Partial Counterfactual Identification from Observational and Experimental Data

Abstract

This paper investigates the problem of bounding counterfactual queries from an arbitrary collection of observational and experimental distributions and qualitative knowledge about the underlying data-generating model represented in the form of a causal diagram. We show that all counterfactual distributions in an arbitrary structural causal model (SCM) could be generated by a canonical family of SCMs with the same causal diagram where unobserved (exogenous) variables are discrete with a finite domain. Utilizing the canonical SCMs, we translate the problem of bounding counterfactuals into that of polynomial programming whose solution provides optimal bounds for the counterfactual query. Solving such polynomial programs is in general computationally expensive. We therefore develop effective Monte Carlo algorithms to approximate the optimal bounds from an arbitrary combination of observational and experimental data. Our algorithms are validated extensively on synthetic and real-world datasets.

Introduction

This paper studies the problem of inferring counterfactual queries from a combination of observations, experiments, and qualitative assumptions about the phenomenon under investigation. The assumptions are represented in the form of a causal diagram (Pearl 1995), which is a directed acyclic graph where arrows indicate the potential existence of functional relationships among corresponding variables; some variables are unobserved. This problem arises in diverse fields such as artificial intelligence, statistics, cognitive science, economics, and the health and social sciences. For example, when investigating the gender discrimination in college admission, one may ask “what would the admission outcome be for a female applicant had she been a male?” Such a counterfactual query contains conflicting information: in the real world the applicant is female, in the hypothetical world she was not. Therefore, it is not immediately clear how to design effective experimental procedures for evaluating counterfactuals, or how to compute them from observational data.

The problem of identifying counterfactual distributions from the combination of data and a causal diagram has been studied in the causal inference literature. First, there exists a complete proof system for reasoning about counterfactual queries (Halpern 1998). While such a system, in principle, is sufficient in evaluating any identifiable counterfactual expression, it lacks a proof guideline that determines the feasibility of such evaluation efficiently. There are algorithms to determine whether a counterfactual distribution is inferrable from all possible controlled experiments (Shpitser and Pearl 2007), or a special type of counterfactual distributions, called path-specific effects, from observational (Shpitser and Sherman 2018) and experimental data (Avin, Shpitser, and Pearl 2005). Finally, there exist an algorithm that decides whether any nested counterfactual is identifiable an arbitrary combination of observational and experimental distributions (Correa, Lee, and Bareinboim 2021).

In practice, however, the combination of quantitative knowledge and observed data does not always permit one to uniquely determine the target counterfactual query. In such cases, the counterfactual query is said to be non-identifiable. Partial identification methods concern with deriving informative bounds over the target counterfactual probability in non-identifiable settings. Several algorithms have been developed to bound counterfactual probabilities from the combination of observational and experimental data (Manski 1990; Robins 1989; Balke and Pearl 1994, 1997; Evans 2012; Richardson et al. 2014; Kallus and Zhou 2018, 2020; Finkelstein and Shpitser 2020; Kilbertus, Kusner, and Silva 2020; Zhang and Bareinboim 2021).

In this work, we build on the approach introduced by Balke & Pearl in (Balke and Pearl 1994), which involves direct discretization of unobserved domains, also referred to as the canonical partitioning or the principal stratification (Frangakis and Rubin 2002; Pearl 2011). Consider the causal diagram in Fig. 1(a), where are binary variables in ; is an unobserved variable taking values in an arbitrary continuous domain. (Balke and Pearl 1994) showed that domains of could be discretized into equivalent classes without changing the original counterfactual distributions and the graphical structure in Fig. 1(a). For instance, suppose that values of are drawn from an arbitrary distribution over a continuous domain. It has been shown that the observational distribution could be reproduced by a generative model of the form , where is a discrete distribution over a finite domain .

Using the finite-state representation of unobserved variables, (Balke and Pearl 1997) derived tight bounds on treatment effects under a set of constraints called instrumental variables (e.g., Fig. 1(a)). (Chickering and Pearl 1997; Imbens and Rubin 1997) applied the parsimony of finite-state representation in a Bayesian framework, to obtain credible intervals for the posterior distribution of causal effects in noncompliance settings. Despite the optimality guarantees in their treatments, these bounds were only derived for specific settings. A systematic strategy for partial identification in an arbitrary causal diagram is still missing. There are significant challenges in bounding any counterfactual query in an arbitrary causal diagram given an arbitrary collection of observational and experimental data.

Our goal in this paper is to overcome these challenges. We show that when inferring about counterfactual distributions (over finite observed variables) in an arbitrary causal diagram, one could restrict domains of unobserved variables to a finite space without loss of generality. This result allows us to develop novel partial identification algorithms to bound unknown counterfactual probabilities from an arbitrary combination of observational and experimental data. In some way, this paper can be seen as closing a long-standing open problem introduced by (Balke and Pearl 1994), where they solve a special bounding instance in the case of instrumental variables. More specifically, our contributions are as follows. (1) We introduce a special family of discrete structural causal models, and show that it could represent all categorical counterfactual distributions (with finite support) in an arbitrary causal diagram. (2) Using this result, we translate the partial identification task into an equivalent polynomial program. Solving such a program leads to bounds over target counterfactual probabilities that are provably optimal. (3) We develop an effective Monte Carlo algorithm to approximate optimal bounds from a finite number of observational and experimental data. Finally, our algorithms are validated extensively on synthetic and real-world datasets.

Preliminaries

We introduce in this section some basic notations and definitions that will be used throughout the paper. We use capital letters to denote variables (), small letters for their values () and for their domains. For an arbitrary set , let be its cardinality. The probability distribution over variables is denoted by . For convenience, we consistently use as a shorthand for the probability . Finally, the indicator function returns if an event holds; otherwise, is equal to .

The basic semantical framework of our analysis rests on structural causal models (SCMs) (Pearl 2000, Ch. 7). An SCM is a tuple where is a set of endogenous variables and is a set of exogenous variables. is a set of functions where each decides values of an endogenous variable taking as argument a combination of other variables in the system. That is, . Exogenous variables are mutually independent, values of which are drawn from the exogenous distribution . Naturally, induces a joint distribution over endogenous variables , called the observational distribution.

Each SCM is also associated with a causal diagram (e.g., Fig. 1), which is a directed acyclic graph (DAG) where solid nodes represent endogenous variables , empty nodes represent exogenous variables , and arrows represent the arguments of each structural function . We will use graph-theoretic family abbreviations for graphical relationships such as parents and children. For example, the set of parents of in is denoted by ; are similarly defined. The subscript will be omitted when it is obvious from the context.

An intervention on an arbitrary subset , denoted by , is an operation where values of are set to constants , regardless of how they are ordinarily determined. For an SCM , let denote a submodel of induced by intervention . For any subset , the potential response is defined as the solution of in the submodel given . Drawing values of exogenous variables following the probability distribution induces a counterfactual variable . Specifically, the event (for short, ) can be read as “ would be had been ”. For any subsets , , the distribution over counterfactuals is defined as:

| (1) |

Distributions of the form are called interventional distributions; when , coincides with the observational distribution. Throughout this paper, we assume that endogenous variables are discrete and finite; while exogenous variables could take any (continuous) value. The counterfactual distribution defined above is thus a categorical distribution. For a more detailed survey on SCMs, we refer readers to (Pearl 2000, Ch. 7).

Partial Counterfactual Identification

We introduce the task of partial identification of a counterfactual probability from a combination of observational and interventional distributions, which generalizes the previous partial identifiability settings that assume observational data are given (Balke and Pearl 1997; Imbens and Rubin 1997). Let be a finite collection of realizations for sets of variables . We assume data are available from all of the interventional distributions in . Note that corresponds to the observational distribution . Our goal is to find a bound for any counterfactual probability from the collection and the causal diagram .

Formally, let be the set of all SCMs associated with , i.e., 111We will use the subscript to represent the restriction to an SCM . Therefore, represents the causal diagram associated with ; so does counterfactual distributions .. The bound is obtainable by solving the following optimization problem:

| (2) | ||||

| s.t. |

where and are given in the form of Eq. 1. The lower and upper bound are minimum and maximum of the above equation respectively. By the formulation of Eq. 2, must be the tight bound containing all possible values of the target counterfactual .

Since we do not have access to the parametric forms of the underlying structural functions nor the exogenous distribution , solving the optimization problem in Eq. 2 appears theoretically challenging. It is not clear how the existing optimization procedures can be used. Next we show the optimization problem in Eq. 2 can be reduced into a polynomial program by constructing an “canonical” SCM that is equivalent to the original SCM in representing the objective and all constraints .

Canonical Structural Causal Models

Our construction rests on the parametric family of discrete SCMs where values of each exogenous variable are drawn from a discrete distribution over a finite set of states.

Definition 1.

An SCM is said to be a discrete SCM if

-

1.

For every exogenous , its values are contained in a discrete domain ;

-

2.

For every endogenous , its values are given by a function where for any , is contained in a finite domain .

For endogenous variables , let denote the collection of all possible counterfactual distributions over , i.e.,

| (3) |

Recall that is the set of all SCMs compatible with a causal diagram . Counterfactual distributions in are defined as . We will next show that discrete SCMs are indeed “canonical”, i.e., they could generates all counterfactual distributions in any causal diagram.

Our analysis utilizes a special type of clustering of endogenous variables in the causal diagram developed by (Tian and Pearl 2002), which we call confounded components.

Definition 2.

For a causal diagram , let be an arbitrary exogenous variable. A set of endogenous variables (w.r.t. ) is a c-component if for every , there exists a sequence such that:

-

1.

and ;

-

2.

for every , and have a common child node, i.e., .

A c-component in is maximal if there exists no other c-component that strictly contains . For convenience, we will consistently use to denote the maximal c-component w.r.t. every exogenous . For instance, Fig. 1(a) contains two c-components and ; while exogenous variables in Fig. 1(b) share the same c-component since they have a common child node .

Theorem 1.

For a DAG , consider following conditions222For every , we denote by the set of all possible functions mapping from domains to .:

-

1.

is the set of all SCMs compatible with .

-

2.

is the set of all discrete SCMs compatible with such that for every exogenous ,

(4) i.e., the number of functions mapping from domains of to for every endogenous .

Then, are counterfactually equivalent, i.e.,

| (5) |

Thm. 1 establishes the expressive power of discrete SCMs in representing counterfactual distributions in a causal diagram . Henceforth, we will refer to in Thm. 1 as the family of canonical SCMs for . As an example, consider a causal diagram in Fig. 1(b) where are binary variables in . Since share the same c-component , Eq. 4 implies that they also share the same cardinality in the canonical family . It follows from Thm. 1 that the counterfactual distribution in could be generated by a SCM in and be written as follows:

More generally, Thm. 1 implies that counterfactual probabilities in any SCM could be generically generated as follows: for ,

| (6) | ||||

Among above quantities, is a discrete distribution over a finite domain . Counterfactual variables are recursively defined as:

| (7) |

where is the value assigned to variable in constants .

Related work

The discretization procedure in (Balke and Pearl 1994) was originally designed for the “IV” diagram in Fig. 1(a), but it can not be immediately extended to other causal diagrams without loss of generality (see Appendix E for a detailed example). More recently, (Rosset, Gisin, and Wolfe 2018) applied a classic result of Carathéodory theorem in convex geometry (Carathéodory 1911) and showed that the observational distribution in any causal diagram could be represented using finitely many latent states. (Evans et al. 2018) proved a special case of Thm. 1 for interventional distributions in a restricted class of causal diagrams satisfying a running intersection property.

Thm. 1 generalizes existing results in several important ways. First, we prove that all counterfactual distributions could be generated using discrete exogenous variables with finite domains, which subsume both observational and interventional distributions. Second, Thm. 1 is applicable to any causal diagram, thus not relying on additional graphical conditions, e.g., IV constraints (Balke and Pearl 1994). More specifically, we introduce a general, canonical partitioning over exogenous domains in an arbitrary SCM. Any counterfactual distribution in this SCM could be written as a function of joint probabilities assigned to intersections of canonical partitions. This allows us to discretize exogenous domains while maintaining all counterfactual distributions and structures of the causal diagram. We refer readers to Appendix A for more details about the proof for Thm. 1.

Bounding Counterfactual Distributions

The expressive power of canonical SCMs in Thm. 1 suggests a natural algorithm for the partial identification of counterfactual distributions. Recall that the canonical family for a causal diagram consists of discrete SCMs with finite exogenous states. We derive a bound over a counterfactual probability from an arbitrary collection of interventional distributions by solving the following optimization problem:

| (8) | ||||

| s.t. |

where and are given in the form of Eq. 6. The optimization problem in Eq. 8 is generally reducible to a polynomial program. To witness, for every , let parameters represent discrete probabilities . For every , we represent the output of function given input using an indicator vector such that

Doing so allows us to write any counterfactual probability in Eq. 6 as a polynomial function of parameters and . More specifically, the indicator function is equal to a product . For every , is recursively given by:

For instance, consider again the causal diagram in Fig. 1(b). The counterfactual distribution and the observational distribution of any discrete SCM in and be written as the following polynomial functions:

| (9) | |||

| (10) |

where are parameters taking values in ; , , are probabilities of the discrete distribution over the finite domain . One could derive a bound over from by solving polynomial programs which optimize the objective Eq. 9 over parameters , subject to the constraints in Eq. 10 for all entries . We refer readers to Appendix D for additional examples demonstrating how to reduce the original partial identification problem to an equivalent polynomial program.

It follows immediately from Thm. 1 that the solution of the optimization program in Eq. 8 is guaranteed to be a valid, tight bound over the target counterfactual probability.

Theorem 2.

Given a DAG and , the solution of the polynomial program Eq. 8 is a tight bound over the counterfactual probability .

Despite the soundness and tightness of its derived bounds, solving a polynomial program in Eq. 8 may take exponentially long in the most general case (Lewis 1983). Our focus here is upon the causal inference aspect of the problem and like earlier discussions we do not specify which solvers are used (Balke and Pearl 1994, 1997). In some cases of interest, effective approximate planning methods for polynomial programs do exist. Investigating these methods is an ongoing subject of research (Lasserre 2001; Parrilo 2003).

Bayesian Approach for Partial Identification

This section describes an effective algorithm to approximate the optimal bound in Eq. 8 from finite samples drawn from interventional distributions , provided with prior distributions over parameters and (possibly uninformative). Given space constraints, all proofs for results in this section are provided in Appendix B.

More specifically, the learner has access to a finite dataset , where each is an independent sample drawn from an interventional distribution for some . With a slight abuse of notation, we denote by the set of variables that are intervened for generating the -th sample; therefore, its realization . As an example, Fig. 2 shows a graphical representation of the data-generating process for a finite dateset associated with SCMs in Fig. 1(b); the intervention set .

We first introduce effective Markov Chain Monte Carlo (MCMC) algorithms that sample the posterior distribution over an arbitrary counterfactual probability . For every , , endogenous parameters are drawn uniformly over the finite domain . For every , exogenous parameters are drawn from a Dirichlet distribution (Connor and Mosimann 1969). Formally,

| (11) |

where the cardinality and hyperparameters .

Gibbs sampling is a well-known MCMC algorithm that allows one to sample posterior distributions. We first introduce the following notations. Let parameters and be:

| (12) | ||||

We denote by exogenous variables affecting endogenous variables ; we use to represent its realization. Our blocked Gibbs sampler works by iteratively drawing values from the conditional distributions of variables as follows (Ishwaran and James 2001). Detailed derivations of complete conditionals are shown in Appendix B.1.

-

•

Sampling . Exogenous variables , , are mutually independent given parameters . We could draw each corresponding to the -th sample induced by independently. The complete conditional of is given by

(13) -

•

Sampling . Note that parameters are mutually independent given . Therefore, we will derive complete conditionals over separately.

Consider first endogenous parameters . For every , fix . If there exists an instance such that and , the posterior over is given by, for ,

(14) Otherwise, is drawn uniformly from .

Consider now exogenous parameters . For every , fix . Let be the number of instances in equal to . By the conjugacy of the Dirichlet distribution, the complete conditional of is,

(15)

Doing so eventually produces values drawn from the posterior distribution over . Given parameters , we compute the counterfactual probability following the three-step algorithm in (Pearl 2000) which consists of abduction, action, and prediction. Thus computing from each draw eventually gives us the draw from the posterior distribution .

Collapsed Gibbs Sampling

We also describe an alternative MCMC algorithm that applies to Dirichlet priors in Eq. 11. For , let denote the set difference ; similarly, we write . Our collapsed Gibbs sampler first iteratively draws values from the conditional distribution over for every as follows.

-

•

Sampling . At each iteration, draw from the conditional distribution given by

(16) Among quantities in the above equation, for every , if there exists an instance such that and , ,

(17) Otherwise, the above probability is equal to .

For every , let be a set of exogenous samples . Let denote unique values that samples in take on. The conditional distribution over is given by as follows, for ,

(18) where , for , records the number of values that are equal to .

Doing so eventually produces exogenous variables drawn from the posterior distribution of . We then sample parameters from the posterior distribution of ; complete conditional distributions are given in Eqs. 14 and 15. Finally, computing from each sample gives a draw from the posterior .

When the cardinality of exogenous domains is high, the collapsed Gibbs sampler described here is more computational efficient than the blocked sampler, since it does not iteratively draw parameters in the high-dimensional space. Instead, the collapsed sampler only draws once after samples drawn from the distribution of converge. On the other hand, when the cardinality is reasonably low, the blocked Gibbs sampler is preferable since it exhibits better convergence (Ishwaran and James 2001).

Credible Intervals over Counterfactuals

Given a MCMC sampler, one could bound the counterfactual probability by computing credible intervals from the posterior distribution .

Definition 3.

Fix . A credible interval for is given by

| (19) | ||||

For a credible interval , any counterfactual probability that is compatible with observational data lies between the interval and with probability . Credible intervals have been widely applied for computing bounds over counterfactuals provided with finite observations (Imbens and Manski 2004; Vansteelandt et al. 2006; Romano and Shaikh 2008; Bugni 2010; Todem, Fine, and Peng 2010). Let denote the number of samples in that are drawn from an interventional distribution . Assume that the prior distribution over has full support over Borel sets in . It follows from the law of large numbers that the credible interval converges to the optimal bound in Eq. 8 as the sample size grows (to infinite) for all (Chickering and Pearl 1997).

Let be samples drawn from . One could compute the credible interval for using following estimators (Sen and Singer 1994):

| (20) |

where are the th smallest and the th smallest of 333For any real , let denote the smallest integer larger than , i.e., ..

Lemma 1.

Fix and . Let function . With probability at least , estimators for any is bounded by

| (21) | ||||

We summarize our algorithm, CredibleInterval, in Alg. 1. It takes a credible level and tolerance levels as inputs. In particular, CredibleInterval repeatedly draw samples from . It then computes estimates from drawn samples following Eq. 20 and return them as the output.

Corollary 1.

Fix and . With probability at least , the interval for any is bounded by and .

Corol. 1 implies that any counterfactual probability compatible with the dataset falls between with . As the tolerance rate , converges to a credible interval with high probability.

Simulations and Experiments

We demonstrate our algorithms on various synthetic and real datasets in different causal diagrams. Overall, we found that simulation results support our findings and the proposed bounding strategy consistently dominates state-of-art algorithms. When target probabilities are identifiable (Experiment 1), our bounds collapse to the actual counterfactual probabilities. For non-identifiable settings, our algorithm obtains sharp asymptotic bounds when the closed-form solutions already exist (Experiments 2); and obtains novel counterfactual bounds in other more general cases which consistently improve over existing strategies (Experiment 3 & 4).

In all experiments, we evaluate our proposed strategy using credible intervals (ci). We draw at least samples from the posterior distribution over the target counterfactual. This allows us to compute credible interval over within error , with probability at least . As the baseline, we include the actual counterfactual probability . We refer readers to Appendix C for more details on simulations and additional experiments with other causal diagrams and datasets.

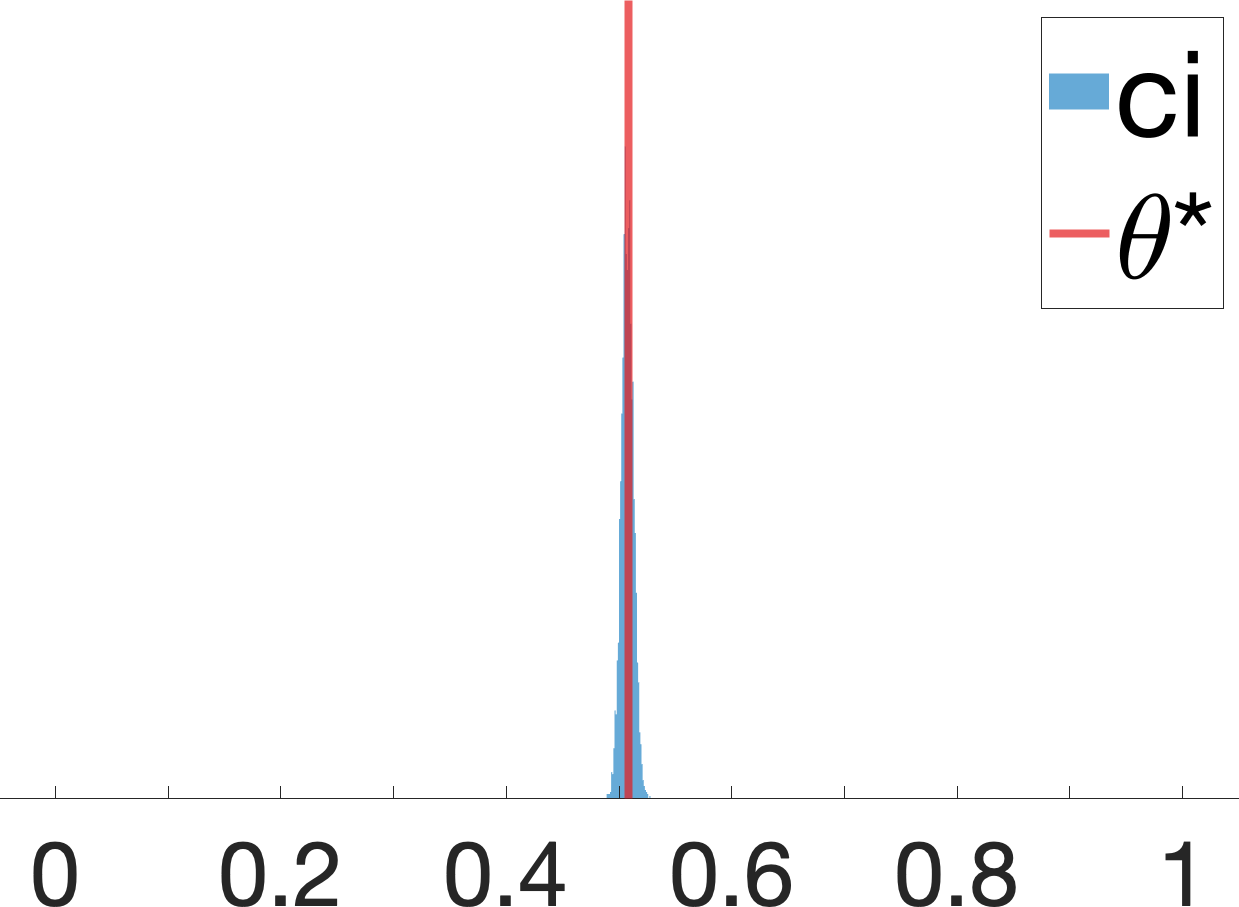

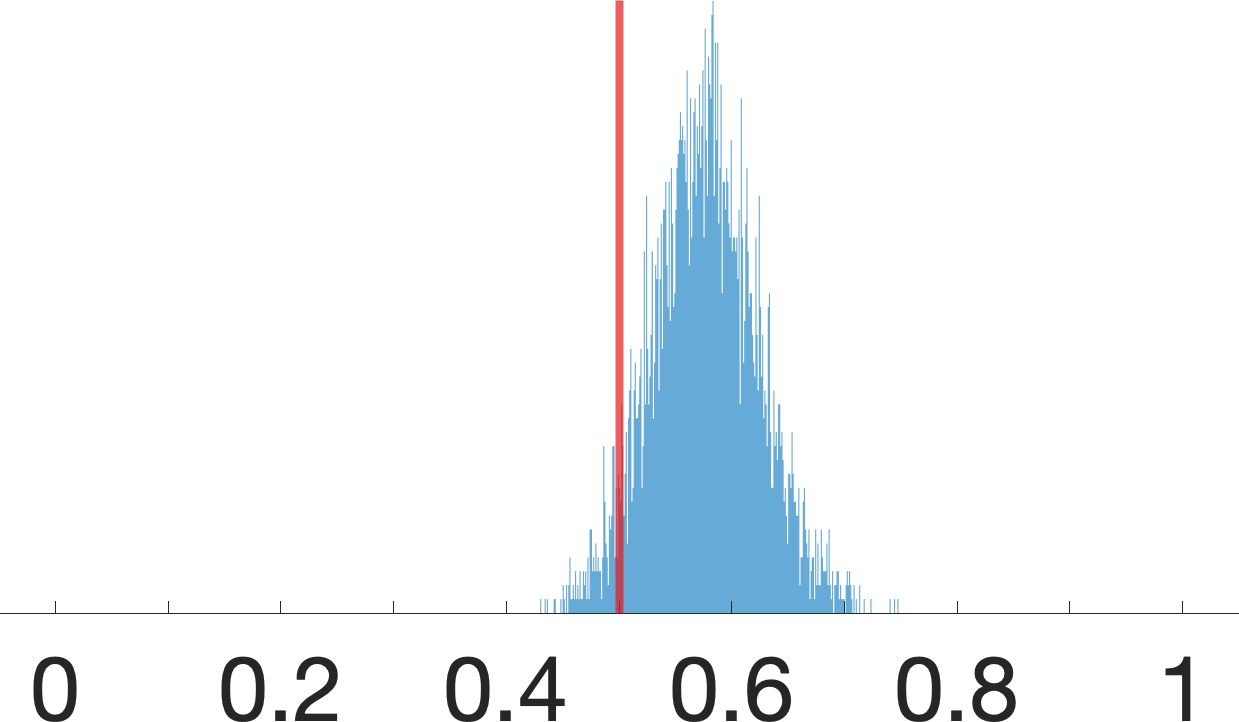

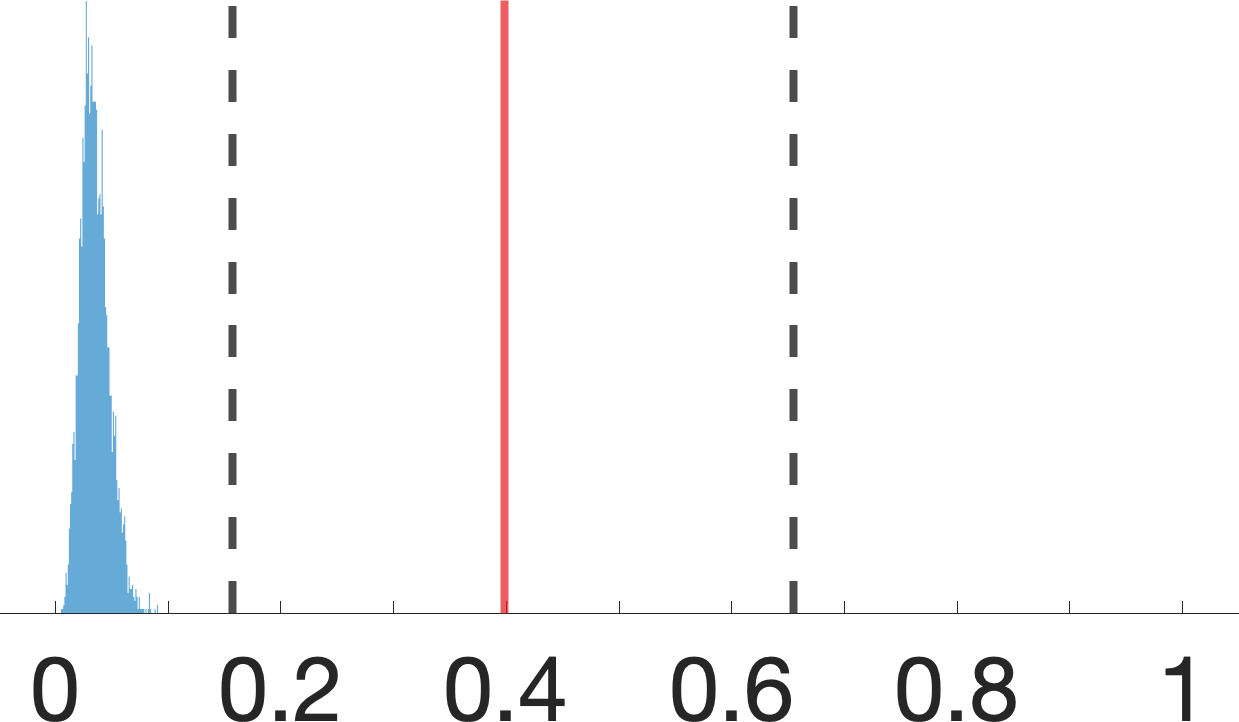

Experiment 1: Frontdoor Graph

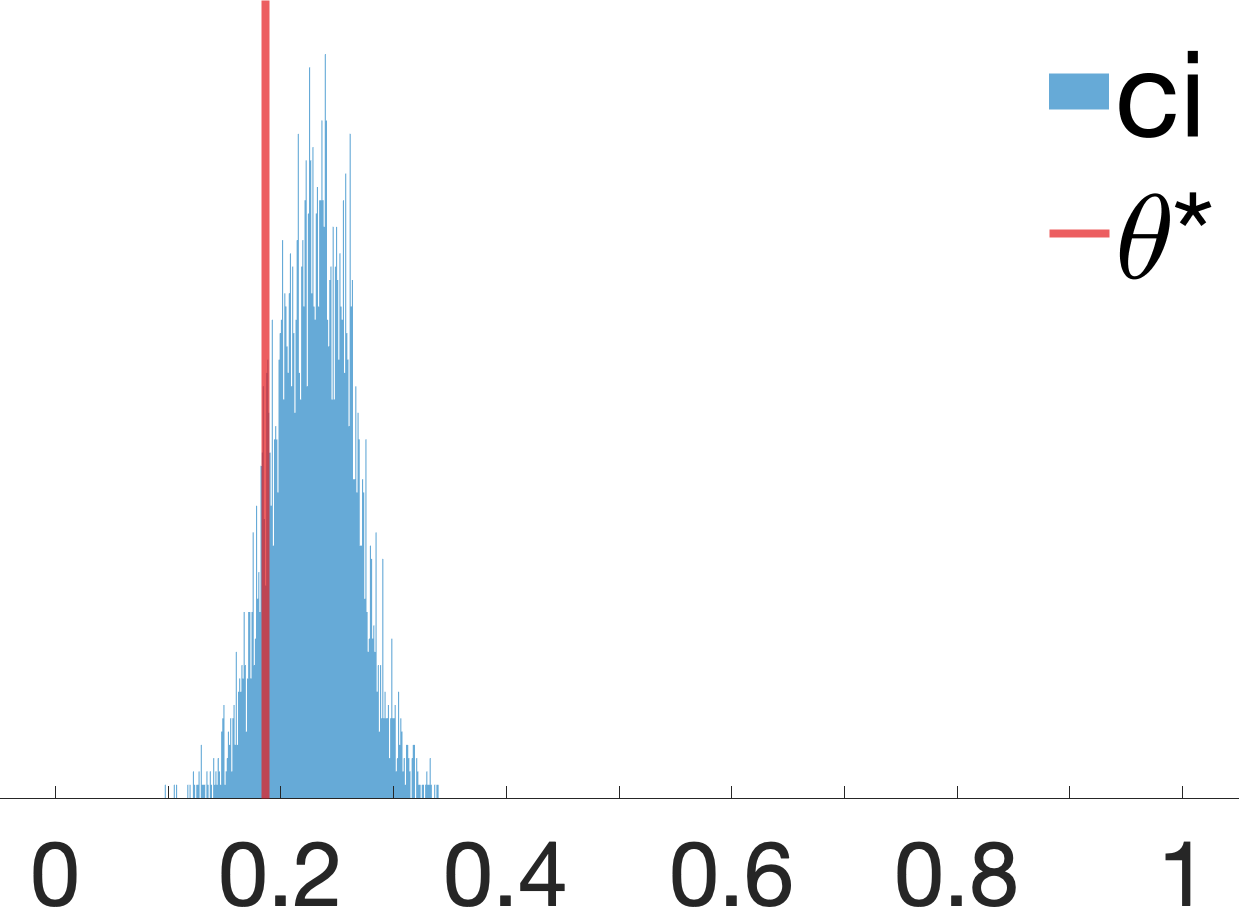

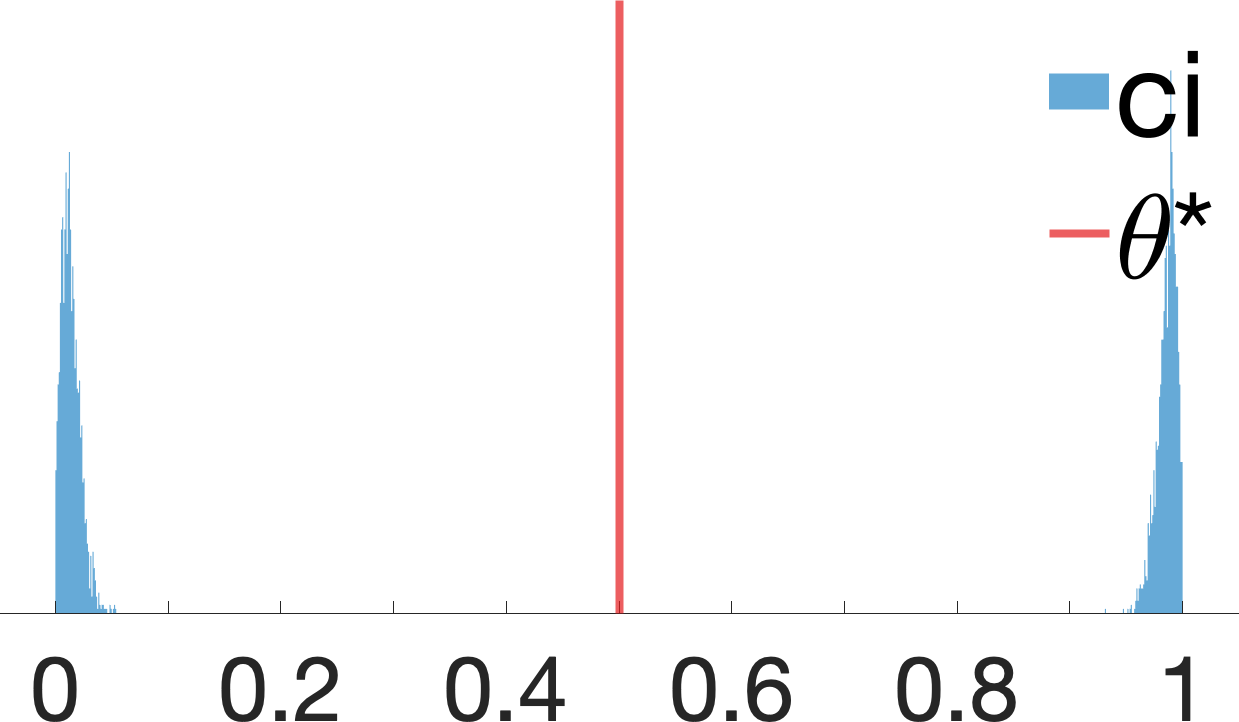

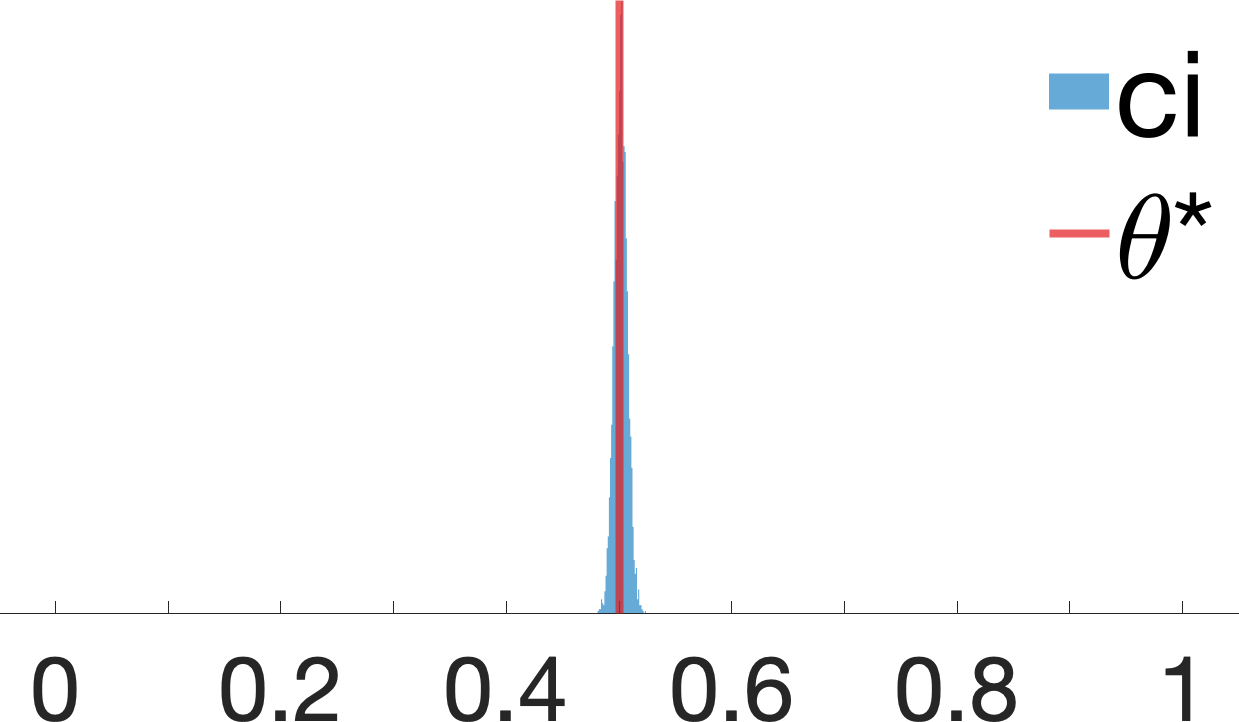

Consider the “Frontdoor” graph described in Fig. 1(c) where are binary variables in ; . In this case, any interventional probability is identifiable from the observational distribution through the frontdoor adjustment (Pearl 2000, Thm. 3.3.4). We collect observational samples from a synthetic SCM instance. Fig. 3(a) shows samples drawn from the posterior distribution . The analysis reveals that these samples collapse to the actual interventional probability , which confirms the identifiability of in the “frontdoor” graph.

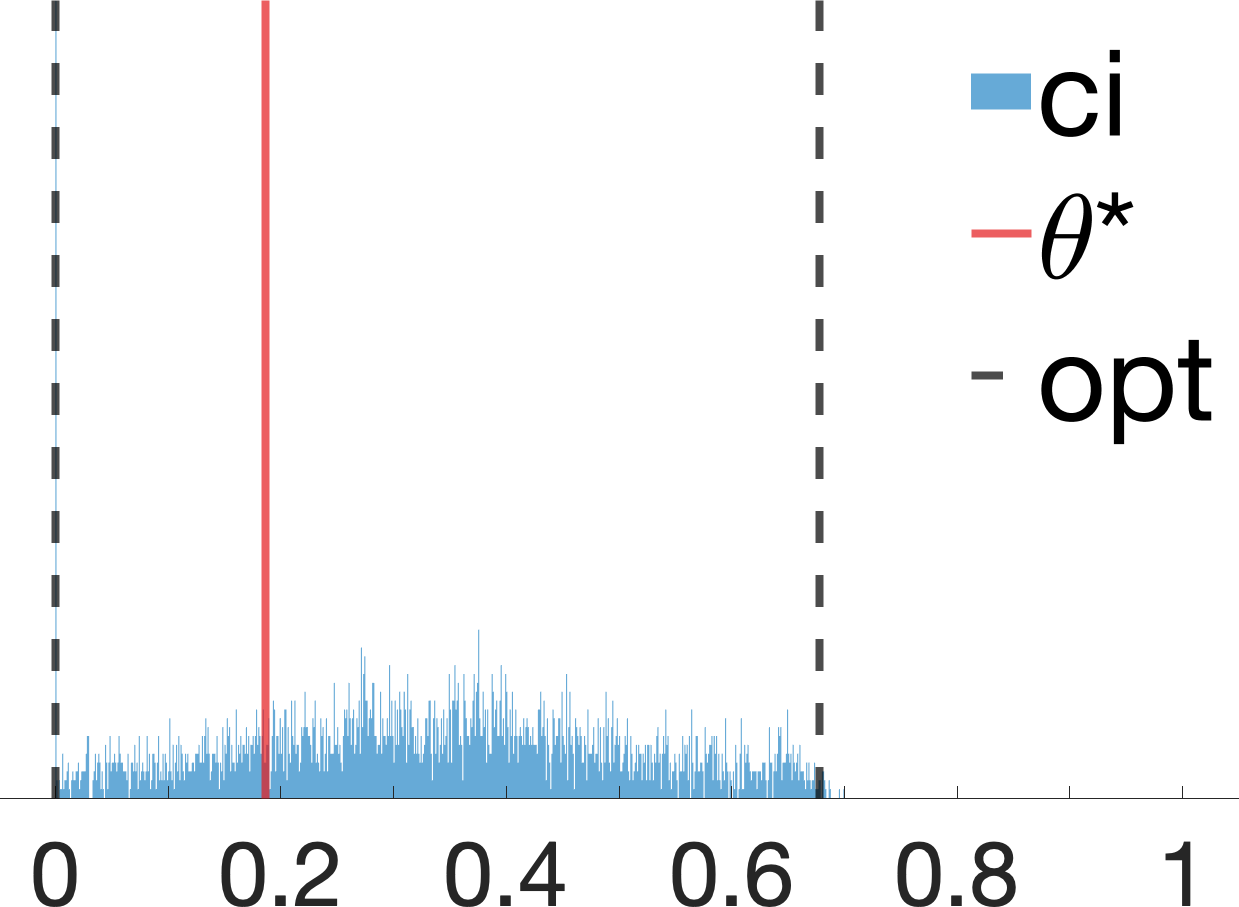

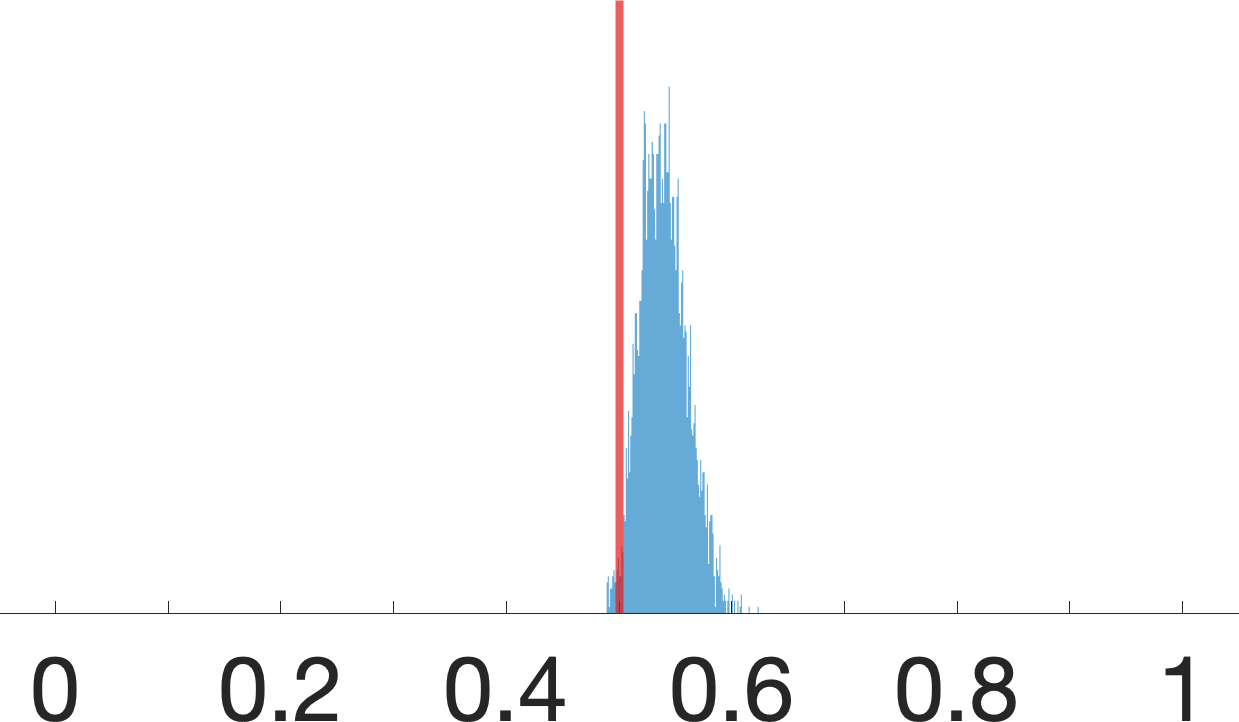

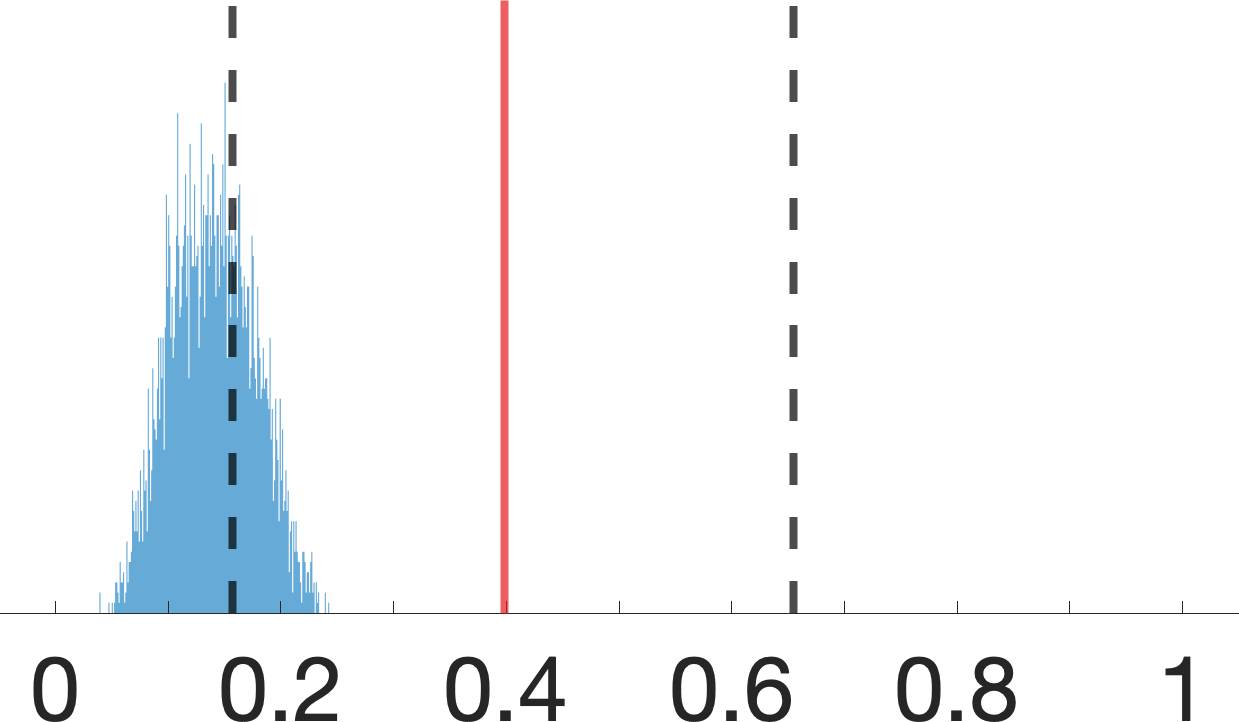

Experiment 2: Probability of Necessity and Sufficiency (PNS)

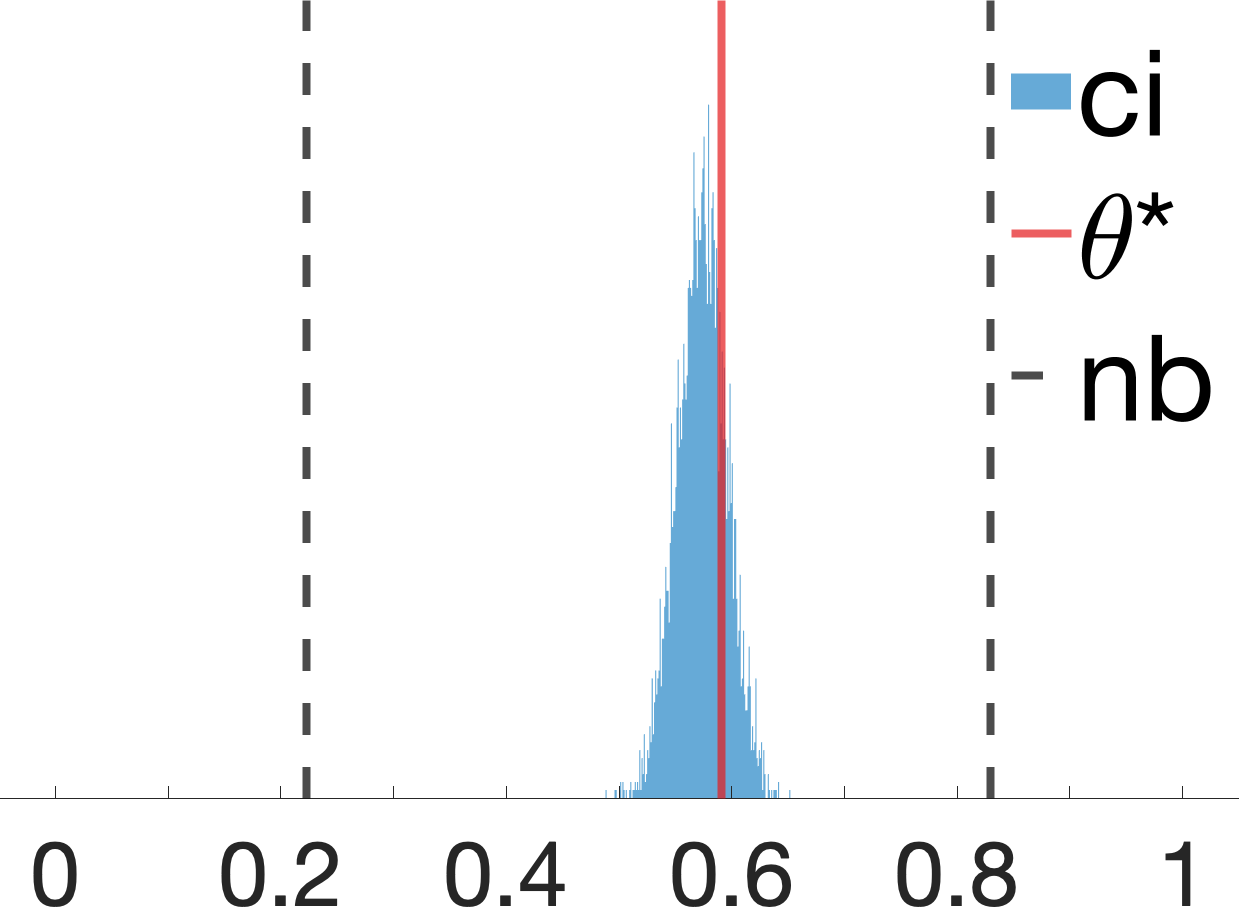

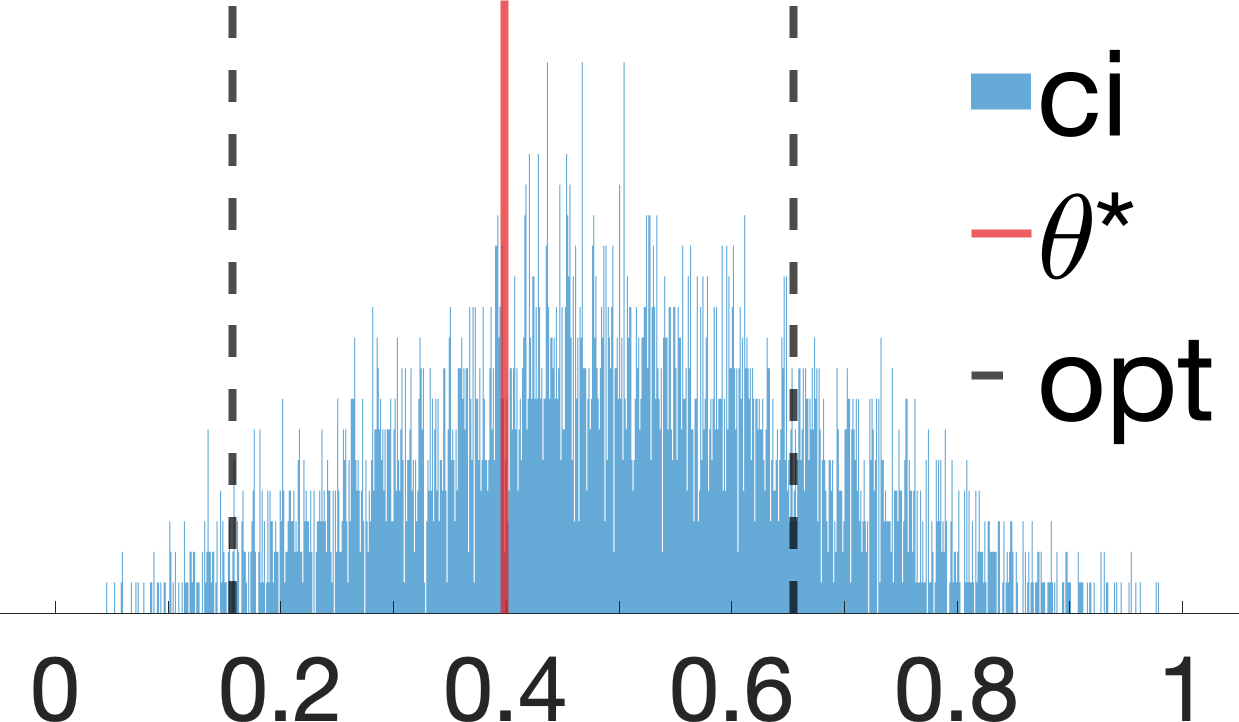

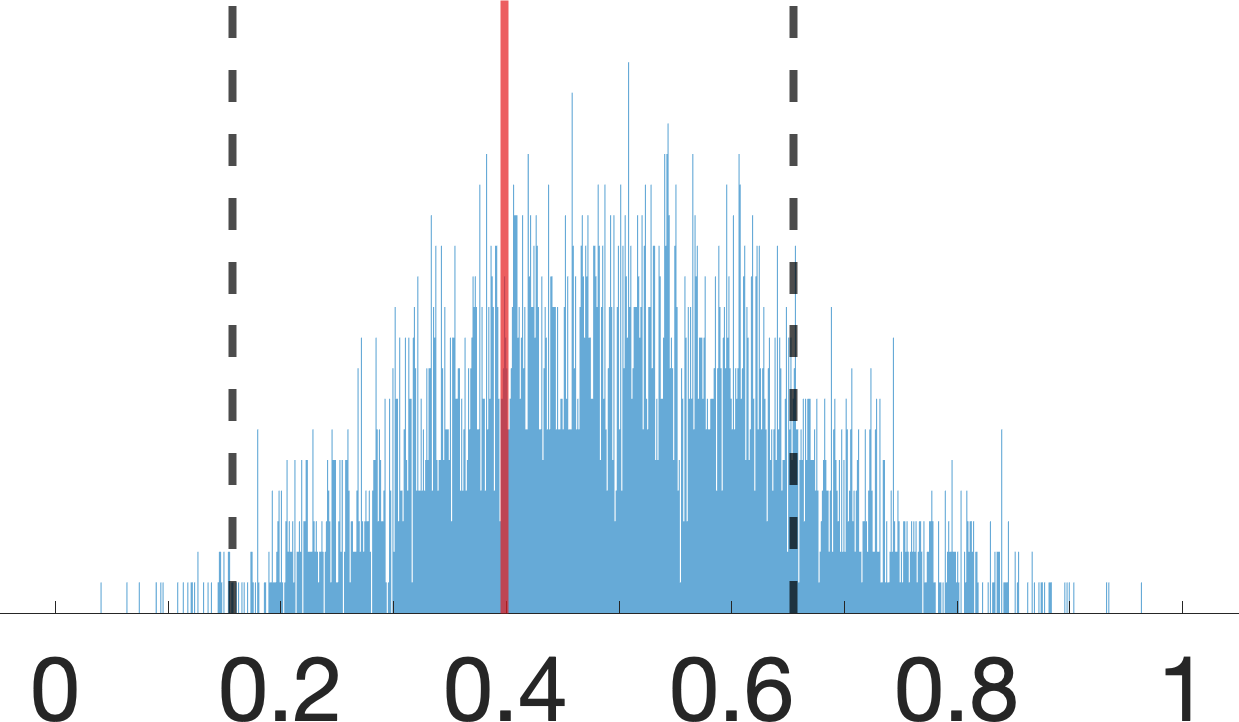

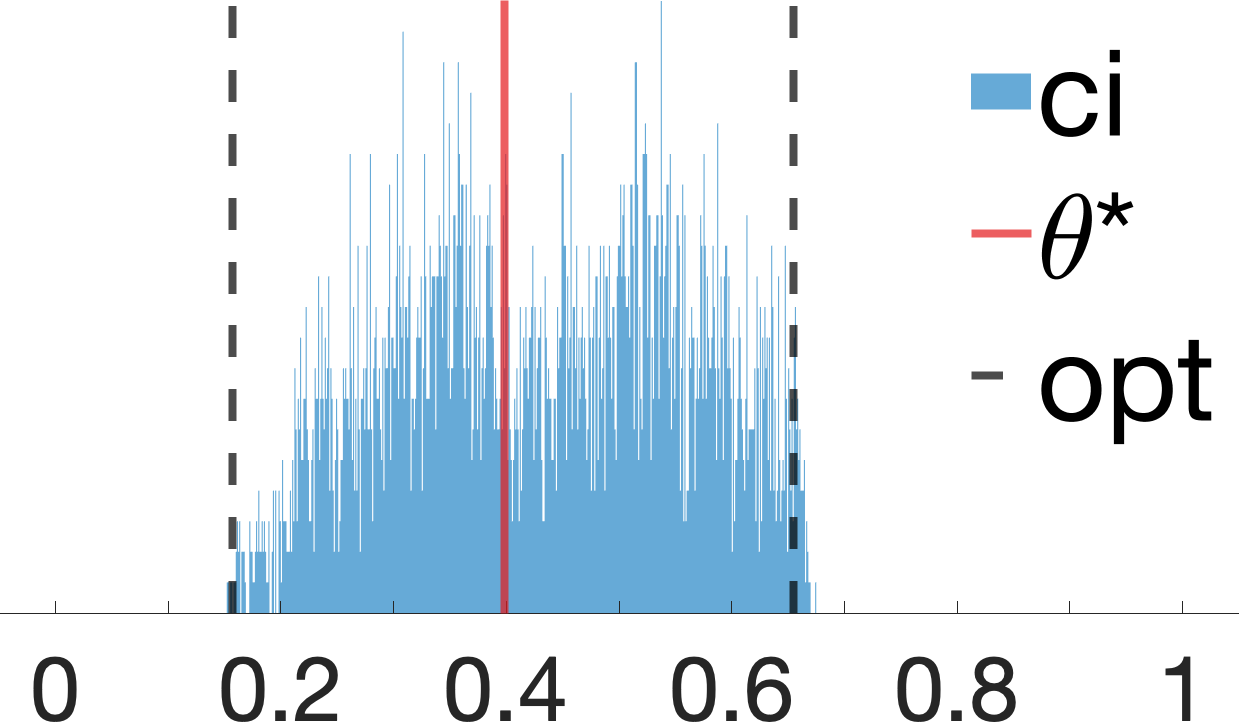

Consider the “Bow” diagram in Fig. 1(d) where and . We study the problem of evaluating the probability of necessity and sufficiency from the observational distribution . The sharp bound for from was introduced in (Tian and Pearl 2000) (labelled as opt). We collect observational samples from a randomly generated SCM instance. Fig. 3(c) shows samples drawn from the posterior distribution over . The analysis reveals that the credible interval (ci) matches the optimal PNS bound over the actual counterfactual probability .

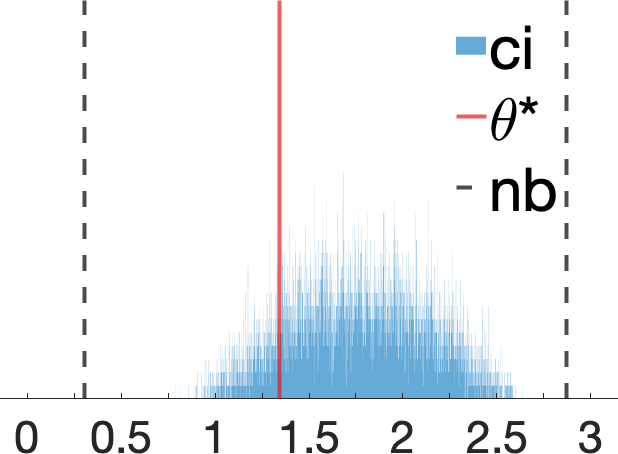

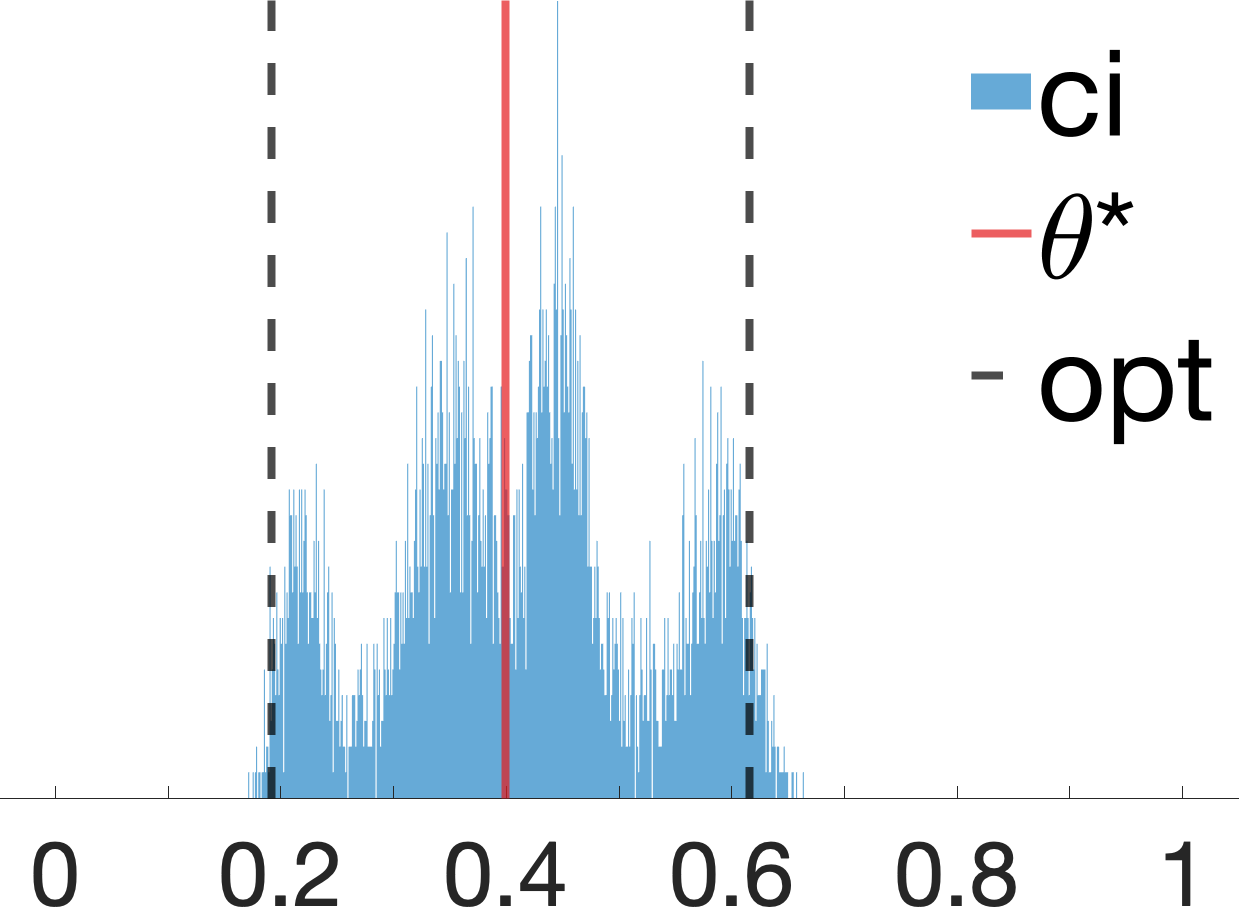

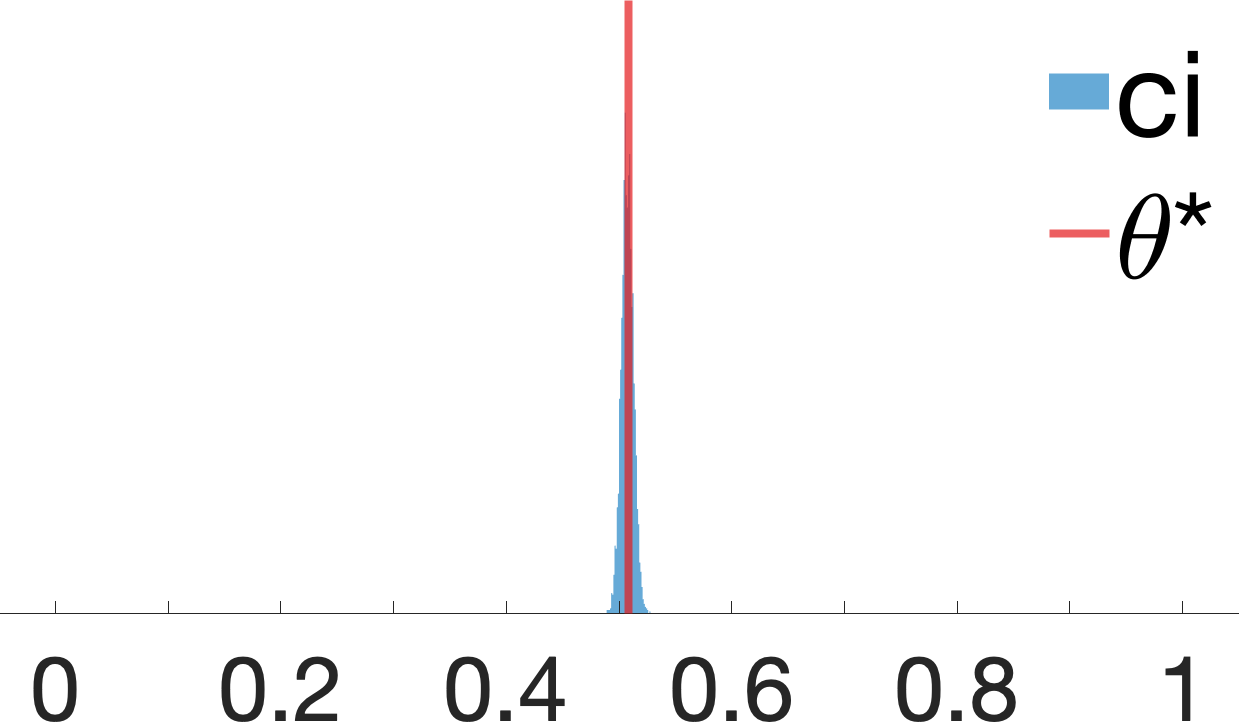

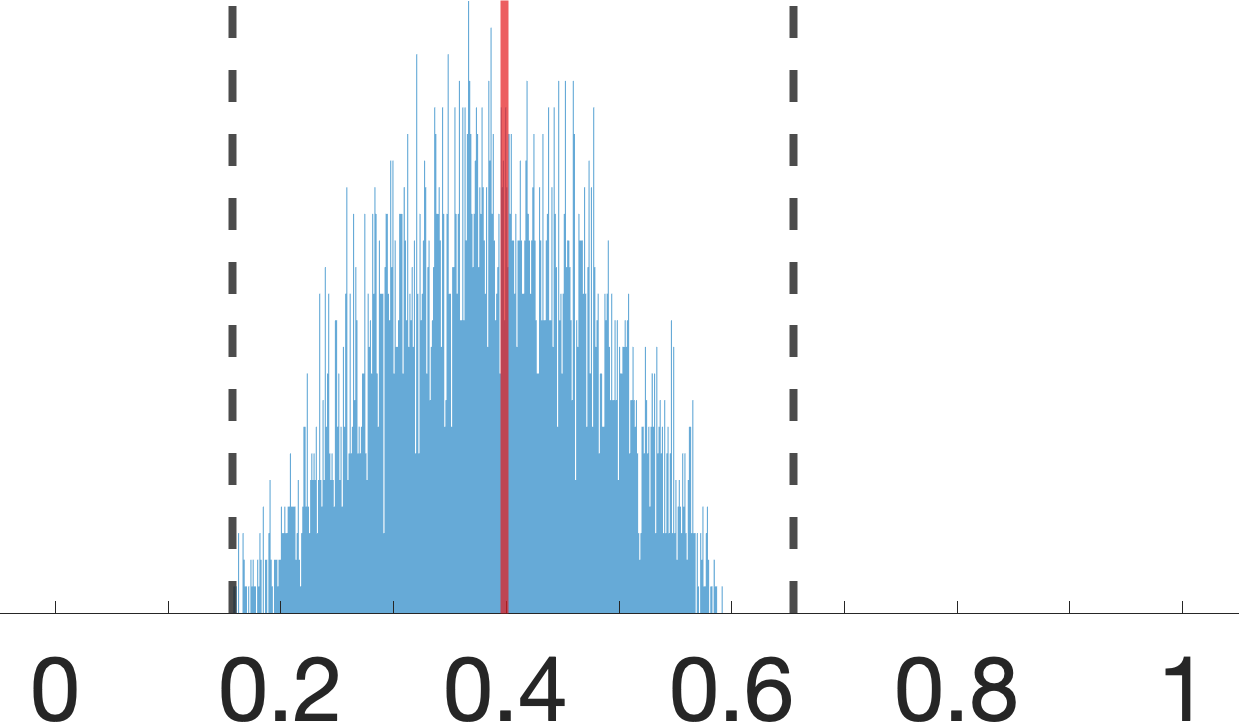

Experiment 3: International Stroke Trials (IST)

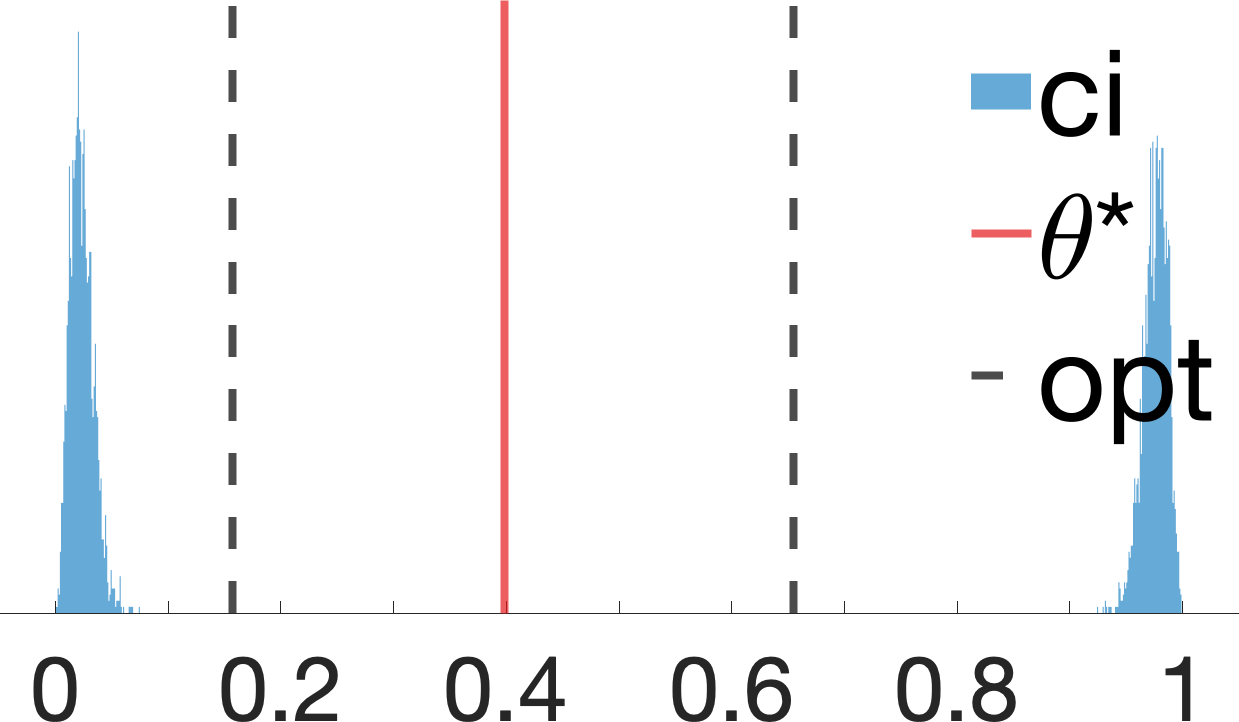

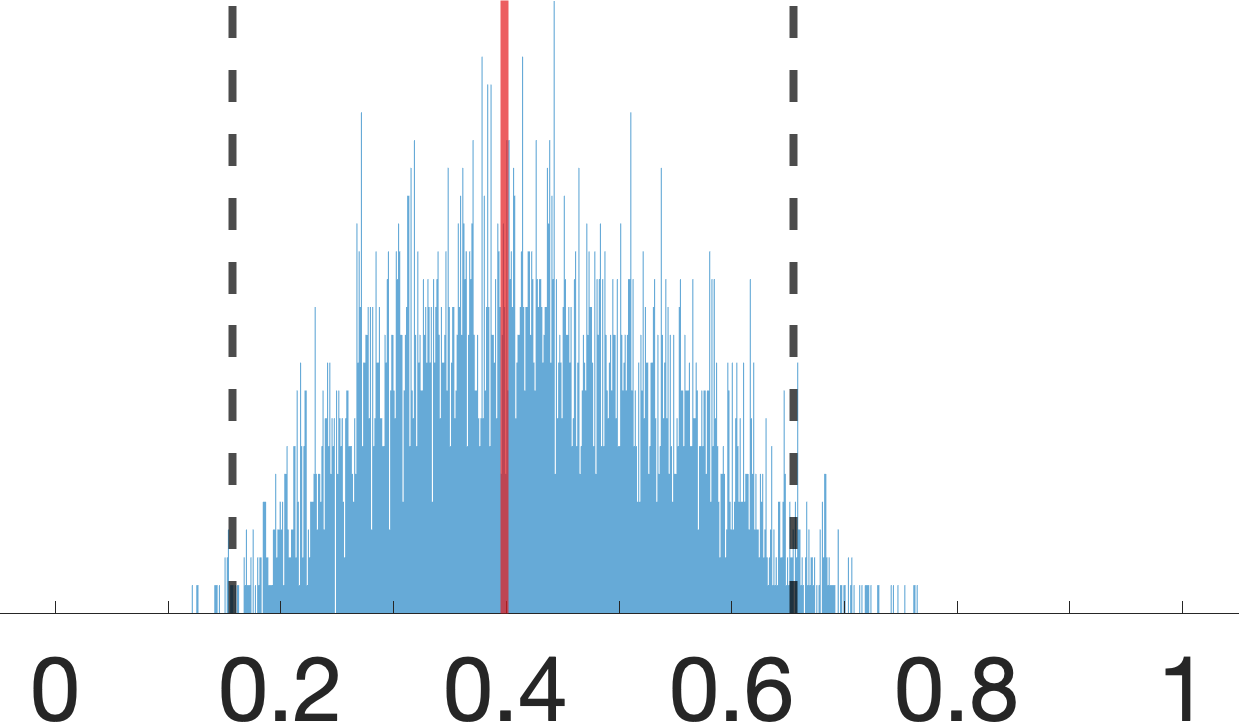

IST was a large, randomized, open trial of up to days of antithrombotic therapy after stroke onset (Carolei et al. 1997). In particular, the treatment is a pair where stands for aspirin allocation; stands for heparin allocation. The primary outcome is the health of the patient months after the treatment. To emulate the presence of unobserved confounding, we filter the experimental data following a procedure in (Kallus and Zhou 2018). Doing so allows us to obtain synthetic observational samples that are compatible with the “IV” diagram of Fig. 1(a) where . We are interested in evaluating the treatment effect for only assigning aspirin . As a baseline, we also include the natural bound (Manski 1990) estimated at the confidence level (nb) (Zhang and Bareinboim 2021). The analysis (Fig. 3(c)) reveals that both algorithms achieve effective bounds containing target causal effect . The credible interval is , which improves over the existing strategy ().

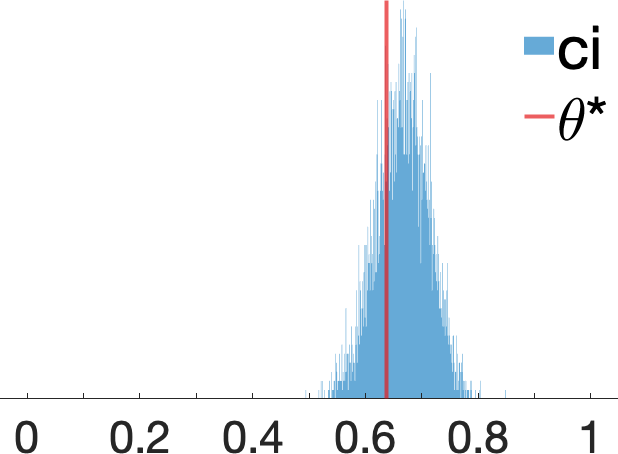

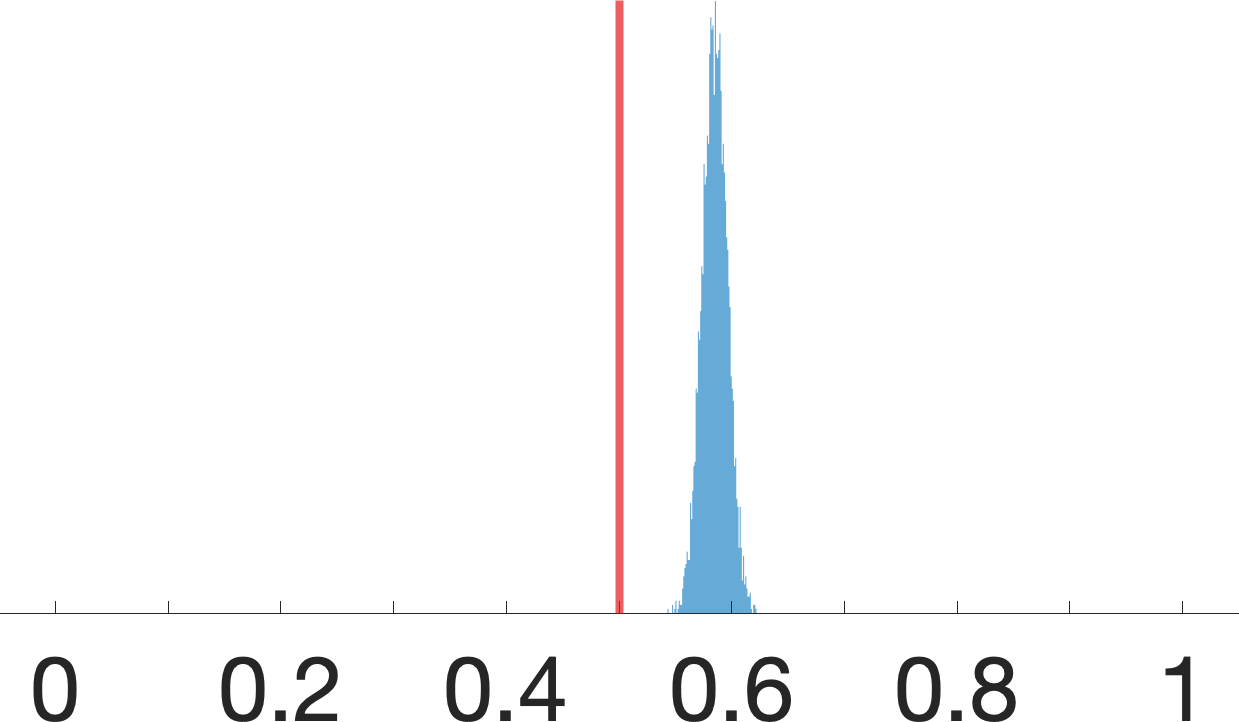

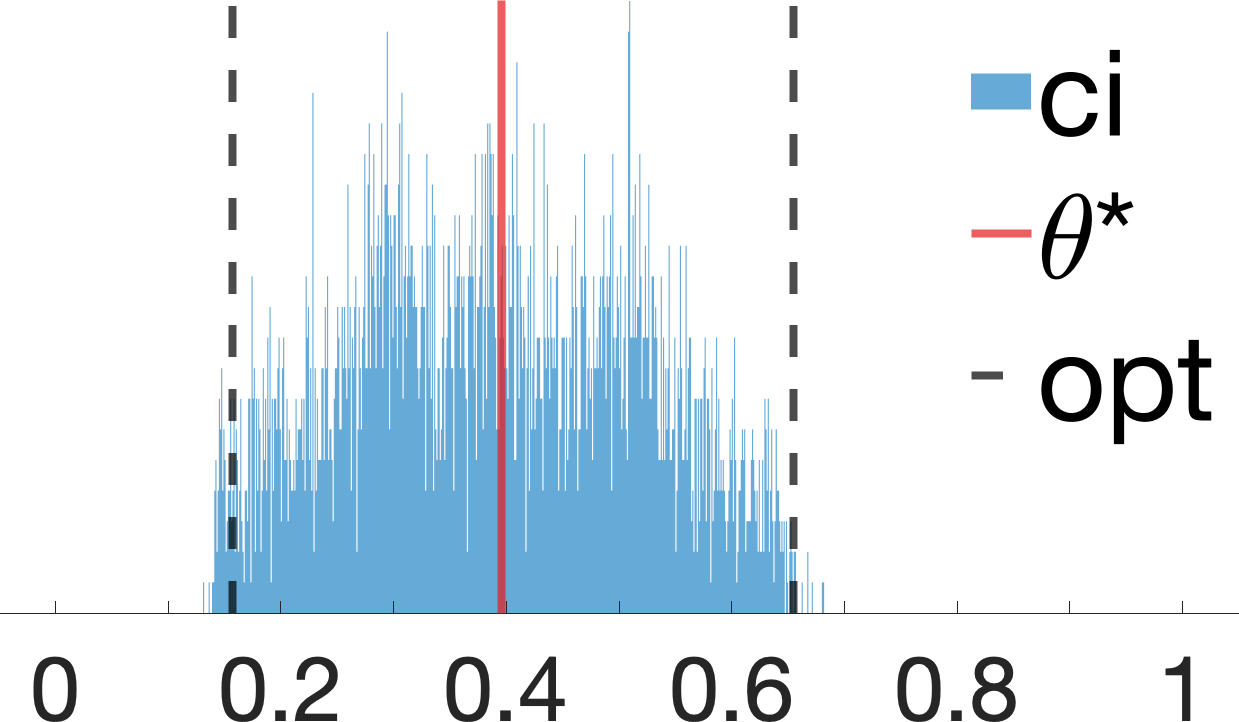

Experiment 4: Obs. + Exp.

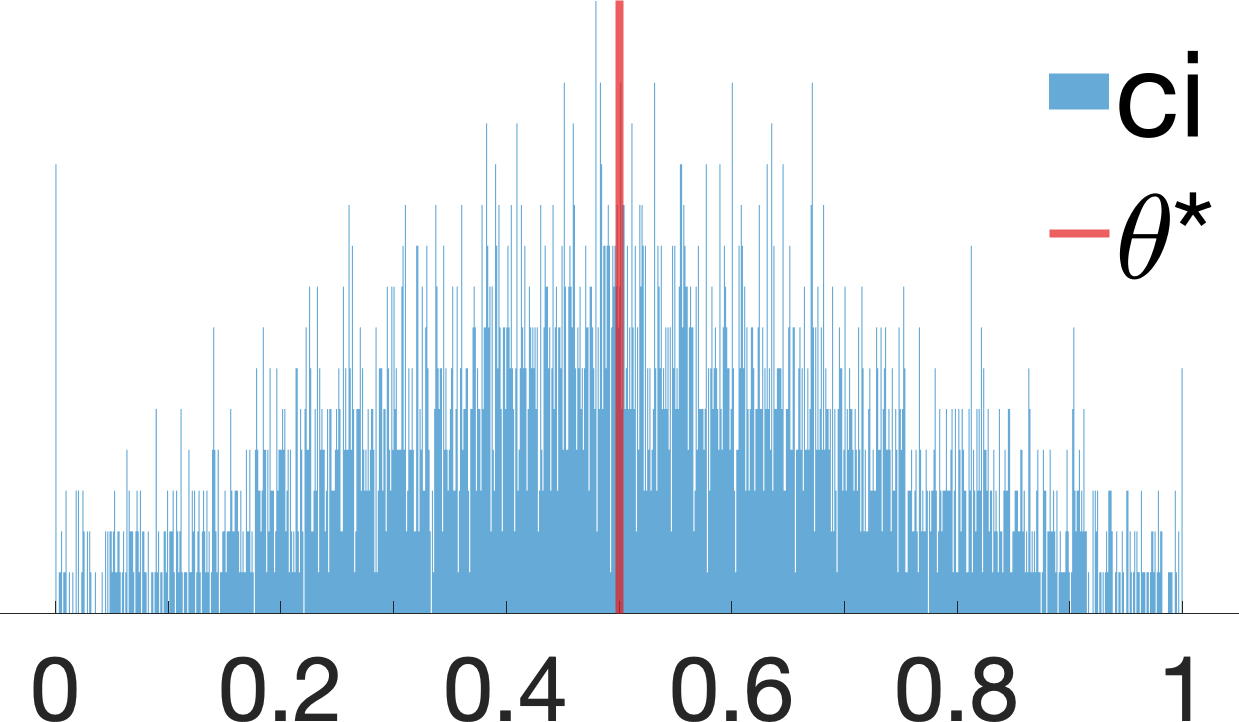

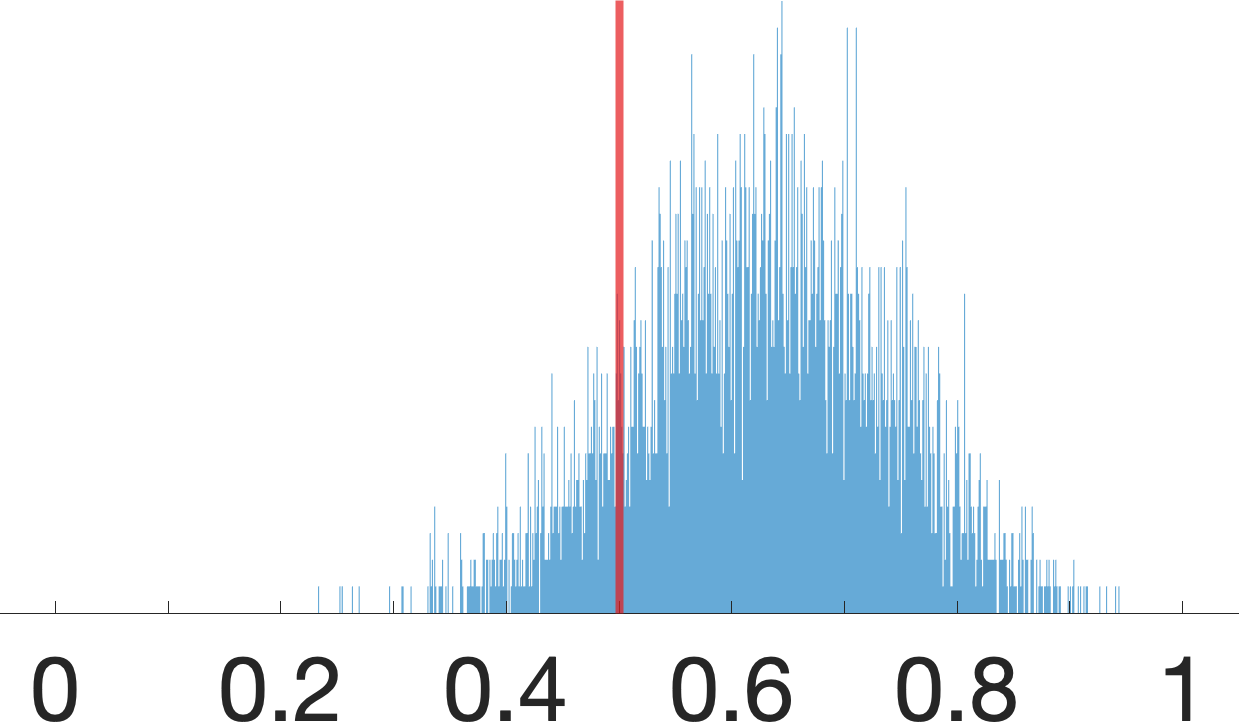

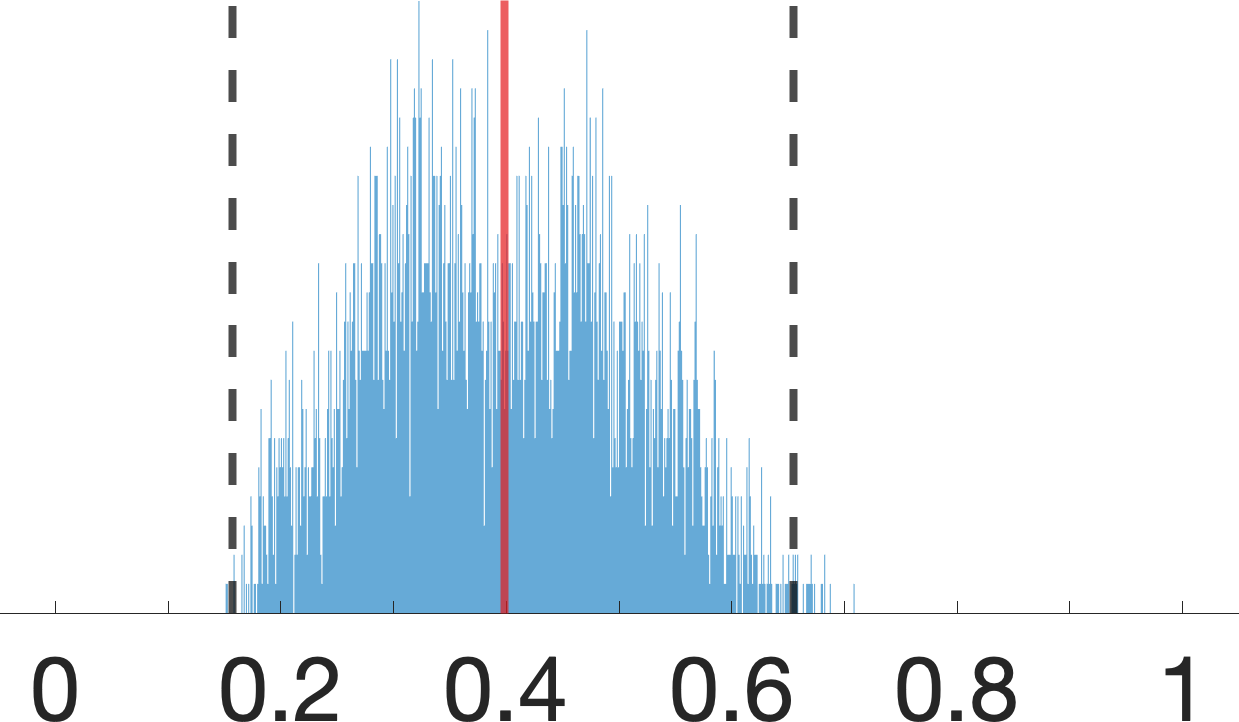

Consider the causal diagram in Fig. 1(b) where and . We are interested in evaluating counterfactual probabilities from the observational distribution and a collection of interventional distributions induced by interventions for . We collect samples from a SCM instance of Fig. 1(b) where each sample is an independent draw from or . To address the challenge of the high-dimensional exogenous domains, we apply the proposed collapsed Gibbs sampler to obtain samples from the posterior distribution . Simulation results are shown in Fig. 3(d). The analysis reveals that our proposed approach is able to achieve an effective bound that contains the actual counterfactual probability . The credible interval (ci) is equal to . To our best knowledge, no existing strategy is applicable for this setting.

Conclusion

This paper investigated the problem of partial identification of counterfactual distributions, which concerns with bounding counterfactual probabilities from an arbitrary combination of observational and experimental data, provided with a causal diagram encoding qualitative assumptions about the data-generating process. We introduced a special parametric family of SCMs with discrete exogenous variables, taking values from a finite set of unobserved states, and showed that it could represent all counterfactual distributions (over finite observed variables) in any causal diagram. Using this result, we reduced the partial identification problem into a polynomial program and developed a novel algorithm to approximate the optimal asymptotic bounds over target counterfactual probabilities from finite samples obtained through arbitrary observations and experiments.

References

- Avin, Shpitser, and Pearl (2005) Avin, C.; Shpitser, I.; and Pearl, J. 2005. Identifiability of Path-Specific Effects. In Proceedings of the Nineteenth International Joint Conference on Artificial Intelligence IJCAI-05, 357–363. Edinburgh, UK: Morgan-Kaufmann Publishers.

- Balke and Pearl (1994) Balke, A.; and Pearl, J. 1994. Counterfactual Probabilities: Computational Methods, Bounds, and Applications. In de Mantaras, R. L.; and Poole, D., eds., Uncertainty in Artificial Intelligence 10, 46–54. San Mateo, CA: Morgan Kaufmann.

- Balke and Pearl (1997) Balke, A.; and Pearl, J. 1997. Bounds on treatment effects from studies with imperfect compliance. Journal of the American Statistical Association, 92(439): 1172–1176.

- Bareinboim and Pearl (2012) Bareinboim, E.; and Pearl, J. 2012. Causal inference by surrogate experiments: -identifiability. In de Freitas, N.; and Murphy, K., eds., Proceedings of the Twenty-Eighth Conference on Uncertainty in Artificial Intelligence, 113–120. Corvallis, OR: AUAI Press.

- Bauer (1972) Bauer, H. 1972. Probability theory and elements of measure theory. Holt.

- Blackwell and Girshick (1979) Blackwell, D. A.; and Girshick, M. A. 1979. Theory of games and statistical decisions. Courier Corporation.

- Bugni (2010) Bugni, F. A. 2010. Bootstrap inference in partially identified models defined by moment inequalities: Coverage of the identified set. Econometrica, 78(2): 735–753.

- Carathéodory (1911) Carathéodory, C. 1911. Über den Variabilitätsbereich der Fourier’schen Konstanten von positiven harmonischen Funktionen. Rendiconti Del Circolo Matematico di Palermo (1884-1940), 32(1): 193–217.

- Carolei et al. (1997) Carolei, A.; et al. 1997. The International Stroke Trial (IST): a randomized trial of aspirin, subcutaneous heparin, both, or neither among 19435 patients with acute ischaemic stroke. The Lancet, 349: 1569–1581.

- Chickering and Pearl (1997) Chickering, D.; and Pearl, J. 1997. A clinician’s tool for analyzing non-compliance. Computing Science and Statistics, 29(2): 424–431.

- Connor and Mosimann (1969) Connor, R. J.; and Mosimann, J. E. 1969. Concepts of independence for proportions with a generalization of the Dirichlet distribution. Journal of the American Statistical Association, 64(325): 194–206.

- Correa, Lee, and Bareinboim (2021) Correa, J.; Lee, S.; and Bareinboim, E. 2021. Nested counterfactual identification from arbitrary surrogate experiments. In In Advances in Neural Information Processing Systems. Forthcoming.

- Durrett (2019) Durrett, R. 2019. Probability: theory and examples, volume 49. Cambridge university press.

- Evans (2012) Evans, R. J. 2012. Graphical methods for inequality constraints in marginalized DAGs. In 2012 IEEE International Workshop on Machine Learning for Signal Processing, 1–6. IEEE.

- Evans et al. (2018) Evans, R. J.; et al. 2018. Margins of discrete Bayesian networks. The Annals of Statistics, 46(6A): 2623–2656.

- Finkelstein and Shpitser (2020) Finkelstein, N.; and Shpitser, I. 2020. Deriving Bounds and Inequality Constraints Using Logical Relations Among Counterfactuals. In Conference on Uncertainty in Artificial Intelligence, 1348–1357. PMLR.

- Frangakis and Rubin (2002) Frangakis, C.; and Rubin, D. 2002. Principal Stratification in Causal Inference. Biometrics, 1(58): 21–29.

- Galles and Pearl (1998) Galles, D.; and Pearl, J. 1998. An axiomatic characterization of causal counterfactuals. Foundation of Science, 3(1): 151–182.

- Halpern (1998) Halpern, J. 1998. Axiomatizing Causal Reasoning. In Cooper, G.; and Moral, S., eds., Uncertainty in Artificial Intelligence, 202–210. San Francisco, CA: Morgan Kaufmann. Also, Journal of Artificial Intelligence Research 12:3, 17–37, 2000.

- Imbens and Manski (2004) Imbens, G. W.; and Manski, C. F. 2004. Confidence intervals for partially identified parameters. Econometrica, 72(6): 1845–1857.

- Imbens and Rubin (1997) Imbens, G. W.; and Rubin, D. B. 1997. Bayesian inference for causal effects in randomized experiments with noncompliance. The annals of statistics, 305–327.

- Ishwaran and James (2001) Ishwaran, H.; and James, L. F. 2001. Gibbs sampling methods for stick-breaking priors. Journal of the American Statistical Association, 96(453): 161–173.

- Kallus and Zhou (2018) Kallus, N.; and Zhou, A. 2018. Confounding-robust policy improvement. In Advances in neural information processing systems, 9269–9279.

- Kallus and Zhou (2020) Kallus, N.; and Zhou, A. 2020. Confounding-robust policy evaluation in infinite-horizon reinforcement learning. Advances in Neural Information Processing Systems.

- Kilbertus, Kusner, and Silva (2020) Kilbertus, N.; Kusner, M. J.; and Silva, R. 2020. A Class of Algorithms for General Instrumental Variable Models. In Advances in Neural Information Processing Systems.

- Lasserre (2001) Lasserre, J. B. 2001. Global optimization with polynomials and the problem of moments. SIAM Journal on optimization, 11(3): 796–817.

- Lewis (1983) Lewis, H. R. 1983. Computers and intractability. A guide to the theory of NP-completeness.

- Manski (1990) Manski, C. 1990. Nonparametric bounds on treatment effects. American Economic Review, Papers and Proceedings, 80: 319–323.

- Parrilo (2003) Parrilo, P. A. 2003. Semidefinite programming relaxations for semialgebraic problems. Mathematical programming, 96(2): 293–320.

- Pearl (1995) Pearl, J. 1995. Causal diagrams for empirical research. Biometrika, 82(4): 669–710.

- Pearl (2000) Pearl, J. 2000. Causality: Models, Reasoning, and Inference. New York: Cambridge University Press. 2nd edition, 2009.

- Pearl (2011) Pearl, J. 2011. Principal Stratification – A goal or a tool? The International Journal of Biostatistics, 7(1). Article 20, DOI: 10.2202/1557-4679.1322. Available at: http://ftp.cs.ucla.edu/pub/stat_ser/r382.pdf.

- Richardson et al. (2014) Richardson, A.; Hudgens, M. G.; Gilbert, P. B.; and Fine, J. P. 2014. Nonparametric bounds and sensitivity analysis of treatment effects. Statistical science: a review journal of the Institute of Mathematical Statistics, 29(4): 596.

- Robins (1989) Robins, J. 1989. The analysis of randomized and non-randomized AIDS treatment trials using a new approach to causal inference in longitudinal studies. In Sechrest, L.; Freeman, H.; and Mulley, A., eds., Health Service Research Methodology: A Focus on AIDS, 113–159. Washington, D.C.: NCHSR, U.S. Public Health Service.

- Romano and Shaikh (2008) Romano, J. P.; and Shaikh, A. M. 2008. Inference for identifiable parameters in partially identified econometric models. Journal of Statistical Planning and Inference, 138(9): 2786–2807.

- Rosset, Gisin, and Wolfe (2018) Rosset, D.; Gisin, N.; and Wolfe, E. 2018. Universal bound on the cardinality of local hidden variables in networks. Quantum Information & Computation, 18(11-12): 910–926.

- Rubin and Wesler (1958) Rubin, H.; and Wesler, O. 1958. A note on convexity in Euclidean n-space. Proceedings of the American Mathematical Society, 9(4): 522–523.

- Sen and Singer (1994) Sen, P. K.; and Singer, J. M. 1994. Large sample methods in statistics: an introduction with applications, volume 25. CRC press.

- Shpitser and Pearl (2007) Shpitser, I.; and Pearl, J. 2007. What Counterfactuals Can Be Tested. In Proceedings of the Twenty-Third Conference on Uncertainty in Artificial Intelligence, 352–359. Vancouver, BC, Canada: AUAI Press. Also, Journal of Machine Learning Research, 9:1941–1979, 2008.

- Shpitser and Sherman (2018) Shpitser, I.; and Sherman, E. 2018. Identification of Personalized Effects Associated With Causal Pathways. In UAI.

- Tian and Pearl (2000) Tian, J.; and Pearl, J. 2000. Probabilities of causation: Bounds and identification. Annals of Mathematics and Artificial Intelligence, 28: 287–313.

- Tian and Pearl (2002) Tian, J.; and Pearl, J. 2002. A general identification condition for causal effects. In Proceedings of the Eighteenth National Conference on Artificial Intelligence, 567–573. Menlo Park, CA: AAAI Press/The MIT Press.

- Todem, Fine, and Peng (2010) Todem, D.; Fine, J.; and Peng, L. 2010. A global sensitivity test for evaluating statistical hypotheses with nonidentifiable models. Biometrics, 66(2): 558–566.

- Vansteelandt et al. (2006) Vansteelandt, S.; Goetghebeur, E.; Kenward, M. G.; and Molenberghs, G. 2006. Ignorance and uncertainty regions as inferential tools in a sensitivity analysis. Statistica Sinica, 953–979.

- Zhang and Bareinboim (2021) Zhang, J.; and Bareinboim, E. 2021. Bounding Causal Effects on Continuous Outcomes. In Proceedings of the 35nd AAAI Conference on Artificial Intelligence.

Appendix A A. On the Expressive Power of Canonical Structural Causal Models

In this section, we provide the proof for Thm. 1 which establishes the expressive power of discrete SCMs in representing counterfactual distributions in an arbitrary causal diagram containing observed variables with finite domains.

Recall that and in Thm. 1 are collections of all SCMs and discrete SCMs (thereafter, canonical) compatible with a causal diagram respectively. Since , the reverse direction of Eq. 5 is self-evident. The main challenge here is to prove the other direction. That is, given an SCM with arbitrary exogenous domains, we want to construct a discrete SCM with finite exogenous domains such that and are both compatible with the same causal diagram and induces the same set of counterfactual distributions .

To illustrate the idea of this constructive proof, consider as an example the “Bow” graph in Fig. 1(d) where are binary variables in ; the exogenous variable takes values in the real numbers . Let domain be ordered by and . We denote by the set of all functions mapping from domains of to , i.e.,

| (22) | ||||||

Consider the following families of SCMs:

-

1.

is the set of all SCMs compatible with the “Bow” graph in Fig. 1(d).

-

2.

is the set of all discrete SCMs compatible with the “Bow” graph in Fig. 1(d) with the cardinality .

Our goal is to prove that and are counterfactually equivalent for binary . Since intervening on has no causal effect on (Galles and Pearl 1998), it is sufficient to show that for any SCM , one could construct a discrete SCM so that

| (23) |

The construction procedure is described as follows. Let the exogenous variable in be a pair where and . Values of and are given by the following functions, respectively,

| (24) |

It is verifiable that in such , the counterfactual distribution is given by, for ,

| (25) | ||||

For any SCM , we define the exogenous distribution of the discrete SCM as, for ,

| (26) | ||||

It follows immediately from Eqs. 25 and 26 that and induce the same counterfactual distribution , i.e., the condition in Eq. 23 holds. This means that when inferring counterfactual distributions in the “Bow” graph of Fig. 1(d) with binary , we could assume that the exogenous variable is discrete and takes values in the domain , without loss of generality.

Our goal is to generalize the construction described above to any SCMs compatible with an arbitrary causal diagram. The remainder of this section is organized as follows. In Appendix A.1, we introduce a general canonical partitioning (Balke and Pearl 1994) over exogenous domains for any SCMs with discrete endogenous variables. This allows us to write counterfactual distributions as functions of products of probabilities assigned to intersections of canonical partitions in every c-component. Appendix A.2 shows that probabilities over canonical partitions could be represented using discrete exogenous variables taking values in finite domains. This allows us to prove Thm. 1 for any causal diagram in the theoretical framework of measure-theoretic probability. Finally, we describe in Appendix A.3 a more fine-grained decomposition for canonical partitions, which provides intuitive explanations for the discretization procedure.

A.1 Canonical Partitions of Exogenous Domains

For every endogenous variable , let denote the hypothesis class containing all functions mapping from domains of to . Since are discrete variables with finite domains, the cardinality of the class must be also finite. Given any configuration , the induced function must correspond to a unique element in the hypothesis class . Such mappings lead to a finite partition over the exogenous domain .

Definition 4.

For an SCM , for every , let functions in be ordered by where . A equivalence class for function , , is a subset in such that

| (27) |

Definition 5 (Canonical Partition).

For an SCM , is the canonical partition over exogenous domain for every .

Def. 5 extends the canonical partition in (Balke and Pearl 1994) which was designed for binary variables in the “IV” diagram of Fig. 1(a).

As exogenous variables vary along its domain, regardless of how complex the variation is, its only effect is to switch the functional relationship between and among elements in class . Formally,

Lemma 2.

For an SCM , for each , function could be decomposed as:

| (28) |

Proof.

As an example, consider an SCM associated with the “IV” graph of Fig. 1(a) where are binary variables contained in ; are continuous variables drawn uniformly from the interval . Values of are decided by functions defined as follows, respectively,

| (29) | ||||

We show in Fig. 4 the graphical representation of canonical partitions induced by functions and respectively. A detailed description is provided in Table 1. It follows from the decomposition of Lem. 2 that functions in Eq. 29 could be written as follows:

Let denote the product of indexing sets . For any index , we use to represent the element in restricted to . We omit the subscript when it is obvious; therefore, , . Our next result establishes a universal decomposition of counterfactual distributions in any SCM using canonical partitions.

Lemma 3.

For an SCM , for any 444For an arbitrary subset , we will consistently use as a shorthand for the probability .,

| (30) | ||||

where variables of the form ; every is recursively defined as:

| (31) |

Proof.

We will first prove the following claims: for arbitrary subsets , for any ,

| (32) |

Let be a subgraph obtained from the causal diagram by removing all incoming arrows of . We will prove Eq. 32 by induction on .

Base Case .

Recall that an intervention set values of variables as constants . For any , let be the values assigned to in . It is verifiable that

| (33) |

As for every variable , we must have its parent nodes since . This implies

| (34) |

The last step follows from the decomposition in Lem. 2. Eqs. 33 and 34 together imply that

The last step follows from the definition of variables in Eq. 31 given an index .

Induction Case .

Assume that Eq. 32 holds for . We will prove for the case . For every , is given in Eq. 33. For every , the decomposition in Lem. 2 implies:

The last step hold by conditioning on events , . Since we assume Eq. 32 holds for Case , the above equation could be further written as

A few simplification gives:

| (35) |

Eqs. 33 and 35 together imply that

Again, the last step follows from the definition of variables in Eq. 31 given an index .

We are now ready to prove Eq. 30. The statement of Eq. 32 implies that for any ,

Simplifying the above equation gives:

In the above equations, the last two steps hold since variables are not functions of exogenous variables . This completes the proof. ∎ Let denote the collection of all maximal c-components (Def. 2) in a causal diagram . For instance, in the “IV” diagram of Fig. 1(a), contains c-components , . The following proposition shows that probabilities over canonical partitions factorize over c-components in a causal diagram.

Lemma 4.

For an SCM , let be the associated causal diagram. For any ,

| (36) |

Proof.

For any c-compoment , let the set of exogenous variables affecting (at least one of) endogenous variables in . By the definition of c-components (Def. 2), it is verifiable that for two different c-compoments , their corresponding exogenous variables do not share any element, i.e., . We complete the proof by noting that exogenous variables in are mutually independent. ∎

As an example, consider again the SCM compatible with Fig. 1(a) defined in Eq. 29. The event occurs if any only if and . This implies

The last step holds since and are two different c-components. It is verifiable from Fig. 4 that , . The above equation could be further written as:

The last step follows since variables are drawn uniformly at random over the interval .

A.2 Bounding Cardinalities of Exogenous Domains

Lems. 3 and 4 together allow us to write any counterfactual distribution in an SCM as a function of products of probabilities assigned to the intersections of canonical partitions in every c-component. To prove the counterfactual equivalence in Thm. 1, it is thus sufficient to construct a canonical SCM from an arbitrary SCM such that (1) are compatible with the same causal diagram ; and (2) generate the same probabilities over canonical partitions. This section will describe how to construct such a discrete SCM.

We start the discussion by introducing some necessary notations and concepts. The probability distribution for every exogenous variable is characterized with a probability space. It is frequently designated where is a sample space containing all possible outcomes; is a -algebra containing subsets of ; is a probability measure on normalized by . Elements of are called events, which are closed under operations of set complement and unions of countably many sets. By means of , a real number is assigned to every event ; it is called the probability of event .

For an arbitrary set of exogenous variables , its realization is an element in the Cartesian product , represented by a sequence . If now , , we may be interested in inferring whether a sequence of events for every occurs. Such an event is represented by a subset . The products with running through generate precisely the product -algebra . The product measure is the only probability measure with restrictions to that satisfies the following consistency condition

| (37) |

for arbitrary . It is obvious that is a probability measure. Consequently,

| (38) |

defines the product of probability spaces , . It is adequate to describe all “measurable events” occurring to exogenous variables .

Recall that for subsets , counterfactual random variables (or potential responses) is defined as the solution of in the submodel induced by intervention given the configuration . For any , let the inverse image be the set of values generating the event , i.e.,

| (39) |

Evidently, we are dealing with a -measurable mapping . Because of this measurability, the inverse image is an event in for any realization . Thus is defined as the probability of taking on a value . Similarly, for any subsets , , the probability of a sequence of counterfactual events is defined as:

We refer readers to (Durrett 2019; Bauer 1972) for a detailed discussion on measure-theoretic probability concepts.

For a c-component in a causal diagram , we denote by the union of exogenous variables affecting an endogenous variable for every . Let exogenous variables in be ordered by , . For convenience, we consistently write as the probability space of , . The product of these probability spaces is thus written as

| (40) |

For any SCM compatible with the diagram , the joint distribution over events defined by canonical partitions associated with variables is given by

| (41) |

Our goal is to show that all correlations among events , , induced by exogenous variables described by arbitrary probability spaces could be produced by a “simpler” generative process with discrete exogenous domains.

Lemma 5.

Any distribution in Eq. 41 could be reproduced with a generic model of the form:

| (42) |

where every exogenous variable takes values in a finite domain , .

(Rosset, Gisin, and Wolfe 2018, Prop. 2) applied a classic result of Carathéodory theorem in convex geometry (Carathéodory 1911) and showed that the observational distribution in any causal diagram could be generated using discrete exogenous variables, assuming that exogenous variables are drawn from distributions characterized with well-defined probability density functions. We here present a constructive proof that applies to the general framework of measure-theoretic probability theory.

Proof of Lemma 5.

Let be a vector representing probabilities of . Note that for every , there are equivalence classes . is thus a vector with elements. Since , it only takes a vector with dimensions to uniquely determine . We could thus see as a point in the -dimensional real space. Similarly, is vector in where the -th element is equal to

Fix an exogenous variable . We define function as the distribution over canonical partitions when is fixed as a constant . That is,

| (43) | ||||

The associativity of the product of probability spaces (Bauer 1972, Ch. 3.3) generally implies:

| (44) | ||||

Let be a vector in representing probabilities of and let be vector in where the -th element is equal to . Applying Fubini’s Theorem (Durrett 2019, Thm. 1.7.2) implies that function is -measurable. That is, yields a probability measure for a set with respective to Borel sets in real space with average

| (45) |

It can be shown that the probability vector is a point lying in the convex hull of a set (see (Blackwell and Girshick 1979, Thm. 2.4.1) and its extension to arbitrary probability measures in (Rubin and Wesler 1958)). This means that there exists a finite set of vectors and a sequence of positive coefficients such that

| (46) |

The above equation implies

| (47) |

Indeed, we could further reduce the number of coefficients by removing linearly dependent vectors. If vectors are not linearly independent, there exists a non-trivial solution such that . It is verifiable that for any real value

| (48) | |||

| (49) | |||

| (50) |

The last step holds since . Therefore, coefficients , , satisfy

| (51) |

Let be the largest value such that for all . Consequently, there must exist a coefficient . We could then remove the corresponding vector from the base. This procedure continues until all remaining vectors are linearly independent. Since , there are at most linearly independent vectors, i.e., .

Finally, we replace the probability measure with a discrete distribution over a finite discrete domain . Doing so generated a new SCM , with cardinality , that reproduces probabilities over canonical partitions in the original SCM . Repeatedly applying this procedure for every exogenous completes the proof. ∎

Lems. 3, 4 and 5 together yield a natural constructive proof for Thm. 1 in an arbitrary causal diagram . See 1

Proof.

By the definition of c-components (Def. 2), it is verifiable that for two different c-compoments , their corresponding exogenous variables do not share any element, i.e., . Therefore, we could repeatedly apply the construction of Lem. 5 for every c-component . Doing so generates a discrete SCM satisfying conditions as follows:

-

1.

is compatible with ;

-

2.

and share the same set of structural functions ;

-

3.

and generate the same joint distribution over the intersections of canonical partitions associated with every c-component.

It follows from Lems. 3 and 4 that and must coincide in all counterfactual distributions over endogenous variables. This completes the proof. ∎

A.3 Decomposing Canonical Partitions

This section provides a more fine-grained decomposition for equivalence classes in canonical partitions. Such a decomposition provides new insights to the discretization procedure.

Definition 6 (Cell).

For an SCM , for each , a subset is a cell if where , for every .

Obviously, for , any subset of is a cell. However, the same is not necessarily true for . As an example, consider an SCM associated with the causal diagram of Fig. 1(b) where are binary variables in ; are continuous variables drawn uniformly from the interval . More specifically,

| (52) | ||||

Canonical partitions are described in Fig. 6. For points on the boundary, we include them in the equivalence class with a higher indices . As an example, consider the equivalence class , i.e.,

| (53) |

It is a subset in the union of two cells given by

| (54) |

However, one could not write the equivalence class as a product of intervals in , i.e., is not a cell.

Our next result shows that each equivalence class in the canonical partition could be decomposed into a countable union of almost disjoint cells.

Definition 7 (Covering).

For an SCM , for every , let be an arbitrary subset of . Consider the following conditions:

-

1.

is a countable set of cells.

-

2.

For any , and are almost disjoint, i.e.,

(55) -

3.

is a subset for .

Then, is said to be a covering for .

Lemma 6.

For an SCM , for every , let be the equivalent class for an arbitrary function . There exists a covering for such that

| (56) |

Proof.

We first consider a weaker version of the covering cells which does not require every pair of cells to be disjoint. That is, condition (2) in Def. 7 does not necessarily hold. For any , define a set of coverings :

| (57) |

where represents the set of all subsets of .

Recall that every is associated with a probability space . The product measure is the only probability measure with restrictions to which satisfies the independence restriction in Appendix A. It follows from the construction of product measures (Bauer 1972, Theorem 1.5.2) that such a probability measure must satisfy the following property: for any ,

| (58) |

Therefore, we could obtain a covering for an arbitrary equivalence class such that

| (59) |

What remains is to show that every pair are almost disjoint. This is equivalent to proving the following:

| (60) |

By basic properties of probability measures,

| (61) |

Therefore, it is sufficient to show that

| (62) |

Suppose now Eq. 62 does not hold. This means that there exists a covering such that

| (63) |

By the definition in Eq. 57, is also a covering in . The property in Eq. 58 implies:

| (64) |

which contradicts Eq. 59. This completes the proof. ∎

Henceforth, we will consistently refer to a set of cells as a covering if they satisfy conditions both in Def. 7 and Eq. 56. For instance, consider the equivalence class in Fig. 6(a) and cells defined in Eq. 54. Since , forms a covering for . By noting that finite segments in (e.g., a line ) has zero measure, we have

| (65) | ||||

The existence of covering cells also allows us to decompose probabilities over intersections of equivalence classes across canonical partitions. Formally,

Lemma 7.

For an SCM , for any , there exists a sequence of coverings for , , such that

| (66) |

| * | ||||||||

|---|---|---|---|---|---|---|---|---|

| * | * |

.

Proof.

For every , let be a covering for defined in Lem. 6, i.e., it satisfies Eq. 57. We first show that, for any subset ,

| (67) |

Let . Since is a covering of , we must have the following:

| (68) | |||

| (69) |

Next, we show that the above inequality relationships are both tight. Suppose at least one of inequalities in Eqs. 68 and 32 is strict. We must have

The above equation implies

| (70) |

which contradicts Eq. 57. This means that the statement in Eq. 67 must hold, which implies, for any ,

| (71) |

Recall that each cell is a product where is a subset in . Since exogenous variables are mutually independent, we must have, for any ,

| (72) |

This completes the proof. ∎

Consider again the SCM described in Eq. 52. Note that only function in the hypothesis class compatible with event is . Similarly, event corresponds to function ; event corresponds to the function . The decomposition of Eq. 30 gives:

| (73) |

Among above quantities, is covered by cells defined in Eq. 54. and are covered by cells and , respectively, given by

| (74) |

Applying the decomposition in Eq. 66 implies

| (75) |

Eqs. 73 and 75 together give the evaluation

One could verify the above equation from the parametrization in Eq. 52 using the three-step algorithm in (Pearl 2000) which consists of abduction, action, and prediction.

A.4 Decomposing Covering Cells

For an arbitrary cell , we will call every “side” the projection of onto domain , for every . Observe that for disjoint cells, their projections onto the same domain may not necessarily be disjoint. As an instance, equivalence classes and in Fig. 4(a) are covered by (almost) disjoint cells and respectively. Their projections onto are intervals and , which overlap in the sub-interval . This observation suggests that every covering cell could be further decomposed, which will be our focus in this section.

The collection of all projections of covering cells defined in Lem. 7 onto an exogenous is given by

| (76) |

Lems. 3 and 7 shows that all counterfactual distributions in any SCM could be written as a function of probabilities over intersections of above projections, i.e.,

| (77) |

To prove the counterfactual equivalence of canonical SCMs, it is thus sufficient to show that probabilities in Eq. 77 could be generated using a discrete distribution.

For convenience, we will slightly abuse the notation and consistently represent Eq. 76 using a countable set . We will also utilize a special type of subsets in domain generated by intersections over projections and their complements, which we call atoms.

Definition 8 (Atom).

For an arbitrary , let be a countable collection of subsets in . For any , an atom is defined as:

| (78) |

Observe that these atoms are pairwise disjoint, and that . For instance, consider again canonical partitions described in Fig. 6. Covering cells for generates a collection of projections onto the exogenous domain of , i.e.,

| (79) | |||||

For an indexing set , atom is given by

Table 2 shows atoms computed from all indexing sets . We obtain a set of atoms with positive probability measures, given by

| (80) |

Evidently, one could write probabilities over any intersection of projections in as a summation over some atoms . To witness, we show in Fig. 7 more fine-grained partitions over exogenous domains associated with following the decomposition of atoms .

In general, one could represent probabilities of any event generated by a finite set of projections using the decomposition of atoms. However, as the number of projections , there could exist uncountably many such atoms. Therefore, one could not immediately represent their measures as a discrete distribution. Next, we show that it suffices to consider only a countable set of atoms with positive measures.

Lemma 8.

For an SCM , for every , there exists a countable set of atoms defined in Eq. 78 such that and for any ,

Proof.

Formally, we define

It is verifiable that is a -algebra generated by projections . Furthermore, the intersection is a measurable set in . Therefore, it is sufficient to show that for any event ,

| (81) |

We first show that there exists a countable set of atoms that covers domain , i.e.,

| (82) |

Take and define by induction, for all , if , then let

| (83) |

where is an atom with the largest positive measure among all atoms contained in .

If we repeatedly apply the above construction, one of two things may happen:

-

1.

For some , and in this case, satisfy Eq. 82.

-

2.

For all , . In this case, we have a countable set of atoms of positive measures. We now prove Eq. 82 by contradiction. If Eq. 82 does not hold, then there is an atom such that . By our choice of at each step, we have that, for all ,

(84) Therefore,

(85) Contradiction, since the probability measure is finite.

For any event , since , Eq. 82 implies

| (86) |

Therefore,

| (87) | ||||

| (88) | ||||

| (89) |

The last step holds since is a union of atoms and atoms are pairwise disjoint. This completes proof. ∎

We are now ready to prove the counterfactual equivalence for canonical SCMs with discrete exogenous domains.

Lemma 9.

For a DAG , let be an arbitrary SCM compatible with . There exists a discrete SCM compatible with such that , i.e., and coincide in all counterfactual distributions.

Proof.

Let the countable set of atoms defined in Lem. 8 for every . We construct a discrete SCM from as follows.

-

1.

For every , pick an arbitrary constant in each atom .

-

2.

Define distribution for every in as:

(90)

Doing so generates a discrete SCM satisfying conditions as follows:

-

1.

is compatible with ;

-

2.

and share the same set of structural functions ;

-

3.

and generate the same distribution over the intersections of projections of covering cells defined in Eq. 77.

It follows from Lems. 3 and 7 that and must coincide in all counterfactual distributions over endogenous variables. This completes the proof. ∎

A mental image for the discretization procedure in Lem. 9 is described as follows. We first partition the exogenous domain for each into a countable collection of atoms. By doing so, we obtain a partition over the product domain for every . Such a partition consists of countably many (almost) disjoint covering cells (Def. 6) formed by products of atoms (Def. 8). Every cell is assigned with a unique function in the hypothesis class mapping from domains of input to . Given any configuration , for every , one could find the cell containing the constant and generate values of following the associated function . As an example, we show in Fig. 7 a graphical illustration for this discretization procedure for the SCM described in Eq. 52.

Finally, to construct a discrete SCM, it is sufficient to pick an arbitrary constant in each atom, assign it with the probability measure over the corresponding atom, and replace the exogenous with a variable drawn from a discrete distribution over constants . Repeatedly applying this procedure for every exogenous results in a canonical SCM with discrete exogenous domains. Also, one could further reduce cardinalities of exogenous domains by shrinking the support of the constructed discrete distribution. This could be done by re-weighting probabilities assigned to constant in each atom while maintaining probabilities over canonical partitions. Indeed, it is possible to bound the total number of atoms with positive probabilities to a finite value. The existence of such probability measures is guaranteed by the classic result of Carathéodory theorem (Carathéodory 1911), following a similar procedure in the proof of Lem. 7.

Appendix B B. Markov Chain Monte Carlo for Partial Counterfactual Identification

In this section, we will show derivations for complete conditional distributions utilized in our proposed Gibbs samplers. We will also provide proofs for non-asymptotic bounds for empirical estimates of credible intervals used in Alg. 1.

B.1 Derivations of Complete Conditionals

Sampling .

It is verifiable that variables , , are mutually independent given parameters . This implies

The complete conditional over , , is given by

Among quantities in the above equation,

and

Sampling .

For every exogenous variable , we denote by the set of parameters . Similarly, for every endogenous variable , let . Obviously, parameters and are mutually independent, and they do not directly determine values of a variable (exogenous or endogenous) simultaneously. We must have

The above independence relationship implies that to draw samples from the posterior distribution , we could sample distributions over and for every and every separately.

Recall that for every , any , is an indicator vector such that

The complete conditional distribution over , given by Eq. 14, follows from the fact that in any discrete SCM, the -th observation of is decided by

where is a unique element in such that .

Sampling .

At each iteration, draw from the conditional distribution given by

Among quantities in the above equation, by expanding on valus of parameters , one could rewrite the posterior distribution for every as follows

| (91) |

The complete conditional over , , follows from the definition of discrete SCMs. The -th observation of is decided by

for a unique such that . Formally, if there exists a sample such that and , the posterior over is given by

Otherwise,

Marginalizing probabilities over the domain in Eq. 91 gives the complete conditional distribution over .

B.2 Monte Carlo Estimation of Credible Intervals

Recall that for samples drawn from , the empirical estimates for credible interval over are defined as:

| (92) |

where are the th smallest and the th smallest of . One could apply standard concentration inequalities to determine a sufficient number of draws required for obtaining accurate estimates of a credible interval. See 1

Proof.

Fix . If , this means that there are at most instances in that are smaller than or equal to . That is,

The last step in the above equation follows from the standard Hoeffding’s inequality.

If , this implies that there are at least instances in that are larger than or equal to . That is,

The last step follows from the standard Hoeffding’s inequality. Similarly, we could also show that

Finally, bounding the error rate by gives:

| (93) |

Replacing the error rate with completes the proof. ∎

As a corollary, it immediately follows from Lem. 1 that Algorithm CredibleInterval (Alg. 1) is guaranteed to from a sufficient estimate of credible intervals within the specified margin of errors. See 1

Proof.

The statement follows immediately from Lem. 1 by setting . ∎

Appendix C C. Simulation Setups and Additional Experiments

In this section, we will provide details on the simulation setups and preprocessing of datasets. We also conduct additional experiments on other more involved causal diagrams and using skewed hyperparameters for prior distributions. For all experiments, we will focus on Dirichlet priors in Eq. 11 with hyperparameters for some real . This is equivalent to drawing probabilities from a Dirichlet distribution defined as follows:

| (94) |

All experiments were performed on a computer with 32GB memory, implemented in MATLAB. We are migrating the source code to other open-source platforms (e.g., Julia), which will be released once the code migration is done.

Experiment 1: Frontdoor

We study the problem of evaluating interventional probabilities from the observational distribution in the “Frontdoor” diagram of Fig. 1(c). We collect samples from an SCM compatible with Fig. 1(c). Detailed parametrization of the SCM is provided in the following:

| (95) |

where probabilities are given by

Each observation is an independent draw from the observational distribution . We set hyperparameters , .

Experiment 2: PNS

We study the problem of evaluating the counterfactual probability for any from the observational distribution in the “Bow” diagram of Fig. 1(d). We collect observational samples from an SCM compatible with Fig. 1(d). Detailed parametrization of the SCM is defined as follows:

| (96) |

where probabilities are given by

Each observation is an independent draw from the observational distribution . In this experiment, we set hyperparameters .

Experiment 3: IST

International Stroke Trials (IST) was a large, randomized, open trial of up to days of antithrombotic therapy after stroke onset (Carolei et al. 1997). The aim was to provide reliable evidence on the efficacy of aspirin and of heparin. The dataset is released under Open Data Commons Attribution License (ODC-By). In particular, the treatment is a pair where stands for no aspirin allocation, otherwise; stands for no heparin allocation, for median-dosage, and for high-dosage. The primary outcome is the health of the patient months after the treatment, where stands for death, for being dependent on the family, for the partial recovery, and for the full recovery.

To emulate the presence of unobserved confounding, we filter the experimental data with selection rules , , following a procedure in (Zhang and Bareinboim 2021). More specifically, we are provided with a collection of IST samples where is the age of the -th patient. For each data point , we introduce an instrumental variable . Values of the instrumental variable for the -th patient are decided by

| (97) |

We then check if satisfies the following condition

| (98) |

where parameter is given by

If the above condition is satisfied, we keep the data point in the dataset; otherwise, the data point is dropped. After this data selection process is complete, we hide columns of variables . Doing so allows us to obtain synthetic observational samples that are compatible with the “IV”’ diagram of Fig. 1(a).

In this experiment, we set hyperparameters and . As a baseline, we estimate the treatment effect for only assigning aspirin from randomized trial data containing subjects.

Experiment 4: Obs. + Exp.

We study the problem of evaluating counterfactual probabilities from the combination of the observational distribution and interventional distributions , , in the causal diagram of Fig. 1(b). We collect samples from an SCM compatible with Fig. 1(b), which we define as follows:

| (99) |

where for any real , the operator denotes the largest integer smaller than , i.e., ; probabilities are given by

Each sample is an independent draw from the observational distribution or an interventional distribution . To obtain a sample from , we pick a constant uniformly at random, perform intervention in the SCM described in Eq. 99 and observed subsequent outcomes. In this experiment, we set hyperparameters and .

C.1 Additional Simulation Results

We also evaluate our algorithms on various simulated SCM instances in other more involved causal diagrams. Overall, we found that simulation results match our findings in the main manuscript. For identifiable settings (Experiment 5), our algorithms are able to recover the actual, unknown counterfactual probabilities. For non-identifiable settings, our algorithm consistently dominates existing bounding strategies: it achieves sharp bounds if closed-formed solutions exist (Experiments 6); otherwise, it improves over state-of-art bounds (Experiment 7). Finally, for other more challenging non-identifiable settings where existing strategies do not apply (Experiments 8), our algorithm is able to achieve effective bounds over unknown counterfactual probabilities.

In all experiments, we evaluate our proposed strategy using credible intervals (ci). In particular, we draw at least samples from the posterior distribution over the target counterfactual. This allows us to compute credible interval over within error , with probability at least . As the baseline, we also include the actual counterfactual probability, labeled as .

Experiment 5: Napkin Graph

Consider the “Napkin” graph in Fig. 8(a) where are binary variables in ; take values in real . The identifiability of interventional probabilities from the observational distribution could be derived by iteratively applying inference rules of “do-calculus” (Pearl 2000, Thm. 4.3.1). We collect observational samples from an SCM compatible with Fig. 8(a), defined as follows:

| (100) |

where probabilities are given by:

Each observation is an independent draw from the observational distribution . In this experiment, we set hyperparameters , , and . Fig. 9(a) shows a histogram containing samples drawn from the posterior distribution of . Our analysis reveals that these samples converges to the actual interventional probability , which confirms the identifiability of in the napkin graph.

Experiment 6: Double Bow

Consider the “Double Bow” diagram in Fig. 8(b) where and . We study the problem of evaluating interventional probabilities from the observational distribution . We collect observational samples from an SCM compatible with Fig. 1(b). The detailed parametrization of the SCM is defined as follows:

| (101) |

where probabilities are given by:

Each observation is an independent draw from the observational distribution .

(Balke and Pearl 1997) introduced a closed-form bound over from the observational distribution for the “IV” diagram in Fig. 1(a) with binary . It is verifiable that such a bound is also applicable in Fig. 9(b) with binary endogenous domains, and is provably optimal (labeled as opt). To obtain a credible intervals, we apply the collapsed Gibbs sampler with hyperparameters and . Fig. 9(b) shows samples drawn from the posterior distribution of . The analysis reveals that our algorithm derives a valid bound over the actual probability ; the credible interval converges to the optimal IV bound .

Experiment 7: M+BD Graph

Consider the “M+BD” graph in Fig. 8(c) where and . In this case, interventional probabilities are non-identifiable from the observational distribution due to the presence of the collider path . We collect observational samples from an SCM compatible with Fig. 8(c). The detailed parametrization of the SCM is provided as follows:

| (102) |

where probabilities are given by:

Each observation is an independent draw from the observational distribution .

In this experiment, we set hyperparameters and . Fig. 9(c) shows samples drawn from the posterior distribution of . As a baseline, we also include the natural bounds introduced in (Robins 1989; Manski 1990) (nb). The analysis reveals that all algorithms achieve bounds that contain the actual, target causal effect . Our algorithm obtains a credible interval , which improves over the existing bounding strategy ().

Experiment 8: Triple Bow

Consider the “Triple Bow” diagram in Fig. 8(d) where and . We are interested in evaluating the counterfactual probability from the combination of the observational distribution and interventional distributions . To our best knowledge, existing bounding strategies are not applicable to this setting. We collect samples from an SCM compatible Fig. 8(d). The detailed parametrization of the SCM is provided in the following:

| (103) |

where probabilities are given by:

Each sample is an independent draw from the observational distribution or an interventional distribution . To obtain a sample from , we pick a constant uniformly at random, perform intervention in the SCM described in Eq. 103 and observed subsequent outcomes.

In this experiment, we set hyperparameters and . Fig. 9(d) shows samples drawn from the posterior distribution of . The analysis reveals that our proposed approach is able to achived an effective bound that contain the actual counterfactual probability . The credible interval (ci) is equal to .

C.2 The Effect of Sample Size and Prior Distributions

We will evaluate our algorithms using skewed prior distributions. We found that increasing the size of observational samples was able to wash away the bias introduced by prior distributions. That is, despite the influence of prior distributions, our algorithms eventually converge to sharp bounds over unknown counterfactual probabilities as the number of observational sample grows (to infinite).

Experiment 9: Frontdoor