimal values independently for each level by ignoring the errors due to the approximations of the various expectations, if , we obtain

| (106) |

where we used the notation . We refer to this set of values as quasi-optimal since they are obtained in the hypothesis in which the expectations are computed without any approximations. Note also that, since the control variates and are known on the same set of samples the values can be estimated using (66)-(67).

We now analyze the estimator (LABEL:eq:lambdar) in more details. We can recast it in the form

| (107) |

where we defined

| (108) |

Since by the central limit theorem [56, 37] we have , using the independence of the estimators , , the total variance of the estimator (107) is

Now, the first order optimality conditions

lead to the tridiagonal system for

| (109) |

where we assumed and . The system (109) can be rewritten as

The above expression permits to conclude that the quasi-optimal values computed in (106) solves the above system up to error and thus they are a sufficiently good approximation in the case in which . The following Theorem holds true [24]

Theorem 3.5.

We summarized in Algorithm 3.4 the details of the hierarchical MSCV method applied to the space homogeneous problem (52) in combination with a deterministic solver.

-

1.

Sampling: For each control variate , we draw a number of i.i.d. samples from the random initial data and approximate these over the mesh . Denote these control variate dependent number of samples for by

and set .

-

2.

Solving:

-

(a)

For each control variate and for each realization of the random input data , , the resulting model is solved with mesh widths . We denote the resulting ensemble of deterministic solutions for at time by

-

(b)

For each realization , the underlying kinetic equation (1) is solved with mesh widths . We denote the solution at time by , .

-

(a)

-

3.

Estimating:

-

(a)

Estimate the quasi-optimal vector of values as

(111) where we used the notation , .

-

(b)

Compute the expectation of the random solution with the control variate estimator

(112) where

-

(a)

Regarding the error bound that we obtain using (107) with the values given by (106) le us observe that if, at each stage, we denote

then by the error bound (80) we have

where is a suitable constant and we defined

| (113) |

| (114) |

Thus one can prove the following result

Proposition 3.4.

3.5.2 The space non homogeneous case.

In a space non homogeneous setting the hierarchical multi-fidelity MSCV estimator (107), based on the control variates , , with increasing level of fidelity for the solution to (1), is

| (116) |

with and where now the optimal values of are obtained from the quasi-optimal solution (106) using (108) or by the correction introduced by the solution of the tridiagonal system (109) if relevant. In this case, the extension of algorithms 3.4 and estimate (115) to the non homogeneous case follows straightforwardly simply replacing and with and , and is omitted for brevity.

For sake of clarity and due to its importance in practical applications, we describe the details of the hierarchical method in the case . We consider as the equilibrium state associated to the system of Euler equations (10) with , and corresponding to the limit case in (1). As a second control variate we consider as the solution of the BGK model (17). Both models are solved for the same initial data . Now, the Euler equations are used as control variate to improve the computation of the expectation in the BGK model, that in turn is used as control variate to improve the computation of the expectation in the full Boltzmann model.

The hierarchical two-level estimator reads

| (117) |

where . If we define and their optimal values are computed as solutions of system (109) for

with , which gives

The quasi-optimal values are instead obtained assuming and are characterized by

| (118) |

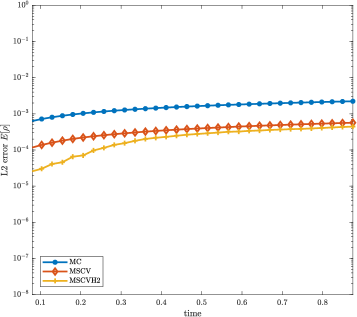

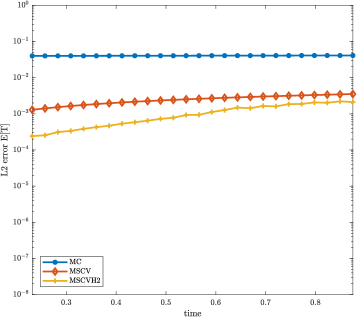

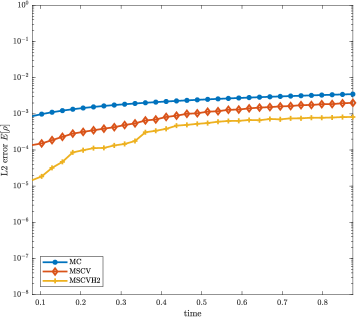

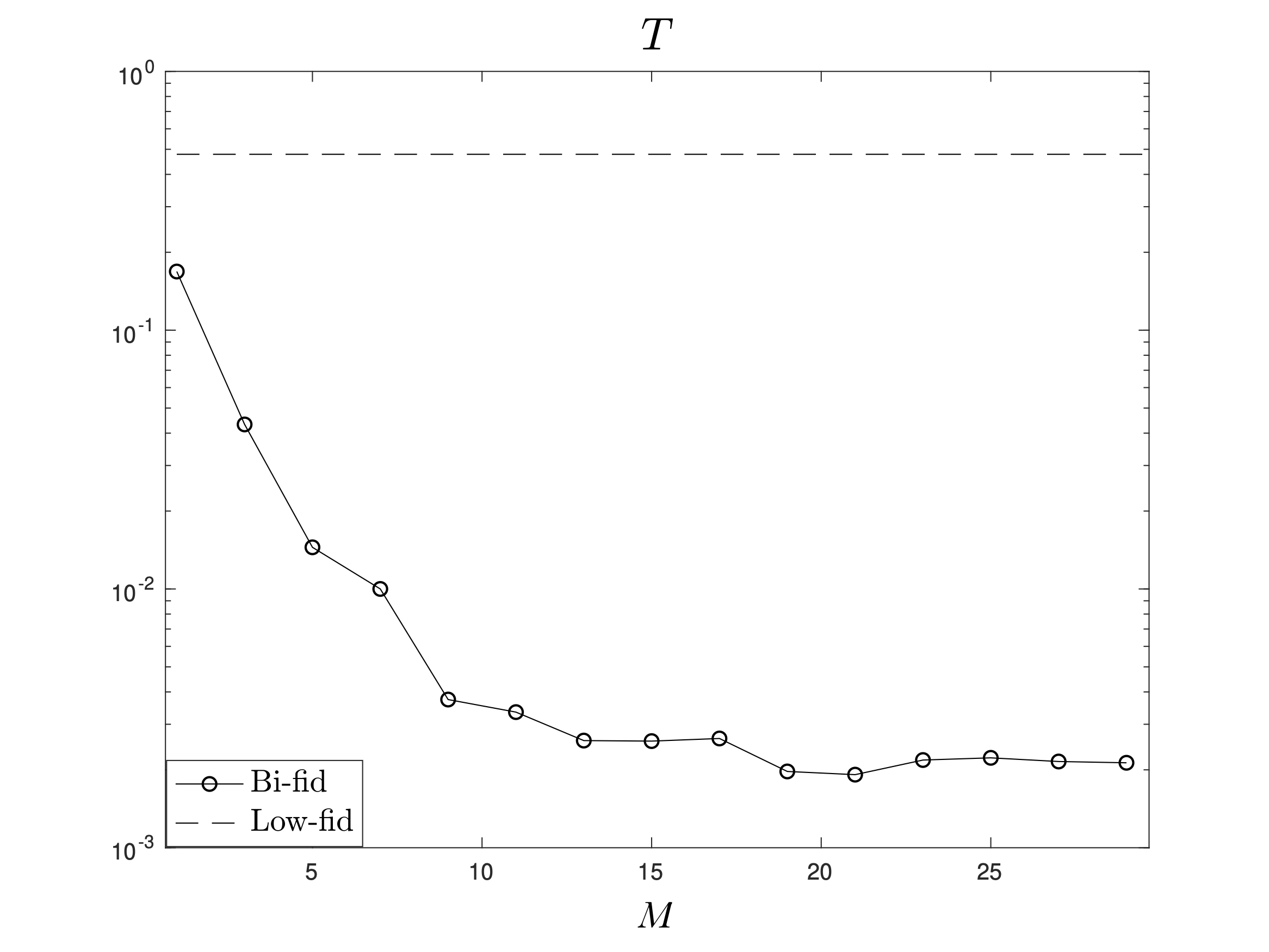

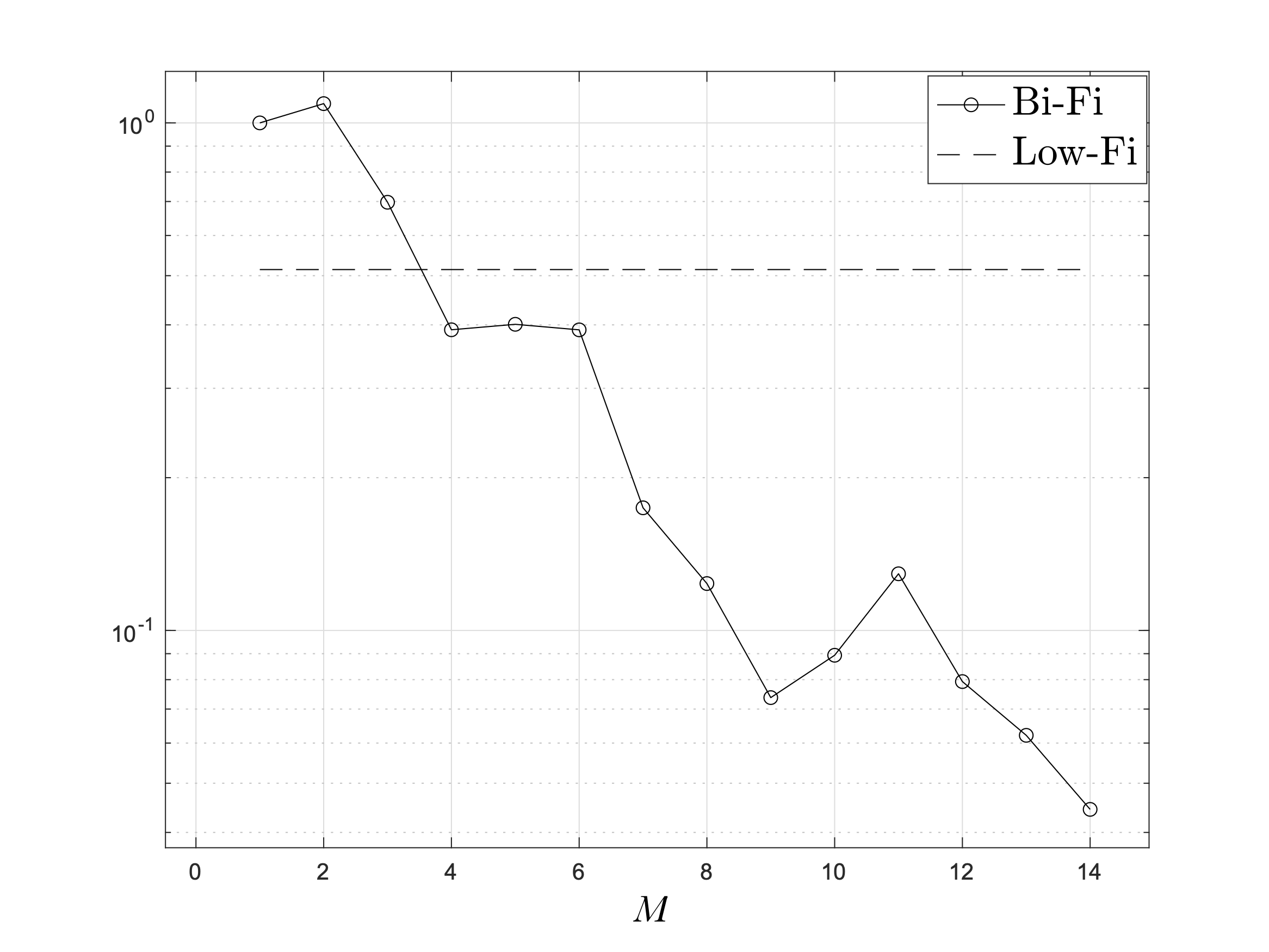

In Figure 6 we compare the results of the MSCV approach with two hierarchical levels (MSCHVH2) against the standard MC and the bi-fidelity MSCV method based on the BGK model discussed in Section 3.3.2. The initial conditions are given by Sod problem with uncertainty (3.3.2). The Boltzmann equation has been solved with the same discretization parameters as in Figure 3. For this situation, we perform three different computations corresponding to , and . The norms of the errors for the standard MC method, the MSCV approach and the MSCVH2 method for the expected value of the temperature and the density as a function of time are shown in the figure. The number of samples used for the BGK model is while for the compressible Euler system is . In all regimes the gain of the hierarchical two-level approach is remarkable and improves for smaller values of the Knudsen number.

3.6 Mean-field control variate methods

In this section we discuss two important issues that have remained open since the previous presentation of the MSCV method. Namely, how to couple the MSCV strategy with particle-based solvers in physical space, and how to extend the range of applicability of the methods to other kinetic equations where an equilibrium state is not known and thus the classical closure of rarefied gas dynamics cannot be adopted.

As a prototype example to develop our arguments, we will consider the Boltzmann model for socio-economic interactions with uncertainty introduced in Section 2.2.

3.6.1 The DSMC method for kinetic equations.

Let us first recall the classical Direct Simulation Monte Carlo (DSMC) method for the solution of the Boltzmann equation [9, 65] in case without uncertainty. We are in particular interested in the evolution of the density solution of (21) with initial condition . The DSMC method in the form originally proposed by Nanbu [65] is reported in Algorithm 3.5. We refer to [71, 88, 74] for an introduction to Monte Carlo methods for kinetic equations.

-

1.

Let us consider a time interval , and let us discretize it in intervals of size .

-

12.

Compute the initial sample particles ,

| for | to | |||

| given | ||||

| set (stochastic rounding) | ||||

| select pairs uniformly among all possible pairs, | ||||

| - | perform the collision between and , and compute | |||

| and according to the collision law (18) | ||||

| - set , | ||||

| set for all the particles not selected | ||||

| end for |

The kinetic distribution as well as its moments are then recovered from the empirical density function

| (119) |

where is the the Dirac delta and are the samples of particles at time . For any test function , if we now denote by

we have

| (120) |

Hence, by assuming that we have that , where is the expectation of the observable quantity with respect to the density to be distinguished from used to denote the expectation in the random space of uncertainties. Thanks to the central limit theorem we have [12]

Lemma 3.2.

The root mean square error is such that for each

| (121) |

where with

| (122) |

While the moments of the distribution can be easily computed via (120) if one is interested in the shape of the distribution function one must do an appropriate reconstruction. For example, one can operate as follows: set up a uniform grid in where each cell has width and subsequently define a smoothing function such that

Then, the approximation of the empirical density (119) is obtained by

| (123) |

In the simplest case, , where is the indicator function, (123) corresponds to the standard histogram reconstruction. Then, the numerical error of the reconstructed DSMC solution (123), can be estimated from

as [76]

Theorem 3.6.

The error introduced by the reconstruction function (123) satisfies

| (124) |

where depends on the derivative in velocity of and is given by

| (125) |

3.6.2 The combined MC-DSMC method for uncertainty quantification.

Let assume , , solution of a PDE with uncertainties only in the initial distribution , . The MC sampling method for the uncertainty quantification has been formulated in Section 3.2. The only difference with respect to (49) is the way in which the deterministic kinetic equation is solved since here a DSMC method is used.

The empirical kinetic distribution in presence of uncertainty is given by

being the samples of the particles at time such that .

While the algorithm is similar to the deterministic case, the error analysis is different and the following result holds true [76]

Lemma 3.3.

The root mean square error of the MC-DSMC method satisfies

where and with .

Let us now consider the reconstructed distribution with uncertainty

| (126) |

and let us focus on the accuracy of the expectation of the solution . One can give, using

the following estimate [76]

3.6.3 Mean Field Control Variate DSMC methods

In order to improve the accuracy of standard MC sampling methods, we introduce a class of mean field control variate methods playing the role of the low-fidelity model. The key idea is to take advantage of the reduced cost of the mean field model which approximates the asymptotic behavior of the original Boltzmann model. More precisely we consider two different control variates strategies obtained by the mean field approximation: the direct numerical solution of the mean field model and its corresponding steady state. In the sequel most of the analysis is reported for a general quantity of interest .

Let us denote by the solution of the mean field model (22) complemented by the same initial distribution of the high fidelity model. As discussed in Section 2.2 for small values of the scaling parameter we have

being solution of the high-fidelity Boltzmann model (21). Therefore, also the equilibrium distribution is such that

In this setting, the parameter dependent control variate method with can be formulated introducing the quantity

| (129) |

By the same arguments as in Section 3.3 we can state also the following

Theorem 3.8.

The optimal value which minimizes the variance of (129) is given by

| (130) |

where denotes the covariance. The corresponding variance of is then

| (131) |

where

is the correlation coefficient between and . In particular, we have

Of course, the control variate formulation in (129) can be modified using the steady state of the mean-field model (22)

| (132) |

Then, for the mean field control variate steady state (132), a similar results holds in the large time limit, as the ones shown in Theorem 3.8.

Let us now give the details of the Mean Field Control Variate (MFCV) algorithm. To that aim, we recall that using realizations of our random variable to define the Mean Field Control Variate (MFCV) estimator, we have

where denotes the exact value of the expectation of the quantity of interest or its numerical approximation with negligible error. Furthermore, we have the following notations

being and the solutions of the Boltzmann-type and the mean-field models, respectively, relative to th realization of the random variable . The corresponding MFCV algorithm based on a DSMC method is reported in Algorithm 3.6.

-

1.

Sampling: Sample independent identically distributed (i.i.d.) samples of the initial distribution , from the random initial data .

-

2.

Solving: For each realization ,

-

3.

Estimating:

-

(a)

Estimate the optimal value of at time by

which in the mean field steady state control variate case becomes

-

(b)

Compute the the expectation of any quantity of interest of the random solution field with the mean-field control estimator

-

(a)

Concerning the evaluation of moments, by ignoring the error term due to the approximation of , we have the following [76]

Lemma 3.4.

The root mean square error of the MFCV-DSMC method satisfies

| (133) |

where and with .

In the case of the reconstruction function (126), we have

where the first term is bounded as in Theorem 3.7 and the second term can be bounded using Lemma 3.4 with . Thus we have the following result.

Theorem 3.9.

As a consequence when the solution of the high-fidelity model is close to the solution of the control variate the statistical error due to the uncertainty vanishes. This justifies the use of a large number of samples in the velocity space in agreement with the reconstruction used in order to balance the last two error terms in (134).

3.6.4 Application to socio-economic sciences

We present two numerical examples concerning kinetic models in socio-economic sciences. We will denote by MFCV-S the case where the steady state of the mean-field model is analytically known and is used off line as control variate and by MFCV the case where the Fokker-Planck equation (22) is numerically solved and used as a time dependent control variate. The mean field model is solved by the second order structure preserving method for nonlocal Fokker-Planck equations developed in [77]. The solutions are averaged over runs to reduce statistical fluctuations. In order to compute with negligible error we adopt a stochastic collocation approach with collocation nodes.

We first consider the kinetic model for opinion formation (23) with uncertainties present on the initial distribution or on the interaction strength. We assume that and the initial distribution is given by

| (135) |

We also assume

| (A) |

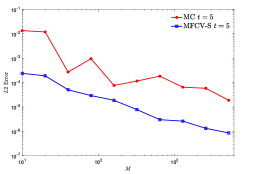

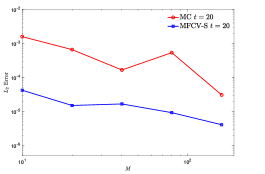

and thus we obtain a steady state of the Fokker-Planck equation of the form given by (25). The Boltzmann equation is solved with particles. The number of grid points of the mean field model is set to and the number of samples we have chosen is which correspond to a computational cost comparable to for the Boltzmann solver. In Figure 7 (left) we report the error of the expected density obtained by the standard MC and MFCV-S methods for increasing number of samples at time . We obtain an improvement in accuracy for the MFCV-S between one and two orders of magnitude using the same number of samples.

As a further case for opinion dynamics we consider the kinetic model (23) with

| (B) |

so that the resulting steady state of the Fokker-Planck model is the Maxwellian-like distribution (24). The initial data in this case is (135) in the deterministic setting . In Figure 7 (right), we report the error of expected probability distribution function computed by the MC and MFCV-S method at the final time for different number of samples. As in case (A) we obtain an improvement between one and two orders of accuracy for the MFCV-S method compared to the classical MC method.

We study now two test cases related to the wealth exchange CPT model defined by (26). First, we consider uncertainty in the initial condition and secondly in the saving propensity. The computational domain is the interval . Let us first consider and the initial distribution defined by

| (136) |

Furthermore, we consider

| (C) |

so that the large time behavior of the Fokker-Planck model is given by (27) with . As a second case, we consider uncertainty in the interaction

| (D) |

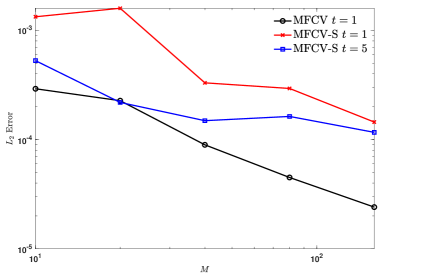

The initial condition is uniformly distributed on , so that the large time behavior of the Fokker-Planck model is given by (27) with . The DSMC solver for the Boltzmann model uses particles. For the mean field scheme instead we consider and we choose which gives a comparable cost of the full Boltzmann solver for .

In Figure 8, we compare the error of computed by the MFCV or MFCV-S method at fixed times but for different number of samples . We obtain that the error of the expected probability distribution function of the MFCV-S method is considerably smaller at larger times. In comparison to the MFCV-S method, MFCV method is able to be more accurate even at early times.

4 Bi-fidelity stochastic collocation methods

In the examples of multi-fidelity models that were discussed in the previous section, high-fidelity samples are not selected based on any criteria other than the fact that they are small in number compared to low-fidelity samples. Here, following [55, 30, 54, 6] we explore a different direction and we focus on stochastic collocation methods based on bi-fidelity algorithms. The main idea is that within the bi-fidelity approximation, one employs the cheap low-fidelity model to explore the random parameter space and to select the most important parameter points in this space. After that, by applying exactly the same approximation rule learnt from the low-fidelity model, one solves the high-fidelity model. Following the above idea, we first review the BFSC methods in its generality. After we focus on its application to efficient uncertainty quantification for the Boltzmann equation of Section 2.1, the linear transport equation of Section 2.3 and finally the epidemic transport models of Section 2.4.

4.1 A Bi-fidelity stochastic collocation (BFSC) algorithm

To set the stage for the discussion, we first introduce basic notions in the following. We let be the solution of a complex system subject to uncertainty, where and are the spatial and temporal variables. is a -dimensional random variable. Here is the support of , where the probability distribution is defined. For the sake of simplicity, we denote by when from the context the dependence on the other variables will be clear. Let us assume now the high-fidelity solutions and low-fidelity solutions are available. Let also be the number of affordable low-fidelity simulation runs, which, in principle, is very large due to the reduced complexity of the model. On the other hand, denotes the number of high-fidelity simulation runs that can be afforded and it is typically very small, i.e. the setting is such that . Note that in this section, to simplify notations, we will use to denote the number of samples used by the low-fidelity model instead of as in Section 3.3. Let finally , be a set of sample points in .

We denote by the low-fidelity snapshot matrix corresponding to the solution of the low fidelity model for the sample point . To this matrix we can associate a corresponding low-fidelity approximation space, i.e. the space spanned by the set of sample points ,

Similarly, the high-fidelity snapshot matrix, i.e. the matrix obtained from the sample set , and the corresponding high-fidelity approximation space, i.e. the space spanned by the solutions computed at nodes , are defined as follows:

The main idea of the BFSC method is to construct an inexpensive surrogate of the high-fidelity solution in the following non-intrusive manner

| (137) |

where is expected to be the number of high-fidelity samples and where correspondingly is a subset of size of the sample space of size . In other words, we approximated the solution of the high fidelity model in the space spanned by . When constructing such algorithm one seeks for to be as small as possible, since large means more high-fidelity simulations and consequently prohibitive computational efforts. Thus, the central idea of the BFSC algorithm is to use cheap low-fidelity models to learn the coefficients in (137), and then apply the same approximation rule to a limited number, but selected, of high-fidelity samples to construct the bi-fidelity approximations of high-fidelity samples.

The BFSC algorithm for approximating the high-fidelity solution consists of offline and online stages. In the offline stage, we employ the cheap low-fidelity model to explore the parameter space to find the most important parameter points, i.e. a small number of samples permitting to give a suitable approximate solution. During the online stage, we learn the approximation rule from the low-fidelity model for any given , and apply it to construct the bi-fidelity approximation. Thus, to construct the BFSC approximation in (137), one essentially needs to answer the following two questions:

-

—

How to choose a good collocation nodal set that results in a good approximation of the high fidelity solution in the random space?

-

—

How to recover the coefficients in an efficient manner? In other words, what is the efficient reconstruction algorithms that can be realized without resorting to an intensive use of the high-fidelity solver?

These two questions, if properly addressed, constitute the key to the efficiency and accuracy of the algorithm. We outline the key ideas in Algorithm 4.7.

-

1.

Offline stage

-

(a)

Select a sample set .

-

(b)

Run the low-fidelity model for each .

-

(c)

Select “important" points from and denote it by . Construct the low-fidelity approximation space .

-

(a)

-

2.

Online

-

(a)

Run high-fidelity simulations at each sample point of the selected sample set . Construct the high-fidelity approximation space .

-

(b)

For any given , run the low-fidelity model to get the corresponding low-fidelity solution and compute the low-fidelity coefficients by projection:

-

(c)

Construct the bi-fidelity approximation by applying the sample approximation rule learned from the low-fidelity model:

-

(a)

We address in the following the two main questions permitting to construct an efficient and accurate BFSC method: the proper point selection in the random space and the efficient construction of the bi-fidelity approximation.

4.1.1 Point selection.

To select the subset , we search the parameter space by the greedy algorithm proposed in [66, 106]: we gradually select the important point set from a candidate set . The method works as follows.

-

—

Start with a trivial subspace , and assume that the first important points have been selected.

-

—

We choose the next point as the point that maximizes the distance between its corresponding low-fidelity solution and the approximation space , spanned by the low-fidelity solutions on the existing point set , i.e.,

(138) where is the distance function between and subspace .

Thus, the greedy procedure essentially serves the purpose of searching the linear independent basis set in the parameterized low-fidelity solution space until all important points are selected. Let us remark that the whole algorithm allows an efficient implementation by standard linear algebra operations, if is chosen as squared Euclidean distance. Let be the Gramian matrix of the low-fidelity solution , i.e.,

| (139) |

where be an inner product space corresponding to the high-fidelity solution. Similar defintion holds for . We then apply the pivoted Cholesky decomposition to the matrix ,

| (140) |

where is lower-triangular and is a permutation matrix due to pivoting. This will produce an ordered permutation vector , from which we choose the first points to define . This procedure guaranteed that can can form a linearly independent collection [66]. More details and properties of the algorithm can be found in [66, 106]. We remark that other point selections strategies can be used in this setting [81].

4.1.2 Bi-fidelity approximation.

Once the important point set is selected, we can construct the low- and high-fidelity approximation space, and , respectively. For any given new sample point , we project the corresponding low-fidelity solution onto the low-fidelity approximation space :

where is the projection operator onto a Hilbert space and the corresponding projection coefficients are computed by the following projection:

| (141) |

where is the Gramian matrix of , defined by

| (142) |

These low-fidelity coefficients serve as the surrogate of the corresponding high-fidelity coefficients of . Therefore, the sought bi-fidelity approximation of can be constructed via (137). We emphasize that if the low-fidelity model can mimic the variations of the high-fidelity model in the parameter space, the low-fidelity coefficients can be a good approximation of the corresponding high-fidelity coefficients for a given sample . The whole procedure of the bi-fidelity algorithm for a given is summarized in Algorithm 4.7. It is worth noting that since the number of low-fidelity basis is typically small, the cost of computing the low-fidelity projection coefficients by solving the linear system (141) is negligible. Therefore, the dominant cost of the online step is one low-fidelity simulation run. If the low-fidelity solver is much cheaper than the high-fidelity solver, the speedup during the online stage can be significant as we will demonstrate with some examples in the rest of the survey.

4.1.3 An empirical error bound estimation.

An error bounds analysis for the bi-fidelity method was derived in [66, 105] in a rather general setting. Nonetheless, the results presented are largely theoretical. For practical applications of the BFSC approach, it is important to answer the following two questions:

-

—

Given a low-fidelity model, is this model good enough to build a reasonably accurate BFSC approximation for practical purposes?

-

—

How to efficiently estimate a reasonably good error bound on the entire parameter space?

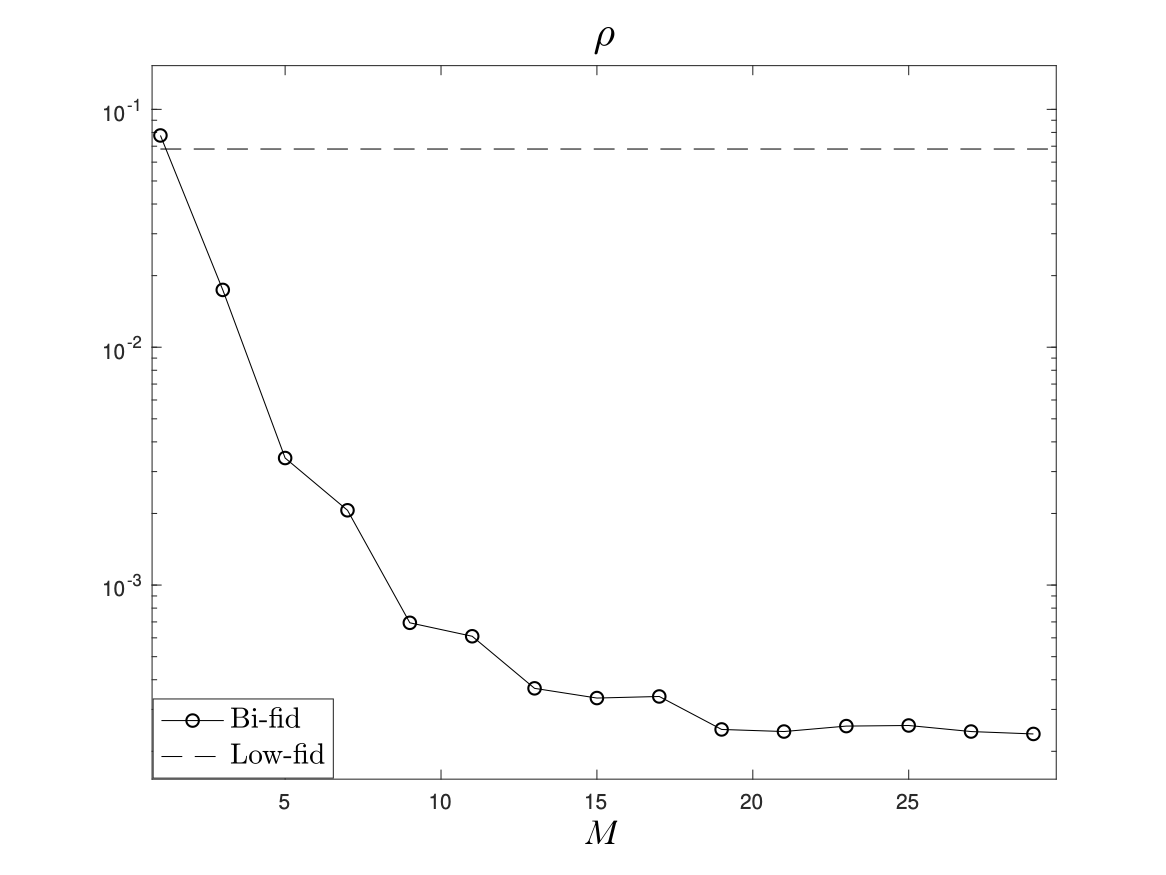

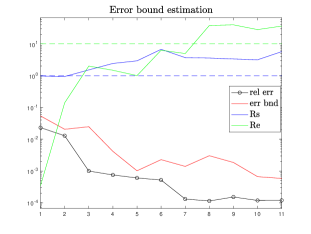

In other words, an inexpensive but effective quality indicator (EQI) of the approximation is of practical importance. In realistic applications, a priori assessment of the model quality and prediction errors is very important. In this direction, a previous study [32] introduced a novel empirical error bound estimation approach with ease of implementation to evaluate the performance of the bi-fidelity surrogates a priori. We will briefly describe the methodology here. In [32], two important quantities have been identified which are useful to build the approximation quality indicator for the BFSC approximation:

-

—

, model similarity which characterizes the similarity between the low/high-fidelity models:

(143) If , the low-fidelity model is informative for the point selection.

-

—

, the ratio between the projection error and the distance error,

(144) when is too large, it indicates the greedy algorithm is less effective for point selection of high-fidelity samples. This suggests that one should stop collecting new high fidelity samples since the improvement in the result is likely marginal.

Empirically, one can than fix thresholds for and in such a way that the BFSC approximation can usually deliver results which are reasonably accurate, i.e. better than the low-fidelity solutions.

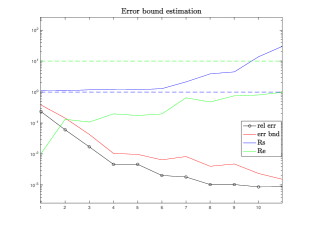

Using and the observation in [32, Theorem 1], for any given new point , one has

| (145) |

To remove the dependency of the new HF sample on the above right-hand side, one uses as the testing points served as an error surrogate for the BFSC approximation in the entire parameter space. If the LF and HF models are similar (i.e., ), one can choose some proper constants and , such that for the first pre-selected important points ,

| (146) |

Notably, in the right-hand side of the inequality, the first term only depends on the inexpensive low-fidelity data and the second term needs the high-fidelity solution at – the -th point of the pre-selected important points without the need of the high-fidelity sample for a new given . Essentially, can be regarded as a test point to serve as an error/quality indicator of the BFSC approximation in the entire parameter space. This can be advantageous if the high-fidelity solver is very expensive.

We acknowledge that the above error bound estimation, though not rigorous, is a useful quantity to access the quality of the BFSC approximation in practical applications. In the following numerical experiments, our empirical results suggest that this error bound estimation is effective if the constants and are set to be 1 [32, 54].

4.2 A BFSC method for the Boltzmann equation

In this section, we consider the application of the bi-fidelity algorithm to the study of the the Boltzmann equation under the hydrodynamic scaling and with multi-dimensional random parameters presented in Section 2.1 and already analyzed in Section 3 using MSCV method.

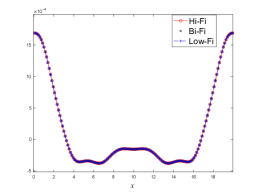

To examine the performance of the bi-fidelity method, numerical errors are computed in the following way: we choose a fixed set of points that is independent of the point sets , then evaluate the following error between the bi-fidelity and high fidelity solutions at a final time :

| (147) |

where is the norm in the physical domain . In the following two examples, the spatial domain is chosen to be with grid points. The velocity domain is chosen as with . We denote and as the number of grid points used in velocity discretization of the low-fidelity and high-fidelity solver respectively. The -dimensional random variable is assumed to follow the uniform distribution on . Let also the size of training set be . We examine the error of bi-fidelity approximation with respect to the number of high-fidelity runs by computing the norm defined in (147).

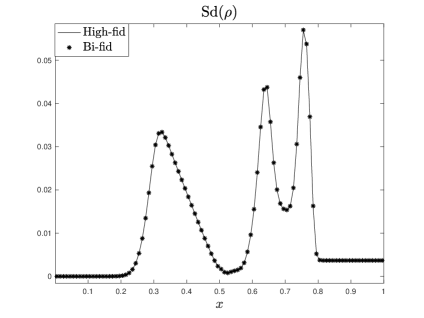

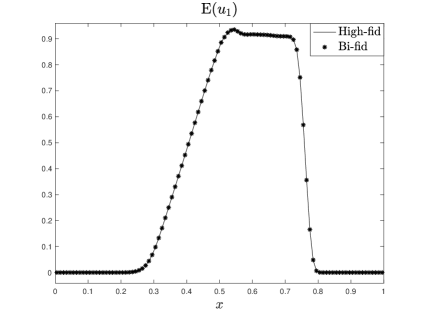

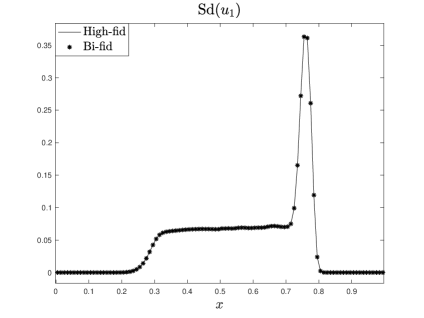

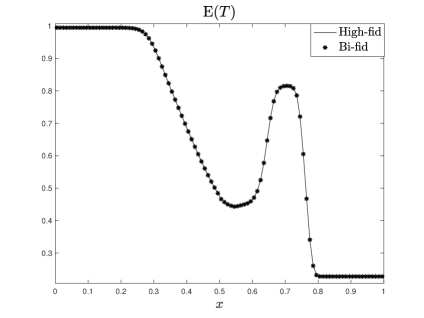

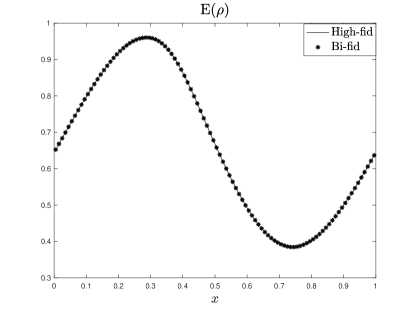

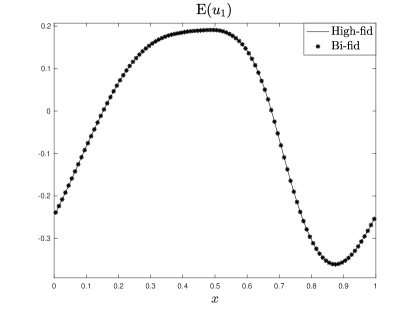

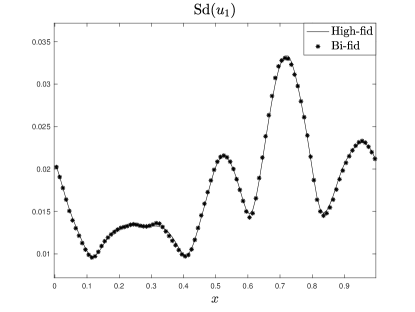

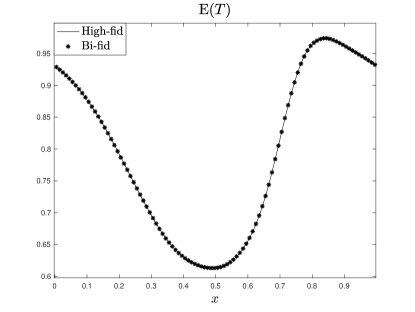

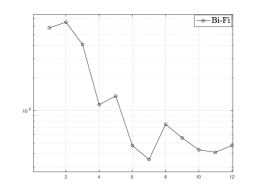

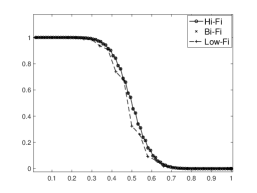

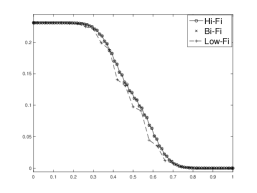

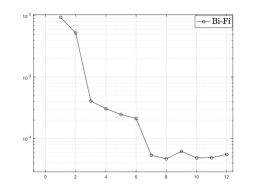

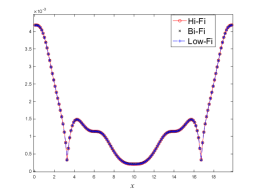

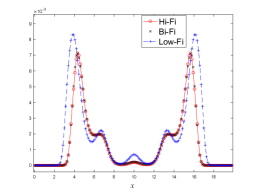

First, we consider a benchmark Sod shock tube test. Assume the random cross section

and the uncertain initial distribution given by

where the initial data for , and is