2021

[1]\fnmJoanna \surJanczura

1]\orgdivFaculty of Pure and Applied Mathematics, \orgnameWroclaw University of Science and Technology, \orgaddress\streetWyb. Wyspiańskiego 27, \city Wrocław, \postcode50-370, \countryPoland

2]\orgnameKGHM, \orgaddress\streetM. Skłodowskiej-Curie 48, \cityM. Skłodowskiej-Curie 48, \postcode59-301, \countryPoland

On the distribution of the product of two continuous random variables with an application to electricity market transactions. Finite and infinite-variance case.

Abstract

In this paper we study the distribution of a product of two continuous random variables. We derive formulas for the probability density functions and moments of the products of the Gaussian, log-normal, Student’s t and Pareto random variables. In all cases we analyze separately independent as well as correlated random variables. Based on the theoretical results we use the general maximum likelihood approach for the estimation of the parameters of the product random variables and apply the methodology for a real data case study. We analyze a distribution of the transaction values, being a product of prices and volumes, from a continuous trade on the German intraday electricity market.

keywords:

product, Gaussian distribution, log-normal distribution, Pareto distribution, Student’s t distribution, correlation coefficient, electricity marketpacs:

[MSC Classification]60E05, 91B26, 62E15, 65C20, 33-02

1 Introduction

One of important problems in statistics and applied mathematics is the recognition of distributions corresponding to various functions of two (or even more) random variables. In the literature different transformations of two random variables, such as a sum, product, ratio, etc., are considered. In this paper we focus on the product function, i.e we analyze the random variable defined as

| (1) |

where and , called marginal random variables, have continuous distributions.

The considered problem is not new and there are various examples of random variables for which the product is analyzed in theory and in practice. Particular emphasis is placed on the product of two random variables that come from the same class of distributions, see eg. logistic ; pearson ; eliptically ; trapezoidal . In this case one can find interesting approaches used in the analysis of the distribution and probabilistic properties of the product random variable. The special attention is paid to the case when two considered random variables are Gaussian or Student’s t distributed, see e.g. Ahsanullah_2014 ; student_t ; gauss2 ; gauss1 ; student_statistical . The other interesting cases one can find also in exponential , where exponentially distributed random variables are considered or in dirichlet , where Dirichlet distributed random variables are examined. For other references, see also beta ; beta2 ; pareto2 ; beta_statistical . Different classes of distributions are also considered in the literature and the product of such random variables is analyzed, see eg. normal_laplace ; gauss_laplace2 ; gama_weibul ; gama_beta ; pareto_gama ; beta_statistical and references therein.

Beyond theoretical considerations, the random variables that arise as a product (or other functions) of two variables have found various interesting applications including finance, risk management, economy, but also physical sciences, reliability theory, hydrology, and many others, see eg. appl1 ; appl2 ; appl3 ; appl4 ; appl5 ; appl6 ; appl7 ; appl8 ; appl10 .

There are known general formulas that can be useful when one considers the random variable defined in Eq. (1). For instance, in the general case the probability density function (PDF) of is given by gauss1 ; rohatgi2015

| (2) |

where , is a two-dimensional PDF of the vector .

In this paper we separately study examples of finite- and infinite-variance distributions of the marginal random variables. The sample distributions of the first class considered in this paper are the Gaussian and log-normal, while of the second class - the Student’s t Ahsanullah_2014 and Pareto distributions Mardia_1962 . We consider two cases. In the first one the marginal random variables come from the same class of distributions, while in the second one - they are representatives of different classes.

Obviously, the general properties of the product simplify when the marginal random variables are independent. In that case, the corresponding bi-dimensional random vector has the PDF that is a product of the marginal densities, i.e. we have

| (3) |

where and are the PDF’s of the marginal distributions corresponding to and , respectively.

The situation is much more complicated when the marginal random variables are statistically dependent. In that case the simplest way to express the dependence between them is the correlation coefficient. However, the correlation coefficient equal to zero does not always correspond to the case when the marginal random variables are statistically independent. From the distributions considered in this paper, this is the case for the Student’s t and Pareto ones. Moreover, for the infinite-variance random variables, the correlation coefficient is infinite as well. Thus, various other approaches might be also considered. One of the ideas utilizes copula as the dependency measure appl5 ; copula2 ; copula3 . Other dependency measures, adequate for infinite-variance random variables are presented e.g. in wylomanska2015codifference ; slkezak2019codifference ; stable ; nowicka1 .

The main goal of the paper is to determine probability density functions of the product random variable for the considered distributions and examine, how the probabilistic properties of the marginal random variables influence the distributional properties of the final product.

The second goal of the paper is the analysis of the distribution of the product random variable when the marginal random variables come from different classes of distributions. The main attention is paid to the analysis on how the parameter responsible for distribution tail influences the PDF of the product random variable.

The obtained theoretical properties are used for the estimation of the product random variable parameters. We use a general idea based on the maximum likelihood algorithm. With the Monte Carlo simulations we confirm the effectiveness of the procedure. Finally, the methodology is applied to real data from the energy market. We analyze a distribution of the transaction values, being a product of prices and volumes, from a continuous trade on the German intraday electricity market. We show that using the derived product distribution a good fit to the transaction values data can be obtained, being at the same time consistent with the corresponding prices and volumes distributions.

The rest of the paper is organized as follows: First, we discuss the probabilistic properties of a random variable that arises as a product of random variables coming from two exemplary finite-variance distributions. Next, in Section 3 we provide similar considerations for the exemplary random variables from infinite-variance class of distributions. In Section 4 we discuss the case when the marginal random variables come from different classes of distributions. The probabilistic properties of the product random variable are calculated and the influence of the parameters of the marginal distributions is discussed. The next part is devoted to the practical aspects of the obtained results. Namely, in Section 5 we propose a general methodology for the estimation of the parameters for the product random variable, while in Section 6 we apply the methodology to a real-data case. We analyze the transactions data from the German electricity market settled on the EPEX energy exchange. Last section concludes the paper and presents other possible applications of the proposed methodology.

2 Product of finite-variance distributed random variables

In this section we consider exemplary distributions of and that belong to the finite-variance class, namely the Gaussian and log-normal ones. We recall the known results for the product of two-dimensional Gaussian distribution and derive the corresponding formulas for the log-normal one. It is worth mentioning, that for these distributions the independence between and is equivalent to the zero valued correlation coefficient and in that case the PDF of the two-dimensional vector is given by Eq. (3).

2.1 Gaussian distribution

The two-dimensional Gaussian distributed random random vector has the following PDF Roussas_2015

| (4) |

where , is the correlation coefficient between random variables and ; are the corresponding expected values, while are the corresponding standard deviations. The cases or are not considered in this paper. However, they correspond to the situation when , with . As a consequence, the product random variable has a chi-square distribution with one degree of freedom. It is easy to see that, when , the PDF of the random vector is just a product of the PDFs of the Gaussian distributed random variables.

For simplicity we assume that . In that case the PDF of the random variable defined in (1) is given by Gaunt_2018

| (5) |

where , is the Bessel function of the second kind with a purely imaginary argument of zero order. Recall that the family of the modified Bessel functions of the second kind for order is given by . The formula for in the general case with can be found in general_normal .

One can show that the PDF given in Eq. (5) corresponds to the variance-gamma distribution PDF: . The expected value and the variance of in the general case are given by Craig_1936

| (6) | ||||

| (7) |

It is interesting to note that, for correlated marginal variables the individual scale parameters, influence also the expected value of the product, , and for central marginal distributions we have . On the other hand, if , then the product expectation is just the product of the individual means, . The variance of the product is equal to the product of individual variances only if and the marginal variables are uncorrelated. Otherwise, it is a function of all individual parameters.

2.1.1 Log-normal distribution

The two-dimensional log-normally distributed random vector with parameters , and is defined in the following way log_multi

| (8) |

where is the Gaussian random vector defined by the PDF in Eq. (4) with the parameters and . Thus, the marginal random variables and have the representations

| (9) |

and in the general case the parameter is the correlation between and . This influences also the correlation between and . Indeed, one can easily show that the covariance between and is as follows

| (10) |

The PDF of is given by Yerel_BVLN

| (11) |

where . If , the marginal variables and are independent and the PDF given in (11) is a product of PDFs of one-dimensional random variables with the log-normal distribution. The cases and are not considered in this paper. However, one can notice that in these cases the product random variable has still the log-normal distribution.

One can show that the random variable defined in Eq. (1) in the considered case has also one-dimensional log-normal distribution. Indeed, from Eq. (9) one has

Since and are jointly Gaussian, the random variable still has the Gaussian distribution with the expected value and the variance . Thus, the PDF of has the following form

| (12) |

for . The resulting product distribution is still log-normal with the following parameters: and . Hence, the coefficient influences the scale parameter of the resulting distribution.

3 Product of infinite-variance distributed random variables

In this section, we consider exemplary distributions of and that belong to the infinite-variance class of distributions. The considered cases are the Student’s t and Pareto. In contrast to the finite-variance distributions considered in the previous section, the zero correlation coefficient does not correspond to the case when the marginal random variables are statistically independent.

3.1 Student’s t distribution

A common method of construction of a two-dimensional Student’s t distributed random vector is based on the following observation. Let us assume that is the two-dimensional Gaussian vector defined by the PDF in Eq. (4) with the parameters , and , and is the one-dimensional random variable with chi-square distribution with degrees of freedom. Moreover, assume that and are independent. Then the random vector defined as

| (13) |

has a two-dimensional Student’s t distribution with degrees of freedom and its PDF is given by Lai_2009

| (14) |

The marginal random variable (and ) has the one-dimensional Student’s t distribution defined by the PDF given by student_baza

| (15) |

where is the gamma function, i.e. for such that . Note that the number of degrees of freedom, , is equal for both marginal variables. For the random variables and described by the PDF in (14) have the following covariance

| (16) |

One can see that, although the zero correlation coefficient corresponds to , it is not equivalent to the independence of the random variables and , since in that case the PDF of a random vector (see Eq. (14)) is not a product of the PDFs of the marginal distributions (see Eq. 15). Similarly, as for the previously considered examples, the cases and are not analyzed in this paper.

In the case when the random vector is described by the PDF given in Eq. (14), then using formula (2) one obtains

| (17) |

The integral in Eq. (17) has no closed form and can be expressed by means of the Appel hypergeometric special function. However, one can obtain its value with numerical calculations.

If the random variables and are independent and are described by the Student’s t distributions of PDFs given in Eq. (15) with degrees of freedom and for X and Y distributions, respectively, then the PDF of the vector is given by a product of marginal densities of and . Thus, the product random variable has the following PDF for Ahsanullah_2014

| (18) |

Similarly as in the previous case, the above integral can only be calculated numerically, as it has no closed form representation.

When one considers the random vector of the two-dimensional Student’s t distribution defined by the PDF in Eq. (14), then the expectation (when ) and the variance (when ) of the random variable can be calculated based on its PDF (see Eq. (17)). In this case, there are no closed forms for the mentioned statistics. However, when and are independent random variables, then the expected value (if ) and the variance (if ) of the random variable are given by Ahsanullah_2014

| (19) |

The variance of the product of independent marginal variables is just a product of the individual variances. Moreover, it tends to the variance of one of the variables if the number of degrees of freedom of the second variable, or , goes to infinity. If both parameters, , then the variance of the product decreases to 1.

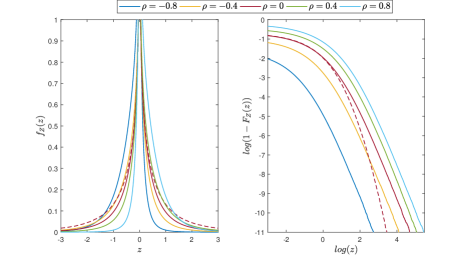

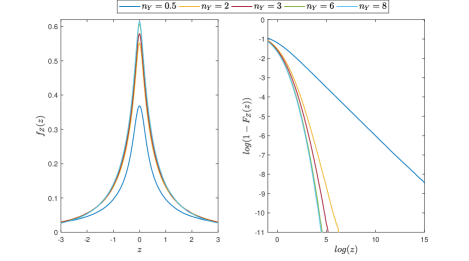

In Fig. 1 we demonstrate the PDF and the distribution tails (1-cumulative distribution functions, 1-CDFs) of the random variable that is a product of marginal random variables from the two-dimensional Student’s t distribution described by the PDF (14) for different values of the parameter. The resulting PDF is symmetric only if . Otherwise, it is right-skewed for and left-skewed for . The distribution tails are clearly heavier than in the Gaussian case. For the comparison, we also show the plots for the corresponding product of independent Student’s t marginal variables, i.e., with PDF given by Eq. (18). The resulting distribution is again symmetric, however, its tail is lighter than in the corresponding case of dependent marginal variables.

3.2 Pareto distribution

The two-dimensional Pareto distributed random vector with parameters has the following PDF Mardia_1962

| (20) |

The above parametrization corresponds to the Pareto distribution of the first kind paret . The parameter is responsible for the behavior of the distribution tail. The marginal distributions of and are given by

| (21) |

Note that the shape parameter is the same for both marginal distributions. For , the random variables and described by the PDF (20) are positively correlated. The covariance and correlation are given by, respectively

| (22) |

It is interesting to note that here the correlation between the marginal variables is governed by the shape parameter . As a consequence, with such parametrization, and are always positively correlated.

When the random vector is described by the PDF given in Eq. (20) using formula (2) one obtains

| (23) |

The integral in Eq. (23) has no closed form and can be expressed by means of the Appel hypergeometric special function. However, one can obtain its value with numerical calculations.

As one can see, the two-dimensional Pareto distribution defined by the PDF in Eq. (20) does not cover the case with uncorrelated marginal random variables. In the case when and are independent and are described by the Pareto distributions of the PDFs given in (21) with and , respectively, then the PDF of the vector is given by the product of the marginal PDFs, and .

Lemma 1.

Assume that the independent random variables and have Pareto distribution with parameters and , respectively. Then, for , the random variable defined in (1) has the following PDF

| (24) |

When the PDF of has the following form

| (25) |

Proof: The proof comes directly from formula (3) and the fact that the PDF of the random vector is given by the product of marginal PDFs of and for and . .

When one considers a random vector of the two-dimensional Pareto distribution defined by the PDF in Eq. (20), then there are no closed forms for the expectation (when ) and the variance (when ) of the random variable . However, when and are independent random variables, then the expected value and the variance of the random variable are given by Mardia_1962

| (26) | ||||

| (27) |

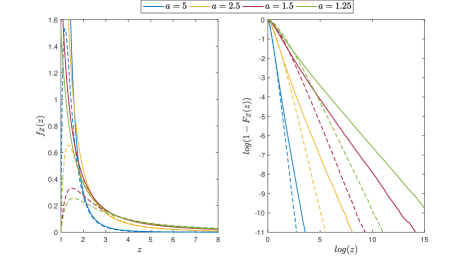

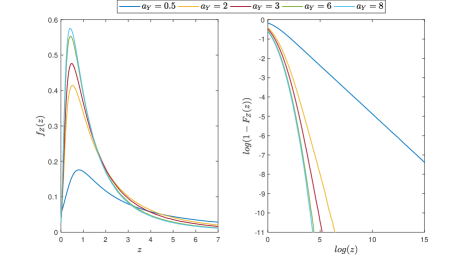

In Fig. 2 we plot the PDF and the corresponding distribution tail of the random variable that is a product of marginal random variables from the two-dimensional Pareto distribution described by the PDF (20) for different values of the parameter. Recall that the correlation (if exists) is directly related to the shape parameter , i.e. . So it is influenced by the distribution tails. With larger (lower ) the probability of extreme observations becomes lower. In all cases, the distribution tails behave like a power function with a clear linear shape in the double logarithmic scale. For comparison, we also show the plots for the corresponding product of independent Pareto marginal variables. In this case, the probabilities of extreme observations are lower than for the corresponding dependent Pareto distribution, but the power tail behavior is preserved.

4 Product of finite- and infinite-variance distributed random variables

The distribution of the random variable that arises as a product of two other random variables belonging to different families of distributions is of considerable importance and current interest in various applications. In this section, we examine the case when one of the marginal random variables is finite-variance distributed, while the second one belongs to the infinite-variance class. The product random variable shares some properties of both marginal variables, but on the other hand it exhibits additional interesting features. In this section, we assume that the marginal random variables are independent.

4.1 Gaussian and Student’s t distributions

We assume that the one-dimensional random variable has the Gaussian distribution with parameters and , while the one-dimensional random variable has the Student’s t distribution with the PDF given in Eq. (15) with . We assume that and are independent, thus the PDF of the random vector is just the product of the corresponding marginal PDFs of and . Using Eq. (3) one obtains the PDF of the random variable

The PDF of has no closed form representation and its calculation requires numerical computation of the integral in Eq. (4.1). Using the fact that for independent random variables the expected value of the product is the product of expected values, one can easily show that

| (29) |

when . The expectation and the variance of the product are simply the products of the corresponding moments of the marginal variables. Note that the variance decreases to with .

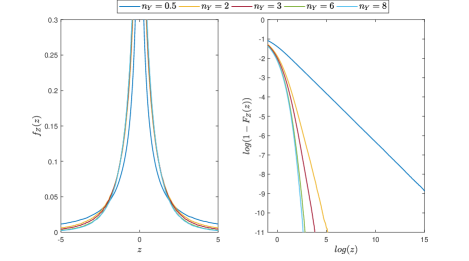

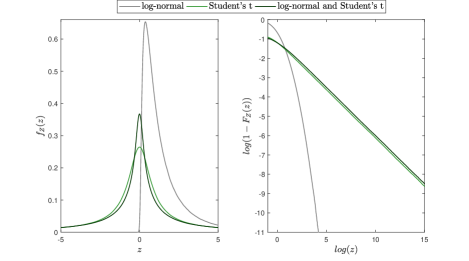

In Fig. 3 we plot the PDF and the corresponding distribution tail of the random variable that is a product of two independent random variables from the standard Gaussian (i.e. ) and Student’s t distributions for different values of the parameter. The resulting distribution is symmetric around zero. The shape of its tail is clearly dependent on the value of the parameter. For larger values of the tails are close to the Gaussian ones, while for lower they become much heavier, resembling rather the Student’s t tails. These three distributions, namely, the Gaussian, Student’s t and their product, are compared in Fig. 4. One can see that the product has a lighter tail than the Student’s t distributed random variable but a heavier tail than the Gaussian one.

4.2 Gaussian and Pareto distributions

Assume that is a Gaussian distributed random variable with parameters and and is a Pareto distributed random variable with parameters and . Moreover, we assume that and are independent.

Lemma 2.

The random variable defined as a product of and has the following PDF

| (30) |

where is the Gamma function and is the upper incomplete Gamma function defined as .

The proof of this lemma is given in Appendix A.

Using the fact that when , for we have

| (31) |

This indicates that the PDF of has power-law behavior and thus in the considered case the Pareto distribution dominates the tail behavior.

The expected value of in the considered case, when , is equal to zero and the variance of , if is given by

| (32) |

The variance decreases to the product of the marginal variables scale parameters squares, , as the Pareto shape parameter .

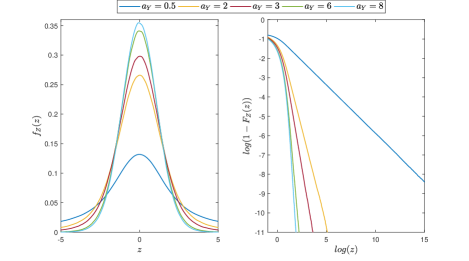

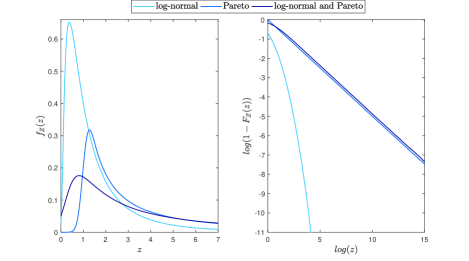

In Fig. 5 we plot the PDF and the corresponding distribution tail of the random variable that is a product of two independent random variables from the Gaussian and Pareto distributions for different values of parameter. Moreover in Fig. 6 we demonstrate the comparison of the PDFs and distribution tails of and , and the corresponding random variable for selected values of the parameters. One can see that the product has a lighter tail than the Pareto distributed random variable but a heavier tail than the Gaussian one. However, the power-law behavior, which corresponds to Eq. (31), can be easily observed.

4.3 Log-normal and Student’s t distributions

In this section, we assume that the one-dimensional random variable has the log-normal distribution with parameters and , while the one-dimensional random variable has the Student’s t distribution with the PDF given in Eq. (15) with . We assume that and are independent. Using Eq. (3) one obtains that the PDF of the random variable is given by

| (33) | ||||

The PDF given in Eq. (33) has no closed form representation and requires numerical calculations. However, using the independence assumption, one can easily show that

| (34) |

when . Similarly as for the Gaussian-Student’s t case, the variance decreases to the variance of with .

In Fig. 7 we plot the PDF and the corresponding distribution tail of the random variable for different values of the parameter, while in Fig. 8 we show a comparison of these three distributions. The picture is similar as the one obtained for the Gaussian - Student’s t case (see Fig. 3) with slightly heavier tails, especially for higher values of parameters.

4.4 Log-normal and Pareto distributions

As the last case, assume that is a log-normally distributed random variable with parameters and and is a Pareto distributed random variable with parameters and . Moreover, assume that and are independent.

Lemma 3.

The random variable defined as a product of and has the following PDF

where and are the PDF and CDF of the standard Gaussian distribution, respectively.

The proof of this lemma is presented in Appendix B.

The expected value of (when ) and the variance of (when ) are given by

Here, both marginal variables can take only positive values. Hence, the product variable is also positive and its expected value (if it exists) is greater than 0, . The expected value, as well as, the variance of are the products of the corresponding moments of the marginal distributions. Their existence is directly related to the existence of the moments of the Pareto marginal distribution.

In Fig. 9 we plot the PDF of the random variable and the corresponding distribution tail for different values of parameter, while in Fig. 10 we demonstrate the comparison of the , and distributions. As can be observed the tail parameter of the marginal Pareto distribution has a large impact on the tail of the product distribution.

5 Parameters estimation - simulation study

Based on the formulas for the PDF, , derived in the previous sections, we illustrate how the parameters of the product distribution can be estimated. To this end, we simulate samples of random vectors from the analyzed distributions and calculate the product of each simulated pair, . The Gaussian random vectors are generated using the Cholesky decomposition. The simulation of the vectors from the log-normal and dependent Student’s t distribution is based on the relation with the Gaussian distribution. In the case of dependent Pareto variables, the method based on conditional distributions is used, based on the fact that . First, is generated using the marginal distribution . Next, is generated using the conditional distribution with from the first step. For both steps, the inverse CDF method is applied. The independent Student’s t, independent Pareto, Gaussian-Student’s t and Gaussian-Pareto vectors simulation is based on the corresponding one-dimensional distributions.

The estimation of parameters is based on the maximum likelihood method. Thus, we have

| (36) |

where is the vector of parameters and is the corresponding product probability density function. Since analytical solutions do not exist in any of the considered cases, the maximization is performed numerically. Note that for the product of the multivariate Gaussian distribution with the method of moments estimators can be also straightforwardly derived, using the exact formulas for the moments. Note also that the scale parameters of the individual marginal distributions can not be inferred separately from the product, as they jointly yield the scale of the resulting one-dimensional variable, e.g., for the Gaussian distribution we have , for the log-normal distribution , while for the independent Pareto .

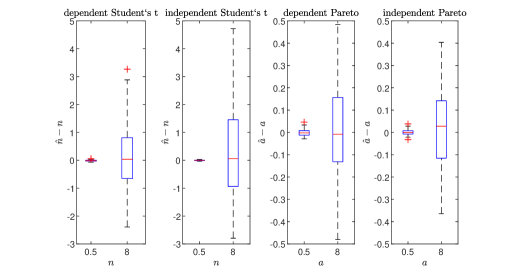

In Fig. 11 we plot the boxplots of the errors of the shape parameter estimation for the product of the Student’s t (i.e., ) and Pareto (i.e. ) distributions. The dependent variables case (see Eq. (15) for Student’s t and Eq. (21) for Pareto) as well as the independent one (see Eq. (18) for Student’s t and Lemma 1 for Pareto) are considered. The other parameters are set to , and . In the independent Pareto case, the same shape parameter for both variables, , is considered. The boxplots are plotted for two simulated values of the shape parameter, namely, or and or . The obtained error distribution is spread around 0, with much larger deviations in the lighter tails case (i.e., and ). Such an effect might be caused by the fact that for larger values of the shape parameters the differences between distributions become smaller. In the case of the Student’s t distribution, the errors are not symmetric around zero with more cases of overestimation of the parameter . In the case of the Pareto distribution, there is no visible asymmetry.

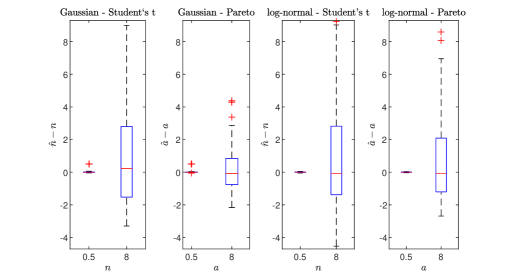

Finally, in Fig. 12 we plot the boxplots of the errors of the shape parameters for the products of different marginal distributions, namely, the Gaussian - Student’s t, the Gaussian - Pareto, the log-normal - Student’s t and the log-normal - Pareto case. For the Gaussian and log-normal distributions we assume and , while the scale parameter of the Pareto distribution is equal . The errors are analyzed in two cases representing the infinite- ( for Student’s t distribution or for Pareto distribution) as well as finite-variance ( for Student’s t distribution or for Pareto distribution). The obtained estimation results are similar to the purely Student’s t or Pareto distributions (see Fig. 11). The higher errors are obtained for the higher values of the and parameters. Furthermore, the effect of overestimation of the Student’s t degrees of freedom can be noticed.

6 Real data application - distribution of electricity transaction values

In this section, we demonstrate the possible application of the theoretical results discussed in the previous sections to a real-data case. We use the transactions data from the German electricity market settled in the EPEX energy exchange. Each transaction is characterized by two values: the volume of sold energy (in MWh) and the price (in EUR/MWh). The final transaction value, being the amount of the total profit for the energy seller or a total cost for energy buyer, is the product of these two variables. Hence, knowing the product distribution is important for profit/costs planning in energy companies.

The data comes from a continuous trading on the intraday market. A transaction is settled each time two bid and sell offers meet. Hence, each data point corresponds to a different offer and usually a different market participant, so the sample points can be assumed independent. One of the main characteristics of the electricity market is its seasonality on the yearly, weekly, and daily level RWeron_energy . To avoid the possible influence of the transaction time on its distribution, we analyze separately the transactions being settled in different hours. The data points within one hour are assumed to be identically distributed.

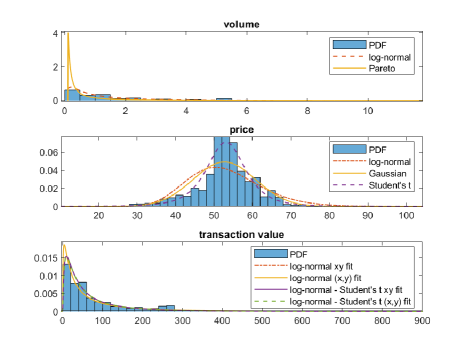

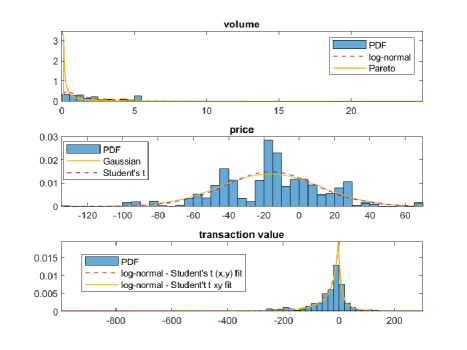

We analyze vectors , where is the volume and is the price of the -th transaction within a given hour and is the number of transactions during this hour. We also analyze a sample of the transaction values being a product of each and , i.e. . For an illustration, we have chosen two representative hours, namely, hour 14 from 20th December 2020 and hour 8 from 15th March 2020. The first case shows a typical picture that is observable for most hours, while the second case illustrates the less frequent but typical for the German electricity market situation where some of the transaction prices are negative. Negative prices are a unique feature of electricity markets caused by the limited ability to store electricity and the fast development of production from renewable energy sources NegativePrices . If there is a short-term oversupply of electricity due, for example, to wind or solar production, the producers from conventional energy sources might be willing to pay for the reception of electricity instead of stopping the production units.

The corresponding PDFs are plotted in Figs. 13 and 14 for 20th December and 15th March, respectively. The correlation between the volume and price samples is not significant. Hence, we assume that the corresponding and random variables are not correlated. Since the volume can not be negative, the only distributions from the ones analyzed in the paper that can be fitted to the volume sample are the log-normal and Pareto. For the price sample, the Gaussian, log-normal (for positive data) and Student’t t with location and scale parameters are fitted. The resulting densities are plotted in the corresponding panels of Figs. 13 and 14.

For both analyzed hours, the log-normal distribution density function resembles the shape of the volume histogram. On the other hand, the Pareto distribution clearly overestimates the probability of small volumes. Hence, for the product analysis, we will only consider the log-normal distribution for the first coordinate. Looking at the price distribution for the data from hour 14 on 20th December 2020 (see Fig. 13), we can observe that only the Student’s t PDF resembles the shape of the obtained histogram, especially around the mean, where the Gaussian and log-normal probabilities are underestimated. The picture for the second considered data set, i.e., the price distribution from hour 8 on 15th March 2020 (see Fig. 14), is different. First, there is a significant probability of obtaining negative values. Hence, in this case we do not fit the log-normal distribution, which can take only positive values. Second, the Gaussian and the Student’s t PDF produce a similar fit. Recall that with increasing degrees of freedom in the latter case, the distribution tends to the Gaussian one. The tails for this hour are lighter than for the 20th December data. Overall, from the set of considered distributions, only the Student’s t can be well fitted to the prices from both analyzed hours.

Next, we analyze the resulting product, i.e., the transaction value distribution. To this end, we proceed in two ways. Firstly, we use the parameters estimated for the one-dimensional samples of the random variables and (i.e., volumes and prices) and use the formulas for the product PDF derived in Sections 2-4. Based on the results obtained for the one-dimensional samples we show only the product of log-normal distribution or log-normal and Student’s t distribution (log-normal-Student’s t). Secondly, we also fit the derived PDFs to the sample of the product . We can observe that the final product PDF obtained by these two ways in the case of log-normal-Student’s t overlaps and resembles the shape of the sample histogram, confirming a good fit. As mentioned before, due to the negative prices apparent in the second analyzed hour, the log-normal distribution can be fitted only to the first dataset. In this case, we can observe a discrepancy between the density obtained using the coordinates and its product . Comparing the obtained shapes of the distribution for both hours, we can see a clear difference between these cases. The transaction values for hour 8 on 15th March 2020 take both negative and positive values, with long left tails of the distribution. On the other hand, there are no negative transaction values for hour 14 on 20th December 2020 and the distribution is right skewed. Overall, only the log-normal-Student’s t case from the considered distributions set is flexible enough to be reasonably applied to both analyzed representative hours and the obtained distribution resembles the data well.

7 Conclusions

In this paper, we have discussed the distribution of a random variable that is a product of two continuous random variables. The main attention was paid to the influence of the parameters of the marginal random variables on the final product characteristics. We have considered exemplary distributions belonging to the classes of finite as well as infinite-variance distributions. For both cases, we have discussed how the correlation coefficient between the marginal random variables influences the probabilistic properties of the product. In the case of the Gaussian and log-normal distributions, the non-zero correlation coefficient indicates the statistical dependence of the random variables, while in the second case, i.e., the Student’s t and Pareto distributions, this statement is not true. The most interesting case was the product of the random variables coming from different classes of distributions, for which we have derived the explicit form of the PDF for the Gaussian-Pareto and the log-normal-Pareto case.

The theoretical results were applied in the proposed estimation methodology. We used a general approach based on the maximum likelihood technique. The presented Monte Carlo simulations clearly indicate the effectiveness of the algorithm. Finally, the real data analysis was presented. Based on the data from continuous trading on the German energy market, we have shown a good reasonable fit of the product of log-normal and Student’s t distribution to the transaction values. Since the transaction value is the final profit/cost for a trader, finding a proper density describing its distribution, which is also consistent with the prices and volumes data, can help an energy market participant in strategy planning.

Another potential application of the proposed methodology could be the market risk area in metals and mining business. Mining companies are exposed to two or more market risk factors, like metal prices and currency exchange rates. These factors behavior is often characterized by non-Gaussian distributions, what can be reflected by the discussed in this paper, log-normal and Student’s t distributions. From a business perspective of an international mining company, which trades the excavated resources in different than national currency, it is valuable to analyse the selling price also in the national currency, that is a product of the commodity price (usually quoted in USD) and USD/national currency exchange rate. A case study related to the modelling of the copper prices for a polish mining company one can find in reso . It has been shown that the behavior of metal price in PLN exhibits specific characteristics, that follow directly from the properties of the individual variables. These properties need to be reflected in optimizing strategies aimed at mitigation of the unacceptable for company market risk.

Acknowledgments

The work of A.W. was supported by National Center of Science under Opus Grant 2020/37/B/HS4/00120 ”Market risk model identification and validation using novel statistical, probabilistic, and machine learning tools”. J.J. acknowledges a support of NCN Sonata Grant No. 2019/35/D/HS4/00369.

Data Availability

The datasets generated during the current study are available from the corresponding author on reasonable request. The energy transactions data analysed in this study are available from the EPEX SPOT exchange.

References

- \bibcommenthead

- (1) Nadarajah, S.: Exact distribution of the product of two or more logistic random variables. Methodology and Computing in Applied Probability 11, 651–660 (2008)

- (2) Nadarajah, S.: Some algebra for Pearson type vii random variables. Bulletin of The Korean Mathematical Society 45, 339–353 (2008)

- (3) Nadarajah, S.: On the product xy for some elliptically symmetric distributions. Statistics & Probability Letters 75, 67–75 (2005)

- (4) Garg, M., Sharma, A., Manohar, P.: The distribution of the product of two independent generalized trapezoidal random variables. Communications in Statistics - Theory and Methods 45, 6369–6384 (2016)

- (5) M. Ahsanullah, M.S. B. M. Golam Kibria: Normal and Student’s T Distributions and Their Applications, pp. 7–102. Atlantis Press, Netherlands (2014)

- (6) Nadarajah, S., Dey, D.K.: On the product and ratio of t random variables. Applied Mathematics Letters 19(1), 45–55 (2006)

- (7) Li, Y., He, Q., Blum, R.S.: On the product of two correlated complex Gaussian random variables. IEEE Signal Processing Letters 27, 16–20 (2020)

- (8) Seijas-Macías, A., Oliveira, A.: An approach to distribution of the product of two normal variables. Discussiones Mathematicae Probability and Statistics 32, 87–99 (2012)

- (9) Nadarajah, S.: The product t density distribution arising from the product of two Student’s t PDFs. Statistical Papers 50, 605–615 (2009)

- (10) Malik, H.J., Trudel, R.: Probability density function of the product and quotient of two correlated exponential random variables. Canadian Mathematical Bulletin 29(4), 413–418 (1986)

- (11) Homei, H.: The stochastic linear combination of dirichlet distributions. Communications in Statistics - Theory and Methods 50, 2354–2359 (2019)

- (12) Tang, J., Gupta, A.: On the distribution of the product of independent beta random variables. Statistics & Probability Letters 2, 165–168 (1984)

- (13) Bhargava, R., Khatri, C.: The distribution of product of independent beta random variables with application to multivariate analysis. Annals of the Institute of Statistical Mathematics 33, 287–296 (1981)

- (14) Nadarajah, S.: On the product of generalized Pareto random variables. Applied Economics Letters 15, 253–259 (2008)

- (15) Pham-Gia, T., Turkkan, N.: The product and quotient of general beta distributions. Statistical Papers 43(4), 537–550 (2002)

- (16) Nadarajah, S., Kotz, S.: A note on the product of normal and laplace random variables. Brazilian Journal of Probability and Statistics 19(1), 33–38 (2005)

- (17) Nadarajah, S., Kotz, S.: On the linear combination, product and ratio of normal and Laplace random variables. J. Frankl. Inst. 348, 810–822 (2011)

- (18) Nadarajah, S., Kotz, S.: On the product and ratio of gamma and Weibull random variables. Econometric Theory 22(2), 338–344 (2006)

- (19) Nadarajah, S., Kotz, S.: On the product and ratio of gamma and beta random variables. Allgemeines Statistisches Archiv 89, 435–449 (2005)

- (20) Nadarajah, S.: Sum, product and ratio of Pareto and gamma variables. Journal of Statistical Computation and Simulation 80, 1071–1082 (2010)

- (21) Galambos, J., Simonelli, I.: Products of Random Variables: Applications to Problems of Physics and to Arithmetical Functions (1st Ed.). CRC Press, Boca Raton (2004)

- (22) Podolski, H.: The distribution of a product of n independent random variables with generalized gamma distribution. Demonstratio Mathematica 4, 119–124 (1972)

- (23) Wilson, P.S., Toumi, R.: A fundamental probability distribution for heavy rainfall. Geophysical Research Letters 32(14) (2005)

- (24) Cigizoglu, H.K., Bayazit, M.: A generalized seasonal model for flow duration curve. Hydrological Processes 14(6), 1053–1067 (2000)

- (25) Ly, S., Pho, K.-H., Ly, S., Wong, W.-K.: Determining distribution for the product of random variables by using copulas. Risks 7(1) (2019)

- (26) Salo, J., El-Sallabi, H.M., Vainikainen, P.: The distribution of the product of independent Rayleigh random variables. IEEE Transactions on Antennas and Propagation 54(2), 639–643 (2006)

- (27) Yang, Y., Wang, Y.: Tail behavior of the product of two dependent random variables with applications to risk theory. Extremes 16, 55–74 (2013)

- (28) Bhargav, N., da Silva, C.R.N., Chun, Y.J., Leonardo, E.J., Cotton, S.L., Yacoub, M.D.: On the product of two – random variables and its application to double and composite fading channels. IEEE Transactions on Wireless Communications 17(4), 2457–2470 (2018)

- (29) Nadarajah, S., Kotz, S.: Sociological models based on Fréchet random variables. Quality & Quantity 42, 89–95 (2008)

- (30) Rohatgi, V.K., Saleh, A.K.M.E.: An Introduction to Probability and Statistics. Wiley Series in Probability and Statistics. John Wiley & Sons, New Jersey (2015)

- (31) Mardia, K.V.: Multivariate Pareto distributions. The Annals of Mathematical Statistics 33(3), 1008–1015 (1962)

- (32) de la Peña, V.H., Ibragimov, R., Sharakhmetov, S.: Characterizations of joint distributions, copulas, information, dependence and decoupling, with applications to time series. Lecture Notes-Monograph Series 49, 183–209 (2006)

- (33) Jeong, B., Lee, W., Kim, D.-S., H, H.S.: Copula-based approach to synthetic population generation. PLoS ONE 11(8), 0159496 (2016)

- (34) Wyłomańska, A., Chechkin, A., Gajda, J., Sokolov, I.M.: Codifference as a practical tool to measure interdependence. Physica A: Statistical Mechanics and its Applications 421, 412–429 (2015)

- (35) Slezak, J., Metzler, R., Magdziarz, M.: Codifference can detect ergodicity breaking and non-gaussianity. New Journal of Physics 21(5), 053008 (2019)

- (36) Samorodnitsky, G., Taqqu, M.: Stable Non-Gaussian Random Processes: Stochastic Models with Infinite Variance. Chapman and Hall, New York (1994)

- (37) Nowicka, J.: Asymptotic behavior of the covariation and the codifference for ARMA models with stable innovations. Communications in Statistics. Stochastic Models 13(4), 673–685 (1997)

- (38) Roussas, G.G.: Joint and conditional p.d.f.’s, conditional expectation and variance, moment generating function, covariance, and correlation coefficient. In: An Introduction to Probability and Statistical Inference, 135–186 (2015)

- (39) Gaunt, R.E.: A note on the distribution of the product of zero-mean correlated normal random variables. Statistica Neerlandica 73(2), 176–179 (2018)

- (40) Aroian, L.A., Taneja, S.V., Cornwell, L.W.: Mathematical forms of the distribution of the product of two normal variables. Communications in Statistics - Theory and Methods 7(2), 165–172 (1978)

- (41) Craig, C.C.: On the frequency function of $xy$. The Annals of Mathematical Statistics 7(1), 1–15 (1936)

- (42) Aitchison, J., Ho, C.H.: The multivariate Poisson-log normal distribution. Biometrika 76(4), 643–653 (1989)

- (43) Yerel, S., Konuk, A.: Bivariate lognormal distribution model of cutoff grade impurities: A case study of magnesite ore deposit. Scientific Research and Essay 4(12), 1500–1504 (2009)

- (44) Lai, C.D., Balakrishnan, N.: Continuous Bivariate Distributions. Springer, New York (2009)

- (45) Cochran, W.G.: The distribution of quadratic forms in a normal system, with applications to the analysis of covariance. Mathematical Proceedings of the Cambridge Philosophical Society 30(2), 178–191 (1934)

- (46) Hossain, A.M., Zimmer, W.J.: Comparisons of methods of estimation for a Pareto distribution of the first kind. Communications in Statistics - Theory and Methods 29(4), 859–878 (2000)

- (47) Weron, R.: Modeling and Forecasting Electricity Loads and Prices : a Statistical Approach / Rafał Weron. Wiley finance series. John Wiley & Sons, Chichester, England; Hoboken, New York (2006)

- (48) August, B., Horsch, A.: Negative market prices on power exchanges: Evidence and policy implications from Germany. The Electricity Journal 33(3), 106716 (2020)

- (49) Bielak, L., Grzesiek, A., Janczura, J., Wyłomańska, A.: Market risk factors analysis for an international mining company. multi-dimensional heavy-tailed-based modelling. Resources Policy 74, 102308 (2021)

Appendix A

Proof of Lemma 2.

Let us first note that the CDF of is given by

| (37) |

Thus, the CDF of takes the form

We consider separately , and . For one obtains

Now, calculating the derivative of with respect to for one has

where is the upper incomplete Gamma function and is the lower incomplete Gamma function. For the CDF of is given by

Now, taking the derivative of with respect to for we obtain the following formula for corresponding PDF

The last case is . In this case, the CDF of is given by

One can also show that

Thus, finally we obtain the thesis.

Appendix B

Proof of Lemma 3.

Using the same reasoning as in the proof of Lemma 2 one obtains that the CDF of takes the following form for

Thus, from (37) we obtain for

Now, taking the substitution in the both above integrals, we obtain

To make the calculations simpler, in the first integral we put the substitution and in the second one . Then we obtain

Calculating the derivative of with respect to one has

where and are the PDF and CDF of the standard Gaussian distribution, respectively.