High-dimensional inference for dynamic treatment effects

Abstract

Estimating dynamic treatment effects is a crucial endeavor in causal inference, particularly when confronted with high-dimensional confounders. Doubly robust (DR) approaches have emerged as promising tools for estimating treatment effects due to their flexibility. However, we showcase that the traditional DR approaches that only focus on the DR representation of the expected outcomes may fall short of delivering optimal results. In this paper, we propose a novel DR representation for intermediate conditional outcome models that leads to superior robustness guarantees. The proposed method achieves consistency even with high-dimensional confounders, as long as at least one nuisance function is appropriately parametrized for each exposure time and treatment path. Our results represent a significant step forward as they provide new robustness guarantees. The key to achieving these results is our new DR representation, which offers superior inferential performance while requiring weaker assumptions. Lastly, we confirm our findings in practice through simulations and a real data application.

keywords:

[class=MSC2020]keywords:

pinkpantonePANTONE 17 1926 TCX RGB[RGB]207 92 120 \definespotcolorgreenpantonePANTONE 16 4728 TPX RGB[RGB]0 164 180 \definespotcolorbluepantonePANTONE 19 4151 TPX RGB[RGB]0 192 259 \startlocaldefs \endlocaldefs

, and

1 Introduction

The complexity of a given disease or economic policy often manifests in the diversity and size of the personal characteristics pertaining to each individual or economy under consideration, causing a considerable degree of heterogeneity in observed outcomes. However, the utility of randomized control trials (RCTs), especially over time, is frequently curtailed by prohibitive costs or ethical concerns. In contrast, the accessibility of time-varying observational studies has burgeoned of late. The ubiquity of data-driven decision-making is evident in various aspects of daily life, such as the continuous monitoring of individuals’ health using mobile devices and consequential medical interventions, tracking of online presence and real-time measurement of economic and social policies implemented to enhance public health. The present study contributes novel insights to the literature by proposing a novel framework to construct confidence intervals pertaining to dynamic treatment effects amid high-dimensional observations. In a Job Corps real-data analysis, our novel framework provides more accurate estimates of the long-term impact of additional schooling over time on wages, which has important practical implications for designing effective policies aimed at increasing educational attainment and improving economic outcomes.

In light of intricate notational complexities, we exemplify our ideas and findings for two-stage trials while affirming that the same theoretical framework and methodology developed are extensible to multiple-stage trials; see, e.g., Section 5. Consider a two-stage series of binary treatment assignments, denoted by and , and an outcome of interest, . Alongside this, a set of possibly high-dimensional sequential pre-treatment covariates and , possibly of different dimensions, are also observed. The potential or counterfactual outcomes, , refer to the outcome that a participant would have experienced had they followed a particular treatment sequence, , which may differ from the treatment they were observed with. Our parameter of interest is the dynamic treatment effect (DTE) between two treatment paths, and , which is defined as follows:

| (1.1) |

Estimating the DTE is a challenging task when there are multiple exposures involved. The influence of past treatments on future confounders and treatment choices complicates the identifiability of (Rosenbaum and Rubin, 1983). Adjusting for confounders may not have a causal interpretation, even when all confounders are measured and the regression is correctly specified (Daniel et al., 2013). In this context, alternative methods such as Sequential Multiple Randomized Control Trials (SMART) (Hernán et al., 2016), Structural Nested Mean (SNM) (Robins, 1997), and Marginal Structural Mean (MSM) models (Murphy et al., 2001) have become the gold standard for addressing these challenges. This paper contributes to the field by establishing robust MSM model estimations with new effective rates.

1.1 The doubly robust representations

Throughout this work, we assume that any treatment-specific variable can only be affected by past treatments or past covariates; and not the future. This is sometimes called temporal ordering. We also assume a “no interference” setting and Assumption 1 below (Robins, 1987, 2000a; Murphy, 2003).

Assumption 1.

(a) (Sequential Ignorability) and where with . (b) (Consistency of potential outcomes) (c) (Overlap) Let be a positive constant, such that and . Here, the propensity scores are defined as and .

The following lemma provides a doubly robust (DR) representation of . This result is consistent with previous studies in the literature, including works by van der Laan and Gruber (2012); Orellana, Rotnitzky and Robins (2010); Murphy et al. (2001); Bang and Robins (2005). We consider the MSM models where we adjust for confounding variables that may affect both the treatment assignment and the outcome of interest. In an MSM, the treatment assignment and the outcome of interest are modeled separately using propensity scores and together with the first-time and second-time conditional means, and . Throughout this work, we use and as well as and to refer to the working models, i.e., the population-level approximations of the propensity scores and conditional means, respectively.

Lemma 1 (A DR representation of ).

Let Assumption 1 hold. Suppose that at least one of and is correctly specified, and at least one of and is correctly specified, i.e, (a) either or , but not necessarily both and (b) either or , but not necessarily both. Then

| (1.2) |

Based on Lemma 1, consistent estimates of are expected as long as at least one nuisance model is correctly parametrized at each exposure time. However, this goal has not been achieved yet; see Babino, Rotnitzky and Robins (2019) for an overview. The main obstacle is the estimation of interlocking nuisance functions, especially the first-time conditional mean, as it cannot be identified directly through the observable variables as . Under Assumption 1, existing DTE literature typically considers the following nested representation of ,

| (1.3) |

and suggests a nested regression (NR) of the conditional means – as long as an estimate of is obtained, one can use as the imputed outcomes and perform regression to construct ; see, e.g., Murphy et al. (2001). We formalize these properties under high-dimensional linear working models, naming the resulting DTE estimator the “dynamic treatment Lasso” (DTL) estimator. We show that the nested-regression approach faces certain limitations and fails to attain the DR property equivalent to Lemma 1. Among the multiple factors contributing to this, the biggest one is arising from a peculiar model misspecification that we identified arising from the nested representation in Equation (1.3). In the event of a misspecified linear working model , the corresponding will inevitably be misspecified as well, leading to , even when is itself linear. Besides the linearity of , additional conditions on are necessary for the correctness of the nested-regression-based linear working model, as discussed in Section 2.3.

This issue necessitates the use of specialized methods for which we propose a new DR representation of the first-time conditional mean function ; see (1.4) below. It provides tools to quantify the DR property of the resulting DTE estimate and to develop correction techniques that can mitigate the DR gap by achieving the estimation under model conditions equivalent to Lemma 1.

Theorem 1 (A DR representation of ).

Suppose that either or holds. Let Assumption 1 holds. Then, for any ,

| (1.4) |

Utilizing the two DR representations (1.2) and (1.4) simultaneously, we propose a sequential doubly robust Lasso (S-DRL) estimator. The proposed estimator is consistent as long as either the conditional mean function is truly linear or the propensity score function is truly logistic (or both) for each exposure time. To the best of our knowledge, this is the first estimator that matches Lemma 1 conditions empirically. The inverse probability weighting (IPW) methods (Robins, 1986, 2000a; Hernán, Brumback and Robins, 2001; Robins, 2004) require all the propensity score models to be correctly parametrized. The covariate balancing methods (Kallus and Santacatterina, 2021; Yiu and Su, 2018; Viviano and Bradic, 2021) require all the conditional mean models to be correctly parametrized. Perhaps unexpectedly, the standard low-dimensional DR methods (Robins, 2000b; Murphy et al., 2001; Bang and Robins, 2005; Yu and van der Laan, 2006) and the targeted maximum likelihood estimation (TMLE) (van der Laan and Gruber, 2012) require either all the propensity score functions or all the conditional mean (or density) functions to be correctly parametrized. The “multiply robust” (MR) estimator of Babino, Rotnitzky and Robins (2019) reaches better robustness than all of the aforementioned methods. In general -stage trials, they allow for the first conditional mean models and the last propensity score models to be correctly parametrized for any . The DTL estimator allows the first propensity score models and the last conditional mean models to be correctly parametrized. Our S-DRL estimator is strictly more robust in terms of consistency; see Table 1.1 and Remark 1 for further details.

| Nuisance models | Consistency | ||||||

| logistic | logistic | linear | linear | S-DRL | DTL | MR | |

| ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | |

| ✗ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | |

| ✓ | ✗ | ✓ | ✓ | ✓ | ✓ | ✓ | |

| ✓ | ✓ | ✗ | ✓ | ✓ | ✓ | ✓ | |

| ✓ | ✓ | ✓ | ✗ | ✓ | ✓ | ✓ | |

| ✗ | ✗ | ✓ | ✓ | ✓ | ✓ | ✓ | |

| ✗ | ✓ | ✗ | ✓ | ✓ | ✓ | ✗ | |

| ✓ | ✗ | ✓ | ✗ | ✓ | ✗ | ✓ | |

| ✓ | ✓ | ✗ | ✗ | ✓ | ✓ | ✓ | |

The S-DRL estimator demonstrates superior estimation rates in high-dimensional contexts when compared to the DTL estimator; see Table 3.1 as well as Remark 5. Root-sample-size inference based on the S-DRL estimator is guaranteed when two product-sparsity conditions are satisfied, whereas the DTL method requires three product-sparsity conditions, as demonstrated in Theorems 3 and 5. The errors in nuisance estimation at different stages have a parallel effect on the estimation; see the consistency rate in Theorem 6.

The estimation of the in-between outcome models is intrinsically linked to regression with imputed outcomes. We have developed a novel cone-set analysis of imputed Lasso estimates that is of independent interest to other imputed, high-dimensional regressions. Existing Lasso proof techniques provide conservative bounds only; see Section 4. Our results are adaptive to the imputation error and can be used to guide the selection of tuning parameters in high-dimensional regression models with imputed outcomes.

In the multi-stage exposure setting, we extend our method and develop DR representations to identify both the expected potential outcomes and conditional means, as shown in Section 5. While the consistency rate and asymptotic normality require intricate proofs, we anticipate they hold analogously to those in the two-stage case. It is worth noting that Theorem 11 provides new DR representations that are independent of any specific parametric models, allowing the sequential doubly robust (S-DR) method to be utilized with non-parametric nuisance estimates, which enhances its versatility.

1.2 Organization of the paper

In Section 2, we introduce the DR estimators of the DTE, including the proposed S-DRL estimator, the DTL estimator, and a general DR estimator. The theoretical properties of the considered DTE estimators are established in Section 3. In Section 4, we formalize the supporting theoretical discoveries, including a general theory for imputed Lasso estimation and the consistency results of the nuisance estimates. We further extend our setting to the case of multi-stage treatments and provide general DR representations for the intermediate conditional means in Section 5. Section 6 presents numerical results, including simulation studies and an application to the National Job Corps Study. Further discussion is provided in Section 7.

1.3 Notation

For any , let denote the function given by , . Then the -Orlicz norm of a random variable is defined as Two special cases of finite Orlicz norm are given by and , which correspond to sub-Gaussian and sub-exponential random variables, respectively. The notation denotes , and denotes as . The notation denotes for all and with constants . Define as the logistic function and as the corresponding link function throughout.

2 The doubly robust estimators

We observe a collection of independent and identically distributed (i.i.d.) samples , drawn from the same distribution as . In the following subsections, we present three DTE estimators: the new sequential doubly robust Lasso (S-DRL) estimator, the dynamic treatment Lasso (DTL) estimator, and the general DR estimator.

2.1 The sequential doubly robust Lasso (S-DRL) estimator

We focus on the high-dimensional scenario, and consider linear (working) models for the conditional means and , along with logistic (working) models for the propensities and . The population minimizer approximating is defined as with , whereas that of approximating is with . Here

| (2.1) | ||||

| (2.2) |

One can also consider a feature map (e.g., a polynomial basis) and a working model with some defined correspondingly. We focus on , although the results apply more broadly. The above working models can be estimated with many regularizations. Throughout this work, we focus on the -regularization, albeit the theoretical developments apply more broadly. With a subset of training data , where , we define

| (2.3) |

| (2.4) |

with tuning parameters . Observe that for , we utilize all of the observations regardless of its treatment path, whereas for , only those whose treatment path matches regardless of what is. The best linear working model for the second-time conditional mean is denoted as

| (2.5) |

An estimator of (2.5) can be obtained similarly with :

| (2.6) |

| (2.7) |

| (2.8) |

Estimation of the first-time conditional mean

Recall that and are defined in Equations (2.2) and (2.5), respectively. We propose the following DR imputed outcome

With this in mind, we consider a linear working model for the first-time conditional mean

| (2.9) |

To estimate the best linear slope based on a subset of training data , we consider an additional sample splitting with , where and are disjoint subsets of . Using the first half of the subsamples , we first obtain the second-time nuisance estimates and as (2.4) and (2.6), respectively. Then, for each , we construct a DR imputed outcome

| (2.10) |

Based on the DR imputed outcomes , we propose a DR estimate:

| (2.11) |

where . To regain full sample size efficiency, we can always swap the samples and , repeat the procedure, and average the results.

The S-DRL estimator of the DTE

For each and for any , define the DR score function based on the DR representation (1.2):

| (2.12) |

We propose the sequential doubly robust Lasso (S-DRL) estimator of :

where are the nuisance estimates of (2.6), (2.11), (2.3), and (2.4), respectively. A cross-fitting technique is used. The details are provided in Algorithm 1; see Chernozhukov et al. (2018); Smucler, Rotnitzky and Robins (2019) where the cross-fitting leads to weaker sparsity restrictions than those without it, such as Farrell (2015); Tan (2020).

2.2 The dynamic treatment Lasso (DTL) estimator

| (2.13) |

In this section, we formally define a dynamic treatment Lasso (DTL) estimator based on the DR score (1.2) of and the nested representation (1.3) of . Here, -regularized nuisance estimates , , and will be the same as before; see (2.3), (2.4), and (2.6) above. Estimation of the first-time conditional mean model is different. Based on the best linear approximation , (2.5), of , we introduce the following nested “best linear working model”:

| (2.14) |

Note that the two linear working models and are not necessarily the same; see Section 2.3 for detailed comparisons. We consider the following imputed Lasso estimate of , defined as with

| (2.15) |

Now we introduce the dynamic treatment Lasso (DTL) estimator of :

where is defined in (2.12) and are the nuisance estimates as in (2.6), (2.15), (2.3), and (2.4), respectively; see Algorithm 2 for details.

2.3 Comparisons between the first-time working models and

In the dynamic treatment setting, the relationship between the linear conditional mean function, , and its corresponding approximations, and , obtained via different identification strategies, is not straightforward. Specifically, a linear is only a necessary condition for correctly specified linear working models; it does not guarantee equality. Additional conditions are required to ensure that and . In the following, we will discuss these necessary conditions in detail.

The working model

The proposed S-DRL approach utilizes the following identification . This representation remains valid for a linear as long as either is truly logistic or is truly linear and not necessarily both. In this case, we also have the following equivalent expressions of :

That is, satisfies . Hence, whenever (a) is a linear function and (b) either is a logistic function or is a linear function. It is worth noting that Condition (b) is already a prerequisite for the identification of DTE, as stated in Lemma 1. Consequently, there is no need to introduce any other conditions beyond those outlined in Condition (a).

The working model

The DTL estimator relies on the nested-regression identification for which Conditions (a) and (b) above are insufficient for ; see Example 1 below. Additional conditions are needed. For instance, if we further assume the following:

-

(c)

Under the treatment groups and , the best linear slopes are the same while regressing on , i.e., , with defined in (2.5) and

One sufficient but not necessary condition for (c) is that the second-time conditional mean function is also linear; see further justifications in Section A of Supplementary Materials (Bradic, Ji and Zhang, 2023).

The misspecification errors of and

Now we consider the case where is possibly non-linear and compare the misspecification (approximation) errors of the linear working models and . As long as Condition (b) above holds, we have

Hence, we have the following conclusions. (1) When is linear, , and both of them are the best linear approximations of the true conditional mean among the group , i.e., . (2) When is non-linear and is logistic, and in general. If Assumption 3 holds, the strict inequality above holds in that as long as . That is, the nested “best linear approximation”, , is in general sub-optimal. If we further consider the case where is linear, then we have and possibly ; see also an illustration in Example 1 below.

Example 1 (A misspecified linear model when the truth is indeed linear).

In what follows, we turn our attention to the nested-regression approach and offer an illustrative example that demonstrates how for a linear , a logistic , a non-linear , and a non-logistic . To facilitate our discussion, we consider the case where both and are one-dimensional covariates with supports in . We assume follows a uniform distribution on , and consider an independent that follows a Bernoulli distribution with a probability of success . We further assume

It is not difficult to verify that and , where . Notably, the nested-regression approach based on a linear working model is misspecified, even though the true conditional mean is linear. Furthermore, because both the first-time conditional mean and propensity score models are misspecified, the DR representation of in Equation (1.2) is no longer valid when the nested-regression-based working model is considered. However, since the second-time propensity score is truly logistic, the S-DRL approach leads to and the incidental validity of the DR representation of through Equation (1.2).

2.4 The general DR DTE estimator

In this section, we present a general doubly robust (DR) estimator of the DTE. We assume that we have access to estimators , , , and of , , , and , respectively. The functions , , and can be directly estimated using observable variables, while the remaining nuisance function can be identified using either the proposed DR representation (1.4) or the usual nested representation (1.3). We consider flexible estimation strategies for all nuisance functions, including both parametric and non-parametric methods. Using the DR representation of given by (1.2), we propose a general DR estimator of the DTE through a cross-fitting procedure. For any , randomly split into equal-sized parts with . For the sake of simplicity, we consider as an integer. Based on the training samples , construct , , , and as estimates of the nuisance functions , , , and , respectively. For each , let

| (2.16) |

The general DR DTE estimator and the corresponding variance estimate are then defined with and as

| (2.17) |

3 Asymptotic properties

Here we establish consistency and asymptotic normality of the S-DRL, DTL, and the general DR estimator.

3.1 Properties of the S-DRL estimator

We use , , , and to denote sparsity levels of the nuisance parameters as defined in (2.5) , (2.9), (2.1) and (2.2), respectively. The number of covariates, and , are possibly much larger than ; for simplicity, we consider .

Assumption 2.

Define , and let , . Suppose that there exist positive constants and , such that and are sub-Gaussian, with , , and

| (3.1) |

where is defined in (2.12) and .

Assumption 3.

Let be a sub-Gaussian vector such that for and . Let for any , with .

Assumptions 2 and 3 are fairly general even among the high-dimensional literature. As , we allow -norm bounds of and to diverge or to shrink to zero. When all the nuisance models are correctly specified, under the overlap condition in Assumption 1, where denotes the centered conditional effect at the first exposure. A sufficient condition for Assumption 2 is i.e., the “normalized” residuals have constant -norms. Note that, we allow to be dependent on while assuming and to be constants independent of ; and are both allowed as . The following Assumption 4 is an overlap condition for the working propensity score models, which is additionally required only when model misspecification occurs.

Assumption 4.

Let and be such that for a fixed constant .

The following theorem characterizes the consistency rate of the S-DRL estimator of .

Theorem 2 (Consistency of the S-DRL).

Suppose that at least one of and is correctly specified, and at least one of the models and is correctly specified. Let Assumptions 1-4 hold. Assume that , and either (a) almost surely, with a constant , or (b) . Then the sequential DR Lasso (S-DRL) estimator, , as defined in Algorithm 1, satisfies

as , with and

We categorize bounded and unbounded covariate support and add a restriction to for the latter. The DR imputed outcome (2.10) has an unbounded -Orlicz norm for any . Yet, if has bounded support, no extra sparsity condition is required as the inverse probability weighting is stable and the DR imputation has a well-behaved tail distribution.

Remark 1 (Comparison with low-dimensional DR DTE estimators).

Lewis and Syrgkanis (2021) applied debiased machine learning and g-estimation techniques in the framework of SNM models. However, the “blip functions” and – which are defined as and , respectively – are considered low-dimensional and correctly specified for consistent estimation. MSM models with low-dimensional confounders have been studied extensively, with significant theoretical advancements made in the seminal work of Tchetgen and Shpitser (2012). Additionally, Robins (2000b), Murphy et al. (2001), Bang and Robins (2005), and Yu and van der Laan (2006) explored DR DTE estimation with low-dimensional nuisances, proposing consistent and asymptotically normal DTE estimators given that either (a) all conditional mean models are correctly parametrized or (b) all propensity score models are correctly parametrized. More recently, Babino, Rotnitzky and Robins (2019) proposed a multiple robust (MR) estimator that allows for an additional model misspecification scenario (c), where only the first-time conditional mean model and second-time propensity score model are correctly parametrized. However, all of the aforementioned approaches require low-dimensional, parametric nuisance estimates that are root- consistent.

Our proposed method accommodates high-dimensional and possibly non-parametric nuisance estimates, which may not necessarily be root- consistent. This approach allows for a consistent estimate of the DTE even in challenging scenarios where only the second-time conditional mean and first-time propensity score models are correctly specified (misspecification scenario (d)). This scenario is more common in practice due to the difficulty of identifying the first-time conditional mean model. When is linear, as per (1.3), a linear would require to be linear in – an unlikely scenario if any of the are binary or discrete.

When all the nuisance models are correctly specified, we further establish asymptotic normality results and the corresponding rate DR property of the S-DRL estimator.

Theorem 3 (Asymptotic normality of the S-DRL).

Suppose that all the nuisance models , , , and are correctly specified. Let Assumptions 1-3 hold. Assume that , and either (a) almost surely, with some constant , or (b) . Additionally, assume the following product-rate condition:

| (3.2) |

Then, with in (3.1) and in (2.8), the S-DRL estimator satisfies and as .

Theorem 3, as per Bang and Robins (2005), indicates that the S-DRL estimator achieves the semiparametric efficiency bound when all nuisance models are correctly specified.

Remark 2 (Comparison with static ATE estimators).

We compare sparsity conditions in Theorem 3 with the literature on estimating ATE through DR for a single exposure. The ATE can be seen as a special case of the DTE where we assume that and are completely random. This allows root- estimation of and . Consequently, Theorem 3 requires and , which are less restrictive than Farrell (2015); Tan (2020); Dukes and Vansteelandt (2021); Dukes, Avagyan and Vansteelandt (2020); Avagyan and Vansteelandt (2021) and are aligned with Chernozhukov et al. (2018); Smucler, Rotnitzky and Robins (2019).

3.2 Properties of the DTL estimator

With slight abuse of notation, let .

Theorem 4 (Consistency of the DTL).

Theorem 5 (Asymptotic normality of the DTL).

Remark 3 (Comparisons between the S-DRL and DTL estimators).

Consistency. Theorems 2 and 4 establish the consistency of two distinct estimators, S-DRL and DTL. While both estimators necessitate correct specification of at least one of and , their requirements on and differ due to their distinct conditional mean models. Specifically, S-DRL mandates either or , which can be guaranteed by the linearity of or the logistic form of . In contrast, DTL imposes the stricter condition of either or , which may not be fulfilled even when is linear, as discussed in Section 2.3. For a comprehensive summary, see Table 1.1.

Rate of estimation. Different rate of estimation of S-DRL and DTL are presented in Table 3.1. Table 3.1 reveals a symmetrical pattern in the rates of S-DRL, whereas DTL exhibits an asymmetric behavior – the sparsity levels and appear to be more influential than and . When either or are misspecified, there is no difference in the rates. However, when they are both correctly specified, the rate of DTL contains additional terms that involve the sparsity level (and under certain circumstances). Notably, if is relatively large, S-DRL exhibits a faster consistency rate than DTL.

Asymptotic normality. The S-DRL and DTL estimators are both asymptotically normal, as proven in Theorems 3 and 5. When , their asymptotic efficiency is the same. However, they require different sparsity conditions. The DTL estimator requires three product-sparsity conditions, specifically: (a) the first-time conditional mean and first-time propensity score , (b) the second-time conditional mean and second-time propensity score , and (c) the second-time conditional mean and first-time propensity score , which are given in equation (3.4). On the other hand, the S-DRL estimator only requires two product-sparsity conditions, as defined in (3.2). These correspond to (a) and (b) above, with (c) becoming irrelevant. The S-DRL estimator is known as (sequential) rate DR because it is asymptotically normal when the product-sparsity of the nuisance parameters is for each exposure time; see more details in Remark 2.

[b] Correctly specified models Consistency rate of Consistency rate of ✓ ✓ ✓ ✓ LHS ✗ ✓ ✓ ✓ LHS ✓ ✗ ✓ ✓ ✓ ✓ ✗ ✓ LHS ✓ ✓ ✓ ✗ LHS∗ ✗ ✗ ✓ ✓ LHS ✗ ✓ ✗ ✓ LHS ✓ ✗ ✓ ✗ LHS∗∗ ✓ ✓ ✗ ✗ LHS

3.3 Properties of the general DR estimator

In this section, we provide a new consistency result of the general DR DTE estimator. Here we consider arbitrary working models , , , and , which may not follow the logistic or linear forms as before. For each , define the corresponding DR score function as

| (3.5) |

with

| (3.6) |

Assumption 5.

For positive sequences , , , and , let and Moreover, for , and with probability approaching one. For and defined in Assumption 2, , , , , and , for constants and .

The probability measures and corresponding expectations above are with respect to a fresh draw (or ). Note that Assumption 5 allows for to differ from while requiring a overlap condition consistent with the existing literature; see, e.g., Chernozhukov et al. (2018). The condition, satisfied by sub-Gaussian random variables, controls the tails of , , and . The last two conditions of Assumption 5 aim to ensure the interpretability of the results by bounding the “normalized” conditional second moments.

Theorem 6.

The aforementioned theorem yields two distinct conclusions that warrant discussion. The first pertains to the conditions that are necessary for achieving root- consistency, while the second relates to the issue of consistency under model misspecification. If all the models are correctly specified, and root- consistency happens as long as and .

If, on the other hand, at least one of the nuisance models is correctly specified at each exposure time, is a consistent estimator as long as . Model misspecification can take an asymmetric form in terms of estimation rates. Specifically, while is symmetric in the rates themselves, the dependence of on and/or can introduce potential asymmetries. For example, when performing -regularized nested regression, Theorem 10 indicates that depends additively on as , where is the estimation error of when is known. As a result, the consistency rate of includes an additional term , as illustrated by the DTL estimator in (3.3).

On the other hand, if we consider a new DR approach based on the DR representation (1.4) to estimate , the corresponding will depend on both and . For instance, when all the nuisance models are correctly specified, Theorem 9 indicates that -regularized DR estimation leads to a symmetric rate with , resulting in if and . The approach used to estimate the first-time conditional mean determines the persistence of the symmetry.

Theorem 7.

(Asymptotic normality of the general DR estimator) Suppose that all the nuisance models , , , and are correctly specified. Whenever Assumptions 1, 5 hold and the rates of estimation satisfy the following product conditions

| (3.7) |

then the estimator satisfies and as (and potentially ), where and are defined in (3.6) and (2.17), respectively.

Remark 4 (Rate double robustness).

The topic of rate double robustness in the presence of multiple exposures has been addressed in Bodory, Huber and Lafférs (2022), but the authors require three product-rate conditions, including as stated in their Assumption 3.1, in addition to the two product-rates (3.7). As a result, this does not allow for relatively large values of and , which is permissible in our setting. For example, consider a special case where is completely random and is a constant function. In conjunction with the sequential ignorability condition of Assumption 1, we have , allowing to be identified directly through observable variables. In this scenario, both and can be estimated with a root- rate. Therefore, Theorem 7 only requires , i.e., and are consistently estimated. In comparison, Bodory, Huber and Lafférs (2022) additionally require , which may not be feasible when and are only known to be Lipschitz continuous, and the covariate dimensions satisfy .

Our proof relies on a nuanced decomposition of the second-order estimation bias resulting from the estimation errors of and . Leveraging the Neyman orthogonality of the DR score (E.2), we reformulate the second-order bias as the product . In our analysis, we then examine this product collectively rather than as separate terms, resulting in a cohesive flow of the arguments. We show that the population effect of this term is exactly zero whenever the model is correctly specified – a condition fullfilled when discussing asymptotic normality in high-dimensional regimes. We then showcase that the sample equivalent is negligible and does not contribute to the estimation error.

4 Supporting theoretical discoveries

This section presents supplementary findings that, while not the primary focus of the research, may nonetheless be informative or valuable.

4.1 An adaptive theory for imputed Lasso with high-dimensional covariates

Let be i.i.d. observations and let be an independent copy with and . Suppose that there exists, possibly random, . Note that for some, and possibly all observations, outcomes are imputed, i.e., estimated using . The true population slope is defined as Then its estimator is

| (4.1) |

for . The following result delineates properties of such imputed-Lasso estimator, .

Theorem 8 (General imputed Lasso estimators).

Let and . Suppose that for , , and with and potentially dependent on . For some , define the event For any , let . Then on the event , when we have

with probability at least , where are constants independent of and . Moreover, if , , and , then with , as ,

| (4.2) |

The above result is of independent interests as it provides a general theory for any Lasso estimators based on imputed outcomes. It contributes to the literature in three specific aspects: (a) The “imputation error”, , can be dependent on and even possibly correlated with covariates ; (b) We allow every to be fitted using the same set of observations , i.e., s are also possibly dependent on each other; and (c) The tuning parameter is of the same order as the one chosen for the fully observed data and is independent of the imputation error or any sparsity parameter.

Compared with the existing literature, Theorem 8 requires weaker sparsity assumptions and provides better rates of estimation. Imputed Lasso of Zhu, Zeng and Song (2019) requires , , and . That of Lewis and Syrgkanis (2021) requires an ultra-sparse setup and . In contrast, we only require and . Additionally, Zhu, Zeng and Song (2019) choose a tuning parameter and provide upon requiring strict conditions for assuring model selection consistency; see Theorem 2 therein. Lewis and Syrgkanis (2021) take and establish ; see Theorem 13 therein. In contrast, we allow . The imputation error only appears in our final estimation rate (4.2) additively, and its effect does not explode as the sparsity level grows.

Theorem 8 requires development of new proof techniques: the standard Lasso inequality followed by the cone-set reduction are not valid in this instance. In fact, the error, , no longer belongs to the accustomed cone set, . Instead, we identify a new set, , and show that the error vector belongs to the union of the above two sets. This enables us to avoid choosing a tuning parameter dependent on the imputation error, as is done in the above literature. Moreover, our results are adaptive to the imputation error in that when there is no imputation, i.e., , our result reaches the standard consistency rate in the high-dimensional statistics literature, e.g., Bickel, Ritov and Tsybakov (2009); Negahban et al. (2012); Wainwright (2019).

4.2 Theoretical characteristics of nuisance estimators with imputed outcomes

As a result of constraints on the length of the main file, we have included the theoretical properties of the nuisance estimates , , and as defined by equations (2.6), (2.3), and (2.4) respectively, in the Supplementary Materials (Bradic, Ji and Zhang, 2023) where we show , , and . Now we establish the properties of the first-time conditional mean model estimates, where imputation is required. We first consider the DR-imputation-based estimator defined as (2.7) and the corresponding conditional mean estimate .

Theorem 9.

Theorem 9 elucidates that the consistency rate of is subject to the fidelity of the second-time nuisance models and More specifically, when both models are accurately specified, the DR imputation error contributes multiplicatively to the consistency rate in Theorem 9(a). In contrast, when only one of and is correctly specified, the estimation error of the correctly specified model contributes additively to the rates presented in Theorem 9(b) and Theorem 9(c). It is noteworthy that these results do not rely on the correctness of the first-time conditional mean model per se.

In the following, we also provide the consistency results of the nested-regression-based estimator, , defined in Equation (2.15), and the corresponding conditional mean estimate .

Theorem 10.

Remark 5 (Comparison between and ).

The present remark compares the consistency rates of two estimators, and , in different scenarios. (a) In the case where is nonlinear and is logistic, estimators converge to distinct targets, and , respectively. Here, represents the optimal linear slope approximating the true conditional mean function , while is the optimal linear slope approximating the misspecified model ; see discussions in Section 2.3 above. When the first-time conditional mean is linear, converges to the true linear slope, and a consistent estimate of is obtained. However, typically converges to some that differs from the true linear slope, resulting in an inconsistent estimate of . (b) When is linear and is logistic, . However, in this case, exhibits a faster consistency rate than . This can be attributed to the fact that the DR imputation error contributes to the consistency rate of in a product form Theorem 9(a), while the imputation error from nested regression contributes in an additive form Theorem 9(c), which then dominates if . Consequently, the S-DRL estimator constructed based on has a faster convergence rate than the DTL estimator, which is constructed based on ; see Table 3.1. The enhanced convergence rate exhibited by the S-DRL estimator implies a reduction in the requisite level of sparsity conditions necessary for the inferential guarantees. (c) In the scenario where is linear and is non-logistic, the targets and are identical and and have the same consistency rates, as seen in Theorem 9(c) and (4.3).

In general, can be seen as a conditional average treatment effect (CATE) parameter through the well established nested representation (1.3). Outside of dynamic settings, DR approaches for CATE estimation typically rely on DR influence function representation of the conditional means. When those conditional means independently are not smooth enough, Kennedy (2020) proposes to instead use DR imputations for the joint estimation of the difference of the conditional means. Here, the nested structure of , where the true outcome is never observed, prevents direct influence function approaches. Instead, our approach leverages cases when has sparser structure than .

5 Advancing multi-stage treatment estimation with DR methods

The objective of this section is to expand upon the methodology of sequential doubly robust estimation by considering its application in multi-stage settings. Consider exposure times and suppose that we observe i.i.d. samples . Let be an independent copy of . For each , let and denote the covariate vector and the treatment assignment at the -th exposure time, respectively. Let denote the observed outcome variable at the final stage. Denote and for any . Let be the counterfactual outcome corresponding to the treatment path . The DTE between any treatment paths is now defined as

We define the conditional mean and propensity score functions as

| (5.1) | ||||

| (5.2) |

where for the sake of simplicity, we denote with and . For each , we denote and as the working models for the conditional mean and propensity score, respectively. Additionally, with , we set and . Note that, under the Assumption 6(b) below, we have . To identify for any , we assume a multi-stage version of Assumption 1 in the following; see also, e.g., Murphy (2003); Robins (2000a, 1987).

Assumption 6.

(a) (Sequential Ignorability) for each . (b) (Consistency of potential outcomes) (c) (Overlap) Let be a positive constant, such that for each .

The following proposition presents a well-known DR representation of under the multi-stage dynamic setting; see, e.g., Bang and Robins (2005); Murphy et al. (2001).

Proposition 1.

Let Assumption 6 hold. For suppose that at least one of and is correctly specified, i.e., either or . Then

| (5.3) |

According to Proposition 1, a consistent estimate of should be achievable as long as we can consistently estimate at least one of the nuisance functions or for each exposure time . In the present context, the propensity score functions of (5.2) are identifiable via observable variables. Additionally, by Assumption 6, , thereby facilitating its estimation using the corresponding samples. However, the remaining conditional mean functions for stages cannot be identified directly. To address this challenge, we propose DR representations of these intermediate conditional means, as an alternative to the conventional nested representation of (5.4).

Theorem 11.

Let Assumption 6 hold. For and , suppose that either or is correctly specified, i.e., either or . Then , where

Theorem 11 can be regarded as an overarching, comprehensive, umbrella result that subsumes a range of components, particularly encompassing Proposition 1 as a specific case when . Indeed, is a conditional mean function at “stage zero”. Theorem 11 indicates that can be identified through a DR representation using all the conditional means and propensity scores at later stages. Therefore, can be estimated sequentially backward in time based on the DR imputations.

For example, if we use linear working models for the conditional means and logistic models for the propensity scores, and either the true conditional mean is linear or the true propensity score is logistic at each later stage , we can get a consistent estimate of the using DR imputed linear regression. By repeating this process backwards, we conclude that if either the conditional means or propensity scores are correctly parametrized at every stage , we can estimate all nuisance functions consistently, leading to a consistent estimate of . An alternative approach to our proposed sequential doubly robust method is the nested estimator (Murphy et al., 2001). This approach represents all conditional means using the following equation:

| (5.4) |

However, in order to ensure the consistency of the nested estimator for , it is essential that all subsequent conditional mean functions exhibit true linearity. Interestingly, even the multiply robust approach presented by Babino, Rotnitzky and Robins (2019) falls short in achieving the same level of robustness as the S-DRL method. Further insights can be found in the comments following Theorem 1 and Table 1.1. Our method demonstrates a growing advantage as the number of exposure times increases. For instance, in the case of exposure times, consider all the cases including correctly or incorrectly parametrized and for each , our method enables out of possible cases. In contrast, the nested-regression-based and multiply robust approaches only allow for cases. This conclusion is independent of the particular parametrization used – nonparametric, smooth models are permissible – and extends to the difference of means as well.

6 Numerical Experiments

6.1 Simulation studies

We illustrate the finite sample properties of the introduced estimators in several simulated experiments; auxiliary settings are relegated to Section C of the Supplementary Material (Bradic, Ji and Zhang, 2023). We consider and , and use as well as . Below we use and . We decompose into two components as and consider and unless specified differently. For each , and .

M1: Correctly parametrized models

Consider and , with . Let , , and

The outcomes are with parameters and .

M2: Weakly sparse and dense

Let and

Define and let . Let . The parameter and , .

M3: Non-linear and non-logistic

Consider . Let , where

Define and . Let and . The parameter has the same as M2 and . The parameter and . Let

For M1, and ; for M2, , are chosen from , , and ; for M3, , are chosen from , , , , , and . We replicate settings 500 times. We report S-DRL as well as a version S-DRL’, which has constructed with and build on the whole sub-sample . We also present (a) DTL, Algorithm 2, (b) IPW with -regularized logistic PS, (c) an empirical difference estimator (empdiff), , and (d) an oracle DR estimator constructed with the true nuisances. All methods use -fold cross validation for selection of tuning parameters.

| Method | Bias | RMSE | Length | Coverage | ESD | ASD | ||

| empdiff | 0.734 | 0.734 | 0.274 | 0.004 | 0.234 | 0.070 | NA | NA |

| oracle | 0.003 | 0.220 | 1.091 | 0.954 | 0.325 | 0.278 | 0.000 | 0.000 |

| IPW | 0.864 | 0.865 | 1.342 | 0.346 | 0.319 | 0.342 | NA | NA |

| DTL | 0.124 | 0.189 | 0.876 | 0.894 | 0.264 | 0.223 | 0.141 | 0.216 |

| S-DRL | 0.131 | 0.202 | 0.880 | 0.880 | 0.271 | 0.224 | 0.227 | 0.337 |

| S-DRL’ | 0.126 | 0.188 | 0.876 | 0.894 | 0.259 | 0.223 | 0.135 | 0.193 |

| empdiff | 0.731 | 0.731 | 0.137 | 0.000 | 0.111 | 0.035 | NA | NA |

| oracle | -0.006 | 0.121 | 0.602 | 0.956 | 0.178 | 0.153 | 0.000 | 0.000 |

| IPW | 0.534 | 0.538 | 0.959 | 0.454 | 0.287 | 0.245 | NA | NA |

| DTL | 0.033 | 0.097 | 0.488 | 0.930 | 0.136 | 0.125 | 0.032 | 0.052 |

| S-DRL | 0.031 | 0.098 | 0.489 | 0.930 | 0.142 | 0.125 | 0.050 | 0.070 |

| S-DRL’ | 0.028 | 0.098 | 0.489 | 0.932 | 0.138 | 0.125 | 0.033 | 0.044 |

Tables 6.1 and 6.2 show the estimation and inference results for the DTE estimators, while Table B.3 focuses on estimation performances, as valid inference is unlikely with misspecified models. Our summarized findings, shown in Tables 6.1-B.3, reveal that the naive empirical difference estimator has large biases due to confounding between outcome and treatment assignments. The IPW method also performs poorly, with large biases and RMSEs, and confidence interval coverages far from the desired . The DTL, S-DRL, and S-DRL’ estimators behave similarly in Table 6.1 (under M1), with correctly specified nuisance models and relatively low sparsity levels. The S-DRL method’s additional sample splitting in Algorithm 1 (Steps 5-7) leads to larger estimation errors in the first-time conditional mean estimates than those in the DTL and S-DRL’ methods. Consequently, when , the S-DRL estimator’s RMSE is slightly larger than that of the DTL and S-DRL’ estimators, but they have similar RMSEs when . In terms of inference behaviors, the corresponding confidence interval coverages are below the desired when . However, increasing the total sample size to brings the coverages closer to . Estimating under M2 is more challenging than estimating . As a result, the DR estimates of in the S-DRL and S-DRL’ methods have significantly smaller estimation errors compared to the nested regression used in the DTL method, as shown in Table 6.2, leading to smaller RMSEs and coverages closer to . Moving on to M3, both and are misspecified. Table B.3 shows that the estimation errors of with the S-DRL and S-DRL’ are substantially smaller than those of the DTL. Consequently, we see an improvement of the RMSEs in the S-DRL and S-DRL’ estimators.

| Method | Bias | RMSE | Length | Coverage | ESD | ASD | ||

| oracle | -0.021 | 0.691 | 4.146 | 0.950 | 1.029 | 1.058 | 0.000 | 0.000 |

| empdiff | -0.204 | 0.601 | 1.576 | 0.636 | 0.848 | 0.402 | NA | NA |

| IPW | -0.153 | 2.542 | 12.747 | 0.970 | 3.718 | 3.252 | NA | NA |

| DTL | -0.013 | 0.714 | 4.151 | 0.950 | 1.060 | 1.059 | 0.361 | 0.365 |

| S-DRL | -0.023 | 0.686 | 4.144 | 0.952 | 1.008 | 1.057 | 0.139 | 0.136 |

| S-DRL’ | -0.027 | 0.689 | 4.145 | 0.952 | 1.019 | 1.057 | 0.126 | 0.122 |

| oracle | -0.029 | 0.572 | 2.942 | 0.936 | 0.835 | 0.751 | 0.000 | 0.000 |

| empdiff | -0.099 | 0.408 | 1.116 | 0.630 | 0.598 | 0.285 | NA | NA |

| IPW | -0.101 | 2.510 | 11.928 | 0.978 | 3.643 | 3.043 | NA | NA |

| DTL | -0.053 | 0.569 | 2.950 | 0.934 | 0.843 | 0.753 | 0.163 | 0.161 |

| S-DRL | -0.026 | 0.554 | 2.942 | 0.940 | 0.838 | 0.750 | 0.040 | 0.040 |

| S-DRL’ | -0.029 | 0.560 | 2.942 | 0.940 | 0.843 | 0.751 | 0.040 | 0.042 |

| oracle | -0.030 | 0.608 | 2.990 | 0.948 | 0.893 | 0.763 | 0.000 | 0.000 |

| empdiff | -0.156 | 0.485 | 1.260 | 0.608 | 0.683 | 0.322 | NA | NA |

| IPW | -0.086 | 2.099 | 10.088 | 0.984 | 3.136 | 2.574 | NA | NA |

| DTL | -0.019 | 0.607 | 2.983 | 0.940 | 0.903 | 0.761 | 0.273 | 0.275 |

| S-DRL | -0.013 | 0.565 | 2.988 | 0.948 | 0.854 | 0.762 | 0.082 | 0.083 |

| S-DRL’ | -0.012 | 0.574 | 2.987 | 0.948 | 0.863 | 0.762 | 0.080 | 0.081 |

| Method | Bias | RMSE | Bias | RMSE | |||||

| oracle | 0.013 | 0.119 | 0.000 | 0.000 | 0.007 | 0.098 | 0.000 | 0.000 | |

| empdiff | 0.149 | 0.162 | NA | NA | 0.157 | 0.159 | NA | NA | |

| IPW | -0.035 | 0.465 | NA | NA | -0.164 | 0.493 | NA | NA | |

| DTL | -0.003 | 0.273 | 0.151 | 0.196 | 0.012 | 0.199 | 0.076 | 0.077 | |

| S-DRL | 0.009 | 0.224 | 0.087 | 0.096 | 0.024 | 0.166 | 0.036 | 0.040 | |

| S-DRL’ | -0.007 | 0.207 | 0.067 | 0.074 | 0.016 | 0.170 | 0.031 | 0.033 | |

| oracle | 0.005 | 0.062 | 0.000 | 0.000 | 0.003 | 0.047 | 0.000 | 0.000 | |

| empdiff | 0.142 | 0.142 | NA | NA | 0.142 | 0.142 | NA | NA | |

| IPW | -0.276 | 0.525 | NA | NA | -0.390 | 0.487 | NA | NA | |

| DTL | 0.010 | 0.126 | 0.038 | 0.040 | -0.001 | 0.101 | 0.021 | 0.021 | |

| S-DRL | 0.013 | 0.108 | 0.016 | 0.016 | 0.000 | 0.089 | 0.007 | 0.007 | |

| S-DRL’ | 0.004 | 0.106 | 0.015 | 0.015 | -0.007 | 0.090 | 0.007 | 0.007 | |

| oracle | 0.001 | 0.096 | 0.000 | 0.000 | 0.011 | 0.059 | 0.000 | 0.000 | |

| empdiff | 0.149 | 0.149 | NA | NA | 0.143 | 0.143 | NA | NA | |

| IPW | -0.221 | 0.469 | NA | NA | -0.249 | 0.478 | NA | NA | |

| DTL | -0.028 | 0.212 | 0.090 | 0.091 | 0.010 | 0.135 | 0.048 | 0.049 | |

| S-DRL | -0.012 | 0.160 | 0.037 | 0.039 | 0.011 | 0.113 | 0.016 | 0.016 | |

| S-DRL’ | -0.029 | 0.165 | 0.031 | 0.032 | 0.002 | 0.116 | 0.015 | 0.015 | |

6.2 Application to National Job Corps Study (NJCS)

Job Corps (JC) is the largest and most comprehensive federal job training program in the US for disadvantaged youth between 16 and 24 years old. Each year, about 50,000 participants receive vocational training and academic education at JC centers to improve their job prospects. On average, a JC student spends 8 months at a local center, completing around 1,100 hours of instruction, which is roughly equivalent to one year of high school. For a more detailed description, refer to Schochet, Burghardt and McConnell (2008) and Schochet (2001).

Numerous studies have investigated the effects of Job Corps on wages. Lee (2009) highlighted sample selection issues in their analysis. Zhang, Rubin and Mealli (2008) separated the causal effects of JC enrollment on wages from those on employment. Flores et al. (2012) found that longer exposure to JC training is associated with higher future earnings. Chen and Flores (2015) separated the effects of sample selection from noncompliance, while Huber et al. (2020) distinguished between the causal direct and indirect effects in the presence of mediators. In addition to studying the effects of Job Corps in single-time treatment settings, researchers have also explored the dynamic treatment setting offered by Job Corps. Bodory, Huber and Lafférs (2022) investigated the effects of JC’s educational and training programs and found positive impacts on fourth-year employment compared to no program participation. Meanwhile, Singh, Xu and Gretton (2021) analyzed the total, direct, and indirect dynamic dose response of job training on employment. Their study concluded that a few class hours in the first and second years significantly increase employment in the fourth year. In this section, we will evaluate the effects of sequential job training programs on wages using the S-DRL and DTL methods, as defined in Algorithms 1 and 2.

| Method | SE | CI | p-value | |||||||

| 568 | 315 | DTL | 6.201 | 5.652 | 0.549 | 0.270 | [0.020, 1.078] | 0.042 | ||

| S-DRL | 6.208 | 5.641 | 0.567 | 0.273 | [0.032, 1.102] | 0.037 | ||||

| 568 | 336 | DTL | 6.200 | 5.424 | 0.776 | 0.313 | [0.163, 1.389] | 0.013 | ||

| S-DRL | 6.209 | 5.390 | 0.819 | 0.314 | [0.204, 1.434] | 0.009 | ||||

| 336 | 315 | DTL | 5.410 | 5.639 | -0.229 | 0.335 | [-0.886, 0.428] | 0.493 | ||

| S-DRL | 5.371 | 5.626 | -0.255 | 0.337 | [-0.916, 0.406] | 0.450 |

We analyze a dataset of 11,313 individuals, with 6,828 assigned to the Job Corps and 4,485 not. They are interviewed 1, 2, and 4 years post-randomization. For each year , represents the treatment assignment in the -th year. We assign for non-enrollment, for enrollment without program participation, for high-school-level education, and for vocational training. The baseline covariate vector, , has 909 characteristics, while includes 1,427 characteristics. In total, there are 2,336 covariates. The outcome is the log-transformed wage . We exclude 2,610 individuals with missing treatment stages that are missing completely at random (Schochet et al., 2003) and an additional 133 with missing covariates or outcomes, resulting in a final sample of 8,570 individuals.

Above: within the subgroup ;

Below: within the subgroup .

Above: within the subgroup ;

Below: within the subgroup .

Above: within the subgroup ;

Below: within the subgroup .

Above: within the subgroup ;

Below: within the subgroup .

Above: within the subgroup ;

Below: within the subgroup .

Above: within the subgroup ;

Below: within the subgroup .

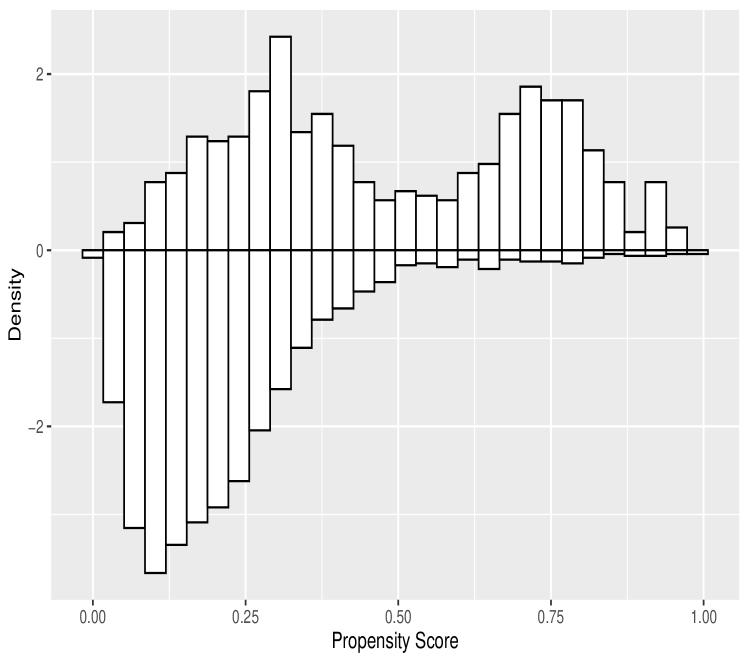

Table 6.4 shows estimated DTEs between treatment paths vs. , vs. , and vs. . Both the S-DRL and DTL methods suggest that vocational training has a positive impact on achieving higher wages by showing non-zero effects between the first two paths. On the other hand, the estimates between paths and are negative, and their corresponding confidence intervals contain zero, making it impossible to determine if academic education is beneficial or detrimental. However, our analysis does suggest that individuals seeking higher-paying jobs would benefit more from vocational training compared to academic education, which only provides high school-level education without any significant vocational training. The S-DRL estimates have a slightly greater distance from zero compared to DTL’s, with similar standard errors, leading to slightly smaller p-values. Figure 1 examines the overlap of estimated propensity scores, displaying mirror histograms of estimated propensity scores within the treatment and control groups. The substantial overlap seen in the mirror histograms indicates that the inverse propensity score weights are relatively stable. Figure 1(d) displays bimodal patterns in the histograms due to a binary confounder variable that significantly influences the propensity score estimate of , with a close association between a participant’s decision to enroll in second-year education and their attendance in the class during the final weeks of the first year.

7 Discussion

This paper aims to enhance the understanding of estimating causal parameters in multi-stage settings. While prior DR literature has recognized the importance of the stage-zero DR representation for the expected potential outcome, it has overlooked the fact that all the intermediate conditional mean functions can also be identified in a DR manner. This approach leads to better theoretical guarantees and greater flexibility in modeling dynamic dependencies, which can be complex and involve multiple time exposures. Furthermore, our findings have significant practical implications beyond parametric models, especially in situations where doctors or policymakers cannot rely on randomized treatments or simplistic treatment rules. With the ability to model dynamic treatment effects using robust principles, new avenues of discovery are emerging, including optimal treatment rules and determining the best treatment times. Our approach also enables the exploration of further important issues, such as mitigating network spillover effects through robustness perspectives and enriching balancing methods with better robustness properties. The significance of our work lies in the fact that it allows researchers to estimate treatment effects in complex settings more accurately and provides a valuable tool for policymakers seeking to make informed decisions based on robust causal inference methods.

8 Acknowledgement

This work was supported in part by NSF awards CNS-1730158, ACI-1540112, ACI-1541349, OAC-1826967, the University of California Office of the President, and the University of California San Diego’s California Institute for Telecommunications and Information Technology/Qualcomm Institute. Jelena Bradic’s work has been supported by the NSF grand DMS-1712481. The majority of this work was done while Yuqian Zhang was with the Department of Mathematics, University of California San Diego.

Supplementary Materials for the “High-dimensional inference for dynamic treatment effects”, Bradic, Ji and Zhang (2023)

This supplementary document contains additional justifications and the proofs of the theoretical results presented in the main document. All the results and notation are numbered and used as in the main text unless stated otherwise. Statements introduced in the Supplementary Materials only are numbered using an alphanumerical scheme. Supplementary Materials includes further discussions on the nuisance models, additional numerical results, Auxiliary Lemmas S.1-S.18 with their proofs used for establishing the main results, Theorems 1-11.

References

- Avagyan and Vansteelandt (2021) {barticle}[author] \bauthor\bsnmAvagyan, \bfnmVahe\binitsV. and \bauthor\bsnmVansteelandt, \bfnmStijn\binitsS. (\byear2021). \btitleHigh-dimensional inference for the average treatment effect under model misspecification using penalized bias-reduced double-robust estimation. \bjournalBiostatistics Epidemiology \bpages1–18. \endbibitem

- Babino, Rotnitzky and Robins (2019) {barticle}[author] \bauthor\bsnmBabino, \bfnmLucia\binitsL., \bauthor\bsnmRotnitzky, \bfnmAndrea\binitsA. and \bauthor\bsnmRobins, \bfnmJames\binitsJ. (\byear2019). \btitleMultiple robust estimation of marginal structural mean models for unconstrained outcomes. \bjournalBiometrics \bvolume75 \bpages90–99. \endbibitem

- Bang and Robins (2005) {barticle}[author] \bauthor\bsnmBang, \bfnmHeejung\binitsH. and \bauthor\bsnmRobins, \bfnmJames M\binitsJ. M. (\byear2005). \btitleDoubly robust estimation in missing data and causal inference models. \bjournalBiometrics \bvolume61 \bpages962–973. \endbibitem

- Bickel, Ritov and Tsybakov (2009) {barticle}[author] \bauthor\bsnmBickel, \bfnmPeter J\binitsP. J., \bauthor\bsnmRitov, \bfnmYa’acov\binitsY. and \bauthor\bsnmTsybakov, \bfnmAlexandre B\binitsA. B. (\byear2009). \btitleSimultaneous analysis of Lasso and Dantzig selector. \bjournalThe Annals of Statistics \bvolume37 \bpages1705–1732. \endbibitem

- Bodory, Huber and Lafférs (2022) {barticle}[author] \bauthor\bsnmBodory, \bfnmHugo\binitsH., \bauthor\bsnmHuber, \bfnmMartin\binitsM. and \bauthor\bsnmLafférs, \bfnmLukáš\binitsL. (\byear2022). \btitleEvaluating (weighted) dynamic treatment effects by double machine learning. \bjournalThe Econometrics Journal \bvolume25 \bpages628–648. \endbibitem

- Bradic, Ji and Zhang (2023) {barticle}[author] \bauthor\bsnmBradic, \bfnmJelena\binitsJ., \bauthor\bsnmJi, \bfnmWeijie\binitsW. and \bauthor\bsnmZhang, \bfnmYuqian\binitsY. (\byear2023). \btitleSupplement to “High-dimensional inference for dynamic treatment effects”. \endbibitem

- Chakrabortty et al. (2019) {barticle}[author] \bauthor\bsnmChakrabortty, \bfnmAbhishek\binitsA., \bauthor\bsnmLu, \bfnmJiarui\binitsJ., \bauthor\bsnmCai, \bfnmT Tony\binitsT. T. and \bauthor\bsnmLi, \bfnmHongzhe\binitsH. (\byear2019). \btitleHigh Dimensional M-Estimation with Missing Outcomes: A Semi-Parametric Framework. \bjournalarXiv preprint arXiv:1911.11345. \endbibitem

- Chen and Flores (2015) {barticle}[author] \bauthor\bsnmChen, \bfnmXuan\binitsX. and \bauthor\bsnmFlores, \bfnmCarlos A\binitsC. A. (\byear2015). \btitleBounds on treatment effects in the presence of sample selection and noncompliance: the wage effects of job corps. \bjournalJournal of Business & Economic Statistics \bvolume33 \bpages523–540. \endbibitem

- Chernozhukov et al. (2018) {barticle}[author] \bauthor\bsnmChernozhukov, \bfnmVictor\binitsV., \bauthor\bsnmChetverikov, \bfnmDenis\binitsD., \bauthor\bsnmDemirer, \bfnmMert\binitsM., \bauthor\bsnmDuflo, \bfnmEsther\binitsE., \bauthor\bsnmHansen, \bfnmChristian\binitsC., \bauthor\bsnmNewey, \bfnmWhitney\binitsW. and \bauthor\bsnmRobins, \bfnmJames\binitsJ. (\byear2018). \btitleDouble/debiased machine learning for treatment and structural parameters. \bjournalThe Econometrics Journal \bvolume21 \bpagesC1–C68. \endbibitem

- Daniel et al. (2013) {barticle}[author] \bauthor\bsnmDaniel, \bfnmRhian M\binitsR. M., \bauthor\bsnmCousens, \bfnmSN\binitsS., \bauthor\bsnmDe Stavola, \bfnmBL\binitsB., \bauthor\bsnmKenward, \bfnmMichael G\binitsM. G. and \bauthor\bsnmSterne, \bfnmJAC\binitsJ. (\byear2013). \btitleMethods for dealing with time-dependent confounding. \bjournalStatistics in Medicine \bvolume32 \bpages1584–1618. \endbibitem

- Dukes, Avagyan and Vansteelandt (2020) {barticle}[author] \bauthor\bsnmDukes, \bfnmOliver\binitsO., \bauthor\bsnmAvagyan, \bfnmVahe\binitsV. and \bauthor\bsnmVansteelandt, \bfnmStijn\binitsS. (\byear2020). \btitleDoubly robust tests of exposure effects under high-dimensional confounding. \bjournalBiometrics \bvolume76 \bpages1190–1200. \endbibitem

- Dukes and Vansteelandt (2021) {barticle}[author] \bauthor\bsnmDukes, \bfnmOliver\binitsO. and \bauthor\bsnmVansteelandt, \bfnmStijn\binitsS. (\byear2021). \btitleInference for treatment effect parameters in potentially misspecified high-dimensional models. \bjournalBiometrika \bvolume108 \bpages321–334. \endbibitem

- Dümbgen et al. (2010) {barticle}[author] \bauthor\bsnmDümbgen, \bfnmLutz\binitsL., \bauthor\bsnmVan De Geer, \bfnmSara A\binitsS. A., \bauthor\bsnmVeraar, \bfnmMark C\binitsM. C. and \bauthor\bsnmWellner, \bfnmJon A\binitsJ. A. (\byear2010). \btitleNemirovski’s inequalities revisited. \bjournalThe American Mathematical Monthly \bvolume117 \bpages138–160. \endbibitem

- Farrell (2015) {barticle}[author] \bauthor\bsnmFarrell, \bfnmMax H\binitsM. H. (\byear2015). \btitleRobust inference on average treatment effects with possibly more covariates than observations. \bjournalJournal of Econometrics \bvolume189 \bpages1–23. \endbibitem

- Flores et al. (2012) {barticle}[author] \bauthor\bsnmFlores, \bfnmCarlos A\binitsC. A., \bauthor\bsnmFlores-Lagunes, \bfnmAlfonso\binitsA., \bauthor\bsnmGonzalez, \bfnmArturo\binitsA. and \bauthor\bsnmNeumann, \bfnmTodd C\binitsT. C. (\byear2012). \btitleEstimating the effects of length of exposure to instruction in a training program: The case of job corps. \bjournalReview of Economics and Statistics \bvolume94 \bpages153–171. \endbibitem

- Hernán, Brumback and Robins (2001) {barticle}[author] \bauthor\bsnmHernán, \bfnmMiguel A\binitsM. A., \bauthor\bsnmBrumback, \bfnmBabette\binitsB. and \bauthor\bsnmRobins, \bfnmJames M\binitsJ. M. (\byear2001). \btitleMarginal structural models to estimate the joint causal effect of nonrandomized treatments. \bjournalJournal of the American Statistical Association \bvolume96 \bpages440–448. \endbibitem

- Hernán et al. (2016) {barticle}[author] \bauthor\bsnmHernán, \bfnmMiguel A\binitsM. A., \bauthor\bsnmSauer, \bfnmBrian C\binitsB. C., \bauthor\bsnmHernández-Díaz, \bfnmSonia\binitsS., \bauthor\bsnmPlatt, \bfnmRobert\binitsR. and \bauthor\bsnmShrier, \bfnmIan\binitsI. (\byear2016). \btitleSpecifying a target trial prevents immortal time bias and other self-inflicted injuries in observational analyses. \bjournalJournal of Clinical Epidemiology \bvolume79 \bpages70–75. \endbibitem

- Huber et al. (2020) {barticle}[author] \bauthor\bsnmHuber, \bfnmMartin\binitsM., \bauthor\bsnmHsu, \bfnmYu-Chin\binitsY.-C., \bauthor\bsnmLee, \bfnmYing-Ying\binitsY.-Y. and \bauthor\bsnmLettry, \bfnmLayal\binitsL. (\byear2020). \btitleDirect and indirect effects of continuous treatments based on generalized propensity score weighting. \bjournalJournal of Applied Econometrics \bvolume35 \bpages814–840. \endbibitem

- Kallus and Santacatterina (2021) {barticle}[author] \bauthor\bsnmKallus, \bfnmNathan\binitsN. and \bauthor\bsnmSantacatterina, \bfnmMichele\binitsM. (\byear2021). \btitleOptimal balancing of time-dependent confounders for marginal structural models. \bjournalJournal of Causal Inference \bvolume9 \bpages345–369. \endbibitem

- Kennedy (2020) {barticle}[author] \bauthor\bsnmKennedy, \bfnmEdward H\binitsE. H. (\byear2020). \btitleTowards optimal doubly robust estimation of heterogeneous causal effects. \bjournalarXiv preprint arXiv:2004.14497. \endbibitem

- Lee (2009) {barticle}[author] \bauthor\bsnmLee, \bfnmDavid S\binitsD. S. (\byear2009). \btitleTraining, wages, and sample selection: Estimating sharp bounds on treatment effects. \bjournalThe Review of Economic Studies \bvolume76 \bpages1071–1102. \endbibitem

- Lewis and Syrgkanis (2021) {barticle}[author] \bauthor\bsnmLewis, \bfnmGreg\binitsG. and \bauthor\bsnmSyrgkanis, \bfnmVasilis\binitsV. (\byear2021). \btitleDouble/debiased machine learning for dynamic treatment effects. \bjournalAdvances in Neural Information Processing Systems \bvolume34 \bpages22695–22707. \endbibitem

- Murphy (2003) {barticle}[author] \bauthor\bsnmMurphy, \bfnmSusan A\binitsS. A. (\byear2003). \btitleOptimal dynamic treatment regimes. \bjournalJournal of the Royal Statistical Society: Series B (Statistical Methodology) \bvolume65 \bpages331–355. \endbibitem

- Murphy et al. (2001) {barticle}[author] \bauthor\bsnmMurphy, \bfnmSusan A\binitsS. A., \bauthor\bparticlevan der \bsnmLaan, \bfnmMark J\binitsM. J., \bauthor\bsnmRobins, \bfnmJames M\binitsJ. M. and \bauthor\bsnmGroup, \bfnmConduct Problems Prevention Research\binitsC. P. P. R. (\byear2001). \btitleMarginal mean models for dynamic regimes. \bjournalJournal of the American Statistical Association \bvolume96 \bpages1410–1423. \endbibitem

- Negahban et al. (2012) {barticle}[author] \bauthor\bsnmNegahban, \bfnmSahand N\binitsS. N., \bauthor\bsnmRavikumar, \bfnmPradeep\binitsP., \bauthor\bsnmWainwright, \bfnmMartin J\binitsM. J. and \bauthor\bsnmYu, \bfnmBin\binitsB. (\byear2012). \btitleA unified framework for high-dimensional analysis of -estimators with decomposable regularizers. \bjournalStatistical Science \bvolume27 \bpages538–557. \endbibitem

- Orellana, Rotnitzky and Robins (2010) {barticle}[author] \bauthor\bsnmOrellana, \bfnmLiliana\binitsL., \bauthor\bsnmRotnitzky, \bfnmAndrea\binitsA. and \bauthor\bsnmRobins, \bfnmJames M\binitsJ. M. (\byear2010). \btitleDynamic regime marginal structural mean models for estimation of optimal dynamic treatment regimes, part I: main content. \bjournalThe International Journal of Biostatistics \bvolume6. \endbibitem

- Robins (1986) {barticle}[author] \bauthor\bsnmRobins, \bfnmJames\binitsJ. (\byear1986). \btitleA new approach to causal inference in mortality studies with a sustained exposure period – application to control of the healthy worker survivor effect. \bjournalMathematical Modelling \bvolume7 \bpages1393–1512. \endbibitem

- Robins (1987) {barticle}[author] \bauthor\bsnmRobins, \bfnmJames M\binitsJ. M. (\byear1987). \btitleAddendum to ”a new approach to causal inference in mortality studies with a sustained exposure period – application to control of the healthy worker survivor effect”. \bjournalComputers & Mathematics with Applications \bvolume14 \bpages923–945. \endbibitem

- Robins (1997) {binproceedings}[author] \bauthor\bsnmRobins, \bfnmJames M\binitsJ. M. (\byear1997). \btitleCausal inference from complex longitudinal data. In \bbooktitleLatent Variable Modeling and Applications to Causality \bpages69–117. \bpublisherSpringer. \endbibitem

- Robins (2000a) {bincollection}[author] \bauthor\bsnmRobins, \bfnmJames M\binitsJ. M. (\byear2000a). \btitleMarginal structural models versus structural nested models as tools for causal inference. In \bbooktitleStatistical Models in Epidemiology, the Environment, and Clinical Trials \bpages95–133. \bpublisherSpringer. \endbibitem

- Robins (2000b) {binproceedings}[author] \bauthor\bsnmRobins, \bfnmJames M\binitsJ. M. (\byear2000b). \btitleRobust estimation in sequentially ignorable missing data and causal inference models. In \bbooktitleProceedings of the American Statistical Association \bvolume1999 \bpages6–10. \bpublisherIndianapolis, IN. \endbibitem

- Robins (2004) {binproceedings}[author] \bauthor\bsnmRobins, \bfnmJames M\binitsJ. M. (\byear2004). \btitleOptimal structural nested models for optimal sequential decisions. In \bbooktitleProceedings of the Second Seattle Symposium in Biostatistics \bpages189–326. \bpublisherSpringer. \endbibitem

- Rosenbaum and Rubin (1983) {barticle}[author] \bauthor\bsnmRosenbaum, \bfnmPaul R\binitsP. R. and \bauthor\bsnmRubin, \bfnmDonald B\binitsD. B. (\byear1983). \btitleThe central role of the propensity score in observational studies for causal effects. \bjournalBiometrika \bvolume70 \bpages41–55. \endbibitem

- Rudelson and Zhou (2012) {binproceedings}[author] \bauthor\bsnmRudelson, \bfnmMark\binitsM. and \bauthor\bsnmZhou, \bfnmShuheng\binitsS. (\byear2012). \btitleReconstruction from Anisotropic Random Measurements. In \bbooktitleProceedings of the 25th Annual Conference on Learning Theory (\beditor\bfnmShie\binitsS. \bsnmMannor, \beditor\bfnmNathan\binitsN. \bsnmSrebro and \beditor\bfnmRobert C.\binitsR. C. \bsnmWilliamson, eds.). \bseriesProceedings of Machine Learning Research \bvolume23 \bpages10.1–10.24. \bpublisherJMLR Workshop and Conference Proceedings, \baddressEdinburgh, Scotland. \endbibitem

- Schochet (2001) {bbook}[author] \bauthor\bsnmSchochet, \bfnmPeter Z\binitsP. Z. (\byear2001). \btitleNational Job Corps Study: The impacts of Job Corps on participants’ employment and related outcomes. \bpublisherUS Department of Labor, Employment and Training Administration, Office of Policy and Research. \endbibitem

- Schochet, Burghardt and McConnell (2008) {barticle}[author] \bauthor\bsnmSchochet, \bfnmPeter Z\binitsP. Z., \bauthor\bsnmBurghardt, \bfnmJohn\binitsJ. and \bauthor\bsnmMcConnell, \bfnmSheena\binitsS. (\byear2008). \btitleDoes job corps work? Impact findings from the national job corps study. \bjournalAmerican Economic Review \bvolume98 \bpages1864–1886. \endbibitem

- Schochet et al. (2003) {barticle}[author] \bauthor\bsnmSchochet, \bfnmP\binitsP., \bauthor\bsnmBellotti, \bfnmJ\binitsJ., \bauthor\bsnmRuo-Jiao, \bfnmC\binitsC., \bauthor\bsnmGlazerman, \bfnmS\binitsS., \bauthor\bsnmGrady, \bfnmA\binitsA., \bauthor\bsnmGritz, \bfnmM\binitsM., \bauthor\bsnmMcConnell, \bfnmS\binitsS., \bauthor\bsnmJohnson, \bfnmT\binitsT. and \bauthor\bsnmBurghardt, \bfnmJ\binitsJ. (\byear2003). \btitleNational Job Corps study: data documentation and public use files. \bjournalvols. I-IV). Washington, DC: Mathematica Policy Research, Inc. \endbibitem

- Singh, Xu and Gretton (2021) {barticle}[author] \bauthor\bsnmSingh, \bfnmRahul\binitsR., \bauthor\bsnmXu, \bfnmLiyuan\binitsL. and \bauthor\bsnmGretton, \bfnmArthur\binitsA. (\byear2021). \btitleKernel methods for multistage causal inference: Mediation analysis and dynamic treatment effects. \bjournalarXiv preprint arXiv:2111.03950. \endbibitem

- Smucler, Rotnitzky and Robins (2019) {barticle}[author] \bauthor\bsnmSmucler, \bfnmEzequiel\binitsE., \bauthor\bsnmRotnitzky, \bfnmAndrea\binitsA. and \bauthor\bsnmRobins, \bfnmJames M\binitsJ. M. (\byear2019). \btitleA unifying approach for doubly-robust regularized estimation of causal contrasts. \bjournalarXiv preprint arXiv:1904.03737. \endbibitem

- Tan (2020) {barticle}[author] \bauthor\bsnmTan, \bfnmZhiqiang\binitsZ. (\byear2020). \btitleModel-assisted inference for treatment effects using regularized calibrated estimation with high-dimensional data. \bjournalThe Annals of Statistics \bvolume48 \bpages811–837. \endbibitem

- Tchetgen and Shpitser (2012) {barticle}[author] \bauthor\bsnmTchetgen, \bfnmEric J Tchetgen\binitsE. J. T. and \bauthor\bsnmShpitser, \bfnmIlya\binitsI. (\byear2012). \btitleSemiparametric theory for causal mediation analysis: efficiency bounds, multiple robustness, and sensitivity analysis. \bjournalThe Annals of Statistics \bvolume40 \bpages1816. \endbibitem

- van der Laan and Gruber (2012) {barticle}[author] \bauthor\bparticlevan der \bsnmLaan, \bfnmMark J\binitsM. J. and \bauthor\bsnmGruber, \bfnmSusan\binitsS. (\byear2012). \btitleTargeted minimum loss based estimation of causal effects of multiple time point interventions. \bjournalThe international journal of biostatistics \bvolume8. \endbibitem

- Viviano and Bradic (2021) {barticle}[author] \bauthor\bsnmViviano, \bfnmDavide\binitsD. and \bauthor\bsnmBradic, \bfnmJelena\binitsJ. (\byear2021). \btitleDynamic covariate balancing: estimating treatment effects over time. \bjournalarXiv preprint arXiv:2103.01280. \endbibitem

- Wainwright (2019) {bbook}[author] \bauthor\bsnmWainwright, \bfnmMartin J\binitsM. J. (\byear2019). \btitleHigh-dimensional statistics: A non-asymptotic viewpoint \bvolume48. \bpublisherCambridge University Press. \endbibitem

- Yiu and Su (2018) {barticle}[author] \bauthor\bsnmYiu, \bfnmSean\binitsS. and \bauthor\bsnmSu, \bfnmLi\binitsL. (\byear2018). \btitleCovariate association eliminating weights: a unified weighting framework for causal effect estimation. \bjournalBiometrika \bvolume105 \bpages709–722. \endbibitem

- Yu and van der Laan (2006) {barticle}[author] \bauthor\bsnmYu, \bfnmZhuo\binitsZ. and \bauthor\bparticlevan der \bsnmLaan, \bfnmMark\binitsM. (\byear2006). \btitleDouble robust estimation in longitudinal marginal structural models. \bjournalJournal of Statistical Planning and Inference \bvolume136 \bpages1061–1089. \endbibitem

- Zhang and Bradic (2022) {barticle}[author] \bauthor\bsnmZhang, \bfnmYuqian\binitsY. and \bauthor\bsnmBradic, \bfnmJelena\binitsJ. (\byear2022). \btitleHigh-dimensional semi-supervised learning: in search of optimal inference of the mean. \bjournalBiometrika \bvolume109 \bpages387–403. \endbibitem

- Zhang, Chakrabortty and Bradic (2021) {barticle}[author] \bauthor\bsnmZhang, \bfnmYuqian\binitsY., \bauthor\bsnmChakrabortty, \bfnmAbhishek\binitsA. and \bauthor\bsnmBradic, \bfnmJelena\binitsJ. (\byear2021). \btitleDouble Robust Semi-Supervised Inference for the Mean: Selection Bias under MAR Labeling with Decaying Overlap. \bjournalarXiv preprint arXiv:2104.06667. \endbibitem

- Zhang, Rubin and Mealli (2008) {bincollection}[author] \bauthor\bsnmZhang, \bfnmJunni L\binitsJ. L., \bauthor\bsnmRubin, \bfnmDonald B\binitsD. B. and \bauthor\bsnmMealli, \bfnmFabrizia\binitsF. (\byear2008). \btitleEvaluating the effects of job training programs on wages through principal stratification. In \bbooktitleModelling and Evaluating Treatment Effects in Econometrics \bpublisherEmerald Group Publishing Limited. \endbibitem

- Zhu, Zeng and Song (2019) {barticle}[author] \bauthor\bsnmZhu, \bfnmWensheng\binitsW., \bauthor\bsnmZeng, \bfnmDonglin\binitsD. and \bauthor\bsnmSong, \bfnmRui\binitsR. (\byear2019). \btitleProper inference for value function in high-dimensional Q-learning for dynamic treatment regimes. \bjournalJournal of the American Statistical Association \bvolume114 \bpages1404–1417. \endbibitem

SUPPLEMENTARY MATERIALS FOR THE “HIGH-DIMENSIONAL INFERENCE FOR DYNAMIC TREATMENT EFFECTS”

This supplementary document contains additional justifications and the proofs of the theoretical results presented in the main document. All the results and notation are numbered and used as in the main text unless stated otherwise. Statements introduced in the Supplementary Materials only are numbered using an alphanumerical scheme. Supplementary Materials includes further discussions on the nuisance models, comparison with the oracle inverse propensity score estimator, additional numerical results, Auxiliary Lemmas S.1-S.18 with their proofs used for establishing the main results, Theorems 1-11.