Inequality in economic shock exposures across the global firm-level supply network

Abstract

For centuries, national economies created wealth by engaging in international trade and production. The resulting international supply networks not only increase wealth for countries, but also create systemic risk: economic shocks, triggered by company failures in one country, may propagate to other countries. Using global supply network data on the firm-level, we present a method to estimate a country’s exposure to direct and indirect economic losses caused by the failure of a company in another country. We show the network of systemic risk-flows across the world. We find that rich countries expose poor countries much more to systemic risk than the other way round. We demonstrate that higher systemic risk levels are not compensated with a risk premium in GDP, nor do they correlate with economic growth. Systemic risk around the globe appears to be distributed more unequally than wealth. These findings put the often praised benefits for developing countries from globalized production in a new light, since they relate them to the involved risks in the production processes. Exposure risks present a new dimension of global inequality, that most affects the poor in supply shock crises. It becomes fully quantifiable with the proposed method.

Interconnected supply chains forming complex networks span the globe as a consequence of centuries of globalization Chase-Dunn et al. (2000). International production and trade played an essential role in increasing economic growth Frankel and Romer (1999); Pavcnik (2002); Ventura (2005), reducing global income inequality, especially due to above average growth in China and South Asia Firebaugh and Goesling (2004), and has been argued to positively affect sustainable development Xu et al. (2020). Previous studies also argued that international production can have negative effects. Globalization allowed firms to execute strongly polluting tasks abroad Oita et al. (2016); Zhang et al. (2017); Peters et al. (2011); Wiedmann and Lenzen (2018) and to outsource labor intensive tasks to countries with weaker labor-rights Fernández and Sotelo Valencia (2013); Blackstone et al. (2021) or unsafe or violent working conditions Hobson (2013); Bolle (2014); Butt et al. (2019). International trade creates demand for and facilitates the spread of problematic goods such as conflict minerals Mizuno et al. (2016). Importantly, international trade relations also act as direct and indirect transmission channels for economic shocks, such as supply or demand reductions Gephart et al. (2016); Starnini et al. (2019); Klimek et al. (2019); del Rio-Chanona et al. (2020).

Several recent works show that production networks act as transmission channels for economic shocks. A study on natural disasters in the United States Barrot and Sauvagnat (2016) finds substantial evidence that shocks propagate from suppliers to customers. Similarly, shock spreading on the firm-level production network subsequent to the Great East Japan Earthquake 2011 has been estimated to have caused a drop in 2.4% of GDP, more than 100 times more than the immediate direct losses Inoue and Todo (2019). In a similar study, the effect of the Great East Japan Earthquake has been estimated to have caused a significant 0.47 percentage point decline in Japan’s real GDP growth Carvalho et al. (2021). In the short term, some firms were affected orders of magnitude stronger. Further, the Great East Japan Earthquake also provided evidence for the cross-country spread of economic shocks. Using firm-level data Boehm et al. (2019) shows that close affiliates of Japanese corporations in the USA experienced large drops in output in the months following the earthquake.

So far, risks of international economic shock propagation are typically studied on highly aggregated flows of goods between countries Lee et al. (2011); Gephart et al. (2016); Starnini et al. (2019); Klimek et al. (2019); del Rio-Chanona et al. (2020). However, the intricate topology of the firm-level global supply network has a potentially crucial role for how economic shocks spread across countries. The importance of knowing the detailed network topology for understanding the spreading of shocks has been shown extensively in the finance literature. Shock propagation mechanisms were first developed for financial networks, consisting of banks and liabilities between them Boss et al. (2004); Iori et al. (2008); Battiston et al. (2012); Thurner and Poledna (2013); Diem et al. (2020); Pichler et al. (2021). The potential of a local disruption, e.g. the default of a single bank, causing a system-wide large disruption in a financial network (financial crisis) is called its systemic risk. A full assessment of the exposures created by a financial agent and thus its systemic risk contribution to the system is not just given by its size (i.e. the sum of its direct exposures), but depends crucially on its position in the network. Reasonable quantification of systemic risk involves the detailed knowledge of financial networks; A particularly practical quantity (network centrality measure) is the DebtRank Battiston et al. (2012); Thurner and Poledna (2013); Bardoscia et al. (2015); Poledna et al. (2015) that relates the failure of a bank to the caused systemic losses.

Only recently, these ideas were applied and generalized to the real economy and supply networks Fujiwara et al. (2016). In networks formed by the supply-demand interactions between firms, the default of a single company may cause –through cascading dynamics– disruptions in large parts of the system. A corresponding Economic Systemic Risk Index was developed specifically for production networks Diem et al. (2021). In a similar direction, agent-based-modelling approaches for estimating the economic cost of the failure of a group of firms, known as regional adaptive input output models, have been developed in the context of (natural) disaster impact assessment Hallegatte (2008); Inoue and Todo (2019); Krichene et al. (2020); Markhvida et al. (2020).

Works of this kind demonstrate that network effects on the firm level are relevant and are too large to be ignored. The standard approach of quantifying exposures is the input-output (IO) analysis on the sector-level. There, all networks below the sector level are ignored. Illustrative examples of shock spreading on the single firm level are the global shortage in hard drives subsequent to the 2011 flood in Thailand Haraguchi and Lall (2015), or the ongoing shortage in computer chips Sweney (2021); Isidore (2021). In the wake of the COVID-19 crisis, the distress of one firm –Taiwan Semiconductor Manufacturing Company, Limited– lead to production interruptions and layoffs in companies on the other side of the globe, e.g. in European and US car manufacturers Waldersee (2021); Williams and Bushey (2021).

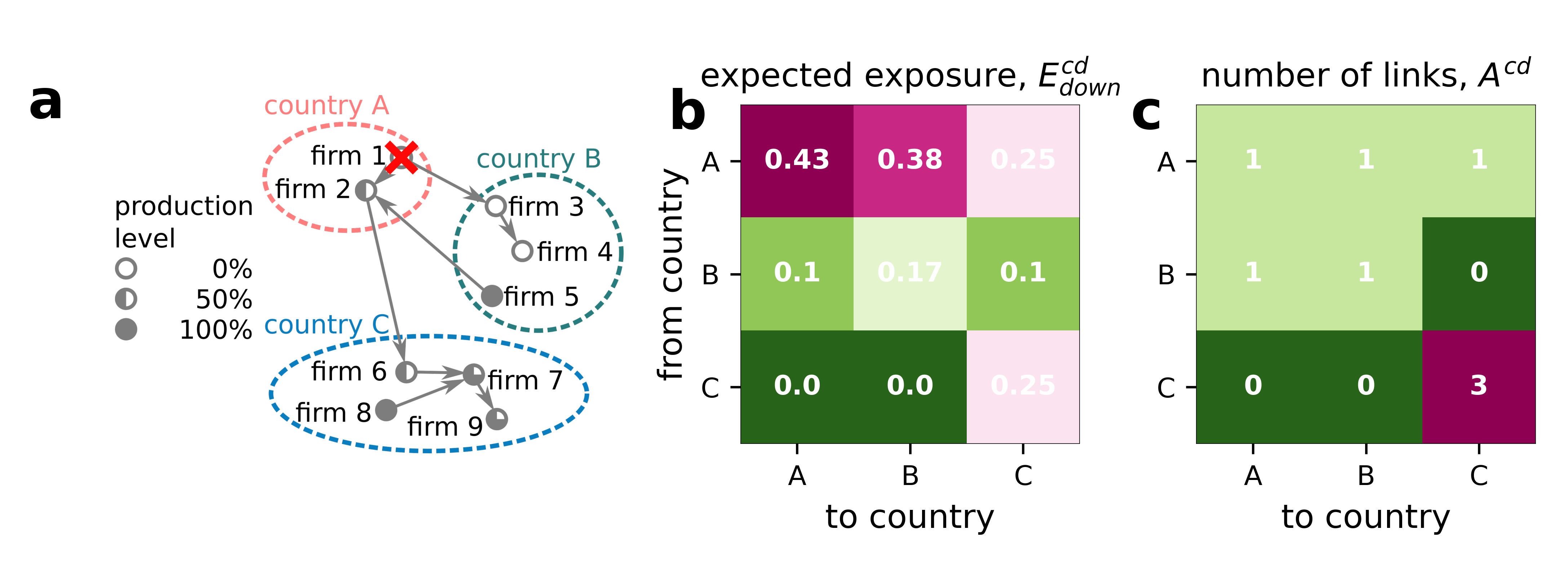

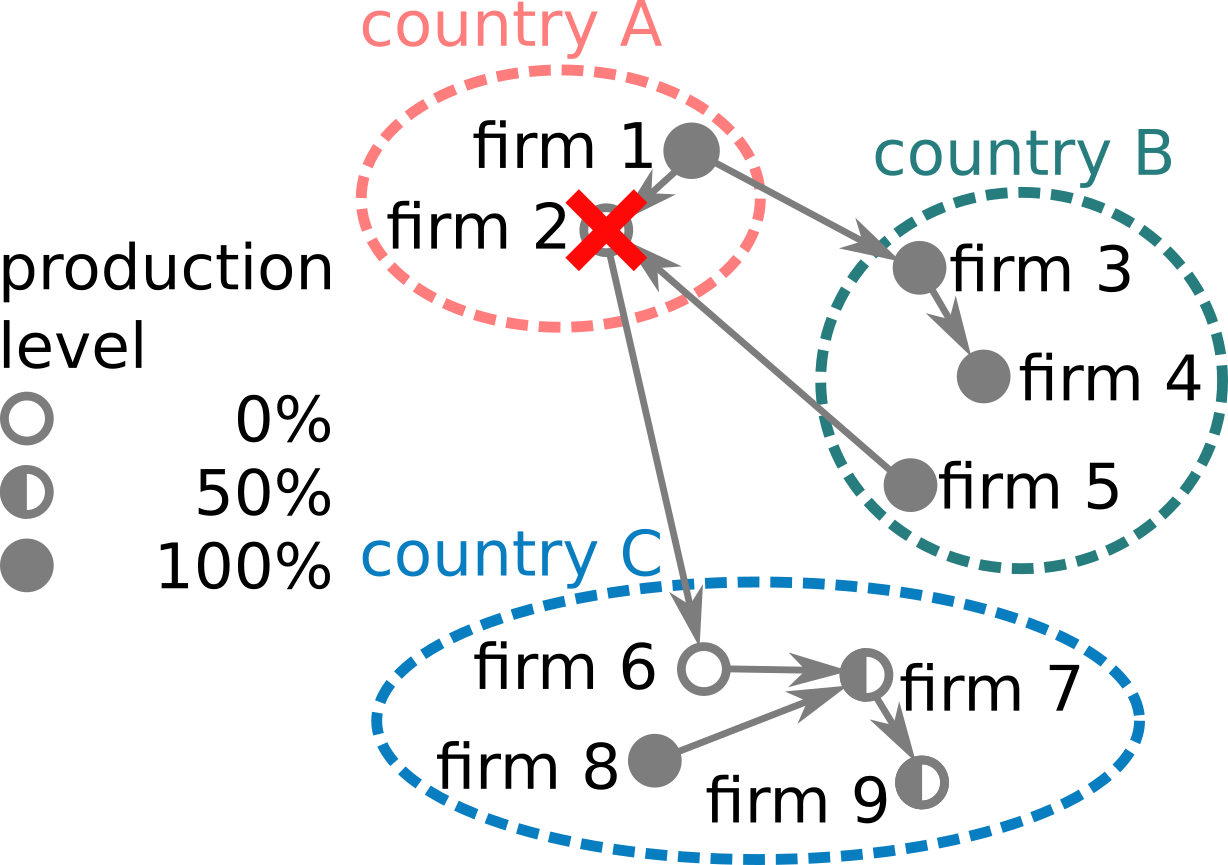

The underlying principle of the above approaches is the understanding of shock propagation on the underlying economic networks in combination with the corresponding actual economic mechanics. Note that there are important differences between financial and production networks. In the former links (assets and liabilities) are stock quantities, while in the latter links represent traded goods and services which are flow quantities. In this work we focus on production networks and their systemic risks only. In Fig. 1a we show the situation for a cascading failure in an international production network subsequent to the failure of an initial node, firm 1, marked by the red cross. Because firm 1 will no longer produce any goods, it cannot supply inputs to firms 2 and 3, so they have to reduce their production as well and cannot supply to their customers (ignoring potential substitution effects). Iterating this logic leads to a new stable configuration of reduced production levels shown in Fig. 1a. The filling of the nodes mark the reduction in economic activity (production). In the case of a supply shock, we call this mechanism the downstream propagation of shocks or the downstream cascade. The same logic applies to demand reductions that propagate upstream, or equivalently, cause an upstream cascade (not shown).

The argument that all involved parties benefit from international trade dates back to David Ricardo’s theory of comparative advantage Ricardo (1891). However, because trade links can act as channels for shock transmission in production networks, it exposes firms and countries to risks they usually can neither assess, nor control. Therefore, quantitative measures are needed that allow us to compare the benefits with the inherent production risks of a globalized economy. Here we develop a novel measure to quantify a country’s exposure to economic shocks from international production and trade, based on a microscopic shock propagation mechanism. It is an estimate for the expected economic loss a country is exposed to if an arbitrary firm fails in another country. As such it is also a novel measure for a country’s resilience to supply network shocks originating in other countries. For this, we define the direct exposure to be the production losses caused by a (temporary) production failure of a direct supplier (customer) firm. Indirect –or, equivalently, higher order– exposures result from the propagation of the direct shocks along indirect supply relations (supplier of a supplier and so forth). In the following, the term ‘exposure’ refers to the sum of direct and indirect exposures. We can then quantify differences in the countries’ risk exposures, and discover how these exposures are distributed across the globe. The estimated exposures can then be put into perspective with measures of gains from globalized production and trade. We focus on an accurate description of international economic shock propagation and compare the exposure to direct and indirect production losses with GDP growth, as a straight forward proxy for profits from globalized production and trade.

We use a global firm data set, see Materials and Methods, as a starting point to reconstruct an international firm-firm supply network. We use it to compute a number different exposures, based on the concept of DebtRank, see SI Text 1. While DebtRank in its basic form quantifies the systemic relevance of a node by aggregating the losses it could cause in the entire network, here we generalize it such that the systemic relevance of firms to specific countries can be quantified. We thus adapt the cascading mechanism underlying on supply networks in Fujiwara et al. (2016) to quantify the effect of the failure of each single firm on every national economy. We define the following quantities:

The Country-Firm Exposure, , of country to firm , quantifies the fraction of the national production of country, , that is lost in case of firm ’s failure. This includes direct and indirect shocks transmitted through the network; for details, see Materials and Methods. We define the Country-Country Exposure, , as the expected exposure of a country to production losses originating from random firm failures in country . Assuming that the default probability for firm is , it is calculated by forming the expectation values over all production losses, , where is located in country and is the number of firms in country . Lacking information on firm default probabilities, we assume equal for all firms in a country. Note that the expected exposure, , measures the robustness of country to shocks from country , low (high) values imply high (low) robustness. measures a country’s relative production reduction. For absolute numbers, we define a country’s Country-Country Exposed Value, , by multiplying the relative expected exposure with the economic size of the affected country, . We approximate a firm’s size by its number of links, , and the economic size of a country by the sum of its firm-sizes, the total degree, . To distinguish between up- and downstream effects, we define the above measures for both up- () and downstream () separately. We define the total (imported) exposure as .

We exemplify the quantities by calculating them for the toy example in Fig. 1a. The default of firm 1 causes production in country B to drop by . The default of firm 2, as shown in SI Fig. S1, SI Text 2, has no effect on country B, . If we randomly pick a firm in country A, now the expected country exposure is the average of the two firms . Figure 1b shows the matrix for the toy network in panel a; dark magenta means high, green means low exposures, respectively. Country A creates the most risk, affecting B and C; C creates the lowest, affecting only itself. For every row the highest value is found in the diagonal, highlighting that firms within countries expose each other stronger among themselves than between countries. The comparison of in Fig. 1b with the number of links between countries in Fig. 1c indicates that the systemic risk spreading dynamics contains a lot of effects that are not visible when only considering the links between countries. Both for directly and indirectly connected countries, much of the heterogeneity in shock spreading is lost when ignoring the firm-level network topology. The information loss by aggregation is best seen when comparing different realizations of the firm-firm level supply network, , that have the same country-level aggregation, . For example, if we rewire the outgoing link of firm 5, such that it now supplies firm 2 instead of firm 1, we preserve the number of links between countries , but the exposure of countries A and C to B would be substantially larger than compared to the situation shown in Fig. 1.

Results

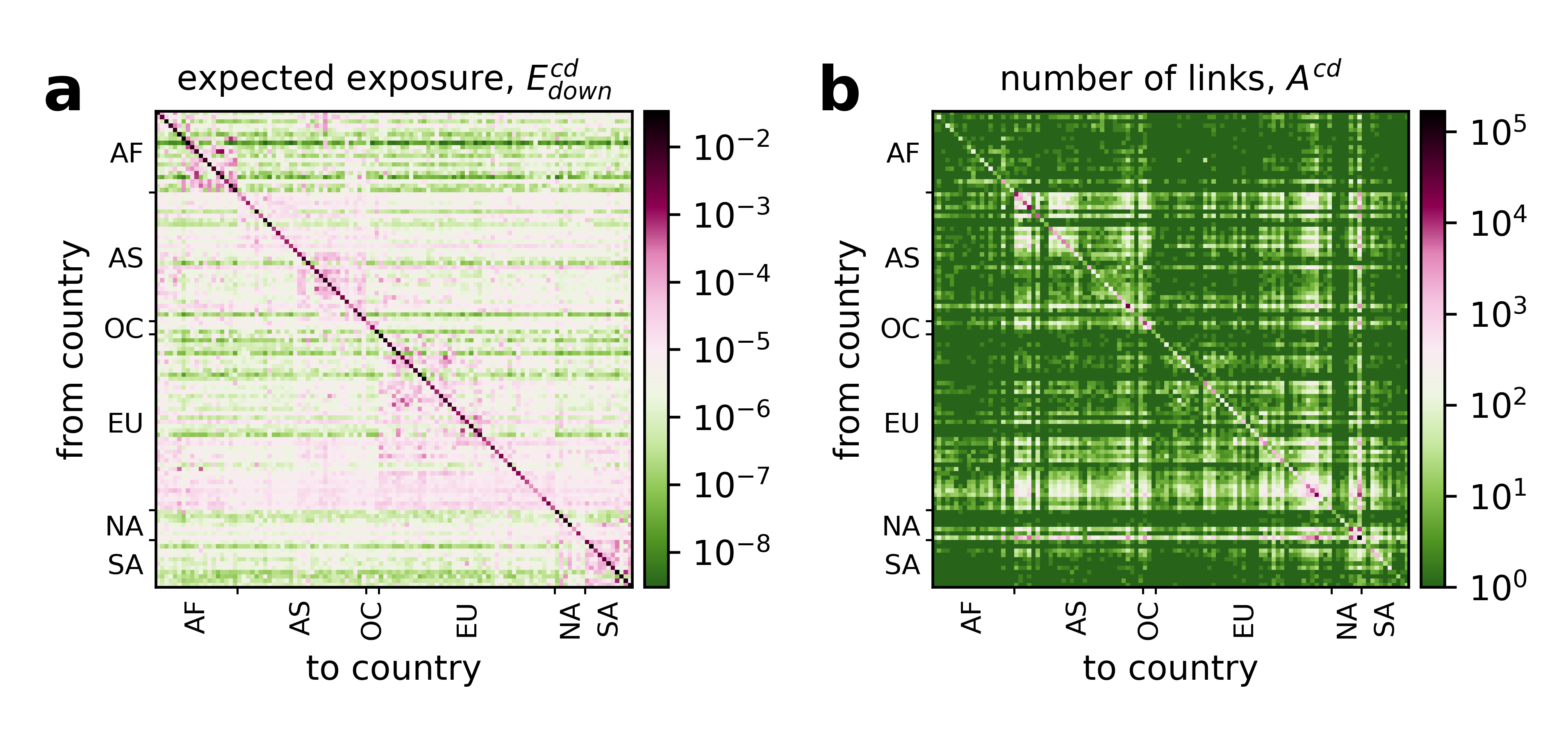

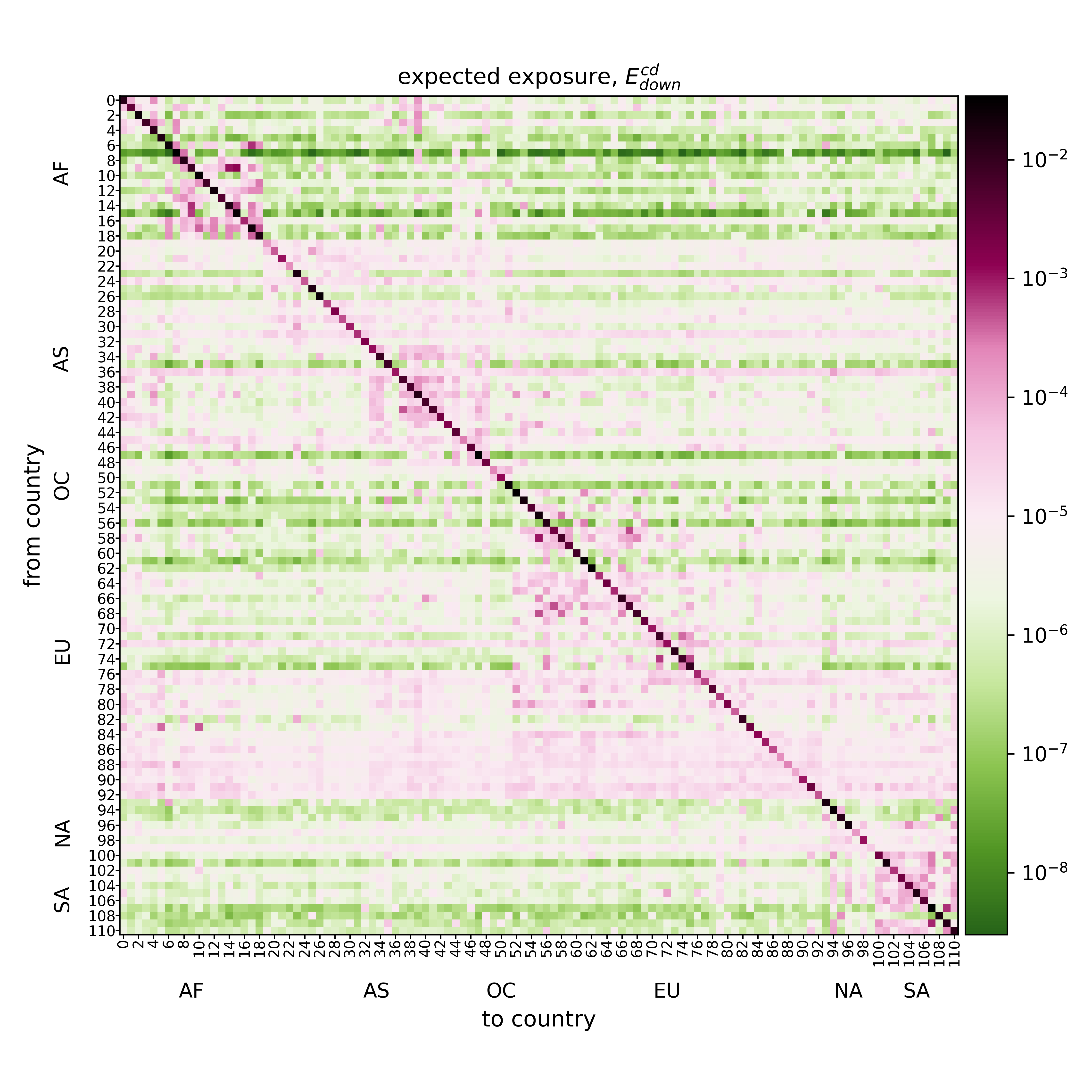

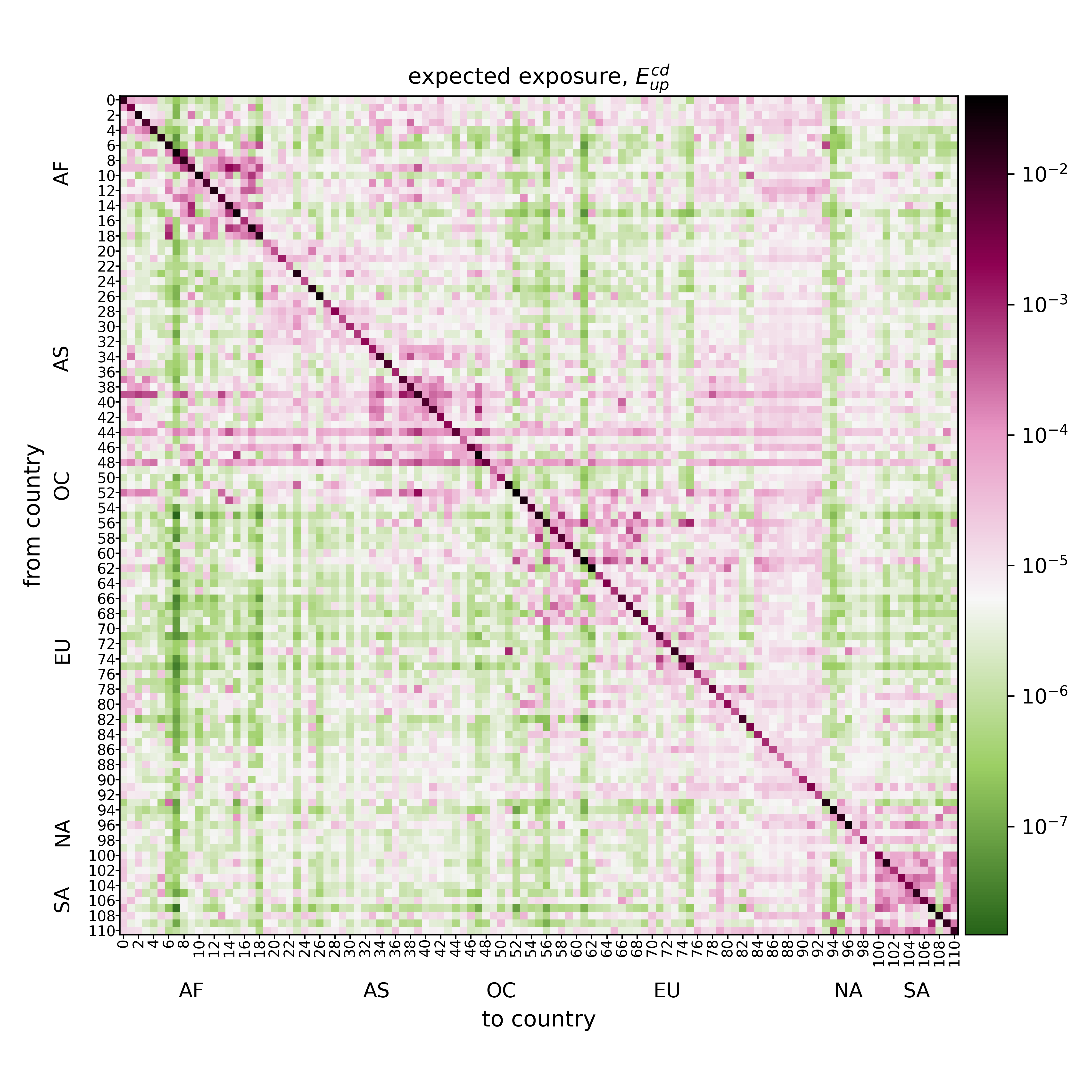

First we analyze the network structure of the expected exposure between countries, . We find that country country exposures cluster in geographic regions. We see this by sorting the countries according to regions and continents in Fig. 2. Figure 2a shows ; panel b shows the number of firm-firm links, , between countries and . Quantities are in logarithmic scale. The strongest connectivity and exposure is found within countries, as seen in the high values along the diagonal in the and matrices. The effect is much stronger for than for .

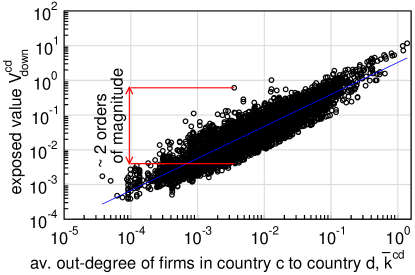

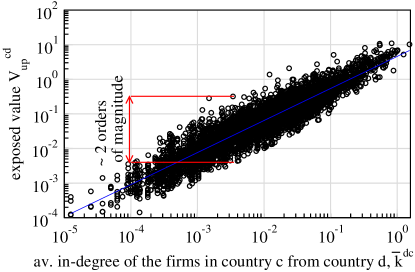

Economic exposure can be expected to be strong between countries in the same geographic or economic region, such as the European Union or the United States-Mexico-Canada Agreement. Figure 2a clearly shows a corresponding block-diagonal structure, highlighting closely connected regions on all continents, even differentiating between sub-regions, such as northern and sub-Sahara Africa. Further prominent blocks are seen in the middle east and south Asia, eastern Europe, in contrast to northern, southern and western Europe which expose almost all countries, and South America. The magenta colored horizontal lines in Fig. 2a indicate that some countries export downstream exposures to almost all other countries. They are particularly notable for a block of western European, several Asian and North American countries. Rich economies appear to expose countries beyond their own region. For a more detailed visualization and discussion of , containing single country indices, see SI Fig. S2 and SI Text 3. For , presented in Fig. 2b, these structures are only barely visible, except faintly for parts of Europe (EU), Asia (AS) or South America (SA). In SI Text 4, we investigate this aspect further by comparing the exposed value to the average number of links from firms in country to country , . Although and are highly correlated (Pearson’s , ), we find variations of up to two orders of magnitude in for a given , see SI Fig. S3.

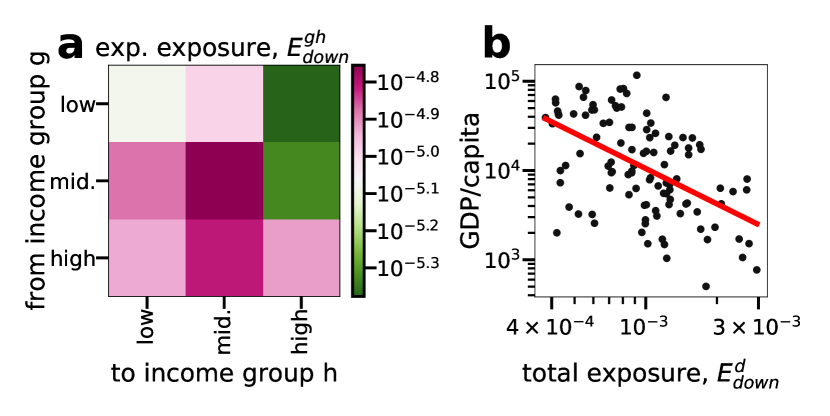

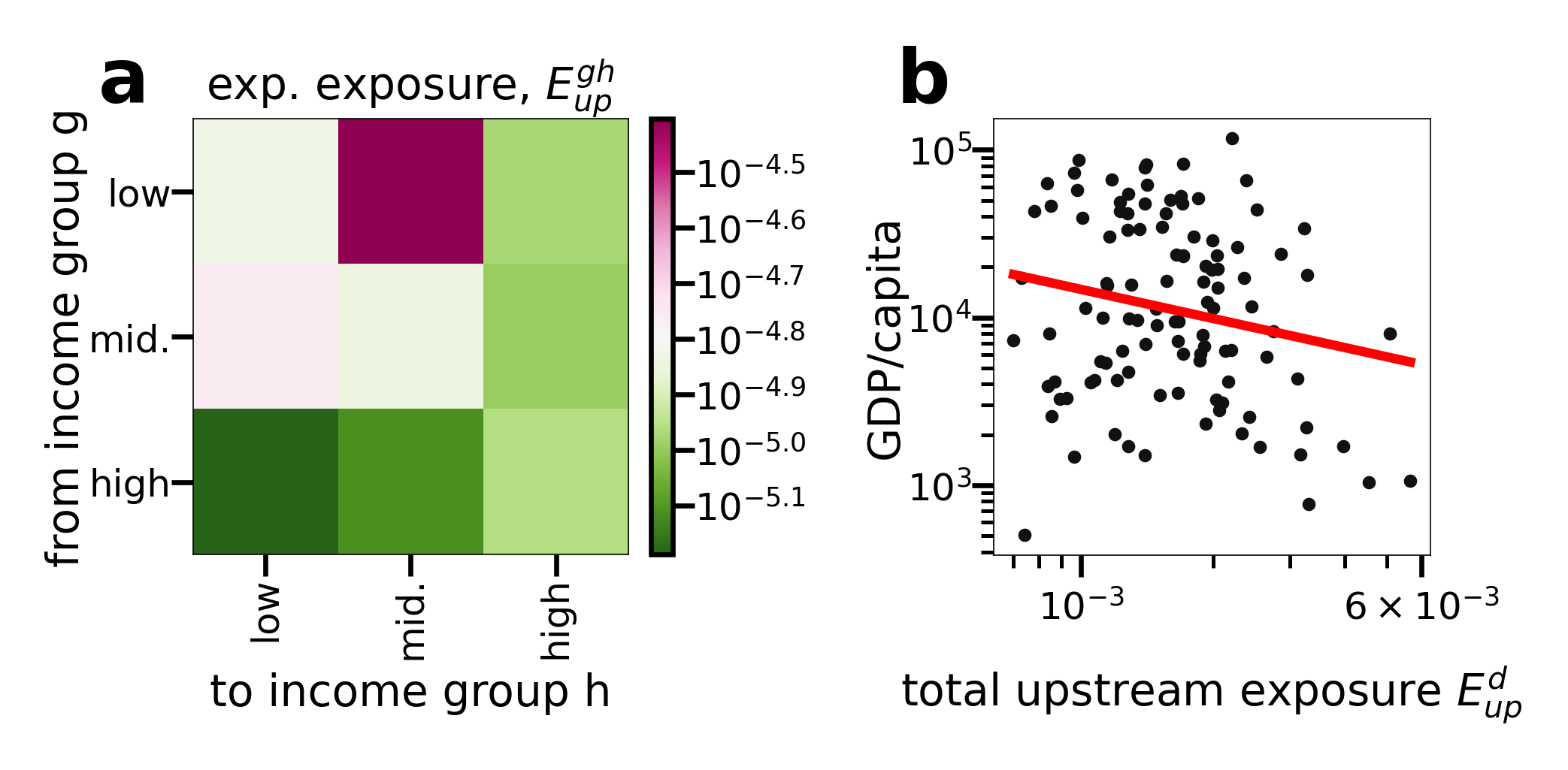

The obvious asymmetry in in Fig. 2a suggests large differences in how systemic risk is distributed around the globe and that exposure to economic losses is usually not reciprocal. In Fig. 3a we change the aggregation scale to three income groups, containing the same number of countries, based on their GDP per capita –low, middle and high. We plot the respective , where and denote the respective country income groups. Three facts become obvious. First, firms in high income countries export much more distress to middle and lower income groups than they import from these. Second, firms in high and middle income countries are most exposed to firms in countries from their own respective groups. Firms in low-income countries receive relatively little risk from their own income group but more from middle and high income countries, indicating that these countries’ economies are more exposed to the wealthier trading partners. Third, the dark color of the column for middle income countries in Fig. 3a indicates that they are exposed to most of the risk.

In Fig 3b we plot the total exposure, , versus GDP per capita showing an anti-correlation (Pearson , ). This indicates that countries with a low GDP per capita are more exposed than countries with a higher. To control for confounding factors, we perform a multivariate linear regression, where GDP per capita is the dependent variable and , GDP, imports, exports, imports per capita and exports per capita are the independent variables. The results of the regression analysis are shown SI Tab. S2 and SI Text 5 and indicate that only and exports per capita have a statistically significant influence on the dependent variable. The model explains 67% of the variance and is highly significant (adjusted , ).

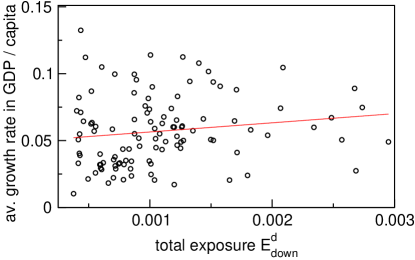

Generally, high risks are thought to be compensated with higher expected returns Sharpe (1964, 1966); Fama and French (2015). We check for the existence of such a “risk premium” by comparing with the average annual growth of GDP per capita in the respective country over the past twenty years. A high growth rate has been causally connected to successful export strategies Van den Berg and Lewer (2015); Ramzan et al. (2019). SI Figure S4, in SI Text 6, shows that there is little to no correlation between the variables (insignificant Pearson correlation of ). Countries seem not to be compensated for taking systemic risk. In SI Text 6 we check for the robustness of this result by comparing with the average annual GDP growth over 5 and 10 years.

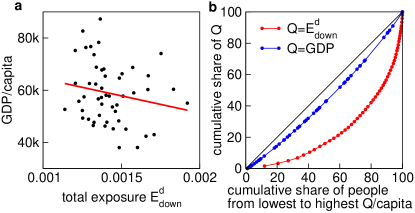

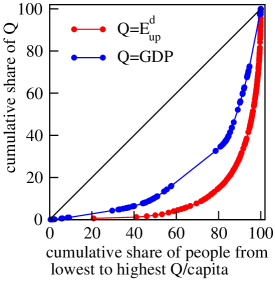

To find out how equally exposures are distributed across the globe, in Fig. 4 we plot the respective Lorenz curve, i.e. the cumulative share of population (sorted by their countries’ per capita) versus their cumulative share of global expected exposure, . 80% of population that are least exposed to risk are exposed to only around 10% of all risk, or vice-versa, 20% of the most exposed population carries around 90% of the risk. For comparison, in Fig. 4 we also show the Lorenz curve for the GDP. Clearly, GDP is distributed somewhat more equally than the , which is also shown by the Gini coefficient. We find Gini coefficients for the GDP and total exposure to be and , respectively.

So far we only considered downstream shock propagation by simulating supply shortages. The analysis for the upstream cascade is discussed in SI Text 7. We find similar structures with respect to the expected upstream exposure matrix (analogously defined as ) in SI Fig. S6. The distribution of upstream exposure by income group in SI Fig. S7 reveals a different picture than for downstream risk. Most risk is between low- and middle-income countries and high-income countries neither create nor are exposed to risk. The respective Gini coefficient is 0.81 and therefore higher than for GDP, again to the disadvantage of poor countries (Pearson’s correlation between GDP per capita and is , ), see SI Fig. S8.

Discussion

We present a method to quantify the exposure of countries to production losses caused by firm defaults in other countries based on global firm-level supply network data. We introduce the expected Country-Country Exposure, , as the expected relative loss of production in country after a firm-failure in country . The method enables us to demonstrate that exposures to other countries is highly structured on a regional level, and that high income countries expose a large fraction of the globe to economic losses. Low income countries are disproportionately strongly affected by high exposure values. Somewhat contrary to intuition, it seems that higher exposure is not positively correlated with higher gains in GDP growth rates in recent decades. Global economic exposure of the type discussed is distributed more unequal than income per capita.

The presented metric confirms the intuition that expected exposures of countries are highest to firms within their own economies, and on the international level exposures are strongly influenced by geography. When countries are sorted by continent, the country exposure matrix, , shows a prominent block-diagonal structure. This is not unexpected, since it is known that exposure increases with connectivity, see SI Text 4, and because trade intensity decreases with distance Anderson (2011). Several wealthy countries create significant exposures beyond their region and thus export systemic risk to other countries. We show that the number of trade links between countries are bad predictors for the direct and indirect exposures between countries. Similarly, company size has been found to be a bad predictor for firms’ systemic riskiness in supply networks Diem et al. (2021); Fujiwara et al. (2016).

To understand if the asymmetry of few countries exposing many countries and many countries exposing only a few is related to their average income level, we separate countries into low-, middle-, and high income groups. We find that firms in high income countries have a privileged position, in the sense that they are only exposed to risk from other high income countries, but expose all other groups. On the other hand, low income countries hardly expose others, while they themselves are exposed strongly. Middle income countries are sizeably exposed to all three income groups. The asymmetry of exposure does a priori not provide any indication whether rich or poor countries have higher total exposure. On the one hand, poor countries could be more dependent on inputs from rich countries, on the other hand rich countries could depend more on highly integrated global value chains and, hence, be more exposed to systemic risk. A regression analysis solves the puzzle and we find that GDP per capita correlates negatively () and, hence, poor countries have a higher total exposure. The presented results on the spreading of supply shocks, are complemented in SI Text 7 with the analogous analysis for demand shocks. We find qualitatively similar results. Again, there is high inequality to the disadvantage of low income and advantage of high income countries. With the currently available data we find no evidence for a “risk premium” in the sense that higher exposures would co-occur with significantly higher economic growth rates. The expected exposure is not significantly correlated with the growth of GDP per capita during the past 20 years before the COVID-19 crises (, ).

We investigate the inequality of exposures across the globe and find that exposure is highly concentrated with a Gini coefficient of 0.83 (compared to 0.59 for GDP). This additional dimension of global inequality adds to a number of other forms of inequality such as inequality with respect to health, (formal) education, and wealth Goesling and Baker (2008). Inequality impedes economic growth Barro (1999); OECD (2015) and has been associated with being one of the driving factors for the collapse of societies Turchin (2016). In their Agenda 2030 the United Nations set to “reduce inequality within and among countries” (SDG 10) as one of the 17 sustainable development goals (SDGs) United Nations General Assembly (2015). Future research should investigate if the network structure of the global supply network locks in already existing inequalities. For social networks it has been shown that their structure can procreate inequality DiMaggio and Garip (2012); Karimi et al. (2018). Similarly, our results suggest that structural inequality in production and trade networks between countries is significant and should be taken into consideration in future efforts to fight inequality in its various forms. Since exposure inequality arises from the structure of the supply network on the firm-level, it is important to understand the processes that let firms from different income countries enter into production and trade relations and how this could happen with creating less risk exposure to poorer countries. Strategies of incentivizing firms to become systemic risk sensitive could be a starting point Leduc and Thurner (2017); Poledna and Thurner (2016).

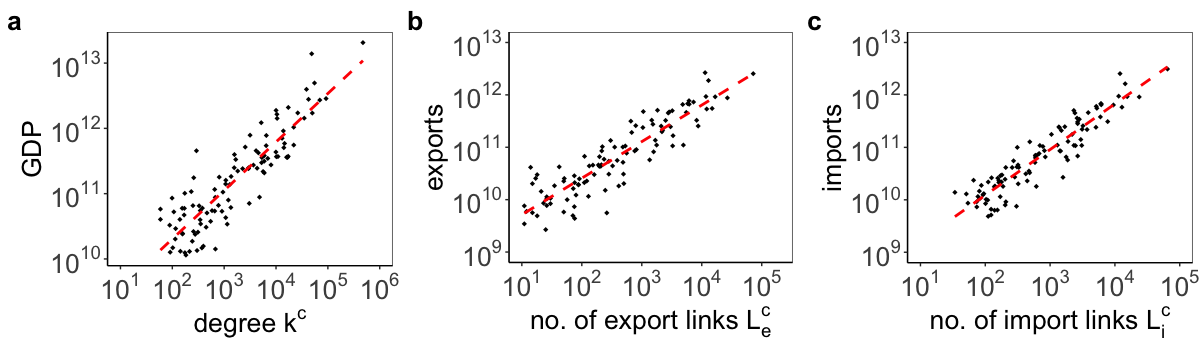

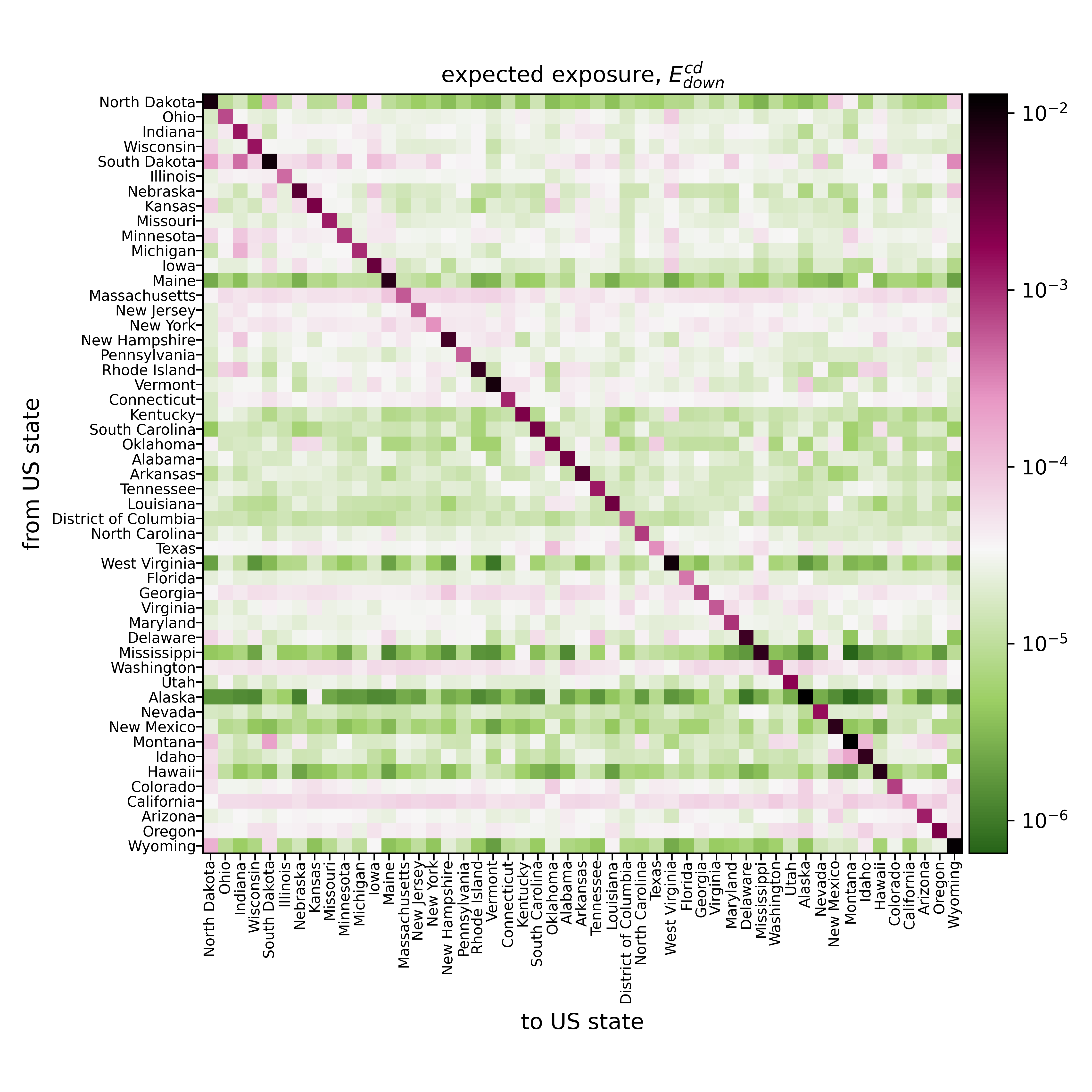

The presented work shows how to calculate international direct and indirect economic exposures between countries that is methodically based on previous work on financial and supply networks Battiston et al. (2012); Fujiwara et al. (2016). The present work is only a first step in the direction of quantifying systemic risk flows around the globe and has several limitations that need improvement. First, our approach disregards completely the nature of the products. An accurate description shock propagation must include the type of the goods and their firm-level production functions. Only then can a supply network be considered a realistic production network. At the moment, the shock spreading dynamics are practically limited to the special case of linear production functions that are typically underestimating the actual shock spreading risks Diem et al. (2021). Second, the current dataset lacks information on the firm’s revenues and the traded volumes. In SI Fig. S9, in SI Text 8, we show that GDP, imports, and exports all have a high correlation with a country’s total degree, outdegree, and indegree. More detailed supply network information would improve the quality of our results by capturing relative effects in the supply network propagation. Third, the dataset is compiled by firms centered in the US, entailing a potential reporting bias. To ensure the robustness of our results, we perform the same study for states in the USA. Although the heterogeneity in the US is much lower, we find similar trends, such as high inequality to the benefit of rich states, for details see SI Text 9. Fourth, the shown results were derived for the spreading of supply and demand shocks separately. We find qualitatively similar results; there is high inequality to the disadvantage of low income and advantage of high income countries. However, it would be desirable to design a measure that is able to capture up- and downstream risk simultaneously, similar to the ESRI quantity recently presented in Diem et al. (2021). Fifth and finally, we assume the same default probability, , for every firm and simulate the ensuing cascade of production interruptions. This is certainly unrealistic, and heterogeneous default probabilities of companies should be taken into account, as well as information on correlated shocks, e.g. due to natural disasters or climate change. However, this is presently practically impossible due to unavailability of corresponding data.

The presented work allows us to derive three immediate policy implications: First, we conclude that the (global) distribution of exposure to economic shocks must be traced on granular representations of the underlying networks. For this a global effort on collecting and monitoring the according data is necessary. This would allow to anticipate and prepare for globally spreading supply shocks. Second, since inequality is deeply embedded in the economic structure of the global supply network, future efforts to reduce inequality, such as the goals formulated in SDG 10 in the United Nations’ Agenda 2030, must include the systematic restructuring of the global production network to spread exposure risky more fairly. Third, since the developed index quantifies the spread of exposure to economic shocks between countries. The employed firm-level resolution allows us to straight forwardly adapt systemic risk management methods for national economies. A possible incentive scheme could be an appropriately adapted systemic risk tax Leduc and Thurner (2017); Poledna and Thurner (2016) for international supply networks.

Materials and Methods

Data

We use supplier-customer data from the web site of Standard & Poor’s (S&P) Capital IQ platform for the year . The data is comprised of firm identification (ID), name, location, primary industry, and sector as node information. Using the Global Industry Classification Standard (GICS), Morgan Stanley Capital International and S&P grouped the firms into 11 sectors and 158 primary industries. Firms are distributed over 206 countries. The data contains information on 1,403,807 business relationships between firms, such as supplier, creditor, franchisor, licensor, landlord, lessor, auditor, transfer agent, investor relations firm, and vendor. Most relations are of type supplier or creditor (69% supply links, 31% creditor links. The supplier type implies that a firm provides goods or services to other firms, the creditor type indicates that a firm lends money to other firms. For a detailed description of the dataset we refer to Chakraborty and Ikeda (2020). Because we are interested in the flow of goods and services between countries, in the following we restrict our analysis to the 968,627 supplier relations.

We preprocess the data in the following way. We remove all firms that do not have locations or sector classification information. To avoid misleading results from countries with too few firms, we only consider firms from those countries where the total number of firms exceeds . Further, we remove firms from Barbados, Bermuda, British virgin Island, Channel Island, Gibraltar, Monaco, and Cayman Island as these are known for having considerable numbers of offshore firms. We construct an unweighted network with an adjacency matrix, , if there exists a link between firm and and , otherwise. After removing isolated nodes, parallel links, and self-loops, the network contains firms and binary, directed links.

To explain the variation in the amount of distress propagation for different countries, we investigate the relation between distress and certain economic indicators characterizing an economy. We collect data on per capita gross domestic product, per capita exports and per capita imports for the year 2018 in current U.S. dollars from the website of the World Bank https://data.worldbank.org.

Methods

DebtRank is a network centrality measure, initially developed as a financial systemic risk index for investment networks Battiston et al. (2012), and recently adopted for supply networks Fujiwara et al. (2016). In a real economic network corresponds to the overall reduction in economic activity subsequent to the default of an initial firm and a possible cascade of defaults. Here, we adopt the specific underlying cascading mechanism to design a novel country-level indicator. In SI Text 1 we give a brief review of the DebtRank as used in Fujiwara et al. (2016) and here we describe our specific adaptation.

An intermediate result in the calculation of is the matrix , with elements , denoting the distress firm receives if firm defaults (the loss in economic production firm experiences if firm defaults), see SI Text 1. The column contains the shocks firm is exposed to. Row contains the shocks firm causes to all other firms when it defaults. We use to define the effect of a node’s default on a set of nodes , in our study typically corresponding to the firms in a country , . In the following, lower indices denote nodes (firms) and raised indices denote groups of nodes (countries).

Because the global supply chain network lacks information on link-weights and node-sizes, we assigned each edge equal weight and associate the node-size with it’s degree , where represents the degree of the -th node. The degree was chosen as a size proxy to be consistent and self contained in the network setting of the used dataset. However, one could also use any other size proxy such as value added, turnover or employees. We define the weight of a country as the sum of its node weights

The Firm-Country Exposure of node i for country c is

Please note that the weight of the initial node is included in the denominator if it is also contained in the set . This allows the interpretation of this value as the fraction of the economy affected in country after the default of firm .

References

- Chase-Dunn et al. (2000) C. Chase-Dunn, Y. Kawano, and B. D. Brewer, American Sociological Review 65, 77 (2000).

- Frankel and Romer (1999) J. A. Frankel and D. H. Romer, American Economic Review 89, 379 (1999).

- Pavcnik (2002) N. Pavcnik, The Review of Economic Studies 69, 245 (2002).

- Ventura (2005) J. Ventura, in Handbook of Economic Growth, Vol. 1 (Elsevier, 2005) pp. 1419–1497.

- Firebaugh and Goesling (2004) G. Firebaugh and B. Goesling, American Journal of Sociology 110, 283 (2004).

- Xu et al. (2020) Z. Xu, Y. Li, S. N. Chau, T. Dietz, C. Li, L. Wan, J. Zhang, L. Zhang, Y. Li, M. G. Chung, and J. Liu, Nature Sustainability 3, 964 (2020).

- Oita et al. (2016) A. Oita, A. Malik, K. Kanemoto, A. Geschke, S. Nishijima, and M. Lenzen, Nature Geoscience 9, 111 (2016).

- Zhang et al. (2017) Q. Zhang, X. Jiang, D. Tong, S. J. Davis, H. Zhao, G. Geng, T. Feng, B. Zheng, Z. Lu, D. G. Streets, et al., Nature 543, 705 (2017).

- Peters et al. (2011) G. P. Peters, J. C. Minx, C. L. Weber, and O. Edenhofer, Proceedings of the National Academy of Sciences 108, 8903 (2011).

- Wiedmann and Lenzen (2018) T. Wiedmann and M. Lenzen, Nature Geoscience 11, 314 (2018).

- Fernández and Sotelo Valencia (2013) D. C. Fernández and A. Sotelo Valencia, Latin American Perspectives 40, 14 (2013).

- Blackstone et al. (2021) N. T. Blackstone, C. B. Norris, T. Robbins, B. Jackson, and J. L. Decker Sparks, Nature Food 2, 692 (2021).

- Hobson (2013) J. Hobson, Occupational Medicine 63, 317 (2013), https://academic.oup.com/occmed/article-pdf/63/5/317/4255408/kqt079.pdf .

- Bolle (2014) M. J. Bolle, Bangladesh apparel factory collapse: Background in brief, Tech. Rep. (Congressional Research Service, the Library of Congress, 2014).

- Butt et al. (2019) N. Butt, F. Lambrick, M. Menton, and A. Renwick, Nature Sustainability 2, 742 (2019).

- Mizuno et al. (2016) T. Mizuno, T. Ohnishi, and T. Watanabe, EPJ Data Science 5, 1 (2016).

- Gephart et al. (2016) J. A. Gephart, E. Rovenskaya, U. Dieckmann, M. L. Pace, and Å. Brännström, Environmental Research Letters 11, 035008 (2016).

- Starnini et al. (2019) M. Starnini, M. Boguñá, and M. Á. Serrano, Scientific Reports 9, 1 (2019).

- Klimek et al. (2019) P. Klimek, S. Poledna, and S. Thurner, Nature communications 10, 1 (2019).

- del Rio-Chanona et al. (2020) R. M. del Rio-Chanona, Y. Korniyenko, M. Patnam, and M. A. Porter, Applied Network Science 5, 1 (2020).

- Barrot and Sauvagnat (2016) J.-N. Barrot and J. Sauvagnat, The Quarterly Journal of Economics 131, 1543 (2016).

- Inoue and Todo (2019) H. Inoue and Y. Todo, Nature Sustainability 2, 841 (2019).

- Carvalho et al. (2021) V. M. Carvalho, M. Nirei, Y. U. Saito, and A. Tahbaz-Salehi, The Quarterly Journal of Economics 136, 1255 (2021).

- Boehm et al. (2019) C. E. Boehm, A. Flaaen, and N. Pandalai-Nayar, Review of Economics and Statistics 101, 60 (2019).

- Lee et al. (2011) K.-M. Lee, J.-S. Yang, G. Kim, J. Lee, K.-I. Goh, and I.-m. Kim, PloS one 6, e18443 (2011).

- Boss et al. (2004) M. Boss, H. Elsinger, M. Summer, and S. Thurner 4, Quantitative Finance 4, 677 (2004).

- Iori et al. (2008) G. Iori, G. De Masi, O. V. Precup, G. Gabbi, and G. Caldarelli, Journal of Economic Dynamics and Control 32, 259 (2008).

- Battiston et al. (2012) S. Battiston, M. Puliga, R. Kaushik, P. Tasca, and G. Caldarelli, Scientific Reports 2, 1 (2012).

- Thurner and Poledna (2013) S. Thurner and S. Poledna, Scientific Reports 3, 1 (2013).

- Diem et al. (2020) C. Diem, A. Pichler, and S. Thurner, Journal of Economic Dynamics and Control 116, 103900 (2020).

- Pichler et al. (2021) A. Pichler, S. Poledna, and S. Thurner, Journal of Financial Stability 52, 100809 (2021).

- Bardoscia et al. (2015) M. Bardoscia, S. Battiston, F. Caccioli, and G. Caldarelli, PloS one 10, e0130406 (2015).

- Poledna et al. (2015) S. Poledna, J. L. Molina-Borboa, S. Martínez-Jaramillo, M. Van Der Leij, and S. Thurner, Journal of Financial Stability 20, 70 (2015).

- Fujiwara et al. (2016) Y. Fujiwara, M. Terai, Y. Fujita, and W. Souma, RIETI Discussion Paper Series 16-E-046 (2016).

- Diem et al. (2021) C. Diem, A. Borsos, T. Reisch, J. Kertész, and S. Thurner, Available at SSRN 3826514 (2021).

- Hallegatte (2008) S. Hallegatte, Risk Analysis: An International Journal 28, 779 (2008).

- Krichene et al. (2020) H. Krichene, H. Inoue, T. Isogai, and A. Chakraborty, PloS one 15, e0239293 (2020).

- Markhvida et al. (2020) M. Markhvida, B. Walsh, S. Hallegatte, and J. Baker, Nature Sustainability 3, 538 (2020).

- Haraguchi and Lall (2015) M. Haraguchi and U. Lall, International Journal of Disaster Risk Reduction 14, 256 (2015).

- Sweney (2021) M. Sweney, The Guardian (2021), retrieved Oct. 12, 2021.

- Isidore (2021) C. Isidore, CNN Business (2021), retrieved Oct. 12, 2021.

- Waldersee (2021) V. Waldersee, Reuters (2021), https://www.reuters.com/business/autos-transportation/chip-shortage-leads-carmaker-opel-shut-german-plant-until-2022-2021-09-30/, retrieved Oct. 17, 2021.

- Williams and Bushey (2021) A. Williams and C. Bushey, Financial Times (2021), https://financialpost.com/financial-times/car-chip-shortage-shines-light-on-fragility-of-u-s-supply-chain, retrieved Oct. 17, 2021.

- Ricardo (1891) D. Ricardo, On the Principles of Political Economy and Taxation (G. Bell and sons, 1891).

- Sharpe (1964) W. F. Sharpe, The Journal of Finance 19, 425 (1964).

- Sharpe (1966) W. F. Sharpe, The Journal of Business 39, 119 (1966).

- Fama and French (2015) E. F. Fama and K. R. French, Journal of Financial Economics 116, 1 (2015).

- Van den Berg and Lewer (2015) H. Van den Berg and J. J. Lewer, International Trade and Economic Growth (Routledge, 2015).

- Ramzan et al. (2019) M. Ramzan, B. Sheng, M. Shahbaz, J. Song, and Z. Jiao, The Journal of International Trade & Economic Development 28, 960 (2019), https://doi.org/10.1080/09638199.2019.1616805 .

- Anderson (2011) J. E. Anderson, Annual Review of Economics 3, 133 (2011), https://doi.org/10.1146/annurev-economics-111809-125114 .

- Goesling and Baker (2008) B. Goesling and D. P. Baker, Research in Social Stratification and Mobility 26, 183 (2008).

- Barro (1999) R. J. Barro, Inequality, Growth, and Investment, Working Paper 7038 (National Bureau of Economic Research, 1999).

- OECD (2015) OECD, “In it together: Why less inequality benefits all.” (2015).

- Turchin (2016) P. Turchin, Chaplin, CT: Beresta Books. (2016).

- United Nations General Assembly (2015) United Nations General Assembly, “Transforming Our World: The 2030 Agenda for Sustainable Development,” (2015), https://sdgs.un.org/2030agenda.

- DiMaggio and Garip (2012) P. DiMaggio and F. Garip, Annual Review of Sociology 38, 93 (2012).

- Karimi et al. (2018) F. Karimi, M. Génois, C. Wagner, P. Singer, and M. Strohmaier, Scientific Reports 8, 1 (2018).

- Leduc and Thurner (2017) M. V. Leduc and S. Thurner, Journal of Economic Dynamics and Control 82, 44 (2017).

- Poledna and Thurner (2016) S. Poledna and S. Thurner, Quantitative Finance 16, 1599 (2016).

- Chakraborty and Ikeda (2020) A. Chakraborty and Y. Ikeda, PloS one 15, e0239669 (2020).

Acknowledgements

We thank Y. Ikeda for providing the S&P Capital IQ data. The project was supported by Austrian Science Fund FWF under I 3073-N32, Austrian Science Promotion Agency FFG under 857136, and Hochschuljubiläumsstiftung of the Austrian National Bank OeNB under P17795 2018-2021.

Author contributions statement

All authors conceived and designed the study. A.C. analyzed the data. All authors discussed the results and contributed to the manuscript. A.C., T.R. and S.T. wrote the paper.

Additional information

Competing interests The authors declare no competing interests.

Supplementary Information

SI Text 1: DebtRank

The DebtRank of a firm in a supply network Fujiwara et al. (2016) describes the overall reduction in economic activity subsequent to the default of an initial firm and the cascade of defaults caused by it. Here, we provide a brief review of the underlying cascading mechanism and show how to calculate the indicator as used in Fujiwara et al. (2016).

Let us consider a directed and weighted network with nodes . A link from node to has a weight that represents a relative dependency of to . At any time-step t, the nodes are characterised by their state and the amount of financial distress . The state of a node can be “Active”, “Distressed” or “Inactive” at time . We start with the following initial configurations:

and

where is an initial set of “Distressed” nodes, which can be a single node as well. We update the amount of distress as

where the summation is taken over all the neighbours of having state . We also update the state of each node simultaneously as follows

Note that at the next time step, a node in state becomes , which does not propagate any distress to others afterwards. This helps to exclude, in the case of cycles, an infinite number of repercussions in shock propagation. However, an node continues to receive distress from its distressed neighbours without affecting others. The propagation terminates after a finite number of time steps . In the following we set to just consider the default of one node, the generalization to a set of nodes is straightforward. We use the matrix with element denoting the distress firm receives if firm defaults (the loss in economic production firm experiences if firm defaults). The column contains the shock firm is exposed to. Row contains the shock firm causes to all other firms when it defaults. The total amount of distress, i.e. the total loss of production, in the system due to the initially distressed node is measured as its DebtRank

where is the size of the nodes . We include the effect of the initial set of distressed nodes. The quantities discussed in the main text are based on different aggregations of .

Since our global supply chain network does not have link-weights and node size information, we have assigned each edge equal weight and associate the node-size with it’s degree , where and represent degree and in-degree of the -th node, respectively. We choose degree as size proxy, to be consistent and self-contained in the supply network dataset. However, one could also use other size proxies such as value added, turnover or employees.

SI Text 2: Toy example of a cascade of production interruptions

In SI Fig. S1 we show the cascade subsequent to the default of firm 2. Compared to the default of firm 1, country C is hit harder and country B is not affected at all.

SI Text 3: Detailed exposure matrix

In the main text we show that the expected downstream exposure between countries, , is clearly structured by geographic regions. Exposures are highest within countries, then within regions and continents. In SI Fig. S2 we show a large version of the same plot, such that we can label the individual countries. The numbers correspond to the index column in SI Tab. LABEL:tab:SI:country_names.

In Africa (AF) we find two blocks corresponding to north African and sub-Sahara countries. Most of their high exposures are within their region, but it is also instructive to consider the columns of the matrix, showing that, e.g. some north African countries are strongly exposured to Asia and Europe, but not to the Americas.

In Asia (AS) we have three regions, East Asia and Pacific, Middle East and South Asia, but observe only two prominent blocks, suggesting that the regional classification does not fully represent economic regions. Several Asian countries expose countries around the world to medium exposure, highlighted by horizontal white lines.

Oceania and Australia (OC) does not show up as a prominent block, but is rather connected to South Asia. Further, as an industrialized region it creates exposure to most other countries in the world.

The European (EU) countries ares split into four groups, Central and Eastern Europe (CEE), Northern Europe (NE), Southern Europe (SE), and Western Europe (WE). CEE and NE countries form relatively well separated blocks, while SE and WE highly expose all countries. This strongly suggests that SE and WE countries are integrated into the world market more strongly than NE and CEE countries.

In North America (NA) there is no clear block structure visible. However, for Canada (index 97), Mexico (98) and the USA (99) the horizontal white lines show that they highly expose most countries around the globe. The magenta vertical line for the USA between row 100 and 110 suggests that the USA is also highly exposed to disruptions in Southern America.

South America (SA) is visible as a very prominent, dark magenta block. This implies that the economies in SA are tightly interwoven and expose each other strongly.

| index | country name | continent | region | income group |

|---|---|---|---|---|

| 0 | Algeria | Africa | Middle East and North Africa | low |

| 1 | Egypt | Africa | Middle East and North Africa | low |

| 2 | Libya | Africa | Middle East and North Africa | middle |

| 3 | Morocco | Africa | Middle East and North Africa | low |

| 4 | Tunisia | Africa | Middle East and North Africa | low |

| 5 | Angola | Africa | Sub-Saharan Africa | low |

| 6 | Botswana | Africa | Sub-Saharan Africa | middle |

| 7 | Côte d’Ivoire | Africa | Sub-Saharan Africa | low |

| 8 | Ghana | Africa | Sub-Saharan Africa | low |

| 9 | Kenya | Africa | Sub-Saharan Africa | low |

| 10 | Mozambique | Africa | Sub-Saharan Africa | low |

| 11 | Mauritius | Africa | Sub-Saharan Africa | middle |

| 12 | Namibia | Africa | Sub-Saharan Africa | low |

| 13 | Nigeria | Africa | Sub-Saharan Africa | low |

| 14 | Tanzania, United Republic of | Africa | Sub-Saharan Africa | low |

| 15 | Uganda | Africa | Sub-Saharan Africa | low |

| 16 | South Africa | Africa | Sub-Saharan Africa | middle |

| 17 | Zambia | Africa | Sub-Saharan Africa | low |

| 18 | Zimbabwe | Africa | Sub-Saharan Africa | low |

| 19 | China | Asia | East Asia and Pacific | middle |

| 20 | Hong Kong | Asia | East Asia and Pacific | high |

| 21 | Indonesia | Asia | East Asia and Pacific | low |

| 22 | Japan | Asia | East Asia and Pacific | high |

| 23 | Cambodia | Asia | East Asia and Pacific | low |

| 24 | Korea, Republic of | Asia | East Asia and Pacific | high |

| 25 | Macao | Asia | East Asia and Pacific | high |

| 26 | Mongolia | Asia | East Asia and Pacific | low |

| 27 | Malaysia | Asia | East Asia and Pacific | middle |

| 28 | Philippines | Asia | East Asia and Pacific | low |

| 29 | Singapore | Asia | East Asia and Pacific | high |

| 30 | Thailand | Asia | East Asia and Pacific | middle |

| 31 | Taiwan | Asia | East Asia and Pacific | high |

| 32 | Viet Nam | Asia | East Asia and Pacific | low |

| 33 | United Arab Emirates | Asia | Middle East and North Africa | high |

| 34 | Bahrain | Asia | Middle East and North Africa | high |

| 35 | Iran, Islamic Republic of | Asia | Middle East and North Africa | low |

| 36 | Israel | Asia | Middle East and North Africa | high |

| 37 | Jordan | Asia | Middle East and North Africa | low |

| 38 | Kuwait | Asia | Middle East and North Africa | high |

| 39 | Lebanon | Asia | Middle East and North Africa | middle |

| 40 | Oman | Asia | Middle East and North Africa | middle |

| 41 | Qatar | Asia | Middle East and North Africa | high |

| 42 | Saudi Arabia | Asia | Middle East and North Africa | high |

| 43 | Turkey | Asia | Middle East and North Africa | middle |

| 44 | Bangladesh | Asia | South Asia | low |

| 45 | India | Asia | South Asia | low |

| 46 | Sri Lanka | Asia | South Asia | low |

| 47 | Nepal | Asia | South Asia | low |

| 48 | Pakistan | Asia | South Asia | low |

| 49 | Australia | Australia and Oceania | East Asia and Pacific | high |

| 50 | New Zealand | Australia and Oceania | East Asia and Pacific | high |

| 51 | Papua New Guinea | Australia and Oceania | East Asia and Pacific | low |

| 52 | Armenia | Europe | Central and Eastern Europe | low |

| 53 | Azerbaijan | Europe | Central and Eastern Europe | low |

| 54 | Bulgaria | Europe | Central and Eastern Europe | middle |

| 55 | Bosnia and Herzegovina | Europe | Central and Eastern Europe | low |

| 56 | Belarus | Europe | Central and Eastern Europe | middle |

| 57 | Czechia | Europe | Central and Eastern Europe | high |

| 58 | Croatia | Europe | Central and Eastern Europe | middle |

| 59 | Hungary | Europe | Central and Eastern Europe | middle |

| 60 | Kazakhstan | Europe | Central and Eastern Europe | middle |

| 61 | Moldova, Republic of | Europe | Central and Eastern Europe | low |

| 62 | North Macedonia | Europe | Central and Eastern Europe | middle |

| 63 | Poland | Europe | Central and Eastern Europe | middle |

| 64 | Romania | Europe | Central and Eastern Europe | middle |

| 65 | Russian Federation | Europe | Central and Eastern Europe | middle |

| 66 | Serbia | Europe | Central and Eastern Europe | middle |

| 67 | Slovakia | Europe | Central and Eastern Europe | middle |

| 68 | Slovenia | Europe | Central and Eastern Europe | high |

| 69 | Ukraine | Europe | Central and Eastern Europe | low |

| 70 | Denmark | Europe | Northern Europe | high |

| 71 | Estonia | Europe | Northern Europe | middle |

| 72 | Finland | Europe | Northern Europe | high |

| 73 | Iceland | Europe | Northern Europe | high |

| 74 | Lithuania | Europe | Northern Europe | middle |

| 75 | Latvia | Europe | Northern Europe | middle |

| 76 | Norway | Europe | Northern Europe | high |

| 77 | Sweden | Europe | Northern Europe | high |

| 78 | Cyprus | Europe | Southern Europe | high |

| 79 | Spain | Europe | Southern Europe | high |

| 80 | Greece | Europe | Southern Europe | middle |

| 81 | Italy | Europe | Southern Europe | high |

| 82 | Malta | Europe | Southern Europe | high |

| 83 | Portugal | Europe | Southern Europe | high |

| 84 | Austria | Europe | Western Europe | high |

| 85 | Belgium | Europe | Western Europe | high |

| 86 | Switzerland | Europe | Western Europe | high |

| 87 | Germany | Europe | Western Europe | high |

| 88 | France | Europe | Western Europe | high |

| 89 | United Kingdom | Europe | Western Europe | high |

| 90 | Ireland | Europe | Western Europe | high |

| 91 | Luxembourg | Europe | Western Europe | high |

| 92 | Netherlands | Europe | Western Europe | high |

| 93 | Bahamas | North America | Latin America and Caribbean | high |

| 94 | Dominican Republic | North America | Latin America and Caribbean | middle |

| 95 | Jamaica | North America | Latin America and Caribbean | low |

| 96 | Panama | North America | Latin America and Caribbean | middle |

| 97 | Canada | North America | North America | high |

| 98 | Mexico | North America | North America | middle |

| 99 | United States | North America | North America | high |

| 100 | Argentina | South America | Latin America and Caribbean | middle |

| 101 | Bolivia, Plurinational State of | South America | Latin America and Caribbean | low |

| 102 | Brazil | South America | Latin America and Caribbean | middle |

| 103 | Chile | South America | Latin America and Caribbean | middle |

| 104 | Colombia | South America | Latin America and Caribbean | middle |

| 105 | Ecuador | South America | Latin America and Caribbean | middle |

| 106 | Peru | South America | Latin America and Caribbean | middle |

| 107 | Paraguay | South America | Latin America and Caribbean | low |

| 108 | Trinidad and Tobago | South America | Latin America and Caribbean | middle |

| 109 | Uruguay | South America | Latin America and Caribbean | middle |

| 110 | Venezuela, Bolivarian Republic of | South America | Latin America and Caribbean | low |

SI Text 4: Correlation of direct links and country country exposure

Direct trade links represent first order (i.e. direct) exposures. Consequently, the exposed value in country subsequent to the default of a firm in country , , increases as function of the average number of links firms in country have to country .

We quantify the direct influence of one country on another by the average number of out-links of a firm in country to the firms in country , .

In Fig. S3 we plot on the y-axis and on the x-axis. We find that spans five orders of magnitude. Although we observe a high correlation between and (Pearson’s ), we find large variations in , for a given level of average outlinks. The red arrow in SI Fig. S3 highlights that this variation can be more than two orders of magnitude for a given value of average out-degree. This variation can be attributed to higher order exposures that are heavily influenced by the network topology. For a fully connected network –equivalently to an aggregated version of the network– and are perfectly correlated.

SI Text 5: Multilinear regression model for GDP per capita

We perform the following multi linear regression models for GDP per capita and report the results in SI Tab. S2.

Model 1: GDP/capita Intercept + Total downstream imported distress + GDP + Exports + Imports + Exports/capita +Import/capita

The model explains 67% of variance (adjusted ) and the significant covariates are and exports per capita.

We perform a second regression with only and exports per capita as covariates which explains a comparable amount of variance (adjusted , ), see SI Tab. S2.

Model 2: GDP/capita Intercept + Total downstream imported distress + Exports/capita

| Variables | Model 1 | Model 2 |

|---|---|---|

| Intercept | *** | *** |

| Total downstream imported distress, | ** | *** |

| GDP | ||

| Exports | ||

| Imports | ||

| Exports/capita | ** | *** |

| Imports/capita | ||

| Observations | ||

| Adjusted R2 | ||

| p value |

Significance codes for p value:

SI Text 6: GDP growth vs. total exposure

Intuitively we expect higher gains from higher risks. For lack of a better indicator, in SI Fig. S4 we compare total exposure with average annual growth of GDP per capita. International trade is generally associated with higher GDP growth Van den Berg and Lewer (2015); Ramzan et al. (2019). We find no significant correlation between and the average GDP per capita growth rate over 20 years, between 1998 and 2018 (Pearson ), see SI Fig. S4. We test our results for robustness by calculating the correlation with 5- and 10-year growth, but find no correlations (10-year growth: Pearson ; 5-year growth: Pearson ). Note that we are limited by data availability and can only compare exposures on the 2017 network with historical growth rates.

SI Text 7: Upstream exposures

In the main text, we have studied the downstream propagation of shocks, reflecting the impact of a supplier default. We can also study upstream cascades to show the impact of a customer’s default. SI Figure S5 shows the variation of upstream exposed economic value with average in-degree of firms in country from the firms in country , . Here also, we observe that these two quantities are strongly correlated (), but retain a lot of variance, indicated by a red arrow which shows a variation of two orders of magnitude for a given value of .

We explore the structure of the upstream country-country exposure matrix in SI Fig. S6. Contrary to intuition, it is not simply the transpose of its downstream counterpart. It shows similar structures, such as high values within countries and similar clusters of geographic regions. Confirming expectation, some countries that created a lot of downstream exposure, such the block of northern, southern and western European countries, now receive downstream distress when passing buyer-supplier relations the opposite way. However, some countries, such as several Middle Eastern countries, very prominently create a lot of upstream exposure that was not visible in the downstream cascade, see SI Fig. S6.

We show the average upstream distress exposure matrix between firms in low, middle and high income countries in SI Fig S7a. It shows that firms in low and middle income countries affect each other more than any other pair of groups. High income countries experience little and create little exposure.

We plot the total upstream exposure with GDP per capita of the countries in SI Fig S7b. It shows that these two quantities are negatively correlated (), reflecting the fact that countries with lower GDP per capita receive more upstream imported distress, however with a weaker effect and lower significance.

We investigate the concentration of exposure to upstream cascades with the Lorentz curve in SI Fig S8. Again, is concentrated more strongly than GDP with a Gini coefficient of , compared to a Gini coefficient of for GDP.

SI Text 8: Relationship between aggregate firms degree and macroeconomic variables

Our dataset lacks information on the traded volumes (i.e. link weights) and firm level information such as revenue. We assume equal weights on all links () and verify that this approximation is justified on the aggregate level by comparing it to macroeconomic variables. We calculate the total degree , total export links , and total import links of firms in a country. The total degree for a country , is measured as the total number of links of all firms in country . represents the total number of outgoing links of all firms in to firms in all other countries. Similarly, represents the total number of incoming links of all firms in the from firms in all other countries. SI Figure S9 shows that these quantities are strongly correlated with GDP, total exports and total imports with the Pearson correlation coefficients , , , and , respectively.

SI Text 9: Results for states in the USA

Here we study downstream shock propagation in the national supply network of the USA, aggregated to the 50 states of the USA. In SI Fig. S10 we plot the exposure matrix between US states, sorted according to the regional classification by the US census bureau. Here, similarly to the exposures in the global supply network, the strongest exposures are along the diagonal –within the respective states–. However, we do not observe a pronounced block structure, indicating that exposures are not stronger within geographic regions. This can be explained by less pronounced regional differences, a shared cultural history and a lack of trade barriers within the US. The more pronounced structure is that large, rich states create a lot of exposure to the rest of the country, visible as bright and magenta horizontal lines.

SI Figure S11 (a) shows that the states with lower GDP per capita receive more total exposure than states with higher GDP per capita. Albeit the correlation being insignificant (), the data shows a weak negative relationship between GDP per capita and , as indicated by the red trend line in SI Fig. S11 (a). We investigate the inequality in total exposure and GDP for US states with the Lorentz curves in SI Fig. S11 (b). The Gini coefficients are found to be and for total exposure and GDP, respectively. This indicates that, albeit less than for the global supply network, total downstream exposure is more concentrated than GDP among states in USA. We conclude that, despite lower inter-state heterogeneity we find visually similar results to the global supply network.