Clustering Market Regimes using the Wasserstein Distance

Abstract.

The problem of rapid and automated detection of distinct market regimes is a topic of great interest to financial mathematicians and practitioners alike. In this paper, we outline an unsupervised learning algorithm for clustering financial time-series into a suitable number of temporal segments (market regimes). As a special case of the above, we develop a robust algorithm that automates the process of classifying market regimes. The method is robust in the sense that it does not depend on modelling assumptions of the underlying time series as our experiments with real datasets show. This method – dubbed the Wasserstein -means algorithm – frames such a problem as one on the space of probability measures with finite moment, in terms of the -Wasserstein distance between (empirical) distributions. We compare our WK-means approach with a more traditional clustering algorithms by studying the so-called maximum mean discrepancy scores between, and within clusters. In both cases it is shown that the WK-means algorithm vastly outperforms all considered competitor approaches. We demonstrate the performance of all approaches both in a controlled environment on synthetic data, and on real data.

1. Introduction

Time series data derived from asset returns are known to exhibit certain properties, termed stylised facts, that are ubiquitous across asset classes. For example, it is well-understood that return series are non-stationary in the strong sense, and exhibit volatility clustering (for a full recount, see [Con01]). In particular, understanding the heteroskedastic nature of financial time series data is relevant for market practitioners. An observed sequence of asset returns (or, for multiple assets, a tuple of sequences) exhibits periods of similar behaviour, followed by potentially distinct periods that indicate a significantly different underlying distribution. Such periods are often referred to as market regimes. Our interest in swiftly and accurately detecting changes in market regimes is motivated by a multitude of financial applications (both classical and modern): Most naturally, an accurate detection of shifts in market behaviour is tantamount for making optimised investment decisions or trading strategies. But also within the arena of recent, deep learning-based methods for pricing hedging and market generation [HMT19, BHL+20], the detection of significant shifts in market behaviour is a central tool for their model governance, since it serves as an indicator for the need to retrain the ML-model. Henceforth, we call the task of finding an effective way of grouping different regimes the market regime clustering problem (MRCP).

In this paper, we propose a methodology to classify segments of the historical evolution of market returns into distinct regimes. We do so by devising a modified, versatile version of the classical -means clustering algorithm to group distributions of asset returns into regimes, which exhibit a higher degree of homogeneity. The way modify the classical algorithm is twofold: Firstly, by a shift of perspective, we consider the clustering problem as one on the space of distributions with finite moment, as opposed to one on Euclidean space. Secondly, our choice of metric on this space is the Wasserstein distance, and we aggregate nearest neighbours using the associated Wasserstein barycenter. We motivate why the Wasserstein distance is the natural choice for this particular problem in Section 1.2. Accordingly in later sections we also present different numerical setups to demonstrate how to navigate how reactive/robust the algorithm is on different datasets. The latter will depend on the precise application at hand and the modellers appetite for more swift or more robust indicators.

We benchmark our results with two alternative approaches. The first applies the classical -means algorithm to the first moments associated to each segment of market returns. The second is a more classical approach: We implement a version of the hidden Markov model (HMM) using appropriate modifications to make results comparable to ours. We test each algorithm both on real and synthetic data. The success of the unsupervised learning algorithms in the real data setting is evaluated using a marginal maximum mean discrepancy (MMD) metric, a metric arising from a powerful two-sample test which has experienced a notable rise in popularity in recent machine learning literature. Overall, we show that our data-driven and non-parametric methodology accurately partitions financial return series into distinct clusters which are both distinct from each other whilst remaining internally self-similar, relative to a more naive approach based on moments or HMMs, which we verify on synthetic parametric data as well as on historical time series, where our algorithm correctly identifies all (now historically known) periods of unusual market activity as they arise.

1.1. The market regime clustering problem

Let us start by giving an overview of related literature and existing insights on the MRCP. Recall that the MRCP is defined as the task of classifying segments of return series , where

Any vector can be associated to an empirical measure for with atoms. Thus, the problem of classifying market regimes is equivalent to assigning labels to probability measures , where is the set of probability measures on with finite moment.

Historically, approaches to solving the MRCP vary depending on their applications: for instance, a modeller may be interested in regime classification over different time scales: from microseconds, to months or years. Further variations may come according to the modeller’s choice of framing the problem; for example, one may wish to segment regimes via change points detection methods, which are place (as the name sugests) emphasis on change-points rather than on the regimes themselves (see [NHZ16] for an overview). Another example is the more general outlier detection problem [CFLA20, KSH20], which is a special one-class case of the MRCP. Those studying such a problem are often more interested in identifying anomalous datum, as opposed to characterising the distribution such datum are generated from.

Some of the early attempts at analysing financial return series to extract regime switching signals fall under the umbrella of technical analysis, where signals such as temporal moving average crossovers and support level breaches are used as indicators for a regime change for a particular financial asset or a collection of assets, see Achelis [Ach01] for a comprehensive guide. More rigorous statistical analyses of financial time series have also been employed to detect regime changes. A classical approach is performing dynamic PCA on inter-asset covariance matrices, see Pelletier [Pel06] for an example on high-dimensional synthetic Markovian asset price paths.

Another classical approach to the MRCP is via Markovian switching models and HMMs. To the author’s knowledge, this technique was introduced in the work of Hamilton [Ham89], in which the state term signifying the regime is given by an AR process. For a more detailed history of the Markov switching model, we refer the reader to [Kua02] and to [LR09], [Gui11] for their use in empirical finance. The hidden Markov model approach is not altogether model-free as it makes two main assumptions: first, the latent state variable specifying the current regime is Markovian, and secondly, that the likelihood of observing a return given the latent state variable is given by some parametric distribution, often Gaussian. Other approaches include agent-based models as shown in Lux and Marchesi [LM00], Bayesian approaches as seen in Maheu, Thomas and Song [MMS12], or more data-driven approaches as seen in Lahmiri [Lah16].

Previous work on the problem of clustering families of distributions via non-parametric unsupervised learning approaches has been found in Nielson, Nock and Amari [NNA14], where a modification of the classical kmeans algorithm is used to cluster histograms via mixed -divergences. An approach to empirical distribution clustering via -means is also given in Henderson, Gallagher and Eliassi-Rad [HGER15] in a non-financial context. Other works have utilised the Wasserstein distance for clustering problems, see for instance [LW08, YWWL17], where in the latter distributions are represented as weight-mass pairs, and clustering is considered in the context of images and documents, or [MZGW18] for an approach using variational optimal transport. Such approaches are similar to the work in this paper as they often employ classic unsupervised learning algorithms with some modification that allows them to handle distributional datum. Our approach seeks to meld the financial regime-switching and clustering worlds together in an attempt to provide a robust, non-parametric approach to a posteriori market regime clustering.

1.2. Motivation for using

In this section, we motivate our perspective on the clustering problem and the choice of the Wasserstein metric (14) for this purpose, which has recently seen a swift rise in artificial intelligence and machine learning, see for instance [NSW+20].

Given that our clustering problem is defined over the space of probability measures , there exist many candidate one could employ: classical choices include the Kolmogorov-Smirnov statistic or the Kullback-Leibler (KL)-divergence. We argue that either of these choices are inadequate for the given problem statement. It is well known that the Kolmogorov-Smirnov statistic lacks the sensitivity required to distinguish between elements of the clustering set (see [MS83]). The KL-divergence has been employed in the literature as a distance function within a clustering algorithm see [ABS08] for a -medians implementation with generalised Bregman divergences, and [NNA14] for general -divergences. We note that our clustering problem is over empirical measures and thus requires an estimation of the probability density function associated to each measure if the KL-divergence is to be employed. Barycenters with respect to the symmetrized and non-symmetrized versions of the KL-divergence have been shown to exist ([Vel02]), and [NN09] for more general Bregman divergences), however these rely on algorithmic derivations. We argue that our approach is much simpler, elegant and scalable when compared to the alternatives.

The Wasserstein distance is a natural choice for comparing distributions of points on a metric space . The distance function appears in the expression (14) characterising the distance and furthermore, the Wasserstein distance metrizes weak convergence111A sequence converges weakly to iff as . Moreover, if is a Polish space, then is also Polish (see [AG13], Theorem 2.6 for the case ).. Thus, measures that are close in the Wasserstein sense are also close in the classical narrow sense as well.

In our examples we focus on the univariate case , since computing the Wasserstein distance in between empirical measures is particularly tractable, though a multivariate characterisation of our results is also possible (see next paragraph). From Proposition 2.5, the algorithm to compute the -Wasserstein distance between two empirical measures with atoms is . It is important to note that other comparative distances share this property. However, the Wasserstein distance also has a natural aggregator candidate in the Wasserstein barycenter, which is fast to calculate in the case where . Other comparative distances either do not have a natural candidate for aggregation (Kolmogorov-Smirnov) or a canonical aggregator which is tractable to calculate (KL-divergence).

In the case where , the Wasserstein distance is also viable as a choice of metric on . Although has shown to be an effective tool to tackle the curse of dimensionality associated to sequences on , it becomes computationally too demanding to solve when extending to higher-dimensional data ([RPDB11], Section 2.2). Recently, the sliced Wasserstein distance as seen in [RPDB11], [BRPP15] and [KNS+19] has been employed to extend the to . It does this by projecting distributions onto via points on the unit sphere in , and returns the expected one-dimensional Wasserstein distance of such projections. This turns the complex problem of calculating into an operation, where is the number of points taken. Recently, Bayraktar and Guo [BG21] showed that the max sliced Wasserstein metric is strongly equivalent to the classical Wasserstein distance in the cases .222The authors would like to thank Claude Martini and Frédéric Patras for informing us of this.

1.3. Problem setting and notation

We begin by giving an overview of the problem setting. First, we introduce the notion of a data stream.

Definition 1.1 (Set of data streams, [BKA+19], Definition 2.1).

Let be a non-empty set. The set of streams of data over is given by

| (1) |

In this paper, we take and fix . In the context of the MRCP, elements will be price paths associated to a financial asset.

Given , we define the vector of log-returns associated to by

| (2) |

so . We use the following expression to highlight that we may to wish partition the original stream of data (2) into potentially overlapping segments equal length.

Definition 1.2 (Stream lift, [BKA+19], Section 3.3).

Let be a space of streams over a non-empty set . Let be another non-empty set, and let . We call a function

a lift from the space of streams to the space of streams of segments over .

Thus, for and with , we define a lift from to via

| (3) |

where is the maximum number of partitions with length that can be extracted from with sliding window offset parameter . We obtain the stream of segments by applying to .

Finally, as stated in the introduction, the main idea of this paper is to lift the regime clustering problem from one on Euclidean space to one on the space of probability distributions with finite moment with . This requires defining a family of measures via the map .

Definition 1.3 (Empirical measure, [GBC16], Section 3.9.5).

Let such that for . Furthermore, let

be the function which extracts the order statistic of , for . Then, the cumulative distribution function of the empirical measure associated to is defined as

| (4) |

where is the indicator function.

Thus, we can associate to each segment of data the empirical measure for . This gives us a family of measures

| (5) |

It is this family which will be the subject of our clustering algorithm.

1.4. The -means algorithm

Suppose is a stream of data over a normed vector space . We further assume that each has been standardised coordinate-wise, that is,

| (6) |

The -means clustering algorithm is a unsupervised vector quantization method which assigns elements of to distinct clusters. Each of these clusters are defined by central elements called centroids, which are initially sampled from .

At each step of the algorithm, one first calculates the nearest neighbours

| (7) |

associated to each for , where is the metric induced by the norm on .

Remark 1.4.

Classically, one chooses , but we note here that any normed vector space could be chosen.

Each set is then aggregated into a new centroid for via a function , so

For a given a tolerance level and a loss function , the -means algorithm terminates at step if the stopping condition

is satisfied. The algorithm outputs the final clusters and the quantizations . We conclude this section with the assumptions associated to the -means algorithm that, if satisfied, will result in uniform and isotropic clustering of a data set .

Proposition 1.5 ([KMN+02]).

Given data , the -means algorithm produces suitable clusters if the following is true:

-

1.

There exist natural clusters in the data .

-

2.

Each cluster within is of roughly equal size.

-

3.

Within-cluster variation (cf. Definition A.2) is uniform. That is, for small we have that

-

4.

Clusters are spherical in shape, so we expect the nearest neighbours to the centroid to be contained within a ball where is uniform across all clusters .

If conditions (1)-(4) are satisfied, then optimal clusterings will be suitable.

Counterexamples to suitability include forcing clusters on data with fewer than natural clusters available. Another classical example is the problem of clustering concentric data , which violates assumption (4) in Proposition 1.5. We note that do exist other clustering algorithms which do not share the drawbacks of -means, in that they do not make assumptions regarding the number or shape of the clusters (hierarchical clustering), nor do they enforce that data points belong to one individual cluster (fuzzy c-means clustering, see for instance [CDB86]). Exploring other clustering algorithms for the MRCP is a topic for future research.

1.5. The maximum mean discrepancy

Evaluating derived -means clusters on a stream of data is typically done by evaluating the final total cluster variation or inertia (cf. Definition A.3). Here, are the final clusters obtained from a given run of the -means algorithm. Naturally the value of is dependent on the normed vector space one decides to cluster the steam of data on (assuming it is feasible, a natural choice may be ). Of course one could make a different choice by transforming sets of datum , see Section 3.1. Since the total cluster variation depends on , one cannot use it in evaluation between clusterings on different choices of .

In this section, we outline an integrable probability metric on the space of distributions called the maximum mean discrepancy (MMD), which will be used as part of a robust methodology for confirming goodness-of-fit of clustered market regimes. The MMD has been shown to be a robust estimator under both dependence and presence of outliers [CAA21] and has been employed frequently in the quantitative finance and machine learning literature, see [BHL+20], [ACADF20], [BBDG19].

We provide a brief introduction here and refer the reader to the literature [GBR+12], [GBR+07], [GFHS09] for further details. We begin by introducing the following.

Problem 1.6 (Two-sample test, [GBR+12], Problem 1).

Let be a metric space. Suppose and are independent random variables defined on . Suppose that and , where are Borel. If we draw samples and where for and for , when can we determine if ? That is, we wish to implement a test for the two-sample problem

| (8) |

We introduce the following test statistic associated to Problem 1.6.

Definition 1.7 (Maximum mean discrepancy, [GBR+12], Definition 2).

Let be a class of functions and let be defined as in Problem 1.6. Then, the maximum mean discrepancy (MMD) between and is defined as

| (9) |

If and are samples where and , then a biased empirical estimate of the MMD is given by

| (10) |

Clearly, the value of the MMD between two measures is determined by the function class one decides to calculate the supremum in (9) over; in particular, it is not even guaranteed to be a metric. Often the MMD is employed in the context of studying mean differences between datum in a typically higher-dimensional feature space. This motivates the use of kernel methods to define , which is often chosen to be the unit ball in a reproducing kernel Hilbert space (RKHS) , where is the associated reproducing kernel. That the MMD is a metric depends on the associated kernel being universal (cf. Definition B.3) if is compact. If is non-compact, the following property is enough to guarantee that this is the case.

Definition 1.8 (Characteristic kernel, [FGSS09], Section 2).

Let be a non-empty set. A kernel on is called characteristic if the mean mapping

| (11) |

is injective.

The Gaussian kernel

| (12) |

is characteristic to the set of Borel measures on and indeed makes the MMD a metric on . For more details we refer the reader to Theorem 2 in [FGSS07] or to Appendix B, Theorem B.4 for more details.

We will use the MMD with to validate how effective a given clustering algorithm is in the case that we are unable to infer true regime labels, i.e., when we are working with real data. A key notion to define how similar a collection of samples are to each other is the following.

Definition 1.9 (Within-cluster self-similarity (homogeneity)).

Let be a stream of data with observations. Let be the unit ball in a universal RKHS . For , we define the self-similarity score associated to to be

| (13) |

where and are samples drawn pairwise from for .

2. -means on the space of distributions

In this section, we outline our modification to the -means algorithm which allows us to cluster the set (5) directly on the space of probability measures with finite moment. Central to this paper is the following distance metric on .

Definition 2.1 (-Wasserstein distance, [AGS05]).

Suppose is a separable Radon space. The -th Wasserstein distance between measures is defined by

| (14) |

where

is the set of transport plans between and .

The -Wasserstein distance (14) is the solution to the Kantorovich-type optimal transportation problem between measures and for the cost function . For our applications, existence of an optimal plan realising the Wasserstein distance between measures is guaranteed by continuity of the metric and the fact that will be empirical measures and thus posses compact support. We refer the reader to [San15] for further details.

Remark 2.2 (Relationship to the ).

The Wasserstein distance (14), via its equivalent dual formulation, is a special case of an integral probability metric (see, for instance, [WGX21], Definition 1). In the case where , the dual representation is given by

| (15) |

where denotes the space of continuous -functions over with Lipschitz constant . Since are probability measures, we can write (15) as

Thus is an integrable probability metric over the function class , which is given by the unit ball in the space of functions

where

In what follows, we choose the -Wasserstein distance to be our metric on . As explained in Section 1.2, this distance is natural and tractable to use on the space of probability measures.

Our next decision we need to make is how we aggregate nearest neighbours into central elements for . One of the advantages of choosing the Wasserstein distance to be the metric we apply on our clustering space is the existence of the following, which gives a natural way to “average” a family of measures under .

Definition 2.3 (Wasserstein barycenter).

Suppose is a separable Radon space and let be a family of Radon measures. Define the -Wasserstein barycenter of to be

| (16) |

Remark 2.4.

Since the -means algorithm requires repeated evaluations of elements on clustering space under the given metric, tractability of the non-linear optimisation (14) becomes relevant. In the case where measures are absolutely continuous, there exist a closed-form solution to (14).

Proposition 2.5 ([KNS+19], Equation (3)).

Suppose and let . Moreover, suppose that are absolutely continuous with respect to the Lebesgue measure on . Then, the -Wasserstein distance is given by

| (17) |

where the quantile function is defined as

| (18) |

Proof.

A consequence of the fact that the (unique) optimal transport map pushing onto is given by , and applying a change of variables. ∎

In what follows, we assume that are empirical measures with equal numbers of atoms (this will be the case in our experimental setup). Recalling Definition 1.3, we may write them as

| (19) |

where and are increasing sequences corresponding to the atoms of and . We wish to use (17) to obtain a closed-form expression for the Wasserstein distance between the two measures. Thus, we must consider the well-posedness of (18): every empirical measure on is Radon, and thus one can associate to () a right-continuous function of finite variation given by ([RY04], Theorem 4.3). The function possesses a right-continuous inverse which is nothing but the quantile function from (18), which (in the case of ) can be written as

| (20) |

Moreover for all . Applying (20) to (17), the Wasserstein distance between the empirical measures and is given by

| (21) |

Thus, calculating the Wasserstein distance between two empirical measures can be done in linear time, assuming the atoms of each measure are already sorted ascending. If not, calculating (21) is an operation, where is the number of atoms. This representation also makes calculating the Wasserstein barycenter (16) simple in the case where and some assumptions are made on the number of atoms present in each measure.

Proposition 2.6 (Wasserstein barycenter, empirical measures).

Suppose that are a family of empirical probability measures, each with atoms . Let

Then, the cumulative distribution function of the Wasserstein barycenter over with respect to the 1-Wasserstein distance is given by

| (22) |

Moreover, is not necessarily unique.

Proof.

See Appendix C.1. ∎

The last specification we need to make is regarding the loss function. We do this in the natural way by replacing the squared Euclidean distance in standard -means by the -Wasserstein distance. Let be the centroids obtained after step of the Wasserstein -means algorithm. Therefore, our loss function is given by

| (23) |

Our stopping rule is unchanged; that is, for a given we terminate the algorithm at step if . We give a full statement of the algorithm with the following.

Definition 2.7 (WK-means algorithm).

We summarize with Algorithm 1.

3. Methodology and numerical results

In this section, we cover the methods used to test the WK-means algorithm on stock data. Initially, we test both algorithms on real data. Validation of each clustering algorithm was conducted using the MMD test statistic (10). Finally, we tested both algorithms on synthetic data generated via two different models: one where the associated log-returns were distributed normally, and another where they were not.

3.1. Alternative clustering algorithms as benchmarks

I this section we seek to benchmark our approach via two alternative algorithms. In this section, we briefly introduce these methods.

3.1.1. -means with statistical moments

A natural and more classical approach to clustering regimes may involve studying the first raw moments associated to each measure . With this in mind, consider the image of from (5) under the function

| (24) |

which is the truncated unstandardised -moment map. As each is a sum of Dirac masses, each element of is finite. Thus, for a given we obtain

| (25) |

After standardising each element of component-wise (cf. Remark 3.2), we obtain a clustering set on , which we can apply the standard k-means algorithm to. This motivates the following definition.

Definition 3.1 (Moment -means).

Let be a family of measures. For , associate to each the p-vector for , where is the -moment map from (24).

Remark 3.2 (Magnitude of moments).

The function defined in (24) outputs the first raw moments associated to a measure . Often, moments that appear earlier in the sequence will be of significantly larger magnitude than those that appear later. In order for the -means algorithm to not place undue emphasis on these moments, it is critical that each slice is standardised according to equation (6) for .

3.1.2. Hidden Markov model

As mentioned in Section 1.1, a more classical approach to market regime clustering involves fitting a hidden Markov model (HMM) to observed time series data , that there exist hidden latent states which govern the dynamics of . The transition between the latent states is assumed Markovian, and although they are not directly observable they are represented by a transition density where is the given latent state and are parameters associated to the state, for , and the most common choice of likelihood is a Gaussian one. We refer the reader to [DVR15] for more details.

As another point of comparison to our approach, we fit a Gaussian HMM in both our real and synthetic data experiments. A main point of difference here is that the HMM does not cluster sets of returns: instead, it associates returns at time to a given latent state. We thus can derive accuracy statistics in the case where we run the HMM over synthetic data, but for real data our validation method using the MMD is not possible.

3.2. Validation on real data

In this section, we give results from each algorithm on real data.

3.2.1. Data and hyperparameters

We begin by testing both algorithms on market data. In particular, we use one-hourly log-returns associated to the SPY index from 2005-01-03 to 2020-12-31. Recalling Definition 1.2 and (3), we set the hyper-parameters . This roughly partitions the time-series into weeks, with adjacent partitions within one day of each other. We defer discussions regarding choices of hyperparameters to Section 3.4.

Regarding the number of clusters, we set . Primarily, this is for simplicity as it makes comparisons between each methods simpler. Moreover, it also reflects a stylised fact regarding financial markets, being that market returns can be roughly apportioned into bull and bear cycles. We note that other values of do have financial interpretations - for instance, see Maheu, McCurdy and Song [MMS12].

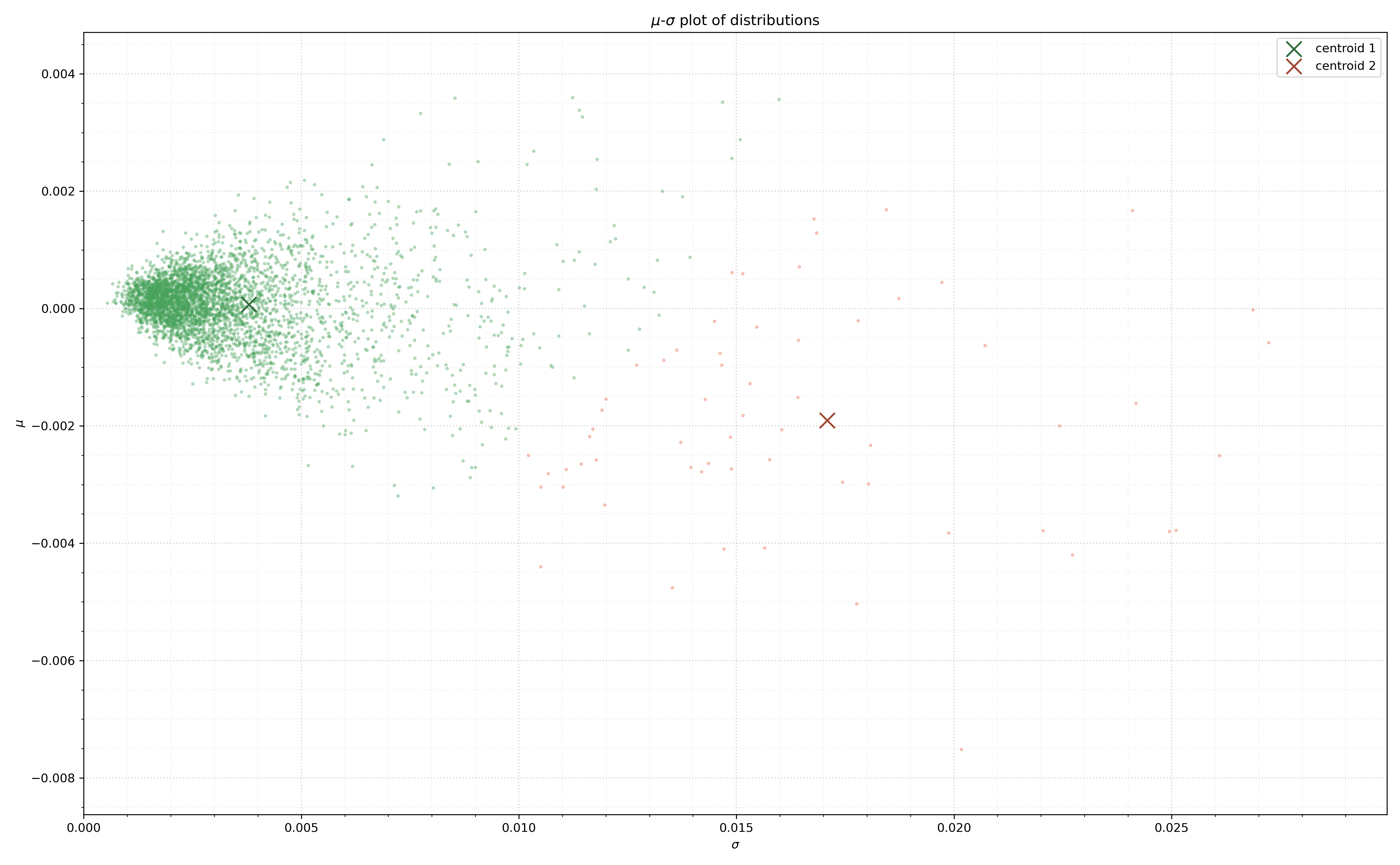

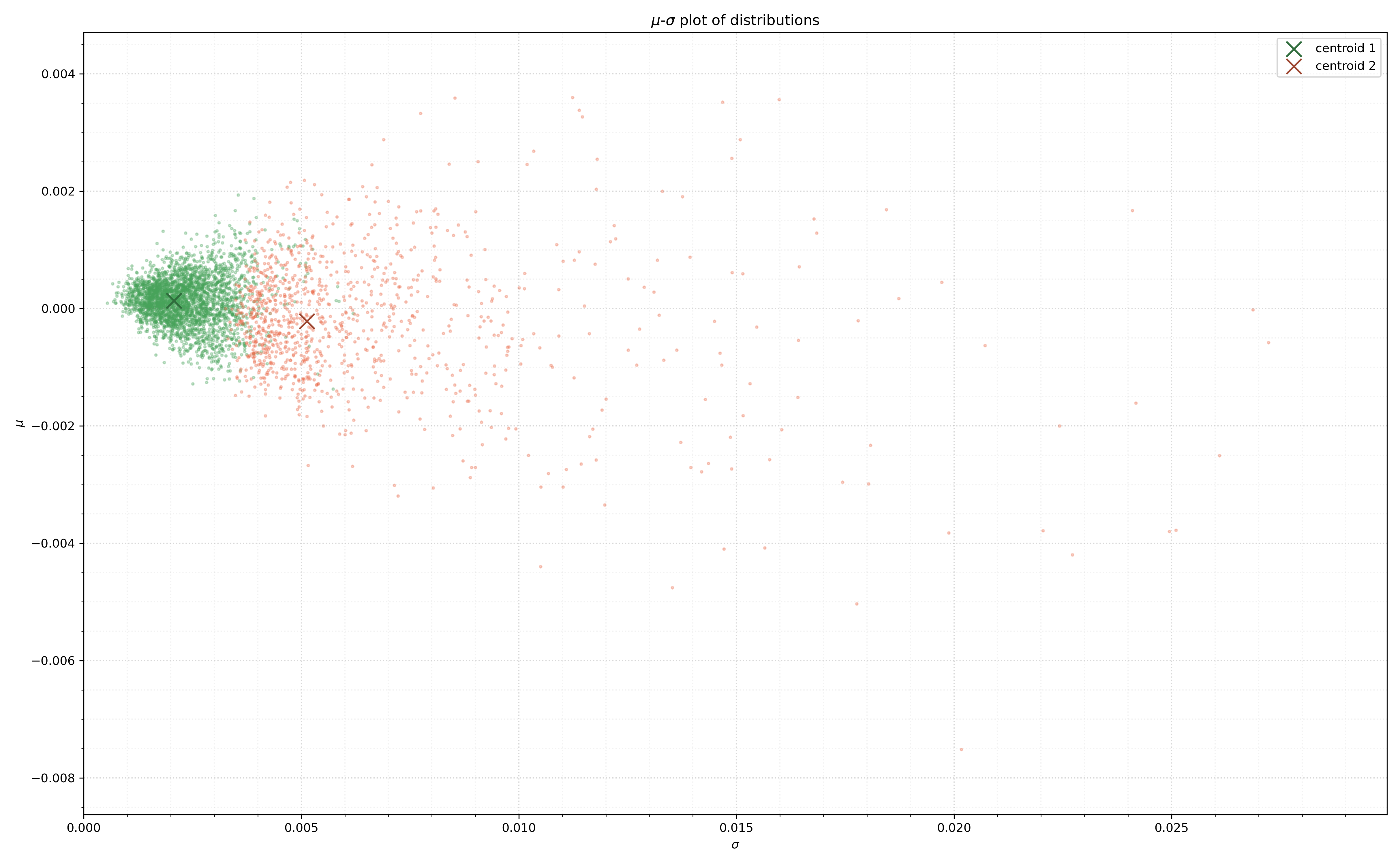

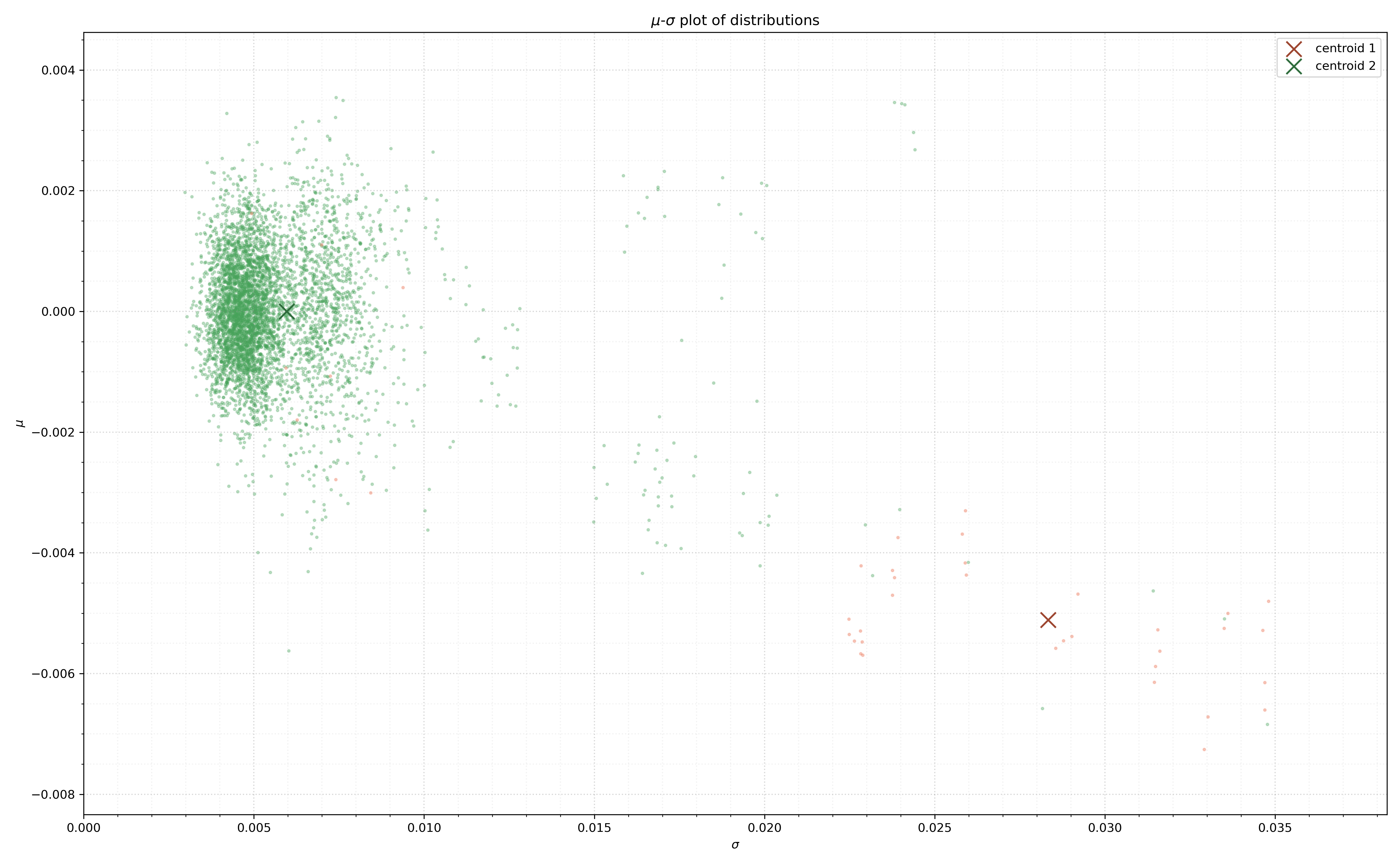

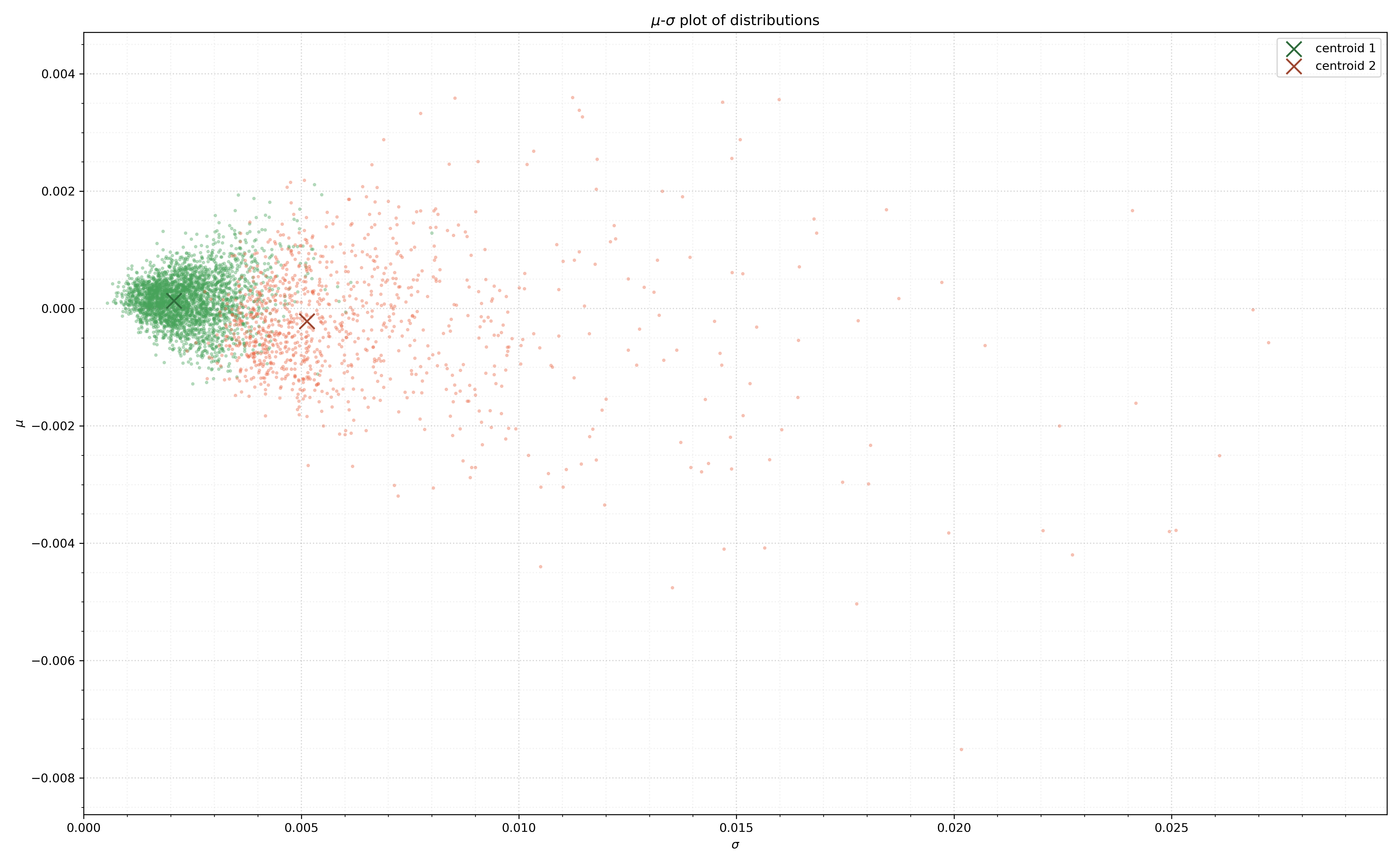

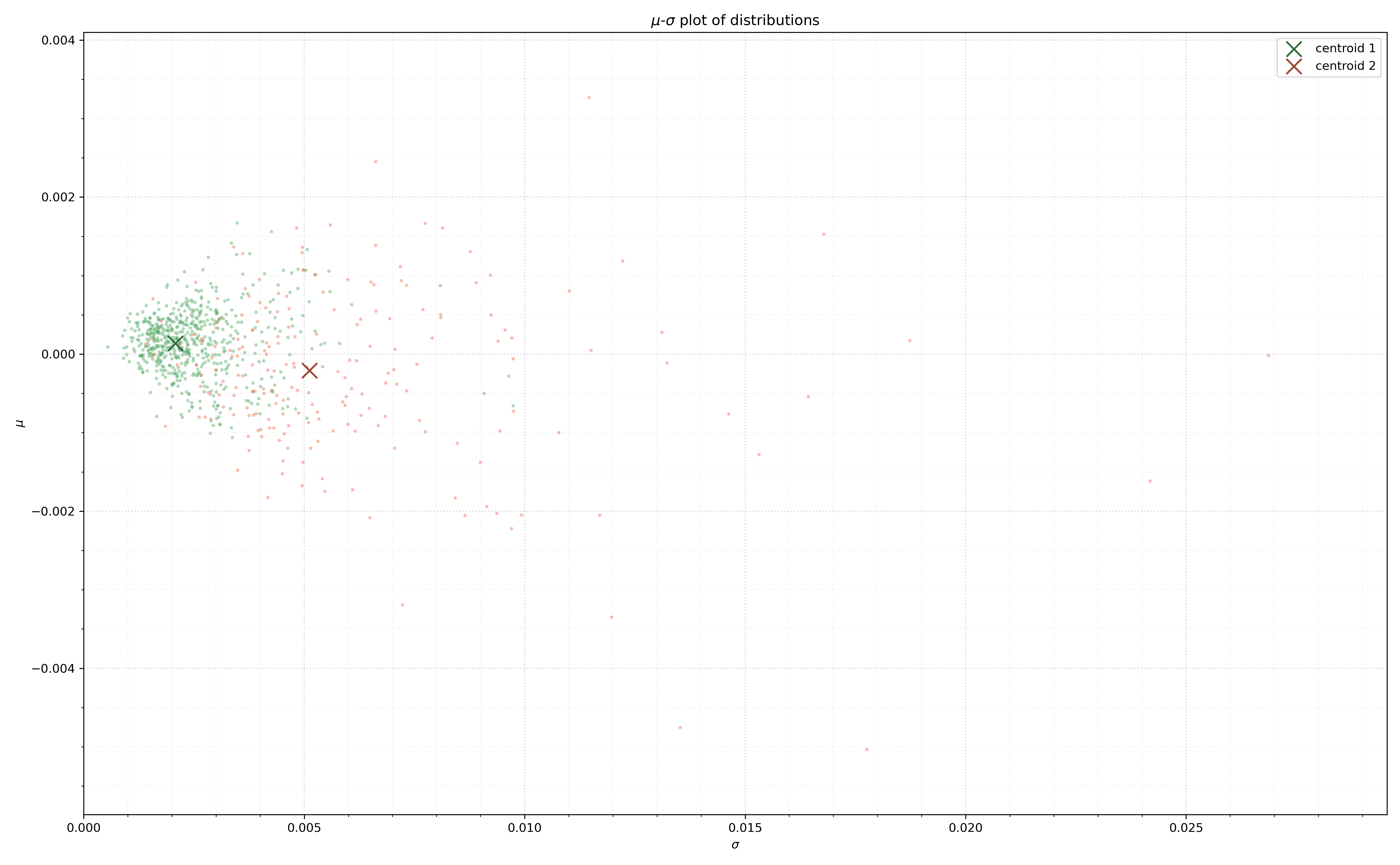

We ran the two algorithms over the lifted steam of data . For each algorithm, we obtained centroids and the nearest neighbours with being the nearest neighbours corresponding to the centroid. In order to display our results, we primarily use two plots. The first is the projection of each distribution onto 2 via the map

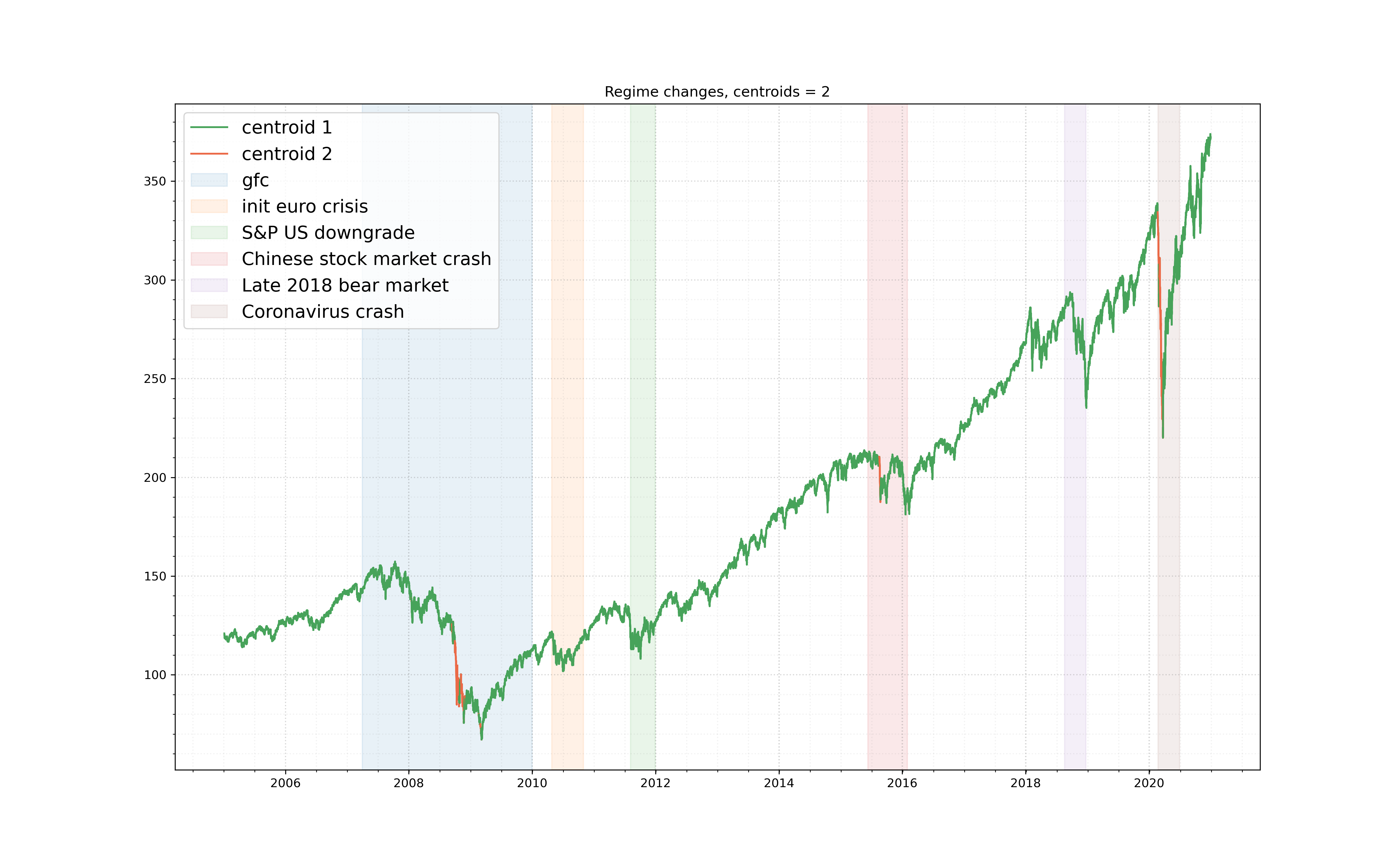

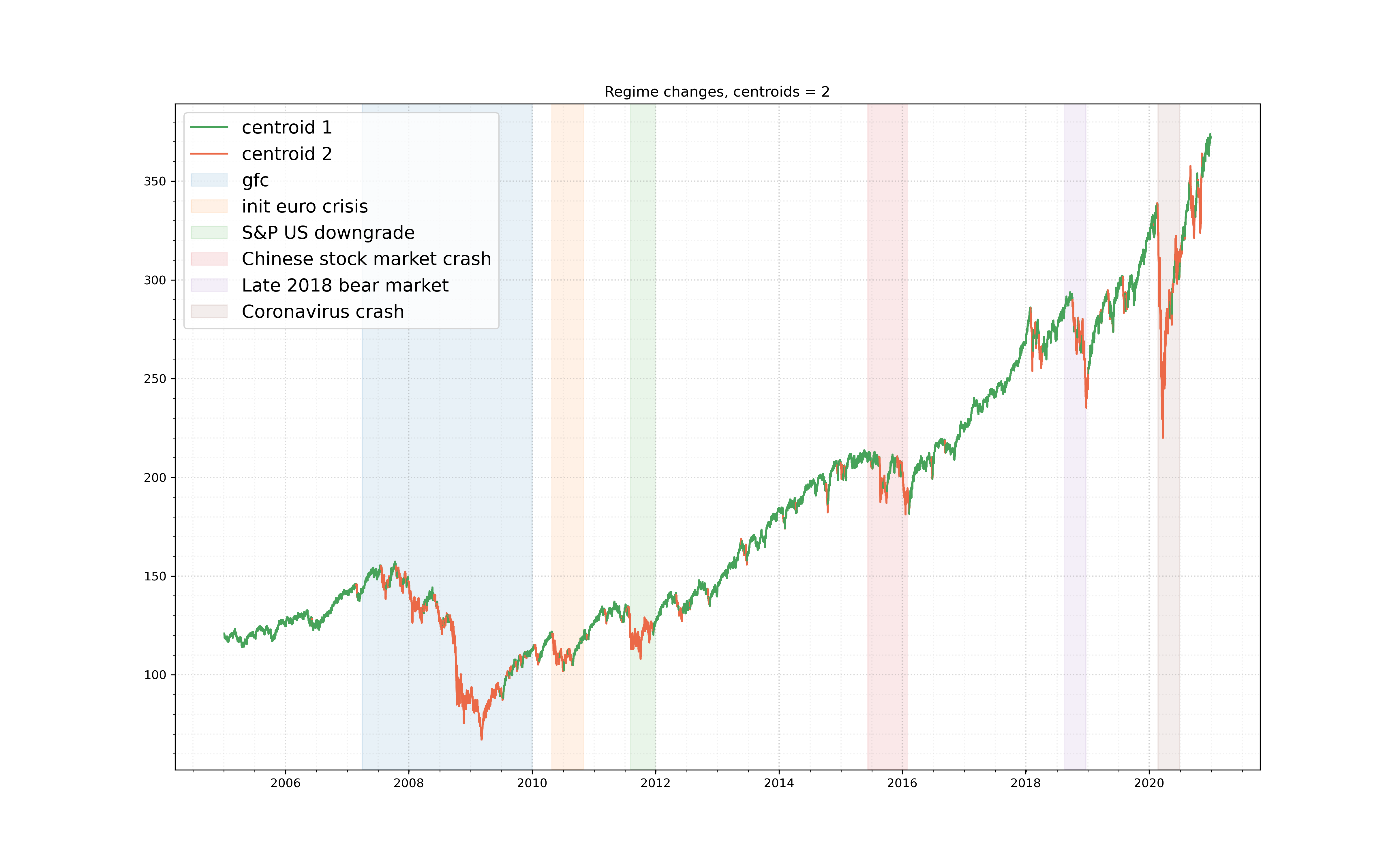

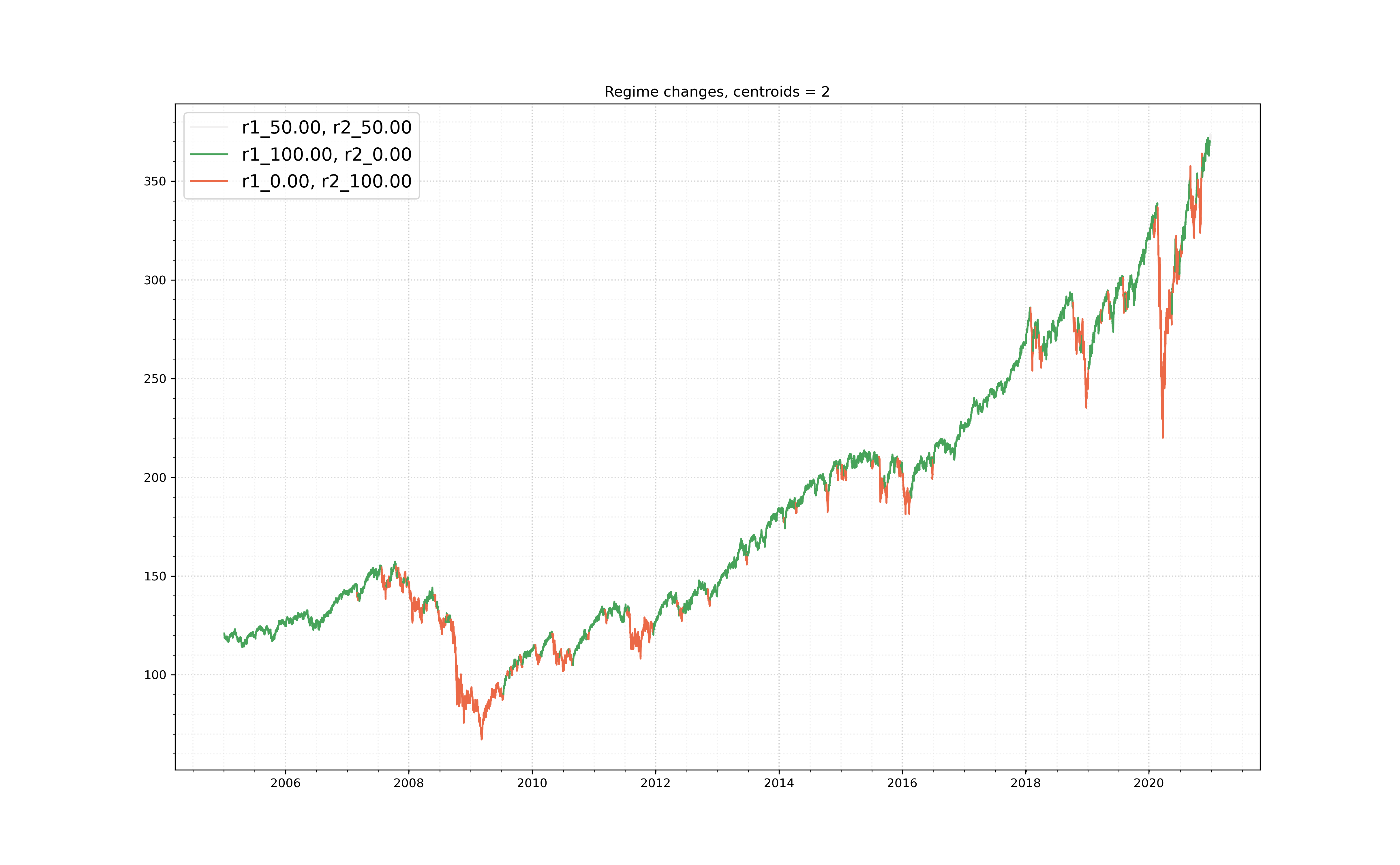

that is, a scatter plot of each measure in mean-variance space. We colour these points according to their centroid membership. Points coloured green correspond to the cluster with lower variance than those coloured red. The second plot we make use of is a time-series plot of stock values , where each partition has been coloured corresponding to its centroid membership. Given that the empirical distributions overlap, a given timestamp may be classified into multiple clusters. Thus, we colour these points according to their average centroid memberships. In the case of with the hyperparameters , a single return can potentially belong to 5 different empirical measures. Thus, there are 6 total potential centroid membership combinations that it can have, and we colour these sections of the price path accordingly.

3.2.2. Algorithm results

We first present the results of running either algorithm over hourly SPY data. Figure 1 gives the scatter plots of each empirical measure coloured according to its cluster membership. The centroids are marked by crosses and coloured accordingly.

From Figure 1(b), we see that the WK-means classifications are much less susceptible to outlier distributions than the MK-means algorithm. We also note that the Wasserstein approach demarcates distributions by variance, which one naturally expects in a financial market setting. Although Figure 1(a) appears to do the same, it is hard to state this definitively as the clustering algorithm seems to primarily group outlier distributions.

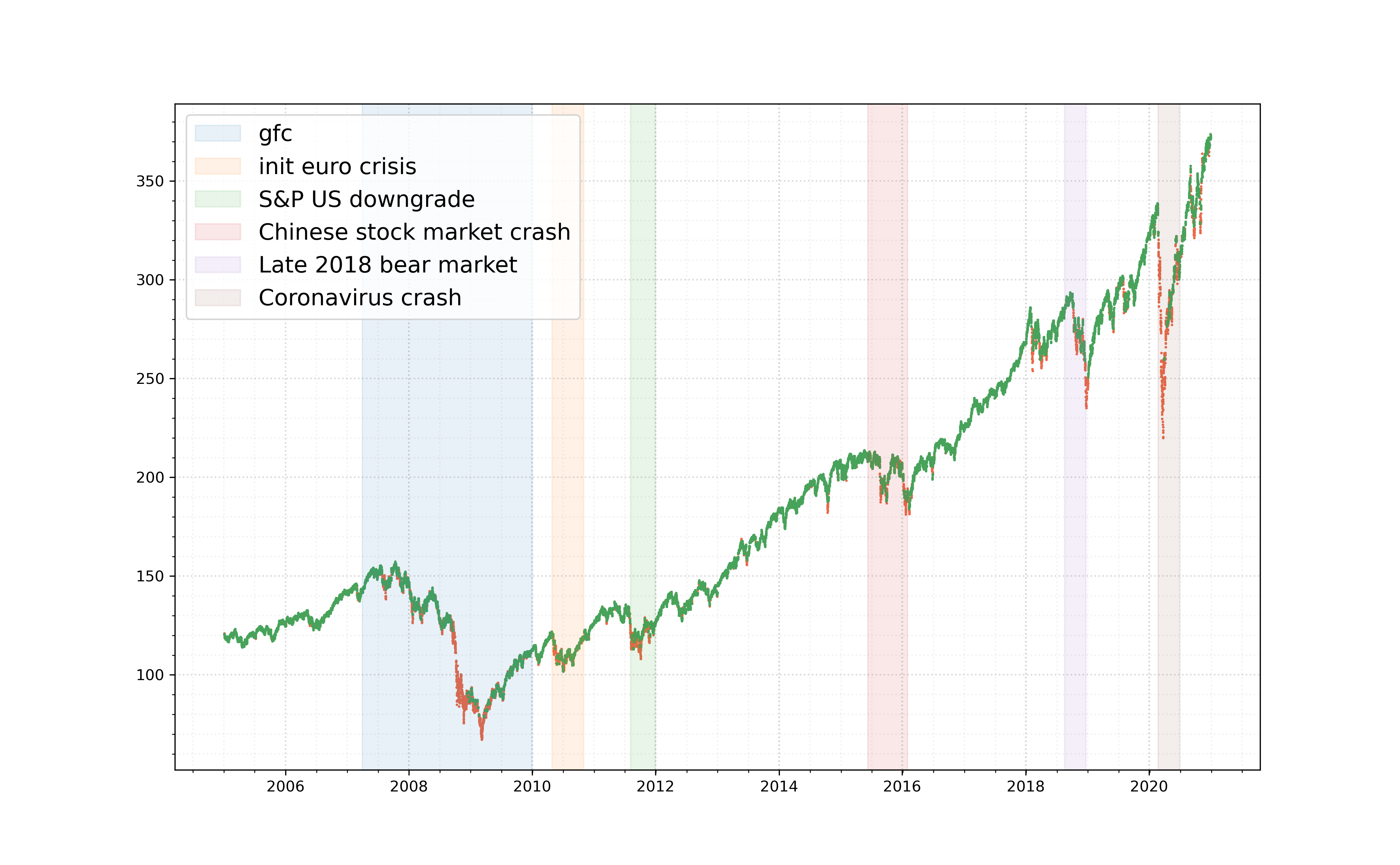

This is made apparent in the graphs presented in Figure 2, where we have associated to each the partition of it is generated from.

Figures 2(a) and 2(b) show that both algorithms are able to separately classify periods of returns associated to the global financial crisis and the more recent market instability due to the coronavirus pandemic. However, only the WK-means algorithm is able to distinguish between more subtle periods of stock market volatility: the beginning of the Eurozone/Greek debt crisis in 2010, the S&P US credit-rating downgrade in 2011, and the 2015/16 Chinese stock market crash were tagged as periods of regime change only by the WK-means algorithm. Note that we can include an example of a Hidden Markov model run with this plot, in Figure 2(c). We note that the results from this approach seem to sit somewhere between the Wasserstein and moment algorithms.

3.2.3. Validation methods

In order to compare clusterings obtained from both algorithms, we use the marginal MMD test introduced in Section 1.5. The two methods of evaluation we consider are applied both between and within clusters . Moreover, both methods of evaluation are similar, in that they involve bootstrapping the distribution of between two sets of samples.

More generally, the definition of an optimal clustering over a set of data is not well-defined, and in the case of financial data, this is certainly true. Heuristically, we would like individual clusters to contain objects that are similar to each other whilst being distinct from objects in other clusters. We note that there do already exist several indexes used to evaluate the result of a given -means clustering, which we recall here.

Definition 3.3 (Davies-Bouldin index, [DB79]).

Suppose is a normed vector space. Let be centroids and clusters over , obtained by applying the -means algorithm characterised by the functions

Suppose is the metric induced by the norm on . Let

be the average distance of cluster elements to the central element for . Then, the Davies-Bouldin index is given by

| (26) |

Lower values of (26) are indicative of a better clustering.

Definition 3.4 (Dunn index, [Dun74]).

Definition 3.5 (Silhouette coefficient, [Rou87]).

Remark 3.6.

It is often computationally expensive to calculate the (28) for every point . Thus, we often use an estimate from fewer samples.

For , define and let be an increasing sub-sequence of , for . Then, the -average Silhouette coefficient is given by

| (29) |

The indexes from Definitions 3.3, 3.4 and 3.5 are often used to evaluate clusters derived from a standard -means algorithm for different values of . We will see that using them to compare clusterings between the MK- and WK-means approaches (for the same value of ) does not capture how appropriate clusterings are in reference to the MRCP. Firstly, such indexes are not agnostic to the choice of and are thus not comparable between algorithms. Secondly, a more appropriate validation method for the MRCP would be between regimes , as opposed to elements of the clustering space . Thus, as an integrable probability metric, the MMD is a more suitable choice to be used to evaluate the appropriateness of either clustering algorithm. Nevertheless we will report the values of these metrics for completeness.

For our between-cluster evaluation, we proceed as follows. Given sets obtained via either the moment- or WK-means clustering algorithm, draw pairwise samples for . We represent each empirical measure by its corresponding vector of log-returns . We then evaluate the test statistic (53) where we choose to be the Gaussian kernel (48) with . We then compare the associated distribution of the MMD between the two histograms generated from the moment- and WK-means methods by reporting the similarity score from Definition 1.9.

Within-cluster evaluation is performed much in the same way as the between-cluster case: for either algorithm, and for each cluster , we draw pairwise samples and evaluate the biased MMD (53). We report the similarity score associated to the empirical distribution of each within-cluster MMD and plot the resulting histograms.

3.2.4. Cluster validation via the marginal MMD

Recall from Section 1 that we stated that a clustering algorithm was successful if the self-similarity and distinctness of derived clusters were appropriately traded off against each other. In this section, we give the scores of each clustering algorithm on the SPY data with references to the indexes introduced in Definitions 3.3, 3.4, and 3.5. In particular, we report the average silhouette coefficient with . Results are given in Table 1.

| Algorithm | Davies-Bouldin | Dunn | |

|---|---|---|---|

| Wasserstein | |||

| Moment |

As noted in Section 3.2.3, scores associated to the first two indexes are not invariant under the choice of and thus do not represent a like-for-like comparison. Yet we note that the average Silhouette coefficient remains higher for the MK-means method than the WK-means, implying that (under the more traditional method of cluster validation) regimes clustered via the former belong to more appropriate clusters than the latter.

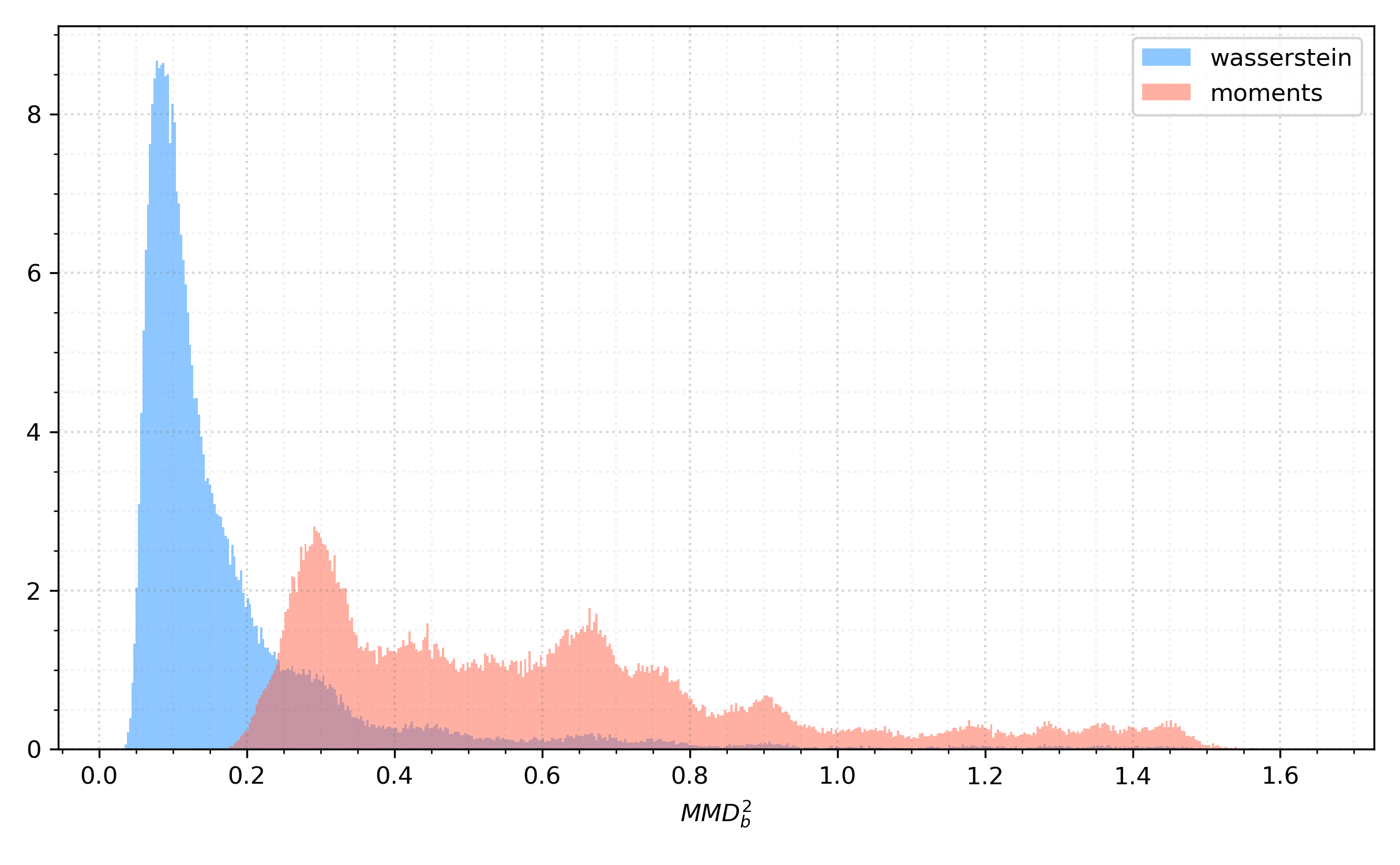

As outlined in Section 3.2.3, we applied our within- and between-cluster validation via the marginal MMD from Definition 1.7 by sampling times from each cluster obtained from either method, and calculating the biased MMD (10). We order samples from clusters in ascending order to ensure like-for-like comparison between sample elements. Figure 3 shows two empirical distributions of the biased MMD between elements in the two clusters formed from the WK- and MK-means method.

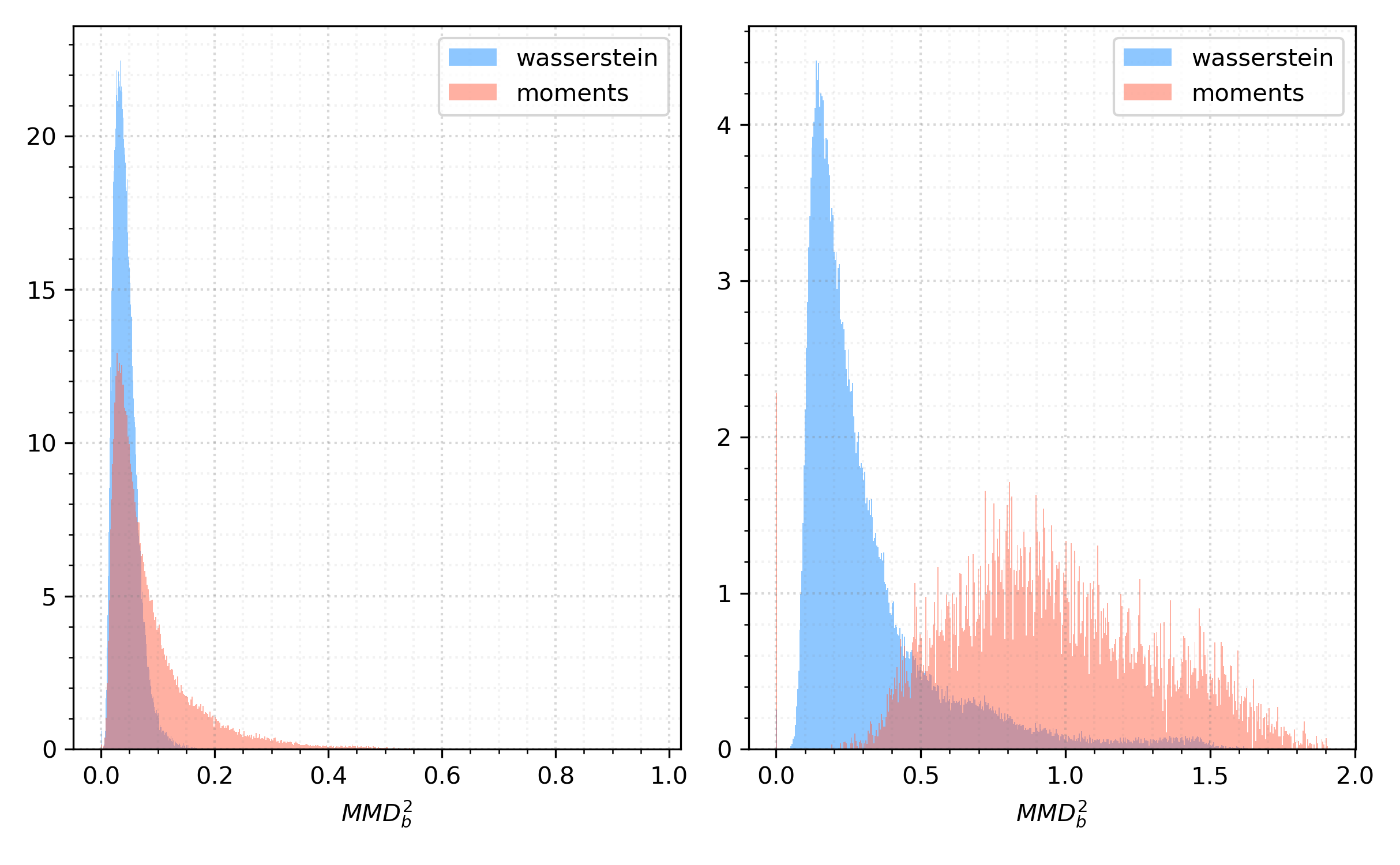

Figure 3, shows that the clusters obtained via the WK-means method are significantly more similar to each other than those obtained from the MK-means method. However, one cannot then conclude that the latter method provides a better clustering result if the disparity within groups is due to one cluster being composed primarily of outlier elements. Figure 4 gives the empirical distribution of the within-cluster MMD for each algorithm. These histograms were derived by calculating the biased MMD test statistic via the sub-sampling technique from Definition 1.9, with .

Both Figure 4 and the self-similarity scores in Table 2 show that the clusters obtained via the WK-means algorithm are significantly more self-similar than those obtained from the MK-means algorithm.

| Algorithm | ||

|---|---|---|

| Wasserstein | ||

| Moment |

3.3. Validation on synthetic data

Evaluating a given clustering algorithm on real market data is difficult for multiple reasons. One is that it is not possible to infer the underlying probabilistic structure associated to the stream of log-returns that a clustering algorithm is run over, and thus one cannot say with any certainty what constitutes a “correct” clustering. A corollary to this is that it is impossible to know exactly at what point a regime change occurs when studying real market data.

Therefore, we evaluated both clustering algorithms on synthetic market data, where we specify beforehand at what times regime changes occur. Because we knew both the underlying probabilistic structure and the regime change periods a priori, we could further evaluate both how accurately either algorithm is classifying sequences of returns into regimes, and how closely the centroids of each cluster correspond to the true distributions associated to the synthetic data.

The methodology is as follows. For a given time interval with , we define a mesh so that each time increment roughly represents one market hour. That is, with , we set

Next, we define the number of regime changes we wish to observe. We specify their starting points and lengths by for , with

and

Each can be a constant or a random variable. We thus obtain the set of disjoint intervals

| (30) |

and their associated complements which partition the interval into two sets. Intervals in will correspond to times where we observe a regime change in our synthetic data, which will start at and end at for .

Once we have run a classification algorithm over a synthetic price path, we consider three measures of accuracy: total accuracy, accuracy during the standard regime (regime-off) and accuracy during the regime change (regime-on). This is calculated in the following way: for , associate to each log-return the empirical measures it was a member of. With our chosen hyperparameters and , one has that and is the first measure that is a member of. Note that if the overlap hyperparameter then . We then calculate which cluster each is associated to, which gives us our predicted labels . We then aggregate these labels into the row vector

where is the number of clusters. In what follows we assume the assignment corresponds to the standard regime and the regime change. We then have the following definitions.

Definition 3.7.

With the notation above, for a given vector of log-returns and cluster assignments , the regime-off accuracy score (ROFS) is given by

| (31) |

Similarly, the regime-on accuracy score (RONS) is given by

| (32) |

Finally, total accuracy (TA) is given by

| (33) |

3.3.1. Geometric Brownian motion

In this section, we discuss how we tested both clustering algorithms on synthetic stock data which was modelled as a geometric Brownian motion. Let be a family of models indexed by a parameter set . Initially, we chose . We then specified two parameter combinations and , corresponding to two market regimes.

We then construct a geometric Brownian motion with associated parameters over intervals for , and with parameters elsewhere. We then run both clustering algorithms on the synthetic data and are returned the clusters with associated centroids as output. Since

| (34) |

the true measures are given by

| (35) |

where is the mesh size. Due to the Gaussianity of the distribution of the true log-returns, it suffices to check the mean and variance of the centroid measures to gauge how close they are to the true measures for .

We begin by testing on geometric Brownian motion paths with

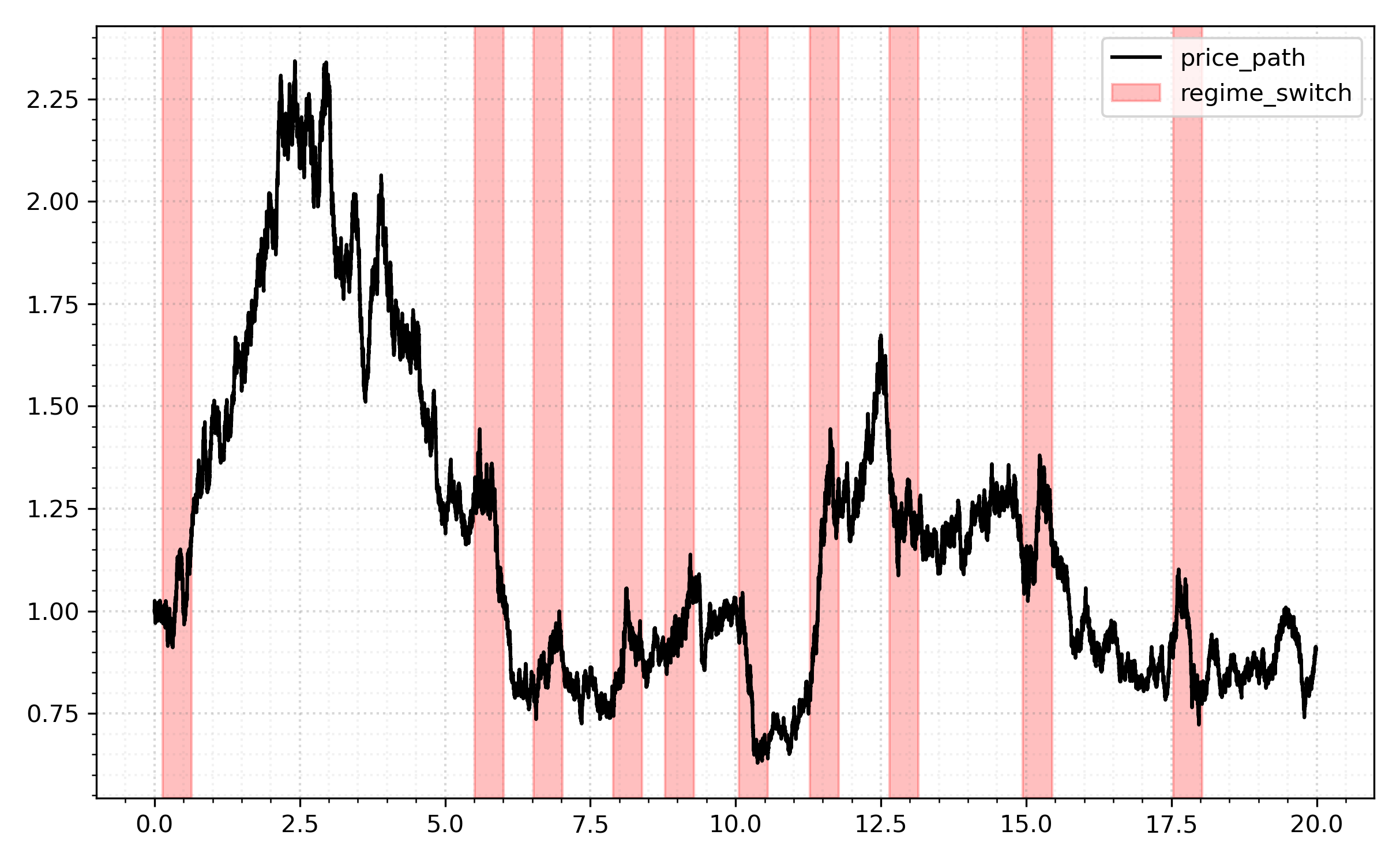

We simulate a path over years with regime changes, and randomly chose each for and fixed . This choice corresponds to regime changes persisting for approximately half a year. Our mesh grid is thus given by

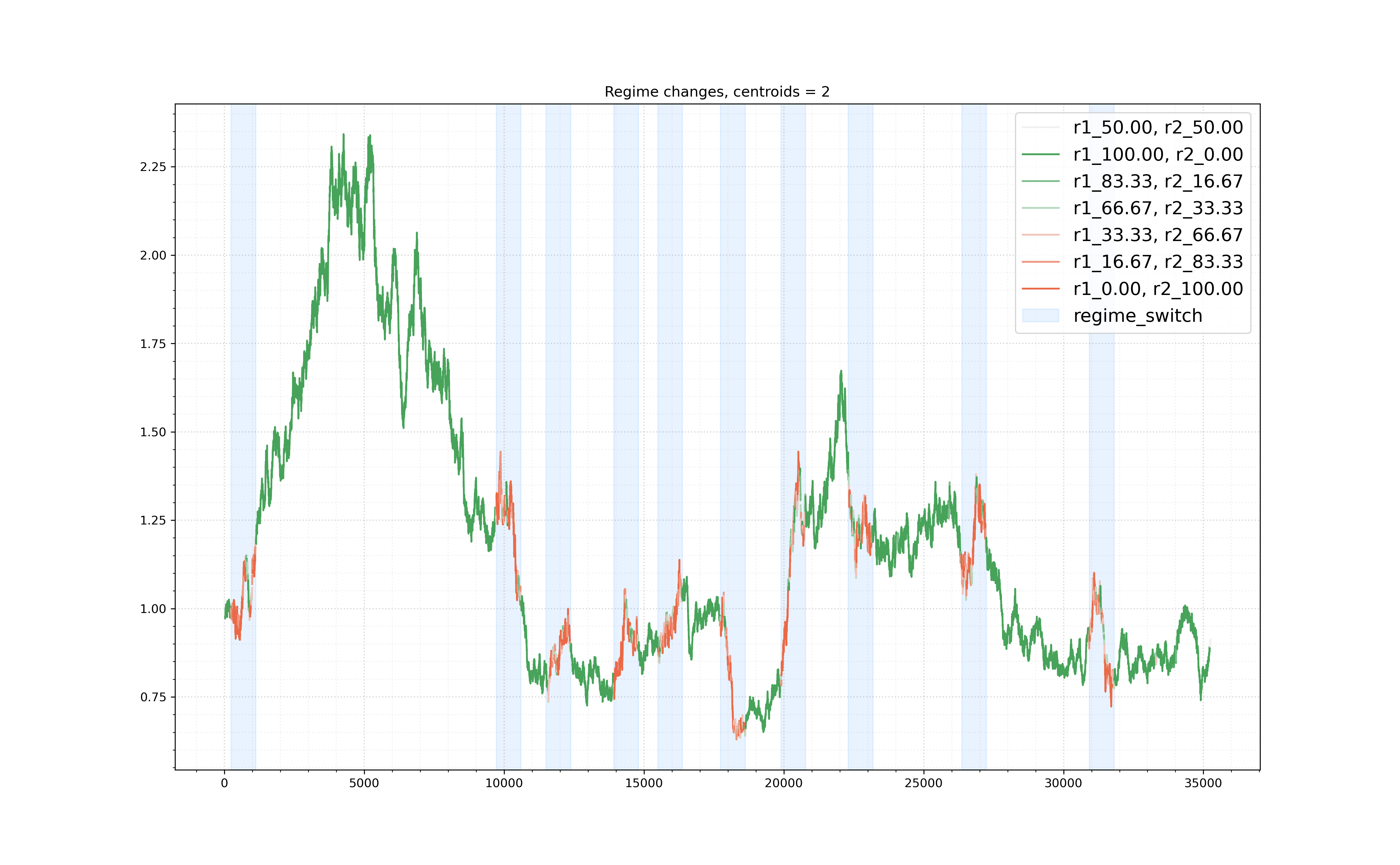

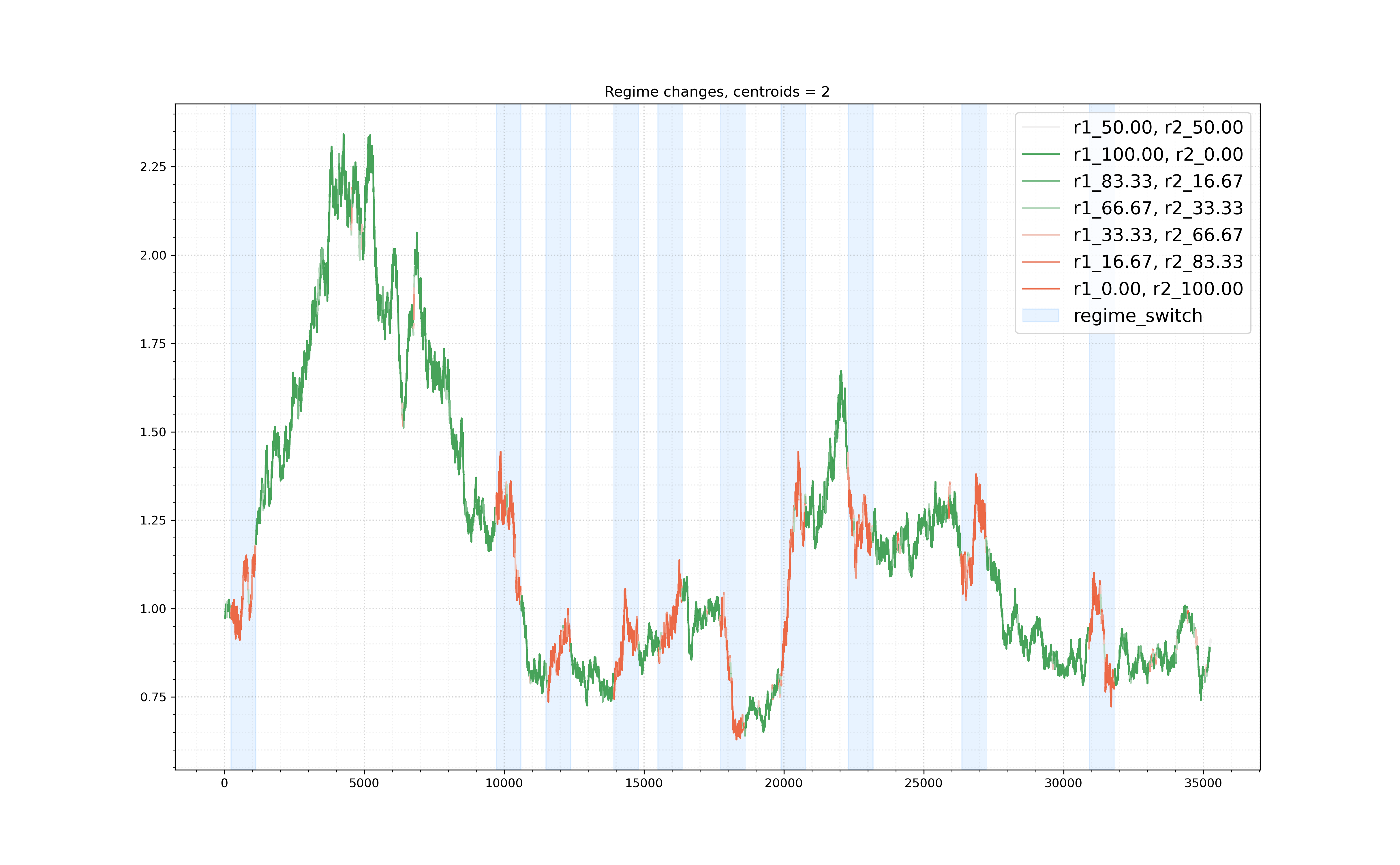

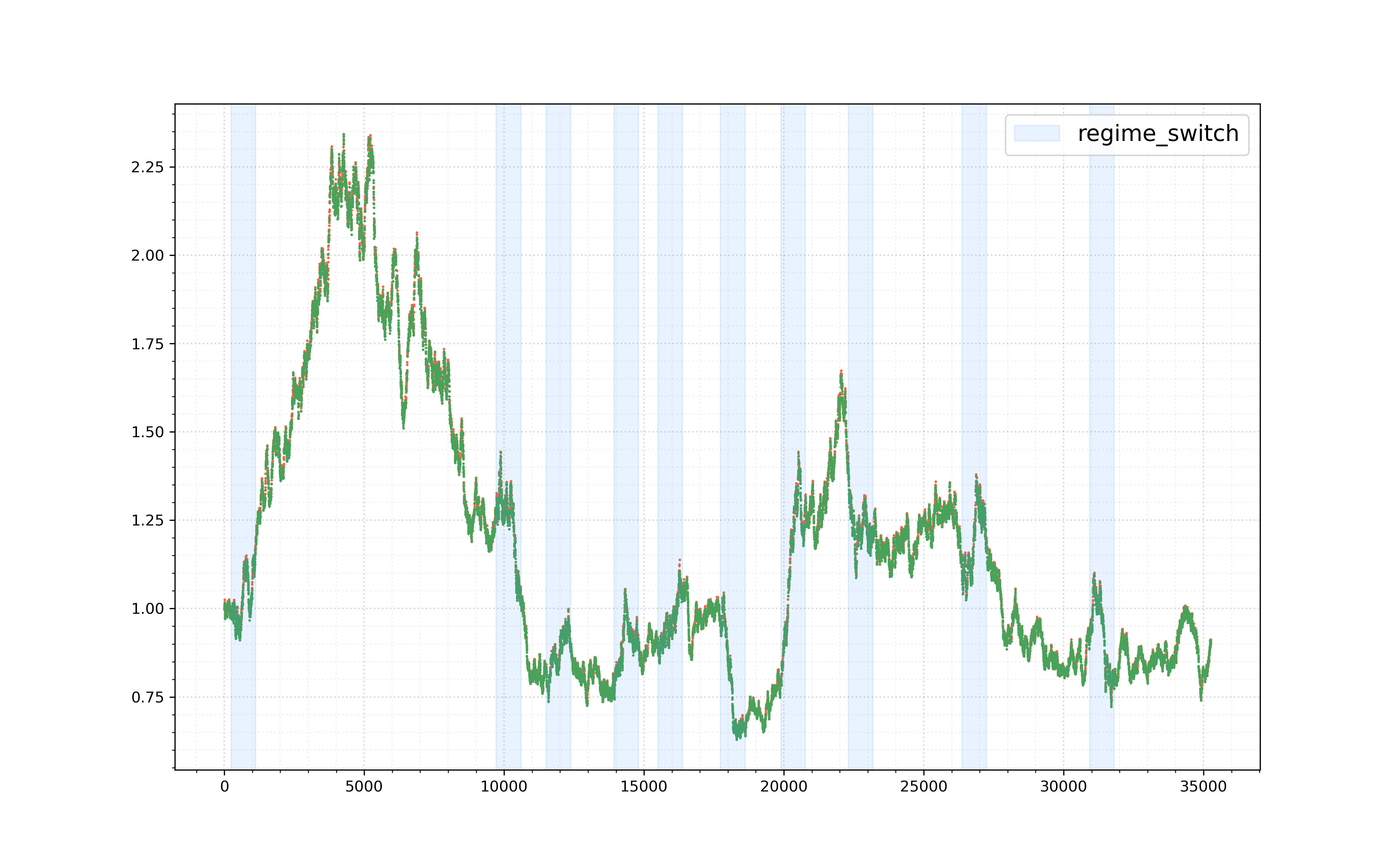

When a regime change occurs, the gBm parameters shift from to . Figure 5 shows an example of such a gBm path, with the regime change periods highlighted in red. Figure 5(b) gives the log-returns associated to Figure 5(a), again with the regime changes highlighted in red.

We ran all three clustering algorithms on the same simulated path data. As seen from Figure 6 and Figure 7, both algorithms perform well - they are able to accurately capture both the regime changes and ends. We give a summary of the accuracy scores of each algorithm in Table 3 for a total of runs.

| Algorithm | Total | Regime-on | Regime-off | Runtime |

|---|---|---|---|---|

| Wasserstein | ||||

| Moment | ||||

| HMM |

It is interesting to note that, even in the Gaussian case, the WK-means algorithm does a better job of picking up regime changes than the standard approach. By comparison, the HMM tends to fail to detect the changes in regime at this fixed level of difference in parameter space and thus cannot determine regime change times at this level of granularity between the two models. We provide the plots of the clustering algorithms in mean-variance space and the historical colouring plots in Figures 6 and 7.

We conclude this section by comparing the centroids obtained from either algorithm to the true measures. In this example, the distribution of the log-returns corresponding to either regime is given by

Since the distribution of log-returns in this model are Gaussian, we study the mean and variance of our obtained centroids and compare these to the true vales.

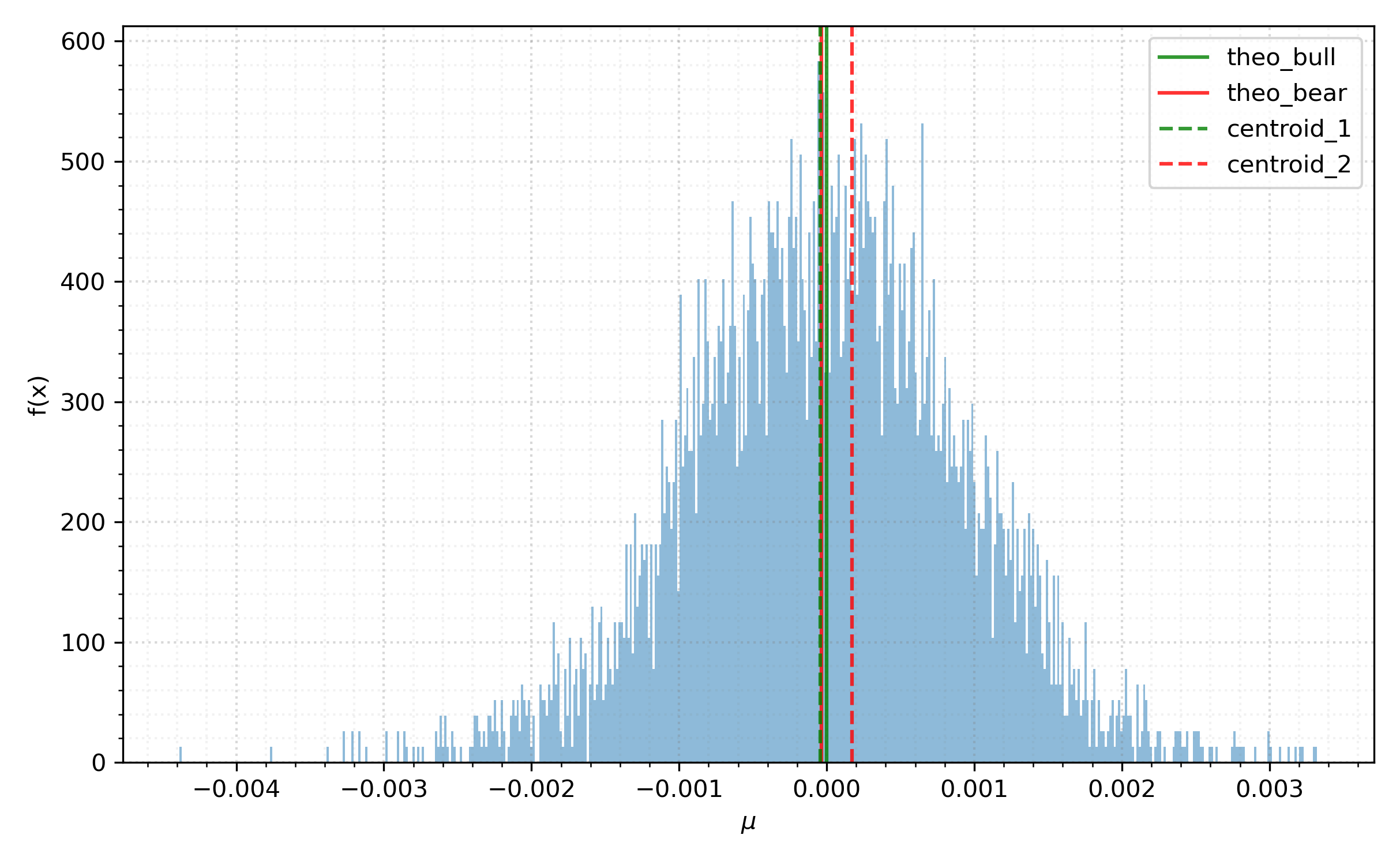

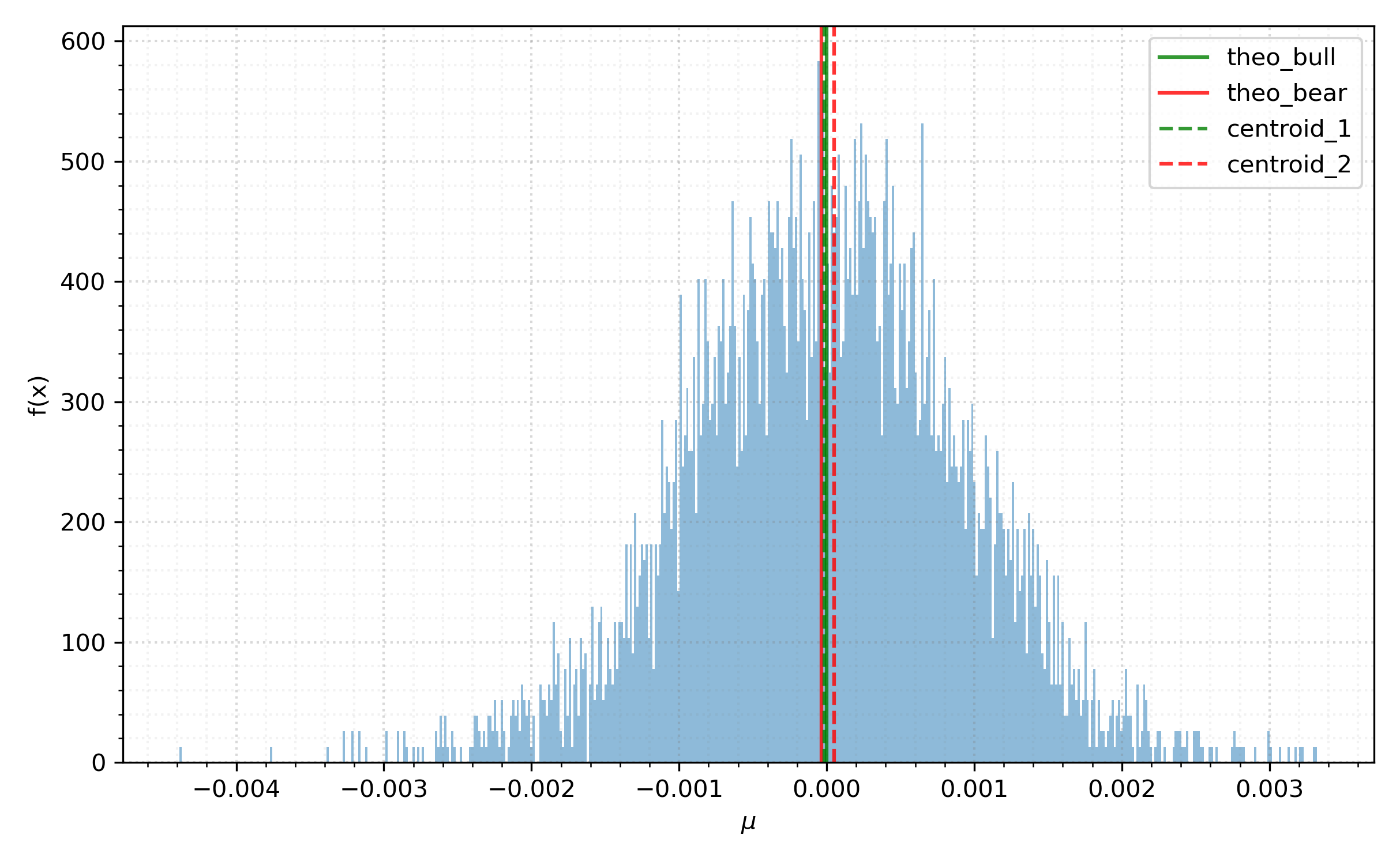

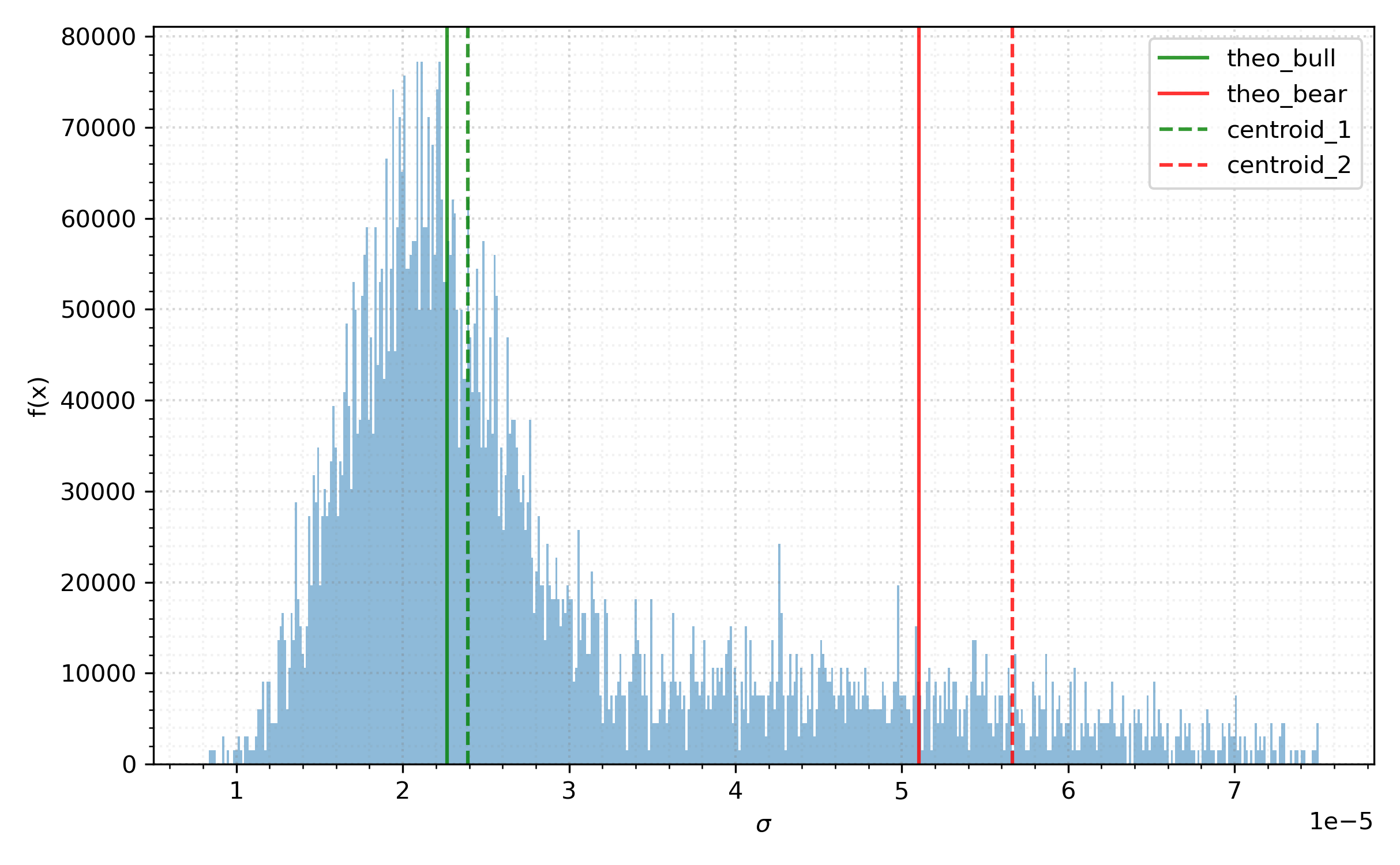

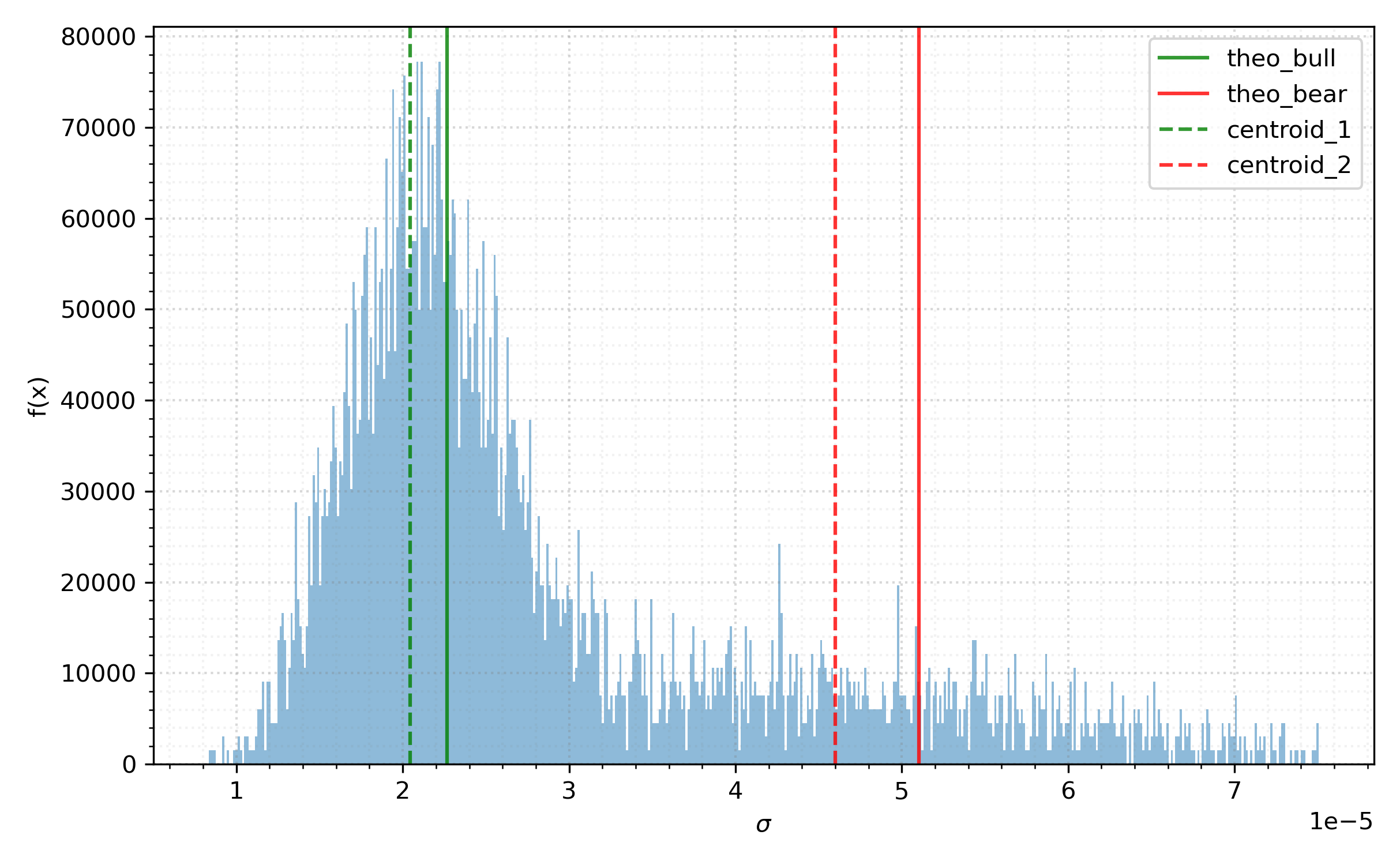

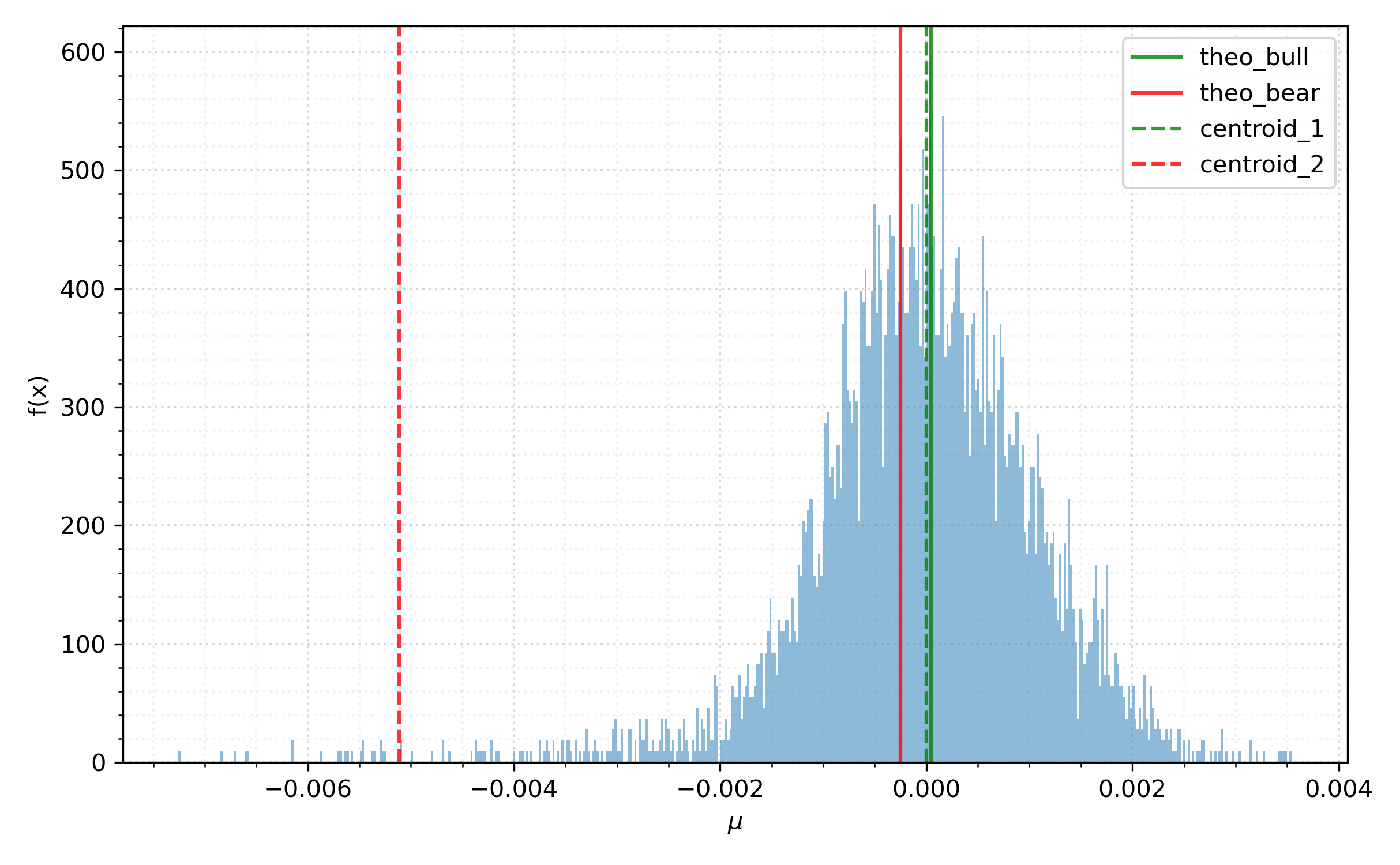

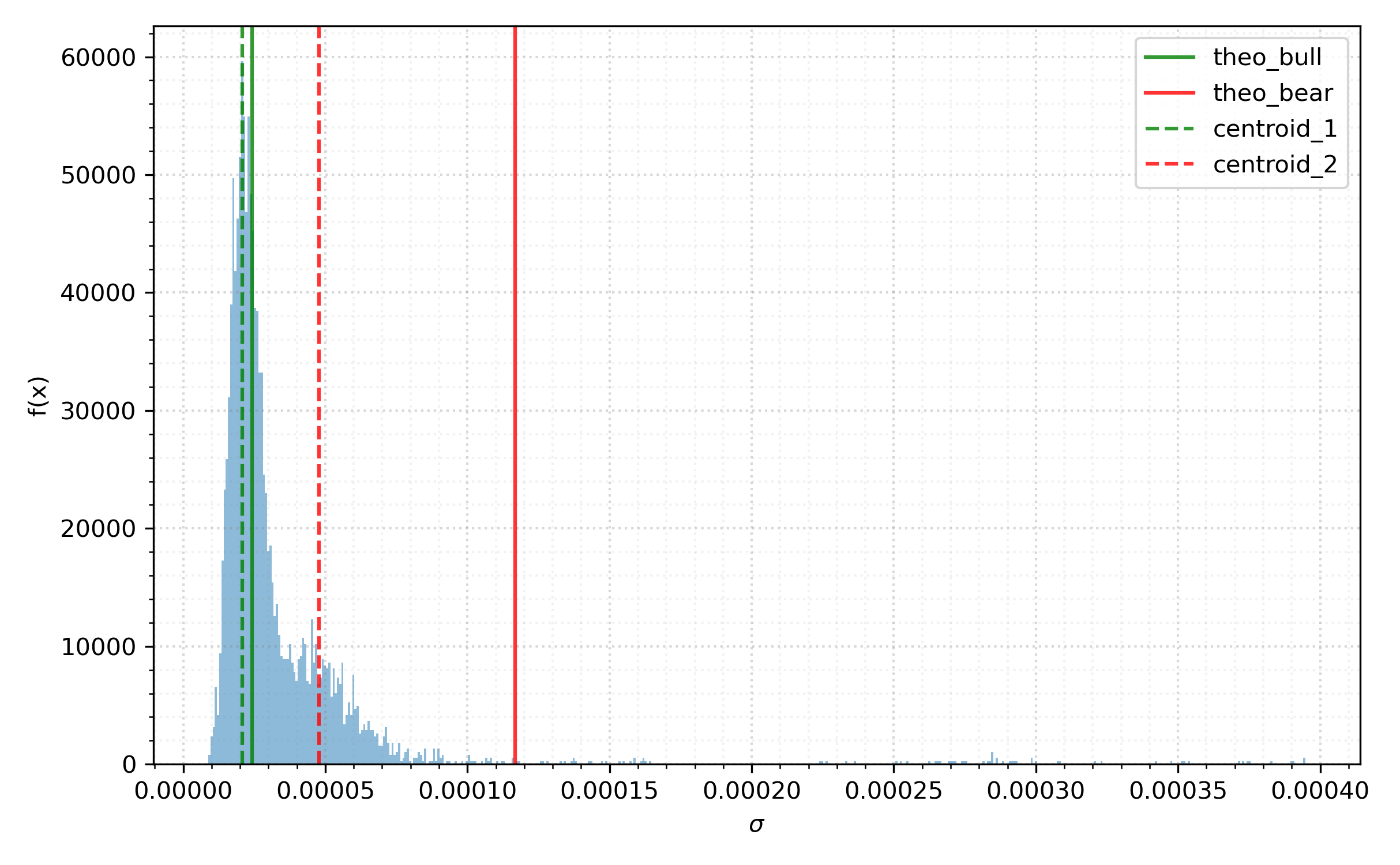

Figure 8 summarizes our findings. In the first row, we display the histogram of the partition means along with solid lines representing the true means and . In Figures 8(a) and 8(b), the dashed lines represent the bull and bear centroid means corresponding to the MK-means and WK-means algorithms respectively. In the second row, we repeat the same procedure with the variances , their true values, and in Figures 8(c) and 8(d) the centroid variances corresponding to the MK-means and WK-means algorithms respectively.

We see that the centroids derived from either algorithm perform well as estimators for the true centroids. We note that it is not altogether unsurprising that the Wasserstein algorithm does not significantly outperform the moments-based method here: since we are working under the assumption that distributions of log-returns under the “true” model are completely determined by their mean and variance.

3.3.2. Merton jump diffusion

In this section, we outline a separate model used to generate synthetic data where the associated log-returns are non-Gaussian. In particular, we model stock prices by a Merton jump diffusion, which is given by the solution to the stochastic differential equation

| (36) |

where

Here, is a Poisson random variable, and . Our model space is given by

| (37) |

The solution to (36) is given by

| (38) |

where , and is the Doléans-Dade stochastic exponential. Let be the log-return associated to a realisation of (38) at a time on a mesh with grid size . Then, [Syn08] gives that

| (39) | ||||

| (40) |

and we will use these quantities to check the suitability of the centroids from either algorithm to the true measures.

To test either algorithm on synthetic data as generated from (37), we apply the same methodology as outlined in Section 3.3. That is, we define two sets of parameters and a partition with regime changes for , where is given by (30). We then run both clustering algorithms over a Merton jump diffusion with parameters over intervals in and parameters elsewhere. In regime switch dynamics are given by the parameter choices

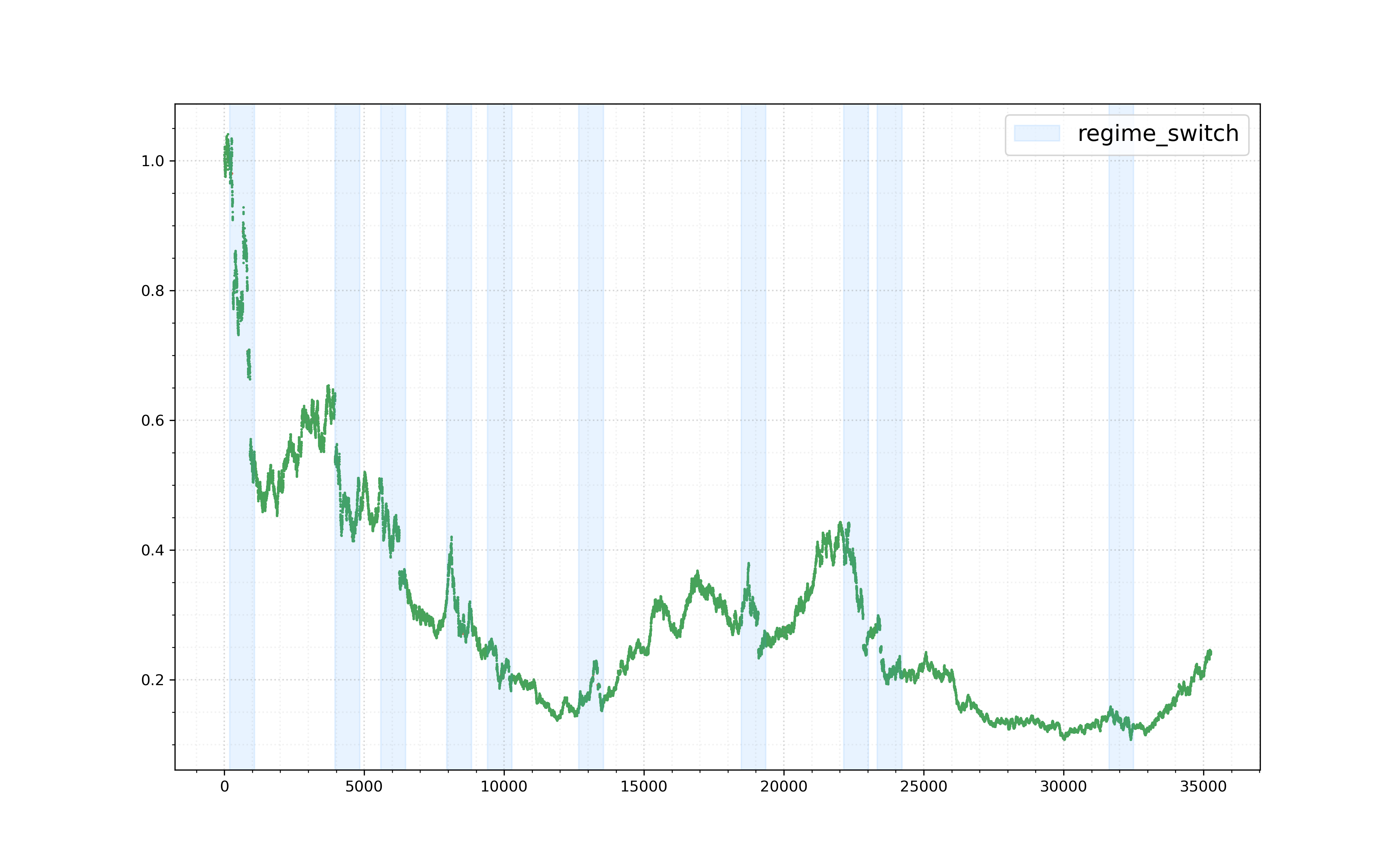

We again set and for . When a regime change occurs we shift the parameters of the Merton jump diffusion from to , and revert them back when the regime change ends. Figure 9 gives an example path and the associated log-returns, with the periods of regime change highlighted in red.

For the example path presented in Figure 9(a), we present plots from all three algorithms where applicable. Figure 10 gives the projection of the derived clusters for the moment- and WK-means algorithm. Here, one can see that the MK-means approach fails to discern between the two market regimes as it is not robust enough to adjust for outlier return series in the bear regime. By comparison, the Wasserstein approach is relatively robust to these outliers, and is able to correctly identify the two different regimes with their associated distributions.

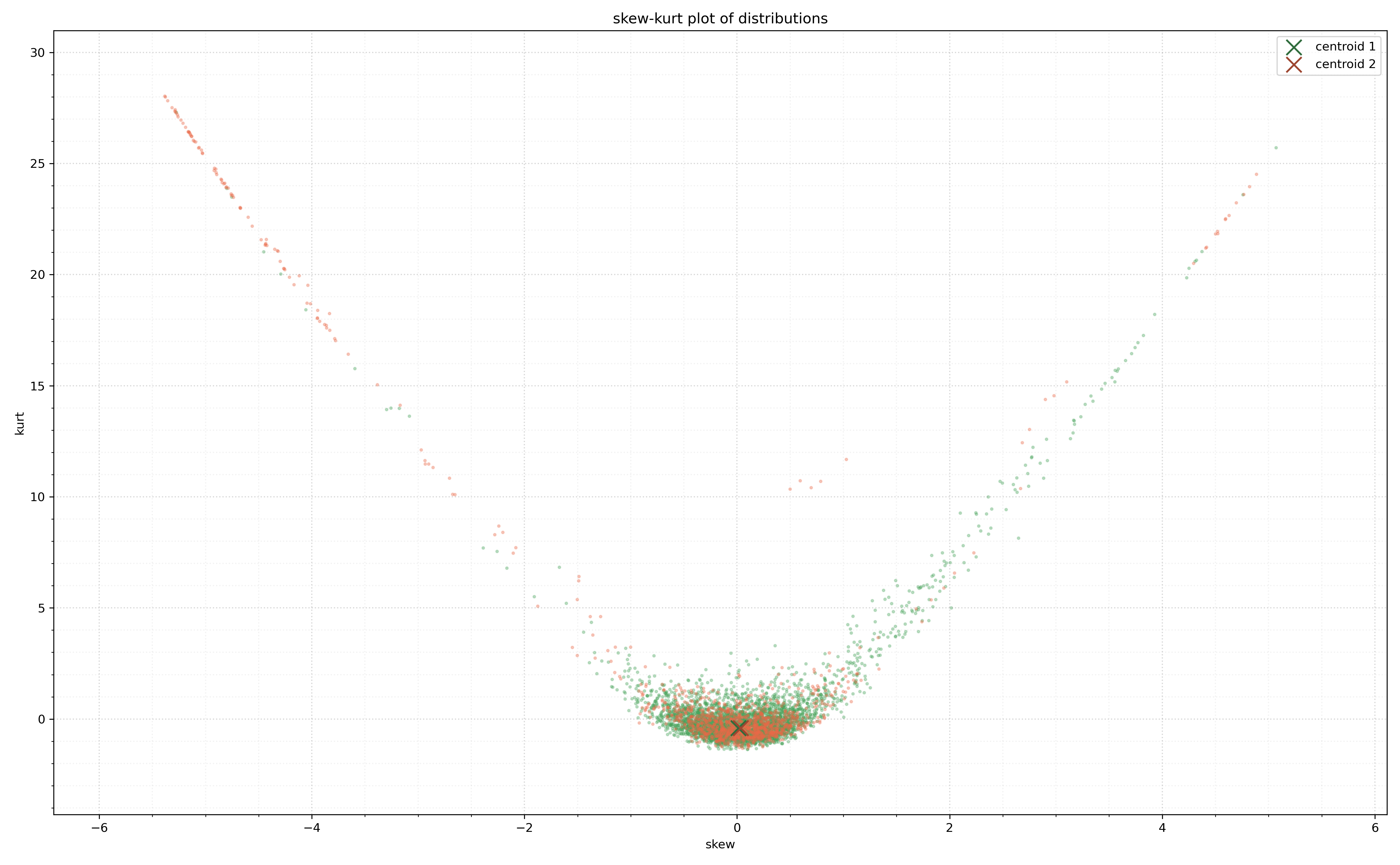

Figure 11 shows the WK-means clusters in skew-kurtosis space. We see here that the algorithm correctly identifies several distributions exhibiting positive skew as belonging to the bull regime. Furthermore, the algorithm is also able to discern between these distributions and those belonging to the bear regime, which are significantly more positively skewed.

We summarize the results for runs with the parameters . It is clear that both the MK-means and HMM approach are unable to discern between periods of regime change and normalcy. As expected, the Wasserstein approach does not fare as well as the Gaussian case, although the difference is negligible. Note that the high accuracy in the regime-on case for the HMM is due to the fact that it never identifies the alternate regime and places all points into the first category. For the path in Figure 9(a), we give the historical colouring plot associated to a run of all three algorithms in Figure 12, which highlights the numerical results obtained from the table.

| Algorithm | Total | Regime-on | Regime-off | Runtime |

|---|---|---|---|---|

| Wasserstein | ||||

| Moment | ||||

| HMM |

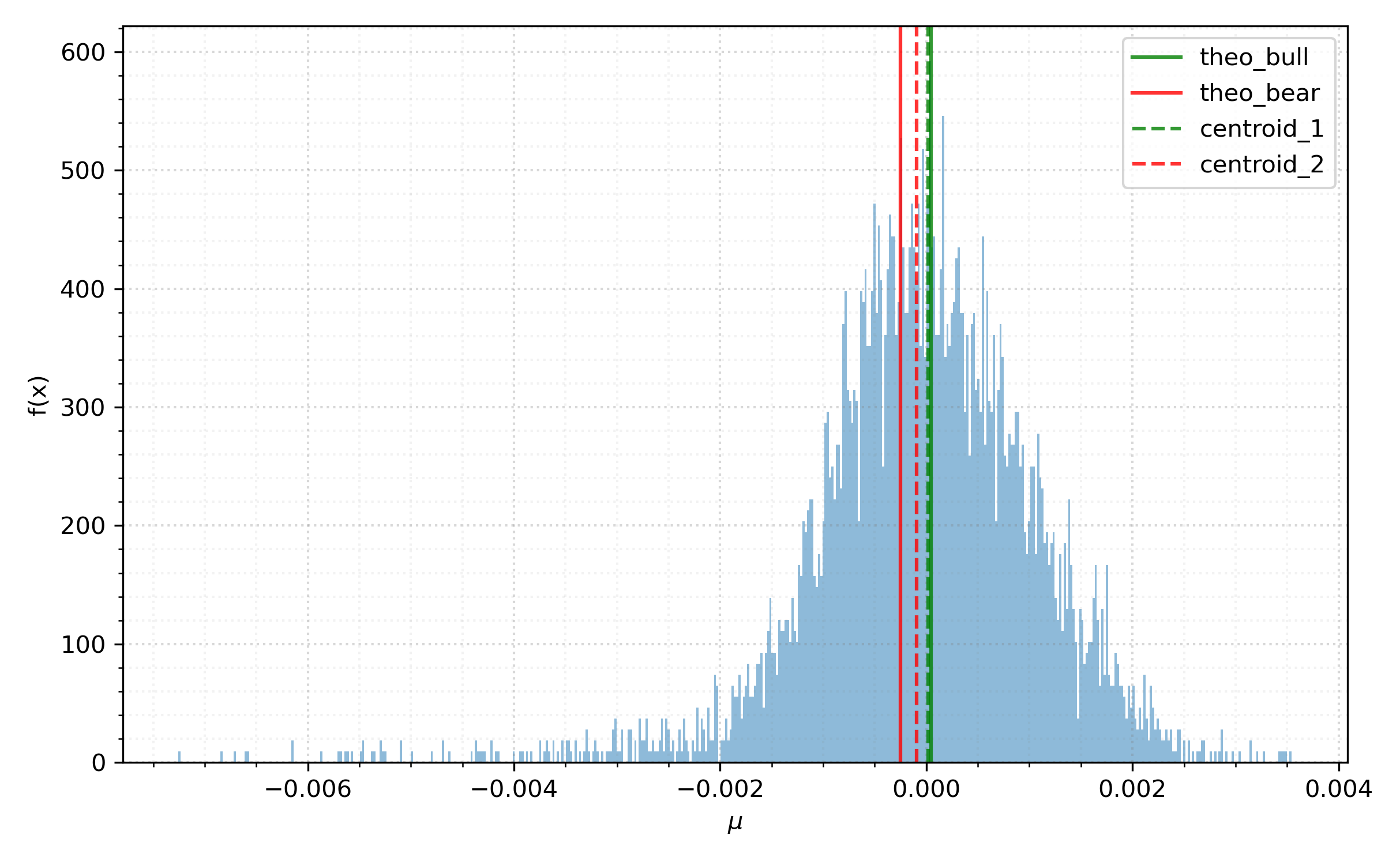

As we did with the geometric Brownian motion example, we conclude the results section with a comparison between the mean and variance of the centroids obtained from either algorithm, and those associated to the true distributions as given by equations (39) and (40). As expected, from Figures 13(a) and 13(c) it is clear that the MK-means centroids do a poor job of approximating the true measures associated to the bull and bear regimes. We compare this to Figures 13(b) and 13(d), where the mean and variance of the WK-means centroids are much closer to the theoretical counterparts.

3.4. Selection of hyperparameters

In this section we give a brief discussion regarding how the choice of hyperparameters affects the results of the WK-means algorithm. We begin with a discussion to the first hyperparameter , which corresponds to the number of returns that form each empirical distribution within the clustering algorithm. Classically one would like to take as large a value of as is feasibly possible in order to best approximate empirically the true data-generating measure. In the regime clustering context, however, this is not always ideal: choosing to be too large can mean that regime changes are not captured, or (in a live data setting) the detection of such changes are lagged. However, certainly if is chosen too small spurious classifications dominated by noise will be made. Thus we believe that the choice of window length hyperparameter is more an art than a science and strongly depends on the application in mind.

Regarding the overlap hyperparameter : heuristically, a larger value of overlap parameter (relative to ) can be thought of in two ways. Mechanically it is a way of increasing the number of samples used in the clustering algorithm, which may be necessary in a low-data environment. Heuristically, by increasing the clustering set with measures that are very similar to each other, one is indirectly making a statement about how representative the observed sequence of log-returns (and thus clustering set measures) relative to what one might deem “standard” conditions. This phenomena can be seen in the simple case when one clusters on S&P 500 data before and after the GFC: for and with , one would expect that the outlier centroid moves significantly faster to its new position than , whereas if is closer to , one expects the centroids to not initially change as much during the onset of the GFC, since new observations are less constituent relative to the corpus of measures preceding them.

We note however that in general the overlap hyperparameter does not have too large an effect on centroids obtained (and, thus, clusters) assuming that one is not operating in too low a data environment, and is suitably chosen. We present the results of clustering on SPY for the hyperparameter choice , the choice we made in Section 3.2, and in Figure 14. Here, one can see that the obtained centroids from either algorithm do not change drastically in spite of the lower data density.

Indeed a simple Kolmogorov-Smirnov two-sample test between the first centroids returns a test statistic score of with an associated -value of , and the second set of centroids yields the same score and -value.

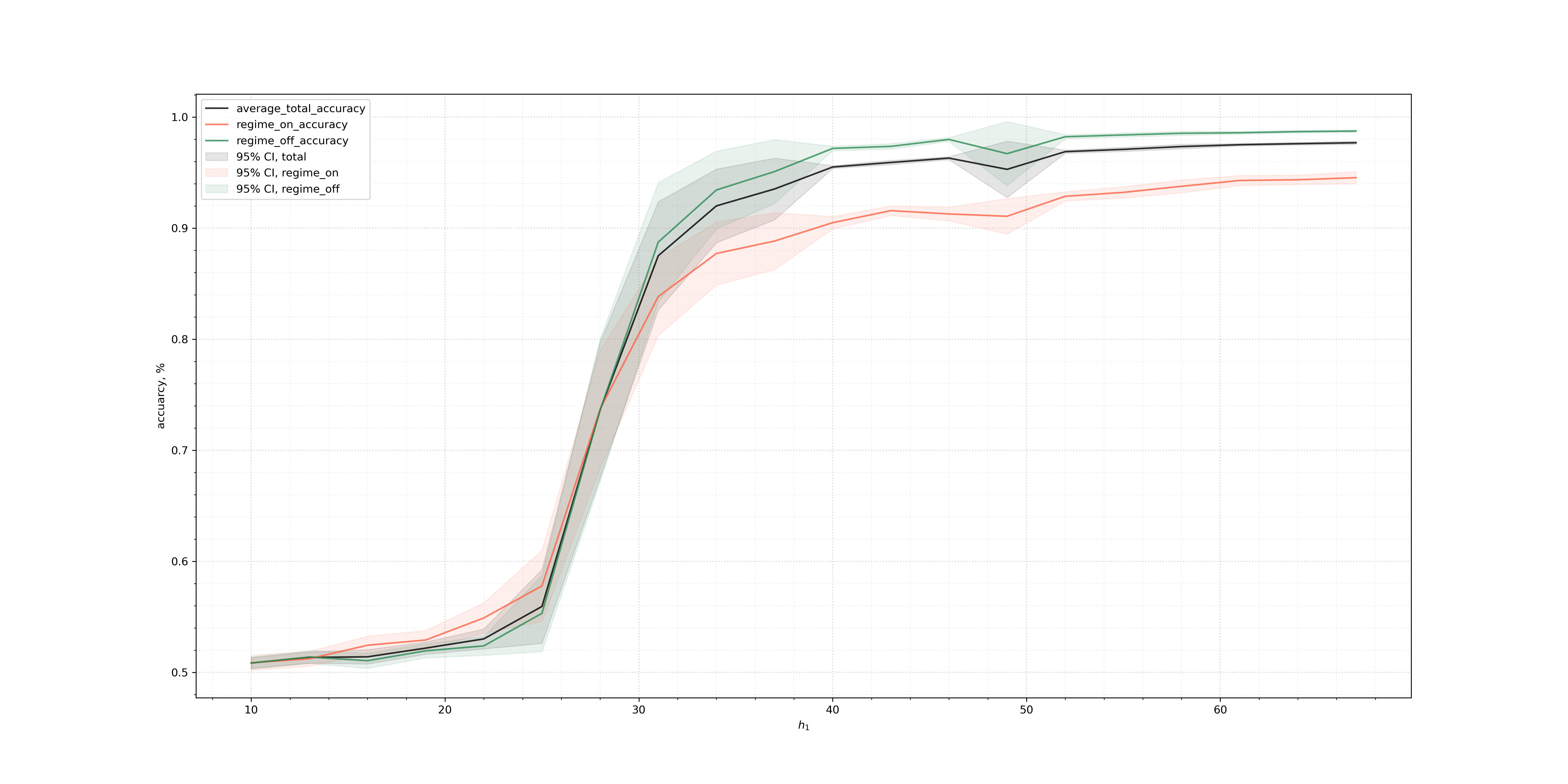

Finally, we test the effect of changing the window length parameter . As stated in the beginning of the section, there exist many incorrect choices for in practice (too small, or too large), but reasonable choices will tend to give robust results. To show this, we chose a sequence of window lengths and set the overlap parameter . We then ran the regime-switching experiment from Section 3.3 with the same switching dynamics as in Section 3.3.2, repeating the experiment times for each hyperparameter choice. In particular, regime changes in this setting lasted for half a year, which amounts to 882 time steps given our year mesh, which means that only an unreasonably large rolling window would miss the given regime change. Figure 15 gives the various accuracy results (total, regime-on, and regime-off) for the window length parameters given by . Past a certain threshold, the window length size does not matter and the model’s accuracy converges.

4. Conclusion

In this paper, we have shown that a slight modification to the -means algorithm does an excellent job at classifying partitions of market returns into regimes. We have verified this on both real data by comparing to known periods of market instability, and on synthetic data where we explicitly determine when the regime changes occur. We have compared this approach to a more standard moments-based algorithm which did not perform as well when returns were non-Gaussian, and a more classical approach using a hidden Markov model, which failed to accurately discern between regimes in the synthetic case. We also showed that clusters obtained via the Wasserstein approach are more self-similar than those derived from the moment-based method.

Future research would include employing other clustering algorithms rather than the standard k-means approach; for instance, fuzzy and hierarchical clustering methods. Further study into the robustness of the derived clusters under the choice of hyperparameters (that is, partitioning of the underlying time series) would also be relevant to understand how stable derived clusters are. We also note that there exist methodologies for determining the optimal number of clusters to be used. Finally, a more analytic and rigorous study of the weak convergence of derived centroids to the true measures (in the synthetic data case) would also be of interest.

Appendix A The -means algorithm

In this section, we outline some of the notation used in the paper, along with some standard results regarding the classical -means algorithm.

Recall that is a stream of data over a normed vector space .

Definition A.1 (Set of clusterings over ).

We write

to be the set of all possible (disjoint) clusterings over .

The -means algorithm returns an element which is locally optimal with respect to the induced metric on .

Before continuing with a more detailed explanation of the -means algorithm, we introduce the following definitions.

Definition A.2 (Within-cluster variation).

Let and let be a steam of data over a normed vector space . Suppose are disjoint clusters over . Associate to each its centroid for . Then, for a given , the within-cluster variation is defined as

| (41) |

Definition A.3 (Total-cluster variation).

With the notation of Definition A.2, define

| (42) |

to be the total-cluster variation corresponding to a clustering on the normed vector space .

Recall that denotes an intermediate disjoint clustering of the set at step . The -means algorithm first assigns nearest neighbours via (7) with respect to . The next step in the algorithm is to update the centroids via an aggregation function which gives a central element from the set of nearest neighbours for . In the classical -means on d, this function is given by

| (43) |

Here, denotes the cardinality of the set . Note that other choices of necessitate different aggregation methods depending on the structure of .

Continuing, the algorithm then updates the centroids via the function :

The new centroids are then compared to via the following stopping rule.

Definition A.4 (-means stopping rule).

Suppose is a normed vector space. For fixed , consider a loss function given by

| (44) |

For a tolerance level , the stopping rule corresponding to the standard -means algorithm is given by

| (45) |

where denotes the step of the algorithm, and we take .

Remark A.5.

Various algorithms which attempt to find the optimal number of clusters that should be used to separate data consider (41) as the loss to be minimised over all possible clusterings. We will not cover these algorithms in this paper (see, for instance [RT99]), and their applications to the MRCP are topics for future research.

A given run of the -means algorithm is characterised by the 2-tuple of centroids and nearest neighbour assignments . We conclude this section with the following proposition.

Proposition A.6.

The -means algorithm converges in finitely many steps to a local minima.

Proof.

Finiteness is guaranteed since the number of possible partitions of datum is at most . Thus, the function necessarily achieves a global minimum. Therefore, the sequence is non-increasing (by definition of the -means update step (7)) and bounded from below, which guarantees convergence to a local minima. ∎

Appendix B The maximum mean discrepancy

In this section, we include extra details regarding the derivation of the MMD from Definition 1.7. In particular we show how one can show the MMD can be employed as a metric on the space of probability measures.

Definition B.1 (Reproducing kernel Hilbert space, [Aro50], Section 1.1).

Suppose is a non-empty set, and let be a Hilbert space of functions . We call a positive definite function a reproducing kernel of if

-

(i)

For all , we have that , and

-

(ii)

For all and , one has that

(46) referred to as the reproducing property.

We call the Hilbert space associated to a reproducing kernel Hilbert space (RKHS).

We can associate to each RKHS the canonical feature map given by . We thus have that

by the reproducing property from Definition B.1. Directly from the definition of a RKHS , we have the following equivalent definition.

Definition B.2 ([BTA11], Theorem 1).

Suppose is a Hilbert space. Define to be the evaluation map. Then, is a RKHS if and only if is continuous.

Proof.

Suppose that is a RKHS. Denote by as the dual of . One has that

| (47) |

so in particular the linear operator is bounded with operator norm equal to , which is well-defined by positive definiteness of . Since the upper bound in (47) is achieved by , is bounded with operator norm . Since is bounded, it is continuous.

Now suppose that is bounded, so . By the Riesz representation theorem, there exists an element such that . Define . We then have that and by construction. Thus, properties (1) and (2) are satisfied in Definition B.1, so is a RKHS. ∎

In what follows, we will choose our function class from Definition 1.7 to be the unit ball in a RKHS with associated reproducing kernel

| (48) |

called the Gaussian kernel. Importantly, such a RKHS has the following property, as shown in Steinwart [Ste01].

Definition B.3 (Steinwart [Ste01], Definition 4).

Let be a compact metric space. Suppose is a RKHS with associated reproducing kernel . We call universal if

-

(i)

is continuous, and

-

(ii)

is dense in , the space of bounded continuous functions on , with respect to the supremum norm .

This choice of RKHS ensures that the MMD is metric on the space of Borel probability measures, which allows us to conclude the following.

Theorem B.4 ([GBR+12], Theorem 5).

Let be the unit ball of a universal RKHS comprised of -functions on a compact space . Suppose are Borel. Then if and only if .

Proof.

For , consider the linear functional given by . We have that

so in particular is continuous if is measurable and . By the Riesz representation theorem, there exists a such that . In particular,

We call the mean embedding of in . From (9), we have that

| (49) |

Here, we have used the fact that is a unit ball in . Suppose that . By (49), this implies .

Now suppose that . By universality of , for any and there exists a such that

| (50) |

Then, we have that

| (51) |

where we have used the fact that for measures and , (50) gives that

and

since we assumed . Thus as (51) holds for all . ∎

Remark B.5.

Using the definition of the mean embedding, the fact that , and the reproducing property of , we can write (49) as

| (52) |

since, for example,

Given samples and , a biased empirical estimate of (52) is given by

| (53) |

We will use the test statistic (53) to evaluate the success of a given clustering algorithm.

Appendix C The Wasserstein distance

In this section, we include proofs of results regarding the Wasserstein distance.

Proposition C.1 (Wasserstein barycenter, empirical measures).

Suppose that are a family of empirical probability measures, each with atoms for . Let

Then, the cumulative distribution function of the Wasserstein barycenter over with respect to the 1-Wasserstein distance is given by

| (54) |

Moreover, is not necessarily unique.

Remark C.2 ().

When , the proof follows in a similar manner. One will arrive at

Proof.

Assume that , so each measure is comprised of only one atom for . WLOG we can also assume that the sequence is non-decreasing. By convexity of the function for , the Wasserstein barycenter will also have atoms. Then, by (21) the problem of finding the barycenter is equivalent to the optimisation

| (55) |

The minimiser to the right-hand side of (55) is obtained by solving over , where

Since

we have that

| (56) |

In particular, if , then . If , then the (unique) optimizer is given by where . Setting gives (54).

References

- [ABS08] M. Ackermann, J. Blömer, and C. Sohler. Clustering for metric and non-metric distance measures. volume 6, pages 799–808, 01 2008. doi:10.1145/1347082.1347170.

- [ACADF20] P. Alquier, B.-E. Chérief-Abdellatif, A. Derumigny, and J.-D. Fermanian. Estimation of copulas via maximum mean discrepancy, 2020, 2010.00408.

- [Ach01] S. B. Achelis. Technical analysis from a to z, 2001.

- [AG13] L. Ambrosio and N. Gigli. A user’s guide to optimal transport. In Modelling and optimisation of flows on networks, pages 1–155. Springer, 2013.

- [AGS05] L. Ambrosio, N. Gigli, and G. Savare. Gradient Flows: In Metric Spaces and in the Space of Probability Measures. Lectures in Mathematics. ETH Zürich. Birkhäuser Basel, 2005. URL https://books.google.co.uk/books?id=HZqhWIq1-jgC.

- [Aro50] N. Aronszajn. Theory of reproducing kernels. Transactions of the American mathematical society, 68(3):337–404, 1950.

- [BBDG19] F.-X. Briol, A. Barp, A. B. Duncan, and M. Girolami. Statistical inference for generative models with maximum mean discrepancy, 2019, 1906.05944.

- [BG21] E. Bayraktar and G. Guoï. Strong equivalence between metrics of wasserstein type. Electronic Communications in Probability, 26:1–13, 2021.

- [BHL+20] H. Buehler, B. Horvath, T. Lyons, I. Perez Arribas, and B. Wood. A data-driven market simulator for small data environments. Available at SSRN 3632431, 2020.

- [BKA+19] P. Bonnier, P. Kidger, I. P. Arribas, C. Salvi, and T. J. Lyons. Deep signatures. CoRR, abs/1905.08494, 2019, 1905.08494. URL http://arxiv.org/abs/1905.08494.

- [BRPP15] N. Bonneel, J. Rabin, G. Peyré, and H. Pfister. Sliced and radon wasserstein barycenters of measures. Journal of Mathematical Imaging and Vision, 51(1):22–45, 2015.

- [BTA11] A. Berlinet and C. Thomas-Agnan. Reproducing Kernel Hilbert Spaces in Probability and Statistics. Springer US, 2011. URL https://books.google.co.uk/books?id=bX3TBwAAQBAJ.

- [CAA21] B.-E. Chérief-Abdellatif and P. Alquier. Finite sample properties of parametric mmd estimation: robustness to misspecification and dependence, 2021, 1912.05737.

- [CDB86] R. L. Cannon, J. V. Dave, and J. C. Bezdek. Efficient implementation of the fuzzy c-means clustering algorithms. IEEE transactions on pattern analysis and machine intelligence, (2):248–255, 1986.

- [CFLA20] T. Cochrane, P. Foster, T. Lyons, and I. P. Arribas. Anomaly detection on streamed data. arXiv preprint arXiv:2006.03487, 2020.

- [Con01] R. Cont. Empirical properties of asset returns: stylized facts and statistical issues. 2001.

- [DB79] D. L. Davies and D. W. Bouldin. A cluster separation measure. IEEE Transactions on Pattern Analysis and Machine Intelligence, PAMI-1(2):224–227, 1979. doi:10.1109/TPAMI.1979.4766909.

- [Dun74] J. C. Dunn. Well-separated clusters and optimal fuzzy partitions. Journal of Cybernetics, 4(1):95–104, 1974, https://doi.org/10.1080/01969727408546059. doi:10.1080/01969727408546059.

- [DVR15] J. G. Dias, J. K. Vermunt, and S. Ramos. Clustering financial time series: New insights from an extended hidden markov model. European Journal of Operational Research, 243(3):852–864, 2015.

- [FGSS07] K. Fukumizu, A. Gretton, X. Sun, and B. Schölkopf. Kernel measures of conditional dependence. In NIPS, volume 20, pages 489–496, 2007.

- [FGSS09] K. Fukumizu, A. Gretton, B. Schölkopf, and B. K. Sriperumbudur. Characteristic kernels on groups and semigroups. In D. Koller, D. Schuurmans, Y. Bengio, and L. Bottou, editors, Advances in Neural Information Processing Systems, volume 21. Curran Associates, Inc., 2009. URL https://proceedings.neurips.cc/paper/2008/file/d07e70efcfab08731a97e7b91be644de-Paper.pdf.

- [GBC16] I. Goodfellow, Y. Bengio, and A. Courville. Deep Learning. The MIT Press, 2016.

- [GBR+07] A. Gretton, K. Borgwardt, M. Rasch, B. Schölkopf, and A. J. Smola. A kernel method for the two-sample-problem. In B. Schölkopf, J. C. Platt, and T. Hoffman, editors, Advances in Neural Information Processing Systems 19, pages 513–520. MIT Press, 2007. URL http://papers.nips.cc/paper/3110-a-kernel-method-for-the-two-sample-problem.pdf.

- [GBR+12] A. Gretton, K. M. Borgwardt, M. J. Rasch, B. Schölkopf, and A. Smola. A kernel two-sample test. Journal of Machine Learning Research, 13(Mar):723–773, 2012.

- [GFHS09] A. Gretton, K. Fukumizu, Z. Harchaoui, and B. K. Sriperumbudur. A fast, consistent kernel two-sample test. In Y. Bengio, D. Schuurmans, J. D. Lafferty, C. K. I. Williams, and A. Culotta, editors, Advances in Neural Information Processing Systems 22, pages 673–681. Curran Associates, Inc., 2009. URL http://papers.nips.cc/paper/3738-a-fast-consistent-kernel-two-sample-test.pdf.

- [Gui11] M. Guidolin. Markov switching models in empirical finance. In Missing data methods: Time-series methods and applications. Emerald Group Publishing Limited, 2011.

- [Ham89] J. D. Hamilton. A new approach to the economic analysis of nonstationary time series and the business cycle. Econometrica: Journal of the econometric society, pages 357–384, 1989.

- [HGER15] K. Henderson, B. Gallagher, and T. Eliassi-Rad. Ep-means: An efficient nonparametric clustering of empirical probability distributions. In Proceedings of the 30th Annual ACM Symposium on Applied Computing, pages 893–900, 2015.

- [HMT19] B. Horvath, A. Muguruza, and M. Tomas. Deep learning volatility. Available at SSRN 3322085, 2019.

- [KMN+02] T. Kanungo, D. M. Mount, N. S. Netanyahu, C. D. Piatko, R. Silverman, and A. Y. Wu. An efficient k-means clustering algorithm: Analysis and implementation. IEEE transactions on pattern analysis and machine intelligence, 24(7):881–892, 2002.

- [KNS+19] S. Kolouri, K. Nadjahi, U. Simsekli, R. Badeau, and G. K. Rohde. Generalized sliced wasserstein distances. arXiv preprint arXiv:1902.00434, 2019.

- [KSH20] A. Kondratyev, C. Schwarz, and B. Horvath. Data anonymisation, outlier detection and fighting overfitting with restricted boltzmann machines. Outlier Detection and Fighting Overfitting with Restricted Boltzmann Machines (January 27, 2020), 2020.

- [Kua02] C.-M. Kuan. Lecture on the markov switching model. Institute of Economics Academia Sinica, 8(15):1–30, 2002.

- [Lah16] S. Lahmiri. Clustering of casablanca stock market based on hurst exponent estimates. Physica A: Statistical Mechanics and its Applications, 456:310–318, 2016.

- [LM00] T. Lux and M. Marchesi. Volatility clustering in financial markets: a microsimulation of interacting agents. International journal of theoretical and applied finance, 3(04):675–702, 2000.

- [LR09] T. Lange and A. Rahbek. An introduction to regime switching time series models. In Handbook of Financial Time Series, pages 871–887. Springer, 2009.

- [LW08] J. Li and J. Z. Wang. Real-time computerized annotation of pictures. IEEE transactions on pattern analysis and machine intelligence, 30(6):985–1002, 2008.

- [MMS12] J. Maheu, T. McCurdy, and Y. Song. Components of bull and bear markets: Bull corrections and bear rallies. Journal of Business and Economic Statistics, 30, 07 2012. doi:10.2139/ssrn.1939486.

- [MS83] D. M. Mason and J. H. Schuenemeyer. A modified kolmogorov-smirnov test sensitive to tail alternatives. The annals of Statistics, pages 933–946, 1983.

- [MZGW18] L. Mi, W. Zhang, X. Gu, and Y. Wang. Variational wasserstein clustering. In Proceedings of the European Conference on Computer Vision (ECCV), pages 322–337, 2018.

- [NHZ16] Y. S. Niu, N. Hao, and H. Zhang. Multiple change-point detection: a selective overview. Statistical Science, pages 611–623, 2016.

- [NN09] F. Nielsen and R. Nock. Sided and symmetrized bregman centroids. IEEE transactions on Information Theory, 55(6):2882–2904, 2009.

- [NNA14] F. Nielsen, R. Nock, and S.-i. Amari. On clustering histograms with k-means by using mixed -divergences. Entropy, 16(6):3273–3301, 2014.

- [NSW+20] H. Ni, L. Szpruch, M. Wiese, S. Liao, and B. Xiao. Conditional sig-wasserstein gans for time series generation, 2020, 2006.05421.

- [Pel06] D. Pelletier. Regime switching for dynamic correlations. Journal of Econometrics, 131(1):445 – 473, 2006. doi:https://doi.org/10.1016/j.jeconom.2005.01.013.

- [Rou87] P. J. Rousseeuw. Silhouettes: A graphical aid to the interpretation and validation of cluster analysis. Journal of Computational and Applied Mathematics, 20:53–65, 1987. doi:https://doi.org/10.1016/0377-0427(87)90125-7.

- [RPDB11] J. Rabin, G. Peyré, J. Delon, and M. Bernot. Wasserstein barycenter and its application to texture mixing. In International Conference on Scale Space and Variational Methods in Computer Vision, pages 435–446. Springer, 2011.

- [RT99] S. Ray and R. H. Turi. Determination of number of clusters in k-means clustering and application in colour image segmentation. In Proceedings of the 4th international conference on advances in pattern recognition and digital techniques, pages 137–143. Calcutta, India, 1999.

- [RY04] D. Revuz and M. Yor. Continuous Martingales and Brownian Motion. Grundlehren der mathematischen Wissenschaften. Springer Berlin Heidelberg, 2004. URL https://books.google.co.uk/books?id=1ml95FLM5koC.

- [San15] F. Santambrogio. Optimal Transport for Applied Mathematicians. Calculus of Variations, PDEs and Modeling. 2015.

- [Ste01] I. Steinwart. On the influence of the kernel on the consistency of support vector machines. Journal of machine learning research, 2(Nov):67–93, 2001.

- [Syn08] D. Synowiec. Jump-diffusion models with constant parameters for financial log-return processes. Computers and Mathematics with Applications, 56(8):2120 – 2127, 2008. doi:https://doi.org/10.1016/j.camwa.2008.02.051.

- [Vel02] R. Veldhuis. The centroid of the symmetrical kullback-leibler distance. IEEE signal processing letters, 9(3):96–99, 2002.

- [WGX21] J. Wang, R. Gao, and Y. Xie. Two-sample test using projected wasserstein distance: Breaking the curse of dimensionality, 2021, 2010.11970.

- [YWWL17] J. Ye, P. Wu, J. Z. Wang, and J. Li. Fast discrete distribution clustering using wasserstein barycenter with sparse support. IEEE Transactions on Signal Processing, 65(9):2317–2332, 2017.