draft

Efficient Estimation of Average Derivatives in NPIV Models:

Simulation Comparisons of Neural Network Estimators††thanks: We are grateful to Vanya Klenovskiy for excellent research assistance in applying our code

to estimate the Strawberry demand and to Josh Purtell in partially checking our code

documentation. We thank Denis Chetverikov for insightful discussions at the Gary

Chamberlain online seminar. We also thank A. Babii, S. Bonhomme, E. Ghysels, S. Han, G.

Imbens, P. Kline, O. Linton, W. Newey, M. Pelger, D. Ritzwoller, B. Ross, P. Sant’Anna, Y.

Sun, A. Timmermann, D. Xiu, Y. Zhu, and participants at various seminars and conferences

for helpful comments. Any errors are the responsibility of the authors. An implementation

for the procedures is available at https://github.com/jiafengkevinchen/cct-ann.

Artificial Neural Networks (ANNs) can be viewed as nonlinear sieves that can approximate complex functions of high dimensional variables more effectively than linear sieves. We investigate the performance of various ANNs in nonparametric instrumental variables (NPIV) models of moderately high dimensional covariates that are relevant to empirical economics. We present two efficient procedures for estimation and inference on a weighted average derivative (WAD): an orthogonalized plug-in with optimally-weighted sieve minimum distance (OP-OSMD) procedure and a sieve efficient score (ES) procedure. Both estimators for WAD use ANN sieves to approximate the unknown NPIV function and are root- asymptotically normal and first-order equivalent. We provide a detailed practitioner’s recipe for implementing both efficient procedures. We compare their finite-sample performances in various simulation designs that involve smooth NPIV function of up to 13 continuous covariates, different nonlinearities and covariate correlations. Some Monte Carlo findings include: 1) tuning and optimization are more delicate in ANN estimation; 2) given proper tuning, both ANN estimators with various architectures can perform well; 3) easier to tune ANN OP-OSMD estimators than ANN ES estimators; 4) stable inferences are more difficult to achieve with ANN (than spline) estimators; 5) there are gaps between current implementations and approximation theories. Finally, we apply ANN NPIV to estimate average partial derivatives in two empirical demand examples with multivariate covariates.

JEL Classification: C14; C22

Keywords: Artificial neural networks; Relu; Sigmoid; Nonparametric instrumental variables; Weighted average derivatives; Optimal sieve minimum distance; Efficient influence; Semiparametric efficiency; Endogenous demand.

1 Introduction

Deep layer Artificial Neural Networks (ANNs) are increasingly popular in machine learning (ML), statistics, business, finance, and other fields. The universal approximation property of a variety of ANN architectures has been established by Hornik, Stinchcombe and White (1989) and many others. Early on, computational difficulties have hindered the wide applicability of ANNs. Recently, improvements in computing have led to successful applications of deep layer ANNs in computer vision, natural language processing and other areas, with complex nonlinear relations among many covariates and large data sets of high quality.111By high quality we mean data sets with very high signal-to-noise ratios. Unfortunately, many economic and social science data sets have low signal-to-noise ratios. Many problems where deep layer ANNs are extremely effective involve prediction problems (i.e. estimating conditional means or densities)—or problems in which nuisance parameters are themselves predictions. Recently, Farrell et al. (2018) and Athey, Imbens, Metzger and Munro (2019), among others, have applied multi-layer ReLU ANNs to estimate average treatment effects under unconfoundedness and demonstrated their good performance in estimating unknown conditional means and densities of multivariate covariates.It remains to be seen whether ANNs are similarly effective for structural estimation problems with nonparametric endogeneity.

To that end, we consider semiparametric efficient estimation and inference for a weighted average (partial) derivative (WAD) of a nonparametric instrumental variables regression (NPIV) via ANN sieves. Specifically, we assume an unknown structure function satisfies the NPIV model: , where is a continuous random vector of moderately high dimension (including endogenous regressors that are excluded from ), and is a vector of moderately high dimensional conditioning variables. We are interested in efficient estimation and inference for a WAD parameter of the smooth NPIV function , without sparsity assumptions on .222Of course, in lieu of sparsity, we do require smoothness assumptions.WADs of structural relationships are linked to elasticities of endogenous demand systems in economics. It is essentially a treatment effect parameter under confounding and endogenous continuous treatment. Although there is a large literature on efficient estimation of the average treatment effect and other causal parameters under unconfoundedness, there are far fewer results on efficient estimation and inference on the average treatment effect in nonparametric models with endogenous continuous treatment.

This paper makes three contributions. First, we present two classes of efficient estimators for WADs of NPIV models where unknown is approximated by ANN sieves: the optimally weighted sieve minimum distance estimators and the efficient score-based estimators.Under some regularity conditions both types of estimators are root- asymptotically normal, semiparametrically efficient, and hence are first-order equivalent. Second, we detail a practitioner’s recipe that include a step by step guide for implementing these two classes of estimators. Third, and perhaps most importantly, we present a large set of Monte Carlo results on finite-sample performances of various ANN estimators. These are implemented using increasingly complex designs, such as NPIV function containing up to 13 continuous covariates (including endogenous regressors), various nonlinearities and correlations among the covariates.

We now briefly introduce the two classes of efficient estimation procedures that we consider. Both procedures are inspired by the semiparametric efficiency bound characterization in Ai and Chen (2012) (henceforth AC12) for the WAD of the unknown in a NPIV model . The first procedure is based on minimizing an optimal criterion, the optimally-weighted orthogonalized sieve minimum distance (SMD) criterion. This procedure is numerically equivalent to a semiparametric two-step procedure, where the unknown NPIV function is estimated via an optimally weighted SMD in the first step, and the WAD of is estimated using a sample analogue of an orthogonalized unconditional moment (Chamberlain, 1992) in the second step, with the unknown substituted by the optimally weighted SMD estimator from the first step. This will be denoted as OP-OSMD in our paper. AC12 already introduced this procedure and presented a small Monte Carlo study demonstrating its finite-sample performance using a spline SMD in the first step when the unknown is a function of a scalar endogenous variable . It is unclear how this procedure will perform when could be a continuous random vector of higher dimension and when is approximated via a neural network.

The second procedure is based on the efficient score (equivalently, efficient influence function).333The efficient score/influence function approach to efficient estimation has a long history in semiparametrics. See, e.g., Bickel et al. (1993), Pfanzagl (1982), Section 25.8 of Van der Vaart (2000) and references therein, for an introduction. AC12 derived a characterization of the efficient influence (or equivalently, efficient score) for the WAD of a NPIV model. It is also the asymptotic influence function of the OP-OSMD estimator.444This is not surprising since the efficient influence function is unique. The efficient influence is the sum of the orthogonalized unconditional moment (the one used for the OP-OSMD estimator) and an adjustment term accounting for plugging-in estimated , often referred to as the Riesz representer term. Compared to simpler settings, e.g. estimating average treatment effect under unconfoundedness, the Riesz representer term here has no closed-form expression, but is characterized as one solution to an optimization problem over an infinite-dimensional Hilbert space induced by a norm connected to the optimally weighted minimum distance objective. The components of the efficient influence function can nonetheless be consistently estimated via sieve approximations. The procedure using the sample estimated efficient influence (i.e., efficient score) will be denoted as ES in our paper. To the best of our knowledge, there is no published work on theory or simulation on the finite-sample performance of any ES estimator for the WAD in a NPIV model yet.

In this paper we investigate the finite-sample performance of both efficient procedures when the unknown function is estimated via various ANN SMDs and when depends on moderately high dimensional continuous regressors (some of which are endogenous). We describe some stylized findings from our simulations. Our simulations reveal that the ANN OP-OSMD is more stable and easier to implement than ANN ES for estimation of the average (partial) derivative in a NPIV model with unknown conditional variance .

In practice, it could be appealing to report simpler inefficient estimators that are still consistent and -asymptotically normal. It is also possible that computationally simpler inefficient estimators may perform better than the efficient estimators in finite samples, as the efficient estimators often require estimating additional nuisance parameters. For the sake of comparison, we include two first-order asymptotically equivalent inefficient estimators of the WAD of a NPIV function, denoted by P-ISMD and IS. The P-ISMD is a simple plug-in identity-weighted SMD estimator that was proposed in Ai and Chen (2007) (henceforth AC07). The IS is what we call “inefficient score” estimator that is based on sample analog of the asymptotic influence function of the P-ISMD estimator (derived in AC07).555Different inefficient estimators of the WAD can have different asymptotic influence functions and hence different asymptotic variances. That is why we define the IS estimator based on the asymptotic influence function of the P-ISMD estimator of AC07, so that they will have the same asymptotic variance. We note that both P-ISMD and IS are asymptotically efficient for a WAD of a nonparametric regression , in the absence of endogeneity. However, they are no longer efficient for the WAD of a NPIV function identified by the conditional moment restriction (for ).

We compare the finite sample performance of these efficient (OP-OSMD, ES) and inefficient (P-ISMD, IS) estimation procedures in four Monte Carlo designs with moderate sample sizes ( to ).666Since both score-based estimators ES and IS are based on orthogonal moments, we also provide comparison with their cross-fitted versions. The cross-fitting orthogonal moments estimators have become very popular following(Chernozhukov, Chetverikov, Demirer, Duflo, Hansen, Newey and Robins, 2018, 2021) and others, although no published work has applied cross-fit to efficient estimation of WAD in NPIV yet. In Monte Carlo design 1, we estimate a simple nonparametric regression and two-stage least squares data-generating process, as a useful baseline. In Monte Carlo designs 2 and 3, we estimate the average partial derivative of a NPIV function with respect to an endogenous variables using various ANN sieves and spline sieves. In Monte Carlo design 4, we calibrate a data-generating process to the gasoline empirical application (Blundell et al., 2012), and repeat the exercises for Monte Carlo designs 2 and 3.

Our Monte Carlo experiments allow for comparisons along several dimensions:

-

•

For ANN estimators, how much does ANN architecture (activation, depth, width) matter? How much do other tuning parameters matter?

-

•

Across types of estimation procedures, how do ANN SMD estimators compare to ANN score estimators, along with alternative procedures like adversarial GMM (Dikkala et al., 2020)?

-

•

Within a type of estimation procedure, do ANN estimators exhibit superior finite-sample performance compared to linear sieve (e.g., spline) estimators, when dimension of is moderately high?777To be clear, we are not speaking of “high dimension” in the sense.

The main, stylized takeaways from our Monte Carlo experiments are as follows:

-

•

Choices of hyperparameters in optimization—learning rate, stopping criterion—are delicate and can affect performance of ANN-based estimators. Nonconvex optimization could lead to unstable performances. However, certain values of the hyperparameters do result in good performance of ANN based estimators.

-

•

We do not empirically observe systematic differences in finite-sample performances as a function of ANN architecture, within the feedforward neural network family. In our experience, ANN architecture is not as important as tuning the optimization procedure.

-

•

Stable inferences are currently more difficult to achieve for ANN based estimators for models with nonparametric endogeneity.

-

•

ANN OP-OSMD and ANN IS have smaller biases than ANN P-ISMD for the average derivative parameter.

-

•

ANN ES and ANN cross-fitted ES are sensitive (in terms of bias) to the estimation of the optimal weighting in Riesz representer adjustment part. ANN OP-OSMD

-

•

Spline OP-OSMD , spline P-ISMD , spline IS and spline ES for the average derivative parameter are less biased, stable and accurate, and can outperform their ANN counterparts, even when the NPIV function depends on moderately high-dimensional continuous covariates (as high as thirteen in the simulation studies).

-

•

Generally, there seems to be gaps between intuitions suggested by approximation theory and current implementation.

Lastly, as applications to real data, we apply ANN sieve NPIV to estimate average price elasticity of a gasoline demand using the data set of Blundell, Horowitz and Parey (2012), and to estimate average derivatives of a price-quantity relation in differentiated product markets using the data set of Compiani (2019). Both applications involve nonparametric structure functions of multi-dimensional covariates (including endogenous price), and our ANN applications do not impose any semiparametric shape restrictions.

Related literature on ANN NPIVs.

We view various ANNs as examples of nonlinear sieves, which, compared to linear sieves, can have faster approximation error rates for large classes of nonlinear functions of high dimensional regressors. Once after the approximation error rate of a specific ANN sieve is established for a class of unknown functions,888Different ANN sieves have different approximation error rates for different function classes. See, for example, Barron (1993) and Chen and White (1999) for approximation errors rates for single hidden layer ANNs for Barron class; Yarotsky (2017), Shen et al. (2021b), Shen et al. (2021a) for approximation error rates of multi layer ReLU ANNs for typical smooth function class; Schmidt-Hieber (2019) for approximation error rates of deep layer ReLU ANNs for composition function classes. the asymptotic properties of estimation and inference based on the ANN sieve could be established by applying the general theory of sieve-based methods. The nonparametric convergence rates in Ai and Chen (2003, 2007) (henceforth, AC03, AC07) explicitly allow for nonlinear sieves such as ANNs to approximate and estimate the unknown structure functions of endogenous variables. They establish the root- asymptotic normality of regular functionals of nonparametric conditional moment restrictions with smooth residual functions. Due to the small sample size and computational limitation, earlier applications in econometrics have focused on single-hidden layer ANNs. For instance, Chen and Ludvigson (2009) applied single hidden layer sigmoid ANN SMD to estimate the unknown habit function in a semi-nonparametric asset pricing conditional moment model with a time series sample size of about 200 quarterly observations. To the best of our knowledge, Hartford, Lewis, Leyton-Brown and Taddy (2017) is the first paper to apply multi-layer (2 hidden layer) ANNs to estimate an NPIV structural function. Since then, numerous studies have followed up, see Dikkala, Lewis, Mackey and Syrgkanis (2020) and the references there in.999However, as documented in our simulation results, the WAD parameter estimated via plugging in the estimated via adversarial GMM (Dikkala et al., 2020) can be biased. This is not surprising since the tuning parameter choice for nonparametric estimation of may be different from that for the efficient estimation of the WAD. In a project that started after our first draft, Chen, Liao and Wang (2021b) established rate of convergence for multi-layer ANN optimally weighted SMD estimation of general nonparametric conditional moment restrictions for time series data, and proposed ANN sieve quasi-likelihood ratio inference for possibly slower-than-root- estimable linear functionals. However, they do not consider efficient estimation for root- estimable linear functionals of NPIV such as the WAD parameter, which is our parameter of interest.

Our simulation studies and empirical applications indicate that, although multi-layer ANNs can perform well after careful choice of tuning parameters, they have no clear advantage over single hidden layer ANNs or spline sieves for efficient estimation of WAD in a NPIV model when the unknown structure function is a relatively smooth function of multi-dimensional , which is likely the case in economic endogenous demand estimation. Just like the simulation paper by Lee et al. (1993) about the performance of single-hidden layer ANNs on testing nonlinear regression models, our paper documents that ANNs can also be one promising tool in efficient estimation and inference for causal

The rest of the paper is organized as follows. Section 2 introduces the model, and the two classes of efficient estimation procedures. Section 3 provides implementation details for all the estimators considered in the Monte Carlo studies. Section 4 contains three simulation studies and detailed Monte Carlo comparisons of various ANN and spline based estimators. Section 5 presents two empirical illustrations and Section 6 concludes.

2 Efficient Estimation Procedures for Average Derivatives in NPIV Models

We first present the model and recall the semiparametric efficiency bound characterization. We then present two classes of efficient estimation procedures.

We are interested in semiparametrically efficient estimation of the average partial derivative:

where is a known positive weight function, is the partial derivative w.r.t. the first argument and the unknown real-valued function is identified via a conditional moment restriction101010See, e.g., Newey and Powell (2003), Blundell et al. (2007), Andrews (2017) for identification of a NPIV model.

| (1) |

Previously, Ai and Chen (2007) (AC07) presented a root- consistent asymptotically normally distributed identity-weighted SMD estimator of , nonlinear sieves such as single hidden layer ANN sieve is allowed for in their sufficient conditions. AC12 presented the semiparametric efficiency bound of and an efficient estimator based on orthogonalized optimally weighted SMD (see their section 4.2).111111Ai and Chen (2012) derived the efficiency bound via the “orthogonalized residual” approach, which extends the earlier work of Chamberlain (1992) to allow for unknown functions entering a system of sequential moment restrictions. Severini and Tripathi (2013) presented efficiency bound calculation for average weighted derivatives of a NPIV model without assuming point identification of the NPIV function, but pointed out that the -asymptotically normal estimator of linear functionals of NPIV in Santos (2011) fails to achieve the efficiency bound. Chen, Pouzo and Powell (2019) proposed efficient estimation of weighted average derivatives of nonparametric quantile IV regression via penalized linear sieve GEL procedure, without providing any simulation results on how their procedure performs in finite samples.

Since weighted average treatment effects under confounding and endogenous continuous treatments can be regarded as an example of the WAD in a NPIV model, it is important to conduct some detailed Monte Carlo studies to compare finite-sample performance of various efficient estimators of when depends on multi-dimensional covariates . In this paper we present large scale simulation studies focusing on the performance of several estimators of when is approximated via various ANN sieves and is up to -dimensional vector of continuous covariates.

2.1 Efficient score and efficient variance for

In this section, we specialize the general efficiency bound result of AC12 to our setting. We rewrite our model using their notation. Denote the full parameter vector as . The model can be written as the following sequential moment restriction

| (2) | |||||

We define the orthogonalized residual as

which is the residual from a projection of on conditional on , where is the orthogonal projection coefficient:

Orthogonalizing the two moment conditions makes an efficiency analysis tractable—the same technique is used in, e.g., Chamberlain (1992).

We now specialize the results in AC12 to the plug-in model:

| (3) |

where is a scalar and is a real-valued function of , and . Define the following variances:

We recall the efficiency bound characterization for WAD of a NPIV model from AC12 (see their Example 3.3) for the sake of easy reference, and compute

| (4) |

where . Let be one solution (not necessarily unique) to the optimization problem (4). We note that such a solution always exists since the problem is convex, and we have:

| (5) |

Remark 2.1 (Characterization of Efficient Score).

Applying Theorem 2.3 of AC12, we have: the semiparametric efficient score for in (3) is given by

where is one solution to (4). And the semiparametric information bound for is .

(1) If , then cannot be estimated at the -rate.

(2) If , then the semiparametric efficient variance for is: .

In the rest of the paper we shall assume that and hence is a -estimable regular parameter. We note that by definition, the efficient score (indeed any moment condition proportion to an influence function) automatically satisfies the orthogonal moment condition.

2.2 Efficient influence function equation based procedure

From Remark 2.1, the semiparametric efficient influence function for takes the form

| (6) |

Denote

It is clear that is the unique solution to the efficient IF equation , that is

One efficient estimator, , for is simply based on the sample version of the efficient IF equation with plug-in consistent estimates of all the nuisance functions:

In this paper can be various ANN sieve minimum distance estimators (see below), but, for simplicity, the nuisance functions and are estimated by plug-in linear sieves estimators.

2.3 Optimally weighted SMD procedure

Another efficient estimator for can be found by optimally-weighted sieve minimum distance, where the population criterion is (see AC12):

| (7) |

The discrepancy measure is the optimally weighted quadratic distance of the expectation of the two moment conditions

from zero, where the optimal weight matrix is diagonal and proportional to the inverse variance of each moment condition:

Two remarks are in order. First, note that the optimal weight matrix is diagonal because and are uncorrelated by design. Second, since the optimal weight matrix is diagonal and is a free parameter, we can view the minimization as sequential:

This is important because solving the model sequentially while maintaining efficiency suggests a simple way to compute the estimators.

A sieve minimum distance estimator for may be constructed by (i) replacing expectations with sample means, (ii) replacing conditional expectations with projection onto linear sieve bases, (iii) replacing the optimal weight matrix with a consistent estimator, and (iv) replacing the infinite dimensional optimization with finite dimensional optimization over a sieve space for . This paper focuses on approximating by ANN sieves. In particular, a sample analogue of the above objective function is

where and are estimators of and respectively; see Sections 3 and 4 below for examples of different estimators. Let be a sieve parameter space for (e.g., in this paper we focus on various ANN sieves). We define the optimally weighted SMD estimator as an approximate solution to

This is an estimator proposed in AC12.

We may analyze the asymptotic properties of this estimator. Since we may view the optimally weighted SMD problem as either a minimum distance program or a sequential GMM estimator, we may carry out two separate analyses of the asymptotic properties. The analysis of the estimator as a minimum distance problem is a specialization of Ai and Chen (2007, 2012, 2003); Chen and Pouzo (2015), while Appendix B presents a heuristic review of the analysis as a sequential moment restriction, which specializes Chen and Liao (2015). Either approach will lead to the following asymptotic efficient influence function expansion:

| (8) |

Riesz Representer. Lastly, we need to characterize the Riesz representer . The argument in AC03 parametrizes as a “scale times direction” coordinate. For a fixed scale , the minimum norm property of Riesz representers implicitly defines the optimal direction as the following:

| (9) |

Solving the condition

by plugging in then yields

as the solutions for the representers where is defined in (9) above. If we assume completeness condition then as the unique solution to (4) or (5) and .

The consistency, root- asymptotic normality, consistent variance estimation can all be obtained by directly applying AC03, AC07 for single hidden layer ANN sieves. Chen, Liao and Wang (2021b) results can be applied for multi-layer ANN sieves.

3 Implementation of the estimators

In this section, we describe in broad strokes the implementation of the eventual estimators for the average derivative of a NPIV, which often involves estimation of nuisance parameters and functions. These nuisance parameters—which often take the form of known transformations of conditional means and variances—require further choice of estimation routines and tuning parameters, details of which are relegated to Section 4.2.

A note on notation.

Recall that we use to denote the outcome, to denote variables (endogenous or exogenous) that are included in the structural function, and to denote exogenous variables that are excluded from the structural function. Certain entries of and may be shared. Again, the NPIV model is:

| (10) |

Let collect the observable random variables (in the population). The parameter of interest is , where is the partial derivative of with respect to its first argument, evaluated at .

We also set up notation for objects related to the sample. Let there be a random sample of observations. We denote as vectors and matrices respectively of realized values of the random vector . We will slightly abuse notation and write , for a function , to be the -matrix of outputs obtained by applying row-wise, and similarly for expressions of the type .121212This notation conforms with how vector operations are broadcast in popular numerical software packages, such as Matlab and the Python scientific computing ecosystem (NumPy, SciPy, PyTorch, etc.). For a vector valued function , we let be the projection matrix onto the column space of .

Quick map of estimation procedures.

We provide a simple map that connects the above model and estimation approaches to the estimators we implement below.

-

1.

(Section 3.1) For SMD estimators [P-ISMD, OP-OSMD]: Solve sample and sieve version of (7)

-

2.

(Section 3.2) Score estimators [IS, ES]: Estimate the components of the influence functions as in (6). Set the influence functions to zero and solve for .

-

3.

(Section 3.3) Standard error for SMD estimators: Estimate the components of the influence functions as in (8), and take the sample variance.

Additionally, we describe the estimator when the analyst is willing to assume more semiparametric structure (e.g. partial linearity) on the structural function . We also conclude the section with a brief discussion of software implementation issues.

3.1 Sieve minimum distance (SMD) estimators

Consider a linear sieve basis for , where . In sample, let be the projection matrix projecting onto the column space of . For a sample of realizations of , let be the sample best mean square linear predictor (that approximates the conditional mean) of , since it returns the fitted values of a regression of on flexible functions of :

Under the NPIV restriction (10), taking and , we should expect

This motivates the analogue of the SMD criterion (7) in the sample, where we choose so as to minimize the size of the projected residual :

| (11) |

When the norm chosen is the usual Euclidean norm , we obtain the identity-weighted SMD estimator for , .

Given a preliminary estimator for , we may form an estimator of the residual conditional variance by forming the estimated residuals and then projecting onto , e.g. via the linear sieve basis or via other nonparametric regression techniques such as nearest neighbors. With such an estimator of the heteroskedasticity, we can form a weight matrix . Using the norm in (11) yields the optimally-weighted SMD estimator for , .

With an estimated of the structural function , we can form two plug-in estimators of . The first is the simple plug-in estimator:

See AC (2007) for the root- asymptotic normality of this estimator, and its asymptotic linear expansion is of the form:

where

| (12) |

The simple plug-in estimator does not take into account the covariance between the two moment conditions, and . The second estimator, the orthogonalized plug-in estimator, orthogonalizes the second moment against the first:

where is an estimator of the population projection coefficient of the second moment onto the first moment condition :

| (13) |

One choice of is to plug in sample counterparts—plugging in for , plugging in a preliminary (which could be the ) for , and plugging in an estimator for —and finally approximate via a linear sieve regression, say with the basis .

To summarize, the SMD estimator can be implemented as follows.

Identity Weighted SMD Estimator of

-

1.

Sieve for conditional expectation: Choose a sieve basis for : (more details on this later)

-

2.

Construct objective function

-

(a)

Obtain the sample least squares projection of onto

-

(b)

Optimizing : define

-

(a)

Optimal SMD Estimator of

-

1.

Same as Step (1) above

-

2.

Estimate weight function : with a preliminary estimator of (use identity-weighted one for instance), form an estimator by projecting on , the sieve basis for to obtain . Form .

-

3.

Optimizing : define .

Estimators for

-

1.

Simple plug-in estimator. Given an estimator of , use

-

2.

Orthogonalized plug-in estimator

-

(a)

Obtain an estimator of . One can use with being for example the simple plug in estimator and the above estimator of the variance of the first moment.

-

(b)

Obtain

-

(a)

Combining simple plug-in with identity-weighted SMD yields the estimation procedure that we term P-ISMD, and combining orthogonal plug-in with optimally weighted SMD yields the estimation procedure that we call OP-OSMD.

3.2 Influence function-based estimators

We also implement influence function based estimators. As we highlighted in the previous section, one influence function estimator for takes the following form

| (14) |

with defined below. Moreover, given an estimator for and for , we can form the influence function estimator:

Identity score estimator (IS)

One influence function, which corresponds to the influence function of the P-ISMD estimator has taking the following form. We refer to the resulting influence function estimator as IS, for identity score.

| (15) | ||||

| (16) | ||||

| (17) |

Efficient score estimator (ES)

On the other hand, the efficient influence function (ES) uses a different :

where is as in (13), and

| (18) | ||||

| (19) |

are the same as (9), which are also weighted analogues of the identity weighted , (17).

The above formulation writes as a function of ; alternatively, we may follow the strategy in Appendix B and estimate directly. One way to estimate the above representer and hence get a feasible score is as follows. Recall that the definition of is

Let be the basis approximating . Suppose we view that is well approximated by , and that is well approximated by projection onto a basis , then the above definition of yields a finite-dimensional problem that we may solve in closed form to obtain the following. Consider the following quantities

This then implies that . In sample, this amounts to

| (20) |

These can then be used to obtain and the influence function correction term

3.3 Inference for P-ISMD, OP-OSMD, IS, ES

We now discuss how to compute standard errors and confidence intervals—again in broad strokes—for the estimating algorithms P-ISMD, OP-OSMD, IS, and ES. In a nutshell, for the score estimators IS and ES, the estimator is a sample mean of estimated influence functions, and its sample variance is directly the properly normalized variance of the influence functions. As a result, under appropriate conditions, a sample variance of the estimated influence functions is consistent for the variance of the influence functions, leading to consistent estimation of standard errors. For the estimators IS and ES, practitioners can therefore compute the standard errors without adjusting for the estimation of the nuisance parameters.

Similarly, estimating the standard errors for the P-ISMD and OP-OSMD estimators amounts to estimating the variance of the influence function. One approach is to simply use the influence function estimates from IS and ES, and leverage the fact that (P-ISMD, IS) and (OP-OSMD, ES) are respectively asymptotically equivalent.

Another approach is to estimate the variance of the influence functions directly, without necessarily estimating the influence functions themselves. The details are stated in Section 2, and we may turn the theory into estimators by “putting hats on parameters”: replacing unknown functions with their finite-dimensional sieve approximations, conditional expectation with sieve projections, and expectations and variance with their sample counterparts. For convenience, we reproduce the calculation here:

- 1.

-

2.

OP-OSMD: The inverse of the asymptotic variance is

which corresponds to the objective function in (9)

A third approach, which in our experience seems more accurate than analytic standard errors, is a multiplier bootstrap for the SMD estimators. The bootstrap simply replaces the residual in (11) with the weighted residuals where are such that , independently of data, for some positively supported distribution with unit mean and variance (e.g. the standard Exponential distribution). Given a realization of the bootstrap weights , the estimation routines P-ISMD and OP-OSMD would yield an estimate for . Repeating this procedure a large number of times would generate a large number of bootstrapped estimates, whose percentiles form confidence interval boundaries.

3.4 Partially linear or partially additive SMD estimators

Assume is partially linear in its first argument, or, additionally, partially additive in subsets of its arguments. Since is linear in its first argument, the slope on that argument is the average derivative . Therefore, under such a restriction, can be identified with the pair where is some nuisance parameter governing the rest of the function.

3.5 Implementation of neural networks

We now provide a brief recipe on working with neural networks. A feedforward neural network is a composition of layers of the form131313For instance, a ReLU layer is a function of the form for a conformable matrix and a conformable vector.

for some conformable matrix , vector , and nonlinear activation function :, i.e. a -hidden-layer neural network has the representation

where we collect the learnable parameters as . The gradient can be computed efficiently using the celebrated backpropagation algorithm, and, as a result, in practice, neural networks are often optimized via first-order methods such as (stochastic) gradient descent or its variants, such as the popular Adam algorithm (Kingma and Ba, 2014) in the machine learning community. Optimization with neural networks is easiest with an unconstrained, differentiable objective, for which numerous computational frameworks exist. We use PyTorch (Paszke et al., 2017) in this paper.141414See https://pytorch.org/ In particular, (11) is an unconstrained, differentiable objective function, and we may optimize over since the overall gradient may be decomposed into components that are efficiently computed: By the chain rule,

where denote the objective function (11).

Compared to conventional numerical linear algebra packages such as NumPy or MATLAB, PyTorch offers two computational advantages particularly suited for deep learning: automatic differentiation and GPU integration. PyTorch tracks the history of computation steps taken to produce a certain output, and automatically computes analytic gradients of the output with respect to its inputs (See LABEL:lst:torch for an example). Autodifferentiation allows gradient descent methods to be carried out conveniently, without the user supplying analytical or numerical gradient calculations manually.

PyTorch also allows arithmetic operations to be computed on GPUs, which have computing architecture that allows for large-scale parallelization of simple operations. For instance, multiplying two matrices is of order with a naive algorithm, which can be viewed as dot products of size ; GPUs allow for parallelized computing of the dot product operations, in contrast to CPUs, where the level of parallelism is determined by the number of CPU cores. For optimization, we use the Adam algorithm (Kingma and Ba, 2014), which is an enhancement of basic gradient descent by estimating higher order gradients.

3.6 Why linear sieves for certain nuisance parameters

linearsieves We note that even in our ANN implementation, a few nuisance functions are estimated with linear sieves. For instance, the instrument projection, the conditional covariance function , and in (17) are all approximated by linear sieves. It should be in principle possible to use nonlinear sieves, including neural networks, for all of them, and we consider that to be important open work. Here, we detail computational and conceptual difficulties that we have encountered.

First, many nuisance functions take the form of a conditional expectation , for some known or unknown function . This is the case, for instance, with in (13), as well as the conditional variance . In such cases, we can in principle use neural networks to minimize the empirical squared error loss

and use as an estimate. At least computationally, such a procedure makes sense, though its theoretical properties may be delicate. In this work, we avoided using neural networks for and for computational convenience.

Replacing the instrument projection with neural networks is considerably more challenging for sieve minimum distance. In this case, we are not approximating a function, so much as approximating an operator that projects onto . For a given estimate with estimated structural residuals , it is not difficult to project it onto and obtain the estimated projected residuals (by minimizing squared error empirical risk), as well as its squared sample mean . However, it becomes challenging to update the neural network weights on . Since the neural network is trained based on , its weights depend on the weights of in a complex fashion, and the gradient of with respect to ’s weights become computationally intractable. As a result, we could not easily devise a scheme that replaces the instrument projection with nonlinear sieves. Recently, Dikkala et al. (2020) do propose a different method that allows for using nonlinear sieves for the instruments. The performance of this method is compared later in Figure 5.

Lastly, there are nuisance parameters which are defined through an optimization problem that includes its gradient with respect to its input. The nuisance parameters in the Riesz representer display this property, for instancec in (17). To approximate such a parameter, e.g. , with neural networks, we would minimize some criterion function that includes both and . To use current off-the-shelf gradient-based training procedures, we would then require the gradient of with respect to the ’s neural network weights, as well as that of . The former is a niche use-case in deep learning, and so is not well-supported by the autodifferentiation methods in PyTorch.

4 Monte Carlo Studies

We present four Monte Carlo designs in the first subsection. We then describe exactly how we estimated the various components that are needed for the estimators in the next subsection. The last subsection discusses some Monte Carlo results.

4.1 Design Descriptions

We consider a set of Monte Carlo experiments that combine simple but relevant designs that include high dimensional regressors. These designs are also relevant to the kinds of empirical models that are of interests to economists. We describe the four Monte Carlo designs below. A preponderance of our empirical results are based on Monte Carlo design 2.

Monte Carlo design 1.

We thank an anonymous referee for suggesting these designs.151515These designs replace Monte Carlo 1 in an older version of the draft, which is in turn relegated to Appendix A, now as Monte Carlo design 5. Part (a) of this design investigates performance of nonparametric regression (i.e. NPIV with the endogenous variable equalling the instrument), as we vary the noise level. Part (b) of this design investigates a simple NPIV design. Both designs feature neural networks as part of the data-generating process, and as a result serve as optimistic benchmarks.

(a) \CopycondexpConsider the data-generating process

where

is a feed forward neural network with one hidden layer and 40 neurons. We consider estimating for different levels, calibrated to the variance of signal . The variance of the error is some multiple of the variance of .161616 is approximately 14 in our particular randomly generated . We investigate four values of this multiple: 0, 0.1, 1, 10, corresponding to no noise, moderate noise, high noise, and very high noise.

(b) \Copymcsimple We generate i.i.d. standard Gaussians , where and . Let . We generate an endogenous treatment

for some fixed conformable coefficients . Here has 4 rows, and acts coordinate-wise. In other words, the endogenous is a one-layer -network as a function of .

Let be a normal correlated with , and let

be the second stage, for some fixed coefficients . The coefficient of interest is on , with its true value being . To connect with the notation in the previous sections, let and .

Monte Carlo design 2.

The second Monte Carlo DGP is the following, which is an augmentation of the design in Chen and Qiu (2016).

where

The process generating is somewhat complex. First, we generate a covariance matrix , normalized to unit diagonals, where ’s entries are i.i.d. standard Normal. The seed generating the covariance matrix is held fixed over different samples, and so should be viewed as fixed a priori. Next, let denote a correlation level and we let

| (21) |

where is the standard Normal CDF, and and addition are applied elementwise. In the exercises reported, we use for correlation levels. In the high dimensional design, we set the dimension of to be 10 and so the model will have 13 continuous regressors.

Note that this design allows for correlation among regressors both endogenous and exogenous. It also allows for heteroskedasticity and possibly large dimensions by increasing the dimension of . We have also tried different conditional variance of , the simulation results are similar. To connect with the notation in the previous sections, let and . The parameter of interest is .

Monte Carlo design 3.

We modify Monte Carlo design 2 with two changes that allows for some nonlinearity of in . In particular:

(a) enters through . The parameter of interest is .

(b) enters through , where

and , , and . The parameter of interest is

Additionally, we provide a Monte Carlo calibrated to the empirical application in Section 5.1.

Monte Carlo design 4.

calibrated Like Section 5.1, we use 4,812 observations in the full sample as in Chen and Christensen (2018), taken from the 2001 National Household Travel Survey in Blundell et al. (2012). Each observation contains measurements of an outcome variable (log quantity of gasoline), an endogenous treatment variable (log price of gasoline), covariates (log income, log household size, log number of drivers in a household, log household age, total workers in household, and an indicator for public transit), and a price instrument (distance to the Gulf of Mexico).

From a simple linear IV specification,171717Regress on and log income, instrumenting for with . we estimate that the price elasticity of gasoline demand is , and we create simulated data where is the ground truth. We do so by estimating the first stage relationship as well as the relationship of the outcome and the covariates nonparametrically, and build a simulation from these estimated quantities.

-

1.

Estimate with a single hidden layer (15 neurons) sigmoid network. Estimate with the same network architecture. To economize notation, we use to denote the estimated network rather than .

-

2.

Draw (with replacement) from the empirical distribution of the data and form . For each variable in , we add Gaussian noise equal to 10% of the standard deviation of the variable , in order to smooth the distribution of . We use notation to denote the noised-up variables.

-

3.

Let and denote the residuals for .

-

4.

Let and be the predicted price and residualized quantity from the noised-up synthetic data

-

5.

Let , be the simulated price variable

-

6.

Let denote the sigmoid function. Let

where

The sample average derivative of in is exactly . As the structural function of quantity in price (demand curve), it displays heterogeneous price elasticities (in ) and nonlinearity in . Generally speaking, the parameters chosen ensure that the derivative of is negative.

-

7.

Let

be the structural residual in the outcome, which is by design correlated with the structural residual in the price DGP ().

-

8.

Lastly, let .

The synthetic data is . To redraw the data, are redrawn, while are kept fixed.

Next, we provide a step by step guidance on how to implement the estimators.

4.2 Implementation details

We explain here the exact choices of estimators that we used for these Monte Carlo designs. A detailed overview is presented in Table 5. Various ANN SMD estimators for have additional tuning parameters regarding nonlinear optimization, which are described in Table 1.

Below, we describe the procedures underlying Figure 2, which are representative of the procedures in Figures 1, 3 and 4. We also describe the procedures for Figures 5 and 6, which are in turn representative of the procedures in Figures 7, 8, 7 and 9.

| Monte Carlo | Learning rate | # steps |

|---|---|---|

| 1(b) | 0.01 | 6000–10000 |

| 2 | 0.01 | 3000–5000 |

| 3(a) | 0.01 | 7000–10000 |

| 3(b) | 0.01 | 7000–10000 |

| 4 | 0.005 | 6000–10000 |

| 5 | 0.001 | 1500–2000 |

-

1.

Figure 2 reports Monte Carlo means and standard deviations for the design in Monte Carlo design 2, using ANN SMD estimators under a variety of model specifications on true .

In particular, we make the following choices for estimation of various nuisance parameters.

-

(a)

Identity-weighted SMD with simple plug-in: defined in Section 3.1. We specify choices of the linear sieve basis for instruments

-

i.

, where follows the basis choice made in Chen (2007) (p.5581–5582),181818i.e. , where . and contains second-order polynomials for and interactions .

-

i.

-

(b)

Optimally-weighted SMD with orthogonalized plug-in: defined in Section 3.1. We specify estimation details for the nuisance functions :

-

i.

: Form the squared residuals from the identity-weighted estimator and estimate by -nearest neighbors.

-

ii.

: Given an estimate , it suffices to estimate

Form and project it on : i.e. .

-

i.

For Figure 2,

-

(a)

The first column of Figure 2 reports results where the ANN SMD estimators are computed assuming is fully nonparametric.

-

(b)

The second column of Figure 2 follows Section 3.4 in that we assume a partially linear structure on , which is of the form .

-

(c)

The third and the fourth columns of Figure 2 follow Section 3.4 in that we maintain the partially additive structure on , which is of the form , where the unknown is approximated via ANNs. We use ANN sieves to approximate the scalar functions in the 3rd column, whereas the fourth column uses spline sieves to approximate .

-

(a)

-

2.

Figures 5 and 6 reports Monte Carlo means and standard deviations for a wide class of estimators (not limited to ANN SMD) for Monte Carlo design 2.

- (a)

-

(b)

Spline SMD:

-

i.

\Copy

tensorLet be a spline basis for the instrument space of , and let be a spline basis for the structural function . Both and are of the forms where each entry expands into a basis,191919This notation is for a spline with 2 knots, where, between adjacent knots, the spline function is a polynomial of order . and pairwise interactions (of the form , but we do not include more complex interactions ) are included in lieu of tensor product splines. The choice of order for is 1 more than that for .

-

ii.

Given , we estimate P-ISMD, OP-OSMD as in Item 1, where we optimize over candidate structural functions of the form , and estimate and by least squares projections onto the instrument sieve .

-

i.

-

(c)

Score/influence function estimators: Let be the spline bases used for the spline SMD in Item 2(b).

-

i.

IS:

- A.

-

B.

\Copy

wstar can be computed by solving (17). To do so, we approximate with for some coefficients , and the operator with . Doing so makes (17) a least-squares problem in the unknown coefficients . In fact, the closed form solution is

where takes the partial derivative entry-wise. Therefore is the estimator for , and this gives an estimator for by plugging in.

-

C.

Given , we estimate with .

-

D.

Plug and to the inefficient influence function and compute .

- ii.

-

i.

-

(d)

AGMM: First we apply Dikkala et al. (2020)’s code to estimate structural function by . Then compute the simple plug-in defined in Section 3.1.

4.3 Monte Carlo Results

Due to the length of the paper, we report representative simulation results in a sequence of figures and tables below.202020\CopytimeAs a note on computational difficulty, for a single run in estimating OP-OSMD on a sample size of 5000 on a Mac Mini (2020, Apple M1, 8GB RAM), the neural network procedures takes about 33 seconds for Monte Carlo design 2. Spline estimation usually takes about a second, as it is equivalent to solving linear IV problems in closed form.

4.3.1 Performance of point estimates in terms of (Monte Carlo) bias and variance

condexpresultsFor Monte Carlo design 1(a), we compare the performance of a ReLU network (one hidden layer, 40 neurons) with the performance of a spline basis in Table 2.212121Like the spline basis we use in other designs, it is a two-knot cubic spline for each variable with pairwise variable interactions of the form . The performance metric we choose is the scaled integrated MSE:

on 1000 out-of-sample data points. indicates perfect estimation of , and indicates estimation quality on par with using a constant prediction. We find that for low and moderate noise, neural networks perform better than splines, presumably since it captures more complex interaction patterns in . In the high noise regime, neural network underperforms, as neural networks overfit. In the very-high-noise regime, both estimators overfit and are in fact worse than simply using a constant. We caution that these performance of neural networks results from very minimal tuning, in particular, without validation samples. \CopymcsimplediscNext, for Monte Carlo design 1(b), we show the results in Figure 1 for P-ISMD estimators, varying over the dimension . We see that, despite the DGP involving a neural network, using neural network estimators only attains a modest improvement over spline estimators, in terms of slightly lower bias, consistent with our findings in the main text.

| Noise-to-signal ratio | Spline | Neural net |

|---|---|---|

| 0.0 | 0.60 | 0.91 |

| 0.1 | 0.58 | 0.80 |

| 1.0 | 0.48 | 0.30 |

| 10.0 | -0.55 | -2.55 |

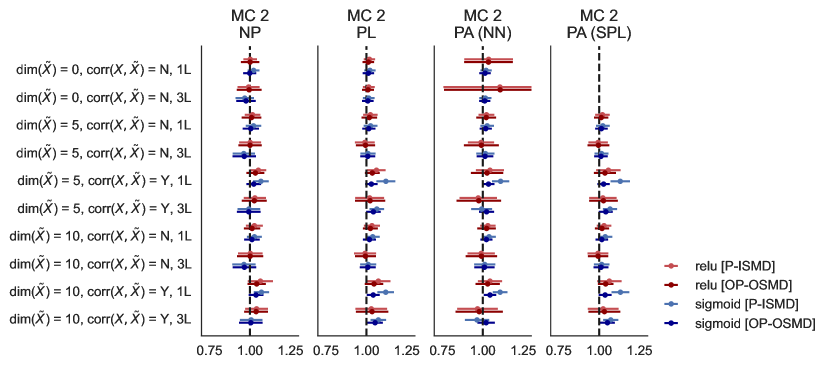

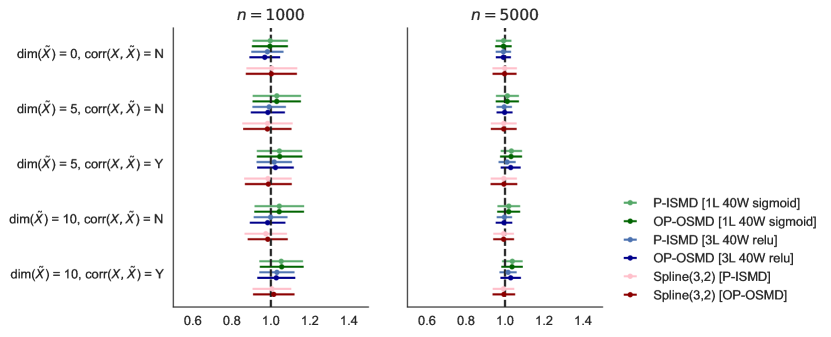

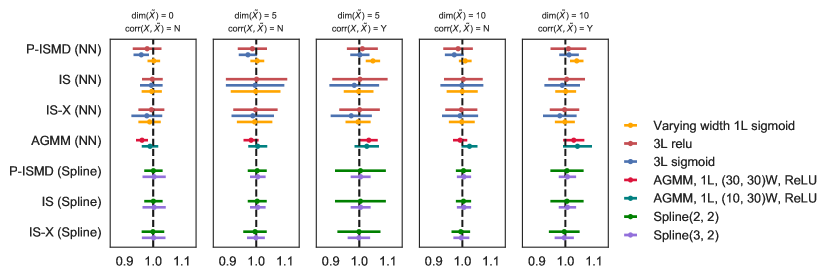

The rest of the figures correspond to more difficult Monte Carlo designs 2, 3 and 4 where the first element of is endogenous (). Figure 2 reports the performance of various ANN SMD estimators for in Monte Carlo design 2. The top display plots the results for and the bottom for . Note here that the columns correspond to various assumptions we maintain on what the econometrician knows about the true structure of in the model The true design is partially additive, and the first column, NP, assumes that the econometrician has no knowledge of the true structure. As we can see, across all implementations (the rows), most of the ANN SMD estimators perform well, which indicates that ANNs seem able to adapt to the unknown structure of . The second column labeled PL (for partially linear) assumes that is partially linear (i.e., ) while the third column labeled PA assumes the correct additive structure (i.e., ) in the Monte Carlo design is known to the econometrician (but the functions within it are of course not known). PA column corresponds to the case where we use ANN sieves to learn all the unknown functions although are functions of scalar random variable. Its performance slightly deteriorates as compared to the NP and PL columns. Notice here that for comparison, the last column for the PA case uses splines to approximate the two scalar valued unknown functions and while is always estimated via ANN (since it is of higher dimensions (at least when ). We see that the spline results are in line with the PL and NP results, and are adequate here.

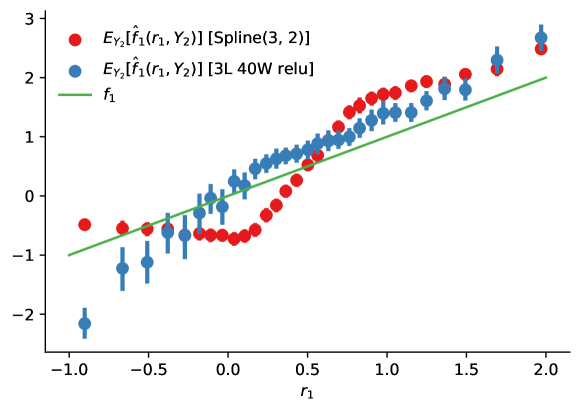

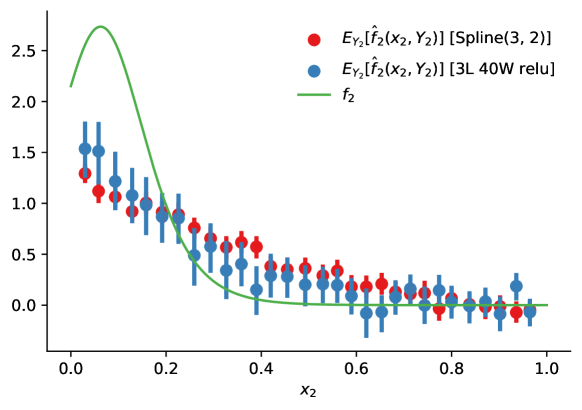

In Figure 3, we report results for the various estimators for Monte Carlo design 3, where the unknown function is now nonlinear in the endogenous (the first element of ). In the top panel (a), we report results for the case with and panel (b) reports results for the case where the unknown function is , where now the derivative depends on the regressor nonlinearly (as the function is highly nonlinear). Both results are for For panel (a) we see that the spline estimator remain well behaved across all designs (across rows), the single-hidden layer (1L) sigmoid ANN estimators remain adequate while both versions of the AGMM estimators (Dikkala et al., 2020) exhibit some bias. In panel (b), spline remains well behaved and so are the ANN estimators. In Figure 4 we show estimates of the partial derivative evaluated at various fixed values for some regressors. Though the estimators do not track the function well, especially in the tails in the bottom display, the average derivative is estimated well. Interestingly, 3L relu ANN222222This fact seems to be robust to architectural choices. seems to estimate the derivative function marginally better than splines, perhaps since ANNs are able to automatically generate rich interaction behavior, whereas specifying tensor products for spline sieves is somewhat onerous.

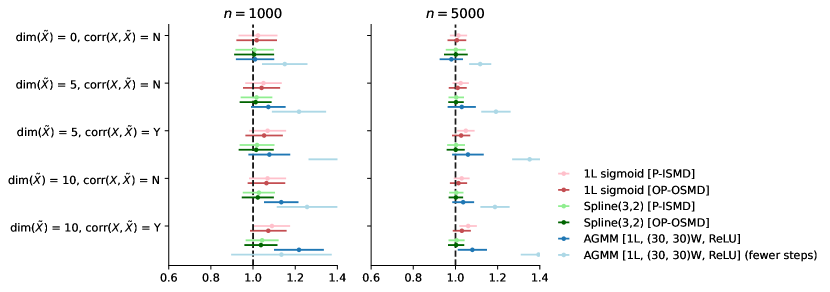

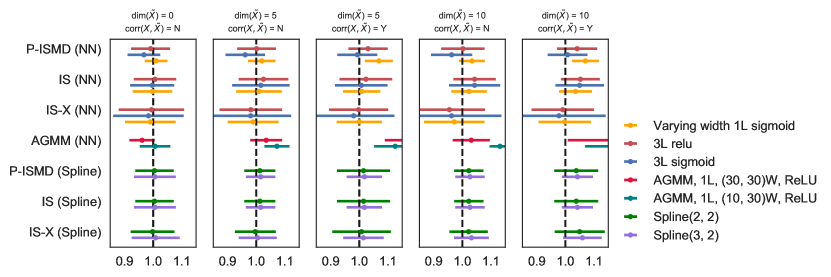

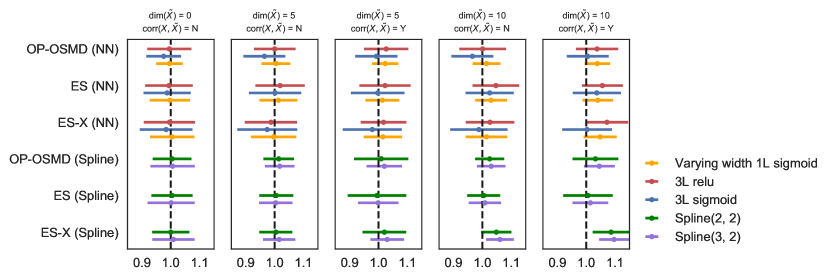

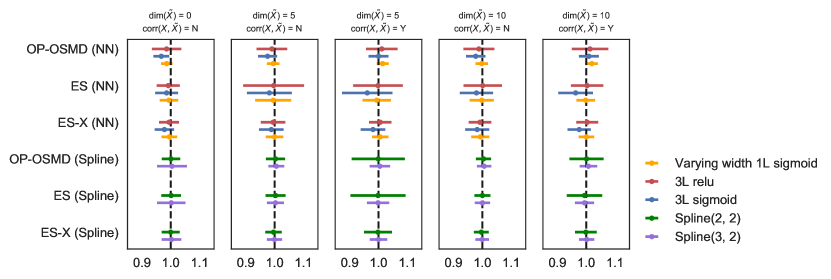

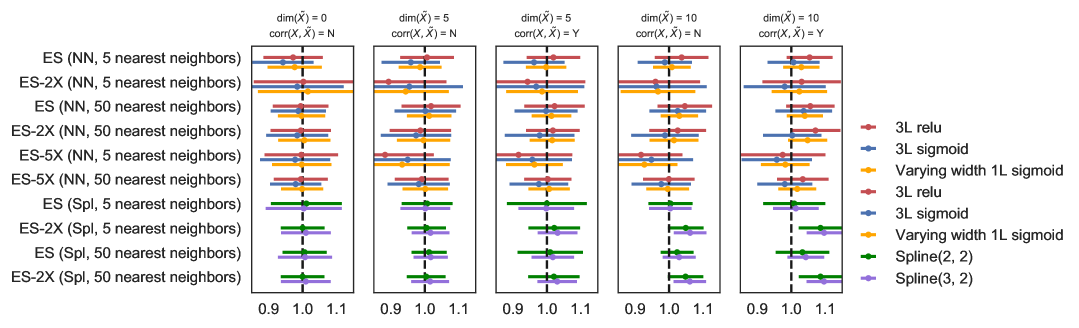

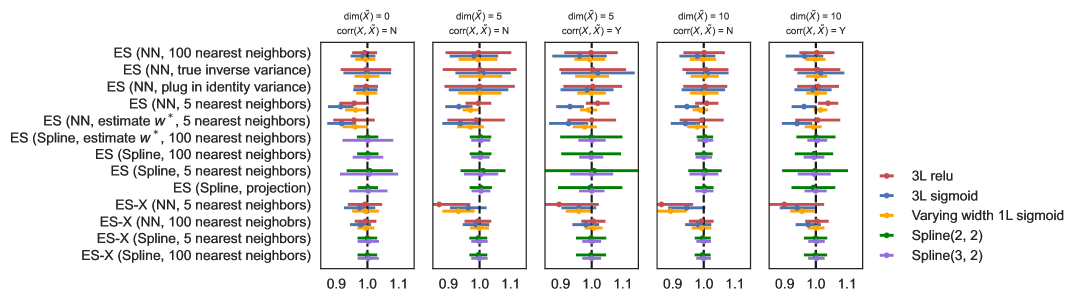

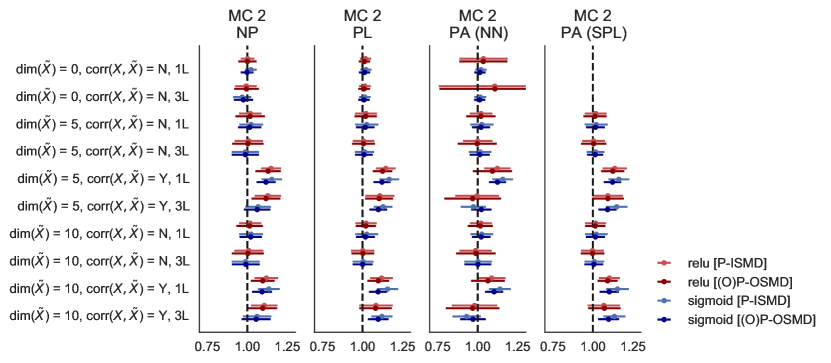

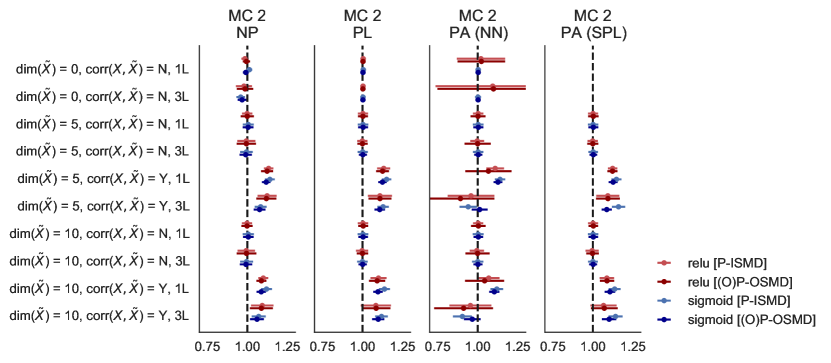

We now examine various implementation choices for Monte Carlo design 2. In Figures 5 and 6, we compare various implementations of ANN estimators and spline estimators in Monte Carlo design 2. In Figure 5, we compare identity-weighted estimators (IS, P-ISMD, AGMM, IS-X). Note that P-ISMD and OP-OSMD are the plug in and optimal plug in SMD estimators. In Figure 6, we compare optimally-weighted estimators that are semiparametrically efficient under suitable regularity conditions (ES, OP-OSMD, ES-X).232323As a reminder, we consider the following estimators: IS or identity weighted score estimator, ES or the efficient score estimator, while IS-X and ES-X are score estimators with two-fold cross fitting. It is important at the outset to keep in mind that all ANN implementations require some non-negligible tuning as the optimization problem is non-convex and the problem itself with endogeneity, correlation among the regressors, and high dimensions is not easy to tune. Also, currently and for NPIV models, there is no theory for data driven approaches to picking width, depth, or activation functions and finite sample behavior in our design varied (For linear splines, there are data-driven choice of sieve terms, see Chen, Christensen and Kankanala, 2021a).242424although we have not implemented any data-driven choice of spline sieve terms in our paper. The results across various combinations of and correlations for indicate first that ANN OP-OSMD and especially spline estimators seem to behave best. In particular, spline estimators require little tuning and are more stable than all ANN based estimators we use. The SMD ANN estimators are adequate with slight bias for the single-layer, varying-width case. IS and ES ANN estimators are generally less biased and slightly higher variance than P-ISMD and OP-OSMD ANN estimators, but we note that good performance of ES (in the ANN case) is very sensitive to the choice of in the “optimally-weighted” Riesz representer estimation. Figures 7 and 8 compare the performances of ES in a variety of choices for . It is interesting that the poor choice of leads to biased estimation of ES and its cross-fitted versions.

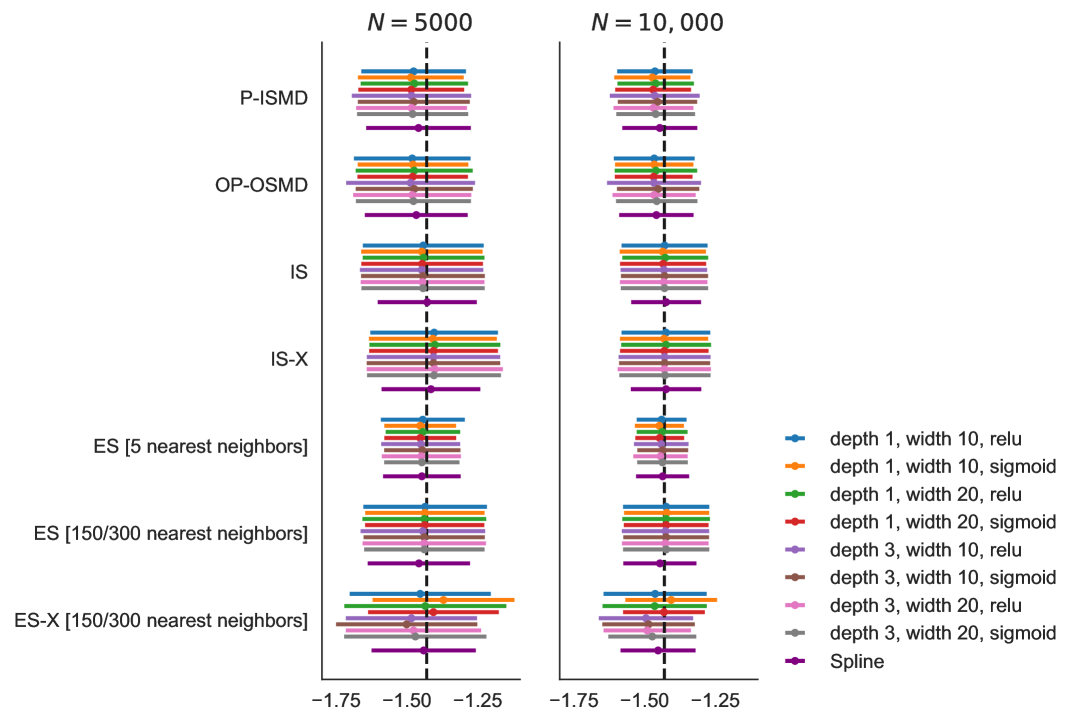

calibrateddiscLastly, Figure 9 examines various estimators on the empirical calibration Monte Carlo design 4. Consistent with the findings in other Monte Carlo settings, we generally find that all estimators perform adequately, with similar performance across a variety of neural architectures. We also continue to find that SMD estimators P-ISMD , OP-OSMD have slightly better mean-squared error performance than the score-based estimators in exchange for slightly higher bias. The one exception is ES with variance estimation with only five nearest neighbors, which performs best across the specifications. We conjecture that this is due to how we constructed the residuals in Monte Carlo design 4. In particular, we multiply standard Gaussians with estimated residuals , which may result in a conditional variance function that is highly non-smooth, and, as a result, a low number of nearest neighbor estimates performs well. In any case, the performance of ES and ES-X continues to show that it is sensitive to , as is shown in Figures 7 and 8.

See Appendix A for additional Monte Carlo results.

4.3.2 Performance of inference statistics

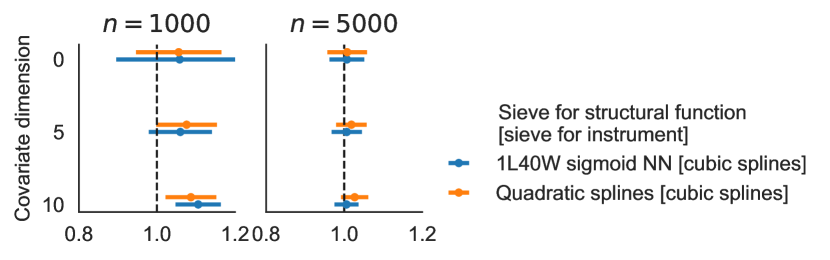

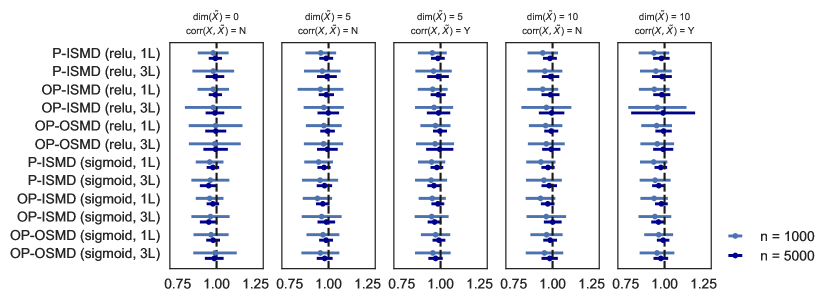

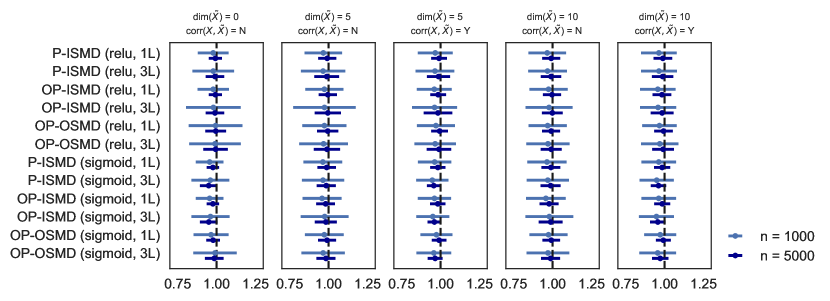

Tables 6 and 7 provides various inference statistics for the ANN SMD estimators P-ISMD and OP-OSMD for Monte Carlo design 2, without assuming any semiparametric structure on beyond smoothness. In particular, we report bootstrapped confidence intervals for ReLU and sigmoid and for depths 1 and 3 when the dimension of the nuisance variables ranges from 0 to 10. The results are also given for sample sizes and Across all specifications, the two ANN estimators perform adequately.

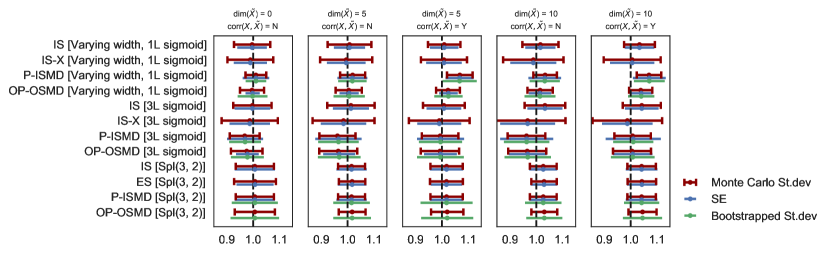

In Figure 10, we examine various standard error approaches for a set of estimators in Monte Carlo design 2. For each of these, we compute the MC standard deviation, a feasible estimator based on the estimator variance derived from theory, and a bootstrapped standard error. Overall, the theory and bootstrapped standard errors are adequate. In unreported results, criterion (SMD) based bootstrap confidence intervals showed reasonable coverage performance.

4.3.3 Overall simulation findings

Overall, it seems that ANN methods are useful in approximating potentially high dimensional functions in NPIV models. Also, in the class of models we investigated, choices of layers, widths or activation functions are not very consequential in terms of finite sample performance. On the other hand, ANN based estimators in these non-standard NPIV models are hard to tune, and a researcher needs to choose many smoothing parameters. These ANN estimators are also unstable in some runs as they are based on highly complex (and non-convex) optimization programs. In addition, ANNs are not as effective in estimating univariate functions. Finally, to our surprise, We find that various plug-in spline SMD estimators appear stable, less biased generally and can outperform ANNs for NPIV models even in high dimensional cases with 13 continuous regressors.

5 Empirical Illustrations

We present two empirical applications of estimating average derivatives with respect to endogenous price of a nonparametric demand for some non-durable goods. We apply ANN sieves to approximate nonparametrically when its argument consists of 7 covariates (for gasoline demand) and 6 covariates (for strawberry demand). In the existing literature researchers have used both data sets to estimate unknown in the model by assuming takes some parametric or semiparametric (such as partially linear) form to avoid the “curse of dimensionality” of . Although served as illustrations, our applications below are the first to estimate the endogenous demand function fully nonparametrically when .

5.1 Gasoline demand

We use data on gasoline demand from the 2001 National Household Travel Survey (Blundell, Horowitz and Parey, 2012). The sample we use include 4,812 observations in the full sample as in Chen and Christensen (2018). We estimate an NPIV analogue of the model (11) in Blundell, Horowitz and Parey (2012), where is the log gasoline demand, and is a vector of 7 random variables consisting of the log gasoline price (possibly endogenous) and the other included covariates following Column (3) in Table 2 of Blundell, Horowitz and Parey (2012). The instrument is the distance from the Gulf coast. We define the estimand as the average price derivative of the unknown structural function , which has an average elasticity interpretation. blundell2012measuring via OLS, and

| P-ISMD | OP-OSMD | IS | |

| Sigmoid [1L] | -1.28 | -1.24 | -1.12 |

| [-1.69, -0.9] | [-1.64, -0.87] | (0.22) | |

| Sigmoid [3L] | -1.24 | -1.28 | -1.11 |

| [-1.65, -0.9] | [-1.64, -0.87] | (0.22) | |

| ReLU [3L] | -1.27 | -1.25 | -1.14 |

| [-1.65, -0.9] | [-1.64, -0.87] | (0.22) | |

| Spline(3, 2) | -1.17 | -1.2 | |

| [-1.57, -0.8] | [-1.6,-0.8] | ||

| Blundell et al. (2012) OLS | OLS | TSLS | |

| -0.83 | -0.85 | -1.24 | |

| (0.148) | (0.15) | (0.2) |

Notes.

The 7 included covariates () are: log gasoline price, log income, household size, driver, household age, number working, public transit distance. We instrument gasoline price with distance to Gulf of Mexico. ∎

Table 3 shows our estimates for the average price elasticity (and bootstrapped confidence intervals). Broadly speaking, these estimates point to a similar range of values and are similar to a parametric two-stage least-squares specification. Across estimator classes, the ANN SMD estimates are slightly larger in magnitude than the spline SMD estimates and the ANN IS estimates. Within the ANN SMD estimator class, architecture choices of the networks do not appear to matter much for the result.

5.2 Strawberry demand

Non-organic

| IS | P-ISMD | OP-OSMD | |

|---|---|---|---|

| Sigm [1L] | -1.649 | -1.530 | -1.747 |

| (0.04) | (0.04) | (0.03) | |

| [-1.8, -1.7] | [-2.3, -1.8] | ||

| Relu [1L] | -1.648 | -1.590 | -1.706 |

| (0.04) | (0.04) | (0.04) | |

| [-1.9, -1.7] | [-2.3, -1.8] | ||

| Relu [3L] | -1.648 | -1.634 | -1.659 |

| (0.04) | (0.04) | (0.06) | |

| [-1.9, -1.55] | [-2.2, -1.5] | ||

| Spline(3,2) | -1.611 | -1.648 | -1.676 |

| (0.04) | (0.04) | (0.04) |

Organic

| IS | P-ISMD | OP-OSMD | |

|---|---|---|---|

| Sigm [1L] | -3.235 | -2.409 | -3.382 |

| (0.07) | (0.09) | (0.06) | |

| [-2.7, -2.44] | [-4.3, -3.5] | ||

| Relu [1L] | -3.236 | -2.197 | -2.129 |

| (0.07) | (0.06) | (0.08) | |

| [-2.4, -2.11] | [-2.4, -2.06] | ||

| Relu [3L] | -3.232 | -2.206 | -2.122 |

| (0.07) | (0.07) | (0.14) | |

| [-3.1, -2.08] | [-2.36, -2.06] | ||

| Spline(3,2) | -3.194 | -3.232 | -3.124 |

| (0.06) | (0.07) | (0.06) |

Notes.

The 6 included covariates () are: strawberry prices (non-organic, organic), income, lettuce demand (taste for organic proxy), state-level sale of non-strawberry fresh fruits, average outside good price. The excluded instruments are 3 Hausman IV (prices in neighbouring markets)+ 2 strawberry spot prices (marginal cost measures). A market is defined at the store-week level and there are markets. ∎

We also consider a setting where consumers choose two substitutable goods. We use the Nielsen dataset from Compiani (2019),252525Our results do not necessarily represent the views of the Nielsen Company. where consumers in California choose from strawberries, organic strawberries, and an outside option.262626For a detailed description of the data, see Appendix G of https://www.tse-fr.eu/sites/default/files/TSE/documents/sem2019/eee/compiani.pdf. We observe the market share of each type of product, their prices, and a variety of covariates at the market (store-week) level. In the analysis, we consider NPIV model where is the log market share of a type of good (non-organic or organic strawberries) and is a vector of 6 random variables, including endogenous prices for both types of strawberries and the outside good, and other market-level covariates. The instruments include Hausman instruments as well as cost shifters such as measurements of consumer taste and income at the market level. We focus on the target parameter , which is the average derivative of with respect to the own-price in logs, which we interpret as a version of price elasticity.272727Under a model of the demand where the NPIV condition defines the demand function , we can understand as a price elasticity. However, this model—which implicitly assumes that endogeneity is additive—may not be consistent with microfoundations of consumer behavior (Berry and Haile, 2016), and so care should be taken in interpreting as an elasticity. Nevertheless, for purposes of our illustration here, we may continue to view as some well-defined function of the distribution of the data. For a more detailed implementation of demand in this setting, see Compiani (2019) where in principle one can also use the neural networks based implementation in this paper in a natural way.

We present the results in Table 4. As is perhaps expected from a casual intuition, estimates of are negative across both products, and more negative for the more price-sensitive product (organic strawberry). Moreover, results are broadly similar across estimation methods (SMD vs. score) and sieve choices (spline vs. neural net), with perhaps more variability for neural networks in organic strawberries. The estimates for non-organic strawberries hover around , and are reasonably stable across choices of tuning parameters and estimators (IS vs. SMD estimators). The estimates for organic strawberries are more variable across specification of nuisance parameters and neural architectures, but seem to be around and , and larger in magnitude than the own-price elasticity estimate for non-organic strawberries.

These estimates are qualitatively similar to Compiani (2019)’s estimates, which reports median own-price elasticities of (0.03) for non-organic strawberries and (0.7) for organic strawberries.282828Interestingly, our estimates are closer to estimates from BLP that Compiani (2019) reports in Figure 4, which are also around -2 to -3. Our estimates are more dissimilar for organic strawberries, for which we offer a few conjectures. First, Compiani (2019) reports estimates following Berry and Haile (2016)’s approach to demand estimation, that accounts for price endogeneity differently. Under his assumptions, it is possible that our estimator is consistent for a different parameter than his. Second, organic strawberry market shares are very small, and hence fluctuates more on a log scale, thereby resulting in worse estimation precision.

6 Conclusion

conc In this paper, we present two classes of semiparametric efficient estimators for weighted average derivatives (WADs) of nonparametric instrumental variables regressions (NPIV) of moderate and high dimensional endogenous and exogenous regressors. We have conducted detailed Monte Carlo comparisons of finite sample performance of various inefficient and efficient estimators of the WADs using various ANN sieves. The simulation studies and empirical applications confirm the theoretical advantage of ANN approximation of unknown continuous functions of moderately high-dimensional variables, after some tuning of hyper-parameters. Perhaps the most practical findings from our large amount of reported and unreported simulation studies using moderate sample sizes are as follows: the ANN efficient SMD estimators have smaller biases than those of the ANN inefficient SMD estimators, and are less sensitive to the tuning parameters than those of the ANN efficient score estimators. In addition, simple spline based estimators of WADs of NPIVs perform very well in terms of finite sample biases and variances. More research is needed to close the gap between approximation theory and finite sample computational performance in applying flexible ANNs to nonparametric models with endogeneity.

References

- Ai and Chen (2003) Ai, C. and Chen, X. (2003). Efficient estimation of models with conditional moment restrictions containing unknown functions. Econometrica, 71 (6), 1795–1843.

- Ai and Chen (2007) — and — (2007). Estimation of possibly misspecified semiparametric conditional moment restriction models with different conditioning variables. Journal of Econometrics, 141 (1), 5–43.

- Ai and Chen (2012) — and — (2012). The semiparametric efficiency bound for models of sequential moment restrictions containing unknown functions. Journal of Econometrics, 170 (2), 442–457.

- Andrews (2017) Andrews, D. W. (2017). Examples of l2-complete and boundedly-complete distributions. Journal of econometrics, 199 (2), 213–220.

- Athey et al. (2019) Athey, S., Imbens, G. W., Metzger, J. and Munro, E. M. (2019). Using Wasserstein Generative Adversarial Networks for the Design of Monte Carlo Simulations. Tech. rep., National Bureau of Economic Research.

- Barron (1993) Barron, A. R. (1993). Universal approximation bounds for superpositions of a sigmoidal function. IEEE Transactions on Information theory, 39 (3), 930–945.

- Berry and Haile (2016) Berry, S. and Haile, P. (2016). Identification in differentiated products markets. Annual Review of Economics, 8 (1), 27–52.

- Bickel et al. (1993) Bickel, P. J., Klaassen, C. A., Bickel, P. J., Ritov, Y., Klaassen, J., Wellner, J. A. and Ritov, Y. (1993). Efficient and adaptive estimation for semiparametric models, vol. 4. Johns Hopkins University Press Baltimore.

- Blundell et al. (2007) Blundell, R., Chen, X. and Kristensen, D. (2007). Semi-nonparametric iv estimation of shape-invariant engel curves. Econometrica, 75 (6), 1613–1669.

- Blundell et al. (2012) —, Horowitz, J. L. and Parey, M. (2012). Measuring the price responsiveness of gasoline demand: Economic shape restrictions and nonparametric demand estimation. Quantitative Economics, 3 (1), 29–51.

- Chamberlain (1992) Chamberlain, G. (1992). Comment: sequential moment restrictions in panel data. Journal of Business and Economic Statistics, 10, 20–26.

- Chen (2007) Chen, X. (2007). Large sample sieve estimation of semi-nonparametric models. Handbook of econometrics, 6, 5549–5632.

- Chen et al. (2021a) —, Christensen, T. and Kankanala, S. (2021a). Adaptive estimation and uniform confidence bands for nonparametric iv. arXiv preprint arXiv:2107.11869.

- Chen and Christensen (2018) — and Christensen, T. M. (2018). Optimal sup-norm rates and uniform inference on nonlinear functionals of nonparametric iv regression. Quantitative Economics, 9 (1), 39–84.

- Chen et al. (2021b) —, Liao, Y. and Wang, W. (2021b). Neural Network Inference on Nonparametric Conditional Moment Restrictions with Weakly Dependent Data. Tech. rep.

- Chen and Liao (2015) — and Liao, Z. (2015). Sieve semiparametric two-step gmm under weak dependence. Journal of Econometrics, 189, 163–186.

- Chen and Ludvigson (2009) — and Ludvigson, S. C. (2009). Land of addicts? an empirical investigation of habit-based asset pricing models. Journal of Applied Econometrics, 24 (7), 1057–1093.

- Chen and Pouzo (2015) — and Pouzo, D. (2015). Sieve wald and qlr inferences on semi/nonparametric conditional moment models. Econometrica, 83 (3), 1013–1079.

- Chen et al. (2019) —, — and Powell, J. L. (2019). Penalized sieve gel for weighted average derivatives of nonparametric quantile iv regressions. Journal of Econometrics, 213 (1), 30–53.

- Chen and Qiu (2016) — and Qiu, Y. J. J. (2016). Methods for nonparametric and semiparametric regressions with endogeneity: A gentle guide. Annual review of economics, 8, 259–290.

- Chen and White (1999) — and White, H. (1999). Improved rates and asymptotic normality for nonparametric neural network estimators. IEEE Transactions on Information Theory, 45 (2), 682–691.

- Chernozhukov et al. (2018) Chernozhukov, V., Chetverikov, D., Demirer, M., Duflo, E., Hansen, C., Newey, W. and Robins, J. (2018). Double/debiased machine learning for treatment and structural parameters.

- Chernozhukov et al. (2021) —, Escanciano, J. C., Ichimura, H., Newey, W. K. and Robins, J. M. (2021). Locally robust semiparametric estimation. arXiv preprint arXiv:1608.00033.

- Compiani (2019) Compiani, G. (2019). Market counterfactuals and the specification of multi-product demand: A nonparametric approach. Available at SSRN.

- Dikkala et al. (2020) Dikkala, N., Lewis, G., Mackey, L. and Syrgkanis, V. (2020). Minimax estimation of conditional moment models. arXiv preprint arXiv:2006.07201.

- Farrell et al. (2018) Farrell, M. H., Liang, T. and Misra, S. (2018). Deep neural networks for estimation and inference. arXiv preprint arXiv:1809.09953.

- Hartford et al. (2017) Hartford, J., Lewis, G., Leyton-Brown, K. and Taddy, M. (2017). Deep iv: A flexible approach for counterfactual prediction. In International Conference on Machine Learning, pp. 1414–1423.

- Hornik et al. (1989) Hornik, K., Stinchcombe, M. and White, H. (1989). Multilayer feedforward networks are universal approximators. Neural networks, 2 (5), 359–366.

- Kingma and Ba (2014) Kingma, D. and Ba, J. (2014). Adam: A method for stochastic optimization. arXiv preprint arXiv:1412.6980.

- Lee et al. (1993) Lee, T.-H., White, H. and Granger, C. W. (1993). Testing for neglected nonlinearity in time series models: A comparison of neural network methods and alternative tests. Journal of Econometrics, 56 (3), 269–290.

- Newey and Powell (2003) Newey, W. K. and Powell, J. L. (2003). Instrumental variable estimation of nonparametric models. Econometrica, 71 (5), 1565–1578.

- Paszke et al. (2017) Paszke, A., Gross, S., Chintala, S., Chanan, G., Yang, E., DeVito, Z., Lin, Z., Desmaison, A., Antiga, L. and Lerer, A. (2017). Automatic differentiation in pytorch.

- Pfanzagl (1982) Pfanzagl, J. (1982). Lecture notes in statistics. Contributions to a general asymptotic statistical theory, 13.

- Santos (2011) Santos, A. (2011). Instrumental variable methods for recovering continuous linear functionals. Journal of Econometrics, 161 (2), 129–146.

- Schmidt-Hieber (2019) Schmidt-Hieber, J. (2019). Deep relu network approximation of functions on a manifold. arXiv preprint arXiv:1908.00695.

- Severini and Tripathi (2013) Severini, T. and Tripathi, G. (2013). Semiparametric efficiency bounds for microeconometric models: A survey. Foundations and Trends® in Econometrics, 6 (3–4), 163–397.

- Shen et al. (2021a) Shen, Z., Yang, H. and Zhang, S. (2021a). Neural network approximation: Three hidden layers are enough. Neural Networks, 141, 160–173.

- Shen et al. (2021b) —, — and — (2021b). Optimal approximation rate of relu networks in terms of width and depth. arXiv preprint arXiv:2103.00502.

- Van der Vaart (2000) Van der Vaart, A. W. (2000). Asymptotic statistics, vol. 3. Cambridge university press.

- Yarotsky (2017) Yarotsky, D. (2017). Error bounds for approximations with deep relu networks. Neural Networks, 94, 103–114.

(a)

(b)

Notes.

Monte Carlo Mean Monte Carlo standard deviation across 1,000 replications.