An SDP dual relaxation for the Robust Shortest Path Problem with ellipsoidal uncertainty: Pierra’s decomposition method and a new primal Frank-Wolfe-type heuristics for duality gap evaluation

Abstract

This work addresses the Robust counterpart of the Shortest Path Problem (RSPP) with a correlated uncertainty set. Since this problem is hard, a heuristic approach, based on Frank-Wolfe’s algorithm named Discrete Frank-Wolf (DFW), has recently been proposed. The aim of this paper is to propose a semi-definite programming relaxation for the RSPP that provides a lower bound to validate approaches such as DFW Algorithm. The relaxed problem results from a bidualization that is done through a reformulation of the RSPP into a quadratic problem. Then the relaxed problem is solved using a sparse version of Pierra’s decomposition in a product space method. This validation method is suitable for large size problems. The numerical experiments show that the gap between the solutions obtained with the relaxed and the heuristic approaches is relatively small.

keywords:

Robust Optimization , Robust Shortest Path Problem , Ellipsoidal Uncertainty , Discrete Frank-Wolfe , Uncertainty , SDP relaxation , Sparse computations1 Introduction

Robust combinatorial optimization consists in taking uncertainty into account in combinatorial optimization problems. For instance, the robust shortest path problem is the problem of finding the shortest route from a place to another, while the distance (either in terms of time or space) of the different parts of the road are uncertain. Many definitions of robustness have been proposed in the literature in the context of optimization. The three most common definitions in the context of combinatorial optimization have been formalized in [1]. These are absolute robust solution, robust deviation and relative robust solution. In all these cases, worst case behavior is considered. For these three definitions, an uncertainty set has to be defined. Many uncertainty sets exist, such as the interval uncertainty, discrete uncertainty, and ellipsoidal uncertainty [2]. Another family of definitions is scenario dependent. In these methods, a decision is taken conditional on the current scenario and the overall optimization problem boils down to a robust two-stage problem [3]. This family splits into the notions of K-adaptability [4], adjustable robustness, bulk robustness and recoverable robustness. In the case where the data can be considered as governed by a certain probability distribution with unknown parameters, distributionally robust optimization [5] is also an interesting approach. It consists in choosing the distribution that is most suitable given a robustness criterion. Yet another approach is the notion of almost robust solution [6] that is feasible under most of the realizations and that can use full, partial or no probabilistic information about the uncertain data. Let us also mention that other alternative generic approaches have also been proposed in the literature: in [7], a near-optimum solution for several scenarios. Another way to tackle uncertainty that is different from robust optimization is online optimization [8], where decisions are made iteratively, and at each iteration, the problem inputs are unknown, but the decision maker learns from the previous configuration before making his decision. After a decision is made, it is then assessed against the optimal one. Finally, let us add that uncertainty theory was used in another line of work as in [9], for instance. This theory has also been implemented in [10] in order to give what they call an uncertainty distribution in the case of the shortest path problem.

This work considers the absolute robust decision with the uncertainty in the cost function modelled by an ellipsoidal uncertainty set. The choice of the ellipsoidal uncertainty set is motivated as follows. Unlike the interval uncertainty set, it takes the correlation of the uncertain variables into account, it reduces the combinatorial aspect of the discrete set, it allows the user to control the level of risk that he is ready to take in order to have the right cost. Finally, it leads to a smooth form for the min-max formulation, as shown in Section 2.1. This smooth form is well known in portfolio optimization, and it is called mean-risk optimization [11]. In [1], it is demonstrated that the robust counterparts of easy problems are usually hard to solve, especially if the uncertainty set is not an interval, but is described by an ellipsoidal confidence region. In this case, the robust counterparts of even linear problems become non-linear. To solve these NP-hard problems, methods exist for the case of non-correlated variables, i.e., for axis-parallel ellipsoids [12, 13, 14, 15]. In the case of correlated variables, branch-and-bound methods exist, as well as improvements by better node relaxations [16]. A heuristic approach called DFW (Discrete Frank-Wolfe) for robust optimization under correlated ellipsoidal uncertainty based on Frank-Wolfe’s algorithm has been proposed in [17]. To the best of our knowledge, it is the first algorithm for robust optimization in the ellipsoidal uncertainty adapted for large size problems.

In order to validate heuristic approaches, one can compare to other exact or heuristic methods, give sub-optimality proofs, or compute lower/upper bounds depending whether it is a minimization or a maximization problem. For minimization problems, lower bounds can be obtained using relaxation schemes such as the ones obtained using Lagrangian dualizations [18] which often result in solving Semi-Definite Programming (SDP) Problems.

Semi-Definite Programming (SDP) is a particular class of convex optimization problems which appears in various engineering motivated problems, including the most efficient relaxations of some NP-hard problems such as often encountered in combinatorial optimization or Mixed Integer Programming [19]. SDP can be written as minimization over symmetric (resp. Hermitian) positive semi-definite matrix variables, with linear cost function and affine constraints, i.e., problems of the form:

| (1) |

where are given matrices. Compact SDPs can be solved in polynomial time. SDP was extensively studied over the last three decades since its early use which can be traced back to [20] and [21]. In particular, Linear Matrix Inequalities (LMI) and their numerous applications in control theory, system identification and signal processing have been a central drive for the use of SDP in the 90’s as reflected in the book [22]. One of the most influential paper for that era, is [23] in which SDP was shown to provide a 0.87 approximation to the Max-Cut problem, a famous clustering problem on graphs. Other SDP schemes for approximating hard combinatorial problems have subsequently been devised for the graph coloring problem [24], for satisfiability problem [23, 25]. These results were later surveyed in [26, 27] and [28]. Numerical methods for solving SDP’s are manifold and various schemes have been devised for specific structures of the constraints. One of these families of methods is the class of interior point methods [29]. Such methods are known to be of the most accurate type, but suffer from being not scalable in practice. Another family of methods is based around the alternating direction method of multipliers (ADMM) technique [30]. ADMM approaches are usually faster as they can be implemented in a distributed architecture. As such, they often appear to be faster and more scalable than interior point methods at the price of a worse accuracy. Other methods can also be put to work as the method of Pierra [31] upon which the present work further elaborates.

In this work, the quality of the solution of the DFW heuristic approach is evaluated by computing a lower bound. This lower bound is obtained by a bidualization of the robust problem, that is a SDP relaxation. In order to solve the corresponding SDP problem, the applied method is the decomposition through formalization into a product space proposed in [31], with a sparse computation to reduce the memory storage necessity. It is shown that this algorithm is a validation method that is also adapted for large size problems.

The paper is organized as follows: Section 2 presents the robust shortest path problem, and recalls two approaches to solve the problem; in particular we oppose the classical CPLEX exact solving approach to an efficient heuristic algorithm, the so-called Discrete Frank Wolfe (DFW) algorithm, proposed in a previous paper [17] that performs well on simulations and is scalable. Since the exact approach is costly, the main contribution of this paper is to propose a validation method for DFW by an efficient relaxation method (SDP) that provides a lower bound for the cost function. This is described in Section 3. Finally, Section 4 numerically validates this approach by showing that the corresponding gap between the solutions obtained with the relaxed and the proposed heuristic approaches is relatively small.

Notation. Throughout the paper, the following matrix notations have been used. Unless stated otherwise, all vectors belonging to for some are column vectors. Furthermore, for some matrix , denotes, for all integers and , the sub-block containing the entries in the rows to and columns to . (resp. ) is short for (resp. ). is the transpose of . Finally, is the block of dimension with zeros everywhere and is the identity block of dimension .

2 The robust shortest path problem

In this section, the robust shortest path problem with the ellipsoidal uncertainty set is stated. The problem form to solve is then given in order to propose a robust solution. Both an exact and a heuristic method for solving this problem are presented.

2.1 Problem statement

Consider the linear programming form of the shortest path problem [32], that can be written as

| (2) |

with being the cost vector and , where is the so-called incidence matrix corresponding to the underlying graph and is the vector with vertices that defines the source and the destination nodes.

This paper considers the particular situation where the cost vector is uncertain, i.e., lies in an uncertainty set . Then the robust counterpart of Problem (2) is the following

| (3) |

In the particular case where the cost vector is a random vector following a multinormal distribution with expectation and covariance matrix , then belongs to the confidence set with probability , where is the following ellipsoid

| (4) |

with being a function of that represents the level of confidence.

One interesting fact about the ellipsoidal uncertainty set is that the - problem (3) can be reduced to a non-linear programming problem (for more details see Section 2.2.1.1 of [33]):

| (5) |

Without loss of generality, it is assumed throughout this paper that . This amounts to replace by , so that Problem (5) reads

| (6) |

where .

The remaining part of this section addresses the robust shortest path problem by solving Problem (6). This problem is a non-linear non-convex problem, so it is challenging to find an appropriate method to solve it.

2.2 Exact method for solving the robust problem

In order to solve the robust shortest path problem, solving Problem (6) is needed. One possible way is to solve this problem in two steps. First, rewrite it as a Binary Second Order Cone Programming problem (BSOCP) (Problem (7)). The solution is obtained by solving Problem (7) in the second step. Problem (7) is stated as follows:

| (7) | ||||

| s.t. | ||||

with being a second order cone. The calculations are detailed in [17, Section 4].

Problem (7) can be solved by branch-and-bound methods, and existing BSOCP solvers such as CPLEX [34] solve this problem. However, for large size problems, it is no longer possible to use branch-and-bound methods, since their time complexity is exponential, and in their worst case, they may need to explore all the possible permutations of the combinatorial problem at hand. Thus a heuristic algorithm named DFW Algorithm (Discrete Frank-Wolfe) has been proposed in [17] and is presented in the following section.

2.3 A heuristic approach based on Frank-Wolfe

As proved in the previous section, solving the robust shortest path problem with a scalable heuristic approach seems mandatory for large size problems. The heuristic algorithm proposed in [17] to solve Problem (6) is based on the Frank-Wolfe algorithm [35]. On one side, the classical Frank-Wolfe (FW) algorithm is a convex optimization algorithm that proceeds by moving towards a minimizer of the linear appromixation of the function to minimize. The heuristic DFW algorithm in turn uses the classical Frank-Wolfe algorithm to minimize over the convex hull of , and due to the integrality of the relaxation, the intermediate gradient steps are feasible solutions for the discrete problem. These gradient steps are good feasible solutions. DFW Algorithm returns the best of these intermediate steps as an approximate solution: more concretely, it is the one that minimizes the objective function among the discovered feasible solutions. DFW Algorithm is detailed in Algorithm 1.

Note the optimal solution of Problem (6), and the approximate solution given by DFW Algorithm. The aim of the next section is to evaluate the quality of the solution .

3 A lower bound by SDP relaxation

The first way to evaluate the quality of the solution given by the DFW Algorithm or any other approach that solves Problem (6) is to compare it with the solution given by the optimal solution of the BSOCP using an exact solver like CPLEX (see the previous section). Since this approach is no longer usable when considering large size problem, an other option to evaluate the quality of the solution has to be proposed. To do so a lower bound by bidualization with an efficient algorithm to solve the corresponding problem is presented in this section.

3.1 Bidualization of a quadratic problem

Before giving a lower bound for Problem (6), a lower bound by bidualization for any quadratic problem is stated. Then, Problem (6) is written as a quadratic problem following the general form.

A lower bound for Quadratic Programming problems is proposed in [26]. This lower bound is the solution of a bidual problem that is written in the form of a Semi-Definite Programming (SDP) problem. This bidualization procedure is nothing but the very known SDP relaxation, as in the following.

Consider the quadratic problem with constraints:

| (8) | |||

where

are quadratic functions defined on , being the dimension of the problem, with the matrices lying in the set of symmetric matrices of size , the values in , and the values in ; it is assumed that .

Applying Lagrangian duality on Problem (8), and applying duality again reproduces the bidual problem of (8) that is given by

| (9) | |||

| (12) |

where the inner product between the matrices and of size is defined by

| (13) |

and where the notation means that is positive semi-definite, for any symmetric matrix .

This bidualization has another interpretation: it is also a direct convexification of Problem (8). Indeed, noticing that (8) can also be written as

| (14) | |||

by setting , and writing a quadratic form as , and then relaxing the nonconvex constraint to , that is convex with respect to . Then, the previous bidualization can be seen as a convexification.

Thus, if is the optimal solution of (8), and is the optimal solution of (9), then the following inequality holds (see [26, Proposition 4.5]):

| (15) |

Hence, solving the SDP problem (9) enables to obtain a lower bound for . In general, this technique is used for the validation of a heuristic method without comparison with the optimal solution. In this case, Problem (9) is easier, since it is a convex problem. Solving (9) gives the lower bound . The distance between the lower bound and the heuristic solution indicates how far this heuristic solution is from the optimal solution. In other research directions, lower bound can be coupled with a branch-and-bound algorithm for computing an optimal solution. However, the focus in the present paper is on proposing a much cheaper heuristics than the branch-and-bound approach, namely the DFW method. In order to validate this heuristics, the quality of the obtained primal solution using a lower bound obtained by solving a polynomial time SDP problem has been evaluated.

3.2 Using the bidualization to compute a lower bound

3.2.1 Bidualization of the addressed problem

This section aims to show how to use the bidualization, explained in Section 3.1, to compute a lower bound for (6). Recall that Problem (6) has another formulation, that is a BSOCP (Problem (7)). Rewriting (7) more explicitly gives

| (16) | ||||

| s.t. | ||||

First, the BSOCP formulation (16) of (6) can be written as a Binary Quadratic Problem (BQP) since the variables and in (16) are such that and for any and . Thus, Problem (16) is equivalent to

| (17) | ||||

| s.t. | ||||

In order to formulate (17) as a problem in the form (8), all the constraints have to been written in the form of equalities. First, the following equivalence holds

Second, the inequality can be transformed into an equality by considering additional variables and as follows:

The problem (17) is then equivalent to the following problem

| (18) | ||||

| s.t. | ||||

Now, Problem (18) is written in a more compact way , i.e., in function of one vector variable , and write each constraint individually. This makes Problem (18) equivalent to

| (19) | ||||

| s.t. | ||||

where the vectors and matrices that appear in Problem (19) are defined as follows

-

1.

the vector of size is defined block-wise as , so that if ,

-

2.

for any , is such that if , and if else, so that , and for ,

-

3.

is an matrix such that and elsewhere, so that and ,

-

4.

for any , is a matrix, such that if and , and if else. So that , , and for ,

-

5.

is an matrix such that and the other entries are zeros, so that ,

-

6.

is an matrix such that and the other entries are zeros, so that .

Then, the bidual problem of (19) is the following

| (20) | ||||

| s.t. | ||||

| (23) |

The last step consists in writing (20) in a compact way with the following change of variable

| (26) |

This can be done using the following changes:

-

1.

For any , write , where is defined by

(29) -

2.

For any , write , where is defined by

(32)

As a result of this change of variable, the bidual problem of (17) can be written as an SDP problem in the more compact way:

| (33) | ||||

| s.t. | ||||

where is defined as follows

| (42) |

that is , , , , and zero elsewhere. The matrix is defined for all by

| (51) |

that is , , and zero elsewhere. The matrix is defined for all by

| (61) |

that is , , , , and zero elsewhere. Also, define the matrix by

| (68) |

that is is the identity matrix of dimension , , and zero elsewhere. Next, for the definition of the matrices , for every , is a matrix such that , and . Finally, is a matrix such that , and .

3.2.2 The biduality gap

Now that the bidual problem (33) of (17) is stated, the lower bound inequality (15) reads here

where denotes the optimal value for a given problem (P). As a result of the equivalence between (6) and (17), val((17)) equals . This gives us an additional inequality:

Or, written differently,

| (69) |

Thus, is a lower bound that allows to evaluate the quality of the heuristic solution of the DFW Algorithm. Hence, the biduality gap is defined as

| (70) |

A corresponding relative gap is defined as

| (71) |

More explicitly, the validation process is the following: first solve the robust shortest path problem using the heuristic approach DFW and find a heuristic solution . Then evaluate the quality of this solution using Inequality (69) by proceeding as follows. Then, is computed, and if the gap between and is small, then the gap between and is small too, since . The only missing step now is to compute . The next section shows how to solve (33) to compute .

3.3 Solving the SDP problem

The above sections aim at showing that a lower bound for the robust shortest path problem is the solution of an SDP problem that has to be solved. As detailed in the introduction, interior point methods are used to solve SDP problems, which gives a first way to solve the SDP problem (33): an option is to implement this resolution using the CVXPY Python package [36] which is a Python-embedded modeling language for convex optimization problems. CVXPY converts the convex problems into a standard form known as conic form, a generalization of a linear program. The conversion is done using graph implementations of convex functions. The resulting cone program is equivalent to the original problem, so solving it gives a solution of the original problem. In particular, it solves the semi-definite programs using interior point methods. It is rather simple to use CVXPY to solve the SDP problem (33): define the function to minimize, the constraints of the problem, and then launch the solver. However this simplicity has a price: the problem definition requires the storage of the matrices that describe the problem. More precisely, there are matrices of dimension : one matrix to define the objective function, and matrices for the constraints. This is a significant issue because of the storage necessity, especially in large size problems. To illustrate how big the storage grows with respect to the problem size, take a medium grid graph with nodes (, ). This problem size requires the storage of matrices of dimension (this takes 3.45 Gigabytes in double precision). A relatively big grid graph with nodes (, ) needs the storage of matrices of dimension (this takes 17.5 terabytes in double precision). But since most of the matrices are sparse, another efficient approach is proposed, where sparse computations are done, which allows us to avoid this main drawback considering the matrices storage. Before tackling this memory storage issue, the following describes the practical algorithm that has been implemented in order to find this .

3.3.1 Pierra’s Decomposition through formalization in a product space

Consider a general minimization problem in a finite dimensional Hilbert space equipped with a norm . Suppose that the goal is to solve the problem

| (72) | ||||

| s.t. |

where is a differentiable function, and are convex subsets of . Exploiting the fact that the constraint space is an intersection of convex sets, Pierra in [31] proposes a method for solving Problem (72). This is described in Algorithm 2, where, for a function , the proximal function associated to , which is defined in [31, Theorem 3.2], is given by

| (73) |

and where , referring to the indicator function for the set , equals if and otherwise. Finally, is a tuning parameter for the minimization step which value is small (e.g. ).

The idea of this algorithm comes from the formalization of the constraint set introducing the set . Indeed, defining , and denoting the diagonal convex D as the subspace of H of all the vectors of the form , with , implies that Problem (72) can be reformulated in H as a minimization problem over . To solve (72), Pierra’s Algorithm can be described in three steps: (i) The first step (line 5 of Algorithm 2) comes from the projection on S, with a part of minimization of the objective function. Here, the proximal function can be explained intuitively as follows: for every constraint space , it both minimizes the function and stays close to , and since partially results from a point that belongs to all the constraint spaces, then converges to the optimal solution; (ii) The second step comes from the projection over the diagonal convex D, represented in line 6 of Algorithm 2; (iii) Finally, the third step is an extrapolation step. In simple words, the extrapolation represented in line 11 is used to center the iterate from time to time, at each iterations: in [31, Section 4], it is explained that without the centring technique, the convergence seems to become ineffective, and on the other side, centring at each iteration can lead to an ineffective extrapolation. It has been proved in [31, Theorem 3.3] that this algorithm converges. All the theoretical background of Pierra’s algorithm can be found in [31].

3.3.2 Pierra’s algorithm adapted to solve the considered SDP problem

This part aims to apply Algorithm 2 to solve (33). In this case, the corresponding Hilbert space is set as , with the norm that is associated to the inner product defined in Section 3.1 by (13), such that . The function to minimize in Problem (72) is given by , and the integer equals . The convex sets are defined as follows:

| (74) |

where , , are respectively matrices and scalars defined by

| (75) |

In the considered case, the proximal function associated to on line 5 of Algorithm 2 is computed using the definition (73) in the following way:

| (76) |

where is the projection on the set . Thus, one sees from (76) that there remains to compute the projections over the constraint spaces defined by (74). Those spaces are of two kinds. First, for any constraint in the form , the following explicit projection formula holds:

Second, concerning the projection on the constraint space ,

where is the eigenvector decomposition of the matrix (see [19, section 20.1.1]). In view of all these considerations, Pierra’s algorithm applied on problem (33) is described in Algorithm 3.

Solving Problem (33) using Algorithm 3 requires the storage of the matrices , , , , , , and , that is in total matrices of dimension . Nevertheless, there is a way to avoid storing these matrices, since Algorithm 3 does not require the whole matrices, but rather the result of operations that mostly include dot products of sparse matrices. Then, doing the calculations and giving the results needed in Lines 5, 7, 10, 12, 14 and 16 of Algorithm 3 in function of , , , and implies that there will be no need for the matrices themselves. All these calculations are detailed in A. This aspect is one of the contributions of this paper.

4 Experimental results

The experimental results aim at evaluating numerically the quality of the proposed solution by DFW Algorithm. As mentioned before, two ways of evaluating the quality of the solutions are possible: the first one is to compare with the exact solution proposed by CPLEX when solving optimally the BSOCP formulation of the problem. The other method is to compute an optimality gap obtained by the bidualization of the problem. For this, an important observation is that the bidual problem (33) is an SDP problem. In order to compute this optimality gap, both CVXPY SDP solver and Pierra’s algorithm are used.

First, the quality of the solution of DFW Algorithm is evaluated by the two methods mentioned before. Then, for the SDP relaxation, solutions obtained by CVXPY and Pierra’s algorithm are compared, and the storage economy resulting from using Pierra’s algorithm is shown. This storage economy is especially due to taking advantage of the matrices sparsity in Problem (33).

4.1 Experimental setup

The robust counterpart of the shortest path problem with an undirected grid graph is considered for different sizes. For a grid graph , the number of nodes is , and the number of edges is . For the definition of Problem (6), the random mean vector and the random covariance matrix are chosen randomly, and is set to .

The implementation of both the computation of DFW robust solutions and the CVXPY based solver are written using Python 3.8.5 and Pierra’s algorithm is implemented using Matlab R2018b.

4.2 Numerical evaluation of the heuristic approach DFW

This part contains comparisons between the solutions obtained using DFW algorithm and CPLEX, as well as computations of the lower bound for the solution of DFW algorithm that is the solution of the SDP relaxation of the original problem. In this part, this lower bound is computed using CVXPY. Finally, the relative biduality gap (defined in (71)) is given, which allows to evaluate the quality of the solution of DFW algorithm, and a performance ratio useful for comparison with other work.

For experiments with DFW algorithm, constant parameters are and . Table 1 shows results for problem sizes . First of all, note that in all the cases processed, DFW algorithm gives the same solution as CPLEX. Second, concerning the relative gap, since we theoretically only have the weak duality for the solved problem, the biduality gap is not necessarily zero even if the solution is optimal. Thus, if the gap is small, it means that the heuristic solution is close to the optimal solution, but the opposite may not be true. Indeed a large gap does not mean that the heuristic solution is far from the optimal solution. In all the processed cases, the lower bound is less than the optimal solution , which validates the developments and the computations. Then, the relative gap is between and . This gap is a metric that allows to measure how far the heuristic approach is from the optimal solution. In other words, the heuristic solution is between and from optimality, in the worst case. To analyze more precisely the obtained gap and to compare with other work, a column is added in Table 1 with a metric named performance ratio used in [37] for the Max-Cut problem. The performance ratio has the following definition:

| (77) |

is then the proportion of in . In the considered case, . This is comparable to , the highest performance ratio obtained for the Max-Cut problem.

It would be interesting to test other cases of larger problems where the comparison with CPLEX is not possible, and check if the relative gap stays in the same interval as the processed cases. Indeed, in the processed cases, DFW algorithm gives the optimal solution, and thus the gap only comes from (see Equation (69)).

Now that the evaluation of solutions given by DFW algorithm is done using both CPLEX and the relative gap computed by CVXPY, an issue remains as discussed in Section 3.3: CVXPY needs a huge amount of memory to store matrices. That has justified the use of an alternative approach with Pierra’s algorithm using sparse computations detailed in A. In the next section, numerical results obtained using Pierra’s algorithm are presented, as well as the resulting gain in memory storage.

| Solution of DFW | Optimal solution by CPLEX | Lower bound by CVXPY | Relative gap RBG | Performance ratio | |

| 3 | 223.8807 | 223.8807 | 169.8902 | 0.3178 | 0.7588 |

| 4 | 302.9097 | 302.9097 | 230.64099 | 0.3133 | 0.7614 |

| 5 | 381.3647 | 381.3647 | 292.6109 | 0.3033 | 0.7673 |

| 6 | 498.444952 | 498.444952 | 401.92866 | 0.2401 | 0.8064 |

| 7 | 524.41995 | 524.41995 | 422.3119 | 0.2418 | 0.8053 |

| 8 | 625.46595 | 625.46595 | 524.83906 | 0.1917 | 0.8391 |

| 9 | 659.0601 | 659.0601 | 542.6984 | 0.2144 | 0.8234 |

| 10 | 604.0187 | 604.0187 | 492.4042 | 0.2267 | 0.8152 |

4.3 Numerical results of Pierra’s algorithm

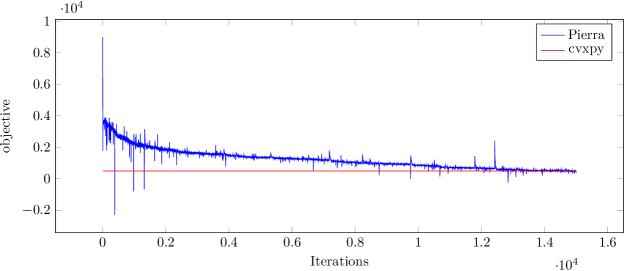

This part shows the results of Pierra’s algorithm for Problem (33) in comparison with the solution of CVXPY for problem sizes . For these experiments, constant parameters are , , and . Table 2 shows the computation time and memory storage needed for both the computation using CVXPY and of Pierra’s algorithm, as well as the percentage of optimality of Pierra’s solution compared to CVXPY after about 10000 iterations. The memory space saving is important. For , the proposed algorithm reduced the memory consumption from 3.45 GigaBytes to 26 MegaBytes: a factor of . In a reasonable computation time, that is however longer than the computation time of CVXPY, Pierra’s algorithm achieves great percentages from optimality. Figure 1 shows an example of the evolution of the objective function along the iterations of Pierra’s algorithm for the problem size , compared to the optimal solution obtained by CVXPY. In this example , and . A very good convergence can be observed at the last iterations shown in Table 2: from optimality.

| Time(s) | Storage needed (mB) | ||||

|---|---|---|---|---|---|

| L | CVXPY | Pierra | CVXPY | Pierra | Optimality percentage of Pierra (% CVXPY) |

| 3 | 11 | 3.7 | 1.29792 | 0.13632 | 96.4% |

| 4 | 49.6761 | 97.2 | 9.2 | 0.50496 | 77% |

| 5 | 145.93 | 631 | 40.45 | 1.358848 | 86% |

| 6 | 394.2456 | 1005.4 | 132.88 | 3.008448 | 92.2% |

| 7 | 935.8 | 2275 | 358.82 | 5.841792 | 92.4% |

| 8 | 2274.85 | 7826 | 841.73 | 10.32448 | 96% |

| 9 | 4724.6 | 22338 | 1776.192 | 16.99968 | 97% |

| 10 | 9244.87 | 63585 | 3451.17 | 26.488128 | 99.93% |

4.4 Discussion

In conclusion of the numerical experiments, it is possible to make the following comments. The lower bounds using Pierra’s algorithm have been provided for small problem sizes. Thus, the contribution of this work is to propose a method to evaluate the solution of a heuristic algorithm for Problem (6) without comparing it with CPLEX, but rather with a lower bound. For this, a challenge has been encountered, since it is well known that using the duality makes the problems easier but bigger, as the dual problem is usually polynomial, but has more variables and more constraints. This challenge has been tackled using Pierra’s algorithm with the sparse computations. Here, the goal is twofold: first, put the algorithm proposed by Pierra in 1984 back in the spotlight for its efficiency even if it has not been used much. The second goal is to show the power of having an explicit algorithm instead of a black box solver. Doing this has made the sparse computations possible, reducing drastically the memory storage necessity.

Interesting future works involve going further in the problem sizes: starting from a grid of size , the problem becomes computationally demanding, as CPLEX becomes unable of giving a solution, and CVXPY for the lower bound necessitates terabytes of memory storage. But before being able to realize that, some challenges concerning Pierra’s algorithm should be dealt with, such as the stopping criteria on line 19 of Algorithm 3 and the performance of the algorithm that has to be sped up. One should note that the architecture of the algorithm allows a very easy parallelization, since the projections on each constraint space are independent (lines 6 to 17 of Algorithm 3). Thus, a parallel implementation could speed up the algorithm.

5 Conclusion

This paper studies the Robust counterpart of the Shortest Path Problem (RSPP) in the case of correlated ellipsoidal uncertainty set. This problem is NP-hard, and exact methods exist to solve it, such as BSOCP solvers. Moreover, a heuristic algorithm named DFW has been proposed in [17]. More precisely, this work proposes a lower bound to validate heuristic approaches that solve the RSPP, such as DFW Algorithm. This lower bound computation replaces the comparison with exact solvers as a validation method. To compute the proposed lower bound, recall that it is the solution of an SDP problem that can be solved by CVXPY using interior-point methods. Unfortunately, the bidual problem is a big problem with much more constraints and more variables than the original problem. Thus, despite its polynomial nature, the resolution of this bidual problem is very time consuming and needs a huge memory space. Therefore, the sparsity of the matrices that define the problem has been exploited to replace the classical solver by a sparse version of Pierra’s decomposition through formalization in a product space algorithm. All this is numerically tested, showing that, due to the results of this paper, a polynomial time evaluation of the quality of the solution of DFW heuristic is possible without having the memory storage issue of the bidual problem.

Acknowledgment

This work has been supported by the EIPHI Graduate school (contract ”ANR-17-EURE-0002”). Computations have been performed on the supercomputer facilities of Mésocenter de calcul de Franche-Comté in Besançon, France.

Appendix A Sparse computations

The aim of this appendix is to detail the computations needed in Algorithm 3, and the replacements done to avoid the storage of the matrices , , , , , , and . Recall that doing this enables us to express all the formulas in function only of , , , and , and thus to avoid the storage of matrices of dimension .

The operation in Line 5

can be replaced by

The operation in Line 7

can be replaced by

with is the vector containing the -th lign of , , since , and .

The operation in Line 10

can be replaced by

with , since , and

The operation in Line 12

can be replaced by

with , since , and

The operation in Line 14

can be replaced by

with , since , and

The operation in Line 16

can be replaced by

with since and

References

- [1] P. Kouvelis, G. Yu, Robust discrete optimization and its applications, Vol. 14, Springer Science & Business Media, 2013.

- [2] Z. Li, R. Ding, C. A. Floudas, A comparative theoretical and computational study on robust counterpart optimization: I. robust linear optimization and robust mixed integer linear optimization, Industrial & engineering chemistry research 50 (18) (2011) 10567–10603.

- [3] A. Ben-Tal, A. Goryashko, E. Guslitzer, A. Nemirovski, Adjustable robust solutions of uncertain linear programs, Mathematical Programming 99 (2) (2004) 351–376.

- [4] G. A. Hanasusanto, D. Kuhn, W. Wiesemann, K-adaptability in two-stage distributionally robust binary programming, Operations Research Letters 44 (1) (2016) 6–11.

- [5] H. Rahimian, S. Mehrotra, Distributionally robust optimization: A review, arXiv preprint arXiv:1908.05659 (2019).

- [6] O. Baron, O. Berman, M. M. Fazel-Zarandi, V. Roshanaei, Almost robust discrete optimization, European Journal of Operational Research 276 (2) (2019) 451–465.

- [7] J. M. Buhmann, A. Y. Gronskiy, M. Mihalák, T. Pröger, R. Šrámek, P. Widmayer, Robust optimization in the presence of uncertainty: A generic approach, Journal of Computer and System Sciences 94 (2018) 135–166.

- [8] E. Hazan, et al., Introduction to online convex optimization, Foundations and Trends® in Optimization 2 (3-4) (2016) 157–325.

- [9] B. Liu, Some research problems in uncertainty theory, Journal of Uncertain systems 3 (1) (2009) 3–10.

- [10] Y. Gao, Shortest path problem with uncertain arc lengths, Computers & Mathematics with Applications 62 (6) (2011) 2591–2600.

- [11] H. Markowitz, Portfolio selection, The journal of finance 7 (1) (1952) 77–91.

- [12] M. Poss, Robust combinatorial optimization with knapsack uncertainty, Discrete Optimization 27 (2018) 88–102.

- [13] E. Nikolova, Approximation algorithms for reliable stochastic combinatorial optimization, in: Approximation, Randomization, and Combinatorial Optimization. Algorithms and Techniques, Springer, 2010, pp. 338–351.

- [14] F. Baumann, C. Buchheim, A. Ilyina, A lagrangean decomposition approach for robust combinatorial optimization, in: Technical report, Optimization Online, 2014.

- [15] A. Atamtürk, V. Narayanan, Polymatroids and mean-risk minimization in discrete optimization, Operations Research Letters 36 (5) (2008) 618–622.

- [16] C. Buchheim, J. Kurtz, Robust combinatorial optimization under convex and discrete cost uncertainty, EURO Journal on Computational Optimization 6 (3) (2018) 211–238.

- [17] C. Al Dahik, Z. Al Masry, S. Chrétien, J.-M. Nicod, L. Rabehasaina, A frank-wolfe based algorithm for robust discrete optimization under uncertainty, in: 2020 Prognostics and Health Management Conference (PHM-Besançon), IEEE, 2020, pp. 247–252.

- [18] S. Boyd, S. P. Boyd, L. Vandenberghe, Convex optimization, Cambridge university press, 2004.

- [19] M. F. Anjos, J. B. Lasserre, Handbook on semidefinite, conic and polynomial optimization, Vol. 166, Springer Science & Business Media, 2011.

- [20] P. Scobey, D. Kabe, Vector quadratic programming problems and inequality constrained least squares estimation, J. Indust. Math. Soc. 28 (1978) 37–49.

- [21] R. Fletcher, A nonlinear programming problem in statistics (educational testing), SIAM Journal on Scientific and Statistical Computing 2 (3) (1981) 257–267.

- [22] S. Boyd, L. El Ghaoui, E. Feron, V. Balakrishnan, Linear matrix inequalities in system and control theory, Vol. 15, Siam, 1994.

- [23] M. X. Goemans, D. P. Williamson, Improved approximation algorithms for maximum cut and satisfiability problems using semidefinite programming, Journal of the ACM (JACM) 42 (6) (1995) 1115–1145.

- [24] D. Karger, R. Motwani, M. Sudan, Approximate graph coloring by semidefinite programming, Journal of the ACM (JACM) 45 (2) (1998) 246–265.

- [25] M. X. Goemans, D. P. Williamson, New 34-approximation algorithms for the maximum satisfiability problem, SIAM Journal on Discrete Mathematics 7 (4) (1994) 656–666.

- [26] C. Lemaréchal, F. Oustry, Semidefinite relaxations and lagrangian duality with application to combinatorial optimization, Ph.D. thesis, INRIA (1999).

- [27] M. X. Goemans, Semidefinite programming in combinatorial optimization, Mathematical Programming 79 (1-3) (1997) 143–161.

- [28] H. Wolkowicz, Semidefinite and lagrangian relaxations for hard combinatorial problems, in: IFIP Conference on System Modeling and Optimization, Springer, 1999, pp. 269–309.

- [29] Y. Nesterov, A. Nemirovski, Interior-point polynomial algorithms in convex programming (studies in applied and numerical mathematics), Society for Industrial Mathematics (1994).

- [30] S. Boyd, N. Parikh, E. Chu, Distributed optimization and statistical learning via the alternating direction method of multipliers, Now Publishers Inc, 2011.

- [31] G. Pierra, Decomposition through formalization in a product space, Mathematical Programming 28 (1) (1984) 96–115.

- [32] A. Schrijver, A course in combinatorial optimization, CWI, Kruislaan 413 (2003) 1098.

- [33] A. Ilyina, Combinatorial optimization under ellipsoidal uncertainty, Ph.D. thesis, Technische Universität Dortmund (2017).

- [34] IBM academic portal, https://www.ibm.com/academic.

- [35] M. Frank, P. Wolfe, An algorithm for quadratic programming, Naval research logistics quarterly 3 (1-2) (1956) 95–110.

- [36] S. Diamond, S. Boyd, Cvxpy: A python-embedded modeling language for convex optimization, The Journal of Machine Learning Research 17 (1) (2016) 2909–2913.

- [37] H. Karloff, How good is the goemans–williamson max cut algorithm?, SIAM Journal on Computing 29 (1) (1999) 336–350.